Abstract

The transgenerational entrepreneurship perspective suggests senior-generation leaders with transgenerational control intentions (TCI) innovate to position the next generation for success, but many family firms fail to do so. We introduce transgenerational control uncertainty (TCU) as a theoretical mechanism explaining when TCI enhances innovation behaviors pre-succession. A multi-respondent, multi-time period survey of private German family firms shows that while TCI helps unleash innovation prior to succession, these effects also depend on lowering TCU as reflected in progress through the succession process. Our study suggests TCU might be a useful new construct for explaining other important differences among family firms.

Introduction

The succession literature has long focused on the necessary steps before the senior generation successfully passes the baton to the next. Involving children in the firm from a young age exposes them to their entrepreneurial legacy (Jaskiewicz et al., 2015), helps them generate knowledge about the firm and its people (Decker et al., 2016), increases their identification with the firm, and motivates their pursuit of relevant education (e.g., De Massis et al., 2008) and work experiences before returning to the firm in adulthood (Le Breton-Miller et al., 2004; McMullen & Warnick, 2015). Effective continuation of the succession process later includes a period of multigenerational leadership, wherein the senior generation works side by side with adult members of the next generation preparing them for eventual takeover (Le Breton-Miller et al., 2004). Along with other important antecedents, such as getting the right education (e.g., De Massis et al., 2008) and building the right succession team (Cater et al., 2016), involvement in the firm during childhood and again in adulthood are central to ensuring that the next generation is prepared and motivated for succession.

It seems unlikely, however, that these steps only impact the next generation and their post-succession decisions. An emerging body of research called the “transgenerational entrepreneurship perspective” (Zellweger et al., 2012a, p. 141) suggests that when the senior generation possesses transgenerational control intentions (TCI)—that is, they intend the next generation to take ownership control and participate in leadership—they are more likely to embrace a long-term orientation (Le Breton-Miller & Miller, 2006; Lumpkin & Brigham, 2011) that motivates them to prepare the firm for continued success prior to passing it to the next generation (Diaz-Moriana et al., 2020; Hoffmann et al., 2019; Strike et al., 2015). Among the most important actions the senior generation can take to prepare the firm is to engage in innovation behaviors (e.g., Alegre & Chiva, 2013; Baregheh et al., 2009). Innovation behaviors are observable actions managers take with regard to innovation, such as revitalizing product lines, introducing new products, or developing new markets. 1 Pursuing such behaviors prior to succession helps the senior generation hand over a healthy firm that can thrive for another generation. Most research, however, has focused on family business innovation in general (Duran et al., 2016) and post-succession (e.g., Zybura et al., 2021), leaving it unclear how the senior generation might (or might not) contribute prior to succession.

Although the transgenerational entrepreneurship perspective anticipates that TCI motivates innovation (e.g., Diaz-Moriana et al., 2020; Strike et al., 2015), family firms often lag their nonfamily peers (Block, 2012; Chen & Hsu, 2009), and many transfer control without experiencing innovation prior to succession (Erdogan et al., 2020; Suddaby & Jaskiewicz, 2020), so TCI alone appears insufficient to inspire many senior leaders to pursue innovation. We therefore ask: When does the senior generation’s TCI lead to more innovation behaviors prior to succession? To help fill this gap in knowledge about when TCI affects innovation, we introduce transgenerational control uncertainty (TCU) as a theoretical mechanism that helps explain when senior leaders’ TCI motivates innovation behaviors.

We define TCU as the senior generation’s perceived difficulty foreseeing whether a next-generation family member will be willing and able to continue the business for another generation. Uncertainty leads entrepreneurs (Shane & Venkataraman, 2000; Stevenson & Jarillo, 1990) and managers (Bernanke, 1983; Bloom et al., 2007; Fuss & Vermeulen, 2006) to reduce or postpone innovation. While the transgenerational entrepreneurship perspective anticipates that senior leaders’ TCI boosts their motivation to pass along a healthy family firm (Strike et al., 2015), we offer TCU as a family-specific source of perceived uncertainty that suppresses senior leaders’ motivation to pursue and support innovation behaviors prior to succession. By progressing through critical steps of the succession process (e.g., Decker et al., 2016; Le Breton-Miller et al., 2004), however, senior leaders should perceive less TCU, allowing their TCI (if they have it) to deliver its full motivational impact. Because childhood involvement and multigenerational leadership are established steps in successful succession processes (Le Breton-Miller et al., 2004), we focus on them as reflections of family leaders’ lower perceived TCU. Childhood involvement motivates the next generation to identify with and join the family firm (Garcia et al., 2019; Jaskiewicz et al., 2015; McMullen & Warnick, 2015), reducing senior leaders’ perceived uncertainty about the next generation’s commitment. TCU is virtually eliminated when the next generation joins the multigenerational leadership team, enabling those senior leaders with TCI to pursue innovation behaviors and support the next generation’s innovation efforts. Empirical analysis based on responses from a multi-time, multi-respondent survey involving 212 family members in 106 German family firms supports this theorizing. When administering the surveys, we also received unsolicited comments and use them to illustrate our theorizing. 2

Our study contributes to the succession literature by offering TCU as a theoretical mechanism that explains when TCI motivates innovation behaviors, thereby connecting the succession literature with the transgenerational entrepreneurship perspective. Prior research focused on how succession processes shape successors and their decisions post-succession (e.g., Zybura et al., 2021); our study shows these steps also affect the senior generation pre-succession. Moving through the steps of succession process reflects increased confidence (i.e., reduced TCU) that a family successor is willing and able to take over for another generation, which is necessary to unleash the motivational power of the senior generation’s TCI (if they have it). Consistent with our theorizing, the impact of senior leaders’ TCI on innovation behaviors is stronger when next-generation members were involved in the business as children. Among those in the multigenerational leadership, only those with strong senior-generation TCI fully unleash entrepreneurial capacity through innovation behaviors.

Our study also contributes to the family-firm innovation literature through our empirical test of the TCI-innovation relationship. While the transgenerational entrepreneurship perspective anticipates that longer decision-making horizons drive the TCI-innovation relationship (Diaz-Moriana et al., 2020; Le Breton-Miller & Miller, 2006; Strike et al., 2015), an alternative explanation is that TCI improves cross-generational tacit knowledge transfer (Filser et al., 2018). By controlling for socialization processes where such knowledge transfer takes place and finding no supportive evidence, our empirical evidence provides initial support of the transgenerational entrepreneurship perspective. Such evidence is important because it has implications regarding which actions are most appropriate for motivating innovation—that is, transferring knowledge or helping the next generation develop new knowledge.

Finally, our research contributes to socioemotional wealth (SEW) research by helping reconcile competing predictions from the transgenerational control and SEW perspectives. SEW is a multidimensional umbrella term for the family’s affective value gained from maintaining family control (Gómez-Mejía et al., 2007). A core prediction is that family owners take strategically conservative actions to protect their SEW, which implies less innovation (Block et al., 2013). The transgenerational entrepreneurship perspective isolates the TCI dimension of SEW 3 to make the opposite prediction—that senior-generation leaders will take action to prepare the firm for the next generation (Zellweger et al., 2012a). We reconcile these opposing views by showing that the senior generation supports innovation behaviors in line with the transgenerational control perspective, but only when their TCI is high and TCU is low. Otherwise, innovation behaviors wane as the SEW perspective predicts.

Succession and Innovation

The succession process might be the most researched topic in the field of family business. Le Breton-Miller et al.’s (2004) seminal review proposes four succession stages that are widely accepted (e.g., Decker et al., 2016). First Steps involves developing a shared vision to guide succession planning. In the Nurturing of Successors stage, which often takes decades, gaps are identified between the needs of the family business and prospective successors’ abilities. Efforts begin to expose children to the family business and transfer knowlegde prior to more formal leadership development and mentoring. The Selection stage is when a successor is formally chosen and a process is set out for eventual leadership and ownership succession. Finally, in the Transition stage, shares are transferred, the successor is phased in, and the incumbent is phased out, often after a long period of working side by side as a multigenerational leadership team.

Throughout these stages, which do not have to proceed linearly, can overlap, and can take decades (for a more recent review, see Decker et al., 2016), the next generation’s exposure to and work within the family firm is critical. Potential successors’ exposure to the family firm starts with part-time or summer jobs (Cabrera-Suárez et al., 2001; Houshmand et al., 2017; Le Breton-Miller et al., 2004) and is strengthened when children are in and around the business interacting with other involved family members and sharing family narratives (Jaskiewicz et al., 2015; Kammerlander et al., 2015). While not all childhood experiences in family firms are positive (Shanine et al., 2022), childhood involvement in family firms, on average, enables potential successors to familiarize themselves with the business, its culture, values, and employees (Le Breton-Miller et al., 2004); initiates relationships with key stakeholders (e.g., suppliers, customers); and fosters successors’ credibility (De Massis et al., 2008; Lansberg & Astrachan, 1994). It thereby increases the next generations’ identification with and commitment to the business (Garcia et al., 2019; Jaskiewicz et al., 2015; Le Breton-Miller et al., 2004; McMullen & Warnick, 2015), fueling entrepreneurship (Schmitt-Rodermund, 2004; Zellweger et al., 2011), enabling successful careers (Houshmand et al., 2017), and enhancing the prospect of intra-family succession (Handler, 1992; Le Breton-Miller et al., 2004).

