Abstract

Decentralization reforms and rapid urbanization place increasing pressure on African urban authorities. In response, land-based finance has been gaining popularity within development discourses as a method of increasing local autonomy and financing local government infrastructure provision. This paper discusses the conceptual basis for land-based finance, the instruments that form part of this approach, and the actual application in several African cities. Drawing on three case studies (Addis Ababa, Harare and Nairobi) and a high-level scan of 29 developments in various African cities, we show how land-based finance is being implemented in practice and discuss the potential for wider uptake. We conclude that African city governments are using land-based financing, albeit in inconsistent ways. We argue that urban authorities should consider the more extensive and progressive use of land-based financing instruments, despite the constraints imposed by both technical and political conditions. A progressive agenda for local government finance in African cities should take land-based finance seriously, as well as the local practices and institutional arrangements through which it operates.

I. Introduction

Over recent decades, African local authorities have experienced an increase in both the scope of their responsibilities (due to decentralization reforms) and the scale of the need (largely due to urbanization). Despite the tendency of national governments to resist relinquishing responsibilities and the pervasive anti-urban bias, both the functions local authorities are meant to perform and the overall area and numbers of people they are meant to serve have grown rapidly.(1)

High levels of poverty and inequality, on the one hand, and constrained fiscal decentralization, on the other, have limited the resources available to African urban authorities to fulfil these expanding functions and to address urban growth.(2) Resources to invest in capital development (i.e. long-term infrastructure investments) have been particularly lacking. Due to the diversity of African cities, trends in income and expenditure are difficult to determine.(3) However, it is possible to point to some shared challenges. For example, African local governments often focus on operational expenses (such as salaries) and have little surplus to invest in capital; significant revenue flows are captured by national state-owned entities (such as utility companies) and are thus not reflected on local government balance sheets; direct lending to local governments for infrastructure is minimal; and local revenue collection (for example, property tax collection) tends to be inefficient and not maximized.(4) The result is that local governments remain unable to shape their own development and deliver much-needed infrastructure services.

This paper focuses on the potential for local governments to address their infrastructure needs through various forms of land-based financing. As we show in Section III, land-based financing refers to a suite of land and planning tools. Agglomeration, increasing land demand, infrastructure investments and planning decisions all drive up the value of urban land. Land-based financing is based on a recognition that property owners and developers benefit from this rising value and should be willing to pay for these gains. Using land-based financing, it is possible for local governments to marshal various instruments to capture this rising value with an eye towards long-term capital investment. They may collect revenue that they can use for urban investment, require direct investment from developers, or use the revenue stream to leverage the finance needed for larger investment projects (i.e. through borrowing). The conceptual basis of this argument is spelled out in Sections II and III. Section II outlines the argument for land-based financing in the urban African context. Section III describes the instruments and preconditions for land-based finance.

