Abstract

This article investigates the association between UK higher education institutions (HEIs) long- and short-term performance measures, and the pay of vice-chancellors/principals (VCs) in an era of intense neoliberalism/financialisation of HEIs, and consequently ascertains the extent to which the VC pay–performance nexus is moderated by VC characteristics. Using a longitudinal sample of UK HEIs, our baseline findings suggest that HEIs that prioritise meeting long-term social performance targets tend to pay their VCs low pay packages, whereas HEIs that focus on achieving short-term reputational performance targets pay their VCs high pay packages. We show further that the VC pay–performance relationship is moderated/explained largely by VC characteristics. Our findings are robust to controlling for alternative governance mechanisms, endogeneities, alternative performance measures and different estimation techniques. Our findings offer empirical support for optimal contracting and prestige theories with significant implications for the sector.

Keywords

Introduction

The higher education (HE) sector has, and continues, to experience rapid neoliberal/financialisation reforms, not only in the UK, but also worldwide (Gerber and Cheung, 2008). Specifically, the HE sector is gradually moving towards private sector-oriented sources of funding, and this is often mainly due to a significant cut of state funding available to HE institutions (McCaig and Lightfoot, 2019). Additionally, the HE sector is shifting towards a more market-orientated approach through the implementation of policies that are aimed at promoting student choice and competition (Geiger, 2006).

The financialisation/marketisation of higher education institutions (HEIs) has negative consequences for the HE sector (Heery, 1998). These negative effects include, for example, rapid increases in: (i) tuition fees, borrowing and loan interest payment for students; (ii) financial debt for HEIs; and (iii) fixed-term contracts, casualisations, redundancies, workload pressures and perennial strikes by staff unions (Geiger, 2004). By contrast, there has been sharp reductions in: (i) staff pension entitlements, morale and welfare; (ii) state funding; and (iii) graduate job opportunities (Taberner, 2018). These challenges have been noted to pose a serious threat to the long-term sustainability of the HE sector (Walker et al., 2019).

Additionally, the increasing financialisation/marketisation of the HE sector has resulted in shifting the focus of HEIs from delivering on their original long-term social transformation and civic responsibilities mandate (Hurt, 2012) (e.g. reducing gender pay/disability/gender/age/BAME employment gap/student dropout rate and widening access and participation for students from poor and disadvantaged backgrounds) towards pursuing short-term reputational performance targets in order to generate income (Taberner, 2018) (e.g. enhancing national/international reputation) (Geiger, 2004). The financialisation/marketisation of the HE sector has, therefore, appeared to have encouraged VCs to inherently focus on achieving short-term observable (metric-driven) performance targets (Walker et al., 2019), and this, arguably, seems to have turned VCs to behave as value-maximising agents, like CEOs of commercial corporations.

Discernibly, the consequences of HE financialisation/marketisation have, arguably, increased media debate and public attention about the fairness of VC pay, especially over the last five years. 1 For example, the UK’s highest-earning VC of the University of Bath resigned her post in 2018 following a pay controversy (Grove, 2018). Similarly, it was announced in 2018 that the VC of Bath Spa University received a payment of £808,000 in her final year, thereby generating increased debate over VC pay (Grove, 2018). Additionally, the VC of De Montfort University resigned his post in 2019 following increased media publicity about the significant increase in his pay in 2018. Similar intense public debates relating to the pay of senior HE sector managers are common in other countries, such as Australia, Canada, New Zealand and the US. These controversies/debates have, consequently, resulted in an increased focus by state bodies, regulatory authorities and professional associations, especially in the UK on VC pay (e.g. UK Parliament, Committee of University Chairs (CUC) and Office for Students (OfS)). For example, the CUC published its first governance code in 1995 (latest 2020; CUC, 1995 to 2020) and a separate HEI senior staff remuneration code in 2018 (latest 2021). These codes recommend that VC/senior manager pay packages should be fair, appropriate and linked to the performance of individuals/institutions. Similarly, the OfS and UK Parliament (Hubble and Bolton, 2019; OfS, 2019) published their independent report in 2019, which suggested that VC pay should be competitive, but high pay must be justified by high performance.

Meanwhile, and given that HEIs are expected to meet various short (e.g. annual national/international research/teaching rankings) and long-term (e.g. addressing key long-term societal challenges/inequalities) performance targets (Ballo, 2020; Dowsett, 2020), arguably and similar to large public corporations, the successful management of such complex institutions requires equally highly talented and experienced senior management teams, who will need to be sufficiently remunerated if they are to perform at their best (Boden and Rowlands, 2020). However, and due to the increasing competition and financialisation/marketisation in the UK HE sector, it has been argued that VCs are more likely to focus on meeting short-term performance targets, since such targets are less costly and quicker to achieve, in order to justify their often relatively high pay (Walker et al., 2019).

Theoretically, much of the existing literature that examines the link between pay and performance has relied on two main theories: optimal contracting (OCT) and prestige (PT) theories (Bebchuk et al., 2002; Focke et al., 2017; Malmendier and Tate, 2009). OCT suggests that highly paid managers are often subject to public scrutiny and criticism, and thus, they are likely to be motivated to improve the short-term performance targets of their institutions in order to justify their pay (Heery, 1998), and hence, OCT expects HEIs that focus primarily on setting and meeting short-term performance targets to pay their VCs high pay packages. 2 Specifically, and with increasing corporatisation (raising funds through traditional debt/bond markets) and managerialism, alternative corporate style pressures and agency problems, such as managerial short-termism and opportunism, can emerge (Geiger, 2006). For instance, in order to protect their own pay rewards and respond to critical stakeholder demands (banks/lenders, government, students and trade-unions), market-driven HEI managers may be motivated to take knee-jerk/myopic decisions that can help meet short-term performance targets (financial surplus and annual research/teaching rankings), but such decisions will impact negatively on long-term performance (graduate outcomes, BAME/disabled/female attainment/employment/pay gap and widening access to poor/less privileged students).

On the other hand, PT suggests that socially/community-oriented institutions are often more concerned about promoting good social relations and networks with the various groups of stakeholders in order to improve their reputation and long-term sustainability (Focke et al., 2017; Malmendier and Tate, 2009). This implies that HEIs that focus on meeting long-term social performance targets are likely to pay their VCs low pay packages. This is because committing to such long-term social performance targets can be costly in terms of investment, as well as likely to take a relatively longer time to impact on social performance (Magnusson, 2016; Malmendier and Tate, 2009). Thus, PT predicts that HEIs that prioritise setting and achieving long-term social performance targets are more likely to pay their VCs low pay packages.