Leaving the family and the firm to gain relevant educational and work experiences is critical for closing successors’ skill gaps (e.g., Jaskiewicz et al., 2015), but transgenerational succession fails if the next generation does not return and instead pursues careers outside the family firm (Combs et al., 2021). Indeed, multigenerational leadership, where both generations work side by side is a signature feature of privately held family firms, in general, and successful succession processes, in particular (e.g., Arregle et al., 2007; Le Breton-Miller et al., 2004). The next generation adds social capital and brings new knowledge and capabilities into the firm (Chirico et al., 2011; Ling & Kellermanns, 2010), so it is perhaps not surprising that entrepreneurial orientation (EO) is highest among family firms with two generations involved (Sciascia et al., 2013), and more generations yield greater investments in emerging technologies and activities needed to achieve radical product innovation (Zahra, 2005).

There is a great deal of variation, however, regarding whether the firm experiences a period of innovation and growth when the next generation returns in adulthood and infuses the firm with new knowledge, skills, and social capital (Arregle et al., 2007; Chirico et al., 2011). On average, family firms underinvest in innovation compared with nonfamily firms (Block et al., 2022; Duran et al., 2016). The theoretical explanation, based on behavioral agency theory (Wiseman & Gómez-Mejía, 1998), is that family firms develop a stock of affective nonfinancial wealth called SEW (Gómez-Mejía et al., 2007), and loss aversion regarding SEW leads to risk-averse decisions and behavior (Gómez-Mejía et al., 2014). 4

SEW is a multidimensional umbrella construct that, in addition to TCI, includes the desire to maintain current family control, strong identification with the business, enhanced emotional bonds among family members, and meaningful relationships with stakeholders (Berrone et al., 2012). Behavioral agency theory predicts that family firms avoid behaviors, such as acquisitions (Gómez-Mejía et al., 2018) and innovation projects (Chrisman & Patel, 2012; Matzler et al., 2015), that might place the family’s current SEW at risk, thus explaining why many family firms pursue fewer innovation activities, even during the final stages of the succession process when multigenerational leadership takes place. If the senior generation identifies strongly with their own accomplishments or perceives succession as a distant event, the period of multigenerational leadership might focus on transferring knowledge about existing routines rather than freeing the next generation to leverage their knowledge and skills to innovate (Jaskiewicz et al., 2015).

Joining others who have questioned treating SEW’s five dimensions as a unified construct (Davila et al., 2022; Hauck et al., 2016), the emerging transgenerational entrepreneurship perspective suggests a distinct role for TCI relative to other SEW dimensions (e.g., Gu et al., 2019; Strike et al., 2015; Zellweger et al., 2012a). This perspective anticipates that senior leaders with TCI will reverse their normal propensity toward strategic conservatism to prepare the firm for the next generation’s success (Diaz-Moriana et al., 2020; Hoffmann et al., 2019). Family CEOs’ TCI, for example, helps explain why the risk-taking postures of family and nonfamily CEOs reverse as they approach retirement (Strike et al., 2015). While nonfamily CEOs, in an effort to maximize pay (e.g., Antia et al., 2010) and exit on a positive note (e.g., Davidson et al., 2007), adopt short time horizons as retirement approaches, family CEOs prefer actions that rejuvenate the firm for the next generation (Strike et al., 2015). Consistent with this perspective, Strike et al. (2015) found that compared with near-retirement nonfamily CEOs, near-retirement family CEOs pursue more international acquisitions and these effects are stronger where a family member eventually succeeds as CEO. Although Strike et al. (2015) did not measure TCI, their findings are consistent with the idea that TCI motivates near-retirement family CEOs’ riskier behavior—the opposite of what behavioral agency theory predicts.

In sum, the succession process is a long multistage process that depends heavily on next-generation involvement, both in childhood and later as part of a multigenerational leadership team. While successful movement through this process helps the next generation innovate post-succession (Zybura et al., 2021), little is known about how progress toward succession influences the senior generation’s motivation to pursue and support innovation pre-succession. Behavioral agency theory expects senior leaders to cling to their own accomplishments (in line with SEW dimensions involving identification with the family firm and maintaining family-firm control), which suggests innovation will wait until after succession. However, by isolating SEW’s TCI dimension, the transgenerational entrepreneurship perspective predicts the opposite; senior-generation leaders will pursue and support innovation to position the firm for another generation of success. However, whether TCI works in the opposite direction of the other SEW dimensions with respect to innovation remains an unanswered empirical question. More importantly, not all senior-generation leaders want (or intend) to pass the firm to the next generation (Hoffmann et al., 2019), and those who do might be uncertain about the next generation’s willingness and ability to take over. Under such conditions, the long-term strategic actions anticipated by the transgenerational entrepreneurship perspective might give way to the strategic conservatism anticipated by behavioral agency theory. We therefore develop theory to explain when the senior generation is motivated to pursue and support innovation behaviors pre-succession.

TCI and Innovation in Family Firms

Whereas the other SEW dimensions—especially the desire to maintain current control—align with behavioral agency theory’s prediction that family leaders act conservatively to protect their SEW (Block et al., 2013; Gómez-Mejía et al., 2007), the transgenerational entrepreneurship perspective anticipates that TCI encourages family leaders to think beyond simply maintaining control toward how strategic decisions impact the next generation’s potential for success (Hoffmann et al., 2019; Strike et al., 2015). It thereby extends family leaders’ decision-making horizon and inspires a long-term orientation (Le Breton-Miller & Miller, 2006; Lumpkin & Brigham, 2011), inspiring senior leaders’ “desire to leave a mark on the firm” (Diaz-Moriana et al., 2020, p. 18) by leaving the business in good standing for their children. Pursuing innovation behaviors is one way through which senior leaders can increase the attractiveness of the family firm and thus increase the viability of transgenerational control (Parker, 2016). These insights were echoed in unsolicited comments by senior leaders during survey implementation:

We are investing a lot to keep up with technological progress and the latest security standards. We always wanted a business that is in good shape for our son to take over.—Managing director (third generation), services company. There is no plan B for us. We want the family firm to survive and leave it in good condition. I think, that is what we owe our children.—Managing director (third generation), construction company.

However, not all senior-generation family leaders possess high TCI (Hoffmann et al., 2019). Innovation behaviors are risky and some fail, so it seems unlikely that senior leaders without TCI would accept such risks to (the other dimensions of) their SEW. Only those with high TCI will do so because such behaviors can help set up a healthier family firm for the next generation. Consistent with the transgenerational entrepreneurship perspective’s prediction that senior leaders’ TCI should foster innovation behaviors prior to succession, we expect that

Hypothesis 1: Senior-generation leaders’ TCI is positively related to innovation behaviors prior to succession.

We submit, however, that the relationship between TCI and innovation behaviors is more nuanced and complex. Many family firms where senior leaders possess TCI do not excel in innovation behaviors (Erdogan et al., 2020). We build upon these observations to suggest that for senior-generation leaders to be motivated to pursue innovation, they also need confidence that the next generation is able and willing to take over and grow the business. We posit that such confidence emerges when the succession process unfolds in a way that reduces senior leaders’ perceived TCU.

Perceived TCU and the TCI-Innovation Relationship

Perceived uncertainty is central to explaining entrepreneurial action (McMullen & Shepherd, 2006; Packard et al., 2017). Uncertainty nurtures a “sense of doubt” (p. 135) that undermines confidence in intentions and beliefs and thereby paralyzes entrepreneurial action (McMullen & Shepherd, 2006). Uncertainty is when potential outcomes cannot be predicted, and unlike risk, a probability distribution cannot be assigned to potential outcomes (Townsend et al., 2018). McKelvie et al. (2011) argued that there are two fundamental sources of innovation-related uncertainty: perceived market uncertainty about how an innovation will be received and perceived technological uncertainty about the direction of future technological changes. These uncertainties cause managers to delay innovation projects until new information becomes available that reduces perceived uncertainty (Bernanke, 1983; Bloom et al., 2007).

