Abstract

This paper describes how the microcredit programme of the Orangi Charitable Trust expanded and developed through supporting the capacity of local organizations to set up and manage credit programmes. It describes the Trust’s evolution from supporting producer and consumer cooperatives, to providing microcredit to small entrepreneurs in Orangi (one of the 18 towns in Karachi city district with around 1.4 million inhabitants), to microcredit in rural areas and other urban centres through 86 partner organizations. By 2010, 39,704 loans worth US$ 7.8 million had been provided in Orangi for small private schools (as government schools are not available), manufacturing units, traders, service providers, building component manufacturing yards and clinics. The Trust had also supported 117,115 loans worth US$ 18 million through partner organizations outside Orangi. Eighty-five per cent of loan repayments are made on time. The Trust and its partners have found that by keeping procedures and products simple and transparent, by supporting staff in partner organizations through learning-by-doing and by recruiting local staff, contact with potential borrowers and loan recovery have been made easier. Those who have taken out loans and those who are interested in loans meet often to discuss progress and difficulties. Initially, partner organizations require financial support, but within two years most generate sufficient funds to cover their overheads. The paper also discusses the new opportunities that the microcredit programmes have provided for women.

I. Introduction

The Orangi Pilot Project–Orangi Charitable Trust’s (OPP–OCT) microcredit programme is the earliest and one of the most important programmes of its kind in Pakistan. It has evolved slowly from an attempt to set up cooperatives of small producers in Orangi in the early 1980s, to providing microcredit to small entrepreneurs in Orangi in the late 1980s, to supporting other NGOs and community-based organizations (CBOs) in both urban and rural areas in Pakistan in promoting microcredit in their areas of operation in the 1990s. At every stage, the programme has been subjected to detailed scrutiny, which has led to a better understanding of the socioeconomic context of Pakistan and of the constraints and potential for the microcredit programme. Its main focus today is on supporting the creation and consolidation of local organizations with a populist culture through the process of microcredit provision and on linking them with each other to create a movement for socioeconomic change.

a. The Orangi Pilot Project

Orangi Town, one of the 18 towns that constitute the Karachi city district, has an unofficial population of about 1.4 million, 86 per cent of which lives in katchi abadis.(1) In 1980, the Orangi Pilot Project (OPP) was established as a result of an understanding between Agha Hasan Abidi, the Chairman of the Bank of Commerce and Credit International (BCCI) Foundation, a Pakistani charity and Dr Akhtar Hameed Khan, the renowned Pakistani social scientist. The purpose was to develop models of community participation and local resource mobilization that could overcome the problems that communities and government face in upgrading poor settlements and in poverty alleviation.

After getting to know Orangi, its various community organizations, entrepreneurs and residents, Dr Khan identified four main issues – sanitation, health, education and employment – and began developing models to tackle them. In 1988, the OPP was upgraded into four independent institutions:

the Orangi Pilot Project–Research and Training Institute (OPP–RTI), which deals with sanitation, housing, education, training, research, documentation and advocacy;

the Orangi Charitable Trust (OCT), which operates the microcredit programme;

the Karachi Health and Social Development Association (KHASDA), which runs a health programme; and

the Rural Development Foundation (RDF), which carries out agriculture-related research and extension.

Dr Khan’s views on development work and the organizational culture that should accompany it were the result of his well-known and tested rural development models, which he felt could also be applied, with suitable modifications, to urban development. He believed that in a period of social dislocation, new local level institutions needed to promote a “…sense of belonging, community feeling, the conventions of mutual help and cooperative action. Without such organizations, chaos and confusion will prevail. On the other hand, if social and economic organizations grow and become strong, services and material conditions, sanitation, schools, clinics, training and employment will also all begin to improve.”(2) The primary purpose of the OPP institutions has been to promote the creation of local community organizations through a process of research, extension and training and to support their autonomy with technical advice and managerial guidance.

Dr Khan also felt that to relate to poor communities, the culture of the OPP should be one of austerity, simplicity and transparency. There should be no bureaucratic procedures, accounts should be transparent, the office should be in Orangi or nearby, and the staff should be, as far as possible, from Orangi itself.(3)

II. From Cooperatives to Microcredit 1983–1987

Dr Khan felt strongly that the problems of present-day Pakistan were similar to those of nineteenth century Europe and the United States, which were addressed by the land grant colleges in the US and by the cooperatives and the folk schools in Europe. He wished to follow “…with necessary modifications, these old methods.”(4)He felt cooperatives were designed to improve the condition of the weak and poor producers and consumers in a capitalist system. In Orangi, he found that most people belonged to the working class. They were day-wage labourers, skilled workers, artisans, small shopkeepers, peddlers and low-income white-collar workers. By promoting producer and consumer cooperatives and providing them with education, training and organizational skills, their incomes and lives would improve and their relationship with state organizations and market forces would become more equitable.

Abbreviations and local terms

BCCI Bank of Commerce and Credit International

CBO Community-based organization

CDN Community Development Network

IFAD International Fund for Agricultural Development

IIED International Institute for Environment and Development

KHASDA Karachi Health and Social Development Association

MIOP Microfinance Innovation and Outreach Programme

MIS Management Information System

OCT Orangi Charitable Trust

OPP Orangi Pilot Project

PO Partner organization

PPAF Pakistan Poverty Alleviation Fund

RDF Rural Development Foundation

RDT Rural Development Trust

UNDP United Nations Development Programme

WWC Women Work Centres

katchi abadis informal settlements

thalla building components manufacturing yard

samjo–seikho–sikhao understand–learn–teach

qingqi a small passenger-carrying cart pulled by a motorbike

A number of attempts at setting up cooperatives were made from 1983 onwards. Perhaps the most successful was the Women Work Centres, which organized stitchers in the garment industry in Orangi and altered their relationship with contractors, middlemen and exporters (Box 2). Another important project was the Banarsi Weavers Cooperative Society,(5)set up to purchase raw materials at wholesale prices and the finished goods of member looms. Similar efforts were made to organize motor parts makers, fret workers, leather workers and a women workers’ cooperative. An OPP employees consumer goods association was also established.(6)

Women Work Centres

The Women Work Centres programme started in 1984 in response to the inflation that forced women to join the informal sector workforce, mainly as stitchers for the garment export trade. Stitchers, organized by contractors who dealt with the exporters, worked in their own homes. The contractors ruthlessly exploited the women economically and there were cases of sexual harassment.

A two-level strategy was devised. A support institution, registered as the Orangi Charitable Trust (OCT), was established to assume the role of the contractor but did not take a profit. The OCT created and equipped work centres with industrial machines, which could increase production, improve quality and be less strenuous to use than the women’s home machines. The OCT also arranged finance for the purchase and distribution of sewing machines to indigent stitchers and for the training of workers, supervisors and managers.

These work centres were each managed by a family and located in their home. The OCT paid them no salary or rent, and the aim was to make them self-supporting. Each work centre was equipped with machines for 10 to 15 workers. Stitchers from the neighbourhood would come to pick up and deliver assignments, which were completed at leisure in their homes except when industrial machines had to be used. The most important functions of the centres were distribution, collection, quality control and packing for the exporters.

