Abstract

This article assesses the impact of the COVID-19 pandemic, the war in Ukraine and geopolitics on geographies of production. Criticizing simplified perspectives on globalized versus intraregional production, we stress the multi-scalarity, the role of industrial policies and sector-specific path dependencies in shaping global production. Based on expert interviews and policy and industry documents, our analysis focuses on the automotive, clothing, and electronics industries. Although concerns for resilience increasingly shape lead firms’ strategies, increased regionalization of production through re- or near-shoring is only one of several strategies. Where it does occur, it has been driven by state policies that tackle certain strategically important products, not production networks as a whole. Hence, while recent events exposed the vulnerabilities of global production, we do not observe deglobalization in the sense of a comprehensive retreat from globalized in favor of intraregional production. Nonetheless, state interventions that are geopolitically motivated and affect firms’ investment decisions have intensified particularly in the United States and the European Union.

Keywords

Introduction

The disruptions to global production networks (GPNs) because of the COVID-19 pandemic and the Russian attack on Ukraine have raised questions about the geographical structure of the current economic order. While the vulnerabilities of globalized production had become apparent even before the pandemic (Lund et al., 2020), debates about a crisis of globalized production, and the rise of deglobalization through re- or near-shoring have intensified ever since in the face of ongoing supply-chain disruptions, geopolitical and geoeconomic conflict, 1 and environmental crises. In this context, the discourse on supply-chain resilience overlaps with the objectives of technological sovereignty, while pronounced industrial policies have been introduced to allocate strategic manufacturing activities in the United States and the European Union (EU). This article provides an assessment of these initiatives and discusses how the COVID-19 pandemic, the Ukraine war, and the geopolitical constellation in their wake have shaped the geographies of production.

In approaching this question, we abandon the pervasive and simplified notion of a dichotomy between globalized production and intraregional production by showing that economic globalization and GPNs are multi-scalar phenomena in which global outsourcing, regional production clusters, and locally concentrated operations are closely interrelated. Furthermore, we emphasize that globalization is shaped politically as corporate strategies are embedded in world trade regimes and industrial policies that have changed due to intensified geopolitical tensions and are intertwined with policies to support digitalization and the green transition. Finally, geographical shifts and related policies play out differently according to path dependencies in specific sectors, thus defying the notion of any universal trend away from globalized production.

Empirically, we provide three case studies of production networks in employment-intensive industries, namely the automotive, clothing, and electronics sectors. While all of these industries have experienced strong trends toward globalization in the recent past, they differ significantly in their geography and governance patterns. Hence, they provide suitable and differentiated material for an examination of possible trends toward deglobalization. The case studies comprise an analysis of primary and secondary data sources on geographical restructuring. Primary sources include policy documents and industry coverage in relevant journals, portals, and conferences, as well as semi-structured interviews with industry experts from the three sectors. We focus on the strategies of lead firms and first-tier suppliers in the EU and the United States with regard to their investment and sourcing practices. A total of 18 semi-structured interviews were conducted with industry experts, representatives of industry associations and companies from the three sectors (see Table A1 in the online Supplemental Appendix). The interviews were analyzed through qualitative content analysis.

We argue that the policy shifts of the post-pandemic era bring about changes in the global division of labor that do not, however, amount to a retreat from globalization. There is an ongoing and accelerated trend toward more multi-tiered production and multipolar consumption structures. The pandemic also triggered concerns over security of supply that feed into intensified geoeconomic conflicts over technological leadership in strategic products. Although in this context concerns over resilience have attracted greater attention by lead firms, the reshoring of formerly offshored activities, or the near-shoring of activities in close proximity to core markets is only one of several strategies that lead firms pursue. Where it does occur, it has been driven by state policies and subsidies that only tackle certain strategically important product categories, not production networks as a whole. And these geographical shifts are riddled with obstacles due to pre-existing economic development paths and the associated power relations. Hence, while COVID-19 and the Ukraine war have exposed the vulnerabilities of global production, we do not observe deglobalization in the sense of a comprehensive retreat from globalized production in favor of intraregional production. What we can observe, however, is stronger political interventions with strategic geopolitical goals that affect firms’ investment decisions in strategically important segments.

In order to answer our main research question of how the COVID-19 pandemic, the Ukraine war and the geopolitical constellation in their wake have shaped the geographies of production, we proceed as follows: we first outline a theoretical perspective on economic globalization as a multi-scalar, politically shaped and sector-specific phenomenon. We then assess the development of global trade after the financial and economic crisis of 2008/2009 based on trade statistics and discuss policy changes in recent years focusing on the revival of strategic industrial policies in the United States and EU. The core empirical section assesses changes in corporate strategies and the geographical structure of production networks in the automotive, clothing, and electronics industries. In the last section, we summarize our findings and briefly discuss their implications for the future of globalized production in the context of multiple environmental and social crises.

Globalization and Deglobalization As a Multi-Scalar, Politically Shaped and Sector-Specific Phenomenon

GPNs are multi-scalar, that is, they integrate different geographical scales and ranges of production processes (local, national, regional, global), with global outsourcing, regional production clusters, and locally concentrated operations being closely linked. This brings into contrast a reductionist global–local dichotomy with a simplistic juxtaposition of offshoring and re-/near-shoring (as at least implicitly assumed by, for example, Brakman et al., 2020; Foroohar, 2022; Pla-Barber et al., 2021 see also Gong et al., 2022 for a similar critique). Also, in the most globalized sectors, such as the clothing or electronics industries, regional suppliers, and concentrations of production in regional or local clusters play an important role. The automotive industry is even more organized within regional hubs around key end markets. Some process-oriented industries, such as metal parts, paper, and cement, operate predominantly intra-regionally (Lund et al., 2019). Hence, regionalization is not necessarily the opposite of globalization, as the regional concentration of production can take place within the logics of GPNs. However, there are phases when production networks have been more locally or regionally based versus more globally based, and in recent decades, globalization has been the main component of capital’s ‘spatial fix’, driven by the availability of ‘cheap’ as well as ‘capable’ production locations after the opening of China, the end of the Cold War, and the new market opportunities (Gong et al., 2022).

The current shape of global, regional, and local production networks is based on the rationalization paradigm of flexible manufacturing, which focuses on economies of scale, short-term efficiencies, and just-in-time production, implying the rationalization, flexibilization, and acceleration of supply chains. In this paradigm, lead firms demand low labor and other direct and indirect production costs from suppliers, as well as quality, speed, flexibility, and the capacity to take on further tasks like warehousing and financing on behalf of the lead firms. For more complex products, this includes anchoring in complex ecosystems and clusters of research and development (R&D) and manufacturing operations. This paradigm makes production networks vulnerable to shocks and reduces their resilience regardless of whether they are organized globally or intra-regionally. Moreover, the investment and sourcing decisions by lead firms are not only aimed at ensuring advantageous conditions for production, but also at market access and proximity. This has increased further with the expansion of markets in large countries of the Global South, particularly China. This also means that regionalization and localization are not just synonymous with near- or re-shoring production units to the EU or the United States, but also with investments in close proximity to Asian end markets or production clusters (Horner and Nadvi, 2018).

The organization and governance of global industries—that is, their geographical configuration, the forms of value creation and appropriation, and the distribution of costs and risks—depend on the strategies of firm and non-firm actors (Coe and Yeung, 2015). The strategies and practices of lead firms, which can be understood as the primary organizing agents of global capitalism (Gereffi, 1994), play a crucial role in the architecture of GPNs based on specific power relations within sectors (Ponte et al., 2019). What is more, in many industries transnational suppliers at the first-tier level have taken on broad functions from lead firms, including the management of far-flung supply chains (Raj-Reichert, 2019). From the perspective of suppliers at lower tiers, this does not necessarily alter the power relations in GPNs. Nonetheless, first-tier supplier strategies need to be considered in their own right, as they are also in charge of relocating production, investing in old or new locations, and changing sourcing networks.

