Abstract

How do owners of family firm portfolios restructure poorly performing firms? To answer this question, we conducted an in-depth qualitative case-study analysis of six poorly performing family portfolio firms, on the basis of 39 interviews, 117 pieces of archival data, and observations we gathered over 2 years. Drawing upon the socioemotional wealth (SEW) perspective and escalation-of-commitment literature, we suggest that family firm owners initially show refraining behaviors toward restructuring their poorly performing portfolio firms. Subsequently, they exhibit escalating behaviors by first investing and then reshuffling assets, to safeguard firm-level SEW. Yet, when retaining these poorly performing firms threatens the existence of the remaining portfolio and, thus, portfolio-level SEW, family firm owners exhibit de-escalating behaviors by divesting. Preferably, they attempt a sale and, when a sale is no longer an option, a liquidation. We developed a model that contributes to a more granular theoretical understanding of the family firm’s restructuring behavior, in the context of portfolio entrepreneurship.

Keywords

Introduction

Socioemotional wealth (SEW) considerations have been at the core of research explaining family firm behavior (Berrone et al., 2012). For instance, studies have investigated how SEW affects international expansion (Pukall & Calabro, 2014), innovation (Fuetsch, 2022; Kosmidou & Ahuja, 2019), mergers and acquisitions (M&A) (Hussinger & Issah, 2019), or family firm growth in general (Moreno-Menéndez & Casillas, 2021). These studies have convincingly argued and shown that firm ownership induces emotional endowments. In turn, these render family firm decisions reliant on nonfinancial rather than financial criteria (Gómez-Mejía et al., 2007) that lead, for instance, to more conservative strategies. Despite our increasing knowledge of family firm decision-making in “growth-related” scenarios, we do not have sufficient knowledge of the effect of their SEW considerations on restructuring that target improving dissatisfying firm (financial) performance. In this context, restructuring refers to the reconfiguration of resources and capabilities (Berry, 2010; King et al., 2022) and consists of a range of strategic tools, such as divestments, asset sales, and organizational structural changes (Bowman & Singh, 1993; Brauer, 2006; Singh, 1993).

Family firm research has emphasized that poor firm performance might bring financial rather than SEW considerations to the fore (Gómez-Mejía et al., 2018). It provides evidence that due to SEW considerations, family firms engage in fewer divestments than their non-family counterparts (Feldman et al., 2016; Kim et al., 2019; Zellweger & Brauer, 2013). Moreover, family firms often escalate their commitment (Sharma & Manikutty, 2005) and feel closely attached to their assets and employees (Block, 2010). Nonetheless, at times, they must divest to safeguard the firm’s long-term viability. Yet, we know little about how SEW affects the specific restructuring activities that family firms undertake, particularly portfolio-owning family firms, in which one business family owns multiple firms with potentially heterogeneous performance. Research often arises on the “one-family-one-firm” assumption (Discua Cruz et al., 2013; Michael-Tsabari et al., 2014), in which divestiture signals a total loss of SEW. However, Zellweger and colleagues (2012) noted that roughly 90% of their surveyed sample of families controlled more than one firm. Hence, SEW considerations in restructuring family firms appear to be more complex because partial divestiture is a possibility. Research remains unclear about where the socioemotional endowment resides (i.e., the appropriate level of analysis) (Brigham & Payne, 2019, p. 328; Hernández Linares & Arias-Abelaira, 2022; Kammerlander, 2022; Swab et al., 2020).

As a result, we currently lack a comprehensive understanding of how family firm owners restructure poorly performing portfolio firms on the basis of their SEW and choose between different restructuring approaches, including but not limited to divestment. Closing this gap is important because restructuring literature has largely omitted family firms (King et al., 2022), ignoring their idiosyncratic restructuring behavior stemming from SEW (Chirico et al., 2020; Meglio & King, 2019). Furthermore, increasingly volatile and disruptive environments will require family firms to restructure even more in the future (Kotter et al., 2021). Accordingly, our study examines the following research question: How does SEW shape family firms’ restructuring of poorly performing portfolio firms?

We attempt to answer this question by employing an explorative multi-case-study approach (Eisenhardt, 1989; Yin, 1994) to investigate six private family businesses with poorly performing portfolio firms that have each restructured at least two of them. In total, the six cases restructured 22 portfolio firms (our level of analysis), ultimately divesting 14. Our main data source was 39 in-depth interviews with supplemental observations and 117 pieces of additional case-related archived material, such as press releases, newspaper articles, videos, annual reports, or firm history books. Our inductive analysis revealed a three-phase restructuring process. We found that family firm owners first showed refraining behaviors regarding their poorly performing portfolio firms, which led to avoiding restructuring activities. In this phase (Phase 0: retention), family firm owners did not explicitly differentiate between firm-level and portfolio-level SEW. Interestingly, when they could not avoid the issue any longer, family firm owners focused on firm-level SEW (Phase 1: escalation). The family firms displayed escalating behaviors regarding their poorly performing portfolio firms, which, in turn, drove their restructuring choices (investing and reshuffling). When these restructuring efforts remained unsuccessful, family firm owners shifted their focus from firm-level to portfolio-level SEW (Phase 2: de-escalation), which led to de-escalating behaviors toward their poorly performing portfolio firms (i.e., divesting or liquidating). To develop a theoretical model of family firms’ restructuring in the context of portfolio entrepreneurship (Sieger et al., 2011) using our data, we drew upon the escalation-of-commitment literature (e.g., Sleesman et al., 2012, 2018) coupled with the SEW perspective (Gómez-Mejía et al., 2007).

Our study findings contribute to the literature in three ways. First, we extend the SEW perspective (Berrone et al., 2012; Gómez-Mejía et al., 2007) to family firm portfolios (Sieger et al., 2011) and present evidence that owners of those portfolios also derive SEW from their non-core portfolio firms, that is, firm-level SEW. Our theorizing that family firm owners base their strategic restructuring decisions on firm-level and overall portfolio-level SEW preservation considerations, with the latter taking precedence when at risk, extends the current SEW logic by distinguishing between two levels of SEW. Thus, we also answer recent research calls (Brigham & Payne, 2019; Kammerlander, 2022; Swab et al., 2020) suggesting that portfolio firms as well as the overall portfolio are both necessary levels of analysis for SEW in the context of family firm portfolios. Our study is one of the first to empirically present different levels of SEW analysis. As such, it goes beyond prior work by providing in-depth qualitative empirical data that shows where SEW resides, and how this point might shift over time.

Second, we advance the literature on restructuring in family firms (for a review, see King et al., 2022) by shedding light on how escalating commitment (Staw, 1976) can contribute to a better understanding of family firm restructuring behavior. We find that after a phase of escalation of commitment (Sharma & Manikutty, 2005), family firms engage in de-escalation of commitment to protect their portfolio-level SEW. We further inform this literature stream by revealing which specific restructuring activities (e.g., reshuffling, investing, divesting) occur throughout the restructuring process. Third, we extend divestment research on family firms (Chirico et al., 2020; DeTienne & Chirico, 2013) by providing novel insights into family firms’ preferences for specific divestment approaches. Building on and extending prior findings that might, at first sight, seem contradictory to ours (e.g., Akhter et al., 2016; DeTienne & Chirico, 2013), we discuss why and how context might affect certain restructuring preferences.

Theoretical Background

SEW Considerations and Restructuring in Family Firms

Restructuring activities promise to improve firm performance (Brauer, 2006; Hoskisson et al., 1994; Shimizu & Hitt, 2005) and renew the firm in a quest for long-term survival (Bergh, 1998; Markides, 1995). Despite these prospects, firms facing restructuring generally exhibit inertia due to barriers such as managers’ emotional attachment to firms (Burgelman, 2002) and sparse restructuring experience (Shimizu & Hitt, 2005). In general, restructuring encompasses a wide range of activities that typically comprise three categories (Bowman & Singh, 1993; Brauer, 2006; Singh, 1993): asset restructuring (e.g., sales), organizational restructuring (e.g., organizational set-up and workforce changes), and portfolio restructuring (e.g., M&A, divestments).

While knowledge of asset or organizational restructuring in family firms is limited (for a review, see King et al., 2022), extant research suggests that family firm owners demonstrate a particularly strong reluctance to divest their entire firm, which would imply the total loss of control (Gómez-Mejía et al., 2007), the coupling of their identity with the firm’s (Deephouse & Jaskiewicz, 2013), their binding social ties with employees, and their transgenerational succession abilities (Jaffe & Lane, 2004; Zellweger et al., 2012), all of which represent important dimensions of SEW (Gómez-Mejía et al., 2007, 2011). To avoid such losses, family firm owners are willing to endure sustained periods of poor firm performance, delaying divestment (DeTienne & Chirico, 2013; Zellweger & Astrachan, 2008). Divesting the entire family firm “is always seen as a failure” (Zellweger et al., 2012, p. 141) rather than an opportunity to renew the firm (Salvato et al., 2010a; Sharma & Manikutty, 2005). Therefore, regardless of the financial considerations, keeping the family firm intact and passing it on to the next generation via family succession is a goal in itself, to safeguard family firm owners’ SEW (DeTienne & Chirico, 2013; Gómez-Mejía et al., 2007). However, when family firm owners must divest their entire firm (e.g., due to sustained poor performance), they prefer divestment via merger over liquidation, and liquidation over sale (Chirico et al., 2020), to maintain at least part of their initial SEW. Hence, SEW-based decisions play a major role in family firm restructuring (Labaki & Hirigoyen, 2020).

