Abstract

There is a general trend of increased marketization of long-term care (LTC) services across Europe, with the natural consequence that market forces will affect the supply of LTC. At the same time, there has been a rapid increase in the use of home-based provision for those requiring LTC support. However, there is little evidence about what the effects of growing domiciliary care provision has on the markets for institutional forms of care. This is important from a policy point of view in terms of managing local markets, access to services, the quality of services and inequality. Using data from England for all care homes and domiciliary care providers registered to provide care to older people during 2014–2016, we assessed if increased domiciliary care supply was linked to increased likelihood of care home closure. Using Cox proportional hazard models of care home closure controlling for care home characteristics including quality and local area measures of needs and income, the findings provide no evidence that domiciliary care provision is a substitute for care homes. In some specifications, there was even a complementary relationship between the two forms of social care: increased domiciliary care supply significantly reduced the likelihood of care home closure. Potential reasons for the complementary relationship and implications for European LTC policy are discussed.

Introduction

Preventative services have formed a key part of long-term care (LTC) for a number of years with policy in many industrialised countries aimed at keeping people out of the highest cost forms of care (usually institutional care) for as long as possible, instead receiving low or intermediate services within their community (Colombo et al., 2011; Genet et al., 2013; Ranci and Pavolini, 2015). At the same time, many countries have seen the increased delivery of LTC services by the private sector (Gori et al., 2015; Knapp et al., 2001; Riedel and Kraus, 2011).

The increased marketization of services means that delivery of LTC is open to market forces. Given these market forces, it is likely that alternative forms of LTC will have an effect on other forms of care. For example, US nursing home performance has been found to be significantly reduced by the presence of assisted living facilities (similar to residential care homes), causing decreased occupancy, higher relative needs of patients, increased market concentration and worse financial performance (Bowblis, 2014; Grabowski et al., 2012; Lord et al., 2018). If different forms of LTC are substitutes then this would have implications for the demand for services, either directly between the different forms or indirectly through competition of providers within services. This then has broad implications for ensuring the adequate delivery of services, the equity of provision and potentially on outcomes of service users through quality of provision (Castle et al., 2007; Forder and Allan, 2014).

There is an increasing level of LTC provided across Europe through domiciliary care (Genet et al., 2013; Spasova et al., 2018). Consideration of any potential detrimental impact that this may have on other forms of LTC must be considered, particularly as, at the same time, public funding (or access to it) is being reduced in many countries (Pavolini and Ranci, 2008; Spasova et al., 2018). This has been the case in England, where there is concern over the precarious financial situation of LTC providers (Humphries et al., 2016). Additionally, the Care Act 2014 included the requirement for local authorities (LAs) (local-level public councils) to ensure that local LTC markets have diversity and choice of provision. The substitutability of different forms of LTC are therefore of particular relevance for European governments; for example, if substitutes, any actions to ensure diversity of choice, such as through promoting one form of care over an alternative, could lead to negative consequences for the local supply of, and the welfare of those who require, the alternative form of care.

Despite its importance, little is known about the impact that domiciliary care provision (also called home care) has on the care homes market in the United Kingdom or, more widely, Europe. The analysis reported here adds to the existing evidence by exploring the influence that domiciliary care supply (i.e. care provided in the home) has on care homes in England. The relationship between domiciliary care availability and care home performance is assessed using a panel of all care homes for the elderly for 2014–2016. Care home closures are utilised as an inverse measure of care home market performance and domiciliary care availability is estimated using geographical measures of supply. The analysis controls for care home characteristics and local area-level need and demand characteristics. The findings of this analysis have broad implications for national LTC policy across Europe given increasing similarity in their systems, including the use of competitive markets (Pavolini and Ranci, 2008).

The rest of the article begins with a discussion of the care homes and domiciliary care markets in England, before theoretical considerations are presented. The data and methods of analysis are described and the findings reported. A discussion of the policy implications is followed by a brief conclusion.

