Abstract

This paper describes how the Asian Coalition for Community Action (ACCA) programme seeks to use finance to augment community-driven development processes in 19 nations and enable their scaling up to the city and national levels. The lack of accessible and flexible finance is a key stumbling block for the majority of community development processes in Asia. The paper begins by examining how this programme approaches the issue of finance in the wider context of community-driven upgrading, and elaborates the role that community networks can play in encouraging collective activities. It then explains how community finance leads to the establishment of community development funds (CDFs), financial platforms made up of contributions from different sources, including community savings, ACCA seed funds and contributions from local/national government or other actors. These both encourage collaboration and increase the scale of what can be done. The paper gives examples of how CDFs can operate at different levels: locally, between groups of communities with shared problems and goals; on a citywide scale (107 citywide funds are now in operation); or at a national level, as in the Philippines, Cambodia and Sri Lanka.

I. Introduction

Imagine a glass vase filled with pebbles, each pebble representing an urban poor community. Although the pebbles are close together, the vital link that binds them is missing. If a large rock is placed in the vase, it will just sit on top and push the pebbles down, unable to connect the pebbles or reach those at the bottom. If instead, a liquid is poured into the vase, it will filter into all the small gaps and bind the pebbles together. The large rock represents the existing systems of formal commercial and development finance, top-down and unmoving, unable to reach those most in need. The liquid represents alternative community-driven financial mechanisms, reaching all those who need it and acting as a bond. One challenge for development is to facilitate the development and implementation of these alternative forms of finance, and this is a challenge that the Asian Coalition for Community Action (ACCA) programme of the Asian Coalition for Housing Rights (ACHR) seeks to meet.

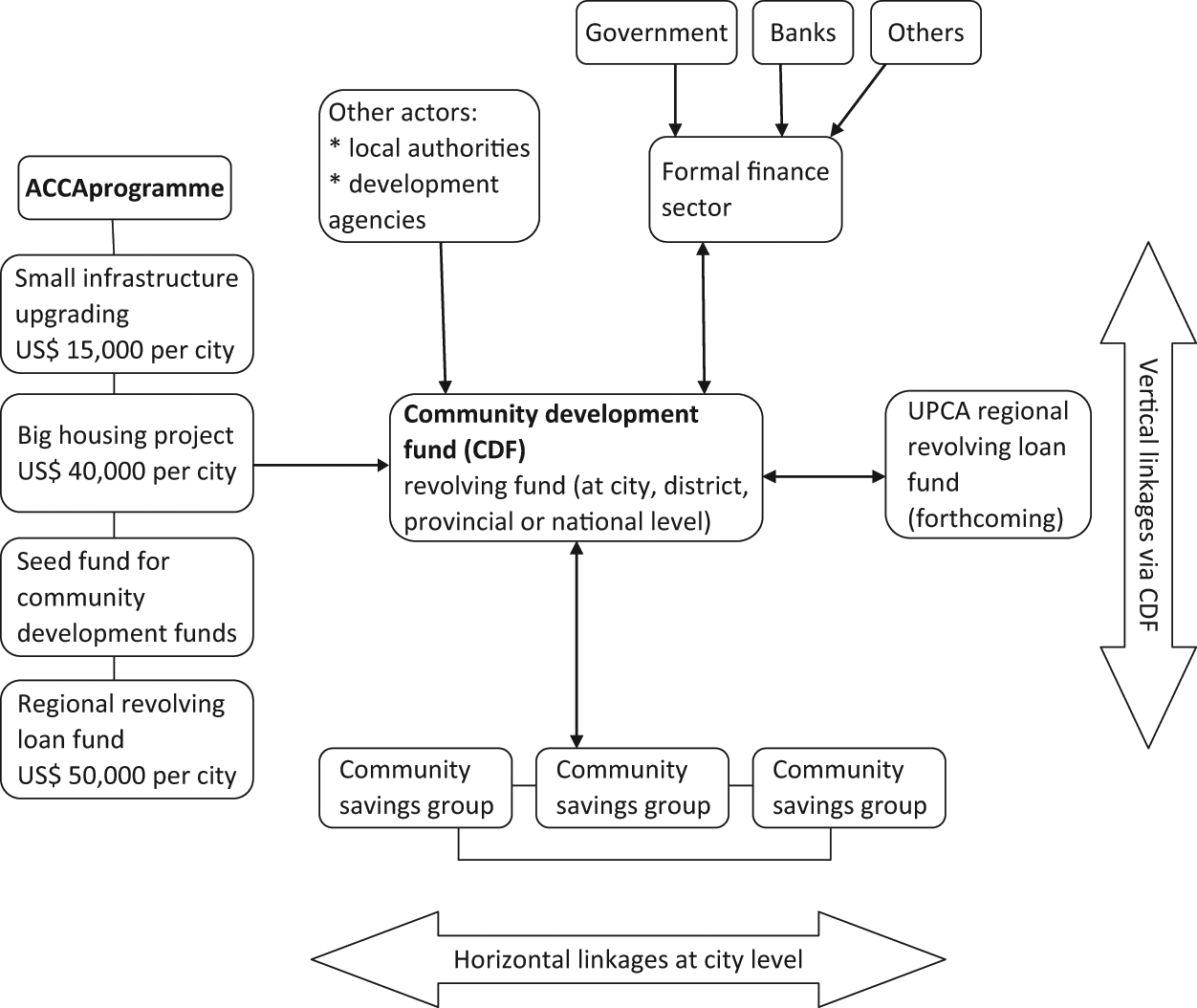

The lack of accessible and flexible finance constrains community development processes in Asia. Moreover, when secured, formal finance systems are not appropriate for low-income households, increasing their vulnerability. The ACCA programme seeks to address this need, using financial mechanisms as a way of linking people together, by providing small amounts of funding to pre-existing community groups and supporting their upgrading and housing projects. ACCA also provides seed funds to emerging community development funds (CDFs), which take the concept of pooling resources beyond individual community savings groups to the city, provincial or national scale, allowing more ambitious projects to be carried out. Crucially, CDFs are a mechanism for encouraging collaboration with other stakeholders, who can contribute to the funds and thus provide a measure of institutionalization to community processes while allowing the poor to retain control of the management of these funds. The flexibility and diversity offered by this approach is a crucial part of development that meets the needs of the poor and that can be sustained.

II. Financial Mechanisms for Community-Driven Development

The ACCA programme is designed to address the need for flexible finance that can be accessed and used by the urban poor as an instrument for development. The programme enables ACHR members to adapt this finance to suit the particular social, legal and political context of their country. First, ACCA processes may be used to strengthen the existing community finance systems, bringing together scattered savings groups into a city level CDF and therefore enabling new possible uses of savings, such as infrastructure and housing. Second, linked savings groups can have a positive political influence, building new political relationships at the city level and beyond, catalyzing a financial system to support community-driven development. The linking process builds a mechanism of checks and balances for the various savings groups, which are no longer operating in isolation, and can also broaden savings groups to include more members.

