Abstract

The enormous growth in house prices in Europe since the 1990s has led to increasing concerns about the affordability of housing for ordinary citizens. This article explores the relationship between housing affordability – house prices relative to incomes – and the demand for redistributive and housing policy, using data drawn from European and British social surveys and an analysis of British elections. It shows that, as unaffordability rises, citizens appear in aggregate to become less supportive of redistribution, interventionist housing policy and left-wing parties. However, this aggregate rise, driven by the predominance of homeowners in most European countries, masks a growing polarization in preferences between renters and owners in less affordable regions.

Introduction

There has been a recent surge in scholarly interest in the political effects of inequality in the advanced industrial world. However, most existing work has focused on inequalities in labour market incomes, neglecting the growing importance of inequality in wealth and, in particular, housing. As Fuller et al. (2020) show, changes in house prices are largely responsible for short- and long-run shifts in wealth inequality in the industrialized world. In most wealthy countries there has been a surge in nominal house prices since 1990, barely broken by the crash of 2008/9 (Knoll et al., 2017), even though incomes have stagnated. This housing boom – and the ensuing growth of wealth inequality – has created winners and losers. Increases in housing prices, which translate into increased rents, mortgage payments and down-payments, often cause severe burden on many households’ budgets (Albouy et al., 2016; Dewilde, 2018; Dustmann et al., 2018). The flip-side of growing unaffordability is the emergence of a large group of ‘winners’: people with modest incomes but rapidly appreciating assets, whose welfare is increasingly attached to their homes not their jobs (Ansell, 2014).

One might expect serious political consequences to housing unaffordability. However, the precise direction of these consequences is not entirely obvious. On the one hand, people unable to enter the housing market might seek greater government support through housing policy or through redistributive transfers. Some scholars viewed the relative success of Jeremy Corbyn’s Labour Party in 2017 as reflecting this squeezed ‘Generation Rent’ (Ansell and Adler, 2019). On the other hand, there are clear beneficiaries of unaffordable housing – those who own it. Homeowners may seek to protect their windfalls from direct taxation or the indirect threat of new construction. Existing work, however, looks only at house prices in absolute terms and looks only at redistribution not housing policy preferences. As yet, we do not have empirical clarity on whether the surge in housing costs relative to incomes raises or lowers the demands for such policies. Nor do we know whether homeowners and renters are reacting differently to this new environment.

In this article, we argue that housing unaffordability plays a key role in shaping both overall support for redistributive fiscal and housing policy and the degree of polarization between renters and homeowners in their preferences. Following Ansell (2014), we claim that higher housing prices relative to income produce a net windfall for homeowners that they are anxious to protect from both taxation and the construction of new housing that might push prices down. Hence, rising unaffordability leads to an aggregate shift to less redistributive policy attitudes, more right-wing voting and greater antipathy to government intervention in housing markets, largely because in almost all European regions, homeowners form a majority and want to protect the value of their housing.

This overall ‘right-ward’ shift masks underlying polarization, however. Renters, since they do not own housing assets, do not benefit directly from rises in the price of these assets. Less affordable housing may make them relatively more supportive of the government intervening in the housing market. Thus, as unaffordability increases we expect to see the preferences of homeowners and renters to diverge substantially. Unaffordability produces polarization.

We test these propositions using a wide variety of data sources. We begin by examining housing unaffordability across Europe, drawing data on affordability from the EU-SILC household panel and matching it at the regional level to policy preferences in the International Social Survey Program. This regional data allows us to move beyond existing work, which largely examines house prices at the national level or within single countries. We show that regions with less affordable housing also tend to have lower support for redistribution and interventionist housing policy and that this effect is mainly concentrated among homeowners. We then turn to the United Kingdom to examine both housing policy preferences and voting outcomes. We start by looking at how regional affordability conditions the housing policy preferences of owners and renters, using the British Social Attitudes Survey. Finally, we develop original measures of housing affordability at the parliamentary constituency level and examine how changes in affordability connect to changes in support for the Conservative Party. These three separate analyses permit us to move from how housing affordability affects individual preferences to its impact on individual behaviour, as well as considering the degree to which housing affordability polarizes not only attitudes towards housing policy itself but also towards the broader role of government in narrowing market differences.

Argument

Although the boom in property prices relative to incomes since the 1990s has been one of the core economic trends of the past two decades, social scientists have only recently turned to examine property prices as determinants of political preferences and behaviour. Early work, beginning with Kemeny (1981) drew out a potential connection between housing markets and support for the welfare state. Kemeny argued that the rise in private homeownership over the 20th century – and accelerating since 1945 – was creating a class of citizens who would depend less on the state for support, having a valuable asset to fall back on, and who would be more tax-sensitive given the costs of affording down-payments and mortgage payments associated with the purchase of a property. Castles (1998) and Conley and Gifford (2006) both demonstrated a cross-national negative relationship between homeownership rates and the size of government.

The political and social effects of the housing market are not about ownership alone. Property prices also matter – both absolutely (as returns to residential investment) and relative to incomes (in terms of affordability). Indeed, the major shift of the past few decades has not been in ownership rates, but the relative price of housing. Furthermore, Fuller et al. (2020) show that the effects of housing on wealth inequality travel through price differences not ownership rates per se. So how might rising housing prices, relative to income, matter for policy preferences?

Existing work looks at absolute prices rather than prices relative to income, thereby largely neglecting housing affordability. Scheve and Slaughter (2001), in important early work, argue that homeowners in areas exposed to international trade tend to be less supportive of free trade as it is likely to push down the value of their house. Ansell (2014), by contrast, examines the determinants of domestic social policy preferences. He argues that rising house prices make owners less supportive of the welfare state and redistribution since increased prices act as a ‘windfall’, increasing homeowners’ permanent income. That, in turn, makes them more tax-averse and less in need of social insurance to cover bad times. Hence, owning a house acts as a form of ‘private insurance’. In this line of scholarship, researchers look at why the value of assets such as housing might matter for policy preferences controlling for labour market incomes. However, rather than looking solely at the impact of housing net of income, we also need to consider housing relative to income.

