Abstract

About 70% of India’s current energy mix comprises of coal, and the increase in generation from renewable (RE) sources is affecting the health of the power system. We investigated this effect through the lens of asset utilisation, cost and the social disruption caused by accelerating RE into the Indian Power System. Our review-driven analysis revealed that increasing RE generation is pushing the coal plants to operate in low-loading conditions, causing heightened wear and tear of the plant as they are not suitable for flexible operation. The novel analysis of social disruption due to market parity between RE and coal-based generation presented a holistic view of the political economy of Indian Power System. We found that transition from coal to RE may have extended socio-political ramifications that can potentially disrupt the national economy at an unprecedented scale. Policy implications outlined by our study for the draft Electricity (Amendment) Bill 2020 include scoping a socio-technical framework which supports just energy transition through better financial support mechanisms for flexible operation of coal plants. Focusing on clean-up over shut-down of coal plants and facilitating investments in battery storage technologies and cross-border electricity trade as RE and conventional fuel reach market parity.

Introduction

The Indian power sector is experiencing transformative changes due to the increase in renewable generation to meet the country’s Intended Nationally Determined Contributions (INDCs) towards the Two-Degree Celsius climate change goals post-2015.1 The challenges associated with this renewable transformation has technological, social and economic implications that need more in-depth attention. India must restore the health of its power sector, enable clean energy transition at all household levels and foster distributive justice in the shift to renewables for meeting the INDC targets.2,3 The current target aims at a six-fold expansion of renewable energy generation to 100 gigawatts (GW) of solar energy capacity and 20 GW of wind energy capacity by 2022.3 Besides, INDC aims to base 40% of the total power generation on non-fossil fuel resources by 2030.1

The stimulus for the increase in renewable generation in India has multiple layers transcending the economic, social and environmental aspects of growth and development. Reducing carbon emissions and decarbonisation of the power sector remains a primary motivation, sustainable development drivers like improving access to clean energy, livelihood generation and poverty alleviation are also critical drivers of this power sector transformation. 4 Around 200 million people in India lack access to electricity, despite India being the world’s third-largest producer and consumers of power. 5 Renewable power generation is critical to meet this deficit through a decentralised and micro-level off-grid planning. It is not only critical to energy security at large but also provides tremendous income generation potential, especially in rural and low-income communities. The Make in India, the Assemble in India and the Skill India campaigns of the Government of India are particularly critical to large-scale renewable-led income generation especially for the population at the bottom of the pyramid.6,7 For example, India’s solar industry employs an estimated 1,03,000 people, including 31,000 in grid-connected and 72,000 in off-grid applications; another 48,000 people work in the wind sector. A further 3,00,000 jobs will be needed to meet India’s renewable targets by 2022 (Jairaj et al.,6 p.12).

While the above projections promise energy and job security for India, the current challenges associated with the increase in renewable energy generation on the power sector are little known. Fossil fuels (coal, oil and gas) made up 75% of the Indian energy mix in 2018, of which 78% of the electricity is produced from coal. 8 The heavy dependence of the Indian power sector on fossil fuels poses concerns for its supply-side security. The energy supply side security can be affected due to increase in import dependence in petroleum, natural gas and coal; high demand of coal to produce power, cement and steel; and geopolitical instability (IEA,7 p.151). Indian energy supply chains need to be more self-sufficient by reducing dependency on import of petroleum, natural gas and coal and by switching to renewable generation as its replacement (IEA,7 p.14). Digitisation, decarbonisation and decentralisation of the Indian power system are crucial for energy self-sufficiency through renewables and achieving holistic grid parity. 9

Grid parity is usually defined as the intersection of the price of the electricity generated by renewable generation and the price of conventional electricity production. Technically, grid parity is a situation in a time when the cost of electricity generated from renewable is equal to or lower than the cost of electricity generation from conventional sources. 10 However, in our conceptualisation of holistic grid parity in the Indian power sector, we factor in the transformational effect of renewables on asset utilisation, cost-competition and employment generation for social change. It forms the motivation for this paper, and we investigate the following research question through a systematic and interpretivist review of government policy documents and relevant published literature. The research question is, ‘What are the challenges posed by increased in renewable generation in the Indian power sector?’.

We further define the scope of this work on investigating the challenges posed by the increase in renewable energy generation on the supply side power sector, with emphasis on the ageing thermal power plants and the draft Electricity (Amendment) Bill 2020 (hereinafter “EB”). The EB 2020, introduced by the Ministry of Power, proposes amendments to the monumental Electricity Act (EA), 2003 to remove pre-INDC specific provisions of the EA 2003.11 In this purview, the EB 2020 proposes policy and functional amendments to address the recurring issues of the Indian power sector (as mentioned above) and to promote further commercial incentive for private players to enter the market in the generation, distribution and transmission of electricity. 11 The proposed EB 2020 is a highly debated energy policy amendment bill in the country, and this study extends this debate by providing an interpretivist view on the impact of the increase of renewable energy generation on coal-powered economy and the society.

To examine the research question, following review objectives are formed, i) explore the challenges and opportunities created by increasing renewable energy generation in the Indian power sector; ii) develop the narrative around the asset, cost and social implications of this changing energy landscape on the coal-dependent economy; and iii) draw critical policy implications for the draft Electricity (Amendment) Bill 2020 under the pressures of accelerated renewable energy generation.

The novelty of this study lies in the interpretivist cross-sectional review of primary and grey literature on three themes shaping the socio-technical landscape of the Indian Power System under accelerated renewable energy transition. The review themes are across asset utilisation, cost competition and social disruption caused due to sudden shift in coal-dependent power sector. This approach aided in developing the narratives on potential systemic disruptions due to accelerated RE generation in India. In doing so, we generate a roadmap of the challenges and the opportunities for the proposed Electricity (Amendment) Bill, 2020 that is crucial to India’s energy security. Such an analysis concerning EB 2020 and the effects of the increase in the renewable generation on the power sector has not been done before in the Indian context and this study contributes uniquely to the current discussions on good energy policymaking 12 in the Global South.

This study is divided into following sections. The next section provides a brief overview of post-2015 status of the Indian Power System. It documents key government policies designed to meet the ambitious 2030 renewable energy generation target of the country. The Review methodology section outlines the cross-section literature review methodology. The thematic reviews are presented in the Results and discussion section across subsections to develop the current narratives of challenges and opportunities from accelerated RE in the Indian Power System. The concluding remarks and the policy implications for EB 2020 are presented in the last section.

Background

Power sector post-2015 accelerated renewable generation

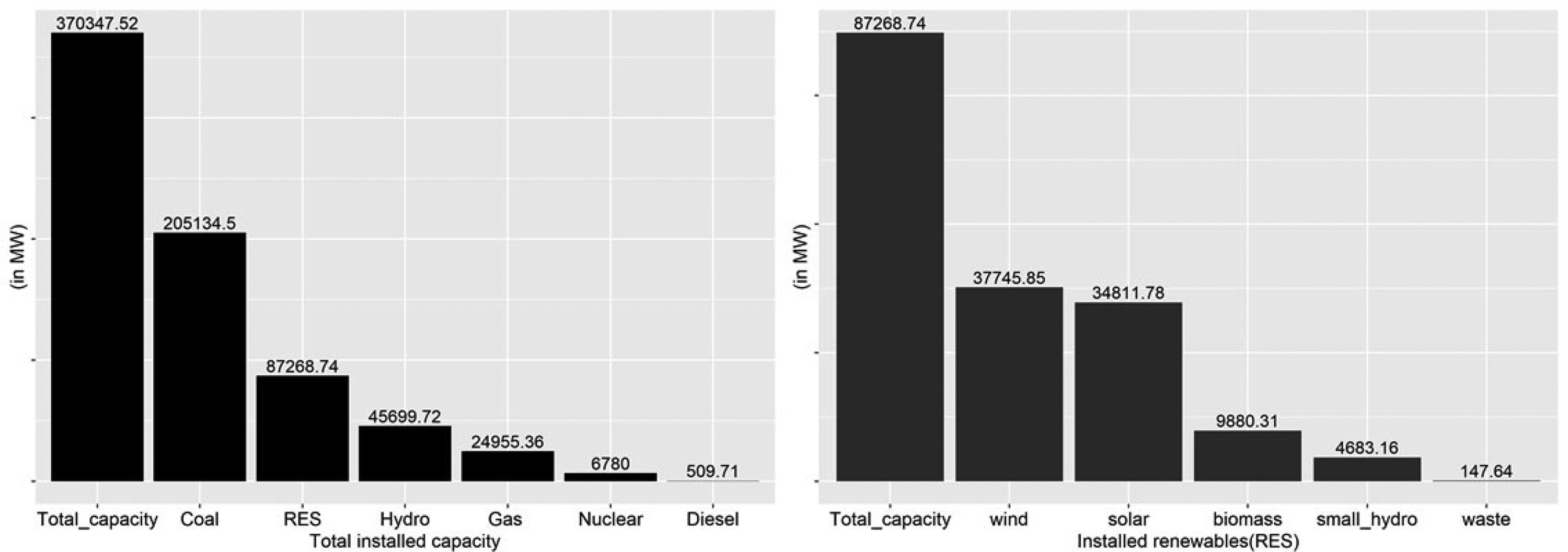

India adopted the 2030 Agenda for Sustainable Development in September 2015, and subsequently ratified the Paris Agreement on October 2016 by submitting the Intended Nationally Determined Contributions (INDCs).1,3 The power sector in India post-2015 is undergoing a critical transformation to meet the 2030 target of 40% power generation through non-fossil fuel-based sources. 1 Currently, India is the third-largest electricity generator in the World behind China and USA with a per capita energy consumption of 1117 kWh (in 2017). Coal power has the highest share (∼78%) among the total installed capacity in 2020 (see Figure 1), while in renewable energy sources wind power had the highest share (∼43%) followed by solar power (∼40%) (see Figure 1). The share of renewable sources in the total energy mix was 23.56%, as per April 2020.13

Total installed capacity and installed renewable share (RES) in India as of April 2020 (Data source: NPP 13 ).

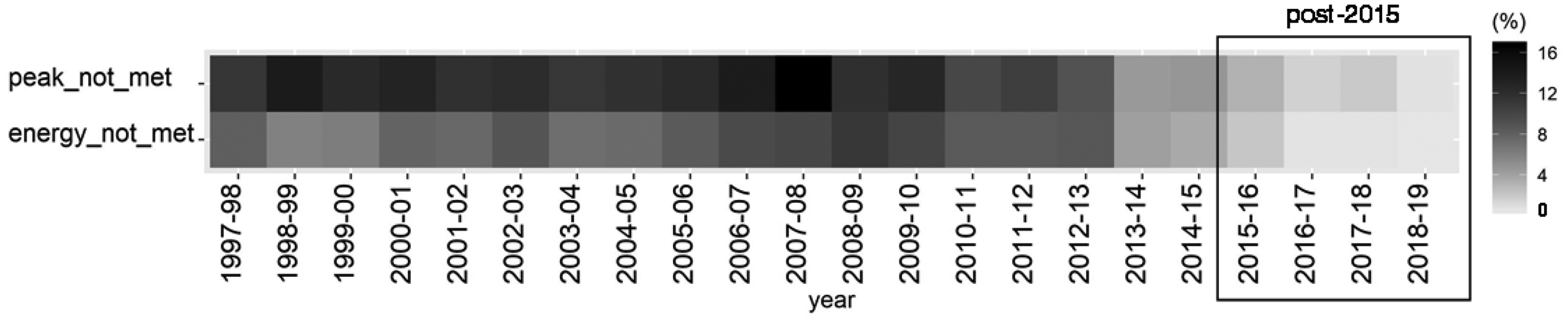

Decarbonisation, digitisation and decentralisation of the power system pose a critical technological and policy challenge for the Indian power sector. 4 Nonetheless, there has been tremendous improvement in the Indian power sector post-2015 that resulted in ‘surplus’ power in 2018 as the total installed electricity generation capacity exceeds 344 GW against a peak demand which has never exceeded 170 GW till date. 9 The surplus country status remains intact even in 2018–19 as the total installed capacity exceeded 370 GW (see Figure 1) against a peak demand of 177 GW (CEA,14 p.53). This trend is an indicator the improving health of the power sector post-2015 policy reforms. Figure 2 further illustrates the ‘surplus’ by showing significant reductions in the ‘not-met’ peak and ‘not-met’ energy demand over the last 22 years, especially the drastic reduction took place in the post-2015 scenario.

A heatmap showing post-2015 improvements in the Indian Power Sector on significant reduction on not met peak load and energy demand (Data source: CEA 14 ) [Note: lower percentage value is better].

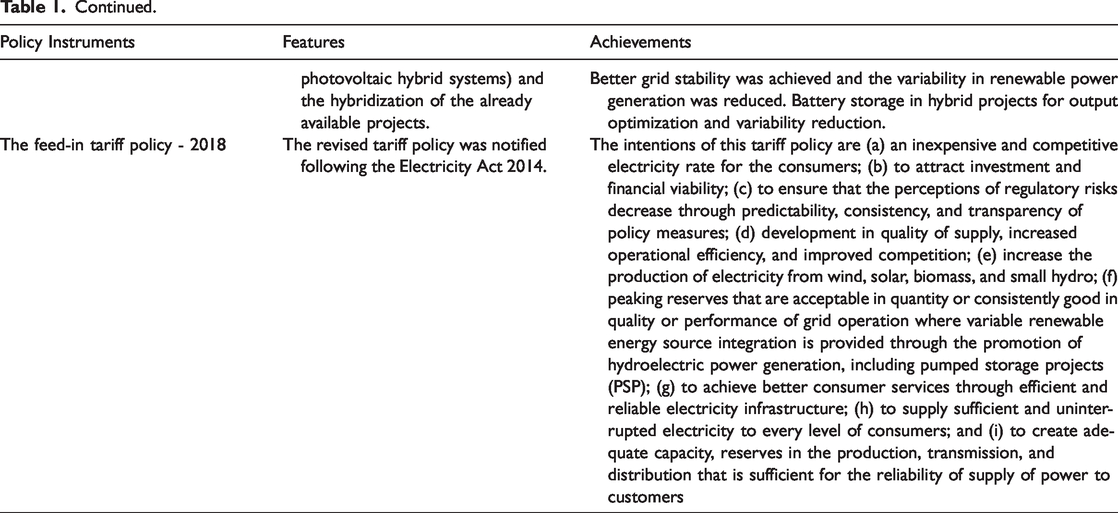

With the strong impetus of renewable-driven growth in the Indian power sector, a host of policy instruments were deployed for driving the energy transformation while fulfilling the INDCs (see Table 1). The policy landscape illustrated in Table 1 further illustrated the paradigm shift in the design of energy policy instruments in the country with a stronger push for ‘Make in India’, ‘Assemble in India’ and ‘Skill India’ initiatives. It is estimated that 3,00,000 full-time equivalent jobs can be created in this ongoing renewable wave for ground-mounted and rooftop solar Photovoltaics (PV) by 2022.6 Currently, India’s solar industry employs an estimated 1,03,000 people, including 31,000 in grid-connected and 72,000 in off-grid applications; another 48,000 people work in the wind sector. 6 However, the current challenges associated with the power sector amidst this transformation needs to be addressed systematically for more substantial societal benefits and sustainable development. The next section expands on the challenges faced by the Indian power sector post-2015 accelerated renewable generations.