Despite the increased controversy/debate relating to VC pay within UK HEIs and worldwide, empirical studies examining the impact of HEIs’ performance on VC pay are surprisingly rare, but particularly acute when it comes to studies that further explore the extent to which VC characteristics can moderate the VC pay–performance relationship. In particular, almost all of the existing empirical studies have been conducted in profit-oriented organisations (Jensen and Murphy, 1990). By contrast, studies examining whether executive pay is linked to performance in non-profitable organisations are rare (Williams et al., 2020). In terms of the HE sector, and to the best of our literature search, none of the existing studies has examined the link between both short- and long-term social performance and VC pay, nor the moderating effect of VC characteristics on the pay–performance nexus. 3 This has, arguably, impaired current understanding of whether VC pay is linked to performance in HEIs. Nevertheless, this is an important academic and policy issue because unlike the current, often emotionally charged, but non-evidence-based public debate, our study can offer different and new insights by providing serious empirical evidence relating to the extent to which VCs are fairly/unfairly paid for their performance.

Consequently, and given the noticeable gaps within the existing literature, our study seeks to extend, as well as make a number of new contributions to the extant literature. First, we contribute to existing research by providing new systematic evidence on the levels of VC pay among HEIs, with specific focus on the UK. Second, we contribute to the current broader public and policy debates relating to the increased financialisation/marketisation of the UK HE sector by discussing the consequences arising from these reforms, with specific focus on VC pay and performance. Third, we contribute to the extant literature by providing first-time evidence on the VC pay–performance nexus in HEIs, and this is done by examining the impact of HEIs’ short- and long-term performance proxies on VC pay. Finally, our study contributes to the extant research by investigating the extent to which VC characteristics can moderate the link between VC pay and HEIs’ performance.

The rest of the article is structured as follows. The next section will review the literature and develop hypotheses. The following sections will present the methodology, and report and discuss the empirical findings; the final section concludes the article.

Theory, empirical studies and hypotheses development

HEIs’ performance and VC pay

Theoretically, prior studies examining the link between an institution’s top management pay and performance have largely utilised two theoretical perspectives: PT and OCT (Bebchuk et al., 2002; Focke et al., 2017). PT indicates that CEOs may sometimes be concerned with meeting the long-term social interests of stakeholders in order to boost their social status and future job prospects in the labour market (Magnusson, 2016; Malmendier and Tate, 2009). Further, PT (Focke et al., 2017; Malmendier and Tate, 2009) suggests that socially/community-oriented institutions are often more concerned about promoting good social relations and networks with the various groups of stakeholders in order to improve their current and future reputation. This implies that HEIs that focus on pursuing the long-term interests of stakeholders are more likely to pay their VCs low pay packages, since committing to such performance targets can be costly in terms of investment, as well as take a comparatively longer time to impact on long-term social performance (McGuire et al., 2003). In this case, PT predicts that HEIs that prioritise meeting long-term social performance targets are more likely to pay their VCs low pay packages.

Empirically, although VC pay has increasingly become controversial/debatable with considerable amounts of anecdotal evidence/suggestions indicating that VCs may be receiving unjustifiably high pay packages that may not usually be linked to the long-term performance of their institutions (Grove, 2018), none of the existing studies has examined the link between HEIs’ long-term social performance and VC pay. This offers an opportunity to contribute to the extant literature in this area of research. For example, and consistent with past evidence (Heery, 1998), McGuire et al. (2003) report a negative CEO pay–performance link for 374 US corporations. Of closer relevance to our current study are the findings of two studies by Milbourn (2003) and Focke et al. (2017), who report that some CEOs may accept low pay packages and pursue the long-term interests of stakeholders if doing so has the potential of improving their reputation and chances of securing more prestigious positions in the future labour market. With respect to the UK HEI context, and with increasing financialisaton/marketisation of the HE sector, market-driven VCs are expected to act in the best interests of powerful stakeholders (banks/lenders, government, students and trade-unions) by prioritising meeting short-term performance targets (financial/research/teaching rankings) over long-term social performance outcomes (BAME/disabled/female/employment/pay gap/widening access) in order to protect and/or increase their rewards. On this basis, and although no existing study has examined the link between VC pay and long-term social performance, we hypothesise that:

Hypothesis 1a: There is a negative association between VC pay and long-term performance in HEIs.

In contrast, OCT suggests that executive pay arrangements result from independent negotiation between strong boards and less influential directors, resulting in the creation of incentives schemes that aim to optimise managerial performance (Bone, 2006). OCT also indicates that linking rewards to performance can be problematic, since it can encourage opportunistic managers to focus on meeting short-term performance targets in order to justify their often relatively hefty pay (Heery, 1998). OCT, therefore, expects HEIs that opt for short-term performance targets may provide high pay packages to their VCs. This is because they are more likely to be able to offer evidence of achieving such short-term targets, and thereby justifying the payment of equally high pay packages (Jensen and Murphy, 1990). Empirically, much of the extant literature has traditionally been conducted in profitable organisations (Jensen and Murphy, 1990), and the findings of these studies support the predictions of OCT and propose that pay is positively influenced by an institution’s achievement of short-term performance targets. In addition, prior studies have largely focused on the impact of financial performance instead of non-financial performance on executive pay, and hence this provides a great opportunity to make new contributions to the literature by examining the effects of both financial and non-financial performance measures on VC pay.

For example, and using a sample of 70 UK publicly listed corporations over the period 1981–1989, Main et al. (1996) report a positive association between CEO pay and short-term financial performance. In addition, Brickley and Van Horn (2002) find a positive association between short-term financial performance and CEO pay among 2134 US non-profit hospitals. Of closer relevance to our current study, a few past studies have examined the effect of short-term financial (Johnes and Virmani, 2020) and/or reputational/ranking (Bugeja et al., 2021; De Fraja et al., 2017) performance on VCs’ pay, with the findings of most of these studies demonstrating that HEIs’ short-term performance is positively associated with VCs’ pay. For example, Walker et al. (2019), who focused mainly on VCs’ basic pay, report that research publication performance is positively related to VCs’ basic pay among UK HEIs. Similarly, Bachan and Reilly (2015) report that VCs’ pay is positively associated with HEIs’ financial and research income performance among 95 UK HEIs. Nevertheless, these studies have mainly focused on the short-term financial performance of HEIs, and surprisingly neglected the impact of HEIs’ long-term social performance on VCs’ pay. Therefore, the current study seeks to contribute to the extant literature by focusing heavily on long-term social performance measures, in addition to short-term financial/reputational performance measures and their impact on VCs’ basic, non-basic and total pay.

In terms of the UK HEI context, and as discussed earlier, the financialisation/marketisation of the HE sector has increasingly encouraged the adoption of metric-driven approaches (financial/teaching/research rankings) to assess the performance of HEIs. Consequently, this, arguably, has turned VCs to behave as value-maximising agents, like CEOs of corporations, by motivating them to focus more on short-term financial/non-financial performance-oriented metrics in order to justify their high pay, and thus we hypothesise that:

Hypothesis 1b: There is a positive association between VC pay and short-term performance in HEIs.

