Abstract

In 2020, the philanthropic sector faced unprecedented demands as it responded to the global pandemic and urgent calls for racial and social justice. Early evidence indicated that US-based donors using donor advised funds (DAFs) responded to those demands by increasing grantmaking. This article uses the concept of organizational slack to explain how and why DAFs allow donors to respond to emergent needs. We apply the concept of slack to the DAF context, creating a conceptual framework that explains variation in DAF giving patterns. We hypothesized that a DAF’s size, number of prior grantees, previous payout rates, contribution frequency, and endowment status predict the amount of slack a donor will have in their DAF to grant to emergent needs. We found that DAF accounts that were larger, had lower payout rates, received frequent contributions, and were non-endowed gave more in 2020. Fundraisers should especially target DAFs with these characteristics during crises.

Donor advised funds (DAFs) are intermediary philanthropic vehicles that allow donors to “make a charitable contribution, receive an immediate tax deduction, and then recommend grants from the fund over time” (National Philanthropic Trust, 2024b). Donors have no legally mandated period in which they must make grants; the timing of grantmaking is instead regulated by sponsors’ internal policies (Colinvaux, 2017; Heist & Stone, 2023). This flexibility in timing has triggered concerns about donor incentives and charitable impact. While DAF donors receive an immediate tax deduction, they are not required to direct those funds to nonprofit grantees right away, separating the tax benefit from the ultimate benefit to charitable causes (Madoff, 2016). However, because of the flexibility DAFs offer, DAF donors can change their grantmaking when unexpected conditions arise. DAFs can be characterized as “rainy day funds” for philanthropy (Bell & Dubb, 2020). Several studies found that US-based DAF donors increased their grantmaking in 2020 in response to the COVID-19 pandemic (Giving USA, 2021; National Philanthropic Trust, 2020; SatoKumar et al., 2020) and to causes related to social and racial justice (Giving USA, 2021; Indiana University Lilly Family School of Philanthropy, 2021). However, these studies were unable to explain which donors changed their grantmaking, to which organizations, and why.

The aims of this article are (a) to provide a theoretical framework for explaining why some DAF donors may be able to respond to unexpected demands on their giving, (b) to provide detailed information about how US-based DAF donors changed their giving in 2020, especially to pandemic-related causes and/or organizations related to social justice, and (c) to provide empirical evidence regarding what types of DAF donors made these changes. We chose the year 2020 to study changes in DAF giving because the outbreak of the COVID-19 virus led to extreme pressures on the U.S. nonprofit sector, especially for organizations involved in providing immediate relief. We also chose this year because, after the murder of George Floyd, national movements related to racial justice heightened attention on the philanthropic needs of organizations that work in this area.

This article introduces a novel conceptual framework that explains how DAFs, as intermediaries, facilitate philanthropic responsiveness during times of crisis. We theorize that changes in DAF grantmaking in 2020 are related to the “slack” that donors have and perceive in their DAF accounts. In organizational behavior, slack is an organization’s ability to draw on reserve resources or redirect resources during crises (Bourgeois, 1981). We apply the concept of slack to individual DAF accounts and provide initial theoretical explanations for why DAFs seem to exhibit philanthropic responsiveness to crises. We posit that different types of DAF accounts will have different levels or kinds of slack that allow for more responsiveness in grantmaking. We operationalize the concept of slack in DAFs using measurable characteristics of DAF accounts and hypothesize that these slack indicators were related to grantmaking in 2020. Next, we provide empirical analyses on DAF grantmaking during 2020 and test our hypotheses.

This article uses a unique dataset of individual, account-level, transaction data from almost 13,000 DAFs at 21 different sponsor organizations across the United States over a 4-year period (2017–2020; Vance-McMullen & Heist, 2022a). The dataset, compiled between 2020 and 2021, was partially intended to be used to assess changes in DAF giving patterns. These data allow us to pinpoint the specific nonprofit organizations that DAF accounts granted to over the years, including the timing and amounts of the grants. We use these data to understand how DAF accounts varied in their grantmaking in 2020, specifically in giving to pandemic-related causes and social justice organizations.

Our empirical analyses show that DAF accounts that were larger, had lower payout rates, received frequent contributions, and were non-endowed gave more in 2020. The relationship between these slack indicators and DAF giving in 2020 suggests that slack is an important driver of flexible giving to emergent needs. This study is the first to establish a conceptual framework linking account-level DAF variations and granting behavior, identifying slack as a fundamental source of heterogeneity in donor action. This framework offers future researchers insights into DAF giving patterns and provides nonprofit professionals with tools for more informed solicitation of supporters using DAFs.

Background on DAFs and Giving During 2020

The use of DAFs has continually increased over the past decade. In 2023, about 1.8 million DAF accounts were in use, comprising $252B in assets and making $55B in grants (National Philanthropic Trust, 2024a). Since 2012, the number of accounts has increased nine times (205,552 in 2012), the amount of assets has increased more than five times ($44.9B in 2012), and grants have increased approximately six times ($8.6B in 2012). DAFs have truly become the fastest-growing form of philanthropy. While the growth in DAF assets is affected by economic factors, Heist and Vance-McMullen (2019) found grantmaking from DAFs to be relatively resilient to market downturns during the recession of 2008–2009. This article explores how DAF grantmaking responds to social disruptions and emergent needs, such as those experienced in 2020.

The literature on DAFs includes the legal and public policy implications of the vehicle (Aanestad et al., 2020; Colinvaux, 2017, 2022, 2023; Colinvaux & Madoff, 2019; Gibbons, 2022; Hussey, 2010), with special emphasis on tax laws (Brooks, 2016; Madoff, 2019; Walker, 2022); ethical issues (Biagi & Hefter, 2023; Habben et al., 2023; Murray, 2023); the effect on community philanthropy (Colinvaux, 2018; Qu & Paarlberg, 2022; Wu, 2020); the impact on the nonprofit sector and the social impact more broadly (Grennan, 2022; Heist & Vance-McMullen, 2019; Hemel et al., 2021; Shakeley, 2015); historical perspectives (Berman, 2015); and international perspectives (Phillips et al., 2021; Tang, 2021). The literature does not have a framework to explain variations in DAF responsiveness and giving behaviors, specifically in response to changes in giving environments. Andreoni (2015) identified warm glow and tax incentives as motivating factors of DAF giving. Heist et al. (2021) explained that the DAF giving process allows donors to separate elements of charitable giving decisions that traditionally occur at the same time. Heist et al. (2022) characterized distinct DAF giving strategies through qualitative methods; however, no quantitative analyses have been done to explain differences in DAF giving. This article hypothesizes and tests a potential mechanism, slack, through which DAF donors shift their giving behavior during crises.

Charitable giving in the United States rose substantially in 2020, with total estimated charitable giving increasing by $22.8B or 5.1% (Giving USA, 2021). One source of grants to nonprofits that increased during 2020 was DAFs (SatoKumar et al., 2020). From a survey of some of the largest DAF sponsor organizations representing about 50% of total DAF assets, National Philanthropic Trust (2020) found that the number of grants increased by 37.4% and the total grant dollars (USD) increased 29.8% in the first 6 months of 2020 compared with the same period in 2019. Vance-McMullen and Heist (2022a) found that spikes in DAF grantmaking during the outbreak of COVID-19 (March/April) did not replace year-end grantmaking, as there was still an additional surge in grants in December.

During 2020, community foundations demonstrated a remarkable capacity to respond to changing needs and meet increased demands. Paarlberg et al. (2020) identified slack as part of the explanation for their resilience and ability to respond. Community foundations were found to be resilient to the COVID-19 crisis by “not only rapidly raising and distributing resources, but also serving as information hubs and referral centers and facilitating cross-sectoral collaboration” (Giving Thought, 2020, as cited in Paarlberg et al., 2020, p. 1120). Community foundations are the most common type of DAF sponsoring organization (National Philanthropic Trust, 2024a). If community foundations were able to meet the increased needs of the pandemic, it may be partially because of DAF resources.

The pandemic’s impact on nonprofits varied by cause. While some nonprofits saw increased donations and revenue, others faced revenue losses (Faulk et al., 2021). Due to the nature of the pandemic, human service organizations and food banks experienced a surge in demand. For instance, 79% of hunger relief organizations (food banks) saw an increase in demand for their existing services during the pandemic (Templeton et al., 2022), and worsening economic and social conditions resulted in greater demand for human service organization programs (Ma & Beaton, 2023; Shi et al., 2020). In addition to pandemic-related giving, a survey from the Lilly Family School of Philanthropy (2021) found that the percentage of Americans who supported causes of racial and social justice increased from 13% in 2019 to 16% in 2020. According to the report, giving increased to support individuals and families affected by racial injustice, grassroots organizations that address specific issues related to racial equity, and nonprofits that address broader issues relating to racial equity (Indiana University Lilly Family School of Philanthropy, 2021). Many donors who increased their giving to these causes did so through a DAF. This article uses account-level DAF data to explore which donors increased their DAF grantmaking during 2020 and what types of organizations benefited from those increases.

Theoretical Framework and Hypotheses

This article adapts an organizational behavior concept—organizational slack—to explain variation in giving from DAFs during crises. We translate the concept of slack to DAFs by drawing upon current DAF research and behavioral science related to charitable giving. This allows us to create a conceptual framework of slack within DAFs. Finally, we use this conceptual framework to hypothesize about DAF giving during 2020, a year during which two major crises emerged—the global COVID-19 pandemic and a movement for racial justice in the United States.

