Abstract

While prior scholarship examines the relationship between community development financial institutions (CDFIs) and economic development, little is known about their effectiveness and impact on cultivating inclusive urban entrepreneurship. The authors contend that greater attention directed toward young firms’ persistent needs for early resource acquisition, coupled with increased emphasis on the activity among business owners from minoritized groups, can extend the extant literature in a more inclusive manner. To do so, the authors trace the diffusion of CDFIs across the United States between 2013 and 2021 to examine their association with underrepresented minority-owned and/or young firms. One finding is that the presence of CDFIs bolsters the share of minoritized firms at the city level. Further, the authors find that this positive relationship holds for young firms owned by minoritized groups. The empirical results are contextualized with a case study of a nonprofit community bank seeking CDFI certification. This example highlights the importance of providing business assistance and financial capital to urban entrepreneurs.

Keywords

Lorena Cantarovici opened the first Maria Empanada in Denver's Lakewood neighborhood in 2011. 1 In 2014, after being turned down by banks to finance a move to a larger restaurant space, Lorena was referred to the Colorado Enterprise Fund—a certified, nonprofit CDFI—where she got her first business loan, which helped her expand to a bigger location, purchase the necessary equipment, and hire the personnel to succeed. The loan helped her grow from a small-scale caterer to the owner of an award-winning, Zagat-rated restaurant now recognized as “One of the 12 Hottest Bakeries in the U.S.” 2 As of 2019, Lorena employs 41 people across three locations, 80% of whom are low- and moderate-income persons and are paid above-market wages, including benefits. 3

Inclusive economic development requires broad access to financial capital and other critical entrepreneurial resources (Fernandes & Ferreira, 2022; George & Prabhu, 2003). However, current conditions within the United States are constrained as there is often a significant gap in the distribution of entrepreneurial resources and capital for minoritized 4 business owners (Robb & Fairlie, 2007). Not only do entrepreneurs from these underrepresented groups have limited access to financial capital (Alsos et al., 2006; Bates & Robb, 2013; Becker-Blease & Sohl, 2007; Coleman & Robb, 2009; Fairlie et al., 2022), they also often encounter lending discrimination (Blanchard et al., 2008; Blanchflower et al., 2003; Cavalluzzo et al., 2002). Compounding this challenge, lending institutions such as banks are less incentivized to invest in these markets due to the perceived risk of failure inherent with young firms (Gans & Stern, 2003). In turn, these banks have significantly decreased their market presence in recent years (Mosley, 2019; Tolbert et al., 2018), which places minoritized business owners at an even greater disadvantage in securing initial and ongoing funding to establish and grow their businesses.

In 1977, the U.S. Congress enacted the Community Reinvestment Act (CRA) to encourage federally insured banks to invest in underserved and low- and moderate-income communities. 5 Moreover, community development financial institutions (CDFIs) and the CDFI Fund 6 were chartered to help overcome resource constraints and financial exclusion barriers for entrepreneurs in these underserved markets (Mosley, 2019). Operationally, CDFIs offer sources of financing and loans to families and businesses in economically distressed communities (Appleyard, 2011). To date, CDFIs participating in the federal bond guarantee program have lent $1.8 billion to spark small business formation in underserved communities. 7

Although existing research has examined the potential role of CDFIs in economic development (Greer & Gonzales, 2016; Newberger et al., 2015), far less is known about their effectiveness in driving inclusive urban entrepreneurship. Capital constraints for minoritized entrepreneurs likely inhibit inclusive and robust regional economic development efforts. The role of agile and context-sensitive financial institutions, such as CDFIs, is a core element of measuring and evaluating development and health in entrepreneurial ecosystems and regional innovation clusters (Johnson et al., 2022; Qian & Acs, 2023). 8

We contend that greater attention directed toward young firms’ persistent needs for early resource acquisition, coupled with increased emphasis on economic activity among business owners from minoritized groups, can add much-needed evidence to the extant literature. The lack of econometric research in this area is surprising because the CDFI lending sector has seen remarkable growth in terms of scale and scope since 2018. In 2023 alone, the number of certified CDFIs increased nearly 40%, and total assets nearly tripled for CDFI banks and credit unions. 9 Prior attempts to evaluate the effectiveness of CDFIs have yielded contrasting results mainly due to the lack of standardized metrics for measuring and comparing business activity among various minoritized groups (McCall & Hoyman, 2023).

This study explores the role of CDFIs in supporting inclusive urban entrepreneurship by drawing from two streams of research: community financial institutions and regional and urban economic development. We leverage rich longitudinal data and trace the diffusion of certified CDFIs across the United States to examine their association alongside that of underrepresented minority-owned (URM) firms and/or young firms nationwide. We find evidence that the presence of CDFIs bolsters the share of minoritized firms in U.S. cities. Further, we find that this positive relationship holds for young firms owned by minoritized groups as well. We contextualize our results with a case study, featuring interviews with top-level leaders at a nonprofit community bank based in Charlotte, North Carolina that is currently seeking CDFI certification. These additional insights highlight the importance of providing business assistance and financial capital to urban entrepreneurs. Such organizations position themselves to build community capital by pursuing missions that foster inclusive development.

Together, these findings suggest that CDFIs may fill funding gaps left underserved by venture capitalists, who have historically overlooked or excluded women and people of color from their portfolios relative to non-minoritized entrepreneurs. 10 More broadly, our paper joins a burgeoning line of work aiming to measure trends in inclusive economic development and entrepreneurship (Barkley & Schweitzer, 2023; Cassell et al., 2023; Feldman et al., 2022; Johnson et al., 2022). We discuss the scholarly, managerial, and policy implications for ongoing and future evaluation of CDFIs and their role in bolstering inclusive economic development.

Data and Empirical Context

Our analysis focuses on CDFIs and the CDFI Fund as government-chartered mechanisms for potentially addressing market failures and systemic exclusion from capital markets among urban entrepreneurs from historically marginalized backgrounds. Established in 1994 by the Riegle Community Development and Regulatory Improvement Act (which was driven by the earlier enactment of the CRA), the CDFI Fund accepts applications from banks, credit unions, venture capital funds, and other mission-driven organizations that aim to improve economic conditions for economically distressed and marginalized areas. Obtaining certification as a CDFI bolsters the economic and training capacities of these institutions in two main ways: (1) It acts as a quality signal to private sector investors who provide additional financing and support to the CDFI; and (2) It enables the CDFI to apply for and receive additional public sector grant funding and guaranteed loans from the federal government. 11

The primary data come from the list of CDFIs published by the CDFI Fund. We focus on the panel of activity from 2013 to 2021, which accounts for the growth in the number of CDFIs across the United States from 198 to 693, respectively. The former year designates the first year with complete administrative reporting on CDFIs, while the latter allows for maximum overlap with the additional data sources used for empirical analysis. Of note, we augment and enhance the data set of CDFI activity with data from the National Establishment Time Series (NETS), U.S. Census American Community Survey (Census), Organisation for Economic Co-operation and Development (OECD), and Pitchbook. NETS reports proprietary data collected by Dun & Bradstreet and traces all U.S. businesses with credit activity, which is useful because it includes granular detail on key characteristics of firms and enables us to define a set of dependent variables tracing both URM-owned and/or young firm activity. 12 Data from the Census and OECD report aggregate detail on demographic and economic activity, while Pitchbook reports detail on private financing deal flow.

