Abstract

Automotive after sales, which include provision of spare parts, customer service, and accessories sales, is one of the most profitable parts of the automotive industry and provides for an ongoing relationship with the customer. In times of recession, performance of after sales remains steady as it is highly independent of macroeconomic behaviors and keeps outstanding margins. Current automotive after sales are predominantly based on fossil fuel power train technologies, involving a significant number of replaceable working parts, lubricants, and supplies, and requiring ongoing manual labor. Current efforts to decarbonize the automotive industry, however, have the potential to disrupt this industry by shifting traditional after sales business models.

The objective of this paper is to review the background and development of policies and actions in relation to the decarbonization of transport with a particular focus upon the role of the automotive after sales sector. The review considers the role of a range of stakeholders including multilateral bodies setting targets for participating nations; national governments; and the automotive industry, operating at varying scales. Electrification of vehicles and discouragement of car use and ownership are identified as key decarbonization strategies that could significantly impact upon car manufacturers and the broader automotive industry, which will in turn impact upon the after sales market. The review concludes that there has been limited research about impacts on after sales markets from transport decarbonization strategies. Areas of impact identified include reduction of working parts, fewer additional units, longer service intervals, changes in labor needs, disruption in customer retention, and changes to the repurchase cycle. In order to explore these potential impacts, the development of alternative future scenarios under different power train technologies and regional factors is recommended as an area for further research.

Introduction

The environmental impacts of transport have gained increasing recognition in recent years in response to challenges posed by climate change and global warming as a result of the use of fossil fuels, which has accelerated greenhouse gas (GHG) emissions. 1 Transport sector emissions are considered to be a high priority concern in relation to environmental sustainability. 2 Some nations, such as China and India, have increased their total CO2 emissions substantially while other regions, such as Europe, have decreased theirs in total. 3 However, Europe has been unable to change the continuing upward trend of CO2 emissions generated by the transport sector 4 due to its’ high dependency on fossil fuels. 5 Although the energy efficiency of the transport sector has grown substantially, 6 trends since the 1980s indicate an increasing rate of energy consumption for both passenger and cargo transport caused by larger vehicles, a decreasing number of passengers per vehicle, longer journeys, larger engine sizes, and less environmentally friendly driving practices. 7

The transport sector worldwide has failed in its attempt to achieve significant reductions in carbon emissions. In the period between 1970 and 2010, for example, transport sector emissions increased by 250%, 8 while energy consumption increased by 220%. 9 Figures from 2010 indicate that 23% of global CO2 emissions from fossil fuel combustion were generated by the transport sector, with road vehicles showing an 80% growth. 8

The European Commission has set a goal to achieve a 60% reduction in GHG emissions produced by the transport sector by 2050, 10 with the use of alternatively fueled vehicles being one of the key strategies proposed to achieve this, combined with the discouragement of car ownership and use. 11 While such proposals promise strong environmental benefits, their impact on related markets (such as automotive sales and after sales) has been relatively understudied. After sales is defined as the supply of services to the customer once the good has been sold. 12 In other words, a good will require after sales service unless it is 100% maintenance free or the replacement cost is much lower than the repair cost. 13 Margins and revenues from automotive after sales comprise a central role in the automotive industry, 14 and after sales show an advantage, represented by the stability of the business during times of crisis. 15

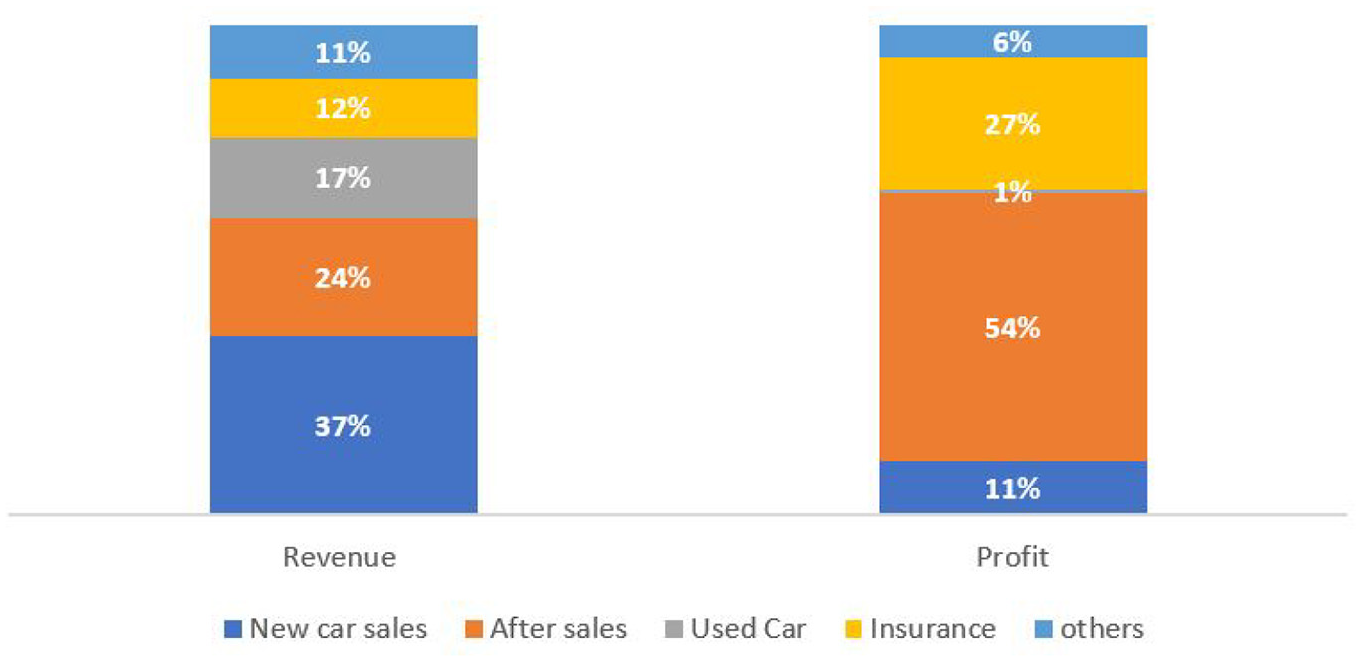

After sales businesses need a basic input, which is a constant growth of units in operation (UIO) – newly sold cars on the road. New unit sales are the base business line in the industry. Furthermore, whilst new sales are more marginally important (approx. 37%) in terms of revenue, after sales are significantly more important (approx. 54%) in terms of profit. 16 Additionally, sales of new units have plummeted rapidly in terms of earnings margins, simultaneously with the increasing extension of car life. Both situations make the after sales business consistently important for manufacturers, wholesalers, and dealers. 16 The current automotive sector dynamic, which is based on constant upward sales of new units, is potentially at odds with the main projected strategies and guiding principles set by policy makers in order to meet transport sector GHG emissions reduction targets. In this paper, we explore potential impacts of decarbonization on the automotive after sales industry.

