Abstract

Between 2021 and 2022, the inflation rate increased precipitously in North America and was higher than had been seen in decades (DeSilver, 2022). In this article, we use a stress process perspective to examine how older adults’ perceptions of changes in cost of living during this period of rapid inflation were associated with multiple measures of psychological distress. A stress process perspective suggests that perceptions of increases in cost of living are likely to act as an “anticipatory stressor” be creating a sense of threat to older adults’ abilities to obtain vital needs (Grace, 2021; Pearlin & Bierman, 2013), in turn creating greater psychological distress. Yet, a stress process perspective suggests that the consequences of financial stress may be weakened when individuals have a stronger sense of control over their lives in a process of “stress buffering” (Pearlin, 1999). Taking buffering by sense of control into account therefore shows how perceptions of increases in cost of living may be especially detrimental to the well-being of older adults who lack a vital cognitive resource to facilitate management of this anticipatory stressor.

To address these questions, we analyze a two-wave national panel study of Canadian older adults, fielded in the Fall of 2021 and again in the Fall of 2022. We examine how perceptions of an increase in cost of living over the year are associated with multiple aspects of psychological distress while taking antecedent selection factors into account, and further consider whether mastery creates contingencies in these associations. This research therefore contributes to the study of the social context of mental health in later-life by not only examining how the individual experience of an increase in cost of living during a period of rapid inflation may shape psychological distress among older adults, but also variations in these mental health consequences based on psychological coping resources.

Background

Individual perceptions of inflation are not entirely subjective, and instead are a clear consequence of direct experiences with inflation. As Shiller (1997) describes, “because shopping, and thereby noticing prices, is an everyday activity for ordinary people, thinking about prices is also a major part of people’s thinking, and the subject of inflation is one of great personal interest for most people” (p. 16). People are highly attuned to inflation because inflation is related to common activities of obtaining needs and wants. Nevertheless, differences in social positions and experiences may affect personal experiences of inflation (Hayo & Neumeier, 2022; Ranyard et al., 2008). Particularly relevant to the current research is that expenditure patterns and emphases vary with age (Basu, 2005; Bernicke, 2005; Blanchett, 2014), leading to inflation experiences in later-life that may vary from the official inflation rate and between different households (Basu, 2011; Kalwij et al., 2018; Nie & Gautam, 2020). Consequently, a macro-economic measure such as inflation does not track individual experiences of inflation, particularly among older adults. It is therefore critical to examine individual experiences of changes in cost of living when seeking to understand the consequences of inflation among older adults.

Within the stress process model, perceptions of increases in the cost of living may be considered a form of “anticipatory stressors,” which “are the worries that people have about the future that have not occurred—and may never—but which nevertheless loom as potential threats” (Grace, 2021, p. 22). Although much research on economic stress has shown detrimental effects of ongoing financial stressors (Guan et al., 2022), far less attention on research among older adults has been paid to anticipated financial problems. We argue, however, that the sense that one is experiencing a higher cost of living is likely to act as an anticipatory stressor through multiple mechanisms. Increases in cost of living represent a threat to one’s ability to obtain necessities, which is inherently stressful (Bierman, 2014). Anticipatory stress may also lead individuals to begin preparation for future hardships (Scott et al., 2019). Consequently, perceptions of increases in cost of living may also create changes in savings and spending behaviors (Hayo & Neumeier, 2022), and curbs on future plans and desired acquisitions can contribute to emotional upset. Similarly, the potential for financial shortfalls may lead to desistence in engagement in leisure activities (Silva, 2022), which, in addition to being distressing in and of itself, may also lead to a loss of social connection and loneliness that is associated with greater psychological distress (Park et al., 2013). In support of these arguments, Grace (2020) showed that college students’ anticipatory stress regarding economic security was associated with greater depressive symptomology, while additional research shows that greater general anticipatory stress can harm psychological functioning in older adults (Hyun et al., 2019). Thus, although there is limited research on financial anticipatory stress and mental health among older adults, these findings support the potential role of perceptions of increases in cost of living as a detrimental influence on older adults.

Despite evidence supporting an association between perceived increases in cost of living and psychological distress, prior applications of the stress process model underscore that several classes of antecedent factors may contribute to spuriousness in this association (Chai et al., 2020; Pudrovska et al., 2005). One set of factors includes pre-existing physical and mental health conditions, which can both lead to subsequent distress and increase risk of escalation in one’s financial burdens (Guan et al., 2022). An additional class of antecedent factors is financial insecurity, such as financial strain and low income, which may contribute to psychological distress (Koltai et al., 2018), and also enhance sensitivities to even small changes in cost of living. A third is low levels of mastery, with mastery referring to a general sense of control over life events and outcomes (Badawy & Schieman, 2020). Low levels of mastery may not only engender psychological distress in later-life (e.g., Morin & Midlarsky, 2016), but individuals who feel powerless to affect their lives may engage in less effective coping strategies (Ben-Zur, 2002), thereby inhibiting actions that deter increases in cost of living as inflation rises. Within this research, we therefore also examine the extent to which taking these three sets of factors into account eliminates associations between perceptions of increases in cost of living and psychological distress.