Supplementary online appendix Figure A1 illustrates the nested nature of the data among three distinct levels: (1) federal government policy, (2) regional economic development, and (3) firm-level activity. This configuration enables us to trace the diffusion of government-certified CDFIs across both geography and time while accounting for demographic, private capital, and economic inequality trends. It also helps us assess shifts in young firm activity and pay particular attention to entrepreneurship among minoritized groups.

The core-based statistical area (CBSA) is our unit of analysis.

13

This designation captures both metropolitan and micropolitan statistical areas and is defined by the U.S. Census Bureau as an entity that comprises a county or counties that are associated with at least one urban “core” of at least 10,000 in population. Advantages of using this unit of analysis include the following:

It captures regional dynamics of entrepreneurial activity as determined by feedback among the three tiers illustrated in supplementary online appendix Figure A1. It reflects city-specific elements that are important for isolating the impacts of CDFIs on local entrepreneurship outcomes. It spans a sufficiently large geographic area to allow for significant spacing between the CDFI and the potential firm-level beneficiaries of its services. That said, we acknowledge that this last point highlights a possible empirical challenge associated with recent increases in remote transactions and telework.

14

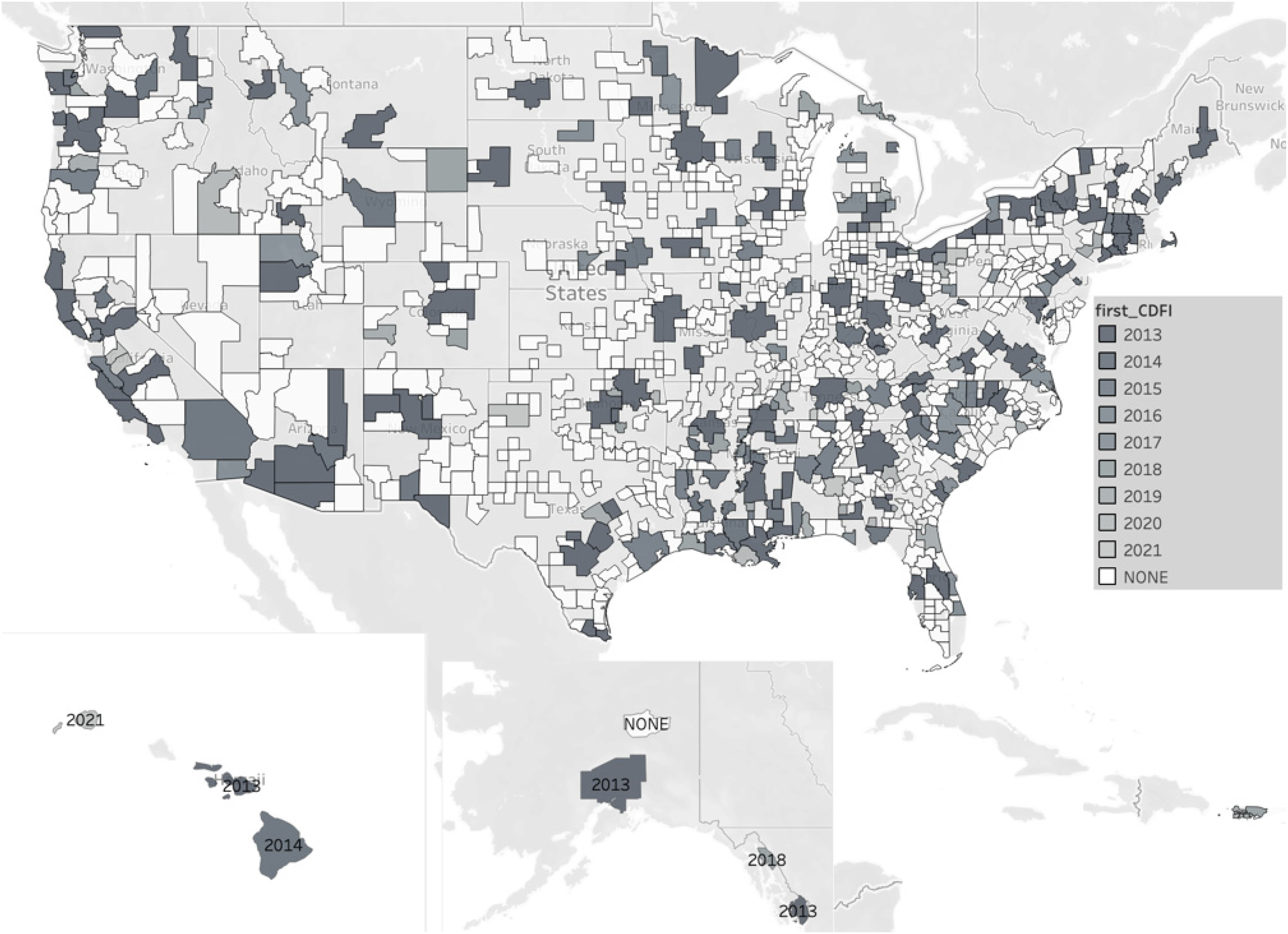

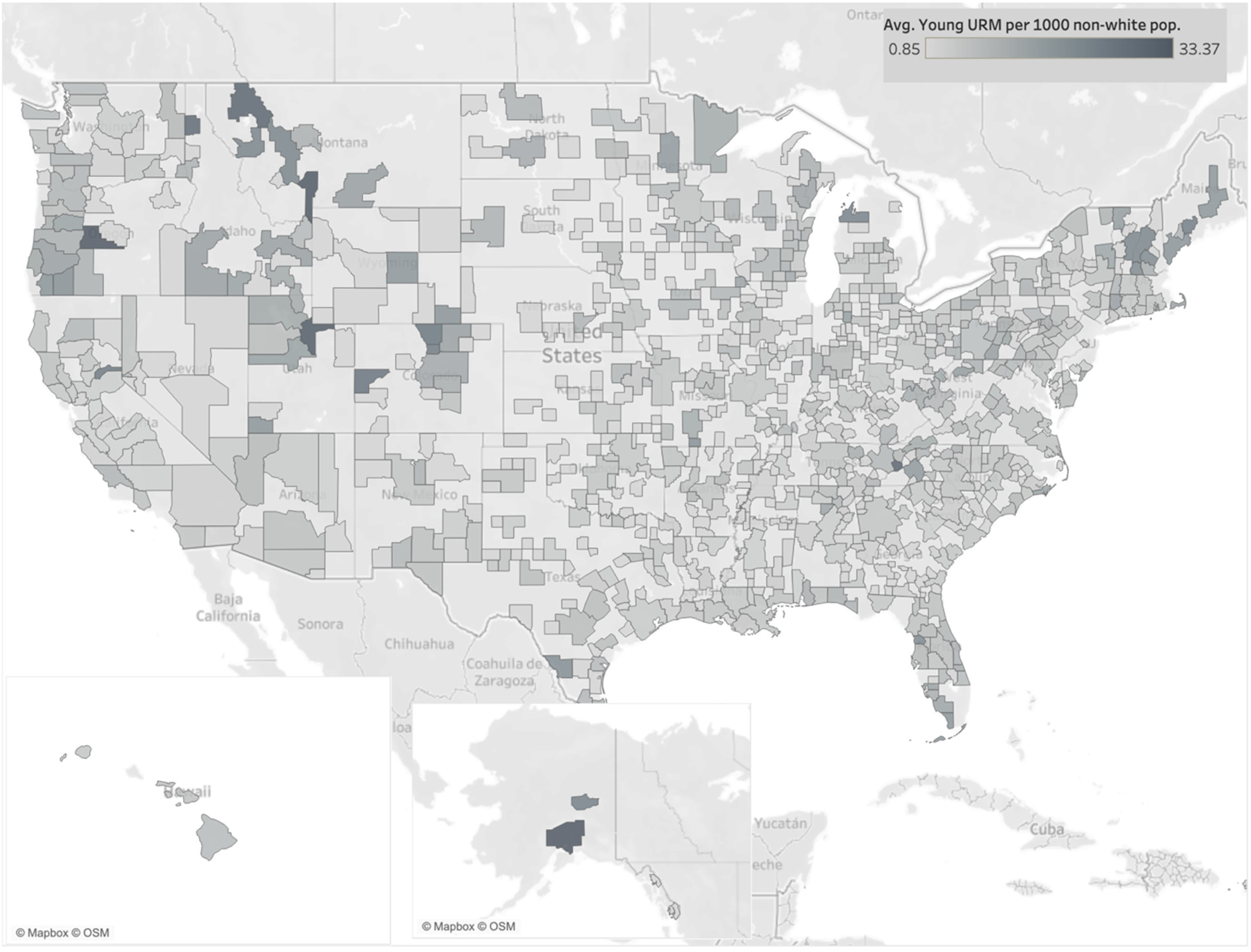

Figures 1 and 2 illustrate the geographic diffusion of CDFIs and scale of young and minoritized firms in the nationwide sample. Specifically, Figure 1 indicates the status (if any) and timing of those cities that first certified a CDFI. Darker urban areas, such as New Orleans, Denver, Minneapolis, and Atlanta, stand out as early adopters of CDFI infrastructure. However, the most common outcome for CBSAs is not to have any CDFIs as of 2021 (refer to the white CBSA designation in Figure 1). Figure 2 shows the relative density of young URM-owned firms across U.S. cities. Such ownership is geographically prominent in the South. However, the ratio of young URM-owned businesses to the non-white population indicates that cities in the Northwest and Northeast lead this activity.