Stakeholders from the automotive sector will need to encourage efforts focused on innovation and new automotive after sales business models.17,18 Dombrowski and Engel 19 argue that scientific approaches and reviews lack understanding about the right way to manage new technologies and their impacts on small after sales business such as minor dealers and garages. Gissler and Muller 16 suggest that businesses and firms involved in the automotive industry and after sales process must begin by studying new technologies which offer potential disruption and innovation in the after sales markets. A potential source of disruption are new technologies which reduce vehicle CO2 emissions and their effects on new and successful after sales business models. 16

The objective of this paper is to provide a comprehensive review of policies and strategies related to transport decarbonization, such as electrification of vehicles, discouragement of car use and reduction in private car ownership, that have the potential to disrupt the traditional and lucrative automotive after sales sector for different supply-side stakeholders and to explore how these policies and strategies could change depending on geographic and political conditions.

In the next section, the methodology applied for the evidence review is detailed. Section three introduces the concept of decarbonization of transport, and discusses the development of policies and instruments to promote decarbonization related to the automotive industry and after sales. Section four depicts the automotive after sales business, including definition, scope, importance, economic characteristics, business components, and involved stakeholders. Section five assesses current policies to incentivize vehicle electrification, while section six assesses potential impacts of decarbonization on after sales and section seven considers the future of internal combustion engine (ICE) vehicles. The final part of this paper summarizes the key findings and conclusions of this review and identifies further research opportunities.

Methodology

In this review, we have examined both academic and gray literature, including consultancy reports, academic articles, specialized blogs, books, electronic encyclopedias, research body reports, newspaper and magazine articles, and company reports, which are segmented by category in Table 1. The aim of this search was to review the relationship between decarbonization of transport, particularly related to electric vehicles (Hybrid electric vehicles (HEV) like the Toyota Prius are excluded from this group due to their main source of propulsion being an ICE. This HEV uses a battery to store energy but it is charged by a regenerative braking system and the ICE, so an outlet power source is not necessary. 20 ) (EVs) and automotive after sales. The search was conducted using keywords related to the three fundamental concepts of this study (decarbonization, EVs, and after sales) such as: decarbonization, decarbonization of transport, after sales, automotive after sales, customer service, automotive spare parts, electric mobility, electric vehicle, CO2 emissions, transport policy, power train technologies, and automotive future trends. Relevant articles were classified and organized by common topic areas as described in Table 1. To find related articles and information, we used academic databases such as PRIMO, Science Direct, Emerald and Springer; as well as more “popular” search engines such as Google Scholar and standard web search engines.

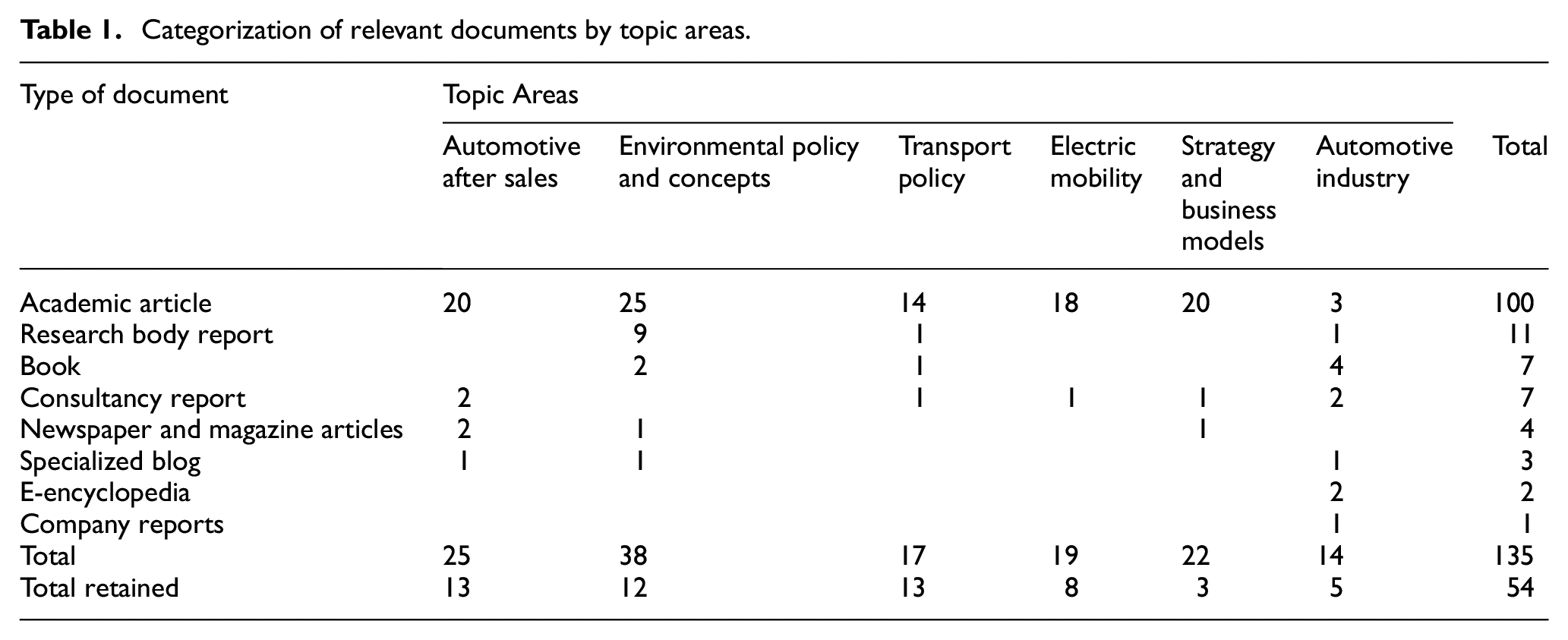

Categorization of relevant documents by topic areas.