Initially, there were difficulties. Neither the exporters nor the stitchers trusted the OCT and in the absence of contractor control and supervision, quality suffered. The contractors also tried to undermine the project. However, these problems were overcome with time, as all parties became familiar with their roles.

SOURCE: Khan, Akhtar Hameed (1989),

Dr Khan was disappointed with the performance of the cooperatives, and concluded in 1987 that “…the social climate in our country, which promotes both dependency and anarchy, is not favourable for cooperative grouping.”(7)The tussle between the various stakeholders with diverse interests penalized the weakest. There were also gaps in the OCT’s understanding of inter-community dynamics, cultural issues and competition and rivalries between the different actors.(8)

In December 1986, in ethnicity-related riots in Orangi, about 400 people were killed and shops and houses were burnt down. The OPP initiated a comprehensive riot repair programme aiming to divert the “…attention of thousands of angry victims from vengeance to reconstruction.”(9)The OPP repaired 130 shops and houses, rebuilt an additional 86 in scattered pockets and decided to provide loans to those affected by the riot. The first loan, to Ghani (a shoe maker), for Rs 20,000 (US$ 233) was the start of the microcredit programme.(10)At the same time, a survey of family enterprises in Orangi demonstrated the need for the promotion of such a programme.(11)

III. Expansion of the Microcredit Programme

Based on the knowledge gained by working in Orangi since 1980, the principles and objectives of the microcredit programme were clearly laid out:

microfinance would be a tool to organize people for community action;

a populist organizational office culture and physical environment would create a productive link with local communities;

initial loans to an individual or organization would be small and monitored for two to three months before any expansion could take place;

meticulous and “agonizing self-appraisal” would be practiced; and

overheads expenditure would be kept low.

In the process, it was felt that the OCT would discover efficient methods of management and create loyal and honest clients.(12) Finance for the programme would be borrowed from Pakistani banks, at market rates, to do away with reliance on foreign donor funding. However, some funding was also received from NORAD, CEBEMO (a Dutch NGO), Swiss Development Corporation and the World Bank.

In this first phase of the programme, from 1987 to 1992, loans were only given to individuals within Orangi through social organizers/supervisors of the OCT. Although the director and joint director approved the loans in meetings, in practice it was the supervisors’ opinions that really mattered. As a result, some clients and the extent of their loans were ill-advised. In 1990, the first serious attempt was made to analyze the reasons for bad debt. The findings helped to shape the policy of being patient with unfortunate and foolish clients and pursuing dishonest ones.(13) At the same time, the programme’s low overheads, only 7.73 per cent by the 1991–1992 financial year,(14) was a great achievement. During this phase, the number of loans increased slowly from 107, amounting to Rs 1.175 million (US$ 13,668) in 1987–1988, to 195, amounting to Rs 2.28 million (US$ 26,563) in 1990–1991.(15)

During this period, loan provision to private schools was also initiated. In Orangi at the time, these schools, which were established by individuals and community organizations, far outnumbered government schools and they required physical improvements and teacher training. Loans were provided for both of these as well as for establishing new schools.(16)So far, 870 loans amounting to Rs 105.89 million (US$ 1.23million) have been given to schools.(17)

Dr Khan also observed that more than 90 per cent of Orangi’s houses were built with financial and technical assistance from local thallas (building component manufacturing yards). Loans were provided to these thallas for upgrading their products and skills, which led to a major improvement in housing in Orangi and to the establishment of autonomous technical support units run by community organizations. In addition, mechanization led to a 300 per cent increase in production, as a result of which Orangi has become a major supplier of building components for the Karachi market.(18)The 386 loans, amounting to Rs 63.54 million (US$ 738,791) to date, have all been recovered.(19)

During this period, the OCT started getting requests from other areas of Pakistan to replicate its microcredit programme. After considerable discussion, it was agreed that the OCT would provide training and seed money for “outside Orangi” partners. Funds were provided by the Infaq Foundation, with a small fund of Rs 8.95 million (US$ 104,070) from the World Bank for a revolving fund.(20)

IV. The Rural Development Trust Experience: Initial Phase 1992–1996

While working in Orangi, Dr Khan kept track of developments in rural Pakistan, analyzing the relationship between the villages around Karachi, the demands of the city for rural products, the network of roads, transport and communication linking the villages to this huge market, and the numerous peasant proprietors eager to become commercial producers.(21)

In 1992, it was decided to set up the Rural Development Trust (RDT) to carry out research and development projects, which could become models for replication through loans from the OCT. A number of demonstration models were developed and the project expanded to Sindh and Punjab. But by the end of 1996, only a small number of supported peasant proprietors had been able to substantially increase their production levels. The OCT did not understand adequately the processes and relationships in rural production and the RDT lacked the technical expertise to develop appropriate and affordable solutions and infrastructure. Projects were launched through influential people, with their own interests in mind. Research and extension packages needed to be dynamic and flexible enough to adapt to new findings, requiring constant monitoring and analysis, which was not done effectively.

Far more successful was the provision of credit for seeds, fertilizer, pesticides, and water and land development, and the demand for loans for these inputs increased.(22)The OCT decided that it would focus only on credit for agro-inputs, providing loans through partner organizations (POs) in different parts of the country, which would be trained in the selection of borrowers and methods of recovery.

Between 1992 and 1995, CBOs and NGOs from Sindh and Punjab were provided with funds, training and regular support visits to operate their own microcredit programmes. The major issue was related to funding the overhead costs of these POs.(23)

In 1994, when the OCT accounts were fully computerized, analysis revealed a mismanagement of Rs 5.4 million (US$ 62,791). Several reasons have been cited for this, most important being the lack of a proper monitoring system and proper operating procedures for the approval of loan applications.(24) This led to major changes in OCT’s organizational structure and methodology.(25)

Despite management problems, there were also positive features. By 1995, 41 affiliated NGOs and CBOs were helping the OCT in loan selection and recovery at no cost to the OCT except for staff training. These partners had issued 1,549 loans amounting to Rs 291.3 million (US$ 3.39 million).(26) The ratio of overheads to disbursed loans fell from 8.73 per cent in 1990–1991 to 4.86 per cent in 1994–1995, while the ratio of mark-up to overheads rose from 128 per cent to 355 per cent.(27) The number of NGOs and CBOs applying to become OCT partners increased considerably, to some extent due to the creation in 2001 of the Community Development Network (CDN), a loose network of OPP partners that met every three months at a different location to present their programmes and discuss their future course of action, often inviting other organizations with similar aspirations.