Organizational Slack and Crisis Performance

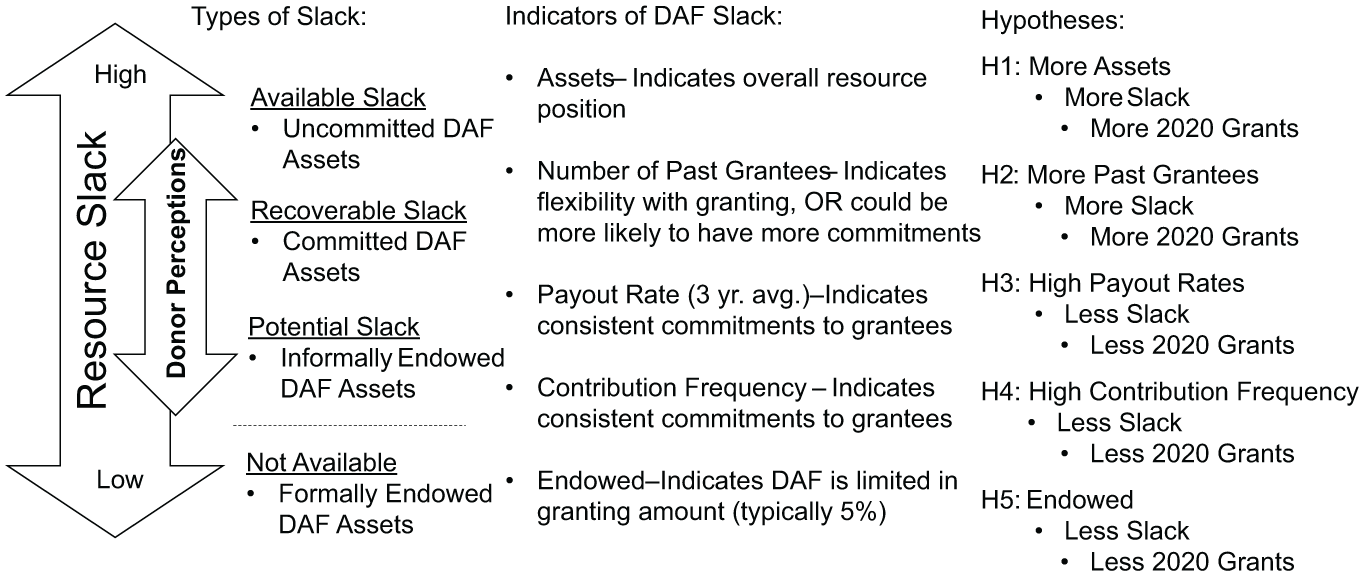

In organizational theory, some organizations perform better during crises than others. Theorists observe that while the total amount of organizational resources is important to successfully navigating changing environments, it is the amount of “slack” in those resources that allows an organization to “absorb environmental variation” (Bourgeois, 1981, p. 29). Firms with resource slack perform better financially and withstand environmental shocks (George, 2005). Vogus and Sutcliffe (2007) applied the concept of slack to explain an organization’s resilience, or the ability to mobilize resources, during crises or unexpected demands. Dolmans et al. (2014) explained that the effects of slack on organizational performance during a crisis were both a matter of the actual resource position and the manager’s perception of resources.

Bourgeois and Singh (1983) categorized three types of resource slack in organizations: available, recoverable, and potential. In a business, available slack refers to cash immediately available to an organization that exceeds its immediate liabilities (Bourgeois & Singh, 1983). Recoverable slack in a corporation considers receivable revenues, inventory that could be liquidated, and expenses that could be cut back. Potential slack includes an organization’s net worth and long-term debts. The categorization of resources as available, recoverable, or potential slack is not purely objective and may vary based on managerial perceptions. Managers who perceive more slack in their organization’s resource position are more flexible in their decision-making (Dolmans et al., 2014). In this article, we operationalize the three types of resource slack within a DAF context, which may be influenced by donor perceptions.

We apply the concept of organizational slack to DAFs by considering donors to be like managers over subsidiary philanthropic organizations. We explore how DAF donors used slack resources in their DAF accounts to respond to crises in 2020. We acknowledge that, technically, DAF donors only have advisory privileges to recommend grants from their DAF account. However, DAF sponsoring organizations almost always follow grant recommendations from donors, making donors the de facto decision-makers (Heist et al., 2021). We analyze how patterns of DAF giving during the year 2020 are similar to the ways that slack affects organizational resource allocations in response to crises.

Slack in the DAF Context

The total assets within a DAF account could be characterized as the account’s resource position, and the resource slack within the DAF can be thought of as available, recoverable, or potential, depending on the type of DAF (endowed or not-endowed) and other indicators of how the donor is using the DAF—their DAF giving strategy. Below, we explain how the various types of slack may be conceptualized within the DAF, how DAF giving strategies may affect the ways donors perceive slack, and how measures of these concepts may be operationalized.

The available slack within a DAF is all the assets that are immediately available for giving. However, distinguishing available and unavailable assets is not straightforward. There are several reasons that assets within a DAF may not be considered available slack. These relate to the structure of the DAF, donors’ commitments to charities, and their giving strategies. First, donors may use an endowed DAF, a type of DAF where the sponsor has policies that preserve the principal amount of assets for long-term growth and regulate the amount available for grantmaking. Typically, donors with a formally endowed DAF can only grant about 5% of the total assets away each year (Heist & Stone, 2023). Similarly, even donors who do not use a formally endowed DAF may perceive their DAF as an endowment, referred to as informally endowed DAFs. They may informally create their own strategy to limit themselves in their annual grantmaking to preserve and grow their DAF assets. For these donors, it is more of their perception of their resource slack that affects the availability of their resources.

Donors may also have arrangements with charities they plan to give to. Donors may have formally made multi-year commitments, similar to pledges, to a certain charity or several charities. Similarly, but less formally, donors may be planning to make grants to specific charities with the assets within the DAF. Donors often create mental budgets for their charitable giving and may consider some of the assets within the DAF already earmarked or committed to certain charities (LaBarge & Stinson, 2013).

Assets in the DAF that are not considered available may still be recoverable or potential. When donors make commitments to charities (which are not legally binding) or create mental budgets for the assets within a DAF, those assets could be considered recoverable slack because donors may choose to reallocate those assets based on an emergency or crisis. When donors choose to use an endowed DAF, the assets are restricted by the sponsor organization’s policies, so the assets are considered unavailable. However, for donors who treat their DAF as informally endowed, the assets could be considered potential slack because they are intended as long-term investments but may be reallocated in an emergency. In a crisis, potential slack may be more likely to be granted to new causes than recoverable slack, because the resources are not pre-committed to other causes that may also have increased needs.

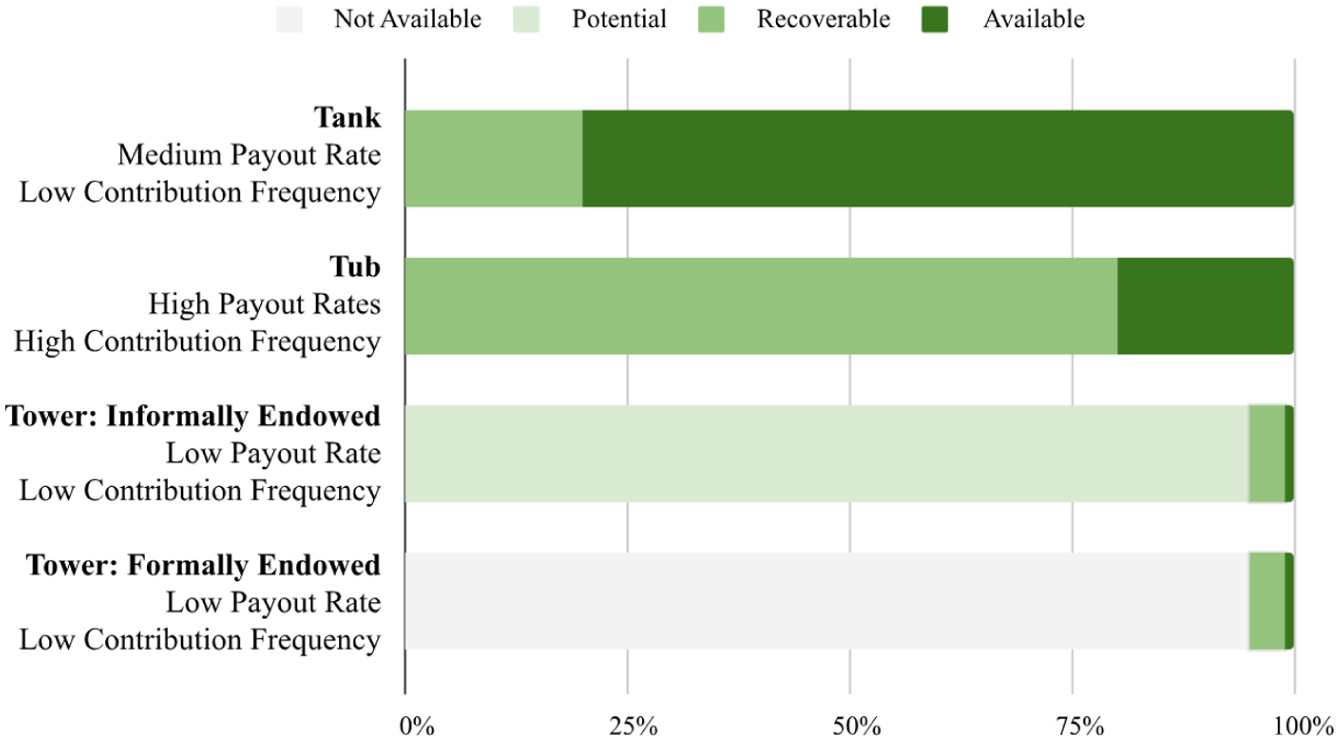

Prior research supports the idea that donor perceptions of DAF resource availability vary, as evidenced by the different strategies donors use when giving. Heist et al. (2022) found three archetypes of DAF donor strategies: tubs, tanks, and towers. Tub donors give through their DAF quickly, typically granting DAF resources within 1 to 2 years. Like a bathtub, they fill it, and they drain it. They contribute regularly to their DAF, but just enough to fulfill their planned grantmaking for the following year (Heist et al., 2022). In this case, the DAF would likely have low year-end assets, high payout rates, and high contribution rates.

Tank donors make large contributions to a DAF when experiencing a wealth event and then grant those funds over an intermediate period, typically 2 to 10 years (Heist et al., 2022). Like a water tank, the DAF is filled with more resources than are immediately needed but are intended for use in the near future. Because they are actively grantmaking, but not spending down completely, tank donors would be expected to have higher assets than tub donors and medium-range payout rates. This group of donors would likely have the most available slack because not all the assets are budgeted for grantmaking.

Tower donors use their DAF to sustain long-term philanthropy (Heist et al., 2022). Like a water tower, the account is intended to be a long-term, sustainable resource. Tower donors use an endowed DAF or treat their DAF as informally endowed, only granting out a certain percentage per year. These donors would be expected to have generally high asset levels and low payout rates. If these donors use a formally endowed DAF, then they would not have much available slack or potential slack, despite high asset levels, because the assets are restricted by endowment policies. Tower donors who take the informally endowed DAF approach would likely have a lot of potential slack because the assets in their DAF could be made available.

Figure 1 provides examples of what the resource slack composition may look like in different DAF giving strategies. The figure presents the slack composition of archetypical DAF accounts based on the literature. Tank donors are depicted as having the most available slack, which is immediately available for granting, with some recoverable slack, which may be informally committed to charities but could be reallocated. Tub donors are depicted as having high levels of recoverable slack because they typically have a mental budget for their giving before contributing resources into their DAF, but could reallocate funds; they may also have some available slack that is not mentally committed. Examples of slack allocation are provided for the two kinds of tower donors: informally endowed DAFs and formally endowed DAFs. Informally endowed DAFs are shown as having high potential slack because their DAF resources are not formally restricted by sponsor policies, and their availability is a matter of donor perceptions. The assets in formally endowed DAFs are not available because of policy restrictions, but are depicted as having some recoverable slack or available slack within their annual grantmaking allocation.