Table 1 shows that an extensive set of 135 documents were initially identified for review. On further inspection, documents were assessed for direct relevance to decarbonization in the after sales market. Features such as recency of publication and regional differentiation scope were also considered. Finally, 54 documents were retained for the review.

Decarbonization of transport

Tapio et al. 7 define decarbonization as the reduction of carbon intensity, or the diminishing of fossil fuel consumption from economic activities such as transport. Decarbonization can also be seen as the effort to decouple the relationship between CO2 emissions and GDP (CO2/GDP). 21 This decoupling has two main routes, the first one called Relative, where CO2 emissions and GDP keep growing but CO2 grows at a lower rate; and the second one, Absolute, where CO2 emissions decrease over time. 22

Geographical contribution of GHG emissions from the transport sector

The search for a sustainable transport policy is gaining importance in the EU, as well as more broadly worldwide. It has been suggested that over 95% of GHG transport emissions come from fossil fuels 23 and transport is over 95% dependent on fossil fuels.7,24 Of these total transport sector emissions, 44% belong to passenger cars and 19% come from heavy-duty vehicles. 25 These figures demonstrate the importance of the transport sector in strategies and policies addressing decarbonization.

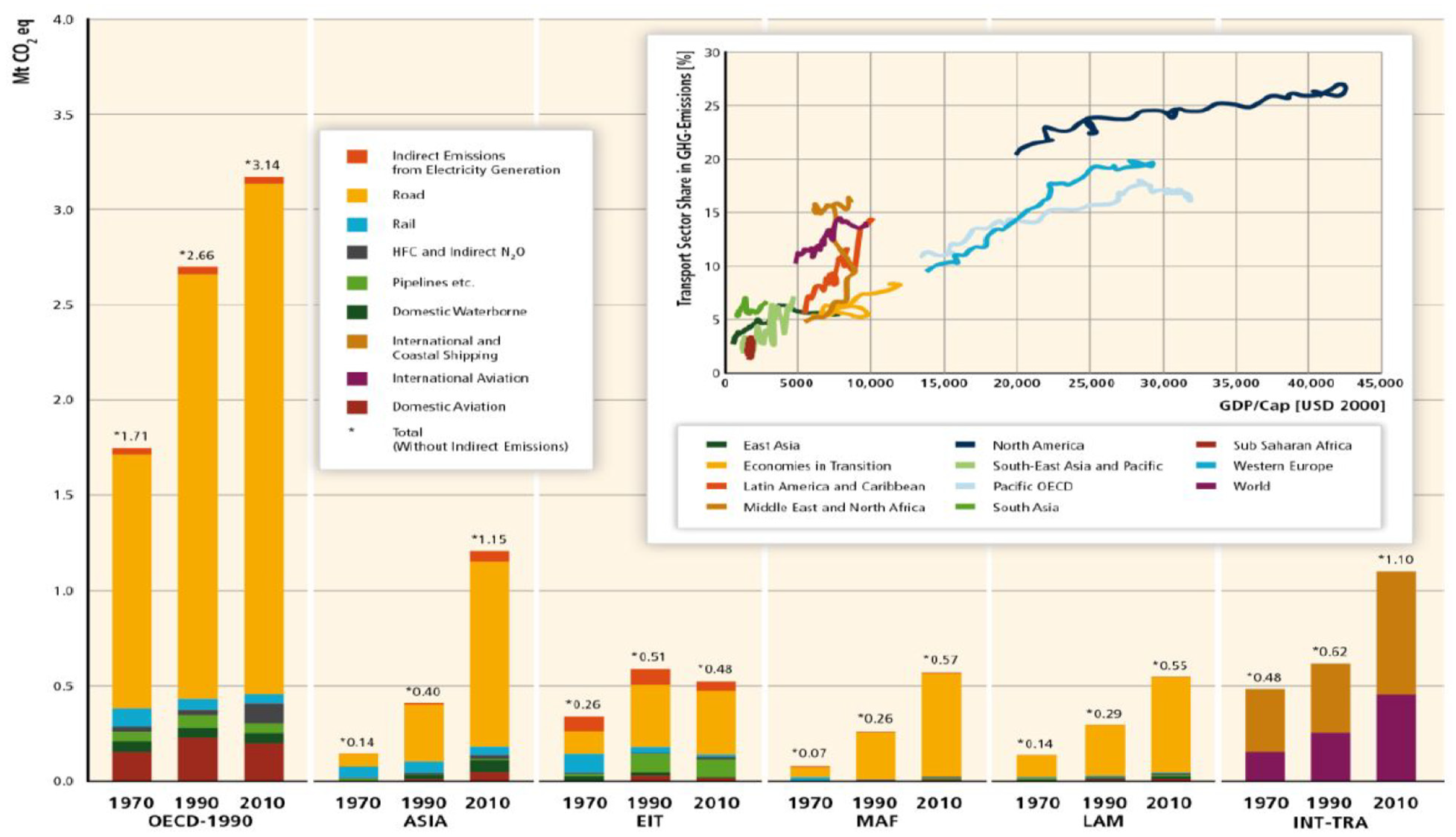

Figure 1 shows the evolution of transport GHG emissions over time by region: Organization for Economic Co-operation and Development (OECD-1990), Asia, Economies in transition (EIT), Middle East and Africa (MAF), Latin America (LAM), and International transport (INT-TRA). In the main graph, these are segmented by type of transport (including road, rail, air, and shipping), while the insert depicts the contribution share of transport sector CO2 emissions versus the GDP per capita by geographic location. 8 The chart clearly depicts that road-based emissions contribute the greatest amount to the overall total. It is also evident that these have been growing across all geographies in the times considered.