The moderating effect of VC characteristics on the VC pay–performance nexus

As noted above, prior studies have largely investigated the direct link between pay and performance among profitable organisations and reported mixed results (Focke et al., 2017; McGuire et al., 2003). A major weakness of these studies is that they failed to consider the moderating effect of senior management characteristics on this relationship. It has been argued that the extent to which a HEI performance can influence senior management pay may be contingent on VC attributes, such as damehood/knighthood and tenure (Breakwell and Tytherleigh, 2010). Consequently, this study seeks to contribute to extant literature by examining the moderating impact of VC attributes (damehood/knighthood, age, gender, academic discipline/specialism and tenure) on the pay–performance nexus. These five VC attributes have been selected due to two reasons, they: (i) can be objectively measured/captured (Breakwell and Tytherleigh, 2010); and (ii) have been examined by prior studies, albeit within different research contexts (Adams and Ferreira, 2009).

Theoretically, PT suggests that long-tenured, reputable and older directors often may be committed to meet and represent the expectations of stakeholders in order to maintain and improve their social status in the labour market (Milbourn, 2003). Hence, PT predicts that older, reputable and long-tenured VCs are likely to accept pay packages that are linked to their institutions’ performance, and this can impact positively on the pay–performance nexus. By contrast, OCT indicates that long-tenured, older and reputable directors often possess high status in the labour market, since they usually have greater skills, knowledge and experience that are necessary to business competitiveness and success (Brickley et al., 2010), and thus OCT expects that long-tenured, reputable and older VCs may receive high pay packages that may not necessarily be linked to their institutions’ performance, which can weaken the pay–performance nexus.

With respect to VC gender, and from a PT perspective, appointing female directors can enhance boardroom efficiency/independence by bringing diverse insights, perspectives and business contracts to a board (Adams and Ferreira, 2009), and this in turn can improve the pay–performance relationship. In contrast, OCT suggests that female directors tend to be less firm in their pay negotiations than male directors (Adams and Ferreira, 2009), and this in turn can weaken the pay–performance nexus. Further, and in terms of academic discipline/specialism, PT proposes that generalist directors tend to be more motivated to maintain and/or further develop their reputation within the job market (Bone, 2006), and thereby they may be more inclined to ensure that their pay reflects the performance of their institutions. By contrast, OCT indicates that generalist directors tend to have diverse experiences across different industries, greater expertise and better business networks than specialist directors (Custódio et al., 2013). Having such expertise is usually necessary to deal with uncertainty, operational complexity and competition (Milbourn, 2003), and thus they may receive high pay packages that may not necessarily reflect their institutions’ performance.

Empirically, there is a scarcity of studies investigating the moderating influence of managerial characteristics on the pay–performance relationship generally, but particularly in the HE sector, and thereby our study attempts to make original contributions in this area of research. The existing empirical evidence is generally consistent with the expectation of OCT and PT that HEIs’ top management attributes may moderate the link between pay and performance (Custódio et al., 2013). For example, Custódio et al. (2013) report that US public listed firms tend to pay generalist CEOs excessively high pay packages, which do not necessarily relate to performance. Similarly, Bebchuk et al. (2002) report that long-tenured managers often receive overly generous pay packages that do not necessarily relate to their performance among US publicly listed corporations. With respect to the age of directors, Brickley et al. (2010) report no link between CEO age and pay among 308 US non-profit hospitals. With reference to director reputation (damehood/knighthood), Milbourn (2003) finds that CEO reputation has a positive and significant moderating effect on the stock-based pay sensitivities among US publicly listed corporations. Finally, and in terms of executive gender, the findings of prior studies (Adams and Ferreira, 2009) suggest that gender diversity may enhance boardroom efficiency by increasing managerial monitoring, which can improve the performance–pay linkage. Therefore, and given that VC characteristics are expected to moderate the link between pay and performance, but no prior empirical evidence regarding this, our final hypothesis to be tested is that:

Hypothesis 2: VC characteristics significantly moderate the link between VC pay and long-/short-term performance in HEIs.

Methodology

Data and sample

To test our hypotheses, we first identified the list of all UK HEIs using the Higher Education Statistics Agency (HESA) website as at 31 July 2014. There were 164 HEIs, consisting of universities, university colleges and other HEIs. HEIs included in our final sample needed to have annual reports for all the period of investigation from 2009 to 2014 and this resulted in excluding 47 HEIs with missing annual reports for one or more years. Therefore, our final sample consists of 117 institutions made up of 3, 8, 16 and 90 Northern Irish, Welsh, Scottish and English HEIs (58 pre-1992 and 59 post-1992). We started our analysis in 2009 because the 2007/08 global crisis had led to significant cuts in terms of funding available to HEIs (Geiger, 2004), as well as the labour-intensive nature of manually collecting the required data. The analysis ends in 2014 because it was the last year for which the required data were available when our data collection started.

We utilised annual reports to collect data relating to VC basic and non-basic pay, community/social contributions index (seven items, each scored 0 or 1;

Research variables and model

To test H1a/b and H2, we created our research models and variables as follows. First, to investigate the VC pay–performance link (H1a/b), our main dependent variable is VC pay. Following classification provided by the CUC (2018/2021), we define VC pay as total pay, consisting of: (i) basic (salary); and (ii) non-basic (bonuses; healthcare, housing and transport allowance; pension contributions; and other in-kind benefits) pay. Further, and following prior studies (Schaefer, 1998), VC pay is scaled by HEIs’ total income to control for any possible size-effects. Second, our main explanatory variable is HEIs’ long- and short-term performance. We used four social outcomes to measure long-term social performance. First, we employed the HESA performance indicator relating to non-continuation in HE (NLHE) to capture UK HEIs’ support for student retention. Second, we developed a broader social contribution index, named Community/Social Contribution Index (CCI). The third social outcome is gender pay gap (GPG), which is measured as the average difference between males’ and females’ earnings divided by males’ earnings (Gerber and Cheung, 2008). Finally, and following classification provided by HESA and past evidence (Ballo, 2020), we computed the proportion of young academic and non-academic (PYS) staff to the total number of academic and non-academic staff aged 35 and under in order to measure HEIs’ contribution to the employment of young staff. 4

On the other hand, we use two main proxies encompassing various elements relating to reputation/teaching quality to measure short-term performance (Dowsett, 2020). The first set of short-term measures relating to reputation of HEIs comes from both QS and THE world university rankings. The second set of short-term measures relating to teaching quality comes from nationally published league tables (CUG; and GUG rankings).

Third, and to test our second research hypothesis (H2) relating to whether VC characteristics moderate the pay–performance nexus, we created interaction variables between the VC characteristics (damehood/knighthood status) (DAM), gender (GEN), age (AGE), educational background (EDU) and tenure (TEN) and HEIs’ long-term (NLHE, CCI, GPG and PYS) and short-term (QS, THE, CUG and GUG) performance measures.

