Abstract

As most previous research on pay transparency focused on individual- or organizational-level dynamics, we have limited understanding of the impact of pay transparency on culture or climate within an organization. This study investigates how procedural pay transparency is associated with the motivational climate in work units within organizations. One might argue that, in the presence of pay transparency, employees may further engage in social comparisons to learn about how they are doing relative to their peers, which leads to an increased performance climate, where success is defined based on relative performance. However, the findings from this study suggest that procedural pay transparency is positively associated with mastery climate instead, that is, a work unit climate where success is defined based on learning, growth, and effort. Furthermore, the results suggest that procedural pay transparency is meaningfully related to sorting and motivational effects through its impact on mastery climate.

Introduction

Pay transparency, that is, disclosing (some aspect of) pay information to employees, is a global trend. The purpose of most pay transparency policies in different geographies is to combat pay discrimination (Cullen, 2023). According to Cullen (2023), among the countries that have implemented laws with this intent, 89% implemented policies that reveal pay gaps horizontally between coworkers of similar seniority within a firm. These policies vary in how pay information is provided, whether it is reporting gender wage gap statistics, disclosing wages or wage ranges for jobs upon request to individual employees or shop stewards, protecting employee disclosure such that workers have the right to talk about their pay, and/or precluding employers to ask about candidate’s salary history.

In 2023, nearly 44.8 million people in the United States, or more than one-quarter (26.6%) of U.S. workers, live in a city or state where employers are required by law to disclose pay information in some form. Many of these initiatives include disclosing pay information in hiring, as part of job postings (e.g., New York, Colorado, Washington, Washington, DC); however, other states require employers to share pay information when requested by employees (e.g., California, Nevada, Maryland, Connecticut). Furthermore, the Society for Human Resource Management (SHRM) 1 reports that companies face growing pressure from the job market, as 62% of job seekers report that including a salary range in a job posting is the most important driver for deciding whether to apply for a position.

In the European Union, there is a lot of variation between countries in the types of policies in effect (for a recent review, see Veldman, 2017). In 2017, only 10 out of 31 countries (32%) had implemented at least one core pay transparency measure as recommended by the EU. Consequently, the new 2023/970/EU directive (in force since June 6, 2023) 2 stipulates multiple measures to aid with progress: On the one hand, employers must make the criteria easily accessible for determining pay setting and progression, indicating the initial pay or its range to potential applicants, and posting job titles in a gender-neutral way. Employers will not be allowed to ask questions related to the applicants’ former or current salaries. On the other hand, employees will also be able to request written information on their individual pay level and the average pay level listed by gender and categories of workers performing the same work, to be provided within two months. The directive also states that workers cannot be prevented from disclosing their pay information. The directive therefore aims to contribute to the enforcement of the principle of equal pay by making information on pay structures more easily available, sanctioning unjustified pay differences, and imposing new obligations on employers. These changes are mainly upcoming, as EU member states will have three years to transpose the directive into national legislation.

Thus, while pay transparency is a trend in the United States and the European Union, among other geographies (Cullen, 2023), variations in policy and law enforcement are significant; in many countries, these measures have been optional (Ceballos et al., 2022). Consequently, variation is also significant in how much private-sector companies and public organizations are willing to offer information, especially on the bases and mechanisms through which pay is structured and distributed. Further, as organizations rely on middle-level managers to primarily set goals, discuss performance, and the career prospects of individual employees, there can also be differences between work units within an organization in the degree to which the management shares information regarding how pay is determined (e.g., Alterman et al., 2021; Fulmer & Chen, 2014). Supervisors and middle managers are key sources for employees for information about pay, performance management, and career progression.

Research suggests that pay transparency can be a double-edged sword (Colella et al., 2007). On the one hand, pay transparency can boost individual task performance (Bamberger & Belogolovsky, 2010; Belogolovsky & Bamberger, 2014; Greiner et al., 2012; Tremblay & Chênevert, 2008), increase help-seeking (Belogolovsky et al., 2016), and reduce gender pay gap (Bennedsen et al., 2022). On the other hand, pay transparency can create pronounced feelings of envy toward coworkers and decrease willingness to voluntarily help them (Bamberger & Belogolovsky, 2017). Pay transparency can also create privacy and social concerns (Smit & Montag-Smit, 2019), lead to greater pay compression (Mas, 2017), and cause employers to bargain more aggressively, thus lowering average wages (Cullen, 2023).

However, pay transparency involves multiple key decisions (Fulmer & Arnold, 2020) that may have a differential impact in organizations. The first decision is communicating about “what,” that is, what, if any, pay outcome information will be shared? For example, it could involve disclosing anything from individual salary numbers, group averages to pay ranges. The second decision relates to communicating about “why,” that is, how transparent will an organization be about why pay is set the way it is (i.e., the processes by which pay is determined)? The remaining two decisions pertain to shaping “how” information spreads: decisions on how the organization disseminates pay-related information (e.g., modes or channels of communication include intranet, human resource[s] [HR] staff or managers, etc.); and how employees communicate about pay among themselves and to what extent they will be discouraged from doing so.

In this study, we focus on procedural pay transparency, which refers to how employees perceive an organization’s transparency about why pay is set the way it is (i.e., pay bases and mechanisms to determine pay). We aim to advance the pay transparency literature in several ways. First, we study how procedural pay transparency relates to motivational climates at the work unit level. Second, we study whether motivational and sorting effects of pay transparency can be explained by motivational climate. Thus, our study also contributes to the literature on motivational work climate. Our empirical study was conducted in Northern Europe in 20 organizations with varying degrees of procedural transparency and is based on 4652 employee survey responses from 127 distinct work units.

Pay Transparency and Motivational Climate

In a competitive, complex, and volatile business environment, companies need more from their employees. Thus, in many organizations, leaders have traditionally focused on building “high-performance” cultures and climates. However, focusing on performance only might not be the best, healthiest, or most sustainable way to fuel results, as it may overwhelm employees, as a performance-driven culture often exacerbates people’s fears by creating a zero-sum game in which people either succeed or fail (Schwartz, 2018), wherein success is defined by social comparison. Thus, it may be more effective to focus on creating growth-based cultures and climates instead. In these work environments, employees feel safe, that is, there is focus on continuous learning through inquiry, manageable experiments, and continuous feedback.

This idea is not new. A long stream of research in the education and sports settings shows that a performance-driven climate might backfire (Ames, 1992). According to this literature, learning environments can be constructed to enhance performance goals with a focus on ability and sense of self-worth that is dependent on doing better than others do (i.e., social comparison). Alternatively, environments can be constructed to enhance mastery goals based on a belief that effort will lead to a sense of mastery, fostering self-referenced feedback that supports personal growth. Research shows that a performance goal fosters a failure-avoiding pattern of motivation, whereas a mastery goal elicits a motivational pattern that is associated with a quality of involvement likely to maintain the behavior (Ames, 1992). Relatedly, achievement goal theory (AGT; e.g., Nicholls, 1989) argues that, whereas “ego goals” emphasize outperforming others, “task goals” emphasize learning and improving. Task and ego goals have also been referred to as mastery–learning and performance–competitive goals, respectively.

