Abstract

Family business research suggests that the population of family firms cannot be regarded as a homogenous group. Therefore, with respect to tax avoidance, we analyze the role of the founder as one dimension of family firm heterogeneity. Specifically, we consider socioemotional wealth loss aversion and find that founders may affect the level of tax avoidance not only when they have direct influence (i.e., serving as CEO) but also when they possess solely indirect influence (i.e., having substantial ownership or a seat on the board). Overall, our results suggest that founders remain attached to their firms despite giving up executive positions.

Introduction

In recent years, both family business research (e.g., Evert, Martin, McLeod, & Payne, 2016; Hoy & Sharma, 2006; Sharma, 2004; Siebels & zu Knyphausen-Aufseß, 2012) and research on corporate tax avoidance (e.g., Hanlon & Heitzman, 2010; Shackelford & Shevlin, 2001; Wilde & Wilson, 2018) have grown significantly. In general, these research areas appear to have developed in a mutually independent manner; thus, insights on the family firm–taxation interface are fairly limited. The few articles that consider tax avoidance in family firms focus primarily on differences between family and nonfamily firms (e.g., Chen, Chen, Cheng, & Shevlin, 2010; Landry, Deslandes, & Fortin, 2013; Mafrolla & D’Amico, 2016; Steijvers & Niskanen, 2014). However, prior family business research indicates that differences among family firms may be at least as large as variations between family and nonfamily firms (e.g., Bennedsen, Perez-Gonzalez, & Wolfenzon, 2010; Chrisman & Patel, 2012; Chua, Chrisman, Steier, & Rau, 2012). Therefore, especially in the context of tax avoidance, more research is needed to examine the differences within the group of family firms.

In this study, we use the socioemotional wealth concept to provide explanations for behavioral complexities within family firms. A major aspect of socioemotional wealth is that when family involvement is high, family firms are more likely to be driven by nonfinancial objectives than by exclusively financial goals (Berrone, Cruz, & Gómez-Mejía, 2012; Gómez-Mejía, Cruz, & Imperatore, 2014; Stockmans, Lybaert, & Voordeckers, 2010). Preserving the family’s socioemotional wealth is a key goal for the controlling family (Gómez-Mejía, Haynes, Núñez-Nickel, Jacobson, & Moyano-Fuentes, 2007). However, prioritizing nonfinancial objectives could lead to economic inefficiencies, such as losing sight of cost minimization. Tax payments generally represent costs, and thus, an increase in tax avoidance leads to a decrease in a firm’s cash outflows. In this context, it is important to explain what we mean by the term tax avoidance. We define tax avoidance broadly; that is, we refer to tax avoidance strategies that can have certain and uncertain outcomes with tax authorities (e.g., Badertscher, Katz, & Rego, 2013; Dyreng, Hanlon, & Maydew, 2008). Uncertain tax avoidance strategies may be challenged by tax authorities at some point. This could cause unwanted public scrutiny and reputational damage, which is why some firms may refrain from avoiding taxes (e.g., Austin & Wilson, 2017). Following this argumentation, tax avoidance could threaten the family’s status in the community and is therefore likely to result in a loss of socioemotional wealth.

However, because family firms are not a homogenous group, the attachment to socioemotional wealth varies within the population of family firms. Although prior family business research investigates heterogeneity by analyzing different types of family firms (for an overview, see Chua et al., 2012), evidence on family firm heterogeneity in the tax-related literature is scarce. In addition to investigating differences between family and nonfamily firms, both Chen et al. (2010) and Steijvers and Niskanen (2014) analyze differences within the group of family firms. Chen et al. (2010) find that compared with a public nonfamily firm, a public family firm’s tax avoidance varies depending on the type of CEO the firm has. Additionally, Steijvers and Niskanen (2014) analyze the association between tax avoidance and CEO ownership and find that family firms with a lower CEO ownership share are more tax aggressive than those with a higher CEO ownership share. Both studies refer to the party that presumably determines the extent of tax avoidance: the family firm’s CEO.

Nevertheless, more detailed insights into whether the perhaps most important individual in a family firm—the founder—can influence tax-related business decisions not only directly (i.e., when serving as CEO) but also indirectly (i.e., after stepping down as CEO) are still missing. Closing this research gap is important to better understand whether and, if so, how founders are able to influence decision making in family firms according to their socioemotional wealth agenda—despite having given up their position in the top management team. Assuming that founders most likely perceive tax avoidance as a potential threat to socioemotional wealth, we attempt to fill this gap by answering the following research question: (How) can founders—with direct or indirect decision-making power—affect the engagement in tax avoidance to enforce their nonfinancial goals?

To address this research question, we first examine whether founder CEOs, who have direct influence on family firms’ decisions because of their executive position, are able to moderate the extent of tax avoidance corresponding to their socioemotional wealth agenda. The association between founder CEOs and tax avoidance has received some attention in the literature (Chen et al., 2010). However, prior findings for U.S. (public) family firms may not be generalizable (Botero, Cruz, De Massis, & Nordqvist, 2015; Klein, 2000) and thus may not apply to family firms in other countries, such as Germany. For example, founder CEOs in U.S. (public) family firms could act in a different way than founder CEOs in German (public and private) family firms because of significant divergences between the German and U.S. corporate governance systems. According to prior research (e.g., Moerland, 1995), the United States is an example of the market-oriented Anglo-Saxon corporate governance system that is determined by a one-tier board structure, that is, managing and monitoring duties are combined (Zhao, 2010). In contrast, Germany provides an example of the network-oriented Germanic corporate governance system that relies on a two-tier board structure, which is characterized by a strict division between the top management team and the supervisory board (Weimer & Pape, 1999). Because board independence within these two corporate governance systems is not identical, the monitoring role (i.e., to oversee and approve the top management teams’ decisions) regarding tax avoidance could be exercised differently (Armstrong, Blouin, Jagolinzer, & Larcker, 2015) and may lead to different decision-making outcomes by founder CEOs. Thus, it is necessary to analyze whether the direct influence of founder CEOs is also associated with tax avoidance in the network-oriented corporate governance system in Germany. These findings could be relevant to other network-oriented countries such as Austria, the Netherlands, or Switzerland, which have adopted similar corporate governance systems (Weimer & Pape, 1999). In this context, it should be noted that we do not address other (more narrowly defined) types of firms, such as lone founder businesses (Miller, Le Breton-Miller, Lester, & Cannella, 2007). We refer to the notion that founder CEOs in family firms are generally assumed to be forward-looking leaders with distinct managerial abilities (Cheng, 2014) and sophisticated tacit knowledge, which they use to maintain socioemotional wealth. As engaging in tax avoidance can be controversial for family firms and may interfere with socioemotional wealth perspectives, we expect and find that founder CEOs are likely to use their direct influence and avoid taxes less than both descendant and hired CEOs.

On this basis, we draw on founders’ strong emotional attachment to their family firms, which is why they are usually reluctant to surrender their influential position (Chrisman, Chua, & Sharma, 1996; Rubenson & Gupta, 1996). Thus, even after stepping down as CEO, founders may exert indirect influence (Davis & Harveston, 1999) to enforce their socioemotional wealth objectives. Therefore, we investigate two channels that founders could use to ensure that the family firm continues to operate in their spirit even if they have passed on their executive position to a descendant or hired CEO. Specifically, we analyze whether founders can affect the engagement in tax avoidance in descendant or hired CEO family firms indirectly by (1) maintaining substantial ownership or (2) having a seat on the (supervisory or advisory) board. We expect and find that founders can use these channels to moderate the family firms’ engagement in tax avoidance in order to pursue their nonfinancial goals. Consequently, we are able to show that if the founder exerts indirect influence in descendant or hired CEO family firms, these firms’ engagement in tax avoidance is similar to that of family firms in which the founder is CEO.

This study contributes to the literature in (at least) three ways. First, we contribute to the ongoing family firm heterogeneity debate by investigating the influence of the founder. Specifically, we add to the literature indicating that founders can affect the level of tax avoidance not only when they have direct influence but also when they possess solely indirect influence. To gain a better understanding of founders’ capability to exert indirect influence, we identify two channels that founders could use to affect business decisions (i.e., maintaining substantial ownership or having a seat on the board). Second, this study offers a theoretical contribution by expanding the knowledge regarding the socioemotional wealth concept. Our results suggest that the emotional attachment of founders to their firms is particularly strong, as they still seem to be involved in corporate decision making even after giving up their executive positions. This strong emotional bond encourages founders to act not only as supervisors; in fact, in terms of decisions that could endanger socioemotional wealth, founders still seem to be “pulling the strings.” Third, from a broader perspective, our study provides insights into why some firms avoid taxes more than others. Recent studies on tax avoidance explore several incentives for avoiding taxes (e.g., Chyz, Leung, Li, & Rui, 2013; Higgins, Omer, & Phillips, 2015; Kubick, Lynch, Mayberry, & Omer, 2016). Similar to the results of Steijvers and Niskanen (2014), our findings suggest that nonfinancial objectives in family firms are likely to be an important determinant of tax avoidance, considering that socioemotional wealth is not directly measured.

