Abstract

The ambitious targets of peaking CO2 emissions before 2030 and reaching carbon neutrality before 2060 (Goal 3060) have emerged as the driving force in the development of China's low-carbon energy policy. Adopting a systematic review approach, this article provides a timely analysis of key Chinese renewable energy and energy efficiency policies under Goal 3060 across five sectors: electricity, industry, transportation, buildings, and local governments. In addition, the review identifies challenges to be addressed and offers policy recommendations. There are five main conclusions: (1) expedite the development of market-based and network-based governance systems; (2) pursue the harmonization of policies by avoiding contradiction and fragmentation; (3) develop new policies, especially in the building and transportation sectors; (4) embrace surveillance technologies to improve implementation and compliance; and (5) ensure just transition by implementing policy to reduce the negative socioeconomic impacts on fossil fuels-based communities and workers. This review serves as a useful guide for scholars interested in China's clean and low-carbon energy transition.

Introduction

Over the past decade, a series of domestic and international challenges has increasingly pressured the Chinese government to place climate change higher on its policy agenda. 1 First, as China becomes the world's largest emitter of heat-trapping gases and contributes to approximately 28% of global greenhouse gas emissions, 2 the urgency of advancing decarbonization in the interest of international relations, climate diplomacy, and global climate landscape has reached an all-time high.3–5 Second, rapid economic development has resulted in increasing energy dependence on foreign fossil fuels—it is expected that the ratios of dependence will be around 70% for oil by 2050 and 50%–60% for gas by 2030. 6 As such, China's low-carbon transition is driven by the desire to enhance national energy security.7,8 Third, decarbonization is closely linked to enhancing the economic competitiveness of China.9–12 The government sees low-carbon transition as a key opportunity for shifting the country's low-value-added, highly polluting industries to being driven by technological innovation.13,14 Finally, the concern for social well-being also drives China's low-carbon transition. In addition to avoiding the negative consequences of climate change, decarbonization can address a wide range of environmental and social issues, such as ecosystem and environment protection, air quality improvement, food security, public health, livelihood, and poverty alleviation.15–19

Under these circumstances, China has been treating climate change as an important socio-economic and political issue.1,20,21 On September 22, 2020, President Xi Jinping announced the targets of peaking CO2 emissions before 2030 and achieving carbon neutrality before 2060 (Goal 3060), which further strengthened China's climate agenda and spurred low-carbon transition. Since mid-October 2021, the “1 + N” policy framework for Goal 3060 has been on the table, comprising of “Working Guidance for Goal 3060” as a top-level design document, “Action Plan for the Carbon Peak” as the overarching document among N policies, and a series of enforcement plans and support schemes in key industries and focus areas (energy, industry, transport, rural–urban development, etc.). Goal 3060 encompasses the dual carbon targets relating to carbon peaking and neutrality. In order to bring the dual carbon prospect within reach, the top-design document has set goals of more than 65% reduction in carbon intensity by 2030, compared to the earlier deadline of 2005, and around 25% share in non-fossil fuel by 2030; furthermore, non-fossil energy consumption is expected to account for over 80% share by 2060. In fact, in 2020, the carbon intensity was 48.4% lower than the 2005 level, and non-fossil fuel consumption rose to 15.9%.22,23 In the context of such rapid policy developments, a fresh review of the progress of China's renewable energy and energy efficiency policies is needed to keep track of the changes in the field.

Adopting a systematic review approach, this article aims to critically examine the predominant renewable energy and energy efficiency policies driven by Goal 3060. The review is organized into five themes: electricity, industry, transportation, buildings, and local government. Considering that electricity is the major contributor (51%) to carbon emissions, followed by industry (25%), transportation (9%), and buildings (5%), 24 energy-related sectors are the foci of this study. Moreover, China's hierarchical government-led structure exists in the policy process, where the central government is a principal policymaking body and local governments are delegated policy implementation and experimentation.25,26 Policies targeting local governments are thus another crucial part of the review. In each theme, we adopted an inclusive search strategy to retrieve papers. Keywords such as “energy,” “low-carbon,” and “zero-carbon” were used in conjunction with “industry,” “transportation,” “buildings,” and “electricity.” These keywords were used to search databases such as Google Scholar and Web of Science. We carefully checked the collected papers to ensure their relevance. Then, a qualitative synthesis of the themes was conducted, focusing on the policy background, policy evolution, and a critical analysis of the policies. In addition to scholarly work, other sources including government documents, research reports, and websites were consulted to support the analysis.