Few studies have investigated restructuring, particularly divestments of family firms, in the context of portfolio entrepreneurship (Akhter et al., 2016; DeTienne & Chirico, 2013; Praet, 2013), though divesting a portfolio firm differs from divesting the entire family firm. Indeed, divesting a portfolio firm in a family firm portfolio allows family firm owners to retain their family firm at least partially. When family firm owners divest their entire firm, the family firm completely ceases to exist (Michael-Tsabari et al., 2014). Studies that do exist on divestments in family firm portfolios suggest that family firm owners particularly attached to their core business are thus more reluctant to divest their core than are other portfolio firm owners (DeTienne & Chirico, 2013). In addition, Akhter et al. (2016, p. 371) identified an attitude that amounts to “if we can’t have it, then no one should,” a pattern that suggests family firm owners preferring to shut down, rather than sell a portfolio firm, even though a sale typically brings greater financial returns (Decker & Mellewigt, 2007; Wennberg et al., 2010). The desire to “restart” the business later and, thereby, regain SEW drives this preference. However, since these studies exclusively considered divestments in family firm portfolios, the family firm literature still lacks a comprehensive understanding of other potential restructuring activities that family businesses use to deal with poorly performing portfolio firms, and how SEW shapes these activities. This is important because such research could shed light on family firms’ idiosyncrasies in relation to SEW, in different periods of poor performance. Furthermore, identifying where the socioemotional endowment resides (i.e., firm or portfolio level) helps to explain restructuring decision-making.

SEW Considerations and Escalation of Commitment in Family Firms

In his seminal work, Staw (1976) described decision-makers often escalating their commitment to an ineffective course of action beyond a financially feasible point (Brockner et al., 1986; Staw, 1981; Staw & Ross, 1978, 1987). Scholars have also referred to such escalating behaviors as “throwing good money (or resources, more generally) after bad” (Sleesman et al., 2012, p. 541). They advance a multitude of reasons to suggest why decision-makers engage in escalating behaviors, including sunk costs (Arkes & Blumer, 1985), positive historical performance (Moon & Conlon, 2002), institutional inertia, emotional attachment, and personal responsibility (Staw, 1976).

The phenomenon of escalation of commitment in the family firm field has only recently started to receive research attention (Chirico et al., 2018; Pongelli et al., 2019; Woods et al., 2012). Research shows that family firm owners are particularly prone to escalating their commitment to their firm as a result of their SEW (Pongelli et al., 2019). Their motivations, stronger than those of decision-makers in non-family firms (Salvato et al., 2010b), include their emotional commitment to the firm (Sharma & Irving, 2005; Zellweger & Astrachan, 2008), their personal responsibility to maintain the family’s identity with the tradition and legacy of the firm, and their extended time horizon (Lumpkin & Brigham, 2011; Zellweger, 2007). Moreover, research suggests that as a result of their SEW, family firm owners escalate their commitment to their firm in the face of performance below aspirations (Chirico et al., 2018). They even use their private funds to support and preserve their failing family firm, mainly for affective, SEW-related reasons rather than for financial returns (Minichilli et al., 2016; Villalonga & Amit, 2010). In a more recent review, Sleesman and colleagues (2018) noted that decision-makers are more likely to de-escalate their commitment when they are not overconfident (McCarthy et al., 1993; Roberto, 2002), motivated extrinsically rather than intrinsically (DeTienne et al., 2008), and not involved in the initial decision (Boulding et al., 1997; Inkpen & Ross, 2001). Some research has progressed in explaining family firms’ escalation of commitment, but knowledge of de-escalation remains scarce (Salvato et al., 2010a).

Despite the overwhelming prevalence of family firms comprising multiple firms (e.g., Sieger et al., 2011; Zellweger et al., 2012), scholars have failed to examine escalating and de-escalating behaviors when the poor performance of one or several portfolio firms (rather than the one and only core family firm) affects only part of the family’s SEW. Using insights from the escalation of commitment perspective (Staw, 1976), we suggest that investigating poorly performing family portfolio firms could advance knowledge regarding how family businesses restructure their portfolios and how (if at all) escalation of commitment as a result of their SEW influences their approach.

Method

Research Setting and Theoretical Sample

We applied an explorative, qualitative research design (Miles & Huberman, 1994; Yin, 1994) based on a multi-case study (Eisenhardt, 1989; McDonald & Eisenhardt, 2020), to extend the literature on family firm restructuring. The lack of research on the restructuring of poorly performing firms within family firm portfolios made a case-study design particularly appropriate (Eisenhardt, 1989). In addition, our case-study approach aligns with research that examined strategic decisions in the family firm portfolio context (e.g., Akhter et al., 2016; Riar et al., 2021), a most suitable approach to answering our research question (Edmondson & McManus, 2007).

We used a theoretical sampling method and chose cases that were likely to replicate or extend theory (Eisenhardt, 1989). This study was embedded in a larger research project focusing on acquisitions in family firms. As our focus was on family firm portfolios, we first developed a long list of German family firms and identified those consisting of multiple firms as those from which to select the sample. To create such a long list, we consulted company lists from industry associations and books outlining the family firm landscape (e.g., German Family Enterprises by Seibold et al., 2019) as well as lists of renowned family firms available on the internet (e.g., Die Deutsche Wirtschaft). We used information from these data sources, as well as potential case firms’ websites, press releases (retrieved from Factiva), and newspaper articles, to identify those with a portfolio of recent acquisitions. We reached out to the family firms via email, starting with those for which we could get initial contact data, for example, through mutual contacts. In a subsequent phone call with decision-makers, we clarified our research purpose and approach (i.e., requesting multiple interviewees including both family and non-family managers), responded to potential questions (e.g., regarding research ethics), and scrutinized the family firms’ fit for the research project (see details below). To become part of the sample for the restructuring study (as opposed to the broader acquisition project), the decision-makers had to confirm that the family had restructured at least two portfolio firms and was willing to openly talk about its related experiences.

We focused on mid-sized family firms from Austria, Germany, and Switzerland, three countries with a high prevalence of established family firms and similar cultural backgrounds (Bornhausen, 2022), which limits external variation (Eisenhardt, 1989). Moreover, we focused on family firms with annual revenues ranging between 200 million and four billion euros, big enough to consist of true portfolios. At the same time, we excluded large conglomerates with professionalized restructuring and divestment processes. While we were open to including firms in several industries, to express variety, we specifically focused on family firms in asset-heavy, established industries that consider family firm reputation relevant, reflecting the core characteristics of the German Mittelstand (Simon, 1992).

