Abstract

Organizational ambidexterity is vital for family firms’ long-term success, yet we still lack sufficient insights into the role of family involvement in top management in this context. Building on research on family firm innovation and diversity, we argue there are curvilinear relationships between family involvement in top management and exploration, exploitation, and organizational ambidexterity. We further propose that these (inverse) U-shaped relationships are affected by family CEOs’ family-centered noneconomic goals. Multisource data on 109 family-managed firms support most of our hypotheses and provide a nuanced understanding of how diversity within top management affects family firms’ innovative behavior.

Introduction

Organizational ambidexterity—that is, the simultaneous pursuit of exploratory and exploitative innovation (Goel & Jones, 2016; Raisch & Birkinshaw, 2008)—has been identified as an important driver of firm performance in general (Gibson & Birkinshaw, 2004) and of family firm performance in particular (Stubner et al., 2012). While exploitation entails a focus on quality and efficiency, enabling firms to closely monitor and optimize their current business activities, exploration comprises a focus on new opportunities as well as future products, services, markets, and customers that allows firms to achieve long-term competitiveness (March, 1991). Research on family firm ambidexterity has highlighted the peculiarities of ambidexterity in such firms (Dolz et al., 2019; Hughes et al., 2018), stemming, for instance, from the specific resources and agency cost constellations in family firms, which influence their willingness and ability to engage in organizational ambidexterity (Veider & Matzler, 2016). In particular, this research has emphasized the effects of family involvement in top management (see Tretbar et al., 2016, for an overview) for achieving organizational ambidexterity, given the important role of top management decision making in explaining firms’ ambidextrous activities (Lubatkin et al., 2006).

However, research so far has produced only scarce empirical findings and drawn partly inconsistent conclusions about how family involvement in top management affects innovation in general and organizational ambidexterity in particular (e.g., Arzubiaga et al., 2019). For instance, while some research argues and shows a positive association of family member involvement and organizational ambidexterity (Stubner et al., 2012), other research argues for a negative influence of family involvement (Hiebl, 2015) and a positive influence of nonfamily management (Veider & Matzler, 2016) on organizational ambidexterity. Similarly, Röd (2019) reveals a positive, linear relationship between involving nonfamily managers and organizational ambidexterity in the respective firm. Clarifying these inconsistencies is of utmost theoretical and practical relevance. First, since family firms differ widely in their ambidextrous behaviors (Veider & Matzler, 2016), we expect that studying the link between family involvement and organizational ambidexterity can advance our theoretical understanding of why family firms make different types of innovation decisions and thus contribute to explaining family firm heterogeneity (Chua et al., 2012). Second, family involvement in top management is a key way how families exercise influence in their firms (Tretbar et al., 2016). Therefore, studying how family involvement relates to firm innovation may reveal new theoretical insights on the role of families in shaping their firm’s future trajectory. Finally, given the need for family firms to continuously innovate (e.g., Röd, 2016), we expect that our study yields useful guidance for family firms on how to set up their top management for achieving organizational ambidexterity as a prerequisite for high firm performance (Stubner et al., 2012).

To theoretically address the question of how family involvement in top management affects exploration, exploitation, and organizational ambidexterity, we build on diversity research and propose that the so far inconclusive results can be disentangled by considering curvilinear effects. Diversity research (e.g., Harrison & Klein, 2007) has suggested that diversity in terms of individual characteristics can manifest itself in different ways with diverging outcomes. Treating family membership as an important diversity aspect in family businesses, we argue that top management teams with similar shares of family and nonfamily members (i.e., highly diverse top management) pursue lower levels of exploitation (U-shaped relationship of family involvement) because diverse opinions and viewpoints on how to achieve exploitation hinder quick decision making (separation aspect of diversity). However, top management teams with similar shares of family and nonfamily members foster exploration and ambidexterity (inverse U-shaped relationship of family involvement) because the diverse backgrounds and experiences support the novelty of innovation and help master complex tasks (variety aspect of diversity). We further argue that these relationships do not hold universally but are crucially dependent on family CEOs’ family-centered noneconomic (FCNE) goals as nonfinancial goals have been found to affect family firm innovation (e.g., Chrisman & Patel, 2012; Patel & Chrisman, 2014) and might also affect how diversity is perceived in the firm. Specifically, we propose that high levels of FCNE goals exacerbate the proposed U-shaped relationship between family involvement and exploitation and weaken the proposed inverse U-shaped relationships between family involvement and both exploration and organizational ambidexterity because CEO FCNE goals induce fault lines between family and nonfamily top managers (disparity aspect of diversity). We test our hypotheses on a sample of 109 German family-managed firms and find support for most of our hypotheses.

We contribute to literature in at least three ways. First and foremost, we advance the literature on innovation and organizational ambidexterity in family firms by revealing curvilinear effects of family involvement. This might explain the inconsistent conclusions regarding the potential firm-level outcomes of family involvement in top management because prior studies have almost exclusively focused on linear effects (Tretbar et al., 2016). Moreover, our investigation of family involvement in top management as an antecedent of exploration, exploitation, and organizational ambidexterity furthers the discussion on explaining heterogeneity in family firm innovation (Chua et al., 2012) as it reveals why some family firms might be more or less innovative. Specifically, our study suggests that family firms make different types of innovation decisions depending on whether their top management consists predominantly of family or nonfamily members or has similar shares of family and nonfamily members.

Second, we make a contribution by studying family CEOs’ FCNE goals as a moderator in the aforementioned relationships. Specifically, we contribute to research on FCNE goals (Chrisman et al., 2012) as we reveal their role in bringing disparity within top management to the surface and confirm their importance as a contingency factor in decision making. We thereby theoretically link family CEOs’ FCNE goals to the scholarly debate on emerging fault lines in the management of family firms (Thatcher & Patel, 2012).

Third, we contribute to family firm research by introducing the diversity concepts of variety, separation, and disparity (Harrison & Klein, 2007). These concepts might help elucidate important family firm decisions and advance knowledge about the circumstances under which family involvement in top management (Tretbar et al., 2016) leads to desirable or undesirable outcomes, such as high or low levels of innovation. So far, research on diversity and research on family firms have largely been developed in parallel. With our study, we integrate both research streams; in particular, we introduce “family membership” as a relevant facet of diversity and theorize on the circumstances that bring different diversity aspects to the surface.

Our findings are also important for practice, in particular for family CEOs and their advisors. We reveal that the choice of hiring additional family versus nonfamily top managers should depend on the family CEO’s goals, the current top management constellation, as well as the firm’s strategic needs.

Theoretical Background

Organizational Ambidexterity and Exploratory Versus Exploitative Innovation in Family Firms

Organizational ambidexterity is defined as the simultaneous pursuit of exploratory and exploitative innovation by firms (Raisch & Birkinshaw, 2008). Research on general management and innovation has dedicated much time and effort to investigating the antecedents and outcomes of organizational ambidexterity (Gibson & Birkinshaw, 2004). Most important, researchers almost unanimously agree about the positive linkages between organizational ambidexterity and firm performance as exploitation allows firms to harvest immediate profits, while exploration sets the path for being competitive in the future (Gibson & Birkinshaw, 2004; Lubatkin et al., 2006). Focusing solely on exploitation can lead firms to support only short-term improvement projects (Raisch & Birkinshaw, 2008), thus diminishing their potential to detect and harvest growth opportunities that are necessary for long-term survival (March, 1991). An excessive focus on exploration at the cost of exploitation, however, can be detrimental to performance as firms run the risk of getting stuck in a cycle of unremunerated search and experimentation and being kept in endlessly ongoing change (Burgers et al., 2008; Raisch & Birkinshaw, 2008). Therefore, simultaneous engagement in exploration and exploitation can significantly benefit firm performance, particularly in family firms (Moss et al., 2014). For long-term survival, family firms need to engage in both exploration and exploitation—that is, they need to strive for organizational ambidexterity (Riviezzo et al., 2015). 1

With regard to the drivers of organizational ambidexterity, researchers have studied a multitude of antecedents at the firm, team, and individual levels (Chang & Huang, 2012; Jansen et al., 2008) as organizations often find it challenging to achieve ambidexterity given the substantially different tasks and activities related to exploration versus exploitation. This literature has revealed that top management plays a particularly vital role in steering ambidexterity (e.g., Alexiev et al., 2010; Kammerlander et al., 2015) as top managers make strategic decisions regarding exploration and exploitation (Cao et al., 2010) and distribute resources within their organizations accordingly (Güttel & Konlechner, 2009). For instance, research has shown that providing external knowledge fosters decisions to develop organizational ambidexterity (Gupta et al., 2006), and Lubatkin et al. (2006) revealed that a firm’s organizational ambidexterity is enhanced by behavioral integration in top management decision making. Other studies have shown that CEOs’ networks positively affect strategic decisions that promote ambidexterity, particularly in the case of effective communication with other top management members (Cao et al., 2010). Also, CEOs’ leadership style can positively affect ambidexterity when it demonstrates a focus on both adaptability and alignment (Gibson & Birkinshaw, 2004). In sum, the internal processes that influence top management decision making are a key determinant of firms’ pursuit of ambidexterity (O’Reilly & Tushman, 1997).

Given family firms’ transgenerational intentions and thus their focus on long-term survival, organizational ambidexterity is also of utmost importance to family firms (McAdam et al., 2010; Miller & Le Breton-Miller, 2006). Moreover, research on family firm innovation has suggested that their idiosyncratic goals (Kammerlander & Ganter, 2015), structures (Duran et al., 2016), and resources (Carnes & Ireland, 2013) render innovation in family firms different from innovation in other firms (e.g., De Massis, Frattini, et al., 2015). In particular, their focus on noneconomic, “family-centered” goals encourages family firm decision makers to engage in idiosyncratic innovation decisions that aim to ensure the survivability of family firms (Chrisman & Patel, 2012). For instance, family firms have been found to prefer exploitative innovation when firm performance exceeds aspiration, yet turn to exploration in case of performance below aspiration levels because of the socioemotional wealth tied to firm ownership over generations (Patel & Chrisman, 2014). As a consequence of such evidence, De Massis et al. (2019) argue that FCNE goals might be an important factor influencing innovation. Moreover, researchers have found that exploration and exploitation in family firms are related to firms’ long-term orientation (Lumpkin et al., 2010), stewardship behavior, and reduced agency costs (Miller & Le Breton-Miller, 2006). Taken together, these studies suggest that family-specific goals and motivations play an important role in understanding innovation decisions in family firms.