Diffusion of CDFIs across CBSAs over time 2013–2021. Note. Darker shading indicates more recent initiation of CDFI at city (i.e., CBSA) level from 2013–2021. White designations for CBSAs are cities with no CDFI activity as of 2021.

Average share of young URM-owned firms per 1000 non-white population by CBSA. Note. Shaded areas reflect the average number of young URM-owned firms (i.e., minority and/or woman owned) per 1,000 non-white population by CBSA from 2013–2021.

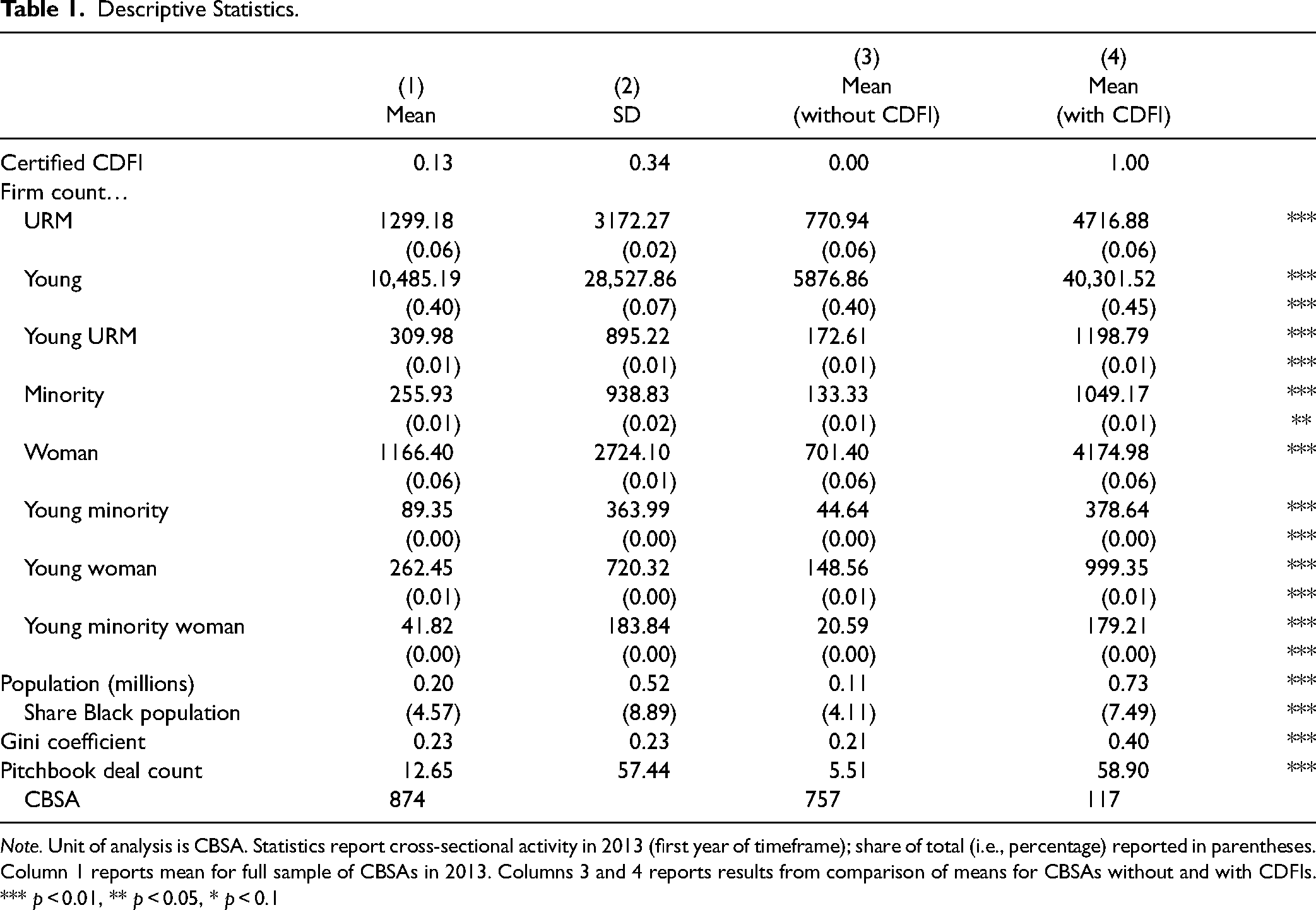

Table 1 reports descriptive statistics. Here, we report cross-sectional results in 2013 for the entire sample of 874 CBSAs. Additionally, we report the results from the comparison of means between those CBSAs with a CDFI by 2013 to those without a CDFI at that time. And as an extension, we also report the descriptive results from the pooled cross-sectional data set accounting for activity over the entire 9-year panel, spanning 2013–2021 (see supplementary online appendix Table A1.) Several initial results stand out from both sets of descriptive results. For one, CDFIs are not yet a widespread phenomenon nationally despite the consistent growth in their numbers in recent years in some urban locales (this complements the illustrative results reported in Figure 1). Second, the number of firms founded by minoritized groups reported by NETS is lower than U.S. Census estimates. This is likely due to sampling features of the NETS data. 15 Usefully, however, NETS enables us to trace annual CBSA-level detail on young firm activity across various designations of ownership (including minoritized groups and the decompositions therein); administrative government sources do not publicly report this level of detail. By relying on NETS to assess longitudinal trends of firm ownership by CBSA, our analysis represents a more conservative, lower bound estimate of the actual activity of ventures led by minoritized groups in each area.

Descriptive Statistics.