Care home and domiciliary care provision in England

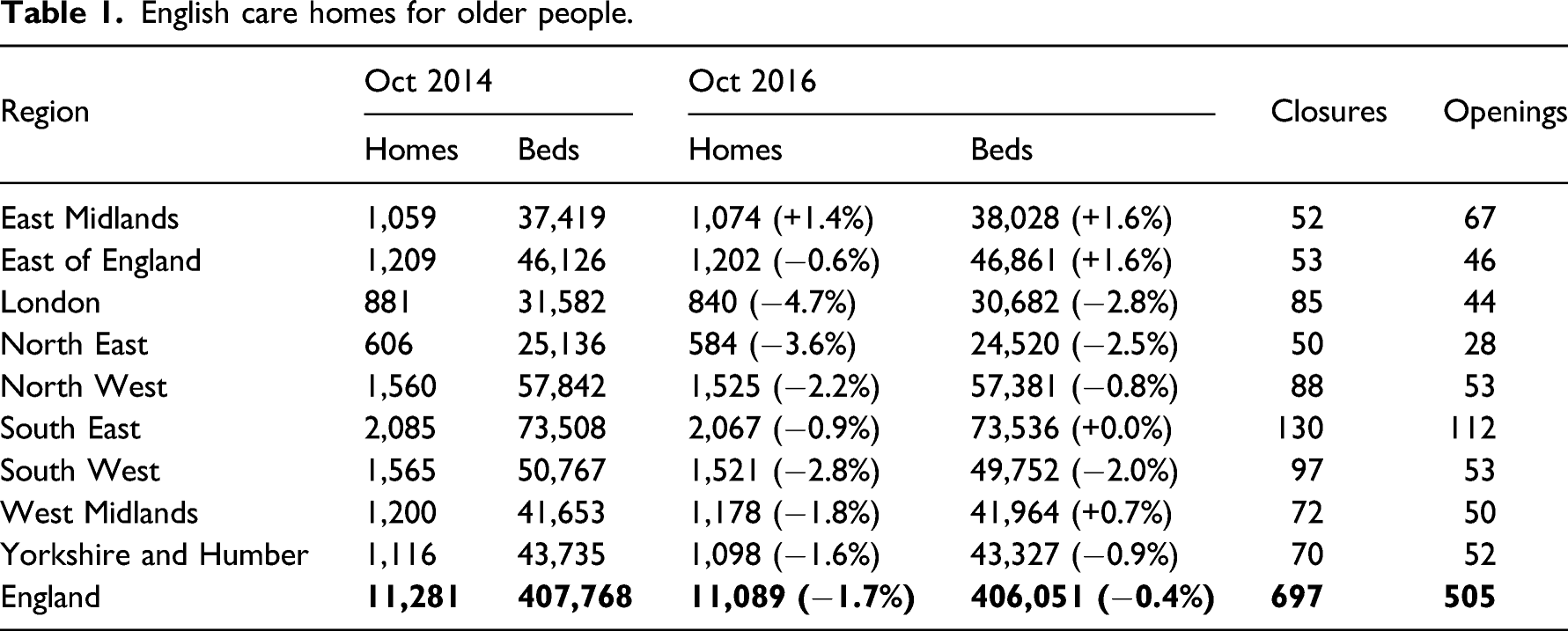

Since the promotion of independent sector delivery of LTC, that is, provision of care by non-public entities, the markets for both care homes and domiciliary care have grown markedly (Forder and Allan, 2011; Ware et al., 2001). The English care homes market for older people consists of over 11,000 care homes, and almost all care home provision is now within the independent sector (about 85% of all homes are owned by private, for-profit, organisations). There are some large organisations which control a sizeable section of the market, but small providers, owning one or two homes, account for a large share of the market and there are high levels of local competition (Forder and Allan, 2014; LaingBuisson, 2015). Increasingly, only people with the very highest needs are supported in care homes (Competition and Markets Authority, 2017).

The number of domiciliary care providers in England that were registered to provide care to older people increased by 26% from October 2012 (5,600 providers) to October 2016 (7,055 providers). Provision varied by region; London and the South East had the greatest number of providers and the North East the fewest. It is estimated that the vast majority of domiciliary care purchased by LAs is provided by the independent sector compared to 56% in 2000 (Department of Health, 2000; UK Home Care Association, 2016). Users with higher needs are increasingly supported by domiciliary care, with a higher intensity of home care use among the fewer users who are publicly supported (Laing and Buisson, 2013; UK Home Care Association, 2016). The market is disaggregated, with almost two out of every three (65%) organisations offering care from one location. There is a wide spectrum of domiciliary care available on the supply side, to the point where the care received can be seen as similar to a stay in a care home (e.g. live-in carers).

Care homes and domiciliary care providers have two demand streams, from private individual payers and from LAs who commission care on behalf of those who cannot afford to (fully) fund their own care. Additionally, for domiciliary care providers, LAs make direct payments to individuals who qualify for support who will then source their own care. 1 For 2016/17, estimated expenditure by private payers on all forms of adult LTC was £10.9bn and public expenditure was £8.1bn and £7.0bn on care homes and support in own home, respectively. One third of the latter expenditure funded domiciliary care directly and one quarter funded direct payments (National Audit Office, 2018). LA funding support for LTC has fallen over time with a concomitant drop in the number of people supported (Fernandez et al., 2013), although expenditure varies by location (Fernandez and Forder, 2015). For care homes, there is a roughly even split between LA-supported residents and private paying residents nationally, although this can depend on location. 2 The extent of private paying domiciliary care provision and provision from direct payments is not known (UK Home Care Association, 2016; Laing and Buisson, 2013).

The majority of care homes cater for a mix of resident-pay types, but there are providers which focus on private payers (LaingBuisson, 2015). There is less knowledge of service user pay-mix in domiciliary care, but it is likely to be similar to the care homes market: as the number of providers has been increasing, the amount of domiciliary care funded by LAs has been falling (UK Home Care Association, 2016; Laing and Buisson, 2013). A further concern in care home markets is that care homes are surviving through cross-subsidisation, that is, private payer fees supporting lower fees paid by LAs (Competition and Markets Authority, 2017), and there are similar concerns for domiciliary care (Bolton and Townson, 2018).