Relative levels – housing affordability – matter in a number of ways. We can think of this both in terms of housing costs relative to income and the value of housing assets relative to income. Housing is distinct from most other categories of consumer spending since it has both consumption and investment value. On the consumption side, annual housing costs reflect how much people are willing to pay for shelter in various locations and qualities of residence. These costs might be incurred through rents or through purchasing a house, typically amortized through a mortgage. When the costs of shelter in a particular location or residence rise relative to the income used to pay these costs, this clearly places pressure on household budgets. For a renter, whose rent payments are fully transferred to their landlord, this has no obvious upside. However, home-owners who pay their housing costs through a mortgage are not solely consuming ‘shelter services’ they are also investing in the very asset in which they live. Eventually, once the mortgage is paid off, they own the asset outright. And the effects of rising house prices only matter when they initially take out a mortgage. From their perspective, higher house prices may produce initially higher down-payments and monthly mortgage payments that in part accrue to the mortgage lender, but they also increase the value of the asset they own. Relative to income, the former is a burden but the latter a boon. And over time the latter massively outweighs the former.

Finally, for those who own their house outright, they incur no housing costs (presuming imputed rents are not taxed) and their investment rises in value. If their incomes stagnate but house prices rise they are substantially better off. The housing boom has created legions of dollar millionaires across the industrialized world. People with relatively modest incomes have found themselves owning properties that are several multiples of their annual income in value. For these people, the ‘affordability crisis’ does not feel like a crisis – it feels like a boon.

So, housing becoming more unaffordable relative to incomes has countervailing effects on people’s material circumstances. What does this mean for their policy and political preferences? In this article we focus on two sets of attitudes. First, we look at attitudes to redistribution, which, following Svallfors (1997), Cusack et al. (2006), and Brady and Bostic (2015), we use as indicative of a general left–right economic dimension. Second, we look at attitudes to government intervention in the housing market in order to make housing more affordable (by subsidizing either housing construction or providing resources to citizens to help them afford housing).

For homeowners, the story is a simple materialist one. 1 When house prices rise relative to income, they become better off since their housing costs remain flat relative to income while the investment value of housing rises. Per Ansell (2014), homeowners will respond by desiring less social insurance and by becoming more tax-averse (see also Ansell and Adler, 2019; Ansell et al., 2018; Stegmueller, 2013). Hence, we expect homeowners to become less supportive of redistributive policies or the parties that support them when housing unaffordability increases.

Similar forces are at work when we consider the effect of rising housing unaffordability on homeowners’ attitudes towards government housing policy. If the value of their asset is rising relative to incomes, homeowners benefit. Government intervention in housing markets, by contrast, may threaten the value of this investment. In particular constructing new houses, by raising housing supply, pushes down the value of existing houses. Government spending on access to housing for non-homeowners or renters has a less direct effect on house prices (and could even boost them) but the problem with these policies from the perspective of homeowners is that they are very unlikely to be beneficiaries of such schemes but will have to pay the taxes needed to fund them. Overall, we anticipate homeowners will thus oppose government intervention in housing markets aimed at improving affordability.

For renters, the effects of growing unaffordability are slightly more complicated. On the whole we would expect rising house prices relative to income would drive renters to more redistributive preferences. Since rents typically rise with house prices, it may be ever harder for them to pay the rent, presuming that incomes remain flat. It will also make it more difficult to ever get on the property ladder. For many renters, these struggles may increase their support for redistribution and the left-wing parties that support it – particularly if they are struggling to make payments. There is a nuance here, though. Redistribution typically means clawing back larger shares in taxation from individuals with higher labour market incomes. For higher-income renters, higher redistribution may be a ‘double whammy’ – losing more of their labour market income and facing higher relative house prices/rents. For authors in the tradition of Kemeny (1981) this effect of taxation making it harder to get on the property ladder is an important component of the homeownership/welfare state trade-off. For renters then, the effects of unaffordability on redistributive preferences may be mixed. Compared to homeowners, however, they are clearly less likely to view redistribution more negatively as relative house prices rise.

With regard to housing policy preferences, renters should have more clear-cut views. Government intervention in housing markets to increase affordability, either by building more houses or subsidizing their purchase, is largely beneficial for renters – it reduces the net cost of getting on the housing ladder and is likely to reduce rents for those who remain tenants. As local unaffordability rises, the benefits of such policies should be particularly salient for renters. 2

Putting these two mechanisms together, we expect that in the medium-run overall rising unaffordability of housing should lead to less support for redistributive policies and less support for left-wing parties. Homeownership in almost every European country hovers over 50% of adults and is typically higher among voters. Combined with the fact that homeowners have straightforward anti-redistributive preferences in the case of rising house prices, whereas renters may have ambivalent attitudes, we anticipate that unaffordability will both drive aggregate preferences away from redistributive or interventionist policies and parties and widen the gap in preferences between homeowners and renters. These expectations are summarized in Hypotheses One and Two.

One: More unaffordable housing should on average lead to lower support for redistribution, interventionist housing policies and the (left-wing) parties that promote them.

Two: More unaffordable housing should lead to greater polarization between homeowners and renters in their preferences about redistribution and interventionist housing policy.

Housing affordability and attitudes: evidence from Europe

In this section, we examine the connection between housing affordability at the regional level and support for redistribution and housing market intervention across Europe. To do so we integrate two well-known existing datasets in an original way. We use the EU-Survey on Income and Living Conditions (EU-SILC) to generate our measures of housing affordability by country and region. 3 We then match this at the regional level to the International Social Survey Programme for 2006 and 2009. Our interest is in examining the macro-level effects of living in countries and regions with different levels of housing affordability on redistributive and housing policy preferences, as moderated by homeownership. In other words, how do people in general – and homeowners in particular – respond to their housing affordability environment when determining their attitudes towards redistribution?

Hypotheses One and Two look at how housing affordability and homeownership structure attitudes about redistribution and housing policy. To capture attitudes about redistribution we use the 2009 ISSP, which asks people whether ‘it is the responsibility of governments to reduce differences in income between people with high incomes and those with low incomes’. This general redistribution question has been widely used by political economy scholars seeking to capture attitudes towards government spending and the role of the state (Cansunar, 2021; Rehm, 2011), including existing work on housing and redistributive attitudes (Ansell, 2014; Ansell et al., 2018). We thus use this question to provide a general indicator as to whether housing affordability concerns provoke general shifts on the standard left–right economic dimension. The ISSP redistribution question, while commonly used, does have limitations – countries start from very different existing baselines of taxation and redistribution. In order to check our analyses of the relationship between affordability and economic left–right measures, in Appendix Table A1 we also examine a number of related dependent variables – party choice, taxing the rich and views on inequality.

We also examine the 2006 ISSP, which asks a question about people’s attitudes towards whether the ‘government has a responsibility to provide decent housing’. This allows us to directly examine whether rising housing unaffordability activates demand for increased or decreased public spending on housing. Unfortunately, the 2006 ISSP does not include a measure of individual housing tenure. However, we use the predicted relationship between individual demographics and homeownership in 2009 to generate a ‘homeownership propensity’ for 2006 in order to separate out individuals who are more or less likely to be homeowners given what we know about the determinants of housing tenure.