Note. Unit of analysis is CBSA. Statistics report cross-sectional activity in 2013 (first year of timeframe); share of total (i.e., percentage) reported in parentheses. Column 1 reports mean for full sample of CBSAs in 2013. Columns 3 and 4 reports results from comparison of means for CBSAs without and with CDFIs. *** p < 0.01, ** p < 0.05, * p < 0.1

Third, the results from the comparisons of means between cities with and without CDFI activity indicate the two sets of cities differ in terms of business owner demographics. Generally, cities with CDFIs exhibit proportionally larger trends of economic and business activity. For example, cities with CDFIs report larger populations, a higher concentration of private capital activity, and even greater racial diversity. At the same time, cities with CDFIs report greater economic inequality—as indicated by the Gini coefficient. 16 The average city with any CDFI infrastructure has six times as many URM-owned establishments and roughly seven times as many young establishments when compared to cities with no CDFI infrastructure. 17

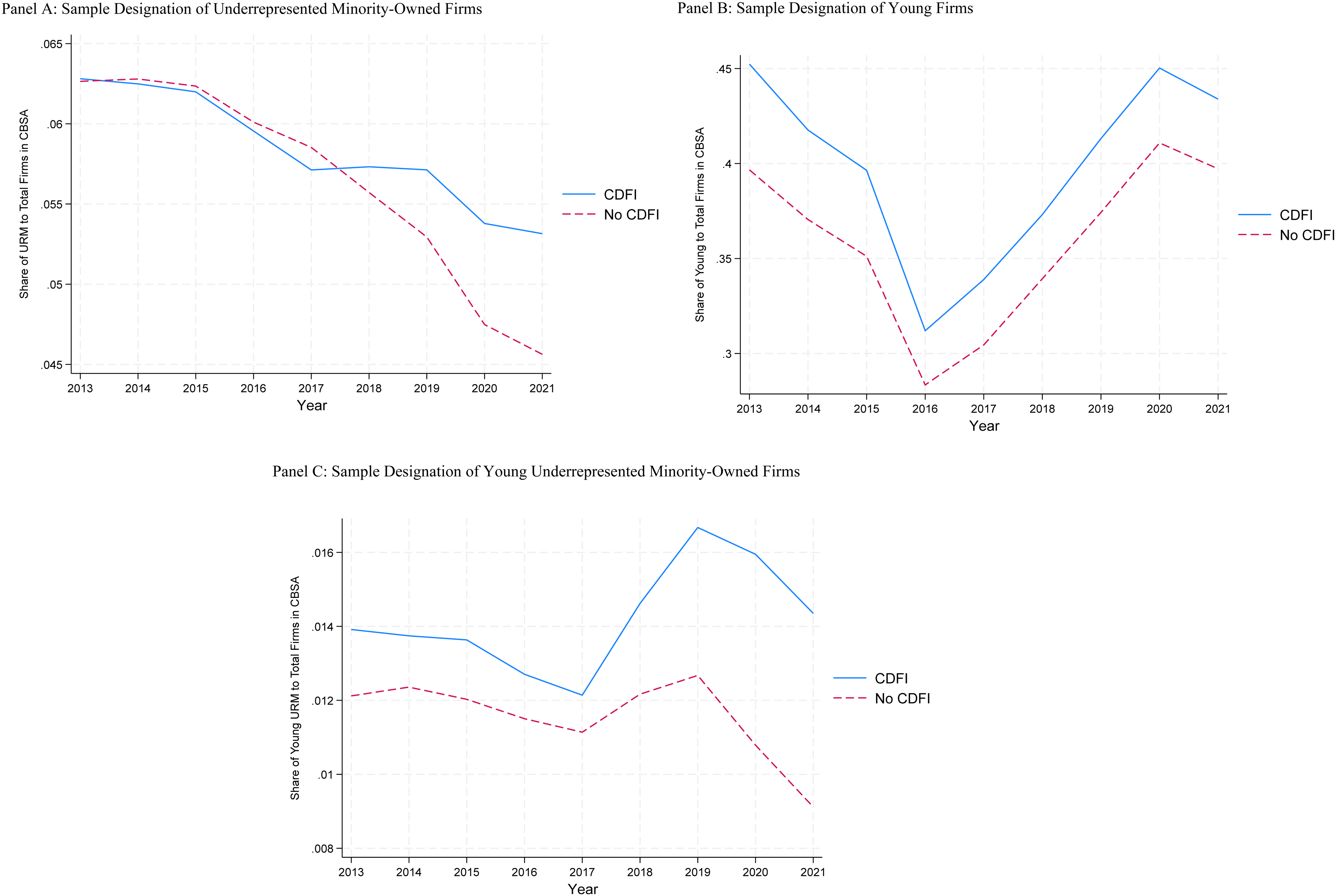

Figure 3 illustrates descriptive, differential trends over time by CDFI designation across three sample designations of firms:

Panel A: underrepresented minority-owned firms (e.g., minority and/or woman owned) Panel B: young (e.g., less than 5 years old) single establishment firms Panel C: young (e.g., URM-owned) firms

Trends of firm activity located in CBSAs with and without CDFIs. Panel A: Sample Designation of Underrepresented Minority-Owned Firms. Panel B: Sample Designation of Young Firms. Panel C: Sample Designation of Young Underrepresented Minority-Owned Firms. Note. Trends reflect aggregate changes in the share of various firm designations to total firms by CBSA. Panel A reports for underrepresented minority-owned firms (minority and/or woman owned); Panel B reports for young firms (firm age 5 or younger); Panel C reported for young, underrepresented minority-owned firms. Solid line reports trends for cities (i.e., CBSAs) with CDFI infrastructure over the timeframe. Dashed line reports trends for cities without CDFI infrastructure over the timeframe.

All three report the share of each sample designation to the total firms in the respective CBSA. We observe the following. Panel A illustrates that cities with CDFIs appear to stabilize the share of URM-owned firms; this stands in contrast to cities without CDFIs, which exhibit a more pronounced decreasing trend. Panel B reports a fluctuating, yet parallel set of trends in the share of young firm activity across cities with and without CDFIs. Finally, Panel C reports an increasing divide in the share of young firms owned by minoritized groups over the extended timeframe. This divergence appears to coincide with the diffusion of CDFIs across the country in the latter years of the panel. Altogether, these descriptive results not only indicate a positive association between CDFIs and inclusive economic development, but also the presence of a possible selection effect. It is possible that cities incorporate CDFI financial infrastructure due to unobserved causes, which in turn may also drive growth in our key outcome variables of interest (e.g., CBSA-level growth rates among minoritized and/or young firms). While we find the differences in activity between cities with and without CDFIs compelling, they undoubtedly contain influence from factors such as policy and economic trends that concurrently drive increases in CDFI activity and entrepreneurial activity. We aim to account for these confounding factors empirically in the next section.

Model

Formally, we set up a CBSA and year fixed-effect regression model specification.