The expansion of the programme necessitated the establishment of branch offices, starting in 2005 in Sindh where most OCT partners are located. An important branch office is in Hyderabad, a large and easily accessible city for the majority of OCT POs in the province.

a. Other important lessons learnt

Apart from the organizational lessons that led to changes in the structure and functioning of the OCT, other important lessons have been learnt:

leaders of cooperatives should have a belief in the programme but no financial interest in it; he/she should be a person of high moral standard, beyond petty issues, able to work with people despite initial constraints;

to be efficient, it is necessary to keep a low profile;

the higher the loan size, the greater the risk of default;

delinquent loans should be considered a weakness of the organization and not the fault of the borrowers;

bad debt should be written off without delay and should not be kept hidden from the community;

the programme should be based on continuous action–research and modified accordingly;

extension of programmes is possible only if the procedures and products are simple and relate to the capability, capacity and potential of the POs; and

skills can be developed in unqualified or semi-qualified people through a process of learning-by-doing.(28)

V. The Vision and The Present Structure

The OCT has no official vision statement, but implicit in its work and methodology is the sense that the country’s destiny will change only when people are organized to bring about positive change.(29) The mission is to empower communities to remove the social, economic, psychological and technical barriers to their development.(30) The objectives are:

to provide credit for the expansion of existing microcredit enterprises in urban communities in Karachi and small towns;

to provide credit for enterprises and for agricultural inputs and livestock in rural areas;

to strengthen the capacity of NGOs and CBOs so as to make them autonomous, self-supporting institutions;

to support microenterprises through guidance and training; and

to provide lines of credit to POs and CBOs.

As with the OPP more generally, it is felt that the vision and mission can only be achieved if the methodology is rooted in a culture of austerity, simplicity and transparency, with which local communities can identify and which they own and control.(31)

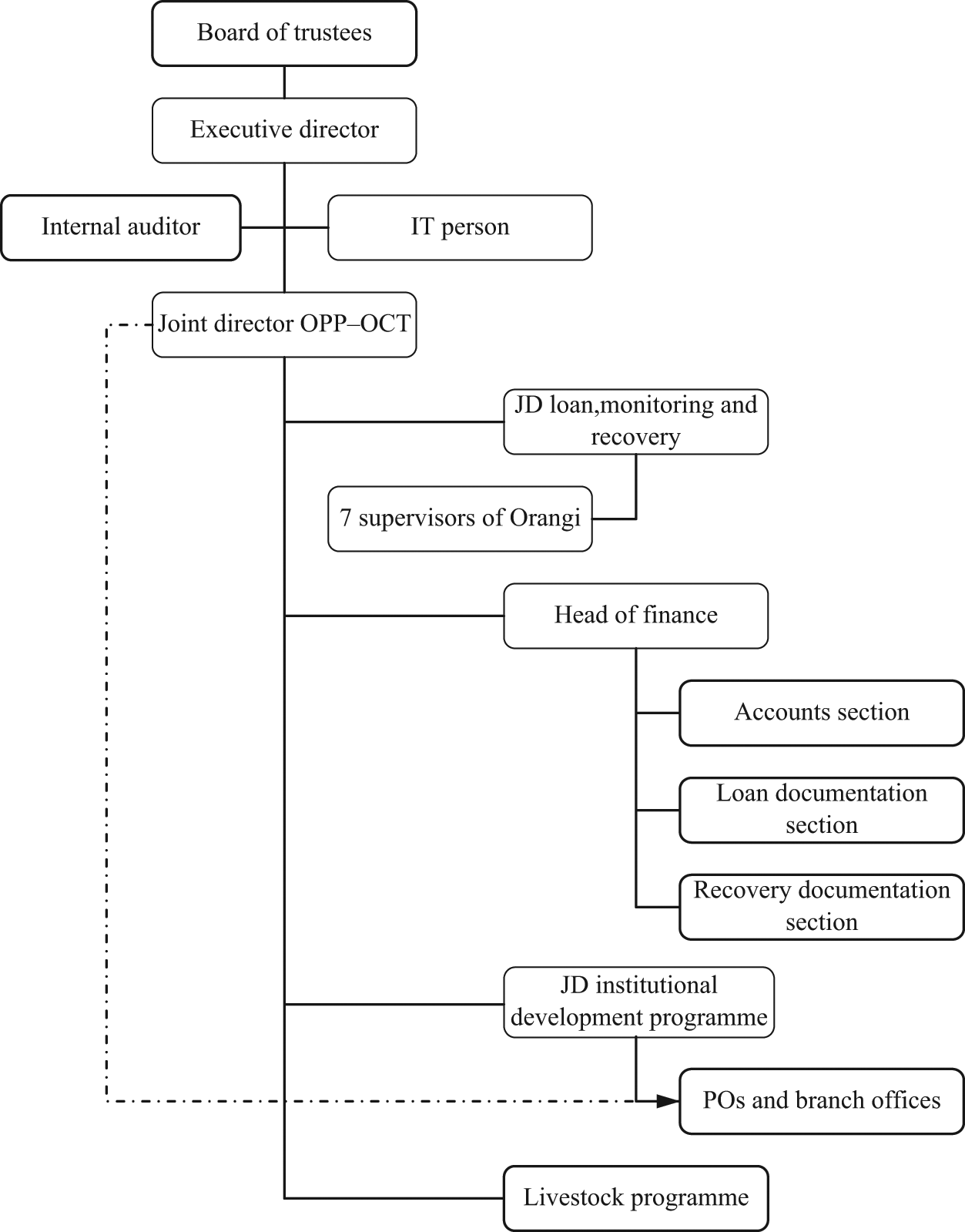

The OCT’s operations are run out of its offices in the informal settlement of Qasba Colony in Orangi Town, Karachi. There are also branch offices in Baldia Town (Karachi), Hyderabad, Jhando Khoso (Hyderabad district), Pirjo Goth (Khairpur district) and Sukkur; also partner organization offices in Sindh, Punjab, and Azad Jammu and Kashmir. Figure 1 shows the OPP’s structure, and the loan process is described in Box 3.

The loan process within Orangi

The process of approving and recovering loans in Orangi and through the Baldia office consists of nine steps:

SOURCE: The information given here is derived from interviews with OCT staff and from Baig, Javaid (1999), “The procedures of the microcredit programme in Orangi”, January (original in Urdu), OPP, Karachi, 23 pages.

Structure of branch offices and partner organizations

Total loans disbursed in Orangi between 1987 and 2010 totalled 39,704 and amounted to Rs 671.75 million (US$ 7.81 million); 14,397 loans have yet to be repaid. Total recovery has been Rs 641.59 million (US$ 7.46 million), of which service charges amount to Rs 112.63 million (US$ 1.3million).(32) Loans have been made to schools, manufacturing units, traders, service providers, thallas and clinics. Almost half come under the RDT programmes for farmers and fishermen, and 18 per cent of the total have been made to women entrepreneurs.