Electricity

The Renewable Energy Law, enacted on January 1, 2006, has spurred developments in wind and solar photovoltaic (PV) power generation, mainly through economic incentives (e.g., subsidy and feed-in tariff (FiT)) to generators and procurement stipulation to electric utilities (renewable portfolio standard [RPS]).27,28 By 2020, China had a total grid-connected capacity of 253 GW of solar and 281 GW of wind power, 29 leading the global solar and wind cumulative installation race for 6 and 8 consecutive years, respectively. 30 However, the new renewable power generation has posed challenges to grid operation, resulting in solar and wind power curtailment problems, most severely in 2016.31,32 This is not only because of the technical difficulties faced by the grid in connecting, transmitting, distributing, and storing, but also because of uneven resource distribution, local economies protection policies and interprovincial power trading barriers.31,32 Furthermore, the burgeoning installation capacity is also rapidly worsening the burden on government subsidy, with regard to maintaining a fixed price policy for the FiT.27,33

Nevertheless, renewable electricity must continue its rapid growth, in order to reach Goal 3060. The government has set goals of boosting the wind and solar power capacity to over 1200 GW by 2030. In fact, the main challenge to Goal 3060 is that China's power sector will remain coal-dominated in the foreseeable future, 34 even though the share of coal in total energy consumption has declined from 72.4% in 2005 to 56.8% in 2020. 22 Therefore, developing new renewable energy policies to decarbonize the electricity sector is crucial.

RPS and green certificate

RPS, which stipulates suppliers’ minimum production share of renewables in the electricity sector (either an absolute increment or a rate of increase), is a common policy tool for renewable electricity development and carbon reduction. 35 It has been reinforced by laws and regulations in countries such as America, Australia, Japan, Britain, and Italy. 36 In 2007, China introduced RPS for grid companies and electricity providers mandated to achieve renewable energy targets, but the policy was overshadowed by the FiT policy. 28 After a decade of debate, a new RPS was introduced in May 2019. 37 According to this new version, the central government assigns renewable energy electricity consumption (REEC) quotas to provinces, and provincial governments are responsible for the minimum proportions, which are fulfilled by grid companies, independent electricity retail companies, and large electricity purchase end-users. Since 2021, provincial REEC quotas have become obligatory targets. The guaranteed grid connectivity of 2021 is no less than 90 million KW. In 2030, each province will be assigned a quota (40% for REEC and 25.9% for non-hydro electricity), in order to meet the total REEC requirement (11 trillion KW).

The government has also introduced the concept of green certificate (GC) as a guaranteed mechanism of renewable energy consumption. 37 It stipulated that local end-users, who are not able to meet the minimum REEC, can purchase GCs via the trading platform, or via consumption quotas acquired from those who have surplus quotas over the minimum requirement. GC is a certification of renewable electricity generation, and one GC corresponds to the production of one-megawatt hour of renewable electricity with producers gaining additional revenue. 38 In China, renewable electricity producers (only for the generation of onshore wind power and solar PV power for now) are qualified to sell GCs to government agencies, public institutions, or individuals. The GC under the RPS was officially introduced, with effect from January 1, 2021. 39 REEC still constitutes the chief approach to RPS, supplemented by GC on a volunteer basis. The combination of RPS and GC is designed to respond to the solar and wind power curtailment and subsidy debt, which has shifted the REEC focus from the producer-side to the consumer-side with more stakeholders being involved. 40 Previously, both RPS and GC encountered several issues within China, such as unclear penalties and inactive GC trading.41,42 The new joint initiative of bringing the GC under RPS needs to be sustained in the future.

Grid parity and phasing out subsidy

In 2021, three major policy documents have been issued to phase out subsidies for solar and wind power.43–45 Household solar PV is the only type of renewable power that enjoys a subsidy of 0.03 RMB/KW. In place of subsidy, the policy of grid parity has been implemented for China's newly filed projects in wind and solar power, in August 2021, including concentrated solar PV, industrial and commercial solar PV, and onshore wind power. The tariff on these new projects must match the local coal-fired power benchmark price or may be fixed on a market-oriented basis. As for the newly approved offshore wind power projects, where the cost is still very high, FiT is set by provincial authorities or by competitive allocation.

The change in policy is mainly because the price of renewable energy has fallen sharply. For example, China's solar PV power cost has fallen by 80%–90% over the past decade, which is now cheaper than conventional coal power. 46 From 2019 to 2020, the cost has declined by 19%. 47 It is thus possible for the government to introduce a subsidy-free policy environment. Looking forward, several studies have suggested that other types of renewable power can also reach parity, but require government policy support, such as concentrated solar PV with GC trading, 48 onshore wind power under a high on-grid coal price (0.5 RMB/KW), 49 and offshore wind power under carbon finance policy. 50 Thus, grid parity has evolved from government policy support, impersonal cost reduction and technical development. 51