Third, for some ACHR members, ACCA creates new funding possibilities, offering grants (more recently augmented by loans) to enable the capitalization of revolving funds. As explained in the paper by Somsook Boonyabancha and Diana Mitlin,(1) ACCA grants are available for two main purposes, namely networking and projects. The project monies can be used to capitalize CDFs, which can help to build relationships between different communities to prioritize key action areas in their city. The projects also provide communities with the opportunity to deliver concrete action of direct benefit to community people, thus linking them together and increasing savings membership for larger funds. ACCA small project funds of US$ 15,000 per city for at least five infrastructure projects, and ACCA big project funds of US$ 40,000 per city for housing improvement or construction projects, both have to pass through a city level CDF rather than going directly to the community. This allows other urban poor communities to see the visible changes arising from the use of the revolving loan fund and motivates them to invest in its management and expansion. Fourth, the CDF facilitates relationships between the community groups and other agencies, helping to build a platform for partnership. These platforms can function at different levels: community, city, district and, sometimes, national.

The ACCA programme as a linking mechanism

A fifth and equally important component, especially for the future of development, is to create bridges between the community financial mechanisms, such as CDFs, and the existing formal finance system, as this is where the bulk of funding lies. The communities are building valuable financial platforms to increase the support available to them; ACCA’s design anticipates that if these platforms are effective and financially robust, then city funds will be able to link with sources of formal finance. The formal finance sector, as a fairly rigid system, is more suited to dealing with a wholesale system through such a platform rather than with individuals; management will be undertaken by the platform committee, giving the finance providers confidence that they will receive repayments.

Thus, the ACCA programme has sought to design a financial tool that can be used to strengthen existing community finance systems, such as savings groups, and draw in new people through activities such as citywide surveys, leading to the establishment of neighbourhood funds and then city-based CDFs. In some cases these have already been established, and then ACCA augments the funds with additional resources to enable them to consider undertaking projects for housing and infrastructure.

III. Collective Mechanisms for Concrete Change on the Ground

It is undeniable that access to finance can be difficult for the urban poor. They usually do not have the means to access formal sources of finance, such as salary pay slips, a legally registered house to serve as capital or even the necessary documents to open a bank account. Often, if someone is in urgent need of funds, they will have to turn to an informal money lender, who in many cases charges usurious rates of interest.

The establishment of savings groups is a first step out of the financial rut. Community level savings groups are usually established with some goal in mind, such as to provide funds for emergency loans or revolving loans for income-generating activities.(2) When there is a wider range of financial tools to hand – such as the ACCA block grant of US$ 15,000 per city for five or more small infrastructure upgrading projects that passes through the city level development fund (CDF) – more possibilities open themselves up to the communities, although there needs to be a citywide process of discussion and prioritizing regarding the use of these funds. As such, it is often better (but not a requirement) when the local neighbourhoods already have established savings groups – as they have the skills to manage finance and often will elect to use the grant money as a revolving fund, although others use it as project grants. Existing savings groups will have an established asset base and more possibilities for pulling in non-members, as everyone benefits from the implemented project, for example a walkway or water supply system. In practice, the implementation of the upgrading project and managing the funds involved follow different models of financial mechanism, such as methods for drawing in government contributions, or the decision to allocate half of the funds as grants and half as loans.

In conjunction with the savings groups, community networks are a necessary component of the ACCA programme, as ACCA projects are a people’s tool for developing collective community processes. ACCA seeks to catalyze communities to organize themselves and implement a collective, community-wide upgrading project. If urban poor communities, so often excluded from formal sources of finance,(3) can build up their own funding system, which they manage according to their needs, then they create many further possibilities. ACCA takes finance a step beyond savings groups, although they remain a vital building block.

Implementing the small infrastructure projects draws in more community people to actively participate, leading to a bigger membership of savings groups and funds and, crucially, the confidence to move forward and link settlements through city activities. This small project can serve as the incentive to keep community savings and collective activities going, as the community can see a visible impact arising from their savings. Allowing everyone within the savings group to have access to the loan is a demonstration of trust; including all community members in the project is a way of giving them a chance to participate, however small or large their income. Thus, small projects serve as a bridging development mechanism, leading not only to more financial savings but also to accumulated trust and confidence. It is up to the community groups to deal with all aspects of managing the loan, from ensuring group guarantees, monthly meetings and collecting repayments, to helping those facing financial difficulties. This is finance that really adapts itself to the context on the ground. Available finance will grow with gains in confidence and trust, while trust grows as more projects are implemented, creating a virtuous cycle. Often, the poor have to pay more for services such as water and electricity than those with higher incomes, but by being organized as a group they can lower these payments and at the same time continually draw in more resources for development by increasing membership and hence savings. It is in this way that small projects and community funds at the neighbourhood level can make a basic fundamental change at the community level.(4)

Crucially, by addressing infrastructure problems themselves, communities are also drawing local authorities into the process, through showing them how community members are capable of implementing projects and that they (the authorities) may also want to play a part in this. When the local authorities see local communities carrying out projects that should be the remit of the government, this can encourage them to make a contribution or continue the project. One example comes from Davao, in the Philippines, where the community undertook a project to build an 18-metre sea wall with ACCA support; as a result of this, the local government extended the sea wall themselves as well as paving the road alongside. When the authorities saw the community members constructing the wall, it served as a polite reminder that this should actually be their job, and so the authorities managed to find funds to lengthen the wall. This opened up the ground for further coordination and interaction. The availability of finance is closely tied to the issue of improving political relationships and partnerships for change in cities, as cities can use cooperation positively. A walkway built with US$ 500 of ACCA support is actually an investment that goes far beyond the original sum, as the community will find other ways of meeting the costs, which in itself is a form of development. The provision of financial support harnesses the survival skills of the urban poor and puts them to use in a planned and productive manner with collective benefits.

Another example of the change in relationships brought about by ACCA projects is the Nong Duang Thung community in Vientiane, Lao PDR, the ACCA first pilot project and community housing project in the country. ACCA’s project money passed via the district level savings group, which allowed the district-wide mechanism to be brought in to facilitate development and assist in successful land negotiations in the country’s first case of squatters being granted a long-term lease on publicly owned land. Faced with the threat of eviction by the government, on whose land they were squatting, the community developed an upgrading project with the help of community architects to survey and map the settlement, expand the savings group to include all 84 households and develop a re-blocking plan.(5) Only a few houses had to be shifted to realign the lane and bring in a water supply, drainage and electricity. With a budget of US$ 40,000 from ACCA, the community agreed that US$ 10,000 should be used as a grant for infrastructure upgrading, while the remaining US$ 30,000 would be revolved for housing improvement loans. In order for funds to revolve more quickly and reach a larger number of households, it was decided that loans should be kept small and repaid within six months, up to a maximum of US$ 500. The interest rate was set at eight per cent, of which four per cent stays in the community savings group and four per cent goes back to the district CDF for the district level welfare fund and to increase the lending capital in the CDF. The community has, within a few years, been able to secure tenure, sit on a committee with local officials, improve infrastructure, renovate houses and still have funds available in the city CDF for residents in their community and other urban poor communities in the district to take out further loans for home improvement.