The article proceeds as follows. In the next section, we provide details on German institutional characteristics. In the third section, we develop our hypotheses, and in the fourth section, we explain the research design. The fifth section presents the results of our analyses. The discussion and conclusions are provided in the final section.

German Institutional Characteristics and Tax Avoidance

In this study, we analyze tax avoidance in Germany. Accordingly, we must (1) explain why the German setting is advantageous and of interest to an international audience, (2) describe the German institutional background regarding taxation, and (3) clarify our understanding of tax avoidance and its associated benefits and costs.

An analysis of the German setting is of interest to a broader audience for several reasons. First, the scant existing research on German family firms emphasizes the prevalence of a generally strong emotional connection that owners and other stakeholders (e.g., the staff) have with firms (Carney, Gedajlovic, & Strike, 2014). Thus, it is likely that the affective bond of founders to family firms in Germany is particularly strong as well. Consequently, specifically in the context of tax avoidance, this could have an influence on founders’ decision-making behavior, and it may provide interesting insights regarding the socioemotional wealth concept.

Second, the member states of the European Union (EU) have to revise their tax codes in accordance with the Anti-Tax Avoidance Directive (ATAD) by the end of 2018 (Council of the European Union, 2016). The purpose of the ATAD is to reduce corporate tax avoidance by implementing a minimum level of protection. In addition to a general anti-abuse rule, the ATAD comprises rules concerning interest limitations, the relocation of assets and exit taxation, controlled foreign companies (CFC), and hybrid mismatches. In contrast to other EU member states, Germany’s tax law fulfills the requirements of the ATAD in many respects (Linn & Braun, 2016). Only a few minor changes will have to be made to fully comply with the ATAD (e.g., the CFC rules require some adjustments). Therefore, during the whole sample period of our study (i.e., 2009-2014), the German corporate tax law was—except for minor discrepancies—already in line with the ATAD. Thus, using the German context is advantageous because the results of our study should not lose much of their relevance in the future.

Third, as mentioned in the introduction, divergences between countries in terms of corporate governance may be significant. Prior U.S. research has shown that board independence has a positive (negative) relation with tax avoidance for low-aggression (high-aggression) firms, indicating an underinvestment (overinvestment) in tax avoidance in the absence of monitoring (Armstrong et al., 2015). In contrast to the United States, the supervisory board in Germany exclusively consists of nonexecutive members. Therefore, we assume that independent German supervisory boards monitor the top management team differently compared with the United States, where board independence is often substantially lower. Specifically, supervisory board members in Germany may constrain the management’s (tax) decisions more frequently because they are not involved in the operational business and, therefore, may not be able to fully comprehend the motives to engage in certain (tax) strategies. Overall, we believe that an analysis of the German setting could represent a worthwhile complement to existing evidence for other countries (e.g., the United States).

With regard to the institutional background in terms of taxation, it is important to acknowledge that corporations and partnerships differ. All German corporations, that is, European public companies, stock corporations, partnerships limited by shares, or limited liability companies, generally face a corporate income tax rate of 15% plus a solidarity surcharge. Additionally, corporations are subject to a trade tax of roughly 14%. The exact rate, however, depends on the respective firm’s municipality of residence. Overall, German corporations face a firm-level tax rate of approximately 30%. This tax rate does not depend on whether a corporation is publicly traded or privately owned. If a corporation pays out dividends, it is necessary to distinguish whether the beneficiary is an individual or another (affiliated) corporation. In the former case, although differences exist depending on whether the equity holding is associated with a private or business property, dividend payments are generally taxed with a flat income tax rate; in the latter case, such payments are generally tax exempt due to an affiliation privilege.

In contrast to German corporations, German partnerships (e.g., limited or general partnerships) are not taxable entities. Hence, not the partnership itself but rather its co-entrepreneurs are subject to income tax plus a solidarity surcharge. Thus, for income tax purposes, a partnership is treated as transparent; that is, operating income is allocated directly to co-entrepreneurs based on their shareholding quota. Therefore, the actual income tax burden of partnerships depends on co-entrepreneurs’ individual income tax rate. However, similar to corporations, partnerships in Germany face an entity-level trade tax.

Overall, there are obvious differences between German corporations and partnerships in terms of taxation. Therefore, we exclude all partnerships to ensure that our results (especially for private family firms) are not driven by different legal forms. In other words, our analysis includes corporations only, which prevents bias stemming from taxation differences between corporations and partnerships.

The literature contains no universally accepted definition of tax avoidance. Tax avoidance is commonly defined as the reduction of explicit taxes, that is, the decrease in payments made directly to tax authorities (e.g., Dyreng et al., 2008; Hanlon & Heitzman, 2010). However, across a range of tax strategies, certain strategies are perfectly legal and can therefore be considered moderate (e.g., investments in municipal bonds). In contrast, other tax strategies fall in a gray area or are even illegal. For example, tax sheltering is based on literal interpretations of government regulation that deviate from the legislation’s original intent and is therefore regarded as a more aggressive tax strategy (Bankman, 1999). In this study, we define tax avoidance broadly; that is, we refer to tax avoidance strategies that can have certain and uncertain outcomes with tax authorities (Badertscher et al., 2013). Such strategies may include—but are not limited to—activities such as investments in intangible assets, the relocation of operations to low-tax countries, income shifting from high- to low-tax locations, and engagement in synthetic lease transactions. Therefore, we do not explicitly address one specific tax strategy but rather focus on the general intention to reduce the corporate tax burden.

Avoiding taxes involves benefits and costs. On the one hand, because tax avoidance can reduce a firm’s tax burden, it lowers cash outflow, which is beneficial primarily for shareholders because it leads to higher after-tax earnings. On the other hand, these benefits of tax avoidance are accompanied by tax and nontax costs. Tax costs include tax expert compensation, the costs of implementing and monitoring specific tax strategies, and penalties imposed by tax courts. Nontax costs of tax avoidance (Scholes, Wolfson, Erickson, Hanlon, Maydew, & Shevlin, 2015) arise particularly from reputational or political damages. Ultimately, the benefits and costs of tax avoidance require decision makers to carefully balance the reasons to speak for and against engaging in tax avoidance. Given the assumption that leaders act rationally in general, the implementation of tax avoidance strategies is beneficial as long as the benefits exceed the costs (Hanlon & Heitzman, 2010).

Theoretical Background and Hypotheses

Socioemotional Wealth, Tax Avoidance, and Family Firm Heterogeneity

Decision-making processes in family firms are driven not only by economic objectives but also by noneconomic goals, such as family control and influence, family members’ identification with the firm, binding social ties, family members’ emotional attachment, and securing the family’s reputation and status in the community (Berrone, Cruz, & Gómez-Mejía, 2012; Cennamo, Berrone, Cruz, & Gómez-Mejía, 2012). Gómez-Mejía et al. (2007) suggest that these noneconomic aspects determine socioemotional wealth, which provides family-specific utility. Consequently, preserving socioemotional wealth is likely to be important to family owners who tend to account for aspects of socioemotional wealth when considering potential outcomes of their strategic decisions with respect to gains and losses. Stated differently, socioemotional wealth loss aversion could encourage family owners to evade threats to their nonfinancial goals (Gómez-Mejía et al., 2014). In this context, family owners are likely to perceive tax avoidance as risky, particularly because of its uncertain consequences. Although reducing tax payments to the government may lead to reduced cash outflow and may therefore maximize firm value, family owners are likely to ultimately prefer socioemotional wealth preservation to engagement in tax avoidance.

In the context of tax avoidance, evidence regarding how these nonfinancial objectives vary within family firms is scarce (Steijvers & Niskanen, 2014). Moreover, family firm scholars stress the family firm heterogeneity debate, suggesting that family firms cannot be regarded as a homogenous unit (e.g., Chua et al., 2012; Pazzaglia, Mengoli, & Sapienza, 2013). A crucial dimension of heterogeneity refers to the party that presumably determines the extent of tax avoidance: family firms’ CEOs. More precisely, CEOs can affect a firm’s tax avoidance strategy by setting the “tone at the top” (e.g., Dyreng, Hanlon, & Maydew, 2010). Because of founder centrality in family firms, founders can play an important role in a family business even without serving as the CEO (Kelly, Athanassiou, & Crittenden, 2000). We therefore analyze whether the association between founders and tax avoidance differs when founders (1) have direct influence (i.e., serving as CEO) or (2) are able to exert solely indirect influence (i.e., after stepping down as CEO).