Electricity market liberalization

Electricity market liberalization is another key policy tool for promoting renewable energy. Electricity reform began in 1985 when domestic private companies and foreign investors were allowed to invest in electricity generation. 52 To address the problems of complicated and inefficient generation tariffs, a separation between government and enterprise was implemented. This led to the foundation of the State Power Corporation in 1997, a new monopolist controlling half of the total generation assets and almost all of the transmission and distribution assets. 52 The year 2002 marked a milestone in China's electricity market reform, because the State Power Corporation was split into the “Big Five” (five large-scale generation corporations with reallocated generation assets) and two transmission companies (State Grid and South Power Grid), leading to a division between generation enterprises and electricity grids.52,53 In 2015, “Document No. 9” initiated an exploration of market-set prices, in which larger industrial users and competitive retailers could directly make deals with coal-fired power plants. 54 According to “Document No. 9,” market entities (power generation enterprises, electricity sales enterprises, electricity users, independent auxiliary service providers, etc.) carry out electricity transactions in market-oriented ways (independent negotiation and centralized bidding), on a yearly, quarterly, monthly, and weekly basis in the medium- and long-term markets, 53 and on a daily basis in the spot market. 55 From then onwards the new market structure and pricing mechanism have been implemented, removing government-generated power from the market. 56 In September 2021, a new variety of green electricity was added to the medium- and long-term markets—the first batch was launched with 259 market entities from 17 provinces, trading 7935 GW. The trading is organized by power trading centers, with the main players being grid enterprises, wind and PV enterprises, users, and electricity sales companies.

However, China's electricity market is still in its infancy. First, there is an imbalance between the coal market and the electricity market, because the electricity price decided by the government cannot change at a pace consistent with the coal price decided by the market. 57 Second, the dual-track electricity price mechanism generates an imbalance in funds, due to the mismatch between spot price and planned price in electricity trading. As there are two types of generating units in the spot markets, marketed and non-marketed, the grid enterprises might pay much more, if the non-marketed generating units settle the bill based on a fixed price, which is higher than the market price. 58

Industry

China's industrial sector accounted for 66% of total energy consumption in 2020 29 and around 50% of total carbon emissions in 2019. 59 Therefore, the improvement of energy efficiency in the industrial sector is crucial. To improve energy efficiency in energy-intensive industries (e.g., iron and steel, petrochemicals, non-ferrous metals, and building materials), the government has proposed, by 2025, a substantial increase of green low-carbon energy consumption in key areas, a rise in the proportion of new energy efficient motors to over 70% and that of new energy efficient transformers to over 80%, and a decrease in energy use per unit of the added value of large industrial enterprises by 13.5% from the 2020 level. 60 To achieve these objectives, the government has enforced three key policy mechanisms: energy efficiency benchmarking (EEB), time-of-use (TOU) electricity pricing, and the carbon market.

Energy efficiency benchmarking

EEB is a useful tool to measure the energy performance of an individual plant or industrial sector, guiding industrial enterprises in carbon reduction.61,62 In November 2021, five Chinese central government departments jointly unveiled EEB for energy-intensive industries in 14 minor key areas, which would come into force from January 1, 2022. These key areas are attached to five categories, comprising fossil fuel processing, chemical product manufacturing, non-metallic mineral products, and ferrous and non-ferrous metal smelting and rolling industries. 63 EEB involves two levels. One is the standard level, which is a compulsory minimum requirement; while the other one is the optimal level, which is a progressive indicator for driving industries to enhance their energy efficiency. Underconstructed and to-be-constructed projects with high energy efficiency would benefit from step tariffs and high-quality financial services. However understandard industrial enterprises are to be compulsorily upgraded to the standard level within 3 years, or even better, such unqualified enterprises are to be shut down. Earlier, the five central government agencies had announced a proportion target of more than 30% of production capacity reaching the benchmark level, in the case of steel, cement, aluminum, and output of raw materials, by 2025.

In the industrial sector, China has implemented the energy efficiency obligations of assigning energy conservation targets to a wide range of enterprises since 2005. An example is the Ten Thousand Enterprise Low Carbon and Energy Conservation Program.28,64 In order to achieve the “dual carbon” goal, EEB is pertinently targeted at high energy-consuming and high-emissions enterprises, with the aim of improving energy efficiency. Local governments, responsible for the implementation of EEB, are urged to make situation-specific plans. While compulsory standards secure carbon reduction, aggressive standards offer incentives to potential industrial enterprises for further improving efficiency, through supporting policies. Transmitting accountability pressure to local governments may lead to a crackdown on disqualified enterprises, though. Coordination between EEB and supporting policies needs to be sustained in the future.

TOU electricity pricing

TOU electricity pricing is a dynamic electricity pricing mechanism, which measures and charges electricity use according to different time periods. 65 The dynamic electricity pricing mechanism has different forms, such as TOU tariffs according to peak and off-peak times of the day, and seasonal tariffs according to high-demand and low-demand seasons. 65 In July 2021, the National Development and Reform Commission (NDRC), as a price-setting agency in China, made progress in TOU. 66 First, the peak-valley price difference would be raised to at least three times, or even four times in places where the peak-to-valley rate exceeded 40%. Second, seasonal electricity price mechanisms would be improved, and mechanisms for critical peak electricity price and deep valley electricity price would be put in place. Third, TOU would be implemented for all commercial and industrial users, except in special cases, and promoted in the residential sector. Extending price differences, developing price mechanisms, and widening the scope of implementation characterize the new TOU policy. Under TOU, electricity users choose the timing of electricity consumption to elude high-peak periods, ultimately cutting peaks and filling valleys for grid stability, thereby improving the efficiency of power use. 65

Carbon market

The cornerstone of China's carbon market is the Emissions Trading System (ETS), which was introduced in 2011, in the form of seven pilots.20,67 As of now, there exist two varieties in China's ETS: carbon emission allowance (CEA), supplemented by Chinese Certificated Emissions Reduction (CCER).

