Abstract

What makes a pension scheme sustainable? Most answers to this question have revolved around expert assessments of pension schemes’ affordability or adequacy. This study shifts focus from the financial or social sustainability of pension scheme designs to their political sustainability. Political sustainability refers to policymakers’ ability and willingness to sustain pension schemes in the face of perceived challenges. We seek to fill a key research gap concerning the political sustainability of pensions by highlighting the processes of parametric adjustment through which pension schemes are sustained. We show how capital, labour and state actors have been able to actively sustain collective defined benefit (DB) pension schemes in two coordinated market economies, Finland and the Netherlands. The two countries have managed to sustain their DB pensions for relatively long periods of time despite facing the same sustainability challenges that have motivated paradigmatic shifts in other pension systems. We find that sustaining has been successful thanks to a governance culture in which policymakers have been willing to keep all pension scheme parameters open for negotiation and an institutional context that made policymakers able to turn parametric pension reforms into power resources for further reforms. Our findings also explain recent changes in the Netherlands, which moved the Dutch system towards collective defined contribution pensions.

Introduction

Sustainability has become an important lens through which to evaluate social policies, including pensions (Cox and Béland, 2013). As early as 1994, the World Bank identified sustainability as an essential criterion for pension reform (1994: 10). The World Bank’s recommended creation of a three-pillar pension system of state, occupational and personal pensions has since become a dominant policy paradigm (Orenstein, 2008). More recently, the European Commission (2016: 6) defined pension sustainability as ‘the fiscal and financial balance between revenues and liabilities (and the ratio of workers/contributors to pensioners/beneficiaries) in pension schemes’. The ILO, meanwhile, referred to pension sustainability as the ‘current and future capacity of the economy to bear the costs of social security’ (2018: 2). In other words, these important policy actors largely perceive pension sustainability as the continued affordability of private or public pensions. Similar understandings of sustainability are also visible in the academic scholarship on pension sustainability (for example, Blake and Mayhew, 2006; Holzmann and Stiglitz, 2001; Meier and Werding, 2010). Recently, research on pension sustainability has broadened to include social sustainability issues such as adequacy (see Grech, 2018; Zaidi, 2012).

We argue that understandings of pension sustainability based on affordability and adequacy understate the institutional context and governance processes through which pension reform takes place. Following Barr and Diamond (2009), we maintain that pension designs are not inherently sustainable or unsustainable but dependent on the successful adjustment of pension parameters over time. We therefore shift focus to the political sustainability of pensions. We define the political sustainability of pensions as the continued ability of pension policymakers to maintain a consensus around a coherent set of pension scheme parameters and avert pressures for their exhaustion or replacement. Only when policymakers are convinced that pension schemes can no longer be politically maintained, are paradigmatic policy shifts looming. The key question is whether policymakers have the willingness and the ability to sustain the pension scheme. To answer this question, we draw on scholarship on the politics of parametric policy adjustment and negotiated reform.

We apply our argument to the case of collective defined benefit (DB) pensions in Finland and the Netherlands. Our focus is on two countries that are among the few mature three-pillar pension regimes that have managed to sustain collective DB pensions as the primary source of retirement income despite adverse demographic, financial and economic conditions. The cases demonstrate exceptional degrees of policymakers’ willingness and ability to sustain key pension schemes through parametric adjustment. Yet, this persistence has not meant the absence of sustainability challenges. In similar historical trajectories, policymakers in both countries periodically faced sustainability concerns over key pension schemes. We identify three waves of adjustment based on perceived sustainability challenges: (1) 1960s–1970s, when policymakers worried over institutional complexity and pension adequacy during the build-up of the pension system; (2) 1980s–1990s, when first concerns over fiscal pressures and demographic ageing emerged and (3) 2000s–2010s, when the long-term viability of the schemes became explicitly questioned. In each phase, Finnish and Dutch policymakers managed to sustain pension schemes through parametric institutional and policy adjustment. Only in the Netherlands, a fourth wave is possibly emerging, in which further adjustments move the policy paradigm towards collective defined contribution (CDC) pensions.

Why have Finnish and Dutch welfare state actors managed to sustain collective pensions successfully despite periodic sustainability challenges? Our comparison first shows that even perceived unsustainable features of pensions can be adjusted to changing circumstances, as long as policymakers and stakeholders regard all pension scheme parameters as negotiable. Here, our study speaks to scholarship on policy concertation that has identified the political advantages offered by negotiated reform, including the possibilities to overcome veto points or to avoid blame for painful decisions (for example, Bonoli, 2012; Ebbinghaus and Hassel, 2000). Both the Finnish and the Dutch pension system are characterized by long traditions of neo-corporatism, in which organized employers and unions share joint responsibility for pension scheme governance. As we will show, the institutional structures of corporatist decision-making have rendered the pension schemes into important power resources for these actors, which motivates negotiated reform.

