Abstract

Even the most conscientious nonprofit organizations can fall victim to fraud. We examine how a nonprofit organization’s Form 990 disclosures and media coverage about an asset diversion influence subsequent donor support. Consistent with a loss in trust, we observe a decrease in donations following a diversion. This decrease is amplified when the diversion is reported in the news. We also find that donations decline more when organizations do not provide transparent disclosures and when losses are higher but only if the diversion receives media coverage. Finally, our results indicate that donors punish organizations less when they report higher recoveries and governance improvements. This study describes mechanisms though which news coverage enhances donor oversight. The media can: (a) directly inform some donors, (b) prompt some donors to obtain further information, and (c) motivate organizations to provide higher-quality disclosure.

Keywords

Introduction

The nonprofit sector in the United States received $485 billion from donors in 2021 (Giving USA, 2022). Prior research suggests that these donors provide more support to nonprofit organizations that are prudent stewards of charitable assets and effectively use donations to further their missions (e.g., Harris et al., 2015; Kitching, 2009; Petrovits et al., 2011; Tinkelman & Mankaney, 2007). Even the most conscientious organizations, however, are vulnerable to stewardship failures and loss from fraud. Fraud is costly, not only because it shifts resources away from the charitable mission but also because it can cause reputational damage and diminish public trust (Bryce, 2007; Chapman et al., 2022). The purpose of this study is to better understand how donors respond to information surrounding incidents of fraud.

Specifically, we examine asset diversions, which are the prevailing type of fraud in the nonprofit sector. 1 The Internal Revenue Service (IRS) defines a diversion as “any unauthorized conversion or use of the organization’s assets other than for the organization’s authorized purposes, including, but not limited to, embezzlement or theft.” Common examples of diversions include theft of cash or inventory, check forgery, false expense reimbursement, and embezzlement by investment advisors. Unlike high-profile scandals involving sexual harassment or conflicts of interest, diversions often do not involve organization-wide corruption, (Lamothe et al., 2023). Diversions, however, occur more frequently than organization-wide corruption (Lamothe et al., 2023). Thus, it is worthwhile to understand the effects of this type of misconduct.

While nonprofit organizations may prefer to handle diversions outside of the public eye, the IRS does not allow them to conceal diversions from external scrutiny. Organizations must indicate on their publicly available IRS Forms 990 if they became aware of a significant asset diversion during the year, as well as provide pertinent details on Schedule O. The IRS provides instructions on what details should be disclosed, but, in practice, the amount and type of information reported varies considerably. Some organizations are not transparent and leave Schedule O blank. Others provide detailed information, including the method of diversion, perpetrator, financial impact, amount recovered via insurance or restitution, and subsequent corrective actions. We investigate whether donors consider transparency, as well as loss amounts and governance improvements reported on the Form 990, when making donation decisions following an asset diversion.

We also study the role of the media in donor decisions. Some (but not all) asset diversions are reported in the press. Media coverage can result in more donors becoming aware of a diversion and underscore that the diversion is relevant. News stories may also prompt donors to seek more information about the organization. Donors, who would not otherwise do so, may read the Form 990 after learning of a diversion from the media to understand management’s assessment of the diversion’s impact and to evaluate the appropriateness of the organization’s response.

Consistent with the effects of reputational damage, we find that donations decrease 5.4% on average following a diversion for a sample of 928 nonprofit organizations. While just under one-third of diversions receive media coverage, the decrease in donations is more pronounced for these diversions. This result is not due to the media only reporting the most egregious frauds as we observe the same effect of media coverage after removing large diversions from our analysis.

We also find that organizations with diversions in the news are significantly more likely to provide transparent disclosures on their Forms 990. Donors appear to reward Form 990 transparency, but only when the diversion receives media attention. Furthermore, subsequent donations are lower when fraud losses are higher but only when the diversion receives news coverage. Finally, subsequent donations are higher when organizations report higher recoveries and governance improvements. Overall, both the 990 and the media play a role in apprising donors about a fraud.

This study contributes to current research and practice along four dimensions. First, Hale (2007) notes that there is little research on the role of the press in the nonprofit sector. We provide evidence that media coverage can inform external constituents about the fraud, direct attention to the Form 990, and provoke organizations to provide better disclosure. Second, our results speak to the decision-relevance of information reported on the Form 990. Organizations not in the news also experience a decline in donations, suggesting donors respond to disclosure of a fraud directly from the Form 990 or indirectly from Form 990 information providers, such as charity watchdogs. Third, we shed light on oversight of the nonprofit sector. Anecdotal evidence indicates that the IRS lacks resources to effectively oversee the tax-exempt sector (Government Accountability Office [GAO], 2014; Lee, 2019; O’Harrow, 2017). Using a sample of frauds reported in the press, Archambeault et al. (2015) note that 10% of organizations did not properly report the diversion on the Form 990, which reinforces the anecdotal evidence of ineffective oversight. They recommend further study of disclosure compliance using a comprehensive sample selected from a Form 990 database; our study answers this call. Finally, organizations that depend on support from grantors and donors rely largely on their reputations (Bryce, 2007; Jaeggi, 2014; Tremblay-Boire & Prakash, 2015). Our study suggests actions that boards and managers can take to reduce reputational risks associated with diversions, such as implementing controls to limit loss amounts, transparent disclosures, and improved governance.

Background and Hypothesis Development

Asset Diversions in the Nonprofit Sector

Nonprofit organizations are established and awarded tax-exempt status to fulfill a charitable mission. Donors provide more capital to organizations that they expect will protect and use their contributions to achieve that mission (e.g., Harris et al., 2015; Kitching, 2009; Petrovits et al., 2011; Tinkelman & Mankaney, 2007). Thus, maintaining a favorable reputation or “public trust” is crucial for any nonprofit that relies on donations (Bryce, 2007; Jaeggi, 2014).

Asset diversions redirect resources from their intended purpose. As the assets were not used appropriately, the IRS requires nonprofit organizations to disclose significant diversions. According to the Form 990 instructions, management should explain on Schedule O the nature of the diversion, the amounts involved, corrective actions taken, and any other pertinent facts. This disclosure is intended to give donors and other stakeholders an understanding of the financial impact and circumstances surrounding the diversion, as well as the organization’s response. Donors may read the Form 990 directly or they may obtain its information indirectly from an intermediary (Gordon et al., 2009; Sloan, 2009). For example, Charity Navigator (2023) considers whether an organization has experienced a diversion and the explanation around any diversion in its ratings methodology.

Donors can also learn about an asset diversion from the media. Miller (2006) notes that the media can provide original information based on investigation or may rebroadcast information from other sources (e.g., police reports, court filings, press releases, Forms 990). Furthermore, media coverage of a diversion may spur some donors to focus more attention on what management reports in the Form 990.

Most research to date documents determinants of diversions, including characteristics of the perpetrators and victim nonprofit organizations (e.g., Archambeault et al., 2015; Eining et al., 2020; Gibelman & Gelman, 2001; Greenlee et al., 2007; Harris et al., 2017; Holtfreter, 2008; Lamothe et al., 2023). There is limited research on the economic consequences of diversions. Archambeault and Webber (2018) find that 29 organizations in their sample of 115 nonprofits experiencing a fraud that received media coverage did not survive at least 3 years beyond the fraud, with younger and smaller organizations more likely to fail. Using macroeconomic data from 1974 to 2015, LeClair (2019) reports mixed results when examining whether major scandals at one organization suppress donations to the entire nonprofit sector. Both studies focus solely on cases of fraud in the news.

We extend the line of research on consequences along multiple avenues. We first examine how donors respond to a broader sample of asset diversions and then investigate how media coverage influences donor response. We also explore whether organizations rebuild trust with donors following a diversion through Schedule O disclosure choices.

Hypothesis Development

Stewardship Hypothesis

An asset diversion signals that the nonprofit organization did not effectively steward its resources and can lower donors’ expectations that future funding will be safeguarded. This loss of reputational capital can damage the organization’s ability to raise funds in the future (Dupont & Karpoff, 2020). Consistent with donors’ preference to support organizations that they perceive are good stewards of their funds, we hypothesize:

A range of donors exist from disengaged, small-dollar individual contributors to the highly engaged, well-funded private foundations. We are not positing that all donors respond to asset diversions. Instead, we conjecture that there are some donors sophisticated and motivated enough to process diversion information and reduce their contributions, on average. This conjecture is supported by anecdotal evidence that institutional and wealthy donors consider an organization’s ability to properly safeguard and effectively use charitable assets (Conkley, 2006; Foster & Ditkoff, 2011; Hedge et al., 2009). 2 Whether donors of any type respond to asset diversions is an empirical question. Donors can be extremely loyal (Preston, 2010). Giving will not be affected if donors (a) do not observe diversion information, (b) opt to “rescue” their preferred organizations by increasing funding to make up for losses, or (c) do not believe the diversion harms the organization’s ability to operate going forward.

