Abstract

Loan book management is important to community credit union survival, particularly in deprived localities. Consistent with agency theory, prior studies of credit unions report an association among individual monitoring mechanisms, trade association monitoring, and female board representation, respectively, and reduced loan losses. This study provides a more nuanced understanding by investigating the moderating influence of these monitoring mechanisms on the relationship between loan losses and deprivation and by considering the effect of bundle combinations of different levels of the two monitoring mechanisms on loan losses. The results reveal that credit unions subject to trade association monitoring have the lowest loan losses. However, in the absence of trade association monitoring, female board representation has a moderating effect on loan losses as deprivation increases. Finally, trade association monitoring and female board representation have a substitutive, rather than a complementary effect on loan losses.

Introduction

Community credit unions (hereafter called credit unions) are self-help, co-operative organizations that offer financial services to their respective communities, including to individuals in deprived localities with restricted access to banks. Credit unions are well placed to mitigate income and health inequalities in deprived localities by providing financial services to those who are financially excluded (Marmot et al., 2020; Saunders, 2019). The increased financial risk from transacting with members who live in deprived localities highlights the importance of financial monitoring to mitigate the threat to credit union survival from loan losses (Chakrabarty & Bass, 2014). Governing boards set strategy, perform a control function, and represent stakeholders. Credit union boards act on behalf of their members and regulators (Van Puyvelde et al., 2012). Therefore, they are exposed to agency conflicts and, as with for-profit (FP) organizations, it is recognized that monitoring mechanisms mitigate agency exposure (Jensen & Meckling, 1976). Prior nonprofit (NP) research investigates the independent association between, respectively, trade association monitoring and female board representation on financial risk in credit unions (Forker & Ward, 2012; Ward & Forker, 2017).

The management literature on FPs however identifies that governance mechanisms do not act independently of each other, that each mechanism has distinct characteristics, roles and functions, and that the effectiveness of one is affected by the presence or level of other governance mechanisms (Rediker & Seth, 1995; Schepker & Oh, 2013). Therefore, financial management is influenced by the efficiency of bundle combinations of governance mechanisms as opposed to one mechanism. It is claimed that a focus on the “independent” effects of governance mechanisms can lead to incorrect conclusions about the effectiveness of individual mechanisms as they interactively influence organizational outcomes in a complex way (Aguilera et al., 2008; Oh et al., 2018).

Theoretically, this study contributes by identifying the significance of bundling different levels of two monitoring mechanisms on the relationship between locality deprivation and loan losses in credit unions. Empirically, the study uses panel data spanning a 10-year period from 2002 to 2011 to examine the effectiveness of bundle combinations of different levels of trade association financial monitoring and female board representation in reducing loan losses in credit unions in Northern Ireland. Given the importance of a credit union’s loan book in generating income to cover costs, maintain statutory reserves and provide distributions, loan losses provide a good indication of credit union financial risk. The ratio of the Registrar for Credit Unions and Industrial and Provident Societies’ (the Registrar’s) recommended allowance for loan losses to gross loans is a consistent measure across all credit unions (Forker & Ward, 2012). 1 The findings provide additional evidence on how a credit union can better manage their loan losses by designing monitoring mechanisms effectively.

The remainder of the article is structured as follows. The next section outlines the literature and develops the hypotheses. This is followed by the data and methodology. Descriptive statistics and results are then outlined. The latter part of the study contains the discussion, limitations, and the conclusions.

Theory and Hypotheses Development

Communities constitute an important dimension in the social environment by facilitating networks and fostering social capital. Communities are not homogeneous as differences result across socioeconomic environments. Deprivation has negative consequences for a person’s wealth and is linked to health inequalities and life expectancy (Marmot et al., 2020). Access to personal credit when used appropriately can help people manage and improve their lives and circumstances (Saunders, 2019). Credit unions are typically located within the community they serve and are designed to cater the needs of members who are financially excluded. Credit unions do not typically receive grant funding, interest income on loans to members is a credit union’s main source of income, thus financial risk and survival is inherently linked to their members’ socioeconomic status (Ward & McKillop, 2005). Credit unions typically require evidence of a period of sustained saving behavior, personal relationships, and member guarantors when making credit decisions. This is of primary importance in deprived localities where information asymmetry is greater and where members have little or no collateral or credit history (Mersland, 2011). Despite the inherent safeguards, the risk of default is higher in deprived localities, and Ward and McKillop (2005) report that credit unions in deprived locations are more likely to have weaker financial performance. Therefore, given the link between member wealth and the risk of default, it is hypothesized that the potential for loan losses is greater in credit unions located in deprived localities:

Monitoring Mechanisms, Locality Deprivation, and Loan Losses

Credit union governance is notable for the close relationship among the board and members, managers, staff, and volunteers. Indeed, in most credit unions, board positions are voluntary, and recruitment is restricted to members only. 2 Accordingly, NP governance extends beyond standard agency theory to incorporate insights from stakeholder, stewardship (Van Puyvelde et al., 2012), and resource dependence theories (RDT; Ward & Forker, 2017). Although there are differences in respect of the categorization of stakeholder groupings as either principals or agents, there is a consistent view that the overarching responsibility of the board is to protect and enhance membership benefits through a variety of functions including access to external resources, advising management, and controlling agency costs. Monitoring mechanisms are predicted to attenuate agency conflicts and reduce financial risk (Jensen & Meckling, 1976). However, many of the monitoring mechanisms identified in FP studies are not available in credit unions due to their legal form, such as the market for corporate control, investor monitoring, and share-based incentives (Oh et al., 2018; Rediker & Seth, 1995).

This study investigates the effectiveness of two monitoring mechanisms available to credit unions on the control of loan losses. The first monitoring mechanism—trade association quarterly monitoring—is external, costly, and targets financial management. Trade associations are self-regulatory bodies that typically provide representation, training, and guidance to their affiliated credit unions (Forker et al., 2014). In addition, some trade associations provide a monitoring role, wherein financial management is assessed by comparing financial ratios to predefined target ratios (PEARLS ratios) set by the World Council for Credit Unions (WOCCU, 2017). These target ratios are recommended and, when breached, may spark a field audit by the trade association (Forker & Ward, 2012). Forker and Ward (2012) and Ward and Forker (2017) report that affiliation to a trade association that provides quarterly financial monitoring is associated with lower loan losses in credit unions in Northern Ireland. Therefore, it is hypothesized as follows:

Moreover, as credit policies typically do not consider a member’s ability to repay the loan, it is hypothesized as follows:

The second monitoring mechanism, female representation on the board (Adams & Ferreira, 2009), is internal and associated with lower loan losses in credit unions (Ward & Forker, 2017). It is reported that women are systematically different to men—cognitively, physiologically, and psychologically (Zalata et al., 2019). Women are on average less aggressive, competitive, self-interested, and overconfident, and more altruistic, cautious, communal, fair, objective, conservative, and responsible. These traits enable them to monitor more intensely relative to men, and FP studies identify that women on boards improve board monitoring (Adams & Ferreira, 2009; Jonsdottir et al., 2015; Zalata et al., 2019). 3 RDT identifies benefits from female representation on boards due to stronger links with the membership and a capacity to build better trust relationships with borrowers compared with men, resulting in lower defaults (Beck et al., 2013; Chakrabarty & Bass, 2014; Hartarska et al., 2014). As an association between female representation on boards and loan losses is noted in credit unions (Ward & Forker, 2017), it is hypothesized as follows:

Variation in the extent of monitoring undertaken by women directors is expected as the literature identifies that shifts in the gender composition of the board influences board dynamics and decision-making (Hillman et al., 2007). Specifically, female voice, or male voice, is only likely when a critical mass of women, or men, is present on the board (Kanter, 1977a, 1977b; Torchia et al., 2011). Female directors on boards with less than this “magic proportion” are likely to be token appointments or may form coalitions that have some impact on board dynamics but are still outnumbered by the dominant group. Hence, decision-making in general does not reflect the gender voice (Joecks et al., 2013). It is also argued that gender no longer influences decision-making when boards are gender-balanced as the focus turns to the different abilities and skills of individuals (Kanter, 1977a). Therefore,

Residual information asymmetry is predicted to be greater in more deprived communities where members have little or no collateral or credit history (Mersland, 2011). Cao et al. (2015) find that when information asymmetry is perceived to be greater, board independence is more important and RDT predicts that female leadership has comparative advantage over boards that do not have female leadership in terms of reduced information asymmetry due to stronger network links (Brown et al., 2012). Consistent with this view, in a study on gender and banking, Beck et al. (2013) suggest that females have comparative advantage in informal settings, as they are better able to build trust relationships with borrowers. Therefore, we expect female leadership to have a relatively stronger influence on the management of loan losses in credit unions located in the most deprived communities. Therefore, it is hypothesized as follows:

Effect of Bundling Trade Association Monitoring and Female Board Representation on Loan Losses

As different monitoring mechanisms are used to reduce agency costs, it is claimed the behavior and effectiveness of each mechanism is influenced by the levels of other mechanisms (Rediker & Seth, 1995), and they interactively influence organizational outcomes in a complex way by either complementing or substituting for each other (Aguilera et al., 2008; Oh et al., 2018). The complementary perspective is that governance mechanisms complement each other to synergistically improve outcomes for the organization. Hence “more” is better. In contrast, the substitutive view is that there are no complementary benefits from using multiple governance mechanisms. When governance mechanisms act as substitutes, fewer mechanisms are required to improve financial management.

Although constrained in NP settings, the substitute versus complement approach can be applied to examine the effect of bundling different levels of two monitoring mechanisms (Rediker & Seth, 1995). In the context of the study site, credit unions choose to affiliate or not to a trade association that undertakes quarterly financial monitoring. Therefore, two distinct levels of external monitoring exist, one low and one high. In addition, to cater for differences in board dynamics resulting from critical levels of males and females (Kanter, 1977a), boards are categorized as male dominant, diversified, or female dominant, with the latter two deemed to be high relative to the former two. Under the complement versus substitute approach, the effectiveness of each monitoring mechanism in mitigating agency cost is influenced by the level of monitoring undertaken by the other monitoring mechanism.

A complementary effect arises when the mechanisms operate synergistically to reduce loan losses. For example, women are reported to undertake monitoring and resource provision roles (Jonsdottir et al., 2015) including strengthening networks with stakeholders, including borrowing members, and may switch efforts to the resource provision role when credit unions are subject to quarterly external financial monitoring. Strengthened links with borrowing members may lead to further reductions in loan losses. Therefore,

A substitutive effect is evident when the benefit of one mechanism is high in reducing loan losses at a low level of the other mechanism and vice versa. For example, when the quarterly financial management system identifies financial weakness, a site visit ensues (Forker & Ward, 2012). Adams and Ferreira (2009) report that female board representation attenuates agency problems by improving monitoring on boards when governance and monitoring are weak. Finally, Mersland (2011) argues that in micro finance institutions, connection to the membership is more important in the absence of monitoring. Therefore,

The Moderating Effect of Monitoring Bundle on the Association Between Locality Deprivation and Loan Losses

Oh et al. (2018) report that organizations have strategic flexibility when designing governance practices and do so to achieve their optimal outcome, depending on their circumstances. Quarterly trade association monitoring is costly. Cost is particularly pertinent for credit unions in deprived locations that operate with higher levels of inherent financial risk. To examine whether credit union boards select different bundle combinations to minimize loan losses given their specific environment, it is hypothesized as follows:

Data and Methodology

Data

The panel data set consists of 1,734 yearly observations from 182 credit unions registered with the Registrar over the 10-year period from 2002 to 2011 and was hand-collected.

Dependent Variable

Loan losses are the Registrar’s ratio of expected loan losses at the financial year-end divided by gross loans outstanding at the year-end (Forker & Ward, 2012). The allowance is made up of 10% for loans overdue between 10 and 18 weeks, 20% for loans overdue between 19 and 26 weeks, 40% for loans overdue between 27 and 39 weeks, 60% for loans overdue between 40 and 52 weeks, and 100% for loans overdue for more than 52 weeks. A higher ratio indicates weaker credit management.

Independent Variables

Community deprivation

Community deprivation is captured by a locality-specific multiple deprivation measure (MDM) assigned to the credit union’s postcode by the Northern Ireland Statistics and Research Agency (NISRA). The MDM is a continuous measure ranging from 2.08 to 83.33. It is time invariant for each credit union. It comprises a low-income factor, a low-employment factor, an education factor, a housing factor, an access to services factor, a social environment factor, and a health factor (NISRA, 2010). The higher the value the more deprived the location. The 2010 MDMs are based on data collected over the period 2007 to 2009. MDMs published in 2005 are also available. However, the 2010 MDM is calculated using different underlying variables, and the two measures are not directly comparable. The differences in the rank orderings by location of the two MDMs between the two periods were statistically tested and were not found to be statistically significant. This lends some credibility to the use of a constant MDM per location over the whole period from 2002 to 2011. The models used in this study were also estimated using the two measures, respectively, but the key regression model estimates were found to be robust to the use of either variant of this measure.

Trade association financial monitoring

Credit unions affiliated to the Irish League of Credit Unions (ILCU) are subject to WOCCU’s (2017) financial management system including quarterly monitoring. All other credit unions are not. Two categorical variables are used to distinguish between credit unions that are subject to quarterly monitoring (T) and those that are not (N). Each variable is coded 1 if T or N, and 0 otherwise.