GHG emissions from transport by geographic location in 1970, 1990, and 2010 segmented by type of transport. 8

Importance of the automotive sector in the environmental context

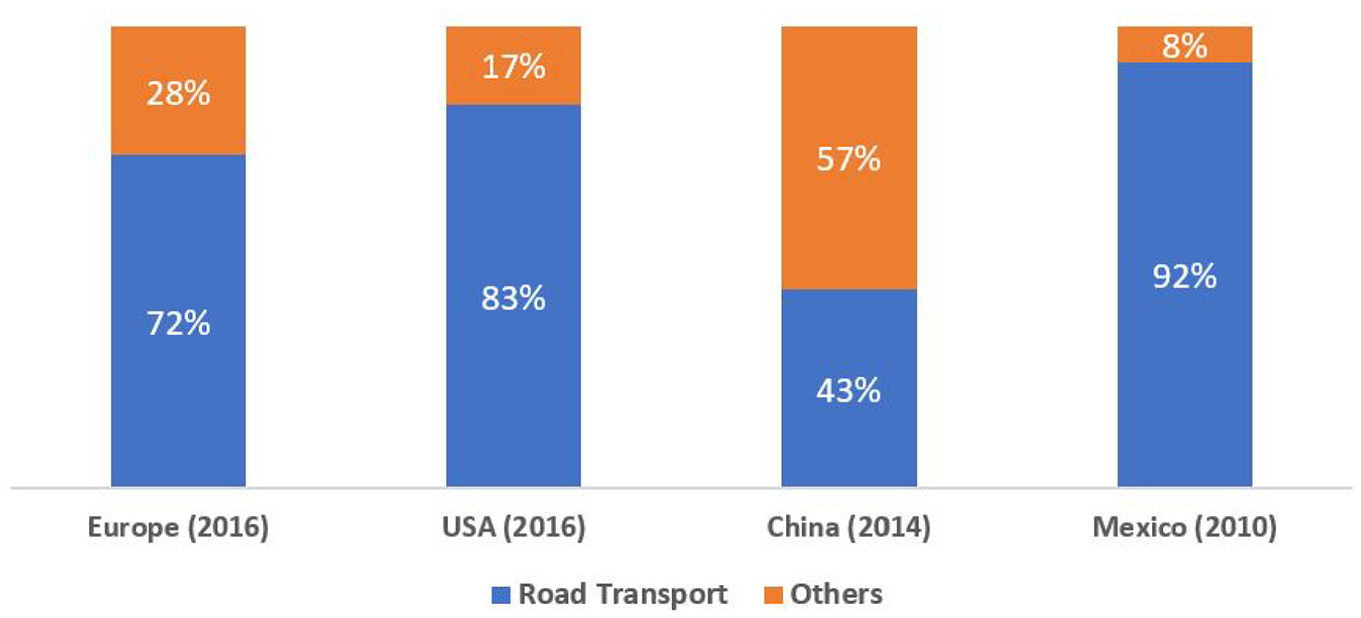

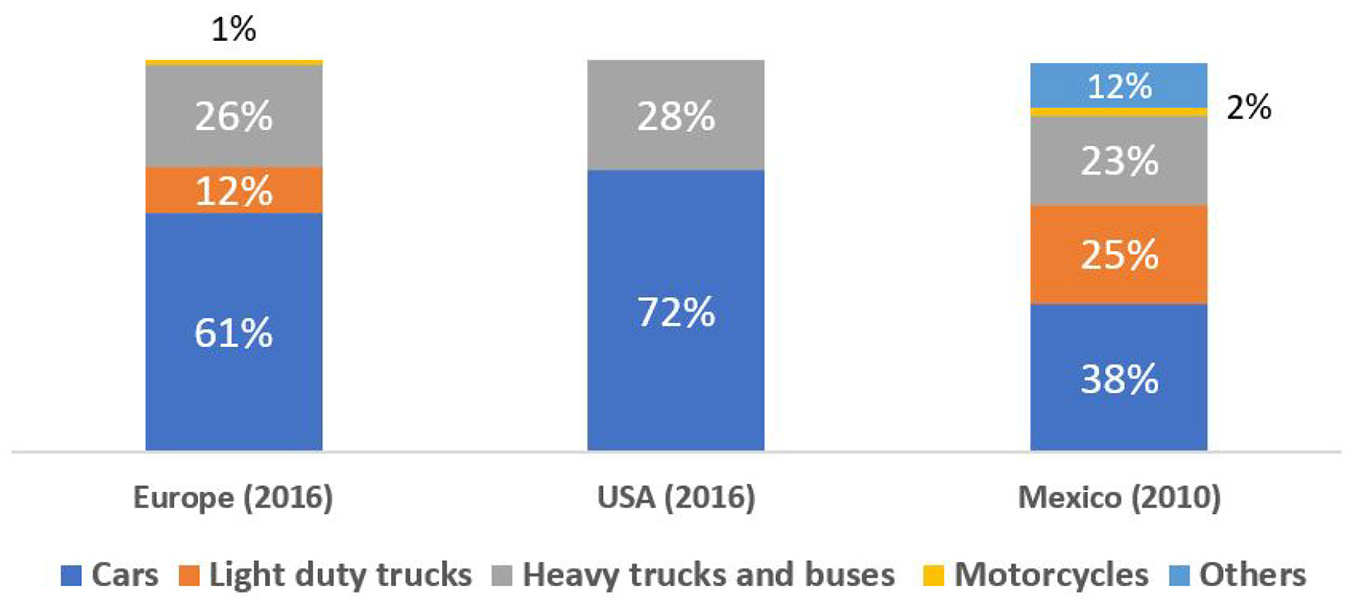

Referring specifically to the transport sector, there was a global rise in CO2 between 1990 and 2016, mainly due to a peak in travel demand which saw a worldwide 45% increase in the average distance traveled by light and heavy duty vehicles due to population growth, economic growth, urban sprawl, and periods of low fuel prices. 23 Hoen et al. 26 conclude that the main opportunity for diminishing the production of CO2 by the transport sector is through vehicle power train alternatives driven by renewable fuels. Globally, evidence shows that transport sector GHG emissions targets are the most challenging to meet. 27 In the EU, road transport is the only sector which continues to show growth in GHG emissions; and in the USA, transport GHG emissions reductions are lagging compared with other sectors. 28 In the period between 1990 and 2013, the Chinese road transport sub-sector has had an almost eight-fold growth in CO2 emissions compared to an average five-fold growth from other sectors. 28 Road transport is the main GHG emissions contributor in the transport sector,9,23,25,28–30 as shown in Figure 2, with passenger cars contributing the largest proportion (Figure 3).