Professor Carol Dweck, an academic who popularized this line of research, noted in her infamous book Mindset: The New Psychology of Success (Dweck, 2007) and TED talk “The Power of Believing That You Can Improve” (Dweck, 2014) that we should cultivate a “growth” mindset (e.g., whereby seeing failure is an opportunity to grow) instead of encouraging a more “fixed” mindset (e.g., focusing on fixed idea of oneself: I am either good or I am not). Her contributions have inspired prominent business leaders such as Satya Nadella at Microsoft, wherein “growth mindset” is defined as a positive and forward-thinking mindset: “It embraces every misstep as a learning opportunity, not as a failure. It is an open-minded perspective that encourages improvement, which leads to success.” 3 Forbes claims that growth mindset culture tripled Microsoft’s value. 4

Most prominently, Nerstad and colleagues (Kopperud et al., 2020; Nerstad et al., 2013, 2018, 2020) brought the measurement of the impact of motivational climate to the field of management studies. Motivational climate refers to employees’ shared perceptions of criteria for success and failure (Nerstad et al., 2013), affected by the policies, practices, and procedures of their work environment, such as communication about how employees are paid and rewarded. The motivational climate consists of two dimensions: mastery and performance. Mastery climate refers to work situations wherein success is defined based on learning, growth, and effort; performance climate refers to work situations wherein success is based on social comparison and normative ability (Nerstad et al., 2018).

A two-wave longitudinal study by Nerstad et al. (2020) found that mastery climate is positively related to individuals’ basic psychological needs satisfaction (i.e., autonomy, relatedness, and competence), whereas performance climate is negatively related. Further, the authors found that basic psychological need satisfaction mediates the relationship between motivational climates and energy at work (e.g., absence of emotional exhaustion and presence of vigor).

Research has also shown that mastery and performance climate can have distinct concurrent impact on outcomes. For example, previous research (Kopperud et al., 2020) has found that a perceived mastery climate reduces the negative spillover between professional and private spheres, thus decreasing employees’ turnover intention. In contrast, a perceived performance climate increases employees’ turnover intention, partly explained by work–home spillover. Perceptions of climates and their impact on individuals are shown to become quite stable over time. A longitudinal study by Nerstad et al. (2020) suggests that a person’s goal orientation and perceptions of motivational climate are strongly interconnected such that exposure to a perceived mastery climate encourages mastery orientation, while a perceived performance climate encourages performance orientation. More specifically, the authors revealed that the perceived motivational climate explains 50% of the between-person variance in mastery orientation and 14% of the between-person variance in performance orientation. As the climates only explain a small percentage of the within-person variation over time (2% of both orientations), the findings suggest that perceived motivational climates to a greater extent explain why people differ in goal orientation (mastery vs. performance).

But how are the climates formed? Organizations can facilitate a culture of transparency, where information about the pay system is openly shared in intranet, training, and job postings (Day, 2007). Further, individual managers can have a substantial impact on the forming of shared, work-unit-level climates. Transparency and open communication form an essential part of fostering a working climate that supports employee growth and development. The same should apply to being open about how the pay system works, creating a sentiment that employees have the necessary information to craft their own careers and grow in the organization. However, as research on pay transparency also shows that openly sharing information about pay may also lead to envious feelings, it is possible that procedural pay transparency is related to a scarcity-driven performance-obsessed climate instead. Therefore, we ask the following two questions:

Does procedural pay transparency contribute to the emergence of performance climate and/or mastery climate in work units?

Does procedural pay transparency affect motivational and/or sorting effects (task performance and/or turnover intentions) via the performance and/or mastery climate?

Method

Sample and Procedure

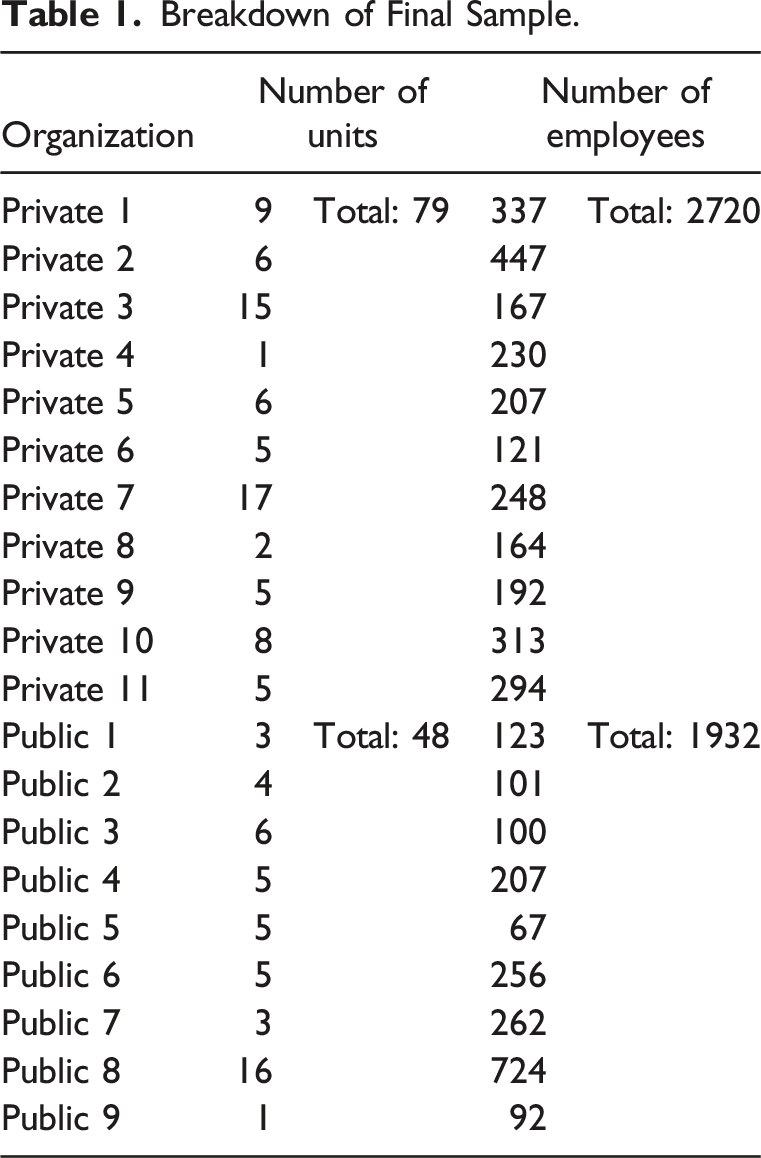

The sample for this study comprised 20 organizations in Finland operating in different sectors (11 from the private sector and nine from the public sector). The companies varied in size from small to large. Each company included between-work units with variance in the extent to which procedural pay transparency was practiced (there were a total of 136 units across the organizations).

We conducted multisource, single-wave data-collection processes across these organizations. Specifically, separate surveys were distributed to HR representatives and employees. The survey for the HR representatives contained questions about the characteristics of their organizations, including whether their companies adopt a performance-based pay practice. All HR representatives from the 20 companies successfully completed the surveys. The survey for the employees included questions regarding their demographics, perceptions regarding their work units (i.e., procedural pay transparency implementation and work climates), turnover intention, and task performance. The survey responses were anonymous and voluntary. In total, 5244 employees completed and returned their surveys.

Breakdown of Final Sample.