Female board representation

As the behavior of women on boards is sensitive to the strength of their voice relative to males (Kanter, 1977a, 1977b; Torchia et al., 2011), female board representation (

Monitoring bundle

In this study, a bundle approach is applied to investigate the effect on loan losses of six combinations of the two specific monitoring mechanisms. The bundle combinations are as follows: quarterly financial monitoring by trade association with female-dominant boards (TF), with diversified boards (TD), and with male-dominant boards (TM); not subject to quarterly financial monitoring by trade association with female-dominant boards (NF), diversified boards (ND), and with male-dominant boards (NM). These yield categorical variables representing the six mutually exclusive bundle combinations kj: k1 = TF, k2 = TD, k3 = TM, k4 = NF, k5 = ND, k6 = NM, where j = 1, . . ., 6, and each variable is coded 1 if adopting that particular bundle combination, and 0 otherwise.

Control Variables

The control variables included to capture other influences on credit union loan losses are size (s = log of total assets), age (AGE = log of age), number on board (n), and a set of year effects (YEAR). Prior studies report that size is important to credit union performance (Forker & Ward, 2012; Ward & Forker, 2017; Ward & McKillop, 2005); therefore, a negative association is predicted between size and loan losses, as larger credit unions are more likely to have an experienced paid manager (McKillop et al., 2005). Age is also important. Young credit unions are less likely to have saturated their potential membership and can be more selective when awarding credit. Hence, a positive association is expected between age and loan losses (Forker & Ward, 2012). Larger boards are assumed to reap benefits under RDT due to the increased links with outside networks. However, they also are associated with increased conflict in decision-making. In the NP literature, Bradshaw et al. (1992) report no association between board size and budget growth, Galema et al. (2012) conclude that larger boards in MFIs are less efficient, and Hartarska and Nadolnyak (2012) find a nonlinear association in community development loan funds. The net impact of the offsetting effects is unclear.

Method

Given the nature of the relatively short panel data available and the fact that the key research questions are focused around either time-invariant variables—for example MDM—or variables that move glacially over time, for example %WOB, we use a correlated random-effects (CRE) linear model that treats the underlying observations as a conventional panel data set. The primary advantage of the CRE approach in the current setting is that it is more flexible than fixed-effects and allows for the inclusion and identification of the effects of both time-invariant and time-varying variables. The CRE model is normally used in balanced panels; however, adjustments by Wooldridge (2019) enable the CRE model to be adapted for unbalanced panels. This model is applied in this study.

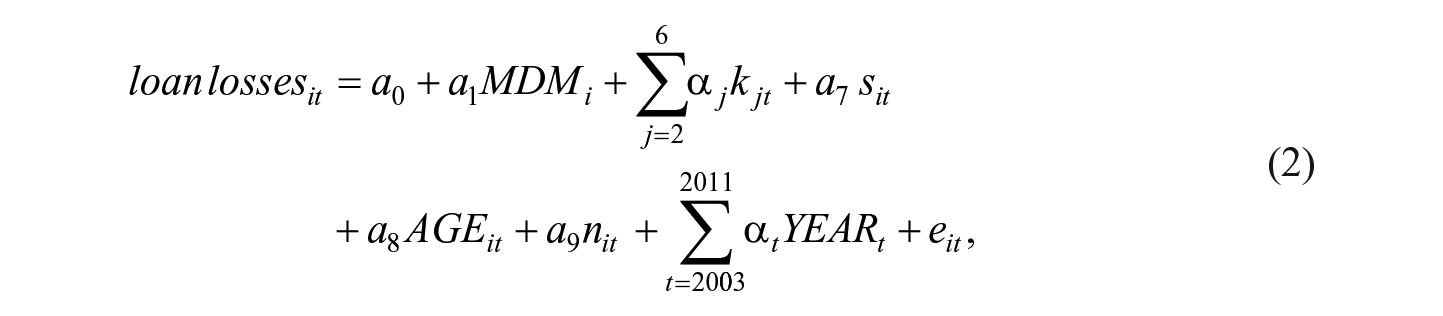

The model specification for estimating the effect of trade association monitoring and female board representation on the association between MDM and loan losses (H1, H2a, H2b, H3a, H3b, and H3c) is specified as follows:

where i = 1, . . ., N; t = 2002 to 2011.

The moderating effect of trade association monitoring on the association between MDM and loan losses is reflected by the interaction variable (Tit × MDMi). The moderating effect of female board representation on the association between MDM and loan losses is captured using the interaction variable (fit × MDMi). The idiosyncratic error term (uit) is model specific.

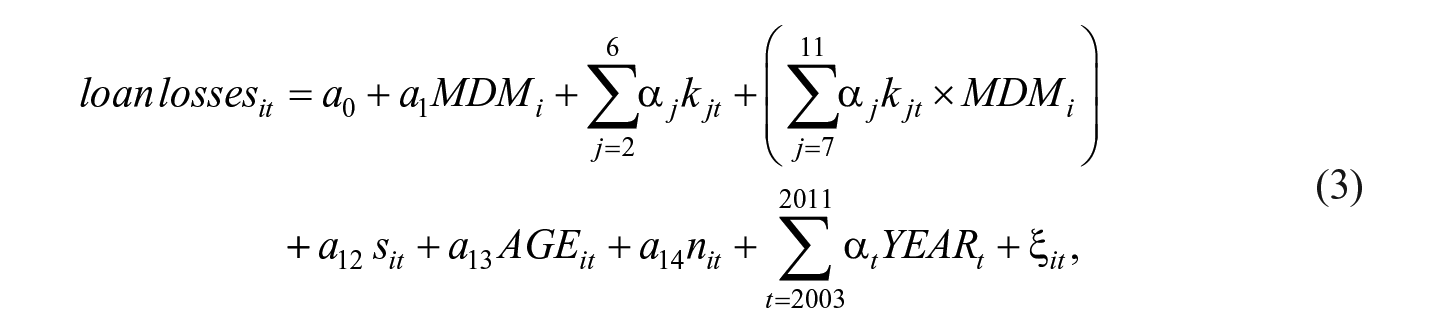

The model specification for investigating whether, when bundled, trade association quarterly monitoring and female board representation have a complementary or substitutive effect on loan losses (H4a and H4b) is given by,

where i = 1, . . ., N; t = 2002 to 2011; and eit is now the idiosyncratic error term.

The final model specification for estimating the effect of monitoring bundle on the association between MDM and loan losses (H5) is as follows:

where i = 1, . . ., N; t = 2002 to 2011; and ξ it is now the idiosyncratic error term.