Theoretical Examples of DAF Slack Resources With Different Giving Patterns.

Indicators of Slack and Hypotheses

The conceptual framework posits that the amount and type of slack varies among DAFs. It also indicates that slack is difficult to measure because it relies on donors’ perceptions and sometimes unobservable commitments to nonprofits. While the types and amounts of slack cannot be directly measured, the available administrative data includes variables that indicate the type of giving strategies within each DAF account. We use the relationships between the indicators of giving strategies and types of slack to hypothesize slack position and test if they correlate with grantmaking in 2020. We control for previous grantmaking, which means that variation in 2020 total grantmaking represents variation in new grantmaking.

DAF Assets (Measured in 2019 Year-End Assets)

Looking at the previous year’s assets allows us to see the starting resource position at the beginning of 2020 and how that might relate to giving patterns. DAF accounts vary widely in their size as measured by assets. Using the same dataset as this study, Vance-McMullen and Heist (2022b) categorized DAF accounts into the following three groups: small (less than $50K), medium (between $50K and $1M), and large (more than $1M). Large accounts made up about 11% of total accounts but held 85% of the total assets; medium accounts made up about 45% of accounts but held 14% of assets; and small accounts made up about 44% of accounts but held 1% of assets. They found that large and medium accounts generally had lower payout rates than small accounts. However, medium and large accounts increased their median payout rates in 2020, while small accounts decreased their payout rates in the same period. According to the report, “this finding indicates that medium and large accounts had more slack, or capacity, to respond to increased demands on the nonprofit sector” (Vance-McMullen & Heist, 2022b, p. 33). In this study, we hypothesize that large accounts have a more robust overall resource position and more slack of all kinds (available, recoverable, and potential), and therefore would have given more overall in 2020 and more to organizations related to the pandemic and social justice causes.

Number of Previous Grantees

Some DAFs grant to more organizations than others. Vance-McMullen and Heist (2022b) found that, averaged over a four year period, more than half of DAFs (51%) granted to less than three organizations a year, with a median of 2.75 grantees. However, almost one third (31%) granted to more than six organizations annually. Given this wide variation, we would expect a range of recoverable slack. It is reasonable to assume an inverse relationship between the number of grantees and the depth of commitment to any single one. Therefore, we assume that those with more grantees perceive greater flexibility in their commitments, making them more likely to redirect funds in times of crises.

Payout Rates

Payout rates measure what proportion of a DAF account is granted out in a year compared with how much is available for granting that year. More information about how payout rates are calculated in this study is provided in the data and methods section. We theorize that low-payout, informally endowed DAFs, which have high potential slack and low recoverable slack, would increase grantmaking in a crisis, because potential slack is not pre-committed to other causes and we assume that potential slack will be perceived as more available for new grantmaking during a crisis than recoverable slack. Tank DAFs, which have medium payout rates, have a mix of available slack and recoverable slack, would also have funds to grant in a crisis, after controlling for their existing levels of support. Tub DAFs, with the highest payout rates, would also have a mix of recoverable slack and available slack, but with a higher proportion of recoverable slack. Tubs would therefore be expected to have the lowest grantmaking after controlling for their existing levels of support.

Contribution Frequency

Like our previous hypothesis, we consider the frequency of DAF contributions as an indication of a DAF giving strategy. We posit that frequent contributions are an indication of a tub strategy, considered to have lower available slack, and thus correlate with less redirectable grantmaking during a crisis. Conversely, those who add money to their DAFs less frequently are more likely to take the tank or tower approach to DAF giving and may have more available and potential slack. We acknowledge that the hypothesis that donors who make more frequent contributions will have less slack may seem counterintuitive. The assumptions are that tank and tower donors make less frequent, but much larger lump sum contributions, while tub donors make more frequent, but smaller contributions, which may already be mentally accounted for.

Endowed Versus Non-Endowed

As explained above, some DAFs are formally endowed, meaning they are regulated by organizational policies that restrict their annual grantmaking to a percentage of assets. In the dataset for this study, only the formally endowed DAFs are labeled as such—a dichotomous variable of “endowed” or “non-endowed.” Informally endowed tower donors are designated as non-endowed, even though they treat their DAF like an endowment. Tub and tank donors are also non-endowed. Those with formally endowed DAFs are considered to have little resource slack of any kind, because their funds are simply not available, while those with non-endowed DAFs are considered to have high potential slack. Because formally endowed DAFs are considered to have less of all kinds of slack than the other giving strategies, we hypothesize that endowed DAFs grant less during times of crises, even when compared with similarly low-payout non-endowed (informally endowed) accounts.

Figure 2 shows the different types of DAF slack, ranging from high to low resource availability and donor perceptions. The figure then shows how these types of slack relate to the indicators of DAF giving strategies, our dependent variables, found in the dataset. Finally, it shows the hypothesized relationships between these indicators and our outcome variable, grantmaking in 2020.

Conceptual Framework of DAF Slack.

Data and Methods

Data

Data for this study came from the Donor Advised Fund Research Collaborative (DAFRC) pilot dataset (Vance-McMullen & Heist, 2022a). The dataset includes account-level DAF data from 21 different DAF sponsor organizations, including 16 community foundations and five religiously affiliated organizations. (For more information about the sample and the data collection process, see Vance-McMullen & Heist, 2022b and Vance-McMullen & Heist, 2022c.) The dataset represents a total of nearly 13,000 accounts open on January 1, 2020, and advised by individuals (not companies or other groups). Online Appendix A includes the descriptive table for the DAFRC dataset and the cleaned data used in the analyses for this study. The data used in this study included account characteristics, some donor demographics, and financial transactions for the years 2017-2020, giving 3 years of data before the pandemic. The financial information for each account included annual asset levels, the date and amount of each contribution into the account, and the date and amount of each grant from the account. All financial data is in U.S. dollars. The grant data also included the name of each grant recipient along with their unique nine-digit Employer Identification Number (EIN). A weight variable equal to the inverse probability of inclusion by the DAF sponsor is also included.

The data was carefully cleaned to address common issues at both the account and transaction levels. At the account-year level, the key focus was on distinguishing open accounts from non-open ones and checking for a complete set of financial records. When available, account opening and closing dates were used to distinguish non-open accounts. When dates were not available, the date of first contribution and/or the first instance of positive assets was used. In addition, account-years with missing beginning-of-year (BOY) assets, contributions, grants, or end-of-year (EOY) assets were dropped from the dataset. At the transaction level, the primary concern was identifying and removing accounting irregularities, such as zeroed or reversed transactions. These were flagged using the EIN, date, and amount, and cleaned from the dataset. Finally, to ensure all independent variables and controls could be calculated in the same way across all accounts, accounts with less than 4 years of data were dropped.

Method

Dependent Variables: 2020 Grantmaking

The primary dependent variables of interest measure DAF grantmaking in 2020. We are interested in both overall (total) grantmaking and the relevant margins—that is, whether and how much to give. The OLS model focuses on total grantmaking by each DAF account in 2020. In the two-stage hurdle model, we examine whether the DAF granted at all (any amount to any organization) in 2020 for the first-stage Logit analysis and, if the account granted in 2020, the amount of grantmaking in 2020 for the second-stage GLM analysis.

These same variables are then used to measure grantmaking to certain groups of charities with connections to the pandemic or social justice. For pandemic-related causes, we use two proxy groups—Food Banks and Human Services organizations. The lists of EINs for both groups were extracted from the Internal Revenue Service (IRS) Business Master File (Urban Institute, n.d.-a) using the National Taxonomy of Exempt Entity (NTEE) codes (Urban Institute, n.d.-b) “P” for Human Services and “K31” for Food Banks. For Social Justice organizations, we used a list curated by Giving Compass (n.d.) and sourced through grantmakers that met three out of the five following criteria (taken directly from Giving Compass’ website): 1) Focus explicitly on equity, effectiveness, systems change, and transparency. Explicitly address racial disparities in their giving strategy. 2) Use a participatory grantmaking process and share the process transparently with the public. 3) Are BIPOC and/or LGBTQIA+—led. 4) Detail components of systems change strategies in their materials (advocacy, organizing, policy change, voter engagement, public-private partnerships, sustained legislative accountability to communities). 5) Center those who have been historically least well served in their giving strategies (funding those furthest from opportunity first).

Independent Variables: Size, Number of Grantees, Payout Rates, Contribution Frequency, and Endowed DAFs

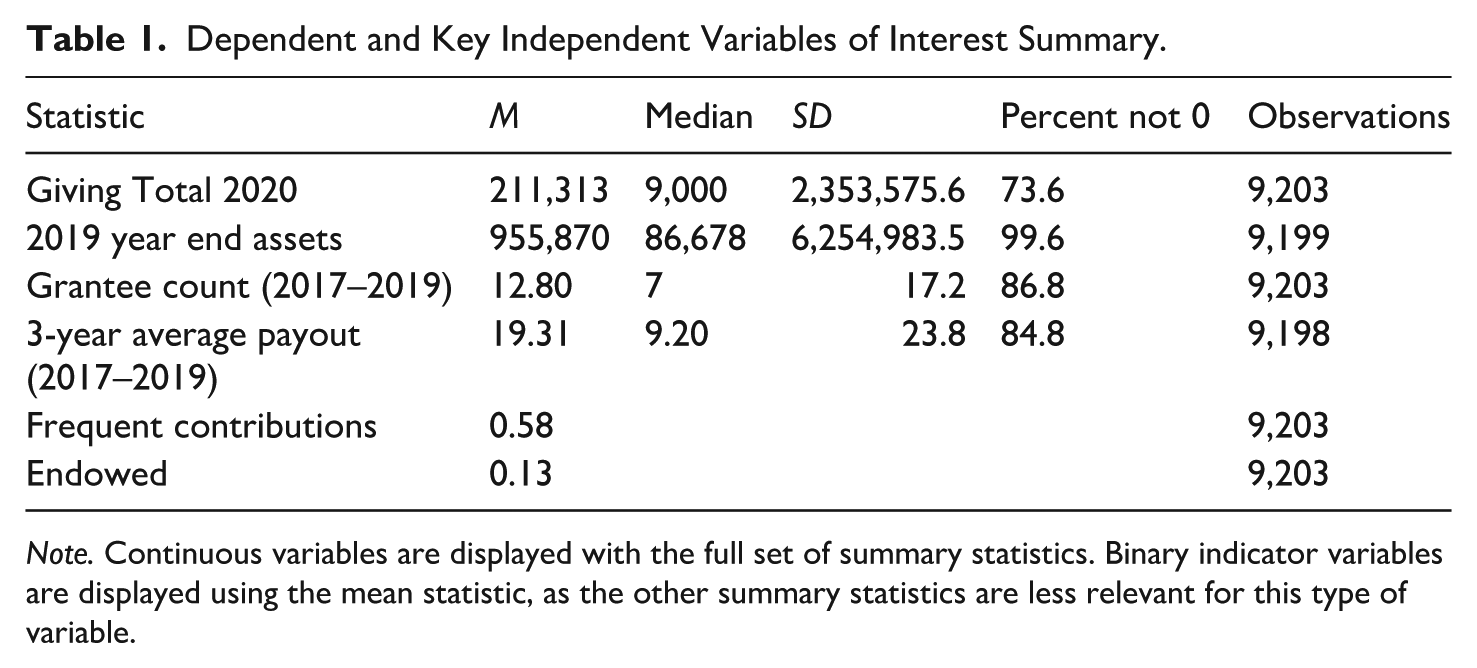

Our independent variables of interest, based on the concepts of available, recoverable, and potential slack within the DAF context, were account size, number of grantees, payout rates, contribution frequency, and formally endowed DAFs (see Table 1). Account size was measured as EOY assets for 2019, which were collected as part of the DAFRC dataset.