A stress process perspective further emphasizes that the effects of stress will vary based on psychological resources (Pearlin, 1999), with mastery identified as a particularly important buffering resource (Pearlin & Bierman, 2013). Mastery tends to be pivotal as a stress buffer because individuals with greater mastery are imbued with more of a sense that they can affect their immediate circumstances and broader life outcomes (Pearlin, 2010), which then weakens the threat posed by external stressors (Bierman & Kelty, 2014). Consequently, individuals with lower levels of mastery are likely to feel a heightened distress because changes in cost of living will be seen as a threat whose consequences they are powerless to mitigate or avoid (Ross, 2011). Conversely, individuals with higher levels of mastery will not only feel less threatened by perceptions of increases in cost of living, they will also be more motivated and persistent in seeking out solutions that minimize challenges caused increases in cost of living (Ben-Zur, 2018; Eshbaugh, 2010). Taking buffering by mastery into account therefore will help to show the circumstances under which perceptions of increases in cost of living may be most potent for psychological distress.

Methods

Data

Data are derived from the Caregiving, Aging, and Financial Experiences (CAFE) study, a national survey intended to examine social conditions and well-being among older Canadians. Data were gathered by the study authors in cooperation with the Angus Reid Forum, a Canadian national survey research firm that maintains an ongoing national panel of Canadian respondents from which nationally representative samples can be drawn. The first wave of the CAFE survey was gathered in late September and early October of 2021 as an online survey conducted among a representative sample of 4,010 Canadians between age 65 and 85. The response rate was 56%. Following baseline data collection, the research team was provided with statistical weights according to the most current age, gender, and region Census data to ensure a nationally representative sample of older Canadians. The follow-up was conducted in late September and early October of 2022, approximately a year later. In total, 2,420 respondents were recontacted, for a 60% retention rate. Analytic methods used to address attrition are described in the plan of analysis.

Focal Measures

Because all scales are derived from pre-existing measures, their individual items are not described in the text and can instead be found in an online appendix.

Subjective evaluation of the change in cost of living was measured at follow-up and was adapted from a measure established by Narisada et al. (2021). Respondents were asked, “How has your experience of the cost of living changed in the past year?” Response choices were as follows: “Gotten much worse,” “Gotten somewhat worse,” “Stayed the same,” “Gotten somewhat better,” and “Gotten much better.” Examination of the raw responses for this measure showed a small portion of respondents indicating either of the got better categories. Responses were therefore recoded to indicate a high increase in cost of living in terms of “much worse,” or a moderate increase in terms of “somewhat worse,” with the combination of the remainder of responses used as the reference group in all analyses.

Psychological distress was measured based on established scales of depression (Karim et al., 2015), anxiety (Spitzer et al., 2006), and anger (Fuqua et al., 1991). Separate principal components analyses indicated one eigenvalue above 1 for each scale at baseline, accounting for 55% of the variance for the depression items, 66% of the variance for the anxiety items, and 76% of the variance for the anger items. At baseline, Cronbach’s alpha for the depressive symptoms scale was 0.88, for anxiety was 0.90, and for anger was 0.83

Self-rated health is a comprehensive indicator of health among older adults (Sieber et al., 2020). Respondents were initially asked to rate their health on a five-level response category: (1) poor, (2) fair, (3) “good,” (4) “very good,” and (5) “excellent.” In order to take non-linearities in associations with distress into account, responses of “fair” and “poor” were combined into a reference category and compared to a moderate health category based on responses of “good” and a strong health category based on responses of “very good” and “excellent.”

Financial insecurity was measured at baseline using income and a scale of financial strain because income indicates recent financial inflows, whereas financial strain indicates difficulties in affording basic needs (Bierman, 2014; Koltai et al., 2018). The rightward skew of income was addressed by using the natural log of responses in the analyses. Financial strain was measured based on a three-item scale from Bierman et al. (2021). A principal components analysis of these items indicated one component with an eigenvalue above 1 that accounted for 77% of the variance in the items, with a Cronbach’s alpha of 0.85. The mean of responses to these three items was used as the measure of financial strain.

Mastery was measured at baseline with a five-item version of Pearlin’s mastery scale previously used in the study of financial stress and mental health in older adults (Pudrovska et al., 2005). A principal components analysis of these items indicated one component with an eigenvalue above 1 that accounted for 61% of the variance in the items, with a Cronbach’s alpha of 0.84. The mean of responses to these fives items was used as the measure of mastery. Mastery is mean-centered in all analyses to enhance interpretation of statistical interaction terms.

Covariates

Covariates used in the statistical analyses focus on background social statuses that may predict placement into change in cost of living and psychological distress. These include gender, education, age, visible minority status, whether retired, and whether living with a romantic partner. For gender, respondents could identify as a man or woman, but could also choose to self-describe. No respondent chose to self-describe, and gender was therefore coded as a dichotomous variable (0 = men, 1 = women). Education was measured as a set of dichotomous indicators, in which post-high school (some college/trade school or university), graduated from trade school, and university undergraduate degree or greater were contrasted to a high school degree; less than 3% of the raw sample at baseline had less than a high school degree, and these respondents were included with the comparison category. Age was measured in years. A common approach to race in Canadian research is a general “visible minority” category (Little, 2016), and in keeping with this approach, visible minority status was a dichotomous variable based on the question, “Would you say you are a member of a visible minority here in Canada (in terms of your ethnicity/race)?” with affirmative answers coded as 1. Dichotomous variables also indicated whether respondents were currently retired and were currently married or living with a romantic partner in a common-law relationship.