The moderating effect of monitoring bundle on the association between MDM and loan losses is captured using the set of interaction variables

Results

Descriptive Statistics

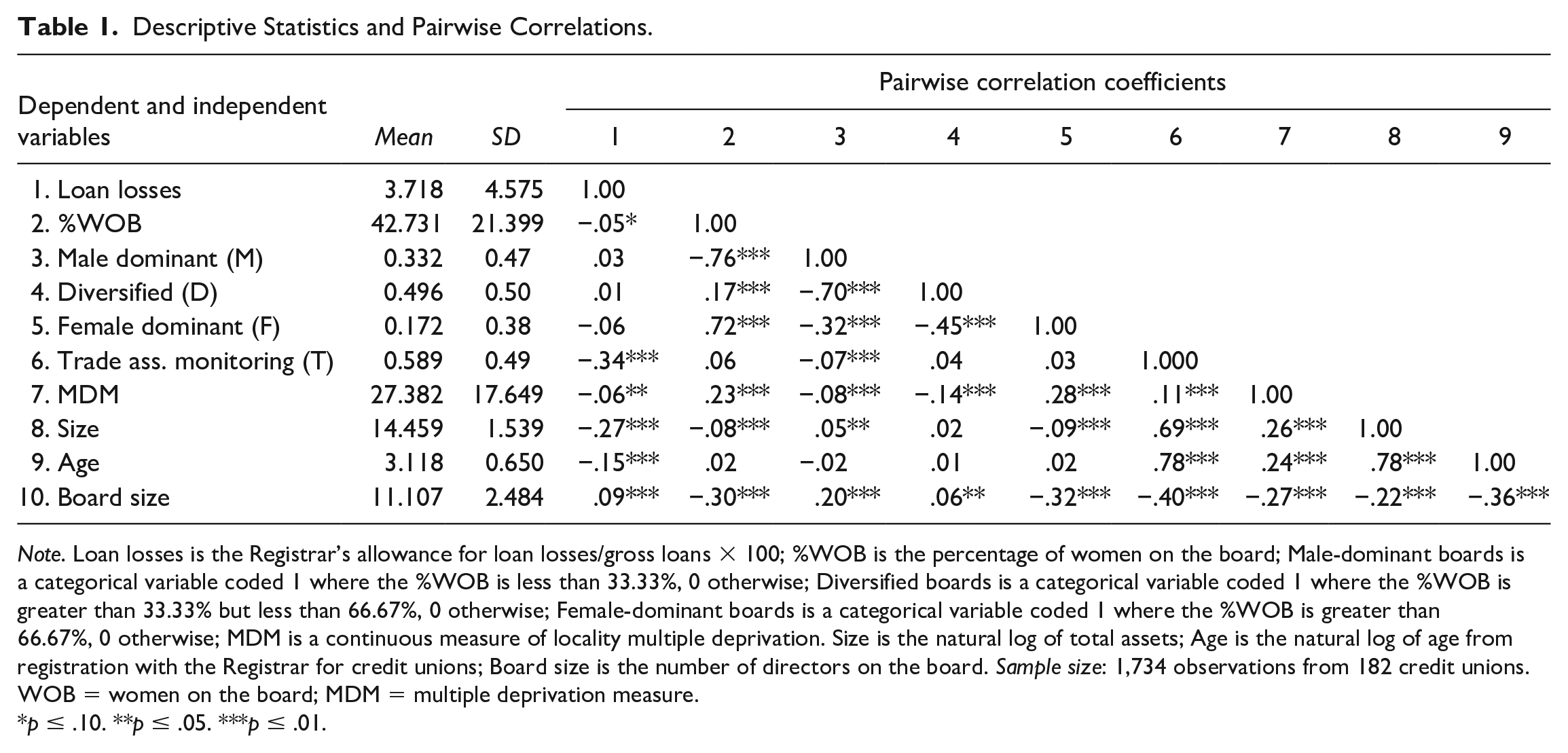

The mean values, standard deviations, and correlations between dependent and independent variables are presented in Table 1 for the sample of 1,734 observations. Consistent with the literature on NPs, a relatively high mean for %WOB of 42.731% is reported in Table 1 (Lanfranchi & Narcy, 2015; Ward & Forker, 2017). Lower loan losses are associated with trade association monitoring (p ≤ .01), deprivation (p ≤ .05), size (p ≤ .01), and age (p ≤ .01). The negative pairwise correlation noted between loan losses and the deprivation measure (p ≤ .05) is contrary to that hypothesized. Finally, board size is positively associated with loan losses (p ≤ .01). However, none of these correlations control for other confounding factors.

Descriptive Statistics and Pairwise Correlations.

Note. Loan losses is the Registrar’s allowance for loan losses/gross loans × 100; %WOB is the percentage of women on the board; Male-dominant boards is a categorical variable coded 1 where the %WOB is less than 33.33%, 0 otherwise; Diversified boards is a categorical variable coded 1 where the %WOB is greater than 33.33% but less than 66.67%, 0 otherwise; Female-dominant boards is a categorical variable coded 1 where the %WOB is greater than 66.67%, 0 otherwise; MDM is a continuous measure of locality multiple deprivation. Size is the natural log of total assets; Age is the natural log of age from registration with the Registrar for credit unions; Board size is the number of directors on the board. Sample size: 1,734 observations from 182 credit unions. WOB = women on the board; MDM = multiple deprivation measure.

p ≤ .10. **p ≤ .05. ***p ≤ .01.