The Direct Influence of Founders in Family Firms

Family business research has paid considerable attention to the role of the CEO position in terms of firm performance (e.g., Anderson & Reeb, 2003; Michiels, Voordeckers, Lybaert, & Steijvers, 2013; Villalonga & Amit, 2006). Likewise, prior tax-related studies have started to acknowledge the importance of the CEO in determining tax avoidance in family firms. Chen et al. (2010) investigate whether differences between U.S. public family and nonfamily firms in terms of tax avoidance trace back to the family firm’s CEO type. Steijvers and Niskanen (2014) recognize that the population of (private) family firms is heterogenous (Chrisman et al., 2005; Westhead & Howorth, 2007); therefore, they execute a more specific analysis within a subsample of (private) family firms by testing the association between tax avoidance and CEO ownership. Referring to the importance of the CEO, we analyze the association between tax avoidance and different CEO types within the group of German family firms. In this context, a family firm’s management team can be led by a founder CEO, a descendant CEO, or a hired (external) CEO (Anderson, Mansi, & Reeb, 2003; Villalonga & Amit, 2006).

Prior research suggests that founder CEOs are central in determining a family firm’s philosophy and strategic orientation (e.g., Athanassiou, Critten, Kelley, & Marquez, 2002; Schein, 1983; Tagiuri & Davis, 1992). Moreover, founder CEOs possess detailed firm-specific knowledge (Morck, Shleifer, & Vishny, 1988) and discretionary power. In fact, by having direct influence as CEOs, founders can set their own agenda and focus on objectives that are not necessarily beneficial to nonfamily shareholders (Chrisman, Chua, & Litz, 2004; Gedajlovic, Lubatkin, & Schulze, 2004). Most important, founder CEOs derive high utility from having comprehensive decision-making capabilities (Gómez-Mejía et al., 2007; Schulze, Lubatkin, & Dino, 2003) and generally do not want to endanger the family’s socioemotional wealth by engaging in tax avoidance. High emotional attachment to the firm reinforces this attitude (Leitterstorf & Wachter, 2016). Overall, founder CEOs are expected to enforce rather moderate levels of tax avoidance.

Once the founder steps down as CEO and therefore loses direct influence, corporate leadership is given to either a descendant or a hired (external) manager. Differences emerge with respect to the goals, values, and commitment to the business between firms managed by descendant CEOs and founder-led family firms (Ward, 1997). Moreover, descendant-led family firms may exhibit reduced motivation, commitment, and incentives to maintain the founder’s leadership style (Andersson, Carlsen, & Getz, 2002). Additionally, descendant CEOs have difficulties taking over the founder’s tacit knowledge (Morck & Yeung, 2003) and social capital (Steier, 2001). Overall, the preservation of socioemotional wealth is likely to be less important for descendant CEOs than for founder CEOs because the former tend to prioritize individual objectives and their own welfare (Villalonga & Amit, 2006). Furthermore, descendant CEOs may focus more on financial goals than on nonfinancial goals and, therefore, could be more willing to engage in tax avoidance than founder CEOs.

In contrast to founder and descendant CEOs, hired (external) CEOs are not attached to the owning family. Hiring external CEOs can be beneficial because they introduce a different perspective and new ways of thinking to the family firm (Blumentritt, Keyt, & Astrachan, 2007; Huybrechts, Voordeckers, & Lybaert, 2012). However, because they lack a family bond to the firm, hired CEOs may not be aware of priorities and values that characterize a specific family firm (Stewart & Hitt, 2012). In general, to fulfill shareholder expectations and maintain their good reputation, hired CEOs focus on maximizing firm value (Cannella, Fraser, & Lee, 1995; Gómez-Mejía, Núñez-Nickel, & Gutierrez, 2001). Therefore, from a socioemotional wealth point of view, hired CEOs generally focus more on achieving financial goals than on balancing financial and nonfinancial objectives (Basco & Pérez-Rodriguez, 2009; Minichilli, Nordqvist, Corbetta, & Amore, 2014; Vandekerkhof, Steijvers, Hendriks, Voordeckers, 2015). Thus, hired CEOs are likely to engage more in tax avoidance than founder CEOs.

Ultimately, based on the argumentation presented above, we suggest that founders exhibit particularly strong socioemotional wealth loss aversion. In contrast, attachment to socioemotional wealth is likely to decrease in descendant and hired CEO family firms. Hence, we expect the following:

The Indirect Influence of Founders in Family Firms

In addition, we investigate whether founders can also affect the top management team when they possess solely indirect influence (i.e., founders are no longer part of the top management team). In this context, prior research emphasizes that founders usually hold a central role because they created the business and are therefore reluctant to surrender their direct influence (Chrisman et al., 1996; Rubenson & Gupta, 1996). More precisely, due to their strong emotional attachment to their firms, founders lack the willingness to resign from executive positions. For this very reason, founders generally want to ensure that family firms continue to operate in their spirit after stepping down as CEOs. Stated differently, founders want to ascertain that (family or nonfamily) successors do not act in an excessively risk-seeking manner (e.g., Harvey & Evans, 1995; Leitterstorf & Rau, 2014; Zellweger, Kellermanns, Chrisman, & Chua, 2012). Hence, in addition to pursuing socioemotional wealth goals when serving as CEOs, we argue that founders in family firms are likely to exert indirect influence even after giving up their formal authority. We argue that founders can use (at least) two different channels to maintain indirect influence.

As a first channel, founders may transfer leadership to a descendant or hired (external) manager while maintaining substantial ownership. Founders are considered to possess substantial ownership if they hold a blocking minority (i.e., more than 25% of the firm’s shares), which enables them to vote against business decisions that could harm socioemotional wealth. Hence, retaining substantial ownership could be a way for founders to remain connected to their firms (Brun de Pontet, Wrosch, & Gagné, 2007). Thus, if the founder stepped down as CEO, we must distinguish between family firms with and without substantial ownership of the founder.

Founders with substantial ownership in family firms that are governed by descendant or hired CEOs are assumed to act as supervisors, teachers, or safeguards (Cadieux, 2007) who intervene if socioemotional wealth is at stake. Stated differently, even after the transition of direct influence, founders likely still affect management’s motives, values, and goals (Kelly et al., 2000), ensuring family owners’ preservation of socioemotional wealth (e.g., Berrone, Cruz, Gómez-Mejía, & Larraza-Kintana, 2010; Deephouse & Jaskiewicz, 2013). In general, because of its uncertain consequences, engaging in tax avoidance is risky and may involve the deterioration of the family firm’s (good) reputation. Specifically, adverse media coverage regarding tax avoidance practices is likely to reduce socioemotional wealth by degrading the status in the community, which is important to most families (Berrone et al., 2012). Thus, socioemotional wealth loss aversion most likely incentivizes founders to monitor the strategic decisions of descendant and hired CEOs. In the context of tax avoidance, we therefore expect that descendant and hired CEO family firms, in which the founder is no longer CEO but still holds substantial ownership, do not avoid taxes significantly more than founder CEO family firms.

Family firms that are managed by a descendant or hired CEO and without the founder as a substantial shareholder are likely to be less restricted by the founder’s influence. In fact, the new CEO can override past practices by implementing plans for the company’s renewal (Mitchell, Hart, Valcea, & Townsend, 2009), which could lead to a change in both leadership style and business strategy (Harvey & Evans, 1995) by putting the CEO’s individual stamp on the family firm (Miller, Steier, & Le Breton-Miller, 2003). Compared with founder CEOs, descendant and hired CEOs may deem preserving socioemotional wealth less important because they prioritize individual objectives (Villalonga & Amit, 2006). Thus, we argue that (family or nonfamily) successors are likely to increase tax avoidance if the founder is not equipped with sufficient ownership to block business decisions that could put socioemotional wealth at risk. Therefore, we expect that family firms in which the founder is neither CEO nor a substantial shareholder engage more in tax avoidance than family firms with founder CEOs.

In sum, we argue that founders—after stepping down as CEO—can use substantial ownership to exert indirect influence. As founders can use their substantial ownership to block business decisions that could threaten families’ socioemotional wealth, we expect that these firms will not demonstrate a significantly different level of tax avoidance than family firms with a founder CEO. Thus, we propose the following hypothesis:

As a second channel, according to prior research, family owners are likely to make use of governance mechanisms such as boards of directors to ensure that the firm’s strategy is aligned with the family’s objectives (Arzubiaga, Kotlar, De Massis, Maseda, & Iturralde, 2018; Lee & O’Neill, 2003; Van den Berghe & Carchon, 2002). Similar to an independent board of directors in the United States, public firms in Germany are legally required to establish a supervisory board (Faghfouri, Kraiczy, Hack, & Kellermanns, 2015), whereas private corporations—unless they exceed certain thresholds—generally are not. However, a growing number of private family firms in Germany voluntarily establish advisory boards that have similar responsibilities (e.g., monitoring executive management and providing strategic advice) to supervisory boards (Blumentritt, 2006; Tillman, 1988).

We argue that founders—despite handing over formal authority (i.e., the CEO position)—are able to use a seat on the (advisory or supervisory) board to exercise indirect influence. More precisely, founders can use the board as a vehicle to pursue their goals and use their position to control and monitor their (family and nonfamily) successors. Specifically, the founder can take a leading role in terms of transactions that require the approval of the board. In this context, the founder will most likely object to risky business practices, such as excessive tax avoidance, that potentially counteract socioemotional wealth considerations.