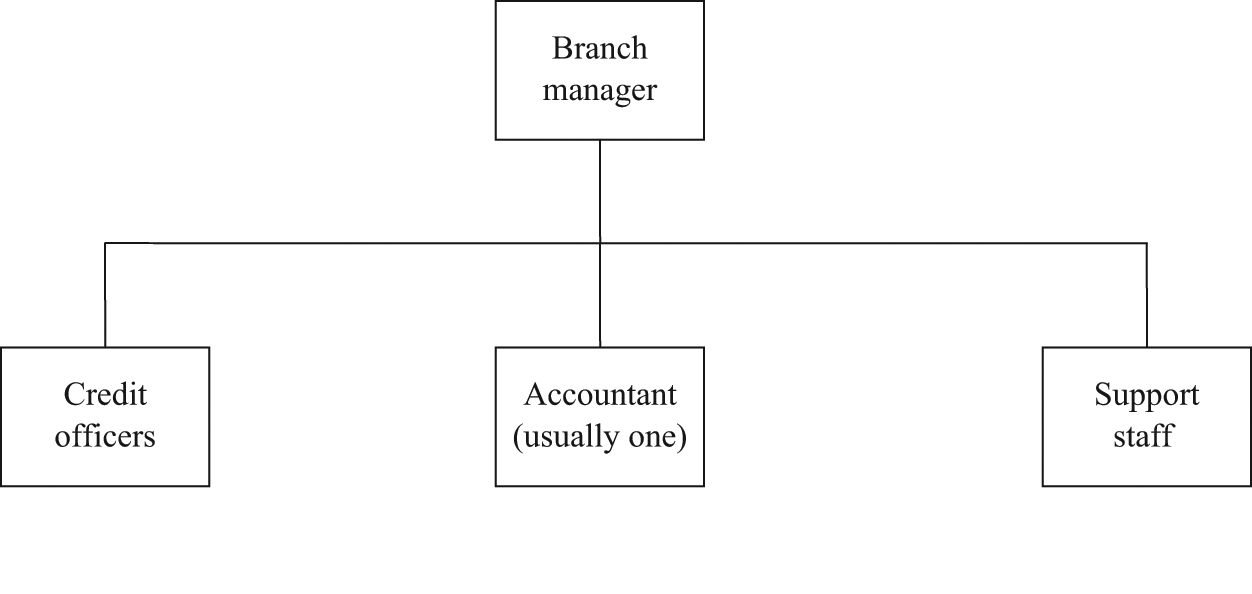

The branch offices and project offices have a similar structure; both are headed by a branch manager, have an accountant (with support staff if the operation is large) and credit officers, often comprising both men and women. The loan committee of the branch offices consists of the joint director OCT, joint director IDP, branch manager and credit officers. The loan committee of the POs is set up by the POs themselves. Although the OCT does not interfere in their membership, some POs include OCT office bearers on their committees. The functioning of the various offices is explained in subsequent sections and in Box 4.

The loan process outside Orangi

The loan process outside Orangi, conducted by partner organizations and branch offices, is similar to that of Orangi but with some important modifications related to local realities and the structure of the loan committee. The loan committee of the branch office discusses all applicants and prepares a final list, which is sent to the OCT head office. The loan section there processes the applications and checks them against computer data to identify any repeat loans, defaulters, new categories or other risk factors. The approved cases are then sent to the accounts section for disbursement.

The project area outside of Orangi is defined either in terms of spatial spread or the availability of staff in the initial stages. The spatial spread can be increased if staff are mobile – for instance with motorbikes. Experience indicates that a credit officer cannot manage more than 350 loans at a time.

SOURCE: Information derived from interviews with OCT staff, from partner organization case studies and from

The OCT has supported 86 NGOs and CBOs, 49 of them outside Orangi, serving 959 areas/villages. As of December 31, 2010, loans issued outside Orangi totalled 117,115, amounting to Rs 1,550 million (US$ 18 million), of which 29,743 have yet to be repaid, in 690 areas/villages. Total recovery has been Rs 1,417 million (US$ 16.47 million), of which service charges account for Rs 170.33 million (US$ 1.98 million).(33)

a. The link with the Pakistan Poverty Alleviation Fund (PPAF) and the repercussions

The Pakistan Poverty Alleviation Fund (PPAF) is an innovative model of public–private partnership sponsored by the government of Pakistan and other donors, and works to empower the poor and increase their income by providing grants and credit to POs engaged in poverty alleviation. Its reach extends throughout Pakistan and it has partnered with 84 organizations, with cumulative disbursements since 2000 of more than US$ 1 billion. And it has been widely recognized for effectively supporting microcredit, water and infrastructure, drought mitigation, education, health and emergency response interventions.

The PPAF first approached the OCT in 1999, but it was only in 2003 that a partnership agreement was finalized. The partnership has brought major changes in the functioning and management culture of the OCT. Because the PPAF covered the running costs of the OCT head office and branch offices and used MIS software to connect the branches and POs to the head office (except where online services were not available), the functioning of the branch offices and POs could be monitored and analyzed.(34) This improved efficiency, communication systems and record keeping, and resulted in a better organizational structure for the OCT, in part because of PPAF reporting and future planning requirements.

The OCT is also the beneficiary of the PPAF’s Microfinance Innovation and Outreach Programme (MIOP), initiated in 2008. Under this programme, the OCT is being supported in operating the Women’s Livestock Cooperative Farming project (see below) and increasing rural outreach through POs. The MIOP was recommended by the Pakistan country strategy paper of the International Fund for Agricultural Development, greatly influenced by the OCT programme.(35)By the end of the financial year 2008–2009, the PPAF had provided the OCT with Rs 309.5 million (US$ 3.59 million) for lending operations, Rs 32.2 million (US$ 372,093) as an operational grant and Rs 4 million (US$ 46,512) as a capital grant, which has supported the OCT and POs with vehicles, laptops, administration costs and overheads.(36)

b. Rural programmes

The OCT also runs a Women’s Livestock Cooperative Farming project, which supports groups of five women with loans of Rs 10,000–15,000 (US$ 116–174.40) each with which they purchase three to five baby male goats. Under the terms of the agreement, they build a shed where all the women keep their animals. The PPAF pays a veterinarian to visit regularly and vaccinate the goats. By the end of the 180-day loan period, the goats are fully grown and ready to be sold at a profit of between 40 and 50 per cent. The programme has expanded rapidly, and over two years 8,654 loans have been provided to rural women.

Agri-loans are provided to small landowners (with less than five acres), contractors (who lease small lots or make yearly cash payments) and sharecroppers (who share the end product with the landowners but are responsible for providing all the agricultural inputs required for production). The POs decide to whom the loans should be provided; the OCT is only interested in recovery and the proper use of the loan money. Loans range from Rs 15,000 (US$ 174) to Rs 25,000 (US$ 290.69), and are normally given in October and November for wheat cultivation and in May and June for cotton growing, and are recovered after six months.