Targets of decarbonization

The first conference on climate change, in Villach, Austria in 1985, heralded a wave of commitments, analysis, and the setting of policies and targets toward decarbonization, driven by multinational organizations and bodies such as the United Nations (UN) and the Organization for Economic Co-operation and Development (OECD) with their respective research members such as the Intergovernmental Panel on Climate Change (IPCC), International Energy Agency (IEA), and the International Transport Forum (ITF). In 2015, the 21st conference of the parties (COP21) saw the Paris agreement as the first international climate consensus with mitigating obligations between all countries. 31 The Paris agreement set a target to keep the average increase in temperature in this century below 2°C above pre-industrial levels and to pursue efforts to limit the temperature upsurge to 1.5°C. 32 More than 170 countries agreed to submit their nationally determined contributions (NDC’s) in terms of CO2. 31

The Paris agreement set GHG emission reduction targets for which strategies such as increasing energy efficiency and switching to low-carbon fuels will be required, along with actions to tackle non-energy emissions. 33 In light of these conclusions, the international community has approached these targets from three directions: GHG emissions mitigation, use of renewables, and energy efficiency.

To meet these targets, it is evident that specific measures must be implemented in the transport sector. 34 Strategies to address this need include improvements in fuel efficiency of internal combustion engines, reductions in amount of travel, and, perhaps most importantly, a focus on alternatively fueled vehicles such as Plug-in hybrid electric vehicles (PHEV), Battery electric vehicles (BEV), and Fuel cell electric vehicles (FCEV). Alternatively fueled vehicles, in particular, have the potential for profound effects on the automotive after sales market.

Policies and instruments related to the decarbonization of transport

Addressing climate change requires effective policies which involve both mitigation and adaptation strategies. Policies are usually focused on reduction of GHG emissions (mitigation) and minimizing the potential impacts of any human activity (adaptation). 35 The aim of any mitigating policy is the reduction of GHG emissions from the transport of goods, services and people, and belongs to the global spectrum, while the reduction of potential impacts from the transport system on climatic changes fits in adaptation policies and belongs to the local scope. 35 A successful transition to decarbonized transport requires a set of policies to be established and adopted on both the demand and supply sides. 36 Electrification of vehicles and the discouragement of car use and ownership have been identified as the most important decarbonization strategies being deployed, 11 and they have the potential to cause significant impacts for car manufacturers and the broader automotive industry, which will in turn impact upon the after sales market.

Automotive after sales

As noted above, after sales refers to the supply of services to the customer once the good has been sold. 12 An after sales strategy involves warranty provision, extended service contracts, repair and maintenance services, and spare parts. 12 The importance of automotive after sales services is being increasingly recognized in the industry as car brands and original equipment manufacturers (OEMs) have realized that they generate more profit (Figure 4). Coupled with this, after sales businesses show advantages such as stability during times of crisis, independence from economic situations, high margins, and the ability to develop ongoing relationships with customers and better understand their needs. 15

Impact of after sales on automotive industry profits, Adapted from Gissler and Müller. 16

As an example, cars continuously require filters, fluid changes, tires, absorbers, brake pads, and other components as they are used by their owners. There is evidence that suggests that the revenues generated by after sales service and spare parts go beyond three times the value of the original acquisition. 37

As noted above, after sales businesses require ongoing growth in UIOs, and the more vehicles a brand network manages to put on the road, the more service and spare parts turnover these brand networks will generate. Additionally, after sales is an enabler for beginning a long term relationship with customers12,38 and a transparent strategic driver for customer retention. 37

The automotive sector operates in a fast-changing environment influenced by competition, customer demand, and the implementation of new technologies, which means an increase of velocity in product cycles. 39 Therefore, new technologies do not only come in the new cars and vehicles, but must be addressed in new workshops and garages, and in electronic spare parts management. 40

Traditional business lines

There are three main areas that comprise after sales businesses: Customer services, spare parts, (which involve their own specialties), and accessories.

Customer service

Automotive customer services are those activities that generate any benefit to the vehicle owner during the life cycle of the car. 39 Services can be divided into technical and non-technical categories. Technical services include maintenance, repair, overhaul, installation or body, and paint restoration. 39 Pre-sales and sales incorporate all the non-technical services which support promotion, marketing, and sales of the vehicle, such as financing, insurance, and customization of the vehicle. 39

These processes and services have as their main resources: staff, information, infrastructure, and technical equipment, 39 which involve fluctuating technicians’ workloads, and internal training, instruction, required materials, tools, workshop formats, and changing working environments. 38