We submit that family-firm leaders confront a third source of perceived uncertainty that comes from the family. The senior generation might have high TCI but face TCU regarding whether a next-generation family member will continue the business for another generation. For senior-generation leaders with TCI, the desired outcome is to hand over the family firm to the next generation as an ongoing concern (i.e., not to be sold by the next generation; Berrone et al., 2012). However, the succession process is inherently uncertain because it depends on many factors, such as the relationship between incumbent and successor, successors’ career plans and willingness to join the firm, successors’ work experience and leadership capabilities, and succession planning (Cater et al., 2016; De Massis et al., 2008; Le Breton-Miller et al., 2004). Unsolicited survey comments echo this perceived uncertainty:

Of my three kids, two have decided to pursue a career outside the family firm. My son [third child] is studying media and publishing, which qualifies him for our business. But, if he takes over the company at some point, I really don’t know.—CEO (third generation), media company. My daughter, who is still doing her studies, will maybe take over the business and join the leadership team in the future. However, I also need to prepare for the scenario that no family member will continue the business. Therefore, I have started to employ external managers to ensure business continuity in any case.—CEO (third generation), manufacturing company. I always wanted to become a helicopter pilot in the German armed forces and already passed all the tests for it. When the federal government decided to downsize the army in 2011, there was no position left for me. This was the first time in my life when I considered joining my parents in the business. Before that, my father managed the business in a way to sell it at the end of his career. Since he knew that I would join the business after my studies, he put more effort in the company to hand it over in good shape in the future.—Next-generation member now active in leadership (fourth generation), construction company.

Conversely, when senior leaders have confidence that the next generation is able and willing to take over and extend the business life as a family firm—that is, when perceived TCU is low—the motivating effect of TCI on innovation behaviors can be unleashed. Senior leaders with high TCI and low TCU should be eager to increase innovation behaviors, thereby making the business more attractive and increasing the likelihood that successors can continue the business for another generation.

Uncertainty research shows that decision-makers avoid or delay key decisions—such as pursuing more innovation projects—to look for cues that help reduce perceived uncertainty (Bernanke, 1983). Accordingly, senior-generation leaders should look for cues that help predict the ability and willingness of the next generation to take over and continue the family firm. Uncertainty research explains that perceived uncertainty surrounding personal relationships is best addressed through interaction in the workplace (Bordia et al., 2003; Kanter, 1985). This insight aligns with family-firm research showing that the next generation’s involvement in the business fosters identification with the family firm, knowledge transfer across generations, and willingness to succeed in the business (Garcia et al., 2019; Jaskiewicz et al., 2015; Le Breton-Miller et al., 2004; McMullen & Warnick, 2015). The senior generation is likely to have greater confidence that the next generation will both want to and be capable of taking over if the next generation has had a long and meaningful relationship with the business, a relationship that begins in childhood (Schmitt-Rodermund, 2004; Zellweger et al., 2011). Accordingly, next-generation members’ childhood involvement in the family firm provides an appropriate proxy reflecting lower perceived TCU among senior leaders.

As described earlier, ample research shows several ways that childhood involvement in family firms facilitates the succession process (De Massis et al., 2008; Lansberg & Astrachan, 1994). Several unsolicited comments from senior leaders illuminate how childhood involvement reflects lower uncertainty perceptions regarding the succession process:

A couple of times a year, we let our children do presentations on core functionalities of our products. We also take them with us from time-to-time when traveling to our foreign subsidiaries.—Managing director (third generation), mechanical engineering company. Of course, I introduced my son to the business early on. But I also gave him a lot of freedom to do whatever he wanted. In the end, he needs to ask the right questions to become an entrepreneur [in the business] himself.—Managing director (11th generation), manufacturing company.

Comments from several next-generation members describe how early business exposure had an influence on their identification with and desire to join the family firm:

As children, we literally grew up in the office. Some of our employees have known me since I was a little boy.—Next-generation member active in leadership (second generation), professional services company. I always used to help my father with this and that on the side or on the weekend—and I still do so today. I can well imagine joining my father in the company at some point in time.—Next-generation member (second generation), retail company.

Although uncertainty is a priori irreducible (e.g., Townsend et al., 2018), new information, entrepreneurial judgment, observation, and learning can partially resolve perceptions of uncertainty (Packard et al., 2017). Applied to our context, senior family leaders with TCI face uncertainty regarding the viability of intrafamily succession. When the next generation has gained a deeper appreciation of the business by working in and around it from childhood, the senior generation has more information about their children’s abilities and willingness to someday lead the family firm, which is reflected in lower levels of perceived TCU. With less uncertainty about transgenerational control (i.e., less TCU), senior-generation leaders should be more confident that pursuing and supporting more innovation behaviors prior to succession will help set up a healthy family firm for another generation (Parker, 2016). We therefore anticipate,

Hypothesis 2: The relationship between senior leaders’ TCI and innovation behaviors prior to succession is positively moderated by next-generation childhood involvement in the business, such that innovation behaviors prior to succession increase more when senior leaders have high TCI, and the next generation was involved in the family business during childhood.

While childhood involvement in the business serves as a proxy for lower perceived uncertainty about the next generation’s ability and willingness to return in the future, it is only once they actually return and assume a leadership position that senior leaders gain full confidence (i.e., experience very low TCU) that transgenerational control and hence family succession will take place (Minola et al., 2016). Entry of the next generation’s human and social capital should increase the firm’s entrepreneurial capacity (Jaskiewicz et al., 2015) and thereby enhance EO (Sciascia et al., 2013) and innovation (Zahra, 2005), but such is often not the case (Erdogan et al., 2020). We submit that whether multigenerational leadership (as a proxy for very low TCU) fuels innovation behaviors prior to succession will depend on senior leaders’ level of TCI.

Although senior leaders’ perceived uncertainty around the potential for transgenerational succession (i.e., TCU) plummets when the next generation joins the leadership team, many senior-generation leaders cling to control and retain relatively low TCI; any transition remains for them in the distant future (Jaskiewicz et al., 2015; Le Breton-Miller et al., 2004). Such senior leaders prize protection of their other SEW dimensions based on continued control and deep identification with the firm and its accomplishments under their leadership. We theorize that such low TCI among senior leaders leads to what Jaskiewicz et al. (2015) call “ordinary” successions, wherein the senior generation retains full control while supervising and transferring knowledge to the designated successor (Le Breton-Miller et al., 2004; McMullen & Warnick, 2015). Designated successors can engage in innovation behaviors by leveraging their (relatively) newly developed human and social capital, but their impact is limited when the senior generation’s low TCI fosters behaviors that are consistent with the past and do not allow successors (and anyone else) to challenge the senior leaders’ past accomplishments (which is part of their SEW). Senior leaders with low TCI will thus prefer modest innovation behaviors prior to succession that do not take full advantage of the next generation’s unique talents.

This situation, we submit, is different when low TCU is coupled with high TCI. In such cases, multigenerational leadership likely resembles what Jaskiewicz et al. (2015) called “entrepreneurial bridging” (p. 42), wherein the senior generation takes advantage of the next generation’s recently gained education and training to expand entrepreneurial capacity. The senior generation might still manage day-to-day operations but, because of their desire to see the next generation succeed (i.e., due their high TCI), they give the next generation authority and resources to engage in innovative behaviors such as introducing new products and entering new markets. Doing so helps resolve the entrepreneurial capacity problem described by Penrose (1959). Fresh from education and work experiences in areas relevant to the business and unburdened with day-to-day operations (because senior leaders do this), the next generation brings additional capacity to pursue new product ideas and new markets with the help of senior leaders. The result is that these family firms, on average, experience “entrepreneurial leaps”—multiple acts of entrepreneurship in short time periods—after the next generation joins the firm’s leadership (Jaskiewicz et al., 2015, p. 42). Several survey respondents from high innovation firms offered unsolicited comments that align with entrepreneurial bridging:

While my father manages day-to-day operations, I focus on customer acquisition, projects to upgrade our infrastructure, and on improving our processes to make us more efficient.—Next-generation member active in leadership (third generation), construction company. As the head of our US subsidiary I am gaining a lot of experience. I focus on growing our market share in North America. At home, my father takes care of the headquarters. Whenever there is something to discuss, we are in close contact.—Next-generation member (third generation), mechanical engineering company. My daughter recently joined the business. She is focusing on renewing our marketing strategy as well as bringing us online. It’s great to see her working on innovation topics. I guess my wife and I simply did not have time for that.—Managing director (third generation), professional services company.

Overall, senior leaders are more likely motivated to act upon their TCI to support the next generation’s pre-succession innovation behaviors if they have more to gain than to lose. Only leaders with high TCI will have sufficient SEW gains (by seeing their TCI fulfilled) to risk some of their “old” SEW, which might be partially lost when outdated accomplishments are replaced with, for example, new products. Conversely, modest TCI might be sufficient to transfer ownership and control but insufficient to motivate senior leaders to pursue and support risky innovation behaviors that would require senior leaders to expose their accumulated SEW to new ideas. Only once TCU is greatly reduced, as reflected by multigenerational leadership, are senior leaders with high TCI motivated to unleash the entrepreneurial capacity of the family firm by pursuing and supporting more innovation behaviors. Stated formally,

Hypothesis 3: The relationship between senior leaders’ TCI and innovation behaviors prior to succession is positively moderated by multigenerational leadership, such that innovation behaviors increase more when senior leaders have high TCI, and the next generation has returned to the business as adult leaders.

