Abstract

We differentiate between “founder involvement,” “founding family involvement,” and the absence of such involvement in a firm. We maintain that family owners and chief executive officers (CEOs) assume a “familial” identity given family relations within the firm, whereas mere founders, influenced by arms-length relations to commercial stakeholders, embrace the opportunity-seeking “entrepreneurial” identity of an independent maker. We theorize and show how founder and founding family involvement shape the turnaround strategy and performance of firms divergently—from each other and from cases without such involvement—and explicate how the respective effects are moderated by crisis severity and firm age.

Keywords

Introduction

Character is revealed during crisis

The current times reveal clear deficits in our understanding of firms that face existential crises. These crises are technically referred to as turnaround situations in “established firms that once performed satisfactorily, specifically in terms of profitability, but no longer do” (Chen & Hambrick, 2012, p. 225; Pearce & Robbins, 1993; Wenzel et al., 2021). Even the most seasoned managers struggle to turn firms around successfully because the skills required—such as motivating disenfranchised employees and doing more with a smaller headcount—differ from those needed in more buoyant conditions (Bibeault, 1982). Similarly, researching turnarounds is challenging because it raises a host of econometric challenges, such as performance extremes, mean reversion, survivorship bias, and missing data, which may further explain why turnaround situations have been sparsely researched.

Driven by practical considerations, scholarly investigations were initially shaped by the desire to find the appropriate countermeasure to turn a struggling firm around. Early research advised efficiency-oriented operational measures (e.g., Hambrick & Schecter, 1983), whereas later research emphasized the benefits of strategic countermeasures (e.g., Barker & Duhaime, 1997). Modern turnaround research has revealed positive effects of their dual implementation (Schmitt & Raisch, 2013). With mixed evidence on its general ramifications, turnaround literature has rarely focused on the antecedents of turnaround management such as governance conditions—one of these being the effect of the founding family (i.e., of the founder or later-generation family members). In particular, how the founding “family affect[s] the outcome of the turnaround process” is largely unknown, especially regarding its performance implications (Trahms et al., 2013 p. 1302).

In non-crisis settings, early research on the family firm–performance link, often driven by agency arguments (Jensen & Meckling, 1976), has generally been divided, with some studies attributing a performance premium to family involvement (e.g., Anderson & Reeb, 2003; Villalonga & Amit, 2006), while others argue the opposite (e.g., Bennedsen et al., 2007; Hillier & McColgan, 2009). Scholars have reconciled these opposing views by arguing that, beyond agency, it is not simply a question of “whether” there is family involvement in firm ownership and management. Rather, it is nowadays considered pivotal to assess “who” the executives and owners are (e.g., a founder versus a later-generation family member), and how their social context shapes their priorities (G. Petriglieri et al., 2018; Van Knippenberg, 2011; Weick, 1995). To examine their divergent effects on firm trajectories, contemporary research distinguishes between (lone) founder and founding family involvement. Importantly, research argues that firm founders typically embrace entrepreneurial identities mirroring a social context of arms-length relations with commercial stakeholders, while post-founder family owners or CEOs are typically affected by a context of family influence in the business, as well as abundant social capital, and assume familial identities. These identities can “blend” given an “in-between” context of both founder and family involvement (Cannella et al., 2015; Miller et al., 2011; Miller & Le Breton-Miller, 2011).

We build on extant work to assess the research question, “How does founder or founding family involvement affect turnaround performance?” We propose that founder and founding family involvement shapes crisis response and subsequent turnaround performance differently, with outcomes that are distinct from a non-crisis setting wherein founder involvement is regularly seen as a performance driver, whereas more “responsible” family involvement may lead to underperformance (Miller et al., 2007). We examine our hypotheses using a panel dataset of three decades of U.S. S&P 1,500 turnaround firms, which we supplement with hand-collected data on the components of founder and founding family member involvement and turnaround responses. We find support for our arguments and discuss their implications for several strands of the literature. In particular, we observe that when several members of the founding family are involved without the founder, family firms are particularly well equipped to handle crises. Indeed, the components of involvement are found to be strong predictors of crises outcomes. For the family firm theory, this suggests that fine-grained components can, to a large extent, overcome issues associated with capturing the intention to pursue a vision of trans-generational, sustainable family control (Chua et al., 1999). As all firms eventually face crises that threaten their survival, our insights are relevant to entrepreneurs, entrepreneurial families, executives, employees, and sometimes, even the (economic) wellbeing of entire communities.

Theory Development and Hypotheses

The influence of founders and their families on firms can be far-reaching and significant (Chua et al., 1999). The organizational ramifications of such influence are shaped by the divergent social contexts wherein the founders and founding family members govern, particularly because of the impact of these contexts on their respective identities (Miller et al., 2011). Because identities drive individuals’ actions in administrative situations (Weick, 1995), a profound understanding of identities is imperative to apprehending the implications of founder and founding family involvement (Van Knippenberg, 2011).

Specifically, the leader identity construct is theoretically and empirically well established (e.g., Ibarra et al., 2014; Petriglieri & Peshkam, 2022) and has three related elements: “individual internalization, relational recognition, and collective endorsement” (DeRue & Ashford, 2010, p. 629). To elaborate, when people associate the meaning of leader with themselves, when others attribute this meaning to them (Shamir & Eilam, 2005), and when the social context they are embedded in endorses their leadership claim (Brewer & Gardner, 1996), they can be said to possess a leader identity. Like all identities, a leader identity is neither a monolithic nor static construct; rather, its meanings, and who can lay claim to them, are shaped by and constructed through social and relational processes (DeRue & Ashford, 2010; Petriglieri et al., 2018). For instance, the meanings associated with being a leader in a military context may be socially negotiated to include being tough in control and command (Thornborrow & Brown, 2009), whereas those associated with leadership in a health care context may be socially negotiated to include being caring, responsive, and collaborative (Pratt et al., 2006). We build on these notions to outline how the social context shapes the identities assumed by founders and founding family members. From this, we derive hypotheses on their firms’ turnaround performance.

The Evolution of Social Context as Firms Age

The social context of firms that involve founders or founding family members is theoretically important because it evolves ontologically with firm age, from founding to maturity. It affects the meanings of the identities assumed by founders and founding family members (Ekeh, 1974; Long, 2011; Miller et al., 2011). Specifically, the social context of young firms with founder involvement, beyond the founder’s key stakeholders (e.g., banks, investors, or early employees), is typically characterized by rudimentary ties based on instrumental exchange, whereas the social context of mature firms with continued founding family member involvement is characterized by evolved resilient ties with various organizational stakeholders that carry more trust and coherence than those in young firms (Miller & Le Breton-Miller, 2011).

Prior work suggests distinct identities for founders, who tend to adopt an entrepreneurial identity characterized by independence, self-efficacy, and risk-taking, and members of the founder’s family, who tend to adopt a familial identity characterized by interdependence, cohesion, and stability (Miller et al., 2011; Miller & Le Breton-Miller, 2011). In the following section, we describe the meanings associated with entrepreneurial, familial, and “professional” identities (the base case without founder and family involvement), along with the respective “local” social context that shapes them.

Founder Involvement and Entrepreneurial Leader Identities

Generally, people become entrepreneurs to build wealth independently by capitalizing on their business ideas. A successful founder’s identity is closely tied to their entrepreneurship and the firms they create (Cannella et al., 2015; Dobrev & Barnett, 2005; Miller & Le Breton-Miller, 2011). In the United States, an entrepreneurial leader identity is highly valued and characterized by independence, self-efficacy, an internal locus of control, and a propensity to take risks (Shane, 2003). The social context of early-stage founder firms is rudimentary and comprises investors, suppliers, or key employees who generally “prioritize economic interest” (Miller & Le Breton-Miller, 2011, p. 1057). Founders interact with these stakeholders in an entrepreneurial fashion with a focus on instrumentality, which aligns with the emerging social context of a young firm that is not yet strongly characterized by established relationships based on trust or coherence.

Family Involvement and Familial Leader Identities

As a firm matures, the interactions between the founder and stakeholders slowly become characterized by higher degrees of trust and coherence, as well as obligation and expectation (binding social ties; Coleman, 1990; Long, 2011; Uzzi, 1997). Continuity in responsibility and long-term orientation allow them to nurture mutually supportive relationships with key actors in their social context and increase their social ties (Asch, 1952; Miller & Le Breton-Miller, 2005). This gives rise to solidarity and shared schemata among organizational stakeholders (Arregle et al., 2007; Carr et al., 2011).

When founder’s descendants inherit responsibility for the firm, they often do so within the local cosmos of this now evolved social context, which may involve multiple family members. At this stage, the firm may be the key source of income and security for the founder’s descendants, and a (shared) source of pride in what the family’s firm symbolizes and embodies in society (Ward, 2004). Founding family members are expected to uphold the firm culture and shared schemata and follow a long-term orientation, not merely from the perspective of growth but also to provide continuity, reliability, and stability to the family and the firm’s stakeholders who make up the mature social context (Miller & Le Breton-Miller, 2005). In this context, the founding family members involved in the mature family firm, particularly when there are multiple, usually adopt a “familial identity” characterized by interdependence, cohesion, and stability—meanings that constitute an identity that is fundamentally intertwined with the firm and its history and culture (Miller et al., 2011).

The Blending of Identities and the Baseline of Professional Leader Identities

We acknowledge that the identities portrayed earlier are, to an extent, the poles of a spectrum since joint founder and founding family member involvement can occur in the intermediate phases. Given that individuals can hold multiple identities (Stryker, 1980), both founder and founding family identities may “blend,” causing individuals to see themselves as “business builders and family nurturers” and to follow the meanings of both identities (Miller et al., 2011, p. 8; Miller & Le Breton-Miller, 2011).

Moreover, we include the case where both founder and founding family involvement are absent and, as a baseline, representing a setting that is governed purely by “professional” executives. Professional leaders tend to aspire toward being characterized as confident, intelligent, and self-aware individuals with integrity (Ibarra, 1999) and strive to be affiliated with the social group of business leaders. Professional leaders’ potential career mobility implies that their identities are usually portable and less intertwined with the firms they lead (Petriglieri et al., 2018). They may draw their identities from being perceived as competent professionals (Baumeister, 1989), primarily guided by performance aspirations and shareholder wealth (Cannella et al., 2015; Cyert & March, 1963; Sundaramurthy & Kreiner, 2008). This short-term orientation often renders their relationships they develop with stakeholders in the firm’s social context more transactional rather than based on sustainable trust and loyalty (Gersick et al., 1997; Petriglieri & Petriglieri, 2010).