Theoretical considerations

At service user level, there is scope for a substitutability between domiciliary care and institutional care. Entry into residential care has been found to be dependent not only on needs-based factors such as limited ability to perform activities of daily living and prior care home use (Gaugler et al., 2007; Luppa et al., 2010), but also on living alone, loneliness and carer stress (Jamieson et al., 2019; McCann et al., 2011). The outcomes of individuals will be an additional consideration as to which form of care to receive. For example, residents in institutional care in the Netherlands were happier compared to those receiving care at home (Kok et al., 2015). Taken together, this evidence would suggest that the decision on which form of LTC to receive is based not only on needs, but also on other social factors and, potentially, outcomes. In other words, there could be a high degree of substitutability between receiving care at home or in an institutional setting.

Given the English LTC market context described above, it is likely that domiciliary care and care home supply are substitutes because their demand streams are similar (at the margin). Private consumers have a clear choice, given the available forms of care, their level of need and the level of expenditure they can afford. These service users tend to be healthier and are increasingly seen as the target market given their higher levels of wealth (Competition and Markets Authority, 2017).

For people supported by public funding, however, the level of substitution is less clear. Individual choice is of primary importance, but that will be subject to cost (Department of Health, 2014). There may be more than one way in which the LTC required to meet the needs of a person can be delivered. If so, this decision is likely to come down to cost – LAs will have a limit on the cost that they would pay for one service if another service could meet those same needs at a lower cost. However, ‘top-up’ payments can be paid by a family member or by the service user if they wished to be supported in a more expensive way than the level of support their LA will provide given their level of needs. This increases the extent that substitution between different forms of LTC could occur.

Financial assessments (means tests) for LA support for the two forms of LTC also differ. For domiciliary care housing wealth is disregarded, whereas it is included for care home provision (Department of Health, 2014). Therefore, there is a margin where it is in the interests of LTC recipients to use domiciliary care over care home services, subject to both their needs and LA cost. Domiciliary care recipients may also receive other services such as meals, technology and day care which will delay the need to move in to a care home (Bolton and Townson, 2018; Wiener et al., 2002).

Overall, costs of care and the incentives within LTC systems will be important factors in the decision by individuals as to which form of care to receive. This is supported by evidence, with UK homeowners significantly less likely to move in to a care home (McCann et al., 2012) and in the Netherlands, while residential care was more expensive overall, it was less costly to the individual to be receiving care institutionally than at home (Kok et al., 2015).

At the firm level, any substitutability in choice of product for consumers will generate competition. Economic theory shows that competition in price and quality between (not necessarily direct) substitutes will lead to a finite number of firms, that is, imperfect competition (Gabszewicz and Thisse, 1980; Shaked and Sutton, 1983). Further, where imperfect competition exists and firms can price discriminate based on location, then this will lead to lower prices and reduced profits (Stole, 2007; Thisse and Vives, 1988). This is likely true for domiciliary care and institutional care. Evidence from the United States finds increased use of home- and community-based services over time instead of nursing home stays (Kane et al., 2013; Young et al., 2015).

Ultimately, increased competition between substitutes could have implications over the viability of the provider (Allan and Forder, 2015; Castle et al., 2009). Certain providers may find it unviable to continue due to long-term losses or because, to achieve profit in the long run, they reduce their quality to a level which brings negative consequence, for example, forced to close by a national regulator. 3

Overall, the impact of substitutability between domiciliary care and care homes for England was unknown, a priori. However, based on the theoretical considerations above, it was hypothesised that domiciliary care was a substitute to care home supply in England, that is, domiciliary care had a positive impact on the probability of care home closure.

Data and methods

A panel of all care homes for older people in England was created for the months from October 2014 to October 2016. These were care homes registered with the Care Quality Commission (CQC), the national health and social care regulator, to provide either residential or nursing care to older people and/or those living with dementia. Care homes were matched across the months by a CQC identifier and then additionally through postal addresses. Exits from the care homes market were treated as full closures where a care home no longer operated at the location.

Domiciliary care competition measures

There are no official measures available of the extent of domiciliary care provision in England. CQC register data includes the location of all registered domiciliary care providers, but not their size. A further complication is that there are exemptions from CQC registration for certain types of carers that provide care at home (Care Quality Commission, 2015). For example, a carer employed by an individual who arranged their own care directly would not currently need to register with the CQC. Therefore, the analysis can only assess the effect of registered domiciliary care providers on the care homes market. Nonetheless, we proceed on the assumption that the register does indicate the prevalence of domiciliary care supply within a market to a good degree.

By definition, domiciliary care provision will be delivered within the home. Therefore, a provider’s registered location may not be an ideal indicator of where care is actually delivered. The limited evidence as to the size of the geographic markets domiciliary care providers serve in England suggests different home care providers operate either in small markets within an LA or across more than one LA (Matosevic et al., 2001; Ware et al., 2001). Ad hoc inspection of some domiciliary care agency websites suggests relatively small markets in distance, but at least some go across LA boundaries. 4

The measure of domiciliary care supply used in the analysis was a count of the number of registered providers:

Control variables

The following controls were used at the care home level: type (residential or nursing), registration to support service users living with dementia, total number of beds (log), an indicator for the size of the provider organisation (0 if provider owns one or two homes and 1 if it runs three or more), the care home’s quality rating (see below) and the level of intra-care home market competition faced by each care home. This was measured for each wave of data by creating a distance-weighted HHI with a market radius of 10 and 20 km around each care home, with the HHI taking values between 0 and 1, and higher values indicating more concentration (lower competition) in the market. 6

For quality, CQC rated LTC establishments as ‘Inadequate’, ‘Requires improvement’, ‘Good’ or ‘Outstanding’. Quality ratings data were available from September 2015 and not all care homes were rated during the analysis timeframe. There was a low level of ‘Outstanding’ ratings nationally (Care Quality Commission, 2017). Therefore, a 0/1 variable for quality was included in the analysis, with homes rated as ‘Good’ or ‘Outstanding’ having a value of 1 and 0 for homes rated as ‘Inadequate’ or ‘Requires improvement’.