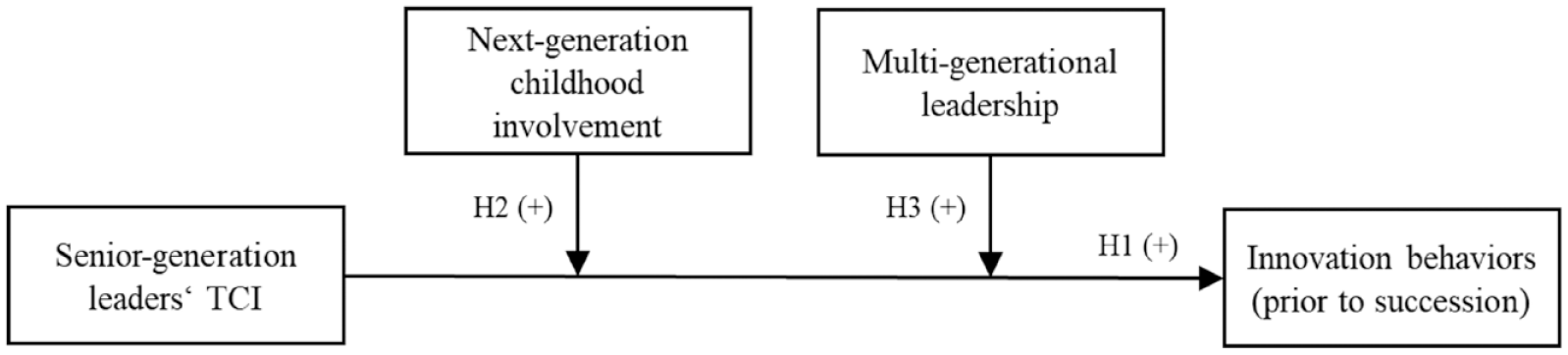

Figure 1 summarizes our research model.

Research Model

Data and Methods

Sample

We collected survey and archival data from German family firms. We define family firms as businesses with at least 50% family ownership (Hoffmann et al., 2019; Zellweger et al., 2012b). Germany is an ideal setting for testing our hypotheses because there are many family firms in the “German Mittelstand,” a group of privately held firms known for their quality and innovation (De Massis et al., 2018, p. 126). We began by contacting 3,053 medium and large German family firms by email. Contact information for 1,500 businesses came from a 2017 list of the “top [largest] family firms” in Germany, and another 1,553 businesses were identified from regional lists (covering all of Germany) provided by a national family firm association and a major German university. We contacted the listed firms individually in the first quarter of 2018 and asked family owners/managers to participate. Over 6 months, three reminders were sent to all nonrespondents. If a senior-generation leader answered our t0 survey first, we asked them whether an adult next-generation member exists and, if so, whether they would forward a survey to them. We did the same with adult next-generation members; if they answered the t0 survey first, we asked whether a senior-generation member was active in leadership and, if so, whether they would forward a survey to them. Respondents were given the option of taking the survey online, over the phone, or face-to-face at a location of their choosing.

A total of 421 family members from 305 family firms completed the t0 survey. After excluding 27 respondents who were not from an owning family and 11 respondents who did not consider their business to be a family firm, we were left with 383 responses from 267 family firms: 183 senior-generation leaders and 200 next-generation members. Comparable to Zellweger et al. (2012a) who achieved an initial 8.2% response rate, we received responses from 8.7% of targeted businesses. Among these 267 family businesses, we received responses from both the senior and the younger generation in 115 cases.

With an average time lag of 4 months, all t0 respondents were contacted again in the fourth quarter of 2018 for the t1 survey with the dependent variable. We targeted one family owner and/or manager to complete the t1 survey. Over the next 3 months, we sent out three reminder emails to all participants where a response from a family owner/manager was still missing. We received 236 completed t1 surveys from 211 distinct family firms, 93 from the senior and 143 from the next generation. For 25 businesses, we received t1 answers from both generations. We had to exclude two cases where t1 survey respondents were no longer active as owners/managers, leaving 111 family firms for which we had t0 responses from both a senior- and next-generation family member and a completed t1 survey.

Seeking responses from two respondents and across two time periods was important because (1) testing our theory required information from both generations and (2) collecting data in two time periods reduces potential for common method bias (e.g., Podsakoff et al., 2003, 2012) and helps establish temporal order of causal relationships (e.g., Mazzola et al., 2013). Such advantages are large relative to the increased risk of nonresponse bias, which can be reduced by establishing representativeness (Hellevik, 2016) as we do below. Both surveys were conducted in German. All scales were translated into German and back-translated by an independent researcher to ensure consistency with the original sources.

In 32 cases, at least one respondent completed the t0 survey in-person or over the phone. During these personal interactions, we followed a strict survey guide with predefined questions. Prior to administering the survey, we asked whether we could take notes, record, and use (anonymously) any unsolicited comments made by respondents. The online version also gave respondents a text box in which to comment. We captured 98 unsolicited comments. While not part of our theory development, many comments spoke to relationships of interest. Thus, we used them above to illustrate and contextualize our hypotheses development.

We collected archival data from the German Federal Gazette (Federal Ministry of Justice and Consumer Protection, 2019), which contains legally mandated balance sheet and income statement data. We used 2017 data, 1 year before the t1 survey, to help establish causality. Archival data were available for 106 out of the 111 family firms. The five firms where no archival data were available are small unincorporated businesses that are not obligated to publish data in the German Federal Gazette. Our final sample is 106 firms with two generations of t0 surveys (212 total), a t1 survey, and complete archival data.

Following Zellweger et al. (2012b), we assessed the potential for nonresponse bias in four ways. First, we compared the means of all variables for early and late respondents (Churchill, 1995). No significant differences were observed. Second, we compared complete and incomplete surveys on those items where both groups had complete answers and found no differences. Third, we compared the 106 family firms in our sample with businesses that were excluded because either (1) only one generation completed the t0 survey or (2) no one completed the t1 survey. Independent samples tests across all variables indicated no significant differences between family firms for which we have complete data and those for which we lacked some data. Finally, we compared sample firms’ number of employees in 2017 to data in the German Business Register (Federal Statistical Office, 2019a). We divided the sample into the following classes (Eurostat, 2019): (1) small: less than 49 employees, (2) medium: 50 to 250 employees, and (3) large: more than 250 employees. In the German Business Register, the small class accounts for 97.7%, medium for 1.8%, and large for 0.5% of all businesses. Our sample is stratified and almost evenly reflects the three classes with 33 small businesses, 38 medium-sized businesses, and 35 large businesses. Medium-sized and large family firms in our sample are overrepresented, presumably because we required two (adult) generations, which is rare in young/small firms. Our sample also requires that legally mandated information is available in the German Federal Gazette. As a result, and similar to Zellweger et al. (2012b), our sample appears representative of established medium- and large-size family firms in Germany, but not representative of very small family firms.

Variables

Dependent Variable

Our theorizing predicts the extent to which firms pursue innovations behaviors prior to succession, such as introducing new/revised products or opening new markets. We expect that such innovation behaviors, a subset of what have been called innovation outputs (Block et al., 2022), will have performance consequences, but these are not our focus. We therefore operationalized innovation behaviors using a seven-item scale (Alegre & Chiva, 2013), which is based on the OECD’s Oslo Manual (Organisation for Economic Cooperation and Development, 2005). The scale was developed to rectify known problems with prior (input and output) innovation measures (Alegre & Chiva, 2013) and is used regularly in innovation studies (e.g., Bradonjic et al., 2019; Dahl, 2011; Piening & Salge, 2015). Using 7-point Likert-type scales ranging from “much worse” to “much better”, respondents were asked in the t1 survey to rate their family firms’ product and process innovation behaviors compared with competitors. Innovation behaviors scores were calculated using the mean of the seven items (α = .77). The full scale is reported in the appendix.

Independent Variable

We measured senior generation’s TCI using Berrone et al.’s (2012) four-item scale (α = .78) in the t0 survey. Respondents had to answer on a 7-point Likert-type scale ranging from “fully disagree” to “fully agree”. TCI was calculated as the mean of the four items. The full scale is reported in the appendix.

Moderator Variables

Based on the findings from Houshmand et al. (2017) and Jaskiewicz et al. (2015), we created a two-item reflective scale for next-generation childhood involvement in the t0 survey: (a) “In our family, children were introduced to the family firm early on,” and (b) “In our family, children were involved in the family firm on weekends, after school, or during school holidays.” Both use a 7-point Likert-type scale anchored with “fully agree” to “fully disagree”, and childhood involvement was calculated as the mean of the two items (α = .76).

To measure multigenerational leadership, we asked each generation about their current role in the family firm and created a dummy variable that equals one if both generations are active in leadership simultaneously, zero otherwise (e.g., Hsu & Chang, 2011). Given that this is factual data obtained directly from those involved, it was not necessary to generate a multi-item scale and establish scale reliability.