To ease interpretation and compare the relative association of each regressor, we standardize all continuous measures (i.e.,

Results

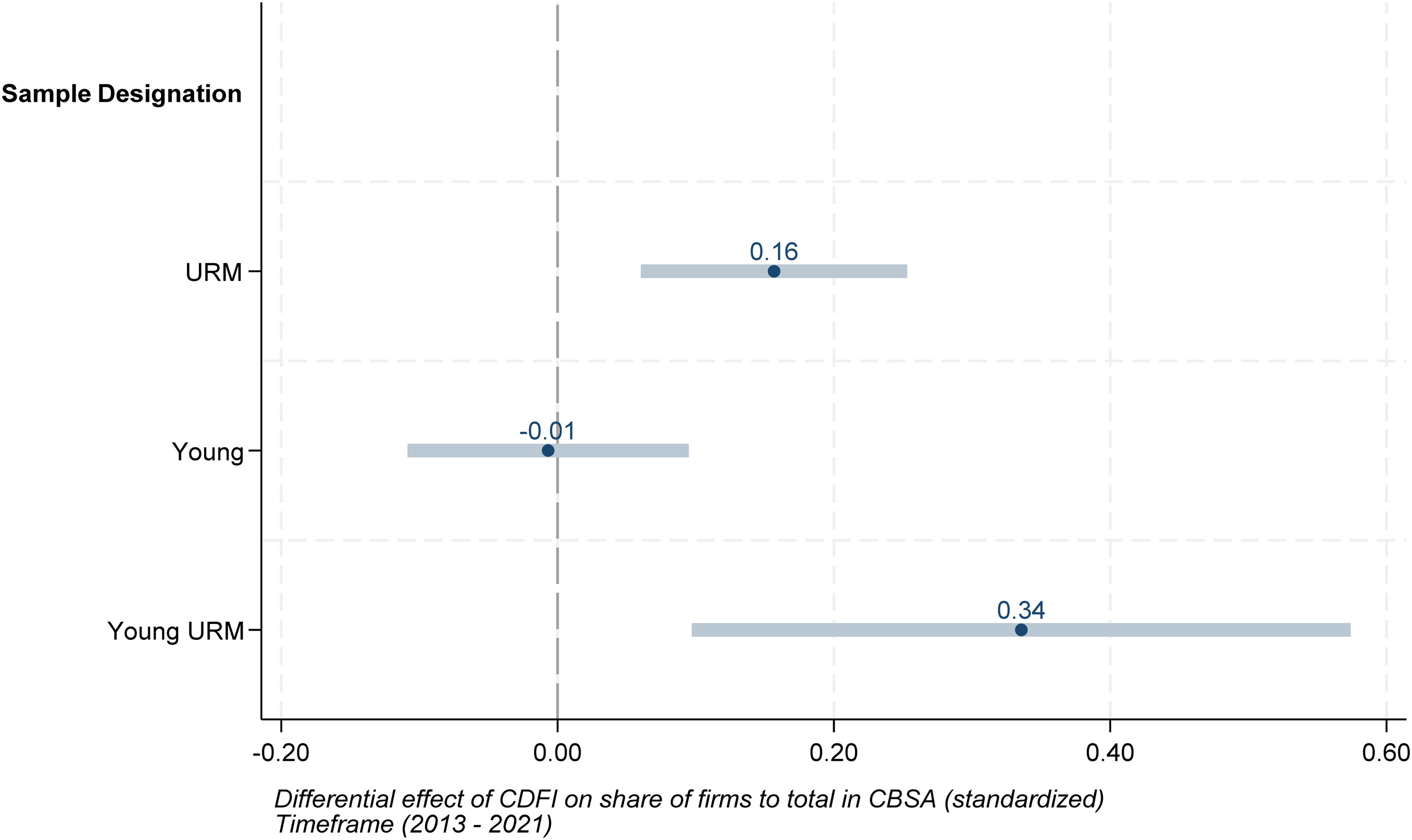

Figure 4 reports coefficients for the primary regressor, CDFI. Operationally, we estimate three separate regressions—one for each dependent variable—and plot the coefficient for CDFI for illustrative comparison. We report the 95th percent confidence interval for each coefficient. Reference to dependent variables is listed along the y-axis. We report the full set of regression results in supplementary online appendix Table A2, Columns 1–3.

Primary results. Note. We report coefficients for the primary binary regressor, CDFI, from a series of CBSA and year fixed effect regressions (Equation 1). Columns 1–3 in supplementary online appendix Table A2 report the complete set of regression results. Here, we report the 95th percent confidence intervals of the CDFI effect. We indicate the measure for the dependent variable along the y-axis. For example, for the first result – URM – this metric reports the share of underrepresented minority-owned firms to total establishments by CBSA.

Where we find evidence of a relationship, the effect is positive. Namely, the differential effect of having a CDFI in a CBSA is associated with a 0.16 standard deviation increase in the share of URM-owned firms (standard error [SE] 0.05). We report comparably positive results for young, URM-owned firms as well. However, the results are inconclusive for young firms. All these results mirror the general trends reported in Figure 3, indicating that CDFIs are associated with growth among the sample of firms with URM ownership rather than young firms exclusively.

We confirm these primary results with a series of empirical extensions. First, we unpack sample designation of the dependent variable across five subsequent decompositions: 20 minority-owned; woman-owned; young, minority-owned; young, woman-owned; young-, minority-, and woman-owned. We report the regression results in Columns 4–8 in supplementary online appendix Table A2. The results are comparable in magnitude to the primary results reported for the share of URM-owned and young, URM-owned firms, respectively. Altogether, these results indicate that CDFIs are positively associated across a breadth of minoritized designations, including both minority-owned and woman-owned firms. Second, we adjust the time frame of the panel and remove data for 2020–2021, which coincide with COVID-19. We report consistent results to the primary results in Figure 4. Third, we tease a part of construction of the counterfactual group by disentangling “never CFDI” CBSAs from “not yet CDFI” CBSAs. We report consistent results in supplementary online appendix Figure A3. 21