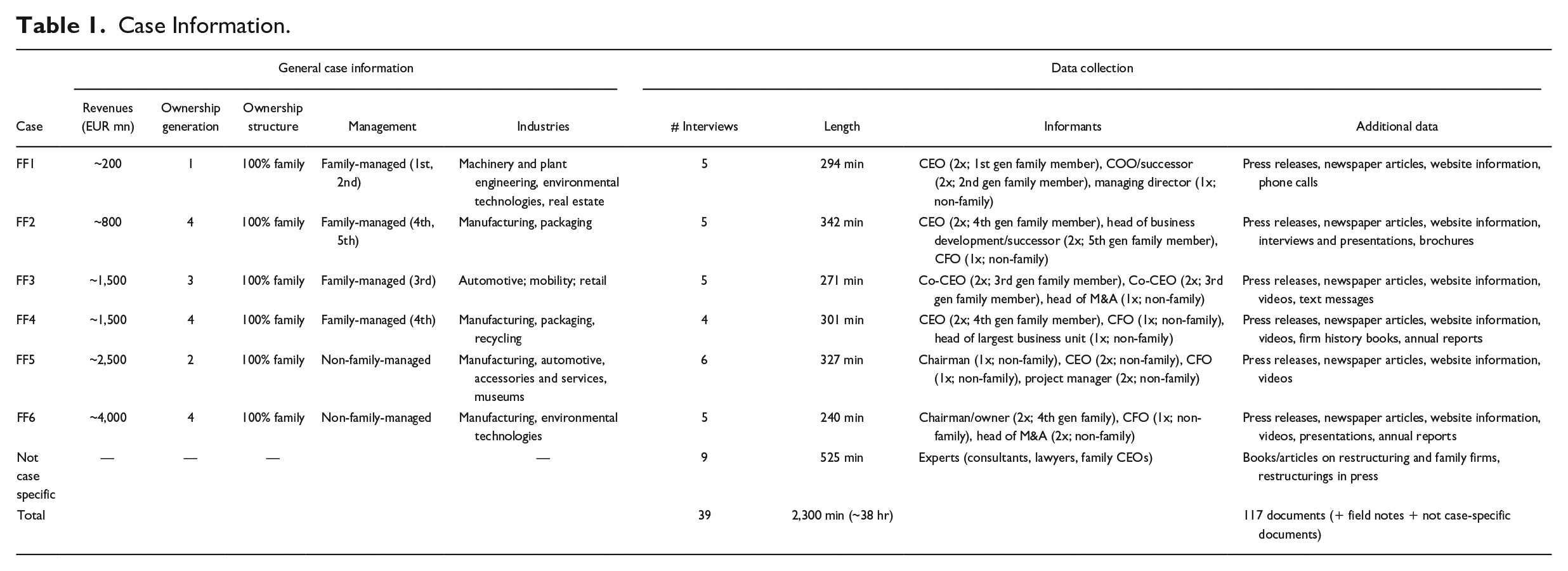

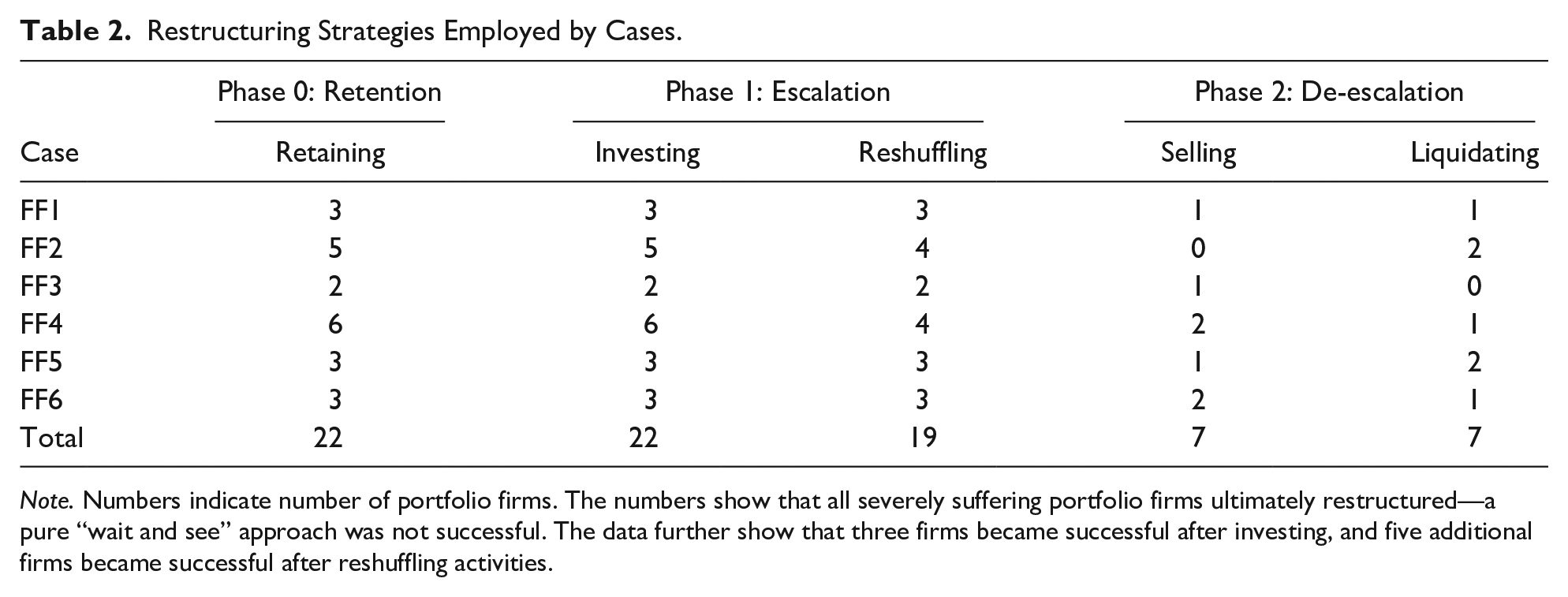

The interviewed firms had to fulfill four theoretical sampling criteria: (1) the family possessed at least 50% of firm control rights (involvement approach) (Chua et al., 1999; De Groote & Bertschi-Michel, 2021; Diaz-Moriana et al., 2020); (2) the family intended to hand over the firm to the next generation (essence approach) (Chua et al., 1999; De Groote & Bertschi-Michel, 2021; Erdogan et al., 2020); (3) the firms consisted of at least three portfolio firms; and (4) the firms had undergone restructuring of at least two portfolio firms. Finally, we selected six private family firm portfolios with poorly performing firms that family members fully owned. The six family firm portfolios encompassed the restructuring activities of 22 portfolio firms (our level of analysis) and the divestment of 14 portfolio firms. Table 1 provides an overview of our cases, and Table 2 summarizes the restructuring approaches the case firms employed.

Case Information.

Restructuring Strategies Employed by Cases.

Note. Numbers indicate number of portfolio firms. The numbers show that all severely suffering portfolio firms ultimately restructured—a pure “wait and see” approach was not successful. The data further show that three firms became successful after investing, and five additional firms became successful after reshuffling activities.

Data Collection

This study employed a combination of primary and secondary data, consisting of two rounds of interviews, archival records, and observations we gathered over 2 years. The primary data source was a set of 39 in-depth interviews with family members (e.g., owners, CEOs, successors), non-family managers (e.g., head of M&A, CFO), and experts (e.g., consultants, lawyers, CEOs of other family firms) that either accompany or decide on restructuring activities on a regular basis. We made sure to interview both family members (typically very knowledgeable about the specific reasons for engaging in certain restructuring activities) and non-family members (e.g., employees working on restructuring and, hence, able to provide a complementary perspective on its execution). We conducted two rounds of interviews with informants from our cases, in line with prior qualitative research involving family firm owners (e.g., Bertschi-Michel et al., 2020; Riar et al., 2021). In the first round, we interviewed all case informants and asked them to provide an overview of their portfolio firms and the restructuring efforts they spent on poorly performing portfolio firms. Next, we delved deeper into each of the poorly performing portfolio firms, asking questions about the different restructuring activities the family firm employed, the motives for their implementation, their order of implementation, the reasons for choosing specific restructuring activities, and the respective outcomes. The initial case interviews lasted 68 min on average and followed a semistructured interview guide that we mostly built on conceptual and empirical insights from family firm research on divestments (e.g., DeTienne & Chirico, 2013; Sharma & Manikutty, 2005) and portfolio entrepreneurship (e.g., Discua Cruz et al., 2013; Sieger et al., 2011; Zellweger et al., 2012).

After a first round of data analysis, we decided to arrange follow-up interviews with all family firm key decision-makers involved in their firms’ restructuring decisions, to resolve any discrepancies and validate our initial insights with our participants (Creswell, 2009). These second-round interviews took place roughly 6 months after the first round. As they already knew the interviewers and the nature of their research, the family firm decision-makers were even more open to sharing the emotions and feelings they experienced throughout the restructuring activities and explaining how these emotions and feelings guided their restructuring decisions. In the follow-up interviews, which lasted 44 min on average, we once again asked informants to recall concrete restructuring examples, allowing for more accurate accounts and limiting the risk of post hoc rationalization (Fisher & Geiselman, 2010). The second-round interviews also allowed a member check (Jick, 1979), where informants could provide feedback on our preliminary findings and the emerging theoretical model (Flick, 2009).

In addition to the interviews with case informants, we also conducted interviews with experts to validate our findings across a broader family firm sample. These interviews averaged 58 min, during which we asked questions about their experiences with restructuring activities employed in (their own) family firm portfolios and the underlying reasons for the restructuring decisions. Throughout the interviews, we paid attention to asking open-ended questions, to encourage informants to share their thoughts and allow for interview flexibility.

All interviews took place in 2020 and 2021, and we recorded and transcribed them verbatim. To triangulate our findings (Eisenhardt & Graebner, 2007; Jick, 1979), we collected and analyzed archival material from the firms’ current and historic websites, press releases, newspaper articles, videos, company presentations, brochures, firm history books, annual reports, phone calls, and text messages. In total, we gathered 117 pieces of evidence from these additional data sources. Prior to the interviews, we oriented ourselves using contained important background information on the cases’ portfolio firms. Later, that material also helped us to analyze our interview data. Triangulating data from multiple data sources and informants allowed us to reduce biased interpretation and improve the findings’ robustness (Patton, 2002; Yin, 2009). More information regarding the archival material used for each case appears in Table 1.