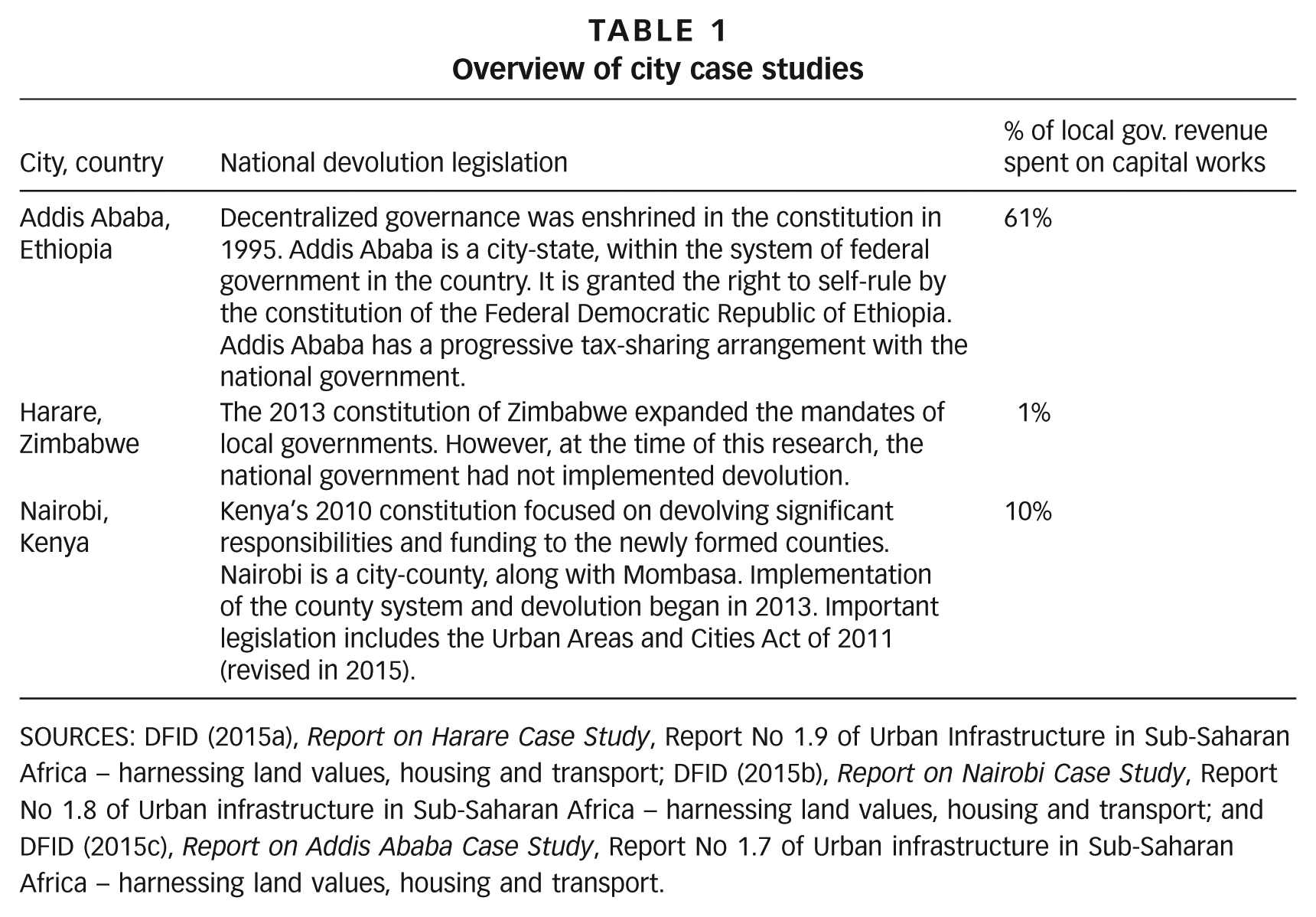

Section IV dives into the practices of land-based finance in sub-Saharan African cities. Here we recognize the divergence between theory and practice. Drawing primarily on three in-depth case studies of land-based finance in Addis Ababa, Harare and Nairobi, the real experiences of African cities are explored. In all of these cases, the local government has some duties and powers. Performing these functions requires capital and operational funding. However, the extent to which they are able to fulfil these functions varies widely, as can be seen in Table 1 (on page 3).

Overview of city case studies

SOURCES: DFID (2015a), Report on Harare Case Study, Report No 1.9 of Urban Infrastructure in Sub-Saharan Africa – harnessing land values, housing and transport; DFID (2015b), Report on Nairobi Case Study, Report No 1.8 of Urban infrastructure in Sub-Saharan Africa – harnessing land values, housing and transport; and DFID (2015c), Report on Addis Ababa Case Study, Report No 1.7 of Urban infrastructure in Sub-Saharan Africa – harnessing land values, housing and transport.