Control Variables

We included several control variables that might influence the relationship between TCI and innovation. We controlled for firm size, measured as the natural logarithm of total assets. Larger businesses pursue more ambitious innovation projects (e.g., Muñoz-Bullón & Sanchez-Bueno, 2011). We controlled for firm age measured as the natural logarithm of years since the firm’s founding; older firms exhibit less innovation on average (e.g., Broekaert et al., 2016). We controlled for firm leverage calculated as total debt divided by total assets; businesses with higher debt ratios have fewer means to pursue innovation (e.g., Muñoz-Bullón & Sanchez-Bueno, 2011). We controlled for firm performance with return on assets (ROA) calculated as net organizational income divided by total assets. Low firm performance can motivate family owners and managers to seek riskier R&D investments (e.g., Chrisman & Patel, 2012). The three variables firm size, firm leverage, and firm performance were derived from archival data published in the 2017 German Federal Gazette. The other controls were measured in the t0 survey. All controls were thus collected earlier and separately from the dependent variable.

It was important to control for the possibility that firms have TCI because their orientation toward innovation gives them a longer time horizon. We therefore controlled for EO using the nine-item Covin and Slevin (1989) scale. Controlling for EO helps account for otherwise unobserved heterogeneity in the firm’s overall innovation posture that likely co-varies with TCI. We also controlled for the likely effects of human capital on innovation by including a measure for next-generation education using a 7-point scale adapted from Mahto et al. (2010), wherein 1 = “no degree”, 2 = “secondary school”, 3 = “junior high-school”, 4 = “A-Levels”, 5 = “vocational training”, 6 = “university graduate”, and 7 = “PhD”.

Finally, we controlled for industry effects with indicator variables based on NACE (Nomenclature of Economic Activities) industry codes (Eurostat, 2008); 95% belong to one of the following industries: food, packaging, and pharma; construction; manufacturing; services; and trade. The remaining 5% make up the omitted category (e.g., Chrisman et al., 2012).

Results

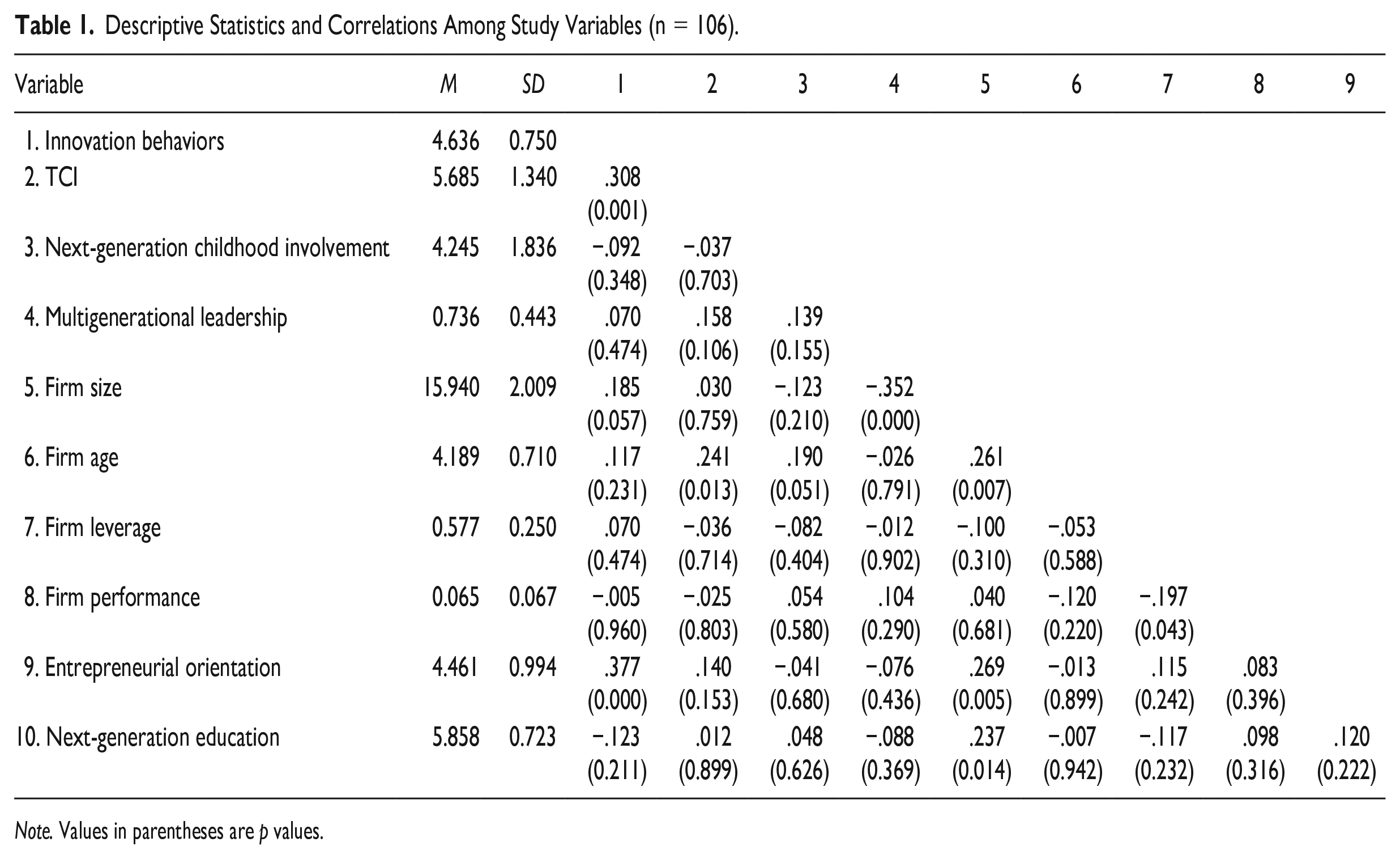

Means, standard deviations, and correlations for all variables are shown in Table 1. On average, sample firms had total assets of 152 million Euros in 2017 and were 85 years old. Twenty-four percent were in manufacturing; 23% in food, packaging, and pharma; 16% in construction; 16% in services; and 16% in trade. Another 5% were in other sectors. On average, firms were owned by the third generation. Senior-generation respondents averaged 63 years in age and the next generation averaged 33 years. Correlations show expected signs except for between the next-generation members’ education level and innovation behaviors, which is negative. 5 Regression results are shown in Table 2. With the highest variance inflation factor at 4.22 (for an industry dummy), all are below suggested cut-offs (Hair et al., 2014).

Descriptive Statistics and Correlations Among Study Variables (n = 106).

Note. Values in parentheses are p values.