The rationale of CEA is cap-and-trade. In the ETS, allowances are allocated by the government to permitted companies and industries, as per limits set on their total emissions. Companies with lower than permitted emissions can sell excess allowances to those with higher emissions and profit from the same. 68 In July 2021, China's national ETS officially started trading with yearly emissions of 4500 MT, as the largest carbon market around the globe. Considering the relatively mature management and well-grounded database of the electricity sector, only 2225 electricity companies have been permitted in the ETS at the moment. At this stage, allowances are granted freely to the key emitters. The trading platform is in Shanghai, while the registry platform is in Wuhan. The main objective of the ETS is to reduce the abatement cost of carbon. Fang et al. 69 suggest that ETS can make emission abatement costs fall by 61.41% to 80.33%. In the long run, multi-sector ETS has harmonized emission abatement efforts as well. 70 However, Feng et al. 67 suggest that the trade-off between efficiency and equity in a networked ETS should be balanced, because poorer areas with more emissions probably constitute net permit sellers. In addition, the yearly carbon trading volume is estimated to be equivalent to only around 4.3% of the total emissions, thereby adversely affecting the vitality of the ETS. 71

CCER involves the certification of reduction in carbon emission from projects in solar, wind, and water energy, carbon sinks, and others. 72 It is an offset mechanism, allowing emitters to purchase CCERs (one CCER is equal to each allowance), in order to offset excessive emissions via the ETS. As the price is lower than that of CEA, CCER has the advantage of reducing abatement costs for emitters. 73 CCER started operation in 2012, promoting low-cost emission reduction and renewables, 74 but has suffered a prolonged suspension from 2017. Overall, Li et al. 74 suggested that realizing the homogeneity and equivalence of carbon CEA and CCER is the premise to realize the minimum national total cost. However, there is a wide gap between China's carbon market and western carbon markets, with regard to factors such as carbon pricing, carbon allocation, emissions sources, and the introduction of laws and regulations. 75

Transportation

Although the transportation sector currently accounts for less than 10% of the total carbon emissions in China, the expansion in demand and infrastructure is contributing to carbon emissions.76,77 Among the transportation subsectors, road transportation constitutes the largest proportion (over 70%) in China. 78 Therefore, the road transportation sector will concentrate upon on-road transportation policies for reaching Goal 3060, including new energy vehicles (NEVs) and vehicle emission standards.

New energy vehicles

As a result of fuel economy, low-carbon fuels, and replacement of petroleum with electricity, the promotion of NEV has become one of the most important policies for mitigating climate change. 79 Motivated by industrial policies, trial programs, fiscal subsidies, and tax incentives, 80 the last decade witnessed a remarkable development in China's NEV. For example, the year 2013 marked a turning point with regard to significant enhancement in volumes of production and sales, thanks to a direct subsidy scheme and the purchase tax exemption, along with the pilot program of “1000 vehicles in 10 cities.”81,82 The NEV policy targets three major technologies: battery electric vehicles, plug-in hybrid electric vehicles, and fuel cell electric vehicles. 82 Sales volumes slumped by 4% in 2019 due to the year-to-year subsidy decline; but, China remained the largest NEV producer and marketer in the world, in 2020, for the fifth consecutive time. 81

Existing NEV achievements and ongoing NEV development are conducive to Goal 3060. At present, there have been two main policy changes in China's NEV program. One is the phasing-down of subsidies, which means gradually reducing subsidies in a planned and focused manner. Having introduced a subsidy scheme in the 2010s, 83 the central government extended the original plan, postponing the scheduled complete termination of subsidies at the end of 2020. 84 Subsidies were scheduled to be slashed by 10%, 20%, and 30% over the previous year, from 2020 to 2022, respectively. Particularly, in 2021, a decline rate of 10%, instead of 20%, was applied to buses, coaches, and other specialized delivery vehicles, to boost electrification in the public sector, along with local voluntary subsidies. Subsidy for fuel cell electric vehicles has been canceled in 2020. Another policy change is the “dual credit” system, composed of the Corporate Average Fuel Consumption (CAFC) credit and the NEV credit. Jointly introduced by five ministries in June 2017, 85 the system was updated to be effective from January 1, 2021. In the new system, one negative CAFC credit can be offset by one extra NEV credit. Therefore, the more NEVs a company produces, the more credits it earns. In addition, the rates of NEV credits during 2021–2023 were required to reach 14%, 16%, and 18%, respectively.