Next, we hypothesize how circumstances surrounding the diversion influence the magnitude of donor response, under the maintained assumption that some donors do indeed care about their funds being effectively stewarded (i.e., that hypothesis 1 holds true).

Attention Hypothesis

The media plays a role in shaping public perception as a third-party that credibly disseminates information about an organization’s performance and impact (Carroll & McCombs, 2003; Hale, 2007). Media coverage of an issue can result in more donors becoming aware of the issue and believing the issue is relevant. Most research examining the influence of the press on charitable giving focuses on natural disasters and finds that donations increase around media coverage of these events (e.g., Brown & Minty, 2008; Martin, 2013; Waters & Tindall, 2011). Two studies report that bad press alters donor perceptions. Balsam and Harris (2014) document that donors reduce support to nonprofit organizations that receive media coverage about their executive compensation. Jones et al. (2019) find that survey respondents are more skeptical about the charitable sector after prominent news stories about fundraising costs at “America’s Worst Charities.” We extend this research to investigate the role of the media in increasing donor attention to fraud and hypothesize:

Hypothesis 2 is based on the notion that media coverage itself provides more donors with information that an asset diversion has occurred and is newsworthy. We posit that the media not only provides information but also can prompt individuals to seek additional information. Survey results suggest that a media story can motivate some donors to research an organization when they otherwise would not (Hope Consulting 2011). We are not aware of any prior nonprofit academic studies that document a link between news coverage and further information seeking but this phenomenon has been reported in health care research (e.g., Metcalfe et al., 2011; Niederdeppe et al., 2008). News of an asset diversion may spur some donors (who normally do not read the Form 990) to obtain detailed information about the organization and the diversion from the Form 990 because the 990 includes management’s assessment of the impact and the organization’s response to the fraud. If so, we expect that media coverage moderates the association between diversion information on the Form 990 and subsequent donations by focusing more donor attention on the Form 990. We discuss this diversion information in more detail below.

Transparency Hypothesis

Nonprofit organizations can voluntarily disclose information in a variety of ways, such as through the distribution of audited financial statements, website messaging, third-party intermediaries, and Form 990 Schedule O details. Research indicates that transparency is associated with greater reliance on donations, lower debt, and better governance (Behn et al., 2010; Harris & Neely, 2021; Saxton et al., 2012). Furthermore, Tremblay-Boire and Prakash (2015) report that nonprofits receiving more media coverage disclose more, consistent with pressure from external constituencies to provide more information.

With respect to asset diversions, IRS instructions require nonprofit organizations to provide specific information in Schedule O. Nevertheless, in practice, the level of detail varies across organizations. Some do not comply with the disclosure requirement, whereas others provide extensive information about the size of loss, root cause of problem, and subsequent remediation.

Reporting that a diversion occurred without providing details about the circumstances results in asymmetric information between the organization and its donors, which can cause donors to assume the worst and reduce support (Milgrom, 1981). Lack of information may also signal that management is not taking the situation seriously. Pfarrer et al. (2008) argue that organizations that discover facts surrounding a transgression and provide an appropriate explanation have a higher likelihood of maintaining legitimacy with stakeholders. In an experimental setting, Chapman et al. (2022) find that trust can be partially repaired after a scandal by acknowledging the violation. Based on this discussion, we hypothesize:

The influence of transparency on donors’ response to asset diversions remains an open question. To date, research offers mixed evidence on donor response to voluntary disclosure. Saxton et al. (2014) report a positive relationship between voluntary web disclosures and donations, which is consistent with donors valuing transparency. Likewise, Harris and Neely (2021) find that GuideStar transparency levels are positively associated with donations. These studies, however, do not examine negative information. In contrast, in an experimental setting, Willems and Faulk (2019) find no evidence that voluntary disclosure mitigates negative donor response following a hypothetical scandal. Also, in an experimental setting, Ling et al. (2020) report that, when fraud is suspected, some donors who are passionate about the organization’s mission will bear costs to obtain information, while other donors will donate elsewhere.

The Form 990 contains 12 pages of complex information and up to 16 attached schedules with detailed disclosures. If donors do not read the Form 990 (or do not rely on information intermediaries who do), they will not respond to an organization’s choice to be transparent. Media coverage of the diversion may cause donors to seek more information in the Form 990. Thus, the attention hypothesis suggests any association between Schedule O disclosure and subsequent donations is stronger for organizations that have diversions covered by the media.

Content Hypothesis

The previous hypothesis predicts that donors value transparency, namely the existence of any qualitative information in Schedule O. For organizations that provide Schedule O, we next consider whether donors use the pertinent details contained therein, specifically about the magnitude of the loss. In terms of Schedule O content, we focus on the amount of the loss for two reasons. First, theoretical predictions about how donors might respond to other content (e.g., mode of diversion) are less clear. Second, disclosure of other content is less standardized than dollar amounts, making it difficult to operationalize in empirical tests.

Larger frauds relative to the organization’s budget likely result in fewer resources available to fulfill their mission. Furthermore, larger frauds are presumably difficult to commit and can signal more systemic problems. Grover et al. (2019) note that the severity of a trust violation, in terms of the magnitude of harm, influences the ability to repair trust, which suggests that organizations with larger losses face more difficulty regaining donor confidence. Thus, we hypothesize:

Some organizations also mention that a recovery of funds occurred, most often via restitution or insurance proceeds. Because recoveries reduce the net amount of the loss and because recoveries can signal stronger controls in place, we hypothesize:

The narrative information contained in Schedule O is not standardized and requires more effort to interpret. Little research exists on how donors use narrative information. In an experimental setting, Buchheit and Parsons (2006) examine the effect of including information about mission effectiveness in a fundraising appeal and find that, although donors view organizations that include this information more favorably, they do not actually give more. Thus, it is an open question if donors process this detailed content. Again, media coverage may point donors to Schedule O and, if so, we expect any association between fraud amounts and donations to be stronger when the diversion is covered by the press.