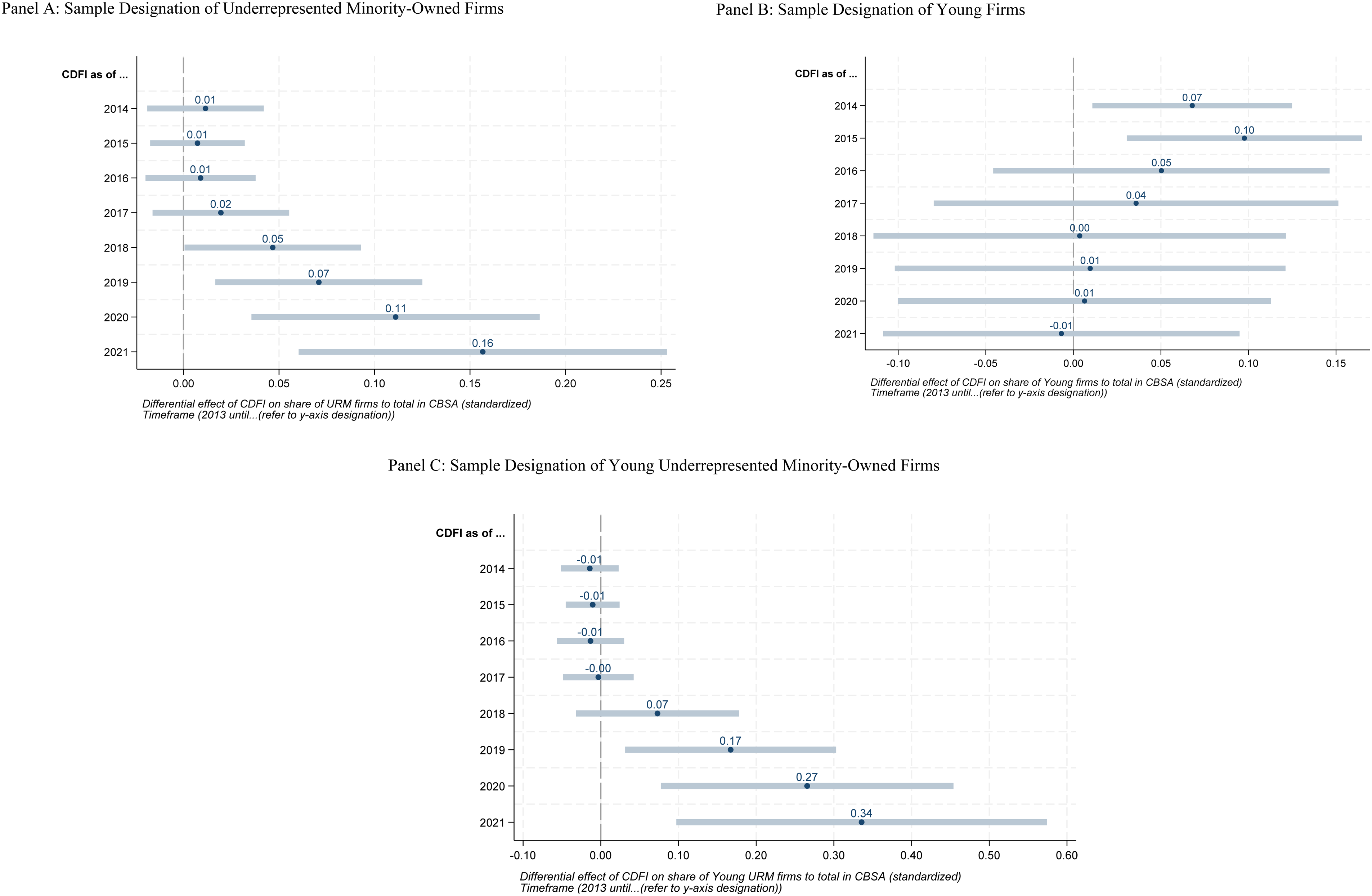

Fourth, we assess dynamic trends of the primary result. Operationally, we adjust the panel time frame. First, we limit it to 2013–2014 and then increase the panel designation by one additional year subsequently until we account for the entire timeframe spanning 2013–2021. Effectively, we re-estimate Equation 1 eight times for each of the three primary dependent variables, respectively. We report the coefficients for CDFI in Figure 5 (Panels A–C). As with the primary results, the dynamic results reveal illustrative and comparable trends for the outcome measure tracing URM and young-URM firms. Notably, there appears to be an initial lag; however, the positive association with URM and young URM firms increases over the extended panel starting in 2018 and 2019. This aligns with the descriptive results reported in Figure 3. Interestingly, in Panel B reporting for young firms, we report positive results over the initial years of the panel, but the results are inconclusive when we account for the larger timeframe.

Dynamic assessment. Panel A: Sample Designation of Underrepresented Minority-Owned Firms. Panel B: Sample Designation of Young Firms. Panel C: Sample Designation of Young Underrepresented Minority-Owned Firms. Note. We report coefficients (and 95th percent confidence interval) for the primary binary regressor, CDFI, from a series of CBSA and year fixed-effect regressions (Equation 1). We adjust the timeframe to examine whether there is a dynamic response. Here, the y-axis denotes the timeframe, which is set from 2013 to 2014, …, 2021. Effectively, we increase the size of the panel by 1 year with each row. Panel title reports detail on dependent variable specification. For example, Panel A reports results for share of underrepresented minority-owned firms (minority and/or woman owned) to total firm activity in CBSA. The metric is standardized.

Taken together, these results suggest that market entry of community-based capital infrastructure providers bolsters the share of firm growth among minoritized and young-minoritized firms. We do not observe a discernible effect on the share of young firms alone.

Extensions: Case Study of Nonprofit Community Bank Seeking CDFI Certification

Our descriptive findings and regression results indicate higher levels of firm and entrepreneurship for minoritized groups in cities with CDFIs relative to those without. However, we are careful not to assume perfect identification with respect to the causal influence of CDFI diffusion on such growth. Indeed, demands for a robust identification strategy would prevent scholars from evaluating the impacts of CDFI formation at all (given that the diffusion of CDFIs is endogenously determined). A standard fixed-effects specification remains somewhat vulnerable to potential sources of bias that result from unobserved time-variant confounding factors that drive both CDFI formation and growth among minoritized business groups. In such cases, we find it useful to triangulate and contextualize quantitative findings using complementary, though distinct, qualitative evidence such as case study interviews. In this section, we include highlights from interviews with executive leaders of a nonprofit community bank seeking formal CDFI certification.

ASPIRE Community Capital was founded in Charlotte, North Carolina in 2016 in response to the limited business resources available to entrepreneurs of color in underresourced neighborhoods. As founder and CEO of ASPIRE, Manuel Campbell's aim was to spur upward mobility and a means of creating wealth for people in local neighborhoods that have long been ignored. ASPIRE's mission is to empower underresourced entrepreneurs by providing them with access to financial products and business resources to radically transform communities. ASPIRE's vision is to create a robust and supportive regional ecosystem that maximizes the potential of every entrepreneur. We emphasize that ASPIRE is presently a prospective applicant for CDFI certification. Our research discovered that ASPIRE was the first organization in the Charlotte metropolitan region to seek formal CDFI certification after initially operating as a provider of business training and technical assistance programs. Our research highlights the possible positive effects of policies that encourage CDFI certification for organizations such as ASPIRE.

Since 2016, ASPIRE has served the Charlotte metropolitan region with training and support services for entrepreneurs, with a focus on attracting talent from minoritized groups—especially women and communities of color. In 2023, ASPIRE began supplementing its services with direct capital assistance in the form of a small business loan fund. While its services are open to all, its target market is low- to moderate-income (LMI) individuals, focusing on supporting Black, Indigenous People, and other people of color (BIPOC) small business owners. In 2023, ASPIRE trained 184 program participants, logging 85 h of technical assistance and producing 110 graduates. Based on estimates provided by ASPIRE's management team, 98% of participants in its technical assistance programs and 100% of participants in its microloan funding program identify as BIPOC. Overall, across both types of programs, 75% of participants are Black females. To serve the BIPOC community directly and expand access to these small business owners, ASPIRE specifically chose its primary business location in one of the most ethnically diverse neighborhoods in the Charlotte region.

A fundamental guiding principle of ASPIRE is the duality of design, meaning this nonprofit organization seeking CDFI certification is designed to bolster human capital and financial capital. ASPIRE provides two broad forms of assistance for community entrepreneurs: (1) business training and technical assistance; and (2) direct capital access through microloans from $1,200 to $50,000 in size. This dual design enables ASPIRE to educate and empower cohorts of business owners who then are better positioned to influence others in the community. Based on our interviews with founder and CEO Manuel Campbell and board vice chair Adam Holtzschue, this multiplier effect is critical for understanding ASPIRE's role in driving Charlotte's entrepreneurial growth patterns among underserved communities. In this way, ASPIRE's impact on its surrounding community is made up of both direct and indirect effects. The former consists of the primary impacts of training, mentorship, and capital on participants in ASPIRE's programming, as described in the quote below: “It's beyond the addition of technical expertise for these young entrepreneurs or entrepreneurs of all ages actually. It is the sense of confidence that is instilled in these individuals. It is a physical and mental transformation for these people to have gone through this. And that translates into energy and, greater opportunity and improved chances for success in their business.” (Adam Holtzschue, vice chair, Board of Directors, ASPIRE Community Capital)

The indirect effect is best seen in the influence ASPIRE clients has upon its peers and other community members. As ASPIRE's founder and CEO, Manuel Campbell, explained: “There's sort of a multiplier effect. You know how this lifts up people who have had fewer opportunities in the past and the effect on the minority community when peers see confidence raised in a fellow entrepreneur. I mean it, never underestimate the power of the example that it sets with others.”