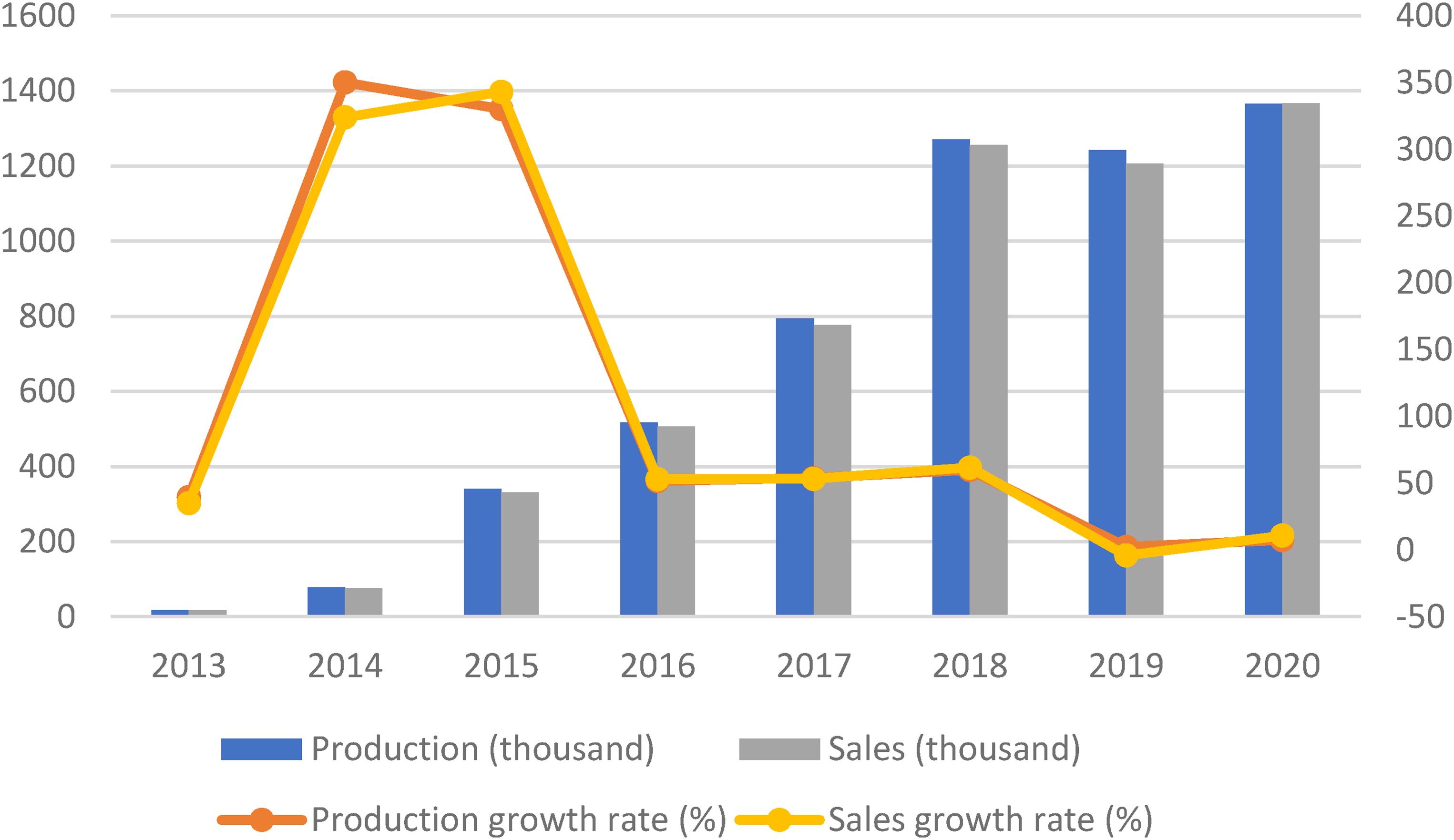

The government aims to increase NEV sales to 20% of total new vehicle sales by 2025. 86 Past years have witnessed the growth momentum in production and sales of NEV in China (Figure 1). In 2022, NEV production and sales increased by 96.9% (7.056 million) and 93.4% (6.89 million), respectively. 87 The NEV market share (market penetration) in 2022 was 25.6%. 87 He et al. 88 observe that, despite rising credit prices and extra NEV credits, medium-sized automakers delay NEV investment to pursue profit maximization, which should be modulated by policy parameters. Within a hierarchical optimization decision-making module, Chen et al. 89 believe that the “dual credit” system cannot do better than decoupled dual credits or singular CAFC credit, as the NEV penetration will increase and the NEV cost will decrease in the future.

Production and sales of NEV (2013–2020). NEV: new energy vehicle.

