Abstract

Taking new energy vehicle (NEV) listed enterprises from 2010 to 2018 as a research sample, this paper empirically analyzes the innovative impact of VC on NEV enterprises by applying the difference-in-difference (DID) model. The results indicate that the intervention of VC has a positive and significant impact on the green technological innovation in NEV enterprises, an impact which is reflected in a significant increase in the number of green invention and green utility model patent applications. Compared with state-owned NEV enterprises, VC plays a more significant role in promoting the green technological innovation of private and foreign NEV enterprises. In the NEV industry chain, VC has significantly promoted green technological innovation of upstream and midstream NEV enterprises. From the perspective of VC, it also finds that, compared with independent and local VC, it is the syndicated and non-local VC that have a more positive and significant impact on green technological innovation in the NEV enterprises. Besides, the high-reputation of VC has not had an “incubating” effect on green technological innovation in NEV enterprises.

Introduction

As China's economy is at a crucial stage of transition from high-speed growth to high-quality growth, it is urgent to continuously improve the quality of economic growth through technological innovation. The NEV industry, as representative of strategic emerging industries in China, is not only the most important driving source of green innovation, but also one of the key industries to adress climate change and build an environment-friendly society.1,2 It has therefore been strongly supported by the government. Since 2010, A array of policies has beeen implemented driven on both the supply and demand sides, such as fiscal subsidies, tax exemptions, government procurement, right-to-way control and so on, to stimulate rapid development of the NEV industry.3,4 By 2015, the sales volume of total NEVs in China had surpassed that of the United States and is now ranked first in the world. However, under the abundant government subsidies, the problem of insufficient green technological innovation capacity of China's NEVs has become increasingly prominent, especially in some core key technologies such as drive motors and plug-in hybrid systems. With the frequent exposure of subsidies defrauded and embezzled by NEV enterprises, NEV industry subsidy policies have been adjusted correspondingly. In 2015, Tressury Department, the Ministry of In dustry and Information Technology, the Ministry of Science and Technology and the National Development and Reform Commission jointly announced the “Notice of Financial Support Policies for the Promotion of NEVs in 2016–2020”, clearly stipulating that from 2017 the central government would gradually reduce subsidies for NEVs. In 2019, the “Notice on Further Improving the Financial Support Policy for the Promotion and Application of NEVs” also made it clear that local government will no longer subsidize the purchase of NEVs. Therefore, under the pressure of withdrawal of fiscal subsidies by the central government and cancellation of purchase subsidies by local government, NEV enterprises are today faced with cash flow shortage difficulties. They are urgently in need of both an introduction of funds from the capital markets to ease their financing constraints and a need to invest more on green technological innovation to promote green and sustainable development.

VC, as a kind of market-oriented means, can not only bring cash flow to the invested enterprises, but can promote the innovation in the high-tech industry by virtue of its mature investment experience and a series of value-added innovation services.5,6 In the early 1990s, about ninety percent of the total invention and innovation of high technology enterprises benefited from VC, which made it the engine of America's economic growth. However, the VC industry in China started late and developed slowly. It was not until the government issued the 2012"Notice on Further Encouraging and Guiding Private Capital to Enter the Field of Technological Innovation” that the domestic VC industry started to develop rapidly. According to the Zero2IPO Database, as of the first half of 2019, China's VC management fund has exceeded 10 trillion yuan, and NEV industry has always been a key investment area for VC, about 50% of listed NEV enterprises have acquired the investment of VC. For example, two well-known international VCs, Sequoia Capital and IDG Capital have invested in China's Nio NEV enterprise in 2015 and 2017 respectively.

In the beginning, VC research mainly looked at the influence of VC on IPO market performance and corporate performance of invested enterprises. Western developed countries have conducted more research on VC and enterprises innovation, in the latest years, scholars in China have also started to study the innovation effect of VC. However, the innovation incentive effect of VC remains controversial. Some scholars find that VC has few incentive effects on enterprise innovation as expected. Wen and Feng 6 find that VC had an U-shaped influence on innovation of small and medium-sized enterprises from the viewpoint of trade-off between value-added and acquisition. Taking 940 manufacturing and business service sector companies in both the United States and the United Kingdom as research objects, Lahr and Mina 7 find that VC had no significant influence on the innovation by firms, or even had a negative impact on future patent applications. However, most scholars have confirmed the incentive effect of VC on enterprise innovation. Using the data on Chinese A-share listed enterprises, Fu et al.; 8 Chen et al.; 9 Zhang and Zhang 10 ; Gu and Qian 11 find that VC can help enterprises improve enterprises capacity to independently innovate. For China's NEV industry start late, and the definition and data collection of NEV enterprises are complicated, few scholars have empirically examined VC on NEV enterprise innovation.

As the world's second largest economy, China plays an important role in addressing global climate deterioration and energy shortages. Under the background of the subsidy exit policy, investigating the impact of VC on NEV enterprises innovation can not only provide an empirical basis for the Chinese government to effectively use market-oriented means to stimulate innovation in NEV industry, but also provide experiences for other countries to make full use of market-oriented means to promote the sustainable development of NEV industry. Based on previous theories, this paper takes 2010–2018 NEV listed enterprises as samples and uses the DID model to explore the relationship between VC and green technological innovation of NEV enterprises. In addition, the ownership of enterprises and industry chain position has also been taken into consideration.

Theoretical analysis and research hypothesis

VC and green technological innovation of NEV enterprises

Since the post-subsidy era, NEV enterprises urgently need to introduce market capital to ease financing constraints, accelerate the process of green innovation and achieve technological breakthroughs. VC, as a capitalized financing method, aims to effectively link capital and technology, inject social capital into high-tech industries, and realize technological innovation of enterprises.

12

On the one hand, VC can provide financial support for NEV enterprises and reduce the negative impact of high investment of green technological innovation in the routine operation of enterprises.13,14 At the same time, it can also provide positive quality signals to external investors and commercial banks to minimize the problems of highly asymmetric information, and ease the financial restriction of NEV enterprises innovation.15,16 On the other hand, VC institutions will participate in NEV enterprises internal management. With a wealth of investment experiences, Venture capitalists are more willing to seek professional R&D personnel and sales teams for NEV enterprises and provide a series of other value-added services to stimulate green technological innovation in NEV enterprises.9,17 NEV is a key industry to cope with golbal environmental pollution and accelerate the green transformation of traditional vehicles, the intervention of VC may enhance the green technological innovation of NEV enterprises.

18

Therefore, the following hypothesis is proposed:

H1:VC can significantly promote green technological innovation of NEV enterprises.

VC, ownership and green technological innovation of NEV enterprises

According to the ownership attribute, NEV enterprises can be divided into state-owned NEV enterprises, private NEV enterprises and foreign-funded NEV enterprises. NEV enterprises with different ownership possess different innovative resource endowment and managers have different views on innovation activities. Both will influence the incentive effects of VC on NEVs green technological innovation. State-owned NEV enterprises tend to have political superiority, possess more innovation resources and excellent R&D teams. However, due to the incentives of principal-agent and performance appraisal system, managers of state-owned NEV enterprises are more inclined to invest in projects with low risks and short-term returns.

19

Green technological innovation activities of NEV enterprises are characterized by high risk, long cycle and great uncertainties.

20

State-owned NEV managers may be less enthusiastic about green technological innovation activities and even create a crowding-out effect on VC. Private NEV enterprises have a small market share and a shortage of talent reserves, and there is “credit discrimination” in borrowing from commercial banks. However, the structure of private NEV enterprises is simple and more flexible, and the supervision and incentive system is relatively perfect. The managers are more willing to enhance the market competitiveness of enterprises through technological innovation.

21

The intervention of VC on one hand can alleviate enterprises innovation financing constraints, on the other hand can release ‘positive signals’, which will help NEV enterprises attract more excellent talents and expand the R&D team.

22

At the same time, venture capitalists can participate in the formulation of innovation programmes with their mature management experiences to ensure the orderly implementation of green technological innovation activities.

23

After the liberalization of the joint venture share ratio policy, foreign-funded NEV enterprises have entered China's NEV market on a large scale, which has intensified the competition in the domestic market. Foreign-funded NEV enterprises mainly achieve enterprises innovation through talent mobilization and technology transfer. In order to gain competitive advantage in the host market, they are more adept at using local financial resources. The intervention of VC can help foreign-funded NEV enterprises to familiarize themselves with the local market environment, broaden the interpersonal network, and thus providing good conditions for enterprises to carry out innovative activities.

24

To sum up, the following hypothesis is proposed:

H2: Compared with state-owned NEV enterprises, VC plays a more significant role in promoting green technological innovation of private and foreign-funded NEV enterprises.

VC, industry chain and green technological innovation of NEV enterprises

Green technological innovation requires resource integration and coordinated cooperation among enterprises in the industry chain. Relying on policy dividends, China's NEVs have formed a complete “up-middle-downstream” industry chain. The main business of upstream NEV enterprises are lithium ore, electrolyte, positive and negative materials and diaphragms; the midstream NEV enterprises are mainly engaged in “three electricity” (batteries, motors and electric control) and circuit systems; and downstream NEV enterprises are new energy passenger vehicles. Among them, upstream core cathode materials high nickel ternary has high technical requirements and still relies on foreign imports. Midstream “three-power system” as the core component of the NEVs, accounts for 50% of the manufacturing cost of the vehicle, but there is a gap with the world's advanced level in terms of technological breakthroughs. Therefore, NEV enterprises in the upper and mid-stream of the industry chain have a huge demand for green technological innovation. Compared with downstream NEV enterprises with better financing status, upper and mid-stream enterprises have serious innovation financing constraints due to information height asymmetrical with external investors.

