Abstract

Despite the abundance of literature related to nonprofit overhead, the following questions remain unclear: (a) How high is too high for individual donors when considering an organization’s overhead? (b) Is there a difference between nonprofit subsectors in individual donors’ aversion to nonprofit overhead? Moreover, (c) Does trust play a role in individual donors’ overhead aversion? This study used a survey experiment and randomly assigned participants to one of four overhead ratio conditions (5%, 20%, 35%, and 50%). We find that individuals’ donations to human service nonprofits substantially decrease when the overhead reaches 35%. In contrast, their donations to health care nonprofits do not decrease until the ratio reaches 50%. In addition, we find that donors lose trust in nonprofits when overhead costs are higher, leading to decreased donations. The findings contribute to the theoretical understanding of donors’ giving behavior, offering practical implications for promoting sustainable giving.

Introduction

Overhead costs, often seen as a necessary evil, play a crucial role in the infrastructure and operations of nonprofit organizations (NPOs). Scholars have emphasized that these costs, which include administrative and fundraising expenses, are essential for NPOs to function efficiently and achieve their mission (Lecy & Searing, 2015). However, this perspective is not universally shared—especially among donors who have a prevalent aversion to NPOs with high overhead costs (Hung et al., 2023; Kim et al., 2024). This “overhead aversion” reflects donors’ tendency to equate lower overhead with greater impact and efficiency (Gneezy et al., 2014; Qu & Daniel, 2021a) and penalize organizations with higher nonprogram costs (Hung et al., 2023). The dichotomy presents a significant challenge for NPOs, as they must balance the need for sufficient overhead to support their operations with the desire to attract and retain donors who prefer minimal overhead expenditures.

The emphasis on the overhead ratio in nonprofits and among donors arises due to the lack of standardized performance measures in the sector, leading to a heavy reliance on financial ratios for evaluation (Eckerd, 2015). In addition, challenges in data collection within nonprofits compound this trend. Some lack resources for comprehensive data gathering, especially for intangible outcomes (Mitchell & Calabrese, 2019). Even when feasible, data may not be publicly accessible to donors (Berrett, 2020). For instance, IRS Form 990, the primary public data source, lacks insight into mission attainment. Despite its imperfections, this leads to reliance on functional expense information for evaluation (Coupet & Berrett, 2019). Furthermore, watchdog organizations’ adaptation of the overhead ratio and donor misconceptions further entrench this focus (Berrett, 2022).

The prevalence of overhead aversion triggers what is known as the “nonprofit starvation cycle.” This cycle is characterized by funders’ unrealistic expectations about NPO operating costs, leading NPOs to attempt to satisfy funders by underreporting their costs and underinvesting in essential systems. Such actions reinforce funders’ misconceptions about NPOs’ need for overhead costs (Gregory & Howard, 2009; Hung et al., 2023). This phenomenon is not confined to a specific geographic region and is observed across various countries (Lecy & Searing, 2015; Schubert & Boenigk, 2019). Moreover, the starvation cycle is challenging to disrupt, even when NPOs are transparent about the use of their administrative budgets (Tian et al., 2020).

While the detrimental effects of overhead aversion are widely recognized in the scholarly literature, certain aspects still warrant further investigation. First, the degree of overhead aversion, as reported in various studies, is based on different overhead cost ratios, such as 5% (Gneezy et al., 2014; Qu & Daniel, 2021a), 20% (Gregory & Howard, 2009; Portillo & Stinn, 2018; Schubert & Boenigk, 2019), 35% (Better Business Bureau Wise Giving Alliance, 2023; Gneezy et al., 2014; Tian et al., 2020), and 50% (Gneezy et al., 2014; Portillo & Stinn, 2018). However, except for one study (e.g., see Allred & Amos, 2022), there is limited evidence of what individual donors perceive as an excessively high overhead ratio. Second, overhead aversion may vary across different NPO sub-sectors (Altamimi & Liu, 2022). Such variation has not been widely tested, leaving us uncertain about which NPO sub-sectors are more tolerant of overhead costs. Finally, trust is a critical factor influencing donations to NPOs (Bekkers, 2003; de Azevedo & Braga de Aguiar, 2021; Frumkin & Keating, 2010; Sargeant & Lee, 2004). However, its role in shaping donors’ attitudes toward NPO overheads remains unexplored.

Intrigued by these unresolved questions, we engaged 1,529 participants in a randomized controlled trial experiment, collecting both quantitative and qualitative responses. These responses allowed us to test hypotheses derived from four propositions. First, beyond a certain critical threshold of overhead ratio, the level of giving from donors will experience a significant decrease. Second, subsectoral differences are evident: Individual donations to health care NPOs are more resistant to increases in overhead costs than are individual donations to human service NPOs. Third and fourth, a high overhead ratio can also reduce individual donors’ trust in NPOs, potentially impacting their donations negatively.

This empirical study offers both theoretical and practical insights. First, it identifies a negative relationship between overhead ratio and individual giving, pinpointing a threshold at which donation amount begins to decrease significantly. This finding is a crucial insight for NPO managers, fundraisers, and donors, as it can guide their decision-making processes and strategies. Second, the observed subsector difference between human service and health care enriches our understanding of overhead aversion. It provides nuanced guidance for practitioners in the two sub-sectors and stimulates further research into overhead aversion across other service domains within the NPO sector. Finally, the role of trust in shaping donors’ attitudes toward overhead costs underscores the importance of trust-building in NPO management. It suggests trust-building as a solution to break the NPO starvation cycle. This finding contributes to the theoretical understanding of donor behavior and offers practical implications for enhancing donor-NPO relationships and promoting sustainable giving.

Overhead Ratio, Trust, and Individual Donations

For nearly two decades, scholars have studied the effect of overhead on giving, with mixed findings. In some cases, overhead spending is negatively related to donations. For example, studying the grant amount awarded by foundations to NPOs across the state of Georgia, Ashley and Faulk (2010) found that the fundraising expense ratio negatively impacts grant awards. Similarly, Tian et al. (2020) experimented and found that overhead negatively affects the decision to donate and the donation amount. In other cases, overhead spending is positively related to giving. For example, using samples of NPOs from across the United States, Calabrese (2011) and Nicholson-Crotty (2011) found that the administrative expense ratio positively affects donations. At the same time, other cases found no relationship between overhead and giving (Frumkin & Kim, 2001; Grizzle, 2015). However, a meta-analysis conducted by Hung et al. (2023), which included 30 studies examining the relationship between overhead and giving, found that overhead negatively affects giving. They attribute the inconclusive results of prior literature to the research design, type of donors, and overhead measures. Despite this abundance of relevant literature, many feel that the question “How high is too high?” when it comes to overhead still has yet to be decisively answered. The literature also fails to study the underlying mechanism of the relationship between overhead and giving.

Donors’ Reactions to Nonprofit Overhead

Different theories have been applied to understand the relationship between donors’ aversion to overhead and their giving habits. These include everything from risk aversion and evaluability bias to impact philanthropy and principal-agent theory. Bowman (2006) posits that people who are considering donating exhibit rationality and prefer avoiding risks. Caviola et al. (2014) and Spiteri (2022) apply evaluability bias, which is the tendency to assign greater importance to an attribute based on how easily it can be evaluated, rather than considering criteria that are deemed more relevant upon reflection (Caviola et al., 2014). At the same time, studies such as Gneezy et al. (2014) and Keenan and Gneezy (2016) use impact philanthropy to explain the relationship between overhead aversion and giving, which suggests that certain donors, specifically impact philanthropists, are driven by the desire to personally effect change. According to this perspective, impact philanthropists prioritize directing their resources toward a specific charitable cause rather than administrative costs, believing the former has a greater potential for creating a significant impact (Keenan & Gneezy, 2016). Others, such as Calabrese (2011), Harris et al. (2015), Surysekar et al. (2015), and Tian et al. (2020), focus on the agency problem between donors and NPOs. While each of these theories suggests that higher overhead leads to a decrease in donations, this study integrates risk aversion and principal-agent theory with a focus on trust to explain the relationship between donors’ aversion to overhead and their giving habits.