The deviating trajectory of the Netherlands since the 2010s shows how the very process of sustaining can also disrupt existing pension policy. Once social partners become unwilling to negotiate particular pension parameters (the contribution rate for employers; the retirement age for unions), possibilities for parametric adjustments are closed off. The Dutch social partners choose to maintain collective administration of occupational pensions at the expense of the policy paradigm. These findings inform our second conclusion: not just policy design, but also governance considerations are necessary for sustaining pensions. If stable political coalitions are central to the political sustainability of social policies (Patashnik and Weaver, 2020), then governance interests and concerns need to be more seriously taken into account if policymakers wish to build sustainable pension schemes.

The outline of this article is as follows. First, we will discuss conceptions of pension sustainability and introduce our conceptual framework for analysing the political sustainability of pensions. We will then present the methodology used in our comparative case analysis and the key characteristics of the two cases. In the following section, we will demonstrate the development and maintenance of collective schemes in our two case countries from the post-war years until today. In the last section of the study, we discuss the importance of these findings and provide some avenues for further research on the sustainability of social policy.

Political sustainability of collective pensions

What makes a pension scheme sustainable? While many policy experts have reviewed the sustainability of national pension systems or schemes, few have identified concrete criteria to assess the sustainability of pensions. Recent scholarship invites two observations. First, many restrict discussions of pension sustainability to a scheme’s fiscal or financial sustainability – in other words, its affordability (Grech, 2018). These definitions pertain most commonly to the affordability of public pensions. Here, pensions appear as an implicit form of public debt, conditional upon the ability or willingness to repay it at given contribution levels (Blake and Mayhew, 2006; Meier and Werding, 2010). This type of sustainability is focused on the given benefits while leaving policy considerations like adequacy as secondary (Grech, 2013). Second, the indicators used to assess pension sustainability conceived more broadly are most commonly the absence or presence of particular policies (for example, an increase in retirement age) rather than the absence or presence of particular problems (for example, increased expenditures and declining adequacy). To give an example, the influential Allianz Global Pension Report measures the sustainability of pension systems by considering a handful of indicators: increase in the legal retirement age; the length of the minimum contribution period; the presence or absence of early retirement and the presence or absence of a demographic factor in the pension formula (2020: 6). This assessment of pension sustainability appears as teleological, whereby the durability of a pension system is observed by the introduction of policies needed to strengthen that sustainability. 1

While affordability is certainly a key concern for pension policymakers, we argue it offers too narrow a scope to form a robust conception of pension sustainability. First, the ‘teleological’ assessment of pension sustainability limits concerns to individual adjustments to scheme design, without taking into account overall coherence. As Barr and Diamond (2009) have argued, no pension scheme is inherently sustainable or unsustainable as sustainability depends on the particular parameters of the scheme and the successful adjustment of these parameters over time. The fact that one parameter, such as the benefit level or the retirement age, is adjusted tells us little about its effects on other scheme parameters (Palier, 2007) or the consequence of each adjustment over time (Hinrichs and Kangas, 2003). Given that different pension policies have different functions (for example, poverty alleviation in basic pensions versus income maintenance in social insurances), policymakers may consider multiple criteria when assessing the acceptability of individual policies (Grech, 2018). A longer-term view of policy processes is thus needed to address the sustainability of pension policy.

Second, the focus on pension policy often excludes from analysis factors other than key policy parameters (such as benefits, contribution rates and the retirement age). Of course, many secondary pension policy parameters such as indexation rules (Schoyen and Stamati, 2013) or portability concerns (Holzmann and Koettl, 2011) also play an important role in the perceptions of sustainability. However, parameters other than those related to scheme design per se, such as investment policies or representation in management, also often motivate pension reforms (for example, McCarthy et al., 2016; Naczyk, 2016). Additionally, policymakers often consider issues that are only indirectly related to pension schemes, such as fiscal policy capacity (Koreh, 2017). A broader institutional and administrative view of pension schemes is thus needed to address the sustainability of pensions.

Finally, the focus on individual schemes excludes from analysing their role in the wider pension regime. Especially in the so-called multi-pillar pension regimes (Orenstein, 2008), a retiree’s pension typically comes from various pension schemes that are mutually coordinated. Adjustments to individual schemes are typically a result of negotiations between various stakeholders, and changes in one pension scheme often involve changes in other schemes as well (Ebbinghaus and Hassel, 2000). For instance, state actors may try to improve the generosity or coverage of occupational pension schemes in order to reduce financial pressures on state pensions. Hence, the policies that are relevant to the perceptions of pension sustainability may exist in multiple schemes in a given pension regime.