VI. The Partnership Model

Most POs came to know of the OCT through their friends or other POs. The monthly meetings at the Hyderabad office, open to everyone, also provided links. The Sindh partners meet there, bring their friends, and people also come out of curiosity. The atmosphere is relaxed and some prospective partners attend many meetings before approaching the OCT.(37)

There is a strong populist Sufi movement in Sindh, promoted by musicians and singers who recite Sufi verse at musical gatherings with a message of love, tolerance and multiculturalism. Almost all the partners are involved in this movement and the OCT director and his staff have also become active Sufi promoters. Many organizations have become an OCT PO through this connection.(38)

The OCT makes sure that potential partners understand the culture and methodology of the OCT before formalizing the relationship. Through group meetings over several months, such as at the Hyderabad office or at individual meetings at the OCT in Karachi, the partner assimilates the culture and methodology of the OCT and the rationale behind it. When the partnership agreement is finalized, the OCT provides the new partner with training and guidance, core funding for operational expenses, and a line of credit at reduced service charges.(39)

Most PO leaders have been social or political activists in their own area or in educational institutions, some as a result of their family’s involvement in the movement against dictatorship in the 1980s.(40)Others became involved because of deprivation, especially related to acquiring an education. Yet others, coming from small towns and rural areas, went to colleges and universities in the larger towns and joined political movements and acquired an understanding of the reasons behind the under-development of their areas.(41)

Many of the POs, prior to their association with the OCT, had dealt with aspects of social injustice, winning small battles,(42)or establishing informal schools and health programmes with local donations. None of these attempts were sustainable because of a lack of funds and clarity of purpose, which led to problems among the members.(43)Many PO leaders and staff had also been exposed to programmes run by international development agencies and organizations working periodically in their areas, including Oxfam, Catholic Relief Services, Indus Resource Centre and various UNDP programmes, which involved some of these activists in their work. Apart from the Indus Resource Centre, programmes lasted for a couple of years and then closed down, leaving the local people who had been involved in them “high and dry”. However, they left behind knowledge and a thirst in local people for improving their conditions.(44) Most of the leadership is critical of the formal and bureaucratic culture of many of these agencies which, according to some of them, does not “give them respect”; some of them were also intimidated by it.(45)

A recurring theme that emerged from the interviews with the leadership of the organizations is the positive role that women have played, often sacrificing their needs and those of the rest of the family to make education possible for the leaders. This has helped determine the positive gender-related attitudes of the leadership.(46)

A place to meet has been important in almost all cases in the development of the leadership and the organization; a shop where people could meet to talk and discuss local issues became a centre of activity;(47) a small library in someone’s home became a place for reading and discussion, leading to political and social activism.(48)

a. Training

Initial orientation and training of PO leadership and staff is conducted over a period of three days at either the OCT offices or the branch offices. They are trained in credit operations, credit appraisal, accounting, and finance and reporting. After this training, PO staff begin their operations, monitored and helped by visiting staff from the OCT and/or other POs. This is really “training-by-doing”, which the OCT feels is the only way its methodology can be transferred effectively. However, initial training in keeping accounts is not enough. The person chosen as an accountant then goes to Karachi and is attached to a senior OCT accountant for more than a month, during which time they learn all the procedures by “doing”. Accountants and directors of the POs visit the head office every month and have their ledgers, cash books and bank statements checked. Over time, they learn how to function independently.

Orientation and training are also conducted at the monthly PO meetings at the Hyderabad branch office. Partners agree on the subject for the next meeting, which increases group cohesion and feelings of empowerment. Some POs are themselves able to provide all the training to potential partners.(49) The OCT encourages this process and visiting staff monitor it through meetings and observations. The organizations created and trained by POs are known as “baby organizations”.

OCT training has no definite timeframe but is a continuous process. Even after the branch and PO staff have become “trained”, they continue to learn. After a year or two (the timing depends on the PO), PO staff manage to produce financial statements, debit–credit entries and correct expenses documentation; also market research, credit appraisal, the introduction of new loan products, financial statements analysis (loans, mark-ups, savings, OCT share); and deal with defaults, making distinctions between good and bad borrowers.(50)

Since 1992, the OCT has provided training to 595 groups consisting of 2,945 participants.

b. Partner organization staff

Below the director come an accountant, credit officers and support staff (caretakers, drivers etc.). Credit officers, who can be either men or women, need to know how to read and write and should be comfortable and familiar with people and the environment in which they work. Many other microcredit programmes require college/university level qualifications, and as a result their credit officers do not come from the areas where they operate. The OCT has demonstrated that although untrained credit officers initially learn their work by “doing”, they become experts in their field. Today, they are the backbone of the OCT branches and PO programmes.

The PO leadership agrees that when staff are recruited from the neighbourhood, they make initiating contact and making loans and recovery easy, and it promotes a sense of ownership of the PO. However, it can also mean favouritism in the loan and recovery process.(51) In most organizations, staff are either related or from the same clan; hiring often happens by word of mouth, with preference given to acquaintances since the handling of money is involved. It is not easy to recruit women. However, the trend is changing A concern is that women do not wish to work alone in an office, so two have to be recruited simultaneously, which is sometimes problematic.(52)

For accountants, college/university qualifications are preferred. They need the skills and education to understand fairly complex concepts and, subsequently, MIS systems. Here again, however, it has been established that persons with no previous accounting experience have been able to manage and maintain branch office and PO accounts effectively through the learning-by-doing approach. Again, it is preferable that the accountants come from the local area. The OCT has a definite view regarding the relationship between the accountants with the programmes, feeling that they should have nothing to do with the field or field staff. Their isolation guarantees their neutrality and transparency.

c. Lending

With their first credit line, the POs can process 10 to 15 loans of not more than Rs 10,000 each. The small amounts reduce risk to a minimum. After six months of monitoring and evaluation, the extent to which the credit line can be increased is determined.

Initially, all loans are given to enterprises because they are easily accessible and as such help the POs in learning-by-doing (there are all sorts of shops and informal businesses in most rural areas and in all small towns), and the loan recovery period is monthly, not seasonal. After the PO has established its credibility, it can start making agricultural loans. The usual ratio is 70 per cent for enterprises to 30 per cent for agricultural loans. As the PO evolves, more agricultural loans can be disbursed.

The urban loans are to hairdressing salons, beauty parlours, grocery shops, drapers and other small businesses. There is an increasing demand for the purchase of qingqis(53) as a result of an improved road system and an increase in the cost and maintenance of animal-drawn vehicles. The agricultural loans, on the other hand, are used for pesticides, fertilizer and seed purchases, tube well digging and maintenance, and packing of final produce.

Two guarantors are required as a condition for issuing loans. Where the PO feels unsure of its clients there is an additional requirement of making the client (and/or his two guarantors) sign an undated cheque made out to the PO as a guarantee in case of non-payment.(54) In the case of enterprise loans, the preferred guarantors are neighbouring business persons, but there can be exceptions at the discretion of the PO. Workers in adjacent shops, landlords and family members can also be considered. For livestock loans, guarantors are not compulsory – the village women taking out these loans are confined to their neighbourhoods and there are no businesses in the area that can act as guarantors.(55)

The OCT feels comfortable letting its POs provide loans to time-tested clients. However, it has been noticed that over time, the informal relationships can result in financial indiscipline and there are more defaults among repeat borrowers than first-time borrowers.(56)

d. Fund management

Forty-two of the POs are financed by the OCT and 10 of these 42 are financed by the PPAF. The areas of operation of their respective funds are kept separate, as are their credit officers and accounts. This guarantees no overlaps, no confusion or a need to coordinate the two programmes.

e. Monitoring

The OCT’s regular meetings are the most important means for monitoring partners and would-be partners. POs are of the opinion that this frequent, personal and formal interaction has created an environment of encouragement and openness that is unusual in lending organizations.(57) The place and frequency of meetings are decided by the partners themselves, and these meetings allow an understanding of the environment and its relation to the POs’ work, enabling POs to look at their programmes in the wider context and to discuss modifications with the other partners.