Fourth, and given that several studies (Brickley et al., 2010) suggest that senior management pay can be influenced by several other individual governance variables, we included six governance mechanisms as control variables in our models. These variables are: the presence of an independent remuneration committee (PRC); the presence of a governance committee (PGC); executive management team size (EBSZ); executive management team diversity (EBDV); executive management team meeting (EBME); and change in VC (VC Change). Finally, we control for number of general HEI characteristics to reduce the possibility of omitted variable bias. These variables are: dummy for post-1992 (PST_92); size of audit firm (BIG4); leverage (LVR); liquidity (LQD); HEI size (HEIZE); growth (GRT); expenditure (CXP); HEI year dummy (HEIYD); and HEI country dummy (HEICD). For brevity, the list of all the variables used in our analysis and their full definitions/data sources are presented in the

Accordingly, we estimate our main models using a random-effects 5 estimator as follows:

where, VCP refers to VC basic, non-basic and total pay; HEIP refers to HEI short- and long-term performance; and CNTS refers to control variables, including the presence of an independent remuneration committee (PRC); the presence of a governance committee (PGC); executive management team size (EBSZ); executive management team diversity (EBDV); executive management team meeting (EBME); and change in VC (VC Change); dummy for post-1992 (PST_92); size of audit firm (BIG4); leverage (LVR); liquidity (LQD); HEI size (HEIZE); growth (GRT); expenditure (CXP); HEI year dummy (HEIYD); and HEI country dummy (HEICD).

Findings

Descriptive and univariate analysis

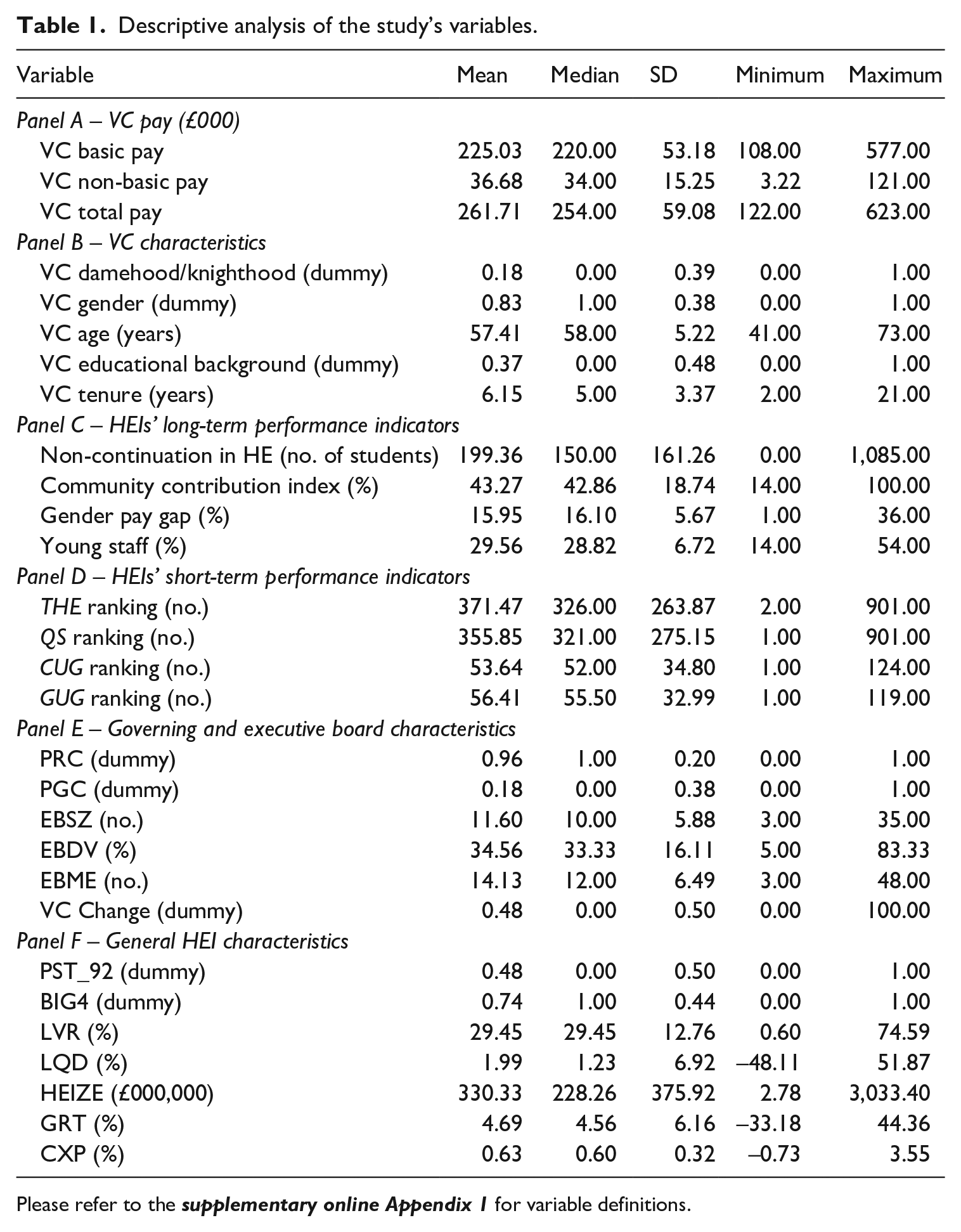

Summary descriptive statistics of the study’s variables are presented in Table 1. Overall, the results indicate that there is wide variability in the distribution of our variables. For example, Panel ‘A’ of Table 1 shows that VC basic pay ranges from a minimum of £108,000 to a maximum of £577,000, with a mean value of £225,030. Similarly, VC total pay lies between £122,000 and £623,000, with a mean of £261,710. Additionally, Table 1 suggests that VC non-basic pay forms a small fraction of total VC pay. Specifically, the mean VC non-basic pay of £36,680 only represents about 14% of the mean VC total pay of £261,710, whereas the mean VC basic pay of £225,030 represents about 86% of the mean VC total pay of £261,710. This evidence implies that VCs receive significantly higher basic pay compared with non-basic pay packages.

Descriptive analysis of the study’s variables.

Please refer to the

Panels ‘B–F’ of Table 1 also reveal that there is wide variability in the distribution of VC characteristics, HEIs’ performance and control variables among our sample. For example, and similar to the findings of Breakwell and Tytherleigh (2010), Panel ‘B’ of Table 1 shows that VC gender ranges between 0 and 1 with an average value of 0.83, implying that UK HEIs are dominated by male (83%) VCs. A detailed discussion of the descriptive statistics of other VC characteristics, HEIs’ performance and control variables is included in the supplementary