A company-centered perspective must be complemented by a perspective on the embeddedness of firm actors in their socio-spatial and political contexts and their interference with non-firm actors (Coe and Yeung, 2015; Henderson et al., 2002). The strong development of GPNs since the 1970s and particularly in the 1990s and 2000s is not only based on technological advances in transportation, information, and communications technology, but also on political decisions and efforts to create a global, neoliberal regime of trade and financial deregulation and hence a global economic area with uniform rules, secured by the World Trade Organization (WTO) and bilateral and regional trade and investment agreements (Raza et al., 2021). State regulations and policies are therefore central prerequisites for the current form of globalized production, and they are changing.

Since the financial and economic crisis of 2008/2009, the role of strategic industrial policy in the context of rivalry for technological leadership and sovereignty, particularly between the United States and China, has been reinforced with further accelerations due to the COVID-19 pandemic and the Ukraine war. The autonomy of states to act is conditioned by domestic power relations, that is, interests and social struggles within states and between different social groups, as well as geoeconomic and geopolitical constraints (Bieling, 2023). In particular, different factions of capital and their institutions, as well as institutionalized labor and civil-society actors, interfere in decisions on trade and industrial policies and the conditionalities of state support (Smith, 2015). Existing power relations developed in the context of GPNs, path dependencies and unintended policy consequences can make GPNs resistant to significant changes (Gereffi et al., 2021).

Sector-specific developments, cycles, and path dependencies also affect on the dynamics of re- and near-shoring. This includes whether the industry is organized around regional clusters based on follow-sourcing (where key suppliers relocate with lead firms), as in the automotive industry, but also in electronics and to a lesser extent in clothing. Investment and sourcing cycles depend on shifts in end markets and technology, such as the increase in online sales of clothing or the shift to electric vehicles (EV) in the automotive industry. Such shifts are also significantly shaped by policies, that is, ambitious goals for EV use or for local battery and semiconductor production, a focus on the circular economy in the clothing sector (although much less ambitious), and by the strategies of non-firm actors, including labor and other civil-society organizations.

Therefore, our conceptual approach sees GPNs as multi-scalar phenomena that are subjected to power relations between firms, as well as between firms and non-firm actors and that emerge in interaction with state policies. There is, however, a historicity to the relationship between the global and the local/regional, between trends toward offshoring versus re- and near-shoring. From a GPN perspective, the question is therefore not whether fully globalized production retreats toward self-sufficient intraregional or local production networks, but whether there occur significant alterations in the relationship between the global and the regional/local in the form of a comprehensive retreat from globalized production in favor of intraregional production, as well as the underlying reasons for such changes.

Twilight of Globalization?

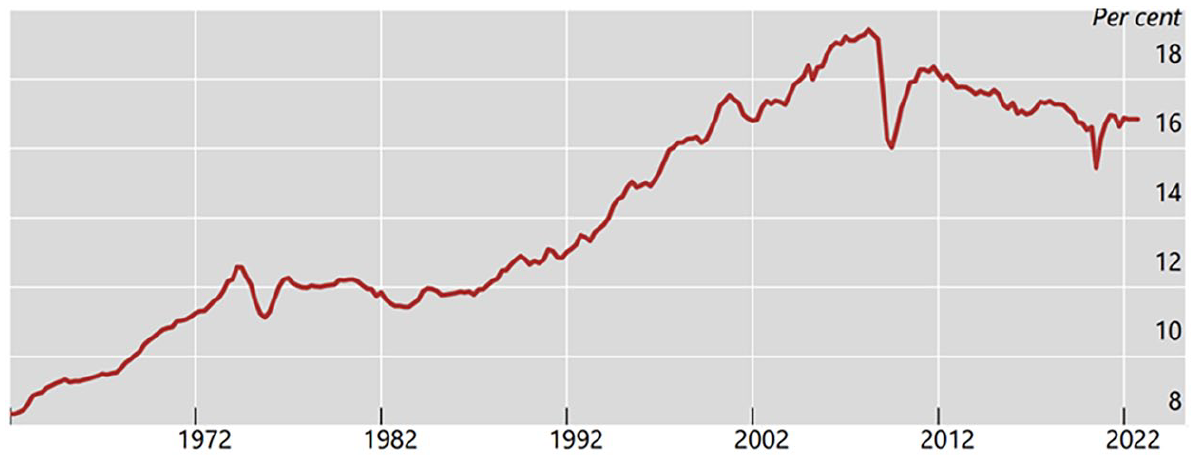

Already since the financial and economic crisis of 2008/2009, there has been the perception that the globalization of production has passed its peak. In view of the slowdown in globalization, The Economist (2019) coined the term ‘slowbalization’. Figure 1 illustrates the ratio of goods exports to gross domestic product (GDP; in constant prices) between 1962 and 2022, which grew substantially from the early 1990s onwards and peaked prior to the financial crisis in 2008/2009, a period called ‘hyperglobalization’. 2 Ever since, this ratio has slightly declined, but remained at the high level of 16%. Hence, aggregate trade data show no substantial evidence for deglobalization, but rather a plateauing at a high level of global integration, with international trade still growing in absolute terms. With regard to services, the trend is still increasing in absolute and relative (over global GDP) terms (Baldwin et al., 2023). However, foreign direct investment did also decrease in absolute terms between 2021 and 2022, but it always fluctuates more than trade, and its volume remained at a high level (beyond 1 trillion annually since 2006, except in 2020 during COVID-19; UNCTAD, 2023).

Global exports of goods over global GDP (%, at constant prices), 1962–2022.

There are different measures for trade in GPNs, including measures that define such trade as goods crossing a border at least twice or measures of GPN participation based on input–output tables. All these measures show a similar picture to Figure 1 of a substantial increase in trade in GPNs in the 1990s and 2000s until the financial crisis in 2008/2009, and stagnation or a slight decline afterwards (Antràs, 2020; WTO, 2022). However, the causes of this stagnation are not seen in a retreat from global economic relations, but particularly in a change in the composition of global demand due to the rise of markets in China and other emerging economies, which absorb a larger share of locally and regionally produced goods (Horner and Nadvi, 2018). Furthermore, some production steps have been consolidated more strongly around regional hubs. These shifts have accelerated post-COVID-19.