At monthly meetings held by the POs, borrowers get feedback on the recovery status. Between the first and the fifth of every month, the PO accountants and directors visit the OCT offices to have their accounts checked. The MIS system that links the POs to the OCT offices allows a proper analysis of the functioning of the POs.

It is clear that monitoring is a full-time activity. Where there have been major defaults, analysis has shown that these were due to the fact that the director of the PO concerned had become involved in other activities and was not paying enough attention to the monitoring process.(58)

f. Recovery

Loans are recovered at the PO offices at 1 pm on the allocated date. It is estimated that 85 per cent of recoveries are made on time.(59)For the rest, different POs have different ways of putting pressure on their borrowers. For example, one PO hires school children who, for a small fee, visit the defaulter’s shop three times a day, usually after a meal, to remind him/her about their instalment.(60)They generally feel that recovery is facilitated by politeness and interaction, rather than coercion.

In other cases, borrowers have been encouraged to form a fraternity of sorts. They meet regularly and make sure that recovery is on-going, aware that if one of them defaults, it will affect the programme adversely. This also leads to an exchange of ideas and the development of new social programmes. In one case, a fraternity donates blood to a local blood bank.(61)Other fraternities are involved in activities such as the Sufi musical programmes.

Unlike the experience in Orangi, the POs are of the opinion that recoveries are better from women than from men. For the first time, women have been involved in an activity outside their immediate environment and they want to demonstrate their credibility.(62)

g. Baby organizations

The OCT is opposed to a culture of competition among POs that is practised in certain organizations, as well as the levering of funds and grants by POs from other organizations and creating visibility for themselves. Decisions should be made collectively and equitably on all issues related to their programmes, with the OCT and its staff keeping a low profile.(63) This kind of culture makes it possible for partners to train and support new POs without the direct support of the OCT,(64) an important process since it would be difficult for the head office in Karachi to train and monitor the growing number of partners.

Branch offices function differently from POs. They may notice changes that need to be made, but have to get approval from head office; in POs, the president or chief executive officer is free to alter the programme. Founding members of a PO have a strong interest in ensuring that their organization is a success; branch offices may not have this same sense of ownership.(65)

h. Role in disasters

During the monsoon season in 2010, Pakistan was devastated by the worst floods in its history, which affected 20 million people. The OCT informed its partners that they should independently begin relief work in their areas. They and their borrowers mobilized local communities, supplied food and medicines to the affected population and supported government departments in their relief work. Later, when relief and rehabilitation agencies, both national and international, began work, the POs were involved. Their training in surveying, documentation and accounting proved very useful in relief and rehabilitation, and also helped in identifying farmers who needed loans to rehabilitate their devastated lands. This relief work, undertaken in coordination with the OPP–RTI, consisted of providing medicines, roofing for shelter, hand pumps and supplies of seeds and fertilizers for 4,000 small farmers at Rs 5,000 (US$ 58) per acre.(66)

Loan recovery for the POs has not been affected in the flood-affected regions, in sharp contrast to the findings of the Pakistan Microfinance Network. They have found that the recent floods have affected recovery in four out of ten borrowers, which will lead to the writing-off of 11 per cent of the microfinance institutions’ balance sheets.(67)

i. Sustainability

Initially, a PO requires financial support from the OCT for administrative overheads and some capital investment, but within two years it can generate sufficient funds to cover its overheads and develop tangible assets and savings through the sale of application forms for microcredit and an agreement fee for each loan, which varies between 3 and 6 per cent of the loan amount.(68) Most POs that were visited would prefer additional finance for providing loans over grants for the development of their institutions. All claimed that they could double their lending within a year if sufficient funds were made available, and that as a result they could earn enough to operate an independent credit programme.

About 40 per cent of total loans being provided today are from the PPAF credit line. If the PPAF withdrew its support, lending and PO earnings would decrease considerably unless the OCT extended funds from its own resources or made alternative arrangements.

VII. Impacts and Repercussions of the Partnership Model

Conversations with PO leadership and staff indicate that many changes have taken place as a result of the microfinance programme, both as individuals and in their work relationships. They now have direct links with families in the villages, so are no longer answerable to village heads. They dress and eat better(69) and are treated with more respect in the market, in government institutions and in the courts of law. Small NGOs are constantly asking them for advice and guidance.(70) The programme has given women the opportunity to travel and interact with people outside their immediate families and neighbourhoods.(71) The success of the OCT programme and its importance in the microfinance world of Pakistan is immensely encouraging to the POs. In 2008, the Mehran Rural Development Organization was runner-up in the Fifth PPAF–Citibank Micro-entrepreneurship Awards.

a. Human resource development

The OCT’s training-by-doing has enhanced the skills of leaders, staff and community members, leading many to seek new and better-paid jobs with government agencies, NGOs and other programmes in the development sector.(72) The trained POs and their staff are now also training new organizations, developing a new culture of learning. According to the OPP–RTI director (also a member of the OCT Board of Trustees), the process is samjo–seikho–sikhao (understand–learn–teach).

The microcredit programme provides staff with the opportunity to travel to other cities and countries, providing exposure to new programmes and ideas. Borrowers’ meetings also add to the knowledge and understanding of grassroots level issues related to the informal credit market and its repercussions, which is then shared with the OCT leadership and staff and POs, at the branch offices and at the head office in Karachi.

b. Changing relationships

The OCT programme has led to linkages between POs and other organizations. For example, the link between the Khajji Cooperative Society and Orix Leasing(73) (to provide a line of credit to expand the programme); also the link between the Sassi Welfare Cooperative and Shah Latif University; and the attempted link between the Khajji Cooperative Society and Tandojam Agriculture University, for a programme to find a solution to diseases of the date palm tree (unfortunately the university lost interest in the project). Some organizations have maintained existing links with NGOs and political parties, but the POs’ point of view is respected more than it was previously. Through programme operations, linkages have been created with the service sector at neighbourhood and district levels; and through flood relief and rehabilitation efforts, there are links with a number of development NGOs as well as government agencies.

i. Changing relationships with middlemen and the market

Agricultural loans have freed small producers from borrowing from the informal sector. They can now take produce direct to the market. Previously, under the terms of an informal loan, the middleman would pick up produce as soon as it was harvested, at a much lower price, and sell it at market rates. Small producers could not hold onto the produce which, after a few months would yield a much better price (Box 5).(74) Some POs are considering the development of storage facilities for their members so that better returns can be realized.