Measures

Procedural Pay Transparency (Unit-Level)

We used five items from Day (2007) to measure procedural pay transparency. 6 The items were as follows: “I know where to go to get answers to my compensation questions”; “I get the information I need about my pay programs”; “Internal job postings provide information about the pay opportunity of job openings”; “My organization provides employees with written information about how pay levels are determined”; and “My supervisor has explained to me how pay levels are determined for the jobs in my organization.” Employees rated the items based on a five-point Likert scale (1 = strongly disagree to 5 = strongly agree). Cronbach’s alpha for employees’ ratings of procedural pay transparency was .77. The collected employee responses were aggregated to the unit level by calculating the mean of procedural pay transparency ratings for each unit. The within-unit aggregation statistics were as follows: rwg = .66; ICC(1) = .10 (p < .05); and ICC(2) = .82. Overall, the aggregation statistics showed moderate agreement (LeBreton & Senter, 2008) as well as acceptable levels of nonindependence and reliability of the unit mean (e.g., Heavey & Simsek, 2017; Kehoe & Collins, 2017) that justify aggregation.

Mastery Climate (Unit-Level)

Four items from Nerstad et al. (2013) were used to measure mastery climate: “Each individual’s learning and development is emphasized”; “One is encouraged to cooperate and exchange thoughts and ideas mutually”; “Employees are encouraged to try new solution methods throughout the work process”; and “Everybody has an important and clear task throughout the work process.” Employees rated the items based on a five-point Likert scale (1 = strongly disagree to 5 = strongly agree). Cronbach’s alpha for employees’ ratings of mastery climate was .80. The collected employee responses were aggregated to the unit level by calculating the mean of mastery climate ratings for each unit. The within-unit aggregation statistics were as follows: rwg = .64; ICC(1) = .06 (p < .05); and ICC(2) = .72. Overall, the aggregation statistics showed moderate agreement (LeBreton & Senter, 2008) as well as acceptable levels of nonindependence and reliability of the unit mean (e.g., Heavey & Simsek, 2017; Kehoe & Collins, 2017) that justify aggregation.

Performance Climate (Unit-Level)

Four items from Nerstad et al. (2013) were used to measure performance climate: “Work accomplishments are measured based on comparisons with the accomplishments of coworkers”; “There exists a competitive rivalry among the employees”; “Rivalry between employees is encouraged”; and “It is important to achieve better than others.” Employees rated the items based on a five-point Likert scale (1 = strongly disagree to 5 = strongly agree). Cronbach’s alpha for employees’ ratings of performance climate was .79. The collected employee responses were aggregated to the unit level by calculating the mean of performance climate ratings for each unit. The within-unit aggregation statistics were as follows: rwg = .69; ICC(1) = .09 (p < .05); and ICC(2) = .80. Overall, the aggregation statistics showed moderate agreement (LeBreton & Senter, 2008) as well as acceptable levels of nonindependence and reliability of the unit mean (e.g., Heavey & Simsek, 2017; Kehoe & Collins, 2017) that justify aggregation.

Turnover Intention (Individual-Level)

Four items from Bozeman and Perrewé (2001) were used to measure turnover intention: “I will probably look for a new job in the near future”; “I often think about quitting [this organization]”; “At the present time, I am actively searching for another job outside [the organization]”; and “I am intending to quit my job.” Employees rated the items based on a five-point Likert scale (1 = strongly disagree to 5 = strongly agree). Cronbach’s alpha for employees’ ratings of turnover intention was .89.

Task Performance (Individual Level)

Three items from Goodman and Svyantek (1999) were used to measure task performance: “I demonstrate expertise in all job-related tasks”; “I am competent in all areas of the job, and handle tasks with proficiency”; and “I perform well in the overall job by carrying out tasks as expected.” Employees rated the items based on a seven-point Likert scale (1 = never to 7 = always). Cronbach’s alpha for employees’ ratings of task performance was .82.

Control Variables

We incorporated five individual-, six unit-, and two organizational-level control variables. At the individual level, we controlled for employees’ age (in years), sex (0 = female; 1 = male), education (ordinally measured: 1 = elementary school-level; 2 = vocational school-level; 3 = undergraduate level; 4 = master level; and 5 = doctoral level), monthly pay (in euros), and full-time status (0 = part-time; 1 = full-time). The five variables were measured via employee self-reports. We included these factors in our analysis to account for variances in our individual-level outcome variables caused by differences in individual demographics. We control for pay-for-performance (the extent to which performance-based pay was offered to individual employees [each organization’s HR department provided the information on the extent to which performance-based pay was offered to individual employees based on an ordinal scale: 1 = none; 2 = up to 10% of total pay; and 3 = more than 10% of total pay]) as well as the unit means of employees’ age, sex, education, monthly pay, and full-time status (unit-level means of the above-mentioned individual-level controls).

The first variable (i.e., pay-for-performance) was incorporated because pay transparency research indicates that differences in variable pay should be accounted for to accurately understand pay transparency’s associations with its outcomes (Belogolovsky & Bamberger, 2014). The latter five variables were controlled to minimize demographics-related biases on employees’ collectively shared perceptions (i.e., work climates). At the organizational level, adapted from Takeuchi et al. (2009), we further accounted for sector-fixed effects (0 = private; 1 = public) and organization size (total number of employees) to account for potential systematic biases they may induce. Information regarding these two variables was obtained from HR managers.

Analytical Strategy

As our study sample was comprised of three levels (i.e., individual [level 1], unit [level 2]; and organization [level 3]), we employed a mixed-effects model with robust standard errors. Adapting Hofmann and Gavin’s (1998) approach, we grand-mean centered nondichotomous predictors and controls and allowed between-organization/unit variability in the intercept. 7 The variability in the intercept was allowed to better account for unobserved unit- and organization-specific biases. Moreover, in examining procedural pay transparency’s indirect relationships with employee outcomes (i.e., turnover intention and task performance) via mastery and performance climates, we used the nested-equations path analytic approach (Edwards & Lambert, 2007; Preacher et al., 2007). To account for the non-normal distribution of the product coefficients in testing indirect relationships, we utilized a bootstrapping procedure with 20,000 repetitions to calculate the confidence intervals of the tested indirect relationships based on the sampling distributions.

