Abstract

Gender inequality in control of household finances is a well-known phenomenon. We investigate whether such imbalance also extends to the delegation of financial decision-making (FDM) responsibilities to one’s spouse in old age. This study reports the results from an incentivized delegation experiment among Australian couples of age ≥60 years. Participants were required to complete FDM tasks, which they had the option of completing independently or delegating to their spouse. The odds of women delegating to their spouse were found to be nearly 25 times higher than that of men. This gender difference in delegation was not explained by differences in financial competence, education, age, or cognitive status. The likelihood of delegation increased with the financial competence of the spouse. Individuals who had the option to delegate selectively delegated more often and earlier than those who could only delegate irrevocably. Our evidence suggests that gender norms and control play a dominant role in the delegation of FDM within older couples and can override specialization or efficiency considerations.

Keywords

Financial management plays an important role in enhancing the well-being of partners in households (Kulic, Minello, and Zella 2020; Lersch 2017). Financial decisions within households are often made by a designated decision maker (Hsu 2016); however, they are more likely to be delegated or shared between older spouses (Gamble et al., 2015) because old age is associated with cognitive decline and a reduced capacity to make financial decisions (e.g. Agarwal et al., 2009; Bonsang and Costa-Font2020). Nevertheless, the transfer or sharing of financial decision-making (FDM) does not always happen in a timely manner, putting older households at risk of making inappropriate financial choices (Finke, Howe, and Huston 2017). FDM is often transferred to the spouse well after the primary financial decision maker has begun experiencing difficulties in handling money (Hsu and Willis 2013).

In most allocative systems, men have traditionally had greater control over household finances (Anderson 2017; Kenney 2006). Poor health, including cognitive decline, can erode the capacity of the primary financial decision maker and make it necessary to share the decisional burden with the spouse (Luehrmann and Maurer 2007). Despite extensive research on the determinants of primary FDM status within the household (Agarwal and Mazumder 2013; Anderson 2017; Dobbelsteen and Kooreman 1997; Hu 2021; Johnston, Kassenboehmer, and Shields 2015), how the transfer of such responsibilities takes place among older couples has received little attention. Our study addresses this gap by providing insights into the delegation behavior of married couples in late adulthood. Previously, Hsu and Willis (2013) examined the transfer of FDM responsibilities to spouses based on efficiency parameters. Their study focused on the relative decline in the primary financial decision maker’s cognitive abilities vis-à-vis their spouse and how this change in “comparative advantage” within the household relates to their willingness to delegate. Similarly, Gamble et al. (2015) also investigated the relationship between cognitive decline and seeking assistance with financial decisions. In contrast, our study looks beyond efficiency considerations to explain delegation behavior. Our primary interest is to understand whether the gender inequality in household FDM also extends to the delegation of these responsibilities to spouse in old age. Because delegation in other contexts has been shown to be related to efficiency or task specialization (Bartling and Fischbacher 2012; Hamman, Loewenstein, and Weber 2010) and control over delegation (Bartling, Fehr, and Herz 2014; Bobadilla-Suarez, Sunstein, and Sharot 2017), we also investigate their role in the transfer of FDM responsibilities to one’s spouse. We address three questions: (1) Does the likelihood of delegating FDM to the spouse differ between men and women? (2) Is the gender difference in the delegation of FDM in couples explained by their relative competence (specialization)? (3) Is the likelihood of delegating FDM to a spouse influenced by the control one has over the delegation decision?

We use an incentivized experiment to observe delegation in married couples of age ≥60 years who undertake a series of FDM tasks that they have the choice to complete independently or delegate to their spouse The participants in our study exhibit a strong desire to retain agency. However, we find that women are far more likely than men to transfer FDM responsibilities to their spouses (with an odds ratio of nearly 25). This gender difference in delegation behavior is not explained by differences in education, financial competence, age, or cognitive status, which suggests that gender identity and norms can override efficiency considerations. Individuals also seem more willing to delegate when they can assign tasks to their spouse selectively. Our study contributes to the literature on (gendered) division of household labor by identifying the factors influencing individuals’ willingness to delegate FDM to their spouse, which is an important marker of their preparedness to avoid financial mismanagement in old age. Decision makers who under-delegate often suffer serious financial loss (Bobadilla-Suarez, Sunstein, and Sharot 2017; Owens, Grossman, and Fackler 2014). Our results raise concerns about women’s financial well-being in old age, since they tend to outlive their husbands (Hsu 2016) and, therefore, disproportionately bear the adverse consequences of poor financial decisions. Also, if financial decisions are not delegated in a timely manner, women may find themselves unprepared to take over such responsibilities in the event of their spouse’s death or loss of decision-making capacity.

Theoretical And Empirical Context

Theoretical explanations for the household division of labor have been proposed in both the economics and sociology literature. These constructs can be grouped under three broad perspectives: efficiency/time availability, bargaining power/relative resources, and gender identity/norms. In the efficiency or specialization framework in economics, family members who have a comparative advantage or are relatively more efficient in market activities specialize in them and spend less time on household activities (Becker 1981). The division of financial management responsibilities among married couples may be part of the overall efficient allocation of tasks within the household, where the spouse with greater expertise in financial matters is responsible for making financial decisions. Conversely, the “nonspecialist” spouse relinquishes FDM rights to the “specialist,” ensuring a more “efficient” outcome for the household. Closely aligned with the efficiency framework is the time availability perspective in sociology, which posits that the time each partner spends working outside the home influences their share of the housework (Davis, Greenstein, and Gerteisen Marks 2007): Partners who spend more time on paid employment would have less time to spend on household labor (Artis and Pavalko 2003). The presence of children in households also leaves women with less time to specialize in market-based activities that could enhance their financial skills (Blair and Lichter 1991).

Empirical studies exploring lower female participation in household FDM find that women display lower levels of financial literacy (Fonseca et al., 2012; Preston and Wright 2019) and are often aware of having fewer financial skills (Lusardi and Mitchell 2011). From a specialization perspective, the gap in financial literacy may explain why men are primarily responsible for FDM within the household. Men may also assume the role of primary financial decision maker because at the time of marriage, the husband is often older than the wife and, therefore, possesses a higher stock of financial knowledge (Hsu 2016).

The second framework of the household division of labor emphasizes the bargaining power of each spouse. In the cooperative bargaining framework, the spouse with more power is likely to make financial decisions (Bertocchi, Brunetti, and Torricelli 2014). According to the relative resources theory, each partner’s bargaining power depends on the resources they control within and outside the household (Mannino and Deutsch 2007). For example, the wife’s contribution to family income is related to the allocation of household labor (Bianchi et al., 2000; Knudsen and Wærness 2008; Mannino and Deutsch 2007). The wife’s age, education level, and income also influence the extent of her participation in household FDM (Bertocchi, Brunetti, and Torricelli 2014). Johnston, Kassenboehmer, and Shields (2015) find that relative age, education, employment, and the wages of male and female partners are significant determinants of who “holds the purse strings.”

The difference in economic power between men and women may result in the latter participating less in household financial decisions. When heterosexual couples in the United States apply for housing loans, men sign first in 89 percent of the applications, which is largely explained by this difference in economic power between the genders (Agarwal et al., 2018). However, whether economic independence gives women “greater voice” in household decision-making is not a settled question. Although some studies show that women’s decision-making power increases with greater economic independence (Lomelí 2008), others (e.g. Bartley, Blanton, and Gilliard 2005) find that changes in women’s economic status do not significantly alter their decision-making power within married households. Women’s earnings are often treated differently from men’s and pooled with the family’s collective income or earmarked for meeting specific family expenses (Phipps and Burton 1998; Zelizer 1989).

The third framework for the allocation of household tasks focuses on gender norms and constructs and how they create inequity in the control of household decisions. Cunningham (2001) posits that individuals are socialized into male or female gender roles with expectations about how they should fulfill them. Contemporary scholarly research in sociology favors more contextual explanations to gendered division of household labor where societal expectations play a major role (Geist and Cohen 2011; Risman and Davis 2013). Foremost among these is the “doing gender” framework which suggests that gender is something that is performed in social interactions due to a sense of moral accountability (West and Zimmerman 1987). For example, to “perform gender” women may spend more time on housework after marriage. This perspective is supported by research showing that the gains made by women in income-producing activities do not translate into a proportional decline in their share of household labor (Fuwa 2004; Knudsen and Wærness 2008). Others suggest that when women earn higher incomes, they still do most of the household chores to emphasize their domestic contributions and de-emphasize economic contributions, to preserve the husband’s dominance (Tichenor 2005; West and Zimmerman 1987). Even among professional couples where men defer to their partner’s decisions, it usually falls upon the women to do the emotional and practical work required in maintaining their work–family balance (Wong 2017).