As board member Ronnie Bryant further explained, the dual design feature of assistance and financing is common across CDFIs: “They are designed to provide a service that the community needs, and the 501(c)(3) status gives funders an opportunity to take a tax break for supporting these organizations.” However, what is unique about ASPIRE's approach to dual design is that the organization first focused on developing human capital by providing training programs and then expanded by providing financial capital. According to board member Steve Cohen, the vast majority of CDFIs follow the opposite pathway, starting as lenders first and only later delivering training. This distinction may have important performance implications for ASPIRE because it may enable the organization to assess the revenue potential and creditworthiness of the participants more accurately before they become loan applicants. This may position ASPIRE to create a stronger and more sustainable business model by reducing operating risks and allowing for reinvestment in the local community and expansion of the lending portfolio.

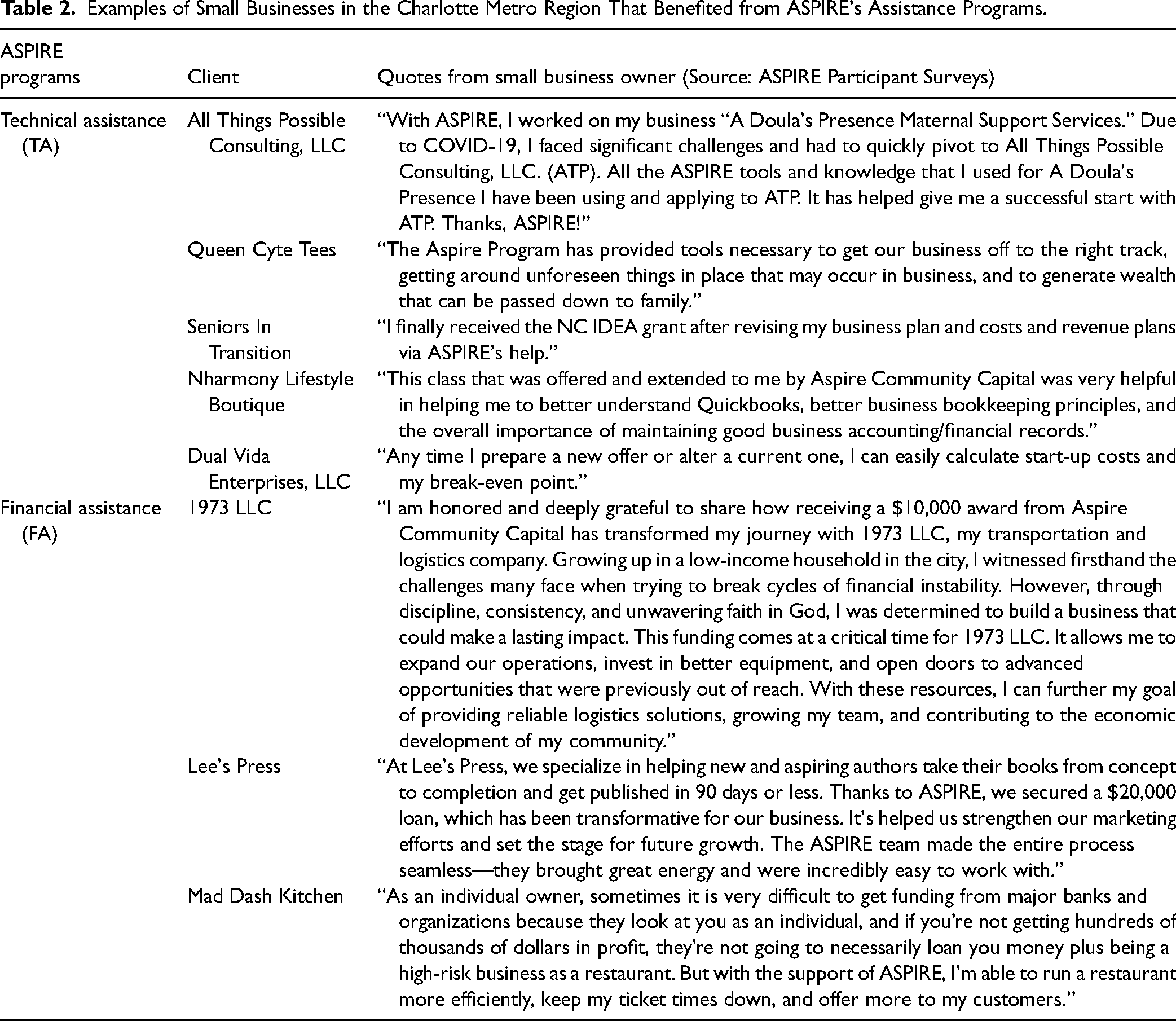

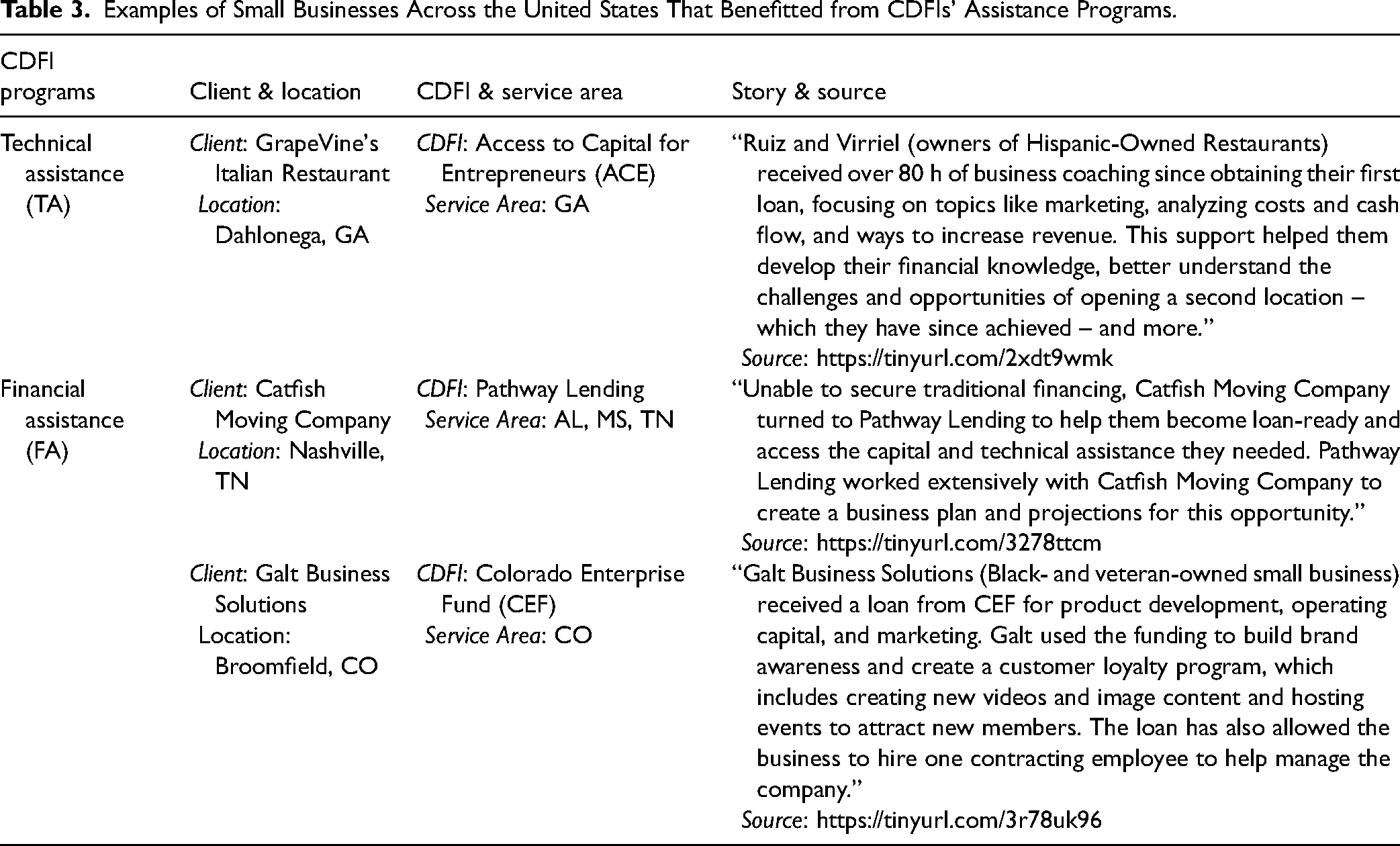

To highlight the perceived value delivered by ASPIRE, we include Table 2, which features quotes from small business owners who participated in ASPIRE's technical and financial assistance programs. We also augment this information with Table 3, which includes additional examples of small businesses outside of Charlotte that benefited from assistance programs offered by CDFIs across the United States.

Examples of Small Businesses in the Charlotte Metro Region That Benefited from ASPIRE's Assistance Programs.

Examples of Small Businesses Across the United States That Benefitted from CDFIs’ Assistance Programs.

As summarized in Tables 2 and 3, prospective applicants seeking CDFI certification and existing organizations with CDFI certification play critical roles in supporting urban entrepreneurs.

Discussion

Our study is motivated by the need to uncover possible root causes of systemic disparities in urban entrepreneurship. Our findings underscore the importance of CDFIs in alleviating resource constraints by providing local resources for minoritized entrepreneurs. Access to sufficient capital for all firms is necessary for creating more inclusive capital markets. While U.S. cities vary widely in the demographic and socioeconomic diversity of the owners of their small businesses, the number and level of activity of young firms that represent diverse populations are essential metrics in determining the overall health of the surrounding economic environment (Cao & Shi, 2021; Guzman & Stern, 2020; Haltiwanger et al., 2013).

Without such levers for inclusion, there is a risk of creating and exacerbating unequal access to opportunities (Guler et al., 2002; Parker et al., 2019). Moreover, the market likely insufficiently addresses the needs of marginalized groups. One example of this phenomenon is the gender gap in medical solutions. A recent study by Koning et al. (2021) reported a robust and sizable connection between inventor gender and the gender-specific focus of inventions, suggesting that the inventor gender gap is partially responsible for thousands of missing female-focused inventions. The generalized point from this study—among others, including Colwell & McGrayne (2021)—is that a harmful feedback loop can form when barriers specifically affect historically marginalized groups. Programs like the CDFI Fund's Financial Assistance and Technical Assistance Awards not only broaden access but also bolster business activity to help address and alleviate such market inefficiencies. 22

In addition, we apply lessons from Robinson's (2007) work that identified financial institutional barriers as a key obstacle for entrepreneurs in urban markets. Related foundational work in the field shows that embeddedness in social and institutional networks can improve local business outcomes (Granovetter, 1985; Uzzi, 1996). Our evidence offers new insights that extend earlier findings regarding relationships between firms and financial institutions operating within the same community. While considerable scholarship has focused on angel or venture capital access (Kerr et al., 2014; Samila & Sorenson, 2011), we shift focus to an essential, yet understudied form of financial access—CDFIs and how they support inclusive economic development. The element of duality of design, in which CDFIs cultivate and provide human capital and financial capital, appears essential in economic development focusing on addressing the needs of urban entrepreneurs.

Limitations