Apart from the type of service provided and the service user a care home is registered to provide care for, there is no further information on level of need within the care home. To control for levels of need and demand, local area-level controls were included, specifically pension credit and disability living allowance uptake percentage (income and needs based benefits, respectively), total population, percentage of population over 65 and average house price. 7 There was no information on residents’ payer-type. It is likely that some controls included would proxy for levels of wealth and therefore the level of self-funding within a local area. However, to further account for this, predicted local area-level LA expenditure per older person on residential care was included. 8 Finally, the region of care home location was included as a control.

Methods

The impact of domiciliary care supply on the likelihood of closure was assessed using survival analysis. Specifically, we estimated Cox proportional hazards regression models on all care homes between October 2014 and October 2016 (Cox, 1972). The Cox proportional hazards model is semi-parametric, does not specify a functional form for the baseline hazard, and assumes that the impact of the explanatory variables on the hazard remains constant over the timeframe examined. The results of the regression models are presented as hazards, with a hazard of 1 for domiciliary care supply indicating that there was no effect on closure likelihood of care homes, and a hazard of under (over) 1 indicating that it reduces (increases) the likelihood of care home closure. The model was estimated both including and excluding quality ratings.

The adequacy of the Cox proportional hazards model for care home closure was assessed using plots of scaled Schoenfeld residuals to look for trends and Schoenfeld residual tests to test for non-proportionality over time. The adequacy of the specification of the model was assessed using a link test. Finally, further extensions to the analysis assessed the robustness of the findings to changes in the sample of care homes, the addition of further variables that could influence closure and alternative measures of domiciliary care supply.

Results

English care homes for older people.