Principal-agent theory has evolved and developed through the contributions of numerous scholars in economics, management, and related fields (e.g., see Arrow, 1985; Hart & Holmström, 1987; Jensen & Meckling, 1976; Levine, 1996). The works of these individuals, among others, have collectively shaped the theory and provided valuable insights into understanding the dynamics of principal–agent relationships. The theory examines scenarios in which one party (known as the principal) assigns decision-making authority or responsibilities to another party (referred to as the agent) to act on the principal’s behalf (Eisenhardt, 1989; Jensen & Meckling, 1976). The principal–agent relationship is characterized by a divergence of interests between the principal, who seeks to maximize the organization’s utility or objectives, and the agent, who may have their own preferences or goals (Jensen & Meckling, 1976). Applied to the NPO-donor relationship, the NPO is the agent, while the donor is the principal. This dynamic is described in Harris et al. (2015, p. 582): Because nonprofit organizations are established to fulfill a charitable mission, they do not distribute profits or operate with clear lines of ownership and accountability (Fama & Jensen, 1983). In the absence of owners, donors often assume the role of the de facto principals in nonprofit principal-agent models. (Hansmann, 1996)

The primary concern of principal–agent theory is to recognize and address potential conflicts of interest that arise due to this divergence. The theory posits that agents, being self-interested, may not consistently act in alignment with the principal’s best interests (Jensen & Meckling, 1976). This misalignment of interests can lead to agency problems, such as moral hazard and adverse selection, resulting in suboptimal outcomes for the principal (Van Slyke, 2005). Adverse selection can occur when information asymmetry is present. According to Van Slyke (2005), information asymmetry is when agents possess more information than principals and can utilize it for their own benefit rather than working in the best interests of the collective contracting parties. This can give rise to moral hazard issues. For example, Surysekar et al. (2015, p. 63) posit that donors who contribute to NPOs encounter an agency dilemma as the managers of these organizations can allocate the donations toward programs and activities that may not align with the donors’ preferences and values.

To address these issues, some suggest monitoring and control mechanisms to reduce information asymmetry and agency costs. For example, the principal may use a combination of “incentives, sanctions, information systems (such as reporting procedures) and monitoring mechanism to motivate and enforce the behavior of the agent toward goal alignment” (Van Slyke, 2005, p. 2). Thus, as a control mechanism in the NPO–donor relationship, donors limit managerial discretion by enforcing restrictions on NPO spending (Hung & Berrett, 2021; Surysekar et al., 2015) or by expecting NPOs to minimize overhead costs (Kim et al., 2024; Shon et al., 2019; Yermack, 2017). Donors may also punish NPOs by withholding donations when NPOs spend (what they consider to be) too much on overhead. This, coupled with the research that shows that donors’ degree of overhead aversion is based on different levels of overhead (BBB Wise Giving Alliance, 2023; Gneezy et al., 2014; Gregory & Howard, 2009; Portillo & Stinn, 2018; Qu & Daniel, 2021a; Schubert & Boenigk, 2019; Tian et al., 2020), leads to:

Subsector Differences in Donors’ Reactions to Nonprofit Overhead

Divergent responses among donors in response to overhead considerations within different nonprofit subsectors have been a subject of scholarly investigation (Allred & Amos, 2022; Caviola et al., 2014; Spiteri, 2022). Caviola et al. (2014) observed a propensity among individuals to exhibit a greater willingness to contribute to charitable causes characterized by a lower overhead ratio. Their study further indicated that overhead aversion extended to both human and animal welfare organizations, albeit without a significant difference between the two.

Building upon Caviola et al.’s (2014) findings, Spiteri (2022) sought to replicate their study, revealing that participants were more willing to donate to nonprofit organizations when the overhead was lower. Notably, the inclination to donate was slightly more pronounced for human causes than animal causes. Concurrently, Allred and Amos (2022) delved into overhead aversion more comprehensively, aiming to ascertain the threshold beyond which donors perceive overhead as excessive. Their examination across diverse nonprofit subsectors identified a 25% overhead ratio as an appropriate upper limit aligning with the expectations for donor acceptance. This threshold appeared most pertinent to causes associated with humans and animals but less applicable to arts and cultural nonprofits, such as museums.

While Caviola et al. (2014) and Spiteri (2022) interpret these dynamics through the lens of evaluability bias, Allred and Amos (2022) propose that processing fluency theory provides a more comprehensive explanatory framework. They posit that the ease with which individuals evaluate information, termed “evaluability bias,” is intricately linked to processing fluency—the theory that the ease of information processing influences behavioral and decision-making outcomes (Allred & Amos, 2022).

According to Allred and Amos (2022, p. 8), “processing fluency would suggest that when it is easier to envision tangible overhead expenses (e.g., facilities, maintenance, etc.), then the tolerances toward overhead might be greater.” Therefore, it is suggested that overhead aversion is least pronounced in health care nonprofits. This stems from the notion that it may be comparatively more straightforward to conceptualize overhead as contributing rather than detracting from the delivery of health care services. Health care nonprofits, such as hospitals, clinics, and other similar health care providers, deliver health care through tangible overhead expenses, such as sophisticated buildings with state-of-the-art medical equipment and technology. This stands in contrast with human service nonprofits, characterized by their diverse range of activities spanning from addressing hunger issues to providing vocational training and advocating for children. Despite the essential of overhead in supporting these operations, donors may not possess a clear understanding of the nature of overhead expenses in these contexts or their direct contributions to the organizational objectives. This leads to:

Nonprofit Overhead and Donor Trust

The principal–agent theory can be applied to NPO overhead spending and donor trust by examining the relationship between donors and NPO managers. In this framework, donors entrust their resources to NPOs with the expectation that these funds will be used effectively and efficiently to further the organization’s mission. NPOs heavily depend on the public’s trust (Bekkers, 2003). According to Bekkers (2003), donors frequently lack knowledge regarding the precise utilization of their donations and the proportion allocated to overhead costs. Essentially, donors need to trust that NPOs will utilize their donations wisely.

NPOs are generally considered more trustworthy than public and for-profit organizations because of the nondistribution constraint (Bekkers, 2003). According to the nondistribution constraint, NPOs cannot distribute their profits to anyone who controls or manages the NPO (Hansmann, 1980). As Bekkers (2003, p. 597) notes: According to this theory, NPOs should be most active in situations of asymmetric information: When it is hard to get reliable information on the quality of the services provided, the NPO character of the service provider signals trustworthiness to the donor. (Hansmann, 1987; Heitzmann, 2000)

In the context of principal-agent theory, the nondistribution constraint functions as a “signal of trustworthiness” that aids in mitigating the agency problem between donors and NPOs (Van Puyvelde et al., 2012, p. 440). By restricting the distribution of profits, the nondistribution constraint aligns the interests of the NPO with donors’ expectations and intentions.