Sample

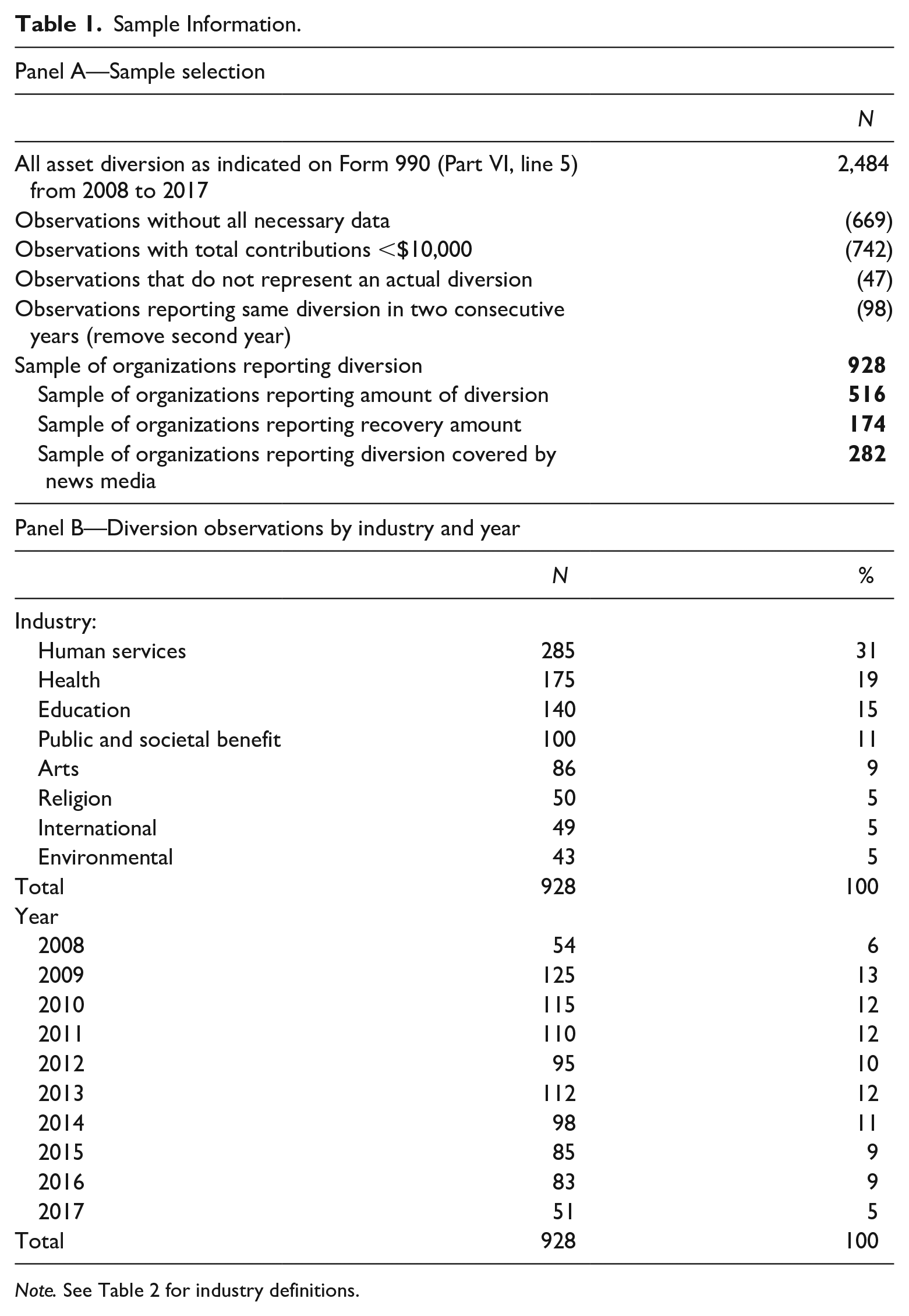

Table 1 outlines our sample selection process. We use the Form 990 filings of all organizations exempt under IRC 501(c)(3) available in the Candid GuideStar database. We first identify organizations in the United States that report an asset diversion between 2008 and 2017. Our sample period begins in 2008 because that was the year when the IRS first required nonprofits to report diversions. Our sample ends in 2017 because that was the latest year with all necessary data available at the time of collection (given our need for subsequent donations and IRS processing delays of Form 990 data). During our sample period, there are 2,484 Form 990 filings where Part VI, Question 5 of the Form 990 indicates that the organization became aware of a material diversion of its assets during the year.

Sample Information.

Note. See Table 2 for industry definitions.

Next, we obtain Form 990 data for each observation from GuideStar or, if the data are unavailable from GuideStar, we hand collect the data from the actual 990s available on the ProPublica Nonprofit Explorer database. We eliminate 669 observations that lack the necessary financial data for our main model. Given our focus on donor decisions, we also exclude 742 observations that report contributions less than $10,000 in the year before the fraud because donations are not a material source of funding for these organizations.

For each organization in our sample, we collect information contained in the asset diversion disclosure in Schedule O if the organization completed Schedule O. We remove 47 observations whose disclosures suggest that an asset diversion did not actually occur. 3 If an organization discloses the same asset diversion in two consecutive years, we only retain the first year of disclosure which removes 98 observations. This process results in a sample of 928 charity-year observations for our main sample. Our sample size decreases to 516 (174) observations for tests on the amount (recovery) of the asset diversion because not all organizations report this information.

We then determine if the media covered each diversion by searching both Factiva and Google News Archive to ascertain whether there was at least one news story describing the fraud at any point in time. Based on this search, 282 diversions in our sample received media attention. We note that these news stories generally originate from police reports, court documents, and (much less frequently) press releases from the organization itself.

For some tests, we use a matched control sample of organizations that did not disclose an asset diversion. Specifically, we identify a match for each observation in our diversion sample based on year, industry, and closest size (measured by total expenses in the year prior to the fraud) from all organizations in the IRS Statistics of Income Charity file with the necessary data available. This process results in a matched sample of 928 charity-year observations that did not report a fraud. Panel B of Table 1 provides the frequency of organizations in our sample by industry and year.

Methodology and Empirical Analysis

Contributions Model Specification

To examine how donors respond to disclosure of an asset diversion, we begin with the donor demand model initially developed by Weisbrod and Dominguez (1986). This model has been refined over time and is used extensively in economics and business research. See Khumawala and Shroff (2023) for a review of this literature. Our base model is as follows:

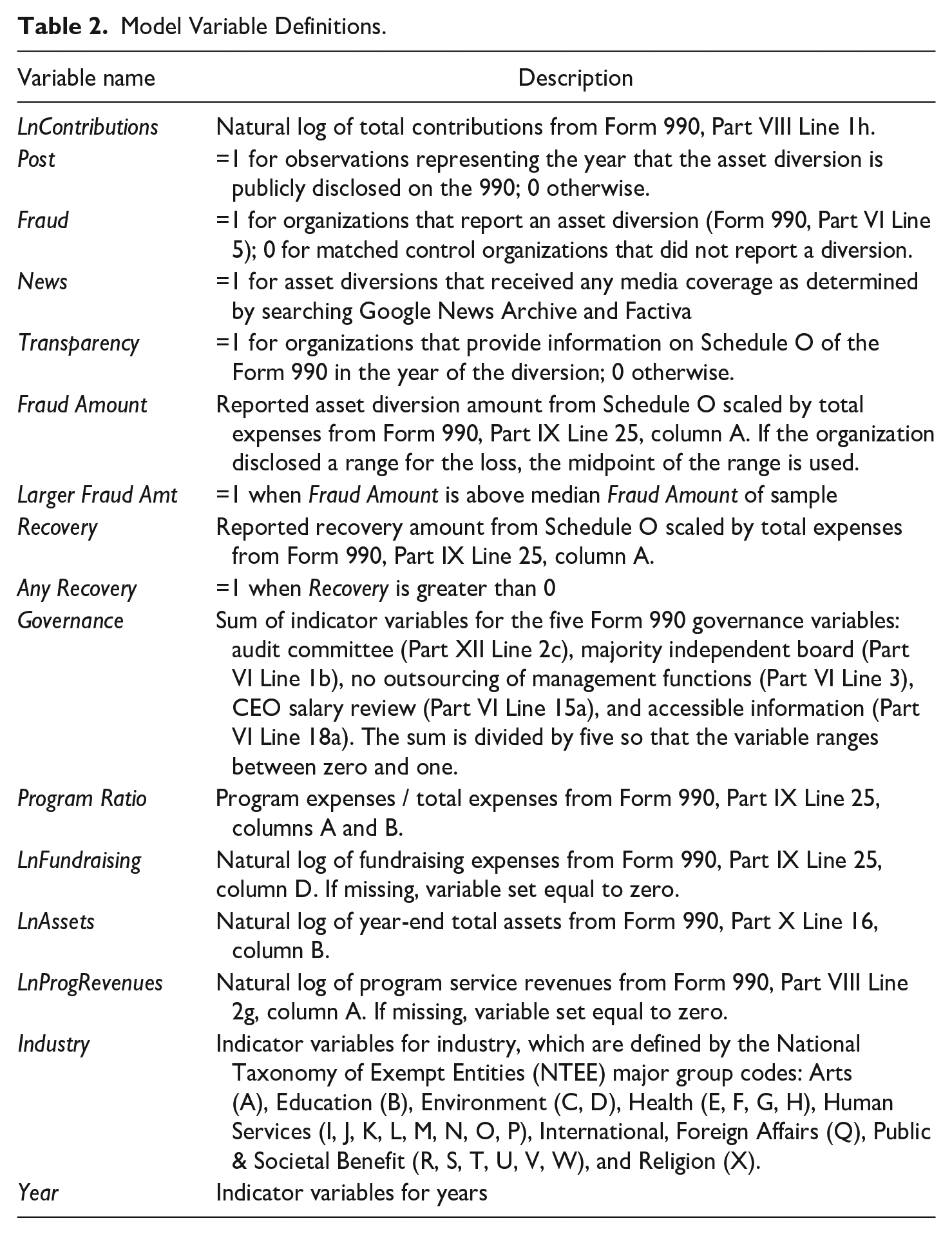

where i is the organization and t is the year. The dependent variable, Contributions, includes donations from individuals, corporations, and foundations, as well as government grants and support from federated campaigns. Consistent with prior literature, we examine the effect of information on subsequent contributions to ensure that the information reported on the Form 990 is available to donors in the period of the contributions. Time t represents the year in which the organization detects the asset diversion. Time t + 1 represents the year in which the Form 990 disclosing the diversion is filed and, as such, the year in which information about the diversion is publicly available. 4

The model includes the standard control variables. Program Ratio serves as a proxy for the efficiency with which an organization supports its mission. If donors care about program efficiency, it is expected to be positively associated with donations. Fundraising is the reported dollar amount of fundraising expenses and is expected to be positively associated with donations because the intent of fundraising is to raise donations. Assets controls for size effects. ProgramRevenues controls for program service revenues, an additional source of revenue for organizations, which can result in crowding-out or crowding-in effects on contributions. Lagged Contributions control for unobservable, time-invariant organizational characteristics that may influence donations (e.g., donor base, managerial talent, board networking effects). 5 All variables are defined in Table 2.

Model Variable Definitions.

To examine how donors respond to asset diversion information, we expand this base model to include the relevant variable(s) of interest. We describe the expanded models for each hypothesis in more detail in the multivariate analysis section below. We estimate our models using robust regression techniques (iteratively reweighted least squares), which addresses influential observations by assigning a weight to each observation with higher weights given to observations that meet the assumptions underlying standard multiple regression.