25

Under the influence of subsidy exit policy, downstream vehicle enterprises prefer to increase vehicle prices to transfer costs to consumers or negotiate with upstream suppliers to increase profits. The weak bargaining power of the upper and mid-stream enterprises has made it reduce the expected revenue and exacerbated NEV enterprises innovation financing. The intervention of VC can bridge the innovation funding gap of upper and mid-stream NEV enterprises, and provide enterprises with heterogeneous innovation resources to accelerate the green technological innovation process of upper and mid-stream NEV enterprises, while the downstream enterprises are more willing to use VC to expand the scale and achieve scale benefits. To sum up, the following hypothesis is proposed:

H3: Compared with downstream NEV enterprises, VC plays a more significant role in promoting green technological innovation of NEV enterprises in the upper and mid-streams.

VC Heterogeneity and green technological innovation of NEV enterprises

VC institutions may differ in their approach to green technological innovation by NEV enterprises. This paper focuses on innovative research in three areas; syndicated venture investment, VC reputation, and local investment. First, Compared with independent VC, syndication of VC enables a connection between VC institutions to realize resource sharing and provide invested NEV enterprises with more capital flows and complementary management experience.26–28 Moreover, syndication of VC releases quality signals through complex network connection, reduces information asymmetry between NEV enterprises and external capital markets,29,30 and thereby providing financial support for green technological innovation by NEV enterprises. Liu et al.

31

finds that syndication of VC is conducive to enterprise innovation performance. Second, reputation of VC. Compared with low-reputation VC, high-reputation VC can raise larger amounts of capital, increase the listing probability of invested enterprises and enable invested enterprises to show strong growth potential.

32

In addition, high-reputation venture capitalist often have rich investment experience and mature relationship networks in the NEV industry, which can facilitate green technological innovation of NEV enterprises. Nahata 32 find that the high-reputation VC significantly promotes invested enterprises innovation performance. Third, local investment. Most VC institutions in China are located in prosperous cities like Beijing and Shanghai; the distribution of VC is unbalanced. From the perspective of geographical proximity, in order to reduce agency and communication transaction costs, VC institutions prefer to select local NV firms.33,34 Local investment has information superiority. It can both reduce information asymmetry between VC institutions and NEV enterprises and facilitate the management and supervision of NEV enterprise green technological innovation activities by VC institutions.35,36 Dong et al.

37

find that local investment of VC institutions can promote the innovation in local high-tech firms. Based on the above analysis, this paper puts forward the following hypothesis:

H4a. Compared with independent VC, the syndication of VC is more conducive to green technological innovation of NEV enterprises. H4b. Compared with low-reputation VC, high-reputation VC is more conducive to green technological innovation of NEV enterprises. H4c. Compared with non-local VC, the local investment of VC is more conducive to green technological innovation of NEV enterprises.

Research design

Model settings

Considering that VC may prefer to invest in enterprises with strong innovation capacities, NEV enterprises with or without VC may already have innovation differences before VC intervention. And, NEV enterprises innovation may also exist differences before and after VC intervention. These may cause sample selection errors and endogenous problems. DID method not only can exclude whether there are differences in green technological innovation of NEV enterprises before VC intervention, but also can exclude the influence of external environment and time factors on research conclusions during VC intervention. Therefore, we apply the DID method to investigate the impact of VC on the innovation of NEV enterprises. Due to the different years of VC entering NEV enterprises, the following model is set up with reference to Chen et al.

9

:

To explore the influence of VC heterogeneity on the green technological innovation of NEV enterprises, the dummy variable of VC is divided by referring to Wu et al.

27

and Sun et al. (2018). Among them, Model (2) is constructed by splitting the VC dummy variable into syndicated VC dummy variable (SVC) and independent VC dummy variable (NSVC); Model (3) is constructed by splitting the VC dummy variable into high-reputation VC dummy variable (HRVC) and low-reputation VC dummy variable (NHRVC); Model (4) is constructed similarly for localized VC (LOVC) and non-localized VC (NLOVC) dummy variables. The specific model settings are as follows:

Variables

Independent variable: VC × Post Among “VC × Post”, “VC” is a dummy variable and distinguishes between the experimental group and the control group. When NEV enterprises have VC intervention VC = 1, otherwise it is 0. “Post” is the dummy variable of time. During the period of VC intervention, Post = 1, otherwise it is 0. At the same time, syndicated VC (SVC), independent VC (NSVC), high-reputation VC (HRVC), low-reputation VC (LRVC), local VC (LVC) and non-local VC (NLVC) are also expressed as dummy variables.

Dependent variable: green technological innovation. Green technological innovation is to deal with green issues, and is an important means to enhance the core competitiveness of NEVs. 38 Due to the long period from the application of enterprise patent to the final authorization, there is a certain lag and uncertainty. Therefore, we ultimately select the number of green invention patent applications (Lngreen1) and the number of green utility model patent applications (Lngreen2) as the indicators of green technological innovation.

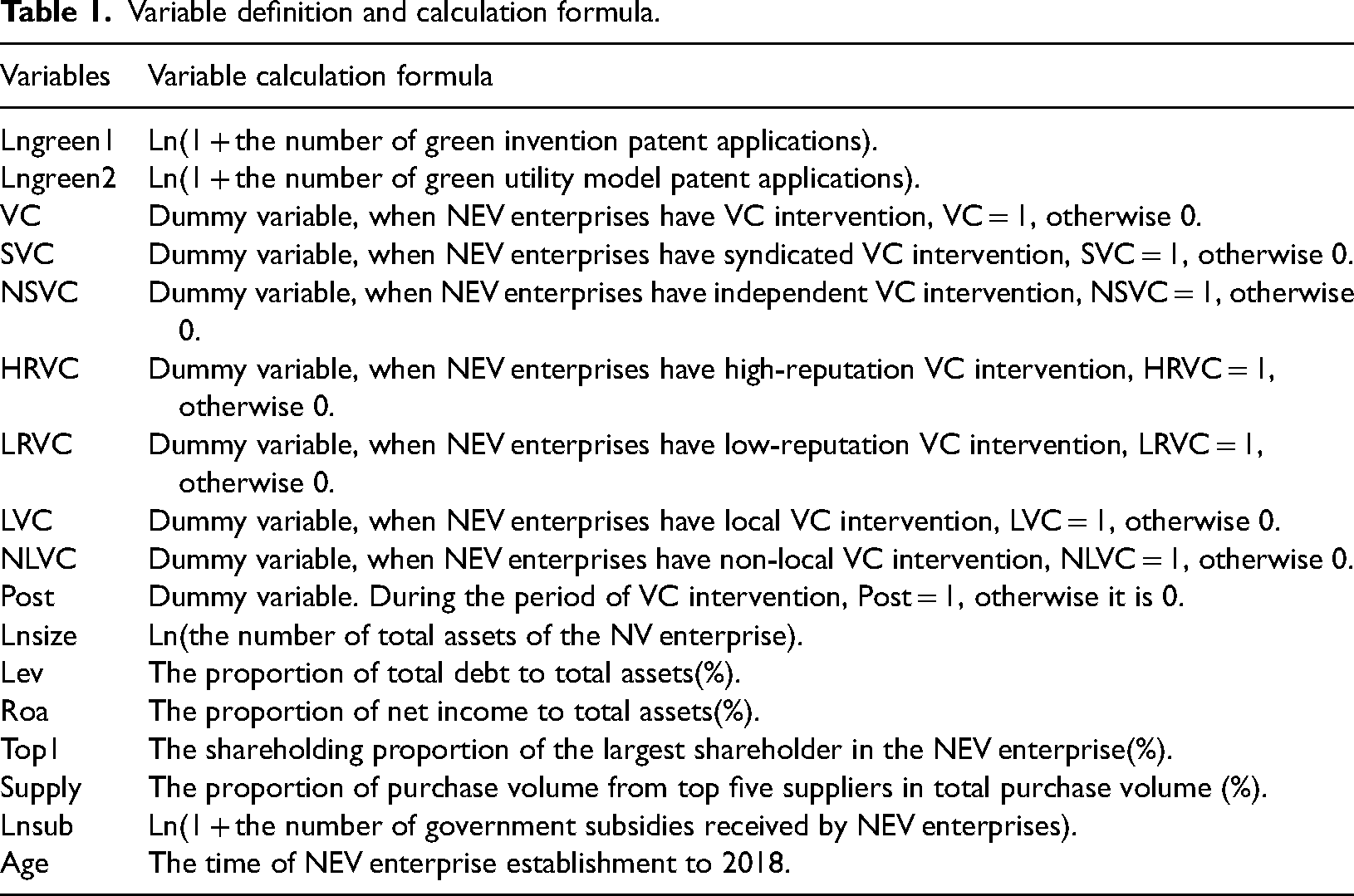

Control variables: Considering that the incentive effects of VC on NEVs green technological innovation may also be affected by other factors, referring to the literature of Chen et al.; 9 Wen and Feng 6 and other scholars, this paper sets the following control variables: Enterprise size (Size), expressed by the logarithm of the total assets of the NV enterprise. Asset-liability ratio (Lev), represented as the proportion of total debt to total assets. Net profit margin (Roa), represented by the proportion of net income to total assets. Supplier concentration (supply), represented by the proportion of procurement volume of the top five suppliers of the total annual procurement volume. 39 Government subsidy (Sub) is expressed as the logarithm of the amount of government subsidies received by enterprises plus 1. Equity concentration (Top1), expressed as the shareholding proportion of the largest shareholder in the NEV enterprise. Enterprise age (Age), expressed by the time of NEV enterprise establishment to 2018. The variable definition and calculation formula are shown in Table 1.