Multivariate analyses

HEIs’ long- and short-term performance and VC pay

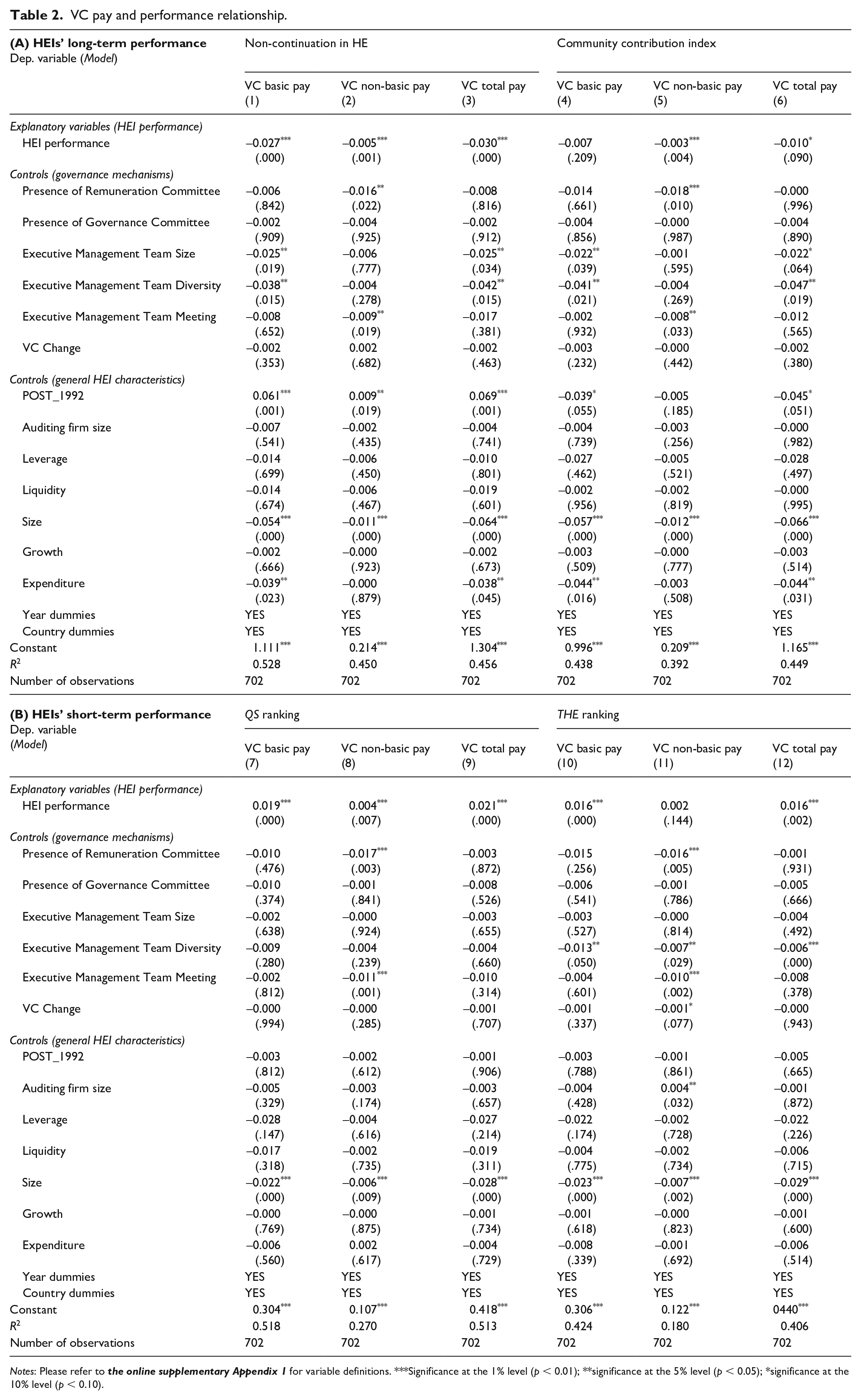

Table 2 presents the multivariate regression estimates of the effect of UK HEIs’ long-term (students’ non-continuation in HEI and community/social contributions) and short-term (QS and THE world university rankings) performance on VC pay (basic/non-basic/total). 6 Overall, the obtained results show that long- and short-term performance indicators are important in explaining the observed differences in the VC pay.

VC pay and performance relationship.

Notes: Please refer to

First, and with regard to the impact of long-term social performance on VC pay, the reported results in Models 1–6 of Table 2 indicate that HEIs that focus on setting and meeting long-term performance tend to pay (basic/non-basic/total) their VCs significantly lower pay packages than their short-term oriented counterparts. Specifically, the reported results in Models 1–3 in Table 2 indicate that student non-continuation in HE is negatively and significantly associated with VC pay, which offers new evidence that is in line with H1a, and the predictions of PT that HEIs with long-term orientation are likely to have a strong incentive to invest in order to improve student retention and continuation rates. This can boost their reputation, as well as attract more future students (Geiger, 2006), and this in turn can impact negatively on VC pay. Second, our results in Models 4–6 in Table 2 indicate that HEIs that focus on meeting the expectations of the wider community/society tend to pay low packages to their VCs, which is also consistent with PT expectations that VCs in long-term oriented HEIs are often more concerned with enhancing their social status and building better relationships with key stakeholders (government agencies, students, parents, donors, unions and the wider community), and thus they often tend to invest heavily in environmental and socially friendly activities (McGuire et al., 2003), which in turn can impact negatively on their pay packages.

Third, Models 7–12 present the multivariate regression estimates of the impact of HEIs’ short-term performance indicators (QS and THE rankings) on VC pay. Overall, the results indicate that VC pay is positively associated with HEIs’ short-term performance, irrespective of the performance or pay metric used. For example, the reported results in Models 7–9 and 10–12 (Table 2) reveal a significant positive effect of QS and THE rankings on VC (basic/non-basic/total) pay, evidence supporting H1b that UK HEIs that prioritise setting and achieving short-term performance targets tend to, on average, pay their VCs higher pay packages than their long-term oriented counterparts. This finding indeed provides new empirical insights relating to existing debates about the fairness of VC pay. Our findings also offer empirical support for the results of past studies (Bachan and Reilly, 2015; Bugeja et al., 2021; De Fraja et al., 2017; Johnes and Virmani, 2020; Walker et al., 2019), who report that VC pay is positively associated with short-term performance. Theoretically, this finding is consistent with the predictions of OCT that linking rewards to performance can be problematic, since it can encourage self-serving managers to focus on setting and meeting short-term performance targets in order to justify their often hefty pay (Heery, 1998).