Donors often stay away from charities that allocate a large portion of expenses to administrative and fundraising efforts. They expect their contributions to be primarily directed toward maximizing social impact, and this allocation pattern may lead them to mistrust these organizations (Gneezy et al., 2014). While the relationship between the level of overhead spending and donor trust has not been empirically tested, numerous scholars have suggested that NPOs can maintain donor trust by minimizing their overhead spending (e.g., see Burt, 2012, 2014; Ebrahim & Rangan, 2010; Ebrahim & Wiesband, 2007; Gibelman & Gelman, 2001; Kearns, 1996; Quosigk & Forgione, 2018; Young et al., 1996). Faulk et al. (2020) discuss the relationship between overhead and trust as expressed through the donation price. They contend that donors are likely to contribute less if they sense a higher risk that their donation will be redirected away from the organization’s programs. Essentially, when donors see more of their donation going toward overhead, they see the price of their donation go up. In other words, “donors’ perceived price of their donation increases when they trust the organization less and when they perceive that donations may be diverted from mission-related activities to other uses” (Faulk et al., 2020, p. 223). Furthermore, it is argued that donors’ reluctance toward overhead spending initiates a cycle that could undermine the effectiveness of NPOs and result in a decline of trust in philanthropy (Hager, 2004; Tian et al., 2020). This, in turn, leads to:

Donor Trust and Donation Amount

NPOs play a critical role in mitigating the challenges posed by principal-agency theory as they are inherently trustworthy due to their nature. Donor trust is crucial because it influences willingness to donate (Balsam & Harris, 2014; Blouin et al., 2018; Sargeant & Lee, 2004; Sargeant et al., 2006). When donors perceive NPOs as reliable agents who will act in alignment with the donors’ values and intentions, they are more likely to trust the organization and be willing to donate. However, should donors perceive a lack of transparency or accountability, it can lead to a breakdown in trust and a decrease in willingness to donate (Farwell et al., 2019).

Similar to the relationship between overhead and trust, the relationship between donor trust and the donation amount can also be understood through the principal health care agent theory, focusing on information asymmetry. The principal health care agent theory highlights the information asymmetry between donors and NPOs, where donors may have limited knowledge about the organization’s internal operations, financial management, and impact (Van Slyke, 2005). This information asymmetry creates a potential agency problem, as donors rely on the NPO to act as their agent and make decisions in their best interests (Van Slyke, 2005). Nonprofits, through their commitment to transparency and mission-driven nature, play a crucial role in mitigating this challenge.

Blouin et al. (2018) argue that voluntary financial disclosure (such as overhead and program ratios) can enhance trust and the decision to donate, suggesting that decreasing information asymmetry increases trust. For example, disclosing financial ratios can improve transparency and reduce information asymmetries between NPOs and donors. In another study, Balsam and Harris (2014) find that NPOs with higher executive compensation experience reduced donor support. In other words, donors punish NPOs that have higher overhead spending. Balsam and Harris (2014) attribute this to a lack of trust in the organization because donors want to ensure their contribution is well spent. Donors may perceive funds spent on compensation or overhead as not supporting an organization’s mission. In related studies, Sargeant and Lee (2004) and Sargeant et al. (2006) examine the relationship between trust and donor giving behavior, finding a positive relationship and suggesting that factors such as commitment and reduced transaction costs mediate this relationship. This leads to:

Method

Experimental Design and Data Collection

This study employed a between-subject survey experiment to understand individual donors’ aversion to NPO overhead. We surveyed 1,600 individuals in the United States via Prolific and received 1,595 responses on July 30, 2022, as five participants did not consent to the use of their responses for data analysis. 1 Prolific’s participants are primarily from Organization for Economic Co-operation and Development (OECD) countries, except Turkey, Lithuania, Colombia, and Costa Rica, where Prolific is unavailable, and South Africa. However, for this study, we restricted our participant selection to individuals currently residing in the United States. Prolific participants must be at least 18 years old. They are mainly recruited through word-of-mouth referrals via social media. After creating an account on Prolific, participants receive notifications about studies they qualify for based on the demographic information they provide. Researchers post studies on Prolific, and email invitations are sent to a random subset of eligible participants every 48 hours until the maximum number of submissions is reached.

Prolific’s data are considered reliable due to the lower likelihood of participant dishonesty and greater naivety. For instance, participants are typically unaware of the experimental hypotheses and have not previously taken part in this study. (Peer et al., 2017). Moreover, Prolific improves the validity of research results by offering clear guidelines on the rights, duties, and compensation of participants (Palan & Schitter, 2018). For instance, high-quality research is expected to follow universal ethical standards by paying participants reasonable compensation for their contribution. Prolific enforces a minimum reward of US$8 per hour, recommending researchers pay participants US$12 per hour. As we expected it would take participants 5 min to complete our survey, this study paid participants US$1 for their contribution (hourly reward of US$12) to ensure data quality. We refined the raw data to improve the accuracy and robustness of our analysis. First, as the average time to complete the survey was 5 min and 3 s, we assumed that participants who spent less than 2 min to complete the survey may not have read the survey questions carefully, while those who spent more than 30 min may have been distracted by other activities (Chandler et al., 2014). This study thus removed their responses to improve data quality (55 responses removed). Second, we removed responses that had a duplicate Internet protocol address as this indicated the same participants filled out the survey more than once (9 responses removed). Finally, we removed two respondents who reported that their age was five. This may be a typo as the two respondents also reported they were older than 18 in a question used by this study to determine participants’ eligibility for participation in this experiment. The data cleaning process removed 66 responses, leaving a total of 1,529 responses for data analysis, which suffices to detect an effect size of f = .10 across four conditions at α = .05 and a power of .80, according to our power analysis.