Spare parts

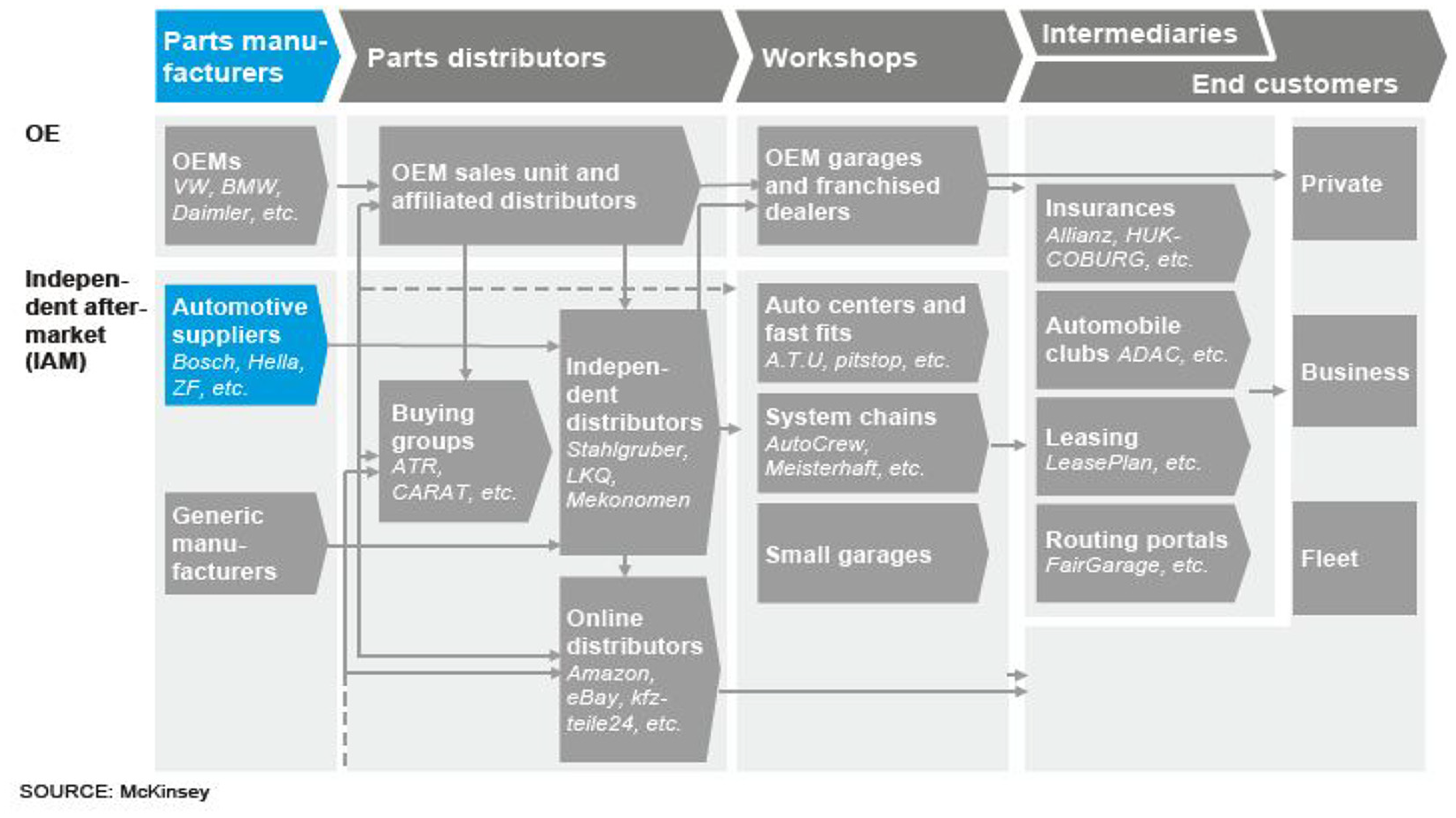

Demand forecasting, parts management, parts production, distribution, and storage are functions included in the spare parts business, which can be clustered and examined in two streams: physical (which involves stock warehousing and transport) and informational (containing order processing and spare parts replenishment). 41 Spare parts businesses and the automotive aftermarket are integrated by five stakeholder groups (parts manufacturers, parts distributors, workshops, intermediaries, and end customers) and two supplier models, original equipment manufacturers (OEMs) and the independent aftermarket (IAM) (Figure 5). These stakeholder groups and supplier models appear consistently in any geographic context, interacting with each other no matter the regional level of integration and firm size. 42

The after-market stakeholders and supplier models flow. 42

Bijl et al. 41 establish the reduction of costs as the main objective in the automotive industry, and this objective can be met by the optimization of physical and informational flows. Most strategies and tactics support the reduction of spare parts inventories to a minimum, supported and aided by robust information systems.

Accessories

The accessories business contains parts and products to satisfy supplementary customer requests on areas of merchandise, technical equipment, and customization of products 15 such as entertainment systems, radios, GPS, upholstery, aluminum wheels, etc. For purposes of this paper, accessories will be considered with spare parts due to them sharing similar specialties such as sales, marketing, and inventory control.

Policies to incentivize vehicle electrification

Electrification of vehicles is a strategy stimulated by the European Commission to decarbonize transport. 26 EVs, however, can have serious impacts on automotive after sales due to this alternative power train delaying or reducing the number of visits of car owners to workshops and garages, which could diminish the after sales income in the automotive sector. 19

As noted above, a number of policies have been enacted in countries worldwide to reduce environmental impacts of vehicles. While many of these are primarily focused on reducing overall vehicle ownership and use, a subset is concerned with encouraging a shift from internal combustion engine vehicles to electric vehicles. For example, in 2010 the European Union declared a policy intended to promote their leadership in clean and efficient vehicle development and reduce transport dependency on fossil fuels. 36 The EU is supportive of electro-mobility projects which involve international standardization of recharging infrastructure and development of electric vehicle technologies, encouraging the use of low-carbon electricity from the grid.

Although in 2016 the European Commission released communication encouraging technological neutrality, it is evident that this communication is inclined toward electric mobility. 43 Similar efforts have been undertaken in the United States, which in 2009 released a legislative act that supports the development of alternative fuels and advanced technologies to support the nation’s energy security. In addition to this national policy, several states (most notably California) have deployed measures supportive of electric vehicles, such as dedicated lanes or parking places reserved for EVs. 44

In the case of Japan, the strategy has been to increase the electrification of road transport by using fiscal incentives; starting with dissemination from the government fleet, then coming downward to municipalities, taxis or car-sharing systems and ending with private owners. 36 In China, the main drivers to encourage the electrification of road transport are to keep the automotive industry on an upward trend, to minimize the dependency of imported fossil fuels and to reduce the pollution caused by cars. 36