Identity Threats Triggered by Existential Firm Crises

Existential firm crises threaten the identities of founders and founding family members. They signal potential harm to the value of their identities and their ability to enact them (Petriglieri, 2011) because their identities are deeply intertwined with the fate of their firms. In the case of founders, the threatened firm is an extension of themselves (Dobrev & Barnett, 2005), and the positive value and self-worth they derive from being an entrepreneur is intimately tied to their venture as their creation. In the case of founder descendants, the threatened firm is an extension of their family (Calabrò et al., 2018; Ward, 2004), and the positive value and self-worth they derive from being a custodian of the family heritage are intimately tied to the success of the firm. We classify the threat to the founders and founding family members’ identities as strong in existential firm crises because the “potential future harm to identity is great” (Petriglieri, 2011, p. 649). If they are unable to turn their firms’ fortunes around, they could lose an important part of their identity. By contrast, the identities of professional leaders are rarely this deeply intertwined with the fate of their employing organization. While a turnaround situation, if mishandled, is likely to harm the track record of professionals (Trahms et al., 2013), and hence the value of their identity, such situations do not normally threaten the entire basis of their identity, as they do for founders and founding family members.

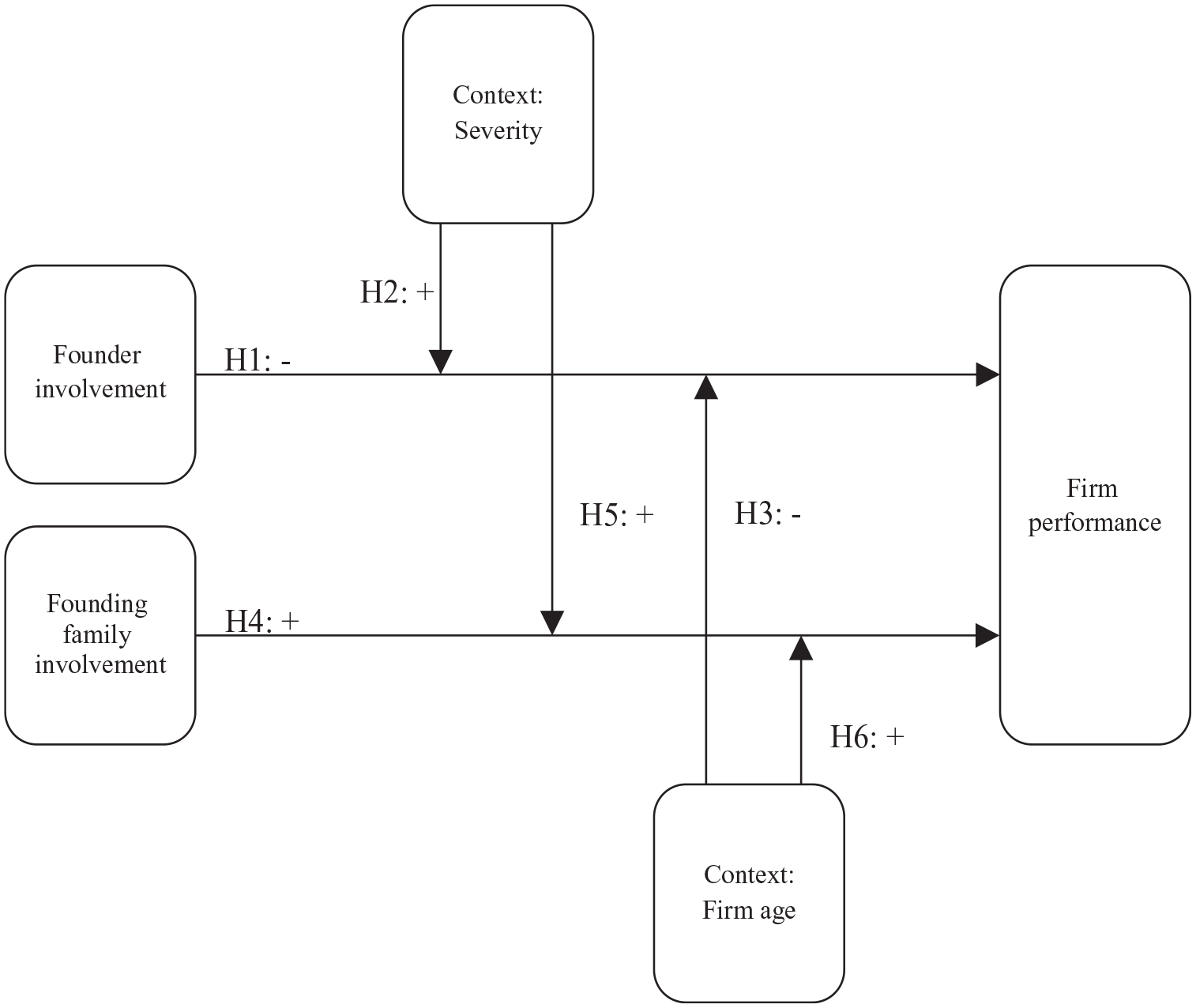

When their identities are threatened, people are driven to act in ways that mitigate the threat. These threat responses are of two types—identity protection and identity restructuring (Petriglieri, 2011). When a person responds to a threat using identity-restructuring, they devalue or exit their threatened identity (Ashforth, 2000; Crocker & Major, 1989). Conversely, when a person responds to a threat using identity-protection, they act to eliminate the threat such that they can continue to claim and enact their valued identity. The identity-restructuring response of devaluing or exiting their entrepreneurial or familial identities is particularly costly for founders and their descendants because this identity is central to their lives (Cast et al., 1999; Gecas, 1982; Olson, 1968). Thus, we anticipate that they will respond to identity threats using the identity-protection response mechanism. Identity-protection responses reinforce the virtues of the threatened identity by targeting the source of the threat (Petriglieri, 2011). Correspondingly, founders and family members are likely to exert influence toward achieving a firm turnaround in ways that align with, rest on, and reinforce the logic and virtues of their (threatened) identities (Petriglieri & Devine, 2016). In the following section, we hypothesize how this coherence shapes a firm’s turnaround performance in cases of founder and founding family involvement (Boyne & Meier, 2009; Pajunen, 2006; Sundaramurthy & Kreiner, 2008). We summarize our hypotheses in Figure 1.

Model of Turnaround Performance and Founder and Founding Family Involvement.

Turnaround Performance and Founder Involvement

We hypothesize that the way in which leaders respond to turnaround situations depends on the identities they hold in relation to the firm, and that these differences impact turnaround performance. Specifically, how firm founders pursue retrenchment and recovery responses to achieve turnaround (Schmitt & Raisch, 2013; Trahms et al., 2013) should align with their entrepreneurial leader identity as risk-taking, opportunity-seeking, independent operators (Gartner, 1988; Shane, 2003). We argue that this identity content should drive founders to favor particularly bold, independent, and far-reaching turnaround responses, without wide consultation with stakeholders, as they strive to set every wheel in motion to save their cherished creation from failure to reinforce their identity. While turnaround responses can indeed increase the chances of firm survival, they also incur costs such as compensation for dismissed employees or buying into new markets. The more turnaround responses a firm uses, the more the costs rise and the more likely it is that the firm experiences marginally decreasing profits of additional turnaround responses (Schmitt & Raisch, 2013). However, while corporate strategy would normally be adapted, and headcounts and assets retrenched only as much as necessary to enhance turnaround performance, founder involvement may risk derogating turnaround performance when founders try any means to save their treasured firm, thus advocating bold and costly degrees of change, rather than optimizing firm’s performance. Moreover, an identity-reinforcing response that relies on the entrepreneurial hallmarks of being autonomous, free, and unbound in restructuring, including employee retrenchment, is likely to cause disappointment in relationships. Employees may implicitly expect limits to employee retrenchment because of their shared histories. Therefore, an unbound response can damage social capital, ultimately resulting in inferior performance (Adler & Kwon, 2002). Finally, given the founder’s involvement in positions that may affect the strategic direction of the firm (Miller et al., 2011), professionalization is unlikely to fully prevent this response in an acute crisis accompanied by the need to reinforce entrepreneurial identity. Thus, we posit:

Firms in crises differ in their degrees of performance severity (Barker & Duhaime, 1997; Chen & Hambrick, 2012; Hofer, 1980). Although the bolder and wider-reaching turnaround responses associated with founder involvement are likely to harm turnaround performance, we argue that they may be less inappropriate when a turnaround situation is particularly severe. While minor strategic adjustments are usually sufficient to resolve less-severe cases, if a turnaround situation is very severe, such as when the magnitude of company losses is high, major strategic reorientation, even at higher costs, is required (Chen & Hambrick, 2012; D’Aveni, 1989).

Indeed, when the turnaround situation is severe, internal and external stakeholders are more likely to be reassured by founders’ unwavering commitment to their firm, their image as capable coordinators of scarce resources (Alvarez & Busenitz, 2001), and their tendency to convey a motivating and anchoring vision of the firm’s recovery (Bono & Ilies, 2006; Bono & Judge, 2003). Stakeholder support can manifest as lower premiums demanded to compensate for potential losses and shield the struggling firm from opportunistic takeover attempts; thus, reassuring stakeholders enhances performance as severity intensifies (Arogyaswamy et al., 1995). We argue that founders’ bold turnaround responses eventually become adequate, but not superior, in extremely severe crises. Therefore, we posit:

As firms age, the longer history of repeated human interactions gives rise to trust and cohesion but also obligations and expectations between the founder and key stakeholders of the firm (Coleman, 1990; Long, 2011; Uzzi, 1997). These ties to internal and external stakeholders favor the emergence of social capital (i.e., goodwill such as “sympathy, trust, and forgiveness” that elicits “information, influence, and solidarity”; Adler & Kwon, 2002, p. 18). Although frequently argued to be a source of competitive advantage (Arregle et al., 2007; Nahapiet & Ghoshal, 1998; Pearson et al., 2008), social capital can turn into a significant liability when “conflicts over priorities” emerge—in other words, when obligations are not fulfilled according to expectation (Adler & Kwon, 2002, p. 31).