The community savings and credit movement has quickly taken off in Lao PDR since its inception in 2002 in a joint project between ACHR, CODI(6) and the Lao Women’s Union (LWU).(7) Initially started in rural areas, the savings groups are expanding into urban areas, and there are now more than 532 savings groups in 22 cities and districts with collective savings of US$ 16 million between 104,000 members. Many villages have 100 per cent savings membership. ACCA has opened up possibilities for communities to use their savings funds beyond income-generating loans for infrastructure and housing, which is especially important now that Laotian cities are attracting foreign investment, putting increasing pressure on the land for the poor.

The ACCA process in Lao PDR is different to that in other countries in that each of the 22 districts received US$ 7,000 as a grant for small projects, in order to nurture all district level processes. Each of the 22 districts has a CDF that is managed through a joint committee, including a savings group representative from the community, a community representative from the sub-district level and a Lao Women’s Union representative. There is also a national fund under the Lao Women’s Union, which in 2011 totalled 600 million kip (US$ 75,300). The savings movement is now increasing beyond the scale of LWU, leading to some differences in administrative processes, and so a constructive solution has been mutually agreed upon to decentralize the central fund to the district level. This will allow the district funds to retain government recognition while allowing continued and unlimited growth; and the extensive scale of savings in Lao PDR really makes CDFs a part of the local system.

IV. From Savings Groups to Community Development Funds – Taking Community Finance to Scale

Savings processes are an essential part of getting communities to organize as a collective and to identify and recognize the issues that the different members of the savings group may face. However, the activities of savings groups in terms of upgrading and other projects are limited by the size of the savings amassed, which are usually insufficient to extend much beyond small loans for livelihoods or emergencies, or possibly house repairs. To achieve larger-scale improvements, communities must look beyond their own savings groups, and community networks play a role in linking different groups facing similar situations. The solution may come through forming larger-scale revolving funds, to which all the involved communities are party – these funds are known as community development funds (CDFs) and they may operate at different levels: the district level, city level, provincially or even nationally. City level CDFs are facilitated by the requirement that ACCA funds for housing projects should not go directly to the community but instead, should be managed through a CDF. This injection of money puts the city CDF in the spotlight and encourages contributions from communities and other actors. Thus, the ACCA programme facilitated the creation of city level funds such as in Bharatpur and Biratnagar in Nepal, both of which received government contributions, as well as the creation of funds in Myanmar, Indonesia and Mongolia. In cases of countries that already had existing funds, the ACCA contribution adds strength to the fund – such as in the Philippines, Lao PDR and Sri Lanka. In Sri Lanka, where many communities have savers who are part of the Women’s Bank, the ACCA process has helped to broaden Women’s Bank membership to all members of a community rather than scattered households, as well as create linkages between the various groups at city and national levels.

It is not necessary or common for each savings group to pool all its savings into the CDF – instead, each community may choose to make a contribution, which gives them a stake in the CDF and thus the right to obtain a loan from it, while still maintaining their community level savings groups for smaller-scale revolving loans. For example in Cambodia, which has provincial level CDFs, each savings group keeps 40 per cent of its savings at the CDF level while the communities decide what remaining proportion of savings should be kept in the community’s control, for example as contingency funds in case of emergencies.(8) The CDFs are managed by committees comprised of community representatives and chaired by a local authority representative in an advisory role. This provincial level fund helps strengthen and sustain community processes and partnerships on a local level. Cambodia also has a national level fund, the Urban Poor Development Fund (UPDF), which allows loans to go to communities that are not yet part of any city or provincial fund.

The ACCA project has contributed to the development of CDFs by providing seed funds, infrastructure grants and housing loans. CDFs serve as the institutionalization of community processes, beyond small-scale, individualized community processes to large-scale, citywide development processes incorporating multiple different stakeholders, from community members to government officials and others, such as academics and NGOs. As a Thai community leader explained:

“We are not building these city funds just so that we can get access to some money. When we build our city development fund, we are building a financial system for the future, for our families, our children and for every poor person in the city. We are building a financial system to change our lives.”(9)

Funds are a stepping stone for addressing difficult issues such as land, for which communities need negotiating tools and need to get the authorities on their side.

CDFs, as financial networks, create both horizontal and vertical links: horizontally between savings groups in a city and different cities in a country, and vertically between poor communities and local and national governments. CDFs require a strong community network if they are to operate effectively with government officials and other possible partners. The CDF committee functions as a joint management committee, bringing together key city actors; even if the local authority has not contributed financially to the CDF, it may play an advisory role and sit on the committee.