A variant of the gender ideology perspective is the gender construction or identity perspective (Lachance-GrzelaBouchard 2010), according to which men and women allocate household responsibilities in a manner that protects and reinforces their gender identities (Bianchi et al., 2000; Erickson 2005). Akerloff and Kranton (2000) incorporate the “sense of self” in economic analysis, where agents follow prescriptions to maintain their self-concepts. In their model, the husband suffers identity loss when his wife earns more than half of the household income and he is required to do more housework. To restore his sense of identity, household tasks are allocated in line with established gender norms, such as men primarily making financial decisions, although this may adversely affect the household’s economic efficiency. Similarly, Bertrand, Kamenica, and Pan (2015) find that the household division of labor is explained by gender norms rather than specialization. Mader and Schneebaum (2013) report that whereas women make more daily spending decisions, men are responsible for making major financial decisions. Even in Sweden, one of the most “gender equal” nations, gender ideology has been found to normalize men’s “natural” entitlement to money and women’s responsibility to make it “stretch” (Nyman 1999).

Although all three frameworks assist our understanding of the division of household tasks, there has been growing criticism of the specialization and bargaining power models in explaining the allocation of household FDM responsibilities. The efficiency model has been questioned because it assumes the household as a single entity with spouses pooling their resources, thereby disregarding the individual preferences of the husband and wife (Mader and Schneebaum 2013). Members with a larger share in the management of household finances may want to influence decisions in line with their preferences (Bertocchi, Brunetti, and Torricelli 2014; Luehrmann and Maurer 2007). While the bargaining power framework accommodates heterogeneity of preferences among household members, the model’s predictions have not always been empirically supported. Notably, women’s decision-making power has not always been found to change with their rising status in the employment market or share of family income (Bartley, Blanton, and Gilliard 2005). Moreover, husbands have been found to typically assume responsibility for major financial decisions (e.g. investments, retirement planning), whereas wives are generally in charge of managing smaller day-to-day financial chores such as paying bills and shopping for groceries (Fonseca et al., 2012).

Hypothesizing The Differential Likelihood Of Delegation To Spouse

The likelihood to delegate to a spouse may differ between individuals across multiple dimensions. Partners of different genders and with differential desires for control, levels of financial competence, and cognitive abilities may have different opportunities and constraints to delegate decision-making to a spouse in old age.

Recent studies in experimental economics show that individuals have an intrinsic desire for control over their decisions and that retaining decision-making rights carries a positive intrinsic value. Owens, Grossman, and Fackler (2014) document the existence of a control premium—a willingness to forego a monetary sum to retain autonomy over decision-making. Similarly, Bartling, Fehr, and Herz (2014) find that individuals intrinsically value decision rights beyond their instrumental benefit, and this preference can influence delegation decisions. The desire for control remains strong even when the decision maker is aware that delegation is optimal (Bobadilla-Suarez, Sunstein, and Sharot 2017).

Research has confirmed the desire of older adults to distance themselves from being categorized as “old” and maintain a relatively “youthful” identity. Townsend, Godfrey, and Denby (2006) find that older individuals do not describe themselves as “old” even when acknowledging their age. They also idolize their age peers who “kept going” and look down on those who seemed to be “giving up.” Similar findings are reported by Minichiello, Browne, and Kendig (2000): Being “old” is seen negatively, and older adults try to disassociate from such categorization by portraying themselves as fit, active, and intellectually developing. Even among the oldest of old, perceived level of autonomy plays an important role in their perception of life satisfaction (Enkvist, Ekström, and Elmståhl 2012), and retaining autonomy seems desirable and negotiable (Pirhonen et al., 2016).

While autonomy is preferred by both genders, the desire for control over FDM may not manifest in equal measure. Pirhonen et al. (2016) conclude that gendered ideals and values play an important role in older people’s conceptions of autonomy. If men are used to making most of the financial decisions on behalf of their family when young, they may experience a loss of autonomy in relinquishing the right to make such decisions in old age. In contrast, women may not feel such a loss of control in delegating FDM to their spouse because doing so does not change the status quo.

Individuals may also under-delegate due to overconfidence or a tendency to overestimate their knowledge (Fischhoff, Slovic, and Lichtenstein 1977). Men have been found to be more overconfident than women (Barber and Odean 2001; Lundeberg, Fox, and Punćcohaŕ 1994), particularly in tasks that are perceived to be in the “male domain” (Lundeberg, Fox, and Punćcohaŕ 1994). Men reportedly feel more confident than women in handling money (Prince 1993). This difference in overconfidence implies that men may not feel the need to delegate even when there is an economic incentive to do so.

Furthermore, older people may prefer to negotiate their level of autonomy based on their abilities (Pirhonen et al., 2016). Dunér and Nordström (2010) observe that older persons want to be in total control of how they receive assistance. Because delegation arrangements can involve different levels of control, we also investigate whether the delegation mechanism itself influences the willingness to delegate. If individuals value control (Owens, Grossman, and Fackler 2014), then they would be more willing to delegate when they are able to retain some control over the delegation decision. For example, individuals who can terminate delegation or delegate tasks selectively when required would be more likely to delegate compared with those who do not.

Sunstein and Ullmann-Margalit (1999, 11) propose that “small, reversible steps” are preferable in delegations when the decision maker “lacks reliable information and reasonably fears unanticipated bad consequence.” If the principal has the control to delegate selectively or revoke delegation at any point, the perceived cost of delegation is reduced. 1 Consequently, the individual may demonstrate a higher willingness to transfer or share decision-making responsibilities than someone who is required to relinquish all control to the delegate. Reversibility ensures that decision-making can be shifted in either direction if problems arise (Sunstein and Ullmann-Margalit 1999).

Data And Method

Sample Selection

Participants were married Australian couples of age ≥60 years and residing in the greater Brisbane area. It was a condition of participation that the couples were married and cohabited in the same residence. After we obtained approval from the university ethics committee, we recruited participants via paid advertisements in community newspapers and presentations to community organizations. All potential participants completed the Modified Telephone Interview for Cognitive Status (TICS-M), which included a validated screening for abnormal cognitive decline (Welsh, Breitner, and Magruder-Habib1993). Because the focus was on FDM in the context of normal aging, exclusion criteria included diagnosis of dementia or other neurological disorder, major psychiatric illness, or serious brain injury. All couples who completed the screening interview were given an A$15 gift card, regardless of their eligibility to participate in the study.

Of 206 individuals who completed the screening, 50 did not qualify because they or their spouse had a medical history that made them ineligible, and/or because they failed to pass the cognitive screening. 2 Among eligible couples, 13 couples declined to participate. Of the remaining 130 individuals who agreed to participate, one couple could not complete all the study components. The final sample comprised 64 couples (n = 128), with an average age of 71.5 years (standard deviation = 6.52; median = 70.17).

Study Design

Both spouses individually participated in (1) a delegation experiment, (2) a financial competence test, and (3) a cognitive assessment. All three components were completed using pen and paper. The couples were given the choice to complete the study at the campus of the first author’s university or at a suitable location at a time convenient for them. No communication between the spouses was allowed, and two separate locations (in the same venue) were used for every couple to ensure that participants completed the tasks without assistance from their spouses. Because every participating couple undertook the study on different dates or time slots, there was no possibility of experiment contamination through information leakage between different couples or any kind of peer effect. Each participant received an A$30 gift voucher. Those who completed the study at the university campus received an additional A$10 per couple, as well as parking permits.

Delegation Experiment

Each spouse was presented with 10 FDM tasks that they would typically encounter in daily life, such as credit card use, household budgeting, and managing investments. In each task, they were required to select the most appropriate response from four choices. Most of the FDM tasks were based on questions from the Moneysmart website, an online financial guidance service provided by the Australian Securities and Investments Commission, and the online edition of The Daily Telegraph, a London-based newspaper that is frequently cited in economics and finance studies (e.g. Sikka 2009; Yeoh 2011). One task was adapted from Agarwal and Mazumder (2013). In each of the questions, the optimal (and sub-optimal) responses were well defined. For example, one task asked the participants:

You want to invest $4,300 for two years. Your bank offers a choice of four deposit accounts. Which account would you choose in order to get the highest return? Account 1—pays 3.1% per annum interest paid on a monthly basis Account 2—pays 3.25% per annum interest paid on an annual basis Account 3—pays 3.24% per annum interest paid on a monthly basis Account 4—pays 3.15% per annum interest paid on an annual basis

Participants were told that every FDM task needed to be either attempted or transferred to their spouse. Participants were required to respond to their own set of tasks before they could attempt the task(s) delegated by their spouse. For each task, one point was awarded to the participant for selecting the most appropriate response, regardless of whether it was provided by themselves or their spouse (where a task was delegated). The points for all 10 tasks were aggregated to assign an FDM score to each participant. Participants were told that if their scores were in the top quintile of our sample, they would become eligible for a random draw to win one of three iPads, five Kindles, and 10 Fitbits. Thus, they were aware that to maximize their own FDM scores and increase their chance of receiving a prize, they needed to decide judiciously whether to delegate tasks to their spouse.