Although founders’ entrepreneurial identities might change slightly over time to incorporate the emerging social ties to organizational constituents (Markus & Wurf, 1987), we argue that founders should largely maintain “their identities [as entrepreneurs] in their current state to achieve a sense of stability and continuity over time” (Petriglieri, 2011, p. 644; Shamir et al., 1993; Smeekes & Verkuyten, 2015). Thus, when an existential crisis arises in a more mature firm, a preference for bold turnaround responses, such as deeply cutting headcount, would be at odds with and appear unjustified to stakeholders who expect mutual support (Long, 2011). Such “broken agreements and the violation of trust” would corrupt emerging social contexts, induce resistance instead of vital support from key stakeholders, and therefore, diminish turnaround prospects (Ford et al., 2008 p. 365; Pajunen, 2006). By contrast, social contexts and expectations of mutual support in younger firms are less evolved due to a shorter history of human interactions, leading to less-pronounced negative resonance to overly holistic turnaround responses ensuing from founder involvement (Coleman, 1990; Uzzi, 1997). Thus, we posit:

Turnaround Performance and Founding Family Involvement

The way in which founding family members advocate retrenchment and recovery responses should also align with the content of their leaders’ familial identities of being interdependent, cohesive, and stable (Miller et al., 2011). These identity meanings include the duty to assume responsibility for those who have worked loyally and respectfully for the firm and are misaligned with employee retrenchment turnaround responses. Instead, we argue that the involvement of founding family members increases the preference for turnaround strategies that are based on togetherness, collective sacrifice, and joint effort: strategies that minimize employee retrenchment and are typically regarded as “responsible restructuring” (Block, 2010; Cascio, 2002). This emphasis on cohesion and commitment to employees, suppliers, and other stakeholders complies with their evolved expectations of solidarity and mutual support. Therefore, these strategies avoid conflicts over priorities (as in the case of founder involvement), and instead evoke consonance with priorities regarding the charted course (Adler & Kwon, 2002; Helliwell et al., 2014). This consonance should enable firms to exploit the positive potential of the nurtured relationships with organizational stakeholders, as the corresponding underlying norms of reciprocity induce these stakeholders to offer vital lifelines to “their” organization (Arregle et al., 2007; Gouldner, 1960). In particular, when a firm with continued founding family involvement is threatened, the beneficial outcomes of leveraged social capital may include renouncing increases in salary, increasing work effort (Cater & Schwab, 2008), remaining lenient on outstanding bills, or even raising credit (Greif, 1989; Pajunen, 2006). As such, social capital endowment should constitute a unique performance advantage in light of founding family involvement, driving turnaround performance compared to other firms that are generally more restrained from garnering this particular resource (Ahrens et al., 2019; Habbershon & Williams, 1999; Pearson et al., 2008). Therefore, we posit:

Organizational recovery becomes challenging with the increasing severity of the turnaround situation, and the collapse of the firm and its social context become a viable threat. In such cases, the more protective response emphasizing togetherness that is associated with founding family involvement should induce key stakeholders to mobilize larger resource reserves and offer greater loyalty, commitment, and effort to the organization. Thus, when a turnaround situation intensifies, carefully nurtured relationships with organizational constituents (Miller & Le Breton-Miller, 2005) should allow such firms to be particularly resilient compared to other firms that cannot draw upon similar degrees of social capital with organizational stakeholders (Lins et al., 2017). Key employees in firms with continued founding family involvement should be more motivated to remain committed, diligent, and supportive to preserve its core functions (Lindström & Giordano, 2016; Nelson, 1989). Usually, a drain of human capital from a severely struggling firm would inflict detrimental attrition as individuals search for shelter from the storm (Arogyaswamy et al., 1995). As the severity of the turnaround situation increases, the turnaround response promoted by founding family members should intensify reciprocal solidarity and cohesion (Adler & Kwon, 2002), making the firm more resilient (Aldrich & Meyer, 2015) and its turnaround performance superior to that of firms without founder and family involvement (Hoffman et al., 2006; Sorenson & Bierman, 2009). Accordingly, we posit:

As time elapses and familial influence continues to be reflected in business practices, social capital endowment becomes more pronounced because of a longer history of repeated human interactions (Arregle et al., 2007; Chrisman et al., 2012). Moreover, by sustainably treasuring evolved relationships and passing on familial values, norms, and obligations to subsequent generations, family members can maintain and accumulate additional social capital over time (Ahrens et al., 2019). Therefore, the performance advantage of founding family involvement in turnaround situations should be even more pronounced as the firm matures and social capital becomes more abundant. Thus, we posit:

Methodology

Sample Selection

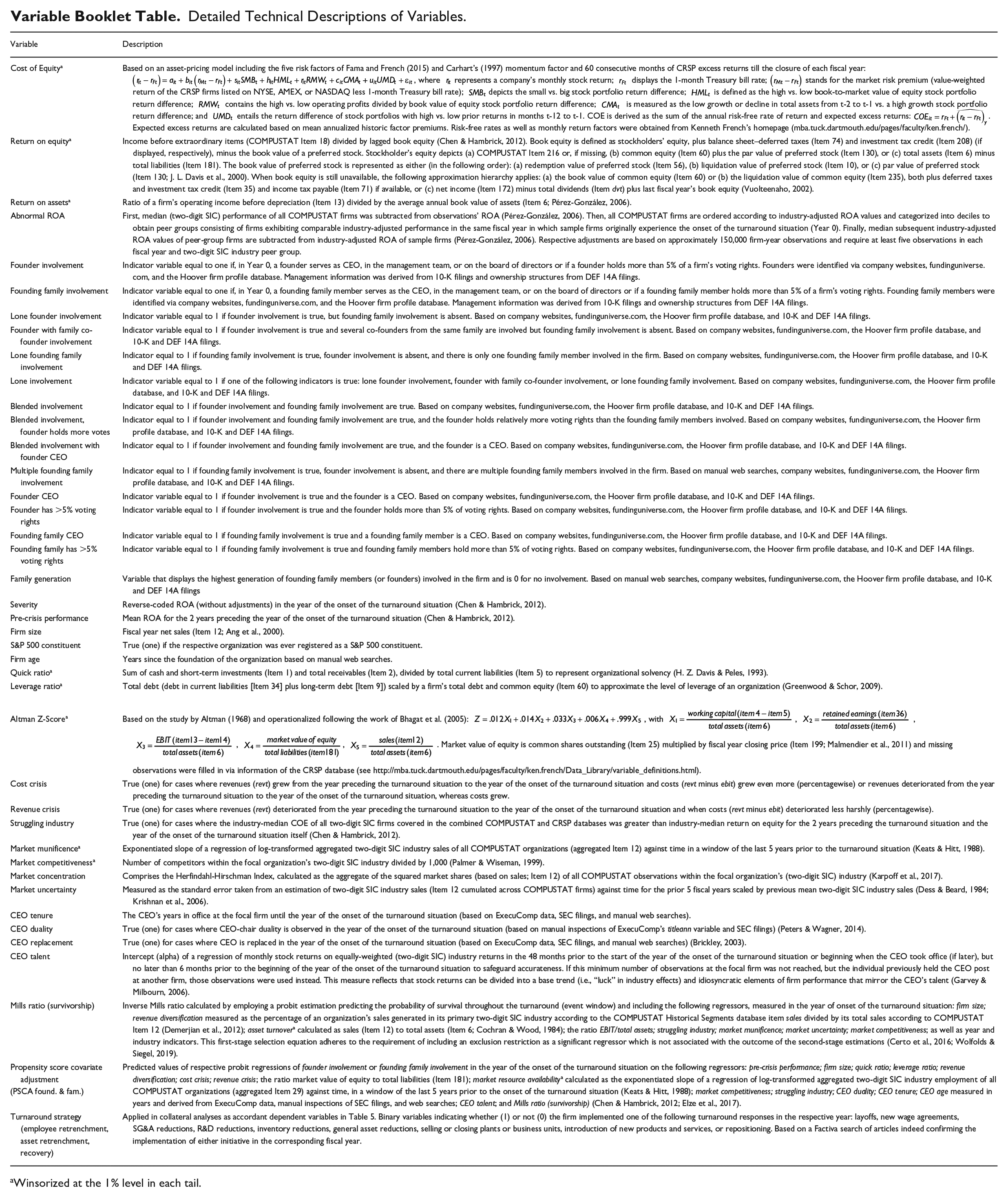

We began our data collection with all nonfinancial S&P 1,500 firms in the COMPUSTAT database between 1994 and 2017. Among them, we singled out those in turnaround situations according to the definition of Chen and Hambrick (2012): firms that perform satisfactorily (a firm’s return on equity exceeds costs of equity [COEs]) for 2 years, followed by 1 year of operating losses before extraordinary items. We followed the work of Fama and French (2018) and utilized a multifactor asset-pricing model involving the five risk factors of Fama and French (2015) and a momentum factor (Carhart, 1997) to estimate COE based on 60 months of return observations using the CRSP database. The measurement of equity values was based on the studies by J. L. Davis et al. (2000) and Vuolteenaho (2002). The Variable Booklet Table provided at the end of this section offers in-depth technical information on these (and all other) variables.

Disregarding cases with missing values and firms that generated more than 50% of sales outside their primary industry to ensure that industry controls remain functional (Chen & Hambrick, 2012; Demerjian et al., 2012; Zhang & Rajagopalan, 2004) yielded an overall sample comprising 190 cases of substantially troubled firms between fiscal years 1996 and 2012 (the first year of the turnaround situation was denoted as Year 0). Inspections of these firms supported the effectiveness of our applied sampling routine. The majority experienced a high likelihood of default (Altman, 1968) and a sharp performance decline in Year 0 (average performance dropped by almost 60%); many even experience a sustained phase of losses across subsequent periods. We analyzed turnaround performance from Year +2 until Year +5 (i.e., 760 observations in total) because turnaround measures usually take a minimum of 2 years to take effect and are conventionally inspected up to 5 years after the decline (Morrow et al., 2004).

Dependent Variable

Turnaround performance was measured as (abnormal) returns on assets (ROA). ROA is a popular indicator of operating profitability and ensured our results would be comparable to the extant literature on turnarounds (e.g., Love & Nohria, 2005; Winn, 1997). ROA is especially suitable in our context because other equity-based measures employed in turnaround situations (e.g., Chen & Hambrick, 2012) might readily be suspected of suffering from strategic equity-related decisions unrelated to fundamental firm performance due to the desire of founders and founder descendants to retain control. Therefore, ROA is frequently preferred in event studies on founder and founding family member involvement (e.g., Pérez-González, 2006). We considered that the plain performance measures of substantially troubled firms are affected by mean reversion; that is, performance trends solely attributable to performance reverting to the mean (Huson et al., 2004). Accordingly, we adjusted our dependent variable for industry and performance trends to capture abnormal performance (ROA) free from mean-reverting tendencies (see the Variable Booklet Table; Barber & Lyon, 1996).

Detailed Technical Descriptions of Variables.

Winsorized at the 1% level in each tail.

Independent Variables

Founder and Founding Family Involvement

We followed the operationalization in several contemporary debate-leading articles (e.g., Anderson & Reeb, 2003; Miller et al., 2007; Miller & Le Breton-Miller, 2011; Pérez-González, 2006; Villalonga & Amit, 2006) to identify founder and founding family involvement while maximizing the comparability of our research. Specifically, we began by hand-collecting information on corporate management, boards, and ownership from SEC filings (U.S. Securities and Exchange Commission) in the EDGAR database (Electronic Data Gathering, Analysis, and Retrival) and determined founder involvement when a founder served as the CEO, was in the management team, on the board of directors, or held more than 5% of a firm’s voting rights (Miller et al., 2011). Correspondingly, founding family involvement was coded as one if a founder’s family member satisfied any of the aforementioned conditions. To code these variables, we first assessed company websites, fundinguniverse.com, and the Hoover firm profile database to identify founders and potential founding family members. Subsequently, we investigated 10-K filings for management and board information, and DEF 14A filings (proxy statements) for ownership structures. Companies with origins in mergers, spin-offs, and carve-outs were excluded because of their natural unavailability of founder information. Furthermore, owing to incomplete data coverage throughout the phase-in period of the EDGAR database (https://www.sec.gov/edgar/aboutedgar.htm), our classification began with the fiscal year 1996. Including these two binary indicators in our main regressions naturally selected all firms without founder and founding family involvement as the comparison group. In the supplemental analyses, we also considered ancillary meso- and micro-level differentiations of founder and founding family member involvement constellations.

