Abstract

The transformations in the welfare state regimes that have occurred globally, over the last three decades or so, have seriously affected the capacity of states to sustain the previous levels of social care and protection. These changes, already being manifested, inter alia, in trends in declining earnings of pensioners have inspired some researchers in this field to explore alternative ways of mitigating their impact on the well-being of the elderly during the retirement period. One of the theories that has been advanced to this effect is the so-called asset-based welfare concept which suggests that the wealth accumulated by people in the form of housing assets presents a financial reservoir that may serve as a source of income for pensioners in time of need. To address these issues, a variety of mechanisms have been developed and presented as ‘equity release products’ that may be used by senior homeowners to improve their living situation. This article contributes to the debate from the perspective of a country in Central and Eastern Europe (CEE), a region that has been rarely included in the scholarly discourse on the topic. While there might have been some level of success in the implementation of these instruments in some countries, the survey findings presented and discussed in this article show that Slovenian elderly homeowners strongly reject all the equity release products that were presented to them as potential options for alleviating financial hardship in old age. These findings lead us to the conclusion that it is highly unlikely that Slovenian elderly homeowners would ever accept and exploit, at any meaningful level of uptake, the investigated equity release mechanisms.

Keywords

Introduction

The literature review on the topic of homeownership shows a growing focus on exploring and describing the attribute of housing as a wealth reservoir and its potential to mitigate financial hardship at a later stage, particularly during the retirement period. This debate has, generally, been conducted under the term ‘asset-based welfare’ (Delfani et al., 2013; Doling and Ronald, 2010a, 2010b; Elsinga, 2015; Kemeny, 1981; Murie and Forrest, 1980; O’Mahony and Overton, 2015; Ong et al., 2013; Sherraden, 1991; Toussaint and Elsinga, 2009). Premised on the observation that housing policy has, over a long period, contributed to wealth accumulation by homeowners, Murie and Forrest (1980) argued that there was an urgent need to recognize other important elements of people’s housing tenure decisions to which, hitherto, little attention had been paid. They maintained that in addition to use, people also buy houses for investment purposes with the aim of acquiring wealth. They suggested that Housing choice and decisions to change dwellings are not just decisions about consumption and use, or about adjusting the dwellings to changing family structure and size; they involve decisions about investment, about using income available once essential needs have been met, about maximizing net income and about returns on savings. (Murie and Forrest, 1980: 3)

In a similar tone, Saunders (1990) described homeownership as a lucrative venture which enables people to make a lot of money. It is this accumulated wealth that the asset-based theories address and seek to describe as a potential source of income during old age through the eventual trading-off of homeownership for a pension (Dewilde and Raeymaeckers, 2008). Homeownership as an instrument of accumulation of wealth has therefore constituted a vibrant scholarly debate in relation to the welfare state transformations that have occurred in recent decades in Western European countries (Hajer, 2009; Kemeny, 1981, 2005). Following up on the intensification of the discussion on the topic, Dewilde and Ronald (2017) have described housing wealth as a critical axis of social, economic and welfare practices in the 21st century.

As is often the case in many areas of housing research, the current literature discourse has mostly focused on situations or case studies in West European countries (Costa-Font et al., 2010 for Spain; De Decker and Dewilde, 2010 for Belgium; Fahey, 2003 for Ireland; Gibler and Tyvimaa, 2015 for Finland; Haurin and Moulton, 2017 for the United States and European Union (EU); Herbers et al., 2014 for Denmark, Sweden and the Netherlands; Leviton, 2001 for the United States; Ong et al., 2013 for Australia and the United Kingdom; Ong et al., 2015 for Australia; Parkinson et al., 2009 for Australia and Britain; Sherraden, 1991 for the United States; Toussaint, 2013 for the Netherlands; Toussaint and Elsinga, 2009; Ronald, 2015 for the United Kingdom), with some rare publications also on East Asia (Chou et al., 2006; Hirayama, 2010; Ronald and Doling, 2012; Yoo and Koo, 2008). However, the post-socialist countries of Central and Eastern Europe (CEE) have, this far, been only minimally included in the academic discourse on the subject. One such example is the contribution on post-socialist housing systems in Europe (Stephens et al., 2016) which addresses welfare regimes, but only marginally touches upon the asset-based concept with reference to homeownership. The comparative paper discussing Hungary, together with Germany and the United Kingdom (Toussaint, 2011) focuses on attitudes to homeownership in relation to financial security, generally, but does not discuss housing equity release specifically in connection with elderly homeowners. Nonetheless, the study finds, in the case of Hungary, that while ‘housing assets are highly relevant to the financial strategies of extended families’, this wealth is ‘only used as a last resort’ (Toussaint, 2011: 330). Similarly, a European level comparative volume (Dewilde and Ronald, 2017) also draws attention, in the case Eastern European countries, especially to the importance of the informal sector, family and kinship networks and the associated characteristic redistribution of housing wealth within the extended family. The importance of the familial ties in East European countries is also identified in another EU study (on household composition) which established that ‘In the Southern and Eastern European countries… extended-family households predominantly consist of multi-generational households in which a couple live with both parents and children’ (Iacovou and Skew, 2011: 476).