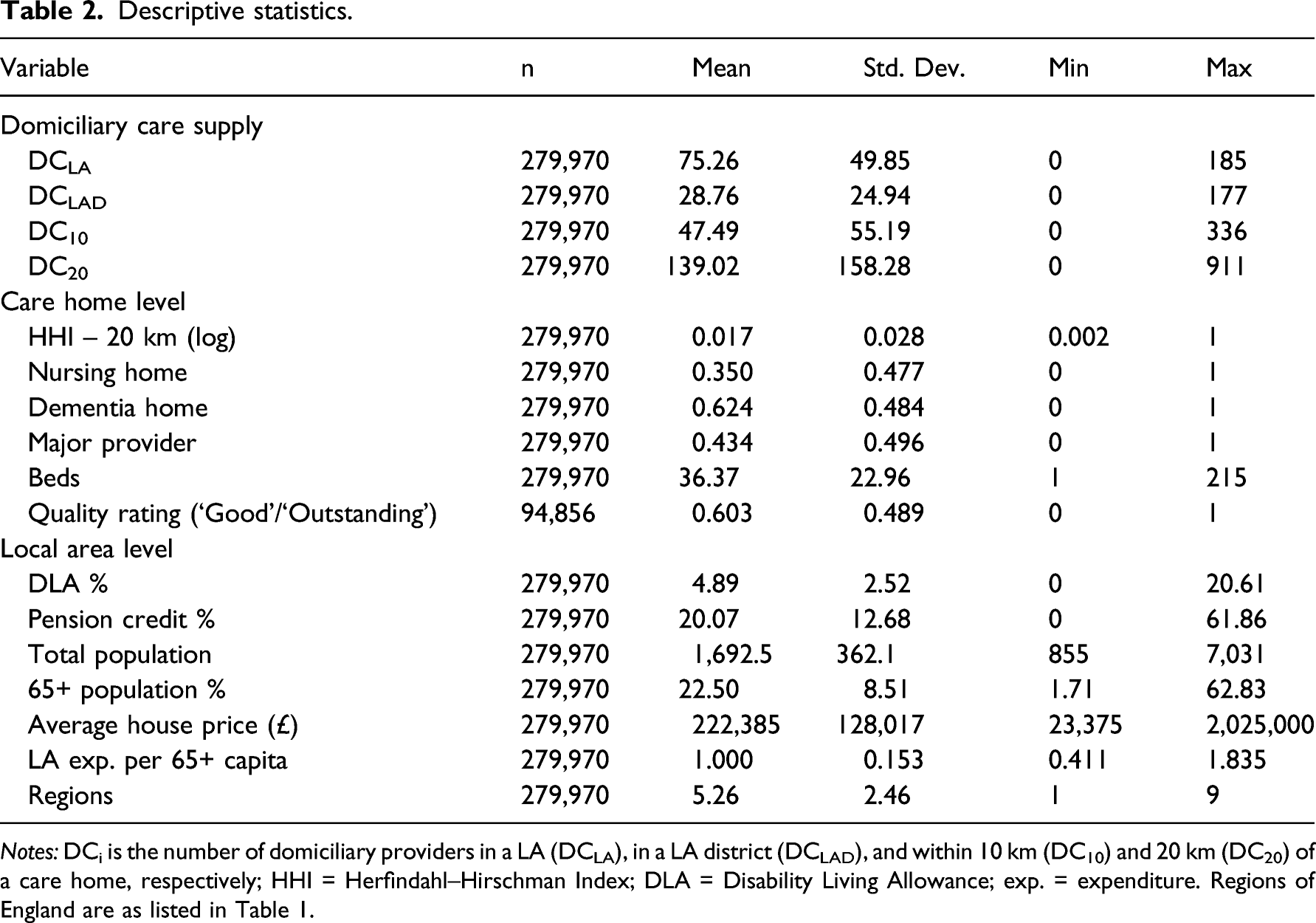

Descriptive statistics.

Notes: DCi is the number of domiciliary providers in a LA (DCLA), in a LA district (DCLAD), and within 10 km (DC10) and 20 km (DC20) of a care home, respectively; HHI = Herfindahl–Hirschman Index; DLA = Disability Living Allowance; exp. = expenditure. Regions of England are as listed in Table 1.

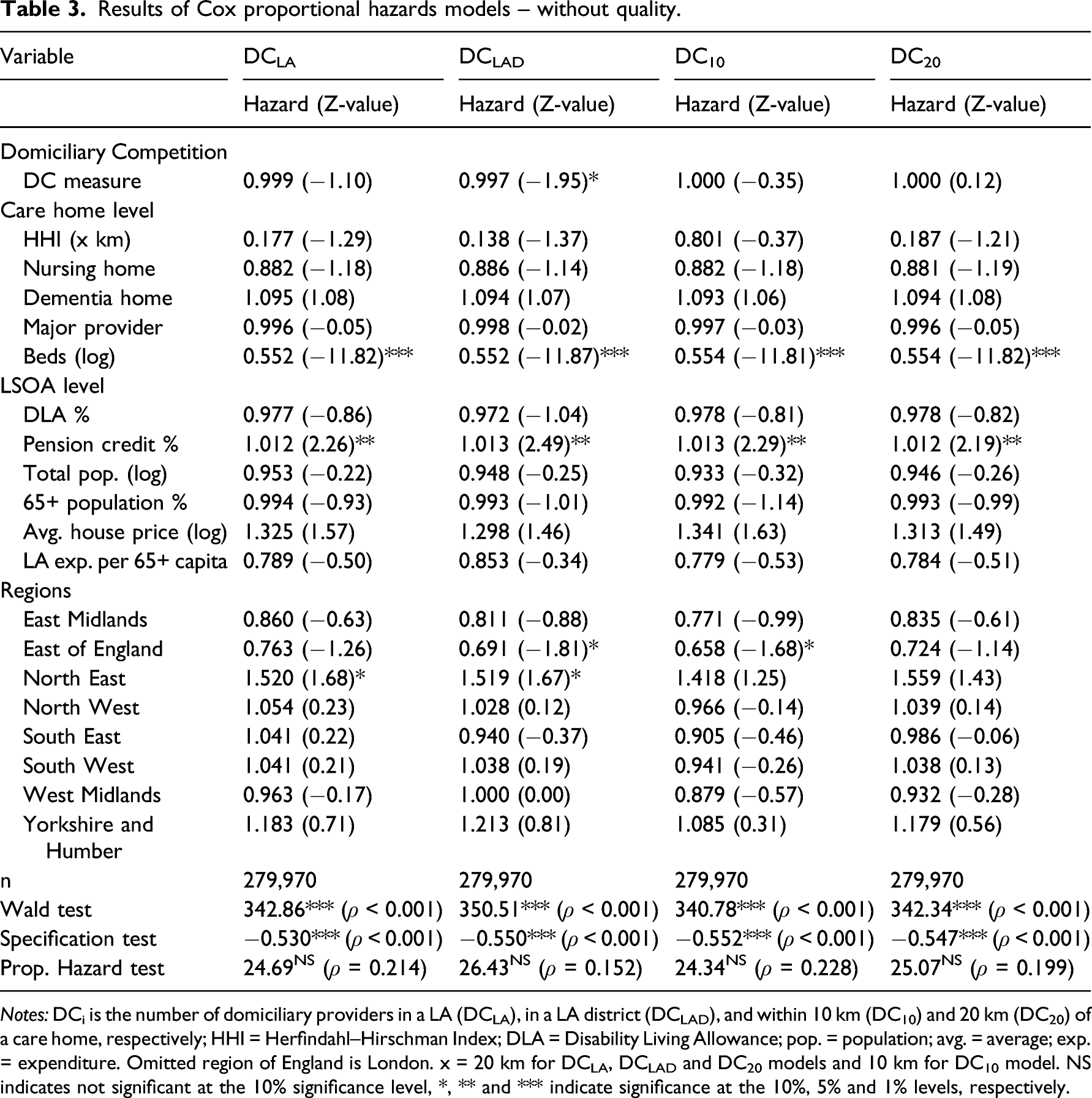

Results of Cox proportional hazards models – without quality.