Variable definition and calculation formula.

Sample selection and data sources

In 2018, the implementation of the “Passenger Cars CAFC and NEV Credit Regulation”(Dual-credit policy) has to some extent changed the original financing channels of NEV industry. NEV enterprises are capable of achieving excess revenues from trading credits, which may alleviate corporate financing constraints and thus affecting the innovation incentive effect of VC. Meanwhile, the new coronavirus epidemic since 2019 has had a serious impact on the industry chain, product sales and patent applications of NEV enterprises. 40 Therefore, to accurately discuss the influence of VC on green technological innovation in China's NEV industry, this paper selects the listed NEV enterprises from 2010 to 2018 as the research samples. In terms of data sources, the CVSource database and Zero2IPO Database released detailed information on VC institutions transactions with NEV enterprises. The screening of listed NEV enterprises is mainly through the “New Energy Car Concept” at www.0033.com, which details the ownership attribute, main business and product types of each NEV enterprise, making it easy to distinguish the state-owned NEV enterprises, private NEV enterprises and foreign-funded NEV enterprises, and also classify the upper, middle and downstream of the NEV industry chain in which the enterprise is located. By excluding the “* ST and ST” enterprises and the enterprises with serious data missing, we finally obtained a sample of 250 listed NEV enterprises. The green patent data of enterprises are obtained from the CNRDS database, which provides the number of green invention patents and green utility model patents applied and granted by NEV enterprises respectively, we confirmed the amount of green patents by proofreading with the patent data published by the State intellectual property Office. A series of financial indicators such as government subsidies, total assets and profit margins are derived from CSMAR database (2010–2018).

Empirical analysis

Descriptive analysis

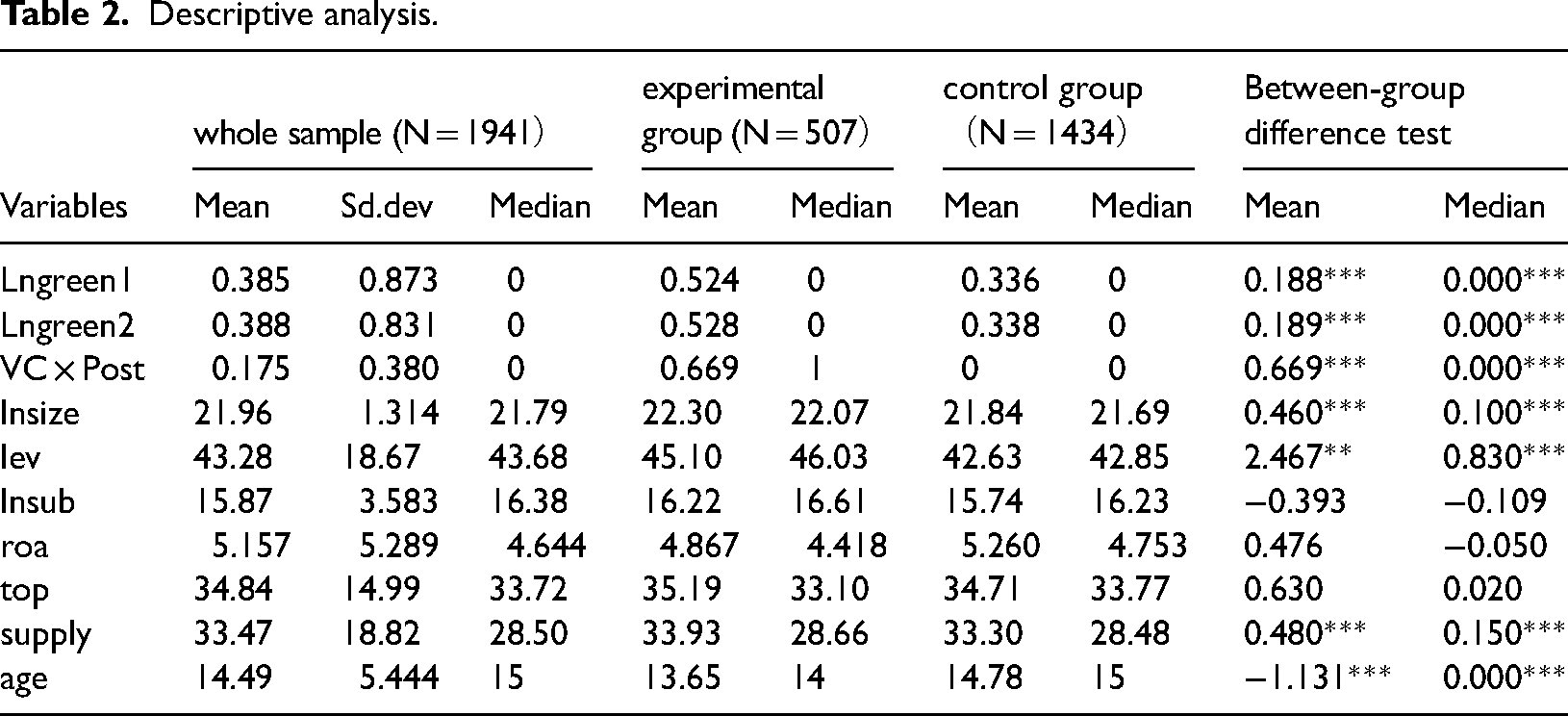

Table 2 is the descriptive analysis of the whole sample and samples of the experimental group and control group with or without the intervention of VC. In the whole sample, the median of Lngreen1 and Lngreen2 are both 0, indicating that at least half of NEV enterprises have no green patent applications in different years, and the standard deviations are 0.873 and 0.831 respectively, reflecting that there is a great difference in green technological innovation between NEVs. From the sample size of the experimental group, it can be obtained that NEV enterprises with VC intervention have exceeded one quarter of the total sample. In the between-group difference test, it is also found that NEV enterprises with VC have larger scale and shorter established time than those without VC. In terms of green patents, NEV enterprises with VC are more capable of green technological innovation.

Descriptive analysis.