Changing relations with the market

In 2007, a good yield of wheat brought the market price down to Rs 750 (US$ 8.70) per tonne, at which price a farmer could not make much profit. Before the advent of microcredit, there would have been no alternative but to sell at this rate, as all expenses were mortgaged against a loan from a middleman. Microcredit allows farmers to use hard cash to buy whatever they need for their farm and negotiate better rates on seeds, tractor rent and fertilizers. The savings might be sufficient to run a home for a few months, after which time the same crop yield might be worth more per tonne, allowing the farmer to make a larger profit, from which he can pay back the remaining loan instalments and have some small savings.

SOURCE: Case studies of Khajji Cooperative Society and Mehran Education Welfare Society.

As their understanding of the market develops, the POs realize the importance of negotiating with middlemen, commission agents and government organizations. For this reason, POs in small towns and rural areas increasingly feel the need for a presence in the district headquarters; some have already shifted their head offices there.(75)

ii. Links with government departments and politicians

Links with political parties and the bureaucratic establishment at the district level have also been initiated as a result of the OCT programme. These relationships can be complex, since politicians and bureaucrats seek links with successful programmes in order to establish their own credibility(76)but can also see them as a threat to their power.(77)

iii. Changing nature of loan applications

Initially, loans were only given to existing enterprises, but more recently they have also been given to new ventures. For example, barbers and tailors who work in enterprises are now applying for and getting loans to establish their own businesses, and loans have also been given for the purchase of qingqis as taxis.(78)

c. The impact on women

In rural Pakistan, women rarely mix with men apart from with members of their family or during work in the fields. Although the OCT programme does not reach a large number of women in percentage terms, it has had an impact on gender relations and has created role models for the younger generation. During the initial stages of the MIOP livestock farming programme, landlords tried to make women believe that the programme would be unsuccessful and that the OCT would take away their children as collateral. Such insinuations are no longer believed. Women who used to be afraid to open their door to a stranger and who would send a male to repay their loan, now walk in groups to the branch offices.(79) Husbands are now aware of their wives’ earning potential and marital relationships have changed as a result. Most important is that any profits made by women are seen as their own.(80)

In meetings, women now discuss the use of credit money, village issues and children’s education.(81)They are more assertive and have developed the skills to negotiate for their economic and social interests.(82)Many have participated in OCT meetings and have travelled outside their villages; some have visited Karachi and two of them participated in a South Asian Network Meeting in Thailand. However, there are no women accountants in the POs because it is unthinkable for a rural woman to visit Karachi every month, which is an OCT requirement for accountants; yet, the PO women’s leadership feel that if only one woman became an accountant and regularly went to Karachi, the taboo would be broken and others would follow. The women involved in the PO programmes are approached by younger women who wish to be like them;(83) but loan programmes for women can only be promoted through women credit officers, and women are reluctant to work alone in an all-male office.

Earnings from loans are invested by women in better food and clothing for the family; home construction is still seen as a man’s responsibility. The next investment is daughters’ weddings and sons’ secondary education. Women also reinvest in their businesses, purchasing chickens or accumulating the earnings from three loans to buy a cow; and some have invested in sewing machines and are now involved in the stitching business.(84)

d. Axioms from the field

During the course of conversations with the authors, the leaders and staff of the POs made a number of interesting statements. Some are listed here:

“…if one works for people, people work for him;

knowledge has given me a third eye;

do more work but show less;

education is important but staff should be skilled, confident, honest and loyal to the organization;

flexibility and ease in operations results in greater mobilization of would-be clients;

we should take on projects for which we have some level of skill;

the programme is run on values not on rules;

a change in economic status will bring the social change in the lives of individuals;

interaction (with people) educates;

microcredit professionals have Marxist thoughts and capitalist actions;

a low profile is necessary…”

VIII. Major Findings

This section presents the major findings related to the larger context and the sustainability issues of the OCT.

The OCT microcredit programme was not the result of a pre-conceived blueprint. Its primary purpose was always the creation of local level institutions. In this respect, it is very different from other microcredit programmes in Pakistan.

The OCT programme does not cater to the poorest sections of society, as it lends to already existing businesses. This also applies to its rural loans, as it lends to small landowners or to sharecroppers who invest in agricultural inputs for production; these are the better-off among the sharecroppers. The recent trend among POs of giving loans to tailors and barbers who work in other people’s establishments is reaching out to a comparatively poor but skilled clientele; and the MIOP livestock farming project has the potential to reach out to the poorest of the poor. However, access to the poorest has yet to be established.(85) By not lending (or even attempting to lend) to the poorer/poorest of the poor, the OCT has avoided the crisis faced by many microcredit programmes and their borrowers.(86)

Rural Sindh and its small towns are undergoing a process of major social change. Young men are returning after acquiring a college or university education in the district headquarters or at the Sindh University in Jamshoro. Women are also being educated and a few attend colleges and universities. These young people aspire to an urban middle-class lifestyle and the values that go with it. Small businesses and a growing service sector provide them with the necessities to fulfil these aspirations. The OCT programme is helping to consolidate this new middle class in social, economic and political terms. One advantage of this is that the power of the feudal elements, which until recently controlled every aspect of life in the rural areas and to a lesser extent in the small towns, is rapidly decreasing.

The OCT has managed to create local level institutions that are manned and owned by local leaders and staff. This is an important achievement and is primarily due to the OCT’s non-bureaucratic, democratic, transparent and populist culture, without which the OCT leadership would not be able to understand local conditions, the people it works with, their aspirations nor the requirements to fulfil these. However, the OPP institutions feel that skills are easier to transfer than the OPP culture.

It has been proven conclusively by the OCT that academic qualifications are not necessary to being a good credit officer or support staff to the PO programmes. The skills required for these jobs can be created by training-by-doing. Persons with no training in accountancy can become accountants through a similar process. The training-by-doing process has made possible the creation of local level institutions, owned and managed by local people.

The changing lifestyles and values of the leadership, staff and urban borrowers of the OCT programme are likely to change the collective culture of the OCT and the programme’s social dimensions. The OCT and PO leadership are aware of the danger, and to deal with it they have created the Microfinance Organizations Network of Pakistan, which links 30 out of the 31 POs. It is felt that through this network, the values of the programme will be protected and changes will be suitably guided.

The importance of a visionary to guide the programme has been raised by a number of PO leaders. Akhtar Hameed Khan was such a visionary, and it was felt that after him the OPP programmes would collapse or fossilize. However, new leadership emerged and Anwar Rashid is also seen as a visionary. The freedom to observe and reflect, which the OCT culture promotes, will in the opinion of the authors bring forward persons able to guide and modify the programme in a changing context.

Similar concerns regarding staff and members of the Board of Trustees have also been expressed by detractors, who feel that with the minimal turnover, the present staff and board will grow old and there will be no one to replace them who understands their culture. This could result in a “crisis of culture” for the OPP institutions and a change in direction in their programmes. The OCT understands these concerns, but they need to be addressed.

Despite the POs’conviction, backed by their achievements, that they could more than double their outreach if sufficient funds were available, it is clear from conversations with the OCT accounts section and a survey of the literature of the Pakistan Microfinance Network that such funds are not available in the market.