Overview of post-2015 challenges in the Indian Power Sector

While accelerated power generation through the renewables were significant progress of the Indian power sector post-2015 reforms. The integration of 175 GW installed capacity from renewable energy sources (RES) by 2022 remains a significant challenge.7,15 The accelerated generation further poses challenges in the flexibility of thermal plant operation and its low plant load factor (PLF) as the thermal capacity need to be ramped down considerably during the time of peak solar generation. 15 It assumes that the coal plants will flex their output (both upward and downward) and produce at a lower level than their design capacity. This impacts both the plant efficiency and creates wear and tear, which can have more profound ramifications in reducing the overall efficiency and reliability of the Indian power system (Tongia,15 p.27). The costs associated with bit ramping and start-stop operations remain uncertain and it is also not known who will bear it. It is especially severe for ageing (sub-critical) thermal power plants, and it would have severe economic and operational penalties.16,17 Besides, studies have shown that even the super-critical plants need to be designed for flexing as they have a lower ability to flex-down.15,17 Alternatively, they will lose their super-critical (efficient) operations.

Investment in flexing is unlikely to be borne by RE produces, and thus thermal plants would pass on such costs to consumers. In an experimental flex testing at the National Thermal Power Plant (NTPC) Dadri it as found that coal plants would be paying many tens of millions per GW to reduce their output. 17 Besides, the current state of the Indian power system lacks adequate balancing capacity owing to steep ramping requirements. 9 It has a further systemic effect on the DISCOMs. The Government of India (GoI) launched the ‘UDAY’ scheme to enable the DISCOMs to reduce their interest burden, cost of procured power and Aggregate Technical & Commercial (AT&C) losses. However, the results have not been encouraging; the average AT&C losses of DISCOMs on an All-India basis has hardly reduced from 20.74% in FY 16 to 18.76% in FY 18. In general, the AT & C losses are higher in the DISCOMs of poorer states as compared to the developed states. 18 Accelerating the progress of state-owned distribution companies (DISCOMs) towards financial sustainable continues to be a critical challenge of the Indian power sector.

Other structural challenges include reduced offtake of power due to supply-demand mismatch related to Power Purchasing Agreements (PPAs) for new RE capacity addition. 9 Grid balancing and grid integration remain a critical problem both technically and financially. The Ministry of Power (MoP) has approved a project comprising inter-State and intra-State transmission systems collectively called ‘Green Energy Corridors (GEC)’ to be completed by 2020 to facilitate the integration of 175 GW of RE. 9 The grid can be balanced by using hydropower and pumped storage plants, enhancing gas supplied to the existing gas-starved power plants for using them as peaking plants and deployment of grid-scale battery storage to handle the intermittency of RE. 9 Replacing Diesel Generator (DG) sets with RE power-cum-storage plants can be a viable solution too to the intermittency problem. In addition, access to low-cost global finance like the Green Climate Fund (GCF) is critical for India to accelerate its progress towards the achievement of its INDCs. 19 In this purview, large-scale disposal of energy storage devices like batteries and the implementation of new environmental norms leading to the retirement of units remain critical power sector challenges in India. 9 This paper further explores these challenges through an analytical framework presented in the Review methodology section for drawing critical inferences for the draft Electricity (Amendment) Bill 2020.

The draft Electricity (Amendment) Bill, 2020

The proposed draft Electricity (Amendment) Bill, 2020 (herewith ‘EB’) has its backbone on the Electricity Act 2003, the Electricity (Amendment) Bill 2014 and the Indian Renewable Energy Act 2015.11,20 The proposed EB 2020 has critical significance post-2015 as it is proposed amendments in the EA 2003 to foster INDCs commitments amidst the energy transformation of the Indian power system. Besides, EB 2020 also intends to address the current challenges of the power system, as mentioned in the previous section.

The EA 2003 is considered as the foundation of the post-2015 Indian Power Sector and its sustainability drivers. 3 Some of the salient features of the act were the novel introduction of the National Electricity Policy, a focussed approach to rural electrification, delicensed generation, the constitution of the load dispatch centres, a centralised transmission utility, open access regulations, electricity supply code, the National Tariff Policy, Central Electricity Authority (CEA), regulatory commission, appellate tribunal, reorganisation of the electricity boards and the development of the power markets.3,20 The Electricity (Amendment) Bill 2014 consolidated all previous acts of the Indian Power Sector, including the EA 2003. The Bill was designed with the sole aim of introducing competition in the distribution segment through the mechanism of bifurcation of carriage (transmission and distribution business) and content (electricity business).3,20 The focus of the EB 2014 was the segregation of commercial losses from technical losses, bifurcation of T&D business from electricity business, supplier switch through choices given to end consumers, measures to secure the grid, strength the regulatory framework of the country, to strengthen the provisions to provide non -discriminatory open access, promotion of RES for clean energy and provisioning of healthy tariff policy and the rationalisation of the tariff structure.3,20

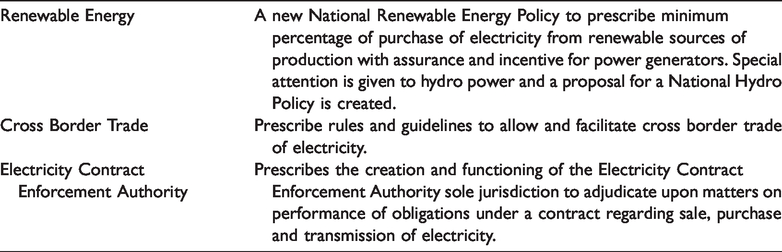

The Indian Renewable Energy Act 2015 and the Ujwal Discom Assurance Yojna (UDAY) (see Table 1) were introduced to further strengthen India’s energy trilemma – environmental sustainability, energy security and energy equity through renewables. The IREA 2015 was a responsive action to ratify INDC at the Indian Power Sector level. 21 The institutional mechanisms under this act were the formation of National Renewable Energy Plan and State-level Renewable Energy Policy and Plan; set-up of various authorities like National Renewable Energy Commission (NREC), National Renewable Energy Advisory Group (NREAG), Renewable Energy Corporation of India (RECI), Renewable Energy Investment Zones and Renewable Electricity Investment Zones. Besides a supportive ecosystem was created through National Renewable Energy Policy (NREP), Renewable Energy Resource Assessment and Testing, and Manufacturing and Skill Development.4,20,21 Moreover, the IREA 2015 established the following economic and financial framework, the National Renewable Energy Fund and the State Green Fund. The act further specified on Distributed Renewable Energy Application and Access, Renewable Purchase Obligations (RPO) and grid balancing and grid integration (also mentioned in the previous section). 21

The UDAY scheme was launched to fix the financial and operational issues faced by the DISCOMs. The DISCOM liabilities were partly taken over by the states, and the states could raise bonds by offering attractive terms. 22 The bonds were well subscribed and offered attractive yields. A recent study had shown that development financial institutions like the World Bank, the Asian Development Bank, etc., could buy the state-backed bonds for early coal retirement and demonstrated their commitment to dirty-to-clean energy transition. 23 It is further important in the retirement of ageing and expensive coal plants (brownfield plants) that is crucial to India’s RE transition (also discussed in the previous section). However, converting such plants to flexible plants may be more cost-effective in the long run as it can provide a higher degree of job-security to the coal workers. 23 In this study, we further explore this social dimension of thermal power generation reduction due to accelerated RE generation.

The EB 2020 intends to address some the recurring issues of the Indian Power Sector (see the previous section) and to promote further commercial incentive for private players to enter the market in the generation, distribution and transmission of electricity. One of the aims of the new Bill is to bring financial discipline in the distribution companies through Cost Reflective Tariff aimed at eliminating the tendency of some Commissions to be flexible. 24 There is also a provision for Direct Benefit Transfer where it is proposed that tariffs be determined by Commissions without considering the subsidy, which will be given directly by the government to the consumers. Load Dispatch Centres will be empowered to oversee the payment security mechanism. 24 The significant policy changes that this Amendment proposes to introduce in the Electricity Act, 2003 is illustrated in Table 2.

Review methodology

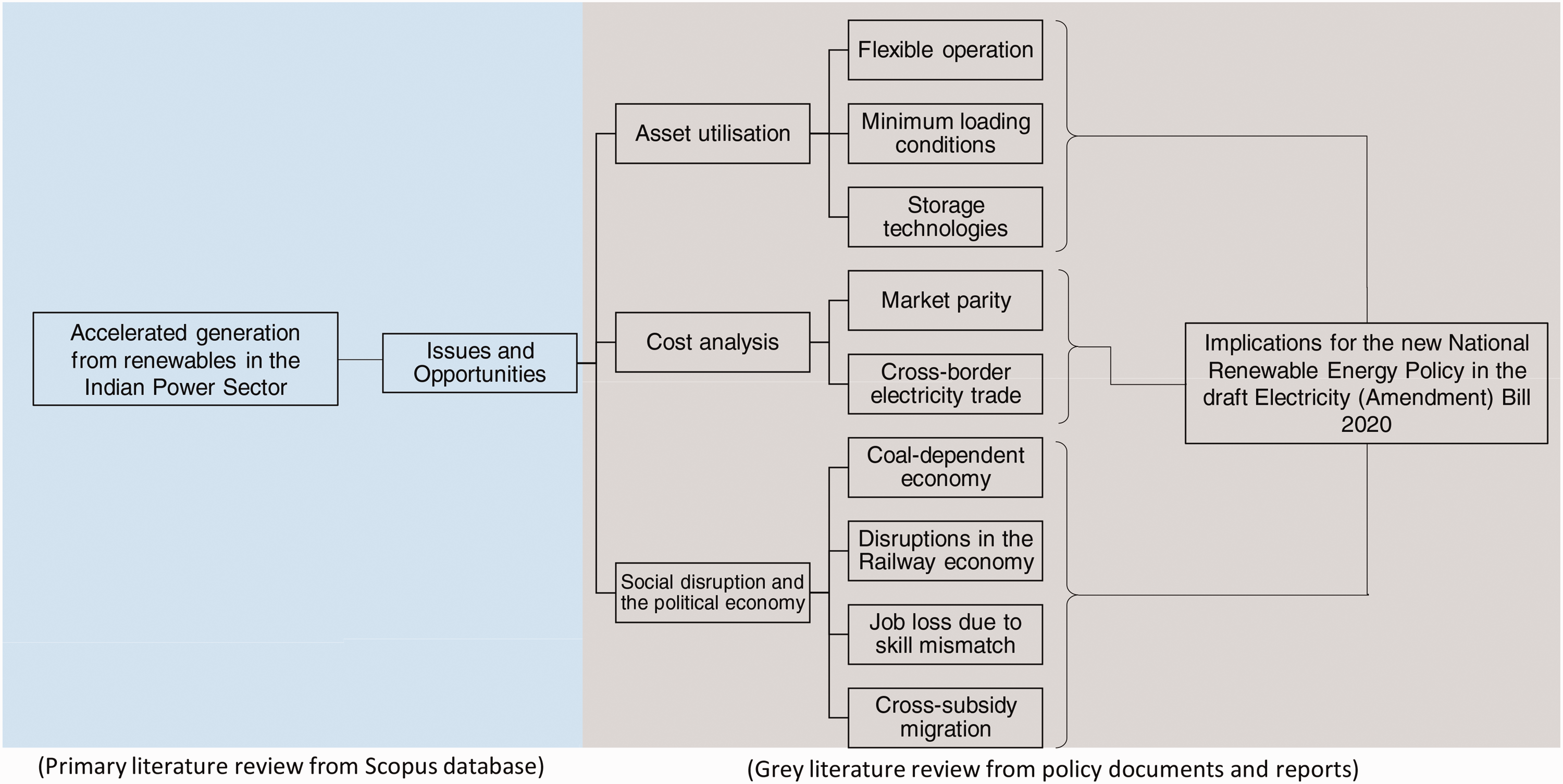

The analytical framework adopted in this study to conduct the systematic literature review is illustrated in Figure 3. The systematic approach consisted of a bibliometric analysis of published literature on the Scopus database with the keywords ‘India’, ‘Power system’ and ‘Renewable energy’. Only the papers published since 2015 were reviewed to be coherent with the post-2015 INDC policy agenda of India. This heuristic search delivered 939 documents from the database that was analysed to explore the co-occurrence network of high frequency words/terms associated with the Indian power sector and renewable integration. The finding from this stage aided in outlining the challenge and opportunities in the present power sector from the state-of-the-art bibliographic lens. The co-occurrence networks were derived from the title, abstract, keywords of the 989 documents using the R-programming language (after the methodological framework by Aria and Cuccurullo 25 ).

The analytical framework for an interpretivist approach to a systematic review of present Indian Power Sector.

The results from the first stage reviews are then collated with the grey literature review of policy documents and reports of institutional bodies. It involved grey literature search in government institutions like the Ministry of Power, national planning bodies like NITI Aayog and national-level energy authorities like National Thermal Power Plant, India Energy Exchange, National Load Dispatch Centres, Central Electricity Regulatory Authorities, etcetera. To streamline this grey literature search concerning the objectives of this study, we divided the review into three key segments (see Figure 3).