Notes: DCi is the number of domiciliary providers in a LA (DCLA), in a LA district (DCLAD), and within 10 km (DC10) and 20 km (DC20) of a care home, respectively; HHI = Herfindahl–Hirschman Index; DLA = Disability Living Allowance; pop. = population; avg. = average; exp. = expenditure. Omitted region of England is London. x = 20 km for DCLA, DCLAD and DC20 models and 10 km for DC10 model. NS indicates not significant at the 10% significance level, *, ** and *** indicate significance at the 10%, 5% and 1% levels, respectively.

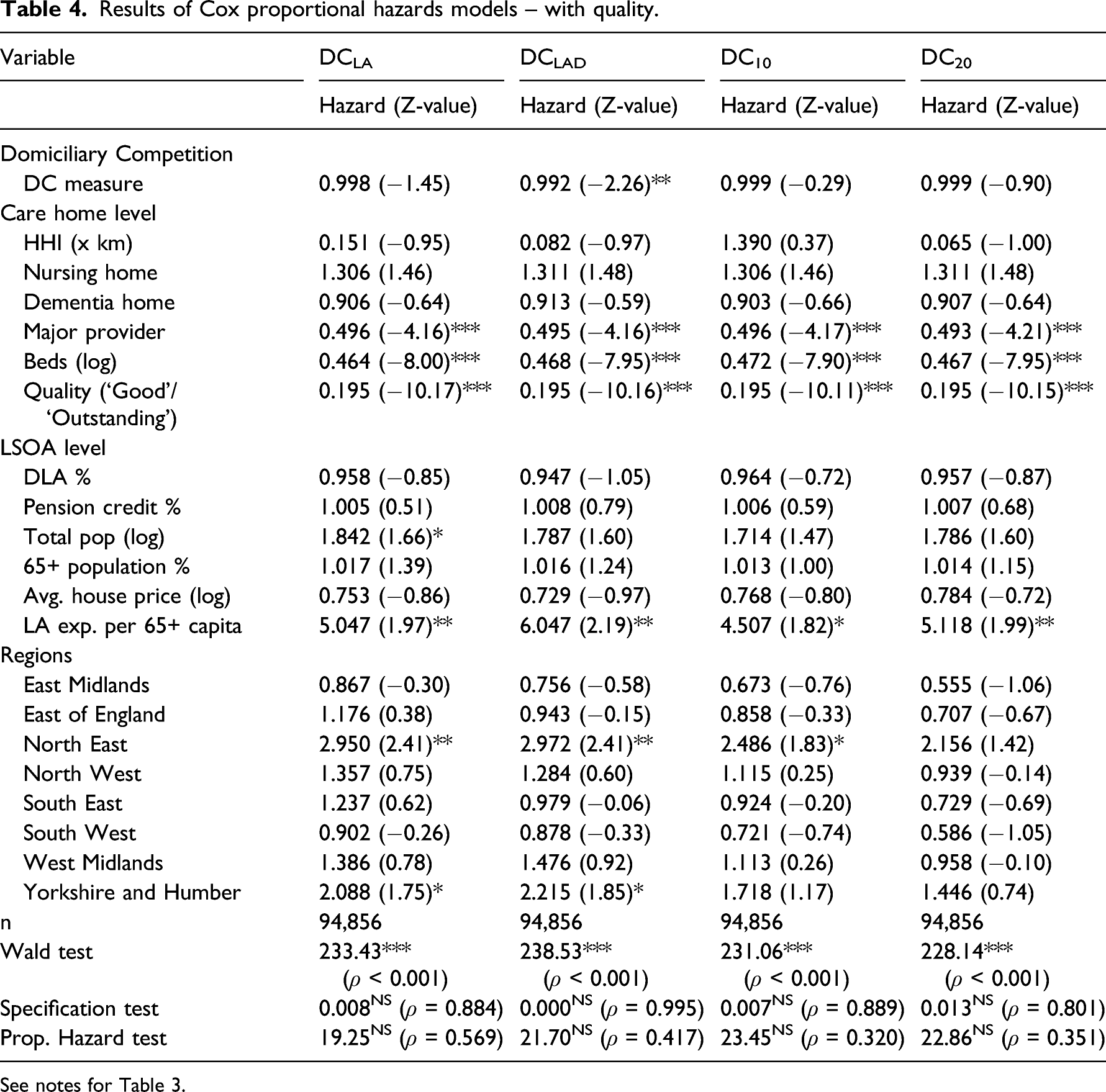

Results of Cox proportional hazards models – with quality.

See notes for Table 3.

The results in Tables 3 and 4 show that there was generally a negative influence of domiciliary care supply on the likelihood of care home closure. However, only for DCLAD was the effect significant, at the 10% level in Table 3 and 5% level in Table 4. The greater was domiciliary care competition in a LA district market the less likely a care home was to close. The hazard value for DCLAD of 0.997 in Table 3 suggests that for every extra domiciliary care provider in the LA district the likelihood of closure fell by 0.3%. This implies that a care home located in a LA district with 59 domiciliary care providers, the 90th percentile, would be 11.4% less likely to close than a care home with the median of 21 domiciliary care providers in their LA district, ceteris paribus. With the inclusion of quality in Table 4 the size of the influence on probability of closure is stronger for DCLAD and the equivalent figures for the same example level of domiciliary care provision were 0.8% and 30.4%, respectively.