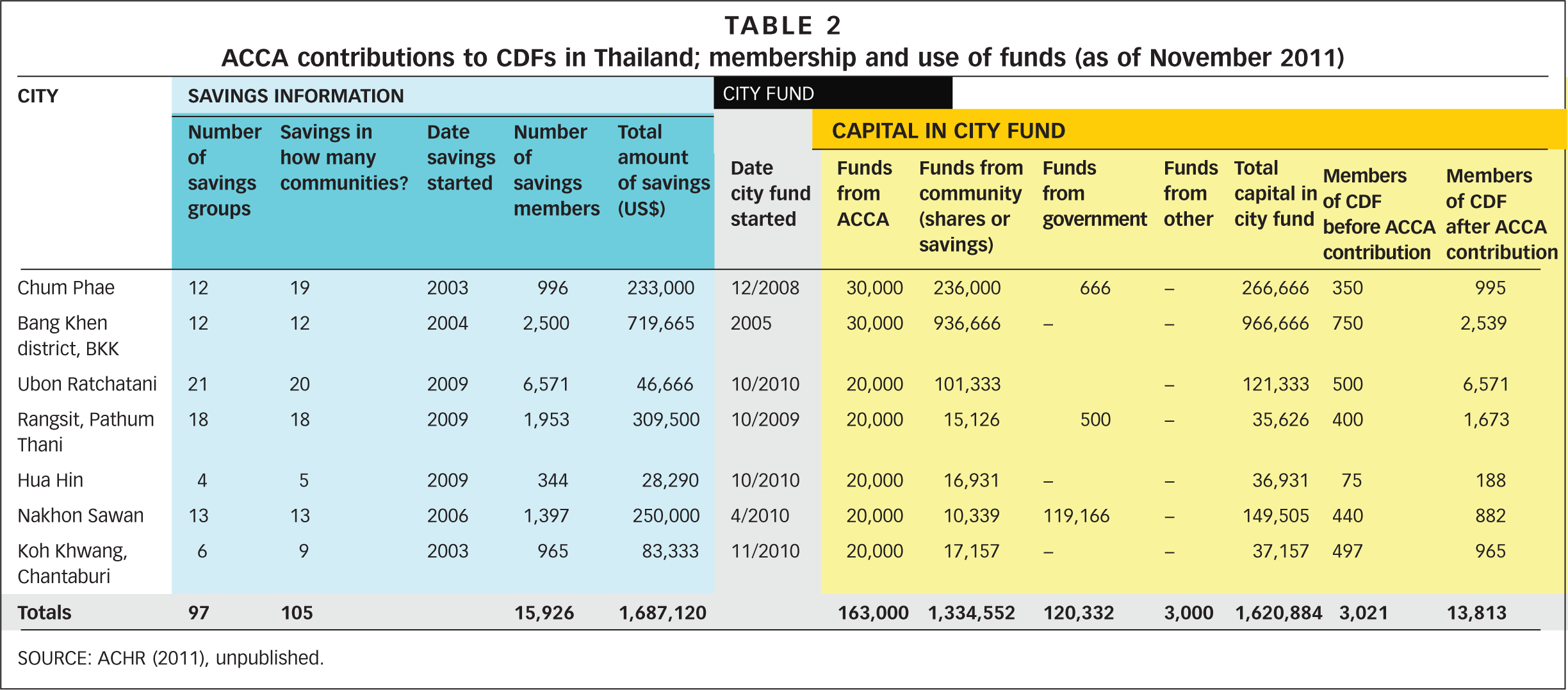

The ACCA programme in Thailand led to the formation of CDFs at the city level, initially in the Bang Khen district of Bangkok and in the town of Chum Phae in northeast Thailand. Thailand is now well-advanced in the development of CDFs, as the urban poor have extensive experience of upgrading through the Baan Mankong programme(10) and have come to realize that CDFs give them the freedom to continue upgrading activities without having to follow the procedures required to obtain a government loan through CODI. The success of these first two funds and the initiatives they have enabled has led to the formation of many other CDFs, a scaling-up process that is being facilitated by the national network of low-income community organizations (NULICO) with the eventual goal of every city having a CDF. There are now 62 CDFs in operation and 243 in the process of formation across the country, while the Baan Mankong programme has led to the upgrading of more than 91,000 houses across 260 towns. The CDFs allow lending and the giving of grants for different purposes. Most are structured under a number of different funds, from loans for housing repairs to disaster funds as insurance against housing damage.

These CDFs allow the community the freedom to manage the allocation of funds for various purposes, which extend beyond housing to address issues of welfare, disaster and other city specific matters that affect groups beyond the urban poor. In Chum Phae, the network decided to buy a rice field using the CDF, and this type of unconventional solution to ensure food security is possible because the city level fund is theirs to use. The CDF allows for a more extensive financial support programme and leads to more people joining the fund once its practical uses have been demonstrated (Table 2). While local authorities may not always contribute funds, they support the CDF by playing an advisory role and providing facilities for meetings.

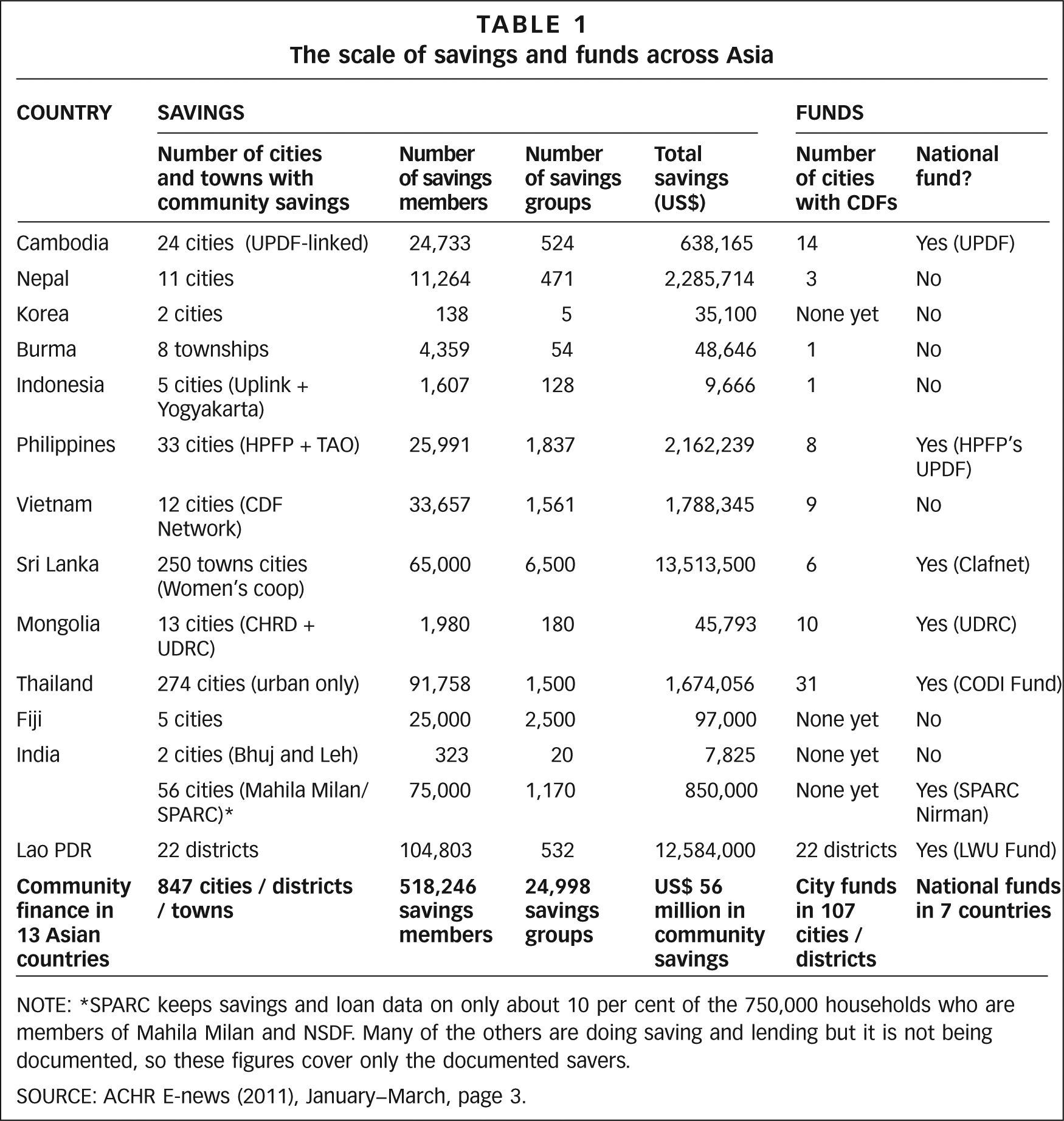

The scale of savings and funds across Asia

NOTE: *SPARC keeps savings and loan data on only about 10 per cent of the 750,000 households who are members of Mahila Milan and NSDF. Many of the others are doing saving and lending but it is not being documented, so these figures cover only the documented savers.

SOURCE: ACHR E-news (2011), January–March, page 3.

ACCA contributions to CDFs in Thailand; membership and use of funds (as of November 2011)

SOURCE: ACHR (2011), unpublished.