Severity

We referred to the study by Chen and Hambrick (2012) and measured a firm’s turnaround severity by reverse-coding plain ROA in the year of the onset of the turnaround situation (Year 0).

Firm Age

We conducted manual web searches to code a firm’s age (in years) since inception, which served as a proxy for the maturity of a firm’s social context (Freeman et al., 1983; Thornhill & Amit, 2003).

Control Variables

Following the turnaround literature, we included a comprehensive control vector addressing the firm, industry, and CEO levels. At the firm level, we controlled for resource endowment by including firm size (log-transformed sales), quick ratio (short-term liquidity divided by total current liabilities), and leverage ratio (debt to equity; Audia & Greve, 2006). Altman’s (1968) Z-Score proxied an organization’s risk of default and pre-crisis performance (mean ROA for Years 2 and 1) served as a measure of fundamental organizational strength (Chen & Hambrick, 2012). To delineate an internal or external reason for the crisis (Pearce & Robbins, 1993), we included cost crisis and revenue crisis indicators that were “true” if there was a pronounced cost or revenue issue, respectively, in Year 0 compared to the base case when neither situation was evident (see the Variable Booklet Table). CEO replacement in Year 0 controlled for subsequent effects of CEO turnover (Brickley, 2003). S&P 500 constituent controlled for effects of high-profile firms among general S&P 1,500 constituents (Fama & French, 1993).

At the industry level, we followed Dess and Beard (1984) and Krishnan et al. (2006) and regressed industry sales at the two-digit SIC level against time and divided the standard error of the regression coefficient by mean industry sales to obtain a proxy for the industry’s dynamism (market uncertainty). To delineate industries in fundamental turmoil, struggling industry showed that, in Year 0 and the 2 years preceding the turnaround situation, the median COE at the two-digit SIC industry level of all COMPUSTAT and CRSP firms was above the median return on equity (Chen & Hambrick, 2012; Morrow et al., 2004; Schmitt & Raisch, 2013). In addition, calculated across all COMPUSTAT firms and following the work of Palmer and Wiseman (1999), market competitiveness was specified as the number of rival firms within the focal firm’s main industry divided by 1,000 and controlled for corporate strategic behavior and corresponding performance implications (Ferrier, 2001; Hambrick & Finkelstein, 1987). Further industry controls included market munificence, calculated as the exponentiated slope of a regression of log-transformed COMPUSTAT two-digit SIC industry sales against time for the previous 5 fiscal years (Keats & Hitt, 1988; Li & Tang, 2010), and market concentration, specified by the Herfindahl-Hirschman Index (Karpoff et al., 2017). At the CEO level, we captured heterogeneity related to tenure, measured in years (according to ExecuComp, SEC filings, and supplementary web searches); the duality of the CEO and board-chair positions, collected via ExecuComp’s “titleann” variable and complemented with manual searches in SEC filings (Peters & Wagner, 2014); and CEO talent, following the approach of Garvey and Milbourn (2006), which is outlined in-depth in the Variable Booklet Table, to control for respective performance implications (e.g., Zhu & Chen, 2015).

Naturally, the observation of turnaround performance was restricted to firms that survived the crisis. Thus, to capture the effects of sampling-induced endogeneity, we correct for this non-random sample composition by including an inverse Mills ratio (Heckman, 1979) based on the estimation of a firm’s probability of displaying performance across our event window. The specification of this selection equation, outlined in full detail in the Variable Booklet Table, satisfied the criteria for valid exclusion restrictions (Certo et al., 2016; Wolfolds & Siegel, 2019) and yielded a control for survivorship bias (Heckman, 1976).

Furthermore, founder or founding family member involvement might be more likely for some firms than for others. We controlled for this unobserved heterogeneity by predicting the likelihood of their occurrence (Elze et al., 2017). In particular, we calculate probit estimations of founder and founding family involvement on an array of antecedent variables: (a) firm characteristics (i.e., pre-crisis performance, firm size, quick ratio, leverage ratio, revenue diversification, cost crisis, revenue crisis), and the ratio of market value of equity by total liabilities (Altman, 1968); (b) industrial characteristics (i.e., market resource availability, market competitiveness, and struggling industry); (c) CEO characteristics (i.e., CEO duality, tenure, age, and talent); and (d) the correction for survivorship bias. The predicted values of these two models were included in our main regressions as a propensity score covariate adjustment (PSCA; Chatterjee & Hambrick, 2007; Chen & Hambrick, 2012; Gerstner et al., 2013; Tang et al., 2018).

Empirical Strategy

An initial assessment using Breusch-Pagan Lagrangian multiplier tests (Breusch & Pagan, 1980) revealed that the data were not poolable, ruling out ordinary least squares (OLS) estimations. Moreover, Wooldridge tests revealed a first-order serial correlation of the error terms (Drukker, 2003; Wooldridge, 2002). Hence, since our key predictor variables displayed high degrees of temporal stability, we applied generalized estimating equations (GEEs; Crossland et al., 2014), which derive maximum likelihood estimates while accounting for autoregressive correlation structures observed in the error terms that would otherwise yield overly optimistic results (Liang & Zeger, 1986). GEE are even advocated as “especially appropriate” for the type of data we investigated (Miller & Le Breton-Miller, 2011, p. 1066). Accordingly, we parameterized GEE using a Gaussian distribution of the regress and, an identity link function, a covariance structure addressing first-order autocorrelation and heteroskedasticity-robust standard errors (Huber, 1967; White, 1980). Nevertheless, our findings based on GEE remained robust when employing more naïve OLS estimations, with standard errors clustered at the firm level, or random-effects regressions. According to the condition numbers and variance inflation factors, multicollinearity concerns were dismissed (Belsley et al., 2005; O’Brien, 2007). All specifications included year indicators (Year +5 was omitted), and the continuous variables and interactions were mean centered to facilitate their assessment.

Data Analysis

Results

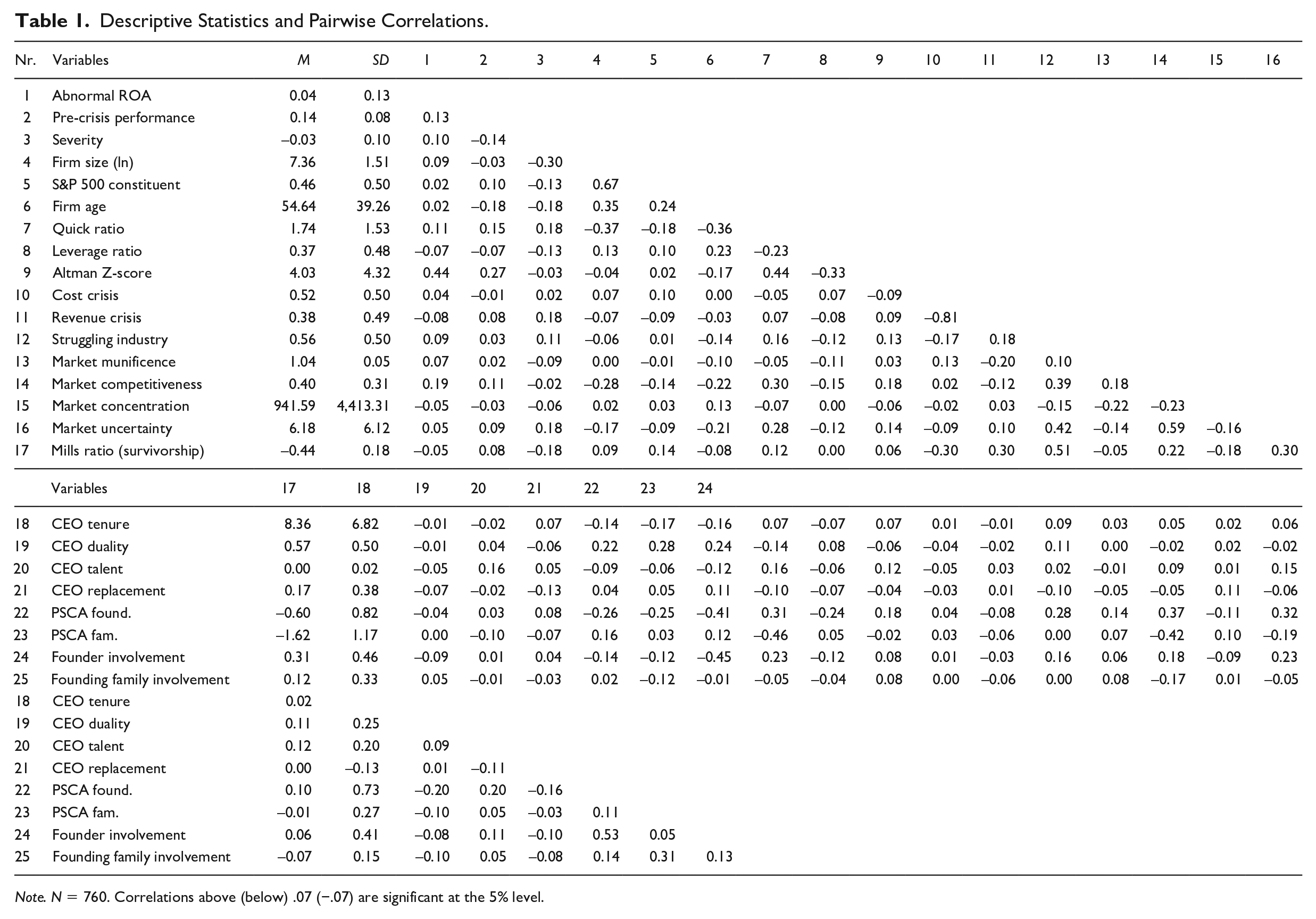

Table 1 displays the descriptive statistics and correlations. Table 2 presents the results of our main regressions.

Descriptive Statistics and Pairwise Correlations.

Note. N = 760. Correlations above (below) .07 (−.07) are significant at the 5% level.