We argue that the concept of political sustainability (Patashnik and Weaver, 2020) allows us to address the importance of policy processes and acceptability, wider characteristics of pension schemes and the broader pension regime. When applied to pension schemes, political sustainability can be understood as the continued ability of policymakers to maintain a consensus around a coherent set of pension scheme parameters and avert pressures for their replacement. By a coherent set of parameters, we mean pension scheme characteristics that individually may not be advocated or supported by all policymakers, but that together form a balanced whole that makes the overall scheme acceptable for the ruling coalitions. Which parameters are relevant for such analysis is an empirical question. Hence, our conception moves away from the conceptions of pension sustainability as a ‘tick-box exercise’ – the presence or absence of individual scheme parameters – to the actual process of sustaining the principles and structures of pension schemes. 2

The process of sustaining is strongly shaped by the institutional context of the pension system. As Ebbinghaus (2011) notes, multi-pillarization has elevated the role of private actors in pension governance and policymaking. After all, multi-pillarization increases the importance of occupational pensions, which are either employer-dominated or jointly managed by employers and unions. At the policy level, pension reform has often occurred through policy concertation, or negotiated reform that involves cooperation among organized employers, unions and sometimes the state (Ornston and Schulze-Cleven, 2015). Such policy concertation is particularly common in pension systems with traditions of neo-corporatism or social pacts (Baccaro, 2003). Policy concertation brings a number of advantages to the policymakers involved: for instance, the possibility of overcoming veto points (Ebbinghaus and Hassel, 2000), exchange of information (Culpepper, 2002) and the possibility of avoiding blame or claiming credit for policy outcomes (Bonoli, 2012). Scholars of policy concertation stress the role of the state that may offer sticks (for example, the threat of unilateral action) or carrots (for example, the offer of rewards) to incentivize stakeholders to reach a consensus (Ornston and Schulze-Cleven, 2015). In short, the willingness and ability of pension policymakers to make the necessary adjustments to render a pension scheme sustainable is a function of the institutional context in which they operate.

Nevertheless, a major research gap exists: what determines the willingness and the ability of pension policymakers to sustain pension schemes instead of letting them drift or displacing or exhausting them as part of paradigmatic policy shifts? Put differently, why and how do key policy actors increase the legitimacy of pension policy, the governance capacity over pension schemes or/and the momentum to build consensus for reform, when they perceive that the coherence of pension parameters is compromised and consensus appears to crack? Next, we seek answers to this question through a comparative case study of collective DB pensions in the Netherlands and Finland.

Towards the comparative case study

Our comparative case study is focused on reforms of key pension schemes in Finland and the Netherlands. Both countries have a mature three-pillar pension regime, in which collective DB pensions – mandatory occupational pensions in the Netherlands and mandatory national earnings-related pension insurance schemes in Finland – offer an important source of old-age pension income for the elderly. This differentiates them from other mature multi-pillar regimes, such as Sweden or Denmark, where sources of retirement income are more fragmented. Mandatory country-wide or industry-wide participation guarantees high coverage in both countries. In the Netherlands, collectively bargained occupational pension plans can be extended to entire industries. As a result, a large majority of Dutch occupational pension scheme members participates in collective DB plans: 88.7% in 2020 (De Nederlandsche Bank, 2020). In Finland, all private and public sector work done in the country must be insured through the earnings-related pension insurance schemes. Both schemes also represent early cases of funded (the Netherlands since 1952) or partly funded 3 (Finland since 1962) large-scale pensions in Europe. Extensive reliance on funding differentiates the schemes from collective DB schemes in countries like Austria or Italy.

Finland and the Netherlands are also very similar in terms of pension governance practices. In both countries, social partners (that is, industry-wide and central unions and employer associations/confederations) bargain collectively over pension schemes and jointly govern pension fund boards. In the Netherlands, pension funds are managed by bipartite boards, with equal representation for employer and union-affiliated trustees. In Finland, pension insurance companies and funds are also managed by bipartite boards, with varying proportions of representation. At the national level, the social partners (peak organizations for employers and unions) play a crucial role in pension policymaking: in the Netherlands, central labour market organizations meet within corporatist institutions such as the Socio-Economic Council (Sociaal-Economische Raad) and the Labour Foundation (Stichting van Arbeid), while their Finnish counterparts engage in bipartite or tripartite ad hoc negotiations. Such negotiations often extend beyond individual pension schemes as reforms in occupational/earnings-related schemes are often coupled with reforms in the statutory/basic pensions (for example, Kangas et al., 2010).