Dependent and Key Independent Variables of Interest Summary.

Note. Continuous variables are displayed with the full set of summary statistics. Binary indicator variables are displayed using the mean statistic, as the other summary statistics are less relevant for this type of variable.

The number of grantees was calculated as the number of unique organizations that a DAF gave to in the years 2017–2019. The variable was Winsorized so that accounts with more than 100 grantees were top-coded.

Payout rates were calculated at the account level for each year that data was available using the following equation: 1

Payout rates for each account were then averaged across the years 2017–2019, giving us a 3-year average payout rate. We used a 3-year average because of how much variation there was in payout rates between years for some accounts. The average provides a more accurate assessment of DAF account activity over time. We Winsorize the payout variable so that outlier payout rates over 100% do not bias the analysis. 2 Therefore, our payout rate takes on values between 0 and 100.

Contribution frequency was calculated by separating frequency rates into a binary variable representing high (=1) versus low (=0) contribution frequency. High contributors were those who contributed yearly or had non-opening contributions from 2017 to 2020. Low contributors were those who had opening contributions only or no contributions at all during this time.

Formally endowed DAFs were identified in the dataset with a binary variable for endowed (=1) or non-endowed (=0) for each account. This information was provided by the DAF sponsors.

Based on Table 1, we see that the average asset size at 2019 year’s end was $955,870 and the average 3-year payout rate (2017–2019) was 19.3%. Both variables have a right-skewed distribution, with medians falling substantially below the means. More than half (58%) of accounts were considered frequent contributors, and 42% were considered infrequent. The average account gave to 12.8 grantees before 2020, although the median was 7. Only 13% of accounts were formally endowed.

Account Characteristics (Control Variables)

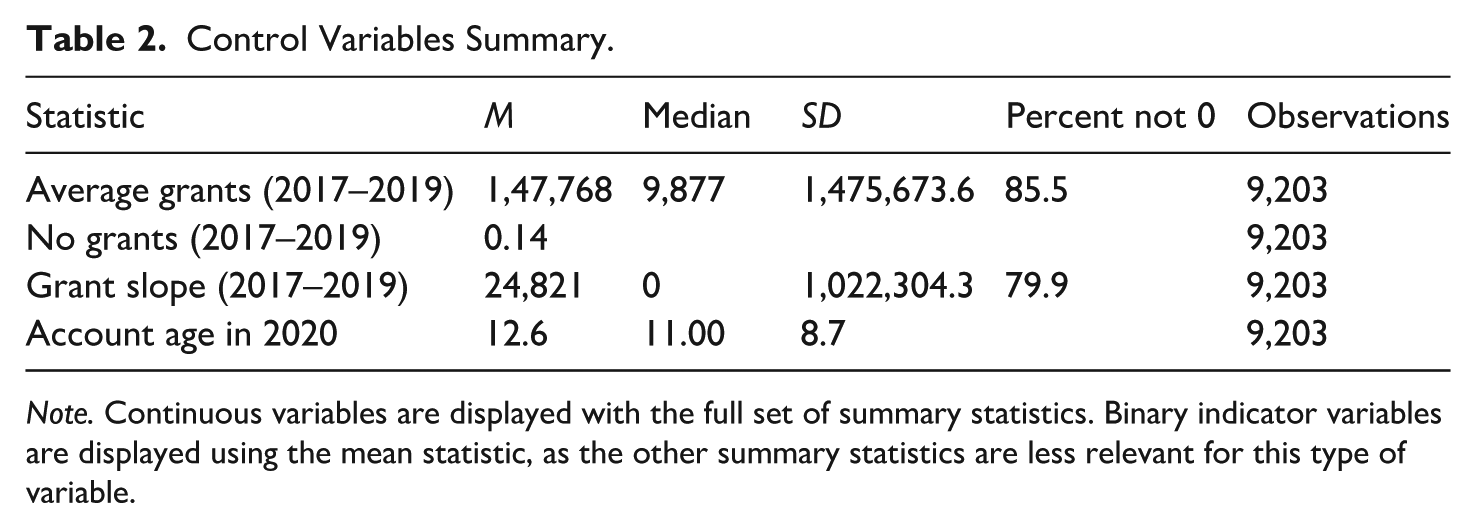

Our analyses include several account characteristics that may also influence grantmaking as control variables (see Table 2). The first of these is prior grantmaking, which we calculate as the average of the previous 3 years. Table 2 shows summary statistics for prior grantmaking. In the analysis model, we use an IHS transformation. In addition, we include a dummy variable indicating whether the DAF did not (=1) make any grants in the previous 3 years. This allows for the possibility that those not making grants will behave differently from those who previously made grants. We also calculate a “slope” of the grant amounts over the past 3 years; this helps us control for whether a DAF’s grantmaking is trending upward or downward. The slope variable is calculated by fitting a linear trend to the grant data from 2017, 2018, and 2019. A positive slope indicates grants are trending upward, a negative slope indicates grants are trending downward, and a 0 slope indicates that grants remained constant during this time. Finally, we include the age of the account, or the number of years the account had been open in 2020, as a control variable. Prior research has suggested that the account age plays an important role in giving patterns (Heist et al., 2024).

Control Variables Summary.

Note. Continuous variables are displayed with the full set of summary statistics. Binary indicator variables are displayed using the mean statistic, as the other summary statistics are less relevant for this type of variable.

Econometric Model

The relationship between slack and DAF giving in 2020 is estimated using two models. First, we use ordinary least squares (OLS) multiple regression. We draw on value-added models from the education economics literature to account for differences in pre-2020 giving at the account level (Bacher-Hicks & Koedel, 2023). 3 We estimate:

Here,

The three independent variables related to giving control for account-specific differences in pre-2020 giving along three dimensions: the extensive margin of whether the account was giving; the intensive margin of how much was given (using a non-linear IHS transformation); and the trend in giving (the slope). Note that the dependent variable, 2020 giving, is included without transformation in the model as recent research has shown that for non-negative, right-skewed data with many zeros, untransformed dependent variables yield more accurate coefficients than those transformed using natural logarithms or IHS transformations (Mullahy & Norton, 2022).

In addition to the standard OLS model, we also employ a two-stage hurdle model (also known as a two-part hurdle model). The two-stage hurdle model is specified with the same independent variables as in the OLS model. The hurdle model’s first stage employs a logistic regression to estimate the probability of giving any amount greater than zero in 2020. The second stage models the amount of giving (the non-zero donations) using a generalized linear model (GLM). Specifically, we use a gamma distribution with a log link function. The gamma distribution is appropriate for right-skewed continuous data where there are many smaller values and a few large outliers, such as in health care expenditures or donations. The log-link function transforms the linear predictor into the positive domain, which is appropriate because the second stage is focused on positive giving. The log-link function also allows the model coefficients to be interpreted in terms of percentage change.

The two-stage hurdle model is preferred to the OLS model for several reasons. First, this model fits the data well. Our data has many zero values, particularly when analyzing giving to special areas like food banks, and a few large outliers. Importantly, the model features ensure that predicted giving (i.e., the combination of covariates and their coefficients) is in the range of observed values. (In contrast, the OLS model can often predict negative giving.) Second, the two-stage hurdle model is better matched to donors’ actual decision-making processes, in which the decision to give is often made before the decision of how much to give (Dickert et al., 2011). Appropriately, two-stage hurdle models are becoming more standard in the donation literature (Forbes & Zampelli, 2014; Oxley, 2023; Wang, 2023). Finally, the model allows us to test the relationship between the variables of interest and giving separately for the extensive (whether or not to give) and intensive margins (how much is given) for 2020 grantmaking, leading to additional nuance in our findings.

The chosen models are preferable to fixed effects and difference-in-differences (DiD) models for three main reasons. First, the dataset includes three pre-pandemic periods. Fixed effects models are less appropriate when there is substantial variation and a small number of time periods. This limitation also affects the application of DiD models, as it makes confirming the parallel trends assumption difficult. Second, including fixed effects for those accounts that never change giving leads to the exclusion of many cases when estimating the extensive margin using logit functional forms. Third, because all accounts encountered the economic and social conditions of 2020, there is no “untreated” group to serve as a control in a DiD analysis. While the binary independent variables could be thought of as representing treated and untreated accounts, applying a dose-response DiD analysis for continuous independent variables requires strong assumptions. In particular, the model would rely heavily on the parallel trends assumption; as previously mentioned, this assumption is difficult to test when the number of pre-treatment periods is small.