The moderating effect of VC characteristics

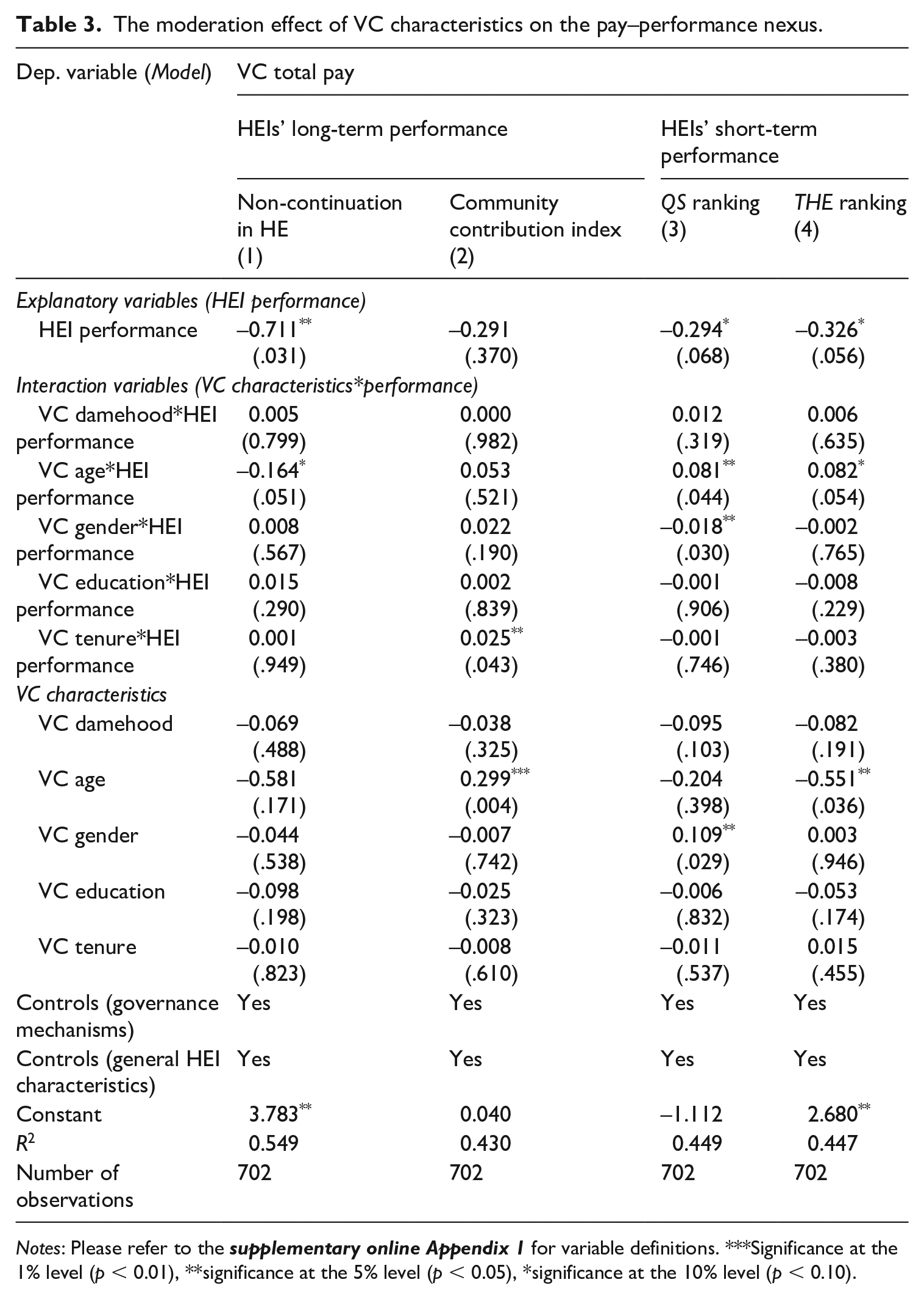

To further investigate the effects of potential moderators on the pay–performance link, we created interaction variables among VC characteristics, HEIs’ long- and short-term performance proxies, and the results are reported in Table 3. Noticeably, the interaction has improved the magnitude of the coefficients relating to the long-term (NLHE and CCI) and short-term (QS and THE) performance measures, which implies that VC characteristics significantly moderate the pay–performance nexus. This offers new empirical support for H2. For example, the magnitude of coefficients of NLHE and CCI have improved from −0.030 (Model 3) and −0.010 (Model 6) in Table 2 to −0.711 (Model 1) and −0.291 (Model 2) in Table 3, respectively, implying that VC characteristics generally moderate the link between HEIs’ long-term performance and VC pay. Further, the reported results in Table 3 (Models 3 and 4) indicate that the extent to which HEIs’ short-term performance influences VCs’ pay is contingent on VCs’ characteristics.

The moderation effect of VC characteristics on the pay–performance nexus.

Notes: Please refer to the

Regarding the interaction variables, our evidence reported in Table 3 suggests that VC characteristics have a moderation effect on the pay–performance nexus, which again supports H2. For example, and consistent with the predictions of PT (Focke et al., 2017; Malmendier and Tate, 2009), the coefficient of VC Age*HEI performance on VC total pay in Model 1 of Table 3 is negative and significant, implying that young VCs, particularly with increasing marketisation of the HE sector, are less willing to support policies and practices that promote social contributions of HEIs, and this can in turn weaken the link between pay and long-term social performance of HEIs. Similarly, our evidence indicates that VC age positively and significantly moderates the short-term performance–VC pay link in Models 3 and 4 of Table 3, indicating that young VCs are more likely to focus on meeting short-term performance targets in order to establish and/or boost their social status and job prospects in the labour market (Milbourn, 2003).

Further, the reported results in Models 1, 3 and 4 of Table 3 indicate that VC gender diversity negatively moderates the QS ranking–VC pay linkage, which is in line with H2 and predictions of PT that female VCs are more concerned with the wider social and public benefits of HEIs, and hence they are less likely to focus on meeting short-term performance targets (Adams and Ferreira, 2009), and this in turn can impact negatively on the short-term pay–performance relationship.

Additionally, the reported results in Model 2 of Table 3 indicate that VC tenure positively moderates the community contribution index–pay nexus. This positive moderating impact of VC tenure is consistent with the predictions of PT that long-tenured VCs are often committed to meeting and representing the expectations of stakeholders by supporting long-term social contributions of HEIs (Breakwell and Tytherleigh, 2010), and thereby they are inclined to ensure that their pay reflects the long-term social performance of their institutions. Finally, the insignificant impact of VC damehood*HEI performance (Models 1–4) on total VC pay do not provide support for H2, as well as OCT and PT theories.