With regard to the simultaneous pursuit of exploration and exploitation, qualitative research in the tourism industry has revealed that “family firms apply ambidexterity in a completely different way than do their [nonfamily] counterparts” (Röd, 2016, p. 198, referring to Weismeier-Sammer, 2014). However, despite this relevance, research on organizational ambidexterity in family firms is rather scarce (e.g., Allison et al., 2014; Moss et al., 2014). While some researchers have argued for and empirically revealed increased levels of organizational ambidexterity in family firms compared with other types of firms (e.g., Lubatkin et al., 2006; Stubner et al., 2012), others have proposed a negative relationship between family involvement and ambidexterity as well as high levels of heterogeneity among family firms with regard to their ambidexterity (Hiebl, 2015). In sum, this body of research not only highlights the idiosyncrasies of family firms’ exploratory, exploitative, and ambidextrous behavior but also reveals substantial heterogeneity among family firms.

Top Management in Family Firms and Family Firm Innovation

Prior research on family firms has focused significant attention on investigating the consequences of family involvement in top management (Arzubiaga et al., 2019; D’Allura, 2019), specifically the proportion of family managers in top management. For example, a literature review by Tretbar et al. (2016) revealed that family involvement in top management is an important source of heterogeneity among family firms (Chua et al., 2012). Interestingly, however, scholars have argued that the effects of family involvement on firm-level outcomes can be positive as well as negative depending on whether family managers are regarded either as beneficial stewards who provide unique resources (Liang et al., 2014) or as “untalented offspring” promoted due to nepotistic preferences (Schulze et al., 2003). For instance, family involvement in top management might reduce conflicts stemming from agency problems (Duran et al., 2016) and increase the number of top managers who are highly committed to the firm (Zahra et al., 2007), and it drives firms’ contract design (Cruz et al., 2010), knowledge sharing (Zahra et al., 2007), and financial performance (Minichilli et al., 2010). In contrast, other scholars have argued that a high level of family involvement leads to negative consequences, such as more relational conflicts (Kellermanns & Eddleston, 2006) and lower acquisition of external knowledge (Kraiczy et al., 2014). Although research on family involvement in top management as an antecedent of innovation is still scarce (Arzubiaga et al., 2019), Kraiczy et al. (2014) revealed that having fewer nonfamily managers is associated with less external knowledge and thus leads firms to introduce fewer new products.

Interestingly, scholars have recently started to provide arguments about potential nonlinear relationships between family involvement in top management and firm-level outcomes, thereby acknowledging that family involvement can come with both advantages and disadvantages (Bauweraerts & Colot, 2017; Liang et al., 2014; Mazzola et al., 2013; Sciascia & Mazzola, 2008). For instance, research has found an inverse U-shaped relationship between family involvement and firm performance (Chirico & Bau, 2014; Patel & Cooper, 2014).

Diversity Research as a Theoretical Basis for Understanding Family Firm Innovation

Management and innovation research has increasingly investigated the question of how diversity within top management, such as gender-, education-, and tenure-related diversity (Bantel & Jackson, 1989; Dezsö & Ross, 2012; Heyden et al., 2017), affects innovation (Talke et al., 2011). We extend this emerging debate by proposing family membership as an important facet of diversity in family firms. This is a reasonable amendment because family members who are part of top management generally have different experience and goals than nonfamily members (De Massis, Kotlar, et al., 2015; Miller et al., 2014), and their family-specific goals are likely to influence their strategic decisions. Research has repeatedly produced ambiguous results regarding the effects of diversity on organizational outcomes, such as innovation in general and organizational ambidexterity decisions in particular (García-Granero et al., 2018). While the debate is still ongoing, research seems to converge on the idea that diversity benefits creative tasks (Mello & Rentsch, 2015; Milliken & Martins, 1996; Shin et al., 2012) but hampers routine tasks (Mansoor et al., 2013; Watson et al., 1993).

To advance the theoretical debate on how diversity affects organizational decisions and outcomes, Harrison and Klein (2007) conceptualized three different aspects of diversity: variety relates to the effects stemming from differences in knowledge and experience among members, separation refers to the outcome of variance in opinions and attitudes, and disparity is closely tied to the effects of differences in status. Variety has mostly been associated with beneficial diversity outcomes, whereas separation and disparity have generally been linked to negative organizational outcomes (Harrison & Klein, 2007). While Harrison and Klein mostly associated the three forms of diversity with various different measures or facets of diversity (e.g., tenure is associated with separation and educational background is associated with variety), we explicitly advance the idea that also one facet of diversity—such as the percentage of family members in top management—can be associated with how salient different forms of diversity are when top management makes innovation decisions depending on the activities required for the specific decisions. Hence, we propose that family membership diversity has different effects on firms’ decisions to pursue exploration versus exploitation versus organizational ambidexterity activities and that these effects also depend on the family CEO’s goals.

Development of Hypotheses

We first propose that for top management decisions to pursue exploration, the variety aspect of diversity is particularly salient. The goal of exploration is to come up with new ideas, products, services, and processes, which requires the integration of various knowledge, expertise, and “out-of-the-box” thinking (Goel & Jones, 2016; Taylor & Greve, 2006). To achieve this goal, managers need to contribute their diverse expertise, experience, and network ties (Argote & Ingram, 2000; Harrison & Klein, 2007), which highlights the beneficial nature of variety within top management when making such strategic decisions. For example, based on arguments from information processing theory (Ashby, 1956), scholars have theorized and empirically revealed that greater variety leads to more creativity (Jackson et al., 1995) because different pieces of knowledge can be combined (Austin, 2003) to generate new ideas. Thus, it appears that the variety aspect of diversity within family firms’ top management is particularly salient for making exploration decisions.

Having similar shares of family and nonfamily top managers might provide such variety in decision input regarding how the firm should pursue exploration. While both family and nonfamily top managers should be motivated to propel exploration and thus ensure long-term firm survivability (Diaz-Moriana et al., 2019), they might address exploration from different angles and provide heterogeneous—that is, diverse—resources. For example, family top managers’ decisions are often guided by a deep understanding of the firm’s history and values (McConaughy et al., 2001) and thus tacit knowledge about the firm, its customers, and its industry (Cabrera-Suárez et al., 2001). In contrast, nonfamily members might bring expertise from various industrial and geographical contexts as they often have diverse professional backgrounds and provide an outsider perspective (De Massis, Kotlar, et al., 2015; Hiebl, 2015; Miller et al., 2014), which enables them to search for broad sets of external exploration stimuli (Lazzarotti & Pellegrini, 2015).

Given this heterogeneity regarding approaches to exploration, we argue that family membership diversity in top management—that is, top management with similar shares of family and nonfamily members—is associated with higher levels of exploration. If top management consists of only family managers, the firm’s exploration approaches are likely missing the external perspective provided by nonfamily managers; thus, there is little variety within top management to inform exploration decisions. As more nonfamily managers are added to top management, increasingly more variety can be harnessed to inform exploration decisions as the firm can come up with exploration ideas based on both family and nonfamily perspectives. A maximum of exploration is reached when top management consists of similar numbers of family and nonfamily managers given that both perspectives are equally considered in exploration decisions. If nonfamily members dominate top management, exploration decisions are likely mainly influenced by external nonfamily approaches, thus neglecting the family firm’s specifics, and agreement on decisions to pursue exploration that fit the family firm likely decreases. Hence, we propose the following:

In contrast to the specific activities related to exploration decisions, we argue that activities related to exploitation make the separation aspect of diversity more salient for such innovation decisions. Exploitation is related to an organization’s efforts to build on knowledge that already exists within the firm (Levinthal & March, 1993) and is driven by decision makers’ desire to achieve efficiency gains. While exploration, as discussed above, benefits from the creative combination of various perspectives, to succeed in the “routine task” of improving efficiency for exploitation, managers must make fast and effective decisions. Such fast decisions need to be based on shared opinions and quickly reached consensus within the team about how exploitation should be carried out—for example, through process innovations, cutting costs, or reducing product features. Hence, rather than the variety aspect that comes into play for creative tasks (e.g. exploration), we expect the separation aspect, which likely dominates in case of routine, efficiency-driven aspects requiring fast action, comes to the fore for exploitation decisions.

The separation aspect of diversity, however, emphasizes that in diverse teams, diverging opinions and attitudes often cannot be resolved (Harrison & Klein, 2007). For example, using arguments from theory on intergroup conflict and on self-categorization (Tajfel & Turner, 1979), researchers have argued that when separation arises, fault lines occur between the diverse subgroups involved such that diversity is accompanied by less cohesion and more conflicts, ultimately leading to decreased task performance (Harrison & Klein, 2007). Indeed, each subgroup might insist on its own opinion and approach and defend them against the opinions and approaches put forward by the other subgroup(s). That is, when family firms make decisions about the exploitation activities they should pursue, the separation aspect of diversity within top management may be particularly salient and may in turn be detrimental to exploitation.

Both family and nonfamily top managers are generally motivated to engage in exploitation, but they tend to have different motivations and take different approaches. Family top managers tend to support exploitation because it typically increases product quality and hence firm reputation (Patel & Chrisman, 2014) and because exploitation can contribute to family firms’ long-term transgenerational intentions (Zellweger et al., 2012). However, nonfamily top managers likely engage in exploitation because their bonuses are frequently tied to achieving short-term goals (Hall & Nordqvist, 2008). Therefore, nonfamily managers likely focus on measures such as cost efficiency, which run counter to the attitudes and values of many family top managers (Block, 2011), leading to separation of the two groups.