Results of the impact VC on green technological innovation of NEV enterprises

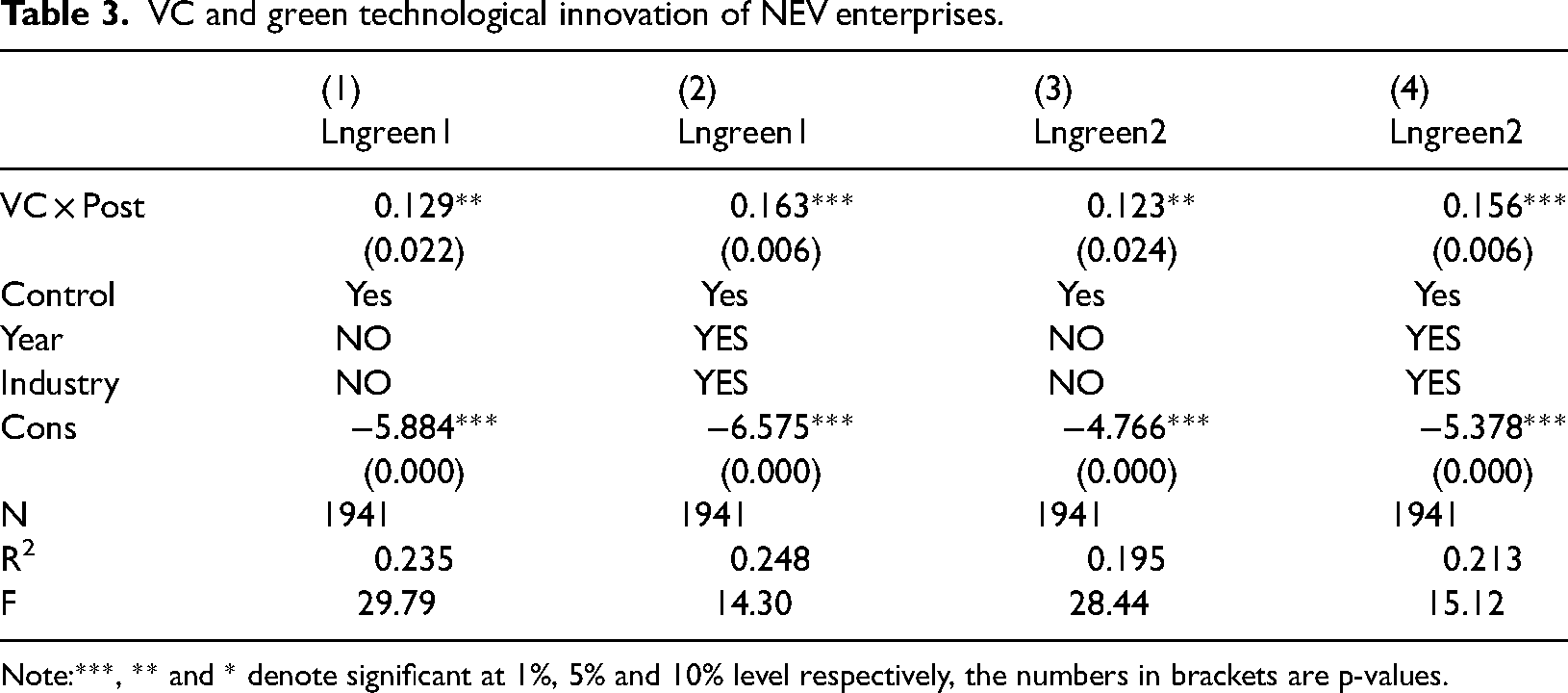

Table 3 shows the OLS regression results of VC on green technological innovation of NEV enterprises. In column (1) and column (3), the coefficients of VC are significantly positive (0.129 and 0.123) at the 5% level. In column (2) and column (4), the influences of year and industry effect on enterprise innovation are controlled, the coefficients of VC are significantly positive (0.163 and 0.156) at the 1% level. When there is VC intervention, the number of green invention patent applications and green utility model patent applications of NEV enterprises will increase by 16.3% and 15.6% respectively, indicating that VC is beneficial to green technological innovation of NEV enterprises, and Hypothesis 1 is true. This is consistent with the conclusions of Qi et al. 41 and Dong et al. 42 Using a sample of environment-friendly enterprises, Dong et al. 42 confirm that the intervention of VC can significantly improve the quantity and quality of enterprises innovation. Taking Chinese listed NE enterprises as a sample, Qi et al. 41 explore the mechanism of VC on enterprise innovation, and conclude that VC can stimulate NE enterprises innovation by providing capital and implementing shareholder incentives. Our findings firstly confirm the incentive role of VC in the innovation of NEV enterprises, which can provide an empirical basis for the government to effectively combine market-oriented means and administrative means to promote the sustainable development of NEV industry.

VC and green technological innovation of NEV enterprises.

Note:***, ** and * denote significant at 1%, 5% and 10% level respectively, the numbers in brackets are p-values.