Vehicle emission standards

Tougher on-road emission standards can mitigate emissions over the long term. 90 In China, stricter national vehicle emission standards are contributing to Goal 3060. The Ministry of Environmental Protection (predecessor of the Ministry of Ecology and Environment) and the General Administration of Market Supervision jointly issued the China 6 Emission Standards for light-duty vehicles (LDVs) on December 23, 2016 and the China VI Emission Standards for heavy-duty vehicles (HDVs) on June 28, 2018.91,92 Each of them has two sets of emission limits—a and b—to be applied at two stages on a national scale. For LDVs, China 6-a, commencing in July 2020, is slightly more rigorous than Euro 6 and slightly less rigorous than the US Tier 3. Furthermore, China 6-b will reach the average limits of the U.S. Tier 3 of 2020. 93 For HDVs, China VI-a was sequentially implemented across different vehicle types from 2019 through 2021. Compared to the emission limits of China V, those of China VI are remarkably lower in nitrogen oxide (77%) and particulate matter (67%), which is equivalent to Euro VI. 94 In addition, the on-board diagnostic (OBD) vehicle-mounted system, which tests emission-related components of vehicles to report faulty diagnosis, has been updated to the more stringent OBD II system. 93 However, the implementation of vehicle emission standards has encountered challenges, such as fraud during production compliance and in-use inspection tests, and unreliable retrofitting. 95

Buildings

Based upon the life cycle of China's buildings in 2020, energy consumption accounted for 45.5% of the total (around 2.27 billion TCE) and carbon emission constituted 50.9% of the total (5.08 billion T). 96 By 2030, it is predicted that building energy use will be around 40% of total energy consumption and building carbon emissions will reach a peak, in the context of more policies. 97 To limit the emission impacts of buildings, the Action Plan of “1 + N” policy system set three goals in urban and rural construction, to be achieved by 2025. The goals include the full implementation of green standards for newly constructed buildings, 8% replacement rate of renewable energy in urban buildings, and 50% replacement rate of solar panels in newly constructed public and industrial buildings. 98 Given the above, China has implemented the measures of building energy codes, existing building retrofits, the whole-county rooftop solar PV pilot program, and building integrated PVs.

Building energy codes

Building energy codes are intended to promote building energy performance by laying down guidelines and rules for the design of buildings and compliance with the provisions of building construction. 99 In the context of Goal 3060, in October 2021, the Ministry of Housing and Urban-Rural Development (MOHURD) issued an updated standard for energy conservation and renewable energy use in buildings, which will come into effect from April 1, 2022 onward. 100 Its prominent feature is the mandatory codes for carbon intensity introduced for the first time in the building sector. Accordingly, carbon intensity has to be reduced by 40% in the case of new residential and public buildings, compared to the 2016 levels, resulting in an average decrease of 7 kg CO2/(m2a). Another feature of the updated standard is the design of new and public buildings. The average energy consumption is required to decrease by 30% for the former, and by 20% for the latter, compared to the standards of 2016, including a 75% average energy saving rate in severely cold zones and cold zones, 65% in other climate zones, and 72% in public buildings. The new energy codes cover new buildings, existing buildings, renewable energy systems, construction, testing, acceptance, and operation, which cover all the key stages of the building life cycle. However, implementation challenges need to be addressed, such as poor enforcement in small cities and towns, unsatisfactory compliance rates, breaks in the monitoring of the life-cycle energy performance, insufficient information and awareness, and immature financial regulation systems.99,101

Existing building retrofits

Since the 1980s, the foci of the existing building retrofits in China have extended from the residential buildings in northern areas to various building types in varied climate zones, from building envelope alone to high-efficiency power applications and environmental optimization, and from the energy efficiency of the separated building to the whole-process sustainability of the complexes and communities. 102 The element of green was added to the existing building retrofits during the 11th Five-Year Plan (FYP) period (2006–2010), which was essential for carbon emission reduction and energy efficiency improvement. It included heating engineering projects, innovating in renewable energy and energy efficiency equipment, grading energy performance, and offering economic incentives.103,104 In the 13th FYP, the MOHURD set the objectives of existing building green retrofits, covering 500 million m2 of residential buildings and 100 million m2 of public buildings. 104 Under the 3060 Goal, China aims to achieve at least 350 million m2 of existing building retrofitting projects, 100 million m2 of residential buildings and accumulative 250 m2 of public buildings during the 14th FYP period (2021–2025). 105 Additionally, the MOHURD has been deploying a national strategy of urban renewal, wherein green retrofitting of existing public buildings is a vital component, relating to the reduction of pollution and carbon emissions, metering and monitoring of energy consumption, and evaluating low-carbon performance. In January 2022, the State Council issued a general plan for energy conservation and emissions reduction during the 14th FYP period (2021–2025), which stressed upon retrofitting projects. 106 As seen in previous instances, the challenges faced by such projects include inadequacies in punishment and post-retrofit performance, lack of flexibility and coordination among policies, limited financial support and return on investment, scarcity of public awareness, and the underdevelopment of novel technologies.103,107–109