In contrast, the preservation of socioemotional wealth could be less important for (advisory or supervisory) boards on which the founder does not have a seat. These boards may tend to focus more on financial goals than on nonfinancial goals and are therefore less reluctant to approve tax avoidance mechanisms. Overall, we expect that founders can use their seats on boards to wield indirect influence and to prevent tax avoidance practices that are not in line with socioemotional wealth considerations. We therefore hypothesize the following:

Research Design

Sample

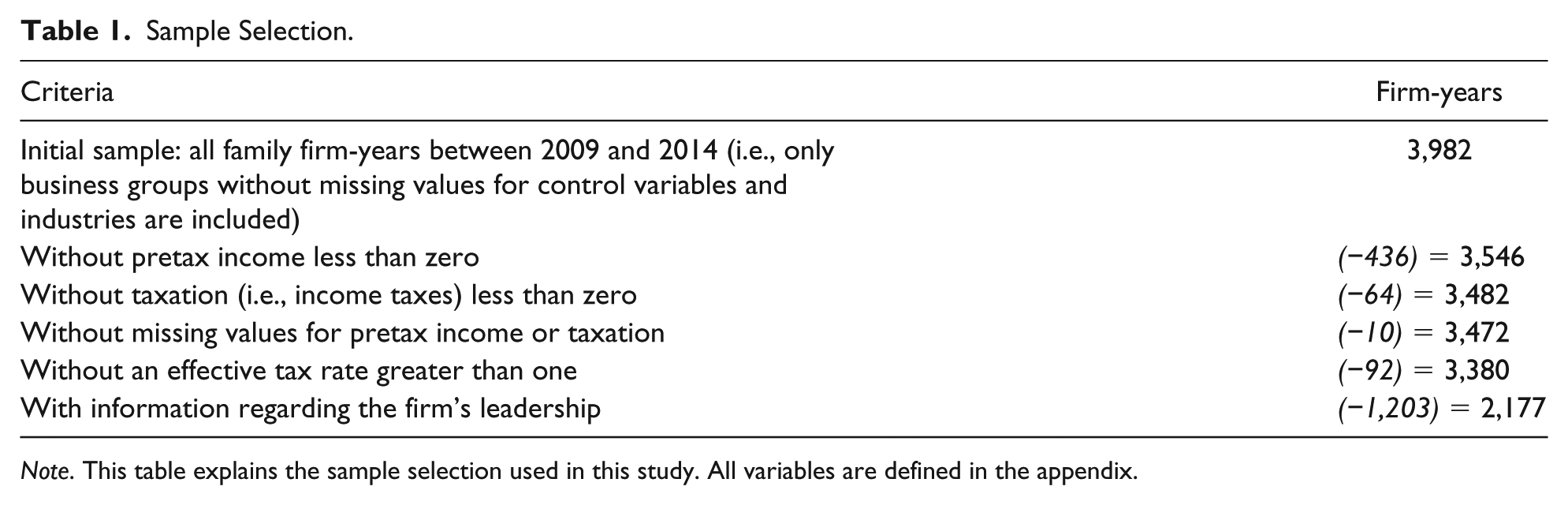

We obtain our consolidated German data from Bureau van Dijk’s Amadeus database. Table 1 reports our sample selection process. In general, we classify firms as family firms if founders or family members (by either blood or marriage) hold at least 30% of the firm’s equity. We apply this threshold for both public and private family firms and hand-collect information using Bureau van Dijk’s Amadeus Shareholders database and publicly available sources (e.g., company websites). 1 Similar to Ali, Chen, and Radhakrishnan (2007), the “family firm” attribute is supposed to be sticky; that is, it is assumed that the mid-2015 classification applies to the entire observation period of this study.

Sample Selection.

Note. This table explains the sample selection used in this study. All variables are defined in the appendix.

When analyzing public and private family firms, one may be concerned about differences in financial statements because public family firms are generally organized as business groups, whereas private family firms occasionally remain stand-alone entities. While (public and private) business groups in Germany file consolidated (and unconsolidated) financial statements, stand-alone firms file only individual financial statements. Referring to public and private firms’ earnings quality, Bonacchi, Marra, and Zarowin (2017) suggest that the contradictory results of prior research in this field (e.g., Ball & Shivakumar, 2005; Burgstahler, Hail, & Leuz, 2006; Givoly, Hayn, & Katz, 2010; Hope, Thomas, & Vyas, 2013) relate to the inclusion of different types of financial statements in the samples. Considering these findings, we ensure that the organizational structure does not drive our results. Therefore, we use consolidated financial data of (public and private) business groups only; that is, our analysis includes only family firms with at least one subsidiary. Moreover, due to firms’ different approaches to taxation, we focus on corporations only. Given these requirements, our sample initially consists of 814 family firms (3,982 firm-years) for the period from 2009 to 2014.

We exclude all firm-years with either a negative pretax income or negative income taxes because negative effective tax rates are difficult to interpret (Dyreng et al., 2008). This step reduces our sample to 3,482 firm-years. We also exclude all firm-years for which the pretax income or income taxes are missing. Additionally, we exclude firm-years with a calculated effective tax rate greater than 1 (92 firm-years are excluded). Furthermore, to test our hypotheses, we need information regarding the firm’s leadership (1,203 firm-years are excluded), which reduces our sample to 2,177 firm-year observations of 516 family firms.

Method

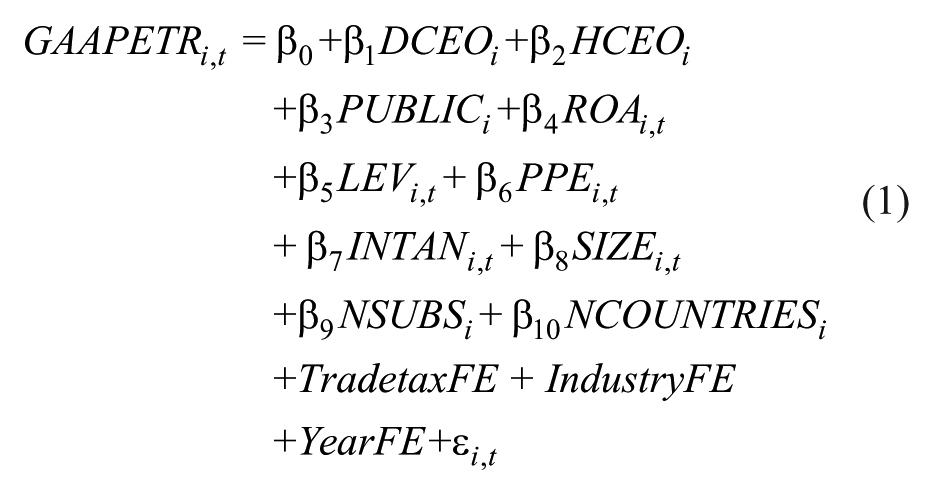

To test the proposed hypotheses regarding the association between tax avoidance and family firm heterogeneity, we estimate multivariate regression models and control for firm-specific variables. The regression equation (1) that we use to test Hypothesis 1 is calculated as follows:

where i represents the firm, t represents time, and

Variables

Dependent Variable

For the tax avoidance measure, we use the GAAP (generally accepted accounting principles) effective tax rate (GAAPETR). We define GAAPETR for firm i in year t as the total income tax expense (Taxation) divided by the pretax book income (PTBI). We use Taxation as a measure of the total income tax expense, which comprises all (i.e., paid, accrued, and deferred) taxes related to the accounting period t of firm i. 2 PTBI represents the pretax book income for firm i in year t. As mentioned above, we define tax avoidance broadly and focus on the general intent of reducing the corporate tax burden. Because the GAAPETR captures both the current and the future tax liability, it seems to be the most appropriate measure for a firm’s overall level of tax avoidance. Higher values of GAAPETR are assumed to reflect less tax avoidance.