Results

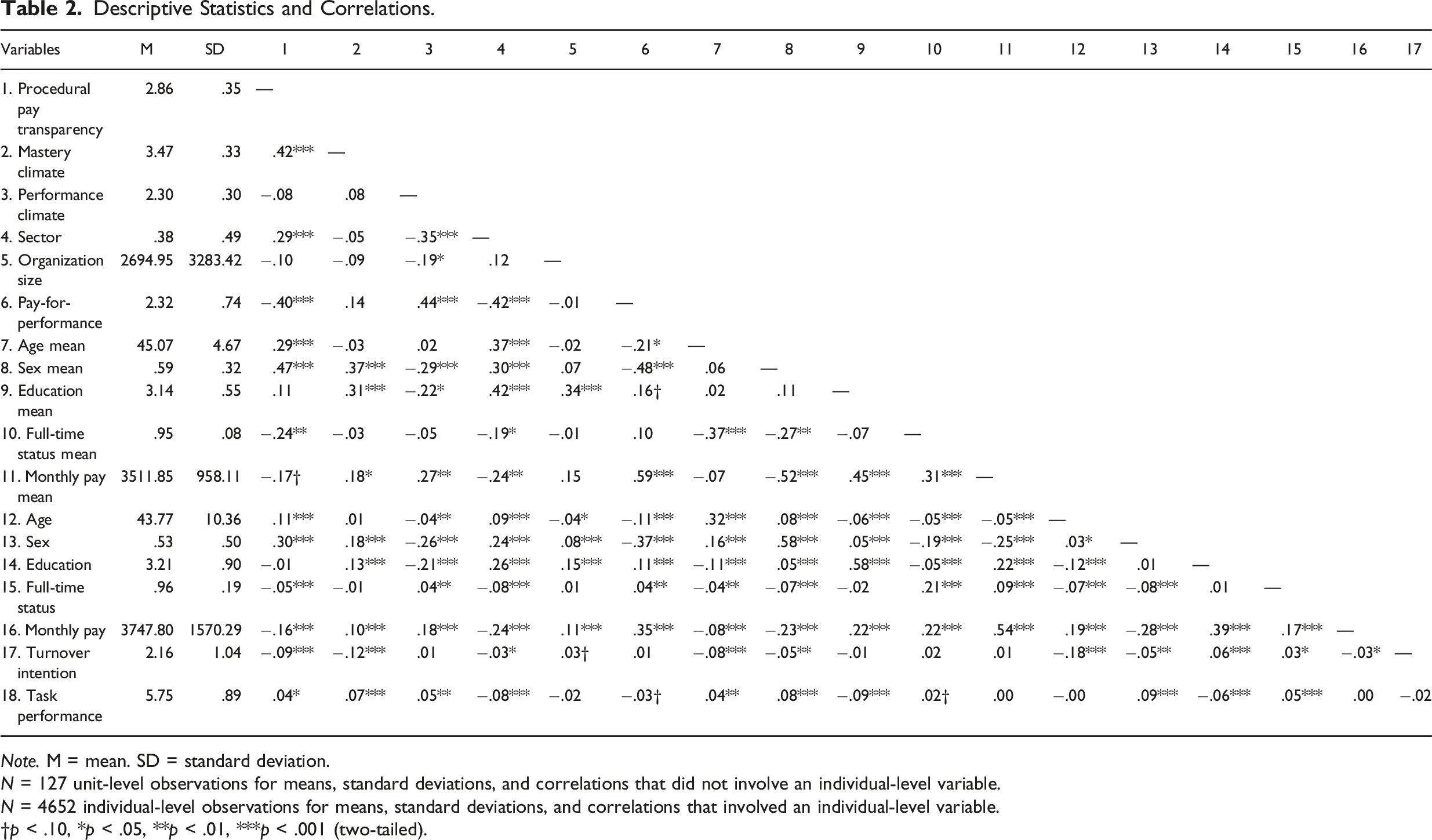

Descriptive Statistics and Correlations.

Note. M = mean. SD = standard deviation.

N = 127 unit-level observations for means, standard deviations, and correlations that did not involve an individual-level variable.

N = 4652 individual-level observations for means, standard deviations, and correlations that involved an individual-level variable.

†p < .10, *p < .05, **p < .01, ***p < .001 (two-tailed).

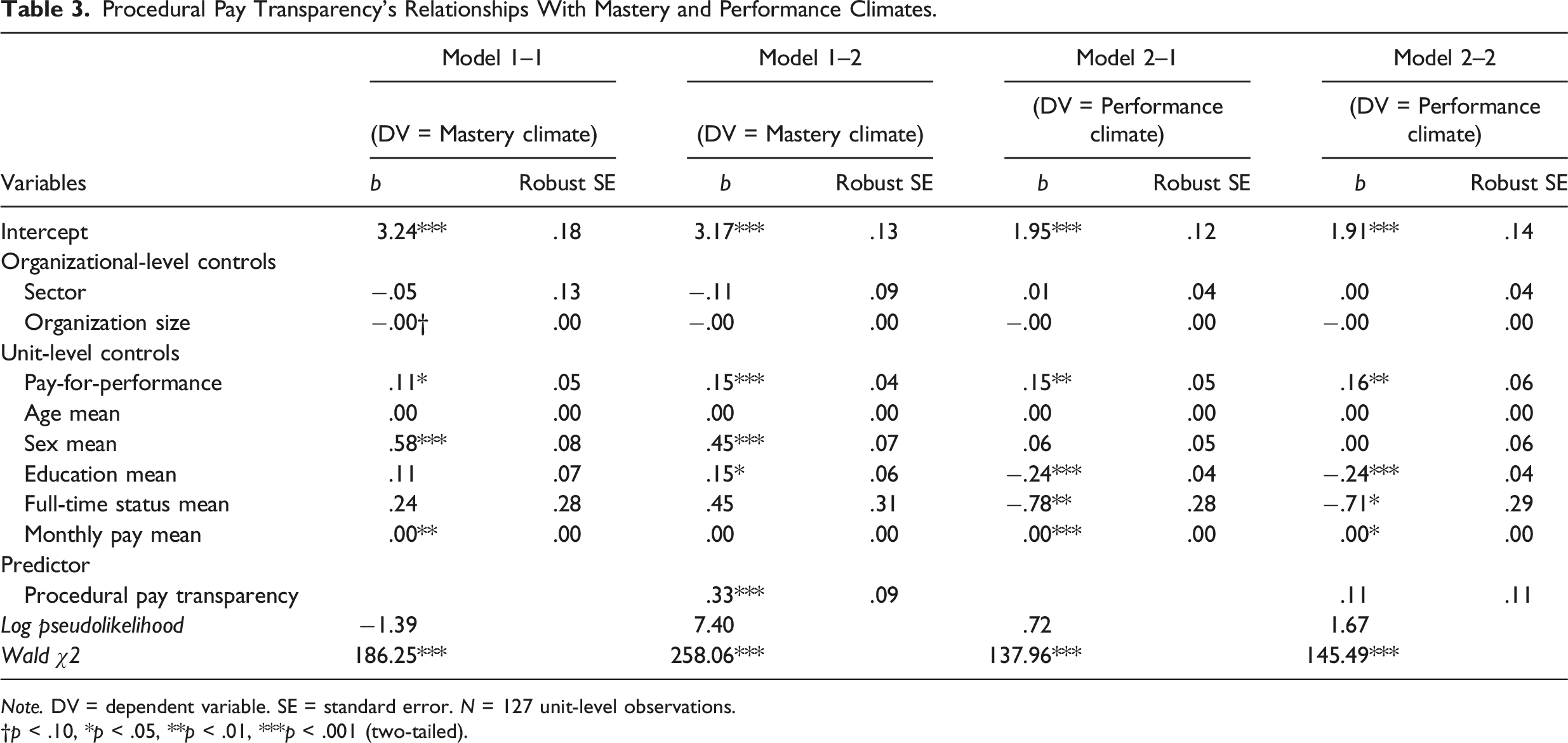

Procedural Pay Transparency’s Relationships With Mastery and Performance Climates.

Note. DV = dependent variable. SE = standard error. N = 127 unit-level observations.

†p < .10, *p < .05, **p < .01, ***p < .001 (two-tailed).