Recent Policy Changes in the United States and EU

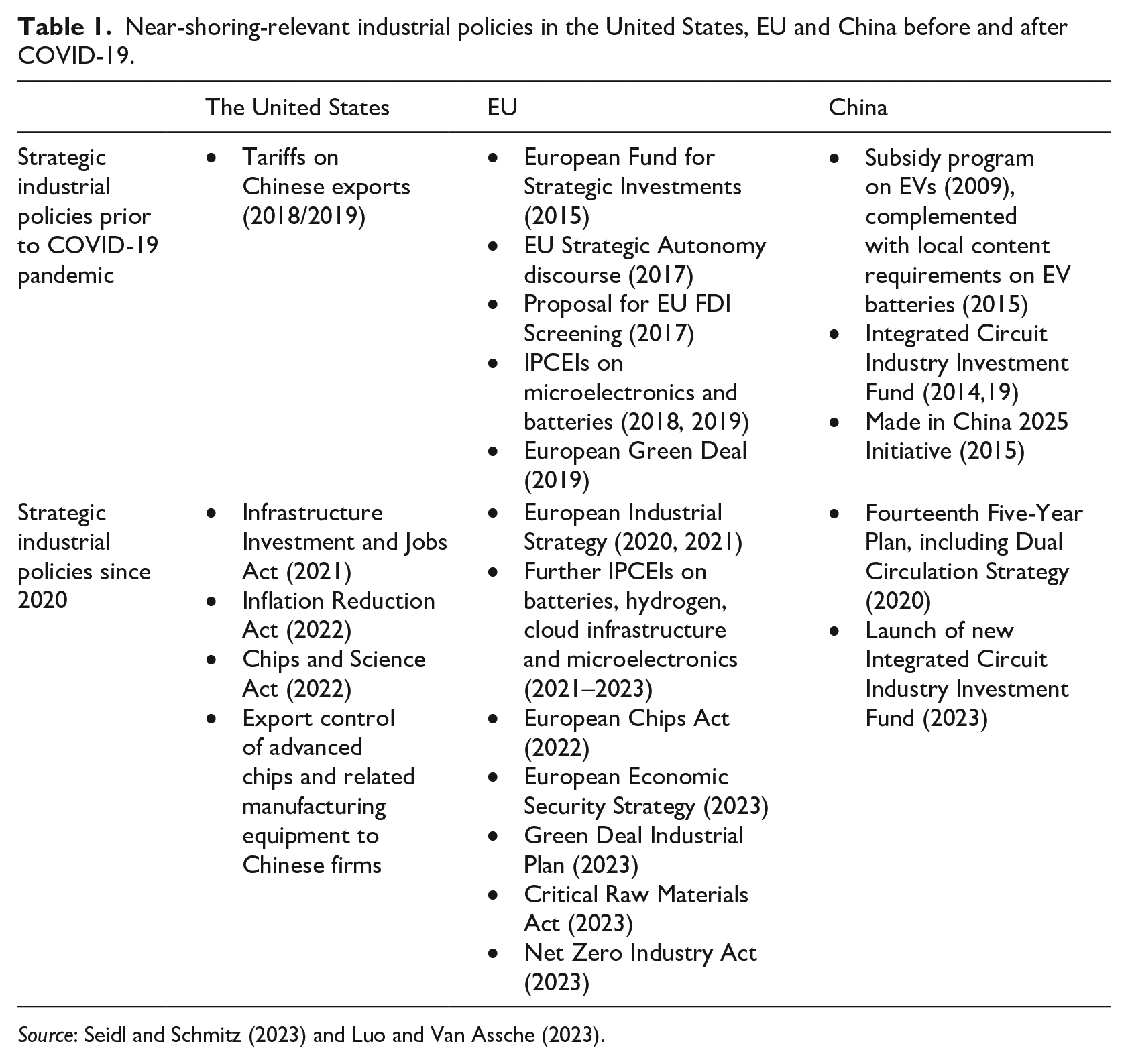

The re-emergence of strategic industrial policy in the United States and EU dates back to the aftermath of the financial and economic crisis of 2008, as Table 1 shows. Many other countries have industrial policies, particularly if they have an automotive and electronics sector, and these policies have generally intensified since the 2000s. But the big shift since the COVID-19 pandemic that was accelerated by the Ukraine war has been the implementation of more interventionist policies in the United States and the EU. Important reasons for this are the goal of defending or regaining technological leadership from China in high-tech and new green and digital activities (Eder and Schneider, 2018), which has accelerated in the context of increased geopolitical tensions, particularly with China. The linking of environmental concerns with geopolitics is termed, by Riofrancos (2023), the ‘security-sustainability nexus’. China’s ‘Made in China 2025’ initiative, announced in 2015, and the related dual circulation strategy, announced in 2020, were crucial in this regard, as it foresaw a focus on technological autonomy, increased domestic consumption, and support for domestic industry through large subsidies and strategic mergers and acquisitions (Butollo and Lüthje, 2017; Schmalz et al., 2022). China has become the dominant producer in areas such as batteries, photovoltaic modules, wind turbines and more recently electronic vehicles (Teece, 2019), and built up large transnational companies such as Huawei, ZTE, Tencent, Baidu, Xiaomi, and Alibaba. However, the rivalry is also over different concepts of the global world order, with China pursuing its own globalization project, most prominently through the Belt and Road Initiative (BRI) announced in 2013 (Bieling, 2023).

Near-shoring-relevant industrial policies in the United States, EU and China before and after COVID-19.

Source: Seidl and Schmitz (2023) and Luo and Van Assche (2023).

In the United States, the shift to a neomercantilist policy orientation became pronounced during the Trump administration starting in 2016 (Helleiner, 2019). With the slogan ‘America First’ and the related trade war, the United States aimed to slowdown Chinese development and debated the decoupling of US production networks from China. Tariffs on Chinese products increased more than six-fold, from an average of about 3% in the first quarter of 2018 to nearly 20% in 2020. These tariffs affect two-thirds of all Chinese exports to the United States, but there are also important product exemptions (Bown, 2021). The Biden Administration continued this stance toward China, focusing more on cooperation with aligned countries and adding interventions on an unprecedented scale. Key policies are the bipartisan Infrastructure Investment and Jobs Act (IIJA) (2021), the Chips and Science Act (2022), and the Inflation Reduction Act (IRA) (2022), which are a blend of green industrial, national security, and structural policies. Most importantly, the IRA contains subsidies and tax credits that are estimated to be worth US$369 billion for green technologies, but as there is no cap, some estimates see these expenditures amounting to up to US$1200 billion over the next 10 years (Bistline et al., 2023). Support under the IRA is linked to ‘buy American’ or ‘local content’ stipulations, meaning that only innovations and products that are largely developed or produced in the United States are eligible for funding.

In the EU, the shift toward interventionist industrial policies is not yet as strongly pronounced. There has been, however, a clear irritation of the competition-based paradigm in response to US policy measures (Schneider, 2023). Since 2007, there has been a discursive come-back of industrial policy linked to green growth and digitalization. However, it is only since 2018/2019 that competition law and the EU’s state-aid regime been contested, supported by new German and French interests (Seidl and Schmitz, 2023). This can be seen in debates around strategic autonomy, economic security and reshoring, which are increasingly resulting in actual policy shifts. The latter include the European Green Deal (2019), the EU Industrial Strategy (introduced in 2020 and renewed in 2021, which includes the monitoring of dependencies on specific products and the definition of strategic areas), the Green Deal Industrial Plan (2023), and the Chips Act (2022). Important Projects of Common European Interest (IPCEIs) allow for selective support in specific areas such as batteries, microelectronics, hydrogen, and cloud infrastructure. Compared to the United States, the overall volume of subsidies is still much smaller, but state-aid rules are becoming increasingly flexible, and member states are being allowed to pay out substantial state aid, for example, to semiconductor and battery companies.

What has been portrayed as the ‘revival of industrial policy’ did not suddenly emerge during the COVID-19 pandemic and the Ukraine war, as these events reinforced a shift that was already taking shape after the financial crisis of 2008, and has reached unprecedented levels of subsidization within the past 3 years, particularly in the United States. These policies affect investment across industries, although their impact varies according to the geopolitical and geoeconomic significance that is ascribed to particular industries and segments.