Independent Variables

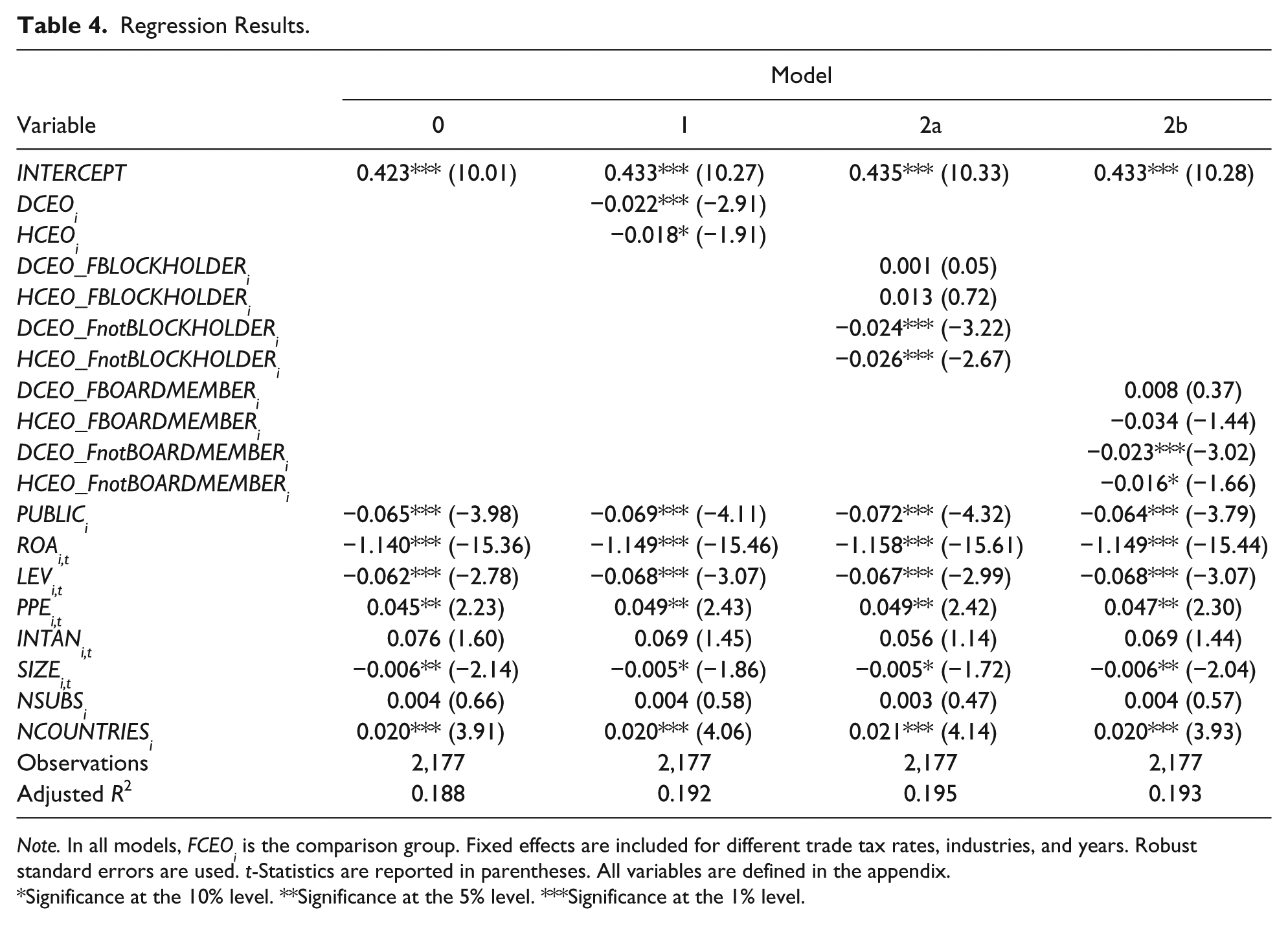

Three indicator variables are used to investigate Hypothesis 1. FCEO is the base group; it is equal to 1 if the founder leads a family firm and 0 otherwise. Similarly, DCEO (HCEO) is equal to 1 if a descendant (hired manager) leads a family firm and 0 otherwise. To determine who is the CEO of a family firm (i.e., the founder, a descendant, or a hired manager), we hand-collect information using publicly available sources (e.g., company websites and company registers). It is important to note that we investigate in Hypotheses 2a and 2b the difference between the founder’s direct and indirect influence. Therefore, in each test, we compare the founder’s direct influence (i.e., FCEO remains as the base group) with two different channels of indirect founder influence. To test Hypothesis 2a, we modify regression equation (1) by dividing the group of descendant CEO (hired CEO) family firms into two subgroups: DCEO_FBLOCKHOLDER (HCEO_FBLOCKHOLDER) is equal to 1 if the founder of a family firm with a descendant CEO (hired CEO) still holds more than 25% of the firm’s shares. We require founders to hold more than 25% of the firm’s shares to be considered substantial shareholders because this constitutes a blocking minority that enables founders to vote against major strategic firm decisions. Consequently, DCEO_FnotBLOCKHOLDER (HCEO_FnotBLOCKHOLDER) is equal to 1 if the founder of a descendant CEO (hired CEO) family firm is not a substantial shareholder (i.e., the founder’s share ≤25%) of this firm and 0 otherwise. Likewise, to analyze Hypothesis 2b, we distinguish whether the founder of a descendant or hired CEO family firm has a seat on the supervisory or advisory board: DCEO_FBOARDMEMBER (HCEO_FBOARDMEMBER) is equal to 1 if the founder of a family firm with a descendant CEO (hired CEO) is a member of the board. Likewise, DCEO_FnotBOARDMEMBER (HCEO_FnotBOARDMEMBER) is equal to 1 if the founder of a family firm with a descendant CEO (hired CEO) does not have a seat on the board and 0 otherwise. We gather information on whether a founder is part of the board from the firms’ annual reports.

Control Variables

Drawing on prior studies (e.g., Chen et al., 2010; Dyreng et al., 2008; Frank, Lynch, & Rego, 2009; Manzon & Plesko, 2002; Mills, 1998; Rego, 2003), we include eight variables to control for differences in firm characteristics that could be related to tax avoidance. PUBLIC is an indicator variable that is set to 1 if a firm is classified as a public family firm and 0 otherwise (i.e., private family firm). Prior literature has identified several specific features of publicly traded firms. An important aspect is exposure to capital market pressure (e.g., Badertscher, Katz, Rego, & Wilson, 2017; Desai, 2005; McGuire, Wang, & Wilson, 2014). Based on this characteristic, prior studies find that public firms may engage more in nonconforming tax avoidance than private firms (e.g., Badertscher et al., 2017; Cloyd, Pratt, & Stock, 1996; Mills & Newberry, 2001). Therefore, because public (family) firms are likely to avoid income taxes more than private (family) firms, we include the indicator variable PUBLIC.

Additionally, return on assets (ROA; net income divided by total assets) and leverage (LEV; the ratio of long-term debt plus the debt included in current liabilities to total assets) control for a firm’s operating performance and its leverage, respectively. Furthermore, capital-intensive firms may be affected by divergences between financial accounting standards and tax rules; in particular, depreciation charges are likely to differ between the two systems. The inclusion of property, plant, and equipment (PPE; the ratio of the current year’s net property, plant, and equipment to total assets) accounts for these differences. Similarly, intangible assets (INTAN; the level of intangible assets scaled by total assets) are often treated differently for financial accounting purposes than for tax purposes, and the incorporation of INTAN as a control variable accounts for this differential treatment. Furthermore, we incorporate SIZE (the natural logarithm of total assets) because tax avoidance may vary depending on firm size. We also control for the number of countries in which a firm operates (NCOUNTRIES; the natural logarithm of the number of countries) in addition to the number of subsidiaries that it maintains (NSUBS; the natural logarithm of the number of subsidiaries).

Additionally, we insert fixed effects to control for varying trade tax rates within Germany. Finally, we include industry fixed effects and year fixed effects in all models to account for deviations in tax avoidance among firms in different industries (Donohoe, 2015) and to capture tax law changes that were made during the observation period (Heim & Lurie, 2012).