The first segment deals with the issues arising due to changes in asset utilisation in the power sector post-2015 INDC commitments. We based the rationale behind this investigation of changes in the asset utilisation on the current policy requirements to accommodate accelerated power generation from renewable energy sources (RES), decommissioning of inefficient thermal power plant, and flexible operation or low-capacity utilisation of the thermal power plants. This approach was critical as it can aid in strengthening of the envisaged new National Renewable Energy Policy as per the draft Electricity (Amendment) Bill 2020 (see Table 2).

The second analytical element of our grey literature review methodology was the cost and choice analysis in the post-2015 policy space. We examined the drivers to bring-in market-parity between conventional fuels and RES (see Figure 3). The market parity arguments were presented based on the levelized cost of electricity (LCOE) generated from the thermal power plant to solar power plant for 2020. It shaped an objectivistic purview of RE integration into the coal-dependent economy of India. With flexibility and low loading conditions becoming the reform drivers in the ‘clean coal’ space, we further explored the issues that arise at an operation and maintenance (O&M) level in thermal power plants. Here, we developed the narratives on the cost of maintaining a high inventory of consumable spares and secondary fuel due to the increase in O&M of coal power plants owing to flexible operation due to the increase in RE generation. In addition, we evaluated the opportunities of a revenue stream through cross-border energy trade (CBET) that can create a robust market place of energy exchange with the neighbouring countries.

Besides, CBET is a proposed critical addition to the draft Electricity (Amendment) Bill 2020 (see Table 2). Our analytic arguments derived during the review process for evaluating the opportunities in CBET were based on the following parameters, the difference in consumption and cost of production; optimal utilisation of RE resources; fostering economic growth and regional integration, and seasonal complementarities with neighbouring nations. A similar approach was adopted by Wijayatunga et al. 26 and Singh et al. 27 ). In doing so, we also derived critical inference from the draft Central Electricity Regulatory Commission’s (CERC) Cross Border Trade of Electricity framework. 28 To derive a holistic overview of the policy space in this regard, we evaluated the implications of CBET on the Indian States through Renewable Purchasing Obligations (RPOs) and its implication on the Indian Energy Market.

A critical contribution of this study is the development of narratives around potential social disruption caused due to the increasing power generations from RES. To evaluate the breadth of social disruption, we reviewed the available literature around the political economy of disruptions due to the increase in generation from RES. We observed that there was a significant primary literature gap on this topic and most of the literature was in the form of think tank reports. It further elucidates the novelty of this study towards this literature gap.

With this epistemological background, we provided an interpretivist view on the decline of the coal-dependent economy and its ramifications on millions of livelihoods. Especially when the coal-economy dependent states of India usually have a low GDP per capita. 29 Our parallel line of interpretivism was based on the potential disruptions in the railway economy that operates on heavy cross-subsidisation from coal freight to lower passenger fares. We further explored its effect due to the accelerated generation from RES. Lastly, we examined the possible shift from fuel import dependency to technology import dependence affecting the national security of India.

Results and discussion

Bibliometric analysis of current literature on the Indian Power System and renewable integration

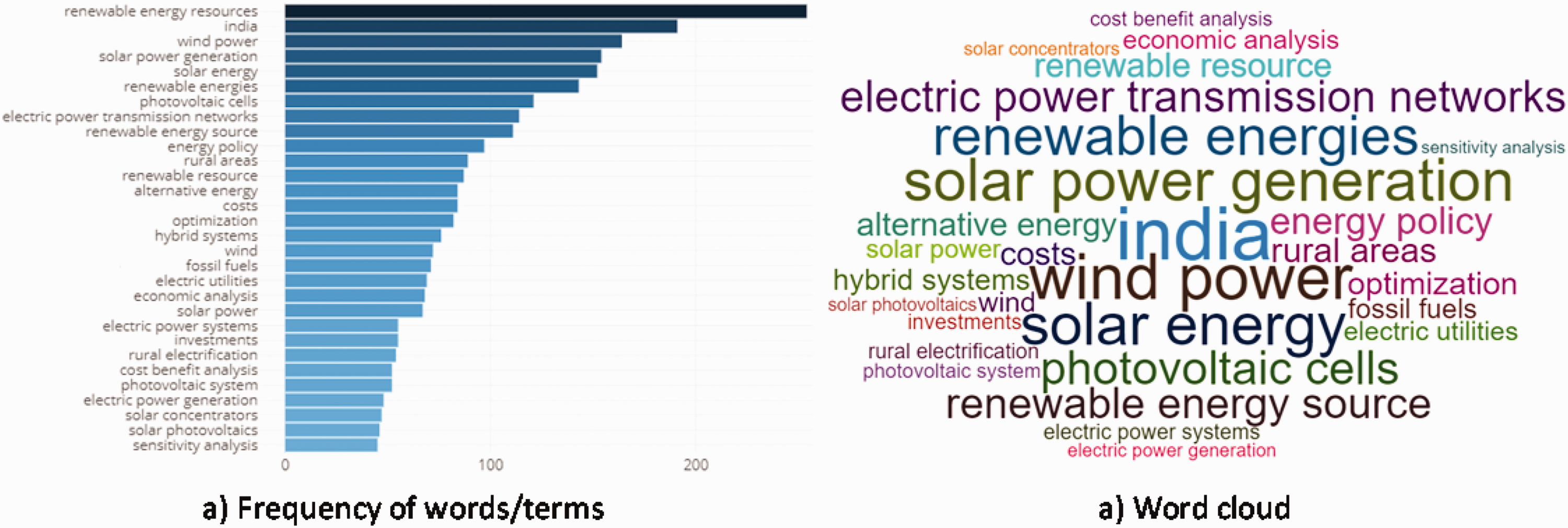

Figure 4 illustrates the high-frequency words/terms in the state-of-the-art literature on Indian power sector and renewable energy from the Scopus database of 939 research articles. Terms like ‘wind power’, ‘solar power generation’ and ‘solar energy’ have highest frequency indicating the focal point of research articles have been on the renewable technology development and its feasibility analysis (see Figure 4(a)). The word cloud in Figure 4(b) represents the most repeated words that also shows ‘economic analysis’, ‘cost benefit’ and ‘optimization’ as high frequency terms in the current literature. A critical inference that can be drawn here is that post-2015 research focus on Indian power sector have mostly been on the capacity expansion and feasibility analysis shaping the technocratic-only discussions. It also shows the gap in socio-technical research efforts in handling the energy renewable energy transition.

High frequency words/terms in the state-of-the-art literature on Indian power system and renewable integration from the Scopus database (n = 939).

From the purview of the power system, higher representation of terms like ‘electric power transmission network’, ‘hybrid systems’ and ‘electric utilities’ (see Figure 4(a)) shows research focus has been on the technical aspects of the renewable integration in the power system. At the same time, high frequency words were also associated with ‘rural electrification’, ‘rural areas’, ‘energy policy’ and ‘investments’ (see Figure 4) indicating a significant focus of the energy policy space is on ensuring rural electrification which involves renewable solutions. We found that the current literature lacked topics dedicated to exploring the social, economic and environmental challenges from accelerated RE generation.

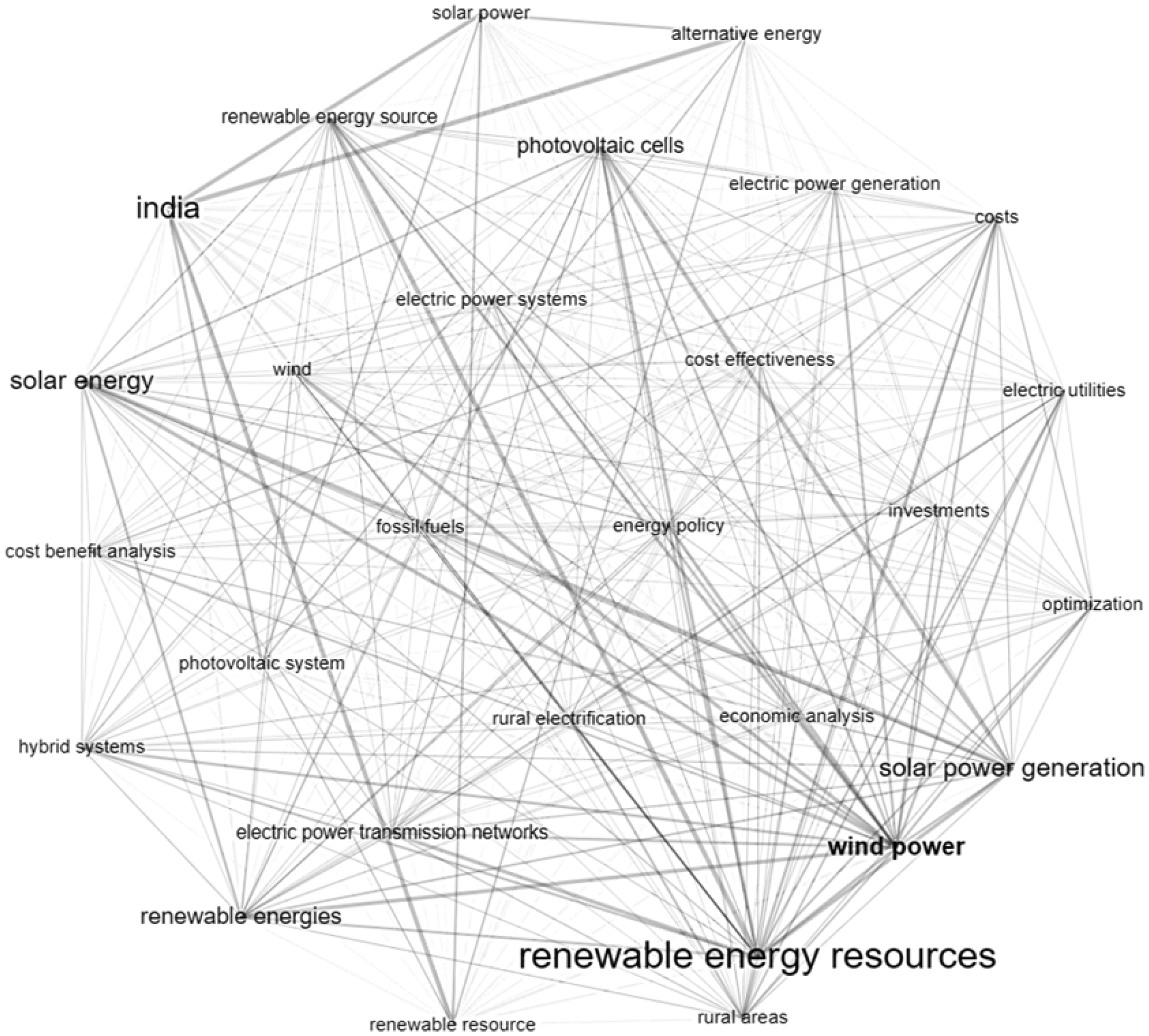

Figure 5 further illustrates the co-occurrence network of high frequency terms associated with the keywords ‘India’, ‘power system’ and ‘renewable energy’. The size of the terms corresponds its frequency counts in the database of 939 documents, the lines illustrate the interconnections. The state-of-the-art discussion on ‘renewable energy resources’ have strong interconnections with terms like ‘photovoltaic cells’, ‘wind power’, ‘solar power generation’, ‘transmission networks’ and ‘energy policy’ representing the current research landscape concerning RE technology and policy space (see Figure 5). Further interconnections can also be observed with the terms ‘fossil fuels’, India’, rural electrification’ and ‘renewable energy resources’ indicating the growing research on renewables for rural off-grid electrification and reduce dependence on fossil fuels. However, the studies do not explicitly connect future renewable policy design with the broader sustainable development goals. Table 3 further illustrates critical studies that imply on the socio-technical dimensions of post-2015 accelerated renewable generation in India.

Co-occurrence network of terms in the current bibliography on Indian power system and renewable integration in the Scopus database (n = 939).

Critical literature illustrating the effect of accelerated renewable energy generation in the Indian power system.

Issues arising due to asset utilisation

The significant changes observed post-2015 are in asset utilisation in coal-based power plants, transportation of coals to these power plants and introduction of storage technologies to meet the reserve criteria for peak demand. The asset utilisation for thermal coal plants was the retirement of the less efficient power plants, also known as brownfield coal plants, is a significant issue of the Indian Power Sector. 23 The low capacity utilization and fuel switching also led to a decline of additional coal power plant expansion in the country in the backdrop of post-2015 renewable policies. A significant challenge remains with the strategies for flexible operation to counter withstanding at low loading condition and defining technically achievable minimum loading condition. 15 The minimal loading conditions is the lowest possible net load a generating unit can deliver under stable operating conditions. It is measured as a percentage of normal load or the rated capacity of the unit. 17 Determination of minimal loading conditions is critical for flexible operation of thermal power plants, also known as Minimum Thermal Loading (MTL). The factors deciding MTL are off-peak and peak grid demand, solar & wind generation as well as generation from other types of sources at the time of off-peak and peak grid demand (CEA,17 p.1).

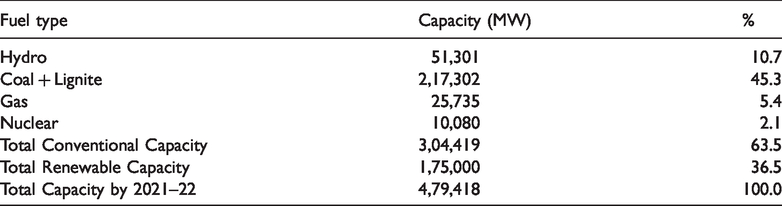

A recent study by the Central Electricity Authority (CEA), Government of India (GoI) on the Flexible Operation of Thermal Plant for Integration of Renewable Generation 17 had presented a methodology for calculating the MTL with the assumption that all fuel sources operate as business-as-usual (BAU) and all thermal units ramp up/ramp down at the same rate simultaneously (see Annexure – I of CEA 17 ). Other assumptions included a 10% reserve of coal, and as Auxilliary Power Consumption (APC) deteriorates with low load operation, APC of 7% at maximum load and 9% at minimum load is considered. The BAU generation forecast was for 2021–22 with the assumed installed capacity illustrated in Table 4.

Assumed Installed Capacity for 2021–22 under BAU conditions for determining minimum loading conditions of thermal power plants (Data source: CEA 17 ).