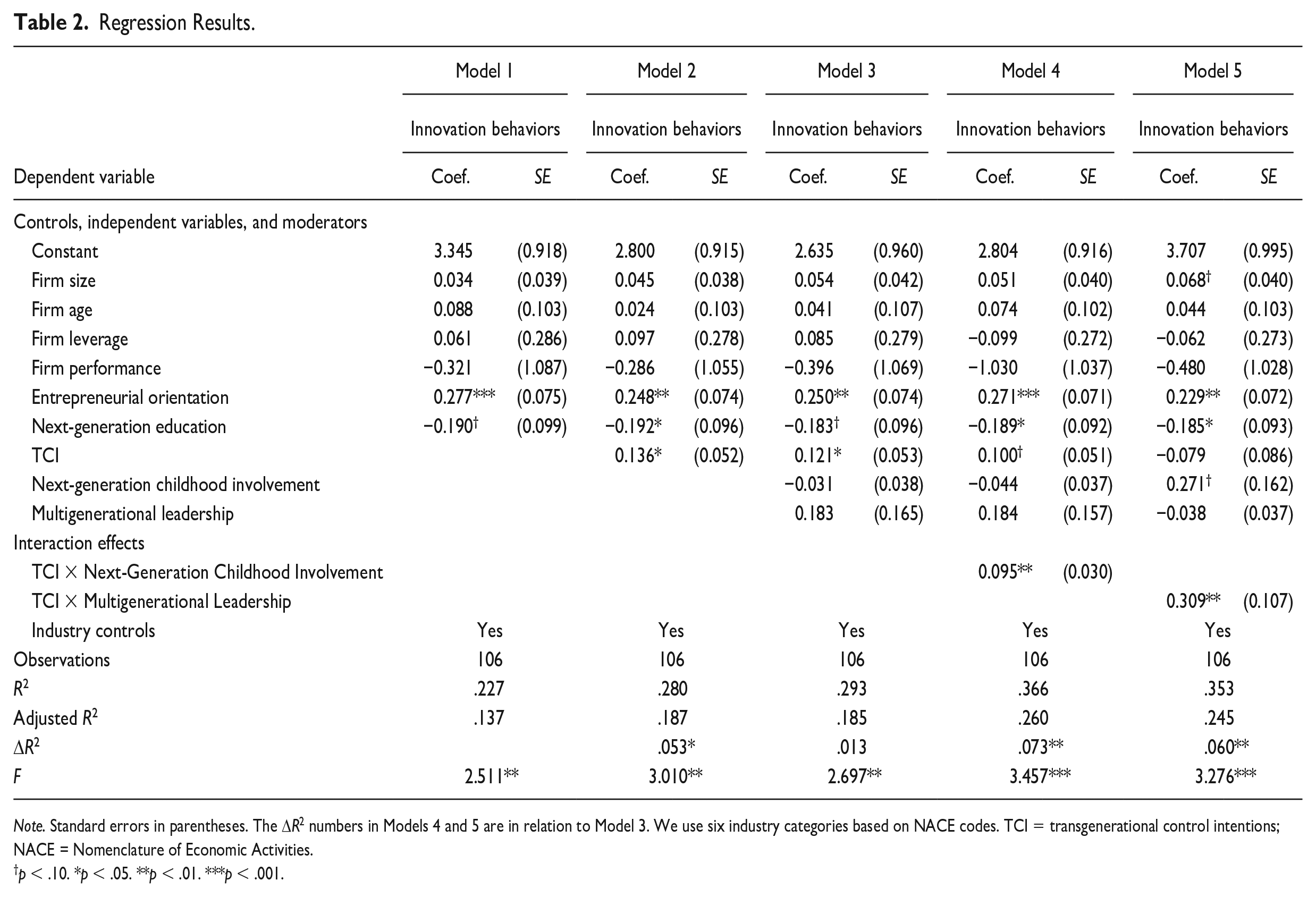

Regression Results.

Note. Standard errors in parentheses. The ΔR2 numbers in Models 4 and 5 are in relation to Model 3. We use six industry categories based on NACE codes. TCI = transgenerational control intentions; NACE = Nomenclature of Economic Activities.

p < .10. *p < .05. **p < .01. ***p < .001.

Table 2 shows multivariate regressions focusing on TCI, childhood involvement, and multigenerational leadership. 6 Model 1 includes all controls, and Model 2 adds TCI. Hypothesis 1 anticipates that senior leaders’ TCI increases innovation behaviors. Supporting Hypothesis 1, the coefficient for TCI is positive and significant (β = .136, p < .05).

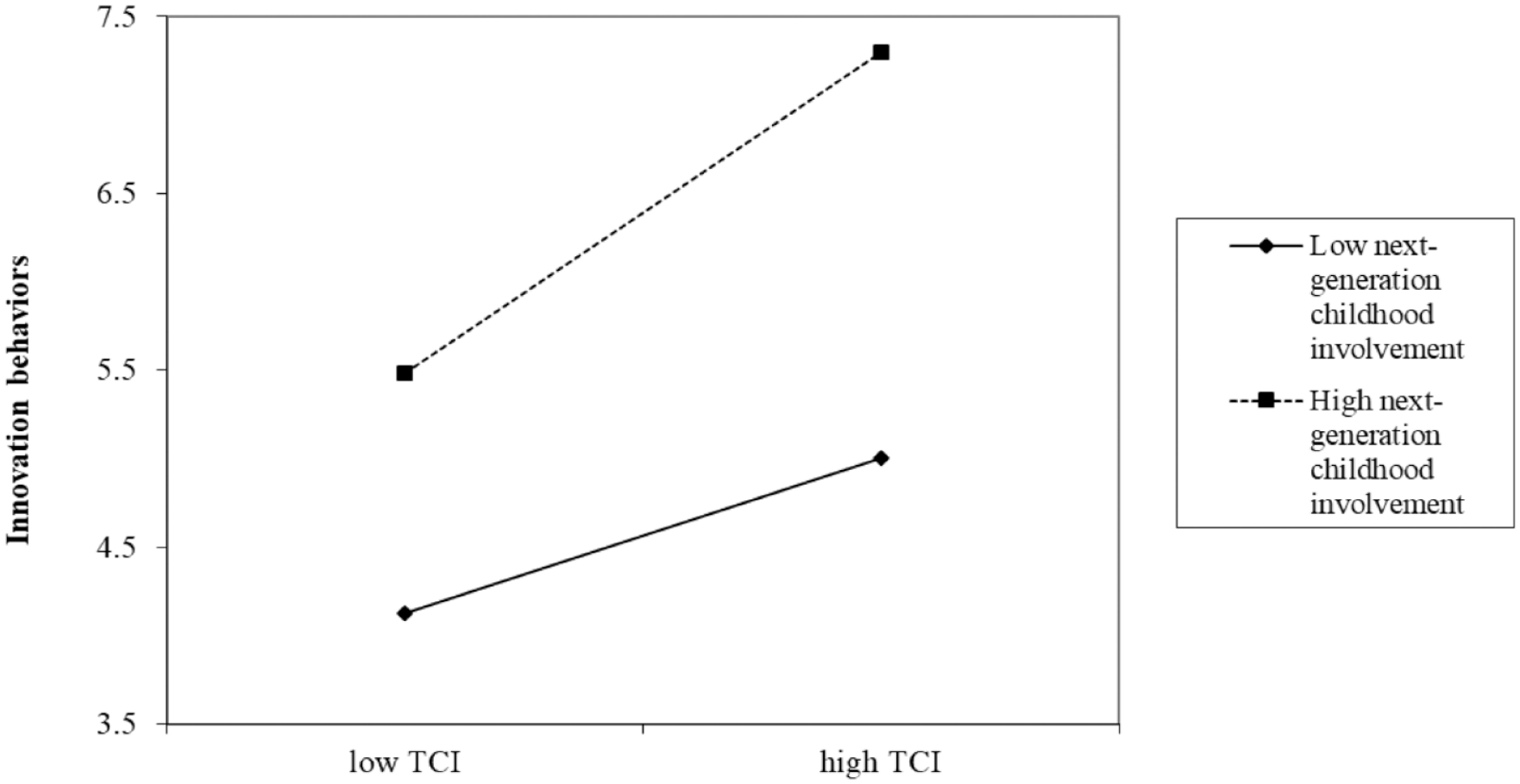

Hypothesis 2 predicts that childhood involvement increases the impact of TCI on innovation behaviors. Model 3 adds childhood involvement and multigenerational leadership as independent variables, and Model 4 adds the TCI × Childhood Involvement interaction, which is positive and significant (β = .095, p < .01). Hypothesis 2 is thus supported. Family firms with (1) high childhood involvement of next-generation members and (2) senior leaders with high TCI show an increase in innovation behaviors prior to succession of 57.3% over the average family firm. Figure 2 depicts the interaction. A simple slope analysis shows that family firms with both low (one standard deviation below the mean) and high childhood involvement (one standard deviation above the mean) show positive and significant relationships between TCI and innovation, but high childhood involvement family firms show more pre-succession innovation behaviors overall and such innovation behaviors increase significantly more rapidly as TCI increases. This finding is confirmed by a marginal effects analysis, as described by Busenbark et al. (2022). The slopes are significantly different from each other such that the relationship between TCI and innovation behaviors is positive and significant at the median value of childhood involvement (M = 4.5; p = .017) and above (Q3 = 7; p < .000), while the relationship between TCI and innovation behaviors prior to succession is insignificant (Q1 = 2.5; p = .411) for lower levels of childhood involvement.

Interaction Between TCI and Next-Generation Childhood Involvement.