Empirical Analysis

Descriptive Statistics

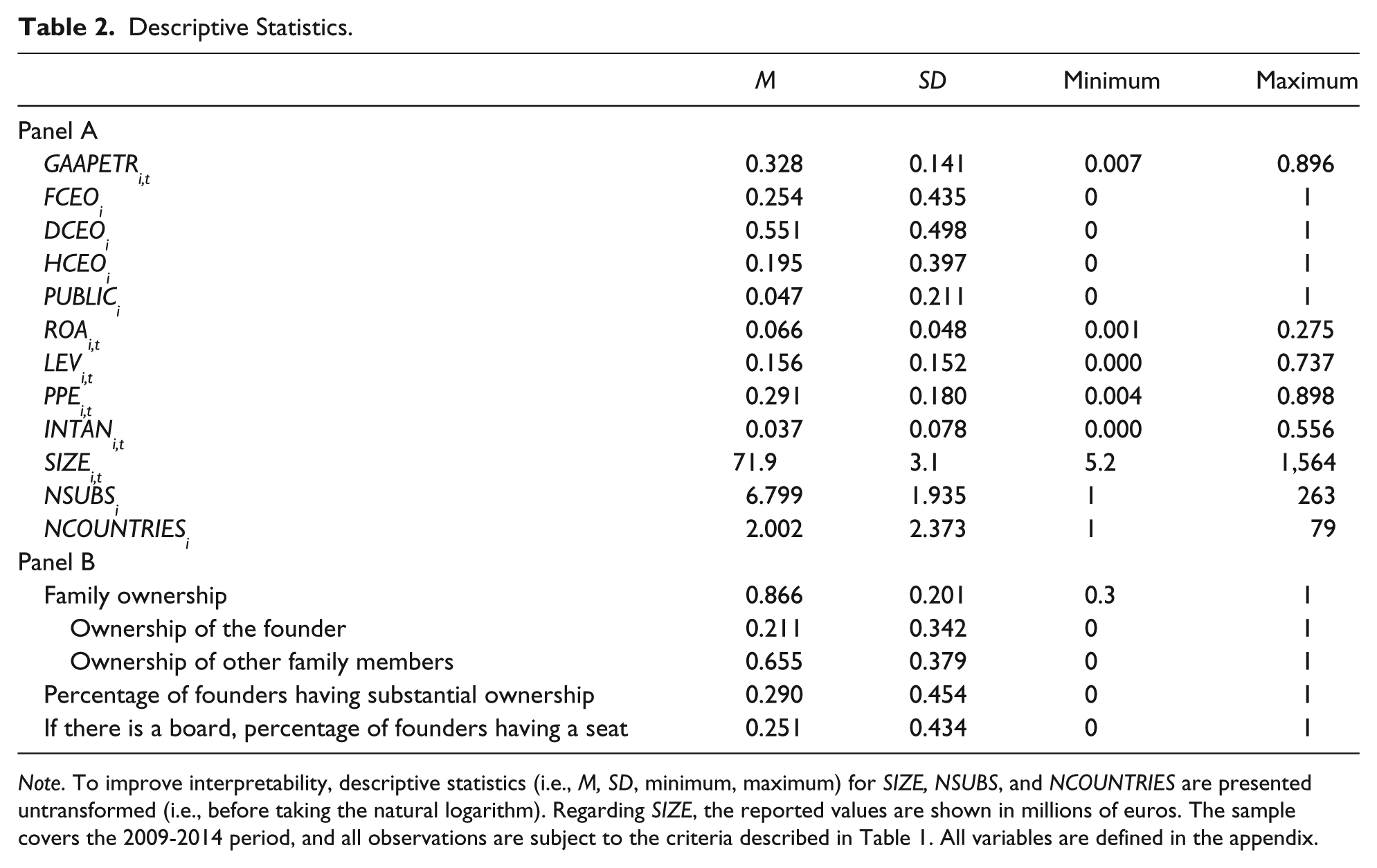

In Table 2, Panel A, we present descriptive statistics for firm characteristics of our sample. Within our sample, the average family firm shows a GAAPETR of 32.8%, has approximately €72 million in total assets, and owns approximately seven subsidiaries domiciled in two different countries. The number of subsidiaries (NSUBS) ranges from 1 (i.e., to fulfill the criterion of business groups) to 263, whereas the number of countries in which a family firm has subsidiaries (NCOUNTRIES) varies between 1 and 79. For the mean firm-year, PPE constitutes 29.1% of total assets, and INTAN equals 3.7% of total assets. Additionally, one quarter of the family firms in our sample are founder-led (25.4%), whereas more than half are descendant-led (55.1%). Less than 5% of the family firms in our sample are public family firms. Panel B of Table 2 reports descriptive statistics regarding the founder. The average founder holds 21.1% of the family firm’s equity. Additionally, 29% of the founders are substantial shareholders (i.e., more than 25% ownership). If there is an advisory or supervisory board in place, the founder has a seat in 25.1% of the cases.

Descriptive Statistics.

Note. To improve interpretability, descriptive statistics (i.e., M, SD, minimum, maximum) for SIZE, NSUBS, and NCOUNTRIES are presented untransformed (i.e., before taking the natural logarithm). Regarding SIZE, the reported values are shown in millions of euros. The sample covers the 2009-2014 period, and all observations are subject to the criteria described in Table 1. All variables are defined in the appendix.

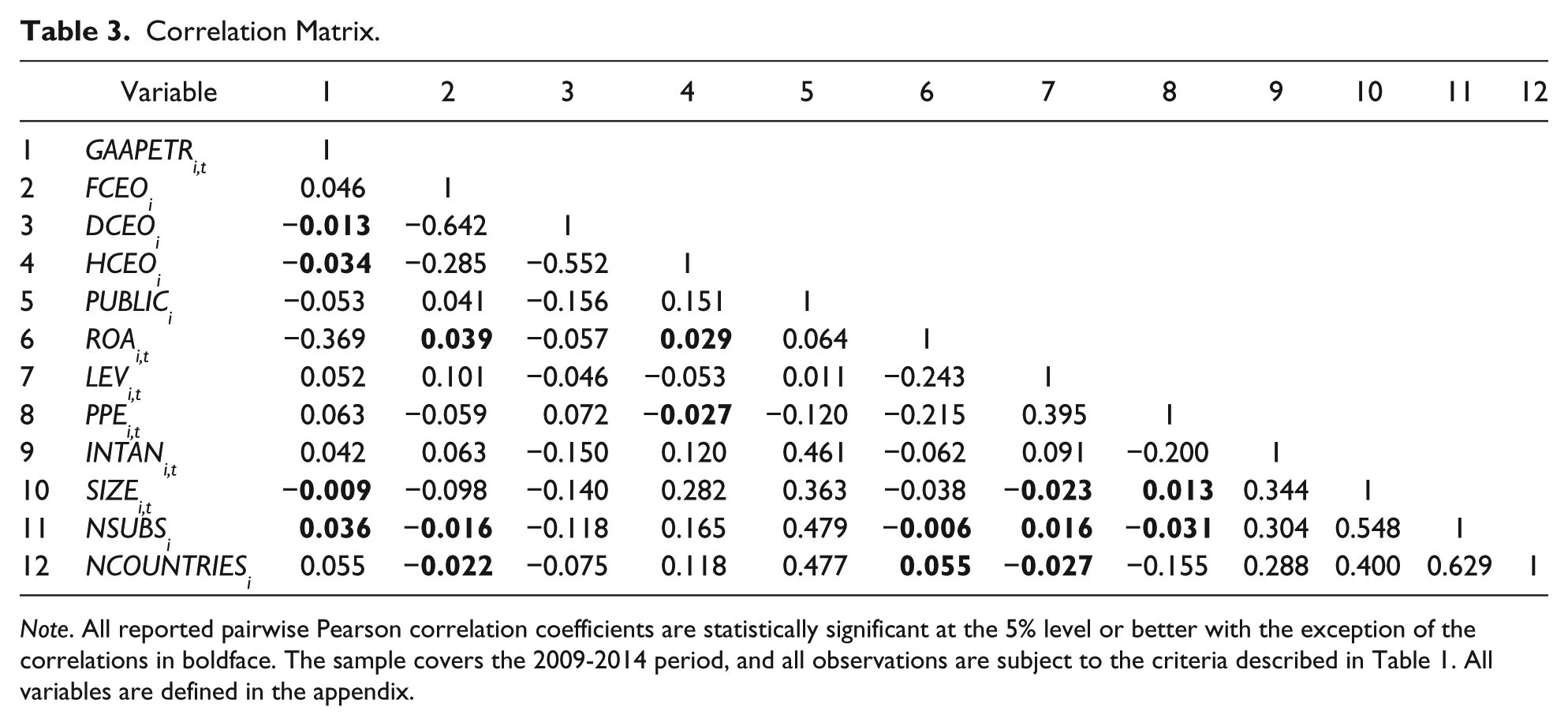

We also provide Pearson correlations in Table 3. All reported correlations are statistically significant at the 5% level or better, with the exception of the correlations in bold. Although certain variables are significant for the Pearson correlations, the magnitudes of the correlations are small. Nevertheless, consistent with prior studies (e.g., Kroll, Walters, & Wright, 2008), we conduct a test of collinearity by regressing the dependent variables on all the independent variables and calculating the variance inflation factors (VIFs) for each variable. We find that the average VIF is 1.67, and the highest VIF across the regressions is 2.19, which is well below the generally accepted threshold of 10. This finding suggests that multicollinearity is not a problem in our model.

Correlation Matrix.

Note. All reported pairwise Pearson correlation coefficients are statistically significant at the 5% level or better with the exception of the correlations in boldface. The sample covers the 2009-2014 period, and all observations are subject to the criteria described in Table 1. All variables are defined in the appendix.