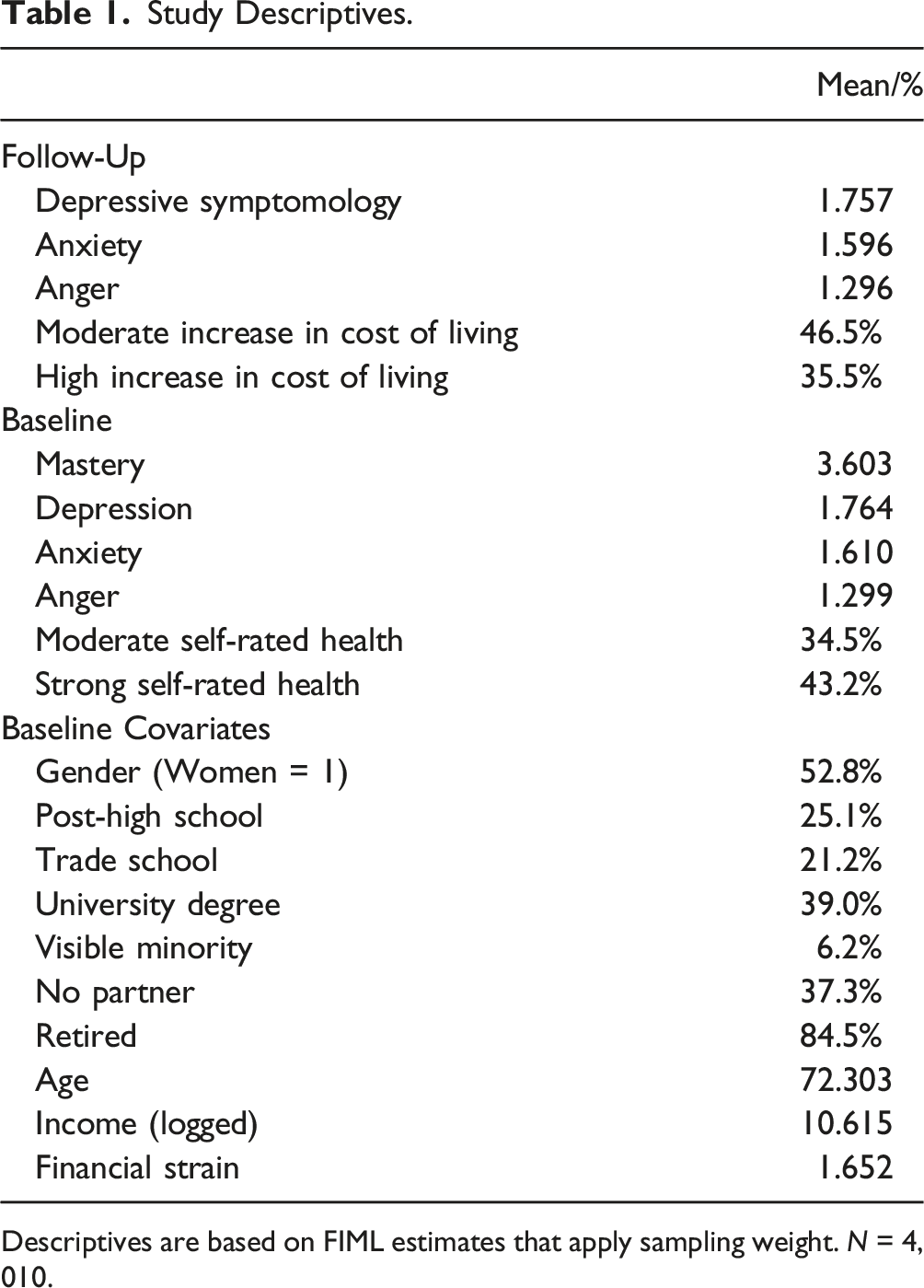

Study Descriptives.

Descriptives are based on FIML estimates that apply sampling weight. N = 4,010.

Plan of Analysis

The main analyses utilize multiple regression models based on full-information maximum likelihood estimation (FIML). FIML uses all of the information that is available from each case (Enders, 2010), thereby accounting for data missing due to sample attrition and other factors. As a result, our final analytic sample retains all 4,010 baseline respondents. Although each of our outcome variables was somewhat right-skewed (skewness = 1.05 for depression, 1.45 for anxiety, and 1.99 for anger), analyses utilized heteroskedastic-resistant standard errors, thereby addressing the possibility that skewness in the dependent variables could affect significance tests.

Analyses of each distress outcome is examined using the same set of models. First, the association between perceptions of an increase in cost of living and the outcome is estimated with background controls. Since this is the first study that, to our knowledge, assesses the relationship between perceptions of increases in cost of living due to inflation and psychological distress using longitudinal data, we took steps to rule out the possibility of observing a spurious relationship due to pre-existing selection factors. The next three models therefore introduce controls for baseline financial insecurity, mastery, and then baseline self-rated health and psychological distress. Although research shows that health problems can increase financial burdens (Richard et al., 2018), this order was chosen because longitudinal analyses suggest that the stronger association is one in which financial strain is antecedent to well-being (Chai et al., 2020), with financial strain tending to precede mastery (Klug et al., 2021). Thus, first controlling for baseline health conditions could obscure the contributions of antecedent financial insecurity and mastery to spuriousness. The last model then tests interactions between mastery and the cost of living indicators, which facilitates a test of the buffering role of mastery. Finally, we present a summary of the “semi-standardized coefficient with respect to y” (Long, 1997, p. 16; emphasis in original). The semi-standardized coefficients present group differences in units of standard deviations of the outcome, and can therefore be used to compare the strength of associations with perceived increases in cost of living across the distress outcomes.