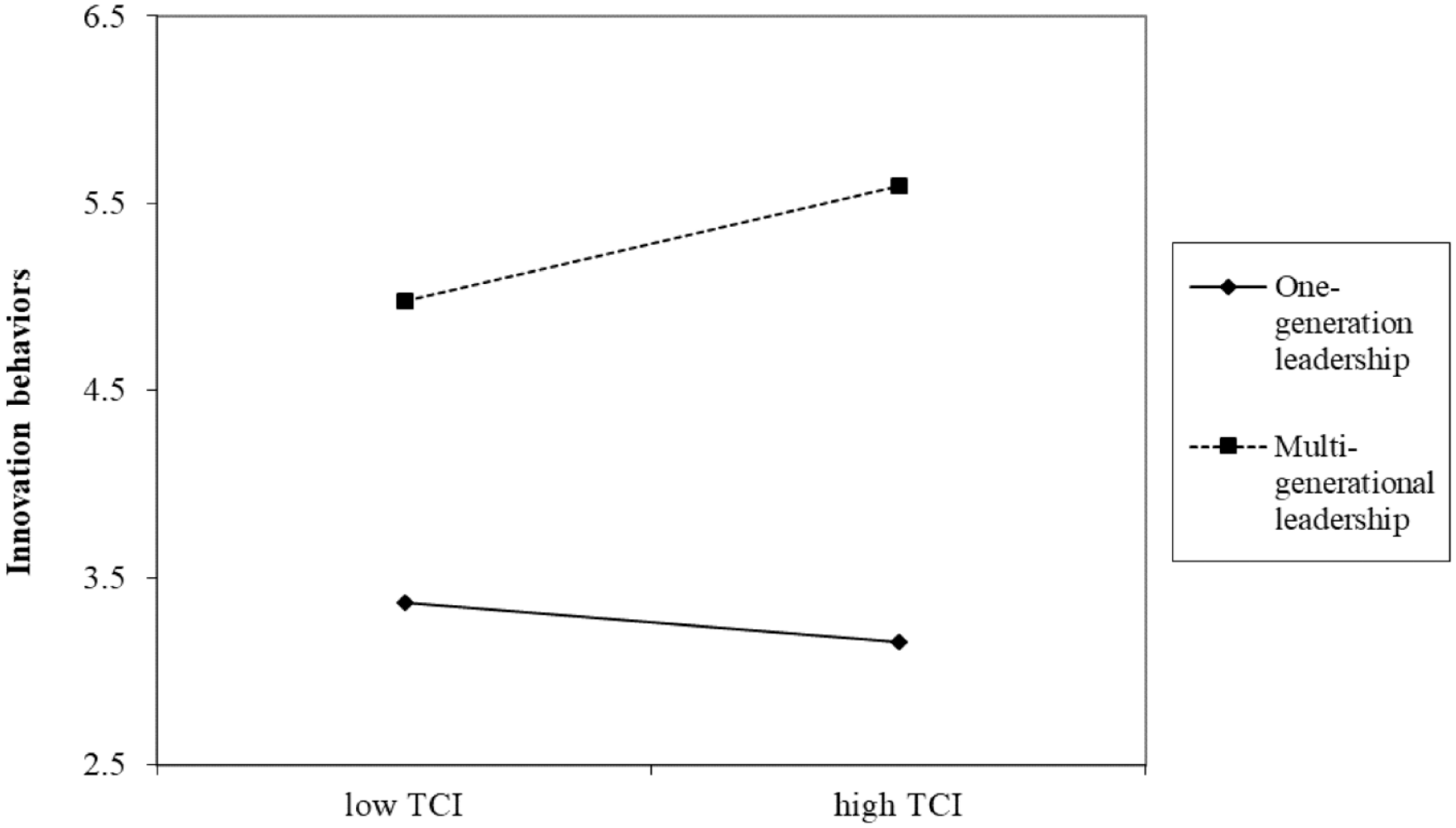

Hypothesis 3 posits that multigenerational leadership motivates senior leaders with high TCI to pursue and support innovation behaviors prior to succession. Model 5 adds the Multigenerational Leadership × TCI interaction, which is positive and significant (β = .309, p < .01), lending support to Hypothesis 3. If the senior leader has high TCI, multigenerational leadership increases innovation behaviors by 20.6%. Figure 3 depicts the interaction. A simple slope analysis shows no significant relationship between TCI and innovation behaviors with only one generation in leadership, but the relationship is positive and significant in firms with multigenerational leadership, and the slopes are significantly different from one another such that multigenerational leadership is associated with significantly higher innovation behaviors (p < .000), while one-generational leadership is not (p = .368) (Busenbark et al., 2022).

Interaction Between TCI and Multigenerational Leadership.

Robustness Tests

We ran a series of tests to investigate the robustness of our findings. First, to ensure that we effectively control for market dynamics in different industries, we added the average growth rate of each industry in Germany over the prior 3 years (Federal Statistical Office, 2019b). Results remain unchanged.

Second, our theory is that childhood involvement reflects decreased senior-generation TCU by increasing the next generation’s desire to return and take over, which implies that childhood involvement should also increase the next generation’s TCI. Using the same controls as in the primary analysis, childhood involvement relates positively and significantly (β = .131, p < .01) with next-generation TCI.

Third, our theory is that both succession process stages influence the TCI-innovation behavior relationship, so we ran both interaction terms in the same model. Both remain significant at p < .05 despite moderate dangers of multicollinearity (condition indices > 30).

Fourth, because the desire for SEW preservation declines after the second generation (Cruz & Nordqvist, 2012; Gómez-Mejía et al., 2011; Le Breton-Miller & Miller, 2013), we replaced the control for firm age with a self-report of which generation currently owns the firm. Results remain unchanged.

Fifth, because age can influence family leaders’ appetite for innovation behaviors, we added controls for predecessor and successor ages. Results are unchanged.

Sixth, as an alternative approach to controlling for industry effects on innovation behaviors, we calculated industry-adjusted innovation by subtracting the mean innovation for each firm’s sector from its innovation. We re-ran all our models using industry-adjusted innovation behaviors as the dependent variable. Results are unchanged.

Seventh, although innovation behaviors are risky and outcomes unclear, such behaviors, on average, impact financial firm performance positively (Andriopoulos & Lewis, 2009; Calantone et al., 2002). To test whether this is the case in our data, we regressed innovation behaviors and controls (from the main analysis) on firm profitability measured using an item from Eddleston et al. (2013): “How would you rate your firm’s current profitability as compared with your competitors?” on a 5-point Likert-type scale ranging from “much worse” to “much higher”. Consistent with expectations, ordered logistic regression analysis resulted in a positive and significant coefficient for innovation behaviors (Coef. = .848, p < .01). However, because innovation behaviors and firm performance were both measured at t1, we cannot exclude the possibility of reverse causality.

Eighth, we investigated the potential that the TCI-innovation behavior relationship is due to better inter-generational knowledge transfer (Filser et al., 2018) rather than a longer time horizon. Because knowledge transfers through socialization processes, we measured socialization using the mean of two items derived from Jaskiewicz et al. (2015): (a) “We often talk about the family firm at home” and (b) “We often talk about the family firm at family meetings/reunions”. Both items were measured in the next generation’s t0 survey using a 7-point Likert-type scale (α = .78). Socialization (β = .048, n. s.) had no direct effect or interaction effects with TCI on innovation behaviors prior to succession. Although null results should be interpreted with caution, our results suggest that the TCI-innovation behavior relationship is due to senior generations’ longer time horizon more so than knowledge transfer between generations.

Ninth, to ensure that our measure of innovation behaviors captures innovation behaviors, not the outcomes of these behaviors, we eliminated one item from the previously validated seven-item scale that reflected an innovation outcome—the growth of market share relative to competitors. We re-ran the analysis without this item. Results remain unchanged.

Finally, it is possible that family firms with high TCI senior leaders that are progressing successfully through the succession process might focus on more radical innovations. To explore this possibility, we re-ran the analysis two more times, once with the one item that asked about more radical innovations (e.g., “Extension of product range outside the main product field”) as the dependent variable and once with the innovation scale sans that item. Comparing the coefficients revealed a significant difference for the coefficients: TCI × Childhood Involvement interaction, indicating that family firms with high childhood involvement and senior leaders with high TCI pursue more explorative actions. For TCI × Multigenerational Leadership, coefficient differences are insignificant. We discuss implications of our robustness tests in the Discussion section.

Discussion

Much is known about succession processes and the key steps that make them work (De Massis et al., 2008; Decker et al., 2016). Potential successors are exposed to the firm early and throughout their youth through family stories and through part-time and summer jobs (Le Breton-Miller et al., 2004). Skill gaps are identified and potential successors are encouraged to pursue relevant education and work experience (Le Breton-Miller et al., 2004). Finally, one or more adult children bring their newly developed human and social capital back to the family firm where they work with and learn from the senior generation (Decker et al., 2016).

These steps not only shape the next-generation post-succession, but it also affect the senior generation pre-succession. The emerging (and growing) transgenerational entrepreneurship perspective suggests that senior-generation leaders with TCI have a longer time orientation (Le Breton-Miller & Miller, 2006; Lumpkin & Brigham, 2011) that motivates them to prepare the firm for the next generation’s continued success post-succession (Diaz-Moriana et al., 2020; Strike et al., 2015; Zellweger et al., 2012a). Among the most important actions the senior generation can take to prepare the firm is to engage in acts of innovation, such as developing new products and markets (Baregheh et al., 2009), and to support the innovation behaviors of the next generation once they join the leadership team (Jaskiewicz et al., 2015). However, not all family firms innovate in the years prior to succession, suggesting that other factors are needed to help explain when TCI motivates the senior generation to pursue and support innovation behaviors prior to succession. We contribute transgenerational uncertainty (TCU) as a theoretical mechanism that explains when TCI motivates senior-generation leaders to pursue and support innovation behaviors prior to succession. Perceived uncertainty is known to reduce or delay innovation (Bernanke, 1983; Bloom et al., 2007) and TCU is a source of uncertainty unique to family firms. If senior-generation leaders are uncertain about the next-generation members’ ability and willingness to take over, there is less motivation to act on their TCI.