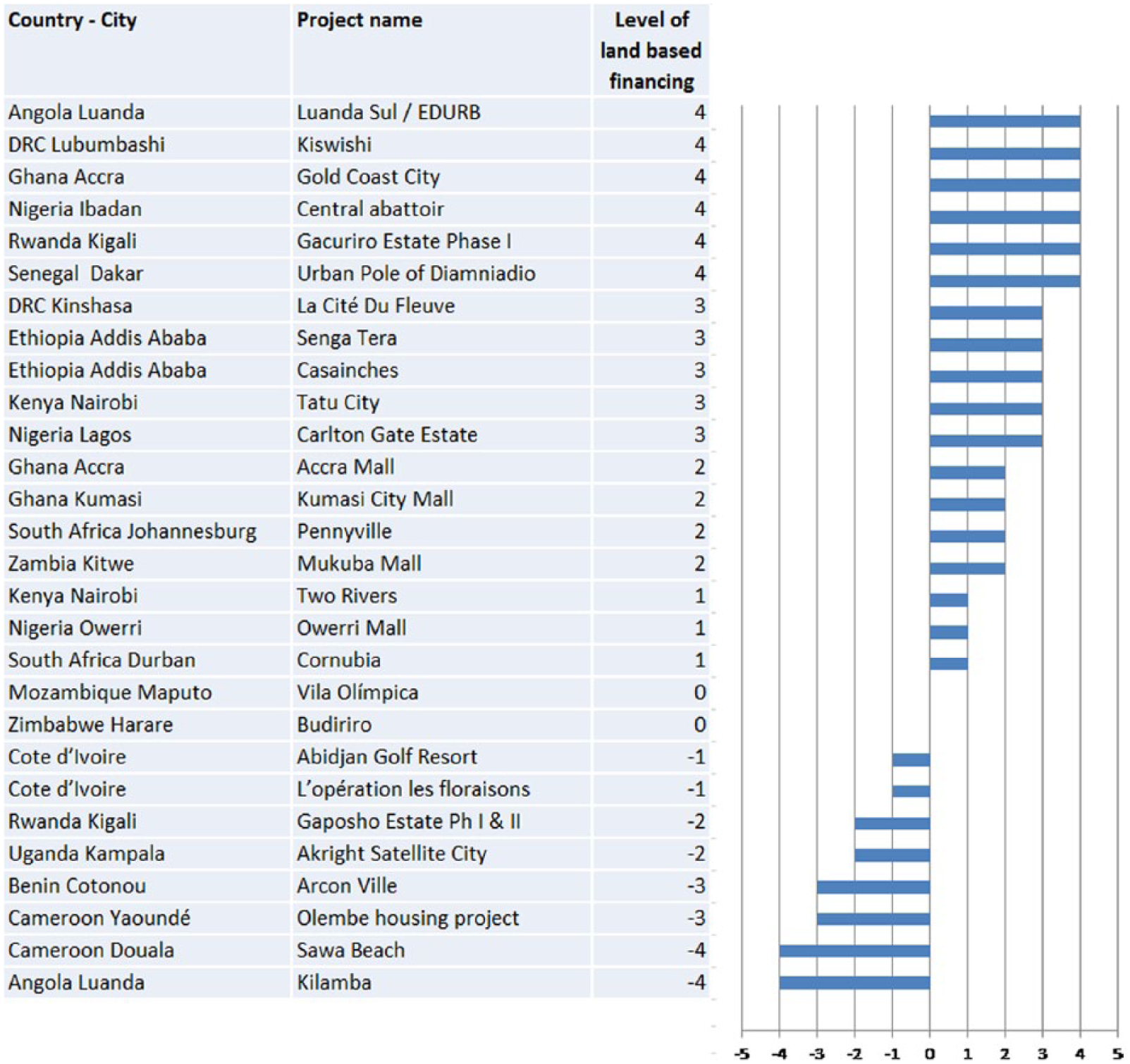

Section IV also draws on rapid assessments of 29 commercially driven land development projects in 22 of the largest cities in sub-Saharan Africa, spread across 16 countries. The countries were: Angola (Luanda Sul and Kilamba projects), Benin (Arcon Ville project), Cameroon (Sawa Beach and Olembe housing projects), Cote d’Ivoire (Abidjan Golf Resort and L’operation les floraisons), the Democratic Republic of Congo (La Cité Du Fleuve and Kiswishi projects), Ethiopia (Senga Tera Redevelopment and Casainches), Ghana (Gold Coast City, Accra Mall and Kumasi City Mall), Kenya (Tatu City and the Two Rivers project), Mozambique (Vila Olímpica), Nigeria (Owerri Mall, Central Abattoir and Carlton Gate Estate), Rwanda (Gacuriro Estate Phase 1 and Gaposho Estate Phases 1 and 2), Senegal (Urban Pole of Diamniadio), South Africa (Pennyville and Cornubia projects), Uganda (Akright Satellite City), Zambia (Mukuba Mall project) and Zimbabwe (Budiriro Housing Development). In both the in-depth case studies and the rapid assessments, the aim is to understand how and to what extent land-based financing is applied.

These data were collected by a large team of scholars and practitioners across various institutions, led by a team of associate professors from the African Centre for Cities. The authors of this paper were directly involved in data collection in the three case study cities. Data collection involved a review of legislation and policies, site visits to various projects, and between 15 and 30 interviews per case with actors in the land and finance sectors. All case studies and assessments were undertaken in 2015 as part of a project for the UK Department for International Development (DFID). A series of topical and county reports were produced as part of this project and are referenced in the bibliography of this paper.

In the concluding section of this paper (V), we argue that there is considerable scope to expand land-based finance and improve the functioning of existing tools. To do so successfully, it is important to understand the contextual issues in each country and city, particularly the political economy of land development: who decides which developments will be approved and the extent to which public funds will be used to support an approved project. Important issues include the functioning of land markets, property development, and city planning. Critically, we do not aim to position land-based finance as a panacea for African local governments’ infrastructure deficits or revenue constraints. There are undeniable technical and political constraints to easy application. Instead, we hope that this paper will encourage deeper consideration of the integral relationship among local government finance, urban land, and infrastructure provision in African cities.

II. Conceptual Framework

This section provides an argument for land-based financing in African cities. By explaining the “fiscal gap” that requires the mobilization of funds and then providing an overview of the current ways in which local governments raise money to fund infrastructure and operations, it lays out the basic vocabulary for understanding land-based finance.

a. The urban fiscal gap

Many cities in sub-Saharan Africa experience a gap between the money that is available to finance urban infrastructure and the money that is needed to meet a growing backlog in services.(5) It is difficult to estimate this fiscal gap in urban Africa. The majority of studies that look at Africa’s fiscal gaps use country-level aggregations and data.(6) They focus on national rather than urban infrastructure. However, the World Bank has attempted to address this knowledge void. According to the World Bank, addressing the need for urban infrastructure in Africa would cost between US$ 12.5 and 35 billion per year (depending on how costs are measured).(7) This estimate uses a “base cost” model, which means the real fiscal need is likely much higher. Importantly, this modelling does not differentiate between the levels of government, but aggregates the total gap regardless of responsibility.