Descriptive Statistics

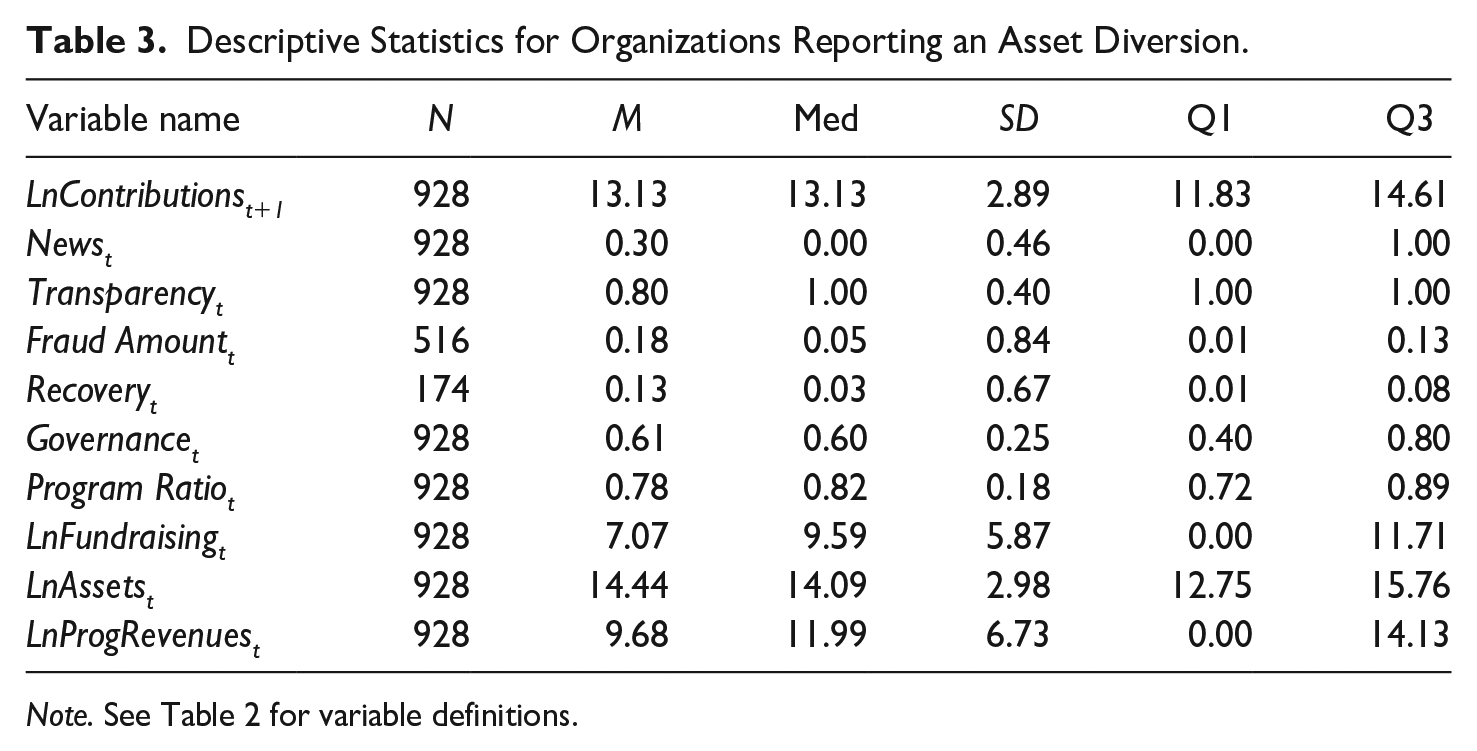

Table 3 provides descriptive statistics for the sample of diversions. News is an indicator variable set equal to one if the diversion was covered by the media. Notably, only 30% of diversions receive media coverage. Untabulated additional analysis reveals that news stories are more often published before the Form 990 reporting the diversion is filed; for the subsample of diversions in the news, media coverage occurred before the 990 was filed in 70% of the cases, suggesting that the 990 can supplement news stories with more recent information in some cases.

Descriptive Statistics for Organizations Reporting an Asset Diversion.

Note. See Table 2 for variable definitions.

Transparency is an indicator variable set to 1 for organizations that include any content in Schedule O and 0 for those that leave Schedule O blank. Eighty percent of organizations provide Schedule O information. This means that 20% do not properly follow IRS instructions. Notably, there were 70 nontransparent organizations in our sample that checked the asset diversion box in two consecutive years. Only 2 of these 70 organizations completed the Schedule O in the second year. In other words, preliminary evidence indicates that many organizations engage in serial noncompliance.

Untabulated results also indicate 89% of organizations in the news are transparent while only 76% not in the news are transparent. This difference is statistically significant. Delving even deeper, organizations with frauds in the news before the Form 990 is filed are significantly more likely to be transparent that than organizations in the news after the Form 990 is filed (92% vs. 84%, respectively). This evidence is consistent with prior findings the media can positively influence nonprofit disclosures (Tremblay-Boire & Prakash, 2015).

Fraud Amount equals the amount of the asset diversion reported on Schedule O scaled by total expenses. Fraud Amount is a continuous measure of the loss relative to the size of the organization’s budget and reflects the potential impact on the organization’s operations. The average fraud loss for the 516 observations that report a diversion amount is 18% of total expenses. This number is skewed by some larger frauds; the median Fraud Amount is 5% of total expenses. Recovery equals the amount of diversion that the organization recovered (or expected to recover) according to Schedule O scaled by total expenses. For the 174 observations that report a recovery amount, the recovery is 13% of total expenses on average. The median Recovery for these organizations is 3%.

Univariate Analysis

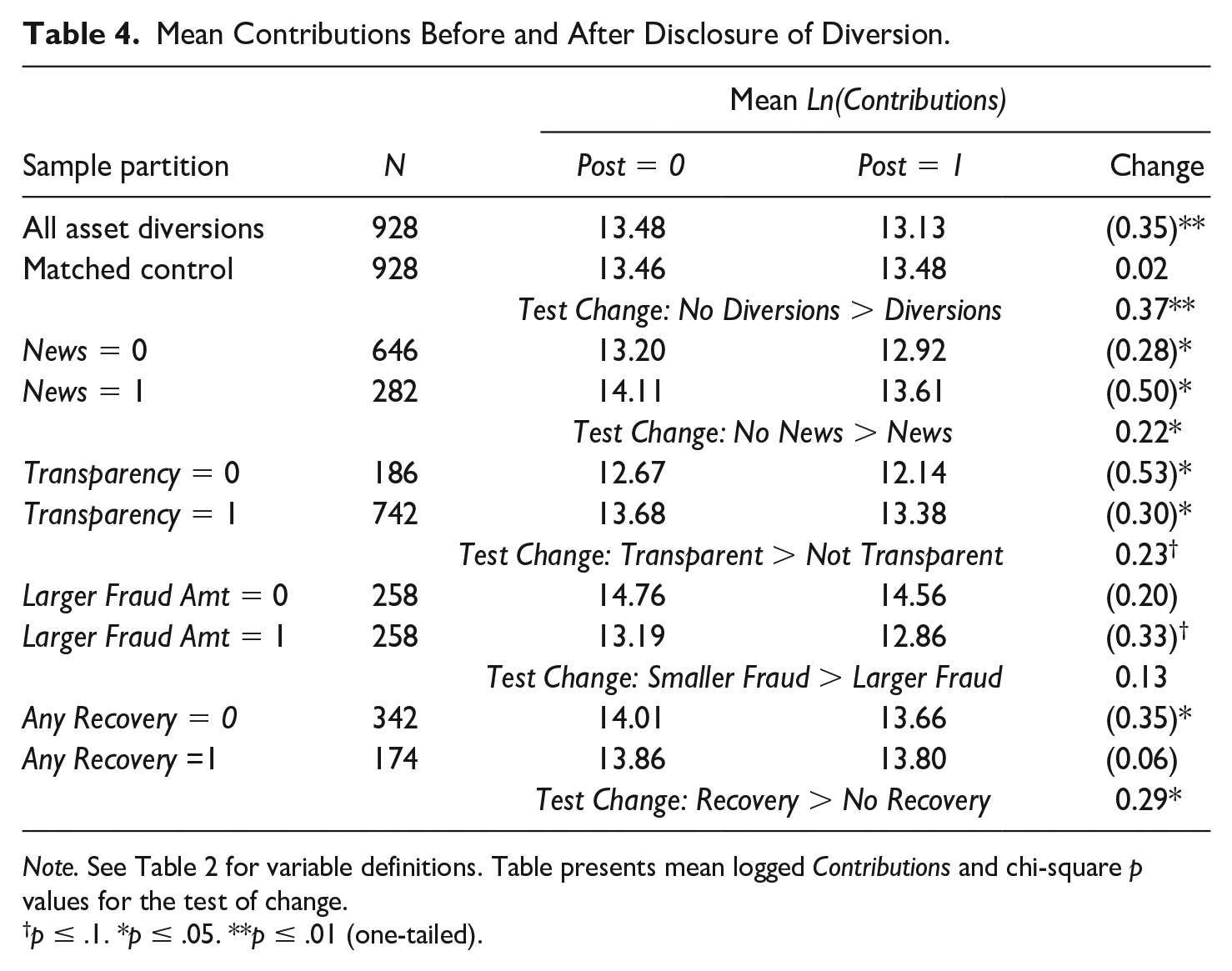

Table 4 provides descriptive evidence that speaks to each hypothesis by examining the change in donations from the year the diversion occurs (Post = 0) to the year the diversion is disclosed (Post = 1). For the sample of diversions, the mean natural log of total contributions fell from 13.48 to 13.13 (i.e., from $715,000 to $504,000 in real terms). The decrease of 0.35 represents a statistically significant decline. Next, we examine the change in contributions for the control sample that did not disclose a diversion. The matched control sample did not experience a decrease in contributions (13.46 vs. 13.48). Moreover, the change in contributions experienced by the asset diversion sample is significantly lower than the change in contributions experienced by the control sample. Overall, this preliminary evidence supports the stewardship hypothesis.