Robustness tests

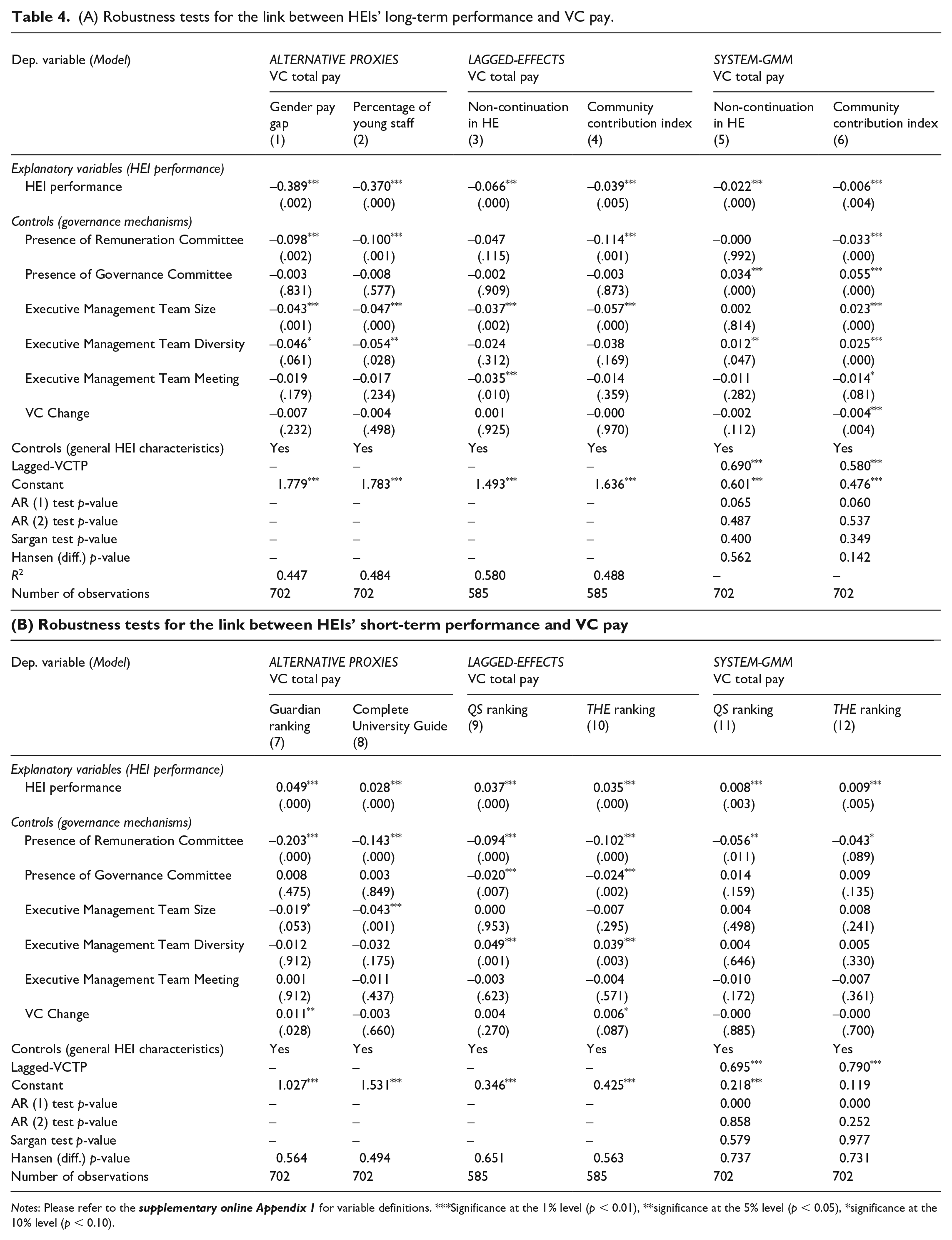

We perform different additional tests to deal with various types of endogeneity issues and the usage of different proxies of performance. First, and in order to identify whether our results hold for the usage of different performance measures, we used alternative long-term (GPG and PYS) and short-term (GUG and CUG) rankings. The results are presented in Models 1, 2, 7 and 8 in Table 4, suggesting that our findings appear not to have been affected by the usage of alternative long- and short-term performance proxies.

(A) Robustness tests for the link between HEIs’ long-term performance and VC pay.

Notes: Please refer to the

Second, to control for possible endogeneity problems that may arise from simultaneous relationships among our study variables (e.g. current year’s HEI performance can be affected by past year’s VC pay), lagged-effects are estimated in Models 3, 4, 9 and 10 of Table 4, whereby the current year’s VC total pay is affected by the previous year’s HEI performance and control variables. Using lagged-effects model helps to mitigate possible problems associated with simultaneity endogeneity, by ensuring that current values of VC pay cannot affect past values of HEI performance and control variables. The obtained results in Models 3, 4, 9 and 10 of Table 4 remain very similar to those that have been reported in Models 3, 6, 9 and 12 of Table 2, implying that our findings seem to be robust to the estimation of a lagged structure.

Finally, and although great efforts were made to mitigate possible endogeneity problems among our study’s variables by using lagged structure and random-effects models, Wintoki et al. (2012) argue that dynamic endogeneity can influence the association between dependent and independent variables, whereby the future values of the independent variables (i.e. HEIs’ short- and long-term performance) can be affected by the current values of the dependent variables (i.e. VC basic/non-basic/total pay), which in turn can be influenced by the past values of the independent variables (i.e. HEIs’ short- and long-term performance). Further, Wintoki et al. (2012) suggest that, and unlike random-effects, using dynamic-system generalised method of moments (GMM) helps in alleviating possible endogeneity problems associated with unobserved institution-specific heterogeneities (i.e. HEIs’ performance and VC pay can be jointly determined by unobserved HEI-specific heterogeneities, such as differences in VC talent, skills, network, reputation, experience; and differences in HEIs’ location, mission, size, business culture and governance arrangements). In addition, and different from random-effects regression models, dynamic-system GMM controls for potential simultaneous endogeneity by allowing past values of dependent variables (i.e. VC basic/non-basic/total pay) to affect the current values of the independent variables (i.e. HEI short- and long-term performance). Therefore, and to address any potential unobserved heterogeneities, dynamic and simultaneity endogeneity, and following prior studies (Bone, 2006; Wintoki et al., 2012), we conducted dynamic-system GMM estimation.

Dynamic-system GMM automatically generates its own internal instruments, which are derived from the lagged-values of the explanatory and dependent variables (Wintoki et al., 2012). We next performed different tests to check the validity of our instruments, including the Arellano–Bond test for first-order (AR1) and second-order (AR2) serial correlation, as well as the Sargan test for over-identification and the difference-in-Hansen test for exogeneity. As shown in Table 4, all of our Models (5–6 and 11–12) pass the second-order (AR2) serial correlation test for the validity of employed instruments. Further, the results of the Sargan test for over-identification and the difference-in-Hansen test for exogeneity indicate that our instruments are valid. The results reported in Models 5–6 and 11–12 in Table 4 have similar directional signs and levels of significance, and hence our results appear not to be driven by any endogenous associations.

Discussion and conclusions

Research contributions

This study has investigated the extent to which HEIs’ performance can impact on VC pay using a longitudinal sample of UK HEIs. Specifically, and relying on insights drawn from optimal contracting (OCT) and prestige (PT) theories, we examine the impact of both: (i) long-term; and (ii) short-term performance targets on VC pay, and consequently ascertain whether VC characteristics can moderate this relationship. In doing so, our study extends, as well as makes several new and original contributions to existing literature.

First, we offer systematic evidence for the first time on the level of VC basic, non-basic and total pay in the UK. We find that VCs in UK HEIs receive significantly higher basic pay than non-basic pay packages. Second, unlike much of the existing literature that has mainly been conducted in profitable organisations and focused mainly on financial performance measures (Jensen and Murphy, 1990), our study offers timely evidence in relation to the impact of HEIs’ long- and short-term financial/non-financial performance on VC pay. Our central evidence indicates that, on average, HEIs that commit to setting and meeting long-term social performance targets tend to pay their VCs less, whereas those that pursue short-term performace pay their VCs more. Specifically, our results indicate that VC pay is negatively related with HEIs’ long-term social performance, but positively related to short-term performance, and thereby offering support for the predications of both OCT and PT. In this case, our evidence extends existing findings that do not only show a positive link between VC pay and short-term financial performance (Johnes and Virmani, 2020; Walker et al., 2019), but also offers new evidence relating to the association between VC pay and long-term social performance.