Potential Impacts of decarbonization policies on automotive after sales

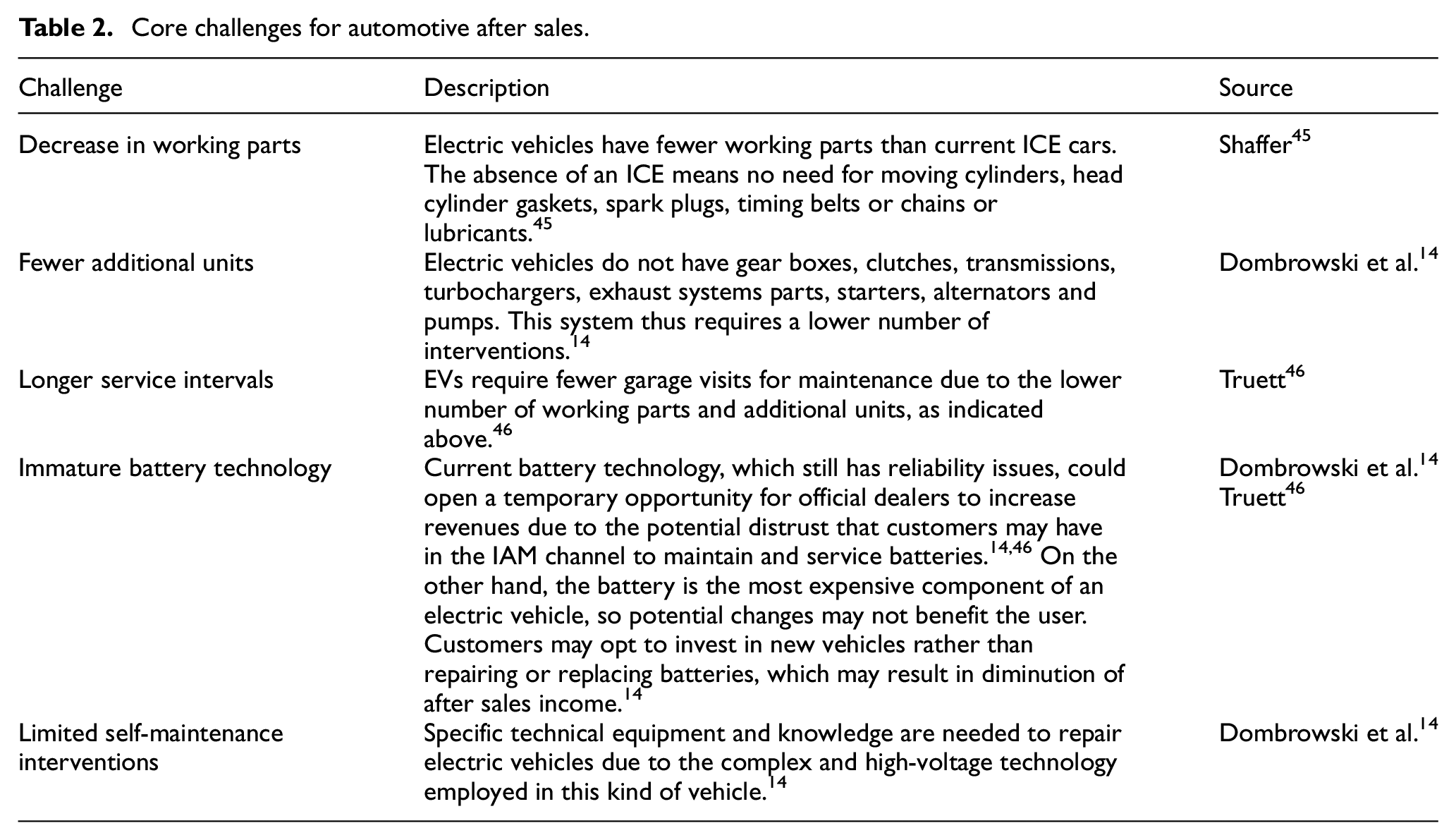

The electrification of transport and the EV industry are currently in a maturation period, developed and supported by governments and their public policies; however, the electric power train market penetration rate will depend not only on emissions regulation, but also on factors such as fuel and battery price. 34 The transition towards electric mobility generates five core challenges for automotive after sales, as shown in Table 2.

Core challenges for automotive after sales.

Other studies have also identified challenges associated with human resource training, customer retention, and business models.18,46–48

Improvements in vehicle technology can generate longer service intervals, which reduce maintenance and repair interventions as shown in Germany, which saw a 14% reduction of employees in dealers and workshops between 2000 and 2013. 47 Preliminary research indicates that BEVs require a drastically lower work load in repair interventions only compared to PHEVs, which require lower load work in both repair and maintenance activities. Human resource safety also has the potential to be a major issue in workshops, as new technologies will require higher staff qualifications and competencies. 47

Carlisle & Co., a Massachusetts-based consultancy firm, conclude that if service departments lose periodic maintenance interventions it is likely that customer retention and loyalty will decrease. 46 This is due to the importance of after sales in creating a bond between customers and brands, and their role in brand-building during the product life cycle. 12 The after sales service is a channel to find customer needs and a strategic driver for customer retention. It is one of the continuous ties that customers have with a brand. 37

EVs appeal to fleet owners due to their relative lower total cost of ownership (TCO) in comparison to ICEs as a result of lower fuel consumption and maintenance costs. Though they are currently generally more expensive than ICEs, EVs and their lower TCO provide opportunities for new business models to appear in the landscape. For example, in car sharing models the initial purchase price of the car is removed for the user, and fleet operators are attracted because of lower fuel and maintenance costs as well as the potential to have higher vehicle utilization rates, especially in densely populated areas when compared with private cars. 34 These new business models have the potential to bring new players like digital platforms to the after sales market and increase the bargaining power of current stakeholders, such as fleet operators who are projected to provide 20% of spare parts expenditure by 2025. 49

The future of ICEs – dying or a contender?

As noted in Table 2, ICEs currently have a number of advantages over EVs from the after sales business profitability point of view. The additional maintenance and repair functions, alongside associated technical labor interventions, associated with ICEs contribute 45% of European after sales income and spare parts generate the other 55%. 42