Our core independent variables are regional housing affordability and individual home ownership. We begin by setting out the development of our housing affordability variables. We analyse eight countries in 2006 (Denmark, Finland, France, Germany, Norway, Spain, Switzerland and the UK) with 58 regions and 11 countries (Austria, Belgium, Denmark, Finland, France, Germany, Norway, Spain, Sweden, Switzerland and the UK) with 70 regions in 2009 using the cross-sectional EU-SILC household survey. We group households by country and NUTS2 region and calculate statistics on housing affordability for these region–country–year groups. 4 For each variable we use the EU-SILC’s survey weights to calculate weighted averages for each group. 5

We use a variety of different measures of housing unaffordability at the regional level. We begin with the average monthly cost of housing in euros at the regional level for all households (Average Cost). We split our measure of average costs into those paid on average by homeowners in that region (Owner’s Cost) and those paid by renters in that region (Renter’s Cost). We also look at the regional coefficient of variation in housing costs – the standard deviation divided by the mean (COV Cost). As measures of relative cost we look at average housing cost as a proportion of average gross income (Cost/Gross Inc) and as a proportion of net income (Cost/Net Inc.), all measured at the regional level. Figure A2 provides a graphical presentation of housing costs in Europe between 2006 and 2017. 6

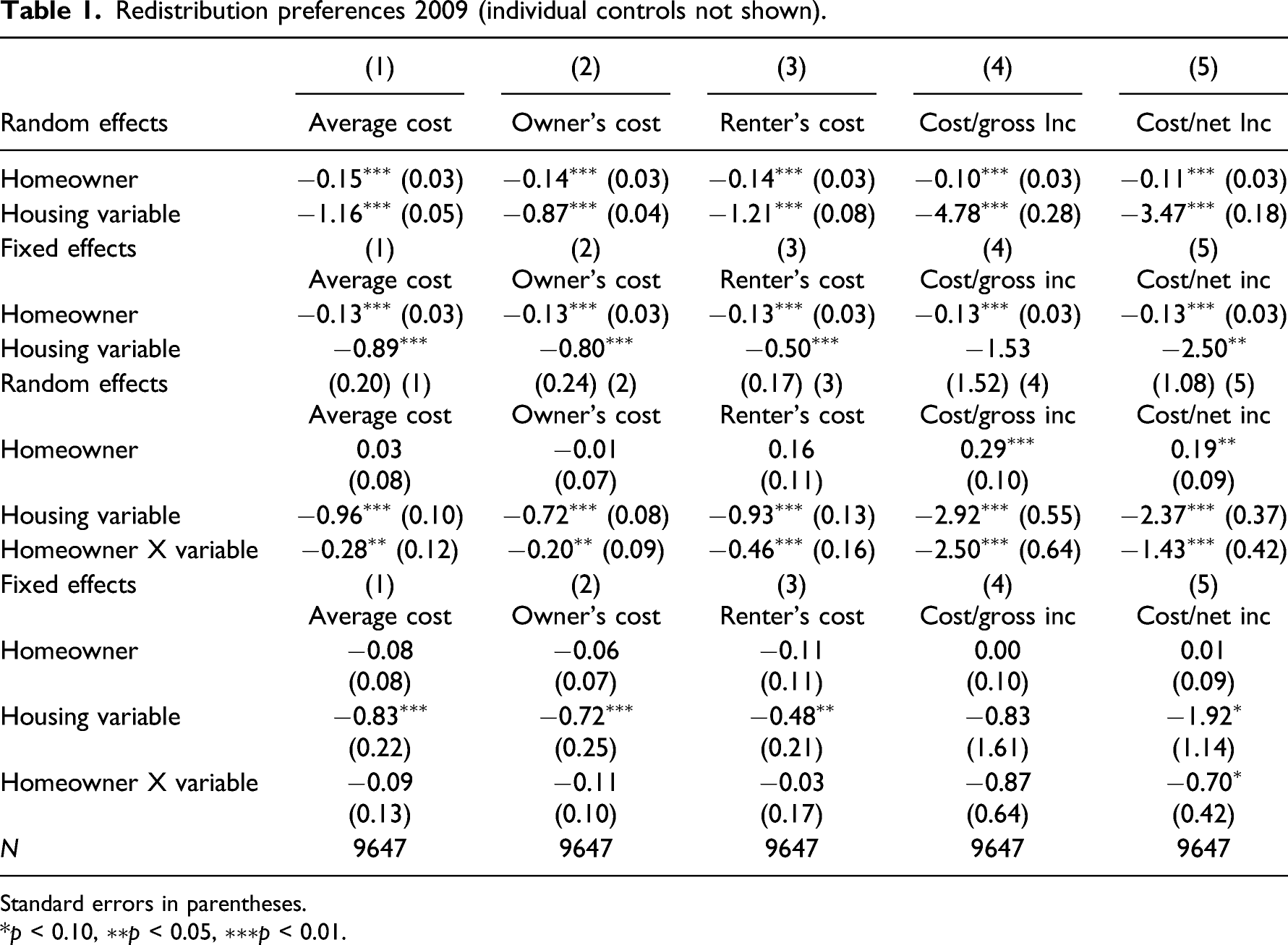

Redistribution preferences 2009 (individual controls not shown).

Standard errors in parentheses.

*p < 0.10, ∗∗p < 0.05, ∗∗∗p < 0.01.

The top two panels show the direct effects of homeownership and housing affordability on redistributive preferences and with country random effects or fixed effects. We see strong evidence of two things – first that homeowners tend to be less supportive of redistribution in general and second that regional levels of higher housing costs tend to reduce support for redistribution. Focussing on Model 5 – regional housing costs as a proportion of net income – we see moving from the 10th to 90th percentile on this variable lowers support for redistribution by 0.66 – over half a standard deviation. Except in Model 4 we also find the same pattern for within-country regional differences in affordability – that is, in more unaffordable regions there is less support for redistribution, even netting out the general national level of unaffordability.

Moving to the bottom two panels we see that the relationship between higher housing costs (absolute or relative to income) and declining support for redistribution is particularly strong among homeowners, especially in the random effects models.