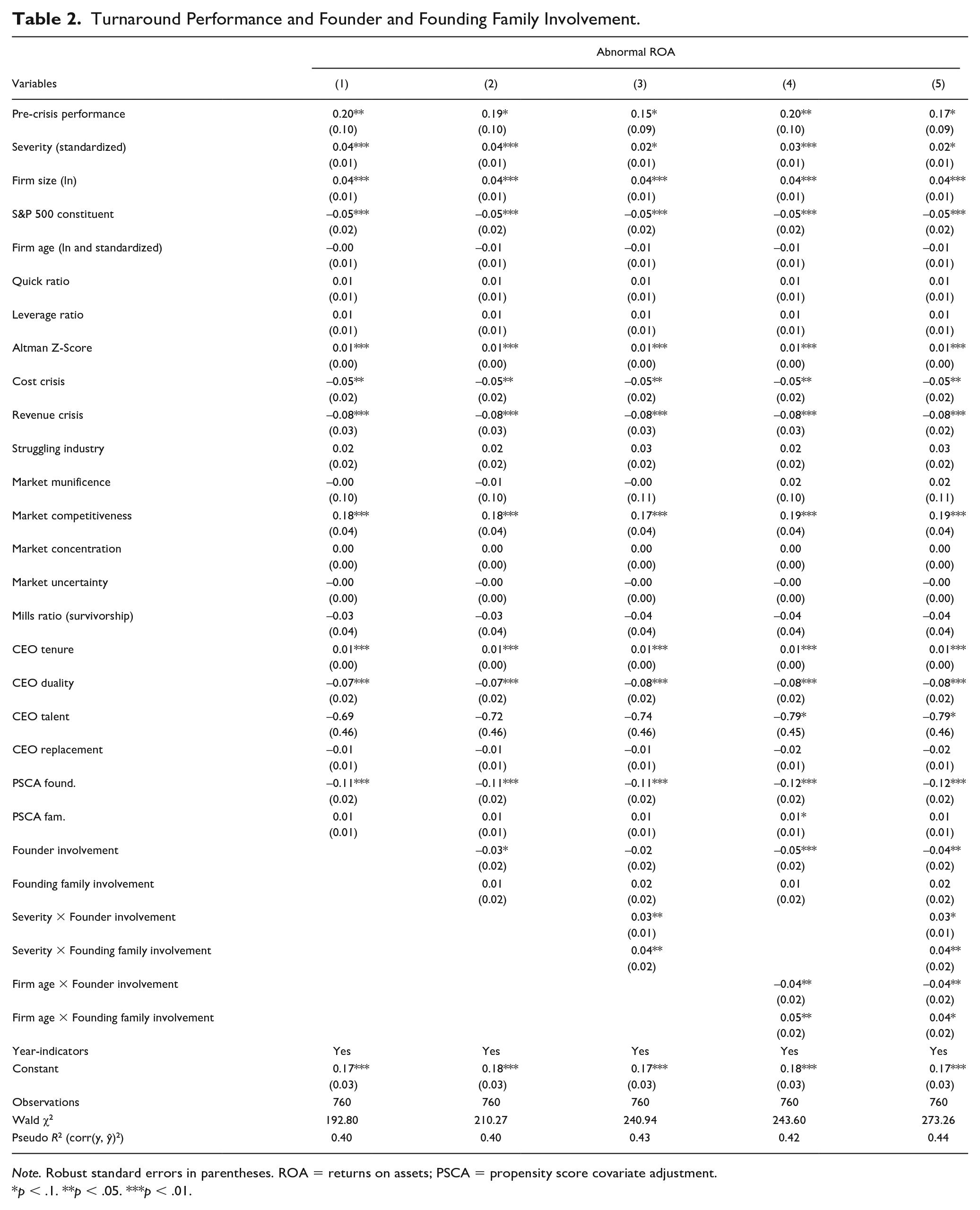

Turnaround Performance and Founder and Founding Family Involvement.

Note. Robust standard errors in parentheses. ROA = returns on assets; PSCA = propensity score covariate adjustment.

p < .1. **p < .05. ***p < .01.

Model 1 contained all control variables and subsequent moderators. Model 2 tested the main effects of founder involvement and founding family involvement on subsequent abnormal turnaround performance. The negative and marginally significant relationship between founder involvement and abnormal ROA (Model 2; β = −.031; p = .058) supports the theoretical reasoning outlined in H1. In terms of effect size, compared to cases without founder and founding family involvement, founder involvement was associated with an inferior abnormal ROA of 3.1 percentage points. Albeit contrary to our postulations, the main effect of founding family involvement on abnormal ROA was insignificant (Model 2; β = .009; p = .677). This means that the average turnaround performance in firms with founding family involvement is (at this general level) not significantly different from that of firms without founding family involvement. We return to this coherence in more fine-grained meso- and micro-level collateral analyses in the following sections, where we find support for H4 for the sub-case of post-founder multiple founding family member involvement.

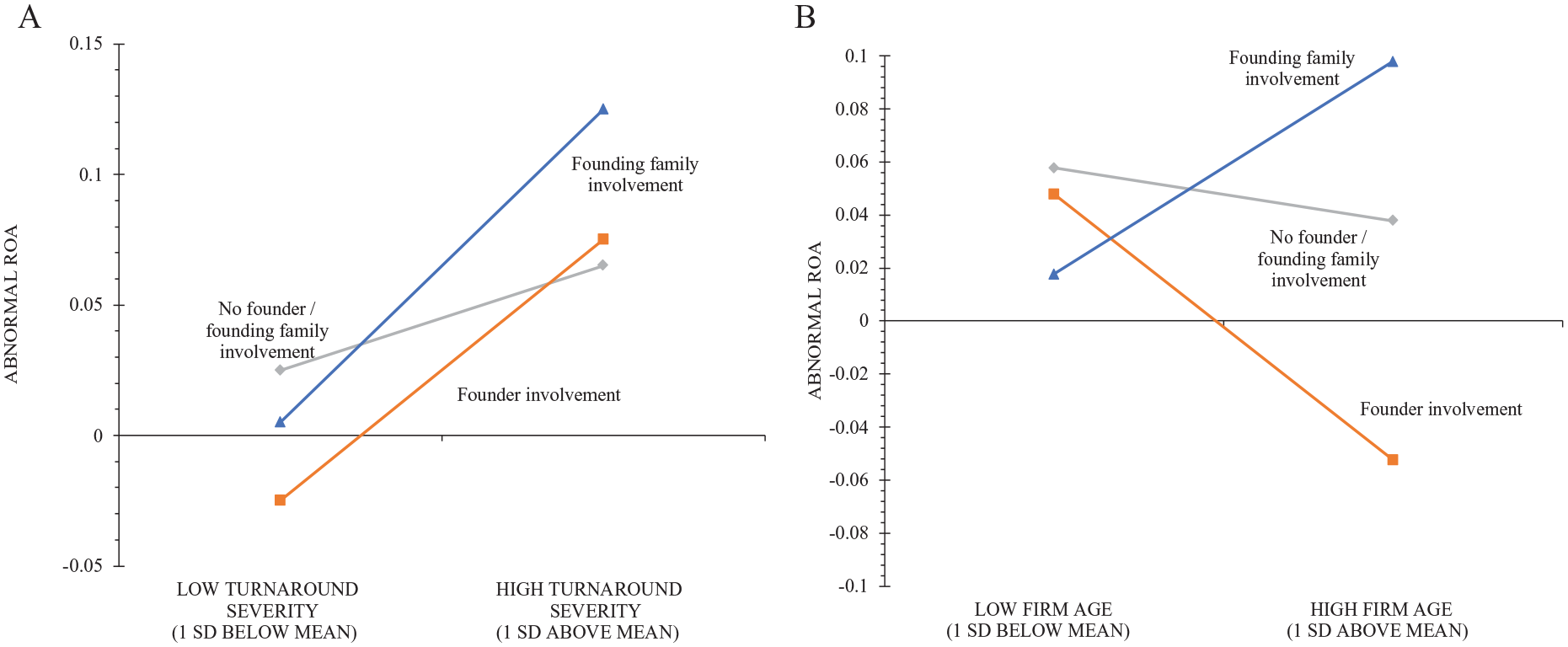

In Models 3 and 4, we analyzed the contingency effects as outlined in H2 and H5 (severity), and in H3 and H6 (firm age). In support of our argumentation behind H2, the interaction of founder involvement and severity in Model 3 was significantly positively related to performance (Model 3; β = .032; p = .013). In support of H5, we also found a significantly positive interaction effect of founding family involvement and severity on abnormal ROA (Model 3; β = .042; p = .034). We visualize the economic significance and magnitude of these effects in Figure 2A, assuming mean values for all control variables. Figure 2A shows that, in general, the average turnaround firm tends to perform slightly better when the severity of the decline is higher; however, this increase in turnaround performance is greater in firms with founder or founding family involvement, or both, than in firms without such involvement. This is noteworthy because founder involvement appears to aggravate crises in low-severity situations, and because it sheds light on the insignificant base effect of founding family involvement in Model 2.

Turnaround Performance Effect of Founder and Founding Family Involvement.

Model 4 incorporated the interactions between firm age and founder and founding family involvement. While the interaction of firm age and founder involvement is significantly negatively related to abnormal ROA (Model 4; β = −.040; p = .023), the coefficient of the interaction between firm age and founding family involvement is positive and significant (Model 4; β = .046; p = .017), providing empirical evidence corroborating H3 and H6. The magnitudes of these effects are shown in Figure 2B. Correspondingly, Figure 2B shows that the average firms’ turnaround performance is largely unrelated to firm age. However, turnaround performance deteriorated harshly in the case of founder involvement, while firms with founding family involvement experience a sharp increase in turnaround performance when firm age was high (both compared to firms where this is not the case). In Model 5, we confirmed the independence of the aforementioned effects by jointly including all predictor variables.

Collateral Analyses—Beyond the Polar View: The Landscape of Blended Identities

Family business literature acknowledges that the involvement of founders and founding family members can occur in heterogeneous constellations (Neubaum et al., 2019), causing entrepreneurial and familial identities to blend (Miller et al., 2011; Miller & Le Breton-Miller, 2011). Technically, our main analyses captured such blended cases wherein founder and founding family involvement were simultaneously present. However, in post hoc analyses, we further disentangled these cases to examine the insignificant effect of founding family involvement on a firm’s turnaround performance in our main analyses (H4).

Generally, we expected that the effects we theorized in H1 and H4 would be most salient when no such blending occurs. Moreover, as these hypothesized effects are of opposite direction, the compound effect in case of blending these identities should arguably lie between both “poles,” depending on which identity is more prominent. In this landscape of cases, the effect of “lone founders,” that is, founders without any other involved family member, should be closest to what we hypothesized in H1, whereas cases of founders involved with a familial co-founder already entail some minor blending. “Classic” blended identities, that is, cases of joint involvement of the founder and founding family members should arguably be located between both poles and may be further distinguished into cases where the founder holds greater voting power, the CEO position, or is involved in a less-dominant way. Finally, founding family involvement may also be distinguished into an archetypical “familial identity” with multiple founding family members involved without the firm’s founder (which is closest to the case hypothesized in H4) and in cases where there is a “lone founding family member,” that is, where the family involvement has, for some reason, dried up (is lacking) and, hence, the familial identity is strongly blended with that of an entrepreneurial investor (or even a detached professional). Therefore, in line with our arguments in H1 and H4, we expect lone founder involvement to exert the most negative association with subsequent turnaround performance, multiple founding family involvement (without founder involvement) to exert the most positive association with subsequent turnaround performance, and blended cases to exhibit performance levels between these poles.

