Abstract

The purpose of this paper is to understand the conditions that influence family CEOs’ resilience in times of crisis. Drawing upon social cognitive theory and adopting a fuzzy-set qualitative comparative analysis analytic approach, the article analyzes data from 67 family businesses. The findings show that CEO resilience emerges from the interplay of different sets of conditions in single- and multi-generational family businesses. The study makes the contribution that CEO resilience is contingent on dynamics at individual, family, and business levels, suggesting that CEO resilience in crisis times reflects a “crisis bricolage” of “making do” with resources that are “in hand” and “within reach.”

Keywords

Introduction

COVID-19 has rekindled the interest in understanding the conditions that enable Chief Executive Officers (CEOs) to be resilient: that is to adapt, develop, and leverage capabilities to navigate uncertainty that emerges from adverse circumstances (Djourova et al., 2020; Gottschalck et al., 2024; Lengnick-Hall & Beck, 2005; Paramita et al 2022; Williams et al., 2017). As the “ultimate decision-maker and the person with absolute authority” (Kesner & Sebora, 1994, p. 328) in family business, the family CEO plays a pivotal role in managing disruptions, creating changes, and influencing organizational strategies and performance (Finkelstein & Hambrick, 1990). Yilmaz et al. (2024) state that family CEOs’ “personal characteristics, resources as well as their relational, cognitive, behavioral, and emotional capabilities will shape the strategic choices and decision-making processes within their firm (Finkelstein & Hambrick, 1990)” (p.71). Indeed, the family CEO, as a central family business member, is an important research area (Yilmaz et al., 2024).

Recent years have witnessed a rapid increase of challenges and crises, such as climate and health crises, the digital and AI revolution, and war. Family CEOs inevitably need to demonstrate resilience to navigate their firms through these challenging times (Conz et al., 2020). Understanding CEO resilience therefore is crucial because the knowledge attained will not only contribute to understanding why some family firms survive during times of crisis and others do not (Finkelstein & Hambrick, 1990; Gottschalck et al., 2024) but also unveil how CEOs manage dynamics in the ecosystem that influence the sustainability of enterprises (Giones et al., 2020). Given the prevalence and contribution of family businesses globally (Andersson et al., 2018; De Massis et al., 2018), this knowledge is particularly important.

However, family CEOs operate in a complex and dynamic environment that blends family and business in a unique manner. On the one hand, having the family in the firm gives CEOs access to “in-house” resources that may contribute to their resilience. These include a commitment to stewardship to retain the business across generations (Davis et al., 2010; Whetten et al., 2014) and non-financial socioemotional wealth (SEW) or “affective endowments” of the family that stems from family relations, networks, and ties (Berrone et al., 2012, p. 259). Memili et al. (2014) find that family CEOs play an influential role in leadership and can disseminate historical and contextual information throughout the organization. This leads to better trust, social capital, and resilience than non-family businesses. On the other hand, CEO resilience can be constrained by tensions in business families. Conflicts occurring in the family domain can spill over to the business, and vice versa, thus “triggering critical downward spirals” (Yilmaz et al., 2024, p. 61). Crises and conflicts occurring in the family business environment may challenge family CEOs’ existing business views, current and future roles, and their power and control dynamics. These findings seem paradoxical, suggesting that family CEOs’ resilience might be nurtured in an idiosyncratic way.

Resilience of family CEOs has been studied from different lenses (Beech et al., 2020; Santoro et al., 2021). However, research on individual-level resilience in family firms is limited (Conz et al., 2020). Gottschalck et al. (2024) in their study of the resilience of small business owners claim that “more insights about cross-level effects on the resilience of small business owners are needed” (p. 2). In addition, Smith et al. (2024) point out that extant resilience research has yet “to take the opportunity to unravel the dynamics of multilevel mechanisms interlocking individuals, the family, and the firm” (p. 7). Echoing the findings of Gottschalck et al. (2024) and Smith et al. (2024), we argue that understanding family CEO resilience and its conditions at multiple levels is important, and thus pose the following question: “What are the conditions that nurture family CEO resilience in family businesses in times of crisis?”

To address this question and capture the multilevel nature of CEO resilience, this study adopts a social cognitive theory (SCT) lens (Bandura, 1988, 2001). SCT holds that human development is complex and dynamic (Garcia et al., 2019), and human functioning depends on the continuous and reciprocal interactions between individuals and their environment (Bandura, 1988). The kernel of SCT is the notion of self-efficacy (Charoensap-Kelly et al., 2021), which arguably forms the foundation of resilience (Milaković, 2021).

This study adopts a fuzzy-set qualitative comparative analysis (fsQCA), which has been widely used in family business and entrepreneurship research (e.g., Pittino et al., 2018; Sahin et al., 2019). This method aligns with our research question because it unravels causal complexity in terms of conjunction, asymmetry, and equifinality (Furnari et al., 2021). That is, it reveals how an outcome can be achieved through different causal paths (equifinality), how a given element could cause or prevent an outcome (causal asymmetry), and how combinations of conditions lead to a certain outcome (causal conjunction; Pittino et al., 2018). The study is based on 67 responses from small- and medium-sized family businesses (SME) from the Flemish region during the onset of the COVID-19 pandemic. Our results show that the resilience of the CEO in single-generational family firms benefits from the presence of e-business capability and family influence on the board, while CEO resilience in multi-generational firms gains from family social capital and the CEO’s age and education.

The research makes the following contributions. By finding the configurations of conditions at the individual, family, and business levels, the research uncovers a multi-level understanding of CEO resilience. This contributes to the debates on resilience in the family business and organizational literature (Ahmed et al., 2022; Conz & Magnani, 2020; Iborra et al., 2020; Iftikhar et al., 2021; Linnenluecke, 2017). Furthermore, by disentangling generational influences, the research contributes to the growing recognition that family firms are heterogeneous and require different considerations from a policy and practice perspective (Jaskiewicz & Dyer, 2017). Finally, we show the appropriateness of SCT in understanding CEO resilience in family firms, especially in reinforcing the significance of the person-environment interaction and highlight the influence of family in CEO resilience.

Literature and Conceptual Background

Social Cognitive Perspective

SCT asserts that the psychological functioning of human beings stems from dynamic and reciprocal interactions between individuals and their environments (Bandura, 1986, 1988, 2001; Garcia et al., 2019). The behavior of executives such as the CEO is shaped by their individual cognitive perception of reality or “a mental framework” (Gottschalck et al., 2024, p. 2). This cognition or mental framework can guide individuals to engage in assessment and anticipation of events (Bandura, 1986, 1988, 2001).

A central tenet of SCT is the concept of self-efficacy or one’s belief in his or her own ability to persevere or accomplish goals in challenging circumstances (Charoensap-Kelly et al., 2021; Stajkovic & Luthans, 1998). Self-efficacy is not a trait of human beings but “a differentiated set of self-beliefs linked to distinct realms of functioning” (Bandura, 2006, p. 307). An individual’s self-efficacy is instilled and strengthened through four experiences (Bandura, 1982; Wood & Bandura, 1989): enactive mastery or personal attainment of goals, vicarious experience or modeling behavior of others, social persuasion that an individual can “do it” and overcome obstacles that may present in achieving the task, and physiological states such as when an individual assesses vigor as a sign of physical capability. Although external cues emanating from the individual’s environment will influence an individual’s judgment about his or her self-efficacy to manage a situation, an individual draws on internal cues such as his or her experience and familiarity with a task as well as his or her capabilities in making a judgment about self-efficacy to manage the task (Gist & Mitchell, 1992). Researchers have documented the connection between self-efficacy and resilience (Milaković, 2021; Ojo et al., 2021) and suggest that self-efficacy is a core component of resilience (Charoensap-Kelly et al., 2021). Importantly, it is acknowledged that when an individual’s belief or self-efficacy is firmly established, they will, in turn, be resilient to adversity (Wood & Bandura, 1989).

CEO Resilience: A Configurational Approach

The notion of resilience originated with the seminal work of Staw et al. (1981) and Meyer (1982), initially focusing on how organizations respond to external threats (Linnenluecke, 2017). Staw et al. (1981) note that in times of adversity, organizations often attempt to avoid risks and show maladaptive symptoms. Meyer (1982) instead argues that businesses can cope with external negative situations. They display adaptability by absorbing the impact of environmental jolts with their slack resources or implementing new practices that align with their ideologies and organizational structures.

Recent resilience research bifurcates along two orientations: individual- and firm-oriented studies (Conz et al., 2020; Korber & McNaughton, 2018). In individual-oriented studies, attributes (Miller & Shamsie, 2001), psychological traits (Simsek et al., 2010), and experiences of managers (Finkelstein et al., 2009) are perceived as predictors that lie at the core of individual resilience. In firm-oriented studies, resilience is positioned as a firm attribute resulting from resources, capabilities, and intrinsic characteristics (Aldunce et al., 2014; Hosseini et al., 2016; Klein et al., 2003) that enable firms to address changes in times of adversity (Pal et al., 2014).