Findings

Changes in DAF Giving in 2020

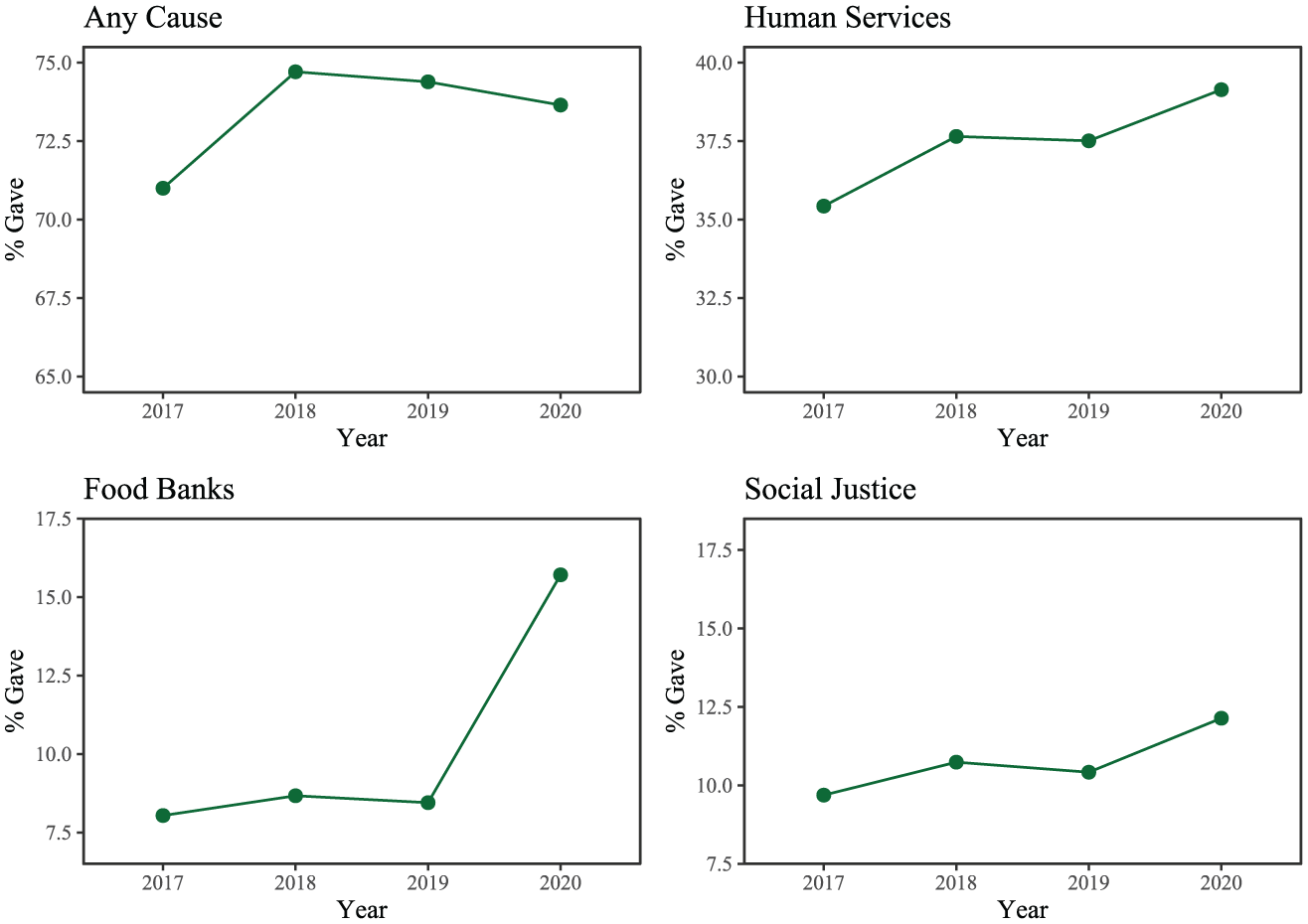

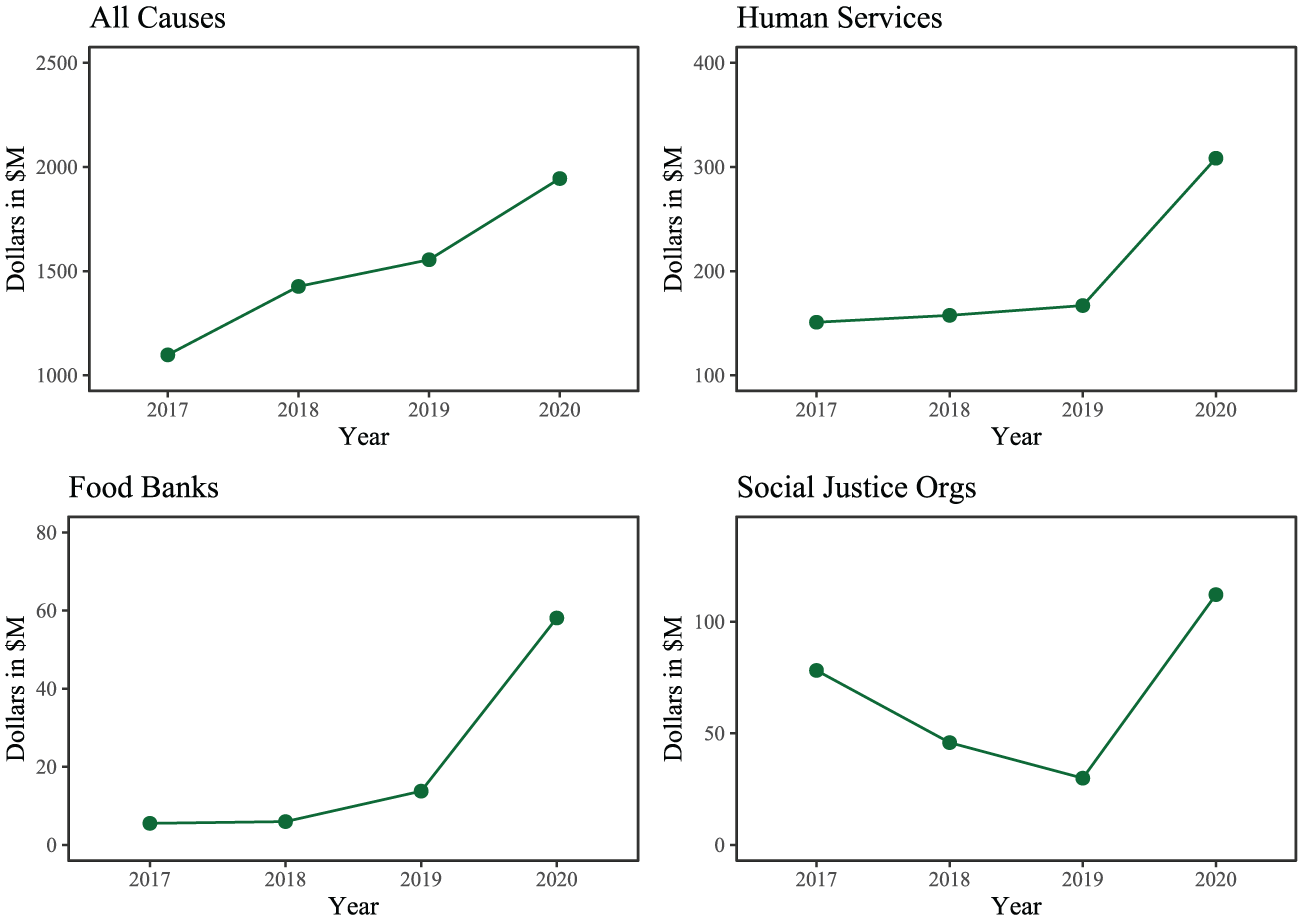

Our first analysis tests our claim that DAF giving increased in 2020, including both giving to all causes and giving to specific pandemic- and social justice-related causes. Figure 3 shows the percentage of DAF accounts that gave at all each year from 2017 to 2020, and the percentage of accounts that gave to Human Services, Food Banks, and Social Justice organizations. The percentage of accounts that gave to any cause slightly decreased in 2020, while the percentage of accounts that gave to the crisis-related causes increased in 2020 (see Online Appendix B for a table). Figure 4 presents the total grant dollars from DAFs during the same period to the same groups, showing a dramatic increase in 2020 compared with previous years (see Online Appendix C for a table) although the percentage of increase varied across the cause areas examined.

Percent of DAF Accounts Making Grants (2017–2020).

Total DAF Grant Dollars (USD; 2017–2020).

Regression Analysis and Hypothesis Testing: Overall Grantmaking in 2020

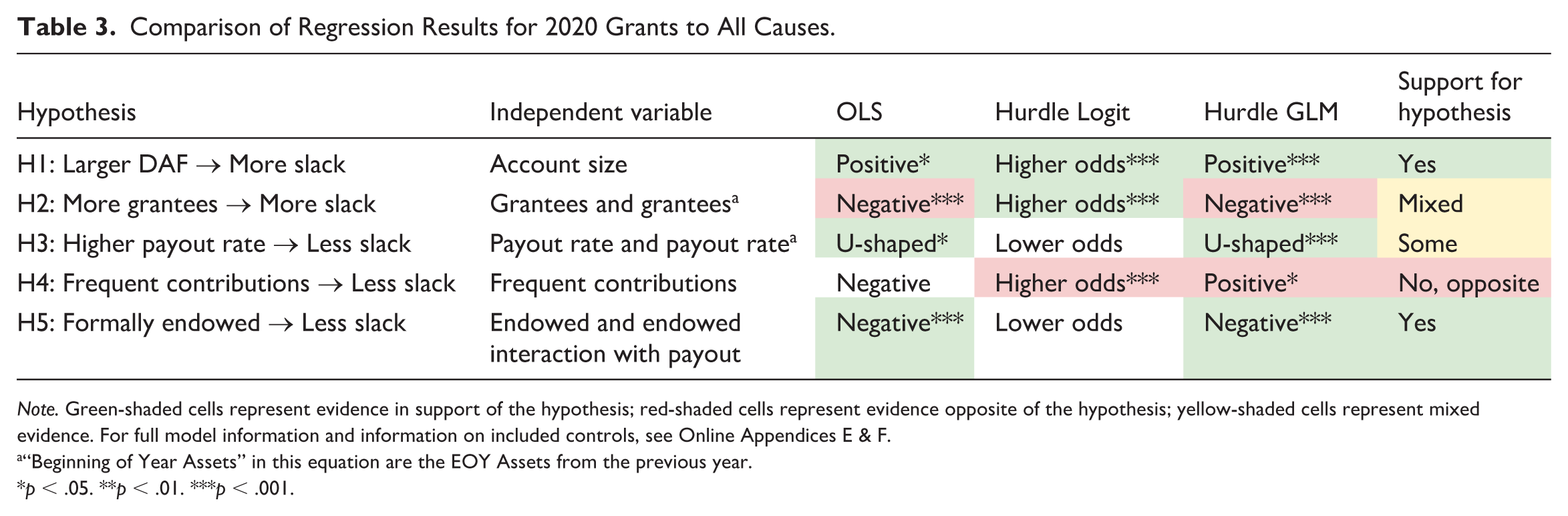

The regression analyses of the slack-related reasons for overall DAF grantmaking in 2020 yielded mixed support for the hypotheses. Table 3 presents both the OLS and the two-stage hurdle model results with a narrative interpretation of the coefficients of each regression, which corresponds to the first part (a) of each hypothesis. Note that the regressions include all control variables that were described in the econometric model section earlier. (See Online Appendices D, E, and F for the full regression results.) The table then presents information about whether the results support each hypothesis. Here, note that the results should be interpreted as correlational rather than causal. Correlational results can establish the predictive value of the factors related to slack, but it should not be inferred that policies that change account characteristics would lead to a change in giving to emergent causes during a crisis. We also present graphs of the predicted 2020 giving based on the combined two-stage hurdle model with the control variables held at the means.