While addressing various issues, the contributions on CEE countries referred to above have one major commonality, that is, they emphasize the importance of the familial component of homeownership and how this has an impact on various aspects of welfare. In view of these indicated commonalities, we suggest that there is a strong likelihood that the circumstances regarding the practical implementation of asset-based welfare mechanisms may, in many CEE countries, be quite similar to those that are described for Slovenia in this contribution. For Slovenia, in particular, a study by Mandič (2016) specifically addresses the aspect of asset-based welfare, with the discussion focusing on the trade-off between old-age care and homeownership. According to the findings of this study, there was, among elderly homeowners, an ‘extraordinarily strong inclination to consume housing wealth’ (Mandič, 2016), and it was concluded that Slovenian elderly homeowners were ‘outstandingly willing to enter residential care and consume their housing wealth for this [welfare] purpose’ (pp. 156, 164). These are surprising findings since they directly contradict the findings of our own research, the results of which are presented and discussed in this article. A very high majority of the senior homeowners that participated in our survey resoundingly rejected all forms of mechanisms proposed to them as options that would enable them to consume their housing equity. These two ‘conflicting’ findings thus present, at this point, a puzzle that we try to explain and solve at the end of the article.

The purpose of this article is, therefore, to examine the validity of the asset-based welfare concept through a case study approach, using the results of an empirical survey that was conducted among the elderly (50+ years) population in Slovenia. The key question to be answered is whether and to what extent the elderly homeowners perceive their homes as assets that can be used to alleviate financial hardship in order to improve their quality of living and their readiness to accept and exploit such mechanisms.

Theoretical background

The notion of asset-based welfare that has been developed over the decades pursues the explanation that under circumstances of steadily diminishing welfare state coverage, individual households are increasingly required, and ought to be able, to assume responsibility for their own well-being (Doling and Ronald, 2010a). Discussing the American situation, Sherraden (1991) argued that generous welfare policies bred dependency on state support among the poor and thus act as a disincentive to self-engagement to better one’s economic situation. However, the author continued, the acquisition of assets enables people to cater for themselves and make long-term plans for future self-reliance. Like all investment goods, owner-occupied housing is therefore believed to have the potential to realize its value in the form of cash that could be tapped should such a need arise (Fahey, 2003; Toussaint, 2011).

It is, however, important to recognize that this debate has mostly proceeded and continues so, primarily, at the theoretical level. From a practical perspective, some writers have raised concerns regarding the accessibility of suitable and, especially, attractive equity release products that need to be available in order for the asset-based concept to be successfully implemented (Burgess et al., 2013; Hirayama, 2010; Leather, 1990). Others have, indeed, raised doubts about the extent to which housing wealth can, in reality, be converted into additional income (Dewilde and Raeymaeckers, 2008). Challenging the practical applicability of the trade-off theory between homeownership and pensions, Delfani et al. (2013) have argued that the successful application of the asset-based welfare concept crucially depends on how housing and pension provision – level of commodification – are organized in an individual country. Emerging from an elaborate description of the various categories of commodification of housing and pension regimes, they conclude that the asset-based welfare concept has a better chance for successful implementation, especially in liberal welfare states, such as the United States and the United Kingdom. With the highest levels of commodification of both housing and pensions, the liberal welfare regimes are described as those in which there is a relatively high level of elderly poverty, thus a higher need for supplementary income during old age. The United Kingdom has, indeed, been identified as the most ‘asset-based welfare’ nation among European countries (Toussaint and Elsinga, 2009). However, concrete evidence on the actual level of uptake is yet to be provided. As has been acknowledged for the United Kingdom by Toussaint (2011), ‘the potential use of housing assets is limited: not everyone disposes of housing assets or wants to consume the asset’ (p. 322). In the case of the United States, where the reverse mortgage instrument is, arguably, the most frequently offered equity release product, Haurin and Moulton (2017) concluded that there was a lack of demand for it having found that only a small share of seniors extracted their home equity. They explain this lack of demand as the result of the complexity of the financial instrument and also point out a lack of basic knowledge about the product. As had been previously found by Leviton (2001), homeowners were very cautious when deciding on reverse mortgages: ‘At this point in their lives, they strongly feared the consequences of making a mistake about their last asset. They saw no opportunity to correct a mistake, no new job to replenish their bank accounts’ (p. 10). This cautiousness due to a lack of knowledge of the contract terms was recognized also by Davidoff et al. (2017) who, as a remedy, suggested an approach that would, in the first place, focus on explaining the basics, meaningfulness and advantages of the particular equity release product.