Robustness checks

DID Estimation

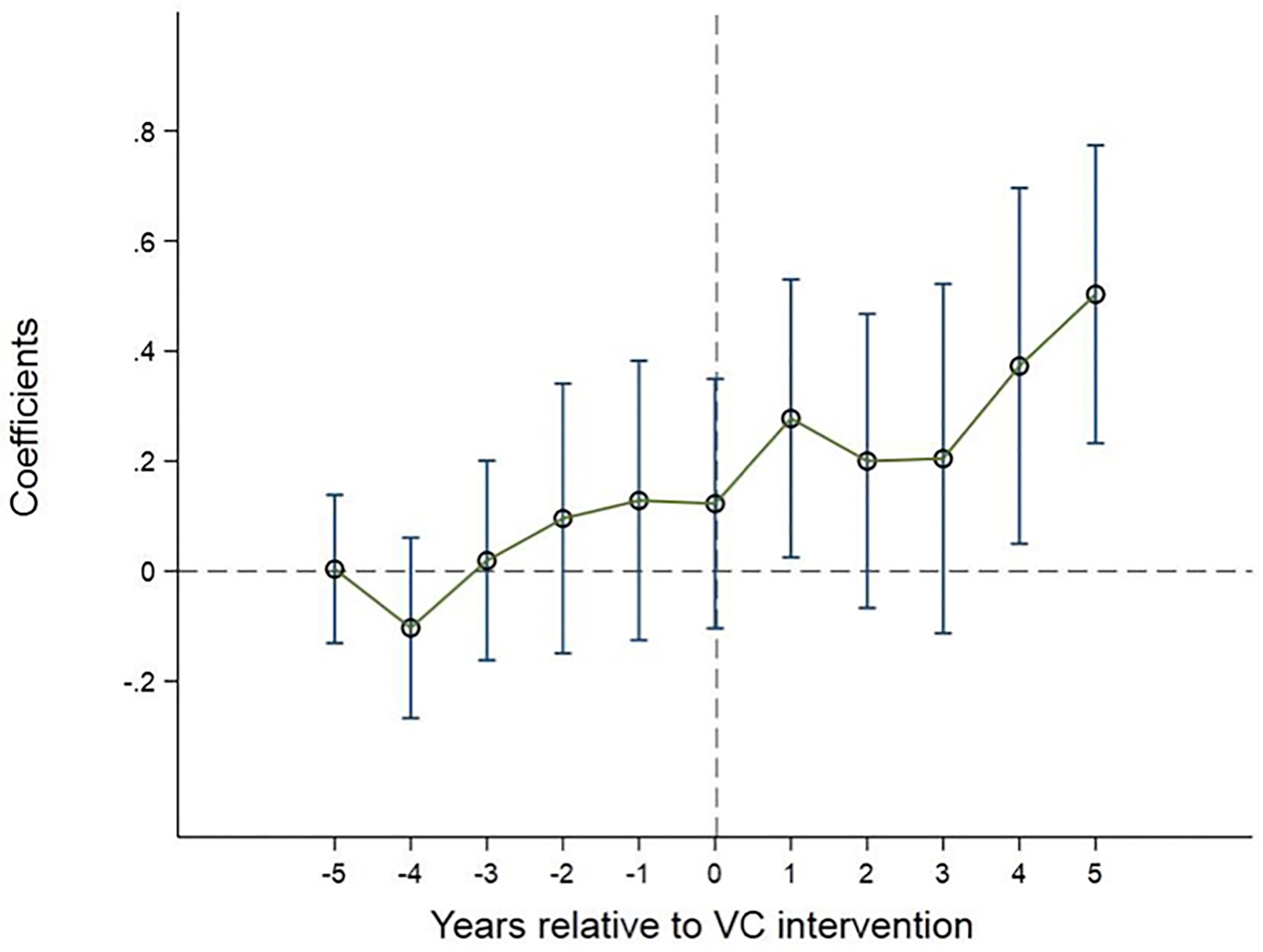

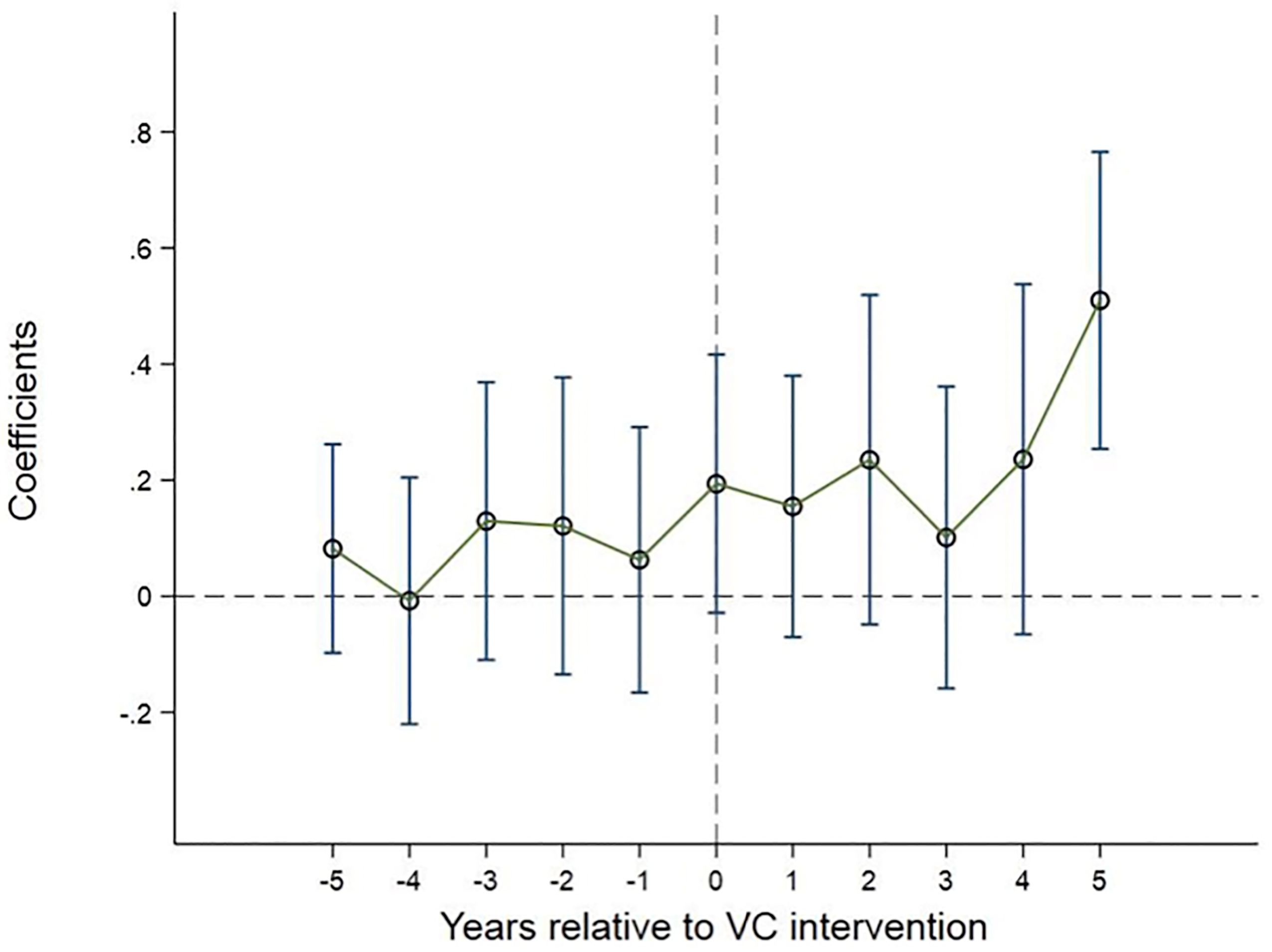

An important prerequisite for the use of the DID model is to satisfy the equilibrium hypothesis, that is, the experimental group and the control group have the same characteristics and development trend line before the event occurs. Figures 1 and 2 are the parallel trends of green invention patents and green utility model patents by NEV enterprises. From the figures, we can see that the coefficients are not significant and the coefficient values fluctuate around 0. This indicates that there is no significant difference in the development tendency of green technological innovation between the experimental group and the control group before VC intervention, which satisfies the equilibrium hypothesis.

PSM Estimation

Parallel trends of green invention patents.

Parallel trends of green utility patents.