Results

Depression

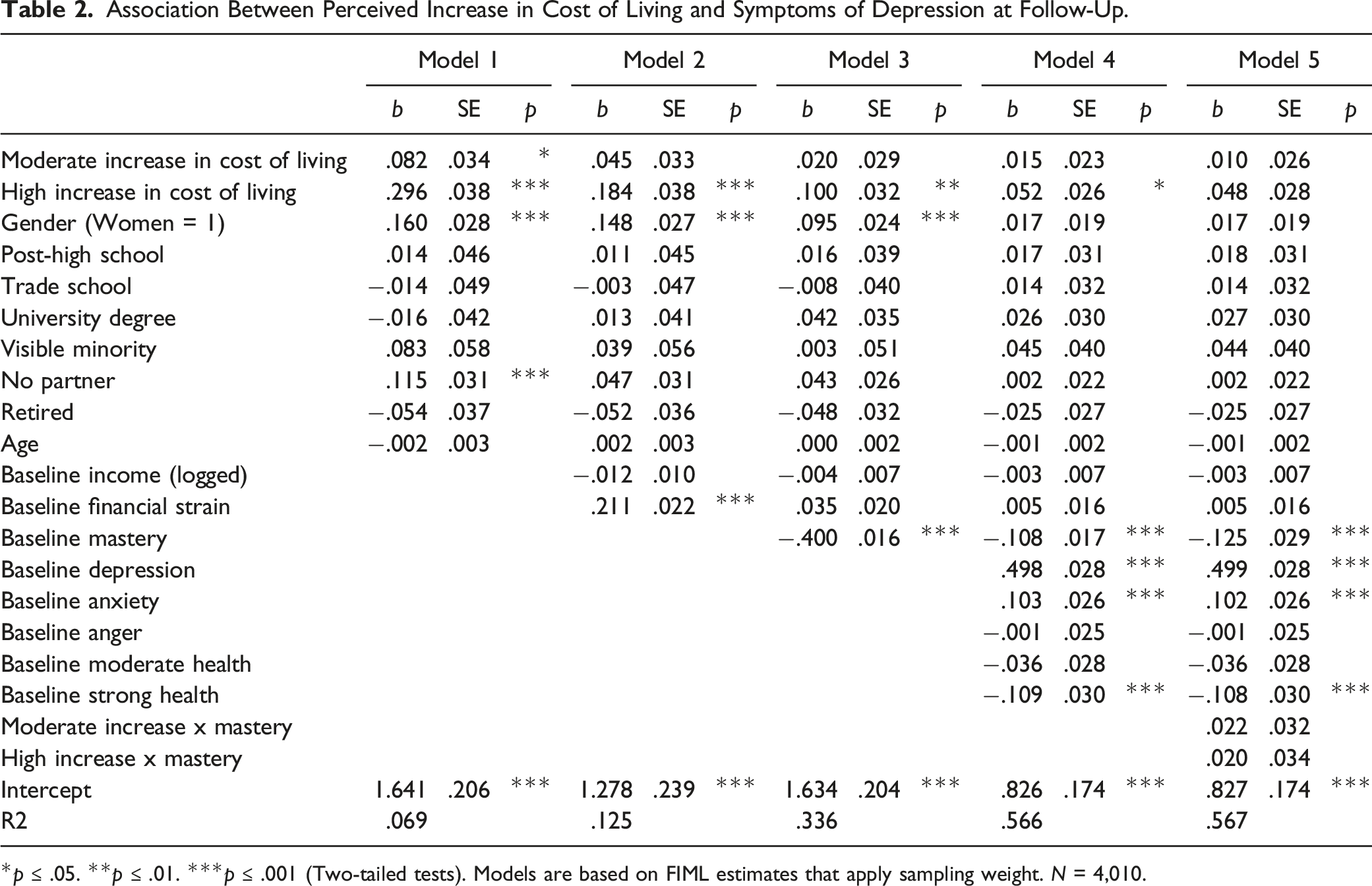

Association Between Perceived Increase in Cost of Living and Symptoms of Depression at Follow-Up.

*p ≤ .05. **p ≤ .01. ***p ≤ .001 (Two-tailed tests). Models are based on FIML estimates that apply sampling weight. N = 4,010.