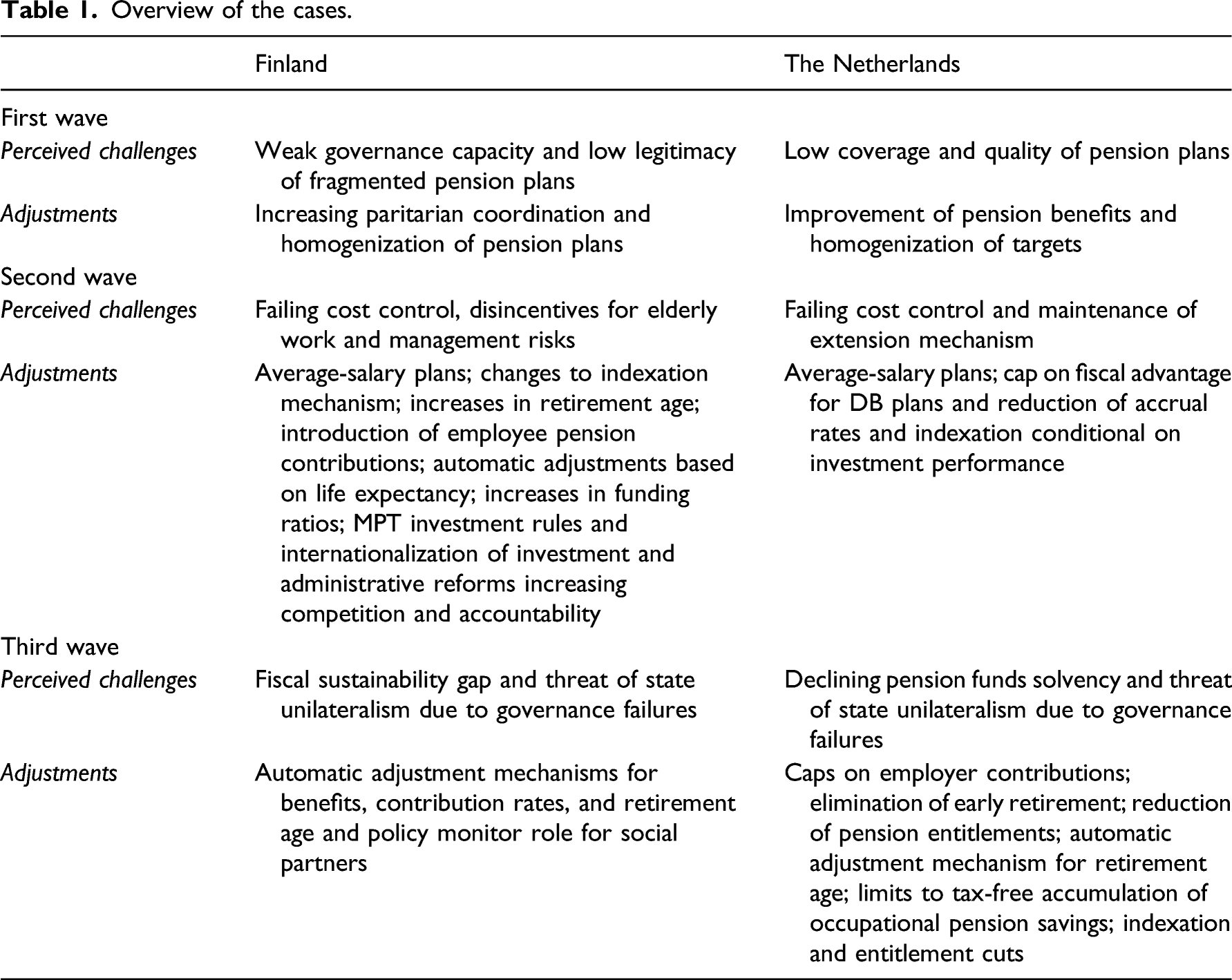

Overview of the cases.

We then identify the key measures through which the sustainability concerns were tackled. We find that, in our two cases, nine types of pension scheme parameters have been (re-)negotiated (see Table 1). On the benefits side, the pension salary (1) and the accrual rate (2) have been adjusted to influence the accumulation of pension rights. The period over which these rights are accumulated have also been adjusted, typically by increasing the years of employment (3), most often by raising the official retirement age directly. Additional conditions for retirement (4) have also been introduced, including more flexible choices between early or late retirement with financial incentives. Indexation (5) of accrued pension rights have been adjusted in numerous ways. On the financing side, contributions (6) paid by employers and/or employees have been adjusted in terms of contribution rates and distribution between different payers. Investment policy and management (7) and regulations (8) have been adjusted to affect the realization of financial returns and investment portfolio allocation. Finally, governance systems (9) have been reshaped in various ways.