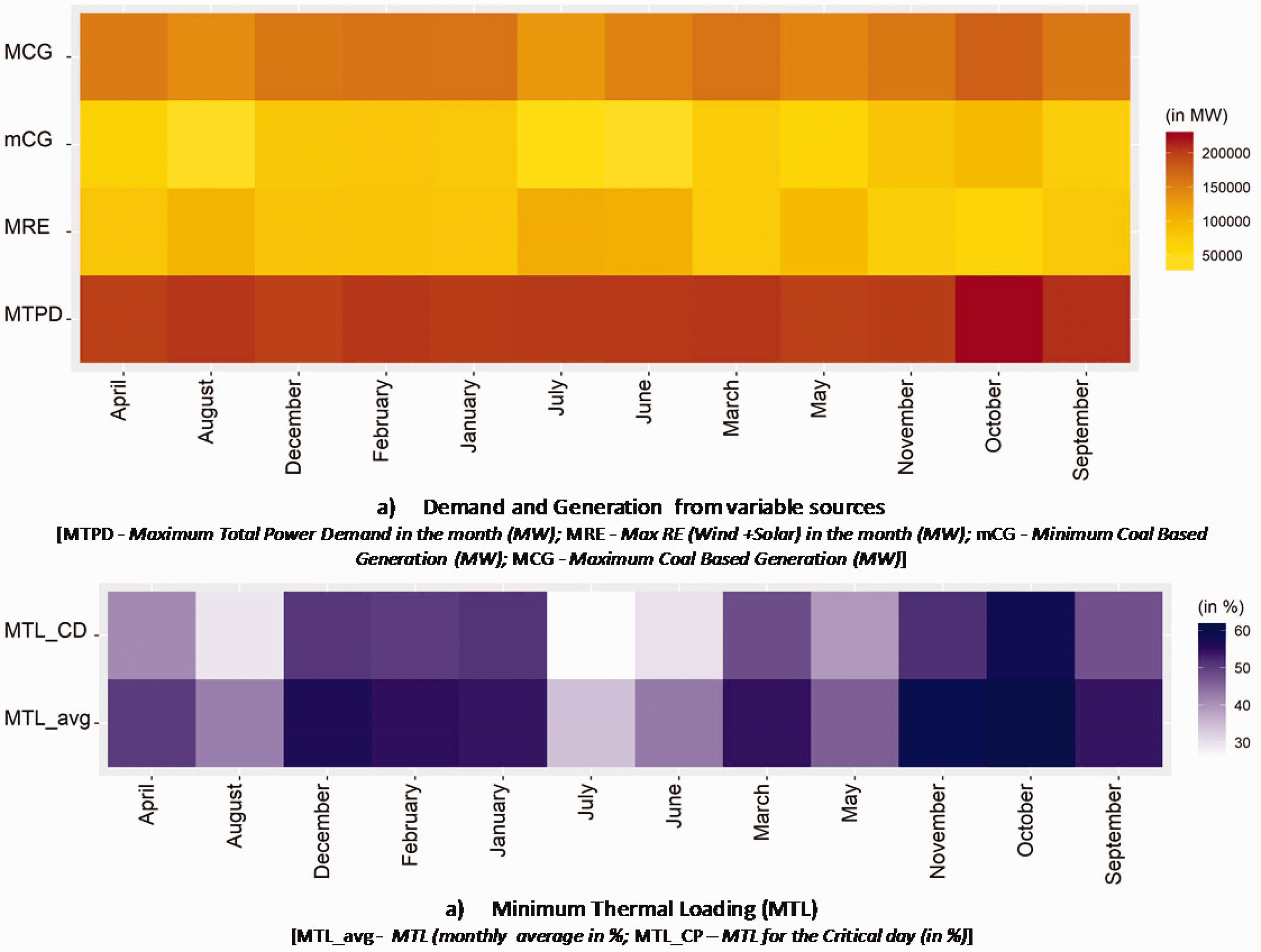

The lowest MTL estimated in the simulation that determined the ‘critical-day’ was 27th July 2021 (see Annexure – I of CEA 17 ). The estimated generation data for the BAU 2021–22 scenario is illustrated in Figure 6. The 108 GW was the highest available generation from RES in the year 2021–22. Thermal power plants were required to operate at an average 25.73% minimum load to accommodate the RES generation into the grid and to balance the system (see Figure 6(b), July). This was the most challenging situation in the system to maintain a stable and secure grid as these systems were not designed to handle a ∼26% MTL. Currently, the flexible operation strategy mandates coal power plants to go low on electricity production while keep it running. However, in such conditions, a reverse shut down is considered as a better option than to keep it running on low production mode to avoid accelerated creep and fatigue. This will in turn increase the spending on operation and maintenance (O&M) of the brownfield coal plants. 17 It is a critical policy decision under accelerated RE generation scenario.

Estimated summary of demand, generation and MTL for the BAU scenario 2021–22 under variable energy sources (Data Source: CEA 17 ).

Additionally, challenges associated with flexibility in operation brings in O&M based factors to the system like mechanical or electrical failures at power plants, substations or transmission lines, the capacity of the power plants on the busbar to reduce the electricity production, time-taken for a shutdown power plant to the point of electricity production, and the ramp-up and ramp-down rate of the power plants for addressing variability and uncertainty of renewable generation.15,17,23

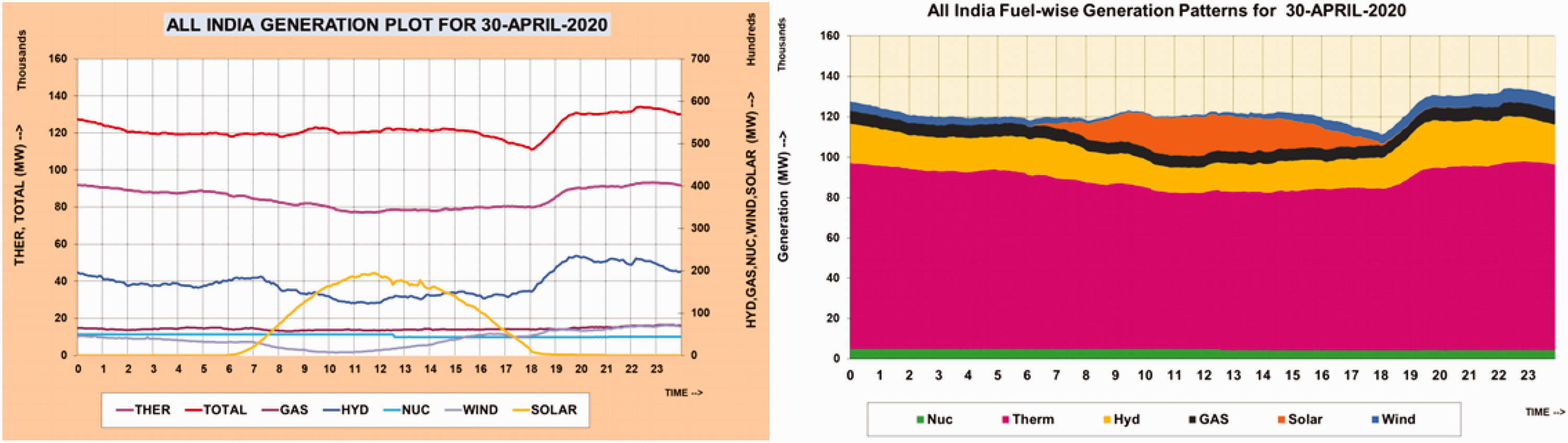

Figure 7 shows a typical day’s behaviour in generation units due to the increase in renewable power generation in April 2020. For example, the peak solar output was highly variable with the other RES (wind, hydro) as well as with the coal, thermal and nuclear generation. The surge in solar generation led to instability in the grid and the thermal generation on the bar was ramped down to accommodate this surge. 40 It was even more significant as April 2020 was a lockdown month in India due to COVID-19 that resulted in significant drop in power demand.41–43 To accommodate this surge in solar power output, thermal generators on the bar was ramped down that led to severe wear and tear of the thermal units. 40 Such behaviour is expected to be become more prominent in future, which requires system readiness to tackle it.

Typical behaviour in all India generation owing to significant additions from RES on a single day (Source: POSOCO 40 ).

Another critical challenge with the post-2015 Indian Power Sector is the decommissioning of the ageing thermal power plants (older than 25 years), also mentioned in the Overview of post-2015 challenges in the Indian Power Sector section. As of April 2019, a total of 2197 MW of coal power plant capacity, across 18 units in 7 plants, retired or converted across India this fiscal. During the same period, 5,712 MW of new capacity has been added. 44 Moreover, an additional 12000 MW of coal power plants will be required to shut down by early 2022 to remain on track with the INDC commitments. 44 The newer coal plants are being built on super-critical technology while the older plants have sub-critical technology which makes flexibility operation even more challenging.15,23

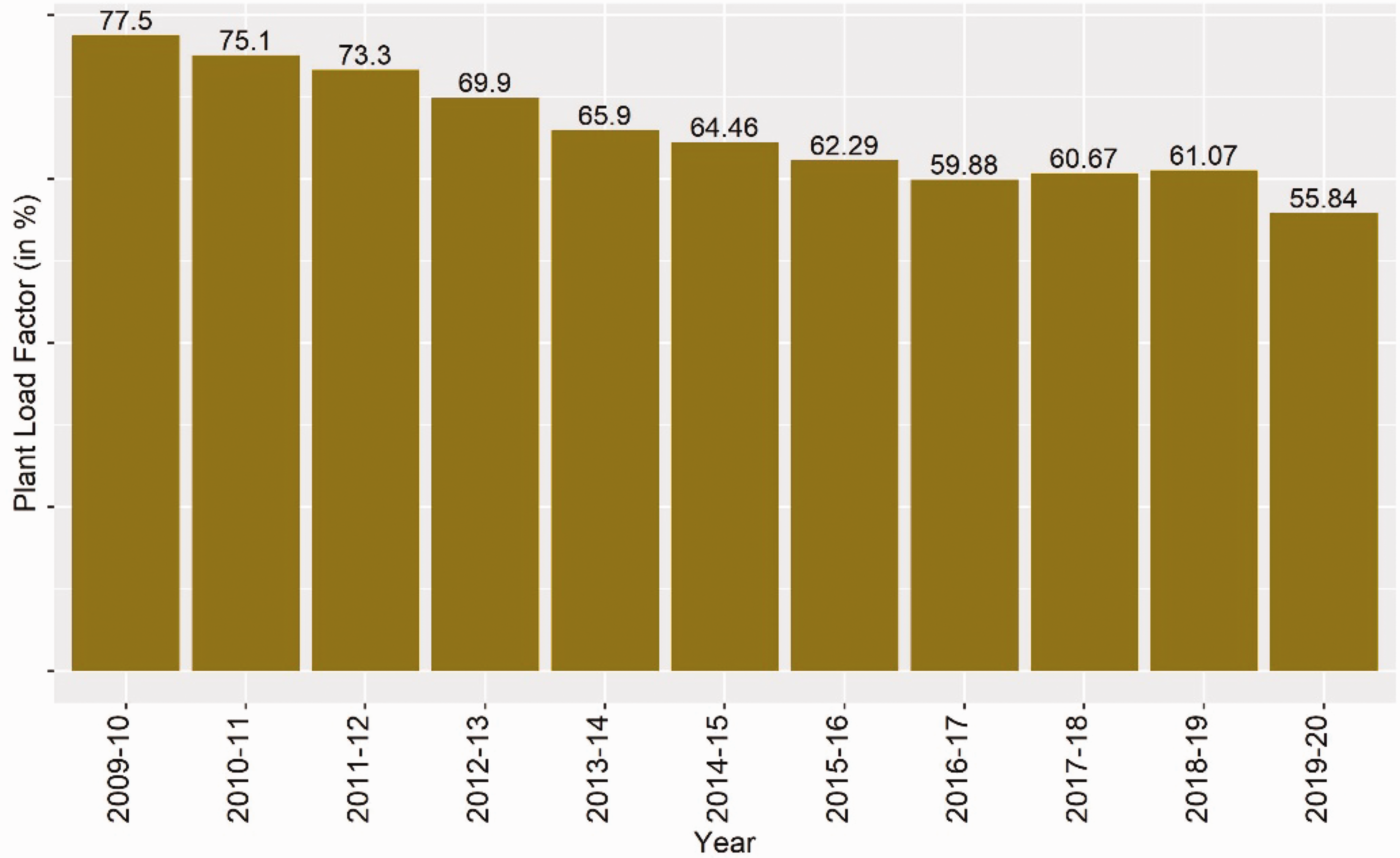

It further indicates the challenges associated with the health of the overall power sector, which is severely affected by the health of the DISCOMs. It is further aggravated by the low plant load factor (PLF) as illustrated in Figure 8. The poor health of the DISCOMs refers to lack of its financial capability, which implicates that there are no takers for all the generation capacity that is in place despite demand (see Figure 8). As of December 2019, the outstanding payments to power generators had risen to INR 74,900 crore (∼USD 10 billion), according to a report by the Institute for Energy Economics and Financial Analysis (IEEFA). 45 Moreover, DISCOMs total outstanding debt to banks and financial institutions is a massive INR 2,28,000 crore (∼ USD 31 billion) in the year 2018–19.45 These debts, coupled with lack of competition, is undermining the country's power distribution and generation sectors and hindering renewable energy investments. 45 This was one of the strong rationales behind amendments to the Electricity Bill, 2020, (see the draft Electricity (Amendment) Bill, 2020 section).

Year-on-year changes in plant load factor (PLF) of thermal power plants (Data source: CEA 14 ).