Monitoring Bundle

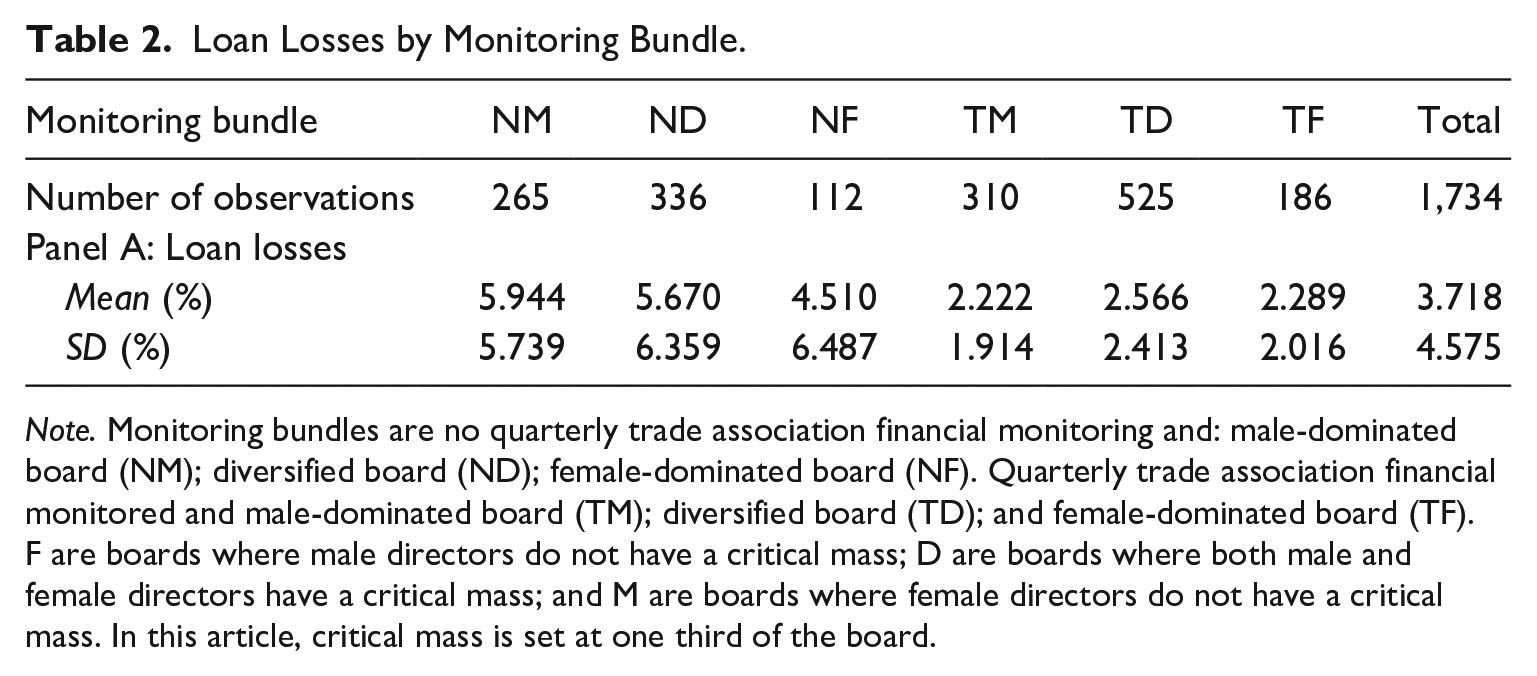

Table 2 presents loan losses across each bundle combination. The mean loan losses for the sample are 3.718%. The best performing bundle combination with the lowest loan losses is TM (mean, 2.222%) and the least effective is NM (mean, 5.944%). The average loan losses and variances in loan losses in bundle combinations with T are smaller to those reported in bundle combinations with N. When the loan losses for each bundle combination are compared with each other, statistically significant differences are detected for all bundle combinations other than NM and ND, and TM and TF (untabulated).

Loan Losses by Monitoring Bundle.

Note. Monitoring bundles are no quarterly trade association financial monitoring and: male-dominated board (NM); diversified board (ND); female-dominated board (NF). Quarterly trade association financial monitored and male-dominated board (TM); diversified board (TD); and female-dominated board (TF). F are boards where male directors do not have a critical mass; D are boards where both male and female directors have a critical mass; and M are boards where female directors do not have a critical mass. In this article, critical mass is set at one third of the board.

Estimation Results

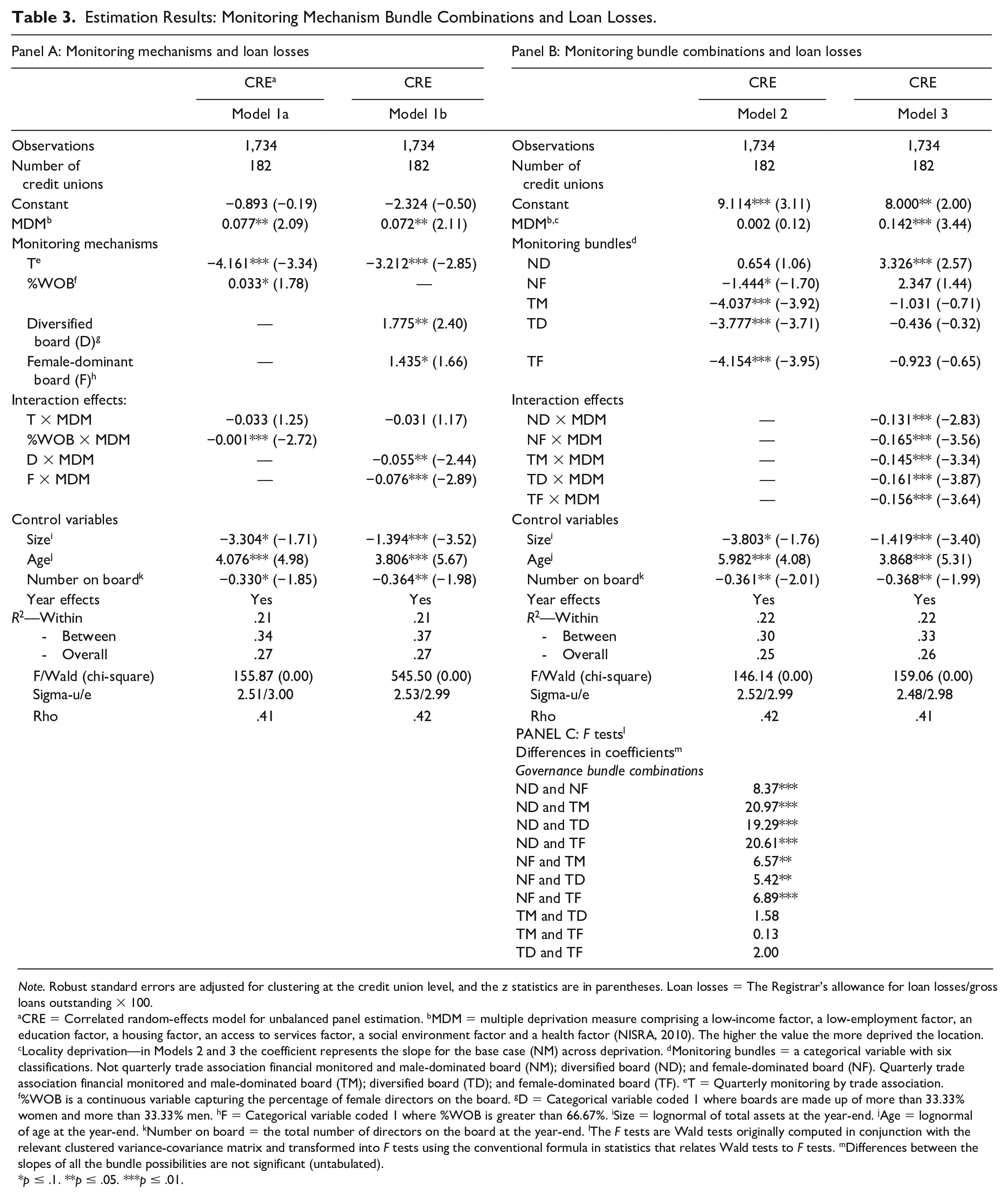

CRE results are presented in Panels A and B of Table 3. Panel A presents the estimates for two variants of Model 1. The first column of Table 3 reports the specification using the %WOB measure (Model 1a), whereas the second reports the specification using the three categorical variables: M, D, and F (Model 1b). Panel B presents the findings for Models 2 and 3, which investigate the relationship between bundle combinations of different levels of trade association financial monitoring (N, T) and female board representation (M, D, F), MDM, and loan losses. The test statistics for the differential effects of bundle combinations on loan losses are relative to the base group bundle combination NM in Models 2 and 3. In addition, F tests are reported in Panel C to determine if the estimated pairwise differences between the monitoring bundle combinations in their effects on reported loan losses are statistically significant.