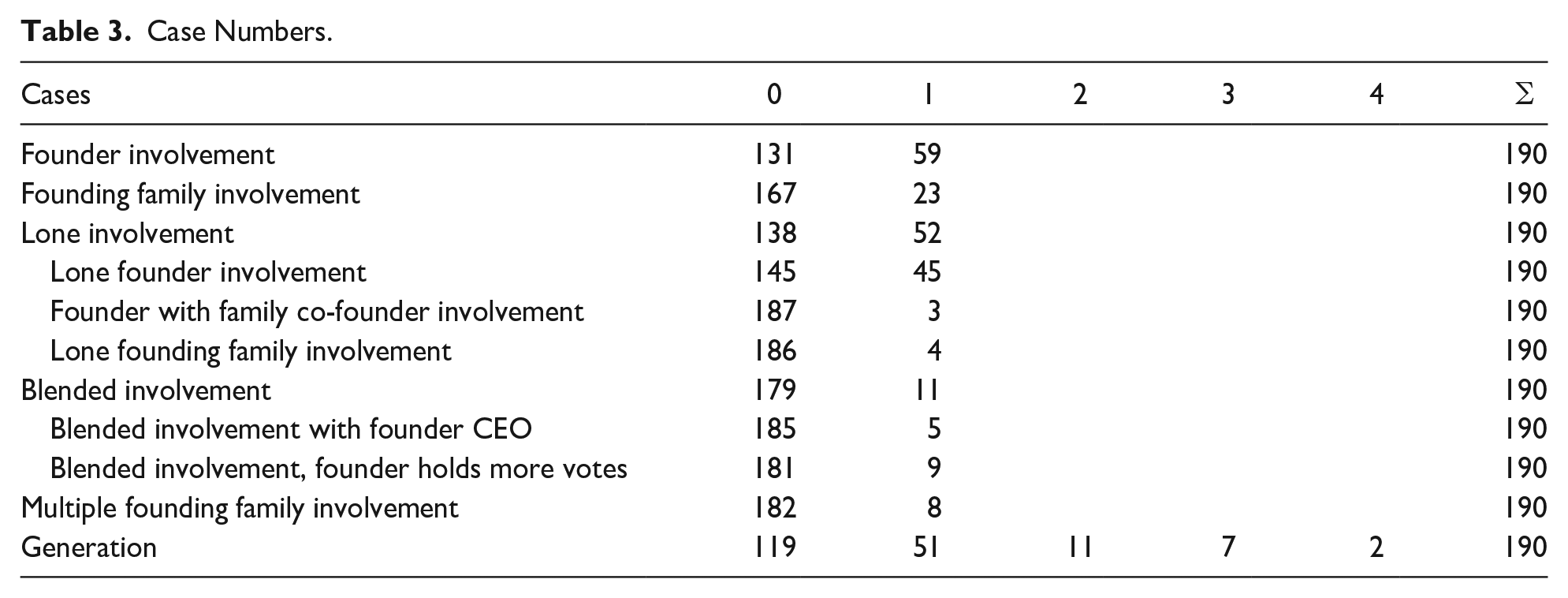

To test these rationales, we coded the ancillary meso- and micro-level differentiations of founder and founding family member involvement constellations. Specifically, lone involvement is true when, besides founder involvement or the lone involvement of a founding family member, no other member of the founding family is involved in the firm. Blended involvement is true when both a founder and a founding family member are jointly involved, and multiple founding family involvement is true when several members of the founding family are involved, but not the founder. We further zoomed in to differentiate between lone founder involvement, wherein, besides one founder, no other family member nor other family co-founder of the founding family is involved; lone founding family involvement, wherein, besides one founding family member, no other member of the founding family nor the founder is involved; founder with family co-founder involvement when there is involvement of multiple persons from one family as founders; and blended involvement with founder CEO and blended involvement when founder holds more votes (than involved family members) to delineate elevated founder involvement in blended cases. Finally, we coded founder CEO, founder has >5% voting rights, founding family CEO, and founding family has >5% voting rights as 1 when true.

The econometric capability to zoom in on these more fine-grained meso- and micro-level constellations was naturally limited given our study’s focus on firms in turnaround situations, which are relatively rare occurrences in a firm’s history. In our sample, we observed 53 cases of founder involvement and 23 cases of founding family involvement. Table 3 provides a nuanced description of the sub-case numbers. In line with a conservative stance, we considered meso- and micro-level evidence as indicative, given the finite number of cases.

Case Numbers.

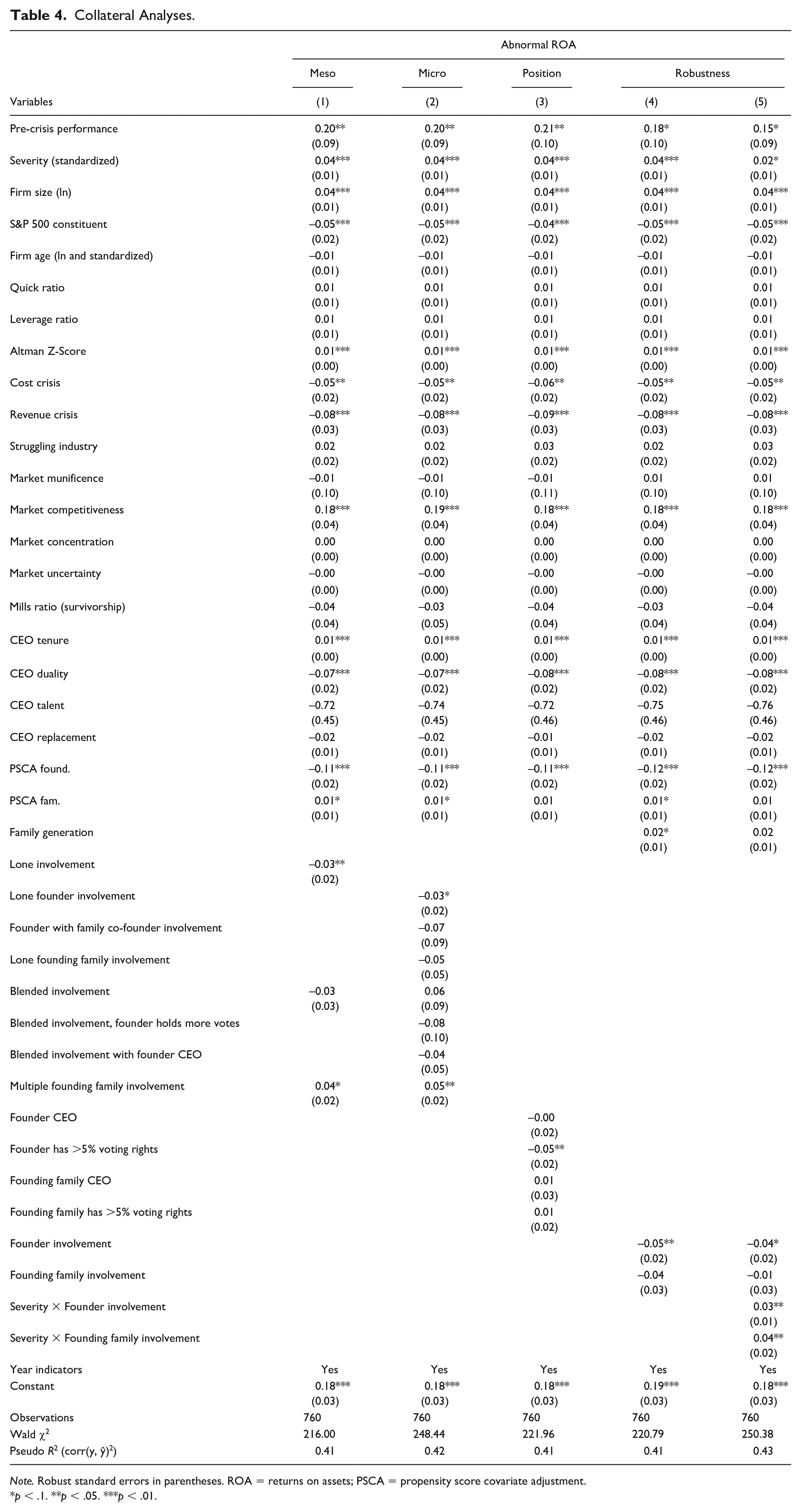

We report these results in Table 4. Model 1 presented meso-level specifications, finding a significant negative relationship between lone involvement and abnormal ROA (β = −.033; p = .033), and a significant positive relation for multiple founding family involvement (β = .044; p = .050), whereas the coefficient for blended involvement remained insignificant (β = −.031; p = .355). Disentangling the heterogeneity of founder and founding family involvement even further in Model 2, which covered micro-level categories, we found further evidence in line with our theorizing. Particularly, we found that lone founder involvement entails a significant negative relation with firms’ abnormal turnaround performance (β = −.031; p = .053), whereas multiple founding family involvement had a significantly positive coefficient (β = .046; p = .044). The coefficients on all other micro categories remain insignificant, although it is notable that in blended involvement, the coefficient turns insignificantly positive when the founder neither holds the CEO position nor has more votes than the founding family members (β = .056; p = .537). Together, the evidence from these analyses aligns with earlier arguments on how heterogeneity in founder and founding family involvement leads to a blending of leader identities that affects organizational outcomes. Moreover, while the indicative nature of this evidence must be considered, it suggests that H4 might only be true for the sub-case of multiple founding family involvement, although it cannot otherwise be confirmed. When multiple founding family members are involved in the post-founder phase, the turnaround performance is significantly higher than that in cases where this is not the case.

Collateral Analyses.

Note. Robust standard errors in parentheses. ROA = returns on assets; PSCA = propensity score covariate adjustment.

p < .1. **p < .05. ***p < .01.

Model 3 further distinguished between the positions taken by founders and founding family members using voting rights above 5% and CEO indicators. Therein, only the coefficient of the founder has >5% voting rights indicator was statistically significant (β = −.052; p = .033), providing more specificity regarding the negative effect of their involvement in turnaround cases. Moreover, Models 4 and 5 in Table 4 demonstrate that our main results for H1–H4 remain essentially unchanged when controlling for the family generation involved in the firm. Because of the inevitable correlation between the family generation variable and our moderator, firm age, we refrained from re-assessing H5 and H6 after controlling for family generation since the ensuing results would be obscured by multicollinearity in the respective variable of interest.