The practical applicability of the asset-based welfare concept has been contested also by Elsinga (2015). In an article entitled ‘The Janus face of homeownership-based welfare’, the author questions the underlying assumption of the entire discourse which appears to consider housing assets as a superfluous good that is there to serve as a pillar of the pension system. Such assumptions seem to totally ignore the existence of some important attributes of homeownership and the various (sometimes not too obvious) functions of a home. The most important among these include the meaning of home to its owner, psychological attachment, familial ties and inheritance considerations (Anton and Lawrence, 2014; O’Mahony and Overton, 2015). A key factor that strongly influences senior homeowners’ decisions in this area are, certainly, bequest considerations. Discussing the topic of reverse mortgages in the case of Spain, Costa-Font et al. (2010) wrote, ‘Spanish society remains deeply entrenched in an inheritance culture where less affluent individuals would be unwilling to take out a reverse mortgage even when faced with economic difficulties’ (p. 390). A similar conclusion was made in the study on the United Kingdom by Toussaint and Elsinga (2009) that ‘downsizing, or selling and subsequently renting a home, were also not regarded as attractive options. People generally aimed to pass on housing wealth to the next generation’ (p. 675). A Korean study (Yoo and Koo, 2008) on the younger generation’s perception of the scheme as a feasible solution to financial hardship showed that children were generally against the idea of their parents applying for the reverse mortgage since this would deprive them of the eventual inheritance. In the case of Australia, Ong et al. (2015) describe the selling up of whole homes in order to release housing equity as an ‘option of last resort’.

The inheritance aspect is of crucial importance and needs to be addressed in a broader context which involves a deeper exploration of complex familial relations. At the basic theoretical level, it is assumed that if elderly households have many children, there is a greater likelihood that these would (financially or otherwise) take care of their parents in the event that such support is required (Haurin and Moulton, 2017). It is thus suggested that elderly people without children would more easily decide to trade off their property for a better pension, while those with children would be less likely to opt for equity release solutions. A study on the subject of equity release in the case of Hong Kong (Chou et al., 2006) indeed found that having children presented a barrier for Chinese elderly people to consider using the reverse mortgage product, due to the ‘traditional customs that older persons will pass their property to the next generation after they deceased’ (p. 723). As has been explained by Ronald and Doling (2012), when the owner uses the financial reserve contained in the home to extract income to pay for necessary welfare, that housing equity ceases to exist, thus denying the next generation all benefits associated with homeownership. In the case of Slovenia, familial ties to homeownership are even more deeply embedded into the traditional family house-building practices, whereby a large majority of such houses were planned and constructed with the aim to continue accommodating the children also after they become adults and create their own families (Sendi, 2017). Described by Gilbert (1999) as ‘sweat equity’, self-built housing thus carries a special meaning and normally holds a value, to its owner, that is worth much more than the ordinary real-estate market value. We therefore argue, in this article, and provide evidence in support of the hypothesis that in the minds of Slovenian elderly homeowners, inheritance considerations may be the strongest barrier that renders all forms of equity release products simply unacceptable.

Method and data

The survey conducted in 2015 covered the population aged 50 years and over. We used a computer-assisted telephone interviewing (CATI) surveying technique. A total of 930 persons responded to the survey. The sample contains 70.7 percent females and 29.3 percent males, which presents a female response rate of almost 2.5 times that of the males. To put this into a national perspective, statistical data for 2016 recorded a gender structure of 51.3 percent females – 48.7 percent males and 57.6 percent female pensioners – 42.4 percent male pensioners (Statistical Office of the Republic of Slovenia, n.d. – SI-STAT data portal). It is useful to explain here that the predominance of female respondents is a standard characteristic that is often observed in almost all large sample surveys in Slovenia. This is especially so in the case of surveys conducted among the elderly population. As some studies have suggested (e.g., Taylor, 2005), females participate in larger numbers in telephone surveys, while the response level of males tends to be higher in the case of online surveys. It will, however, be shown later that the predominance of female respondents was not found to influence the survey results.

Among the respondents, homeowners accounted for 96.9 percent (72.5 percent own house, 24.4 percent own apartment). For the purposes of data analysis, the following age structures (their shares within the sample shown in brackets) were determined: 50–59 (18.3%), 60–69 (31.7%), 70–79 (29.8%), 80+ (17.8%), while 2.3 percent of the respondents declined to state their age. The survey questionnaire consisted of the following three main sections:

Dwelling characteristics (tenure, size, length of stay, dwelling suitability, dwelling maintenance, distance to relatives, attachment to the dwelling, neighbourly relations, etc.);

Household characteristics (household size, economic situation and health situation);

Demographic variables (age, gender, educational level and employment status).

The discussion in this article focuses on the economic segment of the survey. The survey question most relevant to this debate was the one that investigated the level of acceptability, among the elderly, of the equity release mechanisms most commonly referred to in the literature. This question constituted the dependent variable of the analyses which was tested against the following independent variables, that is, the investigated equity release products:

Letting (renting) out part of the dwelling. Offering for rent an entire self-contained apartment in a house or a bedroom or any other such accommodation, which enables the acquisition of an additional monthly income in the form of a rent.

Selling current dwelling to buy a smaller one. Downsizing from a larger to a smaller, less expensive dwelling, thus cashing out part of the equity of the property.