11

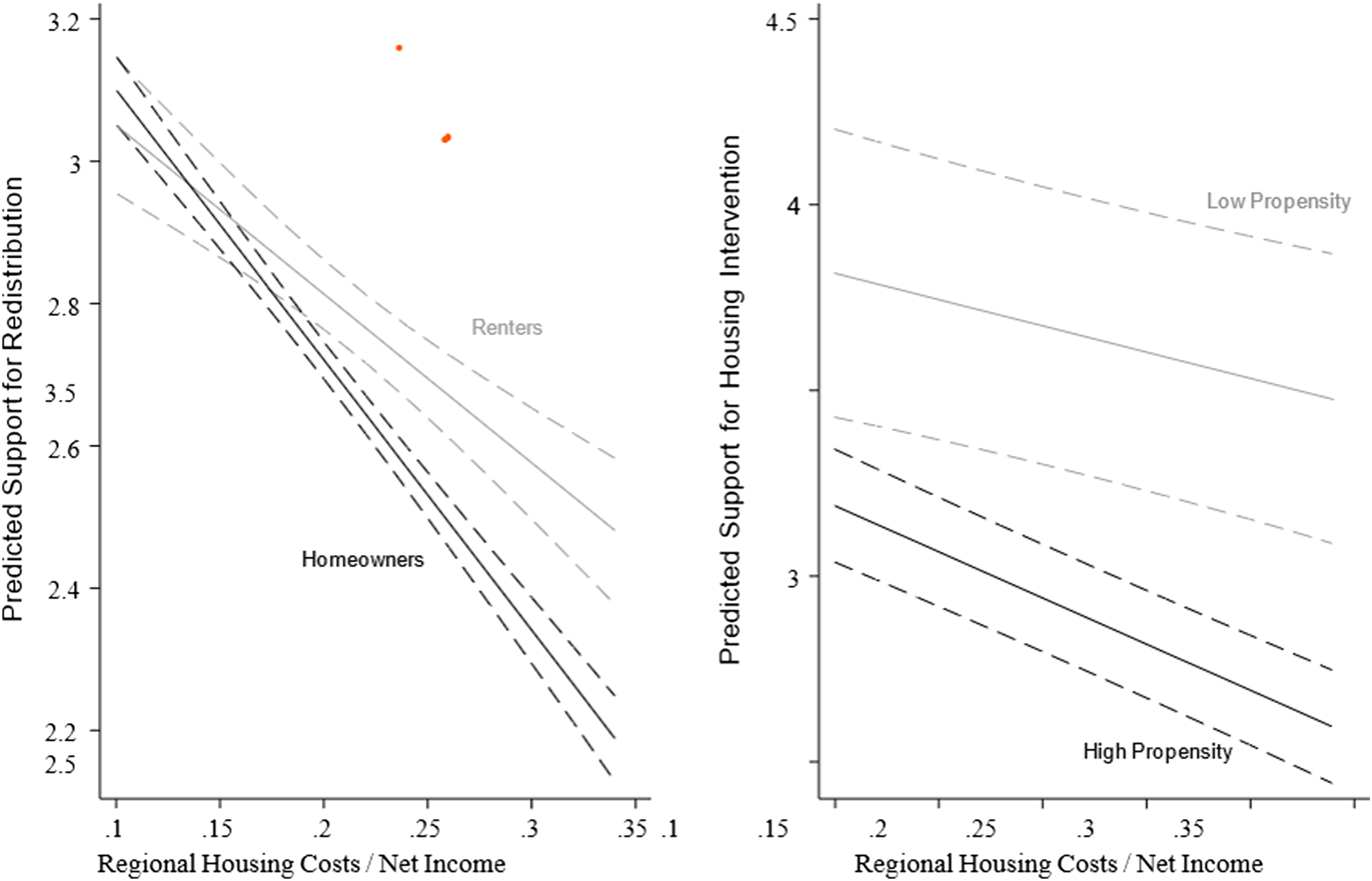

The left figure of Figure 1 demonstrates this pattern with Model 5 from the third panel – we see that homeowners appear to respond to unaffordability more negatively in terms of redistribution preferences vis-à-vis renters. Note though that there does appear to be a general negative relationship between housing costs and redistribution preferences for both groups and this is robust to both random and fixed country effects. Regional housing affordability and predicted support for redistribution (left) and housing intervention (right).

As we noted above, redistributive preferences may not fully account for attitudes along the left–right economic spectrum. In Table A1 in the Appendix we examine three different dependent variables that measure economic left–right preferences – first, vote choice (a five-point scale increasing to the right, drawn from the ISSP’s party choice indicator); second, support for people with higher incomes paying a larger share in taxes (a five-point scale increasing in support); and third, agreeing with the statement that ‘differences in income in [the respondent’s country] are too large’ (a five-point scale increasing in agreement). In all cases we examine the fifth model from the bottom two panels of Table 1– that is the interactive effect of house prices as a ratio of net income and homeownership. We see that homeowners in areas with higher unaffordability are more likely to support right-wing parties, less likely to think the rich should pay more in taxes and less likely to think income differences are too large. Accordingly, we find ample support that the choice of the redistribution question in Table 1 is consistent with wider left–right attitudes.