For example, the Bang Khen CDF saw a substantial increase in membership once ACCA provided a seed fund, as the CDF’s revolving capital increased thus allowing loans to be given for a wider range of uses, including housing and livelihood purposes, and grants for environmental projects. This CDF is supplemented by a welfare fund and an insurance fund, to which each household makes monthly contributions. While eight communities in Bang Khen are in the process of, or have completed, Baan Mankong upgrading, other communities have seen delays in obtaining government loans for upgrading and therefore households have turned to the CDF for loans for housing repairs or construction. Community members find that the process of obtaining a loan from the CDF is faster than through CODI as fewer procedures are required, and therefore they can improve their houses more quickly.

Other CDFs act as “buffer funds”, providing housing loans while the community waits for larger-scale Baan Mankong funding from CODI, or as a buffer margin in case of delays in loan repayments. Similar to the Baan Mankong programme, the loan period is 15 years with an interest rate of four per cent, of which one per cent goes into the welfare fund, one per cent covers management costs and two per cent goes back into the fund. In the first round of loans in Bang Khen, seven households from three communities benefited from a loan directly; in the second and third rounds, this number increased to 69 beneficiaries from seven communities within the CDF. While the scale is smaller than for Baan Mankong, it plays an important role in keeping community processes active through the implementation of housing projects and by demonstrating to other stakeholders the community’s desire to press on with housing improvements, while also opening up possibilities for further development through welfare, income generation and other small initiatives. Loans are operated collectively, so the cooperative within a particular community has responsibility for making the loan applications on behalf of the households concerned as well as ensuring their repayment, while loan applications are considered by a committee made up of different stakeholders in the CDF, including community and local authority representatives.

CDFs can also operate beyond city networks. For example, in Prachuab Kirikan province in Thailand, a network of stateless persons(11) with no legal entitlements has benefited from ACCA small project funding for water supply, toilet construction and electricity projects, and their next stage is to establish a CDF to continue such activities on their own. These stateless groups have had savings groups since 2002, and the formation of a CDF will give them a wider structure under which to implement community development projects as they cannot receive any assistance from the state until they are legally recognized citizens. Similarly, in Ubon Ratchatani, on the Thai-Laotian border, 24 stateless person households living in a number of communities have received loans for housing improvement from the city’s CDF, supported by an ACCA seed fund. These groups have difficulty accessing government support but financial tools such as CDFs can reach them. As such, the CDF is a vital tool for the very disadvantaged groups who cannot access government support. With additional ACCA support, they are able to improve their basic infrastructure services and their housing, and so press for legal recognition.

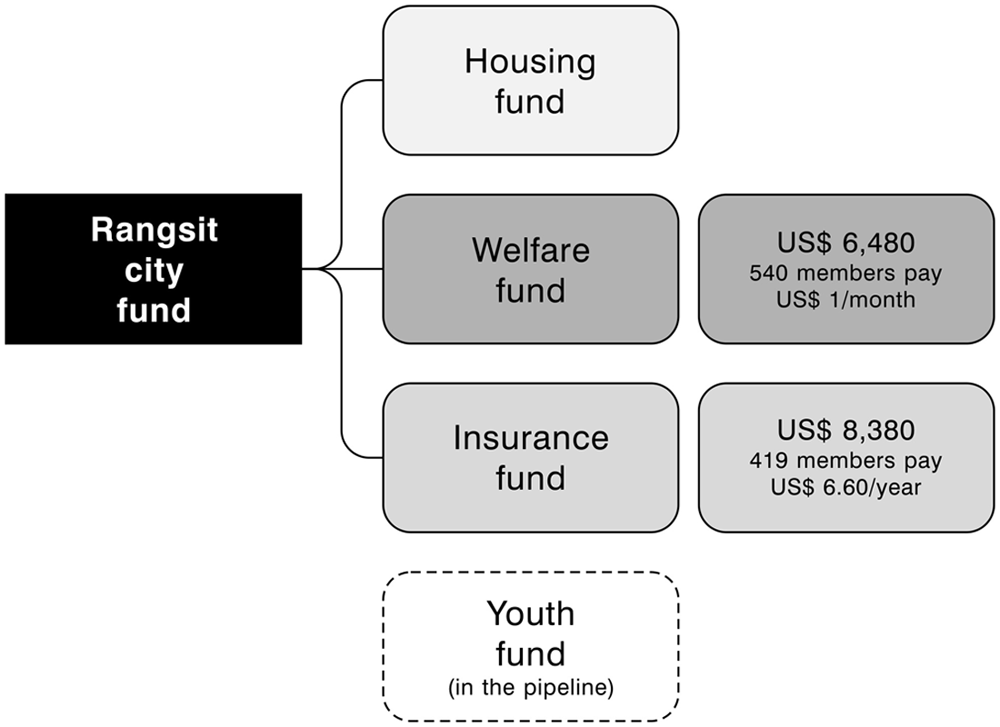

The CDFs have the flexibility to play a role broader than that of the ACCA project, by supporting welfare, disaster relief and rehabilitation and also providing insurance. The types of funds within a CDF are established according to the needs of the community network within that particular city. By pooling together various smaller funds and savings groups, there is scope for larger-scale loans and welfare support within a city, thus allowing citywide upgrading and community development to take place. Figure 2 illustrates the structure of the CDF in Rangsit, which neighbours Bangkok. This city has a total of 22 low-income communities comprising 2,600 households, and 18 of these communities are participating in the Baan Mankong process. The community networks have decided that the main goal of the Rangsit CDF is to support the lowest-income and most vulnerable persons, who may not otherwise be able to participate in community housing improvement activities. The CDF provides grants of US$ 666 to these households and two-year loans for housing improvement and renovation. Three communities have already benefited from CDF loans. In Sangsan community, one household took a loan for US$ 5,050 in order to rebuild their house following a fire, and this loan has already been repaid. Sangsan community also took a loan for US$ 3,333 in order to purchase a machine for making cement blocks, as a form of community industry. These blocks can be used for constructing homes and thus benefit all the communities within the city.

Structure of Rangsit CDF

Another financial tool that has evolved from community processes in Thailand is the creation of a housing and land insurance fund, which offers protection for housing loan repayments in the case of injury or death as well as in the case of damage to housing due to fire, storms or other disasters. This is a way of managing the collective risk to a community cooperative with regard to loan repayments, in the knowledge that many community members face uncertain futures and lack accessible and affordable commercial insurance. Each household pays 200 Baht (US$ 6) yearly to the insurance fund, which CODI capitalized with a 20 million Baht seed fund (US$ 670,000). For example, if the family income earner falls ill, the fund will cover half or all of the family’s loan repayments for three to six months depending on the family’s earning ability, although the rules are adaptable to each specific context. The insurance fund also covers disasters, such as flood damage, and in these situations it would extend also to those who do not have a CODI loan. The insurance fund is currently undergoing a two-year trial phase, with half of the funds maintained centrally through CODI and the other half at the city level. At the end of 2011, the fund had paid out a total of 1,734,495 baht (US$ 57,816) to 452 members, of whom 442 had been affected by disasters, two by serious illness and eight by deaths. These payments are roughly equivalent to the fund contributions received by members. This community insurance fund demonstrates the creativity of community networks in finding flexible and localized solutions to their problems. This is essentially a community-developed financial product, and the fact that the financial system operates on three levels (community, city and national) allows more possibilities for the development of financial mechanisms to address various needs.