With the decreasing PLF (see Figure 8), the majority sub-critical coal power plants pose a crucial challenge in terms of an increase in fuel consumption as the sub-critical plants are primarily designed for baseload operation and are not suited to provide a ramp up and down multiple times a day. Even the commissioned super-critical coal plants need retrofitting to match ramping capabilities required for flexible operation of the power grid. The wear and tear of these super-critical plants will also go up when operated to become flexible in the process of accommodating an increase in renewable generation. 46 The higher fuel consumption of the coal power plants would result in a long-term penalty of increase wear and tear damage and reduced reliability; and in short term penalty of higher heat-rate, increased O&M cost, training requirements and equipment efficiency. 47

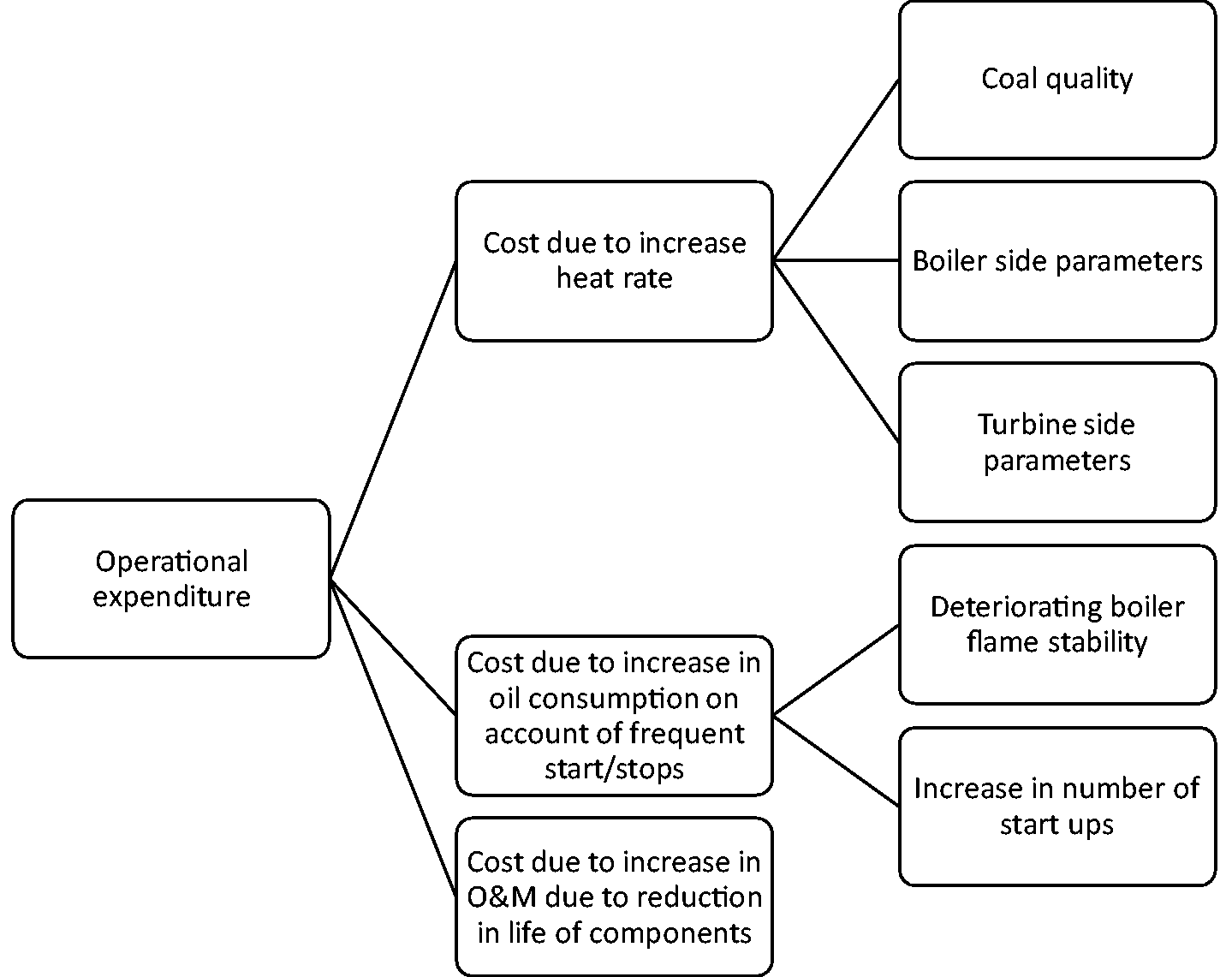

These penalties are the cost enhancements that are involved in enabling a thermal generating unit for the flexible operation that are be categorised as capital expenditure and operational expenditure.17,47 In this case, capital expenditure would be the one-time expenditure incurred to install equipment to enable them with the flexible operation: ramping capabilities and low-load operation. Currently, there is a need to change the design to operate at low technical load (a level of generation up to which coal power plant can survive stability of operation) to accommodate variable and uncertain generation output. These pose a variety of technical challenges like boiler flame stability, flame control, unburned coal and carbon monoxide (CO) emissions leading to further economic and environmental degradation. Thus, adding to the challenges of accelerated renewable transition.

The changes in design require a comprehensive technical and commercial need assessment within the regulatory framework, and also to support the new NREP as per the draft Electricity (Amendment) Bill 2020. 17 It must include capacity building requirement for the workforce, which mean paradigm-shift in training needs, awareness and change in standard O&M procedures, toolkits and working strategies (also recommended by Shrimali 23 ). It would also need a high inventory of consumable spares. This is particularly required under the accelerated RE generation conditions as the coal power plant design to provide baseload and stable output over a period of time need to frequently change its loading leading to increase in switch-on and -off frequency of the power plants. Therefore, causing further damage to the system.

In this purview, the present rate of return on equity shall be reduced by 0.25% in case of failure to achieve the ramp rate of 1% per minute. And an additional rate of return on equity of 0.25% shall be allowed for every incremental ramp rate of 1% per minute achieved over and above the ramp rate of 1% per minute, subject to a ceiling of additional rate of return on equity of 1.00%.

48

This will affect the computation of Annual Fixed Cost (AFC) of the coal power plant, which is less than the desired 1% ramp rate per minute. An example of such investment is when the furnace is at low loading conditions; the instability of fireball may lead to flame failure that will eventually lead to tripping of the coal power plant. It can be addressed by replacing the oil gun system with Plasma Ignition, and Combustion System and this technology also benefit eliminating secondary fuel requirement. The cost estimate of this system per thermal power unit is INR 7.4 Crore (∼ USD 1 million) and abandoning fuel pump station will also reduce the capital cost.

49

The funds required can be expressed as (see equation (1),

49

)

Nonetheless even if the funds are managed, additional funds will be required as the capital cost to maintain a high spare inventory which will be crucial for retrofitting the existing plants for flexibility operations. Literature suggested that rerouting of the funds collected through the ‘Coal-Cess’ can provide a viable funding option. 23 This cess is also called ‘Clean Energy Cess’ and ‘Clean Environment Cess’. In terms of carbon tax equivalent, the 2016 increase in the Clean Energy Cess translated to a carbon price of around INR 400 (∼USD 5) per tonne of carbon dioxide levied at the point of production. 50 Between 2010–11 to 2017–18 the amount collected by the government was INR 86,440 Crores (∼USD 12 billion) which was used to support the renewable development through the National Clean Energy and Environment Fund (NCEEF) rather than retrofitting the ageing coal plants. 50 Policy regulations and fiscal instruments in the management of NCEEF and optimal retirement of ageing coal power plants need to be planned to mitigate the current challenges in the Indian power system (see Table 3).

Another critical expenditure is to meet the operational expenditures incurred owing to the increase in O&M cost as well as a decreased efficiency of the coal plants. The Central Electricity Authority (CEA) suggested that it can be done by establishing relevant cost on per unit basis of the O&M requirements. 17 Since most of the plants will require strengthening of equipment, recurring consumables and accounting losses due to low load operations to make power units sustainable for cyclic operation for providing the required ramping capabilities. 17 The O&M expenditures due to flexibility in operation are illustrated in Figure 9.

Operation and Maintenance (O&M) expenditure routes due to flexible operation of coal power plants (Source: adapted from CEA 17 ).

With plants operating sub-optimally, a high secondary fuel or oil inventory needs to be maintained in with the increase in starting up of the coal power plant. The boiler and turbine side controllable parameter deviates in such a manner that it increases input coal quantity. There is a significant challenge of the deteriorating calorific value of input reaching coal power plant causes an increase in coal quantity (see Figure 9). Training workforce to meet better ramping expectations is needed that would require investment in human resource development. 17 Such policy arguments are needed in the proposed Electricity (Amendment) Bill 2020 (see the draft Electricity (Amendment) Bill, 2020 section).

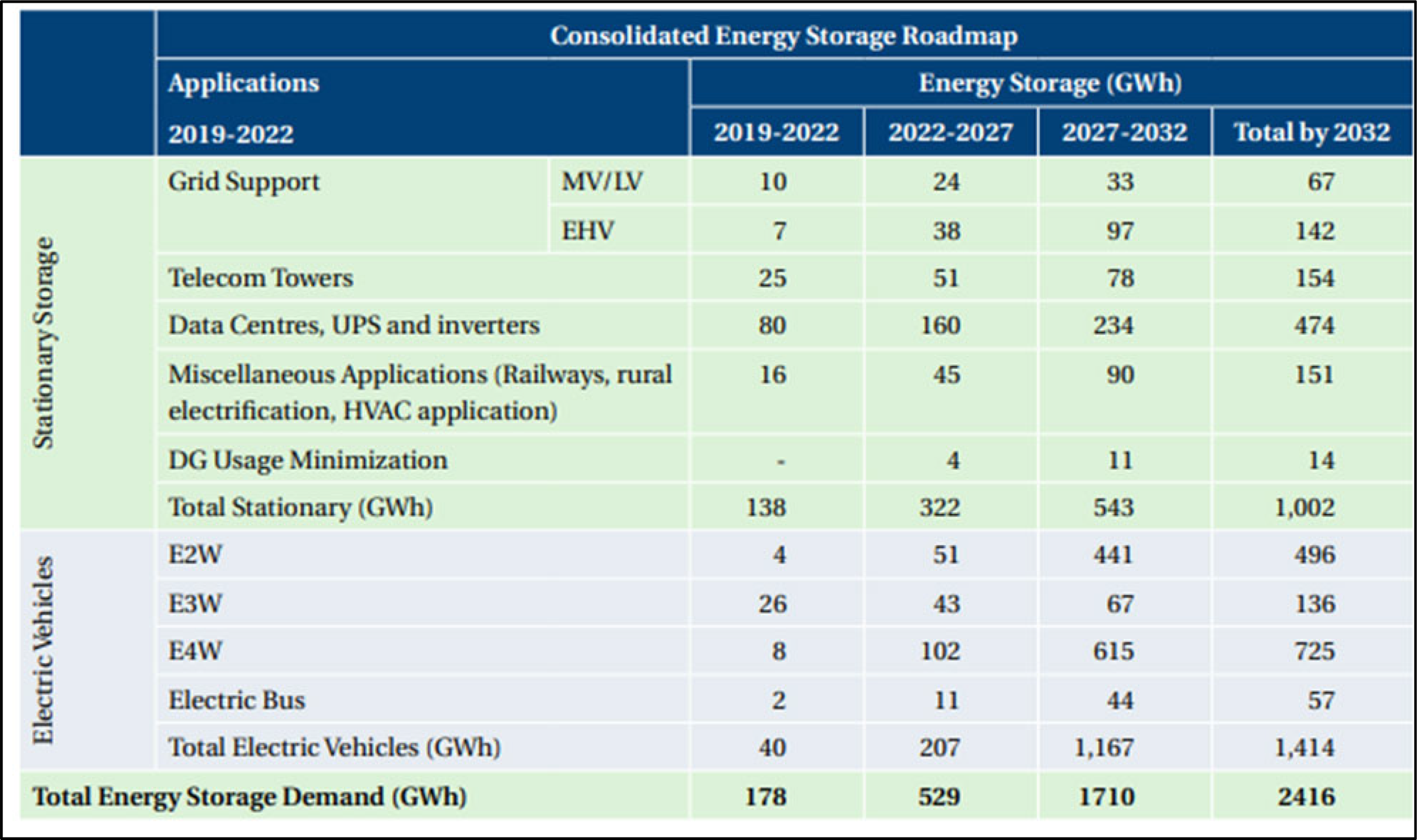

Opportunities in the accelerated RE generation scenario are envisaged through investments in battery storage technology.15,38,51 This is especially critical for easing out the variability and uncertainty of RES (also mentioned in Table 3). A recent study by the International Energy Agency (IEA) have recommended that Indian should start market reforms in the energy storage sectors so that it can cope with the grid parity and flexibility in operations for INDCs’ RES 2022 capacity fulfilment. 51 The energy storage roadmap for 2019–2032 is illustrated in Box 1. 52 This is a critical requirement for improving the health of Indian RE power system through the draft Electricity (Amendment) Bill 2020.