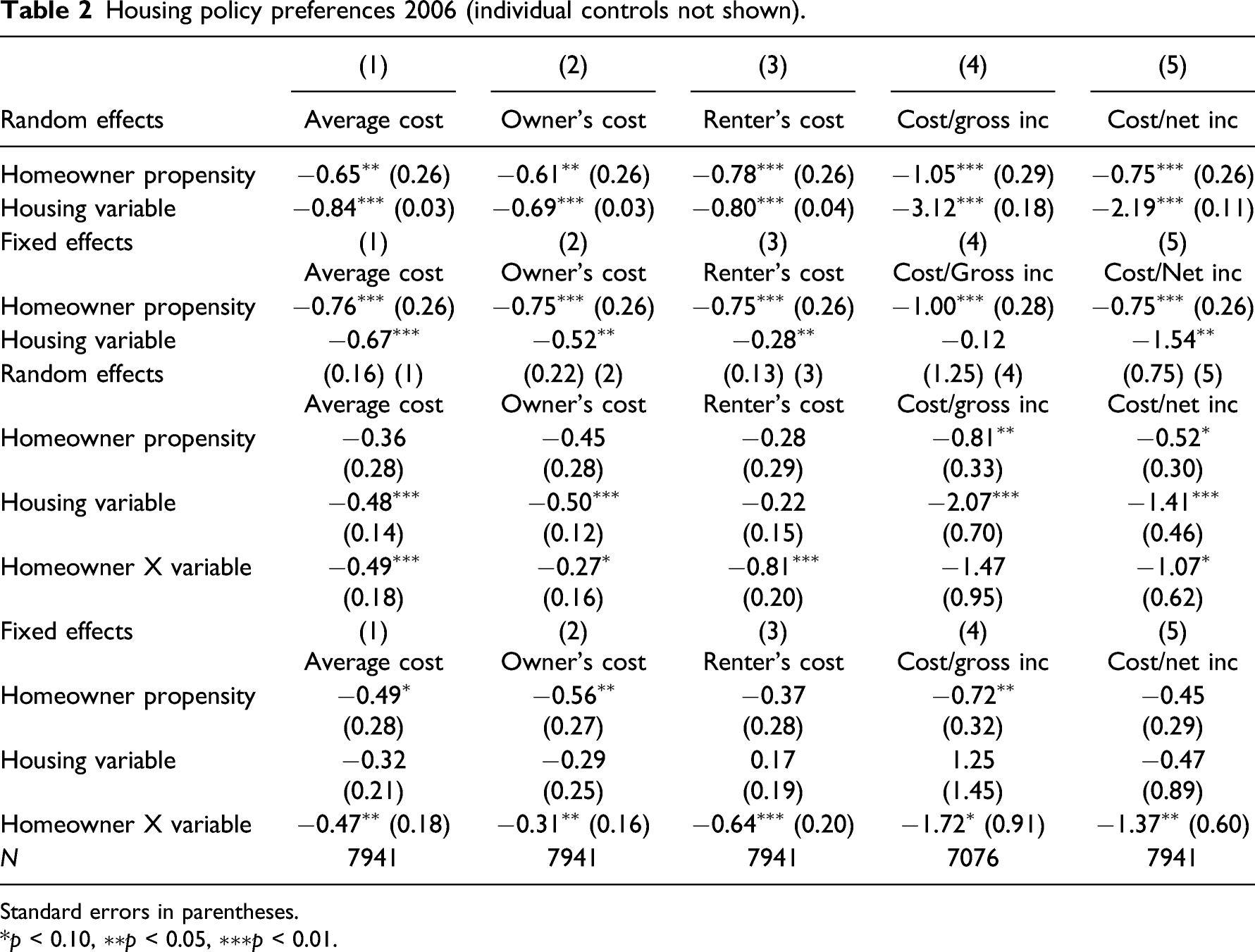

Housing policy preferences 2006 (individual controls not shown).

Standard errors in parentheses.

*p < 0.10, ∗∗p < 0.05, ∗∗∗p < 0.01.

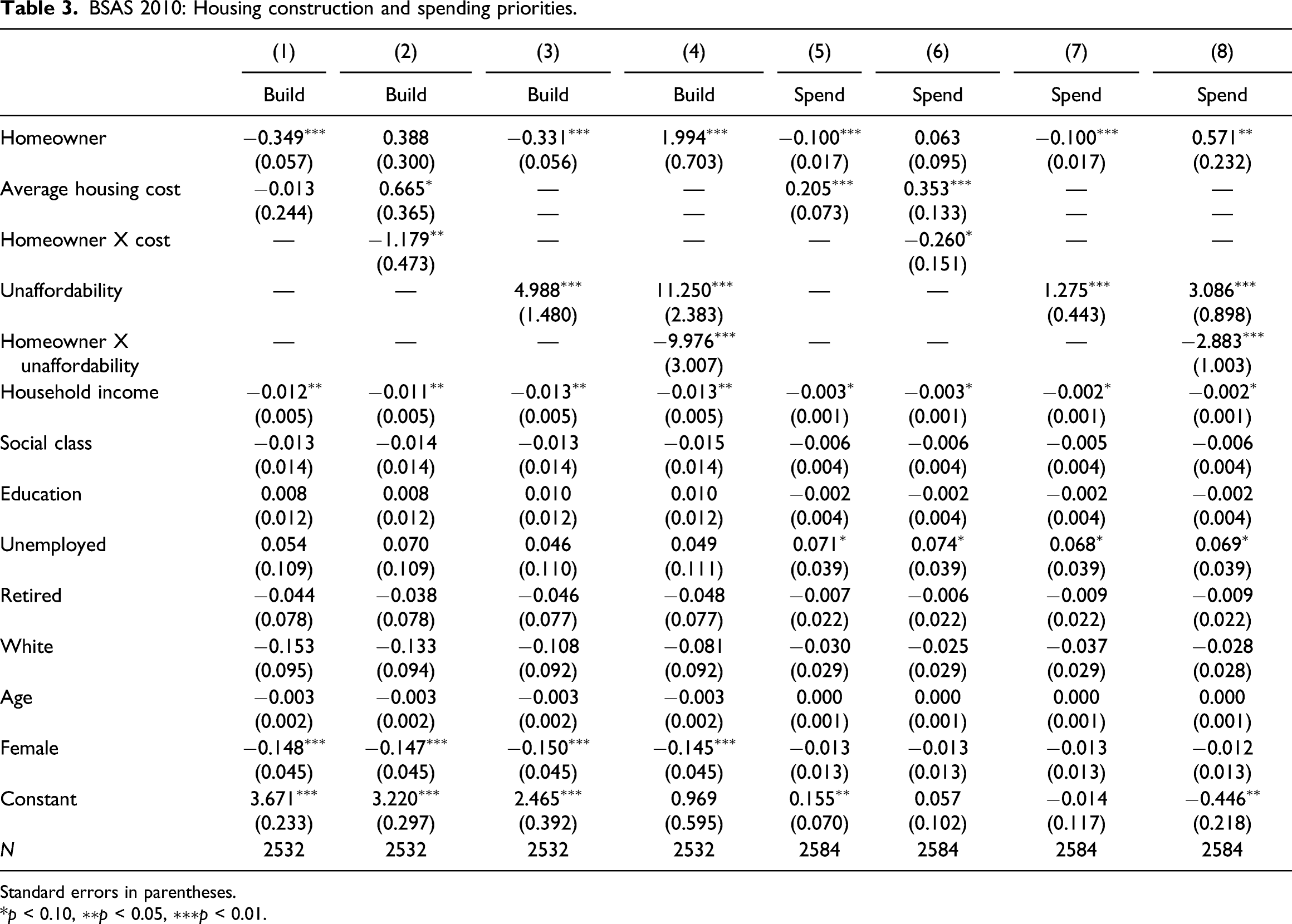

BSAS 2010: Housing construction and spending priorities.

Standard errors in parentheses.

*p < 0.10, ∗∗p < 0.05, ∗∗∗p < 0.01.