Selling to take up rental tenure. Total housing equity withdrawal, that is, transitioning from homeownership to the rented tenure.

Reverse mortgage. Taking a bank loan securitized by the dwelling, whereby the bank pays the owner either the total loan amount as a lump sum or provides the loan by instalments of an agreed monthly rent amount. The reverse mortgage contract allows the loan taker (owner) to continue to occupy the dwelling until death, without being required to repay the loan. Upon their death, the bank sells the property to regain the loan money together with the accumulated interest. The eventual excess amount after sale is paid out to the heir(s). This is the most widely applied product, commonly referred to in official real-estate terminology also as the home equity conversion mortgage (Equity Release Council, 2012).

Selling in exchange for lifetime use. Selling the dwelling on agreement with the buyer that the seller continues to live in the dwelling until they die. Instead of paying for the cost of the dwelling, the buyer guarantees to pay a lifelong monthly rent to the seller and all maintenance and running costs. The buyer assumes the ownership title after the death of the seller. This product is officially known in real-estate terminology as ‘home reversion plans’ (Equity Release Council, 2012).

Selling with deferred transfer of ownership title. This is a version of the ‘home reversion plans’, the difference being that in this case the buyer pays out to the seller the entire sale amount, the seller continues to live in the dwelling without paying any charges, and the buyer assumes ownership of the property after the death of the seller.

The level of acceptability of each one of the defined equity release products was investigated with a measure based on a 5-point Likert-type scale (whereby 1 = not at all acceptable, 2 = not acceptable, 3 = neither/nor, 4 = acceptable, and 5 = very acceptable).