Establishing the exact size of this gap in infrastructure or gap in local government finance is not particularly useful. Frequent references to this gap can be daunting, demoralizing, and ultimately unproductive for African urban authorities, who are already well aware of the deficits in infrastructure, services and capacity. African urban authorities are equally aware of the structural obstacles to accessing significant pots of long-term finance (for example, the high returns that investors require).(8) The urban development literature recognizes that local-level revenue mobilization has the potential to increase authorities’ ability to “internalize” the benefits of urban agglomeration,(9) shape their own urban development trajectory (which is currently being shaped by national state-owned enterprises and the private sector), and improve local service provision (including the much-needed infrastructure).(10) It is therefore more useful to consider the various ways local authorities can and do raise revenue for infrastructure, rather than focus on the hypothetical fiscal gap.

b. Mobilizing finance

A useful point of departure is to unpack the common tools used by African urban authorities to raise revenue and/or cover the costs of infrastructure. These include transfers, own-source revenue, donations and aid, and mobilizing of external service providers through partnership arrangements.

Transfers

Transfers (also known as grants) are designed to overcome the gap between the ability to raise finance (largely held by national governments) and the responsibilities that require this funding (increasingly held by local governments).(11) Transfers are generally broken down into two types: conditional and unconditional.(12) Conditional transfers come with set expenditure obligations. For example, in South Africa, the Human Settlements Development Grant is a large conditional grant transferred to provinces to provide housing subsidies. In Kenya, a range of newly developed conditional grants for health are meant to be transferred to county governments. The grant purpose (be it health, housing, bulk infrastructure, etc.) dictates what expenditures are allowed. Unconditional grants, in contrast, do not have conditions on spending and can be used by local governments for the fulfilment of their general mandates. They can be used for operational or capital expenditure, as the local authority sees fit. Conditional grants tend to be a much smaller share of transfers. For example, in FY 2015/16 Nairobi City County received 13 billion Kenyan shillings in “equitable share” and only 472 million Kenyan shillings in conditional grants.(13)

In much of Africa, transfers are vital to the operations of local governments.(14) Transfers from national governments to sub-national entities account for a large proportion of the total income of local governments. For example, Steffensen(15) shows that national transfers to Ugandan local governments accounted for nearly 90 per cent of their total income in 2003. Local governments in Ethiopia (excluding Addis Ababa) receive around 70 per cent of their income from national transfers.(16) Significantly, instead of depending on transfers, the city administration of Addis Ababa is entitled to raise income tax from its residents directly, which is in contrast to the situation elsewhere in the country, where income tax is collected nationally and then transferred to local governments.(17)

Own-source revenue

Own-source revenue is the revenue that local governments collect within their jurisdictions.(18) This includes the fees, charges and taxes imposed by the local government. A fee or user charge is directly related to the use of a service, such as water, sanitation, parking, market stall rental and the like. Charges can also be indirect. Fees and charges follow the “user pays” principle of public finance, ensuring that those who use a particular service hold the burden of sustaining it.(19) Fines operate in a similar manner and are charged to those who break particular rules and conventions (i.e. noise, parking, etc.).

In contrast to charges, a tax is a proportional payment. According to theories of decentralization, taxes that serve heavily redistributive purposes and that are movable (i.e. taxes on things that can move to capture more advantageous taxation deals) should be collected by national governments to avoid local-level competition and the movement of people and businesses. In contrast, immovable taxes (for instance, on land) are best collected by local government.(20) For this reason, property tax is seen as “good tax” for local government collection within conventional economic theory.(21) It tends to be the only “pure tax” imposed by municipalities,(22) although African cities do raise a wide variety of charges and licence fees that are often construed as taxes by citizens. Taxes, however, are generally used for the provision of public, non-divisible investments or for redistribution purposes.

In many African cities, important “tradeable services”, which are revenue generating (such as water and electricity), are not provided by local governments, but rather by utility companies. Local governments are often left with less lucrative fees and charges (slaughter permits, boda boda [motorcycle taxi] licences and the like). In addition, collecting property tax in African cities remains a challenge.(23) These realities constrain the own-source revenue-raising potential of local authorities, explaining their reliance on national transfers.

Donations

Donations (also referred to as aid) are given for the purpose of development without the need for repayment.(24) Unlike transfers or grants, donations tend to be given by organizations outside of the state. This funding can be given directly to local governments, channelled through NGOs, granted to national governments or regional bodies and subsequently released to local governments, or allocated directly for projects. Aid tends to be more prevalent in low-income African countries where there is a perceived need for development, particularly by foreign governments and NGOs. For example, South African local governments are not major recipients of donor funding, as South Africa is not a low-income county. One of the major concerns around aid is the lack of coordination among donor agencies.(25)

Funding from external service providers

In many cities, there are external service providers appointed by the city or mandated by national government to provide services. Since service providers may be able to bring in external funding such as loans and grants, this is one method that local governments can use to mobilize funding for infrastructure. There are two predominant groups of service providers: parastatal organizations, which are independent legal entities with majority ownership by national, regional or local government, and public–private partnerships, where a service provider is appointed to provide a service requiring investment in infrastructure. As the provision of capital funding is included in the arrangement, the contracts will be in the form of concessions; build, operate and transfer (BOT) financing; or similar contractual arrangements.(26)