We created two sets of 10 FDM tasks for the experiment. For every couple, we assigned a different set to each spouse such that each set was assigned to an equal number of male and female participants. For both sets, the tasks were designed to get progressively more difficult. 3 This design was used for two reasons. First, we wanted to ensure that participants were not overwhelmed by the initial tasks, in which case they might give up prematurely. Second, it also served to check whether participants understood the instructions and seriously attempted to complete the tasks. If both conditions were satisfied, we expected less delegation for the initial tasks, which were easier, than for the later tasks, which were more difficult.

To test whether the option to revoke the transfer of decision-making responsibility influences individuals’ willingness to delegate, we randomly assigned 50 percent of the couples to a “revoke” treatment. While all couples had the choice to delegate FDM task(s) to their spouse at any point, only couples in the “revoke” group could selectively delegate a task to their spouse but revoke their delegation for any of the subsequent tasks. In contrast, for couples in the “no revoke” control group, once an FDM task was delegated, only the delegated person could respond to the subsequent tasks. 4

The serial numbers of any delegated tasks were recorded. Once the participants completed all the allocated FDM tasks they wanted to attempt on their own, they were advised whether their spouse had delegated any FDM tasks to them. The exchange of the FDM task questionnaires between spouses, where required, was managed by two research team members (one stationed at each spouse’s location) who discreetly cross-reported to each other via smartphones.

Financial Competence Test

Both spouses then completed a financial competence test. This assessment investigated whether higher (or lower) competence compared with the spouse, which we used as a proxy for specialization within the household, was related to a lower (or higher) propensity to delegate. We used the 38-item Financial Competence Assessment Inventory (FCAI; Kershaw and Webber 2008), a performance-based assessment that measures strengths and weaknesses in six aspects of financial competence: everyday financial ability, financial judgment, estate management, cognitive ability related to financial tasks, debt management, and support resources. 5 The test included writing checks to pay hypothetical bills, identifying items in bank statements, and selecting items from a shopping menu given a budget constraint. Participants were also tested on their financial awareness, such as their understanding of banking protocols (e.g. overdrafts) and insurance plans. Of 38 questions, 32 were scored on a 5-point scale, from 0 = “no awareness” to 4 = “complete understanding.” The remaining six questions had yes/no responses and were scored 1 or 0 for correct and incorrect responses, respectively. The scores for all responses were aggregated to assign each participant an FCAI score, with higher scores indicating greater financial competence.

Cognitive Assessment

Participants finally completed the Informant Questionnaire on Cognitive Decline in the Elderly (IQCODE), a validated instrument widely used as an index of general cognitive impairment (Jorm 1994). The IQCODE is based on an individual’s ratings of their spouse’s cognitive abilities (16 items) on a 5-point scale. This test asked whether, compared with 10 years ago, these abilities had (1) much improved, (2) slightly improved, (3) not changed much, (4) gotten slightly worse, and (5) gotten much worse. 6 Scores were averaged across all questions for an overall score that ranged from 1 to 5. The IQCODE scores were used as control variables in our explanatory model of delegation.

Empirical Strategy

We first performed descriptive analyses to identify patterns in the delegation of FDM tasks, particularly in relation to gender, financial competence, and level of control over delegation. Next, we fitted several probit regression models to explore how gender, FCAI score (proxy for financial competence relative to spouse), and the option to revoke delegation (proxy for control over delegation) were related to delegation to spouse (a binary response variable, binary as a participant either delegated to their spouse or did not). For independent variables, we constructed dummy variables for gender, FCAI score (whether a participant had a lower score than their spouse), and control (whether the participant had the option to “revoke” delegation). We initially estimated the relationship between delegation and each of these three variables of interest both individually (Models 1–3) and together (Model 4). Next, we included two covariates: participants’ education and age. In our final two models (Models 6 and 7), we also included two IQCODE scores: one completed by the participants representing their perception of the change in their spouse’s cognitive status, and the other by their spouse denoting the spouse’s perception of the change in the participant’s cognitive status over the last 10 years. The full regression Model 6 is represented by

where

Results And Discussion

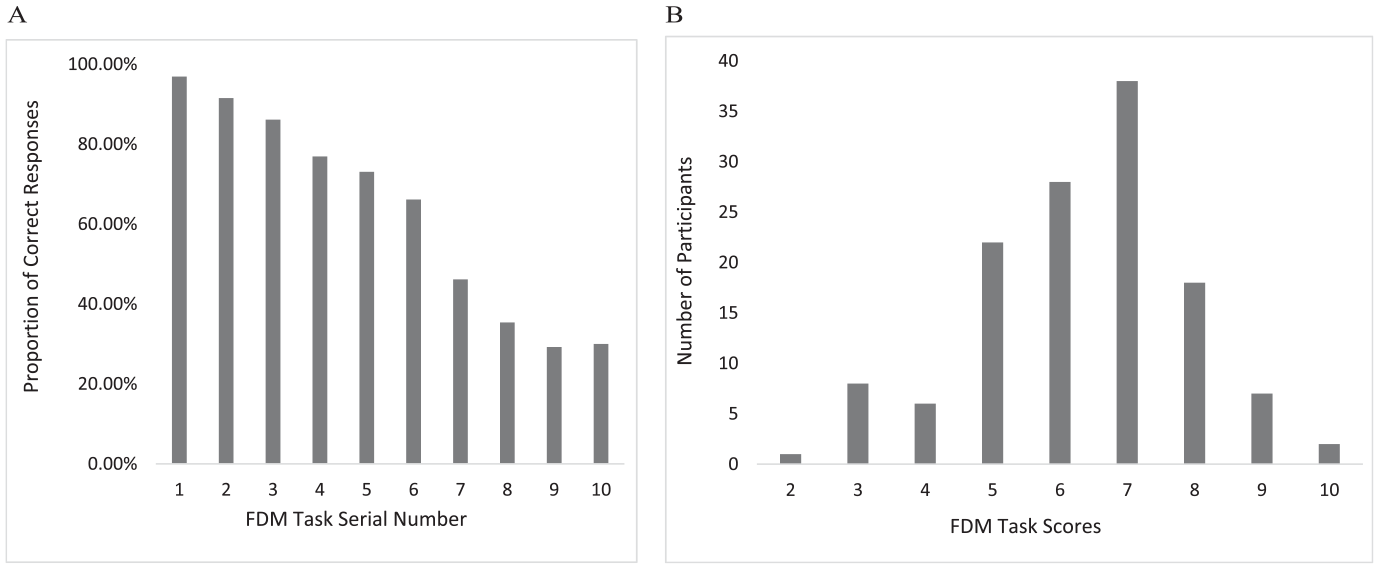

Delegations were observed in only 37 of the 64 couples. Across all 128 participants, only 38 delegated one or more FDM tasks to their spouses. 7 In other words, 70 percent of the participants did not delegate any task to their spouses. Such a high proportion of nondelegating participants in our sample suggests a tendency to retain agency over financial decisions. If participants understood the task instructions and made a serious effort to complete them, we would expect to see them delegate fewer of the initial FDM tasks but more of the later, as the tasks were designed to become progressively more difficult. Participants’ delegation decisions were consistent with this pattern. For the first five FDM tasks, only 10 participants delegated a total of 14 tasks, whereas for the last five FDM tasks, 38 participants delegated a total of 90 tasks. The number of correct responses to individual FDM tasks, as shown in Figure 1A, also suggested that participants found the tasks become increasingly more difficult. The distribution of participant scores, which aggregates the number of correct responses by each participant, is shown in Figure 1B. The median score was 6, with very few participants recording very high or low scores. The minimum score obtained was 2 (recorded by only one participant). Similarly, the maximum score of 10 was obtained by only two participants.

Participant Performance in FDM Tasks. (A) Performance on Individual Tasks. (B) Distribution of Participant Aggregate Scores

Gender, Financial Competence, and Delegation

Descriptive analysis revealed a stark difference in delegation based on gender. Of the 38 participants who delegated, 35 (~92 percent) were women. Of the 64 male participants, only three (<5 percent) delegated one or more FDM tasks to their spouses. In contrast, among the 64 female participants, 35 (~55 percent) delegated one or more tasks to their spouses. The likelihood of delegation among women compared with men was nearly 25-fold (odds ratio 24.54, p < .0001). The results lend preliminary support to Hypothesis 1A.