The other results are largely in line with previous research on care home closures in England (Allan and Forder, 2015; Darton, 2004). Increased size of a care home significantly reduced the likelihood of closure. Competition between care homes did not significantly increase the likelihood of closure. Higher quality significantly increased care home survival – a care home with a ‘Good’ or ‘Outstanding’ rating was one fifth as likely to close compared to a care home rated as ‘Inadequate’ or ‘Requires improvement’. With quality included in the model, provider size and LA expenditure per capita also significantly influenced the likelihood of closure. A care home owned by a provider with three or more care homes was half as likely to close as a one or two home provider-owned care home. Additionally, the higher the relative level of LA-funding of residential care per capita the more likely a care home was to close.

Robustness checks

A number of extensions to the main analysis were performed to assess the robustness of the findings. First, quality ratings were not available across all months of the dataset. A predicted quality rating measure was estimated using LA-level average quality rating, excluding each respective care home’s rating, as an instrument. Inclusion of the predicted quality variable did not change the results for any of the domiciliary care measures and the significant negative quality effect was still apparent. Second, variables were included to reflect potential effects on care home performance from the healthcare system and from the provision of informal care. The former was controlled for using monthly data for total hospital admissions at Clinical Commissioning Group (CCG) level (n = 211) and the latter using data on the percentage of people providing informal care at small area-level (LSOA), as reported in the 2011 national census. There was no change in the main results and these variables did not significantly influence the likelihood of care home closure. Third, it is likely that there is a degree of integration within the two markets with owners providing both care home and domiciliary care services. Care homes that were also registered to provide domiciliary care were identified. For example, in October 2016, there were 498 care homes (4.5%) that were either registered to provide domiciliary care from the same location or that had domiciliary care provision separately registered at the same postcode. 10 Removing these homes from the analysis did not change the results.

Finally, the Supplementary Appendix contains findings of a cross-section probit analysis of likelihood of care home closure when domiciliary care supply was measured using capacity (available supply) and utilisation (number of people supported), data for which were available from a national staffing database. Data on capacity and utilisation were matched at postcode-district level (first half of a UK postcode, for example, SW1) to a cross-section of care homes in April 2015 which included all homes’ status in October 2016. The results were largely similar to those reported in the main analysis. In particular, there was a significant negative influence of domiciliary care capacity on the likelihood of closure.

Discussion

LTC policy in many countries has increasingly focused on prevention and care at home. Despite this, little evidence exists of the impact this has on the performance of care homes. Using data from England this work analysed the influence domiciliary care supply has on the likelihood of care home closure. The analysis found no evidence that increased domiciliary care provision in local markets resulted in care home closures. Indeed, for some specifications there was evidence of a complementarity – more domiciliary care provision significantly improved the likelihood of survival for a care home.

Higher domiciliary care in an area should imply that care home demand from those with lower levels of needs will reduce. Instead, care homes would have to focus on those with higher needs levels. In the United States, substitution between domiciliary care and care home shows some evidence of higher needs levels on entry into a care home over time (Kane et al., 2013; Young et al., 2015). This in turn should increase competition between homes. However, no significant negative competition effect was found in the analysis, unlike earlier work for England (Allan and Forder, 2015).

One potential explanation for these findings is that an increasing older population nationally means that demand pressures allow for growth in both forms of LTC, limiting competitive pressures (Competition and Markets Authority, 2017; Wittenberg et al., 2011). Similarly, slower growth in the number of people able and willing to provide informal care compared to older population growth means that there is scope for increased domiciliary care provision without impacting on the performance of care homes (Colombo et al., 2011; Gaymu et al., 2007; Pickard, 2015). While the analysis found no influence on closures from the inclusion of differences in informal care provision between areas, the effect of changes to informal care over time was not analysed.

Alternatively, the complementary relationship could be an indication of firms offering similar products using the location of their rivals to indicate suitable markets, that is, areas of strong demand (Toivanen and Waterson, 2005). The growing supply of domiciliary care could have utilised the mature care home market as an indicator of where best to locate. This would have implications as to appropriate levels of service provision in areas with lower demand, such as more rural regions with lower populations. LTC policies would need to carefully consider how to promote the availability of services in low demand areas so as ensure geographical inequalities such as those observed for healthcare in England and elsewhere in Europe do not arise (Cookson et al., 2016; Perucca et al., 2019). In England, there is considered a good access to available care home supply for virtually all of the country (Competition and Markets Authority, 2017). However, while nursing home supply became more equally distributed to population over time at the regional level, a wider disparity in places to population was apparent at lower geographical levels (Ford and Smith, 2008).