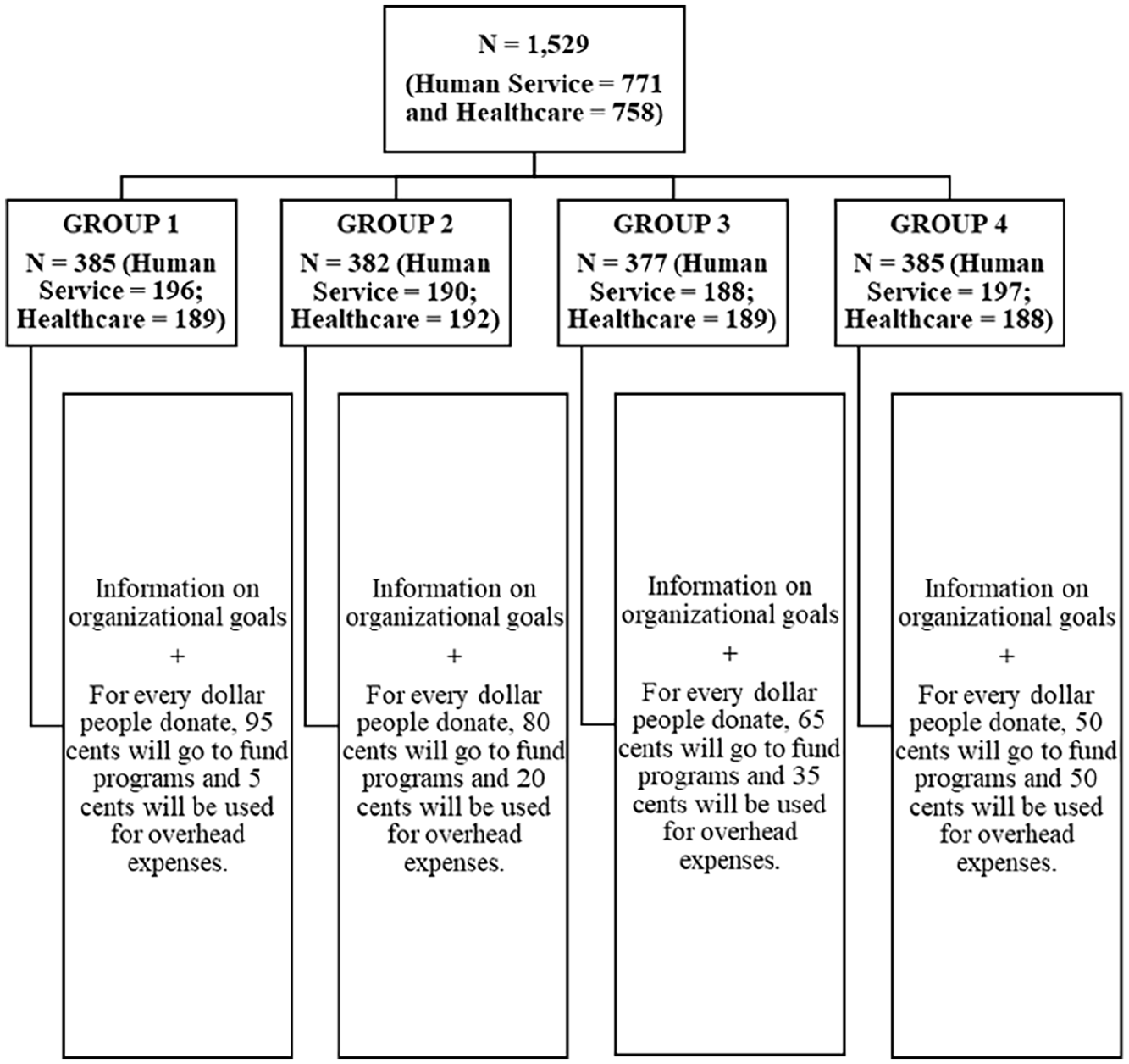

In the experiment, we presented half of the participants with a solicitation letter from a fictitious human service NPO and the other half with a solicitation letter from a fictitious health care NPO. This design enabled us to answer the second research question: Is there a sub-sectoral difference in donors’ aversion to NPO overhead? Our selection of human service versus health care nonprofits was based on (a) human service nonprofits represent the largest sub-sector within the nonprofit industry. This subsector has garnered significant attention due to its strategic role in supporting the social safety net. Many government mandates rely on nonprofits within this sub-sector for their implementation (see Lecy & Van Slyke, 2013; Searing, 2012), (b) the view that health care nonprofits play a vital role in bolstering health equity during the pandemic. They are uniquely obligated to advance community health and are well-suited to enhance population health as trusted clinical care providers within local communities (see Cramer et al., 2021; Rapfogel & Gee, 2021), and (c) the argument in the literature that donors may react to different types of nonprofits differently (Allred & Amos, 2022; Caviola et al., 2014; Spiteri, 2022). Specifically, unlike health care NPOs, which depend largely on commercial income, human service NPOs rely heavily on donations to deliver services. Thus, compared with health care NPOs, donors may be relatively keen on understanding how human service NPOs spend their money and may be more sensitive to the overhead spending of human service NPOs. In addition, by employing fictitious organizations instead of real ones, we can circumvent potential bias stemming from participants’ prior knowledge of an NPO (Coleman, 2018).

As the purpose of this study was to understand donors’ reactions to NPO overhead, we randomly assigned participants to four groups, each of which was presented with a different overhead ratio. Participants in the first group were provided with information about an NPO that spent 5% of its total expenses on overhead expenses, which include administrative and fundraising expenses, as that ratio has been used as a base number by previous studies (e.g., Gneezy et al., 2014; Qu & Daniel, 2021a). Participants in the second group were provided with information about an NPO that spent 20% on overhead, a benchmark that has been driven by funders, individuals, and the nonprofits themselves (e.g., Gregory & Howard, 2009) and used by previous studies (e.g., Portillo & Stinn, 2018; Schubert & Boenigk, 2019) to examine donors’ overhead aversion. Participants in the third group were provided with information about an NPO that spent 35% on overhead. This ratio has been used by the BBB Wise Giving Alliance to advise NPOs on how much they should spend on overhead, and by previous research (e.g., Gneezy et al., 2014; Tian et al., 2020). Finally, participants in the fourth group were provided with information about an NPO that spent 50% on overhead. This ratio has been considered by previous researchers (e.g., Gneezy et al., 2014; Portillo & Stinn, 2018) as a high overhead ratio (Figure 1).

Survey Experiment Design.

Dependent Variable: Donation Amount

This study measured the donation amount by asking participants, “How much do you believe a person like yourself would be willing to give to the nonprofit organization described earlier on a monthly basis if asked?” on a sliding scale of US$0 to US$100.

Organizational Trust

To test Hypotheses 3 and 4, this study measured organizational trust by taking the items used by Pirson and Malhotra (2011). We slightly modified their items to fit in the context of the nonprofit sector. Specifically, participants were asked to answer the following four questions in the survey on a scale of 1 = Strongly Disagree to 7 = Strongly Agree: (a) I trust the organization; (b) I would recommend the organization because I predict a good future for the organization; (c) I would recommend to friends that they donate, volunteer, work for, or work with the organization; and (d) I would interact with the organization. Cronbach’s α of the four questions was .95. We then added the values of all the items to create one organizational trust measure. Organizational trust was a dependent variable in Hypothesis 3, whereas it was an independent variable in Hypothesis 4.

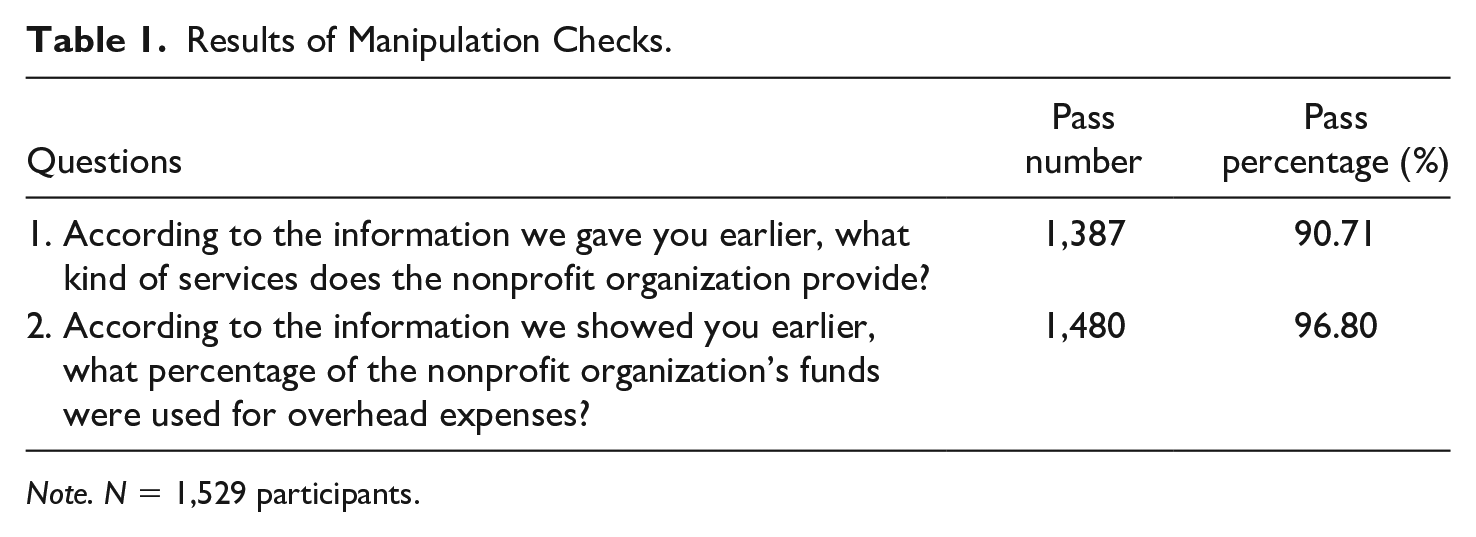

Manipulation Checks

This study conducted two manipulation checks to see whether participants received the important information we delivered. First, we asked participants, “According to the information we gave you earlier, what kind of services does the nonprofit organization provide?” They were given the options of arts and culture, human services, health care, and information not provided. Second, we asked participants, “According to the information we showed you earlier, what percentage of the nonprofit organization’s funds were used for overhead expenses?” They were given the options of 5%, 20%, 35%, 50%, and information not provided.