V. A People-Based Culture of Finance

Collective savings and finance activities do not have only monetary benefits. One key difference between individual and collective savings is that the latter leads to the creation of social capital due to the mutual trust that must exist between savings group members in both the savings and the repayment process. An individual who takes out a personal loan from his or her bank will only develop a relationship with the bank. However, when a group of people come together to save regularly and then use their accumulated savings for a collective purpose such as an infrastructure project, they are fostering the development of bonding social capital between people who already have close ties.(12) When CDFs are created as a community level fund between various communities, this fosters inter-community ties of bridging social capital. While in the cases where government or other stakeholders have also contributed towards a fund, such as a city-based development fund, this boosts linking social capital between communities and other actors. Thus, collective finance is an important tool in fostering social capital across both horizontal and vertical planes, and serves as a vital, although intangible, asset for the poor.

At the community level loans need to be accessible to all, not just to those with the ability to pay. The collective loan system promoted through ACCA is a response to this and leads to the development of community capabilities, as community members have a collective responsibility to ensure that any upgrading processes are inclusive and open to all residents. The communities set their own criteria for access to loans and their management, repayment plans and group guarantees, with monthly and weekly meetings as required. The flexibility that comes with the ACCA funds allows the development of a truly “people-based” culture of finance for urban development. While the size of ACCA contributions is modest, they play an important role in triggering the empowerment of the poor to become financial actors with the means to take concrete action. ACCA believes it is up to each national network or federation to decide how to manage this money. While some countries opt to pass on the funds to the concerned communities as a grant, others, such as Vietnam, Lao PDR and the Philippines, opt to use the project funds as a revolving loan that revolves back to the CDF at the city level, thus stretching out the initial ACCA contribution beyond one project. In this way, communities can take a broader perspective. They are encouraged to be aware of all the low-income groups in their city or network rather than looking just at their own needs. As such, there is a strong emphasis on the horizontal linkages required, which can eventually form the basis of a CDF in order to scale up projects to other communities. As CDFs are managed by a committee that includes community representatives, they have the flexibility to consider each loan on an individual basis and adjust criteria to meet specific local needs, an approach that formal finance systems usually cannot take due to their regulated nature. Many community level savings groups set aside some funds in case there are delays by some households in repaying loans. Communities can adopt this holistic system because they are strongly networked and aware of the needs of their fellow residents.

Cambodia has gone beyond the limited city focus that is supported by ACCA and is “scaling up” by giving smaller grants to a larger number of communities in more cities; and consequently, this has also led to many CDFs being created. The community process in Cambodia operates through a national level development fund, the Urban Poor Development Fund (UPDF), which initially started in Phnom Penh in 1998 with a seed fund of US$ 20,000 from ACHR; it has since spread to most towns and now has US$ 2 million in capital. There are more than 2,000 savings groups in 26 towns, with 24,000 members and combined savings of around US$ 700,000. In addition to the national UPDF fund there are 15 more local level provincial revolving funds funded by a mixture of ACCA, community, government and other sources. Provincial funds address the needs of locally networked communities within a province and the UPDF can supplement these needs where necessary. The UPDF also strengthens the national level network and draws in more groups to join the community process even if they are not a part of a provincial fund. Local community networks can play the politics at the provincial level using individual upgrading projects to draw in government contributions such as land and infrastructure, while the UPDF can focus on national policy. Provincial CDFs, chaired by provincial governors, are a tool for including key local government players in community processes, while maintaining the necessary flexibility to meet specific community needs. Like CDFs in Thailand, this allows a decentralization of processes, increases local flexibility and independence to address specific local needs and reduces the overall threat of being faced with discontinued funding, whether from national government or international donors, while the national spread of the flexible finance model gives it legitimacy.

In those countries that also opt to use the grants for small infrastructure upgrading projects as revolving loans in order to build up their city funds, the limited budget from ACCA can be stretched beyond the original community to meet the needs of others. When combined with the citywide processes of surveying and mapping, as encouraged by ACCA, upgrading and housing needs across the city can be prioritized into a plan of action and local authorities can be drawn into the process. As infrastructure projects can garner the interest of local authorities, this is a useful step to forming the necessary relationships for the authorities to consider buying into a CDF. ACCA helps to move the scale of community finance beyond small savings groups to citywide collaborations through development funds. ACCA also supports international exchanges and as a result international learning opportunities lead to new ideas being imported from another country. For example, on a recent trip to Cambodia, representatives from the Homeless People’s Federation of the Philippines (HPFPI) were impressed with the Cambodian model of provincial CDFs, which allowed wider-scale linkages between savings groups. The HPFPI plans to adapt this model to create three regional CDFs for each of the three regions of the Philippines, which will extend across cities and a number of provinces and provide an example of the capacity of community groups to adapt models to their specific needs.

Nevertheless, it is important to recognize that these alternative financial mechanisms are not always easy to establish. Those managing CDFs need to ensure that they don’t fall into the trap of replicating top-down approaches in financial management, but rather must maintain the flexibility that allows CDFs to cater to the needs of the lowest-income and most vulnerable people as well as those with regular incomes. Regular meetings of community representatives within a city and across cities – as well as across countries – promote discussion and decision-making, leading to shared values and the building of a system and culture and to learning from others’ examples, as in the case above of HPFPI learning from the UPDF model. This regular sharing keeps CDFs flexible and innovative, always looking to improve, broaden and strengthen their systems and thus better able to meet the needs of their members.

This raises the important point of ensuring the sustainability of alternative, community-driven financial mechanisms. The problem raised by many development projects is that they are funded by outside international donors and have a short shelf life. It is unrealistic and unhealthy to assume that international donor funding will continue indefinitely; also, it comes with strings attached and is subject to changing priorities. Moreover, donor finance may be insufficient for the scale of anticipated projects. As such, it is essential to secure the financial contribution of national government, and the ACCA emphasis on scale, by including multiple cities per country, is a way of achieving this, by being widespread enough to encourage policy change. Building platforms between community networks and cities so that they can work together demonstrates possibilities for cooperation and brings structural change, while building possible financial linkages with other systems to support these processes. This policy change is all the more possible where community groups have developed the confidence to lobby for the possibilities of large-scale change offered by community-driven development and financial tools such as CDFs.