Data Analysis

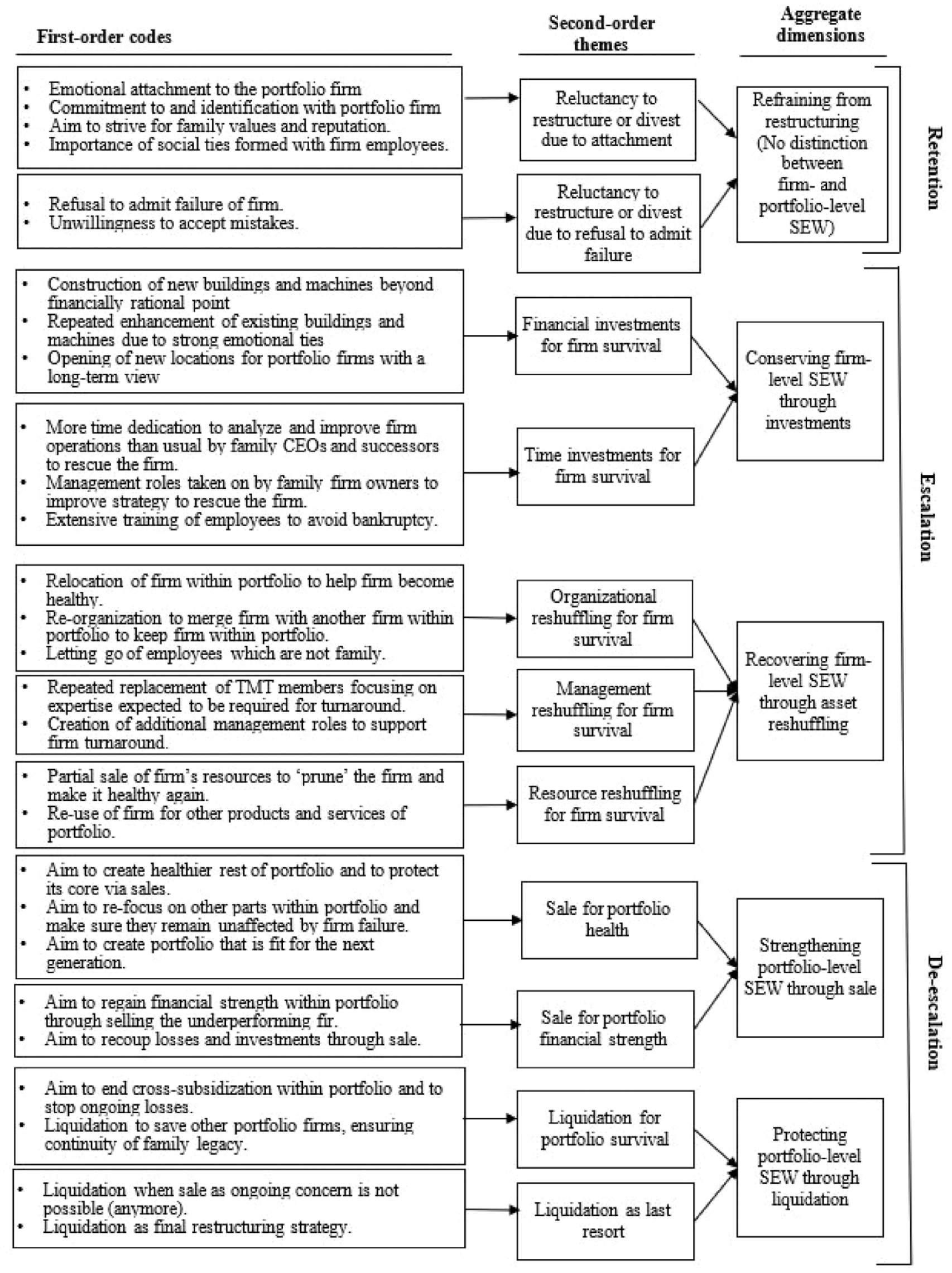

Our analytical approach consisted of inductive analysis of our data from multiple cases, informed by our knowledge of extant research on family firms, in line with prior case-study-based research (e.g., Akhter et al., 2016; Diaz-Moriana et al., 2020; Langley & Abdallah, 2011). In the first step, we carefully reviewed our (interview and archival) data and created case descriptions for each family firm and its poorly performing portfolio firms. These descriptions detailed the restructuring activities that each family firm implemented in the poorly performing portfolio firms, the motives and sequence of implementation for the restructuring activities, and the respective outcomes. Second, following the procedures that Gioia and colleagues (2013) outlined, we inductively coded the data using NVivo software (e.g., Akhter et al., 2016; Riar et al., 2021) (Figure 1 shows the outcome of this coding process). We first used an open coding process to extract first-order codes from the interview data (Mayring, 2008; Van Maanen, 1979), keeping our research question in mind and coding text passages that appeared relevant to the restructuring activities in our cases.

Data Structure.

We coded the material and created categories from emergent themes that we deemed relevant to explaining restructuring activities, forming our first-order codes. Then, we searched for themes to group into higher-level codes, to produce a set of second-order codes. For example, we collapsed data containing instances of investments for the survival of the firm into two second-order codes that we labeled “financial investments for firm survival” and “time investments for firm survival.” Two coders participated in this process and discussed potential discrepancies until they reached consensus. In the last step, we further aggregated the second-order themes into overarching dimensions. In the process, we iteratively switched between data and extant literature. Comparing our data with extant literature showed us that the four aggregate dimensions referring to different restructuring activities corresponded to different SEW levels. For instance, financial and time investments for firm survival were aggregated into the dimension “conserving firm-level SEW through investments.” Following an iterative research tradition (Reay, 2014; Weber, 1990), we returned to our original data to refine our coding (e.g., regarding SEW), to achieve consistency throughout our analysis.

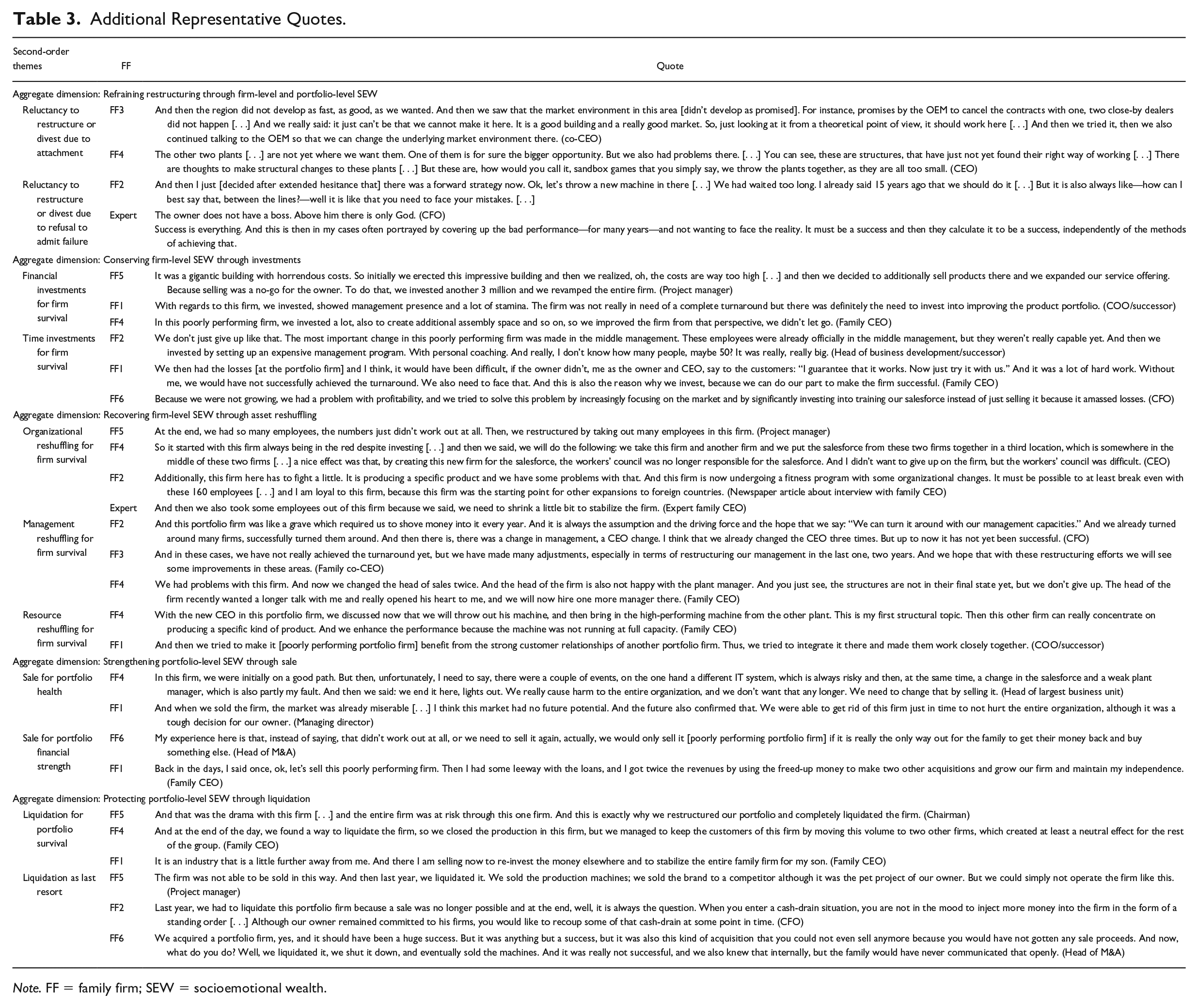

Once we had completed the initial coding, we aimed to detect patterns within and across cases (Eisenhardt & Graebner, 2007; Miles & Huberman, 1994). This comparison enabled us to detect a general pattern concerning how SEW considerations affected restructuring. Moreover, we noticed substantial variation regarding whether the poorly performing family portfolio firms were ultimately sold or divested. Throughout the process, we aimed to triangulate data whenever possible, to validate our cross-case patterns and our emerging theoretical model. All authors participated in the data analysis and resolved rare disagreements through collective discussions to reach consensus (Yin, 2009). To enable external observers to understand the conclusions we derived from our data, additional representative quotes for each second-order theme appear in Table 3. Our coding revealed a model connecting restructuring behavior to SEW preservation considerations that triggered family firm owners’ escalating and de-escalating behaviors.

Additional Representative Quotes.

Note. FF = family firm; SEW = socioemotional wealth.

Findings

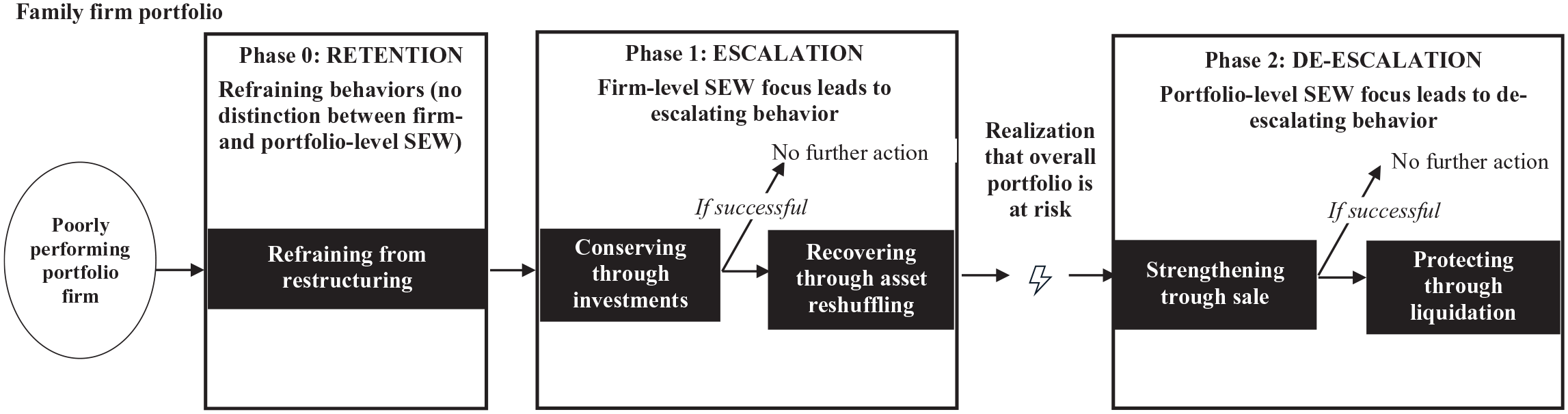

This presentation of our findings reflects the temporal sequence that the family firms followed in addressing poorly performing firms within their portfolios. We highlight how family firm owners’ SEW considerations affected restructuring choices. For this purpose, we differentiate three phases. In Phase 0 (retention), the interviewed family firm owners showed avoidance of restructuring, despite observing their portfolio firms’ poor performance. In Phase 1 (escalation), we found that based on their firm-level SEW preservation concerns, family firm owners escalated their commitment to their poorly performing portfolio firms through substantial investments and asset-reshuffling activities. However, following the realization that their entire family firm portfolio was at risk, in Phase 2 (de-escalation), family firm owners’ portfolio-level SEW considerations led to de-escalating behaviors and, thus, divestment of the poorly performing portfolio firms, preferably via sale rather than liquidation.