Geographical Shifts in the Automotive, Clothing, and Electronics Industries

COVID-19 and the Struggle for Global Dominance in the Automotive Industry

The automotive industry is a producer-driven GPN in which brand producers, in conjunction with large first-tier suppliers, control a multi-tiered supply chain. The technological rupture associated with EV production is currently leading to an upheaval in established structures and a more pronounced overlap between the electronics and automotive industries (Interviews A 2–5). New lead firms such as Tesla and Chinese EV producers emerged, and key components in the EV supply chain, such as batteries and semiconductors, become more important, while parts of the conventional combustion supply chain become obsolete. The COVID-19 pandemic was a substantial shock to the global automotive industry and acted as a catalyst to such developments. While the industry was able to recover quickly from initial disruptions, shortages in vital components, above all microchips, continued to exert a strain (A 1–3). The resulting calls for greater security of component supply are interwoven with a strong push toward a fundamental transformation of the industry toward electric mobility and datafication. Given these developments and the fact that the automotive industry generates significant amounts of revenue and employment, the transformation of the sector is of great geoeconomic significance, which explains the strong political initiatives to shape its trajectories (Krzywdzinski et al, 2023).

In the automotive industry, global fragmentation and regional integration overlap. Many non-complex components and electronic elements, which constitute a growing proportion of automotive value creation are manufactured globally. Yet to an increasing extent, intraregional structures predominate due to the high transport costs of bulky products, the requirements for rapid time-to-market and just-in-time production, and the advantages of the geographical proximity of assembly to the most important sales markets (E-mobil, 2022; Sturgeon et al., 2008).

Asian markets have developed most dynamically, and automotive brands have set up production facilities close to these markets (E-mobil, 2022: 186). While most brand producers continue to rely on European production sites for the global export of premium products, the trend toward setting up manufacturing structures close to major target markets has partially resulted in the losses of production capacities in the United States and Europe. More than two thirds of German automakers’ sales revenues are now generated abroad, 3 and Asian markets are continuing to act as a growth engine for the global automotive industry since the pandemic. Recent geopolitical tensions and increased competition from Asian EV brands are threatening to reduce the main revenue source for European brands.

While intraregional production currently dominates the industry, there is a characteristic division of labor within each region (Krzywdzinski, 2014; Pavlínek, 2018). Mainly driven by the desire to reduce costs, lead firms have orchestrated the build-up of substantial supplier capacities in Mexico (target market the United States) and Central and Eastern Europe (target market Western Europe) in recent decades. For instance, between 2008 and 2016, the share of employment represented by Central and Eastern European suppliers working for German brands increased from just under 40% to around 48% (Frieske et al., 2019: 74). This is facilitated by the industrial upgrading in these locations, which no longer differ greatly from German plants in terms of production technology (Schwarz-Kocher et al., 2019: 109–136).

According to industry experts (A 2,3,5), the post-pandemic situation is characterized by two conflicting tendencies. On one hand, trends toward offshoring production capacities is being reinforced, driven by the technological rupture of the transition to EVs. On the other hand, substantial industrial policy efforts are being made in traditional automotive manufacturing areas to gain production shares within the EV supply chain, in particular, for batteries and semiconductors.

The transition to electromobility is now deepening this intraregional division of labor. In Germany, trade-union representatives expect dramatic effects on employment (A 2,3,5). Brands no longer make major investments in the development of the combustion engine, resulting in accelerated relocation dynamics in these segments (cf. also Krzywdzinski et al., 2023). As further technological developments in these technologies are wound down, the need for technologically advanced sites that integrate innovation and production processes, which had been the main anchorage to keep advanced segments of automotive manufacturing in Germany, diminishes (Schwarz-Kocher et al., 2019).

Simultaneously, intensive efforts are being made to allocate the production of core components to the former core production areas in Central and Western Europe. This is backed by strong state support. The political response to the pandemic has aimed, in particular, at a transformation of industrial structures and strengthening the EV supply chain (Topuria and Gräf, 2023). This is considered to be of great importance if a leading position in innovation-intensive product segments is to be secured. However, it is unlikely that new investments in e-mobility will be able to compensate for job losses (Frieske et al., 2019).

What is more, national and regional governments are undertaking major efforts to attract investments in strategic and high value-added segments of the EV supply chain (A 3,5). Since the pandemic there has been a race to attract investments in the EV supply chain, particularly EV batteries. A large proportion of the funds linked to the United States IRA will be directed at undermining China’s strong position in EV-battery production (TE, 2023: 25). Only a few months after the Act was signed, investments of more than US$13 billion in raw materials production, battery manufacturing and EVs were announced (TE, 2023). Coordinated industrial policies of such dimensions have been missing at the European level so far. The perception of this deficit led to the announcement of a European Sovereignty Fund as a coordinated investment fund at the EU level aimed at decarbonization. In the meantime, most industrial policies that address the EV supply chain are implemented at the national level, for instance, in the form of direct subsidies for battery production facilities.