Results

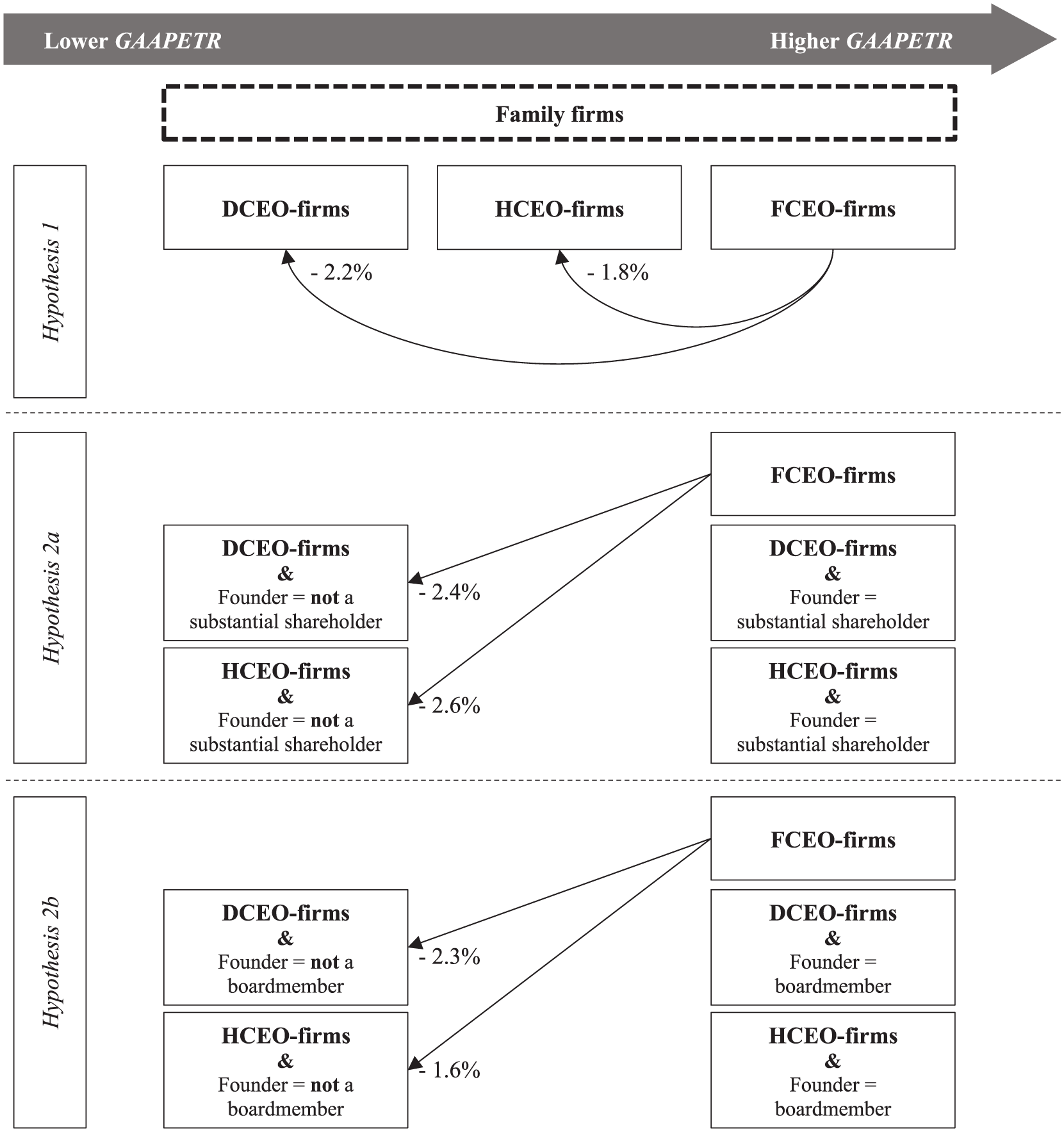

Table 4 presents the results of our ordinary least squares regressions. Model 1 shows the results for whether differences within family firms with respect to tax avoidance can be traced back to the respective CEO type. We find that founder-led family firms avoid taxes less than both descendant and hired CEO family firms. This finding supports Hypothesis 1. Economically, this result indicates that family firms governed by a founder CEO exhibit an average GAAP effective tax rate that is 2.2% higher than that of descendant CEO family firms and 1.8% higher than that of hired CEO family firms. Relating this finding to prior literature, Chen et al. (2010) compare U.S. public family firms governed by different CEO types with public nonfamily firms and find that family firms with a descendant CEO seem to avoid a similar amount of taxes as nonfamily firms, whereas founder and hired CEO family firms exhibit less tax avoidance. Thus, our results seem to be (partially) in line with these findings.

Regression Results.

Note. In all models, FCEOi is the comparison group. Fixed effects are included for different trade tax rates, industries, and years. Robust standard errors are used. t-Statistics are reported in parentheses. All variables are defined in the appendix.

Significance at the 10% level. **Significance at the 5% level. ***Significance at the 1% level.

Based on the result that founder CEO firms engage in tax avoidance less than descendant and hired CEO firms, we extend the analysis by evaluating whether founders can also affect the top management team when they possess solely indirect influence (i.e., founders are no longer part of the top management team).

First, we test whether tax avoidance in descendant and hired CEO firms is mitigated if the founder remains a substantial shareholder of the firm. In Model 2a of Table 4, the coefficients on both DCEO_FBLOCKHOLDER and HCEO_FBLOCKHOLDER are insignificant. This finding indicates that family firms with either a descendant CEO or a hired CEO do not avoid taxes more than founder-led family firms if the founder holds more than 25% of the firm’s equity. In other words, if the founder still possesses indirect influence (i.e., share of the founder more than 25%), a family firm with a descendant or hired CEO will not demonstrate a significantly different level of tax avoidance than family firms with a founder CEO. However, if the founder does not hold a substantial share of the firm’s equity, we find that family firms with a descendant (DCEO_FnotBLOCKHOLDER) or hired CEO (HCEO_FnotBLOCKHOLDER) avoid taxes significantly more than family firms with founder CEOs. These findings are in line with Hypothesis 2a. We can also interpret the economic significance of the coefficients. Descendant (hired) CEO family firms in which the founder has no substantial ownership have, on average, a 2.4% (2.6%) lower GAAP effective tax rate than founder-led firms.

Second, we analyze whether founders use a seat on the board to exercise indirect influence. In Model 2b of Table 4, the coefficients on both DCEO_FBOARDMEMBER and HCEO_FBOARDMEMBER are insignificant, which supports the notion that nonfounder CEO family firms where the founder is a member of the advisory or supervisory board do not avoid taxes more than founder CEO family firms. In contrast, we find that descendant (hired) CEO family firms with boards on which the founder does not have a seat show, on average, a 2.3% (1.6%) lower GAAP effective tax rate than founder-led family firms. These findings support Hypothesis 2b and indicate that founders can use their seats on boards as a vehicle to prevent tax avoidance strategies that could threaten the family’s socioemotional wealth.

In sum, these findings suggest that family firms with descendant or hired CEOs avoid taxes more than founder CEO family firms (Hypothesis 1). However, this effect appears to be mitigated if the founder is able to exert indirect influence in descendant or hired CEO family firms by (1) remaining a substantial shareholder (Hypothesis 2a) or (2) having a seat on the board (Hypothesis 2b). Therefore, as long as the founder is able to wield indirect influence, descendant or hired CEOs are likely to be more cautious regarding tax avoidance.

Finally, Figure 1 graphically summarizes the insights of our main results to provide a better understanding of the tested associations.

Summary of the main results.

Robustness of the Results

To verify our results, we rerun all regressions using another tax avoidance measure: permanent book-tax differences (PBTD), which can be considered as a subset of total book-tax differences. Comparing permanent book-tax differences with the GAAP effective tax rate, research typically considers the former to be a measure of higher tax aggressiveness because these differences reduce a firm’s tax liability while increasing its income (Lisowsky, Robinson, & Schmidt, 2013). Following Frank et al. (2009), we calculate the annual permanent book-tax difference for firm i in year t by taking the difference between pretax book income (PTBI) and the ratio of total income tax expense (Taxation) and the tax rate (Tax Rate). We scale permanent book-tax differences by the lagged total assets. Although the (unreported) results indicate some variation in terms of significance, this robustness test generally corroborates the results of our primary empirical analysis.

Moreover, in our main regression analysis, we use robust standard errors. However, consistent with prior research (e.g., Dyreng et al., 2010; Petersen, 2009), we also cluster standard errors at the firm level. In general, the (unreported) results remain similar.

In additional (unreported) robustness tests, we also scale GAAPETR by a number of alternative scalars—including book assets or book equity—rather than pretax income. We demonstrate that our initial results generally remain economically and statistically unchanged. We also find similar results after setting GAAPETR equal to 0 in the case of tax refunds and equal to 1 when GAAPETR is greater than 1 instead of deleting firms with extreme GAAPETRs (i.e., 0 and 1).

Furthermore, similar to prior research (Ali et al., 2007), the “family firm” attribute in our study is supposed to be sticky. More precisely, it is assumed that the mid-2015 classification applies to the entire observation period (i.e., 2009-2014) of this study. Therefore, the percentage of the family’s equity ownership could be biased. However, Bureau van Dijk’s Amadeus Shareholders database reports information on ownership structure only as of the most recent information update. It is difficult to assess the extent to which this data limitation affects the conclusions drawn from this study. In general, we assume that the ownership percentages are relatively stable over time. More precisely, we suppose that coding is very accurate for 2014, that it has perhaps a few errors in 2013 and potentially a few more errors in 2012, and so forth. We select the last 6 years that are closest to mid-2015 for our sample, ensuring that the miscoding is at an acceptable level for these most recent years. In an unreported robustness test, we use only the last 3 years of our sample, thereby minimizing potential miscoding. We find that the results are similar irrespective of the sample period. Additionally, we believe that the percentage of family ownership is highly persistent over time. To verify this assumption, we compare the used percentage of ownership (mid-2015) to the percentage of ownership in mid-2017. We find variation in the ownership structure of only 5.3% in all firms. However, the new ownership structure would not lead to a different categorization for any firm (i.e., from family to nonfamily firm or vice versa). Therefore, we believe that the stickiness of our ownership data is not a critical issue and does not significantly affect our results.