In this paper, we position our study at the individual level. Consistent with the work of Gottschalck et al. (2024), we define individual-level resilience as “the ability of an individual to cope with adversity and the capacity to adapt to unforeseen events” (p. 1), while this capability is related to factors at the (a) individual (psychological/cognitive), (b) family, and (c) organizational levels (Hartmann et al., 2020; Yilmaz et al., 2024). In the literature, various antecedents of individual resilience have been identified, including personal resources, personal mindsets (Hartmann et al., 2020), support at work, social support in private life, feedback, and recognition in the workplace (Förster et al., 2022), as well as a positive organizational context (Hartmann et al., 2020). Raetze et al. (2021), in their multilevel review of resilience research, however, suggest that business- and team-level antecedents, such as financial and material resources, structural resources, human and social resources, strategies and practices, team characteristics, team resources and processes, and leadership behavior, contribute to individual-level resilience. They highlight the importance of multilevel research on resilience, “since crisis events have the potential to spread across levels of analyses creating complex event clusters and chains” (Morgeson et al., 2015, p. 633). Informed by this, we argue that the factors that are likely to impact CEO resilience do so in combination rather than in isolation.

The multilevel nature of conditions that relate to CEO resilience are a strong indication of causal complexity in terms of conjunction, causal asymmetry, and equifinality (Furnari et al., 2021). That is, conditions that lead to CEO resilience may differ from those that lead to the absence of CEO resilience (causal asymmetry). There may also be multiple configurations of conditions that produce CEO resilience (equifinality; Ragin, 2008; Schneider & Wagemann, 2012). Finally, those conditions may also produce a combined effect on CEO resilience (causal conjunction). In the following paragraphs, we delve deeper into the interplay of conditions that contribute to CEO resilience, namely, CEO’s tenure, age, and education (Hartmann et al., 2020), followed by the family-level conditions such as family social capital and family influence on the board (Förster et al., 2022), and conclude with the business-level condition of e-business capability (Hartmann et al., 2020), which was particularly crucial for family business survival during the COVID-19 crisis (Leppäaho & Ritala, 2022).

The Interplay of Conditions Influencing CEO Resilience

SCT suggests that the psychological resilient nature of CEOs does not come from a vacuum but is a result of person-environment interactions. Informed by the SCT perspective and the literature, we suggest that a key individual-level condition that is associated with self-efficacy of a CEO is his or her tenure or length of work life in the firm (Hambrick & Gregory, 1991; Luo et al., 2014). A longer tenure in the family business helps CEOs build up tacit knowledge (e.g., firm- and market-specific knowledge and general knowhow; Chirico, 2008) and social capital (e.g., networks, relationships, and trust), which enables them to develop positive cognition of themselves during crises and pursue bolder and more innovative business strategies (Boling et al., 2016; Graf-Vlachy et al., 2020). These CEOs are likely to be more confident in their competency and contribute in terms of having access to strategic resources to respond to changing external conditions. However, entrenchment to tradition or past experiences may mitigate their resilience (Finkelstein & Hambrick, 1990). A shorter tenure in the family business on the other hand can also be a strategic asset as CEOs may be able to enhance organizational adaptability to external crises (Hambrick & Gregory, 1991; Luo et al., 2014) by being willing to undertake radical business strategies to prove their executive capabilities (Hoskisson et al., 2016). However, the decision-making by shorter-tenured executives is likely to be constrained by a lack of firm- and industry-specific knowledge (Hamori & Koyuncu, 2015; Quigley et al., 2019) or inadequate experiences.

Given the emphasis on self-efficacy in SCT, we further suggest that the age of the CEO may be related to CEO resilience. Strike et al. (2015) show that as family CEOs grow older, their decision-making tends to become more conservative, which influences their resilience. Older CEOs often prioritize long-term stability over immediate gains; in particular, CEOs near retirement age often prefer legacy and reputation over short-term profit maximization. In addition, the CEO’s level of education may also be related to CEO resilience (Beber & Fabbri, 2012). King et al. (2016) and Farag and Mallin (2018) recognize that CEOs with postgraduate education are more likely to take risks. Similarly, Lee and Moon (2016) find that those with tertiary education are more likely to be high-risk and/or high-performance individuals rather than low-risk and/or low-performance ones. From the SCT perspective, the acquired requisite skills and knowledge that come with education, age, and tenure relate to CEOs’ risk-taking and adaptive decisions. These skills and knowledge are crucial to how individuals navigate through uncertainties (Schunk, 2012).

In addition to the individual-level conditions, there are family-level conditions that are associated with CEO resilience in times of crises (Calabrò et al., 2021; Minichilli et al., 2016). From the SCT perspective, this aligns with the influence of social persuasion from similar and credible others on self-efficacy (Schunk, 2012). Social persuasion in a family business can emerge through family social capital and family influence on the board (Minichilli et al., 2016; Pittino, Chirico, et al., 2020). In family businesses, owing to long-term interactions among family members, both professionally and privately, family social capital can be rich, since family members have developed detailed knowledge of each other’s respective strengths and weaknesses and established shared sentiments and culture (Eddleston et al., 2010; Miller & Le Breton-Miller, 2003). These relational bonds can function as a significant source of CEOs’ belief in the competency of business families during crises such as COVID-19, on the ground that family members’ interactions are based on mutual understanding, trust, and reciprocity, rather than through monitoring and formality (Danes et al., 2009). For many family businesses, this relational and informal way of conducting business goes well beyond the business family (Habbershon & Williams, 1999; Karlsson, 2018).

Family social capital enables CEOs to leverage internal and external social bonds to pursue the business’ strategic aims (Hoffman et al., 2006). In times of crisis, family social capital tied to internal stakeholders may be leveraged to mitigate the shocks on social cohesion and morale (Aldrich & Meyer, 2015; Polyviou et al., 2019), enabling adjustments in business operations, as well as facilitate collective decision-making among family members based on their respective experiences and knowledge (Eddleston et al., 2010; Salvato et al., 2020). Furthermore, by leveraging family networks and relations to external stakeholders, CEOs can receive additional business signals during uncertain periods that can contribute to bridging the information gaps (Stacchini & Degasperi, 2015). Relations with external stakeholders—prominently customers, suppliers, and investors—may also be leveraged to provide support in responding to adverse changes (Miller & Le Breton-Miller, 2003). By leveraging the relationships built upon reputation and trust, rather than contractual solutions, businesses may create favorable conditions that enable them to maneuver during uncertain times (Lins et al., 2017).

However, the presence of family social capital alone cannot be ubiquitously translated to social persuasion (Schunk, 2012) from the family to CEOs’ self-efficacy. Family influence on the business board may also play a role (Hoffmann et al., 2014). For instance, in conjunction with the previously mentioned conditions, family influence on the board may be jointly responsible for the presence or absence of CEO resilience. Family directors have been found to be instrumental in shaping business operations, such as preserving family and business values across generations (Bammens et al., 2011). Family directors also provide relational resources that can be useful in product diversifications (Jones et al., 2008), shield the business from dysfunction based on trust, and guide decision-making toward better financial performance (Basco, 2014). Notwithstanding, Garcia-Ramos and Garcia-Olalla (2011) note that the presence of outside directors on the board have positive influence on business performance in founder-managed firms, while the opposite has been found in businesses led by succeeding generations.

Finally, SCT perceives psychological functioning as a by-product of person–environment interactions (Bandura, 1986; Correani et al., 2020; Wood & Bandura, 1989). During the COVID-19 crisis, a focus on innovation and digitalization became crucial for the survival of many family businesses, and those firms that built up slack resources during calm periods fared substantially better (Leppäaho & Ritala, 2022). However, leveraging the value from slack resources in the case of digitalization necessitates e-business capabilities. E-business capabilities in this study are defined as the capabilities that a business applies “internet-based technologies to conduct both downstream and upstream business activities along the value chain” (Bi et al., 2017, p. 559). E-business capabilities in general enable companies to reduce operational costs, increase sales revenue, and create value through introducing original business models (Remane et al., 2017). In the wake of industry 4.0, e-business capabilities might benefit small-sized family businesses in particular (Müller et al., 2018). E-business capabilities can help small firms leverage value by optimizing internal processes, providing accurate information about product/service specifications that business partners need, and accelerating the speed at which they can respond to customer/supplier needs (Correani et al., 2020). E-business capabilities also allow wider customer/supplier reach, easier communication, and more efficient monitoring across the value chain (Müller et al., 2018).

During COVID-19, e-business capabilities became prominent, due to the repeated lockdowns and distancing measures adopted by policymakers. Businesses assumed smart working for their employees and transformed a significant number of interactions with clients, suppliers, and other stakeholders into an e-business mode (Durakovic et al., 2022). Nevertheless, developing e-business capabilities poses management challenges such as how to utilize digital technologies to grow and be sustainable, and how to develop flexible, agile, or “malleable” organizations that align with digital technologies (Hanelt et al., 2021). These challenges often demand adjustments of approaches, including engaging with business partners and reconstructing internal processes to achieve alignment (Wu et al., 2003). Research further suggests that family business conditions complexify this task. For instance, digitalization challenges family business identity (Caspersz et al., 2017) and can lead to family discord (Tomaselli et al., 2021).