Phase 0—Retention: Firm-Level and Portfolio-Level SEW Leading to Refraining Behaviors

Our analysis revealed that our 22 poorly performing and ultimately restructured portfolio firms were either prior acquisitions or firms newly added to the portfolio. However, although they did not constitute the family firms’ core legacy business, we observed that family firm owners were initially reluctant to restructure them, due to SEW concerns. Our cases showed that at the initial stage, family firm owners did not distinguish between firm-level and portfolio-level SEW, showing a strong emotional attachment at both levels.

The case of family firm FF3 is exemplary for the owners’ emotional attachment to their newly built portfolio firms and their subsequent reluctance to restructure those that performed poorly. FF3 had pursued an active growth strategy in recent years, holding 50 portfolio firms in the broader space of “mobility” that two siblings managed as co-CEOs. One stated that they decided not to let go of a portfolio firm that had been performing poorly since its construction 5 years earlier, based on their attachment to that firm and their continued conviction that it could create value for the family firm portfolio in the long term:

It’s the emotional attachment and the pride and so on, which I have. Therefore, it [restructuring] is not automatically the first solution that I am thinking of. In this case, we thought about it, we looked at it, and the sale doesn’t make much sense, so we want to try it another time. I hope we won’t regret it. (Interview, family co-CEO, FF3)

Similarly, family firm owners also remained strongly committed to portfolio firms that either they or their predecessors had acquired. Indeed, our data show that family firm owners initially shied away from substantially restructuring those that were performing poorly. For instance, FF2’s family CEO stated that he retained a poorly performing portfolio firm that his father had acquired in the 1990s, based on the family’s identification with it. The strong identification partly stemmed from his grandmother’s affinity for the portfolio firm’s line of business. That attachment led to preserving this portfolio firm for two decades, despite its sustained poor performance:

And my grandmother was way more emotionally attached to this specific product [. . .] and once, she dared to tell employees in senior positions that as long as she is alive, this line of business will not be closed [. . .] (Interview, family CEO, FF2)

Moreover, an expert who had been advising family-owned portfolio firms on restructuring for over 15 years confirmed our observations. He claimed that he consistently noticed family firm owners’ emotional attachment to and identification with their non-core, poorly performing portfolio firms and their subsequent reluctance to substantially restructure or divest them. However, along with the emotional attachment and identification aspects, he also recalled that family firm owners were reluctant to let go of poorly performing portfolio firms because of the social ties they had formed with their employees. He explained his socioemotional concerns:

They [family firms] are more emotional. A non-family firm will say, “Let’s get rid of it, call the advisor.” The family firm owner, he [or she] refuses to acknowledge it. These family values: “I cannot do that to them [employees] and he [or she; the buyer] will make a non-family firm out of it.” (Interview, expert)

Further explaining the reasons not to engage in restructuring, FF2’s family CEO did not want to admit his own failure to profitably operate this portfolio firm. He explained,

[. . .] and maybe this got transferred a little bit to my father, who saw it as a responsibility to make an acquisition in this line of business, maybe as a postmortem concession. And maybe this emotional attachment of my grandmother got passed on a little bit. And why do I say this? Well, I believe that the admission of a failure is the bigger motive here than social responsibility [. . .] I would say, we fought for this firm for approximately 20 years. My wife was also involved. We didn’t want to admit it. We did it [retained it] for way too long. We really put pressure on ourselves. (Interview, family CEO, FF2)

Furthermore, the daughter of FF2’s family CEO, who temporarily headed another poorly performing portfolio firm that her father had acquired 4 years earlier, noted that substantially restructuring or divesting this portfolio firm was not an option for her since it would have meant admitting that she failed to return the portfolio firm to profitable levels. She explained her concerns:

And we don’t sell it just because it is a loss-making business. And it would be an admission of my own failure [. . .] I have convinced everybody of the firm’s potential. I never doubted it, not even in the bad years, because I also saw that they made mistakes, which we could not easily prevent from happening. (Interview, head of business development/successor, FF2)

Her statement indicates that she at least partly attributed the portfolio firm’s poor performance to her own actions and decisions, which also highlights her close identification with that firm.

Collectively, our data revealed that our interviewed family firm owners closely identified with and had emotional attachments to the non-core portfolio firms they had built or acquired. Also, they showed concern for the employees of these portfolio firms as well as their reputation (which admitting failure might damage). All represent important dimensions of SEW (Berrone et al., 2012; Gómez-Mejía et al., 2007). However, in these initial phases, family firm owners predominantly spoke about their socioemotional concerns for their portfolio firms in general, failing to differentiate between firm-level SEW and portfolio-level SEW. Thus, we posit that along with the SEW they associate with their core legacy business—as family firm literature has extensively discussed (Gómez-Mejía et al., 2007, 2011)—family firm owners also derive SEW from their non-core portfolio firms. Thus, we propose:

Phase 1—Escalation: Firm-Level SEW Focus Leading to Escalating Behaviors

We further found that once they recognized the need to act in response to their portfolio firms’ continued poor performance, family firm owners engaged in escalating behaviors to ensure firm survival. In particular, our sample family firm owners expended significant resources to restructure their poorly performing portfolio firms, in an attempt to return them to profitable levels and conserve firm-level SEW. One example was FF4, which mainly operated in the packaging business. In recent years, it had established three distinct lines of businesses and 33 portfolio firms, through its forward- and backward-integration strategy. However, at one point, three of its portfolio firms performed poorly and “amassed losses that were adventurous” (Interview, head of largest business unit, FF4). Despite these losses, the family CEO remained committed to his portfolio firms and eventually started to invest in their respective plants, for example, replacing old machinery and constructing new buildings. An article from a regional newspaper summarizes the financial investments in one of them:

[FF4] is investing 15 million euros into this firm. Next to a new machine, which started production in January, there will also be a new building that is being erected in the middle of the firm, for which the old roof needs to be teared [sic] down. (Newspaper article, FF4, 2016)

FF4’s CFO further reported that the family CEO also complemented these financial investments in new machinery and buildings with investments of time in management and human resources in the poorly performing portfolio firm. He explained the excessive amount of managerial attention dedicated to solving the performance issues:

He invests in new plants, we get new machinery, we get training [. . .] and then, of course, presence, presence, presence, going there, talking, initiating things, and checking later if they were implemented; control is also important. He always remains committed to his firms. (Interview, CFO, FF4)

Similarly, due to stakeholder-related concerns, an important part of firm-level SEW, FF2’s family CEO also displayed a strong commitment and dedication to conserving his poorly performing portfolio firms. As a consequence, he invested large amounts of financial resources in returning them to profitable levels. For instance, his daughter described the substantial investments in one portfolio firm that had generated a negative profit contribution for the past 12 years:

There was the poor performance of this firm, it was the worst performer in the entire group, and then, well, I as the head of the plant tried to improve the performance, and we continued to invest on a regular basis. Actually, more than in the other firms [. . .] We invested a lot. And I am not even sure if this was good or bad. But my father didn’t let people go just because the firm wasn’t performing as expected. That is not his way at all. (Interview, head of business development/successor, FF2)

Moreover, in all other cases (i.e., FF1, FF3, FF5, and FF6), the family firm owners also chose to invest in their poorly performing portfolio firms to conserve firm-level SEW. When these investments did not succeed in improving the portfolio firms’ performance, the family firm owners continued to retain them in their portfolio. However, in these cases, they changed their restructuring approach and started to reshuffle the portfolio firms’ assets, in an attempt to recover firm-level SEW. For instance, organizational reshuffling occurred through disposing of some assets via sales or moving often non-performing or old assets, such as machines, from the poorly performing firm to other parts of the portfolio. In some cases, the reverse was also true: they moved machines and equipment from other parts of the portfolio to the poorly performing firm, to help support its operations. Moreover, some firms engaged in management reshuffling, adapting the organizational structure by making the poorly performing portfolio firm report directly to the holding company, to increase managerial attention. The FF4 family CEO illustrated this behavior:

And there were cases when investments flopped [. . .] and then we just tried to conceal the losses by selling some assets of the firm. (Interview, family CEO, FF4)

The case of FF5 is also exemplary for the reshuffling that family firm owners employed with their poorly performing portfolio firms when investments in them proved unsuccessful. One of FF5’s portfolio firms that manufactured automotive accessories had been performing poorly for many years. It was retained within FF5’s portfolio and restructured through the implementation of several organizational changes. For instance, the family firm owners decided to try out different organizational setups (including transferring assets from one portfolio firm to another), hoping for beneficial synergies. FF5’s project manager recalled,

We started one restructuring strategy after the other, but it just didn’t get better. So, we wasted a lot of management capacity. We threw a lot of good money after bad. We [family firms] do that, I think non-family firms would never do that. They would just realize after one year, it is not working out, let’s end it as soon as possible. But we [family firms] can keep it for five, six, seven years [. . .] we restructured once, we took it out of holding and made it part of another firm so that it gets the management attention from them. Then we [the management in the headquarters] also flew up there every month and worked with them. (Interview, project manager, FF5)

Similarly, FF6 also engaged in extensive resource-reshuffling activities, relocating one of its poorly performing portfolio firms’ assets from one country to another, as the head of M&A stated:

So, and ever since that guy [portfolio firm manager] left, it [the portfolio firm] was really just sort of dragged along, but it never really grew up, not at all, it shrank. Then, two years ago, we relocated from Singapore to China, but no employees or anything, just machines and products. (Interview, head of M&A, FF6)

Furthermore, the expert interviews with family CEOs, who had restructured many poorly performing firms within their own portfolios, confirmed the observed patterns. Specifically, one family CEO explained that he engaged in resource-reshuffling efforts through relocation from one plant to another, to turn around one of his poorly performing portfolio firms:

And then we realized after two years of investing that it is not possible to make it profitable, and then we relocated the machines and said, “We have the machines in this location because we said having an additional location is not viable.” And then we used this space, and now we have used machines there and continued it like that pretty well, as [a] service location. (Interview, expert)

These observations reveal that family firm owners are truly committed to their non-core portfolio firms, even in sustained periods of poor performance. Thus, they engage in escalating behaviors (e.g., Sleesman et al., 2012, 2018; Staw, 1976, 1981) to preserve (conserve and recover) the SEW they associate with these specific portfolio firms, that is, firm-level SEW. In particular, our data showed that family firm owners escalate such commitment by first engaging in financial (e.g., new machines/buildings) and nonfinancial and cognitive (e.g., management attention, training) investments. If unsuccessful, extensive asset-reshuffling activities follow (e.g., divestment of machines or relocations), instead of divesting the respective portfolio firms. These findings lead us to propose:

Phase 2—De-Escalation: Portfolio-Level SEW Focus Leading to De-Escalating Behaviors

While the family firms’ restructuring through their escalating behaviors, in the form of investments (conserving) and asset-reshuffling activities (recovering), were successful in improving the performance of eight portfolio firms, 14 could not return to profitability and were ultimately divested. We recognized that family firm owners predominantly made the decision to divest poorly performing portfolio firms when the associated losses and investments started to threaten the long-term survival of their overall family firm portfolio and the SEW associated with it, that is, portfolio-level SEW. An analysis of our sampled firms showed that their first preferred divesting option was to sell the poorly performing portfolio firms; only when the sale was no longer an option did they liquidate the firms. For instance, the co-CEO of FF3 explained the decision to sell a portfolio firm that had amassed sizable losses each year since its acquisition, primarily because she and her brother realized that their remaining family firm portfolio would benefit considerably from divesting this poorly performing portfolio firm:

It is healthier for the rest of the group to downsize, to divest it [poorly performing portfolio firm], to have one less problem area, to focus on other markets, which have real potential. And that’s why we said: “Let’s sell this.” (Interview, family co-CEO, FF3)

However, she went on to note that the decision to divest this portfolio firm was not easy for her, due to the nondominant, yet still existing emotional firm-level considerations:

The sale [of the poorly performing portfolio firm] was really difficult for me because it was just an essential decision for the rest of the firm. (Interview, family co-CEO, FF3)

Similarly, the FF4 family CEO decided to liquidate one portfolio firm, loss-making since its acquisition 30 years earlier. He explained that his long-term perspective—retaining control of the overall family firm portfolio and preserving it as a legacy for the next generation (both important dimensions of SEW)—drove his decision to ultimately divest this portfolio firm after decades of keeping and restructuring. In particular, he had plans to pursue a large-scale investment in another line of business within his portfolio. He explained that the risky undertaking required a healthy family firm portfolio to prevent threatening the overall control. In light of these considerations, he liquidated the loss-making portfolio firm:

It was very, very important, we already had the plan to build a new, big machine. And such a big project with a very large investment sum, which also demands the full attention of a firm, you should only start it when you don’t have unsolved problems in your firm portfolio. And this is a very, very central point. I need to make a large-scale investment from a position of strength to stay in control. And these were the thoughts for the divestment of the firm. (Interview, family CEO, FF4)

He also stated another reason for divesting this poorly performing portfolio firm, namely, the imminent handover to the next generation. Driven by his goal of handing over a strong family firm portfolio that is viable in the long term, he felt affirmed in his decision to divest this poorly performing portfolio firm:

And the upcoming succession process also played a role [in the divestment decision], I don’t want to conceal that. When you have a [portfolio] at this size, then you have problem areas here and there, and the next generation cannot expect that you can successfully hand over 100% of the firm. The old generation should see that the big chunks, those that are structurally problematic, are resolved. This was also a reason for the divestment. (Interview, family CEO, FF4)

By contrast, the same family CEO (FF4) kept another poorly performing portfolio firm, which did not considerably negatively affect the overall family firm portfolio and, thus, did not threaten portfolio-level SEW. Instead, he engaged in continued escalating behaviors through such investments as described above. He noted,

This firm has been loss-making for many years. Now we have a new CEO, and the earnings situation has improved. At the moment, we are at breakeven, which is already a big success. It seems to have been a management problem here as well. The new CEO performs well, and I have hope that he, at least, leads them out of the loss-making state. I am not expecting high profits in this firm, but breakeven would be a great success. Because of the small size of this firm, the loss-making state is not so important for the family firm portfolio. (Interview, family CEO, FF4)

Additional evidence for our finding—namely, that family firm owners divest poorly performing portfolio firms only when they must, to preserve their portfolio-level SEW—appears in the case of FF1. Specifically, its COO and successor stated that he initiated the sale of one poorly performing portfolio firm that had previously received considerable financial resources (noted in Phase 1) to safeguard the survival and reputation of the overall family firm portfolio:

There was an injection of financial resources, which then allowed the firm to survive for around eight months with the hope that we get the business model and the product up and running, to then continue the firm. But when it was time to invest more financial resources into this organization, I sat down with my father, and I said: “I am against throwing good money after bad, but we rather have to look us in the eyes and say, this concept that we thought about just doesn’t work and is hurting the financial situation and reputation of the entire [portfolio] organization and of us.” (Interview, COO/successor, FF1)

Archival data from the sales deal announcement (2017) shows further evidence that FF1 chose its divestment approach to “focus on its core capabilities.”

Finally, we observed that family firm owners’ SEW preservation concerns also affected their preference for how to divest the portfolio firms that threatened their portfolio-level SEW. Specifically, we found that family firm owners preferred to sell portfolio firms as an ongoing concern (i.e., sale) over shutting them down and selling all their individual assets (i.e., liquidation). A sale typically generated greater financial proceeds that the firm could subsequently reinvest in its remaining family firm portfolio, thereby strengthening portfolio-level SEW. For instance, FF5 divested a portfolio firm that had been a cash drain for 6 years by selling the firm to a competitor, to strengthen the remaining family firm portfolio and, thereby, portfolio-level SEW. FF5’s project manager recalled,

And we really shied away from selling it for a long time but in the end, we didn’t see any other way. We were also really fed up, and then the family said: “Ok, we sell it” [portfolio firm] as a beneficial [financially rewarding] move for the remaining firm and for sleeping better at night. (Interview, project manager, FF5)

Similarly, FF3 sold one of its portfolio firms as an ongoing concern because the portfolio firm’s poor performance threatened the portfolio-level SEW. The co-CEO of FF3 further noted that the liquidity generated through the sales of this portfolio firm funded the growth of another portfolio firm in his portfolio, in turn, strengthening the portfolio-level SEW. He stated,

We had the possibility to grow in this region, which also made sense. And then we said: “Ok, let’s do it and sell this firm and shrink a little here to be on solid grounds and rather grow our presence somewhere else [i.e., other portfolio firms].” (Interview, family co-CEO, FF3)

However, of the 14 portfolio firms divested in our cases, only seven could be sold as ongoing concerns. The remaining seven required liquidation; a sale was no longer feasible, due to the portfolio firms’ sustained poor performance by the time the family firm owners finally decided to divest. Two of the seven portfolio firms liquidated in our cases were part of FF2’s family firm portfolio. FF2’s family CEO remarked that as the financial threat stemming from one portfolio firm grew over time, he felt obliged to liquidate it for the survival of the entire portfolio, to at least protect the remaining firms. He said,

We waited so long with the liquidation [of the portfolio firm] until we were really in deep trouble [. . .] and we really worried about it a lot, which was unnecessary. But oh well, it [the entire portfolio] is just a part of us [. . .] and we had to save it. And if you can’t sell [you need to liquidate]. Well, liquidating is always the worst idea. (Interview, family CEO, FF2)

Furthermore, an article about the firm from a regional newspaper published in 2016 emphasized that despite the necessary liquidations, the family CEO felt committed to the employees of the liquidated firms and offered them new jobs in other portfolio firms.