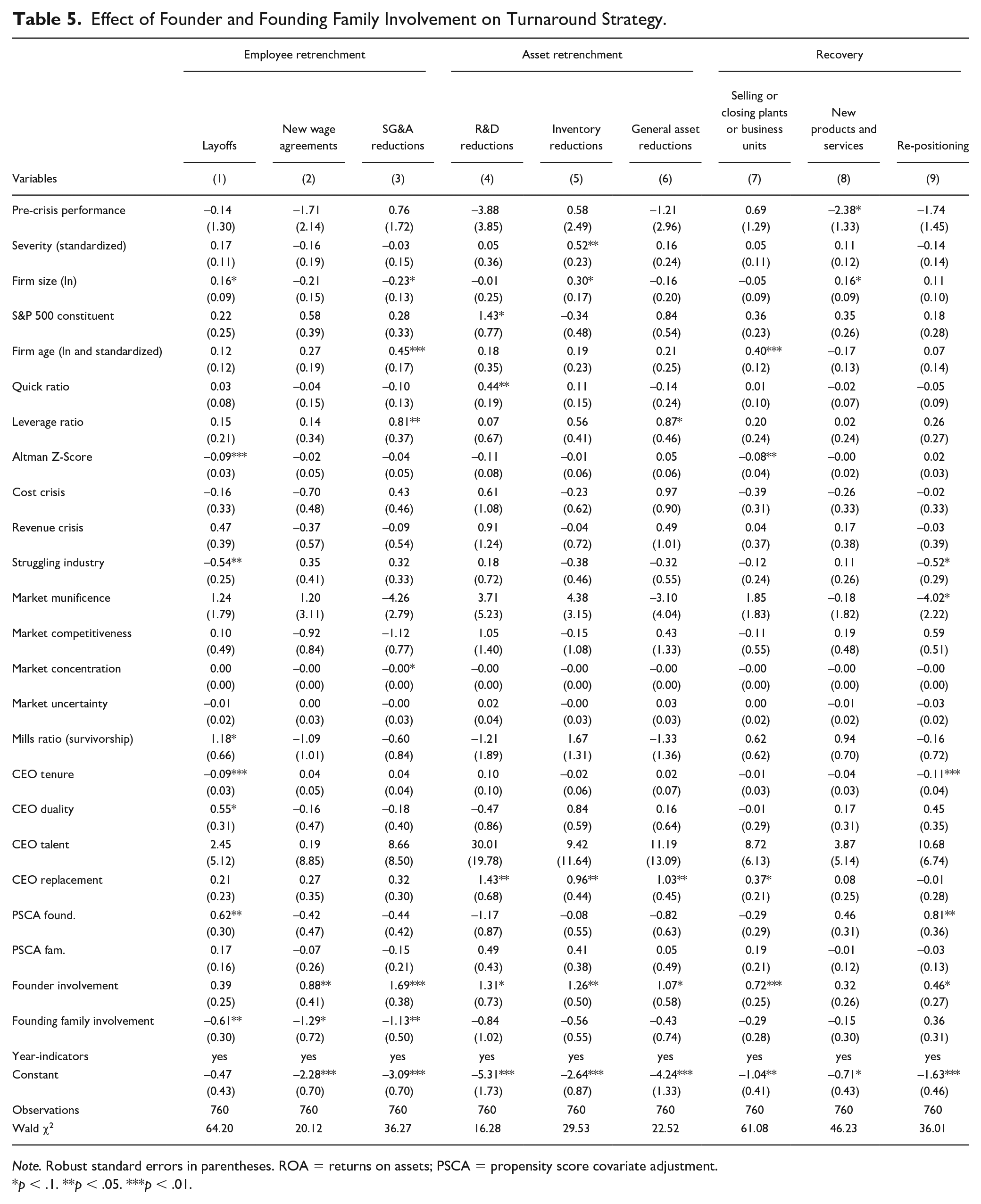

To further substantiate the theoretical reasoning underlying our hypotheses beyond these analyses and elaborate on the behavioral mechanisms, we investigated the specific turnaround responses to depict how founder and founding family involvement affect turnaround strategies (Table 5). We systematically searched the Factiva database to identify whether a set of employee retrenchment, asset retrenchment, and recovery actions had been implemented by the sample firms in years 0 until +3. In total, 7.744 manually assessed articles pointed to these turnaround actions being implemented by our sample firms. The panel probit regression results in Table 5 support our reasoning that founder involvement is positively associated with the likelihood of initiating a broad range of restructuring actions. Except for Model 8, almost all the coefficients of founder involvement on the investigated turnaround responses were (at least marginally) significant and positive. However, founding family involvement was associated with different turnaround responses compared to the other firms only in that they were significantly less likely to pursue employee retrenchment. Thus, these collaterals corroborate our reasoning that founding family involvement is associated with turnaround strategies that particularly reflect responsibility toward employees, that is, trying to refrain from employee-related retrenchment actions to shield (and utilize) social capital endowment.

Effect of Founder and Founding Family Involvement on Turnaround Strategy.

Note. Robust standard errors in parentheses. ROA = returns on assets; PSCA = propensity score covariate adjustment.

p < .1. **p < .05. ***p < .01.

Discussion

This study provides insights into the distinct turnaround behavior and performance associated with founder and founding family involvement. With the survival of the firm and its social context at stake, crises such as turnaround situations threaten the very identities of the founders and founding family members because the value and meaning of “who” they are is deeply intertwined with the fate of the threatened firm. Considering the attached personal and social obligations, the protection of their firm—and thereby the protection of their identity—will often remain the only viable threat response (Petriglieri, 2011; Toubiana, 2020). Eventually, such responses will have implications for organizational survival, employee occupation, and community wealth. Our work sheds light on the notable strengths and weaknesses resulting from founder and founding family involvement during turnaround situations and is relevant to practitioners and policymakers. From a scholarly perspective, it contributes to several theoretical fields.

Governance Research

The question “Does founder or founding family involvement lead to superior performance?” has captivated entire generations of researchers. Our findings strongly oppose what is known about the performance implications of founder and founding family involvement in regular non-crisis settings, wherein superior performance is often attributed to founder involvement (e.g., Miller et al., 2007). In times of crisis, the bolder turnaround responses associated with founder involvement, which align with founders’ entrepreneurial identity as independent, opportunity-seeking, and risk-taking, proved particularly detrimental to turnaround performance. Severe crises are the exception, wherein extreme responses become more adequate, even re-motivating, and their performance implications are similar to those of professional responses. An explanation may be that, under threat, founders prioritize their treasured firms’ existence over the needs of the stakeholders (e.g., employment, social coherence; Norton et al., 2012). We demonstrate that when bold responses are not warranted, such turnaround responses have particularly harmful repercussions, especially in older founder firms. Given the emerging social context and implicit contracts that develop since a firm’s inception, this underlines the general importance of considering the demands of organizational stakeholders in turnaround responses (Bundy et al., 2017) as their weal and woe can be crucial for the success of a turnaround strategy (Pajunen, 2006). While founder involvement is positive in good times, it can be particularly detrimental in bad times.

Our empirical analyses are also the first to shed a distinct light on the unique crisis strategy associated with founding family involvement—a void in management research that scholars are repeatedly urged to address (King et al., 2022; Trahms et al., 2013). Indeed, this crisis strategy appears to reflect the caring and nurturing familial identities of those who govern and the distinct prioritization of responsibility toward their employees (Habbershon & Williams, 1999). We observe that founding family involvement leads to turnaround strategies that advocate trading the short-term financial benefits of employee retrenchment for the benefits of employee retention, for example, in the form of superior stakeholder coherence. Because both effects partly offset each other, this may explain why the performance implications of founding family involvement are generally comparable to those of firms without founder and founding family involvement in times of crisis. In addition, in our sample, founding family involvement co-occurred with founder involvement or as lone founding family member involvement in many cases, such that the meanings of familial identity may not completely apply but blend with an entrepreneurial identity. However, in the sub-case of a prototypical and unblended familial identity, that is, when multiple founding family members (but no founder) are involved, who mutually endorse and reinforce each other’s familial identity, we observe that turnaround performance exceeds the performance of firms without such involvement. This observation informs the study of family firm heterogeneity (Neubaum et al., 2019), as it suggests that the involvement of multiple founding family members without founder interference differs in terms of leader behavior from cases where only a single founding family member (and no founder) is involved (Miller et al., 2011; Miller & Le Breton-Miller, 2011).

Notably, turnaround responses associated with founding family involvement may be considered more “responsible” than other firms because of their reluctance to engage in employee retrenchment (Cascio, 2002). More importantly, as turnaround situations become more severe or when firm age increases, founding family involvement increases firm’s resilience (cf., Lins et al., 2017) and overperformance. Firms with founding family involvement seem able to capitalize on the unique advantages of their evolved social capital endowment, making them particularly resilient in times of crisis (Aldrich & Meyer, 2015). Thus, beyond underlining the necessity of adapting turnaround responses to the social context in which firms operate, our findings highlight the need for family firm leaders to consider their firms’ social capital endowment as a unique competitive advantage in turnaround situations (Brewton et al., 2010; Zahra, 2010; Zellweger et al., 2019).

Therefore, this study constitutes an indirect test of a central conjecture in the governance literature: the assumption that continued founding family involvement facilitates the opportunity to garner and rely on emergent social capital resources as a unique performance driver (Ahrens et al., 2019; Lins et al., 2017; Pearson et al., 2008). Our results imply that social capital that is nurtured by previous generations can be transferred across family generations to ultimately constitute a performance advantage (Ahrens et al., 2019). Taken together, these insights pave the way to an overarching family firm theory that explains the synergies between family and business from an evolutionary perspective (Dyer et al., 2014).

Finally, the evidence presented has implications for the debate on component- and essence-based approaches in family business theory. Chua et al. (1999) suggest that component approaches (e.g., relying on the CEO, board, or ownership involvement of the founding family) fail to capture the essence of the family firm, especially the intention to pursue a vision that is potentially intergenerationally sustainable across family generations. They suggest that components of involvement are weak determinants of family firm behavior. Conversely, we find that the use of fine-grained components strongly predicts firm behavior in crises. Our study suggests that components of involvement can, to a large extent, overcome intention issues (Chua et al., 1999), especially when components adequately capture family firm heterogeneity (Neubaum et al., 2019) and are delineated using theoretical guidance from family firm research (Miller et al., 2011; Miller & Le Breton-Miller, 2011).

Research on Identity Threat

Our work suggests that responses to identity threats—an understudied phenomenon—can have both positive and negative organizational consequences. Therefore, we contribute to the current understanding of the consequences of identity threats (J. L. Petriglieri, 2011). While extant research has particularly emphasized the negative consequences of identity threats (Blanz et al., 1998; Breakwell, 1986), we show that individual-level identity threats (e.g., the prospect of losing the role of a family firm matriarch or patriarch), while imposing psychological strain on the leaders themselves (Lazarus & Folkman, 1984), can lead to positive collective outcomes. This is documented by the superior turnaround performance associated with founding family involvement in cases of high turnaround severity or firm maturity, as well as by the evidence of multiple founding family involvement cases. Thus, what is problematic for firm leaders themselves may not necessarily be detrimental for their firm; in fact, the effects can be opposite in direction. In this regard, our work facilitates a more differentiated understanding of how individual identity threats relate to organizational phenomena.