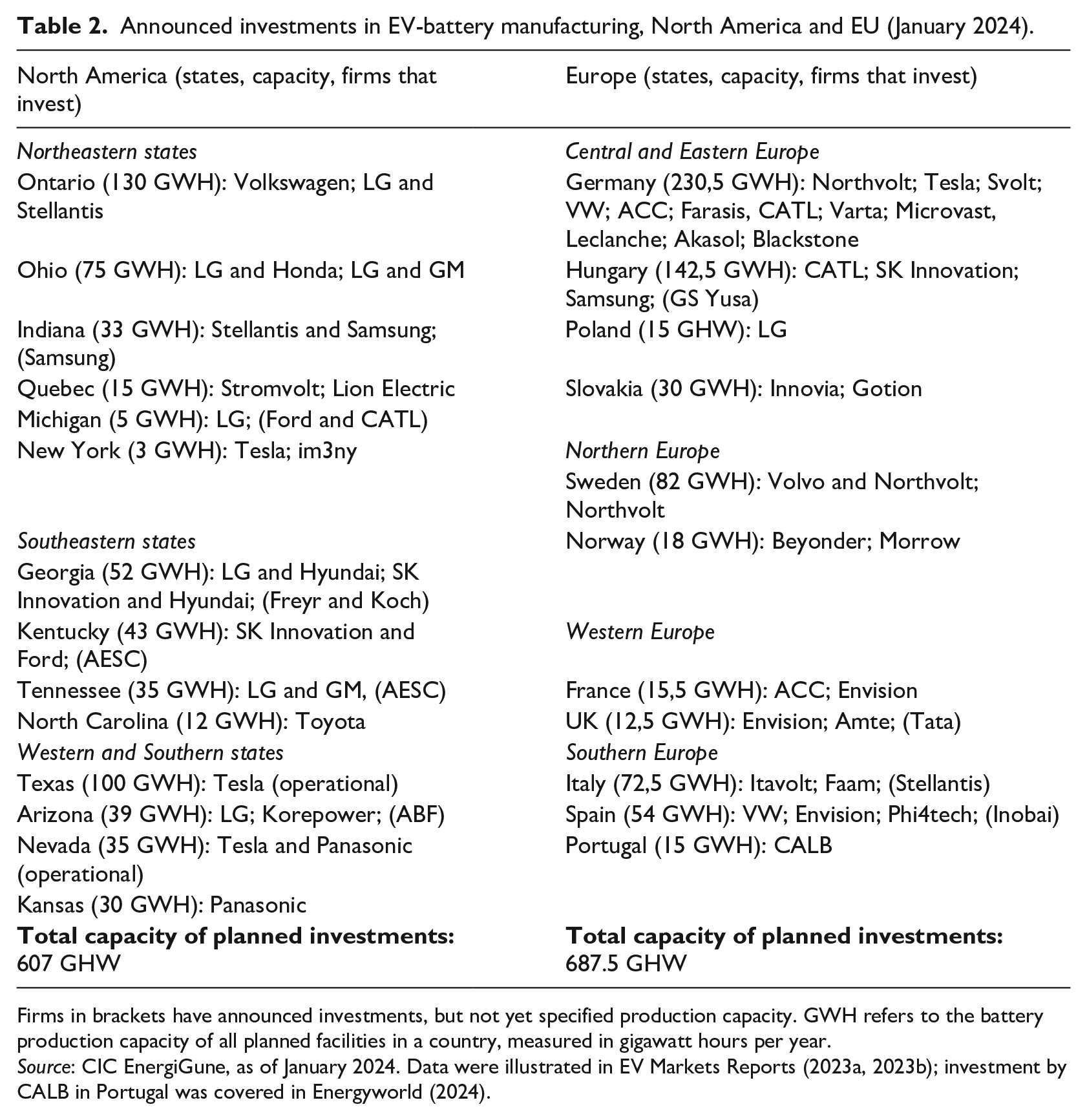

The result is a massive increase of EV-battery production in the United States and Europe, as shown in Table 2. In Europe, battery production volumes are expected to increase at least seven-fold, and it seems possible in the long term that European car manufacturers could become self-sufficient in their demand for batteries and thus reduce dependence on Asian imports (TE, 2023: 10). 4

Announced investments in EV-battery manufacturing, North America and EU (January 2024).

Firms in brackets have announced investments, but not yet specified production capacity. GWH refers to the battery production capacity of all planned facilities in a country, measured in gigawatt hours per year.

Source: CIC EnergiGune, as of January 2024. Data were illustrated in EV Markets Reports (2023a, 2023b); investment by CALB in Portugal was covered in Energyworld (2024).

All in all, the automotive industry is characterized by trends toward an increased intraregional division of labor, including employment losses in former core regions on one hand and huge industrial policy efforts to allocate strategic segments of the EV supply chain—batteries and chips—on the other hand. The latter are not mainly motivated by the goal to avoid supply-chain disruptions, as seen during the pandemic, but are the expression of a global competition for the high value-added segments of the automotive supply chain. This is a competitive quest for national sovereignty in strategically important sectors that is increasingly dependent on comprehensive industrial policies.

COVID-19 as an Accelerator of Multi-Tiered Supply Chains in the Clothing Industry 5

Clothing 6 is a classic buyer-driven GPN, where lead firms, that is, brands or retailers, are in charge of design, branding and retailing, and outsource production to a network of suppliers, largely based in the Global South, especially in Asia. Transnational first-tier suppliers are increasingly taking on functions such as product development, logistics, warehousing, and financing, and are managing their own global production and sourcing networks. The COVID-19 pandemic had far-reaching economic and social impacts on the sector. Supply-chain disruptions started with the outbreak of the pandemic in China, the world’s largest exporter of textile and clothing, but as the pandemic spread this occurred in all regions. This was followed by sharp drops in demand due to lockdowns in consumer markets. In response, some fashion brands in the EU and the United States canceled their orders due to ‘force majeure’ clauses and initially refused to pay their suppliers up to US$40 billion in outstanding invoices. In addition, many lead firms took advantage of suppliers’ overcapacity by exerting price pressure and extending payments terms (Anner, 2022). In 2021, the industry registered a quick recovery, but the Ukraine war caused major brands to close or sell their Russian businesses, while rising inflation and the start of a recession caused further drops in demand.

The pandemic and the Ukraine war hit the clothing sector at a time when it was already experiencing important transformations, including a shift to online sales, increased sustainability requirements, and de-risking from China in the context of increased geopolitical tensions. This has sparked debates on the near-shoring of clothing assembly and the verticality of textile production, where yarn spinning, fabric weaving or knitting, and sewing of clothing are spatially integrated in one country or region.

E-commerce increased sharply as a result of COVID-19. Ultra-fast-fashion companies—Asos, Missguided, and Bohoo Group from the United Kingdom and most prominently Chinese-owned but Singapore-based Shein—grew rapidly and set new standards in supply-chain digitalization, with their data-driven, responsive production of small batch orders that are sent directly to consumers. This strategy allows inventory costs to be reduced significantly compared to physical retailers. As a response, lead firms such as H&M and Inditex are investing substantially in e-commerce. The top 10 buyers (except TJX and Shein) reported an average online share of 26% in 2022 (data from company reports). Expanding online sales requires adaptions within production structures, which include on-shore distribution networks and to some extent near-shore or on-shore assembly for small batch orders, in combination with larger off-shore capacities and the verticality of textile production. Not all buyers and suppliers will be able to develop such structures, which can be expected to remain a selective strategy for specific buyers and product lines.

Due to the significant environmental impact of the textile and clothing sector, sustainability regulations and initiatives have risen (Niinimäki et al., 2020). Growing regulatory initiatives include mandatory corporate sustainability reporting on greenhouse gas emissions, regulations on supply chain due diligence laws (e.g. in the Germany in 2023) and industry specific regulations, most prominently the EU Strategy for Sustainable and Circular Textiles. Against the backdrop of these regulations, but also due to the increasing importance of a ‘sustainable’ image for brands, many in-house sustainability and multi-stakeholder initiatives have emerged. Some lead firms are also aiming to scale the share of fibers that have a lower CO2 content and are recyclable, with start-ups emerging in this area. Parts of sustainable textile production could emerge in the EU or the United States, as these investments are centered in the Global North.

While geopolitics are less important in clothing, they nevertheless play and have played important roles historically, particularly through trade and industrial policy (Pickles et al., 2015). Since the early 2010s, geoeconomics have materialized in a ‘China + 1 strategy’ pursued by buyers and suppliers to reduce dependence on China. This strategy has become particularly important for US buyers in the context of the United States–China trade war since 2018, which lead to the US administration imposing tariff rates of 15% on a total of 31 billion textile and clothing products, a figure that was later reduced to 7.5% (Lu, 2020).

As trade data show, China’s share in global clothing exports declined from 42.9% to 25.9% between 2010 and 2022 (UN Comtrade, 2023). However, the main beneficiaries have been other Asian countries, most importantly Vietnam and Bangladesh, which increased their global export shares from 3.3% to 8.9% and 5.1% to 11.9%, respectively (UN Comtrade, 2023). Nevertheless, China remains the number one clothing exporter, and its role as a textile exporter to other clothing-producing countries also continues to be crucial.

The ‘China + 1 strategy’ gained new momentum when the United States introduced the Uyghur Forced Labor Prevention Act (UFLPA) in 2021. The law bans imports from companies operating in the Xinjiang region, which account for more than 15% of the world’s cotton supply. However, buyers cannot fully de-couple from China, at least in the short and medium terms. In a survey of 30 large US buyers, more than 70% of respondents stated that they have no short-term alternatives to various yarns, fabrics, and textile accessories from China (USFIA, 2023). Balancing the tensions of the UFLPA becomes even more delicate for those firms for whom China constitutes a major end market.

These shifts, in combination with the COVID-19 pandemic and related supply-chain disruptions, have spurred debates about near-shoring. However, the main driver of the near-shoring of assembly and particularly textile verticality is speed-to-market linked to online sales to reduce inventory (interviews C1, C2, C3). Some buyers have begun to stress verticality in combination with sustainability for being as important as labor costs, and first-tier suppliers are increasingly expected to provide three-tier solutions, namely off-shoring, near-shoring, and on-shoring, depending on the type of product (interviews C2, C3). Nonetheless, for US buyers in particular, geopolitical tensions also play an important role. In this regard, investments in Central America are supported by the US government as part of its ‘strategy for addressing the root causes of migration in Central America’, which includes a ‘Partnership for Central America’ that resulted in US$585 million of investments and sourcing commitments by US buyers in the first 2 years (Safaya, 2023).