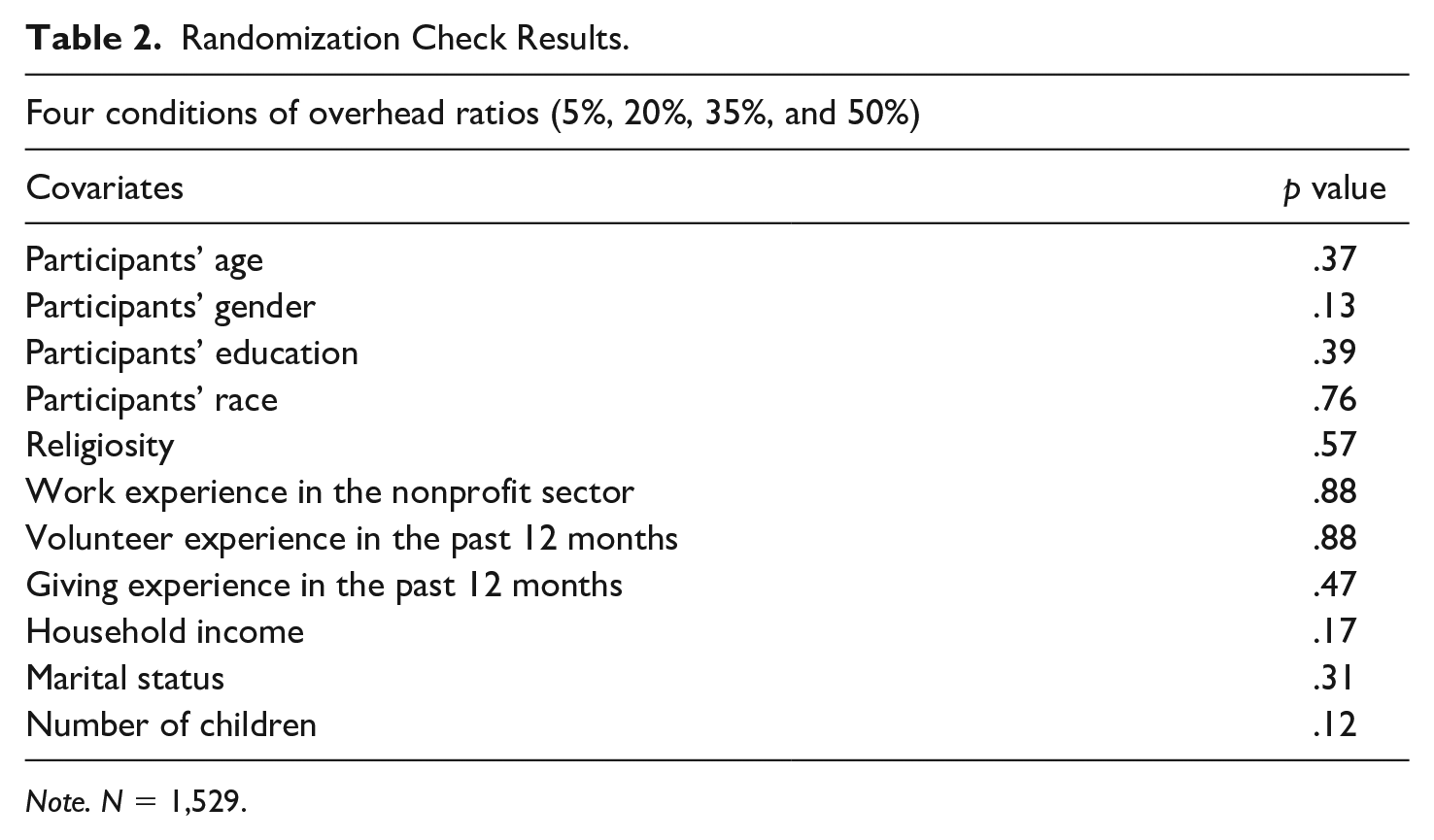

Randomization Checks

To check randomization, this study included demographic characteristics, such as participants’ age, gender, race, religiosity, work experience, educational attainment, household income, volunteer and giving experience, marital status, and children (Lwin et al., 2014; Robson & Hart, 2021). We expected that participants were assigned equally to the four groups (5%, 20%, 35%, and 50% overhead ratio). The means among the four groups were similar for all demographic characteristics.

Results

Participants (N = 1,529)

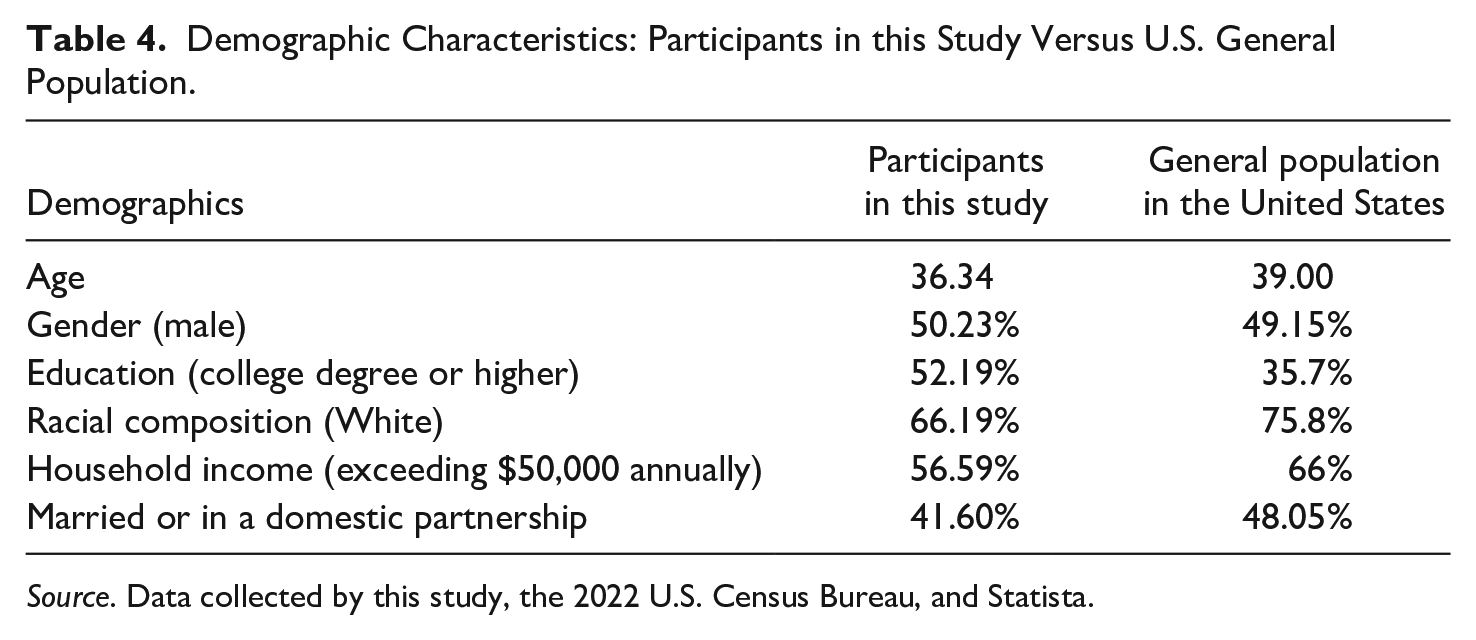

The average age of participants in this study was 36.34 years. Of the participants, 50.23% identified as male, 46.50% as female, and 2.55% as nonbinary. A total of 52.19% of the participants held a college degree or higher. In terms of racial composition, 66.19% were Caucasian/white, followed by Asian American (11.84%), African American/Black (7.29%), and Latino(a)/Hispanic (5.69%). About 24.79% of participants had prior paid experience at an NPO, while 39.57% had attended religious services. Volunteer experience at an NPO in the preceding year was reported by 42.25% of participants, and 70.18% had made charitable donations to an NPO during the same period. More than half (56.59%) of the participants had an annual household income exceeding US$50,000, and 41.60% were either married or in a domestic partnership. Finally, 70.63% of the participants did not have children.