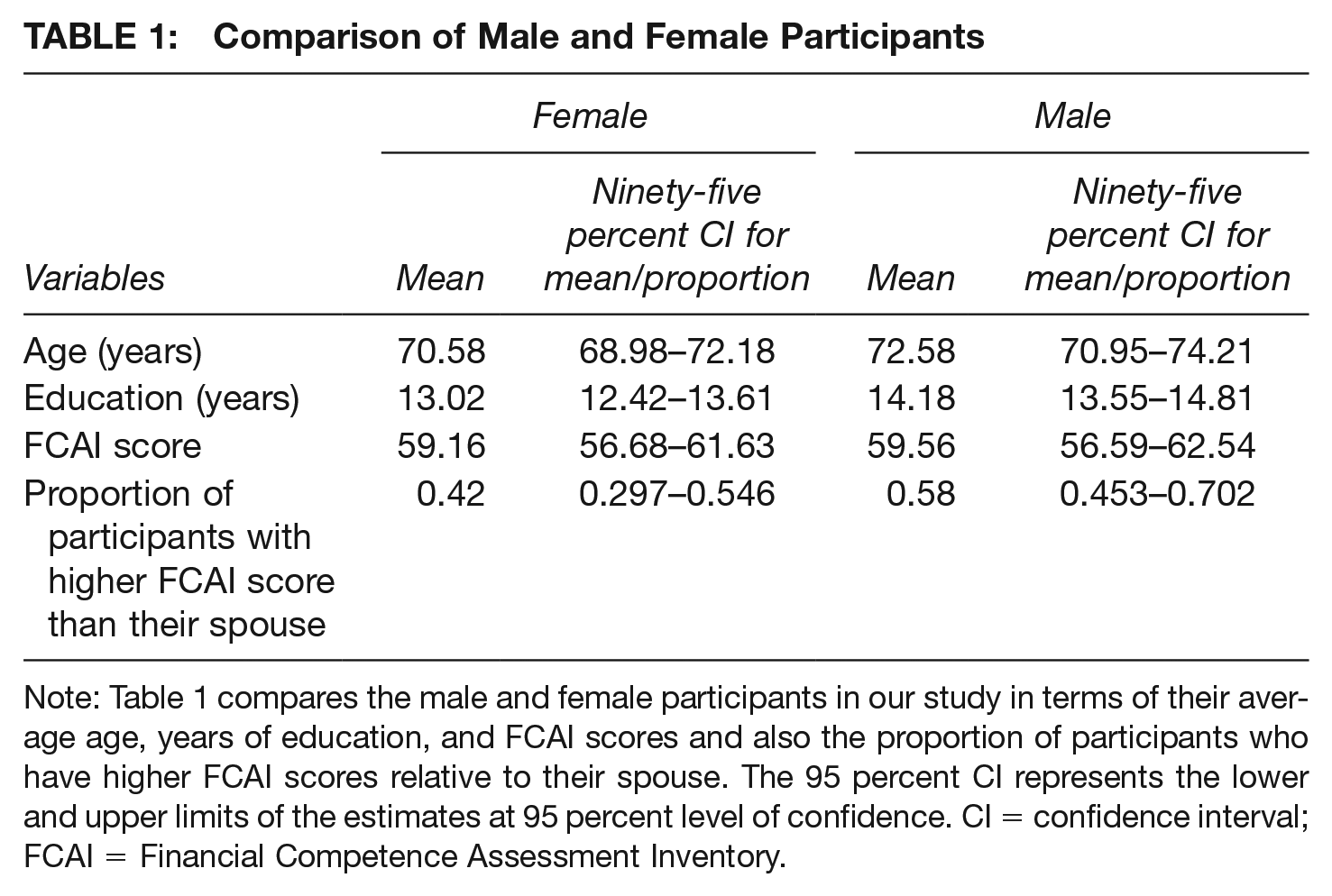

We then examined whether this gender difference in delegation behavior might be explained by the difference in the spouses’ financial competence. For example, if most men in our sample obtained higher FCAI scores than their spouses, this might explain the higher female delegation rate. Table 1 provides descriptive statistics for the male and female participants in terms of their FCAI scores, years of formal education, and age. In 27 of the 64 couples, women had higher FCAI scores than their spouses. t-Tests for difference in means (and proportions) did not show any significant difference between the mean FCAI scores of men and women (or the proportion of men and women who had higher FCAI scores than their spouses). However, men were, on average, more highly educated (p < .01) and slightly older than their spouses.

Comparison of Male and Female Participants

Note: Table 1 compares the male and female participants in our study in terms of their average age, years of education, and FCAI scores and also the proportion of participants who have higher FCAI scores relative to their spouse. The 95 percent CI represents the lower and upper limits of the estimates at 95 percent level of confidence. CI = confidence interval; FCAI = Financial Competence Assessment Inventory.

A concern could be that our FDM tasks were poorly designed, and, therefore, participants’ task performance was unrelated to their financial competence. To assess this possibility, we tested whether the FCAI scores predicted participant performance in the FDM tasks. We found a significant positive association between the participants’ FDM and FCAI scores (Pearson correlation coefficient = 0.298). When we excluded observations of participants who delegated to their spouse (as their FDM scores partly reflected efforts from their spouse), a similar correlation of 0.30 was observed. In both cases, the relationship was statistically significant (p < .01). Given this positive association, we expect that participants with lower (higher) FCAI scores than their spouses would delegate (not delegate) FDM tasks if they behaved strategically to maximize their FDM score in response to the incentives.

To establish which member of the participating couple was the primary financial decision maker in real life, their relative FCAI scores were used as a proxy for “specialization” within a household. We examined whether higher (lower) FCAI scores relative to their spouse made participants more (less) likely to delegate. While many participants (41 percent) with lower FCAI scores than their spouses chose to delegate one or more tasks, most (59 percent) did not. Among participants with higher FCAI scores than their spouses, delegation was significantly lower (18.75 percent). Hence, there is some evidence of participants delegating strategically to maximize their scores.

Because more than 92 percent of the delegations were made by women, we examined their delegation behavior according to their FCAI scores relative to their spouses. Eleven of the 27 (40.7 percent) women with higher FCAI scores than their spouses still elected to delegate. Among the 37 women who had lower FCAI scores than their spouses, 24 (64.9 percent) made delegations. The difference in delegation rates between the two groups was significant (p < .05).

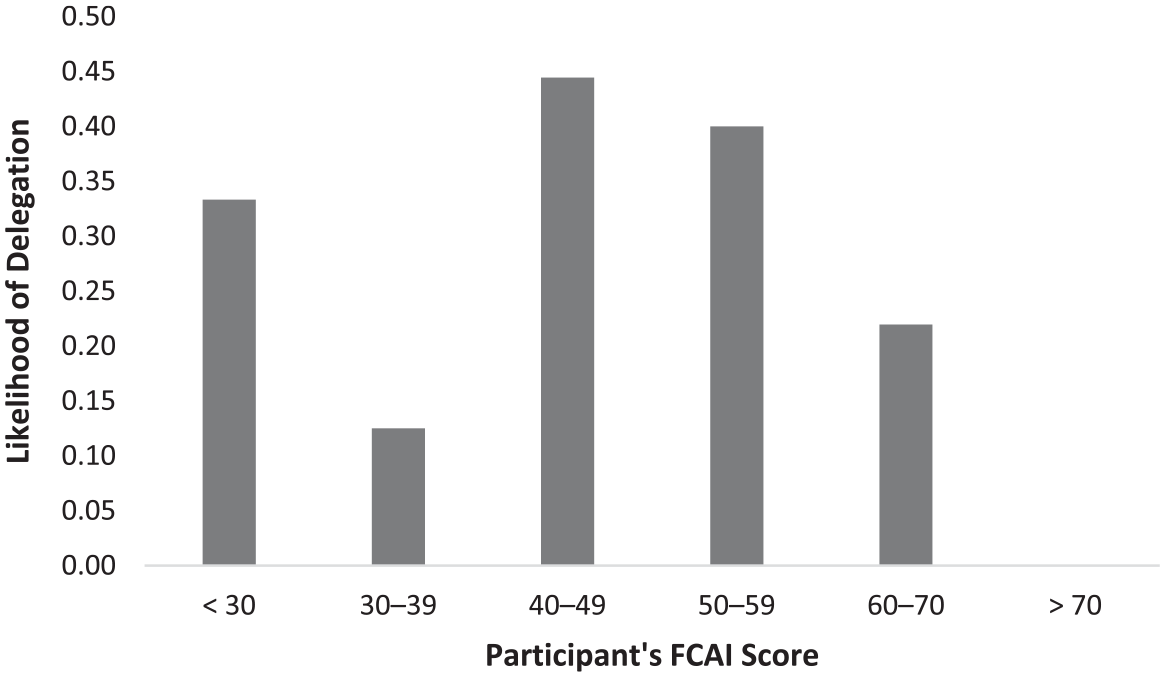

Intuitively, individuals with low financial competence would be expected to delegate more often to their spouse. However, no clear trend was observed in relating participants’ own FCAI scores with their delegation behavior. Figure 2 shows the proportion of participants delegating FDM tasks to spouses, categorized by their FCAI scores. Individuals whose FCAI scores were in the middle ranges (40–49, 50–59) appeared more likely to delegate to their spouses than those with very high or low scores.