We show that pension policymakers in Finland and the Netherlands have shown remarkable willingness and ability to successfully maintain the schemes through parametric adjustment instead of paradigmatic change. We situate our findings in the long-standing traditions of bi- and tripartite governance and the institutional context of coordinated capitalism in both countries. We argue that both factors play an essential role in establishing the sustainability of pension schemes, not just the parameters of the scheme design itself. These findings do not only apply to cases of mature multi-pillar pension regimes like Finland, the Netherlands, Denmark or Sweden, where policymakers’ willingness and ability to negotiate is strongly tied to the collective nature of the pension system (Anderson, 2019). They also are relevant to pension systems, where the absence of such institutional resources might explain on-going abandonment of collective DB pensions, as is the case for instance in the United Kingdom or the United States (Bridgen and Meyer, 2009; Van der Zwan, 2018). Next, we turn to both case studies.

Finland

Regular sustaining of pension schemes has been a key historical characteristic of Finnish pension policy, as most schemes have been reformed parametrically dozens of times to adapt to changing social and economic circumstances (Hinrichs and Kangas, 2003). Our main focus here is on the largest and most influential collective pension scheme, the mandatory earnings-related pension scheme for private sector employees (originally TEL, since 2007 TyEL, according to the abbreviations of the laws defining the scheme). TEL, the old-age pension scheme for private sector employees that came into effect in 1962, was the first large-scale collective DB scheme in Finland. The parameters of public and private schemes have been homogenized during the last two decades, and all mandatory earnings-related schemes are now merged with or based on the parameters of the TEL/TyEL scheme. The scheme is a partly funded 3 social insurance scheme, administered by partly competing private pension providers (pension insurance companies, industry-wide funds and company funds), and includes a number of different pension entitlements (for example, survivor pensions and rehabilitation assistance) (Eläketurvakeskus, 2020b).

The first wave of adjustment based on sustainability concerns emerged in the early years of the TEL. The main sustainability concern was that the emerging pension system was perceived as too complex to gain popular appraisal and risked state capture over pensions. Pension professionals had raised the concern of popular legitimacy by the early 1970s, but it was also voiced by some employers and unions (Hannikainen and Vauhkonen, 2012: 141). A uniform accrual scheme for all old-age pension plans with clear pre-defined conditions for related special pensions, achieved with uniform legislation defining these elements through one pension scheme, was regarded as key to increasing the legitimacy of the system. In the early 1970s, the social democratic majority government raised pension benefit levels as part of the homogenization measures. The government had stated that despite raising benefit levels, it sought to avoid the generation of ‘excessive’ pensions or pension benefits that exceeded the replacement rate of 100% at the individual level, since they would not seem legitimate in the eyes of future generations who would foot the bill (Hannikainen and Vauhkonen, 2012: 167).

In the late 1960s, the central labour market organizations at both sides, but especially the employers, argued that they should also coordinate the simplified system to achieve the aspired stability in governance. The main sustainability concern here was the fear of state capture over pensions. In the case of certain government interventions related to public pensions, the expenditures of the earnings-related pensions could have exceeded its incomes, bringing the scheme in effect under public control (Hannikainen and Vauhkonen, 2012: 143). In order to avoid such problems, social partners argued that the decision-making over all earnings-related pensions should be in the hands of the ‘pensions men’ or the central labour market organizations and their representative pension professionals, who speak for those who pay for the system (Hannikainen and Vauhkonen, 2012: 144). The government accepted their initiatives, since they enabled coordination between pension policy and other economic policy tools and thus expanded the state’s economic governance capacity into crucial domains. As part of the so-called UKK-deal of 1970, the government mandated central labour market organizations as part of a broader incomes policy agreement to take a more overt role in coordinating and governing pension policy. Employers granted labour union access to the management of pensions (through board representation) later in the 1970s in order to avoid emerging cracks in the paritarian block brought by disagreements over investment policy (Sorsa, 2011).

The second wave of adjustment based on unsustainability perceptions ranged from the late 1970s to mid-2000s and revolved around cost control and the appropriate distribution of contributions and benefits over time. First concerns over the costs of an ageing population were voiced already in the mid-1970s, but the issue of an ageing population, rising pension costs and incentives for staying in work dominated the pension debates of 1980s and 1990s (Kangas et al., 2010). These concerns motivated changes in the indexation mechanism, raising the retirement age and adoption of employees’ pension contributions in the early 1990s. Similar unsustainability concerns played an important role in the reforms of late 1990s (Hinrichs and Kangas, 2003). The key reforms adopted then – incentives to work longer, new indexation rules, increased funding ratios and regulations related to the new modern portfolio theory-based investment paradigm – all sought to tackle challenges of population ageing. The objectives and rationale of the 2005 reform were highly similar to the earlier reforms, but the reform also introduced incentives for working longer and a new automatic adjustment mechanism, the life expectancy factor, which tied pension benefit levels to average life expectancy of an age cohort.