Donation Amount ($0 to $100)

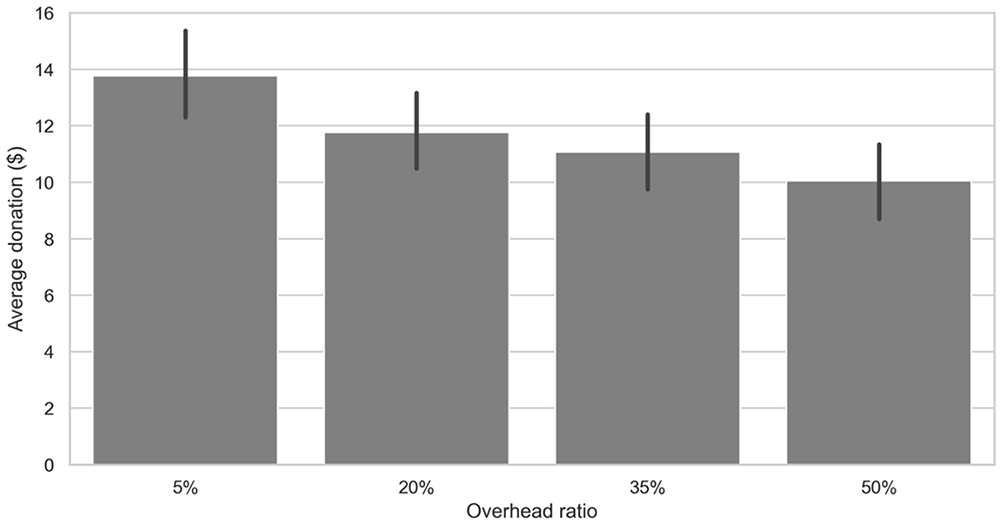

Of the 1,529 participants, 9 (.59%) decided to donate US$100, 349 (22.83%) decided not to donate, and 1,171 (76.59%) decided to donate an amount between US$0 and US$100 (M = 11.67, SD = 16.59). Moreover, participants who were informed about a 5% overhead ratio donated $13.78 (SD = 18.32), those informed about a 20% overhead ratio donated US$11.77 (SD = 15.52), those informed about a 35% overhead ratio donated US$11.08 (SD = 16.24), and those informed about a 50% overhead ratio donated US$10.05 (SD = 15.97) on average. Furthermore, participants who were assigned to the health care group donated US$11.44; those assigned to the human service group donated US$11.90 on average.

Manipulation Checks

To pass our checks, participants’ answers to the two manipulation questions had to match the key information delivered in the vignettes. The vast majority of participants answered the questions correctly, which indicated that most participants absorbed the information relevant for participating in this study (see Table 1).

Results of Manipulation Checks.

Note. N = 1,529 participants.

Randomization Checks

Our randomization produced a balance on various covariates across the four groups (5%, 20%, 35%, and 50% overhead). Specifically, there were no statistically significant differences in participants’ demographic characteristics across the four conditions of overhead ratios (see Table 2). We confirmed that participants were assigned equally to the four groups.

Randomization Check Results.

Note. N = 1,529.

Model Results

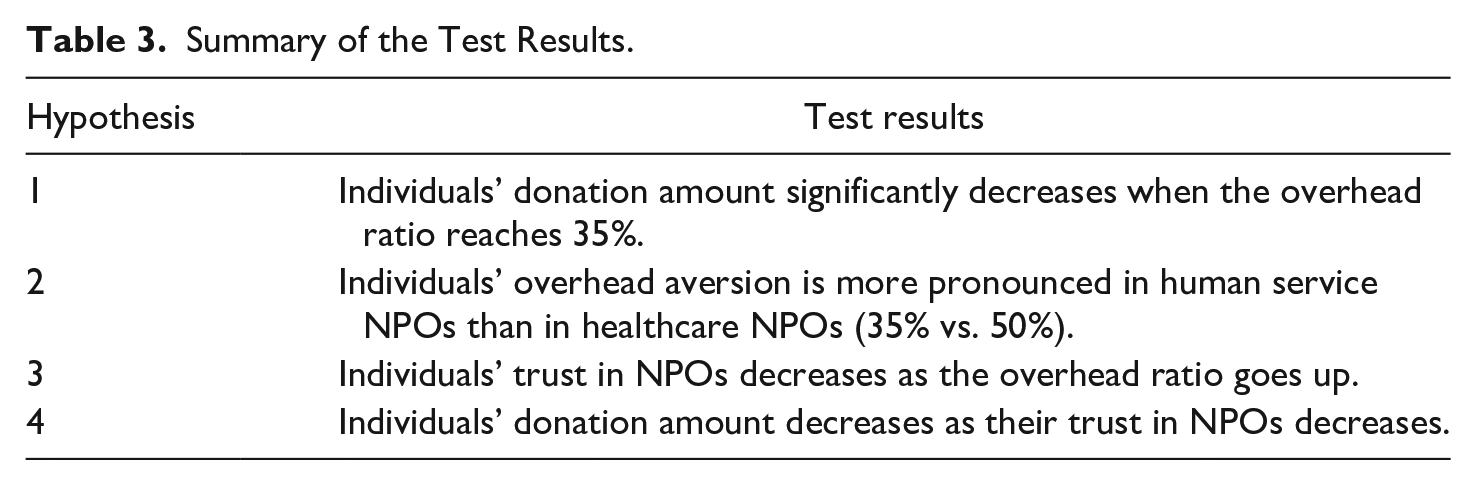

To test H1, we compared the means of the four conditions of overhead ratios by using one-way analysis of variance (ANOVA) to determine whether there was statistically significant evidence that the associated population means were significantly different. The results showed that the donation amount was significantly different for at least one of the four conditions (F = 3.47, p < .02). Our post hoc pairwise comparisons of means showed that the donation amount significantly decreased when the overhead ratio reached 35%. Participants assigned to the 35% condition donated $2.70 less than participants assigned to the 5% condition, b = −2.70, t = −2.25, p < .05. The results suggest that the most effective overhead ratio for maximizing individual donation amounts is below 35%, as the individual donation amount may begin to decline significantly after reaching the 35% overhead threshold. Overall, our results support H1.

To test H2, we conducted subgroup analysis on human service and health care NPOs, respectively. The results from the human service subgroup showed that the donation amount significantly decreased when the overhead ratio reached 35%. Participants assigned to the 35% condition donated US$3.69 less than participants assigned to the 5% condition, b = −3.69, t = −2.13, p < .05. Our results suggest that the decrease in giving becomes statistically significant when the overhead ratio goes beyond 35% for human service NPOs. Moreover, the results from the health care subgroup showed that there was a statistically significant difference between the 5% and 50% conditions. The donation amount may decrease when the overhead ratio reaches 50%. Participants assigned to the 50% condition donated US$3.21 less than participants assigned to the 5% condition, b = −3.21, t = −1.93, p = .05. The results suggest that the decrease in giving becomes statistically significant when the overhead ratio goes beyond 50% for health care NPOs. Overall, our results support H2.