Whole-county rooftop solar PV pilot program

The retention of subsidy policies for household solar PV projects indicates that the deployment of distributed solar PV is lagging behind. In June 2021, the National Energy Administration (NEA) called for proposals on county-level rooftop solar PV pilots on a national scale, 110 and published a list of 676 pilots 3 months later. 111 Under the principle of “installation as far as possible,” the whole-county rooftop solar PV pilot program required the pilots to reach at least 50% of rooftops equipped with PV systems for government buildings, at least 40% for other public buildings (schools, hospitals, and village committees), at least 30% for industrial and commercial buildings, and at least 20% for residential buildings, by the end of 2023.

While the program sets ambitious targets, it remains doubtful whether it can overcome existing barriers to distributed PV, such as rooftop ownership complications, unattractive economic benefits, technical barriers to grid connection, and difficulties in financing, leading to dampened enthusiasm for these projects. While public and government buildings are free from ownership trouble and perhaps less sensitive toward financial returns, industrial, commercial, and residential buildings would remain a problem. 112 As such, more practical business models need to be explored. 113 In addition, the pilot program takes place across a whole county, and given the political pressure upon local governments to achieve the targets, campaign-style and command-and-control enforcement is likely to take shape. Furthermore, in order to simplify implementation, local governments such as those in Gansu, Shanxi, Zhejiang, and Anhui offer the contract to one single enterprise. As central state-owned enterprises are superior in funds, financing, and reputation, they are preferably selected by local authorities, thereby impeding small and private PV companies in China's solar PV markets.

Building integrated PV

Building integrated PV (BIPV) is a technology that makes the PV system a part of the roofs, windows, facades, and shading devices of buildings. 114 BIPV and building-attached PV (BAPV) are two types of PV systems. The main difference between them is that, BIPV can directly incorporate PV systems into building structures (e.g., roof or facade), is more flexible and lightweight, more durable, more wind-resistant, and more aesthetically pleasing, compared to BAPV, which is immobilized by additional mounting structures and moving rails. 115 After the concept emerged in the early 1990s, BIPV has been keenly pursued by Canada, Australia, the United Kingdom, Japan, Sweden, and China, over the past two decades. 116 However, it has not been developed much in China. In the following 5 years, BIPV will be one of the key projects for conserving energy and reducing emissions. 106 Incentive policies have been offered by local authorities. For example, the subsidies vary from 0.3 to 0.4 RMB/KWH and there exist subsidy limits of 1–3 million RMB in some provinces, such as Guangdong, Jiangsu, and Beijing. During the 14th FYP period, China set a goal of over 50 million KW of BIPV. 105 Although the first domestic BIPV-roof standard has been completed, several complex areas remain to be explored, such as technological barriers, rates of building utilization, business models, and market inspection and management. 117

Local government

In China, local governments play an important role in policy implementation. Therefore, local governance is an important part of China's energy policy. In pursuit of Goal 3060, the central government has strengthened incentives for local governments to reduce carbon emissions using three mechanisms: dual control system (DCS), dual control barometer (DCB), and central environmental inspection (CEI).

Dual control system

The 13th FYP (2016–2020) introduced the DCS to control both total energy consumption and energy intensity. 118 Total energy consumption is defined as the amount of energy consumed during a particular period, whereas energy intensity refers to the energy efficiency of the economy, calculated as units of energy per unit of GDP. Accordingly, targets to control energy consumption and intensity were assigned to individual provinces, followed by strict evaluation. In September 2021, the NDRC, China's top economic planning agency, released a new plan for the DCS, which fixed energy intensity as an obligatory goal (a decrease by 13.5% in 5 years and 3% in 2021) and energy consumption as an anticipatory goal. 119 As such, the energy intensity goal is prioritized over the energy consumption goal. For example, the energy intensity goal includes double subgoals. One is the fundamental goal, that is, the minimum requirement of reaching the target, and the other is the incentive goal encouraging local authorities to achieve more. The total energy consumption can be exempted from evaluation if the incentive goal is reached. In order to enhance the flexibility of the DCS implementation, exemptions have also been extended to major projects approved by the State Council and to provinces that have exceedingly met their RPS caps. Such flexible arrangements promote renewable energy use and help balance economic growth and energy conservation. Given the fact that carbon emissions are still rising to a peak, the system considers the flexibility in target setting and evaluation, and the relationship among economic structures, energy consumption, and energy intensity.120,121

The above-mentioned mandatory policy instrument also pertains to China's energy target responsibility system (TRS). It has been popularly applied to issues of energy, environment, and climate change in China, over the past decade, alongside target decomposition and performance evaluation.122,123 However, the deep-rooted TRS problems, such as rationality of target-setting, reasonability of target disaggregation, and reliability of local statistics cannot be resolved easily.122,124–126

Dual control barometer

During the 13th FYP, in conjunction with DCS, a DCB was introduced by the NDRC to score and analyze the conditions of total energy consumption and energy intensity reduction. The barometer report is usually published per quarter, in order to categorize the performance of each province using three-color-level early warnings, namely, the first level in red (a serious situation), the second level in orange (a relatively serious situation), and third-level in green (a smooth situation in general). As DCS is bound up with local officials’ performance evaluation and even their political fortunes,127,128 DCB is an important indicator for evaluating the work of local authorities under DCS.