Probability of Delegation and Participant’s FCAI Scores

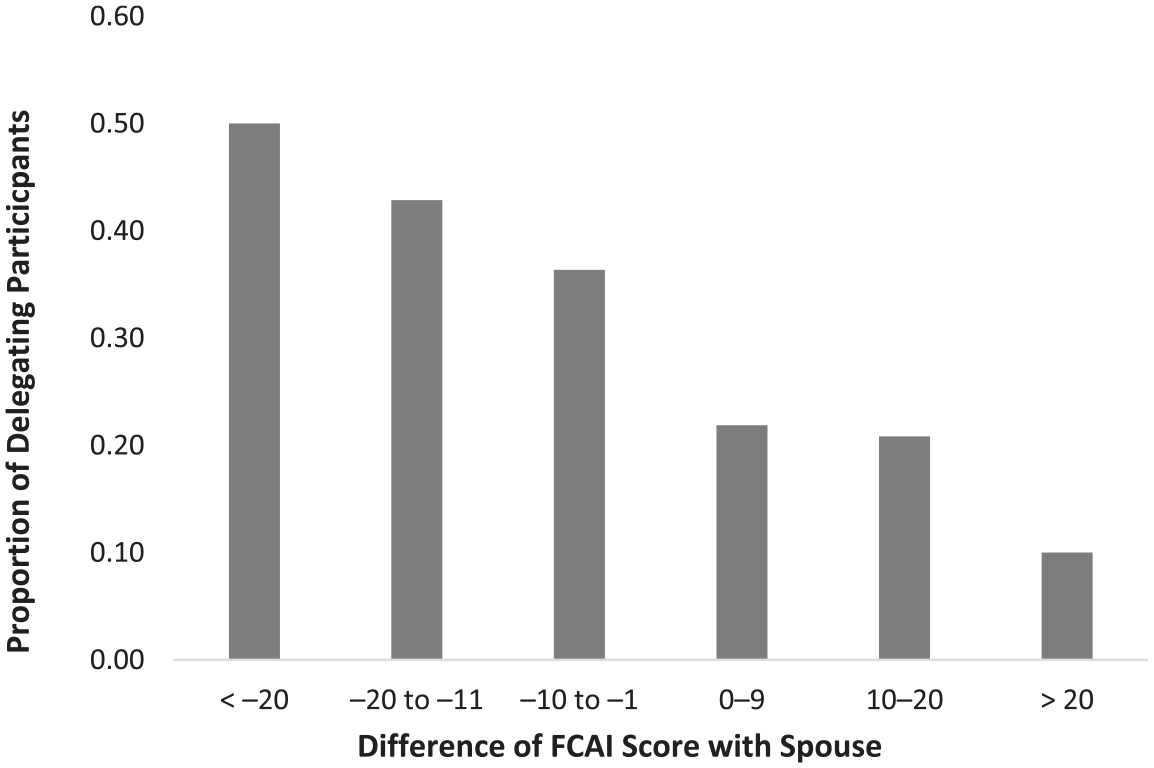

A more distinct delegation pattern emerged when participants were categorized based on the difference between their FCAI scores and those of their spouses. The higher the difference between participants’ FCAI score and that of their spouses, the lower the likelihood of delegating FDM tasks (Figure 3). This result was consistent with the expectations of the “specialization” model of household task allocation where the spouse with higher (lower) competence would be more (less) likely to undertake tasks in that domain and less (more) likely to delegate. It is worth noting that since participants completed the financial competence test after the delegation experiment, their FCAI performance could not have affected their delegation decisions. Moreover, the FCAI scores were not disclosed to participants.

Likelihood of Delegation and Difference Between Spouses’ FCAI Scores

Control Over Delegation

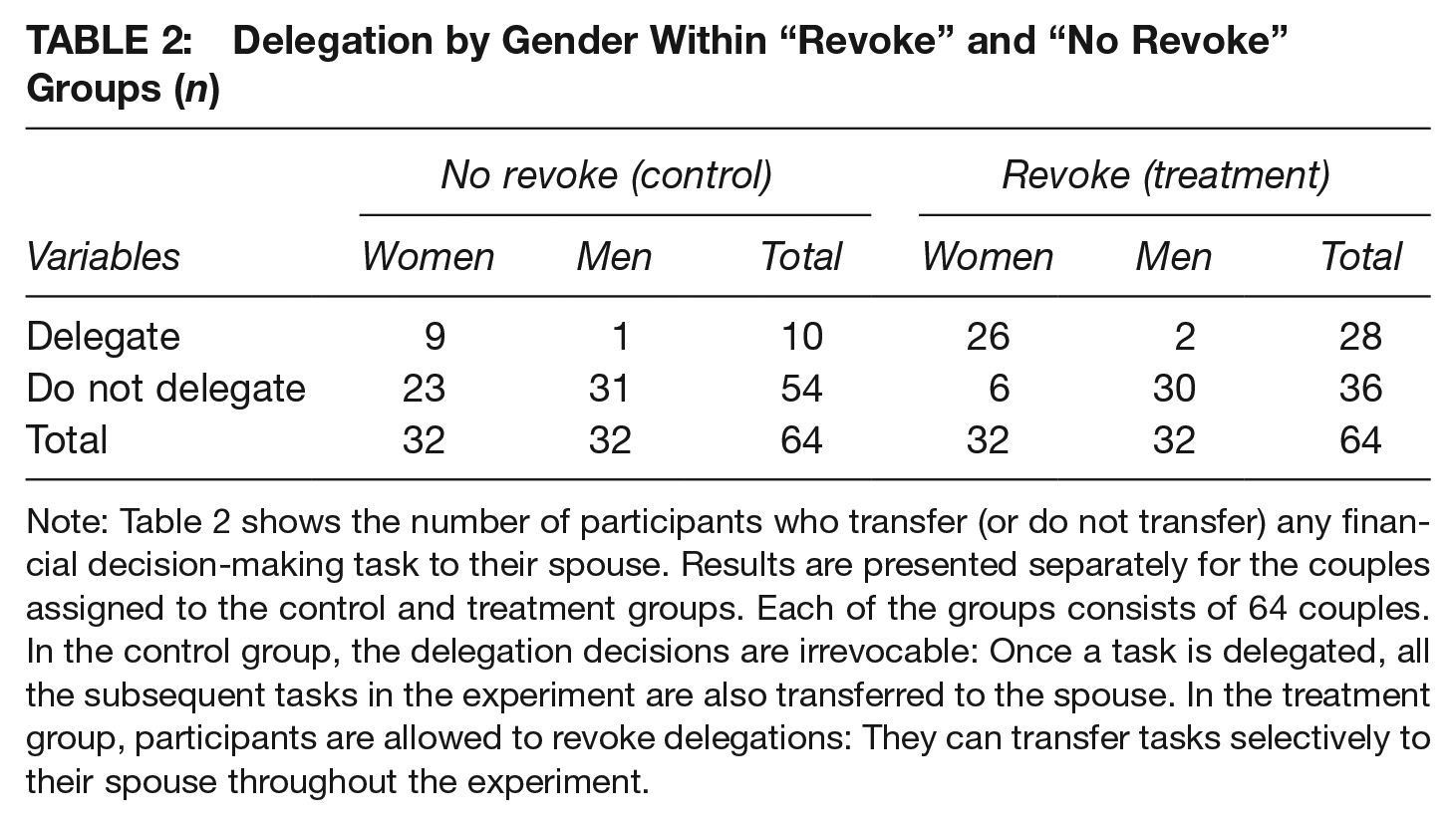

The delegations made by the participants in the “revoke” and “no revoke” groups are shown in Table 2. Only 15 percent of the participants in the “no revoke” group delegated to their spouse, compared with 44 percent in the “revoke” group. Consistent with Hypothesis 2, participants with the “revoke” option were significantly more likely to delegate to their spouse than those who did not have that option (p < .001). In the “no revoke” group, 41 FDM tasks were delegated, resulting in an average of 0.64 tasks delegated per participant. In comparison, the “revoke” group participants delegated 47 tasks to their spouses—that is, 0.73 tasks per participant. Approximately, one-third of the participants in the “no revoke” group transferred two or more FDM tasks to their spouses. However, if we consider only those participants who delegated, a significant difference between the two groups emerged. Among the 10 participants in the “no revoke” group who delegated, 4.1 FDM tasks were delegated on average per participant (median = 4.5), significantly higher than the average of 1.7 FDM tasks (median = 2.0) delegated by participants in the “revoke” group who delegated to their spouse.