Mean Contributions Before and After Disclosure of Diversion.

Note. See Table 2 for variable definitions. Table presents mean logged Contributions and chi-square p values for the test of change.

p ≤ .1. *p ≤ .05. **p ≤ .01 (one-tailed).

With respect to media coverage, organizations with diversions covered by the news and organizations with diversions not covered by the news both report declines in donor support. However, the ones in the news (where the decrease is 0.50) experience a greater drop in donations than the ones not in the news (where the decrease on 0.28), consistent with the attention hypothesis. Likewise, with respect to transparency, there is a decrease is donations for both organizations that are transparent (decrease is 0.30) and not transparent (decrease is 0.53). However, the decrease for the non-transparent organizations is greater than the transparent organizations, providing support for the transparency hypothesis.

We next partition the sample of 516 organizations that report a fraud amount by the magnitude of the loss. Organizations where Fraud Amount is above the median are considered larger frauds (Larger Fraud Amt = 1). Inconsistent with hypothesis 4A, the decrease in donations is not significantly greater for larger fraud amounts. The lack of significance may be due to the artificial partition of the continuous variable Fraud Amount, which will be addressed in our multivariate analysis. Among these 516 organizations, we do observe that nonprofits reporting a recovery amount (Any Recovery = 1) experience a significantly less severe drop in donations than the ones who do not, consistent with hypothesis

Multivariate Analysis

Stewardship Hypothesis Tests

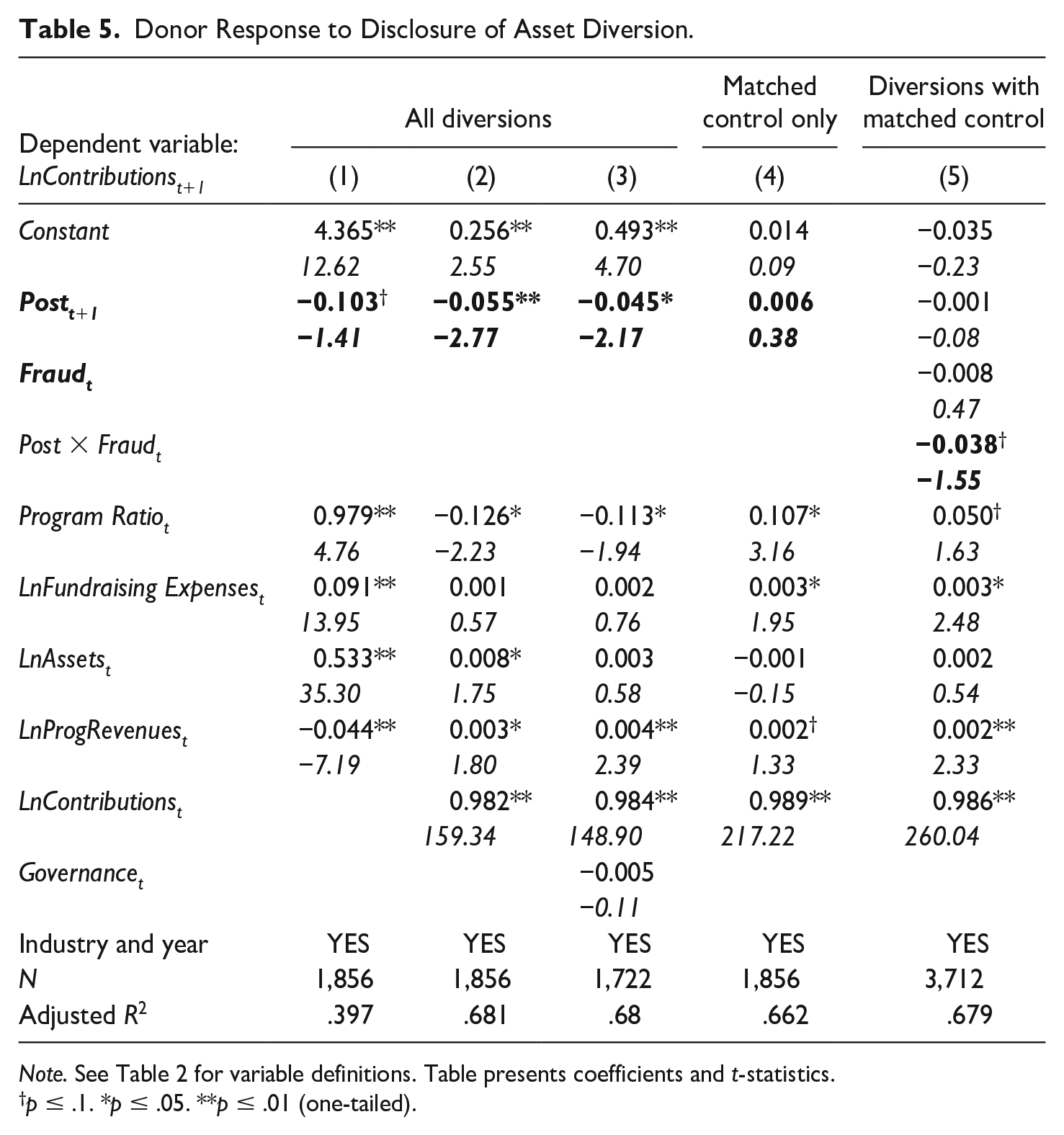

To determine whether donors penalize organizations that report a diversion, we examine contributions received in the year before the fraud is disclosed compared to the year the fraud is publicly disclosed. Thus, we include two observations per organization, resulting in 1,856 observations. We estimate equation (1) and include Post, which is an indicator variable set to 1 if the observation represents the year when information about the diversion is publicly available via the Form 990. We predict the coefficient on Post is negative, consistent with donors reducing contributions to organizations once they learn of a diversion.

Table 5 provides the results for the stewardship hypothesis. In the first column, contributions decline in the year in which an organization discloses an asset diversion as indicated by the negative coefficient on Post. The coefficients on the control variables are all in line with expectations. In the second column, results are robust to the inclusion of lagged contributions, which controls for omitted organizational characteristics. Because we control for lagged contributions, coefficients on some control variables become insignificant or flip signs; this is not surprising as lagged donations control for these effects. In terms of economic magnitude, our evidence indicates there is a 5.4% decrease in contributions, on average, in the year in which an asset diversion is reported (i.e., 100*[exp (−0.055) – 1]).

Donor Response to Disclosure of Asset Diversion.

Note. See Table 2 for variable definitions. Table presents coefficients and t-statistics.

p ≤ .1. *p ≤ .05. **p ≤ .01 (one-tailed).

We address the possibility that governance is an omitted correlated variable because governance is associated with both donations (Harris et al., 2015) and the likelihood of fraud (Harris et al., 2017). Following Boland et al. (2020), we measure Governance using an index comprised of five governance policies that are highly associated with donations: audit committee, majority independent board, no outsourcing of management functions, CEO salary review, and accessible information. 6 As seen in column (3), the number of observations for this test drops to 1,722 because we do not have Governance at t – 1 for every observation. Even when controlling for Governance, the coefficient on Post remains significantly negative. The coefficient on Governance is not significant, which results from the inclusion of lagged contributions in the model. In subsequent tables that do not require t – 1 observations, we include Governance as a control because Governance may also be associated with circumstances surrounding the fraud (i.e., transparency, amount of loss).

The decrease in donations observed in columns (1)–(3) may be driven by macroeconomic factors and not the fraud. Many organizations, regardless of reporting a diversion, experienced a decline in donations due to the recession in the early part of our sample. If macroeconomic factors drive our results, we expect to see similar declines for organizations that did not experience a diversion.