To test H3, we first ran descriptive analysis and then used one-way ANOVA. The results of our descriptive analysis showed that individuals’ trust in NPOs decreased as the overhead ratios went up. The ANOVA results showed that trust is significantly different for at least one of the four conditions of overhead ratios (F = 119.34, p < .001). Our post hoc pairwise comparisons of means showed that participants assigned to the 20% condition are less likely to trust NPOs than participants assigned to the 5% condition, b = −1.38, t = −4.00, p < .001; that participants assigned to the 35% condition are less likely to trust NPOs than participants assigned to the 20% condition, b = −1.98, t = −5.69, p < .001; and that participants assigned to the 50% condition are less likely to trust NPOs than participants assigned to the 35% condition, b = −2.79, t = −8.04, p < .001. The results support H3.

To test H4, we first ran descriptive analysis and then used one-way ANOVA. The descriptive analysis showed that the donation amount decreased as individuals’ trust in NPOs decreased. The ANOVA results showed that trust is significantly different for at least one of the four conditions of overhead ratios (F = 17.16, p < .001). Our post hoc pairwise comparisons of means showed a similar trend. The results support H4. Figure 2 shows individuals’ donations across the four groups. Table 3 summarizes the test results.

Individuals’ Donations Across the Four Groups.

Summary of the Test Results.

To ensure the robustness of our findings, we omitted participants who provided incorrect answers on the manipulation check related to the overhead ratio level. The outcomes of this robustness check have been incorporated into the Online Appendix, demonstrating alignment with the findings obtained from the entire participant pool. Also, we conducted a test on the subset of participants who reported real-life donations, constituting 70.15% (n = 1,073) of the sample (N = 1,529). The results from this subset are mostly consistent with our current findings.

Supplementary Analysis Results

To better understand individual donors’ aversion to NPO overhead, this study asked participants an open-ended question: “Please briefly explain why you did or did not donate to the organization.” Of the 398 participants assigned to the 5% overhead group, 51 mentioned that the organization managed its funds well. For example, participant #1,479 stated: A very high percentage of this organization’s receipts from donors goes to support direct services to program recipients, with only a small percentage for overhead and administrative costs. That is one of my top priorities that I look at when considering organizations to donate my money.

Also, participant #1,363 stated, “I am very impressed with how much money actually goes towards the program and a low overhead, which to me means this is a very trustworthy and important organization to support.”

When the overhead ratio reached 20%, a few participants began criticizing how the NPO managed its funds. Of the 394 participants assigned to the 20% overhead group, 15 expressed concerns about the NPO’s overhead expenses. For instance, participant #320 stated: 20% overhead is a lot in my book. I would prefer to find other opportunities, and I certainly wouldn’t donate to them without a lot more info and a review on some sites that rate charities’ effectiveness and good use of funds.

Moreover, participant #1,189 stated, “They keep too much money for themselves. I don’t trust them.”

The number of participants who expressed concerns about the NPO’s overhead spending jumped to 58, among 397 participants, when the overhead ratio reached 35%. Phrases such as “excessive,” “extreme inefficiency,” and “far too high” started appearing in participants’ statements used to describe the overhead spending. Also, compared with participants assigned to the previous two groups, more participants in this group stated that the NPO cannot be trusted. For example, participant #1,580 stated, “I feel that their overhead is too high, and therefore, I am not convinced they should be trusted. There are many charities which operate just to steal money. I would look for a different organization.” Moreover, participant #599 stated, “The organization seems really untrustworthy. They spend too much on overhead expenses, which gives me the suspicion that they are not using the money for what they say they’re using it for.”

An overhead ratio of 50% was unacceptable to many participants. Of the 403 participants assigned to the 50% overhead group, 124 expressed their concerns about the NPO’s overhead expenses. Strongly worded phrases such as “terrible expense ratio,” “notoriously ineffective,” “extremely bad,” “absurd,” “ridiculously,” and “highly suspicious” appeared in participants’ statements describing the overhead spending. We can feel participants’ frustration by reading their statements: “Their overhead expenses seem astronomical, so I don’t trust that they are working efficiently or putting their donations to good use (participant #1,083),” “I wouldn’t donate to an organization with that high of an overhead cost. That is insane overhead, and they need to re-evaluate their costs vs. benefits (participant #199),” “50% overhead is ridiculous; they are wasting too much money (participant #218),” and “Half of the money donated going to admin costs and overhead seems outrageous to me (participant #411).”

This supplementary analysis provided evidence regarding our Hypothesis 1 test results, which indicated a significant decrease in the donation amount when the overhead ratio reached 35% as at that point there was a big jump in the number of participants who criticized the overhead spending by using words such as “excessive,” “extreme inefficiency,” and “far too high.” The analysis also spoke to our Hypotheses 3 and 4 test results, which indicated that trust played a role in donors’ overhead aversion, as demonstrated by participants’ frequent use of the word “trust” in their statements.

Discussion

This research investigation offers several substantial contributions. As stated in the introductory section, prior studies have employed distinct overhead ratio benchmarks (e.g., see BBB Wise Giving Alliance, 2023; Gneezy et al., 2014; Gregory & Howard, 2009; Portillo & Stinn, 2018; Qu & Daniel, 2021a; Schubert & Boenigk, 2019; Tian et al., 2020). Nevertheless, a critical gap exists in the literature examining donor perceptions concerning an excessively high overhead ratio. By empirically demonstrating that an overhead ratio of 35% is considered high, this study sheds light on individual donors’ relatively lenient attitudes toward NPOs’ administrative and operational expenditures. These findings imply that NPOs have some leeway to allocate donations to bolster their infrastructural capacities. Furthermore, the endorsement of a 35% overhead ratio by the BBB Wise Giving Alliance (2023) adds weight to these conclusions.

Moreover, a notable divergence emerges upon segregating the sample into human service and health care NPOs. Contributors to human service organizations perceive an overhead ratio greater than 35% as high, whereas those supporting health care NPOs consider an overhead ratio greater than 50% as high. This observation signifies that donors contributing to health care-focused NPOs exhibit a heightened tolerance for overhead expenses. This phenomenon aligns with previous scholarly works positing that donors may respond differentially to distinct NPO categories (Allred & Amos, 2022; Caviola et al., 2014; Spiteri, 2022). Specifying the NPO type proves crucial for discerning donors’ reservations concerning overhead expenditures.

Furthermore, while we formulated our second hypothesis around processing fluency and its role in explaining variances among nonprofit subsectors, it is important to consider an alternative explanation. On average, donors display a greater sensitivity toward the financial allocation practices of donative NPOs than toward those of commercial NPOs (Ferris & Graddy, 1999; Hung, 2020, 2021; Yetman & Yetman, 2003). The empirical evidence from this study reveals a discernable difference between human service NPOs, which tend to be donative, and health care NPOs, which tend to be commercial, in terms of their freedom in allocating resources to overhead expenditures. Commercial NPOs enjoy greater flexibility in this regard. In contrast, donative nonprofits face a heightened need for vigilance and accountability in managing their overhead spending, to align with donors’ expectations. To this end, establishing trust emerges as a potential avenue for enhancing the accountability of donative NPOs to their benefactors (Hyndman & McConville, 2018). By fostering and nurturing trustworthy relationships with donors, NPOs can strengthen their accountability and instill confidence in the efficient and effective utilization of funds. This process of building trust can be achieved through various means, such as the use of publicly available communications (i.e., annual reports, annual reviews, and websites) and the use of private mechanisms (i.e., direct reporting, participation, feedback, and observation; Hyndman & McConville, 2018). Cultivating such trust-based mechanisms can reinforce the relationship between donative NPOs and their donors, ultimately bolstering the organization’s sustainability and social impact.