Anxiety

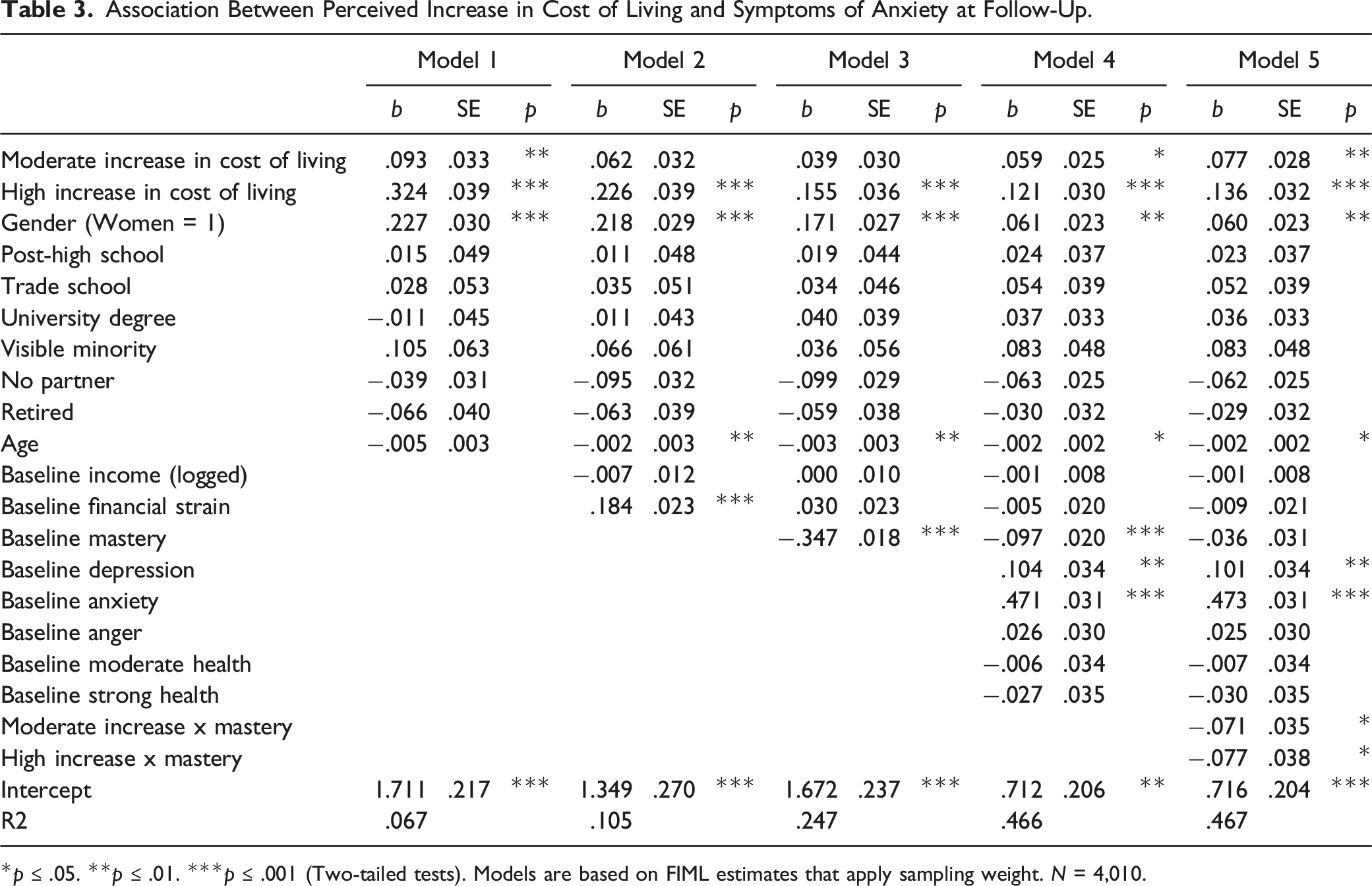

Association Between Perceived Increase in Cost of Living and Symptoms of Anxiety at Follow-Up.

*p ≤ .05. **p ≤ .01. ***p ≤ .001 (Two-tailed tests). Models are based on FIML estimates that apply sampling weight. N = 4,010.