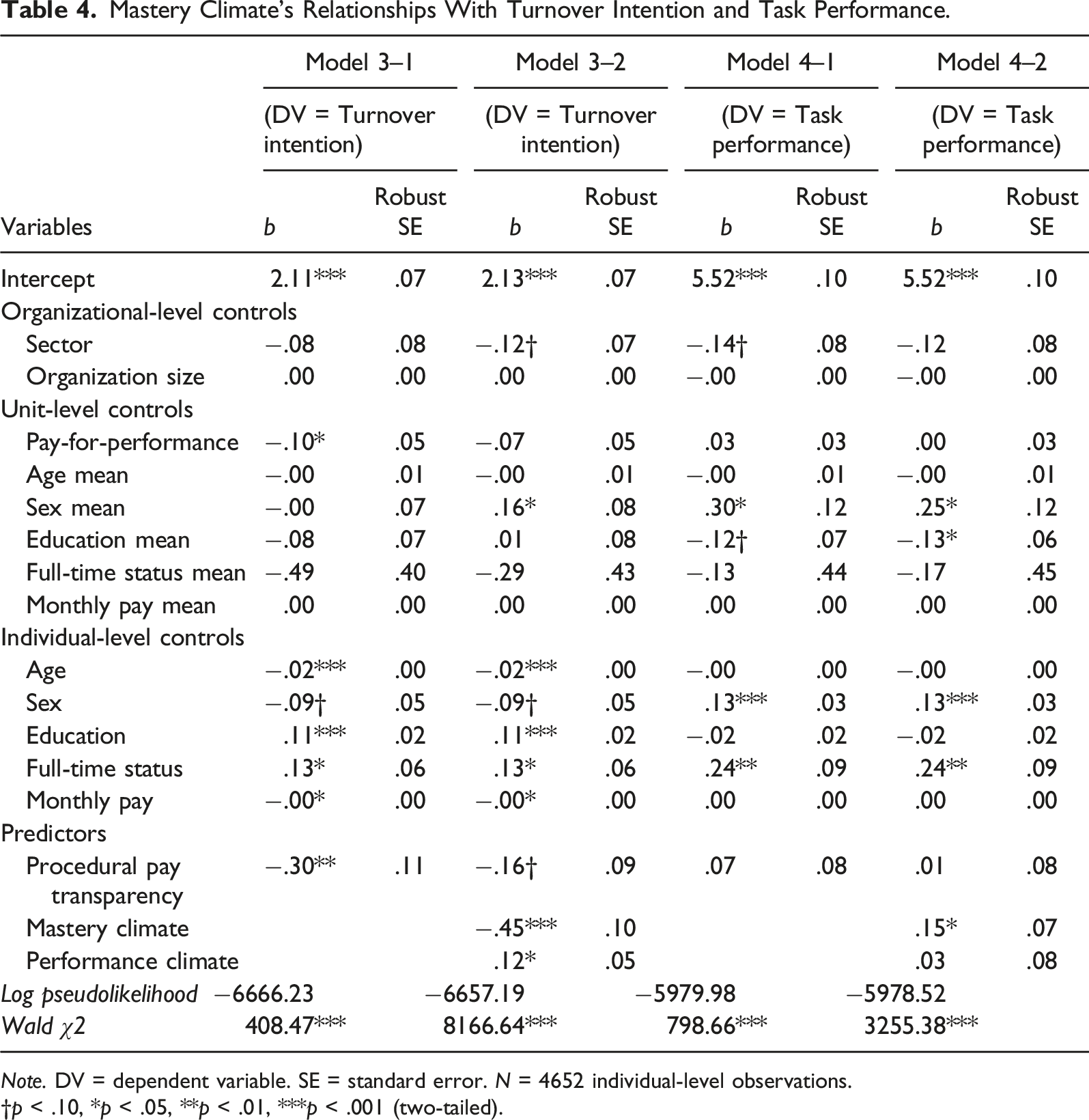

Mastery Climate’s Relationships With Turnover Intention and Task Performance.

Note. DV = dependent variable. SE = standard error. N = 4652 individual-level observations.

†p < .10, *p < .05, **p < .01, ***p < .001 (two-tailed).

Procedural pay transparency’s indirect relationships with turnover intention and task performance via mastery climate were tested using the estimates derived from empirical models, as shown in Tables 3 and 4. The results show that procedural pay transparency’s indirect relationship with turnover intention via mastery climate is negative (b = −.15; SE = .05; significant based on a 95% confidence interval [–.26, −.06]). In addition, the results demonstrate that procedural pay transparency’s indirect relationship with task performance via mastery climate is positive (b = .05; SE = .03; significant based on a 95% confidence interval [.004, .11]).