Linking trust to principal−agent theory and risk aversion involves understanding how trust can effectively mitigate the challenges of information asymmetry and donors’ risk-averse behaviors (Hyndman & McConville, 2018). Information asymmetry is a fundamental issue in the principal−agent, or NPO−donor, relationship (Van Slyke, 2005). This relationship commonly assumes that the principal and the agent possess opposing interests. Notably, many donors tend to exhibit risk aversion, particularly concerning overhead (Gneezy et al., 2014; Qu & Daniel, 2021a). Trust plays a pivotal role (Speckbacher, 2013). When donors trust a nonprofit organization, they are more likely to believe that it will act in their best interests and diligently pursue the stated mission. Consequently, trust reduces the perceived information asymmetry, instilling confidence in donors about the organization’s actions and intentions.

To effectively address information asymmetry and alleviate donors’ risk aversion, NPOs must proactively build trust. In addition to the strategies mentioned earlier, employing effective fundraising strategies is essential to assuage donors’ concerns regarding allocating funds within NPOs. Moreover, adopting frequent and transparent communication with donors concerning the NPO’s financial dispositions and operational endeavors can build trust significantly. Online and offline transparency initiatives should be adopted to offer donors clear insights into the organization’s financial management practices. In addition, elucidating the rationale behind overhead spending is essential to foster donors’ understanding of its necessity for the functioning and sustainability of the NPO.

The prioritization of trust-building efforts by NPOs holds the potential to foster strong donor relationships and disrupt the perpetuation of the nonprofit starvation cycle. This cycle embodies the phenomenon wherein donors maintain unrealistic expectations concerning overhead spending by NPOs, as documented by Gregory and Howard (2009). Consequently, the pressure to minimize overhead expenditures may lead NPOs to neglect essential infrastructure or misreport their financial data, reinforcing donors’ unrealistic expectations and giving rise to a self-perpetuating cycle of underinvestment and inadequate resource allocation. Resolution of the nonprofit starvation cycle necessitates a collective effort beyond the purview of NPOs alone, as posited by Berrett (2022). Indeed, it is incumbent upon NPOs, donors, watchdog organizations, and regulatory agencies to share responsibility in this endeavor (Berrett, 2022).

While providing valuable insights, this study possesses several limitations that necessitate attention and offer avenues for future research. First, a noteworthy limitation of this study is its focus solely on human service and health care subsectors within the NPO landscape. Although the findings confirmed the variations of overhead tolerance by nonprofit subsectors, it leaves other subsectors as uncharted territory. We could speculate that nonprofits similar to those in the human service or health care sectors might have comparable thresholds for overhead aversion. However, expanding future research to include a broader range of NPOs would offer a more comprehensive and confirmative understanding of donor attitudes toward overhead costs. Second, the study’s insights, while intriguing, may not be generalized to all donors and giving contexts because of the demographics of the respondents (Table 4) and research design. In particular, the age of our sample participants tends to be slightly younger than that of the overall population in the United States. As there is a lack of research exploring how these demographic characteristics may influence people’s aversion to overheads, it becomes challenging to ascertain whether and how this unrepresentative sample impacts our results. To further validate and potentially extend these findings, future studies with more representative respondents would be beneficial. Third, scholars have also discovered that the impact of overhead aversion can be mitigated by presenting additional tangible information about the use of donations (Qu & Daniel, 2021b). In our research design, we provided specific details about a nonprofit’s activities, beneficiaries, and performance. However, this information remained consistent across all our experimental conditions. Future research could investigate how variations in such information, combined with overhead aversion, influence people’s giving behaviors. Fourth, a survey experiment presents potential limitations, including issues like social desirability bias, which might have influenced participants’ responses. For instance, it is plausible that our experiment participants might tend to mask their true opinions. They may overstate their preference for a low-overhead nonprofit and exaggerate their aversion toward a high-overhead nonprofit to gain our approval. If this is the case, it could amplify the significance of the differences observed among the four groups. Further studies could explore alternative methods or controls to minimize such biases. Fifth, the current study identifies a relationship between overhead ratio and giving intention, but it does not measure actual giving behavior. Future research could connect this intention-behavior gap by investigating how overhead ratios influence real-world giving, thereby painting a more accurate picture of the phenomenon. Sixth, the findings from this study merely reflect the differences in individual donations among distinct experimental groups (5%, 20%, 35%, and 50%). In reality, individual donations to nonprofits may drop before a nonprofit’s overhead ratio reaches 35%. In other words, 35% might not be the exact threshold point. Future studies can measure the overhead level continuously to examine the exact thresholds. Finally, the distinction between different types of donors and nonprofits is unaddressed in the current study. The nature of giving might differ substantially between individual donors and institutions such as foundations, governments, or corporations. The donors’ tolerance to overhead may vary if they are also beneficiaries. Nonprofits working in different areas may also lead to different levels of overhead tolerance. For example, the tolerance to arts and culture organizations’ overhead may be higher than that of human service organizations because it is easier to imagine what overhead contributes to (Allred & Amos, 2022). Future studies exploring these varying donor and organization types could yield more comprehensive insights into how overhead costs shape different aspects of the giving landscape. These limitations provide fertile ground for further exploration and addressing them could deepen our understanding of the complex dynamics that govern donor behavior concerning NPO overhead costs.

Demographic Characteristics: Participants in this Study Versus U.S. General Population.

Source. Data collected by this study, the 2022 U.S. Census Bureau, and Statista.

In addition to addressing the limitations, future research could explore additional directions. First, researchers could investigate additional factors influencing donor perceptions of overhead ratios and identify alternative thresholds for different nonprofit types. Second, they could track changes in donor perceptions of overhead ratios over time to understand evolving factors shaping attitudes toward nonprofit overhead. Third, they could conduct cross-country comparisons to examine cultural differences in donor perceptions of nonprofit overhead. Fourth, they could employ qualitative methods to uncover nuanced factors influencing donor perceptions of nonprofit overhead. Finally, they could evaluate the effectiveness of trust-building strategies in enhancing donor confidence and trust in nonprofits.

Conclusion

For a long time, it has been widely believed that donors dislike NPOs with a high overhead. This study looks at donors’ overhead aversion and concludes that individual donors on average can tolerate overhead ratios up to 35%. We also conclude that their tolerance is higher with health care organizations (up to 50%). These findings suggest that individual donors are not as strict with how NPOs use money as previous studies suggest. Individual donors actually allow NPOs the freedom to spend on overheads to build the necessary infrastructure for operations. Most importantly, we emphasize the importance of trust-building between NPOs and individual donors to alleviate information asymmetry and break nonprofit starvation cycles.

Supplemental Material

sj-docx-1-nvs-10.1177_08997640241254079 – Supplemental material for How High Is Too High? An Experimental Analysis of Donors’ Aversion to Nonprofit Overhead

Supplemental material, sj-docx-1-nvs-10.1177_08997640241254079 for How High Is Too High? An Experimental Analysis of Donors’ Aversion to Nonprofit Overhead by ChiaKo Hung, Jessica L. Berrett and Ji Ma in Nonprofit and Voluntary Sector Quarterly

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is financially supported by the Department of Public Administration, College of Social Sciences, at the University of Hawaiʻi at Mānoa.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.