Based on these considerations, we argue that having similar shares of family and nonfamily members in top management likely impedes exploitation decisions because the separation aspect of diversity dominates. Due to family top managers’ similar approaches to exploitation, top management consisting of only family members and thus little separation likely find effective and efficient ways to decide which exploitation measures should be implemented. However, with each nonfamily member added to top management, potential separation within the team becomes more salient because there are likely more controversial discussions about which approach to follow for effective and efficient exploitation. For instance, family managers tend to refrain from short-term cost cuts (e.g., downsizing) that harm the firm’s long-term competitive advantage or reputation (Block, 2011), while nonfamily managers likely pursue such cuts because they were trained in such activities in their prior professional careers (Sonfield & Lussier, 2009). Moreover, family managers are likely emotionally attached to the firm and thus reluctant to divest core or traditional business units (Miller & Le Breton-Miller, 2005) to enhance exploitation, while nonfamily managers, due to their lack of shared history with the firm, often do not have such emotional attachment and are instead focused on their job market value outside the family firm (Block, 2011).

While heterogeneity in top managers’ perspectives likely increases the creativity of solutions in the case of exploration, we expect a detrimental effect in the case of exploitation, as it requires efficiency and consistency rather than creativity. Due to the potential conflicts and fault lines that may emerge when family and nonfamily top managers try to agree on specific exploitation paths, we argue that the separation aspect of diversity is particularly influential on exploitation decisions. Specifically, we expect top management with similar shares of family and nonfamily managers to pursue the least exploitation. Hence, a “turning point” (Haans et al., 2016) with minimum levels of exploitation is likely reached when there are similar shares of family and nonfamily managers with diverging attitudes and opinions. When nonfamily members outnumber family members in top management, exploitation decisions are likely made again more smoothly, leading to more exploitation, the smaller the ratio of family managers as opposed to nonfamily managers. In sum, we propose the following:

Organizational ambidexterity can only be achieved when different activities and tasks—namely, those related to both exploitation and exploration—are carried out simultaneously. This simultaneous execution requires firms to move from one set of tasks to another (O’Reilly & Tushman, 2011), be aware of multiple goals at the same time, and balance resource allocation decisions between exploitation and exploration (Raisch & Birkinshaw, 2008). Due to the diverse goals and tasks managers need to consider when making ambidexterity decisions, we expect that the variety aspect of diversity is highly salient for these decisions. Therefore, because “heterogeneous teams can [tackle] complex competitive challenges and uncertain contexts” (Ferrier, 2001, p. 862, as cited in Harrison & Klein, 2007), we propose that diversity within top management can facilitate decisions to pursue organizational ambidexterity.

Specifically, we suggest that diversity in the form of top management with similar shares of family and nonfamily top managers leads to increased levels of organizational ambidexterity. Top management teams consisting solely of family members might be effective in pursuing exploitation but might lack the diverse perspectives needed to achieve exploration. In addition, they likely face problems in addressing the variety of opinions perspectives and combining exploration and exploitation. That is, these teams are unlikely to decide to pursue a high level of organizational ambidexterity; rather, they are likely to focus on exploitation alone. With each additional nonfamily top manager, not only does the perspective on exploration broaden, but the variety of perspectives needed to combine exploration with exploitation and pursue ambidexterity also increases. This increase continues until, in teams with similar numbers of family and nonfamily managers, full exploration and ambidexterity are realized.

Importantly, although we argued above that exploitation is generally lowest in top management teams with similar shares of family and nonfamily members, when deciding about the simultaneous pursuit of exploration and exploitation, top management might split the different tasks associated with exploration and exploitation and delegate responsibilities. For example, each member of top management might rely on his or her specific network (Cao et al., 2010), competencies, and personal preferences to conduct assigned tasks and contribute to organizational ambidexterity. In other words, when making decisions related to their ambidextrous innovation strategy, top management with similar shares of family and nonfamily members might assign certain members to exploitation tasks and certain members to exploration tasks, thereby maximizing the benefits of the variety aspect of diversity (by including the maximum variance of ideas and perspectives into exploration discussions) and minimizing the hazards of the separation aspect of diversity (by constraining related discussions to a team of aligned experts). Hence, we propose the following:

The effects of family involvement in top management on family firms’ exploration, exploitation, and organizational ambidexterity might not be equal for all family firms. Indeed, prior family firm research has emphasized that family firms differ with regard to the emphasis family CEOs put on “family” aspects in their decision making (Berrone et al., 2012) and that such focus on nonfinancial goals might affect their innovation behavior (Chrisman & Patel, 2012; Patel & Chrisman, 2014). To theoretically and empirically spur this scholarly debate, researchers have recently developed the concept of FCNE goals, referring to goals pertaining to the family’s values, attitudes, and intentions (Chrisman et al., 2012). 2 In particular, FCNE goals might affect the relationship between family involvement in top management and ambidexterity as the “exploration and exploitation of family businesses may incorporate elements of . . . family-centered, noneconomic goals” (Goel & Jones, 2016, p. 110). Since CEOs are particularly influential on the decisions made by the top management (Hambrick & Mason, 1984) and family CEOs are known to have a major influence on the family firm’s future trajectory and performance (Duran et al., 2016; Miller & Le Breton-Miller, 2006; Minichilli et al., 2010), we argue that the above derived hypotheses are contingent on family CEOs’ FCNE goals as such goals might give rise to another aspect of diversity: disparity, which denotes status differences between different groups and individuals among top management.

Specifically, we propose that CEOs’ FCNE goals can trigger the salience of disparity between family and nonfamily members within firms’ top management. FCNE goals are focused on one part of family firms’ top management (i.e., family members) but disregard another part of top management (i.e., nonfamily members). Hence, we argue that when family CEOs have strong FCNE goals, family top managers are likely endowed with a specific status (i.e., are included in the scope of the CEO’s attention), while nonfamily top managers might be viewed as belonging to a “lower” status group (i.e., outside the CEO’s attention). Indeed, disparity occurs in groups if some but not all members are “socially valued or [possess a] desired resource” (Harrison & Klein, 2007, p. 1206), such as belonging to the group of individuals the family CEO focuses on when making strategic decisions. Because of such asymmetric treatment, fault lines might occur between family and nonfamily managers (Thatcher & Patel, 2012), leading to conflicts within top management. 3

With regard to exploration, we expect that disparity induced by family CEOs’ focus on FCNE goals impedes the combination of various expertise and knowledge that fosters exploration decisions in the absence of FCNE goals. Hence, disparity likely mitigates the positive benefits of having diverse teams by segregating top management into two groups that do not openly share ideas and information (Harrison & Klein, 2007). Furthermore, family CEOs’ emphasis of FCNE goals, and the resulting disparity, creates an environment that allows family managers to free ride and shirk (Chrisman et al., 2004), which acerbates inequality in top management (Chua et al., 2012). Therefore, family CEOs pursuing FCNE goals are likely to select and implement exploration ideas that concur with their own family-focused preferences and to disregard approaches proposed by out-group members—that is, by nonfamily managers. In other words, strong CEO FCNE goals likely diminish the positive effects of diverse top management on exploration decisions. Thus, we assume that the proposed inverse U-shaped relationship between family involvement in top management and exploration is less pronounced (i.e., flattened) in the case of strong CEO FCNE goals.

Regarding exploitation, we suggest that the negative effects of diversity-related separation might be even stronger in the case of strong CEO FCNE goals. When pursuing strong FCNE goals in strategic decision making, family CEOs might disregard the input and suggestions of nonfamily managers who confront family managers’ attitudes and opinions. As intergroup conflict and self-categorization lead to decreased task performance (Harrison & Klein, 2007), the negative effects of family membership diversity on exploitation may even be strengthened when CEOs have a strong focus on FCNE goals. Especially when top management consists of similar shares of family and nonfamily members (i.e., a high level of diversity), family members might oppose suggestions from nonfamily members, which can in turn lead to fault lines that cause inertia in strategic decision making. Therefore, we assume that the proposed U-shaped relationship between family involvement in top management and exploitation is strengthened with stronger CEO FCNE goals.

Last, with regard to organizational ambidexterity, salient fault lines caused by FCNE goal–driven disparity perceptions might lead to increasing difficulties with delegating tasks and subsequently integrating the proposed innovation decisions. While diverse top management teams might split the various complex tasks associated with ambidexterity and delegate responsibilities accordingly to maximize the benefits of the variety aspect of diversity while minimizing the hazards of the separation aspect (see argumentation for H3), disparity and perceived in-group and out-group status by top managers can complicate and impede such effective task separation. For example, nonfamily managers might refuse to work constructively with family managers on exploration-related issues even though the diverse perspectives of both are needed for effective exploration decision making. Indeed, the already complex pursuit of exploration and exploitation in parallel might be substantially disturbed in case of status differences and feelings of injustice that emerge from disparity perceptions induced by high levels of CEO FCNE goals. Hence, we formally suggest that strong FCNE goals pursued by family CEOs weaken the positive effects of diversity-based variety on organizational ambidexterity decisions. In other words, the proposed inverse U-shaped relationship between family involvement in top management and ambidexterity is less pronounced in the case of strong FCNE goals as the emerging disparity diminishes the benefits of variety. We therefore propose the following:

The inverse U-shaped relationship between family involvement in top management and exploration weakens with stronger family CEO FCNE goals.

The U-shaped relationship between family involvement in top management and exploitation strengthens with stronger family CEO FCNE goals.

The inverse U-shaped relationship between family involvement in top management and organizational ambidexterity weakens with stronger family CEO FCNE goals.

Research Methods

Sample and Data Collection

To test our hypotheses, we collected data from German family firms. We used Bureau van Dijk’s Amadeus database, which lists all corporate organizations in Germany, as the basis and applied three criteria to create our sample. First, we focused on organizations with more than nine employees since we expected that most microenterprises do not pursue dedicated exploration and exploitation. The firm size definition of microenterprises is based on the European Union’s recommendation 2003/361/EG. Second, we excluded organizations from public and financial sectors since we did not expect such firms to significantly engage in exploration. Third, we filtered for all firms with at least 20% ownership by a family or an individual (La Porta et al., 1999) that were also managed by a member of the owning family (family CEO)—a definition frequently used in comparable studies of family firms (Cruz et al., 2010). The focus on firms with family CEOs is necessary due to our aim to study the important contingency effects of family CEOs’ FCNE goals (Hypotheses 4a, 4b, and 4c). La Porta et al. (1999) argued that 20% ownership (voting rights) is usually sufficient to exercise effective control of a firm, which is a prerequisite for a family CEO’s FCNE goals to influence top management’s strategic decisions. Overall, our sampling strategy is consistent with studies conceptualizing family influence in terms of ownership and management (Chrisman et al., 2012; Cruz et al., 2010). The list resulting from our sampling strategy contained about 37,000 firms, from which we drew a random sample of 949 family-owned and family-managed firms for which we had complete contact information.