In sub-Saharan Africa, few public–private partnerships (PPPs) provide urban infrastructure,(27) although private companies have been engaged in water supply in South Africa, Tanzania and Mozambique, with varying levels of success. However, the provision of services by parastatals is common. Water and wastewater services are commonly provided by parastatals.(28) The extent to which these parastatals can raise funds to cover infrastructure investments in cities is an important consideration. Typically, they do not have the fiscal resources to attract commercial lenders, and most funding for these entities comes from national governments, thus failing to truly broaden the range of infrastructure finance sources.(29)

III. Land-Based Financing

For local governments to fulfil their functions and shape the future of African cities, new and innovative revenue-raising instruments are needed or, alternatively, existing instruments must be more robustly deployed. Considering the limited extent to which transfers, cities’ own-source revenue and service-provider funding are currently able to fund much-needed investments in infrastructure, land-based financing becomes an important funding option.

It is important to differentiate land value capture and land-based financing, as these concepts are commonly used together in the literature. The concept of land value capture refers to a suite of instruments that allow the rising value of urban land to be leveraged by the state.(30) This capacity is further enhanced if local governments have control over urban infrastructure budgets or over planning processes (i.e. the ability to regulate development).(31) Land value capture seeks to quantify, collect and distribute the value of urban land that has risen due to state investment and regulation.(32) It is implemented through “instruments designed to tax development value that are applied through the planning system”.(33) Land-based financing refers to a broader category of financing mechanisms that include land value capture as well as contributions made by property owners or property developers, regardless of whether land values are increasing. Suzuki et al.(34) also add the important criterion that money raised through land-based finance mechanisms must be used to fund infrastructure. Crook et al.(35) characterize these instruments as “designed to raise funds from developers to help pay for the infrastructure needed, on the one hand to allow their development to go ahead or to mitigate its impact and, on the other hand simply to pay for infrastructure requirements”.

The concepts of land value capture and land-based finance have been taken up by practitioners, academics and activists in African cities who are concerned with the “social value” of urban land and equity in the urban property market.(36) This section discusses the common instruments of land-based finance and the established preconditions necessary for successful implementation.

a. Instruments

Ad-hoc contributions

Ad-hoc contributions are one-off capital contributions. Developers can make these when requested by a municipality, or when they determine that this contribution is a prerequisite to the development being viable. These contributions can be in-kind and/or financial in nature. In-kind contributions refer to cases where the developer of a project builds additional infrastructure in exchange for the approval of their application. In-kind contributions tend not to refer to the internal infrastructure of a project, as it is common practice for this to be provided by the developer. Instead, they refer to the provision of connector infrastructure, bulk infrastructure, or social and economic infrastructure that might, theoretically, be provided by a local authority. A local authority can also require that property owners within an area that is impacted by a project assist in paying for the infrastructure. This is generally done before the investment occurs so that the finance can be available for the project.(37)

Sale of development rights

Development rights are valuable. When these rights are granted, the value of land is increased. Local authorities can sell development rights to developers. For example, the right to convert rural land to urban land, to increase densities, or to convert residential land to commercial land increases the value of that land.(38) Like the contributions discussed above, the sale of development rights is a one-off transaction. The sale of development rights is an effective way to raise funding for infrastructure, in particular when there is rapidly increasing demand for urban development.

Impact fees and development charges

Impact fees and development charges (terms often used interchangeably in the literature) are one-off capital contributions made by the developer.(39) This charge is designed to cover the costs of the bulk and connector infrastructure associated with the development. A consistent and transparent formula is required for calculating the impact that the development will have on the infrastructure network (thus differentiating these fees from ad-hoc contributions).(40) This instrument has the positive effect of avoiding individual negotiations associated with each property development and mitigating the potential for nepotism or corruption. It also calls on the local authority to ideally ringfence the monies received, either by type of infrastructure service or by service delivery zone, so that the developer has some sense that they will receive the benefit that the payment was intended to cover.

Public land leasing and land sales

Most public authorities own some urban land. This land can be leased or sold to raise revenue for infrastructure provision.(41) For land-sale and land-lease options, the state must have control over a large supply of land (such as in Addis Ababa or Luanda). A proactive urban authority, with the requisite financial resources and technical capacity, can also land bank (such as has been done in many South African cities). This refers to buying up land in areas where it will become more valuable over time (for example, in urban expansion areas or where there will be high levels of infrastructure investment in the future). The purchase of land around a new development (such as a highway or train station), and the subsequent resale of that land by the public sector or relevant authority, is a method to capture some of the gains that an infrastructure investment creates.(42)

Land readjustment

Land readjustment is a tool whereby landowners who own property adjacent to one another pool their land together for reconfiguration and reconstruction. Often, landowners surrender a portion of their land in exchange for infrastructure, or to raise funds to defray infrastructure costs. Some of the land may also be sold to generate additional funding and some may be contributed towards streets and parks.(43)