Estimation Results: Monitoring Mechanism Bundle Combinations and Loan Losses.

Note. Robust standard errors are adjusted for clustering at the credit union level, and the z statistics are in parentheses. Loan losses = The Registrar’s allowance for loan losses/gross loans outstanding × 100.

CRE = Correlated random-effects model for unbalanced panel estimation. bMDM = multiple deprivation measure comprising a low-income factor, a low-employment factor, an education factor, a housing factor, an access to services factor, a social environment factor and a health factor (NISRA, 2010). The higher the value the more deprived the location. cLocality deprivation—in Models 2 and 3 the coefficient represents the slope for the base case (NM) across deprivation. dMonitoring bundles = a categorical variable with six classifications. Not quarterly trade association financial monitored and male-dominated board (NM); diversified board (ND); and female-dominated board (NF). Quarterly trade association financial monitored and male-dominated board (TM); diversified board (TD); and female-dominated board (TF). eT = Quarterly monitoring by trade association. f%WOB is a continuous variable capturing the percentage of female directors on the board. gD = Categorical variable coded 1 where boards are made up of more than 33.33% women and more than 33.33% men. hF = Categorical variable coded 1 where %WOB is greater than 66.67%. iSize = lognormal of total assets at the year-end. jAge = lognormal of age at the year-end. kNumber on board = the total number of directors on the board at the year-end. lThe F tests are Wald tests originally computed in conjunction with the relevant clustered variance-covariance matrix and transformed into F tests using the conventional formula in statistics that relates Wald tests to F tests. mDifferences between the slopes of all the bundle possibilities are not significant (untabulated).

p ≤ .1. **p ≤ .05. ***p ≤ .01.

Deprivation, monitoring mechanisms, and loan losses

Evaluating H1, given the use of the interaction effects in the model estimated in Table 3, requires the computation of the marginal effect of loan losses with respect to MDM. These are calculated using the relevant estimates from Model 1a in conjunction with the average values for T and %WOB from Table 1. The resultant point estimate is computed as 0.015, that is, 0.077 – (0.033 × 0.589) – (0.001 × 42.731). The corresponding asymptotic t ratio for the point estimate of this marginal effect is computed to be 0.00 (p = .957). Therefore, H1, which predicts a positive association between MDM and loan losses is rejected by the data in this case.

Trade association financial monitoring (T) results in lower loan losses, which is consistent with H2a. Using the estimates for Model 1a, the relevant estimated impact effect is computed to be −5.064 (p ≤ .01). 5 Therefore, ceteris paribus, for credit unions with T monitoring, loan losses are 5.064% points lower than credit unions with N at the average level of MDM. The estimated effect for the interaction between the trade association and MDM (i.e., T × MDM) in Model 1a is not found to be statistically significant, thus confirming H2b.

H3a is rejected using Model 1a estimates, as no statistically significant association between %WOB and loan losses is detected when the overall marginal effect is computed. 6 H3b is also rejected using Model 1b estimates to determine the impact effect on loan losses of F and D relative to M. Although credit unions (categorized as F) have lower loan losses relative to the base group in estimation M (−0.646% points lower), the estimated difference is just outside a conventional significance threshold of 10% when using the interaction effects. 7 D credit unions have higher loan losses relative to M credit unions (0.269% points higher). However, the impact effect difference is not found to be statistically significant. 8 Consistent with H3c, %WOB moderates the positive association between MDM and loan losses. The estimate for the interaction term, %WOB × MDM, is found to be negative and statistically significant (Model 1a, coefficient −0.001, p ≤ .01). The results for the interaction terms, D × MDM and F × MDM, in Model 1b confirm the moderating effect of female board representation on the association between MDM and loan losses.

Bundle effects

In Model 2, credit unions with an NM bundle provide the base category in estimation. The loan losses of credit unions with T bundle combinations (TM, TD, and TF) are significantly lower relative to the base case as indicated by the negative estimated coefficients reported (Panel B: TM, −4.037, p ≤ .01; TD, −3.777, p ≤ .01; TF, −4.154, p ≤ .01). In addition, credit unions with an NF bundle have significantly lower loan losses relative to credit unions with an NM bundle (Panel B: NF, −1.444, p ≤ .10). Finally, as reported in Panel C, F tests reveal significant differences in the first seven pairwise comparisons between the bundle combinations ND and NF when compared with the other bundle combinations.

Following Oh et al. (2018), complementary and substitutive effects are investigated by identifying and matching loan loss values for (NM) and high (TF) monitoring bundle combinations and determining the respective marginal benefit (loss). The condition for complementary and substitutive relationships, using the estimates from Model 3, can be expressed as follows: Complementary:

Reduction in loan losses (αNF – αNM) < Reduction in loan losses (αTF – αTM)

Substitutive:

Reduction in loan losses (αNF – αNM) > Reduction in loan losses (αTF – αTM)

Note: Bundles containing T, N, F, and M are identified for illustrative purposes.

The board dynamics literature also suggests that board behavior is influenced by the relative proportions of men and women on the board; hence, the analysis extends to investigate the respective marginal benefit (loss) from bundle combinations with D boards relative to those with F and M boards where the same conditions as above are tested using different combinations of the bundle.