Numerous parametric investment policy reforms and administrative reforms increasing competition and accountability were key for the pursuit of higher profits and lower administrative costs, respectively, from the 1990s to 2000s (Sorsa, 2011). While increasing investment returns was seen as the best way to respond to population ageing, the previous decisions to strengthen paritarian management of investments legitimated shifts to asset classes with higher returns and the professionalization of the investment functions (McCarthy et al., 2016).

The third wave of sustainability perceptions that rose in the 2000s and related reforms differed from previous waves in two respects. First, the sustainability of the pension scheme was questioned explicitly. Specifically, the fiscal sustainability of the Finnish state became the key concern for pension policy. The pension contributions are tax deductible for employees and employers, which means that contribution rates have a direct negative impact on state tax revenue. The idea of a ‘sustainability gap’ (in Finnish: kestävyysvaje), which gained a hegemonic status in Finnish public policy around 2007, was presented as the indicator for the sustainability of the entire welfare state, not just public finances (Eskelinen and Sorsa, 2013). The idea dominated the pension negotiations of 2014–2015 (Lindén, 2016). Second, the reforms focused on not only one or two main parameters but targeted a broad variety of parametric changes simultaneously. For example, still in the 1990s, no actor had explicitly questioned the idea of accruing life-long pension rights after retirement or considered cuts to accrued pension rights politically feasible (Eläkekomitea, 1991: 53–5; HE 118/1995, 1995). In contrast, the 2017 reform introduced various automatic adjustment mechanisms to pension benefits and the retirement age in order to stabilize contribution rates. The 2017 reform tied benefits to life expectancy, introduced an actuarially neutral flexible retirement age, tied retirement age to contribution levels, as well as changed the principles of using certain investment reserves (Eläketurvakeskus, 2020a).

In effect, the third-wave adjustments introduced automatic adjustment mechanisms for all key policy parameters. Technocratic elements were introduced in the governance system as well. For decades, the social partners had been able to determine the contents of reform negotiations and pension legislation and to block government attempts to influence pension policy based on fiscal policy concerns, due to long-term coalitions with key political parties (see Johanson and Sorsa, 2010). But now, the right-wing government was allowed to dictate the objectives of the 2014–2015 negotiations (that is, raising the retirement age and decreasing the sustainability gap). The social partners perceived that if they could not meet the objectives, the government would have imposed a number of measures even without the social partners’ consent and possibly taken the pension scheme under public control. Finding common ground was easier, as the unions now shared the interest of decreasing contribution rates with employers, since the social partners had agreed in the second-wave measures that all contribution rises would be divided 50/50 between employers and employees. The government also offered the social partners – for the first time ever – an official legal status as monitoring bodies over pension policy. Our interviews suggest that neither employers nor labour unions wanted to have been burdened with public perception of broadening the sustainability gap, and hence accepted the previously unacceptable government interventions to gain a technocratic monitoring role.

The Netherlands

Social partner concerns over the future of occupational pensions first emerged in the Netherlands during the 1960s and 1970s. In the pension system’s formative years, during the 1940s and 1950s, the expansion of old-age income dominated the political agenda. With the introduction of an automatic extension of collectively bargained occupational pension plans in 1947 and the statutory pension in 1957, most Dutch citizens gained access to some form of pension. Still, by the late 1960s, large groups of employees were without an occupational pension and social partners worried that existing pensions might not be adequate for those who were already retired. They perceived that the legitimacy of the growing pension scheme might be thus questioned. In 1969, the social partners in the Labour Foundation therefore agreed on a universal pension norm: collective DB pensions would need to generate 70% of final salary in retirement income (Oude Nijhuis, 2013).

A second wave of sustainability concerns entered the Dutch pension debate in the 1980s and 1990s. By then, the expansion of final salary DB plans in the 1960s and 1970s had led to a massive growth in pension entitlements, which in turn imposed major costs on sponsoring employers. Subsequently, several large employers such as Rabobank (1987) and Philips (1997) made the switch to average-salary DB plans. Simultaneously, the so-called purple cabinet of Prime Minister Wim Kok announced new objectives for Dutch occupational pensions. Citing demographic ageing and the subsequent pressures on the PAYGO-financed state pensions, the cabinet expressed a deep worry that pensions would become unaffordable in the long run: counting for an estimated 18–25% of the wage sum by 2030 (Tweede Kamer Der Staten-Generaal, 1996–1997). The cabinet strongly encouraged the social partners to take further cost control measures and threatened to cancel the automatic extension of collectively bargained pension plans. It also made changes to the fiscal treatment of occupational pensions, capping tax-free pension savings at 2% of average salary (Tweede Kamer Der Staten-Generaal, 1996–1997). The state thus introduced a strong incentive for the social partners to reduce one of the pension parameters: the accrual rates.