Another illustrative example of liquidation as the last resort is that of FF4, in which the family CEO ultimately liquidated the portfolio firm that had been loss-making for 10 years, when he failed to sell the portfolio firm as an ongoing concern, due to its poor performance and bad market reputation. His realization that this portfolio firm jeopardized the portfolio’s overall financial strength triggered his ultimate decision to liquidate it. He claimed,

[The portfolio firm] played an important role in the integrated packaging production. And I always thought that we need the volume, this integrated volume for the remaining firms. But, as our market position continuously grew, I was of the opinion that the firm is no longer absolutely necessary for the rest of the group. And the firm was hurting our portfolio’s profitability [. . .] These were my considerations for the divestment [. . .] we looked to sell [the portfolio firm] a couple of times. But a firm that is loss-making is difficult to sell. Then you also don’t get any sale proceeds. Furthermore, the firm had a bad reputation. (Interview, family CEO, FF4)

In addition to this statement, a newspaper article confirmed that liquidating the portfolio firm was a difficult decision for FF4’s family CEO:

For the family CEO, the restructuring of the firm failed [. . .] “The liquidation of this firm with approx. 100 employees was unfortunate and a tough decision [. . .],” said the family CEO. (Newspaper article, FF4)

In summary, we can conclude that family firm owners de-escalate their commitment to poorly performing portfolio firms and divest them when keeping them threatens the long-term survival of their overall family firm portfolio and, thus, their portfolio-level SEW. Thus, we observe a shift in family firm owners’ criteria for strategic restructuring decisions. While these owners generally focus on preserving the SEW that they associate with each firm (i.e., firm-level SEW; see Phase 1), their criterion for restructuring decisions shifts toward preserving the SEW that they associate with the entire family firm portfolio (i.e., portfolio-level SEW; see Phase 2) when the poor performance of one firm puts the entire portfolio at a disadvantage. Thus, our findings suggest that family firm owners are willing to tolerate the loss of firm-level SEW stemming from the divestment of a poorly performing portfolio firm, to preserve their remaining portfolio-level SEW. In other words, portfolio-level SEW preservation takes precedence over firm-level SEW preservation when a poorly performing portfolio firm threatens the family firm portfolio. Furthermore, we found that when divesting, family firm owners generally prefer to sell rather than liquidate portfolio firms that threaten their portfolio-level SEW, predominantly because a sale typically results in greater proceeds. The family firm can reinvest the financial resources the sale generates in the remaining family firm portfolio, allowing family firm owners to enhance their remaining firm portfolio under the family umbrella and strengthen portfolio-level SEW. However, continued poor performance and long waiting times frequently force family firm owners to ultimately liquidate their poorly performing portfolio firms when a sale is no longer an option. In formal terms, we propose:

Discussion

Our study investigates restructuring poorly performing firms in family firm portfolios. The iterative process between data analysis and literature revisitation resulted in our inductive model (see Figure 2), exhibiting the restructuring behavior regarding poorly performing portfolio firms within family firm portfolios. Based on patterns we observed across 22 poorly performing firms in six private family firm portfolios, we propose that family firm owners derive SEW not only from their core legacy business but also from previously built or acquired portfolio firms. We find that when these non-core portfolio firms perform poorly, family firm owners initially refrain from restructuring or divesting (Phase 0: retention), due to SEW concerns. Interestingly, at this point in the process, family firm owners do not distinguish firm-level from portfolio-level SEW. When the performance issues continue, family firm owners attempt to safeguard the SEW they associate with these portfolio firms, that is, firm-level SEW, by escalating their commitment to these firms through investments and, if necessary, through asset-reshuffling activities (Phase 1: escalation). In some of our cases, such escalated commitment solved the performance issues; in others, the poor performance continued. Upon realizing that the ongoing poor performance of a portfolio firm posed a threat, not only to the firm-related SEW but also to portfolio-level SEW, family firm owners de-escalate their commitment and divest (Phase 2: de-escalation). We provide evidence that family firm owners in the specific context that we studied prefer to divest by selling poorly performing portfolio firms as an ongoing concern, rather than liquidating them. Thus, they can reinvest the sale proceeds in their remaining portfolio, strengthening their remaining portfolio and, thus, their portfolio-level SEW. Next, we discuss the theoretical and practical implications of our findings, following them with the limitations of our study and further research avenues.

Theoretical Model.

Theoretical Implications

Our study advances our current understanding of the SEW perspective (e.g., Berrone et al., 2012; Gómez-Mejía et al., 2007, 2011) by providing insights into where SEW “resides” in the family firm portfolio context (e.g., Sieger et al., 2011; Zellweger et al., 2012). Specifically, we extend SEW to family firm portfolios by distinguishing between two SEW levels: firm-level and portfolio-level. One implication of our study is that future research must be attentive to SEW that family firm owners derive from their non-core portfolio firms. This is an important insight, as family firm portfolios are family firms’ most prevalent structure (Zellweger et al., 2012). Prior research has focused on SEW relating to core family firms (DeTienne & Chirico, 2013). Conceptual research by DeTienne and Chirico (2013) suggested financial reward or cessation-based exit for non-core firms; our study highlights SEW concerns also playing an important role in those scenarios. Specifically, the work of DeTienne and Chirico (2013) builds on the notion that in a family firm portfolio, the family firm owners’ SEW will likely be at a higher level in the core firm than in subsequently added firms. Hence, they argue, family firm owners will likely persist with an underperforming core firm and pursue an exit involving non-core firms on the basis of financial reward or cessation, to sustain and ensure the core firm’s family succession and, thus, its longevity. Our empirical study focused on poorly performing non-core firms (i.e., firms added after the foundation of the core business). DeTienne and Chirico (2013) indicate that SEW considerations might have less effect on restructuring these non-core firms, but our case analysis shows the opposite. We found that family firm owners initially show refraining behaviors toward restructuring their poorly performing portfolio firms, due to SEW concerns related to the non-core firm. The owners pursue first escalating and then de-escalating behaviors (i.e., exit strategies) to sustain the family firm portfolio and ensure the core firm’s family succession and longevity. Our cases further extend this research stream by showing that de-escalating behaviors follow an order of preference, first attempting divesting via a sale and, when a sale is not an option, via liquidation.

Another implication of the SEW literature refers to the coupling and decoupling of SEW. Interestingly, in the very early stages of the restructuring process (Phase 0: retention), we could not detect any distinction between firm-level and portfolio-level SEW. Instead, family firm owner-managers referred to emotional attachment, refusal to admit failure due to reputation concerns, commitment, identification, and control intentions in general, without referring to specific levels. When the threat to SEW became evident, SEW decoupling occurred. Based on our interviews, we suggest that the criteria for strategic restructuring decisions in family firm portfolios comprise both firm-level and portfolio-level SEW. While firm-level SEW preservation concerns dominate restructuring decisions in family firm portfolios in general (Phase 1: escalation), portfolio-level SEW preservation concerns take precedence when they are at risk (Phase 2: de-escalation). Hence, we propose a “cascading” effect. In other words, family firm owners shift their criterion for restructuring decisions (Nason et al., 2019; Zellweger & Dehlen, 2012) from firm-level (investing and reshuffling) to portfolio-level (selling and liquidating) SEW when the entire family firm portfolio is at risk. In these cases, when portfolio-level SEW is threatened, family firm owners become willing to give up their firm-level SEW to safeguard their remaining portfolio-level SEW. With these findings, we also respond to recent research calls to further develop SEW (Brigham & Payne, 2019; Kammerlander, 2022; Swab et al., 2020), as we specify the relevant levels of SEW analysis for family firm portfolios (e.g., Sieger et al., 2011; Zellweger et al., 2012). Our research particularly indicates that in family firm portfolios, SEW captures not only the “stock [. . .] a family derives from its controlling position in a particular [core] firm” (Berrone et al., 2012, p. 259) but also the stock derived from the individual (core and non-core) portfolio firm, that is, firm-level SEW accumulating to portfolio-level SEW. Hence, both the portfolio firm and the entire family firm portfolio are essential levels of analysis for SEW in family firm portfolios. Thus, our findings highlighting the importance of distinguishing between firm- and portfolio-level SEW—especially during “bad times”—have important implications for future SEW studies.

Second, we contribute to the literature stream on restructuring in family firms (for a review, see King et al., 2022) and, relatedly, advance the literature on escalation of commitment in family firms (Chirico et al., 2018; Salvato et al., 2010a, 2010b; Woods et al., 2012). We propose that next to the general already-identified antecedents of escalating behaviors, such as ego threat or the desire to “save face” (e.g., Boulding et al., 1997; Sleesman et al., 2018; Zhang & Baumeister, 2006), family firm owners’ SEW preservation considerations on the firm and portfolio levels also constitute a strong antecedent for escalating (firm-level SEW) and de-escalating (portfolio-level SEW) behaviors toward family firm portfolios. Specifically, we find that based on their firm-level SEW, family firm owners escalate their commitment to poorly performing portfolio firms (Chirico et al., 2018; Salvato et al., 2010a), by first investing and then reshuffling their assets. Subsequently, if those tactics fail, they de-escalate their commitment to these portfolio firms, attempting first to sell and resorting to liquidation when they realize that further investing in restructuring threatens their portfolio-level SEW. Thus, we conclude that SEW preservation concerns in family firm portfolios represent a double-edged sword. They can lead to both escalation and de-escalation of commitment to a poorly performing portfolio firm, depending on whether firm-level or portfolio-level SEW considerations prevail. These findings have important implications for research on escalation of commitment in family firms, which thus far has mostly focused on escalation in the restructuring context (e.g., Sharma & Manikutty, 2005), thereby neglecting the important de-escalation strategy.

In addition, our study extends the effort of Chirico et al. (2018) to theorize how emotional ownership in family firms drives the escalation of commitment through two mediation paths: a feeling of responsibility and the investment of capital. Our findings support their study by emphasizing the role of emotional considerations in commitment escalation. Whereas Chirico and colleagues (2018) focus on explaining heterogeneity in family firms’ escalation of commitment by analyzing its drivers, our focus is on studying how escalation of commitment varies throughout the restructuring process. In other words, we complement the interfamily firm perspective of Chirico et al. (2018) with an intrafamily firm perspective. Specifically, our cases show that a phase of de-escalation follows a phase of escalation, both triggered by SEW concerns and characterizing different restructuring behaviors.