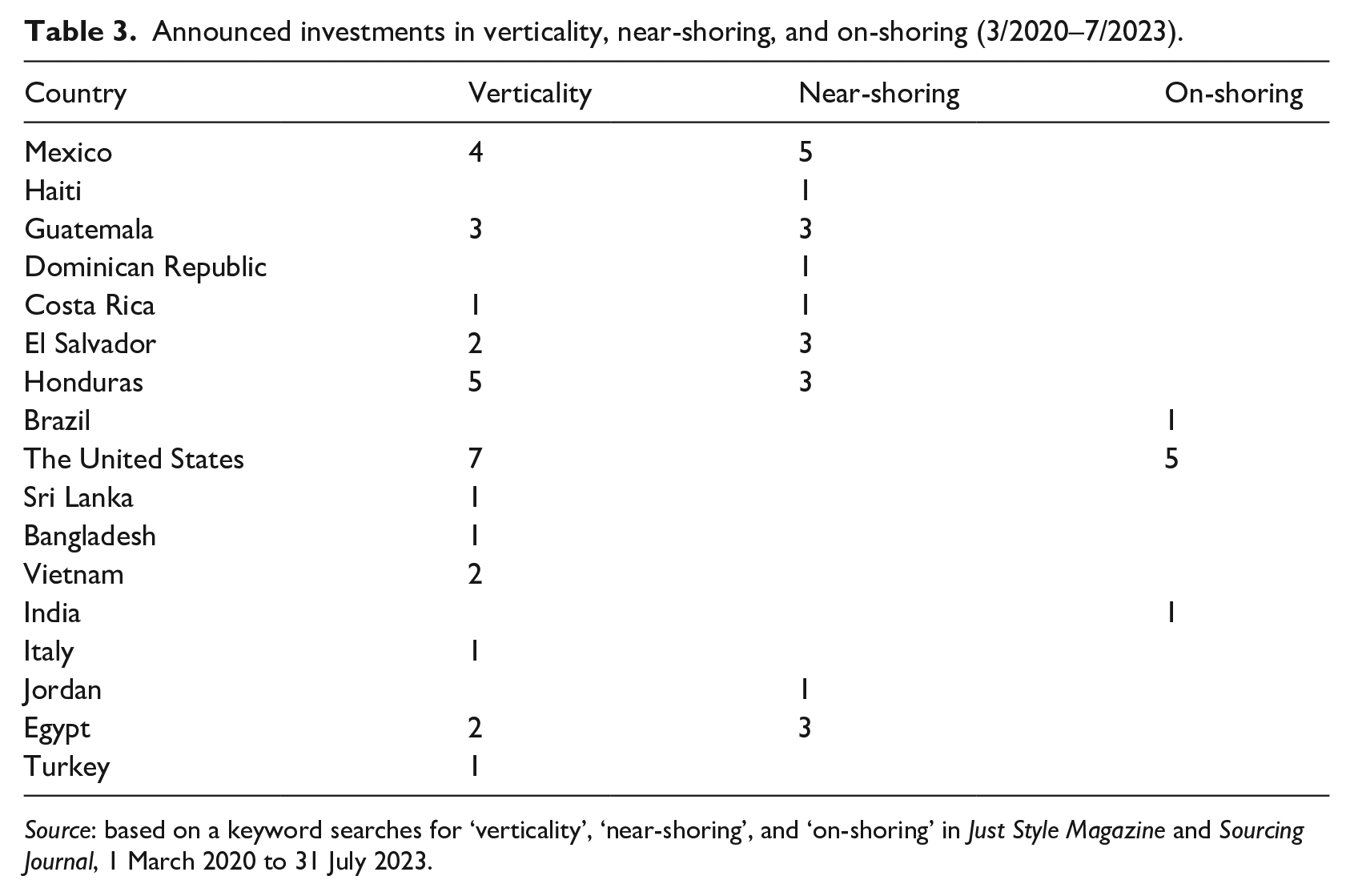

What we can already observe empirically is increased investment in assembly closer to end markets, and particularly in regional verticality and accessories (buttons, zippers, elastics, labels), with off-shore production in Asia nonetheless remaining dominant. Table 3 shows the investments announced in regional verticality of textile production and in the near-shoring and on-shoring of clothing assembly, based on a systematic media analysis of the two main clothing industry journals, Just Style Magazine and Sourcing Journal. Between the beginning of the COVID-19 pandemic and July 2023, 28 investments in verticality, 21 in near-shoring, and six in on-shoring have been announced, particularly focusing on Central America and Mexico. These investments were largely made by transnational first-tier suppliers to provide buyers better near-shoring and multi-tier production solutions (interview C1).

Announced investments in verticality, near-shoring, and on-shoring (3/2020–7/2023).

Source: based on a keyword searches for ‘verticality’, ‘near-shoring’, and ‘on-shoring’ in Just Style Magazine and Sourcing Journal, 1 March 2020 to 31 July 2023.

COVID-19, Semiconductor-Related Industrial Policy, and China + 1 in the Electronics Industry

The electronics industry is a hybrid version of the clothing and automotive industries in the sense that some lead firms outsource production entirely to contract manufacturers, while others keep large chunks of production in-house. In consumer electronics, production is heavily concentrated in Asia, while in industrial electronics, there is a greater diversity of global production locations. The COVID-19 pandemic caused major disruptions in the industry. First, the initial lockdown in China disrupted electronics production and assembly. Later, lockdowns across the world led to an increase in the demand for electronics products, especially remote-working products, which in turn led to an increase in demand for semiconductors. Production capacity was quickly ramped up, but a significant semiconductor shortage persisted in 2021 and 2022, significantly affecting industries such as automotive. Various lockdowns in major electronics production locations, such as China, Malaysia, and India further disrupted electronics supply chains. In contrast, the electronics industry was not particularly affected by the Ukraine war, with the sole exception of the concentration of semiconductor-grade neon gases in Ukraine and Russia, which firms could deal with quite easily (Interview E1).

Despite increasing debates about resilience, the emphasis in the electronics industry seems to remain on operational efficiency and cost rather than on redundancy and the diversification of supply chains (Gereffi et al., 2021). This is mainly because it is difficult to predict where the next supply-chain disruption will occur. In addition, there are several cases where a second or third source does not even currently exist. Bottlenecks in the electronics supply chain are manifold and are especially prevalent in the major intermediate input for various electronics products, namely semiconductors. 7 A recent study of the semiconductor supply chain counted 50 chokepoints where 65% or more of production of an input is concentrated in a single country or region (Ting-Fang and Li, 2022). As one supply-chain manager from a major European semiconductor producer highlighted (Interview E4): ‘Yes, COVID showed that semiconductor supply chains are not resilient. But what can we do? Redundancy for all inputs and for all locations is not a viable solution. That would not even remotely make sense in terms of costs’.

Nevertheless, major shifts are taking shape in the geographies of electronics production. Rather than being the result of firms aiming to make their supply chains more resilient, these shifts are driven by geopolitical and geoeconomic changes and can be categorized into the following trends: the acceleration of ‘China + 1’ strategies in final assembly; aggressive industrial policies to attract semiconductor front-end production, especially in the United States and Europe; and the US attempt to stop China’s rise in semiconductor production.