We contacted all these firms via personal letters and follow-up phone calls after 1 week. We explained that our study focuses on family firm–related topics, thus ensuring participants felt comfortable characterizing their firms as “family firms.” This approach enabled us to focus on (first- and later-generation) family firms, excluding lone-founder firms. For each firm, we asked for the participation of the family CEO, additional family members employed at the firm, and nonfamily employees with direct contact to the family CEO. To encourage participation, we offered firm-specific feedback packages containing empirical results and benchmarking data. A total of 118 firms agreed to participate on contact, representing a response rate of 12.4%, which is similar to other survey-based family firm studies, such as Zellweger et al. (2012; 14.3%) and Cruz et al. (2010; 11%). The response rate is also consistent with the 10.3% reported by the Arthur Andersen Center for Family Business’s survey, which has been used by several scholars in academic articles on family firms (e.g., Schulze et al., 2003). Excluding surveys with incomplete answers as well as micro enterprises, the final sample included 109 firms.

Our study is primarily based on the analysis of data provided by family CEOs, resting on the assumption that family CEOs were best able to provide the information required for this study. This key-informant approach is in line with comparable prior family firm and exploration/exploitation studies (e.g., Dehlen et al., 2014; Kammerlander et al., 2015). We first gathered information on the outcome variables, exploration and exploitation, and the predictor variable, family involvement in top management (cross-checked with secondary data, see below). In a second questionnaire sent 7 days after the first (and answered, on average, within 16.6 days after the first questionnaire), we collected information on family CEOs’ FCNE goals.

CEOs who responded to our questionnaires were, on average, 51.8 years old and had worked in their firm for 20.8 years. Eight CEOs were female (7.3%), and 78.0% of the CEOs held a university (or comparable) degree. Top management teams consisted of 2.6 members on average, which is comparable with similar studies in the family firm context (Chrisman et al., 2015—average number of top management members = 3.4; Kraiczy et al., 2015—average number of top management members = 2.6) and is reasonable as approximately 50% of the sample firms had fewer than 100 employees. The largest top management team consisted of six members, and 17 top managements consisted only of the family CEO. Robustness checks excluding these 17 cases (reported below) confirm the results of the main models. Family members constituted 76% of top management on average. According to the Standard Industrial Classification (SIC), the firms in our sample were mostly from manufacturing (80.7%), consistent with the fact that German industry is dominated by this sector. Furthermore, 3.7% of firms were from construction, 0.9% were from mining, 4.6% were from wholesale, 3.4% were from retail, 0.9% were from transportation, and 5.5% were from services. The firms were, on average, 90.1 years old at the time of data collection and had average revenues (2013) of 55.2 million euros.

Nonresponse Bias

To analyze the possibility of nonresponse bias, we systematically checked for differences between survey respondents and nonrespondents. First, we tested for differences between early and late respondents regarding the explanatory variables (family involvement in top management and CEO FCNE goals) with a one-way analysis of variance (ANOVA), assuming that late respondents were more similar to nonrespondents than to early respondents (Oppenheimer, 1966). We compared both (1) the subsample that completed the survey at a later date (later 50%) with the subsample that completed the survey at an earlier date (earlier 50%) and (2) the subsample that completed Part 2 of the survey within a shorter time interval (shorter interval 50%) with the subsample that completed Part 2 of the survey within a longer time interval (longer interval 50%). There is only a slight indication of potentially higher CEO FCNE goals for nonrespondents (one-way ANOVA probability > F = .03). A subsample comparison of the earliest 30% with the latest 30% yields no indication of nonresponse bias for CEO FCNE goals (one-way ANOVA probability > F = .20).

Second, we tested the representativeness of our sample by comparing the basic firm characteristics (e.g., revenues, number of employees, and firm age) of the participant firms to those of the 949 non–micro-German family firms with family CEOs that we initially contacted for our study. The responding firms in the sample were larger both in terms of revenues and number of employees as well as older than the overall sample. This difference is reasonable since the respondent sample comprised only those firms that were comfortable being characterized as family firms. In our phone calls, many younger and even newly founded firms perceived themselves as owner managed rather than as family managed. Being at an earlier stage, these firms frequently had fewer employees and lower revenues than established family firms. Hence, this comparison suggests that our findings are especially applicable to later-stage family firms and do not necessarily generalize to earlier-stage family firms.

Common Method Bias

Although common method bias is typically not a major problem when the key variable is demographic and nonsubjective (e.g., proportion of family members in a firm’s top management; Schulze et al., 2003), we took several ex ante precautions in the data collection process and performed further ex post analyses. First, we ensured full data confidentiality to participants to decrease tendencies to answer the questionnaires in a socially desirable way and administered the questionnaire items in a randomized order so that respondents could not draw conclusions regarding the hypotheses (Podsakoff et al., 2003). Second, we used a temporally separated approach to measure the variables (Podsakoff et al., 2003).

Third, we collected data from additional family managers employed in the firms (49 family managers from 41 firms, equaling 37.6% of participating firms) to mitigate concerns related to single-respondent bias (e.g., Eddleston & Kellermanns, 2007; Zellweger et al., 2012). When additional family managers replied for a given firm, we used their average rating for analysis. Specifically, FCNE goals were rated not only by the family CEO (M = 4.94; SD = 1.24) but also by additional family managers (M = 5.03; SD = 1.45). The ratings by the family CEO and by additional family managers employed in the firm are significantly and positively correlated (r = .44, p ≤ .01). 4 In further analyses, we relied on family CEOs as key informants (Eddleston, 2008) and used their responses.

Fourth, we validated CEO-provided information regarding top management composition with secondary data from the firm databases (Hoppenstedt and Amadeus), newspaper articles, company press releases, and releases in the German Federal Gazette (Bundesanzeiger). 5 For the few observations for which CEO information and secondary data deviated, we chose CEO information as the CEO’s perception of who is part of top management decision-making processes outweighs potentially incorrect secondary information (Miller et al., 2013).

Fifth, we conducted both an explanatory factor analysis and two confirmatory factor analyses (CFAs) to analyze relationships between the measured items (Hair, 2010; Podsakoff et al., 2003). For the explanatory factor analysis, all items of the respective full model were entered into a factor analysis. The analysis revealed greater than or equal to six factors with eigenvalues greater than 1 for all models, accounting for the better part of the cumulative covariance, while the largest individual factor accounts for less than a quarter of the covariance. This finding supports the conclusion that no single dominant factor explains the covariance in either model (Podsakoff & Organ, 1986). For the CFAs, we first built a “trait model” for each of the dependent variables, wherein we included all items of the independent, moderator, and dependent variables and let them load on their respective constructs while allowing the constructs to correlate (Podsakoff et al., 2003). The goodness-of-fit indices, root mean square error of estimation and standardized root mean square residual, are below 0.1, indicating good model fit for both the exploration and the exploitation models (Steenkamp & Baumgartner, 1998). Correspondingly, the comparative fit index and Tucker–Lewis index are very close to or above the acceptance level of 0.9 for both interactions and models (Steenkamp & Baumgartner, 1998), further supporting the notion that common method bias does not distort our results.

Finally, we aimed to use a marker variable strategy following Williams et al. (2010). Since the marker variable needs to be theoretically unrelated to any of the independent, moderator, or dependent variables, we chose CEO job satisfaction. 6 According to Williams et al. (2010), the relationships in regression models are not skewed by common method variance when the “method-R models” are not significantly different from the “method-U models” in the analysis, which is the case in our data (Δχ2 = 0.01, df = 1, ρ = 0.919 for the exploration model; Δχ2 = 0.032, df = 1, ρ = 0.574 for the exploitation model). Thus, although our marker variable is not perfect, the analysis indicates that the relationships examined in our regression models are unlikely to be affected by common method bias.

Measures

Since we relied on established scale items, all items were translated into German and back-translated into English to ensure consistency, in line with the back-translation test.

Dependent Variables

Firms’ exploration and exploitation have been analyzed with various measures in the past (e.g., He & Wong, 2004; Jansen et al., 2006; Lavie et al., 2010). We followed the approach of Jansen et al. (2006) as their scale is applicable for the broad range of industries and firm sizes comprising our sample. This scale has been used in various organizational contexts, for example, for large corporations (Jansen et al., 2009), small and medium enterprises (Alexiev et al., 2010), and organizational units (Jansen et al., 2006; Jansen et al., 2012). Exploration and exploitation were each measured using six items, with possible responses ranging from 1 (= strongly disagree) to 7 (= strongly agree). Items for exploration include “We invent new products and services” and “Our firm accepts demands that go beyond existing products and services,” while items for exploitation include “We improve our provision’s efficiency of products and services” and “We regularly implement small adaptations to existing products and services.” Subsequently, a firm’s level of exploration (exploitation) was calculated as the mean of the six items associated with exploration (exploitation). Cronbach’s alphas are .73 for exploration and .79 for exploitation, suggesting satisfactory reliability (Hair, 2010). Finally, since the dependent variable, ambidexterity, is composed of the two dependent variables, exploration and exploitation (Jansen et al., 2009), we calculated it as the product of exploration and exploitation (i.e., multiplicative operationalization), which is the dominant operationalization of organizational ambidexterity in recent high-quality management and innovation research (e.g., Cao et al., 2009; Gibson & Birkinshaw, 2004; Jansen et al., 2012; see also meta-analysis by Junni et al., 2013). We report results for additive and subtractive ambidexterity in the robustness checks below.