Would the OCT be sustainable if the 40 per cent of its credit line that is PPAF related were withdrawn? A glance at an extract from the OCT financial statements gives some indication (Appendix 1). It is clear from the statements that if the PPAF withdrew its support, the scale of the OCT programme would certainly be affected, although the low operational costs (4.6 per cent of loans and service charges) could be managed.(87) The OCT could make up for some of the loss from its reserves, and in addition, with an asset-to-liability ratio of 69.5 to 30.5 per cent,(88) it is felt that any financial institution would be willing to support the expansion of the OCT programme.

Footnotes

Appendix 1: Extracts from OCT financial statements,30 June 2010

This paper summarizes a detailed study of the OPP–OCT microcredit programme entitled From Microfinance to the Building of Local Institutions: The Evolution of the Microcredit Programme of the OPP’s Orangi Charitable Trust, Karachi, Pakistan, and included 10 case studies (referred to in the footnotes). The full report is to be published by the Oxford University Press Karachi in February 2012.

1.

Hasan, Arif (2009), Participatory Development: The Story of the OPP–RTI and the URC, Karachi, Pakistan, OUP Karachi, 343 pages.

2.

Khan, Akhtar Hameed (1996a), “A note on welfare work”, Chapter 7, Orangi Pilot Project; Reminiscences and Reflections, OUP, Karachi.

3.

For details see, Hasan, Arif (2001), Akhtar Hameed Khan and the Orangi Pilot Project, City Press, Karachi, 60 pages.

4.

Khan, Akhtar Hameed (1996b), Orangi Pilot Project; Reminiscences and Reflections, OUP, Karachi, page 39.

5.

Banarsi weavers migrated from Benares (now Varanasi) in India to Karachi at the time of partition. Their weaving profession is hereditary and they produce silk cloth inlaid with gold thread.

6.

OPP Quarterly Progress Reports, 1984–1989, OPP, Karachi.

7.

Khan, Akhtar Hameed (1989), Women Work Centres: Story of Five Years 1984–1989, OPP, Karachi, page 30.

8.

OPP Quarterly Progress Report, January–March 1994, OPP, Karachi.

9.

OPP Quarterly Progress Report, April–June 1987, OPP, Karachi, page 1.

10.

Interview with OCT Joint Director Naila Ghias, 7 September 2010.

11.

Khan, Akhtar Hameed (1991), Orangi Pilot Project Programmes, OPP, Karachi, 39 pages.

12.

OPP Quarterly Progress Report, October–December 1990, OPP, Karachi.

13.

OPP Quarterly Progress Report, October–December 1991, OPP, Karachi.

14.

Ismail, Aquila (2006), The Microcredit Programme of the Orangi Charitable Trust, Sama Publishers, Karachi, 172 pages.

15.

See reference 13.

16.

See reference 11.

17.

Accounts Sheets of OPP–OCT until 31 December 2010.

18.

Serageldin, Ismail (editor) (1997), The Architecture of Empowerment: People, Shelter and Livable Cities, Academy Editions, London, 128 pages; also see reference 1.

19.

See reference 17.

20.

See reference 14.

21.

OPP Quarterly Progress Report, October–December 1994, OPP, Karachi.

22.

Interview with OCT Director Anwar Rashid, 7 September 2010.

23.

Derived from OPP Quarterly Progress Reports for 1995 and 1996, OPP, Karachi.

24.

See reference 22.

25.

Interview with OCT Director Anwar Rashid, 6 October 2010.

26.

OPP Quarterly Progress Report, April–June 1996, OPP, Karachi.

27.

See reference 26.

28.

See reference 22.

29.

OCT Institutional Assessment 2010.

30.

See reference 29.

31.

For details see reference 3.

32.

OPP Quarterly Progress Report, July–September 2010, OPP, Karachi.

33.

OPP Quarterly Progress Report, April–June 2010, OPP, Karachi.

34.

Interviews with OCT Director Anwar Rashid and OCT Joint Director Naila Ghias in October 2010.

35.

Interviews with OCT Director Anwar Rashid; see also the Pakistan Country Strategy Paper of the IFAD.

36.

See reference 35.

37.

Case study–07: Saath Development Society.

38.

Case study–08: Mehran Development Organization.

39.

OPP Quarterly Progress Report, January–March 2010, OPP, Karachi.

40.

See reference 38.

41.

Case study–05: Mehran Education Welfare Society.

42.

See reference 41.

43.

Case study–06: Foundation for Rural Development; also case study–01: Khajji Cooperative Society; and case study–09: Indus Community Development Organization.

44.

In almost all case studies.

45.

This surfaced in many informal conversations and is implied in a number of case studies, for example, see reference 37.

46.

Case study–02: Sassi Cooperative Society; also see reference 41.

47.

See reference 41.

48.

See reference 43, case study–01.

49.

See reference 41.

50.

Interview with Javaid Baig, 24 December 2010.

51.

Case study–03: OCT Pir jo Goth Branch.

52.

See reference 51.

53.

See reference 37. A qingqi is a small passenger-carrying cart pulled by a motorbike.

54.

Case study–10: Shadab Rural Development Organization; also see reference 43, case study–09.

55.

See reference 37.

56.

Interview with OCT Joint Director Naila Ghias, 24 December 2010.

57.

Staff from all the organizations that were visited emphasized this.

58.

See reference 43, case study–01; also see reference 41.

59.

See reference 41.

60.

See reference 54.

61.

See reference 43, case study–06.

62.

See reference 46.

63.

Conversations with OCT Director Anwar Rashid and OCT Joint Director Naila Ghias.

64.

The Khajji Cooperative Society trained the Mehran Education Welfare Society, which in turn trained its Foundation for Rural Development (FRD) office, which is now independent.

65.

Conversations with staff from the Foundation for Rural Development.

66.

For details, see reference 32.

68.

All case studies established this.

69.

See reference 43, case study–06.

70.

See reference 43, case study–09.

71.

See reference 46; also case study–04: MIOP Livestock Farming Programme.

72.

See reference 38.

73.

See reference 43, case study–01.

74.

See reference 43, case study–01; also see reference 41.

75.

See reference 43, case study–01.

76.

See reference 43, case study–01.

77.

See reference 43, case study–01.

78.

See reference 37.

79.

See reference 43, case study–09.

80.

See reference 71, case study–04.

81.

See reference 37.

82.

See reference 71, case study–04.

83.

See reference 46; also see reference 71, case study–04.

84.

See reference 71, case study–04.

85.

This summarizes conversations with partner organization leadership and staff and what has emerged from the case studies. It is also supported by the Plan International-supported Poverty Measurement Report of the Microfinance Organizations Network of Pakistan (October 2010).

86.

For details, see Bateman, Milford (2010), Why Doesn’t Microfinance Work? The Destructive Rise of Neo-liberalism, Zed Books, London, 262 pages.

87.

See reference 32, Table 2.

88.

See reference 32, Table 9.