Considering the evolution of a firm’s social context with firm age, our work further suggests that the organizational-level impact of identity threat responses is fundamentally shaped by a firm’s social context and that the consonance (or conflict) of the threat response with the expectations of the firm’s social context triggers a beneficial (or detrimental) echo. Thus, mirroring research on the construction of identities, scholars need to go beyond the individual to fully understand the consequences of individual identity threats. There is a need to study an individual in his or her social context, particularly, the (emergent) structures, norms, and constellations of expectations and obligations that inter alia mark this context (Asch, 1952; Simmel, 1895; Thibaut & Kelley, 1959).

Theories on the Conceptualization of Identities

Foundational research has conceptualized identity as static and driven by the psychological desire for stability of the self (e.g., James, 1890; Strauss, 1959). More recently, management researchers have ignited an ongoing debate about whether identity should be seen as a more dynamic concept and have examined when and how leader identities change (Ashforth, 2000; Ibarra, 1999). Scholars have argued that individuals can “enrich” their identities over time by incorporating experiences and feedback gained from social interaction (Pratt et al., 2006, p. 256). Similarly, they propose that “leaders’ identities tend to shift from individual to more collective orientations as their expertise develops” (Day & Harrison, 2007; Ibarra et al., 2014; Lord & Hall, 2005, p. 592). Notably, at least under threat, our results provide a strong indication that individuals maintain a historical, valued “core identity,” which they “fall back” on in times of crises. This raises questions regarding how much value individuals attach to the gradual enrichment of their identity and how durable or persistent those enrichments are under threat. Consequently, the tight coupling between social context and identity suggested by existing literature may be much looser and entail dysfunctionalities. In the face of an evolving social context, this nuance has considerable practical implications. In our study, it is particularly visible in cases where the founder’s entrepreneurial “core” identity does not grasp the increasing obligations to organizational stakeholders in times of crisis. Crisis performance suffers when founders’ actions are out of step with their firms’ social contexts.

On a trans-generational level (i.e., between firm founders and founder descendants), our results confirm a (core-)identity adoption toward more collective orientations. In fact, a potentially detrimental “ossification” of a core identity (the founder involvement case) can be broken at a trans-generational level between the founder and the next family generation: The identities of incoming family members appear to better reflect the evolving social context of the firm, especially—as our indicative collateral analyses suggest—when multiple family members are also involved in the firm. From an evolutionary and conceptual perspective, this suggests that the adoption and adaptive mutation of leader identities occur mainly between (family) generations and in response to the evolving social context to which the identities of incoming leaders relate (Ashforth, 2000).

This insight carries normative implications for research on leader prototypicality (Ibarra et al., 2014). On the one hand, it suggests that as the social context surrounding the firm evolves, so do stakeholders’ expectations of what constitutes prototypical behavior (Lord & Hall, 2005). On the other hand, even in very severe turnaround situations, the concept of prototypical behavior as a determinant of ultimate effectiveness appears valid (e.g., Giessner & van Knippenberg, 2008). We document that orienting a firm’s turnaround strategy toward the collective good of the social context surrounding the firm benefits turnaround performance in case of abundant social capital (Fu et al., 2010).

Theories of the Firm

Our study of founder and founding family involvement in turnaround situations reinforces identity as a “root construct” (Albert et al., 2000, p. 13) in management research because it shapes strategic action and firm performance (Hambrick & Mason, 1984; March & Simon, 1958). Similarly, it places the social individual at the helm of a firm and as a critical unit of analysis (Asch, 1952) by portraying them in reciprocal relation to an emergent social context, its inherent norms, and the constellations of expectations, obligations, and shared schemata (Thibaut & Kelley, 1959). This perspective holds several important implications for the theory of the firm. First, it goes beyond the notion of agency theory, which debates the unique performance consequences of founder and family involvement in ownership and management from opposing viewpoints (Miller et al., 2011). Some scholars argue that such firms overperform due to resolved Type I agency conflicts (avoiding monitoring costs by reconciling incentives) (Jensen & Meckling, 1976), while others note that they are prone to Type II agency conflicts (seizing private benefits of control at the expense of minority owners) and underperform (Morck et al., 2005). An identity perspective contributes a reconciliatory theoretical explanation by emphasizing that it is the social individual’s identity (i.e., those exerting influence on the firm) that may elicit performance effects. Correspondingly, one may look beyond the question of whether agency conflicts are resolved and consider how influential individuals socially construct their selves and elicit performance effects (Miller et al., 2011).

Second, by incorporating how social forces affect the precedence of specific courses of action at the individual level, our findings may complement frameworks that consider an individual-centric approach to predicting organizational phenomena (Hambrick & Mason, 1984). For example, upper echelons theory posits that the personal characteristics, values, and preferences of those at the firm’s helm affect organizational outcomes (Hambrick & Mason, 1984). It seems logical to extend this framework by acknowledging the interference of a social dimension, namely, an individual’s identity (Stryker, 1987; Tajfel, 1974); however, this has remained overlooked thus far. Notably, such a theoretical extension would fit flawlessly into the upper echelons theory’s well-understood mechanics, as individuals derive considerable degrees of self-esteem and self-efficacy from their identities (Gecas, 1982; J. L. Petriglieri, 2011), making it a key element of personal preference.

Finally, we call for a widening of the lens beyond the individual level to one that also encompasses the group level when explaining a firm’s behavior and performance, to better understand how organizational evolution alters social contexts, and therefore, assumed leader identities, both of which conjointly determine (the heterogeneity of) organizational trajectories (Carroll, 1984; Ekeh, 1974; Long, 2011). By adopting such a perspective, one may begin to understand why the established wisdom that firms with founder involvement are associated with positive effects on firm performance (Adams et al., 2009; Bennedsen et al., 2007; Carroll, 1984; Morck et al., 1988; Villalonga & Amit, 2006) does not apply to the crisis context, where founder behavior (individual level) may conflict with the expectations of the firm’s social context (group level).

Practical Implications

In crisis situations, the way out is often hidden, obscure, and ambiguous. Our work debunks some of the mystery surrounding turnaround management by facilitating our understanding of the turnaround management of firms with founder and founding family involvement—the most predominant governance context worldwide (Faccio & Lang, 2002; La Porta et al., 1999). In particular, we shed light on the distinct turnaround strategies associated with founder and founding family involvement, and the benefits and detriments of their involvement in their firms’ turnaround performance. Enabling reflection on these coherences helps firm leaders, owners, boards, entrepreneurial families, and policymakers respond to existential crises more adequately and make economies more robust.

In this regard, CEOs, board members, and owners may follow our rationale and consider the social context of a firm when designing the most-effective turnaround measures. The distinct crisis responses in Table 5 are particularly insightful for practitioners in this respect. Decision-makers in mature family firm contexts, in particular, should double-check if layoffs or new wage agreements, or more employee-related retrenchment in general, are really necessary; or perhaps a more “responsible” crisis strategy can avoid or reduce such measures and the damage they inflict on the firm’s social capital and social structure (Cascio, 2002).

Another key takeaway is that “taming the founder” can become a major objective in turnaround situations as founders tend to advocate overly “bold” turnaround responses (Table 5). This objective is nontrivial when an endowment of ownership or the duality of CEO and chairman furthers the founder’s power. Yet our analyses suggest that offering an intergenerational perspective to the founder, via the inclusion of founding family involvement, may contribute to such a “taming” by blending their entrepreneurial identity with the meanings of familial identity. Indeed, the collateral analysis in Table 4 suggests that when the founder’s involvement is coupled with that of the founding family, the performance effects may no longer be significantly negative. For practitioners (and advisors), it may thus be helpful to emphasize a long-run family perspective that respects and includes the voice of the next generation in the boardroom and in decision-making, particularly in mature firms. Moreover, for post-founder entrepreneurial families, our work suggests that during crises, the involvement of multiple founding family members may be advantageous. Assuming this to be true, asking for familial support might be wise, and familial identity may be reinforced in such a constellation, which signals reassuring commitment to the firm and its stakeholders. Finally, targeted one-day family firm crisis-management seminars that link topics of retrenchment and recovery with management for the long run, social capital, and responsibility are conceivable flanking measures. They could not only spark self-reflective cognitive processes in founders but also hone crisis-management skills in the board and family.

Limitations and Future Research

Future research may wish to go beyond publicly traded organizations and apply our framework to private firms. The artifacts of various constellations of founder and founding family involvement could reveal effects of considerable magnitude in the highly professional, normed, and regulated setting of S&P 1,500 firms. Presumably, these effects on organizational trajectories are even more pronounced in unregulated and less-controlled settings, such as private or small- and medium-sized companies. In addition, the S&P 1,500 environment implies a limited number of cases within the sub-categories across the landscape of heterogeneous constellations of family and founding family involvement. Although this limitation of our collateral analyses is inevitable, as turnaround cases rarely occur, it could be overcome by future turnaround research that targets family firm heterogeneity using potentially larger samples of a private firm environment to inquire into the full spectrum of family firm heterogeneity. In addition, the greater variation in such a bigger private firm sample could provide more means to overcome the limitation of this study that founder as well as founding family involvement and the moderator firm age are for natural reasons, to some degree, related. Moreover, although we have several selection and firm-level controls in place, all firms, wherein there is post-founder founding family involvement, have arguably survived a family succession process at least once and, thus, possess what could be called “intergenerational survivability.” This is an aspect that we might be capturing incompletely and could be a limitation of this study. While a deeper inquiry into this issue is beyond the scope of this work, obtaining a better understanding of survivability between generations (and how it is linked to crisis behavior) remains a key challenge for future family firm research. As is often seen in leadership research (Hambrick & Mason, 1984), this study relies on an unobtrusive empirical approach that utilizes multiple proxy variables from external sources because of the inherent difficulty of observing overarching constructs (i.e., identity) directly at the individual level. Therefore, we encourage future research to measure leader identity through a finer lens, for example, in interviews across private firms, via its three related elements of individual internalization, relational recognition, and collective endorsement (DeRue & Ashford, 2010). Ideally, this should capture both the components and the essence of a family firm and explore their impact on crisis behavior and outcomes.

Footnotes

Acknowledgements

The authors thank Franz Kellermanns, Danny Miller, Isabelle Le Breton-Miller, Sue Ashford, Donald Neubaum, Keith Brigham, Michael Woywode, and Max Strothenke for their helpful contributions. The authors would also like to thank the anonymous reviewers. Jan-Philipp Ahrens and Marc Kowalzick share the first authorship for this work. This work holds best article nominations from: 9th Annual Conference of German Family Business Research Institutes (2019), 24th Interdisciplinary Annual Conference on Entrepreneurship, Innovation, and Mittelstand (2020), and the European Academy of Management (EURAM), 20th Annual Conference (2020) where it was nominated for the EURAM conference overall award. It also holds the following best article awards: 18th Interdisciplinary European Conference on Entrepreneurship Research (IECER) (2020) and European Academy of Management, 20th Annual Conference (2020), Best Article of the Family Business Research Strategic Interest Group.

Author’s Note

Marc Kowalzick is also currently affiliated with Erasmus University in Rotterdam, the Netherlands.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.