Independent Variable

We measured family involvement as the share of family executives in top management (i.e., dividing the number of family top managers by the total number of top managers), thereby following the operationalization of prior studies (e.g., Minichilli et al., 2010; Sciascia et al., 2013; Sciascia & Mazzola, 2008; Zahra et al., 2007). 7

Moderator Variable

CEO FCNE goals was measured using Chrisman et al.’s (2012) three-item scale, with possible responses ranging from 1 (= strongly disagree) to 7 (= strongly agree): “Family harmony is an important goal in making my business decisions,” “The social status of my family is an important factor in making my business decisions,” and “My business is closely linked to the identity of my family.” The level of CEO FCNE goals was calculated as the mean of the three items, resulting in a Cronbach’s alpha of .68, slightly below the threshold of .7 (Hair, 2010). However, the low number of items in itself can potentially lead to a lower Cronbach’s alpha (Cortina, 1993), and variables with Cronbach’s alphas between .6 and .7 have been used extensively in the literature as well as in similar studies (Shepherd et al., 2013; Zellweger et al., 2013). In fact, some research has suggested that lower Cronbach’s alphas in interaction models can lead to more conservative regression results, thereby increasing the explanatory power of the overall regression model (Aguinis, 1995). In addition, we performed an item–test correlation, measuring how individual items are correlated with the overall scale. All items are highly correlated with the overall scale (coefficients >0.77) and are thus well in excess of the sufficiency threshold of 0.35 (Everitt, 2002); dropping any item would reduce overall scale reliability. Finally, we performed CFAs to investigate whether individual items fail to ideally reflect the data. All items load on one factor, and the respective factor loadings are greater than 0.57, which is above the cutoff threshold of 0.5 (Hair, 2010). Based on these analyses, we conclude that the relatively low reliability of CEO FCNE goals is not a major concern.

Control Variables

Regarding CEO characteristics, we controlled for CEO age (in years). One could argue that older CEOs are less entrepreneurial and focus more on routine tasks than on engaging in exploration (Kammerlander et al., 2015). We also controlled for CEO gender (“0” for male and “1” for female) as masculine and feminine traits have been found to influence entrepreneurial self-efficacy, thereby potentially influencing exploration and exploitation (Mueller & Dato-On, 2008). Furthermore, we controlled for CEO level of education (“1” for bachelor degree or higher education and “0” otherwise) as higher levels of education are connected with higher levels of information search and analysis (Papadakis et al., 1998), which might lead to more exploration and better management of ambidexterity. We also controlled for CEO tenure within the firm (in years) to account for effects connected to CEO experience (Boling et al., 2016; Mom et al., 2009) as experienced CEOs might have better capabilities related to both exploration and exploitation.

Regarding firm characteristics, we controlled for firm size, measured as the natural logarithm of full-time employees, as larger firms have more available resources but are potentially less flexible and are often characterized by inertia (Jansen et al., 2006). We also controlled for prior firm performance as performance can have repercussive effects on innovation behavior (Chrisman & Patel, 2012; Patel & Chrisman, 2014). We asked respondents to assess their firm performance over the past 3 years on a 7-point Likert-type scale with the following three dimensions (shortened from Eddleston et al., 2008): (1) “growth in market share,” (2) “growth in profitability,” and (3) “return on equity.” The Cronbach’s alpha of the performance scale is .75. We also controlled for top management size, defined as the total number of top management members, as it can influence the dynamics of a firm’s decision-making behavior (Alexiev et al., 2010). Finally, we controlled for the firm industry to account for varying innovation intensity and for varying environmental dynamism in the respective sectors (Kammerlander et al., 2015). We used the major categories of the SIC, of which the following seven industries were present in the sample: mining, construction, manufacturing, transportation, wholesale trade, retail trade, and services.

Regarding family characteristics, we controlled for relationship conflict within the family as higher levels of relationship conflict are detrimental to decision quality in general (Simons & Peterson, 2000) and could thus negatively affect the consequent pursuit of both exploration and exploitation. We used the three-item relationship conflict subscale of the intragroup conflict scale developed by Jehn and Mannix (2001), which has been used and adapted to the family firm context in similar studies (e.g., Eddleston & Kellermanns, 2007). The Cronbach’s alpha for relationship conflict is .87. We also controlled for generation, measured by the item “Which generation manages your family business,” as the tendency to preserve established paths might be particularly salient in firms managed by later generations. We also controlled for the level of family ownership, measured by the item “What percentage of the firm is owned by the family,” as family ownership is essential albeit not sufficient for family influence (Chua et al., 1999).

Results

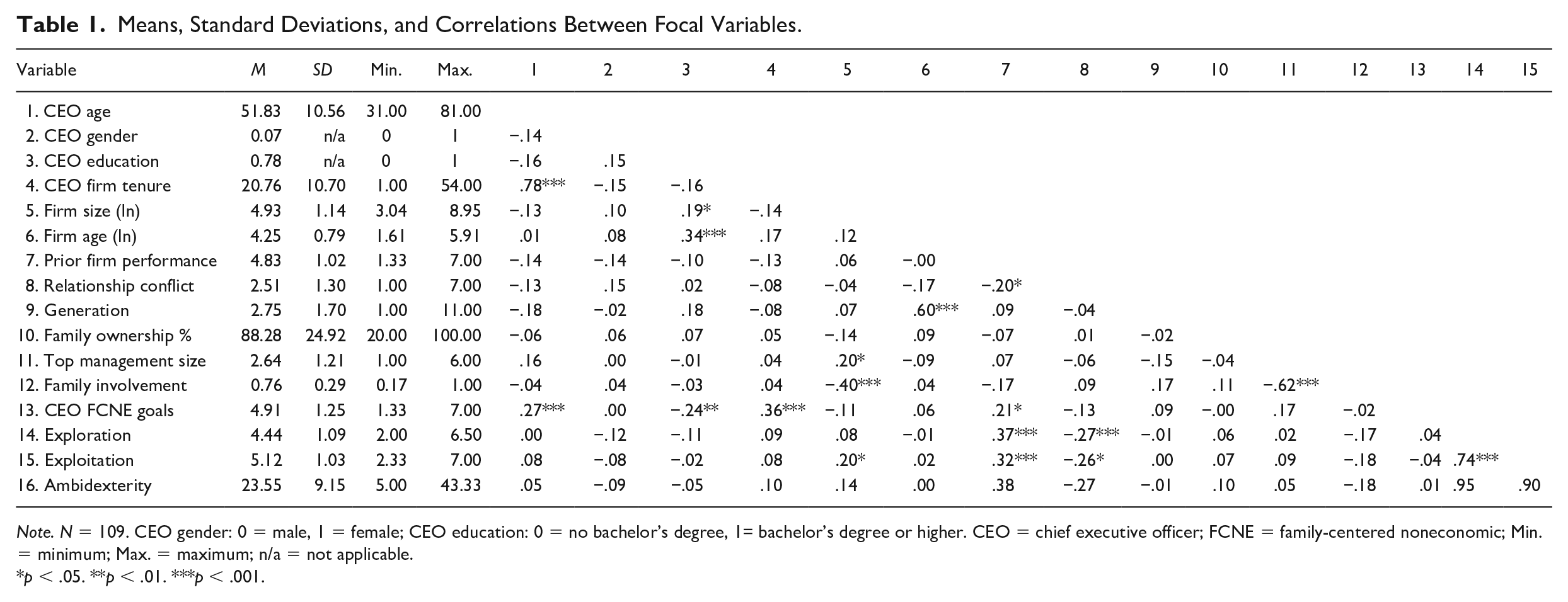

The means, standard deviations, minimum and maximum values, and Pearson correlations (two-tailed) of the variables are shown in Table 1. The bivariate correlations are mostly well below the .7 threshold (Hair, 2010). Additionally, some significant correlations, for instance, those between CEO age and CEO firm tenure, exist with the expected sign. The correlation between exploration and exploitation is positive and significant (r = .74, p < .001), in line with findings from comparable studies (e.g., Gedajlovic et al., 2012). Since significant correlations between independent variables and control variables could raise concerns about the existence of multicollinearity, we calculated variance inflation factors for the measures (Hair, 2010). All variance inflation factor values are well below the cutoff level of 10.0 (Hair, 2010).

Means, Standard Deviations, and Correlations Between Focal Variables.

Note. N = 109. CEO gender: 0 = male, 1 = female; CEO education: 0 = no bachelor’s degree, 1= bachelor’s degree or higher. CEO = chief executive officer; FCNE = family-centered noneconomic; Min. = minimum; Max. = maximum; n/a = not applicable.

p < .05. **p < .01. ***p < .001.

In the next step, we ran separate sets of regression models for the dependent variables: exploration, exploitation, and ambidexterity. Our limited sample size (N = 109) has some implications for the analysis. Specifically, given the accepted rule of thumb that regressions should draw on at least 10 observations per independent variable (1-in-10 rule, Harrell et al., 1984), we were only able to include up to 10 variables in each model. Hence, the models reported in Tables 2 to 4 include only those controls that are significant across multiple models (i.e., CEO firm tenure, prior firm performance, relationship conflict). However, we ran various alternative model specifications with alternative sets of the control variables described in the methods section, including models without control variables. Our results are robust across these alternative specifications (see summary below). Despite our extensive robustness tests, however, we admit that the rather small sample size might render our analysis exploratory to some extent.