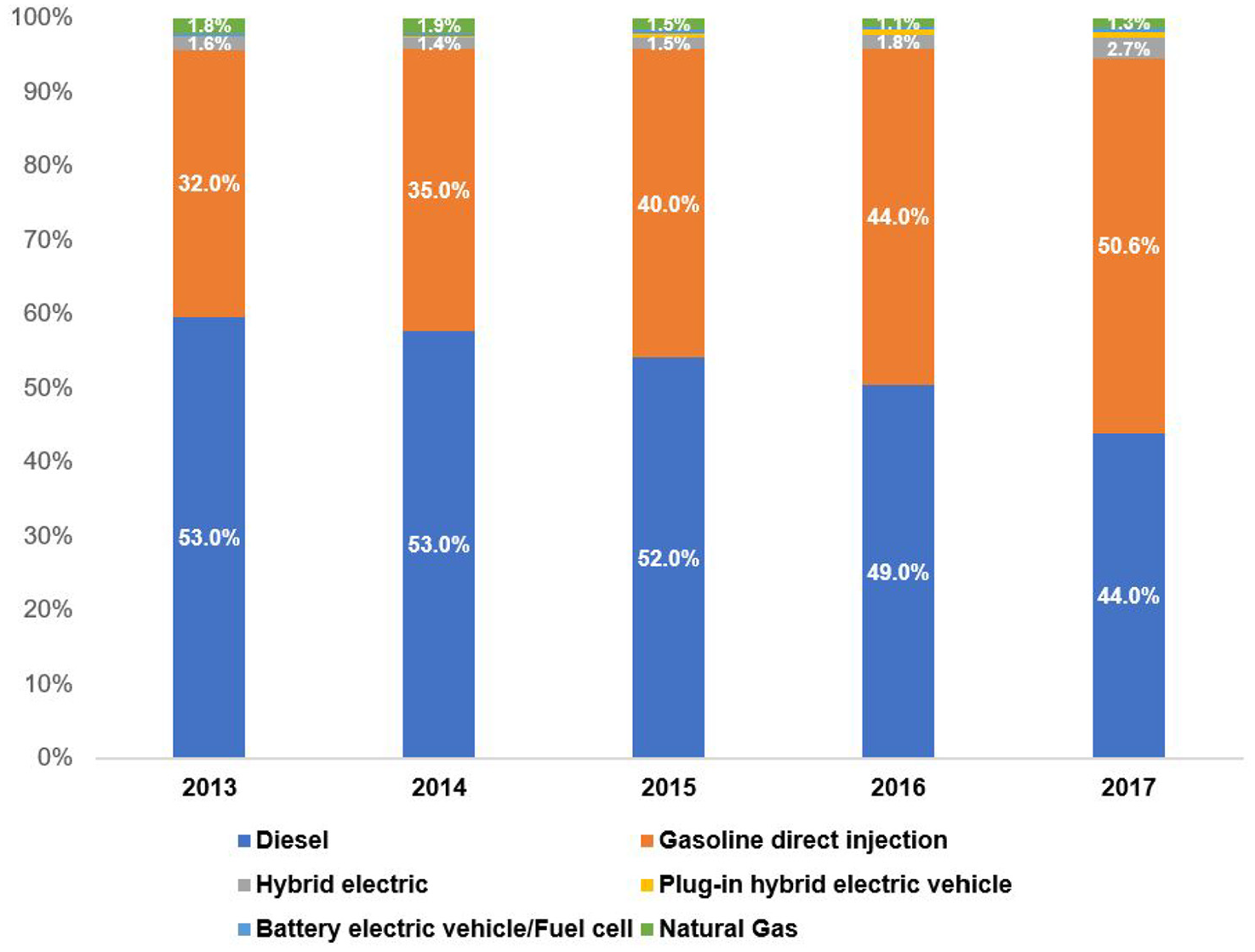

The 2017 share of ICEs (excluding natural gas) in Europe was 94%, while hybrid electric vehicles (HEV) represent only 2.7%, followed by plug-in electric, battery electric, and fuel cell vehicles with a 1.4% share of the market and a 1.3% share held by natural gas. 50 ICEs have improved their fuel efficiency in recent years, which represents additional challenges and doubts about the predominant technology, which could cause barriers to the increase of the electric vehicle market share. 51 Although electric cars will claim more importance in the future, the likely size of this role is not yet known, nor is the rapidity of uptake as Figure 6 shows. In the meantime, ICEs will have the opportunity to evolve, as seen, for example, in Mazda’s announced breakthrough in gasoline engines that could make them about 30% more efficient than their current models. 52

European new cars market share. Adapted from Mock. 50

It is likely that the ICE power train will remain prevalent in the near future. However, in the long-term numerous technologies (including electric vehicles) will be present in OEM’s portfolios. Public regulation and TCO developments will be decisive about the adoption of power train technologies. 34

Summary

This paper has demonstrated that policies related to the decarbonization of transport will influence car ownership, both in total and in type. Fewer units in operation (UIOs) means a lower number of cars coming to workshops and garages for maintenance and repair interventions, and instruments connected to the dissuasion of vehicle use would cause fewer visits (throughputs) to workshops per UIO. Strategies to increase the adoption of electric vehicles will also likely reduce visits to garages per UIO, and will require fewer of the working parts and additional units that currently represent between two thirds and three quarters of the current ICE vehicle service revenue. 46 Furthermore, all these effects will reduce the labor required for services.

Many countries have employed strategies and policies to increase the use of electric cars with the primary intention to reduce environmental impacts. Energy security and industrial policy related to international competition are sometimes also invoked depending on the country. 36 Current after sales business models, no matter the geographic context or level, consistently involve the same stakeholders, thus the substantially lucrative automotive after sales business is jeopardized by the potential growth of electric vehicle market share.

Uncertainties about predominant future power train technologies remain and the shift to EVs does not seem to be straightforward. 53 This suggests that the geographical conditions of regions and countries will play a major role in the definition of the prevalent power train technology. Furthermore, KPMG, 54 in its annual survey, found that the mineral resources profile of each country will decide the type of power train technology to be predominant. It is anticipated that countries such as the USA, with high degrees of raw materials such as oil and gas, will stay with ICEs and fuel cell technology, while nations with high electrical energy capacity, such as China, will choose electric power trains.

Many of the executives surveyed for the KPMG report agree that the technological agenda will primarily be driven by regulators rather than OEMs as it was in the past. 54 The impact of EVs on decarbonization is subject to the geographic and socio-political characteristics of each country; for example, while Norway can supply most of its energy to charge electric cars from clean energy sources, Poland could reactivate the coal mining industry in order to support the demand of electricity for EVs, to say nothing about nuclear electricity in France, which is one of its main power sources. 53

As presented in Table 2, the traditional functions of automotive after sales are significantly challenged by any of the decarbonization strategies currently being promoted around the world, namely: discouragement of car ownership, dissuasion of car use and the adoption of EVs. However, there is a high degree of uncertainty regarding pathways to decarbonization in different countries and this is influenced by issues of energy security and industrial policy interests. This uncertainty encompasses doubts and differences between nations regarding the likely predominant power train in the future and the potential longevity of traditional ICE vehicles.

Conclusions

The review finds that there has been limited research on the impacts of transport decarbonization strategies on after sales markets. Areas of potential impact identified include reduction of working parts and associated labor needs. Although there is not yet a clear vision about when these potential impacts will happen, it is clear that in a potential scenario where EVs become predominant, the frequency of vehicles visiting workshops will be lower and the parts to be replaced will be dramatically reduced. Questions about how to quantify the impacts and at what point the volume of EVs in the total fleet would negatively impact the traditional after sales business (in terms of income and profit) should be the subject of future research, as well as ways to mitigate detrimental impacts.

Policies to discourage car ownership and use and to incentivize an increase in the EV market share will impact upon traditional after sales business models. Priorities regarding national energy security and national industrial policy will further shape the future of alternative power train technologies. Currently, there is no clear projection about a dominant electric power train technology in the long term. The availability of natural resources will frame the choice of which technology will be predominant. For the short term, it is evidenced that ICEs still have a predominant role.

Further research is needed to assess impacts of changing vehicle technologies on automotive after sales areas such as the spare parts supply chain, human resource training, investment in workshop infrastructure, entrance of new players and new business models. These could be evaluated under different technological scenarios in terms of alternative power trains such as: BEV, PHEV, and FCEV or even ICEs, which seems to remain present in the automotive landscape depending on regional factors. Other potential characteristics of the after sales business requiring future study are customer retention and the repurchase cycle.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.