Survey results

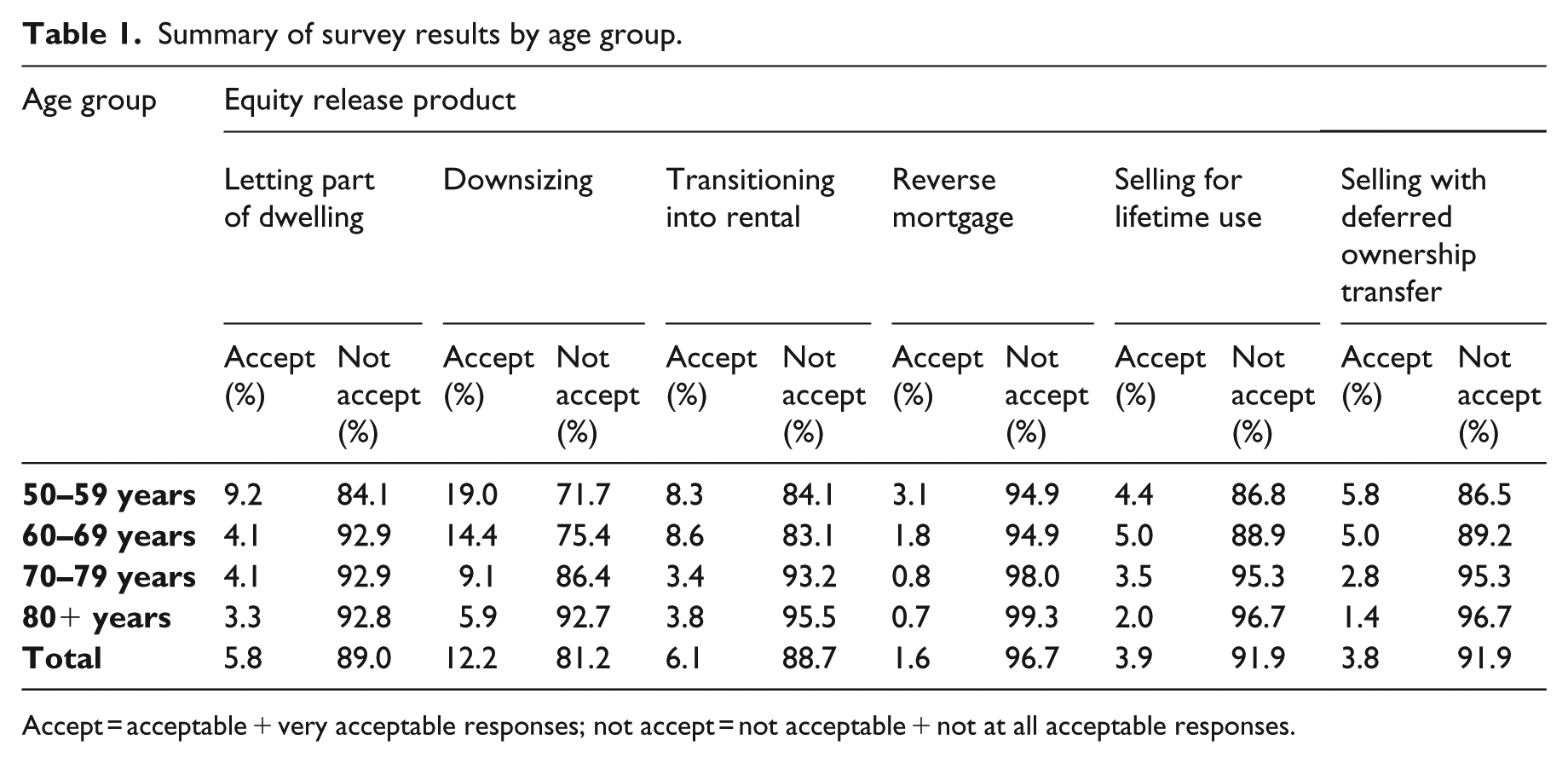

The responses to the survey question are presented by age group, for each one of the six equity release products specified above. In order to be able to gauge better the optimum level of either the acceptability or non-acceptability of a particular product, we sum up the not acceptable and not at all acceptable responses and discuss them together as the not acceptable answers. Likewise, the acceptable and very acceptable responses are summed up as the acceptable responses. Table 1 presents a summary of the general findings for all investigated products.

Summary of survey results by age group.

Accept = acceptable + very acceptable responses; not accept = not acceptable + not at all acceptable responses.

As the figures presented in Table 1 show, letting out part of the dwelling in order to raise some additional income is not acceptable to 89.0 percent of the total number of respondents, with only 5.8 percent indicating that they would accept this product. By age group, the 60–69 (92.9%), 70–79 (92.9%) and 80+ (92.8%) cohorts express an identical level of non-acceptability of the product. For the 50–59 cohort, 84.1 percent reject the possibility of renting part of their dwelling.

Selling to move to a smaller dwelling is not acceptable to 81.2 percent of the respondents, but 12.2 percent would be willing to downsize. It is interesting to note that the age groups rejected the product with an ascending majority, from the youngest towards the oldest cohort, that is, 50–59 by 71.7 % 60–69 by 75.4 percent, 70–79 by 86.4 percent and 80+ by 92.7 percent. Conversely, therefore, the level of acceptability was highest (19.0%) for the youngest (50–59) cohort and lowest (5.9%) for the oldest (80+) age group.

The prospect of selling up to transition into rental housing was rejected by 88.7 percent of the total that responded to this question, while 6.1 percent indicated that this option would be acceptable. This product is not acceptable to about the same percentage of the 50–59 (84.1%) and the 60–69 (83.1%). Similarly, the oldest age groups (70–79 and 80+) expressed about the same level of rejection of the product with 93.2 percent and 95.5 percent, respectively.

The possibility of taking a loan under the terms of the reverse mortgage equity release product was rejected by 96.7 percent of all that responded to the question. By age group, this mechanism was not acceptable to 94.9 percent of both the 50–59 and 60–69 age cohorts, to 98.0 percent of the 70–79 age group, and to 99.3 percent of the 80+age group. Only 1.6 percent of the total number of respondents to this question stated that the reverse mortgage option would be acceptable to them.

The option of selling the dwelling for a monthly rent with continued occupation until death was shown not to be acceptable for 91.9 percent of those who responded to this particular question. The product was strongly rejected by the 70–79 (95.3%) and the 80+ (96.7%) cohorts. With slightly lower percentages, a large majority of the 50–59 (86.8%) and the 60–79 (88.9%) age groups also find this product unacceptable. Of the total that responded, only 3.9 percent indicated an acceptability for this product.

The option to sell with a deferred transfer of the ownership title was rejected by 91.9 percent of the total number of respondents. It is not acceptable to 86.5 percent of the 50–59 cohort, to 89.2 percent of the 60–69, to 95.3 percent of the 70–79 and to 96.7 percent of the 80+, which, once again, reveals ascending levels of rejection, the older the cohort. This product would be acceptable only to 3.8 percent of the total number of respondents.