In conclusion, the literature uncovers a range of internal and external cues that influence CEO resilience. Internal cues include conditions of tenure, age, and education, while external cues emerge from family influence on the board, family social capital, as well as the business-level condition of e-business capability. The SCT perspective suggests that rather than operate in isolation, these conditions may be interconnected across different levels to influence CEO resilience to cope with adversity.

Differences Between Family Businesses Controlled by a Single Generation or by Multiple Generations

When studying CEO resilience in times of crisis, an important distinction must be made between family businesses run by a single generation and those run by multiple generations. Single- and multi-generational family businesses are likely to differ in their conditions fostering CEO resilience because of the following reasons: (a) differences in social persuasion from similar others, and (b) differences in levels of cognitive diversity. In relation to (a), the SCT perspective suggests that a key source of CEO’s self-efficacy is social persuasion from similar and credible others (Schunk, 2012). In family businesses, this social persuasion mainly stems from the interaction between CEOs and family members involved in the family business. When multiple generations are involved in the family business, the older generation, due to their long-term engagement with the existing stakeholders, is often path-dependent in strategic outlook (Sydow et al., 2009), while the younger generation strives to seek new opportunities and challenges the status quo (Hauck & Prügl, 2015). As such, social persuasion from a single- and multi-generational family business varies, which may affect CEOs’ self-efficacy and their resilience (Milaković, 2021; Ojo et al., 2021). In relation to (b), Pittino, Chirico, et al. (2020), in their study of the relationship between generational involvement and business growth, confirm that “the presence of multiple generations increases cognitive diversity” (p. 795). In single-generational family businesses, however, cognitive diversity is less significant. They tend to follow congruent approaches and pursue similar strategies. Past studies suggest that different levels of cognitive diversity may lead to differences in CEO self-efficacy and resilience (Shin et al., 2012).

Research Methodology

Sample and Data

The fsQCA analytical approach was used to understand the interconnectedness between individual-, family-, and business-level conditions and CEO resilience. This approach is appropriate for analysis of a small- to medium-sized sample (Pittino et al., 2018; Ragin, 2008) and is suitable in modeling configurational relationships and equifinality (Schneider et al., 2010), when the knowledge on causal conditions is limited, and when available theories lack explanatory power (Täuscher, 2018).

The data-collection step utilizes the “Bel-first” Bureau van Dijk database, which is a comprehensive national database of businesses in the Flemish region. In the sampling frame, there were a total of 22,813 companies with at least 10 employees in the Flemish region, excluding the Brussels region. The motivation for studying the Flemish region only, rather than all of Belgium, is twofold. First, since the Flemish region contains most of all family businesses in Belgium (approximately 77.0%), this region is arguably an appropriate place for investigation of family business (Ceysens, 2008). Second, the economic significance of the Flemish region in the Belgian economy (Organisation for Economic Co-Operation and Development, 2018) is of particular interest to policy-makers. 1

To yield representativeness, a random sample of 1,000 businesses was selected. The questionnaires were posted with a cover letter to executives or managing directors of businesses in July 2020. In the questionnaire, respondents were asked whether they considered the company to be a family firm to distinguish family firms from non-family firms. Eight weeks after the initial mailing, a second wave was sent to non-respondents. Following the two survey waves, a total of 110 responses were received, leading to a response rate of 11.0%. Of these responses, 79 (71.8%) were from family businesses. Twelve out of 79 businesses were managed by the founders without the involvement of family members from the second generation. Since there is a debate about the classification of these businesses as family businesses (Miller et al., 2007), we removed these lone-founder firms from the sample. A total of 67 family businesses ultimately formed the study sample, while data were collected from family CEOs. As the fsQCA method is suitable for small samples (Ragin, 2008), the sample in the present study is considered sufficient (Huang et al., 2023; Schneider & Wagemann, 2012).

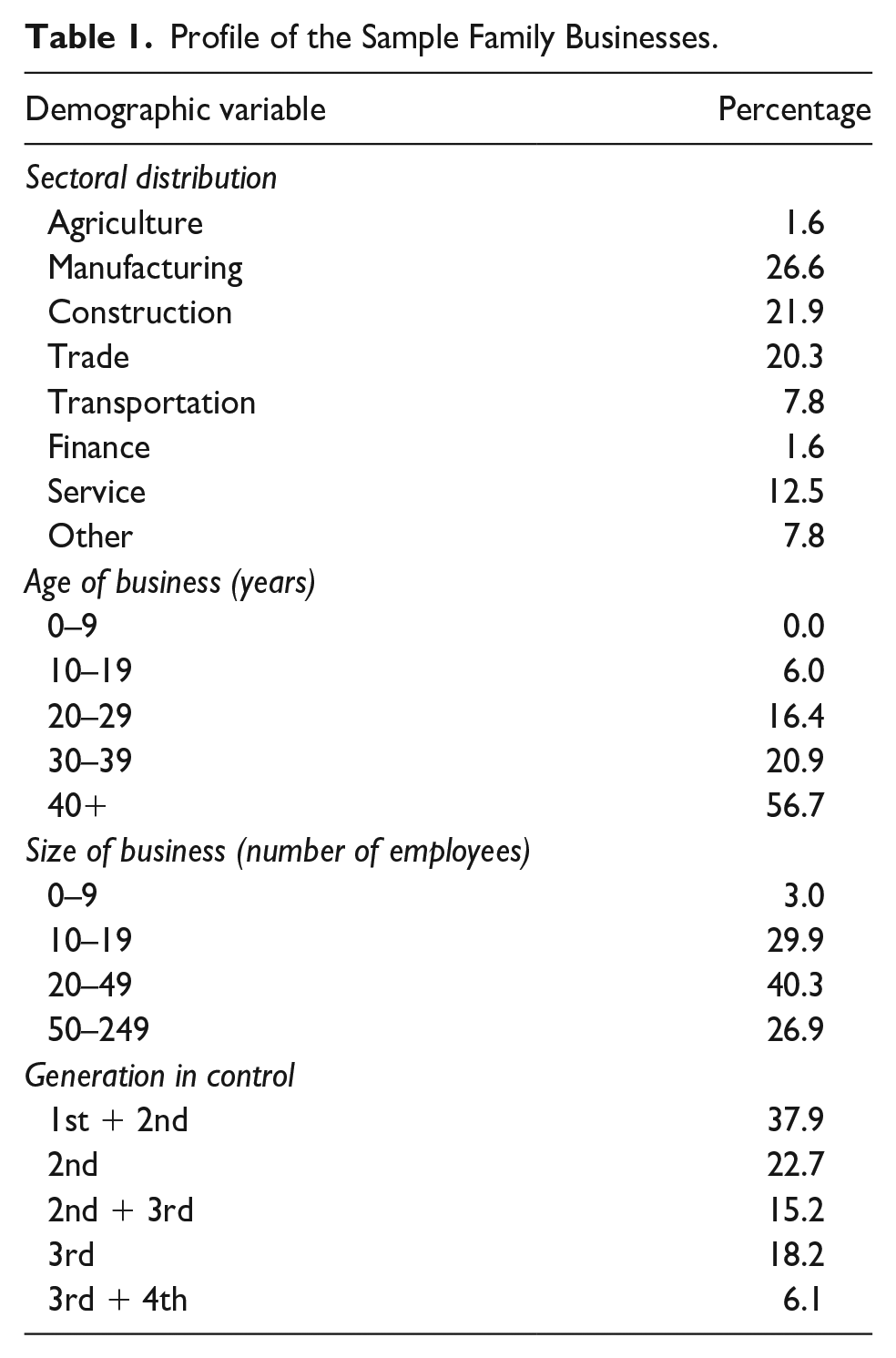

Table 1 presents the profile of the sample companies. In terms of sectoral distribution, most firms are in traditional manufacturing, construction, trade, and service sectors, with fewer in transportation, finance, and agriculture domains. It is found that 56.7% of the firms are more than 40 years old, while 20.9% are between 30–39 years of age. In contrast, only about 6.0% of firms are 10–19 years old. In addition, 40.3% of firms have 20–49 employees, while 26.9% of firms are medium-sized with 50–249 employees. Finally, in terms of the family generation in control, 37.9% of firms are governed jointly by the first and second generations. Meanwhile, 22.7% of businesses are managed solely by the second generation, and 15.2% are jointly managed by the second and third generations. In addition, 18.2% of businesses are administered by the third generation, while 6.1% are managed by the third and fourth generations together.

Profile of the Sample Family Businesses.

To assess the possible presence of non-response bias, early and late respondents were compared on demographic variables, such as business size, age, sector, and generation in control (Stanley & Wisner, 2001). The results show no significant differences between the two groups of respondents at the 0.05 level.

Variables and Constructs

Outcome

The outcome variable—CEO resilience—is based on the construct developed by Santoro et al. (2021). This scale includes items related to a CEO’s intention to look for ways to replace the losses encountered, to learn and develop by dealing with difficult situations, to find creative ways to resolve problems, and to respond to unforeseen changes. Respondents were requested to rate the extent to which each statement accurately described the business behavior based on a five-point scale, anchored by 1 (not describing at all) to 5 (describing very well).