Discussion and Conclusion

We use the socioemotional wealth concept (e.g., Berrone et al., 2012; Gómez-Mejía et al., 2007) to investigate the association between tax avoidance and (different types of) family firms in greater detail. In addition to economic goals, family firms generally pursue (emotion-driven) nonfinancial objectives, for example, securing the family’s reputation and status in the community or maintaining family harmony. Therefore, focusing on nonfinancial objectives could lead to economic inefficiencies by partially ignoring the goal of maximizing firm value, which includes—but is not limited to—cost minimization. In general, a firm’s tax payments are costs, and thus, increasing tax avoidance decreases a firm’s cash outflows. However, tax avoidance should be viewed as a tradeoff between the marginal benefits (e.g., higher after-tax earnings) and both the marginal tax costs (e.g., tax expert compensation or penalties by tax courts) and nontax costs (e.g., reputational damage). This cost–benefit tradeoff could make it less beneficial for family firms to engage in tax avoidance, especially because of potential nontax costs. Both reputational and political costs of being labeled as a “poor corporate citizen” (e.g., Brown & Drake, 2014; Graham, Hanlon, Shevlin, & Shroff, 2012; Hanlon & Slemrod, 2009; Karpoff & Lott, 1993; Kim & Zhang, 2015) could threaten the family’s status in the community and may result in a loss of the family’s socioemotional wealth.

Therefore, from a theoretical point of view, we contribute to the question of why some firms avoid more taxes than others. The tax avoidance literature finds diverse (nonfinancial) incentives for current tax avoidance, such as organizational incentives (e.g., Gallemore & Labro, 2015; Higgins et al., 2015; Kubick et al., 2016; McGuire, Omer, & Wilde, 2014), organizations’ external relationships, e.g., corporate social responsibility (Chun Keung, Qiang, & Hao, 2013) or political connections (Brown, Drake, & Wellman, 2015), and the involvement of other external parties, such as auditors (McGuire, Omer, & Wang, 2012) or labor unions (Chyz et al., 2013). Steijvers and Niskanen (2014) stress the importance of nonfinancial objectives when analyzing tax avoidance in family firms. Building on this thought, we consider the presumably most prominent individual in a family firm: the founder. In this context, we provide further evidence suggesting that a family firm’s founder may be an important determinant of tax avoidance that could have previously been underestimated.

Furthermore, with this study, we join the family firm heterogeneity debate (e.g., Chrisman et al., 2005; Chua et al., 2012; Pazzaglia et al., 2013; Westhead & Howorth, 2007). By showing that tax avoidance differs depending on CEO types, Chen et al. (2010) provide initial evidence that U.S. public family firms are a heterogenous group. While acknowledging the results of their study, it is particularly important to emphasize that findings for specific contexts (e.g., the United States) may not apply to our setting (i.e., Germany). Regarding the performance of family firms, Miller et al. (2007) stress that results are sensitive to the definition of a family firm and the source of the data. Specifically, they highlight divergences between evidence from the United States on the one hand (Anderson & Reeb, 2004; McConaughy, Walker, Henderson, & Mishra, 1998; Villalonga & Amit, 2006) and from Europe and Asia on the other hand (Bennedsen, Nielsen, Perez-Gonzalez, & Wolfenzon, 2007; Claessens, Djankov, Fan, & Lang, 2002; Cronqvist & Nilsson, 2003; Maury, 2006). Therefore, in this study, we may observe a similar pattern; that is, behavioral complexities and tax avoidance outcomes in Germany could be significantly different from those in other settings (e.g., the United States). However, we find that founder CEO family firms avoid taxes less than descendant or hired CEO family firms, which is—at least partially—in line with Chen et al. (2010).

Additionally, to the best of our knowledge, our study is the first to examine whether founders are able to exert indirect influence even after stepping down as CEOs. More precisely, our results indicate that descendant and hired CEO family firms do not differ from founder CEO family firms in terms of tax avoidance if the founder (1) remains a substantial shareholder or (2) has a seat on the board. Stated differently, we contribute to the ongoing family firm heterogeneity debate by showing that the founder’s indirect influence is a factor that mitigates tax avoidance in descendant and hired CEO family firms. Therefore, our results advance existing knowledge by showing that founders’ attachment to their firms is presumably strong and that their influence does not seem to be compromised by giving up direct influence to descendant or hired CEOs. In this context, the socioemotional wealth concept could provide one explanation for the observed associations.

Moreover, our study provides practical implications. We find that there is no significant difference in terms of tax avoidance between founder CEO family firms and nonfounder CEO family firms in which the founder continues to have indirect influence. With this in mind, descendant and hired CEOs in family firms should be aware that the founder’s indirect influence could reduce their opportunities to introduce their own business strategies (Harvey & Evans, 1995) and may therefore limit their options regarding tax avoidance. Additionally, without considering these new insights, prospective shareholders, creditors, or suppliers may reach misleading conclusions regarding the economic orientation of nonfounder CEO family firms. More precisely, ignoring the founder’s remaining indirect influence could lead to the expectation that priority is given to economic goals—even though nonfinancial objectives remain a part of the corporate philosophy.

Finally, we are cautious in drawing political implications from our study’s results. Nevertheless, in recent years, the media have extensively covered the tax avoidance strategies of well-known public firms, resulting in controversial political debates. One outcome of these ongoing debates is the base erosion and profit shifting (BEPS) project of the Organisation for Economic Co-operation and Development (OECD), which provides an action plan to reduce BEPS within all OECD countries (OECD, 2015). However, only a minority of German firms (and firms worldwide) are public firms. Additionally, more than half of the GDP in OECD countries is generated by private firms (e.g., Jacob, Rohlfing-Bastian, & Sandner, 2016). We find that public family firms avoid taxes significantly more than private family firms (i.e., negative coefficient on PUBLIC in all tests). Within our sample, the average GAAPETR for German public family firms is 29.23%, whereas the average GAAPETR for private family firms is 32.99%. Therefore, the need for a comprehensive OECD action plan, which was introduced mainly because of public firms’ tax avoidance strategies, seems to be controversial, and the consequences could be misleading, at least with regard to private family firms.

Readers should use caution when generalizing the results of this German study to other countries for at least three reasons. First, we use GAAPETR as our main proxy for tax avoidance. In the U.S. system, additional tax avoidance proxies could be used (e.g., cash ETRs or unrecognized tax benefits). Data limitations regarding the item “taxation” are pervasive in the Amadeus database. Whereas we can calculate GAAPETRs, we cannot use cash ETRs. Because of the missing value for cash taxes paid, misinterpretations can occur. However, by using GAAPETR, we are confident that our measure represents tax avoidance in Germany in the most precise manner possible. Therefore, all other aspects of tax planning (e.g., tax sheltering, tax fraud, or tax evasion) are outside the scope of our study. These aspects of tax planning may be associated with other—and perhaps different—consequences for public and private family firms.

Second, simplifying assumptions are necessary. We use accounting data, not actual tax returns. When financial statement data are used, another limitation arises because accounting rules vary across countries, especially between U.S. and German firms (U.S. GAAP vs. IFRS and the German GAAP). However, we argue that the two standards are similar in terms of their objectives to inform capital market participants and to include and value assets and liabilities.

Third, on a more general level, any interpretation of our results requires consideration of the German institutional context. However, some German institutional characteristics may be interesting from an international perspective and may add a new viewpoint to the previous literature. More precisely, as the largest economy in the EU, Germany is highly dependent on the well-being of family firms because most (private) firms are family firms. We are confident that the results of our German study have relevance for other countries—at least for countries with a similar level of economic development. However, depending on country-specific aspects (e.g., the economic importance of family firms, stronger capital market pressure, and higher levels of book-tax conformity), the results and their interpretation may vary.

Some data limitations in our study might serve as a starting point for future research. We assume that the “family firm” attribute does not vary within the entire sample period. Therefore, future research could examine in greater detail the association between tax avoidance and time-dependent changes in ownership structure. Additionally, more detailed information on the top management team (e.g., the exact function and/or biographical characteristics of each manager) would enable us to further investigate the association between the top management team and tax avoidance in family firms. Moreover, future research could analyze further channels that founders may use to exert indirect influence (e.g., contractual provisions in donation contracts between founders and descendants). These examples are just a few research ideas that are raised by this study and that we believe can lead to future insights.

Footnotes

Appendix

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.