The patterns are strikingly similar to what we saw for redistribution, providing strong evidence that housing policy preferences and redistribution preferences are driven by similar factors. People predicted to have a higher propensity to be homeowners are less supportive of government responsibility for housing across all nine models. Individuals living in regions with higher housing costs, whether absolute or relative to income, are also less supportive of government intervention in housing. Finally, the interaction effects between homeowner propensity and the affordability measures are also present, including in most of the fixed effects models. Homeowners in more unaffordable regions are even less positively inclined towards government intervention in housing. The right figure of Figure 1 demonstrates that the relationship between net affordability and support for government intervention in housing is substantially stronger for people with a high propensity to be homeowners than those with a low propensity (the negative slope is statistically significant for both groups but larger in the latter case).

Finally, Tables A1 and A2 in the Online Appendix show that the negative effects of housing cost relative to gross or net income at the regional level are robust to other regional controls including regional income, homeownership, income tax burden and housing burden, all taken from the EU-SILC. Homeownership rates and average income correlate negatively with redistribution/housing support. Income tax burden correlates negatively in the random effects models. In sum, we have seen that in regions of Europe with more expensive housing, particularly as compared to disposable income, support for redistribution and government spending on housing is lower and that this effect appears to be particularly concentrated among homeowners. This suggests a potential polarization of European politics as homeowners in expensive areas pull away from those less fortunately situated in the housing market.

Housing affordability in the United Kingdom

We now turn to examine the political implications of housing affordability in a single country: the United Kingdom. We choose to analyse the UK for two reasons. First, the UK has both relatively high unaffordability, with an average ratio of housing costs to disposable income of around 24% in 2010, and high regional variation in affordability (the second highest in the EU-SILC data after Greece). This means affordability is highly salient politically in the UK due to its high level, but that there is also sufficient variation within the country to provide empirical traction for how local differences shape attitudes. Second, the UK has excellent data availability on house prices at the regional and local level, which we can match to surveys and election results. Finally, as Fuller (2019) convincingly argues, the commodification of the UK housing market makes housing inequality particularly salient in the British context.

We begin by looking once more at survey data to examine how regional affordability affects policy attitudes. We employ the British Social Attitudes Survey from 2010 which has a unique set of questions asking people about their attitudes towards housing policy. The BSAS also codes people by which of 12 UK regions they live in, which we can match to housing affordability data from the EU-SILC. We then turn to political outcomes. Here we are able to look at an even lower level of aggregation, calculating housing affordability at the constituency level and seeing how changes in affordability are associated with changes in voting patterns along Britain’s long-standing left–right dimension.

Housing affordability and public attitudes in Britain

We saw in our analysis above of regional data in Europe that housing unaffordability was associated with a divergence between homeowners and renters in their preferences over government responsibility for decent housing. With the ISSP 2006 however we had to estimate the propensity to own a house. By contrast, the British Social Attitudes Survey (BSAS) in 2010 has both information about an individuals’ housing tenure and their views about housing policy. Accordingly, we have a more direct test of whether regional unaffordability polarizes the housing policy preferences of owners versus renters.

We draw two housing policy questions from the BSAS. First, we use a question about housing supply: ‘Would you support or oppose more homes being built in your local area?’, which is on a five-point scale from strongly oppose to strongly support. Second, we use responses to questions asking what respondents’ first and second priority for extra government spending would be. We code this as one if respondents mention housing as a first or second priority and zero otherwise.

We run a series of linear regressions with these two dependent variables and use as our core predictors a dummy for homeownership and an indicator of regional housing – in turn we use monthly average housing costs and these costs as a proportion of disposable income (net unaffordability). 13 In odd numbered models we include these items separately, whereas in even numbered models we include their interaction as well. We also include a wide array of individual-level controls: household income, social class, education, age and dummies for being female, unemployed, retired or White British in ethnicity.