Betterment levies/taxes

A betterment levy is a tax or charge levied on a specific group of properties. It should be based on some measurable feature of the property (such as frontage or area). The tax is based on the projected increase in the value of the property resulting from the investment in public infrastructure that the state has made or will make.(44) Betterment levies have proved successful in Latin America.(45)

Property taxes and property tax surcharges

Property tax is the most basic and commonly applied form of land-based finance for local governments. A property tax is a recurrent tax levied on property by the local government.(46) There are various ways this can be calculated, including a flat rate, an area rate or a value rate, levied on the land, the property or both.(47) In some situations, a property tax surcharge can be levied. Like the betterment levy, a surcharge may be applied in some areas or situations – for instance, if the property is in a business improvement district or receiving benefits from a public investment.(48) Rates can only be seen as an infrastructure financing measure when the operating account is in surplus, which is rarely the case in African cities, and the extra funds available are directed to infrastructure investment or intended for servicing loans or repaying bonds.

Tax increment financing (TIF)

TIF is a tool that allows municipalities to borrow money to promote economic development and then to earmark property tax revenue from increases in assessed values within a designated TIF district for repayment of the loan.(49) This is generally undertaken through issuing a bond or bonds to cover the cost of the infrastructure. There is some debate as to whether a TIF is a land-based financing tool. However, since a TIF allows for property tax revenue to be invested in infrastructure, it is useful to consider here.(50)

b. Conditions for land-based finance

According to the urban public finance literature, there are several enabling conditions that allow land-based financing to contribute to local government revenue generation and infrastructure provision.(51) Without these preconditions being met, it is difficult for the tools discussed above to work well. Considering these preconditions is important for grounding the study of land-based finance, recognizing the limits of these tools, and preventing the inappropriate or universal application of these instruments.

Demand for property

A prerequisite for land-based financing is a sufficient and (ideally) growing demand for urban land and land development. Without this growing demand, and thus increasing land value, there is nothing for the state to capture.(52) In addition, without this demand there will be much more resistance to charges and taxes being imposed on landowners and property developers. Obviously, the need for rising land values creates a challenge for local governments in Africa, as rising land values tend to exclude the poor.(53)

Supply of property

To meet the growing demand for urban land, there must be a flexible supply of urban land. This requires available land that can be utilized for development, active developers (either public or private) to develop this land and bring it to market, and sufficient funding to support the developments.(54) This includes both development finance and end-user finance. Without a responsive supply, increasingly demand will result in the growth of informal development and speculation as the constrained supply pushes up the prices of the available land and property.

Effective and supported local government

The different land-based financing tools require local governments to be capacitated in different ways. Overall, to implement land-based financing, it is necessary to have a supportive national fiscal framework that gives local government the right to collect revenue or enter into contracts to support service provision.(55) There must also be the political will at the local level to implement this financing model, given that taxation is never politically popular. There must be the skills and capacity to implement it uniformly and transparently. Finally, a functional planning system (including a city-wide plan for regulation of land and future development) to guide decision-making is important.(56) Without a functional plan, it is difficult to charge for additional development rights or ascertain where future land value increases will be.

Willing land owners and developers

The limited opportunities for investment in African cities make urban real estate an attractive asset class for local, global and diaspora investors.(57) On the back of this investment, many larger African cities have a growing class of postcolonial landlords.(58) Land-based financing shifts the costs of urban development from the (more general) taxpayer to the landowner. Evidence from studies of property tax reform in Africa shows that efforts to ensure that landowners contribute to the costs of urban development are, unsurprisingly, resisted.(59) This is particularly true in cases where landowners do not feel they are going to see the benefit of payment. The ability of landowning elites to sway the decision-making apparatus of the state away from such land-based financing methods as increased property tax is well-documented.(60) One of the conditions for effectively implementing land-based finance is a weak class of landholding elites. If land elites are well connected to politicians or effectively mobilized among themselves, land-based financing will be more difficult. It is of course possible to align the interests of landholders and developers with the land-based finance agenda; however, this requires a deep understanding of the incentives that these actors respond to, particularly in the medium to long term.

IV. Land-Based Financing In African Cities

It is important to ground the study of land-based finance in the experiences of African cities. This section draws on such experiences from each of the case study cities – Addis Ababa, Harare and Nairobi – as well as from the multi-project study. It looks at: the conditions for land-based finance in African cities (based on conditions spelled out above); the current application of various instruments; and the outcomes and implications of this application. Terminology in this section is aligned with the interviews in each place (with the more conventional terms in brackets).

a. Conditions for land-based financing

Addis Ababa

Important preconditions for land-based finance are in place in Addis Ababa. There is demand for urban land and a strong local government, supported by well-developed fiscal legislation. The fact that all land is state owned offers additional scope. Addis Ababa’s largest constraint is on the supply side.(61) Land can only be released for development once the state has serviced it, and the limited capacity of the state constrains land release. Moreover, much of the unserviced land, which could be used for development, is occupied in peri-urban areas by small-scale farmers, and within the urban fabric by informal settlements. While people whose land is taken for development purposes are compensated for their (generally very modest) structures, they have little say in the process. Increasingly, amidst growing popular opposition, the Ethiopian authorities’ approach to removing occupants from land for development has proved to be practically difficult and politically costly.