Conditions

Individual Level

For CEO demographics, the number of years a CEO has been working with a firm is utilized as an indicator of CEO’s tenure. Next, the absolute age of the CEO is used to measure seniority. Finally, the educational level of each CEO is measured on a five-point scale ranging from 1 (primary school) to 5 (PhD).

Family Level

To assess family social capital, we adapted the scale developed by Carr et al. (2011). Example items include “family members who work in this firm have confidence in one another” and “family members who work in this firm are usually considerate of each other’s feelings.” Responses from participants were recorded on a five-point scale ranging from 1 (strongly disagree) to 5 (strongly agree). Family influence on the board is accessed via a proxy variable, defined as the share of family members present in the board of directors.

Business Level

We adapted the e-business capability scale developed by Wu et al. (2003). Participants were asked to indicate their e-business capability in managing customers, internal processes, and suppliers by using a five-point scale ranging from 1 (strongly disagree) to 5 (strongly agree). Example items include “we use e-business to provide solutions to customer problems,” “we use e-business to facilitate internal communication between employees in different departments and different locations,” and “we use e-business to provide specific online information about product specifications that suppliers/business partners must meet.”

Validation of the Constructs

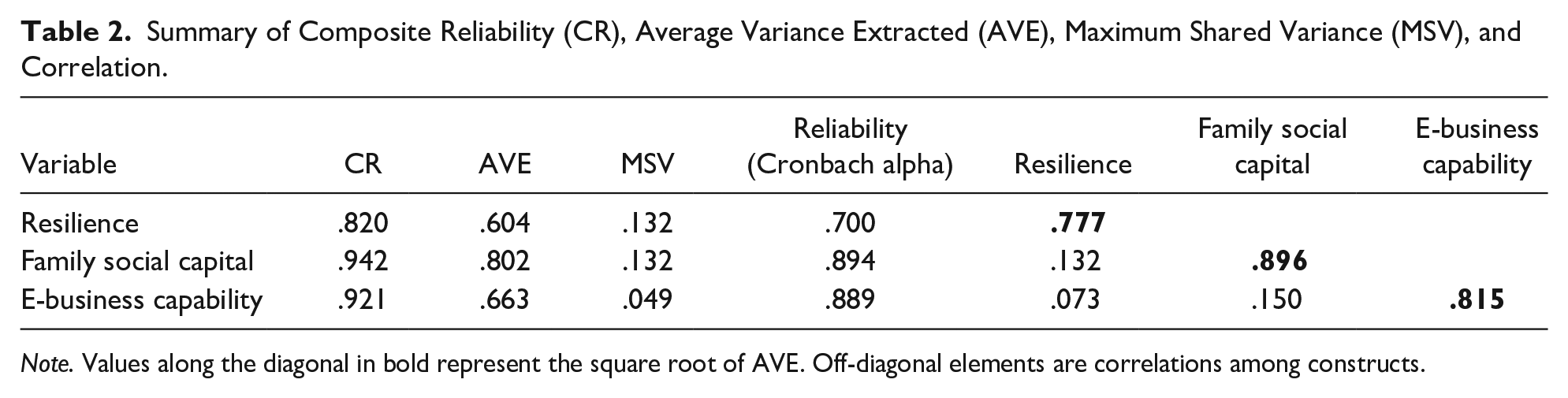

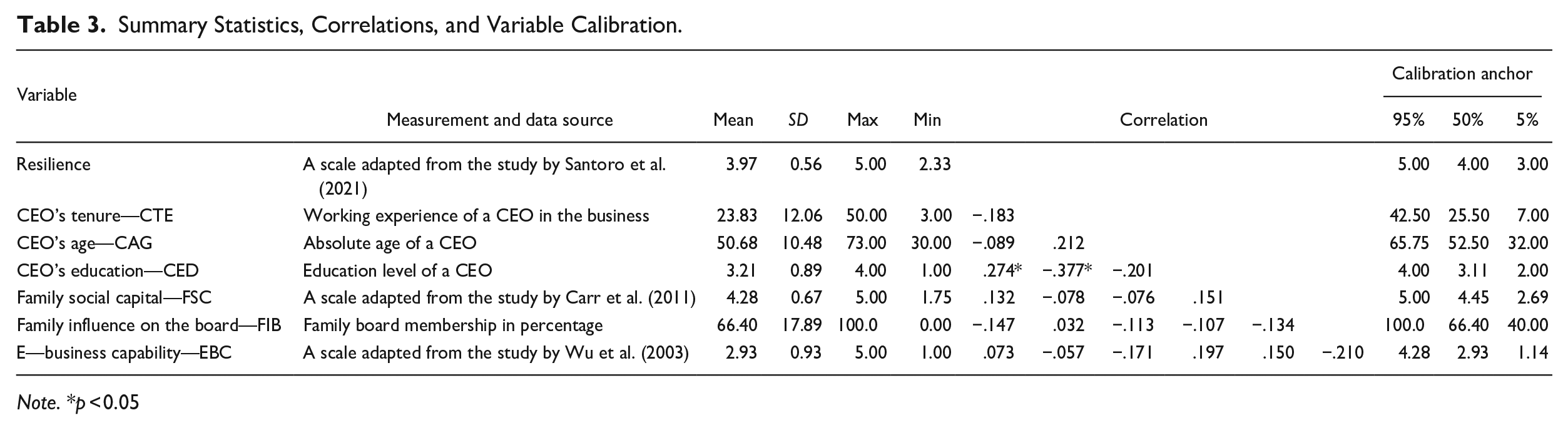

The multi-item constructs CEO resilience, family social capital, and e-business capability were validated through confirmatory factor analysis (CFA). The reliability of each scale is assessed (Table 2), where all constructs show reasonable to strong reliability (respectively, Cronbach alpha for CEO resilience = .700, composite reliability (CR) = .820; Cronbach alpha for family social capital = .894, CR = .942; Cronbach alpha for e-business capability = .889, CR = .921). Moreover, results indicate that each construct is empirically distinct from other constructs. This is evidenced by the fact that in Table 2, all three constructs meet the condition set by Fornell and Larcker (1981) that the square root of their average variance extracted (AVE) is greater than their correlation with other constructs. Furthermore, the fit index suggests that the measurement model provides an acceptable fit for the data: χ2 = 89.483, df = 65, χ2/df = 1.377, p = .000 (Hair et al., 2010). Good fit is also demonstrated by root mean square error of approximation (RMSEA) = 0.076, comparative fit index (CFI) = 0.939, and Tucker-Lewis index (TLI) = 0.927 (Hair et al., 2010). Other fit indices, such as GFI and NFI, are slightly below the value of 0.900. This might be due to the relatively small sample size of 67 in the study (Hair et al., 2010). To avoid multicollinearity, we further examined the intercorrelations among all employed variables. The relatively low values suggest that multicollinearity is not a major problem (Table 3).

Summary of Composite Reliability (CR), Average Variance Extracted (AVE), Maximum Shared Variance (MSV), and Correlation.

Note. Values along the diagonal in bold represent the square root of AVE. Off-diagonal elements are correlations among constructs.

Summary Statistics, Correlations, and Variable Calibration.

Note. *p < 0.05

Fuzzy Sets and Calibration

In an initial step of fsQCA, the outcome and antecedent condition variables were calibrated. The purpose of calibration is to categorize original values into meaningful groupings based on anchor points (Ragin, 2008). In general, calibration should be based on a theory or on substantive knowledge of the phenomenon (Ragin, 2008). However, for our study, there were no theoretically defined membership thresholds we could refer to, nor were there any studies on the topic to show the distribution of the variables of interest. Thus, an alternative approach was followed, that is, direct calibration (Ragin, 2008), which established three thresholds to structure the degree of membership to a set under study. Anchors near the 95th, 50th, and 5th percentiles were used as thresholds, respectively, for full membership (coded as 1), crossover membership (coded as 0.5), and non-membership (coded as 0). This calibration approach has been adopted by Lapeira et al. (2024), Pappas and Woodside (2021), and Sahin et al. (2019). The statistics of outcome and conditional variables and the fuzzy set calibration rules are presented in Table 3.