However, extreme responses, such as power rationing, occur occasionally when local governments are under stress from the DCB. 125 In the context of Goal 3060, China has been increasingly tightening the supervision of “dual high” projects, which involve both high energy consumption and high carbon emissions, such as petrochemicals, steel, and non-ferrous metals. In August 2021, the NDRC published a scorecard for 30 provinces for the first half of the year. With regard to energy intensity reduction, red cards were given to nine provinces and orange cards to 10. As for total energy consumption, eight provinces got red warnings and five provinces orange warnings.

Central environmental inspection

CEI is an administrative monitoring mechanism in environmental governance, which was initiated in 2016. 129 It consists of an interdepartmental team of senior officials, led by a (deputy-)ministerial-level leader, for the purpose of inspecting local environmental policy implementation and environmental protection performance.130,131 At the time of writing, there have been two rounds of inspection, covering all provinces. In the second-round fourth-batch inspection alone, 1035 cadres from eight provinces were held accountable for ecological and environmental issues. 132 Given the fact that the 3060 Goal enhances the focus on climate governance, in 2021, five inspected regions were criticized for their failure in controlling energy consumption and emissions. 133 While CEI is a useful tool in ensuring the implementation of energy policies and regulations, it has limitations because of its periodic nature, accountability issues, public participation deficiency, and burdens for disadvantaged groups.129–131

Conclusions

The year 2020 constitutes a dividing line in China's climate and energy governance, because of Goal 3060. The extant literature tends to take separate sectors as the unit of analysis.134,135 In contrast, we developed a systematic cross-sectoral perspective on China's renewable energy and energy efficiency policies. The comprehensiveness and timely nature of this review can help guide scholars interested in China's low-carbon energy transition.

One key finding is that the Chinese government typically adopts a command-and-control approach and relies on administrative power in energy and climate governance. 136 Goals and regulations are rigidly imposed by the superior government and implemented by local governments, businesses, and social organizations. While this approach can address climate challenges, it tends to result in campaign-style enforcement for local authorities, 129 resulting in high compliance costs and low resource allocation efficiency for enterprises. 136 Market-based instruments can incentivize a cost-effective reduction in carbon emissions. While there is a shift to market-based policy instruments in China, the full potential of market forces remains to be unleashed. Although electricity and carbon markets are featured in China's energy policy, the development has been slow and the government exerts strong control over the markets.1,20 Therefore, market reforms need to center on modifying governance structures and on combinations of electricity and carbon markets.137,138 Furthermore, a long-term, networked, and inclusive policy environment needs to be developed. Alongside top-level design, the long-lasting and networked nature of policymaking can attract long-term investment and inclusive cooperation.

The second conclusion is that the harmonization of policies plays a key role in steering climate governance. Currently, fragmentation characterizes China's low-carbon policies. On the one hand, dramatic renewable electricity generation has led to serious curtailment problems, which have not been completely addressed. On the other hand, Goal 3060 motivates renewable energy development. Furthermore, there is a conflict between climate and economic objectives. While the central government incentivizes local officials to develop solutions to climate challenges, it also wants strong economic performance. 139 These issues of contradiction and fragmentation need to be addressed.

Third, the development of the new low-carbon policy has been uneven across different sectors. While renewable electricity and industrial sectors have received maximum attention, carbon emission reduction in the building and transportation sectors needs more attention. 97 This is important because, as China is transitioning to a high-tech, service-based, and consumption-focused economy, 140 carbon emissions from the building and transportation sectors will become much more significant.141,142

Fourth, the power of surveillance technologies as a policy instrument needs to be better harnessed. The rapid development of surveillance technologies, such as remote sensing and GPS tracking, has provided unprecedented surveillance power. 143 Furthermore, artificial intelligence technologies and big data analysis have substantially enhanced surveillance capacity by automating the monitoring process. In China, poor implementation and compliance are common issues in climate governance. 144 Surveillance technologies can contribute to the enforcement of climate policies by generating real-time compliance data.

Fifth, as China moves toward carbon neutrality, the issue of just transition becomes more salient. Just transition draws attention to the equity and justice issues associated with energy and climate policies and is increasingly recognized internationally as a crucial component of low-carbon transitions. 145 Policymakers must implement policy to reduce the negative socioeconomic impacts on fossil fuels-based communities and workers. 146

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the General Research Fund (12600718) of the Research Grants Council of Hong Kong.