Harare

Harare has few of the prerequisites for land-based financing. Because access to finance is so constrained by the national economic downturn, the demand for land development is relatively limited. On the supply side, Harare does have a seasoned and resilient development sector.(62) However, the challenge of accessing development finance prevents the expansion of supply and demand. In addition, the reluctant embrace of devolution by the national government (in no small part aided by the tensions of opposition politics) creates little room for manoeuvre for the local government. In addition, there are notably inconsistent and often anti-poor applications of land and planning regulations.(63) The provision of infrastructure services (and thus the collection of revenue from users of services such as water, electricity and roads) has been shifted from the city to national agencies, which further undermines Harare’s capacity to implement land-based financing effectively.

Nairobi

Nairobi has some of the preconditions in place for land-based financing. There is a rapidly increasing demand for urban land and a responsive supply. The 2013 devolution process has created opportunities for strengthening and empowering the newly established Nairobi City County. However, land remains highly contested and politicized; the relationship among landholding elites, local bureaucrats and politicians is complex. Whether the will exists to systematically and transparently capture urban land value for investment in urban infrastructure remains unknown.

b. Current application of land-based financing instruments

Addis Ababa

All land is publicly owned in Addis Ababa – owned by the national government but managed by the Addis Ababa City Administration. The state leases serviced land in the city to developers and public institutions. Land leasing is the major form of formal land supply and of land-based finance. It takes two forms: direct allocation and auction.

Harare

Harare implements a basic form of land-based financing, with measures intended to support new infrastructure provision and the maintenance of the existing and extensive network, which is managed by the city:

Nairobi

Nairobi shows a similar pattern to Harare. There are several forms of land-based finance here. These include:

29 projects study

As noted in the methodology section, the 29 studies of individual projects are high-level rapid assessments. Figure 1 (on page 14) rates each project on a scale from -5 to 5 based on a set of criteria. A rating of 0 indicates that there was no land-based financing. In most cases the land-based financing rating is positive, indicating that developers contributed to bulk and connector infrastructure in some way.

Ratings of 29 land-based financing projects in sub-Saharan Africa

In most cases these contributions took the form of in-kind contributions whereby the developers constructed the bulk infrastructure themselves. It is notable that none of the case studies scored a 5, which is the point at which the developer contributes to social and community infrastructure and cross-subsidizes low-income areas as well. At the opposite end of the spectrum, a number of West African case studies indicate subsidization of the developer (Cote d’Ivoire, Benin and Cameroon, as well as Angola in Southern Africa).

c. Outcomes and implications

Addis Ababa

The scale of urban renewal in Addis Ababa has been extraordinary, made possible by state ownership of the land, complemented by the country’s land-leasing system. But there are also downsides to the system in Ethiopia,(71) and more work is needed to ascertain how well it is functioning, given the context and specificity. According to Goodfellow,(72) around 6 per cent of the total revenue of Addis Ababa comes from land leasing. Since land can only be released for allocation or auction once it is serviced, a firm (albeit slow) cycle of collection and investment has been established. However, despite having the financial resources, there is limited technical and professional capacity to service urban land. The insufficient supply of urban land results in incredibly high prices and, consequently, the formation of informal settlements on unserviced areas.(73)

The case of Addis Ababa suggests that state control of land has the potential to shape city development in positive ways. However, matching demand and supply requires state capacity as well as resources. In short, it is not just about money, but also about state operations. In addition, the manner of clearing already occupied land for formal land supply has to be fair and legitimate. In Ethiopia, the occupants of land that is taken to be leased to developers are seldom willing participants in the process, because the compensation offered to them is very low.

This type of land-based financing has limited application beyond Ethiopia, mostly because it requires that the land be owned by the state and that the state and city have a high degree of control over the way the land is allocated for lease.

Harare

The contribution of land-based finance – other than property taxes – in Harare is limited. While the prescribed percentage of new land developments is routinely collected, it remains small. Between US$ 500,000 and 1 million is collected annually from these endowments.(74) There are two main reasons for this. The first is that developers in Harare struggle to access the long-term infrastructure or end-user finance necessary for large developments. This is largely due to macroeconomic conditions. Secondly, Harare does not ringfence the funds it collects from developers. This funding goes into the city’s operating account, rather than a capital account, and is spent on salaries or general operations.