Delegation by Gender Within “Revoke” and “No Revoke” Groups (n)

Note: Table 2 shows the number of participants who transfer (or do not transfer) any financial decision-making task to their spouse. Results are presented separately for the couples assigned to the control and treatment groups. Each of the groups consists of 64 couples. In the control group, the delegation decisions are irrevocable: Once a task is delegated, all the subsequent tasks in the experiment are also transferred to the spouse. In the treatment group, participants are allowed to revoke delegations: They can transfer tasks selectively to their spouse throughout the experiment.

It may seem paradoxical that while participants in the “no revoke” group were less likely to delegate, the average number of tasks they transferred to their spouse was higher than those in the “revoke” group. It is likely an artifact of the experimental design: Once an FDM task was transferred by a participant in the “no revoke” group, the subsequent tasks were automatically transferred to their spouse, regardless of whether the delegator intended to delegate them. In the “revoke” group, where the participants could delegate tasks selectively, the average number of FDM tasks transferred was significantly lower.

Within both the “no revoke” and “revoke” groups, women were more likely to delegate to their spouses. Women in the “revoke” group delegated more often. The proportion of women in the “revoke” group who delegated (81.3 percent) was significantly higher than that of the “no revoke” group (28.1 percent, p < .001). Very few men delegated to their spouse, regardless of the experiment condition (3.1 percent and 6.2 percent in the “no revoke” and “revoke” groups, respectively). Thus, although the “revoke” condition did not appear to influence delegation behavior among men, inferences were limited due to their very low rate of delegation overall.

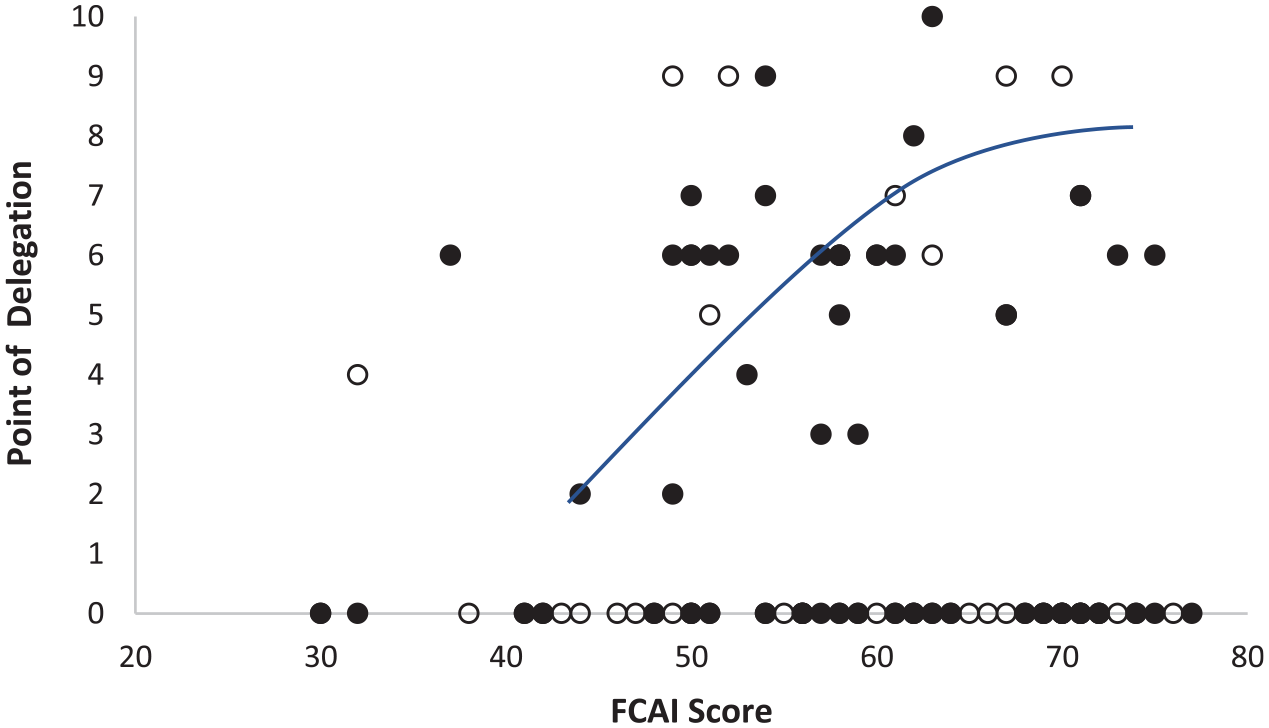

We were also interested to know whether having the authority to revoke delegation (or selectively delegate) influenced the timing of delegation. Figure 4 plots the precise point of delegation, that is, the serial number of the first FDM task each participant delegated against their respective FCAI scores.

Point of Delegation for Participants in “Revoke” and “No Revoke” Groups

Because few participants in either group delegated, there is a preponderance of black and white circles that coincide with the x-axis. The FCAI scores of these participants have a wide spread, suggesting that the reluctance to delegate was not confined to participants with high levels of financial competence. However, among the participants who delegated, the plot shows some propensity to delegate late as the participant’s FCAI score increases. This observation was consistent with our expectation that individuals with greater financial competence would attempt to accomplish more financial tasks without assistance from their spouses. Nevertheless, there were noticeable differences in the timing of delegation between the participants in the “no revoke” and “revoke” groups. The white circles are concentrated in the upper half of the plot, indicating that the participants in the “no revoke” group who opted to delegate usually did so relatively later in the experiment, regardless of their level of financial competence. In contrast, the vertical spread of the black circles in the plot is much wider, indicating that the “revoke” group delegated at different points. These participants also showed a tendency to delegate early (late) with a decrease (increase) in financial competence.

Probit Models for Delegation

To further examine the influence of gender, financial competence, and level of control on delegation behavior, we estimated several probit regressions to predict the conditional probability of delegation to spouses.