Results

Analysis on the Necessary Conditions

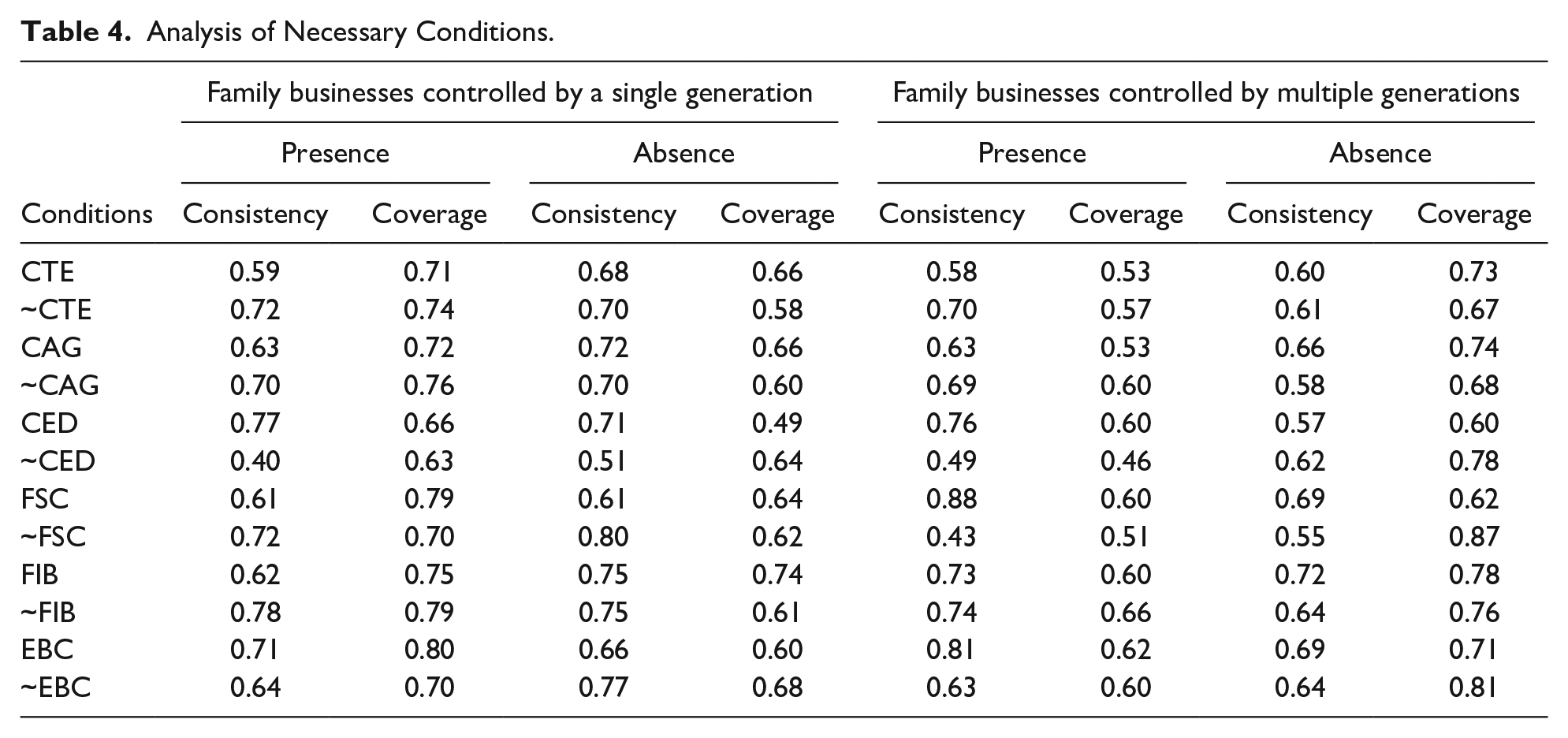

The fsQCA analysis begins with a necessity analysis, which determines if any of the conditions used in the study can be considered as necessary for causing the outcome, that is, always present or absent in all cases where the outcome is present or absent (Pittino et al., 2018; Ragin, 2006). In the necessity analysis, the fsQCA provides consistency and coverage scores, which indicate the degree of fitness of the cases in a dataset to an association of necessity. For a causal condition to be considered as necessary, the thresholds of consistency and coverage are, respectively, 0.90 and 0.80 (Sahin et al., 2019; Schneider & Wagemann, 2012). The sampled 67 family businesses in this study were separated into two groups, that is, those controlled by a single generation or by multiple generations, to explore configurations of conditions that nurture CEO resilience.

Table 4 presents the results of the necessity analysis for a high level of CEO resilience in both groups, as well as for a low level of CEO resilience. For the group of family businesses controlled by a single generation, the consistency scores vary between 0.40 and 0.80, with the coverage scores changing between 0.49 and 0.80 (for both presence and absence). For those family businesses in the hands of multiple generations, the consistency scores are located between 0.43 and 0.88, while the coverage scores vary between 0.46 and 0.87 (for both presence and absence). None of the six conditions passes the thresholds of consistency and coverage simultaneously; therefore, these conditions are not necessary to lead to a high or low level of CEO resilience.

Analysis of Necessary Conditions.

Analysis on the Sufficient Conditions

The sufficient conditions analysis was implemented to identify the conditions that have a sufficient relationship with the outcome variable. The analysis of the sufficient conditions follows three main steps (Fiss, 2011; Ragin, 2008; Sahin et al., 2019). The first step is the construction of a fuzzy set truth table. A rule needs to be outlined to reduce the truth table to meaningful configurations. According to Ragin (2008) and Fiss (2011), in the present study, the consistency threshold was set at 0.80, and the frequency threshold for the number of observations was set at one. That is, configurations with one or more observations and a consistency of more than 0.80 are regarded as sufficient for the outcome. In the third step, the Quine–McCluskey algorithm based on Boolean algebra is used to minimize the truth table logically.

The fsQCA produces three sets of solutions, namely complex, parsimonious, and intermediate solutions (Ragin, 2008). An intermediate solution is often the preferred solution (Ragin, 2008). This is obtained when performing counterfactual analysis on complex and parsimonious solutions including only theoretically plausible counterfactuals (Ragin, 2006, 2008).