Comparison of Regression Results for 2020 Grants to All Causes.

Note. Green-shaded cells represent evidence in support of the hypothesis; red-shaded cells represent evidence opposite of the hypothesis; yellow-shaded cells represent mixed evidence. For full model information and information on included controls, see Online Appendices E & F.

“Beginning of Year Assets” in this equation are the EOY Assets from the previous year.

p < .05. **p < .01. ***p < .001.

Hypothesis 1a

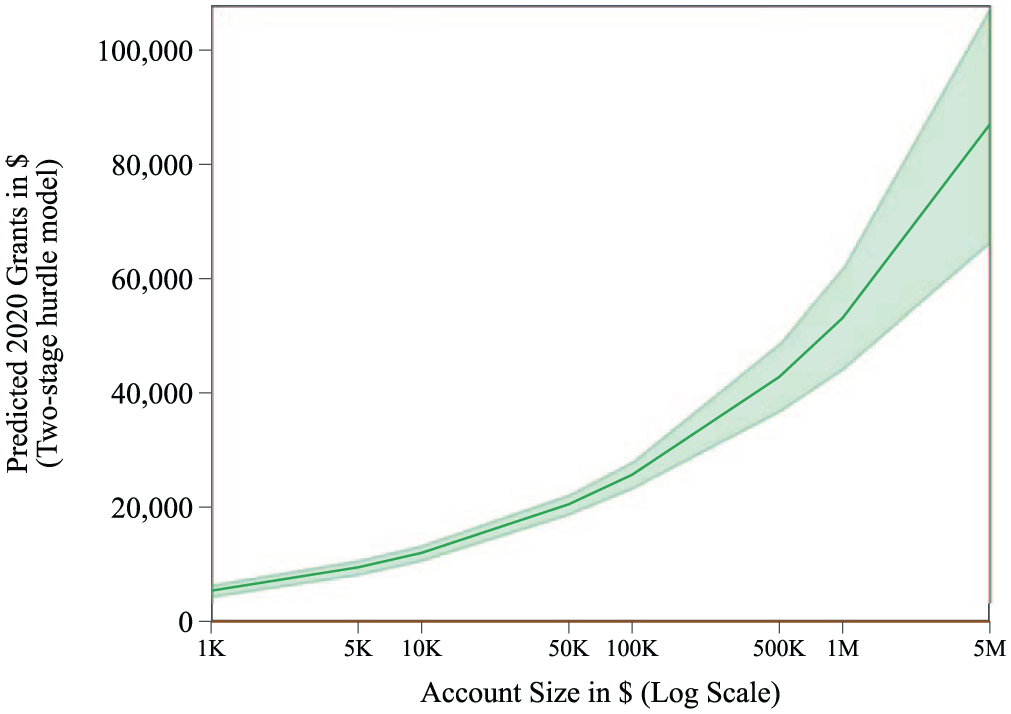

The OLS, first-stage Logit, and second-stage GLM models provide strong evidence for H1a, that larger DAFs have more slack and granted more in 2020, even after controlling for the average grants of the previous 3 years. Figure 5 is a semi-log plot of the predicted values of total 2020 grants with 95% confidence intervals, based on the combined two-stage hurdle model results. As expected, larger DAFs had higher predicted grantmaking in 2020, even after controlling for the average grants of the previous 3 years.

Predicted 2020 Grants (From Combined Two-Stage Hurdle Model) by Account Size.

Hypothesis 2a

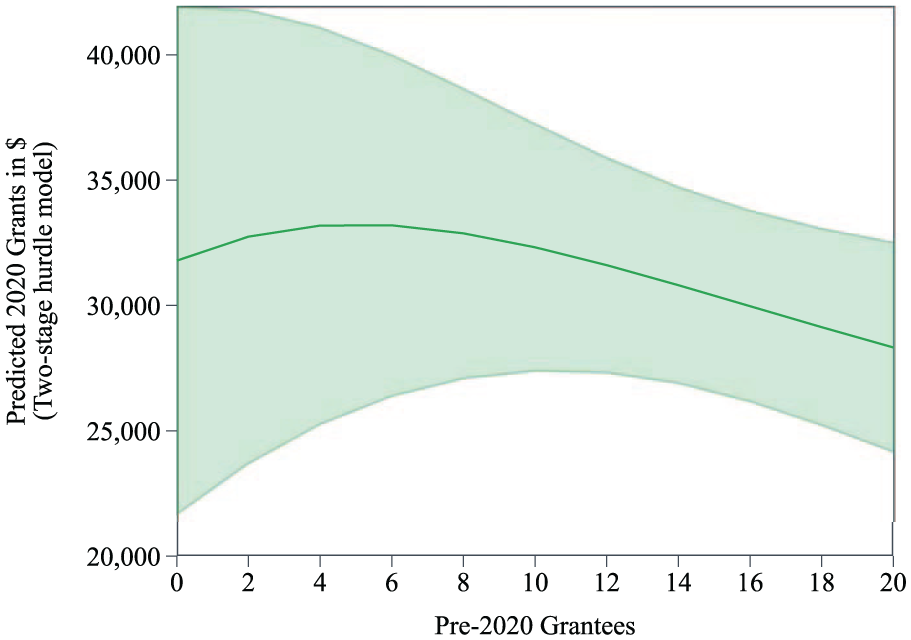

The regressions provided mixed results regarding H2a, that DAFs with more previous grantees have more slack. The OLS results show a U-shaped relationship, which is significant and negative in the relevant range of 0 to 20 grantees. This indicates that as grantees increased, predicted grant amounts decreased, all else held equal. However, the first-stage Logit from the hurdle model showed a significant and positive relationship between grantee counts and giving in the relevant range. This is evidence that DAFs with more previous grantees were more likely to make a grant at all in 2020. The second-stage GLM relationship was negative in the relevant range. Some of this difference is likely due to the greater proportion of accounts making grants. In general, marginal donors tend to make smaller gifts. When combined, the relationship between the number of grantees and total grantmaking was non-linear, with an inverted U-shaped relationship. Predicted giving trends upward as the number of pre-2020 grantees rises from 0 to 4 and then begins to trend downward. The slope was not significantly different from zero in the relevant range, although it would become significant and negative for accounts with a larger number of grantees. The predicted giving from the combined two-stage model is shown in Figure 6. Overall, having additional grantee relationships pre-2020 predicts that an account will be more likely to give in 2020, but the data does not support the hypothesis that it will give more, all else held equal.

Predicted 2020 Grants (From Combined Two-Stage Hurdle Model) by Number of Previous Grantees.

Hypothesis 3a

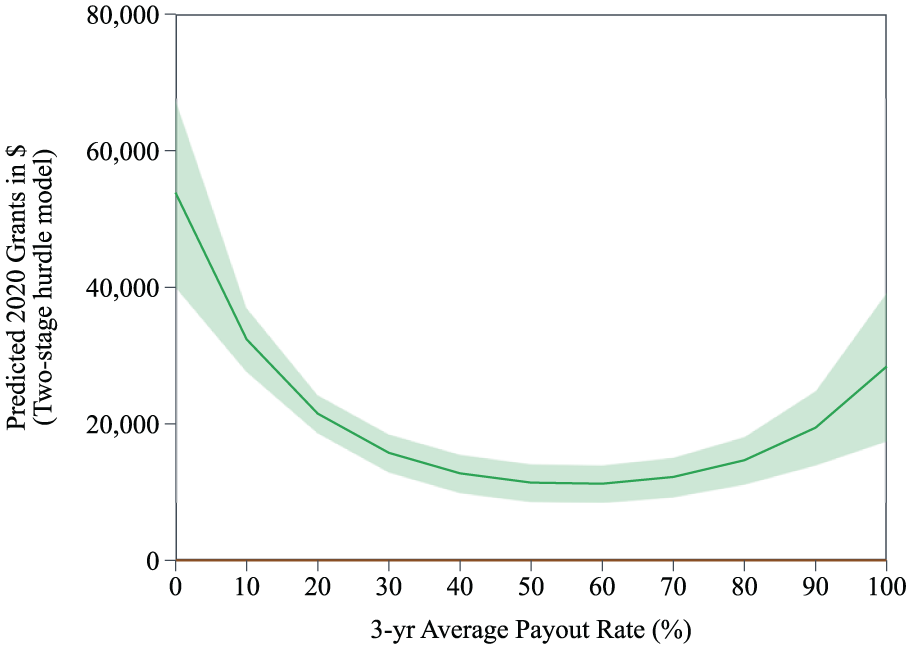

The regressions yield some support for H3a, that DAFs with lower payout rates have more slack and granted more in 2020. The OLS and second-stage GLM results from the hurdle model indicate a U-shaped relationship between payout rates and total grantmaking. Most DAF accounts (approximately 87% in this sample) have payout rates of 50% or less, and the relationship between payout rate and 2020 grants to all causes is negative for these levels of payout, generally supporting the hypothesis. However, the first-stage Logit results from the hurdle model were not statistically significant. In other words, regardless of payout rates, those DAFs that were previously making grants were similarly likely to make grants in 2020 (very few stopped making grants). Only those DAFs that had not made grants from 2017 to 2019 (those with a zero-payout rate) had a statistically significant increase in the likelihood of making grants in 2020. This demonstrates that payout rate predicts the amount of grantmaking, but not the act of grantmaking. Figure 7 depicts predicted giving from the combined two-stage hurdle model. DAFs with lower payout rates (less than about 20%) had higher predicted giving than other DAFs, but DAFs with the highest payout rates (about 90% or more) had higher predicted giving than those with mid-range payout rates. Note here that the graph should not be interpreted to mean that zero payout rate accounts had the highest giving. These accounts are not represented in the graph. Based on these results, we conclude that there is fairly strong evidence that low payout rate DAFs have more slack.

Predicted 2020 Grants (From Combined Two-Stage Hurdle Model) by Payout Rate.