In column (5), we present the results from estimating our model on the matched control sample by itself. Unlike for the fraud sample, where the coefficient on Post is significantly negative, the coefficient on Post for the control sample is not significant. Finally, we estimate our model using both the diversion and control organizations simultaneously and including the indicator variable Fraud, which equals one for the observations in the diversion sample and zero for observations in the control sample. In column (6), the coefficient on Post*Fraud Orgs is negative and marginally significant (p = .058), providing some evidence that the organizations disclosing an asset diversion receive fewer contributions than the control organizations after disclosure. Notably, the coefficient on Post, which reflects the postyear for the control sample in this specification and the coefficient on Fraud, which reflect the year before the diversion is made public for the fraud sample, are not significant. Overall, the results in columns (5) and (6) suggest that the disclosure of the fraud, not sector-wide factors, drive lower donations.

Attention Hypothesis Tests

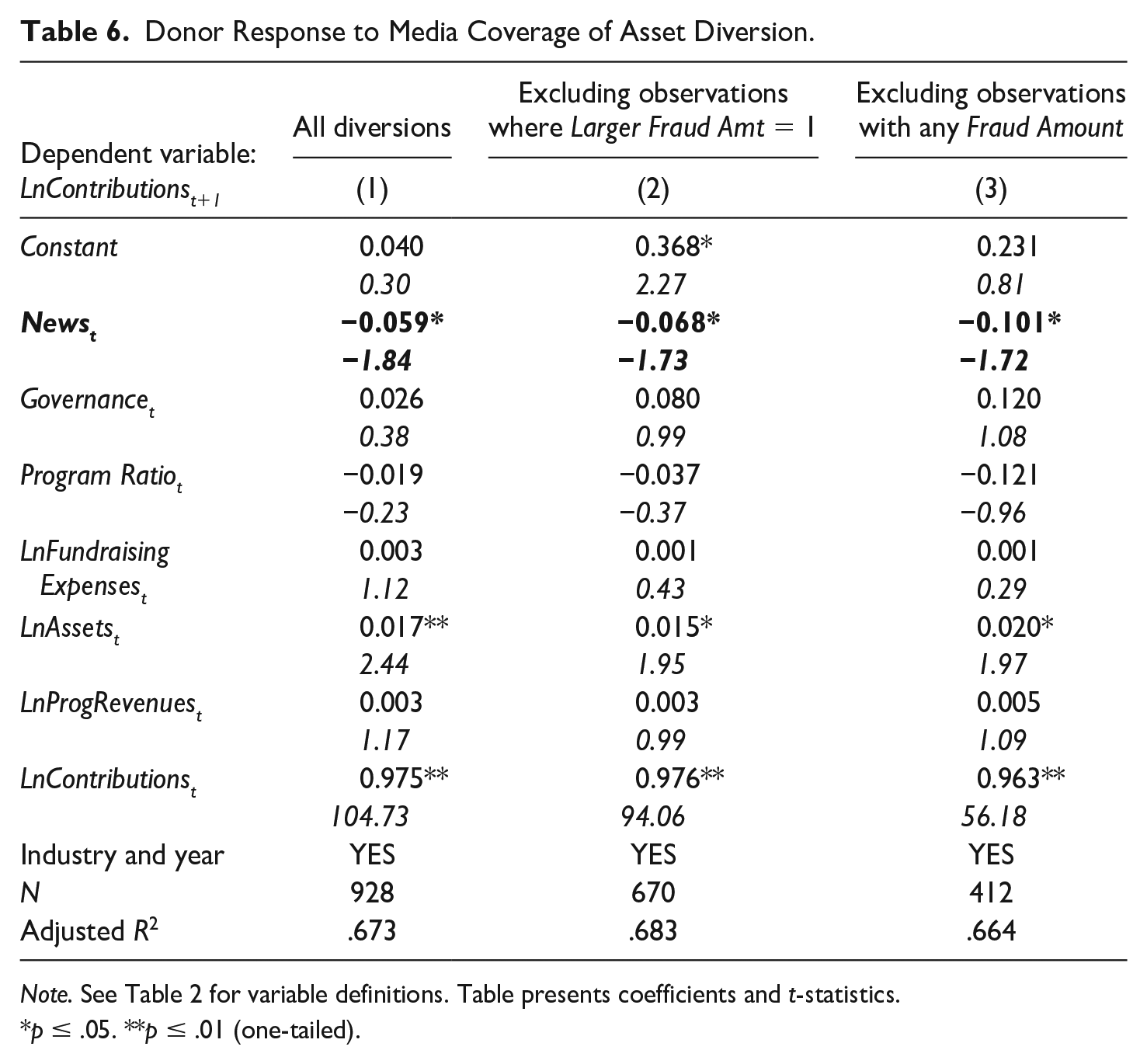

To examine whether media coverage exacerbates donor reaction, we include News in equation (1). We predict the coefficient on News is negative, consistent with more attention to the loss resulting in fewer donations. For this analysis, we are examining cross-sectional differences in organizations disclosing a diversion and, thus, use every observation once.

In Table 6, the negative coefficient on News in the first column indicates that organizations with diversions covered by the media experience steeper declines in donations than organizations with diversions not covered by the media. All else equal, the coefficient indicates nonprofits with frauds in the news receive 5.7% fewer donations.

Donor Response to Media Coverage of Asset Diversion.

Note. See Table 2 for variable definitions. Table presents coefficients and t-statistics.

p ≤ .05. **p ≤ .01 (one-tailed).

It is possible that the media is more likely to cover larger diversions and the decline in donations observed in column (1) results from donors reacting to substantial fraud losses, not media coverage. To address this possibility, we remove the 258 observations with fraud losses greater than median Fraud Amount. Even when removing the largest frauds in column (2), we continue to observe a negative coefficient on News. Finally, in column (3), we remove the 516 observations that report any fraud amount and, thus, the amount of diversion for the remaining observations is unknown. Again, we report a negative coefficient on News, which supports the attention hypothesis and suggests the media results are not driven by larger frauds.

Transparency Hypothesis Tests

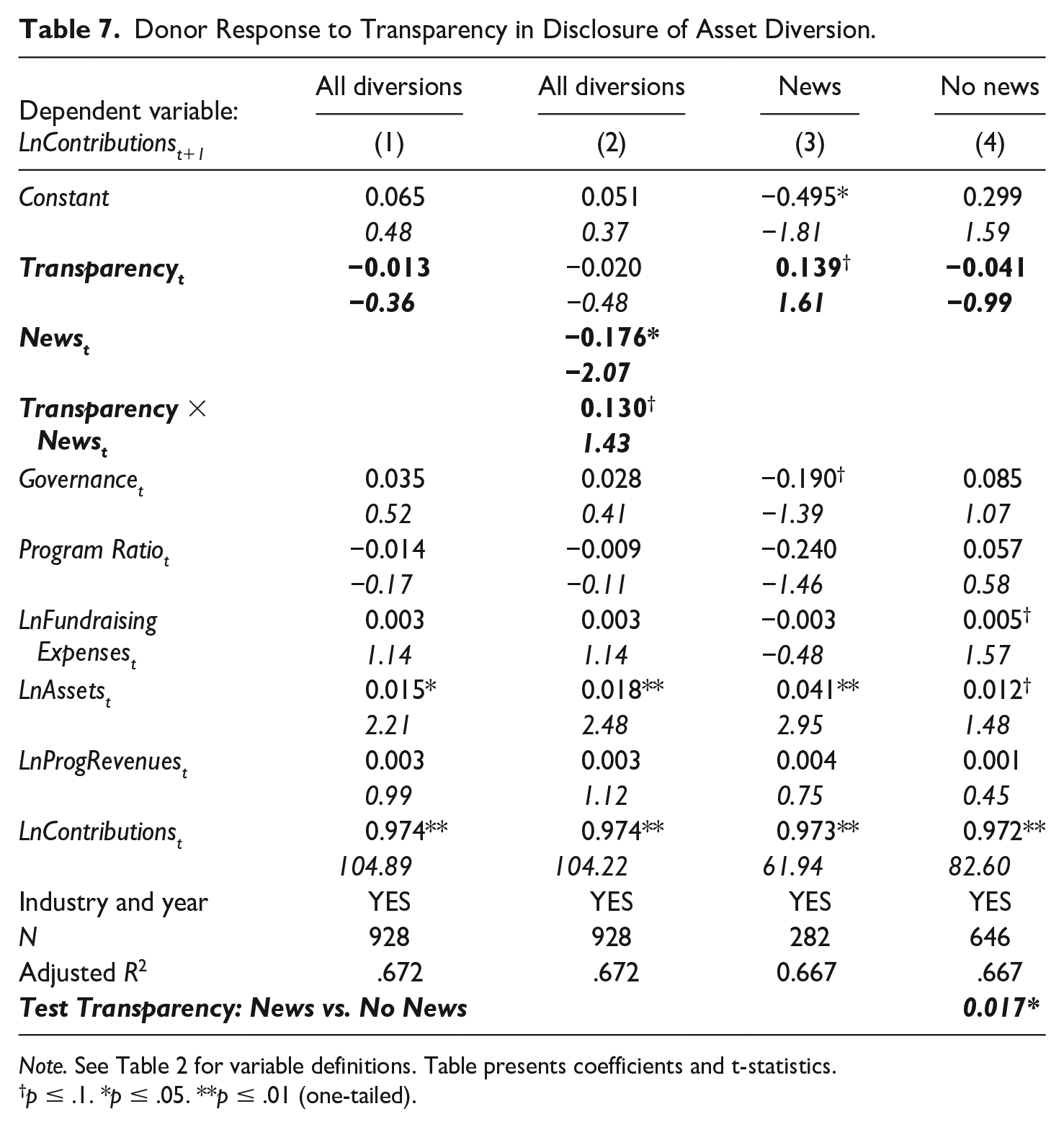

To examine the extent to which disclosures affect donors’ response to diversions, we expand equation (1) to include Transparency. We predict a positive coefficient on Transparency, because a lack of information can increase donors’ assessment of future risk. Table 7 provides the results for the transparency hypothesis. Inconsistent with our expectation, the coefficient on Transparency in column (1) is insignificant.