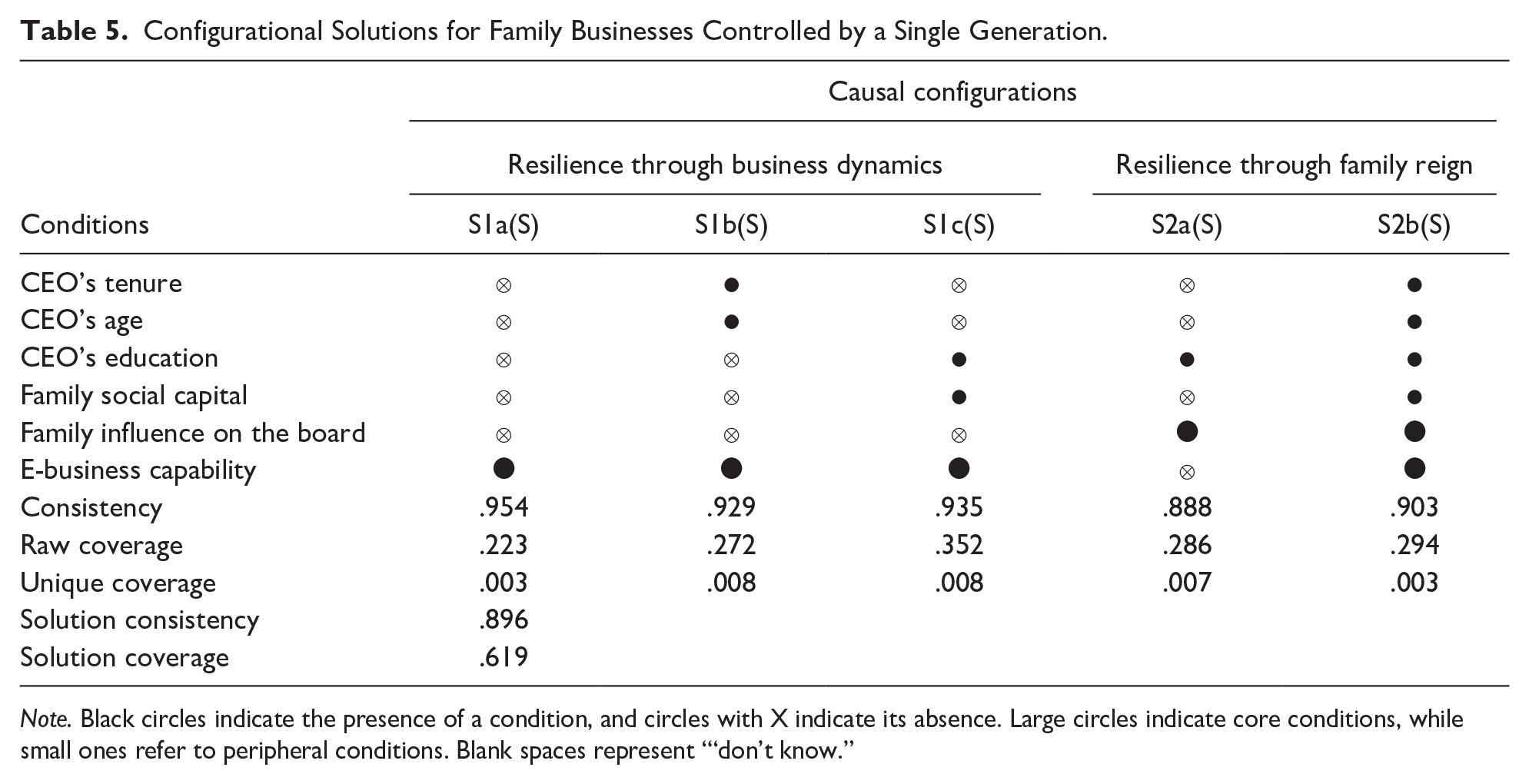

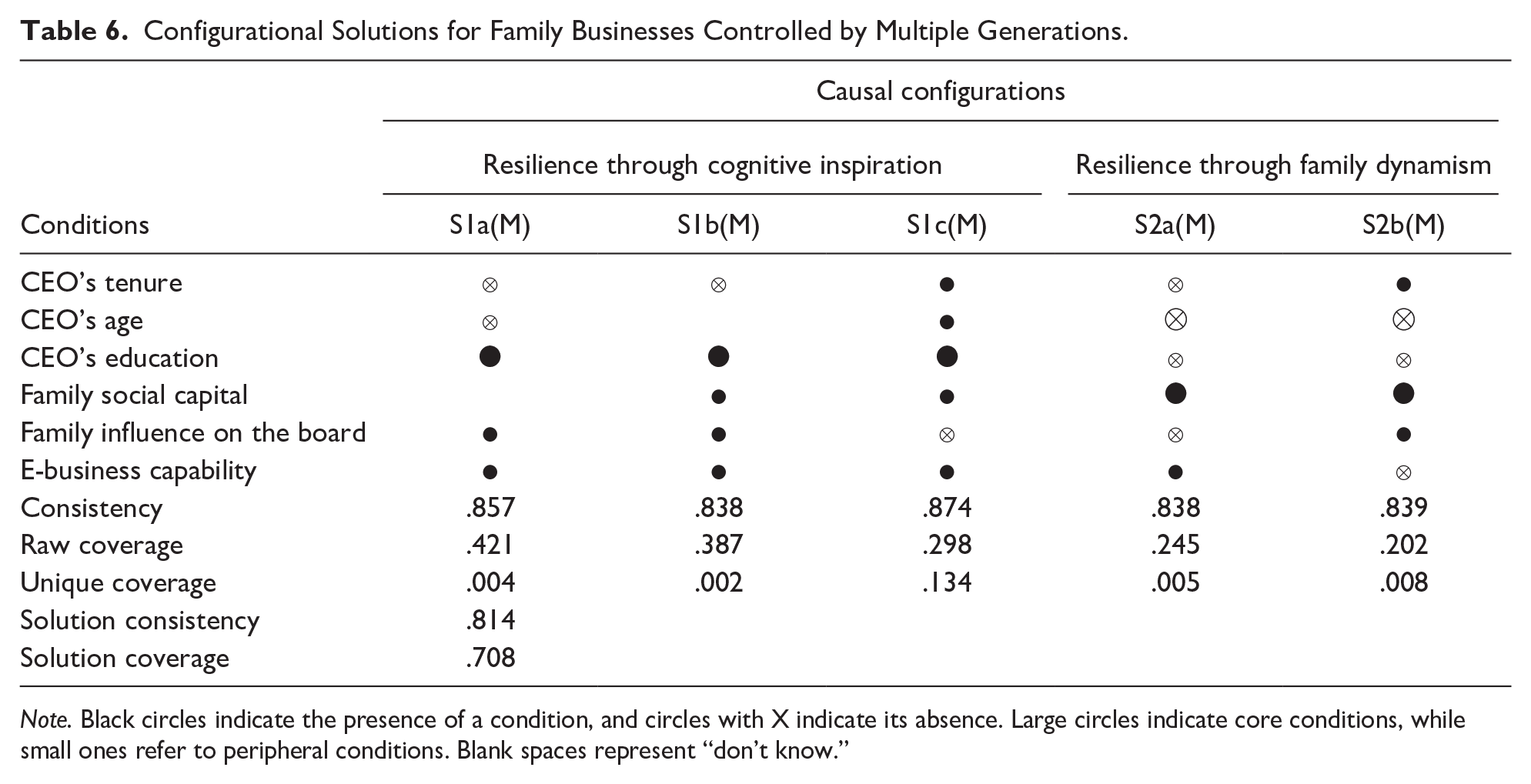

Tables 5 and 6 present the intermediate solutions for the two groups. In the tables, full black circles (●) represent the presence of a causal condition, while circles with a cross-out (⊗) indicate the absence of a causal condition. Blank spaces in a solution represent an “inconclusive” finding, that is, a particular condition does not appear in the configuration. Furthermore, a large circle in a solution represents the presence of a core condition, while a small circle refers to a peripheral condition (Fiss, 2011). The intermediate solution for family businesses managed by a single generation (Table 5) has a consistency of 0.896 and coverage of 0.619, whereas the solution for those managed by multiple generations (Table 6) has a consistency of 0.814 and coverage of 0.708. The consistencies for both groups of family businesses are above the acceptable thresholds of 0.80 (Fiss, 2011; Ragin, 2008). Thus, the solutions provide convincing information on the conditions that lead to the outcome (Ragin, 2008).

Configurational Solutions for Family Businesses Controlled by a Single Generation.

Note. Black circles indicate the presence of a condition, and circles with X indicate its absence. Large circles indicate core conditions, while small ones refer to peripheral conditions. Blank spaces represent “‘don’t know.”

Configurational Solutions for Family Businesses Controlled by Multiple Generations.

Note. Black circles indicate the presence of a condition, and circles with X indicate its absence. Large circles indicate core conditions, while small ones refer to peripheral conditions. Blank spaces represent “don’t know.”

The results for family businesses in the hands of a single generation show five configurational solutions (S1a(S), S1b(S), S1c(S), S2a(S), and S2b(S)), where both core and peripheral conditions are indicated (Table 5). E-business capabilities and a high level of family influence on the board are core conditions. Details of these solutions are described as follows:

S1a(S): Short-tenured, junior, and less-educated CEOs, with the absence of family social capital and family influence on the board, and the presence of e-business capabilities.

S1b(S): Long-tenured, senior, and less-educated CEOs, with the absence of family social capital and family influence on the board, and the presence of e-business capabilities.

S1c(S): Short-tenured, junior, and well-educated CEOs, with the presence of family social capital and e-business capabilities, and the absence of family influence on the board.

S2a(S): Short-tenured, junior, and well-educated CEOs, with the absence of family social capital and e-business capabilities, and the presence of family influence on the board.

S2b(S): Long-tenured, senior, and well-educated CEOs, with the presence of family social capital, e-business capabilities, and family influence on the board.

The results for multiple generations involve another five configurational solutions (S1a(M), S1b(M), S1c(M), S2a(M), and S2b(M); see Table 6). Three core conditions are prominent in these solutions. The first core condition, CEO’s education, is present in solutions S1a(M)–S1c(M), while the second and third core conditions, family social capital and CEO’s age, are shown in solutions S2a(M) and S2b(M).

S1a(M): Short-tenured, junior, and well-educated CEOs, with the presence of family influence on the board and e-business capabilities.

S1b(M): Short-tenured but well-educated CEOs, with the presence of family social capital, family influence on the board, and e-business capabilities.

S1c(M): Long-tenured, senior, and well-educated CEOs, with the presence of family social capital and e-business capability and the absence of family influence on the board.

S2a(M): Short-tenured, junior, and less-educated CEOs, with the presence of family social capital and e-business capabilities and the absence of family influence on the board.

S2b(M): Long-tenured, junior, and less-educated CEOs, with the presence of family social capital and family influence on the board and the absence of e-business capabilities.

Robustness Tests

To evaluate the stability of the configurational solutions, several robustness checks were carried out. First, the consistency threshold was adjusted to 0.83 (Sahin et al., 2019). For both samples, only minor changes were observed. Second, additional robustness checks were carried out by using the same conditions but with innovativeness in family businesses as the outcome variable, instead of CEO resilience. If similar configurations to those for resilience were identified, then the configurational solutions presented in Tables 5 and 6 would not be reliable. The results show, however, that the two models do not produce similar solutions, which suggests the robustness of the proposed conceptual framework for CEO resilience.

Discussion

This study adopts the fsQCA analytical approach to analyze CEO resilience. We argue that the fsQCA technique is particularly useful in our study. This is because the technique captures the complex interconnection between conditions at the individual, family, and business environments, which together and through various paths contribute to similar outcomes (equifinality) in terms of the presence or absence of family CEO resilience. While the traditional regression analysis might highlight the role of individual factors, fsQCA in our study reveals specific combinations that influence CEO resilience. This is important for family business research as family firms are highly heterogeneous. The fsQCA technique can accommodate this diversity by identifying configurations that are effective for certain types of family businesses but not for others (Pittino, Visintin, & Lauto, 2020).

Our results show significant differences in configurational solutions for family businesses controlled by single and multiple generations. For single-generational family businesses, CEO resilience emerges from conditions at the business and family levels. In contrast, CEO resilience in multiple-generation families appears to be associated with personal-level conditions, coupled with family-level conditions whereby it appears a more intimate family relationship fosters the resilience of the CEO. We discuss these findings in the following sections and subsequently indicate a set of propositions postulating conditions at the individual, family, and business levels that influence CEO resilience. We subsequently expand our findings and offer an emergent theoretical perspective, which we call a “crisis bricolage” phenomenon. We conclude this section with our contributions to theory and practice and the limitations of our study.

Understanding CEO Resilience

CEO Resilience in Single-Generational Family Businesses: Resilience Through the Dynamics at the Business and Family Levels.