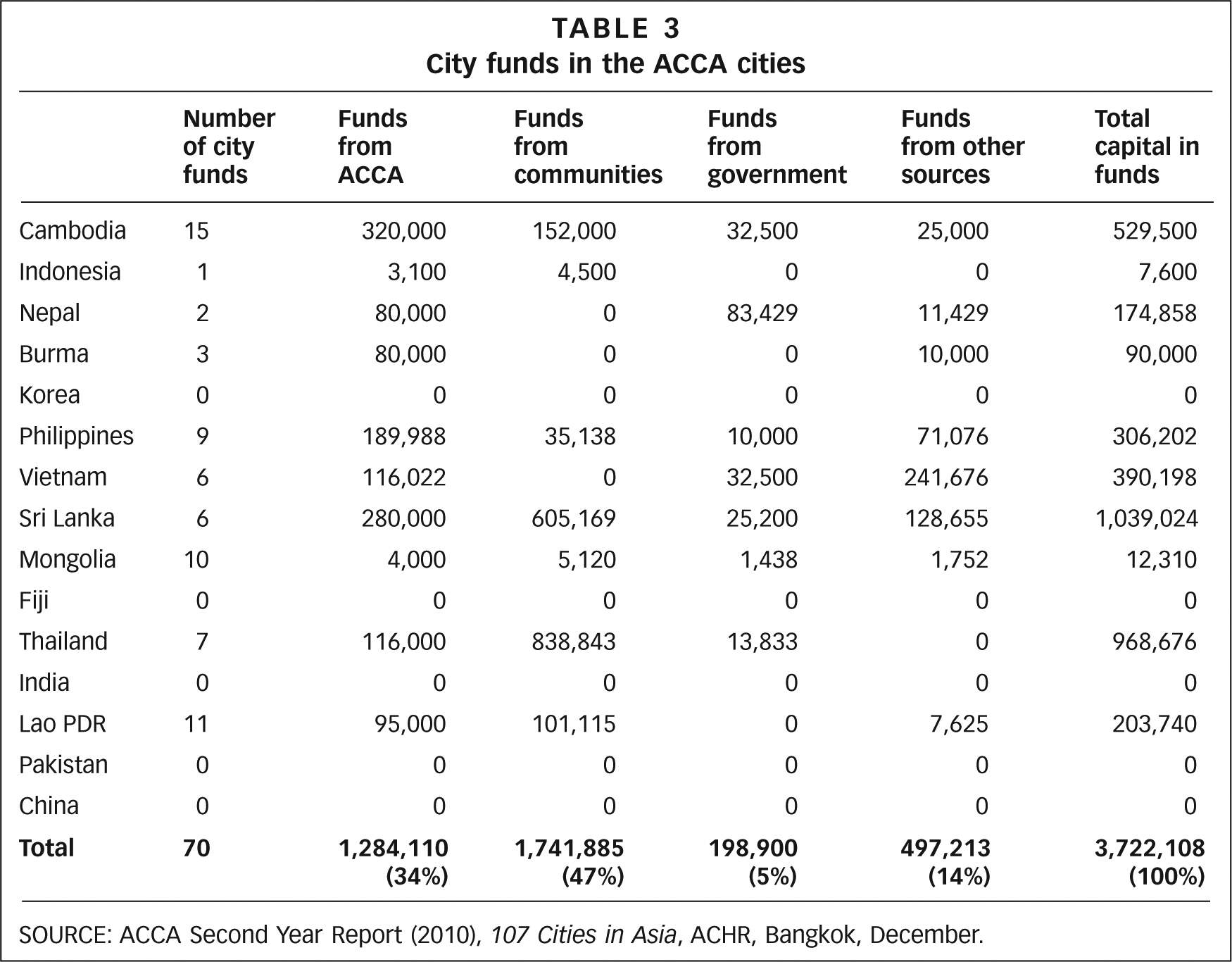

Table 3 shows the variety of models of CDF, with varying contributions from different sources. Nepal, with only two CDFs, has secured contributions from government sources despite the lack of community contributions to CDFs, which suggests that the local government sees CDFs as a good financial mechanism for ensuring that government funds reach grassroots groups. In comparison, Cambodia has 15 provincial CDFs but government contributions are relatively small; instead, local authorities make contributions to ACCA projects in kind, as land and infrastructure (the government contribution has been estimated at US$ 2,464,625 in terms of the value of free land provided to five of the six projects and infrastructure investments in four projects). The government in Lao PDR has also made contributions through land leases. The ACCA approach offers state actors the flexibility to participate in the manner most suited to them, whether it is through providing cash, equipment, land or meeting facilities, or just by being part of the CDF committee.

City funds in the ACCA cities

SOURCE: ACCA Second Year Report (2010), 107 Cities in Asia, ACHR, Bangkok, December.

ACCA recognizes the potential for a regional, Asia-wide revolving loan fund and has experimented with a fund of US$ 200,000 that allows loans of up to US$ 50,000. These loans allow existing cities that have developed citywide activities but have limited funds – or are restricted by the speed at which funds revolve – to continue implementing projects. The regional revolving fund provides two-year loans and so far six cities in four countries have availed themselves of the loan: Nepal, Cambodia, Sri Lanka and the Philippines. The innovative aspect of this revolving fund is that it is experimenting with lending and repayment in local currency, a design that arises from the principle that when working with urban poor groups their situation must be taken into account, rather than placing emphasis on hard currency with its possible additional burdens imposed by fluctuating exchange rates. Loans are given for a five-year period, to be repaid in six-monthly instalments at a four per cent interest rate, which should cover currency fluctuations. There is a need to build a larger regional fund that is friendly to the people’s process, while the structure of CDFs as financial platforms leaves room for possible interface with international financial institutions and the opportunity for linkages to this sector.

VI. Meta-Finance – Bridging a Gap

The ACCA programme demonstrates what access to even very small monies can offer, and the types of infrastructure improvements completed with small project funds exemplify the work that needs financing. ACHR members recognize that the challenge is to multiple the availability of finance, hence the interest in catalyzing institutional developments such as CDFs. Individually, these local improvements do not need much finance, although the monies may be large if these funds are to support the scale of need. Some of the infrastructure improvements are public goods (such as pathways and street lights) – they require organization and may need a scale of investment that is beyond what people can easily collect from their own incomes. A CDF encourages that organization by rewarding it with a loan and, in some cases, with a grant or subsidy. In other cases, such as a housing development, the scale of finance required is larger. If external finance is not available, savings is the major source of investment finance, with evident implications for the speed of consolidation.(13)

What characterizes this type of investment is that it is collectively managed for collective benefits. Specialists in urban development have long recognized that the upgrading of informal settlements requires access to collective finance, or finance that is available to groups wishing to upgrade their neighbourhoods and homes but who do not have the available capital.(14) This finance is very different from shelter microfinance, which has concentrated on individual housing investment, generally outside of any engagement with dysfunctional regulatory frameworks.(15) To help distinguish its different character, it has been called “meta-finance”.(16) Bridging the gap between household-scale investments and larger-scale infrastructure and shelter development finance (which can be provided both by municipalities or specialist development agencies), meta-finance is critical to the development of informal settlements. In part this is because formal financial agencies (be they public or private) are unlikely to work effectively with flexible diverse solutions to improve neighbourhoods. As described in the paper on community architects in this issue,(17) the investments that meta-finance supports are necessarily led by and negotiated between local residents if their monies are to contribute and local solutions that work for all families are to be identified.(18) If residents are not also involved, then the monies are unlikely to be used to good effect.

Meta-finance is not simply finance that falls between micro and municipal (or higher level finance). Nor is it an alternative to larger-scale monies. The ways in which community-scale finance is provided and the way in which it fits within city level planning are both critical components of its effectiveness; hence the institutionalization of the approach within CDFs in ACCA.