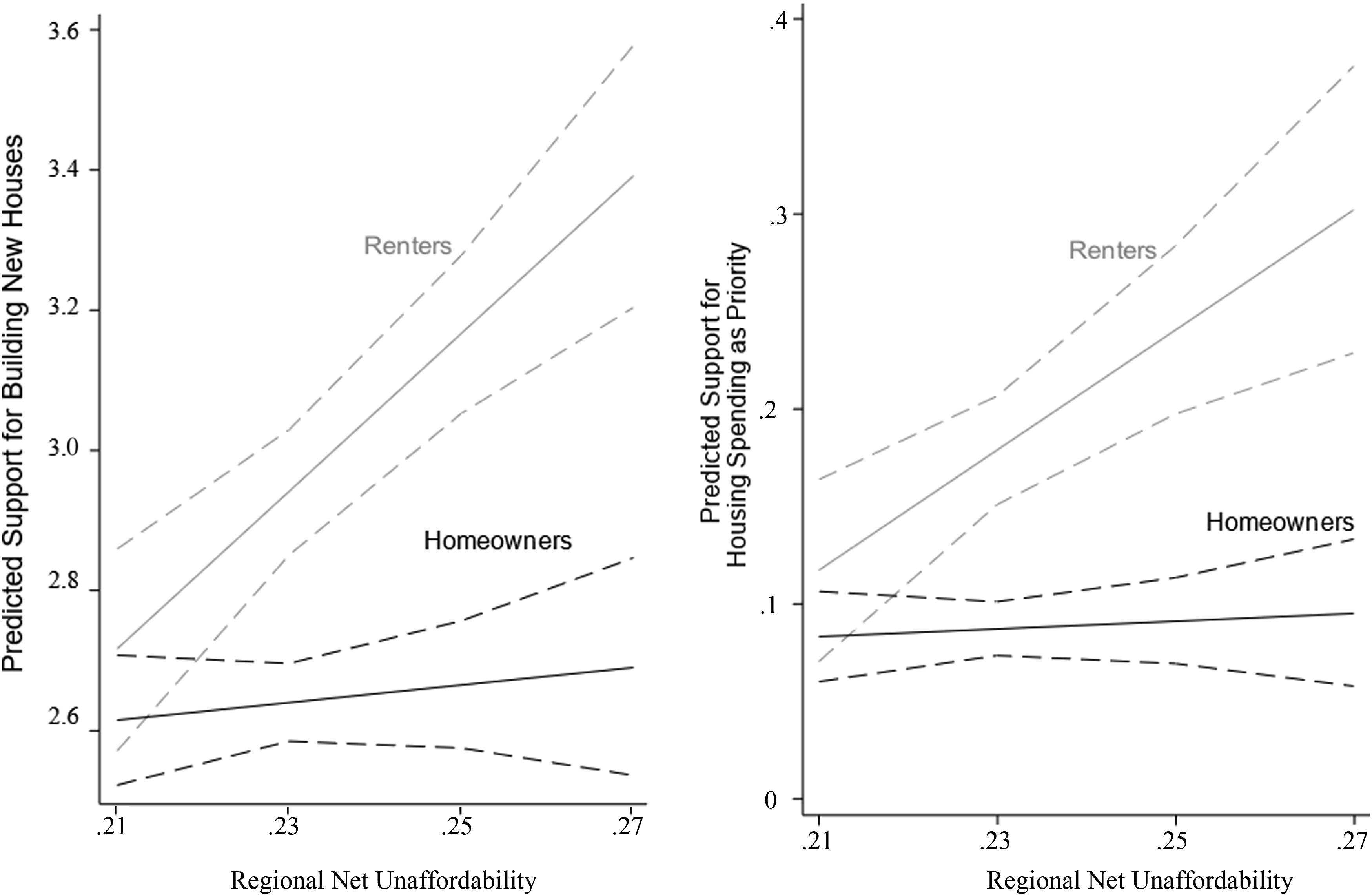

Models 1 to 4 of Table 3 look at support for building new houses locally. In Models 1 and 3 we see a strong negative impact of being a homeowner on support for building houses: an effect twice as large as being female or moving from the 10th to 90th percentile in income. Clearly, on average homeowners are much less likely to support construction. However, this effect is much more pronounced in areas with more expensive housing, as seen in the negative coefficients on the interaction of homeownership with the two regional housing variables.

Renters and owners have greatly diverging preferences, where housing is expensive both absolutely and relative to incomes. This can be seen clearly in the left panel of Figure 2, which uses net unaffordability as the regional context variable.

14

Where housing is relatively cheap (on the left of the graph) homeowners and renters have statistically indistinguishable preferences, but as we move to the most unaffordable areas (on the right) renters and owners are almost a full point apart in their preferences. Net affordability and support for construction (left) and placing housing as a priority for government spending (right).

Models 5 to 8 show a similar story when we turn to placing housing as a priority for government spending. Again, we see homeowners are 10% less likely than renters to view housing as a priority. But this is an average effect – once we take regional variation in affordability into account, we see again that renters and owners have similar preferences in the more affordable areas and diverge substantially in unaffordable areas – by up to 20% points, as can be seen in the right panel of Figure 2.

In sum, the BSAS survey data shows that homeowners are generally unsupportive of interventionist housing policy – as we saw in our analysis of the ISSP – but that this relationship is dependent on local affordability. Where housing is affordable, renters and owners are not polarized in their views. This divergence only emerges in expensive areas.

Housing affordability and elections: Evidence from British general elections 2010–2019

How do changes in the preferences over policies driven by raising housing costs translate into electoral outcomes? We conclude by examining the electoral consequences of housing costs and unaffordability in the UK. We do so by considering the proportion of votes cast at the electoral constituency level for the Conservative Party in England and Wales. As we outlined above, our expectation is that housing unaffordability should be correlated with growing support for the Conservative Party given its positive consequences for the (homeowning) majority of voters.

Our dependent variable is (changes in) the vote share of the Conservative Party at the parliamentary constituency in the General Elections of 2010, 2015, 2017 and 2019. As economic controls, for each electoral constituency and year, we use data from the Office for National Statistics, including estimates of the median gross weekly pay in each constituency, information on gross income reported for each decile and unemployment rates. Data on house prices comes from the UK Land Registry and includes all sales of houses and apartments in each constituency. Finally, we obtain demographic data from the 2011 Census in England and Wales (ethnicity, age structure and immigration status).

We assess voter responses to changes housing prices and (in)affordability using a first-difference model. For constituency i in election year t, we estimate the following equation

Changes in Conservative vote share, income and wealth.

Standard errors in parentheses.

*p < 0.10, ∗∗p < 0.05, ∗∗∗p < 0.01.