Cost and choices before the government

Based on the analytical framework of this study (see Figure 3), the cost analysis was performed to examine the market parity and the options of cross border trade before the government. Availability, affordability and accessibility of electricity remain a challenge to India even in 2020. These factors should be satisfied to make the integration of RES. It should have a competitive advantage and establish resilience in the supply of adequate money flows to the consumer such that they are willing to spend money on purchasing energy.9,15

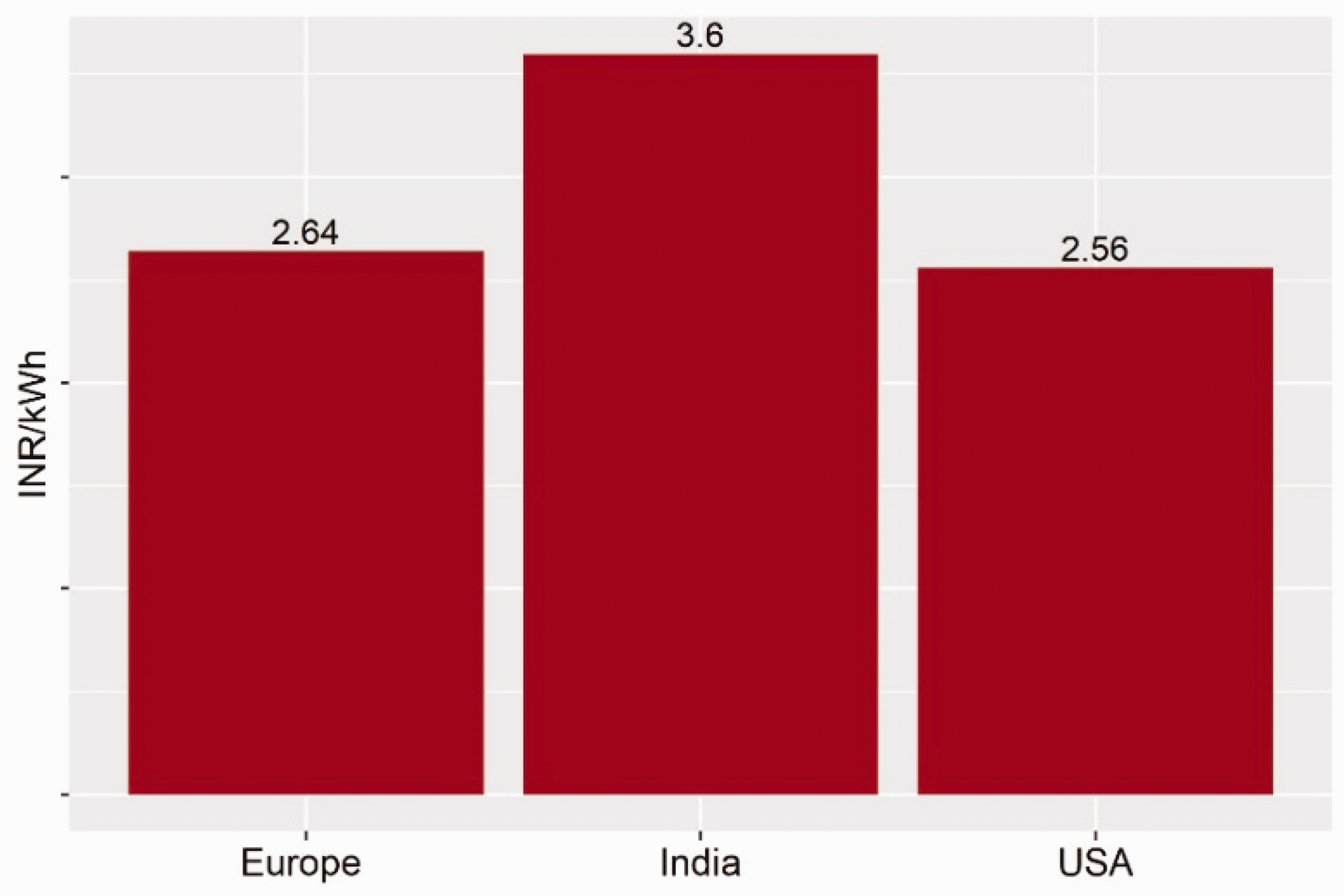

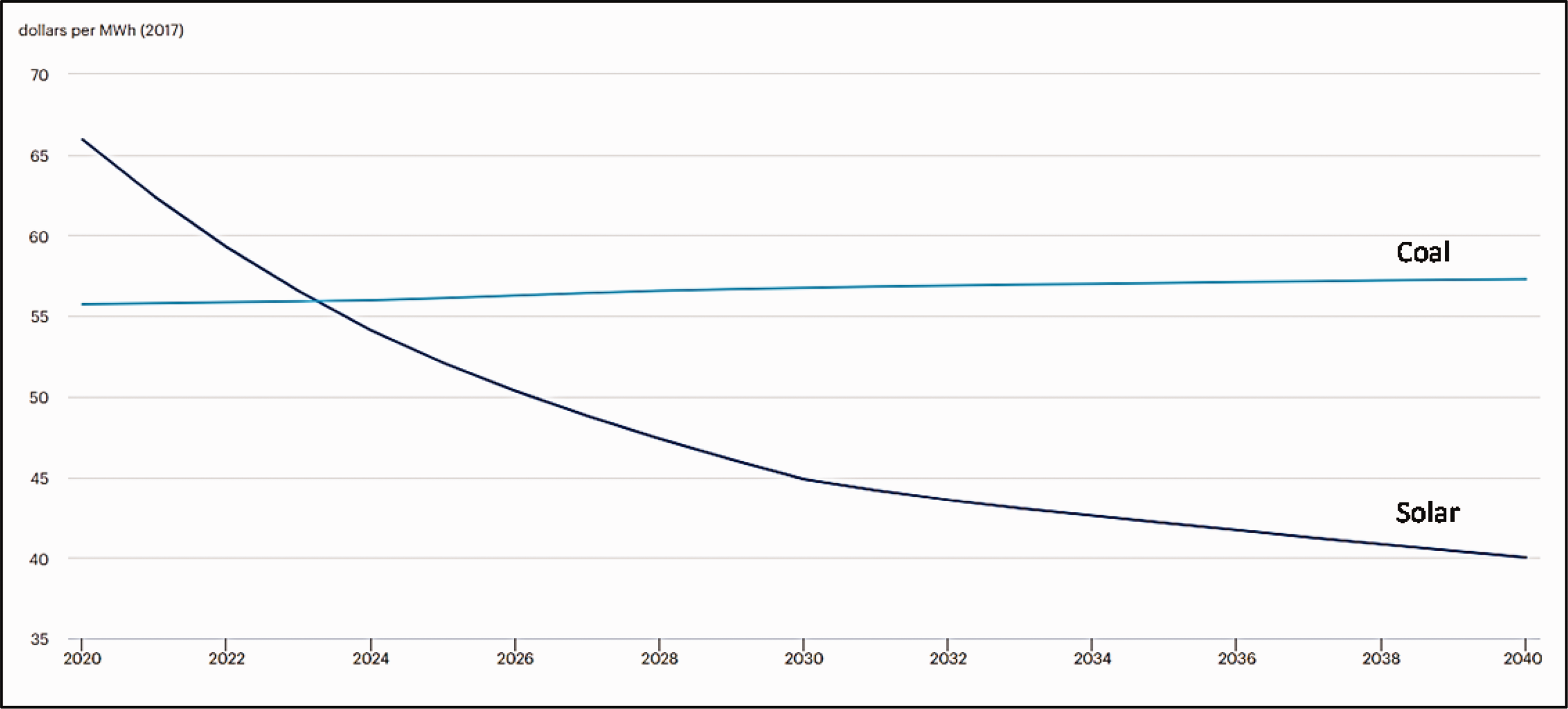

We compared the tariff of conventional fuel with renewable energy tariff and followed the IEA’s New Energy Scenario 2020–2040 pathway (see Box 2). The estimated values for 2020 are illustrated in Table 5 that shows that solar PV-driven renewable energy sources (RES) generation has a competitive market advantage in India in 2020 as compared to coal-based plants. The market parity for solar RES will be stronger in the next decade, as illustrated in Box 2.

Estimate LCOE for market parity in 2020 using IEA’s energy scenario (Source: IEA 53 ).

1 USD = 72 INR.

The second choice under consideration in this section is the cross-border trade of electricity (CBET). CBET outside the national boundary, was found to offer greater benefits as it co-creates value through daily trade activities by more efficient utilisation of resources, as a result of which power system reliability and security get enhanced. Enhancement of power system reliability and security occur as larger forces operate to meet system challenges through reserves and other ancillary services. 27 The key drivers of CBET are the difference in consumption and cost of production, optimal utilisation of resources, higher economic growth and regional integration, and seasonal complementarities. CBET can deepen the market access to the electricity consumers as RE, and conventional fuel reaches market parity. Since it optimises cost that provides cost-value attraction to neighbouring counties in their wholesale power market, where the cost of fossil or non-fossil power generation has market parity difference within INR 1 (∼USD 0.014).

India, Bangladesh and Nepal have signalled interest in increasing the commercial flow of electricity among them, which could be beneficial for the South Asia region. For India, expanding CBET mechanisms could help in integrating wind and solar, in addition to accelerating its beneficial use of Nepal’s large hydroelectric potential and Bangladesh’s GDP growth. 54 A significant barrier for India in CBET is lack of cost competitiveness of Indian electricity wholesale market. A recent study by National Renewable Energy Laboratory in USA had recommended reforms in Indian CBET strategy and regulatory framework to streamline market-based economic dispatch (MBED). 54 Under MBED, generators with a capacity not already obliged through long-term contracts would offer their power into a single, national day-ahead market. Like power markets in the USA and Europe, generators would be able to select the price of their bid for various time blocks at different quantities.54,55 It can provide a cost synergy between the markets, which is currently absent from the Indian case (see Figure 10). Also, MBED allows scheduling of generation and load dispatch in the merit of bid prices and operates flexibly within the technical restriction like powerplant’s ramp rate and thermal limits on transmission lines.

Wholesale electricity market price in India, Central West Europe and USA as per 2019 weighted average rates [Note: Assumed conversion rates 1 Euro = 80 INR, 1 USD = 70 UNR] (Source: IRENA 56 ).