A further explanation to the complementary relationship found is that there is a degree of industry integration taking place. Established care home providers may move to provide local domiciliary care, and vice versa. As already noted, there was certainly a degree of integration taking place and there may be advantages to providers in supplying both services, for example, cross-subsidisation of businesses, increased demand and potential cost savings in recruitment and administration. However, the validity of the first of these potential advantages is open to question given the issues with funding levels across all forms of LTC currently. Moreover, results did not change when removing from the analysis care homes that were also registered to provide domiciliary care.

Adult LTC in England is predominantly delivered by private providers with competition in price and quality, and this is also increasingly the case for many other countries (Marczak and Wistow, 2015; Riedel and Kraus, 2011). As such, the results reported here are of interest for policy internationally and contribute to the debate about the appropriate delivery and management of LTC systems given increasing levels of marketization (Pavolini and Ranci, 2008). It is of benefit for policy that these different forms of care would not seem to be direct substitutes. Many countries across Europe are currently increasing the provision of care at home or in the community, while some countries are increasing the availability of institutional care (Spasova et al., 2018).

The appropriate delivery of care has also gained particular attention given the COVID-19 pandemic. In England, the pandemic was initially considered as a short-term shock to demand in the care homes market, with occupancy levels expected to return to pre-pandemic levels (National Audit Office, 2020). Nonetheless, it is also likely that the impact of the pandemic will have accelerated changes in LTC systems (Werner and Bressman, 2021). The findings in this work indicate that an increase in supply of one main form of LTC need not come at the cost of a reduction in the other. Even so, as changes to LTC systems occur across Europe, in conjunction with increased demand from an ageing population, it is important that both forms of care are available to the population and that their complementary nature is promoted (Ilinca et al., 2015; Werner et al., 2020).

The findings also provide a further implication as to the role the public sector plays in the procurement of services. In England, LAs have market power in the care homes market and tend to pay lower prices compared to those who fund their own care (Competition and Markets Authority, 2017). This public procurement of services will have an impact on the supply-side of the market (Forder and Allan, 2014; Grabowski, 2004). The findings of some estimations in the analysis support this: care homes in areas with higher relative levels of per capita public expenditure on older people in care homes, which would imply a greater reliance on public funding and lower levels of self-funding clients, had a significantly increased likelihood of closure.

Rising demand and decreasing availability of informal care have implications for LTC budgets across Europe which governments must carefully consider (e.g. Pickard et al., 2010). There has been a broad de-universalisation of LTC services, with many countries in Europe cutting funding or restricting availability through stronger eligibility criteria (Gori et al., 2015; Spasova et al., 2018; Szebehely and Meagher, 2018). Adult LTC expenditure in England has fallen largely in real terms and the number of people supported has similarly fallen, although this masks variations locally (Humphries et al., 2016).

Nonetheless, increased choice for consumers from diverse local LTC markets has coincided with policies aimed at giving individuals greater control in their care (Pavolini and Ranci, 2008). An explanation for the complementary relationship found in this analysis for England is the productive market shaping of local markets by LAs to allow providers of many different forms of LTC to achieve success, increasing consumer choice (Needham et al., 2020). However, as noted above, the marketization of care, while promoting efficiency, can lead to implications for access to care and potentially increased inequality (Brennan et al., 2012; Szebehely and Meagher, 2018). Any impact on service users will also depend on the quality of services and their impact on quality of life (Forder et al., 2018; Moberg et al., 2016; Vanleerberghe et al., 2017). Overall, LTC policies across Europe must carefully consider the impact of increased choice and consumer power and how it affects individuals and providers in care markets (Pavolini and Ranci, 2008; Rodrigues and Glendinning, 2015).

Limitations

There are limitations to this research. First, the analysis used data from a relatively short period of time and findings may not fully reflect the domiciliary care and care home relationship outside of this timeframe. The analysis of care home closures also did not include important factors such as care home price, revenue and staffing because of data availability. The lack of data available on changes to informal care provision over the period analysed has already been noted. Further improvements in data availability, for example, temporary versus permanent stays in care homes, different forms of domiciliary care such as live-in care and national data on domiciliary care utilisation, would also improve future analyses. Finally, the findings cannot reflect any changes that the COVID-19 pandemic may have brought to the English LTC system, the impact of which would need to be considered in future research.

Conclusion

Using data for England, this analysis has found that domiciliary care does not have a significant negative influence on care home performance, with some evidence of a complementarity between the two forms of LTC. This finding has potentially important implications for LTC provision in many countries amid growing demand and ongoing reforms that are increasing marketization.

Supplemental Material

sj-pdf-1-esp-10.1177_09589287221083835 – Supplemental Material for Care home closure and the influence of domiciliary care supply: Evidence from England

Supplemental Material, sj-pdf-1-esp-10.1177_09589287221083835 for Care home closure and the influence of domiciliary care supply: Evidence from England by Stephen Allan in Journal of European Social Policy

Footnotes

Acknowledgements

I would like to thank Jeni Beecham and Nick Smith for helpful discussions, two anonymous reviewers for their suggestions and also attendees at the Business and Local Government Data Research Centre (BLG DRC) Conference, London, 28th November 2018.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The study was funded by the National Institute for Health Research (NIHR) Policy Research Programme (References PR-PRU-103/0001 and PR-PRU-1217-21101). The views expressed are those of the author and not necessarily those of the NIHR or the Department of Health and Social Care.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.