Post Hoc Analyses

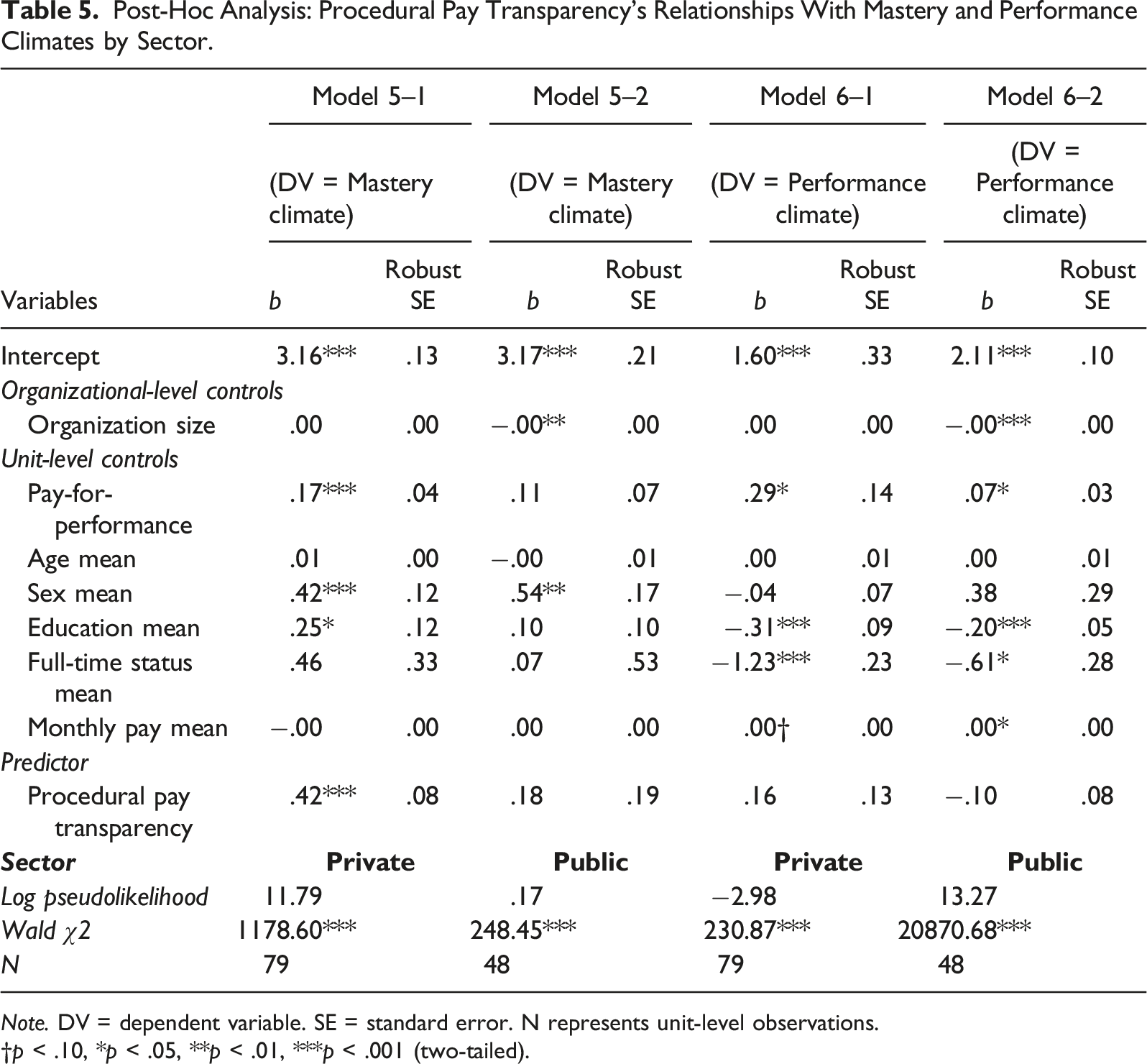

Post-Hoc Analysis: Procedural Pay Transparency’s Relationships With Mastery and Performance Climates by Sector.

Note. DV = dependent variable. SE = standard error. N represents unit-level observations.

†p < .10, *p < .05, **p < .01, ***p < .001 (two-tailed).

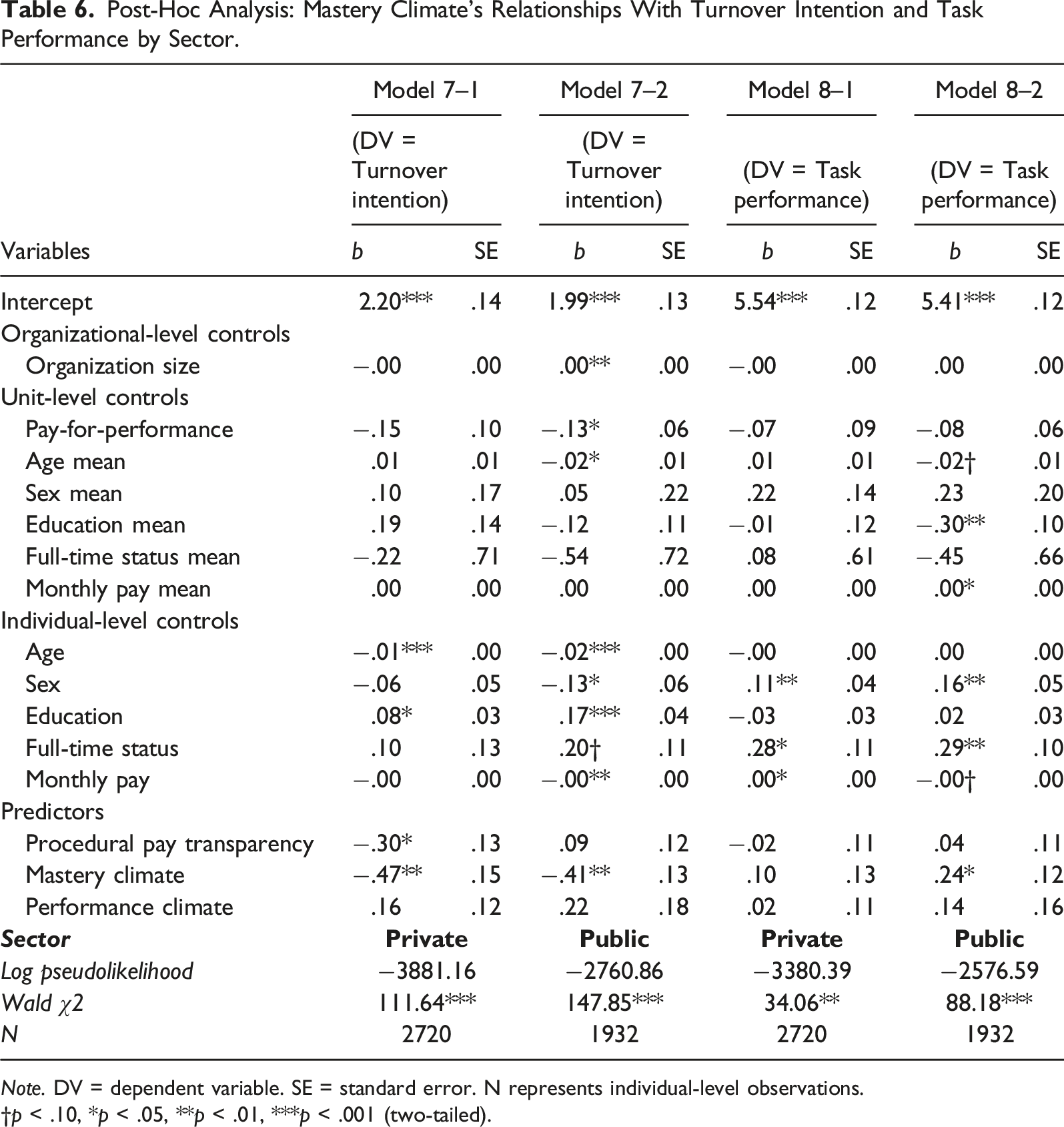

Post-Hoc Analysis: Mastery Climate’s Relationships With Turnover Intention and Task Performance by Sector.

Note. DV = dependent variable. SE = standard error. N represents individual-level observations.

†p < .10, *p < .05, **p < .01, ***p < .001 (two-tailed).

Overall, the relational patterns among procedural pay transparency, motivational climates, and employee outcomes found in the private and public sector subsamples were comparable with what was found in the full sample, albeit there were some differences in terms of statistical significance. While these findings are intriguing, we suggest caution in interpretating the findings and leave it to the readers, as the difference across the private and public sector subsamples may be attributed to multiple factors, including sector-specific differences and reduced statistical power.