Donor Response to Transparency in Disclosure of Asset Diversion.

Note. See Table 2 for variable definitions. Table presents coefficients and t-statistics.

p ≤ .1. *p ≤ .05. **p ≤ .01 (one-tailed).

We next add News and Transparency interacted with News in column (2). The coefficient on Transparency remains insignificant. The coefficient on News is significantly negative, consistent with Table 6. Most interesting, the positive coefficient on the interaction term is marginally significant (p = .07) indicating that organizations can mitigate the spread of bad news by being more transparent about their fraud circumstances.

Organizations in the news may differ from organizations not in the news in terms of fundamental characteristics. To address this possibility, we estimate the regression separately for diversions that receive media coverage (column 3) and diversions that did not receive media coverage (column 4). This analysis is essentially the same as column (2) but this methodology gives the control variables more power to explain the dependent variable when the control variables differ across news coverage. The coefficient on Transparency for organizations in the news is marginally significant while the coefficient on Transparency for organizations not in the news is not significant. The difference between these coefficients is significant, indicating that transparency is positively associated with donations, but only when the diversion receives media attention.

The results in columns (2) and (3) indicate that managers can temper negative media coverage of asset diversions by providing information about the fraud in Schedule O. All else equal, the coefficients indicate that donations are more than 11.6% higher for transparent organizations in the news compared to nontransparent organizations in the news. It is important to note that Transparency is measured as the existence of Form 990 disclosures; it can’t be evaluated in the news stories. Thus, this result is consistent with idea that news focuses donor attention on information contained in the Form 990.

Content Hypothesis Tests

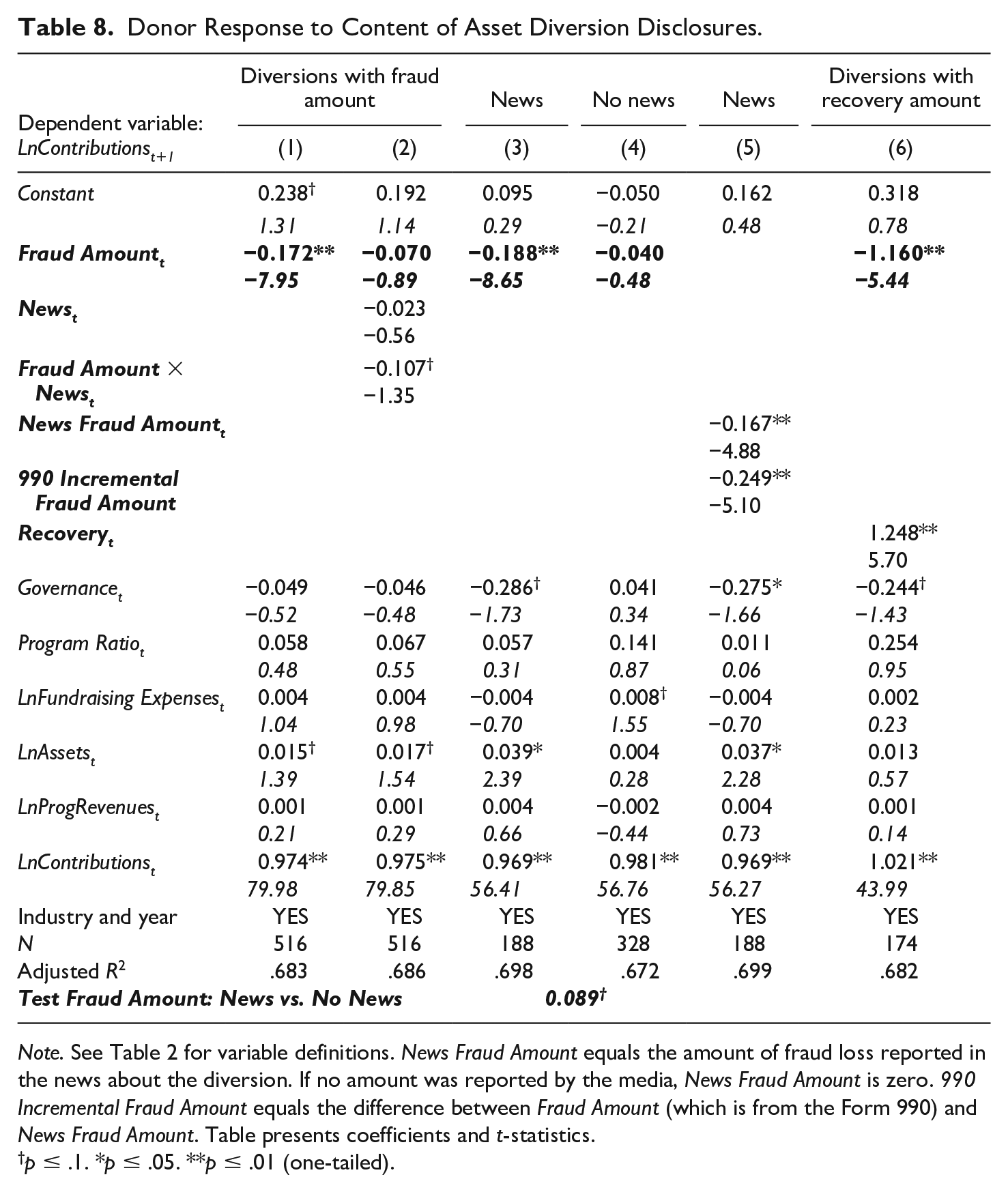

To examine whether the content of the diversion disclosure affects donations, we limit our sample to organizations providing the fraud dollar amount in Schedule O. We predict a negative coefficient on Fraud Amount if greater losses result in more donor distrust. We also expect that donor reaction is less severe for organizations that have larger recovery amounts and predict a positive coefficient on Recovery.

In column (1) of Table 8, the coefficient on Fraud Amount is negative; contributions are negatively associated with the relative size of the fraud loss. In column 2, we interact Fraud Amount with News and observe a negative coefficient on the interaction. We partition the sample by media coverage in columns (3) and (4) and observe a significantly negative coefficient in the news partition. Overall columns (2) through (4) reveal that the negative coefficient on fraud amount is driven primarily by diversions reported in the news, consistent with the attention hypothesis.

Donor Response to Content of Asset Diversion Disclosures.

Note. See Table 2 for variable definitions. News Fraud Amount equals the amount of fraud loss reported in the news about the diversion. If no amount was reported by the media, News Fraud Amount is zero. 990 Incremental Fraud Amount equals the difference between Fraud Amount (which is from the Form 990) and News Fraud Amount. Table presents coefficients and t-statistics.

p ≤ .1. *p ≤ .05. **p ≤ .01 (one-tailed).

While this result suggests that donors respond to the size of the fraud when the fraud is in the news, it does not speak to where the donor obtained information about the loss amount. Recall donors can react to information in the news directly and/or donors can see the news which influences them to read the Form 990 more carefully. In an additional analysis, we take advantage of the fact that the fraud amount reported in the news is not necessarily the fraud amount reported on the Form 990 to better understand where donors receive information. For example, on August 20, 2017, the Associated Press reported that Project VetCare experienced a $90,000 fraud. When Project VetCare filed its Form 990 on November 15, 2017, it disclosed that the fraud was in excess of $150,000.

For the 188 observations that report a fraud amount on the 990 and are covered in the news, we measure News Fraud Amount as the amount of the diversion according to the first media story about the fraud scaled by total expenses. If no amount is mentioned, we set News Fraud Amount to zero. We then compute 990 Incremental Fraud Amount as the amount from the 990 minus the amount from the news. 990 Incremental Fraud Amount reflects information that is on the Form 990 but not in the news. Untabulated results indicate that the mean (median) 990 Incremental Fraud Amount is 0.080 (0.001), indicating that the fraud losses reported on the Form 990 are, on average, higher than the fraud losses reported in the news.