Gender

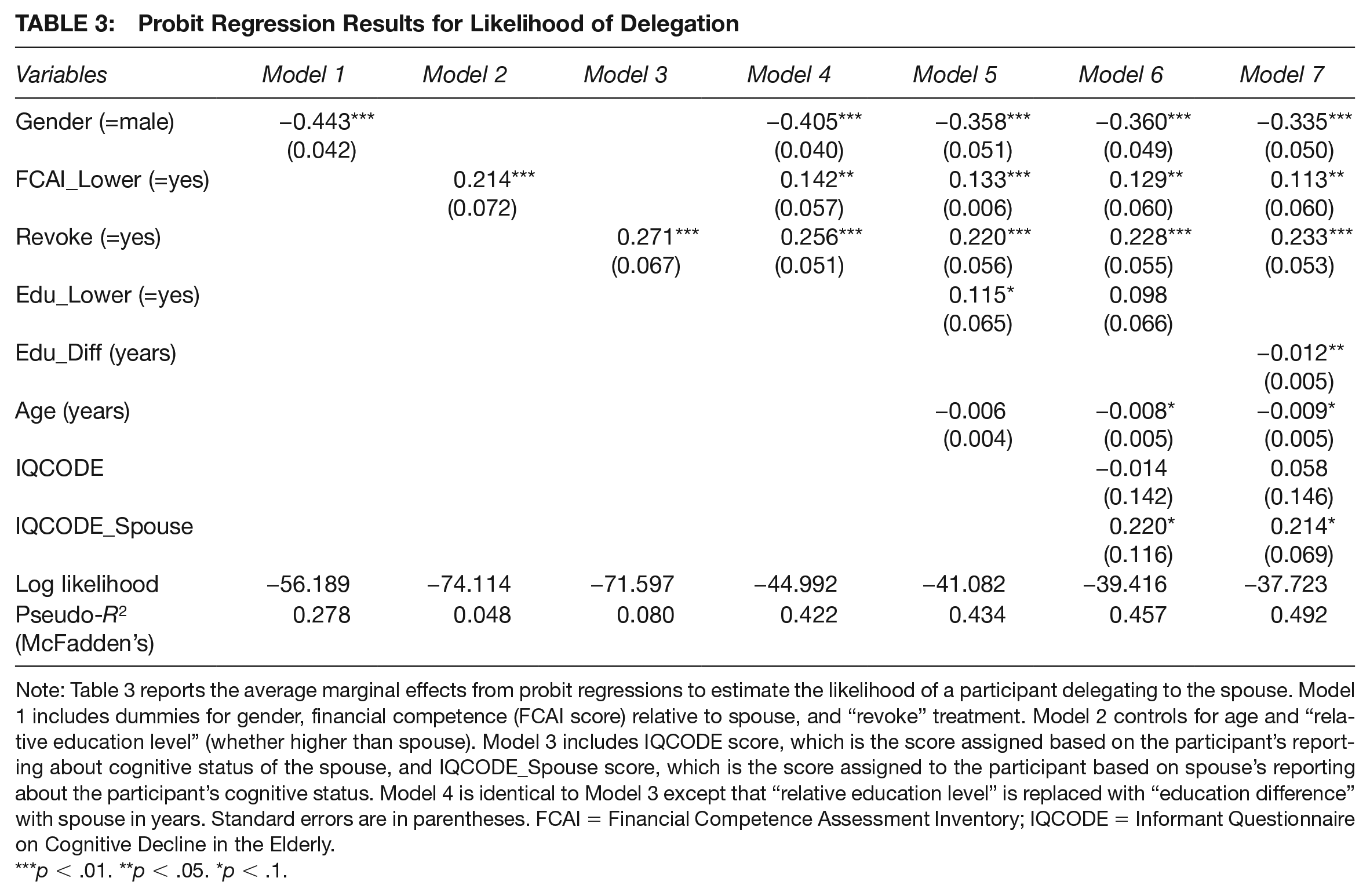

Table 3 reports the average marginal effects of the independent variables on delegation. Individually, all three key variables showed a significant relationship (p < .001) with participants’ delegation behavior. Gender was a significant predictor of delegation behavior, with an average marginal effect of 44 percent in the univariate regression (p < .001). When we controlled for financial competence and control over delegation in Model 4, men were still significantly less likely (40 percent on average) to delegate to their spouses (p < .001). After including other covariates such as age, education, and cognitive status in the subsequent models, gender remained a significant predictor of delegation, with an average marginal effect of −0.335 in our final Model 7 (p < .001). The results support Hypothesis 1A regarding gender and the delegation of FDM in older couples: Men were less likely than women to delegate to their spouses. This difference in the likelihood of delegation between the genders was not explained by differences in their financial competence, level of control over delegation, age, education, or cognitive status.

Probit Regression Results for Likelihood of Delegation

Note: Table 3 reports the average marginal effects from probit regressions to estimate the likelihood of a participant delegating to the spouse. Model 1 includes dummies for gender, financial competence (FCAI score) relative to spouse, and “revoke” treatment. Model 2 controls for age and “relative education level” (whether higher than spouse). Model 3 includes IQCODE score, which is the score assigned based on the participant’s reporting about cognitive status of the spouse, and IQCODE_Spouse score, which is the score assigned to the participant based on spouse’s reporting about the participant’s cognitive status. Model 4 is identical to Model 3 except that “relative education level” is replaced with “education difference” with spouse in years. Standard errors are in parentheses. FCAI = Financial Competence Assessment Inventory; IQCODE = Informant Questionnaire on Cognitive Decline in the Elderly.

***p < .01. **p < .05. *p < .1.

Financial Competence

In our univariate regression of delegation with financial competence as the explanatory variable, participants with lower FCAI scores than their spouses were more likely to delegate (21 percent on average, p < .001), which is consistent with the expectations of the specialization framework. However, this marginal effect diminished substantially in our multivariate regressions when we included gender and level of control (Model 4) and the other covariates (Models 5–7). In our final regression model, the average marginal effect of FCAI score relative to spouse was 0.11 (p < .05). In assessing the relative importance of gender vis-à-vis financial competence in predicting delegation, the marginal effect and pseudo-R2 estimate in our univariate regression models with gender were several times larger than the respective estimates with FCAI score relative to spouse as the explanatory variable.

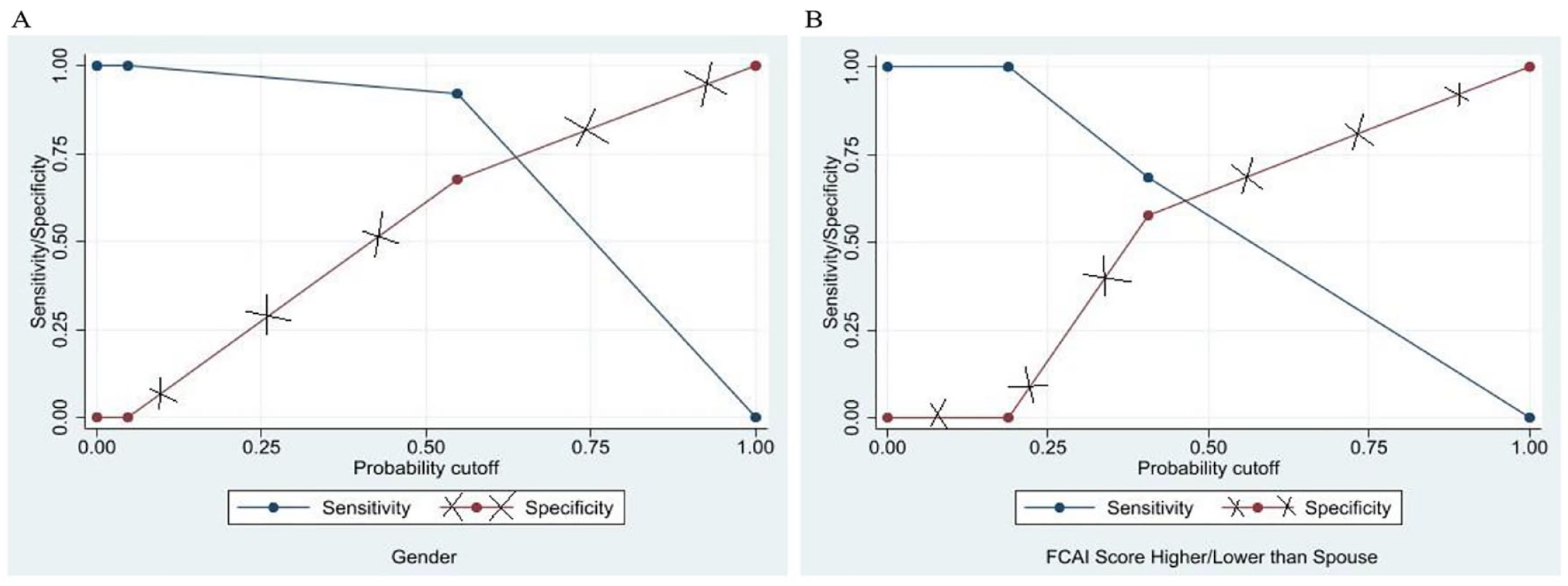

Next, we examined the sensitivity/specificity plots for the regression on gender and financial competence (Figure 5A and 5B, respectively) at various levels of probability of response (delegation). The sensitivity plot of the regression with gender as the explanatory variable remained higher than that with relative FCAI score over almost the entire probability range, suggesting that the former was a better predictor of who would delegate than the latter. The specificity plot for regression with gender also remained similar or larger than that with relative FCAI score, indicating that gender also better predicted who chose not to delegate.

Sensitivity/Specificity Graphs of Delegation. (A) Gender. (B) Financial Competence