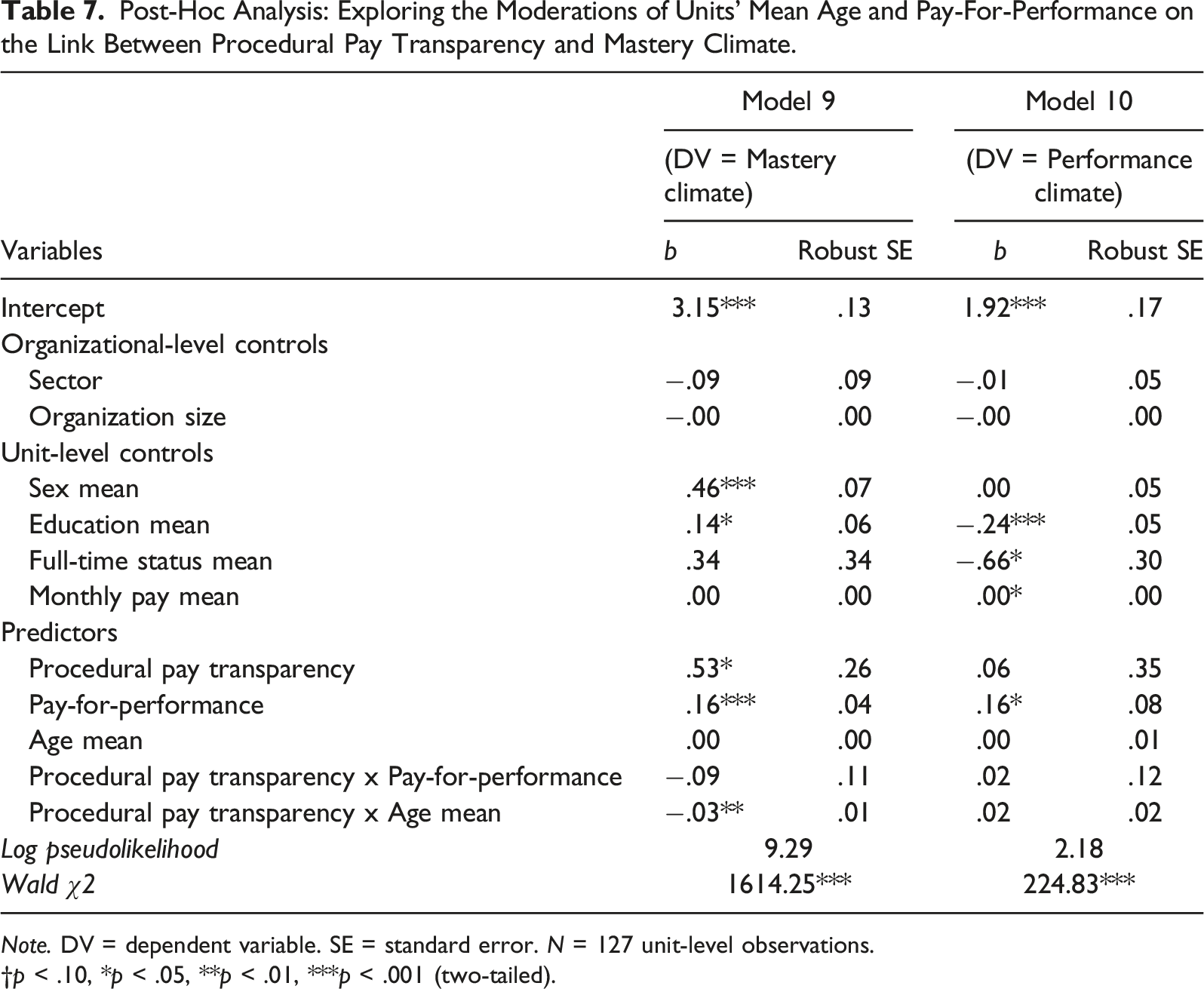

Post-Hoc Analysis: Exploring the Moderations of Units’ Mean Age and Pay-For-Performance on the Link Between Procedural Pay Transparency and Mastery Climate.

Note. DV = dependent variable. SE = standard error. N = 127 unit-level observations.

†p < .10, *p < .05, **p < .01, ***p < .001 (two-tailed).

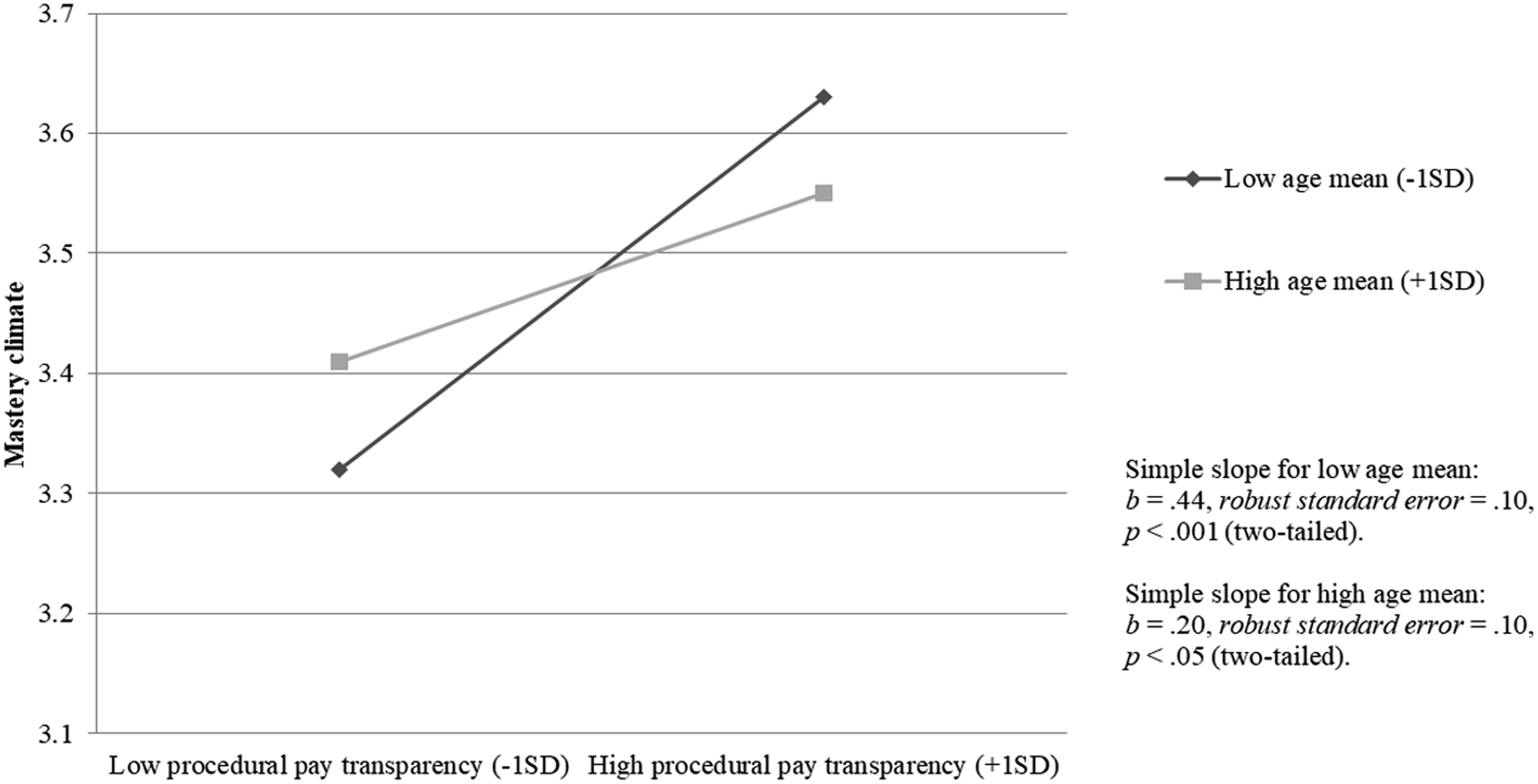

Post Hoc analysis: The interaction between units’ mean age and procedural pay transparency on mastery climate.

Based on the finding that the interaction term between procedural pay transparency and the age mean of the unit is significantly related to mastery climate, we examined how procedural pay transparency’s indirect relationships with turnover intention and task performance via mastery climate differed based on age mean. Using the estimates derived from the empirical models shown in Tables 4 and 7, we found that procedural pay transparency’s conditional indirect relationship with turnover intention via mastery climate was more strongly negative when age mean was one standard deviationbelow the mean (b = −.20; SE = .06; significant based on a 95% confidence interval [–.34; −.09]) than when age mean was one standard deviation above the mean (b = −.09; SE = .05; significant based on a 95% confidence interval [–.19, −.002]). We also found that procedural pay transparency’s conditional indirect relationship with task performance via mastery climate was more strongly positive when the age mean was one standard deviation below the mean (b = .07; SE = .03; significant based on a 95% confidence interval [.01, .14]) than when the age mean was one standard deviation above the mean (b = .03; SE = .02) significant based on a 90% confidence interval [.002, .07]).