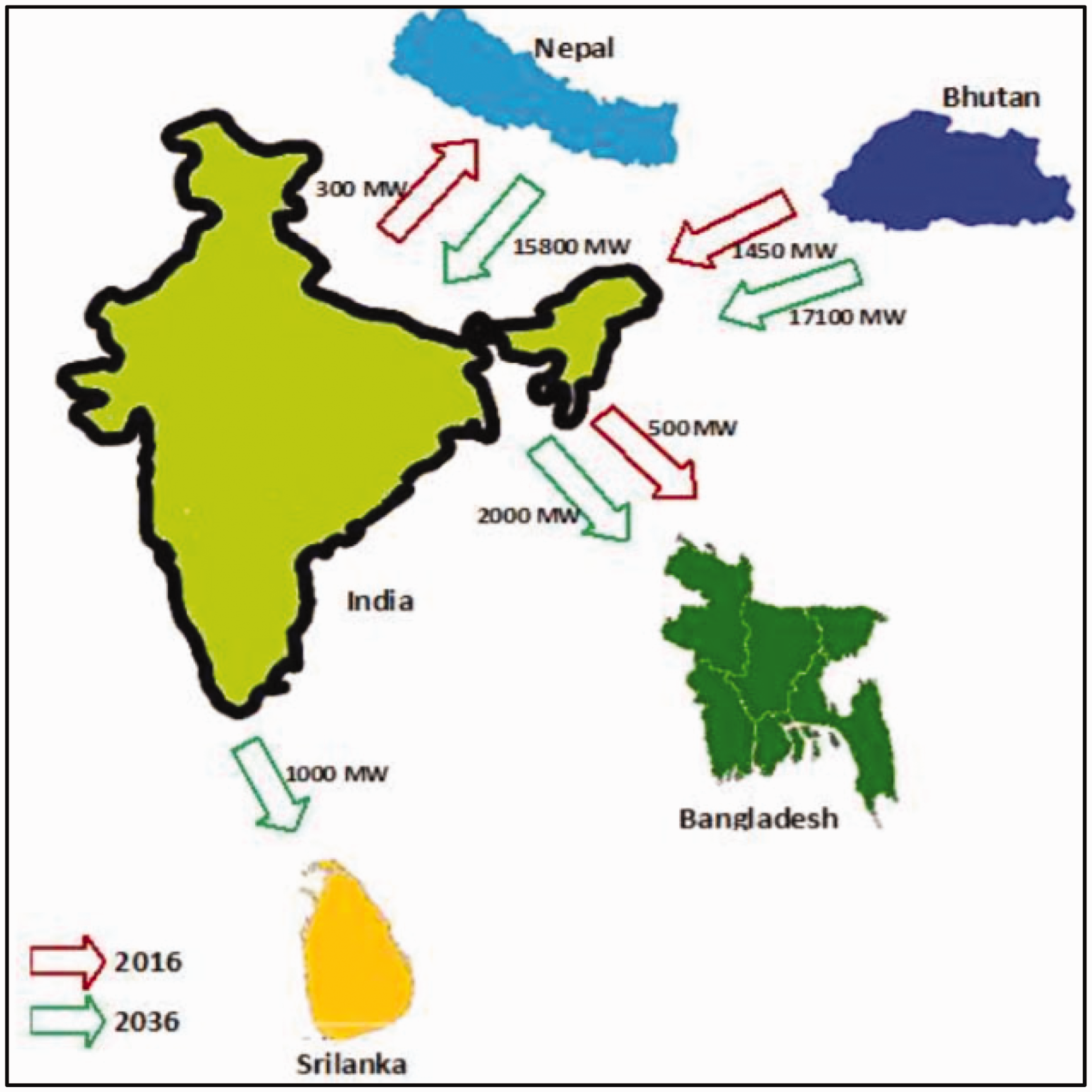

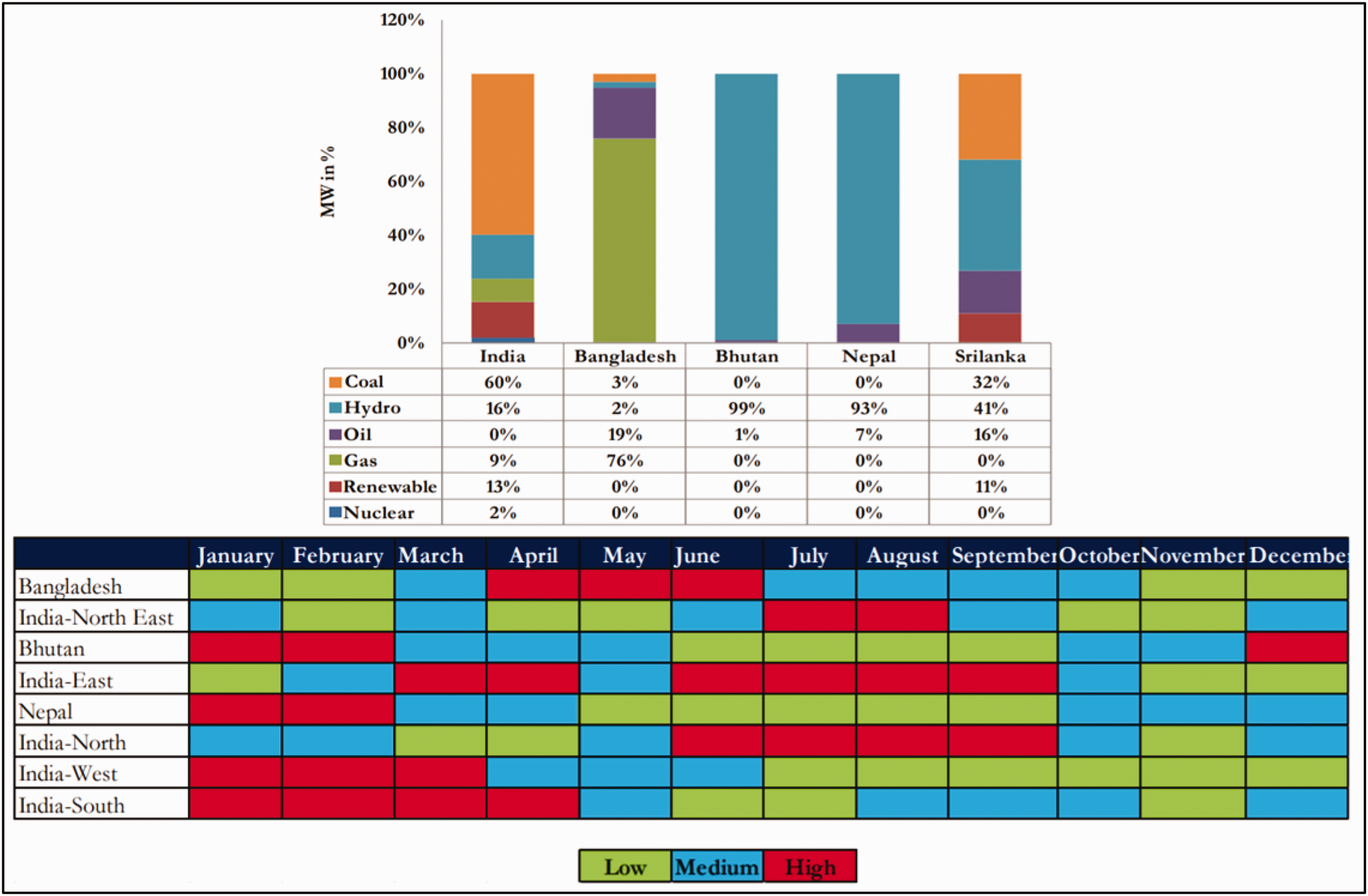

Currently, India’s power trade with its neighbours is one-sided. However, CERC estimates for 2036 showed the tremendous potential of CBET as illustrated in Box 3. India generated about 360 GW of electricity in 2019, of which 184 GW was used to meet the peak demand, and the balance of 176 GW was left utilised as a reserve capacity to provide flexibility and to balance for renewable generation (see the Overview of post-2015 challenges in the Indian Power Sector section). The South Asian CBET creates the possibility to utilise this surplus with the absorption of 92 GW of renewable generation added to the current portfolio of generation capacities by December 2022 (as per CERC 28 ). Moreover, there is a synergistic situation due to seasonality of the energy demand that can bring in mutual benefit through CBET in the neighbouring regions of India (see Box 4). The current estimation of the electrical trade potential is illustrated in Table 6.

Trade projection of cross-border electricity trade for India (Source: Authors computation from CERC 28 ).

APPC: Average Power Purchase Cost; CERC: Central Electricity Regulatory Commission.

A key policy instrument for RE trade within India are the Renewable Purchase Obligations (RPO), see Table 1. RPO mechanism is a powerful tool to balance the shortage and surplus so that the market compels the consumer to use renewable generation and hence increase in demand for electricity from renewable sources. It is the most critical policy driving renewable energy installations in India.34,57

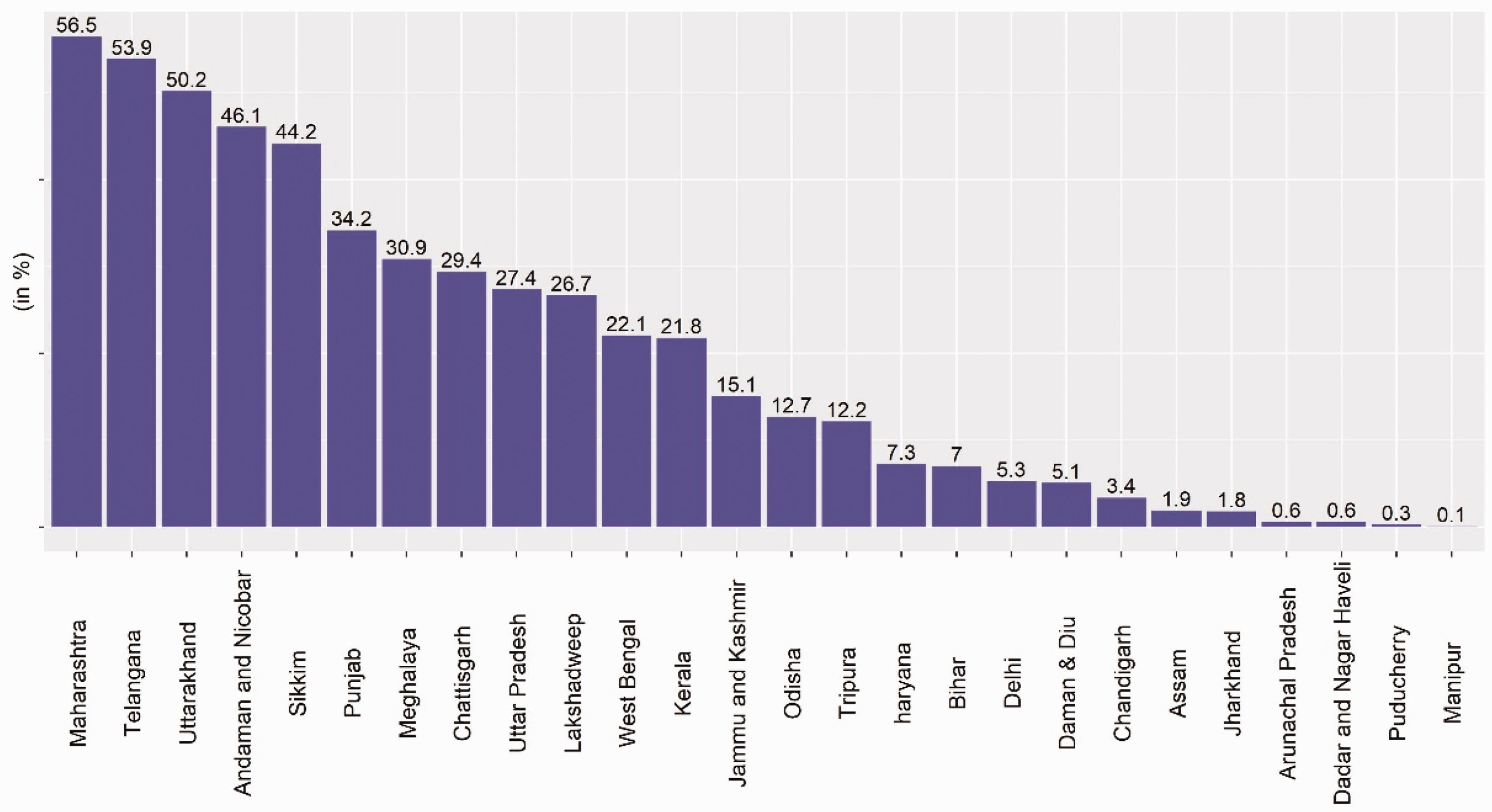

A significant challenge the RPO faces is the lack of enforcement of RPO regulations and the absence of penalties when obligations are not met. 34 The RPOs are prescribed in which a minimum fix percentage of the total consumption of electricity is purchased from renewable energy source under section 86(1)(e) of the Electricity Act, 2003.58 Furthermore, renewable energy power plants are treated as ‘must run’ power plants and are not subjected to merit order dispatch.15,58 Due to it, most of the states in India fall behind their RPOs (see Figure 11) that causes significant loss to the DISCOMs (see Table 3). The draft Electricity (amendment) Bill 2020 include some of the remedial measures to improve the robustness of the RPO.

Indian States and Union Territories with less than 60% RPO compliance in 2017-18 (Data source: Prateek 57 ).

The Ministry of Power (MoP), GoI, had set the target for FY 2019–20 solar RPO at 7.25% and non-solar RPO at 10.25%.

59

It implied that DISCOMs after due compliance can have a free hand in choosing most of the electricity supplied from fossil dominated over non-fossil dominated electricity-generating companies.

59

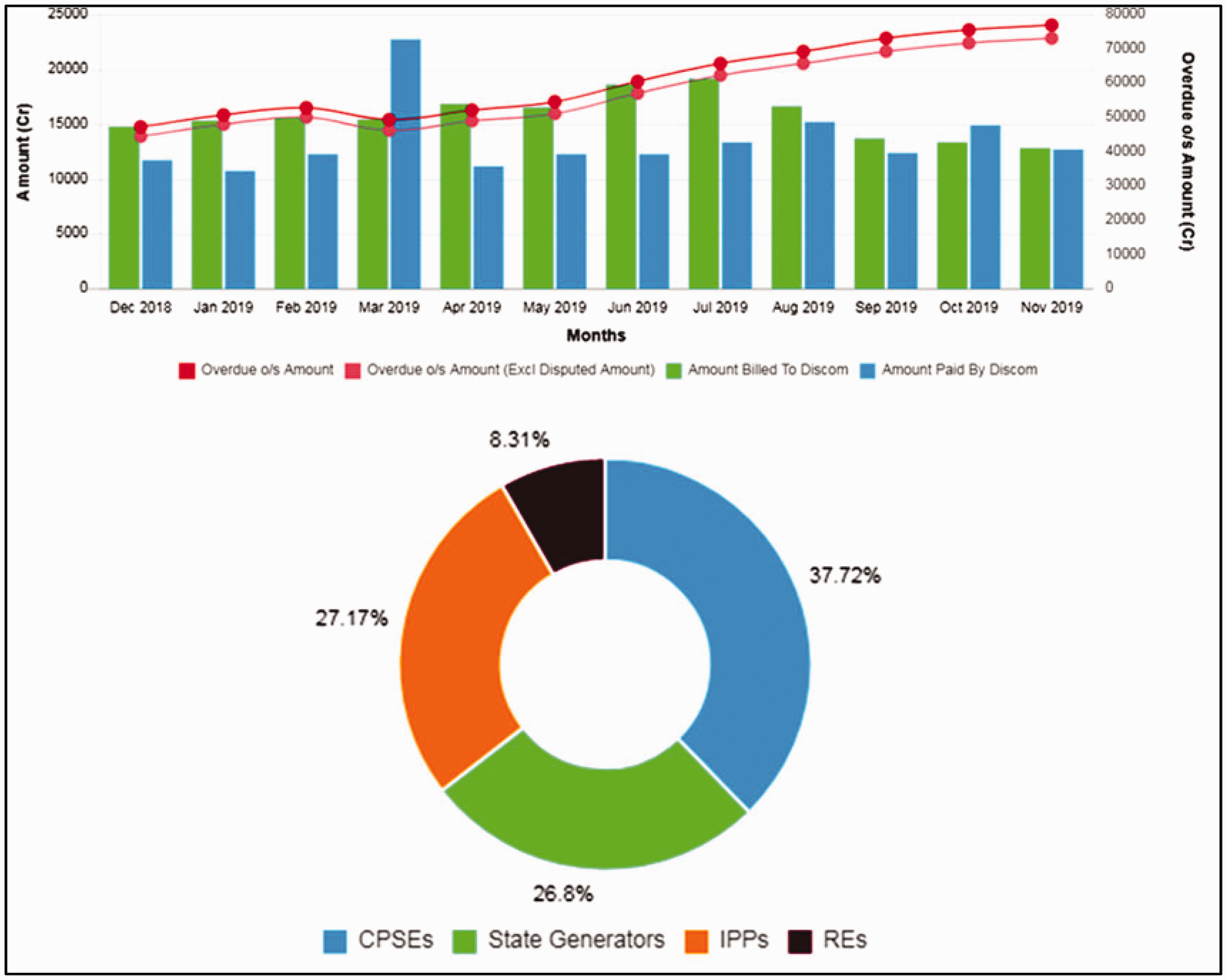

However, the RPO was non-compliant because of the INR 0.74/kWh difference in wholesale price. It is due to the amount receivable to the generating companies (see Box 5). The renewable generators’ overdue was only 8.31% and most of the overdue lie towards fossil-based generation, inefficient billing/recovery mechanism, power theft and the lack of financial strength of the DISCOMs34,57 (see Box 5). Energy storage roadmap for India 2019–32 (Source: ETEnergyWorld

52

). Levelized cost of electricity (LCOE) for solar PV and coal-fired power plants in India in the New Policies Scenario, 2020–2040 (Source: IEA

53

). Projected cross-border electricity trade in India for 2036 (Data source: CERC

28

). Energy mix and seasonality demand in the neighbouring countries of India (Source: CERC

28

). The Payment Ratification and Analysis in Power (PRAAPTI) portal of the Ministry of Power, Government of India, indicating generators overdue (Source: MoP

60

).

Promotion of RE generation through bundling of RE with conventional generation can promote the required impetus for RPOs. 34 Currently, supply remains muted, and trade volume is limited to whatever liquidity of selling bid in renewable energy certificates (REC) market in the exchange. Thud, better prices were discovered in the exchange with solar RECs price increase of 7% in October 2019 and Non-Solar RECs increase of 10% in October 2019, as compared to September 2019 rates (see Table 7). Such push in RECs prices gave necessary motivation to market forces to improve on REC trade. The shortfall of liquidity of sell bid and financial health of distribution companies (DISCOMs) were critical factors for non-compliance of the mandatory RPOs which must be addressed through strict regulatory norms in the proposed draft Electricity (Amendment) Bill, 2020.23,59

Renewable market prices on bundling with conventional sources (Source: IEX 61 ).

Social disruption due to accelerated renewable generation

The third focal point of the systematic review was to investigate the effect of the rapid increase of RE generation on the coal-dependent economy of India (see Figure 3). Here, we studied the RE expansion from the purview of social disruptions and expanded the scope of the problem from a technocratic to a socio-technical policy space. We found a significant gap of interdisciplinary literature on this aspect of rapid RE transition in the country in the Bibliometric analysis of current literature on the Indian Power System and renewable integration section (see Table 3). This section critically synthesises the long-lasting effects of rapid retirement of coal power plants on the political economy of India and calls for socio-technical planning approaches to embrace the current wave of RE transition.

With coal still being the primary energy source (see Figure 1), the economy will inevitably will get affected that will steer institutional and political changes and disrupt the ‘coal-equilibrium’.39,62 Even if the energy transition takes a few decades, the scale of the transition and its significance for regional economies should be considered in the current paradigm of ‘good’ energy policymaking. It is even more crucial to discuss now because of the plans for the new National Renewable Energy Policy (NREP) in the draft Electricity (Amendment) Act 2020.