Hypothesis 4a

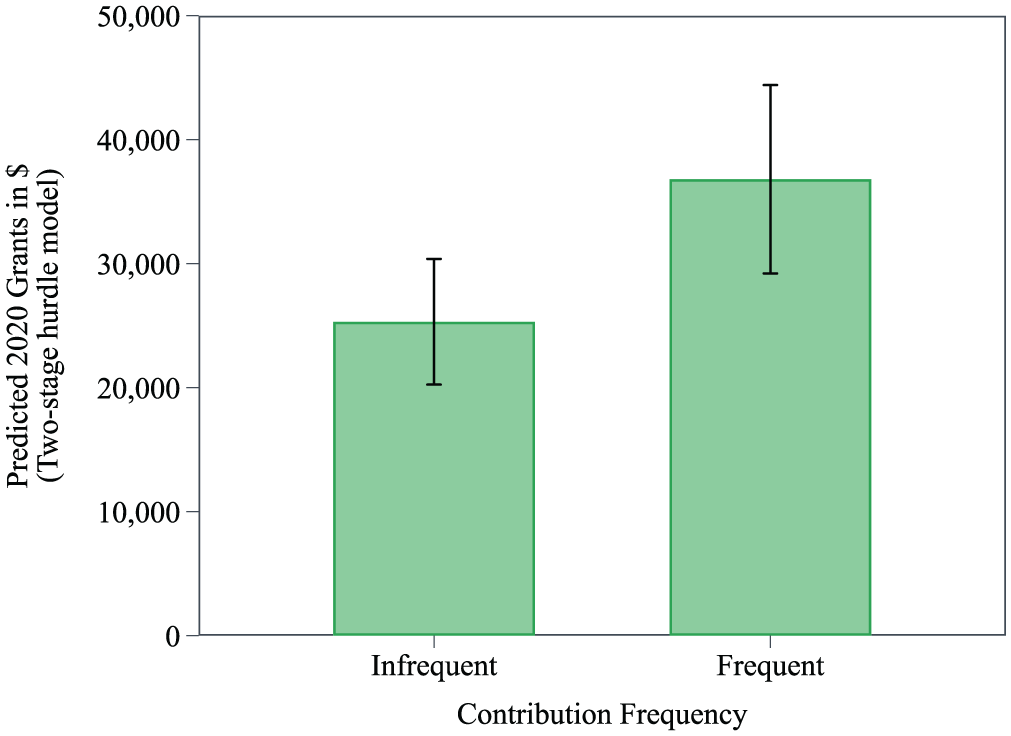

The data do not support H4a, which posited that DAFs with frequent contributions have less slack. The hypothesis was based on the idea that tub donors would mentally budget their annual donations and would have less available slack. Evidence from the regressions supports the opposite conclusion. While the OLS does not have significant results, the hurdle model results indicate that DAFs with frequent contributions are both more likely to make a grant in 2020 (first-stage Logit results) and to grant higher amounts (second-stage GLM results), all else held equal. Figure 8 depicts the predicted giving from the combined two-stage hurdle model (with error bars showing 95% confidence intervals) by contribution frequency. DAFs with more frequent contributions had higher predicted donations than DAFs with fewer contributions, all else held equal. We explore possible explanations for this finding in the discussion section.

Predicted 2020 Grants (From Combined Two-Stage Hurdle Model) by Contribution Frequency.

Hypothesis 5a

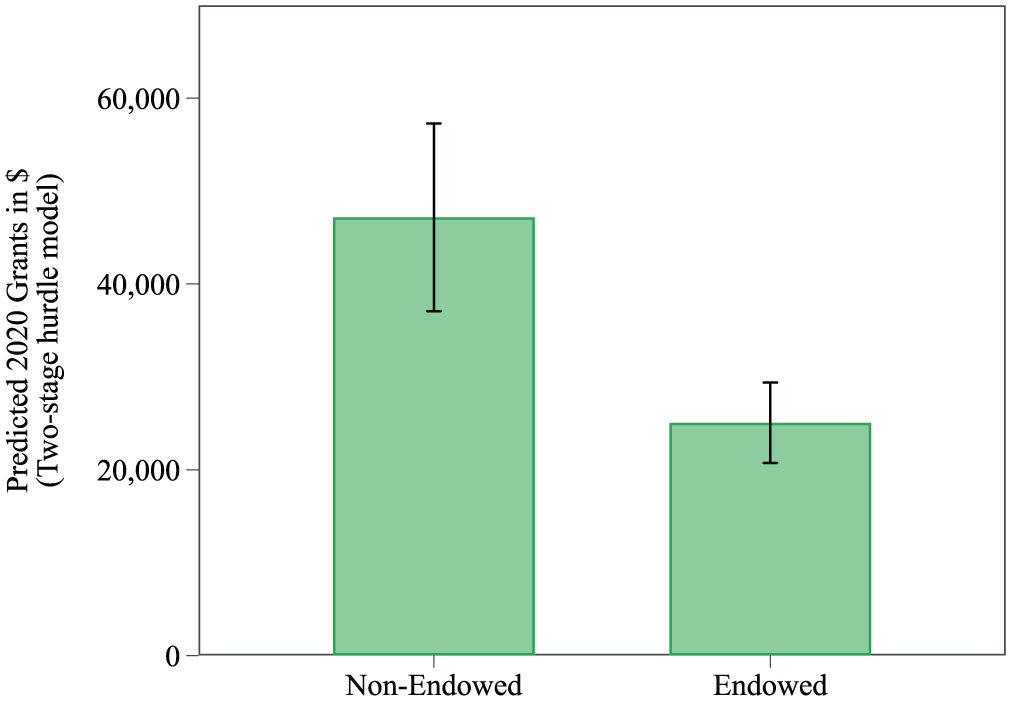

Our results support H5a, which formally endowed DAFs have less slack. Both the OLS and the second-stage GLM models, which include a binary indicator variable and a quadratic control for payout rate, yield significant, negative coefficients on the variable indicating that an account was endowed. The first-stage Logit coefficients from the hurdle model were likewise negative, but not significant. This is relatively strong evidence that, after controlling for prior grantmaking behaviors, non-endowed DAFs are likely to give more in times of need compared with endowed DAFs. Figure 9 compares the predicted 2020 giving (with error bars showing 95% confidence intervals) from the combined two-stage hurdle model for non-endowed and formally endowed DAFs. All else held equal, the non-endowed DAFs had significantly higher predicted values. This finding provides support for the theory that formally endowed DAFs have less slack to increase grantmaking.

Predicted 2020 Grants (From Combined Two-Stage Hurdle Model) by Endowment Status.

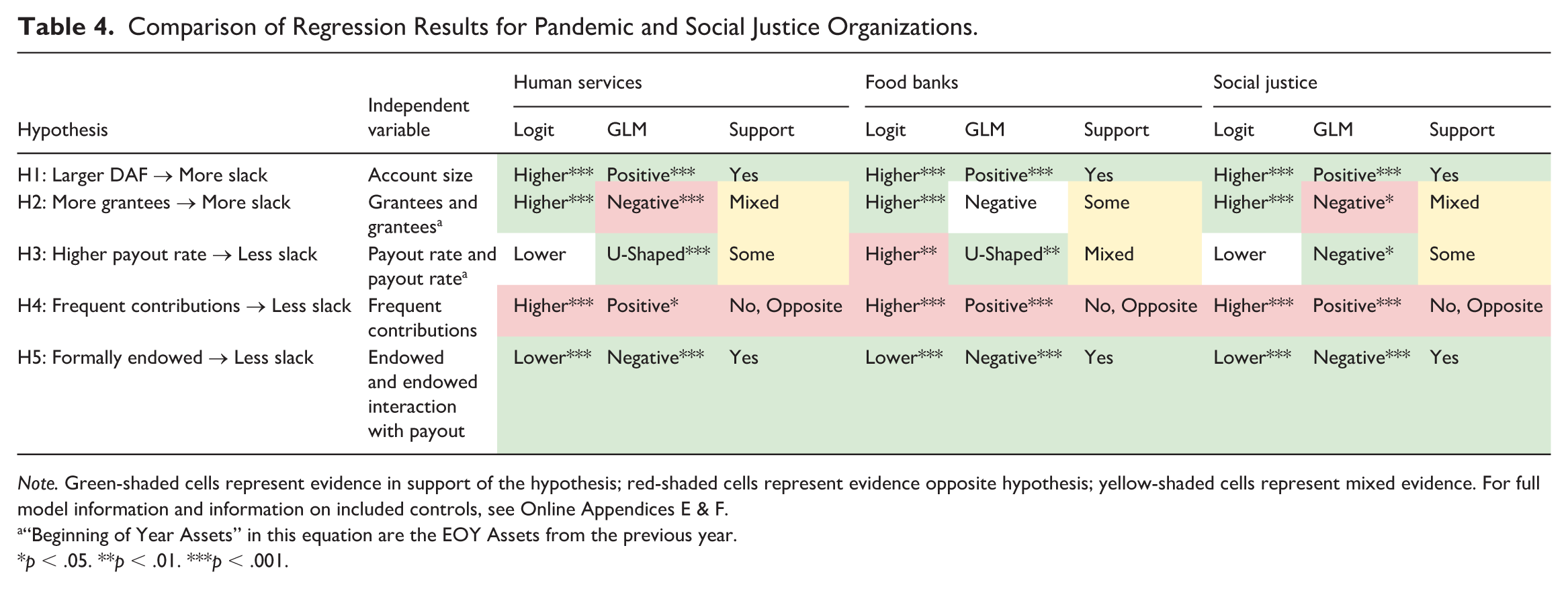

Regression Analysis and Hypothesis Testing: Pandemic and Social Justice Causes

We find the relationship between slack-related factors and giving to the pandemic and social justice was similar to overall giving, with some nuances. Table 4 shows the summary evidence for each hypothesis (b) for each area of giving: Human Services, Food Banks, and Social Justice. In the table, we focus on the preferred two-stage hurdle model. The OLS model found similar relationships, although some were not significant, which reflects the poorer fit between the model and the data. The regression tables associated with Table 4 can be found in Online Appendices G, H, and I.

Comparison of Regression Results for Pandemic and Social Justice Organizations.

Note. Green-shaded cells represent evidence in support of the hypothesis; red-shaded cells represent evidence opposite hypothesis; yellow-shaded cells represent mixed evidence. For full model information and information on included controls, see Online Appendices E & F.

“Beginning of Year Assets” in this equation are the EOY Assets from the previous year.

p < .05. **p < .01. ***p < .001.

Hypothesis 1b

We see consistent evidence for the relationship between size and slack. Even after controlling for previous grantmaking amounts, larger accounts were more likely to give and gave more to pandemic- and social justice-related causes.