Social partners and the state formalized parametric adjustments to DB pension schemes in the 1997 Covenant on Occupational Pensions. In addition to the switch from final to average-salary DB plans, the Covenant committed the social partners to the elimination of automatic adjustments of pension rights to wage or price increases (Stichting Van de Arbeid, 1997). Instead, indexation was made conditional upon investment performance. Both adjustments proved successful. In a 2001 evaluation of the Covenant, it was found that around a third of all fund members now participated in an average-salary plan, up from 25% in 1999 (Werkgroep Evaluatieonderzoek Convenant Arbeidspensioenen, 2001). Additionally, a growing number of funds had made indexation of pension rights conditional on investment performance, covering around 90.4% of active participants who now participated in plans with conditional indexation of pension rights (Werkgroep Evaluatieonderzoek Convenant Arbeidspensioenen, 2001). The Covenant also reiterated the signatories’ commitment to the mandatory extension of occupational pension plans, although some new possibilities to receive dispensation from the extension were also introduced (Werkgroep Evaluatieonderzoek Convenant Arbeidspensioenen, 2001).

Indexation conditional to financial performance increased the importance of investment returns. During the 1990s, many Dutch pension funds had increased their investments in corporate equities, hoping to take advantage of booming stock markets. While the switch to equity investments led to a massive growth in pension assets, it also introduced vulnerabilities to financial market fluctuations. This became painfully clear when average funding levels of Dutch pension funds dropped from 199% (assets/liabilities) in 1999 to 124% in 2002 as a result of the 2001 dot.com crisis (Van der Zwan, 2017). The great financial crisis (GFC) of 2008 further exacerbated the financial problems of DB pension schemes. Had post-2001 funding levels on average still been sufficient to cover outstanding liabilities, after the GFC the average funding level dropped below the required 100% of liabilities (Van der Zwan, 2017). Several pension funds had to take the unprecedented action of reducing the pension entitlements of active and retired workers for millions of beneficiaries.

With funding levels in decline, both policymakers and social partners worried that DB pension promises could only be met by changing contribution rates or repair payments by employers. In other words: the costs of DB pensions would have to go up. Prior to the GFC, influential experts had already advocated limiting contribution rates to ‘futureproof’ the occupational pension system. Now employers increasingly bargained for contribution caps in DB pension contracts (Van der Zwan, 2018). Again the state became a driving force behind further pension reform, when the Minister of Social Affairs instructed the social partners to translate the experts’ findings into concrete proposals. The 2010 Pension Accord laid the basis for more far-reaching reforms in the years to come, because it formalized the shared idea that the policy instrument had reached its maximum level: 17.9% for the statutory pension and on average 20% for occupational pensions (Stichting Van de Arbeid, 2010).

The third wave of adjustment was motivated by perceptions of declining solvency, the need to control costs further and perceived governance failures. With the contribution rate now deemed non-negotiable, political attention switched to other parameters in the DB formula, most importantly the retirement age and investment policies. Immediately after the GFC, political leaders had introduced a new policy agenda for the occupational pension system, which centred on three themes: (1) the creation of new financial rules for pension funds; (2) developing new, more flexible pension contracts and (3) tying pension benefits to increases in life expectancy (Tweede Kamer Der Staten-Generaal, 2008–2009). In the 2010 Pension Accord, the social partners responded to two of these themes by agreeing to gradually increase the legal retirement age and to introduce a new kind of pension contract without a nominal pension promise. The Accord proved to be short-lived, as unions and left-leaning political parties rallied against the proposed increase in the retirement age. Ratification of the Accord finally failed, after members of two of the most influential unions (industrial union FNV Bondgenoten and public sector union Abvakabo) voted against it.

The implosion of the 2010 Pension Accord paved the way for state actors to take a unilateral approach in sustaining the scheme. After the fall of the Balkenende-IV cabinet, a coalition of five political parties reached its own agreement on the future of the pension system, which included a faster increase of the statutory retirement age and a decrease of the tax-free accrual rates for occupational pensions. The new Rutte government set in motion a legislative process to change the financial rules for occupational pensions. Central to the 2015 New Financial Assessment Framework (nFTK) were new rules regarding cutbacks and indexation of pension benefits: while low funding levels would not as quickly be translated into cutbacks of the nominal pension, rules for the indexation of pension liabilities became more stringent. Funding levels had to reach 110% or higher for a fund to award indexation. This meant a further departure from the DB pension promise.