Long-term social disruption of RE is the shift in the political and economic epistemology of the country. India built the philosophical structure of the power system on the principles of gigantism- large-scale infrastructure and monolithic institutions- that could assure economies of scale, faster electrification and centralised coordination.62,63 This approach was soon personified as an enabler to electricity as a means of welfare under the pressures from democratic politics. With each technological revolution, the emerging nation’s demand for subsidised electricity increased, especially in the agricultural and residential sector.63,64 This welfare provisioning became the backbone of the cross-subsidisation mechanism of charging over cost tariffs to industrial and commercial users. Despite causing multiple inefficiencies through price distortions, the perceived political rewards have led to cross-subsidies that today have taken a toll on the DISCOMs 62 (see in the Overview of post-2015 challenges in the Indian Power Sector section). The slowdown of the coal-powered economy due to RE generation can, therefore, have significant political impact and limits to cross-subsidies.

The poor financial health of the DISCOMS is affected by the very structure of welfare and cross-subsidies that proved unattractive to private capital. With post-2015 reforms (see Table 1), the rush to attract private generation had also displaced the careful generation planning, to match new capacity to need. Thus private generation had flourished mostly in the form of captive power plants (CPP) that caused surplus and sometimes high-cost power.9,65 This surplus power without enough well-paying customers due to broken DISCOMs had further stressed the coal power plants. 62 By 2018, about 40 GW of coal capacity were declared non-performing assets (NPAs) with an outstanding debt of Rs 1.74 trillion (∼USD 24 billion), accounting for 20% of the banking sector’s overall NPAs. 66 It had a systemic effect on the downtrend trend in plant load factor of coal powered plants (see Figure 8). It led to the creation of ‘open access’, which with the increase of renewable generation and RPOs (Figure 11) is facing regulatory inefficiencies that the draft Electricity (Amendment) Bill 2020 intends to address (see the draft Electricity (Amendment) Bill, 2020 section).

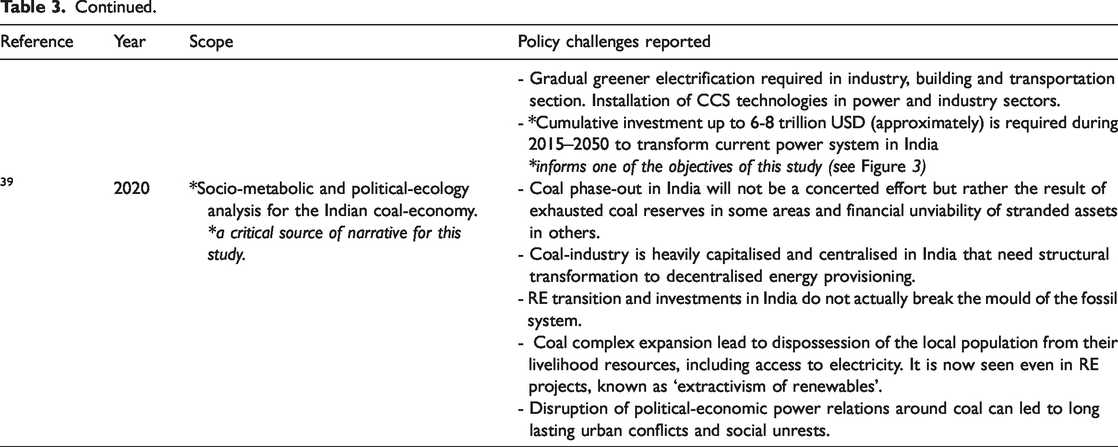

The implications of the social disruptions caused due to accelerated RE generation have three powerful ripple effects. First is the decline of the coal-dependent economy. Coal companies directly employ over half a million people and create the same number of jobs indirectly. Also, the livelihood around coal mines provides critical social infrastructure to around 10–15 million people. 39 Coal-rich states are driven by the royalties from coal mines, for example, in the Indian States of Jharkhand and Chhattisgarh, coal contributes 10% and 9%, respectively to the state economy. 29 The coal-states are predominantly poor with lower-level of industrialisation and lower GDP per capita (except Andhra Pradesh and Maharashtra), and they are not equipped to deal with this disruption.39,62 A RE-driven decline in coal also affects central government financing, especially the coal-cess or Clean Energy Cess. It will, in turn, affect investments in RE and the retrofitting efforts of the existing coal plants to improve their clean energy performance.15,23,67 Besides, coal-intensive industries like steel and washery, fertilizers and chemicals will also be impacted, that in turn, will cause loss of livelihood in millions.

Besides, the continued expansion of coal extraction in India and the rising level of imports constricts the socio-metabolic corridor for clean energy transition, making it extremely difficult to break the mould of the fossil system. 39 It systematically embeds distributive injustice in the RE project like the coal complex expansion projects, including the denial of the local population from their livelihood resources and the sustained lack of access to electricity, even at the vicinity of the project. For example, in a 113 MW Andhra Lake wind power project by Enercon in the Western Ghats of Maharashtra, the villagers who live next to the project do not have access to electricity. The project threatens also their livelihoods and rich biodiversity of the region. 68 Moreover, land is always a contested commodity and similar patterns of violence and extractivism has been observed in renewables as well. Such ‘extractivism of renewables’ can also be central to social disruptions due to accelerated generation from renewable sources in India.69–71

The second ripple effect will on the railway economy. Indian Railway (IR) is built around the same mechanism of cross-subsidisation as the Indian Power Sector. The IR is dependent on coal freight to cross-subsidise passenger freight that has high political significance, in 2016–17, 45% of passenger freight was subsidized. 72 The states who have been leaders in investing in RE are distant from coal mines and import less coal that in turn, increased the freight cost for coal. It made coal-fired electricity even less competitive than RE.15,67 Higher RE generation will further increase the coal freight costs, that will reduce the ability of Indian Railways to rely on over-charging stable coal freight to provide cheap transport for citizens. Passenger fares will have to increase at a political cost, which may reduce investments in RE or compensate with enhanced fiscal support to the already stressed railways. 62

A RE heavy power system will reduce coal and oil import dependency by increasing scope for electrification of transportation and industrial process. This has severe national security ramifications, unless India can manufacture technology indigenously. It further adds on to the Make in India and Skill India efforts of the federal government. The technology import should be reduced in an accelerated RE generation economy, and the skill shift to foster indigenous manufacturing, assembly and dissemination can mitigate part of the social disruption.9,15,23 We believe self-sufficiency in RE technology should be a core agenda for the new NREP that should be placed ahead of more aggressive decommission of the coal powered plants.

Concluding remarks

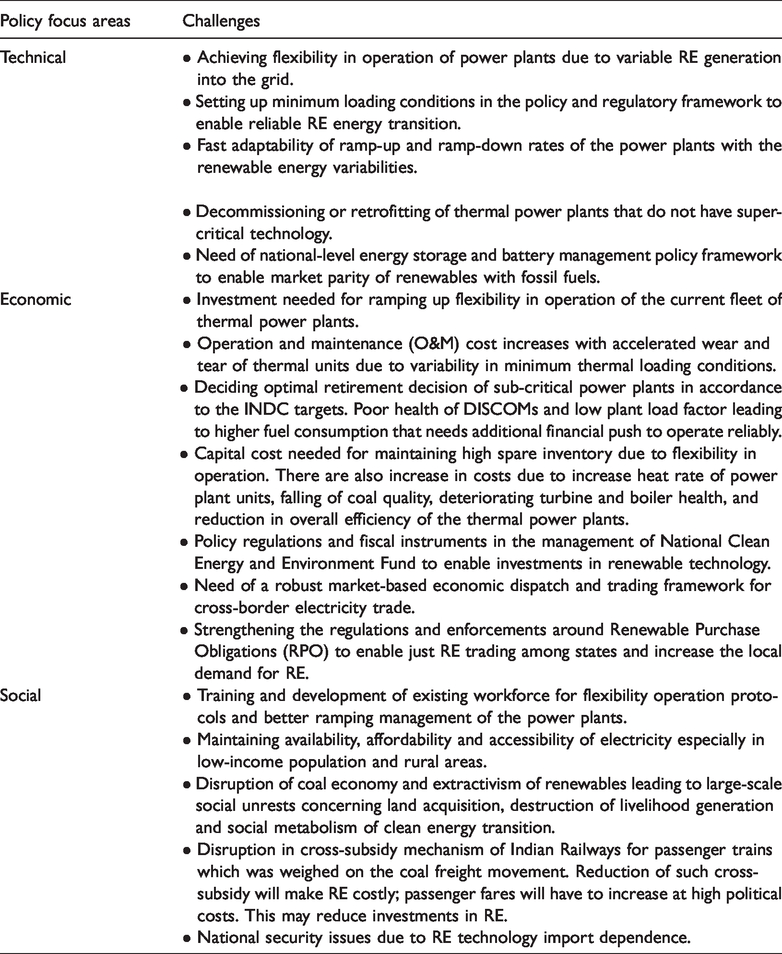

This study presented a systemic review of the challenges that the Indian Power Sector faces due to the accelerated renewable generation post-2015 reforms given its Intended Nationally Determined Contributions (INDCs). While India’s giant leap forward in pursuit of its ambitious 175 GW RE target for 2022 is laudable, the related implications of reduced generation from coal plants is a matter of grave concern. Besides producing operational and fiscal stress on the power system, this transition may also cause potential social disruptions in a predominantly coal-dependent Indian political-economy. Our systemic analysis explored three cross-sectional components of the socio-technical power system of India, such that, we could derive critical focus points for the draft Electricity (Amendment) Bill 2020 (EB 2020) that proposes a new National Renewable Energy Policy (NREP). The critical policy focus areas identified in this review are illustrated in Table 8.

Identified challenges and the policy focus areas.

The conclusion drawn are based on the ontology that the transition to RE is not merely a technological shift in India. It transposes the entire paraphernalia of power generation in terms of the highly interlocked system of technology, institutions and politics. The RE transition can also restructure the current welfarism of Indian electricity system that can alter India’s sustainable development goals. Conclusions that can be drawn from the cross-section approach of this study are:

Current state of RE transition can alter the political mechanism behind clean energy and universal access to electricity in a country like India, where about 200 million people still lacked access to electricity in 2018.5 It can also be the necessary impetus to market reforms and deleverage the state from some of its historical risks and efficiencies. However, oversight and overzealous RE dominant energy system can potentially estrange the vulnerable groups that are dependent on the coal-economy. It can potentially cause loss of livelihood and social disruption to millions of local communities dependent on direct and indirect employment provided by the Coal Industry and the Indian Railways. Moreover, from a political-economic perspective, the potential disruptions to existing cross-subsidy mechanisms may manifest in hefty political costs. Integrating these into the existing national policy framework is critical for their mitigation, lest they may snowball into bigger socio-politico-economic disruptions. This is even more significant as the country tries to lift millions of its citizen from poverty at a time when COVID-19 pandemic and lockdown puts India’s energy model at risk.

73

Cross-sectional policy implications like building resilience inflexible operation of coal plants and providing enough incentives are critical to ensure investments flows for meeting the needed operation and maintenance (O&M) expenditure of the existing coal plants. It would be extremely challenging for India to retire coal plants without investing heavily on battery storage technologies. Moreover, aggressive retirement can have severe social disruptions that can cripple the entire political economy of electricity beyond repair. Supporting this socio-technical system should be at the core of the new NREP, that can, in turn, aid policymakers to make social welfare objectives more direct and explicit. This would make it easier to foster distributive and procedural justice both at the supplier and end-user side and mitigate the social and political disruptions from RE transition. Besides, the market parity between solar Photovoltaics (PV) and coal-based generation may be utilized for providing additional revenue support to meet heightened O&M expenses of the coal power plants necessitated by flexible operation in the RE scenario. This includes capital expenditure needed for retrofit of plants to make them suitable for flexibilization and provisioning for higher spare inventory for the power plants that are frequently affected by low loading due to increase in generation from the RE. It would be beneficial on three counts. First, the health of the existing power generation system would improve significantly, making it resilient and robust to increasing RE generation. Second, it will improve the plant load factor of the coal power plants while technologically transitioning to RE. Third, the revenue generated from the RE may be used to retire unremunerative ageing coal plants and lead to clean-up the coal. Such technological complementarity for ‘clean-up’ should be supported in the proposed NREP and the EB 2020 through policy mechanism and regulatory frameworks. The assertion that half of India’s electricity will still come from coal by 2030 makes the revenue support argument for coal plants a much-needed energy justice strategy.15,23

While the Electricity (Amenedment) Bill 2020 proposed better framework for cross border electricity trade (CBET), India should avail the seasonality and economic growth impetus of the neighbouring countries to sell the surplus and generate revenues for Clean India Energy Fund (CIEF). The proposition of enhanced CBET and investments in battery storage technologies could improve the resilience of the present power system. A structural revision is needed in the CIEF for investments to flow both for RE and for flexible operation and clean-up of coal plants as well as emissions. A more substantial impetus to the ‘Make in India’ initiative should be provided to reduce technology import dependency. A critical step towards sustaining India’s energy and national security.

Indian needed necessary reforms on pricing, regulation, risk allocation and market design before the COVID 19 pandemic. The shift in the behavioural pattern at a large scale, like work-from-home, had affected the load curves. For example, the overall peak demand was down by 25% on 2 April 2020 due to lower requirements from industry and state power distribution companies (DISCOMs) across the country due to the lockdown. 74 Such a shift may cause structural changes in the Indian power system, much before the RE targets for 2022. The benefits accruing from these reforms shall far outweigh the frivolous political costs and improve the resilience of Indian electricity system.

Footnotes

Acknowledgement

An earlier version of this work was presented in Cambridge Zero Climate Change Festival 2020.75

Author’s note

Ramit Debnath is also affiliated with Renewable Integration and Secure Electricity Group, International Energy Agency, France.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Part of this study is supported by Bill and Melinda Gates Foundation through the Gates Cambridge scholarship under the grant number OPP1144 awarded to RD at the University of Cambridge and Energy Transition Small Grants 2020 by the Issac Newton Trust at University of Cambridge. Any finding, conclusion or commendations are that of the authors and do not necessarily reflect the view of the associated organisation.