The configurational analysis shows that CEO resilience in single-generational family businesses is nurtured through conditions at the business and family levels. Particularly, e-business capabilities are prominent among conditions in configurational solutions S1a(S), S1b(S), and S1c(S), suggesting a “resilience through business dynamics” scenario. The effective and efficient use of e-business capability “is a key factor differentiating successful firms from their less successful counterparts” (Bharadwaj, 2000, p. 169). While e-business capabilities can reduce human interference in the operational processes and increase efficiency and transparency, they also offer an opportunity to firms to engage in smart manufacturing/servicing (Müller et al., 2018). Moreover, e-business capabilities can help build new mechanisms to interact with suppliers, customers, and other strategic stakeholders, enabling the establishment of long-term business relationships. From the SCT perspective, this can be interpreted that when family businesses show competent e-business capabilities, the external cue emanating from such capacity inspires the family CEO’s self-efficacy and arouses his or her resilience to overcome the obstacles in times of adversity (Bandura, 1982; Wood & Bandura, 1989).

Furthermore, the study findings provide a nuanced view by highlighting that family influence on the board is a core present condition for CEO resilience in S2a(S) and S2b(S), suggesting a scenario of “resilience through family reign.” Strong family influence on the board nurtures the CEO’s attachment to the business and their desire to create economic and social value (Chirico & Nordqvist, 2010; Soluk et al., 2021). Strong attachment further drives CEOs to be long-term oriented (Davis et al., 1997). They often show a unique sense of responsibility toward businesses, “perceiving the business as a cherished heirloom that demands carrying the burden of preserving it for future generations” (Yilmaz et al., 2024, p. 68). They are willing to use their resources and wisdom and adopt flexible strategies to salvage the business whenever possible. Strong family influence also enables the sharing of family values, which often emphasize loyalty, trust, dedication, and altruism (Minichilli et al., 2016). The transition of these values fosters commitment (Yilmaz et al., 2024) and is conducive to the development of CEO resilience.

Thus, in single-generational family firms, the results suggest that business and family conditions enable CEO resilience. From the SCT perspective, this means CEO resilience extends beyond individual-level conditions and is instead shaped by externalities (Gist & Mitchell, 1992) such as e-business capabilities, as well as social persuasion (Schunk, 2012) from the family. We thus propose that:

CEO Resilience in Multi-Generational Family Businesses: Resilience Through the Individual and Family Dynamics.

In multi-generational family businesses, CEO resilience stems from the individual and family conditions. In configurational solutions S1a(M), S1b(M), and S1c(M), the CEO’s education is a core present condition, suggesting a “resilience through cognitive inspiration” phenomenon. From the SCT perspective, enactive mastery of knowledge and skills as attained through education may inspire the CEO’s self-efficacy to overcome obstacles (Bandura, 1982; Wood & Bandura, 1989). Studies in psychology have confirmed the connections between an individual’s educational attainment, cognitive ability, and decision-making capacity (King et al., 2016). Individuals’ intelligence, informed by education, influences their decision-making ability (Lubinski & Humphreys, 1997), with those having a higher level of intelligence demonstrating greater patience and taking actions less based on impulse (Parker & Fischhoff, 2005). King et al. (2016) further affirm that CEOs with good-quality postgraduate qualifications such as MBAs are likely to feel more confident in taking risks and help the businesses to achieve superior performance. You et al. (2020) note that education improves CEOs’ cognitive capability in dealing with disruptions.

In configurational solutions S2a(M) and S2b(M), family social capital and the age of the CEO are, respectively, core present and absent conditions, suggesting a “resilience through family dynamism” scenario. From the SCT perspective, social persuasion (Schunk, 2012) is influential in CEO resilience. However, in contrast to single-generational family businesses, social persuasion in multi-generational firms is effected through family social capital, especially when younger CEOs are at the helm. Research notes that the presence of multiple generations fosters cognitive diversity (Pittino, Chirico, et al., 2020; Sciascia et al., 2013). The older generation often prioritizes long-term stability (Strike et al., 2015), while the younger generation is apt to seek innovative, yet sometimes risky, solutions (Hauck & Prügl, 2015; McClelland et al., 2012). While the diversity between generations may inspire ideas and perspectives in tackling difficult situations (Wiersema & Bantel, 1992), it may result in decreased effectiveness in decision-making, relational conflict, and disagreement (Villanueva & Sapienza, 2009; Wang & Beltagui, 2023). Under these circumstances, the presence of family social capital may stabilize the firm (Cabrera-Suárez et al., 2015). Moreover, family social capital enables younger family directors to share their networks in times of crisis, while extended networks are conducive to information absorption, inspection, and assimilation (Zahra et al., 2004), facilitating family businesses to promptly react to the threats posed by the crisis. Family social capital may also galvanize family members to behave as stewards (Davis et al., 2010; Wang & Shi, 2021). This stewardship and family cohesiveness can function “as a cushion for the family and the firm in times of crises” (Calabrò et al., 2021, p. 2).

Thus, in multi-generational firms, the results unravel that the individual and family conditions engender an influence on CEO resilience. With time and particularly as family businesses become characterized by multiple generations, the CEO may become more adept at juggling personal- and family-level conditions that subsequently inspire their resilience. To summarize, we offer the following propositions:

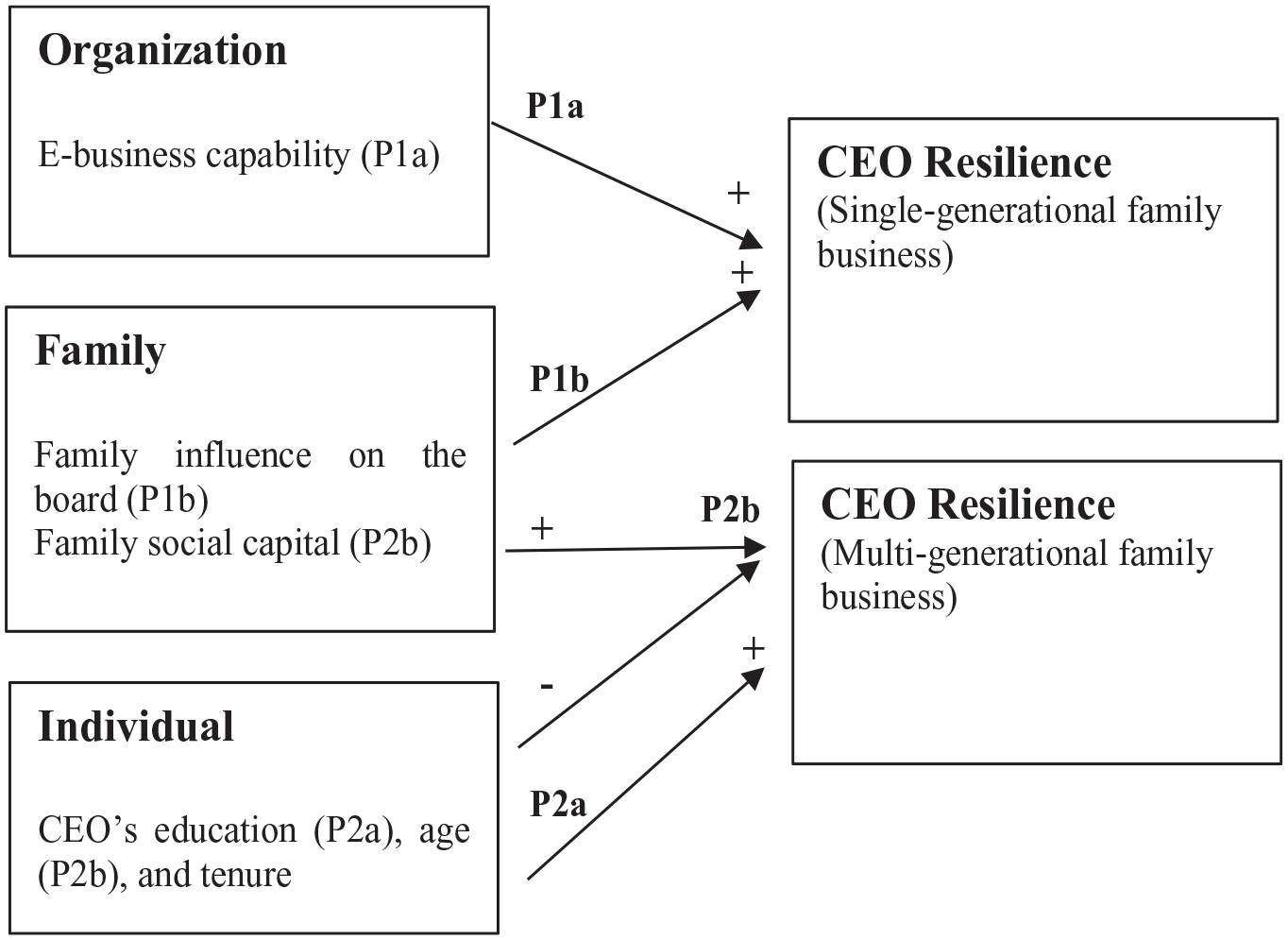

Propositions on Conditions Influencing CEO Resilience in Family Business.