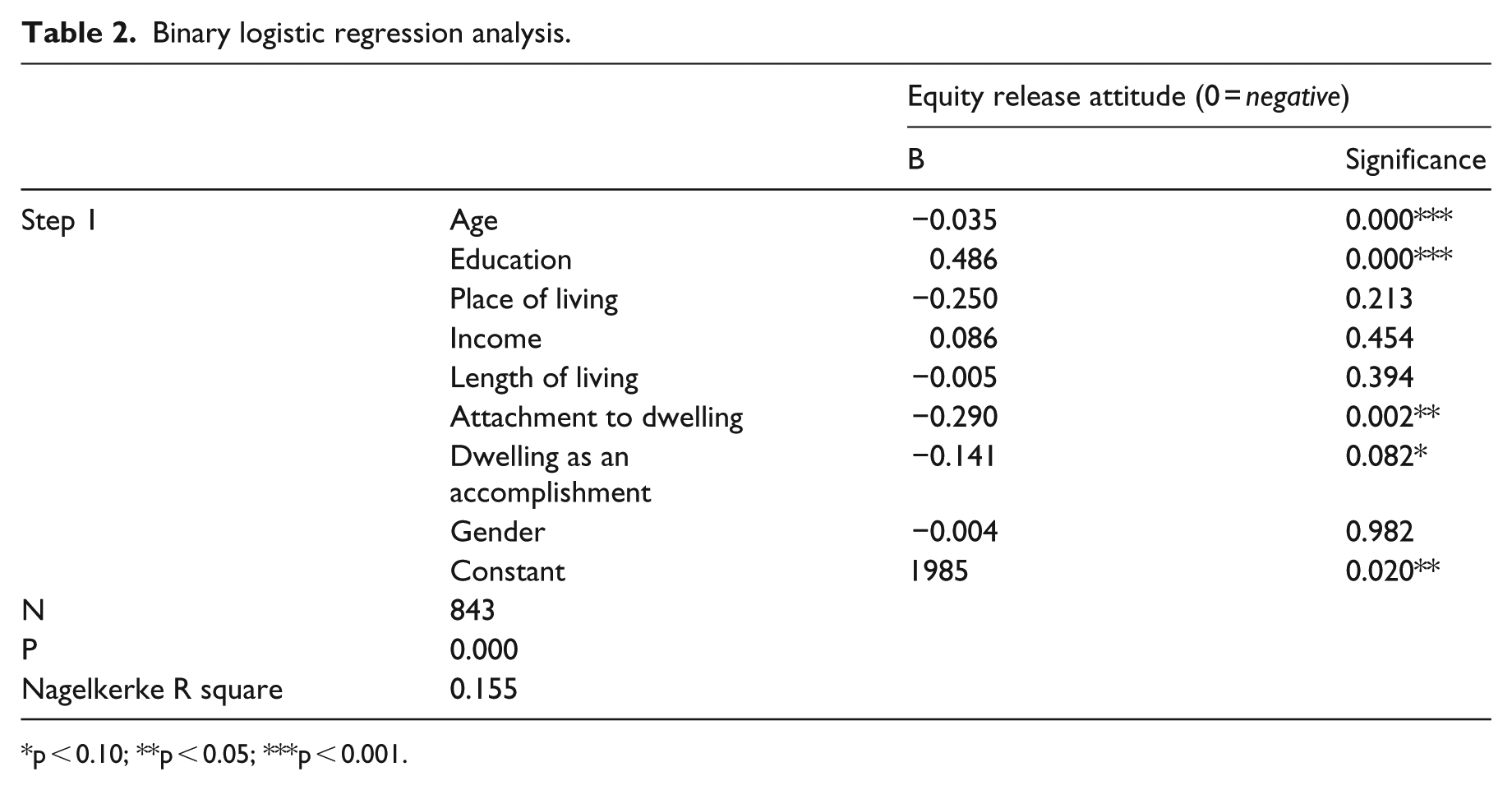

We have further tested the attitudes of respondents towards equity release products in general (Table 2). The dependent variable constructed ‘equity release attitudes’ was binary (due to a very skewed distribution of answers). This variable measured the negative attitude towards equity release (0; that is, for all 6 equity release products, the respondents answered 1 or 2) and (potentially) positive attitude (that is, at least for one equity release product the respondents answered 3, 4 or 5 on the scale of 1 to 5, where 1 means not at all acceptable and 5 very acceptable). The resulting distribution of answers shows that 72 percent of respondents found no option as acceptable. We carried out a logistic regression analysis, with the following independent variables: age, gender, education, place of living (urban or rural), length of living in dwelling, income (measured with ease people can survive on their income), attachment to the dwelling (1 = not attached at all, 5 = strongly attached) and variable that measured that the dwelling represents an accomplishment in life (1 = completely disagree, 5 = completely agree). Initially, we had included in the model also other questions relating to the meaning of housing for respondents, however, these were found to be statistically non-significant, apart from the one that we have included in the final model, that is, dwelling as a life accomplishment.

Binary logistic regression analysis.

p < 0.10; **p < 0.05; ***p < 0.001.

The model is statistically significant. Our findings indicate that men and women do not differ in attitudes towards equity release products, and there is also no difference between respondents living in rural and urban areas. There are also no differences in attitudes due to level of income. The model does, however, show that younger respondents have a more positive attitude towards equity release products in general, as do respondents with higher education. Attachment to the dwelling seems to be a very important explanatory variable for the attitudes towards equity release since those more attached showed more negative attitudes towards the investigated products. Similarly, those who saw their dwelling as presenting their accomplishment in life had a more negative attitude towards the suggested equity release options.

Summarizing the presentation of the survey results, we find that

The reverse mortgage product was the one rejected with the highest percentage of the measure of unacceptability;

Both versions of the home reversion plans (whether monthly rent or cash payment) were rejected with identical percentages by each age cohort;

Downsizing was shown to be the most acceptable option among the products on offer;

Younger cohorts generally indicated a slightly more positive attitude towards equity release;

Attachment to the dwelling plays an important role as does the attribute of a home as a life accomplishment.