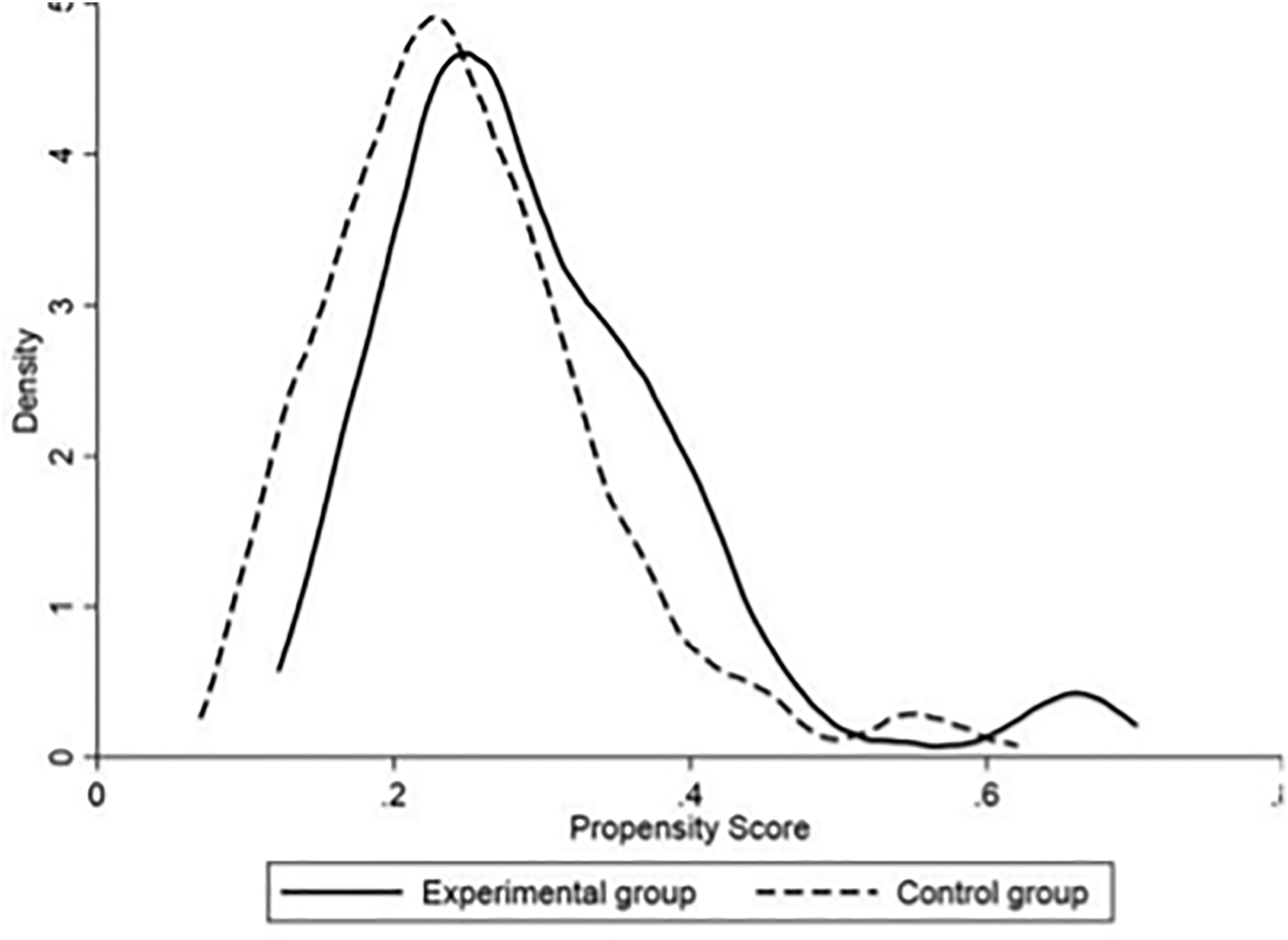

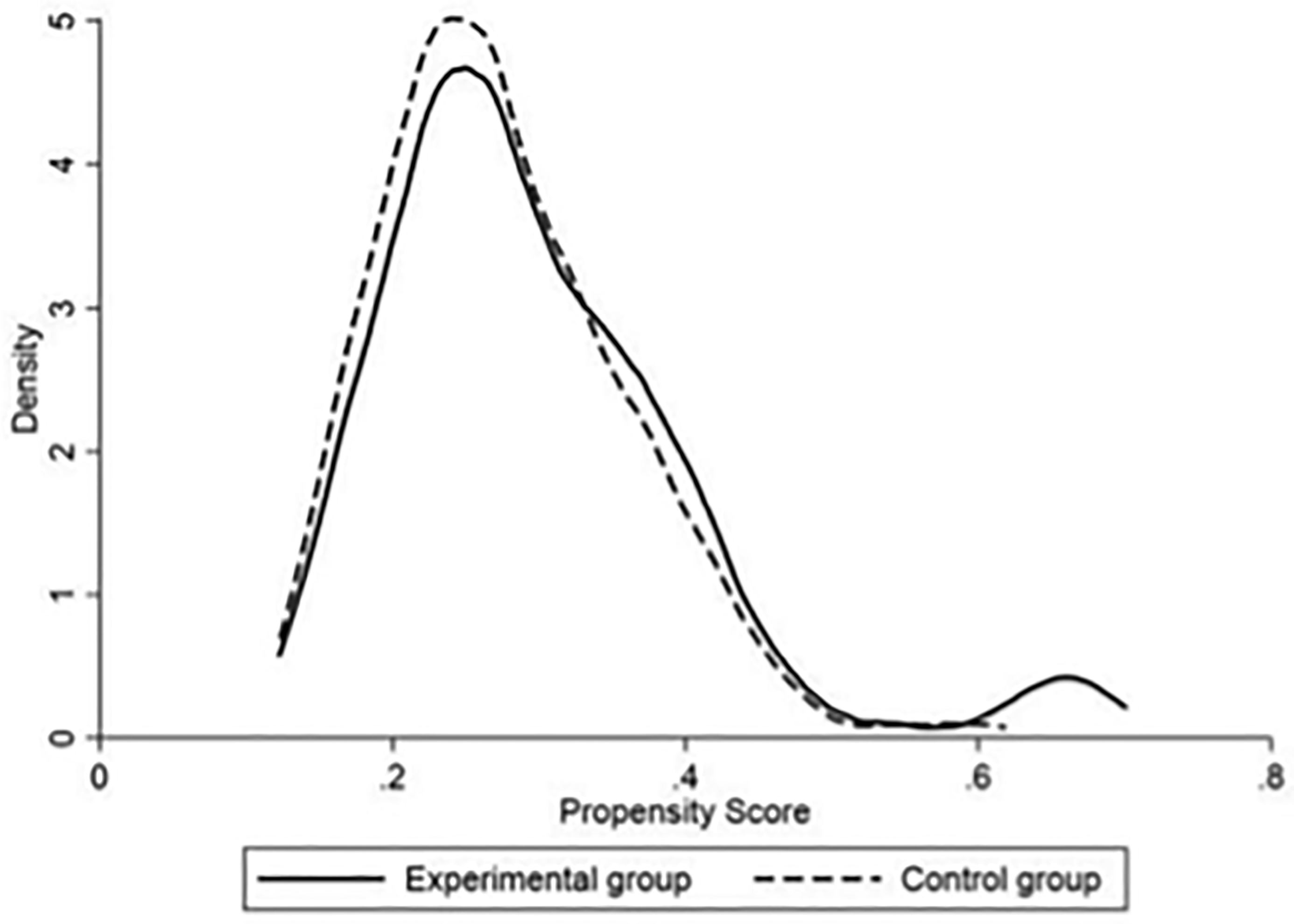

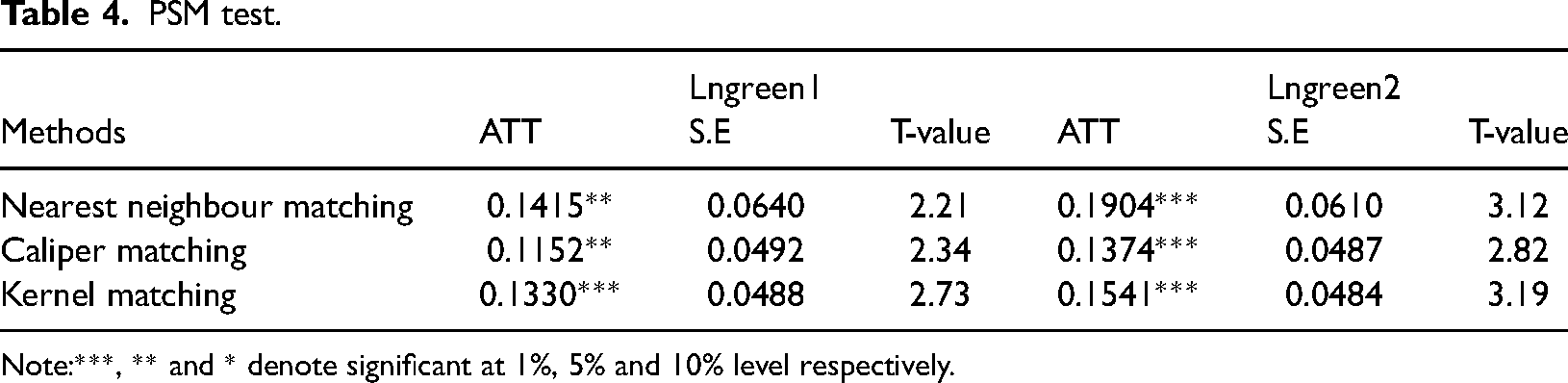

This paper also selects the propensity score matching (PSM) method to deal with sample selection bias, and the matching samples can better meet the preconditions of the DID model. In our paper, matching is performed sequentially using three methods: nearest neighbour matching, caliper matching, and kernel matching. Figures 3 and 4 show the P-score density function graph under one-to-one nearest neighbour matching. It can be seen from Figures 3 and 4 that the variable characteristics of the two groups are relatively close after matching, which indicate that the matching effect is ideal. Table 4 shows the PSM test results. Under the three matching methods, the ATT values of the average treatment effect are all positive and significant at the 5% level. After eliminating the unmatched samples, the DID method is utilized to re-regress. In Table 5, columns (8)-(9) show the innovative impact of VC on NEV enterprises by applying the PSM-DID model. The results are in line with H1, making it clear that VC is conducive to green technological innovation by NEV enterprises.

Other robustness checks

Before matching.

After matching.

PSM test.

Note:***, ** and * denote significant at 1%, 5% and 10% level respectively.

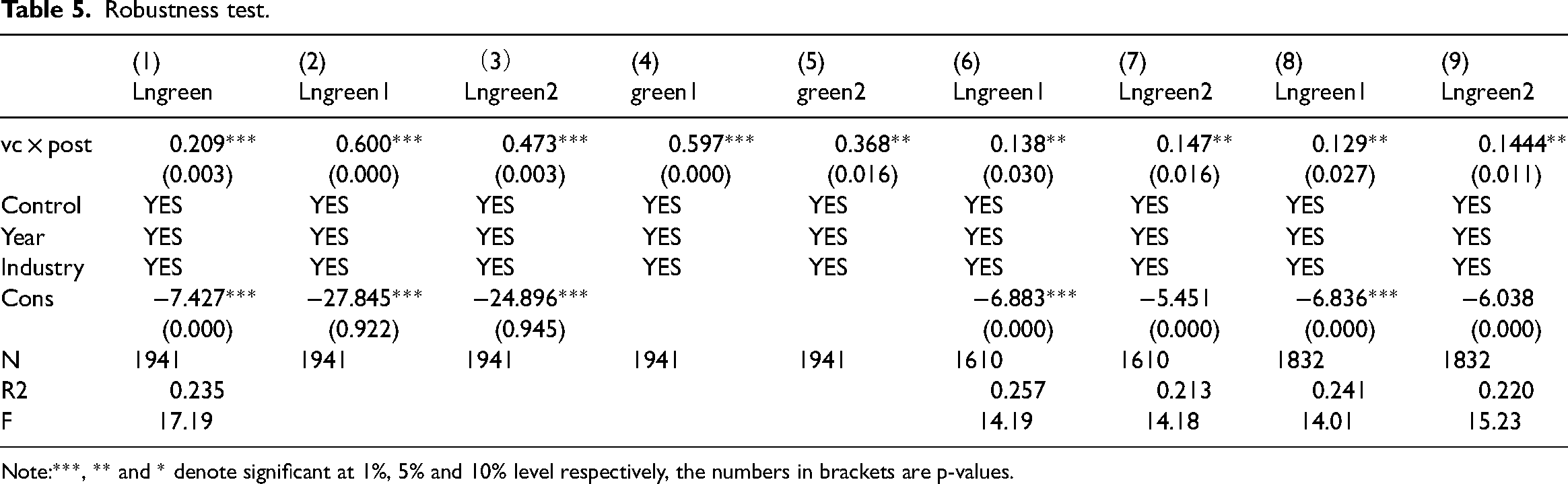

Robustness test.

Note:***, ** and * denote significant at 1%, 5% and 10% level respectively, the numbers in brackets are p-values.

To ensure the robustness of conclusions, Model (1) is further tested by the following robustness tests in Table 5: (1) Replace the independent variable. The total amount of annual green patent application (Lngreen) is used as the proxy variable of green technological innovation. (2) Replace the model. Data of the patent applications are the non-negative censored data, so the Tobit model in columns (2)-(3) and the Negative binomial model in columns (4)-(5) are adopted respectively to re-regress. (3) Since the VC industry developed rapidly until 2012, we exclude the data before 2012 and separately intercept the samples from 2012 to 2018 for empirical research in columns (6)-(7). All results are in line with H1.