VII. Conclusions

The ACCA programme operates with the understanding that ultimately, finance is a tool, a means to an end, not the end in itself. Simply passing funds to communities on the ground is not enough; moreover, although cash transfers have received a lot of acclaim, these financial modalities do not benefit all in the community equally nor will they enable investments in public goods. How the money is passed makes a difference to its effectiveness. The way in which money is managed and controlled is as important as what it is used for, and experimenting with different approaches is part of the learning process. Finance for development needs to be sustainable, and one of the best ways of achieving this is to ensure that there is a national and local level process in which funds are managed in a way that allows community members to play an active role that is adapted to the local socio-politico-legal context.

CDFs as an institution have the flexibility to facilitate these processes. In order to ensure continuous development and empowerment of the capacity of people to improve their living conditions, a secure source of continuous financing is useful to support this development, and CDFs can be a conduit to draw in government and local community funds as well as other interested parties.

Leverage matters because it is proof of buy-in by the state. If local authorities commit money, land or other resources, this demonstrates their confidence in the ability of the community groups to use these contributions productively. City authorities can become allies, helping with land negotiations and contributing equipment, advice and other resources. CDFs institutionalize community finance and offer accountability through the system of a joint management committee; hence, they are a conduit for securing the trust and willingness to participate of agencies outside the communities, which can extend to the formal finance system. This is a vital difference to the people on the ground. They are no longer simply beneficiaries – by being the core actors in the development process, people develop their confidence as well as their homes and infrastructure. This is the way to ensure sustainable development: facilitating processes on the ground so that communities can manage, expand and use the funds through their own initiatives, and development will happen in more ways than one. CDFs can shake up the system and create possibilities for the formal finance system to be drawn into the city development process.

The eagerness of community groups to set up their own CDFs is testament to the desire of the people on the ground to have the independence offered by their own financial system. The scale of activities comes from the community groups themselves, as networks have autonomous processes to spread their activities and assist those needing help, extending their networks and capacities as they go along. This stretches beyond borders, with community groups in various countries supporting each other’s funds. In the case of the National Disaster Fund, which was established following the devastating floods of 2011, Thai communities received contributions from communities in Mongolia and Vietnam, which demonstrates the scale of community solidarity across borders. The next stage is the creation of a regional revolving loan fund under the Urban Poor Coalition Asia (UPCA), which will be managed entirely by community groups on a regional basis.

The ACCA programme has sought to facilitate and experiment with community development finance, in order to put financial resources in the hands of the people and multiply them to reverse a situation of poverty in which people have no money to hand and have to depend on other people’s money and projects. It is a learning experience for those on the ground as well as for the international development community. The focus on finance by people and the possible engagement with the formal finance sector offers a new development direction. While the scale of the sums involved is not huge at present, the processes leverage additional financial resources. Moreover, when finance is in the hands of the people on the ground, it can be integrated with their existing financial management mechanisms such as savings groups, leading to more activities and mutual benefit.

Footnotes

1.

See the paper by Somsook Boonyabancha and Diana Mitlin in this issue of the Journal.

2.

For a further elaboration of the importance of savings for local development, see Patel, Sheela and Celine D’Cruz (1993), “The Mahila Milan crisis credit scheme; from a seed to a tree”, Environment and Urbanization Vol 5, No 1, April, pages 9–17.

3.

Solo, Tova María (2008), “Financial exclusion in Latin America – or the social costs of not banking the urban poor”, Environment and Urbanization Vol 20, No 1, April, pages 47–66.

4.

The importance of access to small monies for upgrading has been recognized by earlier programmes. See, for example, the collection of papers published in 1993 in Environment and Urbanization Vol 5, No 1, April. For a more recent discussion, see Mitlin, D, D Satterthwaite and S Bartlett (2011), Capital, Capacities and Collaboration: The Multiple Roles of Community Savings in Addressing Urban Poverty, Poverty Reduction in Urban Areas Working Paper 34, IIED, London, 71 pages.

6.

The Community Organizations Development Institute (CODI) is a public organization under the Thai Ministry of Social Development and Human Security. It was formed in 2000 through the merging of the Urban Community Development Organization and the Rural Development Fund, with a mandate to empower community organizations to create a strong civil society. CODI is administering the Baan Mankong slum upgrading programme across Thailand, and is also active in rural community development.

7.

The Lao Women’s Union (LWU) was established in 1955 and has a membership of more than 600,000 women nationally. It is mandated to promote gender equality and women’s rights through an extensive network at national, provincial, district and village levels. The LWU is a mass organization that assists women’s economic and social development and also delivers services through development projects.

8.

Phonphakdee, Somsak, Sok Visal and Gabriela Sauter (2009), “The Urban Poor Development Fund in Cambodia: supporting local and citywide development”, Environment and Urbanization Vol 21, No 2, October, pages 569–586.

9.

Thongsuk Phumsanguan, community leader from Chum Phae town, January 2011.

10.

For an elaboration of this programme, see Boonyabancha, Somsook (2005), “Baan Mankong; going to scale with ‘slum’ and squatter upgrading in Thailand”, Environment and Urbanization Vol 17, No 1, April, pages 21–46; also Boonyabancha, Somsook (2009), “Land for housing the poor by the poor: experiences from the Baan Mankong nationwide slum upgrading programme in Thailand”, Environment and Urbanization Vol 21, No 2, pages 309–330; and ![]() .

.

11.

Stateless persons are people who are not legally recognized as citizens of Thailand. In this case, they are Burmese groups living on the Thai–Burma border, who have been affected by historical changes to the countries’ borders.

12.

For a discussion of bridging, bonding and linking social capital, see Woolcock, M (1998), “Social capital and economic development: towards a theoretical synthesis and policy framework”, Theory and Society Vol 27, pages 151–208.

13.

For a discussion of the dependence of housing on savings for housing finance, see Somik, V, Suri A Lall and U Deichmann (2006), “Housing savings and residential mobility in informal settlements in Bhopal, India”, Urban Studies Vol 43, No 7, pages 1025–1039.

14.

UN–Habitat (2005), Global Report on Human Settlements 2005: Financing Urban Shelter, Earthscan Publications Ltd, London, 246 pages; also Mehta, M (2008), “Assessing microfinance for water and sanitation: exploring opportunities for scaling up”, Mimeo, Study for the Bill and Melinda Gates Foundation, Ahmedabad, India, 66 pages.

15.

Daphnis, F and B Ferguson (editors) (2004), Housing Microfinance: A Guide to Practice, Kumarian Press Ltd, Bloomfield CT, 298 pages.

16.

Walker, M (2012), “From microfinance to meta-finance: a new tool to fight global poverty”, Huffington Post, 23 January 2012, available at ![]() .

.

17.

See the paper by Chawanad Luansang, Supawut Boonmahathanakorn and Maria Lourdes Domingo-Price in this issue of the Journal.

18.

For a discussion on the ways in which civil society agencies have used co-production approaches to work with state agencies, see Mitlin, D (2008), “With and beyond the state: co-production as a route to political influence, power and transformation for grassroots organizations”, Environment and Urbanization Vol 20, No 2, October, pages 339–360.