No observational study is without limitations so we highlight a few key areas where additional data would be useful in extensions of this work. For one, this paper represents a foray into estimating impacts of CDFI institutional infrastructure at the level of U.S. cities. Our models and descriptive data represent aggregate trends across a panel of all CBSAs in the United States from 2013–2021. Thus, we are not able to track the mechanisms through which CDFIs drive inclusive entrepreneurship at micro levels, as captured in the transactions, for example, between the firm or individual bank. Additional data on precise lending activity would bolster such research. And while such data demands are not yet available, complementary case studies are more accessible and can build on our early assessment of ASPIRE in Charlotte, NC.

A second set of limitations inheres in the observational nature of the study design. We use careful confounder selection and exploitation of longitudinal variation and city-year fixed effects to enhance the model specification. However, there are inevitably some confounding measures that remain out of reach. Most notably, cities may see increases in institutional capacity alongside CDFIs that also drive growth in firms owned by minoritized groups. If investment and policy trends support CDFIs, they may also lead to increases in other forms of capital investment, training, and mentorship through incubators and educational institutions. Our data include details on the timing of CDFI inclusion, but we lack access to complete records of all relevant institutions. More work remains to account for this breadth of activity and unpack how they interact.

Scholarly, Managerial, and Policy Implications

For scholars, our paper contributes to the literature on the role of capital access in fostering inclusive economic development (Barkley & Schweitzer, 2023; Bates et al., 2022; Cassell et al., 2023; Graves et al., 2023) and community financial institutions (Appleyard, 2011; Bates, 2000; Simmons et al., 2021). We find a notable economic return to the advent of CDFIs, as measured by the formation of URM-owned businesses, especially among young firms. Our empirical study also contributes to a growing list of studies on CDFI activity and proposes a novel econometric approach using longitudinal data at the level of U.S. cities to capture regional economic impacts of community financial infrastructure. Previous systematic review has identified mixed results for the economic impacts of CDFIs (McCall & Hoyman, 2023) with the impacts varying depending on the outcomes measured and the timing of the study. Our study helps to address this tension and bridge the apparent knowledge gap. We do so by updating CDFI analyses to account for activity through 2021 and employing longitudinal establishment data tracing minoritized business groups in a comprehensive and more granular manner.

For managers, our research provides insight into capital access opportunities for minority and woman-owned firms, especially young firms that are often severely constrained in their ability to secure the resources needed to survive and grow in competitive markets. Our research suggests that the dual design principle, featured in our case study of a nonprofit organization seeking CDFI certification, appears to offer invaluable training and support for such communities. For policy makers, our results emphasize the importance of government certification and support in providing financial assistance for CDFIs to strengthen inclusive urban economies, especially among underserved communities. Our findings imply that proposed policy reforms that encourage the entry of new CDFIs or expand the geographic footprint of existing CDFIs are likely to boost the formation rate of minority and woman-owned businesses.

Conclusion

Our research establishes a framework for econometric evaluation of inclusivity outcomes at the level of U.S. cities. Key findings highlight the observable shifts in the rate of business formation that follow the entry of CDFIs into U.S. metropolitan and micropolitan areas. Our study offers new evidence to help guide focused scholarly inquiry, support effective managerial decision making, and formulate sound government policies regarding the role of CDFIs in driving inclusive entrepreneurship and economic development.

Supplemental Material

sj-docx-1-edq-10.1177_08912424251323208 - Supplemental material for The Role of Community Development Financial Institutions in Supporting Inclusive Economic Development

Supplemental material, sj-docx-1-edq-10.1177_08912424251323208 for The Role of Community Development Financial Institutions in Supporting Inclusive Economic Development by Evan E. Johnson, Lauren Lanahan, Amol M. Joshi and Iman Hemmatian in Economic Development Quarterly

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Science Foundation (grant number 2032914), Ewing Marion Kauffman Foundation Junior Faculty Fellowship in Entrepreneurship Research (Joshi), Wake Forest University School of Business.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.