Heterogeneity analysis

VC, ownership and green technological innovation of NEV enterprises

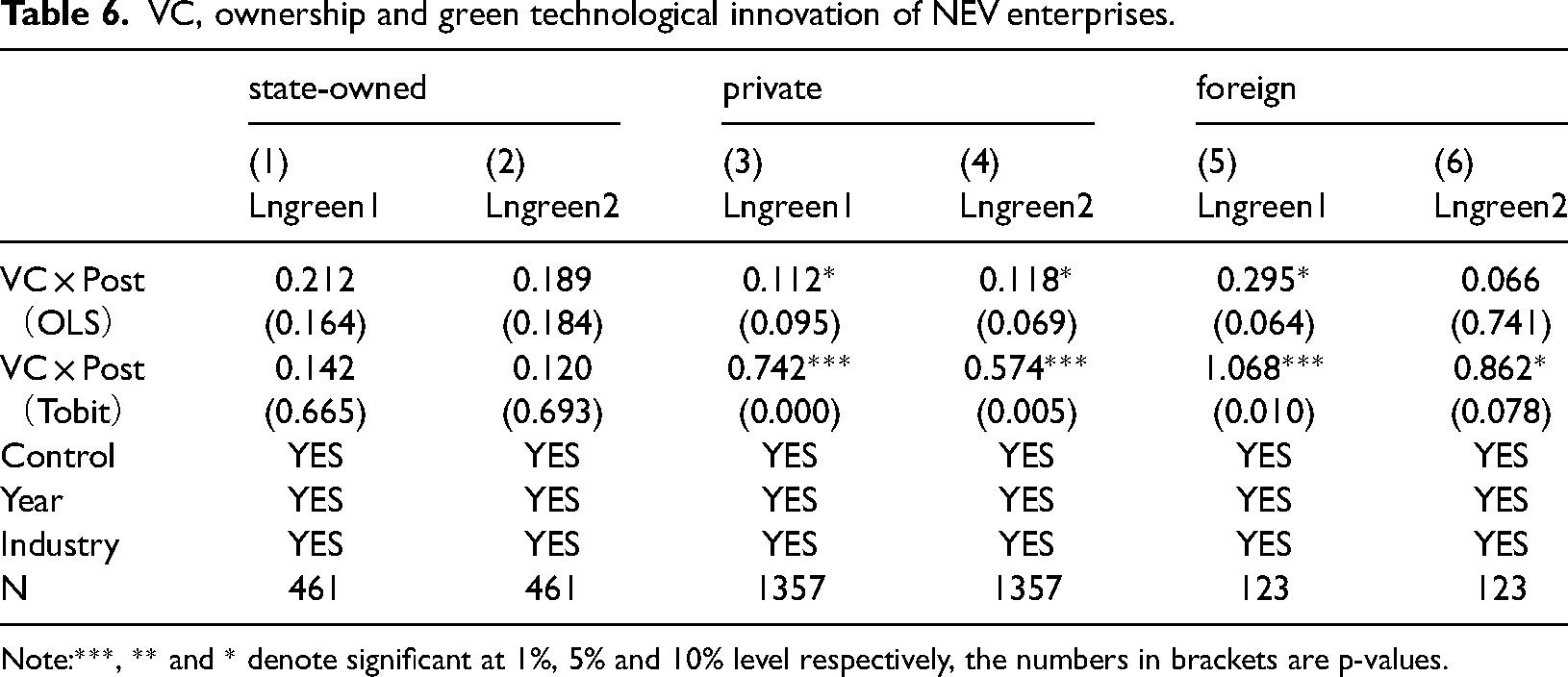

Table 6 shows the regression results of VC on green technological innovation of state-owned, private and foreign NEV enterprises. In columns (1) - (2), the coefficients of VC in state-owned NEV enterprises group are positive, but not significant. In columns (3) - (4), the coefficients of VC in private NEV enterprises group are significantly positive (0.112 and 0.118) at the 10% level. When VC is involved, the two types of green patent applications in private NEV enterprises will increase by 21.2% and 11.8% respectively. In (5)-(6) columns, the coefficient of VC to green utility model patents of foreign NEV enterprises is positive, but not significant; while the coefficient of VC to green invention patents is significantly positive(0.066) at the 10% level. When VC is involved, the number of green invention patent applications by foreign NEV enterprises will increase by 6.6%. To further ensure the robustness of the empirical results, Tobit model is also applied for regression. All results indicate that compared with state-owned NEV enterprises, VC plays a more significant role in promoting green technological innovation of private and foreign NEV enterprises, which is consistent with Hypothesis 2. By applying Tobit and Negative binomial models, Zhuang et al. 43 investigate the relationship between VC and enterprises innovation, and find that compared with state-owned enterprises, non-state-owned enterprises are more willing to introduce VC and cooperate with VC to promote enterprise innovation. Under the background of subsidy exit policy, private NEV enterprises are more likely to use VC to ease financing constraints and achieve green technology breakthroughs. State-owned NEV enterprises have abundant innovation resources and insufficient innovation motivation, so it is difficult for VC to play an “incubation” role for State-owned NEV enterprise green technological innovation. Foreign-funded NEV enterprises prefer local VC to get familiar with the market and financial environment, which can create good conditions for foreign-funded NEV enterprise green technological innovation.

VC, ownership and green technological innovation of NEV enterprises.

Note:***, ** and * denote significant at 1%, 5% and 10% level respectively, the numbers in brackets are p-values.

VC, industy chain and green technological innovation of NEV enterprises

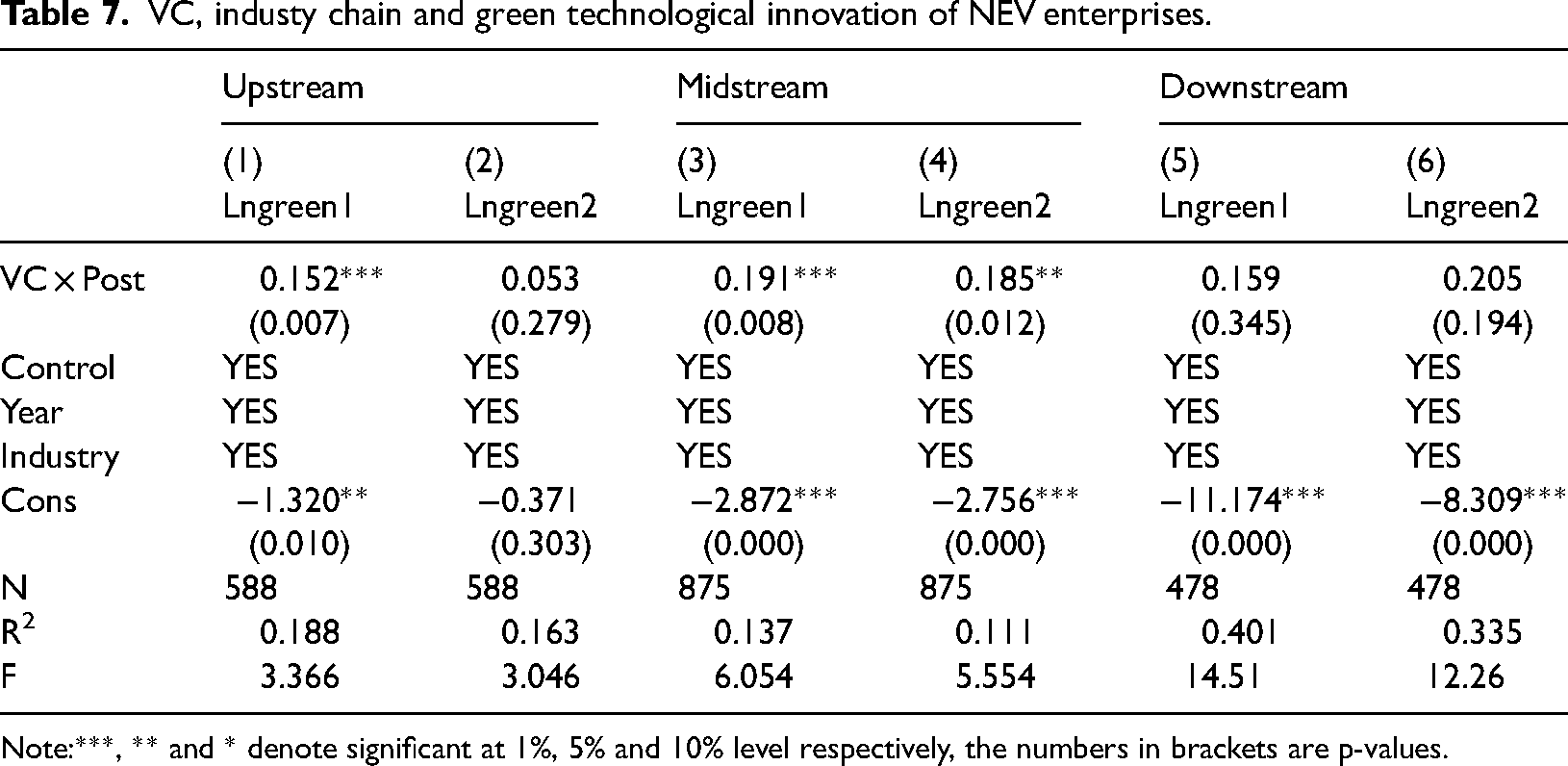

Table 7 shows the regression results of VC on innovation of upstream, midstream and downstream NEV enterprises. As can be seen from columns (1) - (2), the coefficient of VC on green utility model patents of upstream NEV enterprises is positive but not significant, and that on green invention patents is significantly positive (0.152) at the 1% level. When VC is introduced, the number of green invention patent applications of upstream NEV enterprises will increase by 15.2%. In columns (3) - (4), the coefficients of VC in the midstream NEV enterprises group are significantly positive (0.191 and 0.185) at the 5% level. When VC is introduced, the two types of green patent applications of midstream NEV enterprises will increase by 19.1% and 18.5% respectively. In columns (5) - (6), coefficients of VC on downstream NEV enterprises are positive but not significant. The results show that compared with downstream NEV enterprises, VC plays a more significant role in promoting green technological innovation of NEV enterprises in the upper and mid-streams, which is consistent with Hypothesis3. Taking the listed NEV enterprises from 2015–2018 as a sample, Chi et al. 25 examined the impact of government subsidies and market financing on enterprise innovation, and find that the interaction between government subsidies and market financing plays a more significant role in the innovation of upstream and midstream NEV enterprises. The possible reason for our conclusion maybe thathe upstream and midstream NEV enterprises in the industry chain lack of core technologies and thus have a huge demand for green technological innovation. However, compared with the downstream NEV enterprises with good financing conditions, the financing constraints of the upper and midstream NEV enterprises are serious. On the one hand, the intervention of VC alleviates the financing constraints of NEV enterprises; on the other hand, it provides innovative heterogeneous resources for the upper and midstream NEV enterprises of the industry chain by virtue of rich relationship networks.

VC, industy chain and green technological innovation of NEV enterprises.

Note:***, ** and * denote significant at 1%, 5% and 10% level respectively, the numbers in brackets are p-values.