Production in the global electronics industry is highly concentrated in Asia, especially in the final assembly of electronics and semiconductors (Yeung, 2022). Nevertheless, the industry is characterized by multiple fragmentation and reintegration processes that vary by-product category and lead firm. Samsung, for example, produces all its mobile phones in in-house factories, while Apple relies fully on contract manufacturers. Desktop personal computer (PC) and TV assembly are more geographically diverse and strategically closer to end markets because of the bulkiness of the products (e.g. regional production in Mexico for the US market, and in Eastern Europe for the Western European market), whereas mobile-phone and Notebook assembly are concentrated in Asia (Lüthje et al., 2013; Yeung, 2022). In industrial and medical electronics, a larger share of production and final assembly has remained in Europe and the United States. This is again because of the bulkiness of the products, as well as the public and private regulations for specific end markets and time-critical services such as maintenance and repair (Hamrick and Bamber, 2019).

A ‘China + 1’ strategy adopted by lead firms and contract manufacturers already existed before the pandemic. In mobile-phone assembly, India’s and Vietnam’s share went up from 7.4% and 4.3% respectively in 2015 to 20.9% and 11.3% in 2018, at China’s expense (down from 62% to 49%; Yeung, 2022: 150). This trend continues unabated, with other Asian countries, such as India, Vietnam, and Malaysia, being the main beneficiaries (Yang and Chan, 2023).

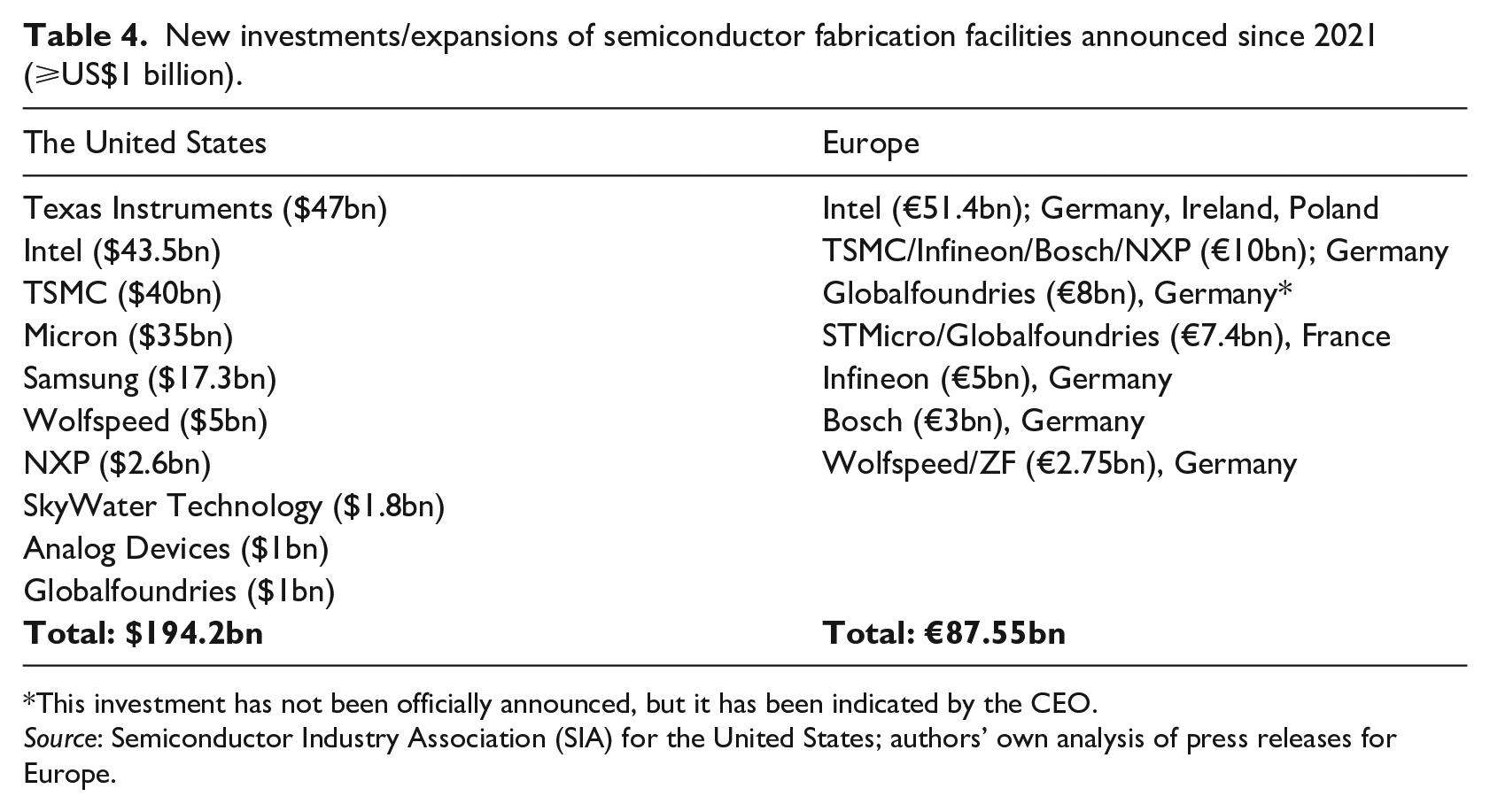

However, the continued ‘China + 1’ strategies for electronics assembly do not seem to have led to near-shoring in Europe or America, especially for Notebooks and mobile phones. The picture is different for semiconductors, where major front-end production investments are being undertaken in both the United States and Europe (Table 4) in the context of large production subsidies, as under the US CHIPS and Science Act and the European Chips Act. While policy support has been around since the emergence of the industry in the 1950s (OECD, 2019), these acts represent a sea change in that they stipulate government subsidies for mass production, and not just for R&D. The subsidies awarded are substantial. In the case of TSMC in Dresden, the German government subsidy, pending EU Commission approval, amounts to €5 billion, that is, 50% of the overall investment. The subsidies are clearly making a difference. 8 Before the European Chips Act, there had only been a single greenfield investment in semiconductor front-ends in Europe in ‘more than a decade’ (European Commission, 2022: 33).

New investments/expansions of semiconductor fabrication facilities announced since 2021 (⩾US$1 billion).

This investment has not been officially announced, but it has been indicated by the CEO.

Source: Semiconductor Industry Association (SIA) for the United States; authors’ own analysis of press releases for Europe.

Other countries are also implementing policies for the semiconductor industry. However, direct subsidies for production investments and their size are unique to the United States and Europe, with the exception of China, where large subsidies have been directed toward semiconductor manufacturing investments for several years (OECD, 2019). The policy shift in the United States and EU can be explained by the semiconductor shortage during the pandemic, which exposed dependencies (East Asia had 81% of global wafer capacity in semiconductors in 2018, while the United States had 10.4%, and Europe 6%; Yeung, 2022), together with the general trend toward more interventionist industrial policies and the importance of semiconductors for future economic growth, digitalization, and the green transition.

Finally, there are also the US export and technology restrictions targeting China. These restrictions started in earnest in May 2019, when Huawei was placed on the US government’s Entity List, and they were broadened and tightened in May 2020 and again in August 2022. In October 2022, restrictions on exports to China of certain advanced semiconductors themselves, semiconductor production equipment and services by US persons were added, with the explicit ‘aim to slow the indigenous ability of China to develop and mass-produce advanced chips’ (CRS, 2023: 21). These export controls are affecting electronics GPNs in that ‘China + 1’ or even ‘no-China’ strategies by electronics lead firms and semiconductor producers are being accelerated. China’s catching up in advanced semiconductors has therefore been slowed down, but its capacities in mature technology nodes continue to increase (Kleinhans et al., 2023).