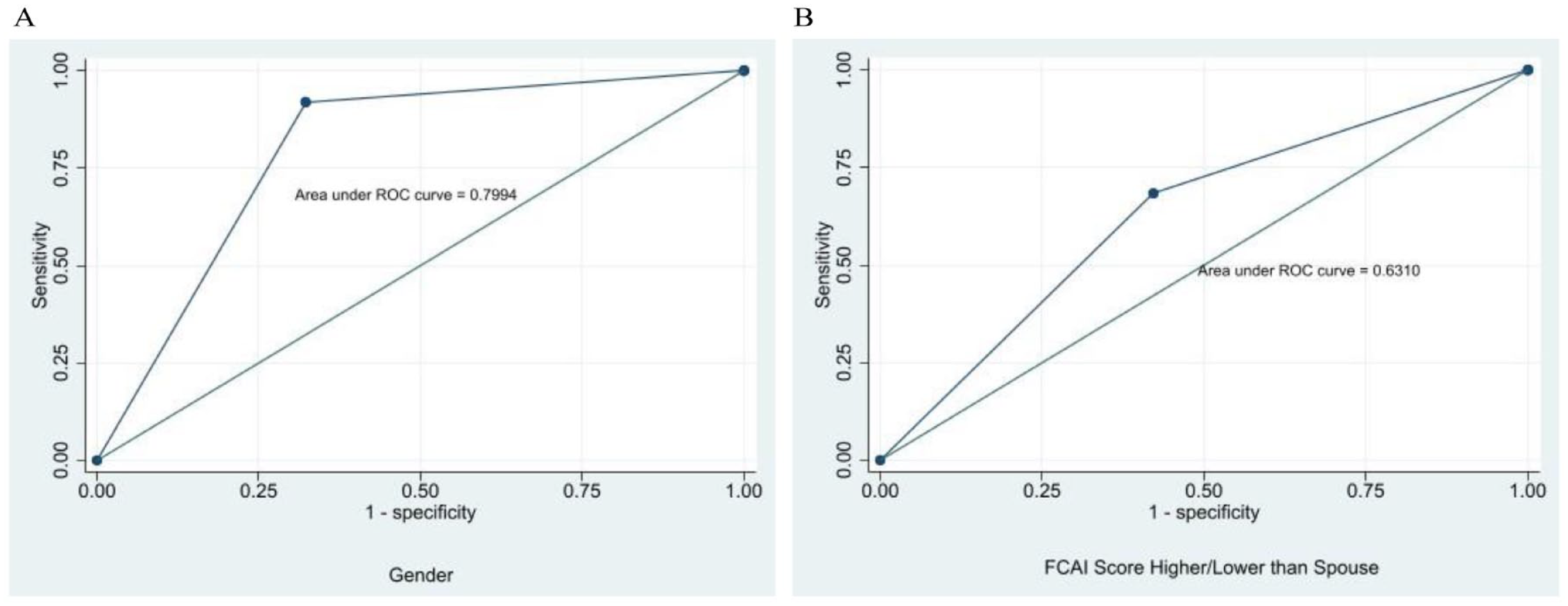

Finally, we examined the receiver operating characteristic (ROC) curves for these regressions. The ROC curves in Figure 6A and 6B are the graphical representations of the tradeoff between the false negative and false positive prediction rates of these two univariate models. The predictive accuracy of the models is represented by the respective areas under the ROC curves. The area under the ROC curve for gender (0.7994) is greater than for financial competence (0.6310), confirming that participants’ gender was a better predictor of delegating FDM than their financial competence relative to their spouse, which supported Hypothesis 1B. 8

ROC Curve. (A) Gender. (B) Financial Competence

Control Over Delegation

We also investigated the relationship between the likelihood of delegation and the control that participants could exercise over delegation. The results confirmed a significant relationship between the option to revoke delegations and likelihood to delegate (Table 3). Participants who had the option to revoke delegation or delegate selectively were significantly (p < .01) more willing to delegate to their spouses than those who did not. The marginal effect was 0.27 for univariate regression and 0.23 in Model 7 when controlling the covariates. This result was consistent with Hypothesis 2, which predicted that participants would be more likely to delegate if they could retain control over future delegations. Conversely, they are less likely to delegate if the delegation is irreversible, resulting in relinquishing control over subsequent decisions.

Education

Model 5 showed a weakly significant relationship between education level relative to spouse and the likelihood of delegation (p < .1). After including the IQCODE variables in Model 6, the relative education level was no longer significant. However, when we measured education gap between the spouses in years in Model 7, the likelihood of delegation significantly increased with it (p < .05).

Cognitive Status

A higher IQCODE (spouse) score, which indicates a participant’s cognitive decline in recent years according to their spouse, increased the likelihood of delegation, although this result was not significant at the 5 percent level in either Model 6 or 7.

Age

A weak negative relationship was observed between participants’ age and their likelihood of delegation (p < .1). Older participants had a lower likelihood of delegating FDM to their spouses, which may seem counterintuitive since age-related cognitive decline is likely to render FDM more challenging. However, delegation within our sample was mostly done by women. Because the husband was older than the wife for most participating couples, women who were very old may have been less willing to delegate to their “even older” husbands with reduced capacity to make financial decisions.

Conclusion

This study reports the strongest evidence to date that gender and control play predominant roles in delegation decisions among older married couples. Men consistently demonstrated an extremely low likelihood of transferring their FDM responsibilities to their spouses: 92 percent of the participants who delegated were women, and this gender difference could not be attributed to differences in financial competence. While the likelihood of delegation increased with the financial competence of spouse, this specialization effect was much smaller than those of gender and the control an individual has over the decision to delegate.

While we do not exactly know why men delegated so much less than women, differences in economic power (relative income) seem unlikely to have played a role because the participants were mostly retired. The Australian government provides the same amount of age pension to both spouses on reaching pensionable age, which would have a dampening effect on any income difference between husband and wife after retirement. 9 A more plausible explanation is their concept of self or identity, as gender is a “universally familiar aspect of identity” (Akerlof and Kranton 2000). If FDM is seen primarily as “men’s work,” husbands may suffer a loss of identity when this task is delegated to their wives. Moreover, if men are usually in charge of FDM in married households, they would have a larger “control premium,” lowering their chances of delegating to their spouse compared with women. An alternative explanation is the higher prevalence of overconfidence among men. D’Acunto (2015) finds that both the salience of the male identity and overconfidence affect men’s beliefs about experiencing positive outcomes; these effects are even stronger among older men, which may make them less willing to delegate. On the other hand, overconfidence could also be a mutually reinforcing (rather than alternative) mechanism in relation to gender identity. Risse, Farrell, and Fry (2018) suggest that men show higher levels of the personality traits that connote a stronger sense of confidence in their capabilities. If gender identity and expectations nudge men to act as primary financial decision makers, it can further inflate confidence in their own abilities.

We found that the willingness to delegate was lower among individuals who were only able to make irrevocable delegations (less control). They were also more likely to delegate late and might have done so only when the tasks became very challenging. This finding has important practical implications. Substituted decision-making mechanisms, such as Power of Attorney, where the legal transfer of authority usually comes into effect immediately on execution (even when the principal has the capacity to make decisions), preclude many older people from delegating, leaving them vulnerable in the event of future incapacity. A better understanding of provisions such as the authority to revoke a Durable Power of Attorney or using a “springing” Power of Attorney that becomes effective only upon the occurrence of specific events may encourage older people to adopt such arrangements.

Four related issues deserve further investigation. First, we did not analyze the potential influence of household wealth or income on delegation decisions. Because some prior studies (e.g. Dobbelsteen and Kooreman 1997) suggest that women in low-income families have greater participation in financial management, it would be worthwhile investigating whether specialization assumes a more influential role in the delegation of FDM within those households. Second, the gender differences observed in our study could be influenced by cohort effects, as all participants were born in the 1950s or earlier. Hu (2021) identifies a cohort-wise decline in male entitlement in managing household financial affairs. It would thus be interesting to examine whether the gender difference in delegation is also attenuated (and to what extent) in future generations of older couples, where women would have enjoyed greater economic independence and social status. Third, although we did not collect information on the ethnicity of the participants, our sample overwhelmingly consisted of people from Anglo-Celtic and other European backgrounds, where couples often live as a nuclear family. More complex household structures may be observed among other ethnicities and cultures. For example, it is not uncommon in Asian and South Asian households for multiple generations to live together, where FDM responsibilities of older parents may devolve to their progenies (see, e.g. Singh and Bhandari 2012). Finally, the gender difference in delegation behavior in our study was observed only within the context of married and heterosexual couples. To draw any general conclusions about gender differences in delegation behavior, future research should examine how individuals delegate to members of other genders who are not their spouses and how same-gender couples delegate to each other.

Footnotes

Authors’ note:

The authors are thankful to Lionel Page, Benno Torgler, Antonia Grohmann, Hazel Bateman, Leonora Risse, and the participants of Australia and New Zealand Workshop in Experimental Economics 2019, Melbourne; BEST Conference on Human Behaviour and Decision Making 2020; and Australian Gender Economics Workshop 2023 for their helpful comments and suggestions; and to Claudia Luke, Kirsty Shadbolt, and Gaurav Gogoi for excellent research assistance. Finally, they express deep gratitude to the Australian Men’s Shed Association, Rhonda Weston, and the University of the Third Age (Toowoomba), and Nelly Haly and the Rosewood Community Centre, for providing them opportunities to promote participation in the study. Funding of this research by the Australian Research Council (Linkage Grant No. LP150100264) and the Dementia Australia Research Foundation is gratefully acknowledged.

Notes

Sylvain Hohn completed his PhD from Queensland University of Technology (QUT) on financial decision-making in late adulthood. His research interest is in the area of behavioral and experimental economics.

Anup Basu is a professor of finance and behavioral economics at the Centre of Behavioural Economics, Society and Technology (BEST) in Queensland University of Technology (QUT). His research focuses on retirement and financial security in old age.

Uwe Dulleck is a professor of behavioral economics at the Centre of Behavioural Economics, Society and Technology (BEST) in Queensland University of Technology (QUT). His research interest lies in the application of behavioral insights in business decision-making, public policy, and regulations.

Julie Henry is a professor in the School of Psychology at The University of Queensland, and is also an affiliate professor at The Queensland Brain Institute as well as The Mater Research Institute. She is a fellow of the Academy of the Social Sciences in Australia and of the Association for Psychological Science.

Nicolas Cherbuin is a professor in the National Centre for Epidemiology and Population Health at the Australian National University. His background is in psychology, neuroscience, and epidemiology, and his main research focus is to investigate the factors that contribute to mental health, well-being, neurodegeneration, and cognitive decline across the life course.