VC heterogeneity and green technological innovation of NEV enterprises

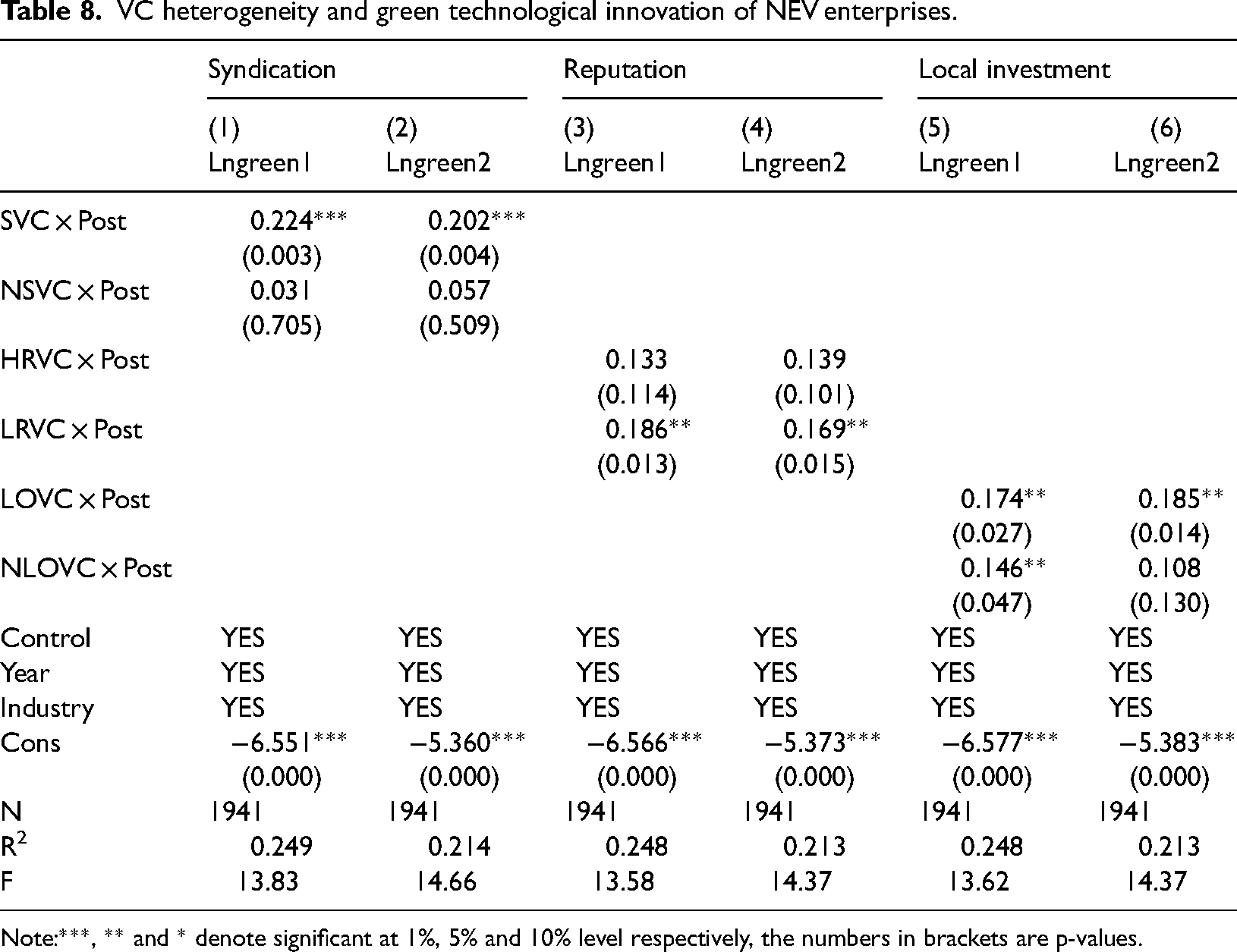

Table 8 shows the impact of the three different heterogeneous VC on green technological innovation by NEV enterprises. (1) Syndicated venture investment. If there are two or more VC institutions jointing in NEV enterprises at the same time during the study period, it will be considered as syndicated venture investment. In columns (1) - (2),The results show that the coefficients of the syndicated venture investment are positive (0.224 and 0.202), and significant at the 1% level, but that of independent VC are not significant. When syndicated VC is introduced, the two types of patent applications of NEV enterprises will increase by 22.4% and 20.2% respectively, indicating that the syndication of VC has a significantly incentive effect on green technological innovation of NEV enterprises; this is in line with the Hypothesis 4a. Liu et al.31 find that compared with independent VC, syndicated VC is more conducive to enterprises innovation, and the more the number of syndicated VC institutions, the stronger the innovation promotion role of syndicated VC.

VC heterogeneity and green technological innovation of NEV enterprises.

Note:***, ** and * denote significant at 1%, 5% and 10% level respectively, the numbers in brackets are p-values.

(2) Reputation of VC. We define the VC reputation based on the “Top 10 Investment Institutions in China's New Energy and Clean Technological Industry of the Year” released on www.chinaventure.com.cn and the “Top 50 VC Institutions” released by the Zero2IPO Research Center. If the VC institutions are on these two lists, they will be considered as high-reputation VC; otherwise, they will be considered as low-reputation VC. In columns (3) - (4), the results show that the high-reputation VC coefficients are positive, but are not significant; the coefficients of low-reputation VC significantly positive(0.186 and 0.169) at the 5% level, indicating that the high-reputation VC does not have the expected “incubation” effect on green technological innovation of NEV enterprises, which is inconsistent with the Hypothesis 4b. However, this is consistent with the findings of Liu et al.31 Using a sample of New Third Board listed enterprises, Liu et al.31 examined the relationship between VC reputation, syndicated VC and innovation. They find that syndicated VC has a more significant role in promoting enterprises innovation, but VC with a high reputation in the invested industry may resist syndicated VC and have a negative impact on the innovation of the invested enterprises. The possible reason for our conclusion maybe that in order to avoid damaging high reputation because of investment failure, high-reputation VC institutions more inclined to choose low-risk investment strategies. 44 Moreover, China's VC industry is not yet mature; the lack of professional capabilities and management experience makes it difficult to play a high reputation role in NEV enterprises green technological innovation. On the contrary, it may be driven by short-term benefits that reduce investment in NEV enterprise green technological innovation.

(3) Local investment. By manually inquiring if the headquarters and office addresses of each VC institution and NEV enterprises, if the VC institution and the invested NEV enterprise are located in the same province (autonomous region, municipality), corresponding VC will be defined as local investment; otherwise, it is non-local investment. In columns (5) - (6), the results show that when the dependent variable is green invention patent, the coefficient of local VC is 0.174, and that of non-local VC is 0.146, both of which are significant at the 5% level. When the dependent variable is green utility model patents, the coefficient of local VC is 0.185, and passes the 5% significance level, and the coefficient of non-local VC is 0.108, but it is not significant, indicating that compared with non-local investment, the local investment of VC is more conducive to green technological innovation of NEV enterprises, which is inconsistent with the Hypothesis 4c. By applying PSM model and Poisson model to investigate the relationship between VC and new energy enterprises innovation, Jiang and Liu 45 also confirm find that VC choosing local investment can rely on the advantages of geographical distance and information accessibility to stimulate innovation in new energy enterprises. The possible reason for our conclusion maybe that on one hand, VC choosing local investment can avoid information asymmetry caused by geographical distance, on the other hand, it may convenient their management and supervision over NEV enterprises to conduct innovation activities. Besides, NEV enterprises innovation relies on geographical aggregation, local investment can narrow the innovation supply chain and accelerate the process of NEV enterprise innovation.

Conclusion and Policy Implications

For the transformation of China's economic growth mode from “extensive” high-speed growth to “intensive” high-quality growth,innovation by enterprises has become the decisive factor. Using the panel data (2010–2018) of NEV listed enterprises in China, this paper empirically analyzes the impact of VC on green technological innovation of NEV enterprises by applying the DID model. The result shows that: First, VC promotes the green utility model patent applications and green invention patent applications by NEV enterprises, stimulating the green technological innovation of NEV enterprises. Second, in the heterogeneity grouping of NEV enterprise ownership, it is found that compared with state-owned NEV enterprises, VC plays a more significant role in promoting green technological innovation of private and foreign NEV enterprises. In the heterogeneity grouping of NEV industry chain location, it also found that VC plays a more significant role in green technological innovation of NEV enterprises in the upper and mid-streams. Third, syndicated and local VC investment have more significant incentive effects on NEV enterprise green technological innovation, while the high-reputation of VC has no “catalytic” effect on green technological innovation of NEV enterprises.

Compared with the existing literature to date, this paper makes contributions in three aspects: First, most scholars have investigated the impact of government administrative methods such as Dual-credit policies, R&D subsidies and promotion projects on the innovation of China NEV enterprises, but few scholars have empirically examined the influence of marketization methods on NEV industry green technological innovation from the micro level. Our paper fills this gap. Second, from the perspective of enterprise ownership and industry chain location, NEV enterprises are systematically differentiated into state-owned, private and foreign types according to the enterprises ownership, and NEV industry chain is divided into upstream, midstream and downstream according to industry chain location, which broadens the research perspective of innovation by NEV enterprises. Finally, combining previous studies, we have confirmed the innovation incentive effect of syndicated VC and local VC, but also drawn opposite conclusion that high reputation VC does not play an innovation incubating role for NEVs. It can enrich the theoretical basis of VC innovation and provide a reference for the sustainable development of NEV industry.

Based upon the above conclusions, we put forward the following policy recommendations:

Faced with a gradual decline of NEVs subsidies, government should vigorously encourage the expansion of the VC industry, guide VC to enter the NEV industry, and give full play to the role of marketization factors in stimulating NEV enterprise green technological innovation. Deepen the reform of state-owned enterprises, encourage VC to enter the state-owned NEV enterprises, and improve the innovation capacity of state-owned enterprises. Accelerate the implementation of the joint venture share ratio policy of enterprise, encourage foreign NEV enterprises to enter the domestic market to accelerate the technological competition of NEV industry. NEV enterprises innovation is characterized by high risk, long cycle and great uncertainties. VCs may select joint investment and local investment to accelerate the integration of local innovation resources and narrow the scope of the innovation supply chain of NEV industry.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Social Science Foundation of China (20BGL046).