While Cirman (2006) has written that the predominance of the homeownership tenure in Slovenia can be partly ascribed to the ‘financial attractiveness’ that households attribute to owner occupation, our study finds that this financial attractiveness of homeownership is not consciously pursued for the purpose of accumulation of wealth that may be eventually extracted during old age. Since homes are almost never traded, Slovenian elderly homeowners do not see the capital value of their housing asset as the most important attribute of their property. Instead, place attachment and the perception of a dwelling as a life achievement are, according to the survey results, aspects to which elderly homeowners put a higher value in relation to their housing asset. Our additional thesis is that underlying all this are very strong inheritance considerations.

Discussion

Generally, the overarching finding is that the Slovenian elderly homeowners strongly rejected all the equity release products presented to them. Regarding letting out part of the dwelling, the responses show that the large majority of homeowners is not prepared to share their property with strangers. One of the key explanations for this may be found in the response to another survey question with which the respondents were asked to indicate the level of importance of certain aspects of homeownership which included, among others, independence and self-reliance. The importance of this attribute of homeownership was stated by 95.5 percent of the total that responded. This clearly shows that homeowners very highly value the aspect of independence and the self-reliance that their home guarantees them. This finding resoundingly confirms Sherraden’s (1991) thesis that people need to own assets in order for them to be self-reliant in life. Second, Slovenia’s private rented sector has, in the past, and continues to be inadequately regulated (especially with respect to landlord–tenant relations, rent defaulting, termination of rental contracts, etc.) such that some potential landlords deliberately stay away from the often very cumbersome private rental market (Sendi, 1999; Sendi and Černič Mali, 2015). Most importantly, however, the rejection of this product may be explained in relation to the characteristically strong familial component of homeownership. In Slovenia (Mandič, 2008; Sendi, 2017), as is the case also elsewhere (Aasve et al., 2002; Delfani et al., 2013; Druta and Ronald, 2017; Hegedüs and Teller, 2007; Mulder, 2003; Yoo and Koo, 2008), elderly people’s houses are very often shared with the owner’s children who usually continue to reside in the parental home whether as singles or even after creating their own families. In such cases, this effectively means that there is no surplus space for eventual renting, and consequently, elderly homeowners would not be expected to consider any such income-raising financial operations as a viable option.

The survey results indicate that the option of selling a large dwelling in exchange for a smaller one would be slightly more acceptable and did, of all the products investigated, score the highest degree of acceptability among all age cohorts. There is a clear explanation here for the higher level of acceptance of the product since downsizing enables the individual to remain within the homeownership tenure. Yet still, a large majority of respondents rejected the product. As Abramsson and Andersson (2012) found, the elderly are generally reluctant to downgrade even in situations where they live in large dwellings with unused space.

Transitioning into rental tenure, applying for a reverse mortgage, selling in exchange for lifetime use or selling with a deferred transfer of the ownership title are all products with one single critical outcome, that is, they effectively mean taking a decision to entirely relinquish the asset, thus encroaching upon the ‘sacred zone’ of homeownership, consequently, inheritance. The familial aspect is particularly important in this regard. First, co-habitation of the elderly homeowners with their offspring and intergenerational bonds naturally implicitly induce a sense of common-ownership of the property between the family members. According to a study by Iacovou and Skew (2011), Slovenian homes have the highest proportion of adult children co-residing with their elderly parents, of all the EU member states. The importance of the family issue was also pointed out as a major factor that influences old people’s decisions in relation to property ownership, in a study which investigated the linkage between demographic change and housing wealth in selected EU countries (Elsinga and Mandič, 2010). In the case of Slovenia, the study found that older people feel very strongly about keeping their property and passing it on to the next generation: ‘a wish to leave a bequest to one’s children was recognized. Some emphasized the need to be self-sustaining, independent of others, it is better to leave something behind than be paid for by others, or leave debts’ (Elsinga and Mandič, 2010: 954). A similar observation was made also in the case of Hungary where it was found that ‘moving house was chosen only as a last resort, and then usually solved only short-term financial problems’ (Toussaint and Elsinga, 2009: 684).

The possibility of extracting housing equity as a ‘last resort’ may also be the explanation for Mandič’s (2016) finding (referred to in the introduction) regarding the ‘outstanding willingness’ of Slovenian elderly homeowners to enter residential care and consume their housing wealth. As the presentation above shows, our survey results reveal completely opposite findings. Elderly homeowners strongly rejected all the equity release products proposed to them. And while it may appear that we have two sets of conflicting findings, both of them are accurate and there is, in fact, no contradiction between them. What needs to be recognized here is that our study investigated six specific equity release products which do not include the aspect of equity release that the study by Mandič discusses. Concretely, Mandič’s (2016) study focused on what the author characterized as ‘The intergenerational flow of resources where adult children cover the cost of residential care in excess of the parents’ pension and in exchange for the housing asset, thus represents a specific case of an informal equity-release scheme’ (p. 165). This clearly shows that the two studies investigated different aspects of the asset-based welfare concept. Mandič’s study very elaborately describes the importance of the familial relations in Slovenian households: The role of adult children is particularly important, looming large at the turning point where a frail parent is no longer able to live independently; adult children were given the major role in consideration of the responsibilities and resources available for resolving such a situation. They were seen as most responsible for organizing the support or a residential home, and also for helping to pay for it. (Mandič, 2016: 165)