The years following the failed Pension Accord saw a reinvigoration of corporatist governance in the Dutch pension system, as the Social and Economic Council continued to develop ideas for a new pension contract (Sociaal-Economische Raad, 2015). Facing critiques of mismanagement of Dutch pension funds in the wake of the GFC, the social partners embarked on a protracted policy process that included various consultations of experts and members of the general public. In 2019, the social partners agreed on a new pension accord, which both unions and employers could claim as an important victory. The 2019 Pension Accord traded a slower increase in the legal retirement age with substantial changes in occupational pension contracts. While the collective nature of occupational pensions was maintained through the mandatory extension and collective administration of occupational pension schemes, pension contracts would no longer promise a defined benefit (Ministerie Van Sociale Zaken en Werkgelegenheid, 2020). In other words, the revitalization of corporatist governance coincided with a system shift towards a CDC system. In all likelihood, the new rules will go into effect from 1 January 2023.

For decades, the DB formula served as a source of legitimacy for Dutch occupational pensions. Over the course of two decades, however, political consensus on the desirability of collective DB pensions gradually disappeared and a new consensus emerged that led the Netherlands on the path to a CDC occupational pension system. Interestingly, this new consensus did not follow the growing popularity of DC schemes, which are still in the minority. Instead, the 2019 Pension Accord was the outcome of a gradual process of paritarian governance through which the political sustainability of DB pensions was increasingly questioned. As employers and unions began to consider particular DB pension parameters as non-negotiable (contribution rates and retirement age), the option of parametric policy adjustment to financial challenges was no longer possible. In this sense, the social partners sacrificed the DB pension promise to be able to maintain powerful positions in the collective pension scheme.

Discussion and conclusions

We have argued that institutional context and governance processes are essential to understand pension sustainability. Expert and scholarly assessments of pension sustainability should not only take into account pension scheme design, but also pension policymakers’ willingness and ability to maintain a coherent pension scheme and avert pressures for its exhaustion or replacement over time – in other words, its political sustainability. Using the cases of Finland and the Netherlands, two mature three-pillar pension regimes characterized by the long-term survival of large-scale, funded and collective DB pensions, we have shown that (1) both sustainability concerns and the set of pension scheme parameters that policymakers regard as acceptable change over time; (2) governance practices inform the perceived coherence of pension schemes and (3) parameters of other pension schemes influence sustainability considerations. We identified three historical waves of adjustment driven by policymakers’ perceived sustainability challenges. The cases showed that the dynamics of the adjustment process itself mattered for pension sustainability as the experiences and outcomes of previous reforms had a major impact on subsequent adjustments.

In both of our cases, policymakers’ willingness to sustain stemmed from their perception of the key collective pension schemes as important power resources. The social partners did not only consider the schemes crucial for the legitimacy of corporatist governance, but also accepted compromises to improve or maintain their own status in pension governance. Governments of the two states, meanwhile, also considered collective pensions essential, often for economic reasons. When cracks emerged in the consensus between the social partners, the state was able to increase its influence. State interventions either fixed some parameters or led social partners to consider certain parameters as non-negotiable. This decreased their ability to maintain a coherent pension scheme. The resulting compromises produced major changes. In the Netherlands, social partners abandoned a long-standing policy paradigm to maintain their governance status, while the social partners in Finland accepted a more technocratic role in pension governance.

Indeed, one contributing factor to the long-term sustaining of key pension schemes in Finland and the Netherlands is the fact that the pension schemes in question have grown relatively large in volume. In multi-pillar pension regimes where primary pension income comes from multiple schemes (for example, Sweden or Denmark) or pension regimes with less mature schemes (for example, Central and Eastern European countries), individual pension schemes are smaller and not necessarily perceived as important power resources. In countries with large-scale collective pensions, key schemes do not involve funding or decentralized administration (for example, Austria and Italy) and individual schemes may simply offer fewer parameters to bring ‘wins’ for policymakers. It also remains to be seen if the social partners continue to be able or willing to sustain pension schemes in their new governance roles (Finland) or policy paradigm (the Netherlands). Whereas automated adjustment of key scheme parameters offers few opportunities for negotiated adjustment in Finland, pension policymakers in the Netherlands have to effectively legitimize the new CDC paradigm while continuing to manage ongoing risks (that is, the retirement age; investment returns). More comparative research is needed to understand how different types of parameters motivate policymakers to sustain pension schemes or not.

Even though our focus has been on pensions, our findings are relevant for the wider scholarship of social policy. Sustainability offers a useful concept for understanding the long-term prevalence of social policies and institutions like pension schemes. However, without explaining why different actors maintain and renew some social policies and welfare institutions but not others, sustainability research will have little to say about the actual longevity of policies and institutions. Our findings can be summarized as the following maxim on sustainability: the capacity to sustain a welfare scheme is primary to any particular conception of sustainability based on a narrow set of policy indicators. In other words: rather than conceptualizing sustainability as a ‘tick-box’ exercise of available policy instruments external to the policy process, scholars of social policy should consider how institutional capacities and governance practice shape the complex ways in which policymakers create sustainable welfare states.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.