Hypothesis 2b

We found mixed results for H2b, that DAFs with more grantees would give more to Human Services, Food Banks, and Social Justice. The Logit regressions in the hurdle model indicated that DAFs with more grantees were more likely to give to these specific causes. But marginal donors make smaller gifts, on average, so there is a significant negative relationship in the GLM results for Human Services. A negative relationship also exists for giving to Social Justice, although it is only significant above six grantees; there is also a negative (although insignificant) relationship for Food Banks. Overall, while the combined two-stage hurdle model generally showed an insignificant relationship, there was a positive relationship between giving and the number of pre-2020 grantees for the lower levels of the grantee count range for Human Services (0 to 10) and Food Banks (0 to 4).

Hypothesis 3b

There is mixed evidence for H3b that lower payout rates indicate more slack for emergent causes. We find some evidence for the hypothesis in the areas of Human Services and Social Justice, but mixed evidence for Food Banks. The first-stage Logit results from the hurdle model are generally insignificant. However, in the case of Food Banks, we see that as payout rates increased, the probability of making at least one gift to a food bank also increased. However, conditional on giving something, lower payout rates do give statistically significantly more to all three areas, up until a certain point—about 50% to 70%. This provides some evidence that it is less common for higher payout rate DAFs to make additional grants to emergent causes.

Hypothesis 4b

We find no support for H4b, that higher contribution frequency indicates lower slack. Like H4a, we find that DAFs with higher contribution frequency demonstrated more slack in giving to Human Services, Food Banks, and Social Justice. They were both more likely to make grants to these areas and to give more when granting.

Hypothesis 5b

We also find that endowed accounts gave less to emergent causes, even after controlling for previous grantmaking and payout rates. This supports the theory that these accounts had less slack in their grantmaking and is consistent with the results of H5a regarding giving to all causes in 2020.

Discussion

The goal of this paper was to investigate how and why DAFs allow donors to respond to emergent needs by examining and explaining the variation underlying the aggregate increase in DAF grantmaking during 2020. Much of the previous literature treats DAFs as monoliths with uniform features and singular effects on society. This is primarily because they focus on the contours of the federal regulations (e.g., Colinvaux & Madoff, 2019; Gibbons, 2022; Hussey, 2010), or rely on aggregated IRS data (e.g., Grennan, 2022; Heist & Vance-McMullen, 2019; Hemel et al., 2021; Qu & Paarlberg, 2022; Wu, 2020). The literature on the responsiveness of DAF donors to crises reports aggregated effects (Giving USA, 2021; National Philanthropic Trust, 2020; SatoKumar et al., 2020) but lacks organization-specific, account-level data to explain the variation of responsiveness among DAFs. Using a unique dataset, this article provides a much more granular analysis by comparing differences between individual DAF accounts. Moreover, by using the concept of organizational slack, this article bridges DAF research and organizational theory, emphasizing the relative autonomy of individual DAF accounts within the same sponsoring organization. This conceptualization of DAFs as mini-organizations being effectively managed by individual donors invites the application of other organizational theories in the study of DAFs and challenges future research to focus on account-level variation between DAF accounts.

We hypothesized and tested key factors related to grantmaking and found that each of the factors tested was at least somewhat predictive. Three of these factors directly aligned with our hypotheses. Account size was a clear predictor of giving. Even after controlling for previous grantmaking and the slope of previous grantmaking, DAFs with more assets granted more. This is strong evidence that larger DAFs have significant resource slack and are most capable of responding to emergent causes. DAF payout rate also predicted giving, with lower-payout-rate DAFs giving more than those with moderate payout rates, all else held equal. Those who took a slower approach to grantmaking were more capable of granting when emergent causes arose, which aligns with the slack concept. While the highest payout rate DAFs were also strong givers, these were much less common in our sample. Finally, endowed DAFs gave less, which we interpret as an indication of lower slack. This is not surprising because the policies that govern endowed accounts do not allow for substantial changes in grantmaking. One important finding from this analysis is preliminary evidence for informally endowed DAFs. DAFs with low payout rates, which were not formally endowed, had higher predicted grantmaking, all else equal. These donors treated their DAFs like an endowment, but retained potential slack and could grant out the principal when needed.

Two of the factors tested had results that were not completely aligned with our initial hypotheses, but still yielded interesting insights related to the concept of slack. The number of prior grantees yielded mixed results. We hypothesized that those who spread their grantmaking more broadly would have more recoverable slack to increase their grantmaking. The inverted U-shaped relationship between number of grantees and grantmaking indicated that having more grantees was associated with more 2020 grantmaking, up to a certain point. Having a large number of grantees, however, was associated with lower 2020 grantmaking, all else equal. The optimal number of grantees was about four organizations for overall giving and Food Bank giving, and 10 organizations for Human Service giving. It is possible that having multiple grantees indicates a more pluralistic approach to philanthropy, allowing for more openness to emergent causes. However, we had hypothesized an inverse relationship between the number of grantees and commitment to the organizations supported, yielding more recoverable slack at higher grantee counts. The evidence here suggests that some donors with many grantees may be strongly committed to all of the organizations they grant to, leading them to perceive those dollars as less recoverable.

The contribution frequency results strongly contradicted our hypothesis. This finding helps refine our conceptualization of slack as it relates to the tubs, tanks, and tower giving models put forth by Heist et al. (2022). We incorrectly thought tub donors, with more frequent contributions, would have less slack. The data instead shows that DAFs with frequent contributions were significantly more likely to make grants and to give larger grants in 2020. Contribution frequency included the years before 2020, so the behavior was already established before the emergent causes arose. It is possible that the pattern of contributing frequently to a DAF draws on other slack resources that are not measured in this study, for example, income, savings, investments, and other assets. So, those who contribute frequently can adjust their annual DAF contributions to meet the demands of emergent causes. If true, this would also explain the behavior of the highest-payout accounts, which were typically tub donors.

The relationship between the tested factors and grantmaking lends evidence to the importance of slack in understanding emergent giving. Interestingly, the patterns of slack giving were very similar across all causes, pandemic-related causes, and social justice organizations. The similarity of the response patterns indicates that the factors that predicted slack giving in this study may also predict slack giving in the future when other emergent causes place unexpected demands on the philanthropic sector.

Limitations

It is important to note some of the limitations to this study’s generalizability to all slack giving. The pandemic and the demands for social justice were particularly poignant causes, and other emergent situations may not evoke such strong philanthropic responses from a broad population. In less urgent crises, philanthropic responses like reallocating recoverable slack may be rarer, which would affect the hypotheses around payout rate and grantees. Another limitation is that our sample skewed toward DAFs held by large community foundations. DAF donors at these types of organizations may be more responsive to the causes in this study than donors at other DAF organizations. Our sample included only US-based DAFs and may not represent DAF behaviors in other countries. Our study also did not capture other forms of giving. So, donors who gave less through their DAF in our study may have given more from their checkbook or some other way during the study period. Therefore, our findings may not explain all forms of philanthropic responses to emergent causes.

This study was also limited in its ability to measure donor characteristics and perceptions. More research is needed to understand the relationship between donor perceptions of slack and actual resources available for giving. We also did not measure the degree of commitment of donors to existing grant recipients. While some donors may be firmly committed to existing grantees, other commitments may be more flexible. Moreover, this study only analyzed giving patterns within a 4-year window. The slack position of a DAF and donor perceptions likely change over the life cycle of the DAF and donor, highlighting the need for more longitudinal research.

Implications

The conceptual framework and findings from this article advance our understanding of both variation among DAF accounts and donor behavior during crises, providing a foundation for future research. Future studies could examine how differences across DAFs influence donor responsiveness to policy interventions, such as tax law changes, as well as to behavioral interventions and sponsor programming aimed at encouraging specific giving behaviors. The concept of slack introduced here could also be applied to understand crisis-related behaviors in other philanthropic intermediaries, such as foundations and giving circles. More broadly, it may offer insights into shifts in individual giving or even governmental budgeting decisions during times of crisis.

The slack concept and findings from this article can help nonprofit professionals better understand DAF donors’ responses to crises, enabling more strategic and timely solicitations. While fundraisers may have previously understood that DAFs can be “rainy day funds,” identifying which specific DAF accounts are most likely to increase their giving—and understanding the type of slack they hold—can help tailor solicitations during urgent situations. Segmenting DAF accounts using the observable characteristics analyzed in this article would involve targeting larger, non-endowed accounts with relatively frequent contributions and relatively modest payout rates. In addition, understanding donor perceptions of their account slack would also help fundraisers identify prospects. In particular, conversations with donors that center around their plans for their funds and the degree to which those plans are malleable would identify those accounts with large amounts of available and easily recoverable slack. These accounts would be relatively good prospects for crisis-related solicitations. Conversely, donors who reveal a strong intention to use their funds for long-term philanthropy or pass their account to the next generation, which are indications of an informally endowed account, might indicate only potential slack and therefore less ready prospects for crisis giving.

Conclusion

In conclusion, this study advances our understanding of DAF grantmaking by treating DAF accounts as distinct entities, each with varied characteristics and philanthropic behaviors. It also translates the concept of organizational slack into the DAF context, which may help illuminate crisis responses in other parts of the philanthropic sector as well. Empirically, it identifies which account characteristics are associated with grantmaking to specific causes and organizations during crises. While such crises remain unpredictable, DAF grantmaking to emergent needs is now somewhat more predictable.

Supplemental Material

sj-docx-1-nvs-10.1177_08997640251374264 – Supplemental material for Give Me Some Slack: Donor Advised Fund Granting During Crises

Supplemental material, sj-docx-1-nvs-10.1177_08997640251374264 for Give Me Some Slack: Donor Advised Fund Granting During Crises by Danielle Vance-McMullen, H. Daniel Heist and Lindsey Walker Eftin in Nonprofit and Voluntary Sector Quarterly

Footnotes

Acknowledgements

We thank Giving Compass for providing the list of vetted Social Justice organizations. We gratefully acknowledge several students at Brigham Young University who worked on this study, including Kortney Wall-Gong, Pohai Kealoha, and Rachel Sumsion. We thank the DAF Research Collaborative (DAFRC), including those DAF sponsors who shared their anonymized administrative data and GivingTuesday Data Commons, DAFRC’s data security and administration provider. This work was supported, in whole or in part, by the Bill & Melinda Gates Foundation [INV-016953]. The conclusions and opinions expressed in this work are those of the authors alone and shall not be attributed to the Foundation.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported, in whole or in part, by the Bill & Melinda Gates Foundation.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data are not publicly available due to ethical, legal, or other concerns. Academic researchers who wish to access the data may contact the authors to submit a data use application to the DAF Research Collaborative.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.