This, specifically, means paying part of the cost when the frail parent is moved to an old people’s care institution. In cases where the potential heirs are not capable of covering the costs for care these are covered by the state, which then has the legal right to repossess as much of the inheritance property (all forms of property) as is required to recover the costs incurred. And while there is no legislation prohibiting the elderly homeowners from transferring property to family members before moving into state-funded care institutions, the prior transfer of ownership is not known to be a common practice. In any case, what needs to be stressed here is that when it comes to this stage in the life of the elderly homeowner, it is the adult children (or other closest relatives) who are normally in control. They are the ones that take the final decision whether or not to move the homeowner into some form of institutional care. It is, therefore, important to recognize that under these circumstances the transfer of ownership of the dwelling from the frail parent to their adult children (or other family members) may not always be understood and explained as a ‘readiness’ or ‘willingness’. As Clark and Deurloo (2006) found when investigating the home-moving behaviours of older people, elderly homeowners give up their dwelling ‘only when they are more or less forced to, and that is mainly for health reasons’ (p. 269).

Conclusion

The survey findings presented above thus clearly show that a large majority of Slovenian elderly homeowners do not consider the equity release products that were presented to them as viable options for improving their economic situation during retirement. Apart from letting out part of the dwelling and downsizing, all the investigated products have one major shortcoming which Slovenian homeowners simply cannot accept, that is, being deprived of the ownership of their housing asset. While the survey findings indicate a slightly more favourable inclination of younger cohorts towards equity release mechanisms, this positive attitude is shown to decrease over time, with age. It may also be important to note that the 50–59 age group are not yet pensioners since the retirement age is currently set at 65 years, for both females and males. The actual truthfulness of this favourable attitude can be investigated and established only though a longitudinal survey, which may be a subject for a future study. At the moment, however, the circumstances described above lead us to conclude that housing assets are almost untouchable in Slovenia, once a homeowner, forever a homeowner.

Concrete proof of this may be seen in the reaction of Slovenian pensioners to the legislation that was adopted in 2010. As part of the austerity measures introduced to combat the financial crisis that began in 2007, the Slovenia government adopted new legislation which abolished some of the previous social welfare transfers. The welfare retrenchment measure most relevant to this discussion was implemented through a legal provision which gave the government the right to repossess inheritance property upon the death of a previous social benefit recipient, as a repayment for the social welfare support provided from the state budget. The abolition of supplementary allowances through the implementation of this measure, of course, meant a lowering of the subsistence income of the poorest pensioners, thus increasing their at-risk-of-poverty threat. This threat notwithstanding, about 13,000 pensioners (33% of the total number of social benefit beneficiaries, at the time) promptly declined the allowances (Ministry of Labour, Family and Social Affairs, information provided upon author’s request). This decision, of course, meant that the lowest income homeowner-pensioners were prepared to live on a lower subsistence budget in order to protect their assets from eventual repossession by the state. Although this particular aspect did not constitute part of our survey, the rejection of state support by poor homeowners in order to protect their inheritance property provides concrete proof of the ‘untouchability’ of inheritance property. This evidence also contradicts the theory that suggests that the ‘asset-rich but cash-poor’ homeowners (Burgess et al., 2013; De Decker and Dewilde, 2010; Delfani et al., 2013; Hirayama, 2010; Leather, 1990) are the categories of pensioners to whom, especially, the asset-based welfare concept applies.

Based on the findings presented above, we argue that whether consciously or not, inheritance considerations broadly constitute the major obstacle to any meaningful implementation of the asset-based welfare concept in Slovenia. The reaction of asset-rich but cash-poor homeowners to government austerity measures is clear proof that there is no trade-off between homeownership and welfare. As such, the notion of asset-based welfare, essentially, does not convey much meaning (if any) to the great majority of Slovenia’s elderly homeowners.

In conclusion, several important questions need to be raised. First, is the concept of asset-based welfare meaningful at all, generally? Second, if it is meaningful, is it feasible? Third, if it is feasible, what is required in order to ensure its successful implementation in practice? Would better knowledge about, and a better understanding of, the specific equity release products help to make them more acceptable to seniors? These are questions that need to be addressed at the global level, whereby the research community must play a leading role in the conducting of the relevant analyses necessary for laying the foundation for the formulation of appropriate national policies. As for Slovenia, in particular, the fourth question would be whether the concept has any chance of ever becoming meaningful to elderly homeowners, given the described specificities of the country’s homeownership tenure.

Footnotes

Acknowledgements

The authors are very grateful to the Editor, Emmanuele Pavolini and two anonymous referees whose comments and suggestions significantly helped to improve the quality of the article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article is based on the findings of the research projects ‘Innovative Forms of Living for the Elderly in Slovenia’ (grant no. J5–6824) and ‘The Model of Quality Aging in Place in Slovenia’ (grant no. J5-8243), both financially supported by the Slovenian Research Agency.