Finally, this study contributes to the extant literature by offering new insights on the moderating effect of VC characteristics on the pay–performance nexus. Our evidence suggests that the link between performance and pay has improved in HEIs with older, gender diverse and long-tenured VCs. In contrast, our evidence indicates that VC status and education background have an insignificant moderating impact on the pay–performance nexus. Overall, our findings demonstrate further that VC pay is not only determined by the type of HEI performance (e.g. short-/long-term performance), but also other factors (e.g. VC/governance characteristics), with clear differences in their effects in terms of the direction, magnitude and statistical significance on the pay–performance nexus.

Research implications

Our findings have a number of important implications for the various stakeholders of HEIs, such as student unions, past, current and prospective students, researchers, governing boards, employee unions, policy-makers, regulators/governments and taxpayers. For employee unions, policy-makers, regulators/governments and taxpayers, the positive link between VC pay and short-term performance provides empirical support for the current intense public debate that suggests that the pay of VCs may not always be fair/linked to long-term performance of their institutions. In fact, our evidence indicates that for VCs that commit to setting and meeting long-term socially transformative performance targets (community contributions/widening access), they are likely to receive lower pay than their counterparts that prioritise the achievement of short-term performance targets (rises in annual research/teaching rankings). For governing boards, senior management, staff and student unions, there appears to be a need for greater input and scrutiny in setting and distinguishing between short- and long-term priorities and performance targets, with greater emphasis placed on rewarding achievement of such long-term targets in comparison to short-term performance. One way of enhancing decision-making, including setting and evaluating HEIs’ performance, may be broadening the senior leadership/management teams. In this case, our evidence indicates that women/ethnic minorities in particular are under-represented in senior leadership and management teams. Increasing the level of diversity within HEIs’ senior management teams and governing boards will be a step in the right direction. In addition, our moderating evidence indicates that young male VCs, who often replace older retiring VCs, are likely to push the logic of marketisation even further, as they are usually more concerned with meeting short-term performance targets in order to justify their pay, as well as to establish their own professional legitimacy. This finding implies that appointing older female VCs can be helpful in ensuring that UK HEIs deliver high long-term social performance that matches the pay of their VCs. Similarly, the positive moderating effect of VC tenure on the community contribution index–pay relationship suggests that long-tenured VCs are more committed to meet and represent the expectations of stakeholders, and hence they are likely to accept pay packages that are linked to their institutions’ long-term performance. This finding can serve as a motivation for UK HEIs to retain long-tenured VCs, who often have greater skills, experience and knowledge that are necessary to deal with uncertainty, operational complexity and competition in the HE sector. Our findings also have important implications for researchers, since we offer early evidence relating to the impact of HEIs’ long- and short-term financial/non-financial performance proxies on VC basic, non-basic and total pay. Our study further provides early evidence regarding the moderating effect of VC characteristics on the pay–performance nexus. Therefore, future studies may offer new insights by drawing on our current research in conducting their VC pay–performance research.

Our findings have implications also for, and/or contribute to, the broader national/international public/policy debates regarding the financialisation/marketisation reforms that have been pursued in the HE sector over the past decades, especially in fostering dysfunctional senior leadership behaviour and strategies. Specifically, our study provides evidence that suggests that increasing financialisation/marketisation of the UK HE sector has shifted HEIs from focusing and delivering on their original civic mandate of facilitating long-term social progression and transformation towards setting and achieving short-term financial surplus and reputational-oriented targets. For example, our findings indicate that financialisation policies may have encouraged the adoption of metric-driven approaches (teaching/research rankings) to assess the performance of HEIs, and this in turn appears to have encouraged VCs to behave as value-maximising agents, like CEOs of corporations, by motivating them to focus more on the short-term performance-oriented metrics in order to justify their usually relatively high pay. Similarly, the short-term focus of VCs as motivated by pay means that HEIs are not committing to long-term investments, which may have negative consequences for individual HEIs and the sector. These negative consequences include increases in tuition fees, borrowing and interest payments for students, financial debt for HEIs, and casualisation/fixed-term/zero-hour contracts, perpetual strikes, redundancies, workload pressure and stress for staff. In contrast, reductions in staff pension entitlements, morale and welfare/wellbeing, and graduate job opportunities for students are observable, and thereby pose serious threats to the long-term sustainability of the HE sector. Together, these neoliberal-oriented reforms aimed at financialising HEIs have further impacted negatively on their ability to bring about social transformation, including reducing the gender pay gap, student non-continuation rates, unemployment of young/disabled people, contribution to the wider community and in addressing other societal social inequalities.

Research limitations and opportunities for future studies

Although our study is important as it highlights the need to link VC pay to performance, it also suffers from a number of limitations, including focusing only on UK HEIs, and hence further research may offer new insights by extending our analysis by including HEIs from other developed and developing nations. Further, and given that it is difficult to manually collect the required data using annual reports, we limited our analysis to the period between 2009 and 2014, which can influence our results, and thus, as data become more easily accessible in the future, further research may extend our study by analysing longer periods of time. Additionally, and similar to most archival studies of this nature, our variables and measures for VC pay, performance, governance and VC characteristics, for instance, may or may not reflect practice. For example, future studies may consider measuring social performance by using some form of index instead of individual measures. Finally, we have only employed the quantitative research approach to analyse our data and this may impair the generalisability of our results, and hence future studies may use qualitative data analysis techniques, such as in-depth case studies to further explore and better understand the impact of HEIs’ performance on VC pay, as well as the role of VC characteristics in explaining this link by interviewing HEI executives, government officials, governors, policy-makers/regulators, staff, students and trade-unions regarding these issues.

Supplemental Material

sj-docx-1-wes-10.1177_09500170221111366 – Supplemental material for Vice-Chancellor Pay and Performance: The Moderating Effect of Vice-Chancellor Characteristics

Supplemental material, sj-docx-1-wes-10.1177_09500170221111366 for Vice-Chancellor Pay and Performance: The Moderating Effect of Vice-Chancellor Characteristics by Mohamed H Elmagrhi and Collins G Ntim in Work, Employment and Society

Footnotes

Acknowledgements

The authors gratefully acknowledge the insightful and timely suggestions by the two handling editors (Professor Alexandra Beauregard and Professor Anne Daguerre), the four anonymous reviewers and the editorial office staff (Amber Davis and Madeleine Hatfield). We would also like to thank Dr Sammar Javed for her assistance in the data collection.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We would like to acknowledge the Leadership Foundation for Higher Education (now part of Advance HE) (UK) for their generous support of this project through the Small Development Projects research funding stream.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.