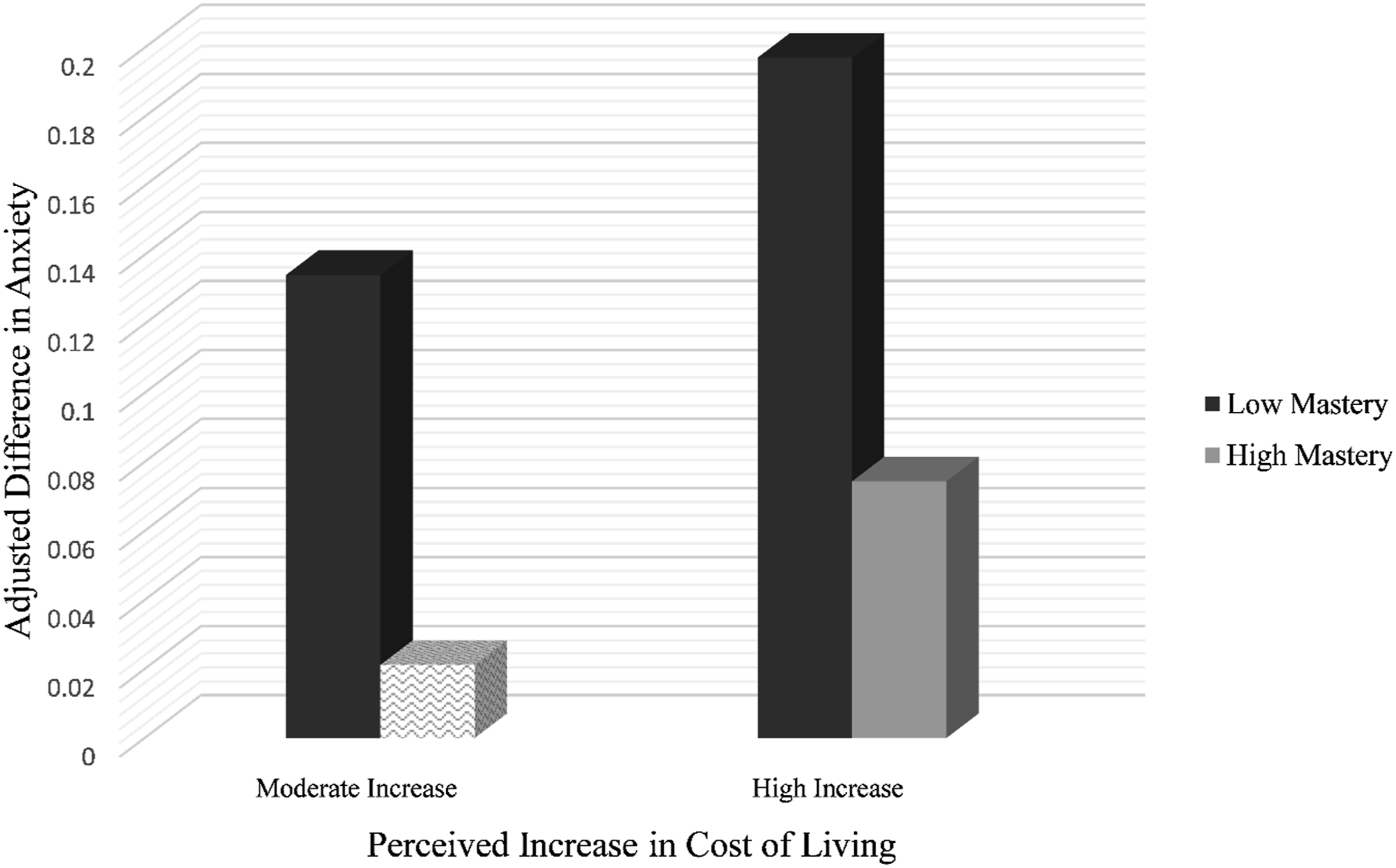

Model 5 shows significant interactions with mastery for both moderate and high increases in cost of living. The direction of the coefficients for these interactions is negative, indicating that higher levels of mastery weaken these associations in a pattern of stress buffering. Figure 1 illustrates this buffering pattern by using Model 5 to show the difference in mean levels of anxiety for moderate and high increases of perceived cost of living at approximately one standard deviation above and below the mean for mastery. Overall, for moderate perceived increases in cost of living, there is a significantly higher level of anxiety at a low level of mastery but not at a high level of mastery, in a clear illustration of stress buffering. For a high perceived increase in cost of living, partial stress buffering is shown because the difference in anxiety is weaker at a higher level of mastery than lower mastery, but a high increase in perceived cost of living is significantly associated with greater anxiety across levels of mastery. Adjusted differences in symptoms of anxiety at low and high levels of mastery. Association Between Perceived Increase in Cost of Living and Symptoms of Anger at Follow-Up. *p ≤ .05. **p ≤ .01. ***p ≤ .001 (Two-tailed tests). Models are based on FIML estimates that apply sampling weight. N = 4,010.