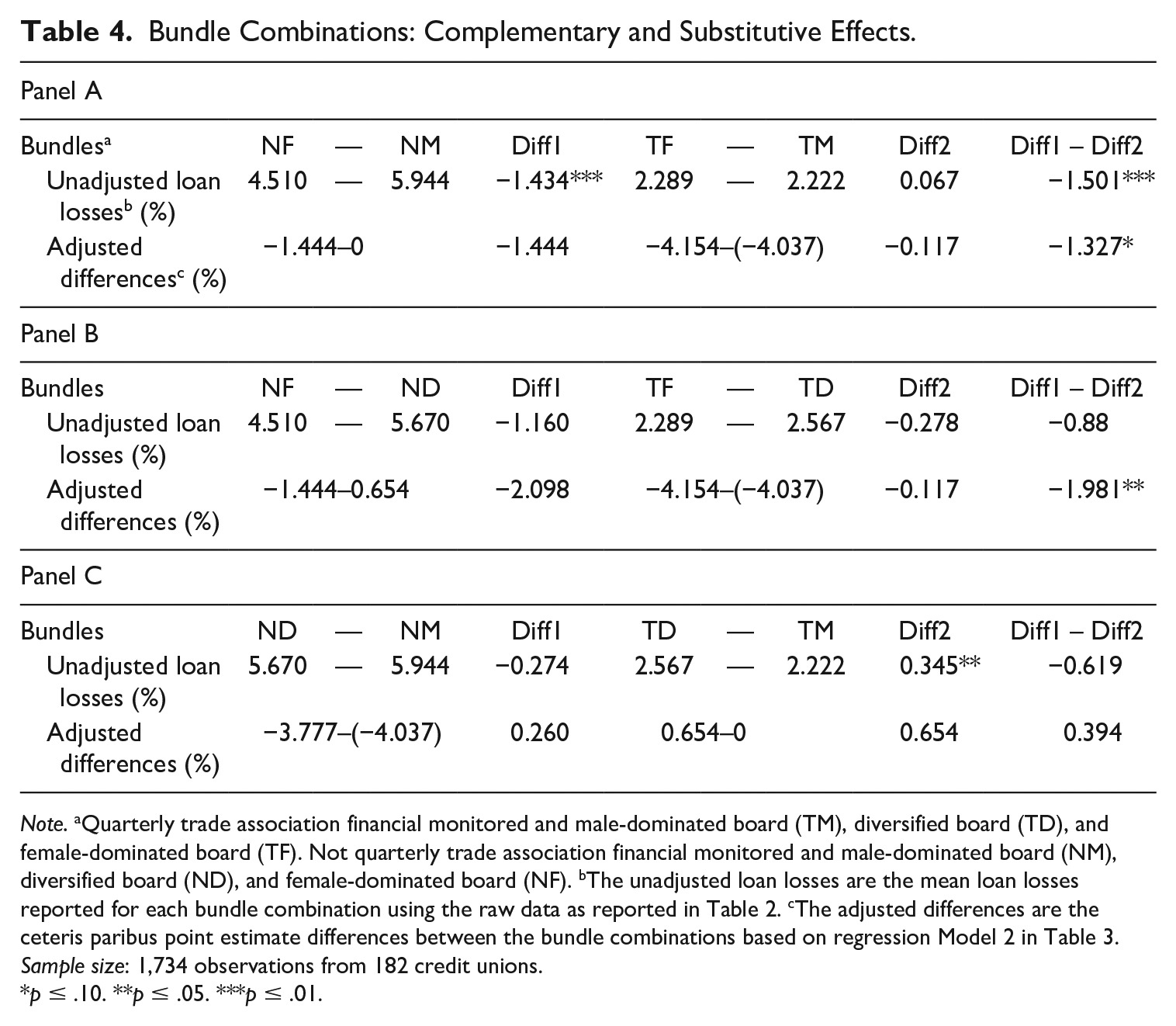

As a prelude to these econometric tests, the differences in the raw data reported from Table 2 are examined in Table 4. Compared with NM bundle combinations, loan losses in credit unions with NF bundle combinations are 1.434% points lower (p ≤ .01), and loan losses in credit unions with TF bundle combinations are 0.067% points higher than in those with TM bundle combinations (Panel A: Diff2). Moreover, the difference-in-difference between these sample average loan loss differences is found to be statistically significant (Panel A: Diff1 – Diff2, −1.501% points, p ≤ .01).

Bundle Combinations: Complementary and Substitutive Effects.

Note. aQuarterly trade association financial monitored and male-dominated board (TM), diversified board (TD), and female-dominated board (TF). Not quarterly trade association financial monitored and male-dominated board (NM), diversified board (ND), and female-dominated board (NF). bThe unadjusted loan losses are the mean loan losses reported for each bundle combination using the raw data as reported in Table 2. cThe adjusted differences are the ceteris paribus point estimate differences between the bundle combinations based on regression Model 2 in Table 3. Sample size: 1,734 observations from 182 credit unions.

p ≤ .10. **p ≤ .05. ***p ≤ .01.

We now formally test the two propositions above using the relevant econometric coefficient estimates obtained from Model 3. The difference-in-difference is found to be negative at −1.327% points—that is, −1.444 – (−0.117)—and statistically significant with an asymptotic t ratio of −1.71 (p = .087). This confirms a substitutive effect and is consistent with H4a.

A similar approach is used to determine whether a complementary or substitutive effect exists between credit unions with an ND bundle (low) relative to credit unions with a TF bundle (high; Table 4: Panel B) and between credit unions with an NM bundle (low) relative to credit unions with a TD bundle (high). As noted in Panel B, loan losses in credit unions with an NF bundle are lower to those reported for credit unions with an ND bundle (Diff1: 1.160% points lower) and they are lower in credit unions with a TF bundle relative to credit unions with a TD bundle (Diff2: 0.278% points lower). The difference is significant when the point estimates reported in Model 3 (Table 3) are compared (Table 4, Panel B, Diff1 – Diff2, 1.981% points, p ≤ .05), indicating a substitution effect. Finally, in Panel C, there is no significant difference in the differences between the loan losses reported in credit unions with the bundle combinations ND and NM relative to those with TD and TM bundle combinations when the raw data and the adjusted point estimates are tested. The results confirm a substitution effect for T and F consistent with H4b.

Bundle interaction effects

Loan losses in credit unions with an NM bundle are positively associated with MDM (Table 3, Panel B, Model 3, coefficient 0.142, p ≤ .01). The estimates for the interaction effects show that when the bundle contains F, D, or T, there is a moderating effect of MDM on loan losses, relative to credit unions with an NM bundle. Moreover, the size, magnitude, and significance of the differences in the slopes between the five other bundle combinations and the NM bundle are broadly similar as reflected by the estimated interaction effects (Table 3: Model 3). To assess the economic impact of MDM, the range value of 81.25 is selected for illustrative purposes (the maximum MDM value is 83.33 and the minimum is 2.08). Thus, credit unions with an NM bundle have loan losses that are 11.54% points (0.142 × 81.25) higher when the location has an MDM of 83.33 and credit unions with a TF bundle have loan losses that are 1.14% points ((0.142−0.156) × 81.25) lower relative to loan losses when MDM is 2.08. The results highlight the important role that bundle component choice plays in reducing loan losses in deprived localities.

Control variables

The results reported in Table 3 are as predicted. Large credit unions and credit unions with larger boards report significantly lower loan losses across all econometric models. Older credit unions report significantly higher loan losses. Finally, relative to the base year, 2002, loan losses reported in later years are significantly higher (untabulated).