Using a multi-respondent multi-time period survey, we found evidence consistent with our theorizing. The impact of senior leaders’ TCI on innovation behaviors is stronger when next-generation members were involved in the business as children. Prior studies had explained how childhood involvement increases the next generation’s identification with and motivation to return to the family firm (Garcia et al., 2019; Jaskiewicz et al., 2015; McMullen & Warnick, 2015). Reflective of this increased confidence in an eventual family succession, we find that the impact of childhood involvement motivates those senior-generation leaders with TCI to engage in innovation behaviors that enhance the next generation’s probability of success. We also found that among those firms with multigenerational leadership—which reflects the virtual elimination of TCU—only those with strong senior-generation TCI fully unleash their entrepreneurial capacity through innovation behaviors. This evidence adds nuance to theory about differences between ordinary successions and those involving entrepreneurial bridging (Jaskiewicz et al., 2015). Ordinary successions are characterized by the senior generation transferring knowledge to the next (Le Breton-Miller et al., 2004). In entrepreneurial bridging, the senior generation manages day-to-day operations and provides support for the next generation as they deploy their newly developed human and social capital to rejuvenate the firm (Jaskiewicz et al., 2015). Our evidence suggests that TCI is an important indicator distinguishing between ordinary and entrepreneurial successions in that entrepreneurial bridging (as expressed by innovation behaviors) seems to occur only when the senior generation has strong TCI.

In addition, our test of the transgenerational entrepreneurship’s perspective with respect to innovation is important because we took steps to rule out knowledge transfer (via socialization) as an alternative explanation (Filser et al., 2018). We found a positive effect of TCI on innovation behaviors even after controlling for socialization processes where knowledge transfer takes place. This test provides additional evidence in support of the transgenerational entrepreneurship perspective’ view that the TCI-innovation relationship is positive because senior leaders’ focus on preparing a healthy firm for the next generation, not just knowledge transfer. This has important implications for family managers, and those who would advise them, regarding which actions are most appropriate for motivating innovation (e.g., transferring knowledge vs. helping the next generation develop new knowledge).

Finally, our test of the transgenerational entrepreneurship perspective and our theorizing regarding when TCI most impacts senior leaders’ innovation behaviors help reconcile competing predictions from the transgenerational control and SEW perspectives. A core prediction of behavioral agency theory with respect to SEW is that family owners take strategically conservative actions to protect their SEW, which implies less innovation (e.g., Block et al., 2013). The transgenerational entrepreneurship perspective isolates the TCI dimension of SEW to predict the opposite—that senior-generation leaders will take action to prepare the firm for the next generation (Zellweger et al., 2012a). Our test of the transgenerational entrepreneurship’s perspective with respect to innovation suggests value in research investigating each SEW dimension’s unique impact. However, our theory about TCU suggests that TCI’s impact only differs from other SEW dimensions under certain circumstances. Only when the senior generation’s TCI is high and their TCU is low, as reflected by successful progression through vital steps in the success process, will senior leaders pursue and support innovation behaviors before succession. Otherwise, such behaviors wane as the SEW perspective predicts.

Implications for Future Research

We focused on childhood involvement and multigenerational leadership as key steps in the succession process that reduce senior-generation leaders’ uncertainty regarding transgenerational control, that is, their TCU. However, there are likely other sources of TCU. Succession research, for example, describes how capability gaps must be identified and addressed through formal education and work experiences (Le Breton-Miller et al., 2004). An extension of our theorizing might suggest that such activities also impact innovation behaviors. Future research might also investigate whether TCU comes from outside the succession process. For example, competitive or technological changes might increase senior leaders’ TCU by creating barriers to the success of even the most thoughtful and talented designated successors.

Future research could further benefit from investigating other consequences of TCU. We investigated innovation behaviors, such as introducing new products and opening new markets (Baregheh et al., 2009), but there is a debate about how family ownership might differentially influence innovation inputs (e.g., R&D investments) versus outputs (Duran et al., 2016). The latter comingles both innovation behaviors and the performance outcomes of such behaviors (Baregheh et al., 2009). Because uncertainty reduces or delays risky investments (Bernanke, 1983; Bloom et al., 2007), one possibility is that TCU impacts innovation inputs more so than the behavioral outputs we investigated. Future research might find, for example, that TCU helps explain differences between family-firm innovation inputs and outputs relative to nonfamily firms. Future studies might also investigate whether TCU or the TCU-TCI combination impacts other risky decisions where family firms are known to behave differently, such as more radical innovation (Block et al., 2013), diversification (Gómez-Mejía et al., 2010), acquisitions (Gómez-Mejía et al., 2018), and internationalization (Arregle et al., 2021).

Our results are consistent with prior evidence suggesting that childhood involvement in the family firm is important, in our case, for reducing senior leaders’ uncertainty around succession. While prior research strongly suggests that childhood involvement in family firms has positive benefits for the younger generation in adulthood, on average (e.g., Carr & Sequeira, 2007; Houshmand et al., 2017), it seems naïve to suggest that such benefits are universal. Family science research shows immense heterogeneity among families (see Jaskiewicz et al., 2017 for a review), suggesting the potential for varied consequences. Recent evidence suggests, for example, that some parenting styles relate to successors’ psychological functioning in ways that result in unproductive employee behaviors (Shanine et al., 2022). When potential successors develop behavioral traits that make them unfit for leadership (Kidwell et al., 2012) or have childhood experiences that make them want to stay away from the family and its firm (Combs et al., 2021), childhood involvement might have the opposite effect from what we theorized and found. Such contingencies seem worth exploring so that researchers might gain a better handle on the heterogeneity among family firms’ succession processes and outcomes.

Finally, our theory and findings have implications for succession research. We found more innovation among family firms with multigenerational leadership teams where the senior generation has high TCI. We suggested that TCI should be higher among senior-generation leaders who view multigenerational leadership as a time for entrepreneurial bridging—a time to leverage next-generation talent to rejuvenate the firm. Our evidence is consistent with theory distinguishing ordinary successions from those involving entrepreneurial bridging (Jaskiewicz et al., 2015), but it is indirect evidence; we do not know for sure that it is the younger generation implementing innovations with support from senior leaders. The anecdotal evidence from our open-ended comments are consistent with Jaskiewicz et al.’s (2015) qualitative study, but it seems that direct investigation of entrepreneurial bridging and the conditions under which it takes place seems worthy of empirical scrutiny, especially given the potential to help researchers craft better advice for practitioners regarding how to transition the firm to the next generation in a way that infuses the firm with a spirit of innovation and entrepreneurship.

Limitations

Like all studies, ours has limitations that offer opportunities for future research. First, while we were able to obtain multiple responses and collected independent and dependent variables at different times, we were limited to a single European country. Germany is attractive because of the abundance of family firms (e.g., De Massis et al., 2018; Hoffmann et al., 2019; Zellweger et al., 2012b), and our sample appears representative of established family firms in Germany, but future research is needed to test our theory in other developed and developing economies. For example, in cultures where power distance between generations is much higher, TCU might matter less because the next generation is under immense social pressure to take over regardless of their personal desires and interests (Sharma & Irving, 2005).

Second, we used childhood development and multigenerational leadership as proxies that reflect the level of uncertainty senior leaders have regarding transgenerational control, which we labeled TCU. We did not directly measure perceptions of TCU. Future research might therefore benefit from developing and validating a scale to measure the senior generation’s TCU as a foundation for investigating its antecedents and consequences.

Third, while the time lag between the independent and dependent variables has advantages in terms of common method bias and reverse causality, the 4-month period might not be long enough to capture the effect of TCI on innovation behaviors, which unfold over a much longer timeframe. Intentions to hand over the business to the next family generation—that is, TCI and its motivating effect on innovation behaviors—might change as family leaders move through their own lifecycles (e.g., Minola et al., 2016). Future research is therefore needed that applies a combination of longitudinal panel data and qualitative research to triangulate on these long-term processes and detect variation along individuals’ lifecycles.

Finally, while we were able to control for socialization processes in which tacit knowledge transfer takes place, our two-item measure likely misses important socialization processes and there are likely other ways through with TCI might influence knowledge transfer, such as motivating the senior generation to spend more time with their children. Thus, we cannot fully rule out knowledge transfer as an alternative to the transgenerational entrepreneurship perspective for explaining the TCI-innovation relationship.

Conclusion

Childhood involvement in the family firm and returning in adulthood to work side by side with the senior generation are central steps in successful family business succession processes. While the impact of succession processes on the next generation is well known, less is known about their impact on the senior generation’s actions. Based on the transgenerational entrepreneurship perspective, we explain how movement through the succession process interacts with the senior generation’s TCI to affect their motivation to innovate and support innovation behaviors. Importantly, we explain why the TCI-innovation relationship is more complex than prior theorizing implies. Senior leaders need low uncertainty regarding their children’s ability and willingness to join the family business and high TCI to pursue innovation and unleash the talents and entrepreneurial spirit of their adult children. Our research draws attention to the important role of the succession process in shaping senior leaders’ response to their TCI before succession and highlights the need to disaggregate SEW dimensions to study firm-level behaviors such as innovation. We hope that our study offers a small step toward a more comprehensive understanding of what drives the most innovative family firms across generations not only after but also before succession.

Footnotes

Appendix

Acknowledgements

We thank Evelyn Micelotta, Alfredo De Massis, and Thomas Zellweger for their very helpful comments on a previous version of this paper. The paper also benefited from the input of three anonymous reviewers of the 2020 Academy of Management Conference.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.