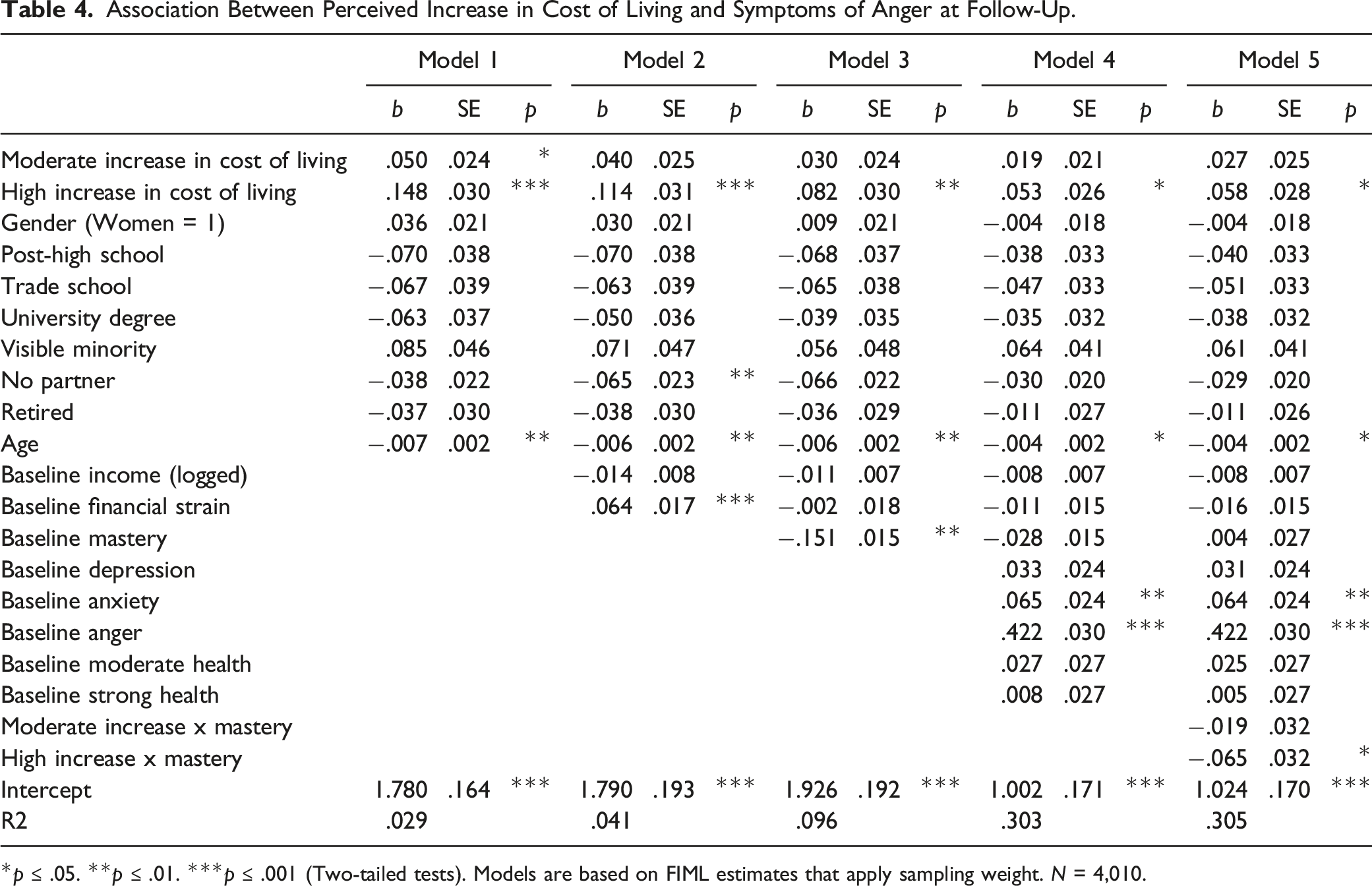

Anger

Table 4 examines the association between perceptions of an increase in cost of living and anger at follow-up. Model 1 shows that, independent of background social statuses, moderate and high perceived increases are both associated with significantly higher levels of anger. Controlling for financial insecurity in Model 2 in turn reduces the coefficient of a moderate perceived increase in cost of living approximately 20% and this difference in anger is no longer statistically significant. The difference in anger at a high perceived increase in cost of living is reduced approximately 25% between Model 1 and Model 2, but this difference remains significant. Model 3 shows that controlling for baseline mastery reduces the coefficient for a high increase in cost of living approximately 30% from Model 2, and the level of significance decreases from p < .001 to p < .01. Model 4 shows that controlling for psychological distress and self-rated health reduces the coefficient for a high increase in cost of living 35% from Model 4, with the significance in this difference further moving from p < .01 to p < .05. Model 5 further shows a significant interaction between mastery and high perceived increase in cost of living, with the negative direction of this coefficient indicating a buffering effect. Ancillary analyses indicated a pattern similar that shown in Figure 1, with the adjusted difference in anger for a high perceived increase in cost of living significant and positive at a low level of mastery (b = .110, p < .05), but not at a high level of mastery (b = .006, p > .05). For individuals with a high perceived increase in cost of living, then, anger was significantly greater at a low level of mastery but not at a high level of mastery, showing a clear pattern of stress buffering. For older adults with a moderate perceived increase in cost of living, though, taking antecedent sources of spuriousness into account negated associations with anger.

Strength of Associations

All semi-standardized differences include a full set of controls. For a large increase in cost of living, the semi-standardized difference in depression was .081, for anxiety was .178, and for anger was .110. When taking contingencies based on mastery into account, the difference in anxiety for respondents reporting a large increase in cost of living at a low level of mastery was .289 and at a high level of mastery was .109; for anger, this difference was .227 at low mastery and not significant at a high level of mastery. For respondents reporting a moderate increase in cost of living, the overall semi-standardized difference in anxiety was .087, but at low mastery was .196 and not significant at high mastery. We therefore see much stronger differences in anxiety and anger—especially at lower levels of mastery—than for depression.

As a guideline for judging the strength of these differences, we note that the semi-standardized coefficient is similar to Hedges’ g, for which a recent extensive analysis ranked effects sizes in the gerontological literature and indicated that a value of .16 was at the 25th percentile and .38 were at the 50th percentile (Brydges, 2019). The difference for depression is therefore generally weak in comparison to much of the gerontological literature. For anxiety and anger at low levels of mastery, though, we argue that these differences are notable in part because they can interpreted as roughly stronger than 25% of the gerontological literature; additionally, the strength of these differences was established over only a year, and then when taking prior levels of multiple forms of distress and economic standing into account. At high levels of mastery, though, associations with anxiety and anger can generally be considered weak in the context of broader patterns of findings in gerontology.