Implementing land-based finance is a challenge in Harare. The city’s weak financial position and the fuzzy nature of devolution make land-based financing instruments difficult to implement. In addition, because many key infrastructure services are provided by national state-owned enterprises, the city is unable to raise land-based finance to cover the costs of this infrastructure. Moreover, much of the unchecked peri-urban development cannot be leveraged by the city through land-based financing, as the peri-urban land cooperatives that drive these developments do not need to make the same contributions as urban land developers.(75)

Nairobi

Nairobi has implemented land-based finance with a model similar to that in Harare. The charges and contributions are not ringfenced. While around 6 per cent of the 2013/14 county revenue came from plan approval, planning and building fees, it is not possible to ascertain how much of this was raised through the infrastructure contribution. Nor is this money allocated for infrastructure; according to local officials, it is lumped in with the operating budget and spent on salaries and other recurrent expenses. The in-kind contribution is not issued in a uniform or systematic manner, making it highly contested and easy to “avoid”.(76) It appears to be implemented in an ad-hoc way, allowing for individual officials to decide the extent of necessary contribution. Importantly, Nairobi has done little to curb rampant speculation in urban land markets or to capture the value of the large-scale investments by national state-owned enterprises (such as the Thika Superhighway). In Nairobi, land and corruption are tightly intertwined, although counter-efforts are growing.(77) The vested interests of unchecked property markets are apparent and undermine the political will for value capture.

29 projects study

The multi-project study shows many cases where some form of land-based finance is taking place. However, it is likely that the bulk and connector infrastructure provided through in-kind contributions are being driven by the immediate needs of property development for both on-site and off-site infrastructure, and may not be part of a redistributive framework of strengthening local government. This could result in pockets of infrastructure provision for the wealthy, with fewer services for the poor.(78) This would clearly undermine the more progressive intent of land-based financing efforts.

V. Discussion and Conclusions

Decentralization processes implemented across Africa have radically expanded the responsibilities of local governments. The fiscal and capacity pressures increasingly faced by African local governments are felt most acutely in growing urban areas, where the need to deliver and the tensions between levels of government are most evident.

This paper argues that land-based financing offers a suite of instruments that could be deployed by local governments to overcome some of the challenges of infrastructure finance and provision. These instruments can be used in different ways and they produce different outcomes. Land-based financing can be used to supplement the existing income streams of local governments, increasing the ability of urban authorities to capture the urban dividend and benefit from the growth of cities.

The empirical research presented in this paper shows that land-based financing is being deployed by some African cities, but to a limited extent. In most cases, the focus is on in-kind contributions made by the developer. This includes the installation of connector and (sometimes) bulk infrastructure needed for their projects to access services. In some cases, these investments serve the wider public; however, the general trend is for developers to contribute only infrastructure that serves their project. In both Nairobi and Harare, notably, developer charges do exist; however, without this funding being ringfenced for capital expenditure, it has little impact on infrastructure provision. In contrast, Addis Ababa is able to use its land-leasing system to raise substantial revenue for infrastructure provision. The high levels of local government empowerment, coupled with the state’s full ownership of land, provides the unique conditions for this.

Additionally, the 29 projects studied reinforce a recognition of the limited and inconsistent application of land-based finance. For some projects, developers have contributed significantly to the infrastructure pool, yet in others, the state has heavily subsidized these developments, raising significant concerns. On the one hand, there is the argument that subsidies should be reserved for servicing land for housing of the poorest citizens. The counterargument is that the state should promote economic development through subsidizing what are often “flagship” property developments. The risk in the latter case is that the state ends up subsidizing property developments that have neither demonstrated financial viability nor targeted the needs of poor citizens, either because of poor market information or undue influence on the decision-making process by vested interests.

The diverse nature of cities militates against a one-size-fits-all approach to land-based financing. As African cities continue to grow, there is a dire need for innovative and locally driven experimentation with land-based financing instruments. These experiments will need to balance the desire to attract economic development, on the one hand, with the fiscal sustainability of local government and the equitable provision of urban infrastructure on the other. They will require in-depth and targeted analysis of the interplay among urban land market forces, urban land governance and local political economic arrangements. In addition, these experiments will need to move beyond the fixation on the quantity of money that local governments have available (i.e. the finance gap), and consider the best infrastructure finance arrangements and configurations for these cities. If this is done, it will open real opportunities for cities to change current urban development trajectories, as well as demonstrate a clearer picture of local government’s role in changing the ways in which urban growth is financed and managed.

Footnotes

Acknowledgements

Special thanks to researchers Tsigereda Tafesse, Innocent Chirisa, Brendon van Niekerk, Brandon Finn and Peter Ngau, all of whom were integral parts of the DFID-funded research team. Special thanks to Diana Mitlin and the anonymous reviewers, who offered invaluable suggestions.

Funding

This document is an output from a project funded by the UK Department for International Development (DFID) for the benefit of developing countries. However, the views expressed and information contained in it are not necessarily those of, or endorsed by, DFID, which can accept no responsibility for such views or information or for any reliance placed on them. This article is also based on work undertaken for the African Centre for Cities’ CityLab Programme. This is part of Mistra Urban Futures, which is mainly funded by Mistra (the Swedish Foundation for Strategic Environmental Research) and Sida (the Swedish International Development Cooperation Agency).