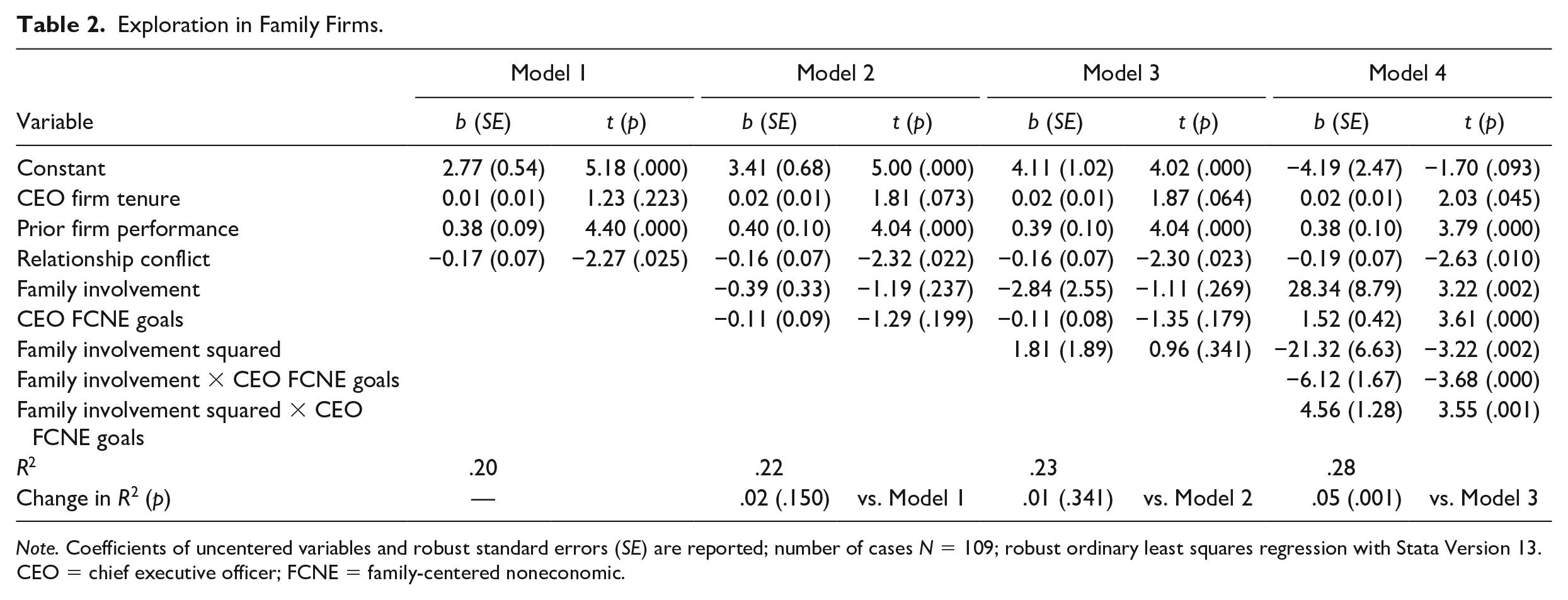

Exploration in Family Firms.

Note. Coefficients of uncentered variables and robust standard errors (SE) are reported; number of cases N = 109; robust ordinary least squares regression with Stata Version 13. CEO = chief executive officer; FCNE = family-centered noneconomic.

Family Involvement in Top Management and Exploration

In Model 1 (Table 2), we estimated the effects of the control variables, which explain a relatively large amount of the overall variance (R2 = .20). We found a positive relationship between prior performance and exploration (b = 0.38, p = .000). We also found a negative association between relationship conflict and exploration (b = −0.17, p = .025), consistent with our assumption regarding conflicts’ destructive impact on clear strategic alignment (Simons & Peterson, 2000). In Model 2, we included the direct effects of family involvement in top management and CEO FCNE goals, both showing nonsignificant associations with exploration. Consistently, the increase in the explained variance is nonsignificant (p = .150).

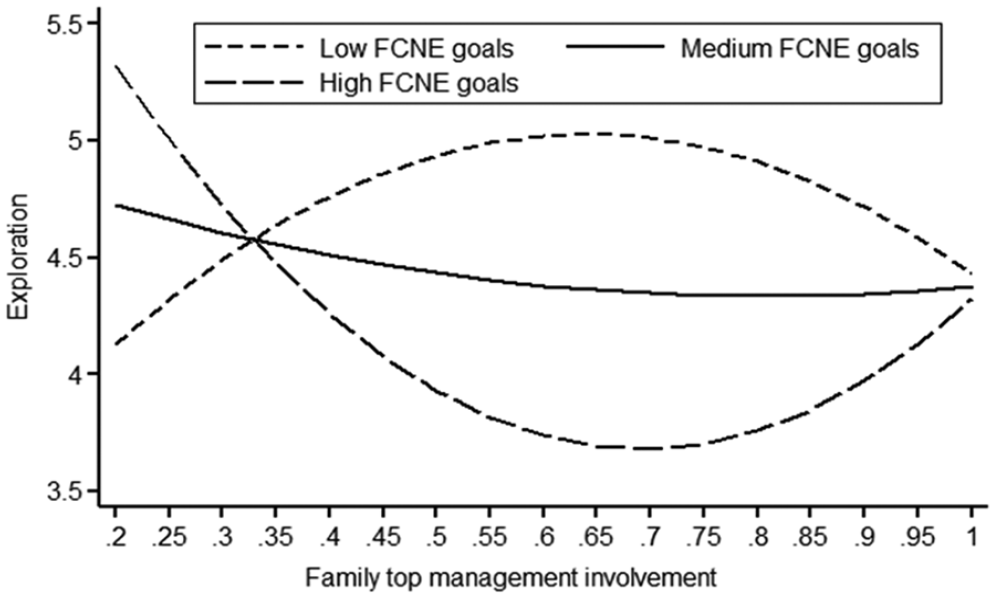

H1 predicts an inverted U-shaped relationship between family involvement in top management and exploration; thus, we included both the linear and squared terms of family involvement in top management in Model 3. We found a nonsignificant coefficient for the squared term (b = 1.81), providing no support for H1. H4a states that the proposed inverted U-shaped relationship between family involvement in top management and exploration is more pronounced when CEO FCNE goals are weak and less pronounced when CEO FCNE goals are strong. To test this hypothesis, we included the interaction terms of family involvement in top management (linear and quadratic) and CEO FCNE goals in Model 4. We found a positive and significant interaction term for family involvement in top management squared and CEO FCNE goals (b = 4.56, p = .001). The explained variance increases by 0.05. The significant nature of this increase (p = .001) underscores the relevance of the nonlinear interaction effect (e.g., Block et al., 2014). Figure 1 displays the relationship between family involvement in top management and exploration at high levels (1 SD above the mean), medium levels (mean), and low levels (1 SD below the mean) of CEO FCNE goals. The figure illustrates that the inverted U-shaped relationship becomes less pronounced as CEO FCNE goals increase, and at CEO FCNE goal values above 4.68, the curve flips to a U-shape, thus supporting H4a. This “shape-flip” effect (Haans et al., 2016) also explains the nonsignificant finding reported for H1.

CEO family-centered noneconomic (FCNE) goals, top management involvement, and exploration.

Family Involvement in Top Management and Exploitation

We first estimated the effects of the control variables in Model 5 (Table 3), which explain a significant amount of the overall variance (R2 = .16). We found a significant positive association between prior performance and exploitation (b = 0.30, p = .000), supporting arguments that past success has a positively reinforcing effect on exploitation (Patel & Chrisman, 2014). Moreover, Model 6 reveals a negative and significant effect of CEO FCNE goals on exploitation (b = −0.17, p = .028) and a significant increase in the explained variance (change in R2 = .04, p = .031).

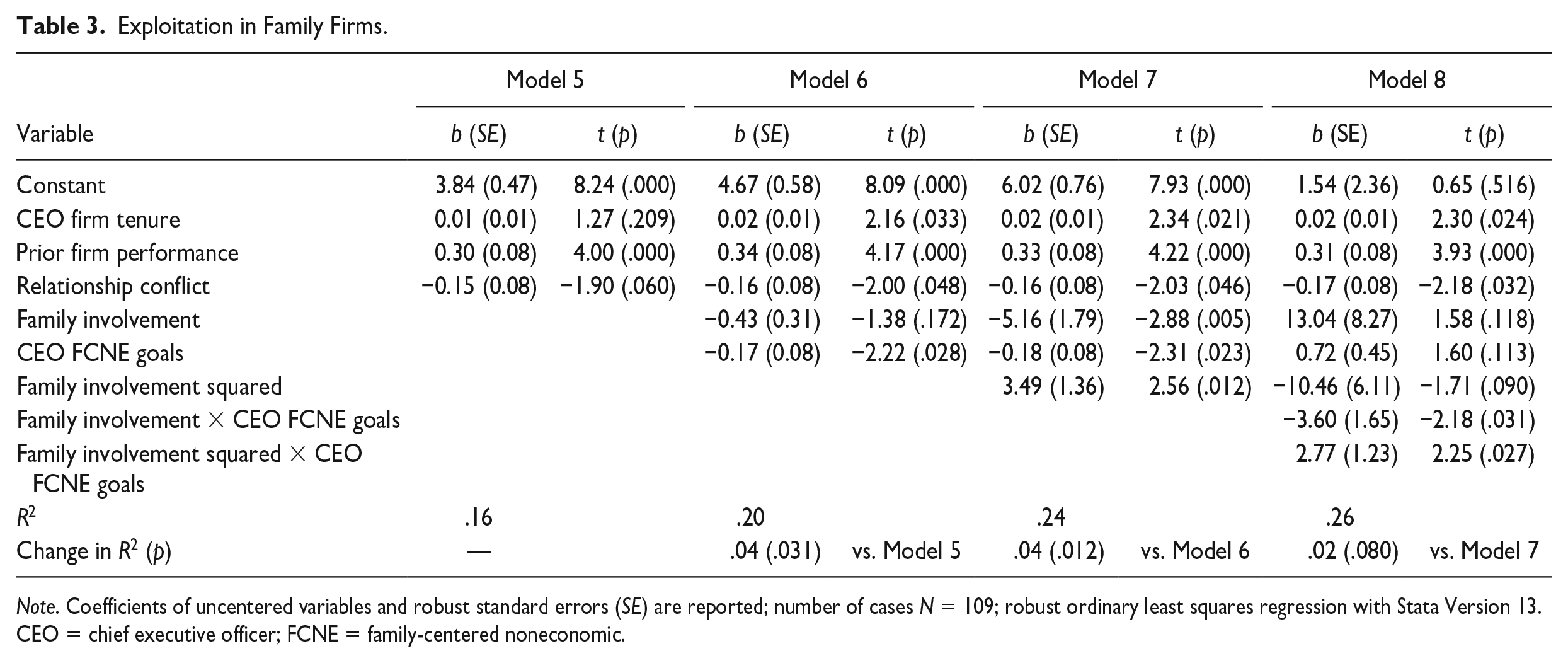

Exploitation in Family Firms.