Furthermore, our study provides novel insights into the sequence of different restructuring behaviors that family firm owners employ to deal with their poorly performing portfolio firms. We categorized the identified restructuring activities into three phases. Initially, in Phase 0 (retention), family firm owners refrain from restructuring and hold on to their poorly performing portfolio firms. In Phase 1 (escalation), these owners show escalating behaviors by expending substantial financial resources to restructure poorly performing portfolio firms, by investing (e.g., plant and retail investments, management investments) and subsequently reshuffling their assets (e.g., machinery, employees). However, when performance issues persist, the owners enter a de-escalation (Phase 2). Here, de-escalating behaviors include restructuring their family firm portfolio through divesting to preserve their portfolio-level SEW. The owners first attempt to sell their poorly performing portfolio firms and, when selling is no longer an option, they liquidate. These findings extend prior research on family firm owners’ general divestment reluctance (e.g., Chirico et al., 2020; Kim et al., 2019). On one hand, we shed light on the specific restructuring behavior in which family firm owners engage—often for decades—to avoid divesting poor performers. On the other hand, we also illustrate family firm owners deviating from their general divestment reluctance. As a result, our study contributes to opening the black box about how family firm owners restructure poorly performing firms in the context of portfolio entrepreneurship (Discua Cruz et al., 2013; Sieger et al., 2011).

Third, our study findings extend prior divestment research on family firms (Akhter et al., 2016; Chirico et al., 2018, 2020). Joining this discourse, we show that the preferred order for divesting poorly performing firms in family firm portfolios is sale as an ongoing concern, followed by liquidation. Specifically, our data suggest that family firm owners prefer to sell rather than liquidate individual portfolio firms, to reinvest the sale proceeds in the remaining family firm portfolio, thereby ensuring portfolio survival (Chirico et al., 2011; Gómez-Mejía et al., 2007) and strengthening portfolio-level SEW. These findings stand in apparent contrast to the study by Chirico et al. (2020), who examine the divestment of entire family firms. The authors posit that family firm owners prefer mergers over liquidation and liquidation over sale. The basis of their order of preference is family firm owners’ portfolio-level SEW preservation considerations. Selling involves the total loss of SEW, so liquidating avoids “the tough emotional choice to sell” (Chirico et al., 2020, p. 1352), and merging protects some portfolio-level SEW. Similarly, our study posits that when considering the divestment of an individual portfolio firm, family firm owners’ preference for selling instead of liquidating reflects their desire to preserve portfolio-level SEW. In other words, family firm owners’ ultimate goal is preserving portfolio-level SEW. Our findings do not contradict but, rather, extend the Chirico et al. (2020) study, reconsidering divestment in the context of family firm portfolios and not assuming that the entire portfolio is up for divestment.

We acknowledge that our findings diverge from those by Akhter et al. (2016), who, in their case study of six Pakistani family firms, found that family firm owners would rather shut down portfolio firms than sell them; their informants claim that “if we can’t have it, then no one should” (Akhter et al., 2016, p. 371). We attribute these divergent findings mainly to two factors. On one hand, Akhter et al. (2016) showed that family firm owners’ goal of re-entering the business at a later point also affected the decision to shut down or sell a satellite business. Their cases revealed that the intention to restart a satellite business at some point in the future was an important contingency factor in the decision to shut down or sell in times of declining performance. In this sense, assuming that family firm owners did not want to sell their portfolio businesses seems reasonable; otherwise, they would withdraw the possibility of restarting them in the future. Conversely, in our cases, the asset-heavy nature of the businesses curtailed the possibility of restarting the business at a later stage. Therefore, we argue that in our industry context, selling the business can offer family firm owners a more favorable option than shutting down. On the other hand, the differences might be due to the cultural, institutional, and economic contexts of the studies (i.e., Austria, Germany, and Switzerland vs. Pakistan). Akhter et al. (2016) focused on Pakistan, a very entrepreneurial country that a very hostile environment characterizes, with uncertainty and rapid changes: “[A] recent study ranked Pakistan fourth in the world in entrepreneurship in terms of efficiency and innovation” (Akhter et al., 2016, p. 376). We suggest that due to the high volatility inherent in frontier markets, for example, Pakistan, shutting down might be preferable to selling, due to the fast-changing environment and the widespread ability of wealthy families to change licenses and contracts to their advantage, a result of the weak legal system (Fisman, 2001; Gedajlovic et al., 2012). Based on this fast-paced environment, we assume that family-owned portfolio firms with poor performance today might become profitable again in the near future, allowing those families that can restart their portfolio firms to gain where those who sold their portfolio firms lose, also in terms of SEW. Conversely, in developed countries, such as Germany, it takes much longer for a business to gain legitimacy, especially in the traditional industries our study investigated. As a consequence, the family firm owners in our study might have felt less likelihood of successfully restarting their business and gaining legitimacy and reputation than the Pakistani family firms in the Akhter et al. study. The matter requires further research, but we expect our results apply mostly to family firm portfolios in developed countries.

Practical Implications

Finally, our study offers important implications for practice. Family firm decision-makers can benefit from our research showing how portfolio restructuring can ensure family firm portfolio survival and, thereby, SEW preservation. In particular, the rather large number of observed forced liquidations in our findings implies encouraging family firm owners to sell poorly performing portfolio firms timely, in a bid to free up financial resources for reinvestment in the survival of the remaining firm(s) and avoid their eventual liquidation. Indeed, even though divesting individual firms is a tough emotional decision for family firm owners, our research suggests that sometimes they must let go of individual firms to avoid threatening their entire legacy. As such, divestment of portfolio firms can foster long-term firm survivability rather than “failure” (Zellweger et al., 2012, p. 141). Moreover, our research might inform family firm advisors that their consulting discussions should include addressing family members’ socioemotional concerns that might hamper restructuring and divestment.

Limitations and Avenues of Further Research

Our study entails some limitations that provide fruitful avenues for further research. First, as with any qualitative research, we acknowledge that our propositions represent analytical rather than statistical generalizations (Yin, 1994). However, the nine interviews with experts and our member checks confirmed the relevance of our theoretical model. Nevertheless, to increase the generalizability of our findings, we encourage scholars to examine our findings across a wider spectrum of family firms. While our study analyzes a heterogeneous sample of private family firm portfolios, for example, variations in firm portfolio size, generational stage, and family CEO presence, (quantitative) studies could research the effect of further firm-portfolio characteristics (e.g., number of portfolio firms, size of individual portfolio firm relative to overall portfolio, difference between “asset-light” and “asset heavy” industries; eponymy) on restructuring behavior toward family firm portfolios.

Second, the cultural, institutional, and economic settings in the countries in which our cases were located (i.e., German-speaking part of Europe) might have influenced our findings. We encourage future research to assess how the replication of our study across diverse cultures and institutional contexts affects the findings. For instance, while our findings might be most relevant in mature and advanced jurisdictions, as we suggest, family firm owners from emerging or frontier markets, such as Pakistan (the focus of Akhter et al., 2016), might deviate from our proposed theoretical model due to their volatile environment.

Third, our study has initiated a novel discussion of the different levels of SEW within family firm portfolios, by differentiating firm-level and portfolio-level SEW. We hope that our study inspires family firm scholars to increasingly move away from the one family-one firm concept and toward considering the complex multi-firm construct that usually characterizes family firms (Discua Cruz et al., 2013; Sieger et al., 2011). Specifically, we call for future empirical research on how different levels of SEW influence the pursuit of various other strategies (e.g., innovation and internationalization) within family firm portfolios. In addition, while our study has advanced our understanding of SEW within family firm portfolios, further research on SEW, its levels of analysis, and its dimensions is paramount, to provide even greater conceptual clarity on SEW (Brigham & Payne, 2019; Swab et al., 2020). Furthermore, future research could study how each of the dimensions of SEW (FIBER) suggested by Berrone et al. (2012) relates to the different phases we identified. For instance, one could expect that (E)—emotional attachment of family members—might be associated with refraining decisions (Phase 0: retention) or that (F)—family control and influence—might link to the control family firm owners exercise when escalating their commitment (Phase 1: escalation).

Fourth, although our study’s methodology substantially emphasized avoiding informant biases and retrospective sense-making through our interview style, multiple data sources, and triangulation, the retrospective nature of our data does not completely rule out biases (Gavetti & Rivkin, 2007; Miles & Huberman, 1994). To further mitigate such concerns, future research could study restructuring family firm portfolios in real time. As the long-time span (up to decades, according to our data) from initial poor performance to divestment might prevent interview-based studies, researchers might think of alternative data collection methods, for example, through analysis of firm-specific archival documents. Such an approach might also enable even more systematic study of path dependence and restructuring decision-making processes within family firm portfolios.

Finally, our data collection process followed our research focus by investigating the restructuring that our six cases implemented with poorly performing portfolio firms. However, we acknowledge that family firm owners might also restructure their firm portfolio for other, non-performance-related reasons, such as to reposition their portfolio or to exploit growth opportunities (Brauer, 2006; Decker & Mellewigt, 2007). Thus, future studies could investigate whether the restructuring motive affects the restructuring behavior in family firm portfolios. Moreover, future research might include cases with struggling core (as opposed to non-core) portfolio firms and investigate the SEW-(de-)coupling in those cases.

Conclusion

Our multi-case study on 22 poorly performing firms belonging to six private family firm portfolios investigated how family firm owners restructure poorly performing firms within their portfolio. Our findings reveal that such owners first attempt to make no distinction between firm-level and portfolio-level SEW, then preserve their firm-level SEW through escalating behaviors, and later preserve their portfolio-level SEW through de-escalating behaviors. Thus, family firm owners engage in diverse restructuring behaviors in the following order of preference: refraining (Phase 0: retention), investing and reshuffling (Phase 1: escalation), selling, and, finally, liquidating (Phase 2: de-escalation). Our study has important implications for the literature on SEW and restructuring, especially regarding divestments in family firms.

Supplemental Material

sj-docx-1-fbr-10.1177_08944865231210901 – Supplemental material for Restructuring of Poorly Performing Family-Owned Portfolio Firms: The Role of Socioemotional Wealth

Supplemental material, sj-docx-1-fbr-10.1177_08944865231210901 for Restructuring of Poorly Performing Family-Owned Portfolio Firms: The Role of Socioemotional Wealth by Marina D. Palm, Vanessa Diaz-Moriana and Nadine Kammerlander in Family Business Review

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.