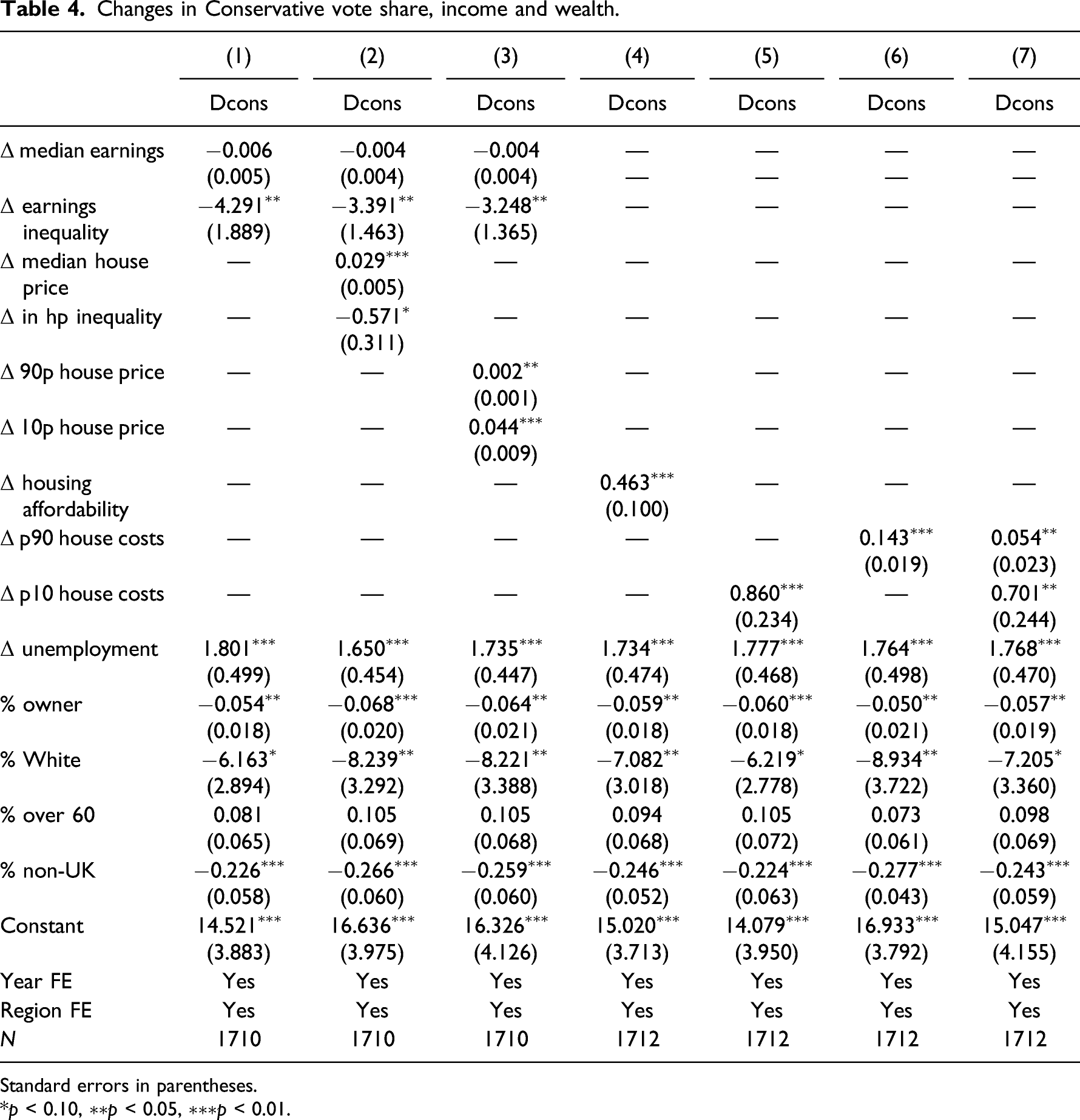

We now turn to the effect of house prices. Model 2 uses the change in median house prices and house price inequality at the constituency level, along with the changes in income and socio-economic controls, election fixed effects and region fixed effects. The results indicate that both changes in house prices and house price inequality affect the Conservative vote share significantly, albeit in different directions. We see that median house price growth increases support for the Conservatives. The estimated impact of a £50,000 increase in median house prices is associated with a roughly 1.5 point increase in the Conservatives vote share. By contrast, increased inequality in house prices, measured as the ratio of 90th percentile and 10th percentile house prices, significantly decreases support for the Conservatives.

Models 3 regresses changes in the 10th and 90th percentile of housing prices, on the changes in the Conservative vote share. A £50,000 increase in the 90th percentile house price is associated with a roughly 0.1 point increase in the Conservatives vote share. Increases in the 10th percentile of house prices have a much stronger positive impact on the electoral performance of the Conservative party: a £50,000 increase is associated with a 2.2 point increase in the Conservatives vote share. The coefficient on changes in the 10th percentile of house prices is larger in magnitude and statistically more significant than the coefficient of 90th percentile of house prices. In other words, prices going up in areas with less well-off homeowners – traditionally Labour voters – appears to convert them into Conservatives.

What about housing affordability – that is, the level of house prices relative to income? Models 4 to 7 examine changes in housing affordability and conservative vote share, presenting a series of models using housing costs and socio-economic characteristics of constituencies. Model 4 shows that where housing costs relative to income rose – that is, affordability declined – the Conservatives picked up votes. Models 5–7 examine the relationship between local changes in the affordability of expensive and cheap houses in each constituency on the Conservative votes. We find that both increases in expensive housing unaffordability (measured as the ratio of 90th percentile house prices to yearly median earnings) and cheap housing affordability (measured as the ratio of 10th percentile house prices to yearly median earnings) draw more votes for the Conservatives.

Conclusion

In this article, we have explored how declining housing affordability across Europe affects preferences for social policy and political outcomes. We have found consistent evidence that declining affordability – driven by increases in housing prices – decreases support for redistribution, especially among homeowners, across Europe and increases votes for the Conservative party in the UK. Our analysis contributes to the literature that highlights the centrality of wealth, especially homeownership, for social policy demand and political outcomes (Fuller et al., 2020; Schwartz, 2009). We theoretically argue and empirically show that relative wealth is powerful in shaping demand for redistribution, housing policy and support for conservative parties.

What are the broader theoretical lessons of these findings? One is that house prices have a significant impact on social policy preferences and voting behaviour, not only in absolute terms but also in relative terms. We find that growing unaffordability creates support for less government intervention in labour market inequality or housing and, consequently more support for the political right. We argued that this result is driven by homeowners, seeking to protect their gains of appreciation from being taxed away or undermined by growing housing supply. We show that this is not simply a function of places with higher incomes having more expensive property – the ratio of housing costs to incomes is a core factor driving this shift in preferences.

Another lesson concerns the consequences of wealth inequality for political polarization. Even if on average, rising affordability reduces the demand for intervention, that may not be the case for renters, locked out of booming markets. Rising unaffordability drives a political wedge between owners and renters and may be an important contributor to the growth of political polarization, including that attributed to age (McCarty et al., 2016; O’Grady, 2019). As Dewilde and Flynn (2021) show in this special issue, homeownership is particularly unequally distributed among the young, potentially detaching many younger Europeans from the housing market permanently, with major economic and political consequences. The political relevance of this type of polarization will of course depend on the ability of actors defined by their wealth to coalesce around housing policy – if income or labour market risk cut across the interests of homeowners this might reduce the size of the ‘anti-redistribution’ coalition. Cultural divides might also split homeowners from one another, as in the case of the Brexit divide noted by Adler and Ansell (2020), which has produced the unusual example of a Conservative Party toying with easing planning laws.

We conclude by noting the policy consequences of our argument and findings. Presuming that centre-right parties are inherently cautious about market interventions, particularly in residential housing, we should not expect that the aggregate growth in housing unaffordability will meet with a thermostatic political response. A number of articles in this volume have suggested an array of redistributive policies from rental controls to tax reform to help younger non-owners (Dewilde and Flynn, 2021; Nolan et al., 2021). Instead, in the medium run, growing housing unaffordability is likely to lead to greater success for right-wing parties and less interest in redistribution, thereby underpinning the overall trend of rising property prices. Accordingly, the surge in house prices we have seen across Europe is self-reinforcing. The beneficiaries of unaffordability will prefer to keep policies and parties in place that keep prices high and rising. However, as we have seen, they do so at the cost of growing polarization between renters and owners.

Supplemental Material

sj-pdf-1-esp-10.1177_09589287211056171 – Supplemental Material for The political consequences of housing (un)affordability

Supplemental Material, sj-pdf-1-esp-10.1177_09589287211056171 for The political consequences of housing (un)affordability by Ben Ansell and Asli Cansunar in Journal of European Social Policy

Footnotes

Acknowledgements

The authors gratefully acknowledge the helpful criticisms and suggestions provided by two anonymous reviewers, the super-reviewer, the special issue editors Brian Nolan and Ive Marx, and the editors of the Journal of European Social Policy. We thank Mads Elkjaer, Laure Bokobza and Jacob Nyrup for their comprehensive feedback.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

This project has received funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation programme, grant agreement number 724949. The ERC project code for this project is WEALTHPOL.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.