Note. Coefficients of uncentered variables and robust standard errors (SE) are reported; number of cases N = 109; robust ordinary least squares regression with Stata Version 13. CEO = chief executive officer; FCNE = family-centered noneconomic.

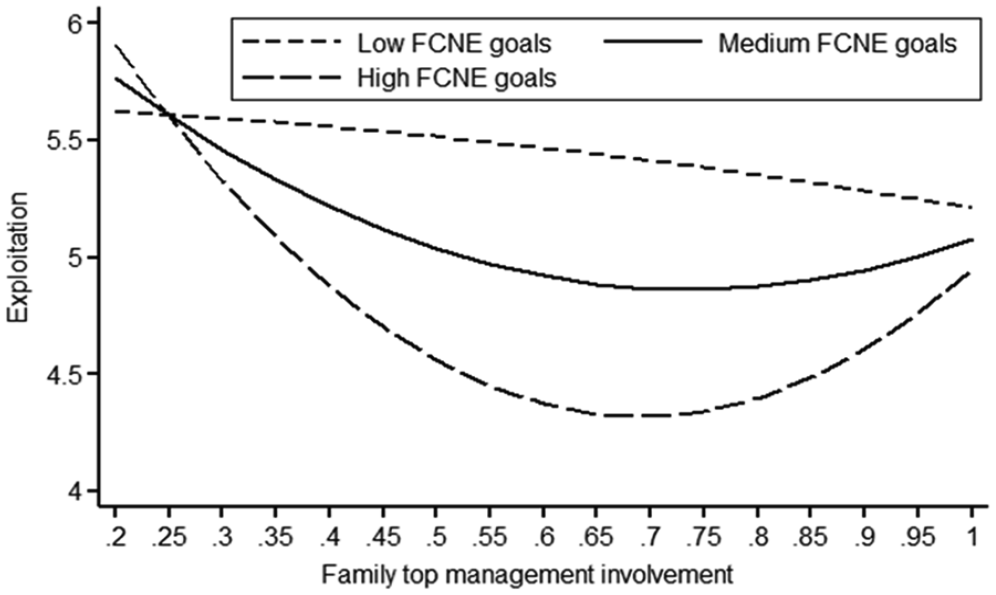

H2 predicts a U-shaped relationship between family involvement in top management and exploitation. We included the linear and squared terms of family involvement in top management in Model 7 and found, in line with our predictions, a positive and significant relationship between the squared term and exploitation (b = 3.49, p = .012). The explained variance in Model 7 increases by 0.04 compared with Model 6, and the Wald test indicates significantly increased model fit (p = .012), lending further support to the existence of a curvilinear effect (Cohen et al., 2013). We examined the curvilinear interaction effect with additional analyses (Haans et al., 2016). In particular, we found that there is a negative and significant slope (b = −4.00, p = .002) at the lower bound of the range of x-values and a positive and significant slope (b = 1.82, p = .036) at the upper bound, consistent with the U-shape. Finally, the location of the curve’s minimum and its 95% confidence interval (x = 0.74 [0.63, 0.85]) are well within the range of the x-values (minimum = 0.20; maximum = 1.00). In sum, these findings suggest a U-shaped relationship (Haans et al., 2016) between family involvement in top management and exploitation, thus supporting H2.

H4b states that the U-shaped relationship between family involvement in top management and exploitation diminishes with weaker CEO FCNE goals and strengthens with stronger FCNE goals. We included the interaction terms of family involvement in top management (linear and quadratic) and CEO FCNE goals in Model 8. We found a positive and significant interaction term for family involvement in top management squared and CEO FCNE goals (b = 2.77, p = .027). This result is illustrated in Figure 2, which displays the relationship between family involvement in top management and exploitation at high levels (1 SD above the mean), medium levels (mean), and low levels (1 SD below the mean) of CEO FCNE goals. The figure shows that stronger CEO FCNE goals steepen the U-shaped relationship between family involvement in top management and exploitation, lending support to H4b.

CEO family-centered noneconomic (FCNE) goals, family top management involvement, and exploitation.

Family Involvement in Top Management and Ambidexterity

Model 9 (Table 4) illustrates that the control variables explain a significant amount of the overall variance in ambidexterity (R2 = .20). Again, we found a significant positive association between prior performance and ambidexterity (b = 3.25, p = .000) and a significant negative association between relationship conflict and ambidexterity (b = −1.33, p = .027). Model 10 reveals a negative and marginally significant effect of CEO FCNE goals on ambidexterity (b = −1.21, p = .077) and a marginally significant increase in the explained variance compared with Model 9 (p = .069).

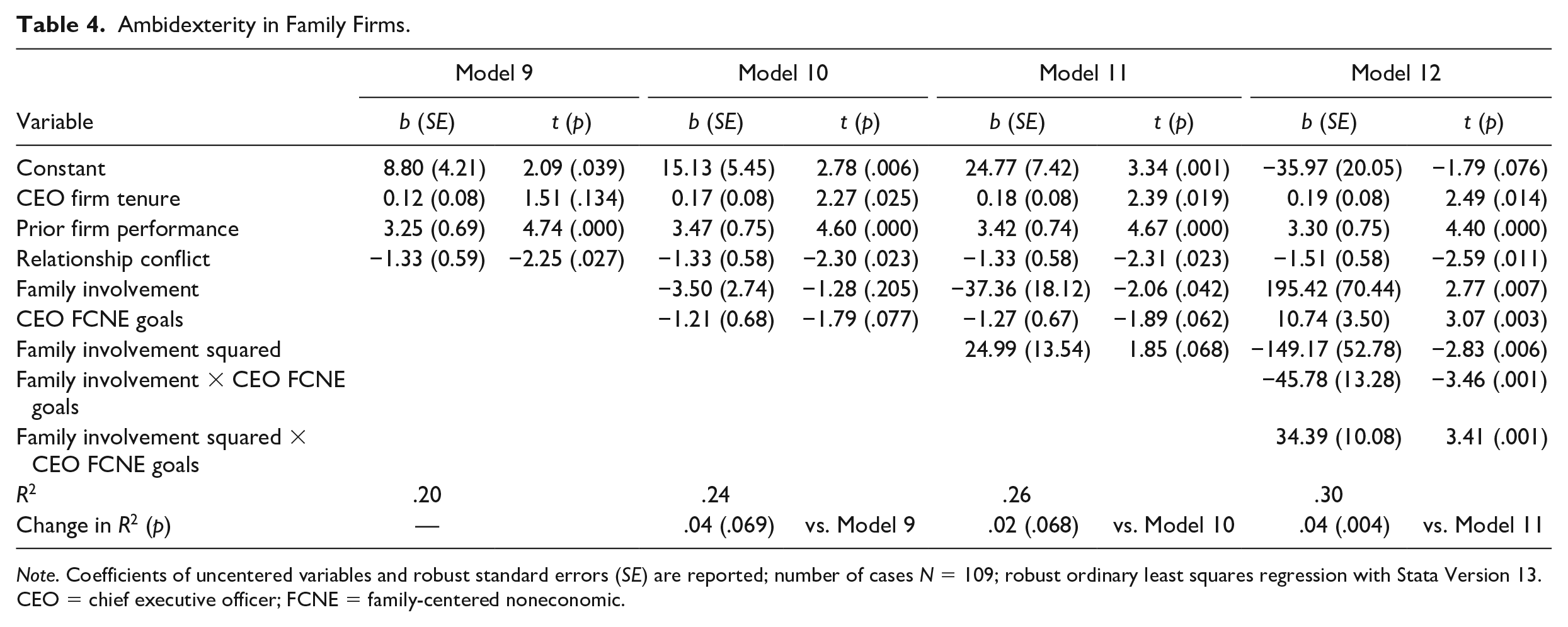

Ambidexterity in Family Firms.

Note. Coefficients of uncentered variables and robust standard errors (SE) are reported; number of cases N = 109; robust ordinary least squares regression with Stata Version 13. CEO = chief executive officer; FCNE = family-centered noneconomic.

H3 predicts an inverted U-shaped relationship between family involvement in top management and ambidexterity. We included the linear and squared terms of family involvement in top management in Model 11, which, contrary to our predictions, shows a positive and marginally significant relationship between the squared term and ambidexterity (b = 24.99, p = .068), indicating a U-shape rather than an inverted U-shape as predicted in H3. The explained variance in Model 9 increases by 0.02 compared with Model 8, and the Wald test indicates marginally significant increased model fit (p = .068).

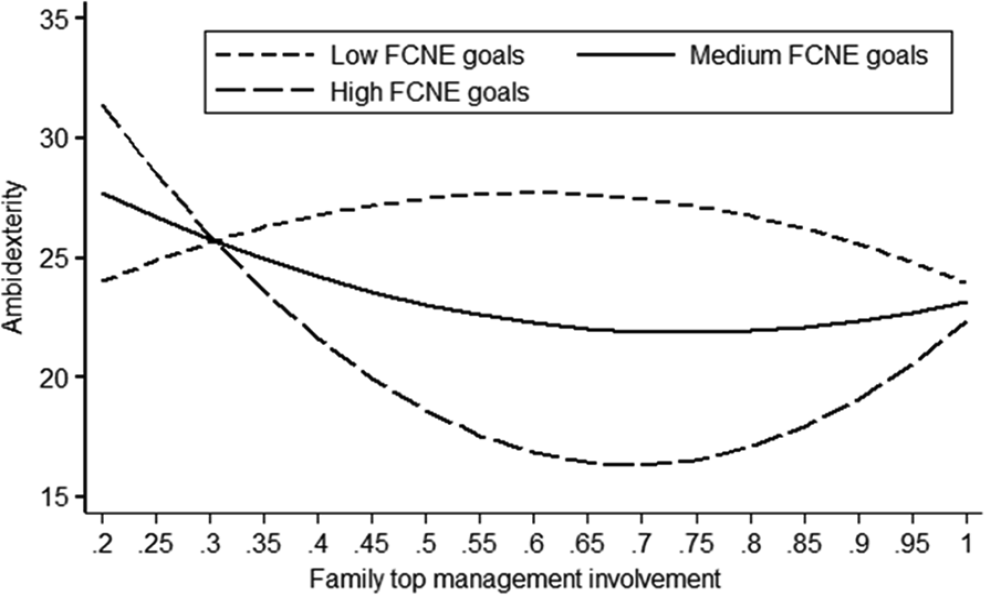

H4c states that the inverted U-shaped relationship between family involvement in top management and ambidexterity diminishes with stronger CEO FCNE goals. We included the interaction terms of family involvement in top management (linear and quadratic) and CEO FCNE goals in Model 12. We found a positive and significant interaction term for family involvement in top management squared and CEO FCNE goals (b = 34.39, p = .001). The result is shown in Table 4, which illustrates the relationship between family involvement in top management and ambidexterity at high levels (1 SD above the mean), medium levels (mean), and low levels (1 SD below the mean) of CEO FCNE goals. The figure reveals that there is indeed an inverted U-shaped relationship as proposed in H3, but this relationship becomes less pronounced as CEO FCNE goals increase, and at CEO FCNE goal values above 4.34, the curve flips to a U-shape, which is consistent with our arguments for H4c.