Robustness testing

Endogeneity is a problem inherent in board studies (Pathan & Faff, 2013). To test for endogeneity of a board’s female composition, data on the percentage of female counselors on local government councils over the period 2002 to 2011 was hand-collected to create an instrumental variable (IV) to capture the extent of the accepted role of females within local communities. Credit union postcodes identified the relevant local council for each credit union. As a preliminary exercise, the percentage of female counselors is correlated with the %WOB of credit unions (0.19, p ≤ .01) and is not correlated with loan losses (−0.02, p = .43). On the basis of econometric testing, the instrument is found to be correlated with the potential problematic regressor (i.e., %WOB), rendering it a relevant instrument but orthogonal to the error structure determining credit union loan losses. The instrument is found to be statistically significant in the first stage regression, with the Wald transformed F test above the Stock–Yogo critical values (Stock & Yogo, 2005). Given the availability of a single instrument, we assess the orthogonality condition by including it in the loan loss equations and find it is statistically insignificant. Assuming it is a valid instrument, the use of the Hausman test reveals that the null of regressor exogeneity cannot be rejected in this case confirming the approach adopted in this study. Therefore, the %WOB is not endogenous with respect to loan losses.

To examine the potential impact of multicollinearity between age and size, the models were re-run with age and size included separately. To determine if the recent financial crisis had an impact, we included a dichotomous variable to capture the period before 2008 and after 2008, instead of separate year effects. In general, the results from these robustness tests portrayed similar directional relations with only minimal differences in statistical significance. The over-riding conclusions from the article remain unaltered by these robustness checks.

Discussion

The key findings are that monitoring mechanisms result in lower loan losses in credit unions, which is consistent with the prior literature. In an extension to this literature, this study provides more nuanced insights including that the effectiveness of different monitoring mechanisms varies relative to the type of monitoring mechanism, the environment, and in the presence of other monitoring mechanisms. Specifically, external trade association financial monitoring has a greater impact in reducing loan losses. This relationship is invariant when credit unions operate with higher levels of financial risk as captured by locality MDM. This finding lends support for the promotion of quarterly financial monitoring by an external regulator as is the case in the United Kingdom and the United States. However, quarterly financial monitoring by an external body is costly in terms of systems and manpower and may not be feasible in emerging economies, in start-up credit unions, and in small credit unions that do not have sufficient membership numbers to generate the economies of scale required to fund the cost.

Consistent with the findings of Chakrabarty and Bass (2014) for cost efficiency, variation in the effectiveness of female board representation in moderating the association between MDM and loan losses is evident. The results highlight that at low levels of MDM, boards with higher %WOB have higher loan losses compared with boards with low %WOB. However, this pattern is reversed when MDM is high. This suggests females have a comparative advantage over males when strategizing credit policy in credit unions in deprived locations when information asymmetry increases. An increased need for additional internal monitoring is satisfied by female board representation, possibly due to stronger links with community networks (Hillman et al., 2007). This result provides more nuanced understanding of the findings of Ward and Forker (2017), specifically, the positive association between female board representation and loan book quality is driven by the superior performance of women in credit unions in deprived localities and in those that are not subject to trade association monitoring.

The differential benefits of bundle combinations with different levels of the two monitoring mechanisms reveals that credit unions with the monitoring bundle (NM) have the highest loan losses. Moreover, the impact of a high monitoring mechanism (T or F) serves to reduce loan losses by more when the other mechanism in the bundle is low (N or M) relative to the impact reported when the other mechanism in the bundle is high (F or T). Thus, these monitoring mechanisms substitute for, rather than complement, each other to reduce loan losses.

The theoretical implications of the findings are that the assumption of independence for monitoring mechanisms should be revised to a bundle approach that considers the costs and benefits of different levels of monitoring mechanism. Although trade association monitoring is associated with lower loan losses, a lower cost internal monitoring mechanism—female board representation—is found to substitute for this more costly mechanism, particularly when credit unions are in deprived locations. Therefore, this study extends theory on the scope of a “bundle approach” by examining in-depth the effect of different levels of two monitoring mechanisms to the context of NP organizations. Moreover, it offers important implications for regulatory design. In particular, a flexible approach is supported to enable credit unions to select the bundle combination of monitoring mechanisms to best suit their environment. Guidance could promote female board appointments to critical levels in credit unions in deprived locations, particularly in the absence of trade association monitoring. The study also offers a potential explanation for the variation across the results in NP gender-based studies on the effectiveness of individual monitoring mechanisms on loan losses.

Limitations and Future Research

The study assumes that affiliation to a specific trade association in Northern Ireland results in stronger monitoring as this trade association undertakes quarterly financial analysis using financial ratios whereas the other credit unions are not subject to quarterly financial monitoring during this period. It is also possible, however, that other services provided by this trade association contribute to lower loan losses (Forker et al., 2014). The findings infer that female director appointments strengthen monitoring in more deprived localities. It is difficult to identify the explicit reason for this comparative advantage over boards that are male dominant. Research identifies a link among female board members, increased independence, and improved monitoring (Adams & Ferreira, 2009). However, we cannot confirm that lower loan losses noted in credit unions in deprived locations is a consequence of additional monitoring by females, as the study does not explicitly identify monitoring activity. Nevertheless, other reasons adduced in the literature support an explanation of a beneficial effect from female directors namely that females foster high levels of trust relationships with borrowers leading to fewer defaults (Beck et al., 2013) and that females have wider networks with the membership (Hillman et al., 2007) enabling them to obtain volunteers and to strengthen bonds that leads to fewer defaults. Finally, other factors that influence board performance that are not controlled for in this study, due to limits on data availability, are auditor quality, director experience, director education, director contacts, years of service on the board, and whether directors worked as a volunteer in the credit union beforehand (Themudo, 2009).

Conclusion

The recent financial crisis has impacted the financial services sector with more stringent regulation being introduced in many countries for financial institutions and a push toward standardization in the rules that apply across different organizational forms. The consequences of increased regulation for small, community, member-governed financial organizations are potentially serious, possibly resulting in closure, as public regulation and external compliance monitoring is costly, and many community organizations do not have the economies of scale to absorb the additional costs.

In general, the findings that choosing financial monitoring by trade association reduces loan losses provide support for financial regulation in credit unions. However, in the absence of trade association monitoring, credit unions with female-dominant boards have a moderating effect on loan losses as deprivation increases. An investigation of the effect of a bundle of different levels of external trade association financial monitoring and internal monitoring by female directors on loan losses report a substitutive effect. The findings provide support for a flexible approach to regulation designed to reduce loan losses in community-based financial institutions, such as credit unions. This evidence is particularly pertinent to the worldwide credit union movement, given the high levels of poverty and the profusion of small credit unions combined with the recent emphasis on increased public regulation and the adverse potential impact that it may have on outreach.

Footnotes

Acknowledgements

The authors acknowledge the excellent advice and suggestions received from the anonymous reviewers and the editor. Special thanks also to Jeffrey Wooldridge for assisting in the application of CRE. The authors, however, take full responsibility for any remaining errors. Finally, we thank participants for feedback at seminar presentations and conferences.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors are grateful to the Chartered Accountant Ireland Education Trust for funding in support of this study.