The overall impact of these developments will likely be that consumer electronics assembly will remain centered in Asia, although a continued partial shift from China to other Southeast Asian countries will occur. Semiconductor front-end production will increase in the United States and Europe, but the majority of front-end production will remain in Asia: for lower technology nodes in Taiwan and South Korea and for mature nodes in China (Kleinhans et al., 2023). Semiconductor backend activities, that is, assembly, packaging, and testing, will continue to be centered in Asia, with significant investments currently occurring in Malaysia and Vietnam, given that the backend is more labor-intensive, with strong path dependencies and local clusters in Asia (Yeung, 2022).

Conclusions: Accelerated Transformations, But No End of Globalized Production

Taking an understanding of globalization as a multi-scalar, politically-shaped, and sector-specific phenomenon as our point of departure, these brief synopses of recent developments in three relevant industrial sectors demonstrate that the COVID-19 pandemic, the Ukraine war and particularly the revival of strategic industrial policies in the United States and EU, partly motivated by the desire to compete with China in high-tech and new green and digital activities, have indeed accelerated processes of structural transformation. This is evident in the transition toward electric mobility in the automotive industry, the acceleration of e-commerce and sustainability initiatives in the clothing industry, and the reshoring of semiconductor production to the United States and EU in the electronics industry. These transitions are about to change the structures and geographies of GPNs, yet none of the analyzed sectors indicate a clear trend toward deglobalization. We are rather witnessing patterns of the reconfiguration of multi-scalar arrangements where significant proportions of manufacturing continue to be organized in globalized supply chains. Significant alterations in the geographical structure of production by and large concern those product categories that are considered strategically important, especially the interwoven segments of semiconductor and EV production. Industrial policy efforts have especially targeted these product groups out of security of supply concerns and the interest in promoting growth and employment in strategically important, high value-added ‘green’ and ‘digital’ industry segments. The clothing industry is a certain exception to this trend as it is not considered a strategic sector to the same extent but has experienced a certain trend toward near-shoring due to lead firms’ interest in multi-tiered production structures and increased verticality.

While the effects of the pandemic and to a lesser extent the Ukraine war exposed the vulnerabilities of specific GPNs, the changes observed had little to do with the general aim of increasing supply-chain resilience. Firm-driven restructuring only occurred in some instances when it was linked to specific business objectives such as increasing online sales in clothing. The main drivers of the geographical restructuring of production are the interventionist industrial policies that coincided with and were reinforced by the pandemic and the Ukraine war—in order to gain competitiveness and technological leadership in strategic fields, as well as to reduce dependencies, especially with respect to China amid a more hostile geopolitical climate. These industrial policies are driven by the concerns of sovereignty, but they are not motivated by or result in a general increase in resilience in supply chains. Global dependencies have only partially been built back, and there have been surprisingly few efforts to enhance the stability of sourcing by creating supplier redundancy or increasing inventories in the three industries. The focus of policy is on strategically important segments of GPNs that are generally high-tech, green and digital, rather than aiming at the general geographical reorientation of global production.

There are significant forces at work that maintain the global scale of production. As the sector studies show, these reflect the path dependencies of the existing international division of labor. There is a concentration of production capacities and capabilities in clusters and regions that are difficult to replace. Particularly in the electronics and clothing industries, we observe an intensified China + 1 strategy, predominantly resulting in shifts to other Asian countries. The strategies of lead firms (and first-tier suppliers) continue to focus on a just-in-time logic and to combine decentralized sourcing with the advantages of regional manufacturing hubs and easy access to relevant end markets. Hence, a global footprint and short-termism in sourcing will continue to shape the post-pandemic era, albeit under markedly different political circumstances, which means that economic decisions on investment and sourcing will increasingly be shaped by geoeconomic considerations.

Overall, the new wave of industrial policy contains a large proportion of generous incentives, potentially covering a substantial part of the investment volume or product end price, but with very few disciplinary measures related to the economic, social, and environmental aspects. The emphasis is placed on ‘carrots’ while ‘sticks’, in the sense of prohibitions and bans, for example, of non-green technologies, are comparatively limited. Furthermore, the subsidy race can be expected to create large inequalities within the United States and the EU, as well as between core economies and countries of the Global South, which do not have the same budgetary means.

Recent ruptures provoke a more fundamental question about the sustainability of the global economic order. To what extent and by what means can industrial and trade policies become a driver of a socio-ecological transformation? The necessary decarbonization of the economy indeed presupposes its greater regionalization and localization. This does not amount to the self-sufficiency of regions, but to a sectorally differentiated deglobalization of production networks. For example, it would be impossible and not meaningful to locate electronics production as a whole at the local level. In contrast, a number of economic activities connected to everyday necessities (e.g. food, clothing, furniture) as well as critical medical or pharmaceutical products, could very well take place more at the regional or local level. More fundamentally, a spatial reconfiguration of GPNs would need to be connected with a change in the rationale of investment if it was to lead to a socio-economic turnaround in the interests of social equality and ecological sustainability from the boundless acceleration and intensification of capital accumulation and consumerist culture toward a prioritization of fundamental products and services, as envisioned, for instance, by the foundational economy perspective. 9 To achieve such transformations, industrial policy measures should not only include ‘carrots’ in the forms of subsidies, but also ‘sticks’ such as the implementation of climate-protection policies and requirements to meet social objectives. What is more, a reversal of trade policies is urgently needed. This requires a new generation of fair-trade agreements that ensure binding compliance with social and environmental standards and the fair distribution of economic gains, costs and risks, while granting policy space for development strategies and focusing on the basic needs of people in the Global North and South.

Supplemental Material

sj-docx-1-crs-10.1177_08969205241239872 – Supplemental material for The End of Globalized Production? Supply-Chain Resilience, Technological Sovereignty, and Enduring Global Interdependencies in the Post-Pandemic Era

Supplemental material, sj-docx-1-crs-10.1177_08969205241239872 for The End of Globalized Production? Supply-Chain Resilience, Technological Sovereignty, and Enduring Global Interdependencies in the Post-Pandemic Era by Florian Butollo, Cornelia Staritz, Felix Maile and Tobias Wuttke in Critical Sociology

Footnotes

Acknowledgements

The authors thank their interview partners for their time and insights into changes in global production networks. Many thanks also go to Oliver Kossowski, Miriam Frauenlob, Ann-Kathrin Katzinski, Fabian Pfeiffer, and especially Leonhard Plank for their great support of the research, and to Werner Raza, Jan Grumiller, and Martin Krzywdzinski for their comments. Many thanks are also due to Lindsay Whitfield for her permission to use two interviews she conducted together with Felix Maile, to Gale Raj-Reichert for her permission to use one interview conducted together with Tobias Wuttke and one interview conducted together with Florian Butollo, and to Martin Krzywdzinski for one interview he conducted together with Florian Butollo. This article builds on an earlier contribution that appeared in German in 2022 (Butollo and Staritz, 2022). It was thoroughly modified, extended and updated for publication in Critical Sociology.

Author’s Note

Florian Butollo is also affiliated with Technical University Berlin, Germany.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Tobias Wuttke and Florian Butollo are grateful to the German Research Fund (DFG) and the German Federal Ministry of Labour and Social Affairs (BMAS) for the funding that made the research for this possible.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.