Emergent Theoretical Perspective—A “Crisis Bricolage” Phenomenon

The first aspect of the emergent theoretical perspective that we offer is that CEO resilience in family firms reflects an interconnected phenomenon. In keeping with SCT (Bandura, 1982; Wood & Bandura, 1989), these include a sense of mastery in the case of education and age (multi-generational firms), social persuasion from family influence on the board (single-generational firms) and family social capital (multi-generational firms), and external cues emanating from e-business capability (single-generational firms). To further nuance this emergent theoretical perspective (Waldkirch et al., 2021), we argue CEO resilience is nurtured by conditions at different levels (i.e., individual, family, and business levels). In the case of single-generational family firms, CEO resilience is associated with the family- and business-level conditions, while in the case of multi-generational family firms, CEO resilience emanates from the interaction of individual- and family-level conditions.

The second aspect of the emergent perspective that we cast light on is the conceptualization of family influence. Despite the differences between single- and multi-generational firms in how conditions at the family level interconnect with those at the individual and business levels, the findings invoke the insight that family-level conditions remain crucial in fostering a positive context that nurtures CEO resilience (Hartmann et al., 2020; Raetze et al., 2021). That is, in times of crisis, the family counts, either through family reign or family dynamism. Potentially, this is because the family can provide a sense of belonging (Björnberg & Nicholson, 2012), identity fit (Akhter et al., 2016), and shared sentiments and organizational culture (Eddleston et al., 2010), which subsequently enables the CEO to be resilient and successfully maneuver the firm during times of crisis.

This observation informs a third aspect of our emergent theoretical perspective, which is that times of crisis trigger resilience through entrepreneurial “crisis bricolage.” Baker and Nelson (2005) invoke Levi-Strauss’s (1962) concept of bricolage when observing that small firms in their study were able to “create something from nothing by exploiting physical, social, or institutional inputs” (p. 329). Our study shows a similar phenomenon. That is, under crisis circumstance, the family CEOs drew on resources that were “in hand” and “within reach” to navigate their firms through the crisis. Arguably, “in-hand” resources were those internal to themselves such as education and age, while the “within-reach” resources undoubtedly sat with the “family” (i.e., family members on the board and the social capital linked to the family) and the “business” (i.e., competency reflected in e-business capabilities). Given the exigency of the crisis, family CEOs “made do” with these resources, whereas in normal times, they may have resorted to other resources such as consultants to assist in operational matters or strategists to plan and execute strategic responses. In short, CEO resilience in difficult times reflects a “crisis bricolage” of “making do” with resources that are “in hand” and “within reach.” It may well be that these resources reflect the essence of family CEO resilience when confronted with adversity.

Contributions to Family Business Research

Resilience in family business is under-researched, and the extant literature is often fragmented (Beech et al., 2020; Conz et al., 2020; Linnenluecke, 2017). Past studies, often positioned at either the family or the business level, identify how factors, such as social capital at the family level (Arregle et al., 2007; Hoffman et al., 2006) and capabilities and resources at the business level (Pal et al., 2014), may influence resilience in family businesses. Studies about resilience at the individual level are scarce, and little is known about the conditions that nurture CEO resilience, especially in times of crisis. By exploring how configurations of individual, family, and business conditions shape CEO resilience, this study contributes to opening this “black box” (Sirmon et al., 2007). Particularly, by adopting this cross-level approach, this paper responds to the calls for further research about sources of resilience (Conz et al., 2020) and for multi-level studies about resilience (Gottschalck et al., 2024; Linnenluecke, 2017; Raetze et al., 2021; Smith et al., 2024).

The second contribution is the findings about the distinctive conditions between generations that influence CEO resilience. While CEOs in single-generational family businesses enjoy the benefits of family influence on board and the presence of e-business capabilities to respond to adverse circumstances (Conz et al., 2020; Lengnick-Hall & Beck, 2005), in multiple-generational firms, CEOs’ efficacy in handling adversity benefit from their education, age, and family social capital. By understanding the dynamics of the unique phenomena of generational influence on CEO resilience, the study contributes to the growing interest in disentangling heterogeneity in family business (Jaskiewicz & Dyer, 2017).

Finally, the study extends the application of SCT to family business studies. Inspired by the SCT that views human functioning as the outcome of continuous and reciprocal interactions between personal factors and environmental influences (Bandura, 1988), we examine CEO resilience by considering configurations of conditions across the individual, family, and business levels that inform self-efficacy and subsequently contribute to the resilience of CEOs. The finding that generational involvement is a contingent factor that affects how the embedded unique resource of family in the business nurtures CEO resilience is salient and helps to reveal the delicacy of CEOs’ psychosocial functioning. As such, our study contributes conceptual insights into the development of SCT, specifically in the family business field.

Implications for Practice

The following practical implications emerge from the study. First, the study underscores that policy initiatives should focus on individual- and family-level conditions, as well as business-level competency to strengthen CEO resilience. For instance, while offering support for e-business capabilities development is crucial, programs that strengthen family influence on the board are equally relevant. Policies that facilitate access to advanced education for CEOs and promote the development of family social capital can also bolster CEO resilience. Such an integrated approach may ensure that family businesses are better equipped to navigate crises by leveraging a combination of educational, familial, and technological resources.

However, policy-makers should also recognize the distinct dynamics of single- and multi-generational family businesses. Tailored policies that address the unique needs of each type are more effective. Enhancing e-business capabilities and strengthening family governance structures are critical for CEOs of single-generational firms. In contrast, multi-generational firms benefit more from policies that support continuous education for CEOs and initiatives that enhance family social capital, especially when younger CEOs take the helm. By recognizing and addressing these differences, policies can be more efficient to enhance CEO resilience. In conclusion, the results suggest that an effective policy framework must adopt a holistic and differentiated approach to supporting family firms in future crises.

Limitations

The study has several limitations that nevertheless offer interesting avenues for future research. First, fsQCA requires 2n cases to operate effectively, whereby n represents the number of variables. This means although a wide range of variables at individual, family, and business levels influence CEO resilience, only a subset of these could be incorporated given the sample size. Future studies, based on a larger sample, could scrutinize other conditions, such as emotional stability (Caprara et al., 2013), self-regulation of the CEO (Pérez-López et al., 2019), and entrepreneurial orientation (Lumpkin & Dess, 1996). For instance, a firm’s entrepreneurial orientation (Covin & Lumpkin, 2011; Lumpkin & Dess, 1996) may foster CEOs’ resilience (Gottschalck et al., 2024). An innovative orientation, for example, suggests a trial-and-error approach as a business routine. Such an experimenting approach demands CEOs to tolerate uncertainties and failure (Gottschalck et al., 2024; Wiklund & Shepherd, 2005).

Second, the fsQCA results suggest family social capital plays a significant role in multi-generational family businesses. Arguably, this is because generational involvement is a source of cognitive diversity and conflicts (Pittino, Chirico, et al., 2020; Sciascia et al., 2013). However, generational involvement can also help CEOs acquire and deploy resources, especially when intergenerational relationships are affable. Different educational and professional backgrounds between generations, as well as their complementary perspectives, may facilitate CEOs in making decisions. Collaborative commitments also assist CEOs in risk assessment and management (Chrisman & Patel, 2012; Kammerlander et al., 2020; Kotlar et al., 2020), enabling them to control businesses and preserve financial and non-financial endowments (Soluk et al., 2021). Hitherto, research in generational involvement is almost untapped. Future studies can delve into this arena and examine multiple generations’ role in challenging times and its impact on CEO resilience.

Third, the current study focuses on the resilience of CEOs in single- and multi-generational family firms, which does not distinguish among the generations in control. Future studies may compare resilience of family CEOs across generations (e.g., 1st, 2nd, 3rd, etc.). Research in such directions may further unfold dynamics of family CEOs and enable understanding of resilience and its evolution across generations. Fourth, the cross-sectional nature of the current analysis places constraints on the findings. Future studies could rely on longitudinal data that provide scholars and practitioners with an even richer picture of those heterogeneous configurational patterns, as well as account for a temporal dimension (Conz & Magnani, 2020). For instance, studies exploring CEO resilience at time t may investigate the adaptive features of CEOs at time (t − 1) and their contribution to the response to the external shock at time (t + 1). Finally, although the analysis draws on a reasonable sample of family businesses, the approach adopted by the study (i.e., fsQCA) lacks qualitative insights. This causes difficulties in discovering configurations that are robust, thematic, and eloquent with internal reasonings (Miller, 2018). Future studies could garner qualitative testimonials and exploit qualitative evidence to enhance the robustness of the study.

To conclude, this article offers important insights into the conditions influencing the resilience of CEOs in times of crisis. By using fsQCA, we offer an understanding of how the dynamics of individual, family, and business influence CEO resilience (Conz et al., 2020; Smith et al., 2024). The dominance of family firms in most economies makes this understanding relevant to a wider cohort of audiences, especially when economies and societies look to assist businesses to recover in the post-COVID era.

Footnotes

Acknowledgements

The authors would like to express their sincere gratitude to Prof. Dr. Nadine Kammerlander, Associate Editor of Family Business Review, and the two anonymous reviewers for their insightful and constructive comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.