Further Robustness Checks and Post Hoc Tests

Alternative Control Variables

We tested multiple alternative model specifications with alternative sets of additional control variables. As a first set of additional controls, we added six dummies for the seven SIC-classified industries in our sample (with services representing the reference category). As a second set of additional controls, we added CEO age, CEO gender, CEO education, and firm size (ln). As a third set of additional controls, we added family generation, family ownership, and management team size. In all these analyses, our results remain substantially unchanged, with the added controls being mostly insignificantly associated with the dependent variables.

Reduced Sample

We excluded extreme values of family involvement in top management to ensure the results are solid with regard to outliers. Specifically, we excluded observations with high leadership concentrations (one top management member only, n = 17) and observations with very low family involvement in top management (<25%, n = 3). These exclusions reduced the sample to 89 observations. Consistent with the findings reported earlier, we found no support for H1 (b = 1.57, p = .420) and the opposite effect as predicted in H3 (b = 26.40, p = .089) but found support for H2 (b = 3.75, p = .035), H4a (b = 3.87, p = .019), H4b (b = 3.06, p = .042), and H4c (b = 32.19, p = .014). The graphs for the respective models are highly similar to those shown in Figures 1 to 3.

CEO family-centered noneconomic (FCNE) goals, family top management involvement, and ambidexterity.

Alternative Scale Versions

Furthermore, we conducted robustness checks using alternative versions of the scales reported in the literature. For exploration, we included the five-item scale used by Alexiev et al. (2010; Cronbach’s α = .72). We also used the four-item exploration (Cronbach’s α = .62) and four-item exploitation (Cronbach’s α = .73) scales used by Jansen et al. (2009). All results are consistent with those reported earlier.

Outlier Analysis

Given that our sample is rather small, one might suggest that the results—particularly, the shape of the curves shown in Figures 1 to 3—are driven by outliers. To address this issue, we split the sample at the mean of CEO FCNE goals and then calculated standardized residuals for the two subsamples. For high CEO FCNE goals (n = 65), the maximum absolute value of the standardized residual is 2.01, while for low CEO FCNE goals (n = 44), the maximum absolute value of the standardized residual is 2.81. Both values are below the rule-of-thumb value of 3 for identifying critical outliers. This finding suggests that outliers are not a major driver of our results or of the shapes of the curves shown in Figures 1 to 3.

Reverse Causality

One might argue that a firm’s strategy affects how managers are recruited to top management. While probably the best way to test for this potential endogeneity is to use a two-stage least squares approach (Baum, 2006), the higher order interactions of our model and the limited data at hand made it impossible for us to identify the appropriate instrumental variables required by this approach. Therefore, we drew on an approach suggested by Landis and Dunlap (2000), who argued that directionality in moderated multiple regression can be tested using a “reverse regression approach.” In this approach, dependent and independent variables are exchanged because “these analyses are not symmetrical and . . . a significant interaction may be observed in one case but not the other” (p. 254). Directionality is indicated when the regression coefficient for the moderator is significant in the original equation but not in the reverse equation. Therefore, we exchanged family involvement in top management (our independent variable) with the respective dependent variables (exploration, exploitation, and ambidexterity) and reran the models shown in Tables 2 to 4. Neither the squared term of the original dependent variable nor the interaction of the squared term with CEO FCNE goals was significant in any of the models. Overall, these results support the causal directions argued in our theorizing (Landis & Dunlap, 2000).

Additive and Subtractive Ambidexterity

In addition to multiplicative ambidexterity, which is most widely used in research (see Junni et al., 2013), we ran ordinary least squares regressions using additive (Lubatkin et al., 2006) and subtractive (He & Wong, 2004) ambidexterity as dependent variables. For the full models, the additive method (R2 = .31) has considerably higher explanatory power than the subtractive method (R2 = .05), consistent with Jansen et al. (2009) and Kammerlander et al. (2015). The findings remain similar to the multiplicative calculations. However, H4c is supported by the additive model of ambidexterity (b = 7.33, p = .001) but not by the subtractive (b = 1.79, p = .132) model of ambidexterity.

Discussion

This study advances our understanding of the relationships between top management composition and exploration, exploitation, and organizational ambidexterity in family-managed firms as it provides new insights into the family firm–specific antecedents of these innovation activities. Specifically, we reveal an inverse U-shaped relationship between family involvement in top management and both exploration and organizational ambidexterity in the case of weak CEO FCNE goals as well as a U-shaped relationship in the case of strong CEO FCNE goals. Moreover, our results reveal a U-shaped relationship between family involvement in top management and exploitation, which is accentuated at high levels of CEO FCNE goals.

Our study contributes to a better understanding of the heterogeneous innovation behavior in family firms (e.g., Chrisman & Patel, 2012; Duran et al., 2016), which is an important predictor of their long-term survival. In particular, we advance the increasing body of research on exploration (e.g., Naldi et al., 2007) and exploitation (e.g., Patel & Chrisman, 2014) in family firms by revealing (1) that family involvement in top management has an important effect on innovation and (2) that this effect is nonlinear. While recent research has substantially increased our knowledge on the innovation investments and outcomes of family versus nonfamily firms (Duran et al., 2016) and on the levels of exploration and exploitation in family versus nonfamily firms (Patel & Chrisman, 2014), we shift the focus to better understanding variance in exploration, exploitation, and ambidexterity among family firms. Specifically, we highlight that family involvement in top management comes along with both advantages and disadvantages regarding exploration, exploitation, and organizational ambidexterity.

Interestingly, Figures 1 and 2 not only illustrate the proposed relationships but also indicate that the absolute levels of both exploration and exploitation (and thus also ambidexterity; see Figure 3) are highest for those family-managed firms characterized by both high levels of FCNE goals and very low levels of family involvement at the same time (left sides of the figures). On the one hand, this finding may have emerged because family CEOs with strong FCNE goals provide sufficient resources for long-term investments into exploration. On the other hand, since the CEO is likely the only representative of the family in top management (or perhaps is joined by only one other family member), disparity-related problems in these nonfamily-dominated teams might be mitigated because the CEO wants to avoid a “one-against-all” situation. Moreover, nonfamily managers are likely particularly open to risk since they take part in the upside potential of risky investments through bonuses and other variable forms of compensation but take only limited part in the downside risk (Stanley, 2010). Furthermore, the figures illustrate that local maximum levels exist for medium levels of family involvement and weak CEO FCNE goals (exploration) as well as for high levels of family involvement and strong CEO FCNE goals (exploration and exploitation). Thus, the relationship between family management and innovation might be more complex than often depicted. We encourage future research on family firms’ top management to theorize not only on potential curvilinear effects but also on configurational effects when exploring how top management affects strategic decision making and (innovation) outcomes.

Research on organizational ambidexterity in family firms is still scarce (e.g., Stubner et al., 2012) despite its assumed relevance for these firms (Hiebl, 2015; Matzler et al., 2015). We introduce family involvement in top management as an important yet so far overlooked determinant of organizational ambidexterity. In line with recent research on the relationship between family involvement in top management and firm performance (e.g., D’Allura, 2019; Mazzola et al., 2013), we reveal curvilinear relationships between family involvement and exploration, exploitation, and organizational ambidexterity. One novel theoretical implication of our study is that these curvilinear relationships are sensitive to specific circumstances and might be more or less pronounced or even reversed under some conditions. Therefore, studying these contextual factors might help explain nonfindings, or contradicting findings, linking top management involvement to organizational outcomes (see Tretbar et al., 2016).

Furthermore, our study makes important contributions to family business theory in general. Specifically, we contribute to research on the effects of family involvement on firm-level outcomes (Tretbar et al., 2016) by integrating insights from diversity research (Harrison & Klein, 2007). We advance the debate on the conditions under which family involvement in top management is beneficial or harmful by arguing and showing that diversity with regard to family membership might affect firm-level decisions related to the pursuit of exploitation and exploration in different ways—at least for low levels of FCNE goals. Family and nonfamily top managers differ in their experience, perspectives, attitudes, and opinions (De Massis, Kotlar, et al., 2015; Miller et al., 2014). Our novel argument is that depending on the specific activity in focus (i.e., exploration or exploitation), either the variety aspect (i.e., multitude and combination of diverse experience, exploration and ambidexterity) or the separation aspect (i.e., disagreement regarding opinions, exploitation) of diversity dominates top management’s strategic decision making and thus influences whether diversity helps or hinders innovation. Although this argument is in line with prior research arguing that diversity has beneficial effects for creative tasks but not for routine tasks (e.g., Mansoor et al., 2013), the novel theoretical implication of our study is that this relationship holds not only for characteristics like gender and education but also for family membership. Thus, we illustrate that future theory on family firms can be further enriched by taking a diversity perspective regarding the interaction between family and nonfamily members within a firm and its top management.