Discussion

Between 2021 and 2022, North America experienced a historic increase in the inflation rate. Older adults’ perceptions of changes in their personal cost of living during this time period were likely to be an important influence on psychological distress by acting as an anticipatory stressor. Our analyses of a national panel study of older adults showed that perceptions of a large increase in cost of living were associated with dimensional measures of depression, anxiety, and anger, even after adjusting for antecedent sources of spuriousness. That we observe adverse effects of reports of changes in cost of living across multiple outcomes serves to demonstrate how macroeconomic shifts can reach into individual lives to broadly shape mental health. People must make individual choices to obtain wants and needs in the context of the structure of the larger economy, and rapid changes in this structure can result in perceptions of a tightening on individual constraints that amplifies psychological distress.

Nevertheless, the degree to which the focal associations were substantially negated by taking into account antecedent sources of spuriousness should also be acknowledged. Controlling for prior levels of financial strain, mastery, and psychological distress all reduced associations between perceived increases in cost of living and distress—especially for moderate increases in cost of living. The extent to which antecedent factors appeared to contribute to spuriousness underscores that perceptions of increases in cost of living in later-life need to be considered by gerontologists as based in prior economic and psychological factors. Cross-sectional analyses of the influence of perceptions of inflation that do not consider pre-existing financial and affective states are likely to present an exaggerated depiction of the mental health consequences of these perceptions.

The focal associations were also substantially stronger for anger and anxiety than depressive symptoms. Previous research suggests that anxiety and anger constitute active forms of distress, while depression is a passive form of distress (Ross & Mirowsky, 2008). It therefore appears that that the individual experience of inflation is more clearly related to active aspects of distress. Greater consequences for activation may in part be due to a sense of increasing costs requiring people to monitor the state of their finances and fluctuations in prices, thereby fomenting a state of alertness. Anger may also result when people experience stressors that are identifiably rooted in the broader economic system, especially when blame can be located in leaders and a system that are beyond individual control. This pattern of findings therefore suggests that research on financial stress in later-life should more commonly examine multiple forms of distress outcomes, and also begin to more elaborately theorize and test the mechanisms that may create distinctions across forms of distress.

The basis of the study in the stress process perspective further prompted examination of the role of mastery in buffering the consequences of perceived changes in cost of living. Mastery buffered associations between a high perceived increase in cost of living and both anxiety and anger, as well as between a perceived moderate increase in cost of living and anxiety, but did not serve as a buffer in the case of depression. The stronger associations between perceptions of cost of living and both anxiety and anger, when compared to weaker associations with depression, suggests that perceptions of cost of living were more activating than enervating. Consequently, there was a minimal effect on depression to buffer, leading to a lack of statistical moderation by mastery when depression was the outcome. Conversely, perceived increases in cost of living led to activated forms of distress, but were not as activating when a high sense of control led people to see these increases as less overwhelming and more amenable to problem-solving (Eshbaugh, 2010; Koltai et al., 2018). Hence, even times of broad economic adversity may have variegated consequences for older adults’ mental health, due in part to differences in psychological resources that older adults possess.

The buffering effects of mastery are especially important to consider because a substantial literature indicates that mastery is not only a matter of individual differences, but mastery also accrues more to individuals with advantages in positions of power, privilege, and prestige (Mirowsky & Ross, 2007; Pearlin, 2010; Thomas Tobin et al., 2021). While additional personal factors may also influence mastery, the tendency for greater mastery to cluster among more advantaged social positions shows how inflationary experiences may differ in their individual outcomes due to psychological resources that are accrued in part through structural advantages.

Several weaknesses in this study should be noted. First, as a study of Canadian older adults, it remains to be seen whether or how these associations will replicate in other national contexts with different financial support systems for older adults. Second, this study examined overall changes in cost of living. More detailed measures that specify changes in costs of vital goods and services (e.g., food, medical care) may find greater clarification in the processes by which changes in cost of living affect the mental health of older adults. Multiple items are also likely to have greater reliability than the single question used in the current study. Third, some research in the sociology of mental health suggests that the effects of chronic stress may differ between externalizing and internalizing outcomes based on gender (Zhang & Axinn, 2022). To address this issue, interactions between gender and the cost of living indicators were tested in ancillary analyses. These tests were not significant for any outcome, but inclusion of behavioral outcomes in future research may show clearer gender differentiation (e.g., Shaw et al., 2011).

Conclusion

The current research presents an important contribution to the study of financial stress and mental health in later-life by showing that personal experiences with inflation form a substantial deleterious form of financial stress for older adults. Large increases in costs of goods and services present challenges to older adults’ abilities to obtain the necessities of daily life. These individual experiences cannot be directly concatenated to a single macroeconomic measure of changes across a vast array of goods and services because inflation experiences depend on individual needs and expenditures. Examining individual perceptions of changes in cost of living reveals older adults’ lived experience of inflation, but the extent of harm caused by these experiences is not unitary, and instead falls more heavily on older adults who lack sufficient psychological coping resources.

Supplemental Material

Supplemental Material - Perceptions of Increases in Cost of Living and Psychological Distress Among Older Adults

Supplemental Material for Perceptions of Increases in Cost of Living and Psychological Distress Among Older Adults by Alex Bierman, Laura Upenieks, and Yeonjung Lee in Journal of Aging and Health

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Social Sciences and Humanities Research Council of Canada, Grand number: #430-2018-00437; Social Sciences and Humanities Research Council of Canada, Grand number: #435-2022-0220.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.