As seen in column (5), the coefficient on News Fraud Amount is significantly negative as expected, given our results in the previous columns. Notably, the coefficient on 990 Incremental Fraud Amount is also significantly negative. This result suggests that the Form 990 does provide incremental information which donors use to make contribution decisions.

Finally, in column 6, we examine the association between recovery amounts and subsequent donations by including Recovery in our model. Recall, only 174 observations report a recovery amount on the Form 990. Nevertheless, the coefficient on Recovery is significantly positive, suggesting donors penalize organizations less harshly when they report larger recovery amounts. In untabulated results, we examine Recovery separately for news and no news observations and find no meaningful inferences, which is likely due to the small sample size (only 58 observations with a recovery amount are in the news).

Supplemental Analysis of Corrective Actions

Our main analysis indicates that donors penalize nonprofits that disclose a diversion, particularly when the diversion is covered by the media. Our results also provide some evidence that organizations can mitigate this negative reaction through transparency and loss recovery. Organizations may also be able to rebuild trust by taking corrective action, notably by improving governance. Organizations with improved governance are more likely to safeguard charitable assets in the future (Harris et al., 2017; IRS, 2008).

Prior research finds that donors reward good governance in general settings (Flynn, 2011; Harris et al., 2015; Kitching, 2009). 7 Furthermore, there is evidence in the for-profit sector that improved governance helps repair firms’ reputations with investors following financial reporting fraud (Farber, 2005). Finally, in an experimental setting, Lauck and Brozovsky (2018) report that potential donors have a more favorable impression of an organization when board oversight is enhanced following a misappropriation. We conduct a supplemental analysis to confirm these results in our setting. Specifically, based on prior research, we expect donors reward organizations that strengthen their governance to reduce the risk of future diversions.

To test this expectation, we include Governance Change in equation (1). Governance Change equals the change in Governance from t – 1 to t + 1 where t is the year the diversion is detected. Of the 861 observations with governance change data, 102 report improvements. Consistent with prior research, untabulated results indicate that governance improvements are positively associated with donations received in the year following the diversion.

We expand this analysis by examining a specific governance mechanism, namely external audits. An external audit is an especially important governance mechanism to help prevent large fraud losses because auditors ensure management implements effective internal controls and audits can result in earlier detection of problems (Garven et al., 2018; Harris et al., 2017; Kitching, 2009; Petrovits et al., 2011). Thus, we include in our model Audit Change, which is an indicator variable set to one if the organization added an external audit in the year of the fraud or the subsequent year. Audit Change equals one for 8% of our sample. In untabulated results, we find that both Governance Change and Audit Change are positively associated with donations received in the year following the diversion. Overall, the evidence from our supplemental analysis confirms prior research that donors value governance safeguards.

Discussion

We find that nonprofit organizations reporting asset diversions experience a decrease in subsequent donations, consistent with fraud undermining donor confidence. Our evidence indicates that the penalty is larger when the diversion is in the news. Furthermore, donors appear to punish organizations more when the loss is larger but only when the diversion is covered in the news. In addition, we find evidence that transparent disclosures help when the diversion is in the news (and no evidence that transparency hurts when the diversion is not in the news). Finally, a supplemental analysis confirms prior research that donors reward good governance, in this case by adopting better governance policies, such as an external audit, following a diversion.

Managerial and Public Policy Implications

This study offers insight into the role that the media plays in donor oversight. We provide some evidence that the media can not only inform external constituents about the diversion but can also steer donor attention toward the Schedule O detailed disclosures, such as the amount of loss. Moreover, organizations with diversions in the news are more likely to be transparent on the Form 990 than organizations with diversions not in the news, consistent with Tremblay-Boire and Prakash (2015). This result suggests that the press influences organizational behavior. Despite the crucial role that the media can play, less than one-third of diversions in our sample are covered by the media, suggesting a lack of investigative resources. For these reasons, the loss of local media outlets (Abernathy, 2022; Felix et al., 2022) has a detrimental effect on the nonprofit sector by reducing oversight and impairing the amount and quality of information used by donors.

The importance of the media does not discount the value of the Form 990 as a source of information. Organizations not in news also experience a decline in donations, suggesting donors respond to the asset diversion checkbox on the Form 990 either directly or indirectly via charity watchdogs. The major revision to the Form 990 implemented by the IRS in 2008 was controversial. As Brody (2012) explains, opponents argued that donors would find the expanded disclosures irrelevant. Our results suggest that the asset diversion and governance checkboxes on the revised Form 990 are relevant to the giving decisions of at least some donors.

Related to the decision-relevance of Form 990 information, we extend research by examining whether donors also use the narrative information on Schedule O. Prior research has documented donor use of standardized financial line items in the main body of the 990 (e.g., Tinkelman & Mankaney, 2007; Weisbrod & Dominguez, 1986; Yetman & Yetman, 2013). There is, however, little work on whether donors consider the exposition provided in Schedule O, which includes details on many topics beyond asset diversions. Responding to Schedule O involves careful reading of inconsistently presented narratives. Our evidence is mixed—donors appear to value the Schedule O details, but only when media coverage spurs them to obtain more information. Notably, our results from a smaller subsample test suggest that donor decisions reflect both the fraud amount from news and the incremental fraud amount from Schedule O, consistent with Form 990 disclosures being decision relevant.

In addition, our study supports prior evidence that there is not robust IRS oversight of the nonprofit sector (Archambeault et al., 2015; Fahrenthold et al., 2022; GAO, 2014; Lee, 2019; O’Harrow, 2017). We find that 20% of organizations do not follow requirements to provide information on Schedule O, implying a lack of IRS monitoring. While there appears to be a lack of federal scrutiny over disclosures, donors in conjunction with the media provide some oversight.

Finally, maintaining public trust is especially important for nonprofits that rely on donations (Bryce, 2007; Jaeggi, 2014). Our results suggest steps that boards and managers can take to reduce reputational risks associated with fraud. Organizations can proactively implement internal controls that will quickly detect diversions and obtain appropriate insurance coverage, both for the purpose of limiting the amount of any loss. If a diversion occurs, organizations can communicate openly with constituents through transparent disclosures. Organizations can also repair trust through governance improvements, such as undergoing an audit and increasing board independence.

Limitations and Future Research

Our study has several notable limitations and provides some directions for further research. First, while our study documents that there are at least some donors who use Form 990 disclosures on diversions, it does not speak to the characteristics of these donors. Our results are likely driven by a subset of sophisticated donors. Identifying how different types of donors (i.e., individuals, foundations, corporations, and government grantors) process fraud information would be a valuable addition to the literature. Likewise, it is worthwhile to better understand the effects of diversions across organizations with a narrow donor base (a few large donors) versus organizations with a broad donor base (many small donors).

Second, we consider circumstances where donors may learn about a diversion from the media or from the Form 990 (either directly or from an information intermediary who uses the Form 990). Our sample of news coverage is relatively small. More research is needed to corroborate the media’s role in spurring donors to conduct more research. Furthermore, there are other information channels whereby donors may learn about a diversion, such as social media or word of mouth from an employee or volunteer. Understanding the role of other channels, especially as local media coverage shrinks and social media plays a more prominent role, is a promising avenue for future research.

Third, our study examines donor response in the year after the fraud. A longitudinal study that assesses any permanent changes in an organization’s behavior, as well as donor response, following a diversion will help nonprofit managers better understand the long-run implications of fraud. It would be especially interesting to understand if certain types of misconduct have longer term effects on the nonprofit’s reputation (e.g., diversions involving board members or executives).

Fourth, the Form 990 contains many disclosures, including programmatic accomplishments, governance, compensation, and functional expense allocations. We examine a small sample of Schedule O disclosures under a narrow set of negative circumstances (experiencing a fraud). It would be useful to investigate whether donors value transparency and use narrative information in broader contexts to inform future Form 990 revisions. Related, our evidence suggests the IRS does not monitor organizations for Schedule O compliance. It would be worthwhile to better understand which sections of the Form 990, if any, are scrutinized by the IRS.

Finally, there have been two notable events in the nonprofit sector since the time period of this study. First, the Tax Cuts and Job Act of 2017 reduced giving incentives for many taxpayers. Second, for Form 990s filed for tax year 2019 and later, the IRS processing delay is now well over 36 months (Clerkin & Koob, 2022). While donors may be able to obtain Form 990s directly from the organizations, they are unable to obtain Form 990s on a timely basis from the IRS or charity watchdogs (who obtain data from the IRS). Future research can investigate how tax law changes affect donation amounts and how information lags affect donor’s use Form 990 information.

Footnotes

Data Availability Statement

The code that produces the findings reported in this article will be made publicly available with assistance from the NVSQ Editorial Team upon acceptance. All data are publicly available for hand collection. We purchased a data set of publicly available IRS Form 990 data, which we are not permitted to make available due to our contract.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.