Discussion

Previous research suggests that pay transparency can be a double-edged sword (Colella et al., 2007). Transparency can exacerbate employee jealousy and facilitate conflicts (Balkin & Gomez-Mejia, 1990). In contrast, drawing from equity (Adams, 1965) and justice (Greenberg, 1990) theories, those favoring pay transparency argue that, by promoting internal consistency, pay transparency reinforces employee trust in management and has positive incentive and sorting effects, thus boosting task commitment and facilitating the retention of strong performers (e.g., Cloutier & Vihuber, 2008).

Whereas full distributive or outcome transparency (publishing individual pay levels) is still relatively rare in organizations, the general trend is that organizations see many benefits in being more transparent in communicating about pay procedures, for example, why pay is set the way it is (i.e., procedural pay transparency). This is also increasingly expected by organizations operating in the EU and becoming more frequent in the U.S. context, too, especially in recruitment situations. According to employee surveys, most employees are in favor of increasing transparency in an anonymous fashion, reporting average salaries by position (for example, based on reports published by CNBC 8 and SHRM 9 in 2022). The results of our study suggest that indeed there might be multiple benefits to increasing procedural pay transparency.

Our study is, to our best knowledge, the first to investigate the impact of pay transparency on motivational climate (e.g., Nerstad, et al., 2013, 2018) in work units within organizations. Intuitively, one might think that, in the presence of pay transparency, employees might collectively focus more on social comparison, for example, how they are doing relative to their peers, which is how success is defined when employees work in a unit characterized by a performance climate; however, the findings of our study suggest that procedural pay transparency is positively associated with a mastery climate instead, that is, a work unit climate where success is defined based on learning, growth, and effort. Our results further suggest that a mastery climate, in turn, is related to meaningful sorting and motivational effects. Employees who perceive that they receive information about why they are paid the way they are also collectively perceive they work in a unit characterized by mastery climate, which in turn is related to lower turnover intentions and higher (self-reported) task performance.

Our study contributes to the literature on pay transparency and motivational work climate. Our research reveals that procedural pay transparency is related to mastery climate; suggesting that openness about pay procedures may fulfill basic employee needs of autonomy, relatedness, and competence (Nerstad et al., 2020). According to previous research, mastery climate supports effort and cooperation, as individuals feel that success is defined by learning, mastery, and skill development (Ames, 1992; Nicholls, 1989). Such a climate has been found to promote more adaptive behaviors, such as better performance, higher levels of work engagement, additional effort, and persistence in the face of difficulty (Nerstad et al., 2013; Ntoumanis & Biddle, 1999; Roberts, 2012). Similar to previous research, in our study, we found that mastery climate supports task performance and is related to a lower level of turnover intentions, in part explained by procedural pay transparency.

In contrast with mastery climate, previous research suggests that performance climate emphasizes normative criteria for success (Roberts, 2012). Thus, normative ability, social comparison, and intrateam competition are emphasized (Ntoumanis & Biddle, 1999). While it may be surprising that openness about pay procedures (procedural pay transparency) was not related to performance climate in our study, and that, in our post hoc analysis, we did not find evidence that the relationship would be dependent on the level of pay for performance in the organizations either, the result is in line with the existing research in the area of organizational justice, thus highlighting that transparency fosters an overall perception of fairness and trust in organizations (e.g., Colquitt et al., 2001). While procedural pay transparency was not related to performance climate in our study, performance climate was related to a higher level of turnover intentions, in line with previous research. Namely, performance climate has been found to be associated with maladaptive employee outcomes, such as performance anxiety, poorer performance, lower persistence, controlled motivation, and turnover intentions (Abrahamsen et al., 2008; Nerstad et al., 2013; Ntoumanis & Biddle, 1999).

Increasing procedural pay transparency offers many potential benefits for employers, given that lack of transparency introduces uncertainty. Employees may think that their employer or superiors have something to hide, as lack of procedural pay transparency has been found to relate to malevolent attributions of the employer somewhat positively and relate to the lack of benevolent attributions strongly negatively (Montag-Smit & Smit, 2021). These attributions generally mediate the relationship between pay secrecy and trust. In contrast, communication about the compensation procedures increases the distinctiveness of the HRM system that creates a “strong” situation, where employees understand what is expected of them and how they are rewarded for their contributions (Bowen & Ostroff, 2004).

Findings from our post hoc analysis suggest that younger employees are more likely to react positively to procedural pay transparency. Young employees are more likely to desire more information, as they are more interested in their own career and development. Further, younger employees are more likely to search for information online (Classdoor, etc.) and change workplaces. According to the 2022 Visier report cited by SHRM 10 , nearly 90% of Generation Z workers (employees up to age 25) reported that they were comfortable discussing their salaries, compared with 53% of Baby Boomers (those between the ages of 58 and 76). Therefore, our results suggest that, if organizations desire to recruit and retain younger employees, they should be encouraged to promote procedural pay transparency.

It is worth noting that this study does not directly inform about distributive (or outcome) pay transparency, another practice that discloses the actual pay levels of individual employees (vs. the disclosure of how pay levels are determined, that is, procedural pay transparency). This is because, in none of the organizations we studied, this was a common practice. Ignorance might be a blessing for those who are paid less (Perez-Truglia, 2020), and if organizations are not able to provide a coherent message across their HR systems, it may be the case that employees don’t feel that the pay system itself is fair (Alterman et al., 2021). Distributive pay transparency, especially revealing pay levels horizontally between coworkers, may induce counterproductive peer comparisons and cause employers to bargain more aggressively, thus lowering average wages (Cullen, 2023). More information is not always better; thus, carefully considering the type of information provided is essential.

Limitations and Future Directions

We suggest readers evaluate the findings of this research in light of the following limitations. First, the presented findings were derived from a cross-sectional data set. In this regard, although we theoretically suggested a certain causal flow, and our results were supportive of the prediction, the causality of our findings may be questioned because alternate relational sequences are possible. For instance, perhaps procedural pay transparency is more actively adopted in work settings where mastery climate is high. Yet, we cautiously suggest that there is a strong agreement in the existing literature that HR practices, for example, procedural pay transparency, meaningfully shape climates in the workplace (Bowen & Ostroff, 2004; Manroop et al., 2014; Sanders et al., 2014). Similarly, prior research has suggested that employee outcomes are shaped by climates and HR practices (e.g., Nerstad et al., 2018; SimanTov-Nachlieli & Bamberger, 2021; Takeuchi et al., 2009).

Second, we acknowledge the possibility that there may be common method biases in our results (see Podsakoff et al., 2003, for a review of common method biases). For example, given that our study variables were measured using Likert scales, the covariations across procedural pay transparency, motivational climates, and employee outcomes might have been, under systematic influences, driven by common scale formats. Moreover, artifactual covariances may have existed across our predictor and outcome variables, given that they were primarily rated by employees. In light of the above possibilities, we encourage future studies to try replicating our empirical models under research designs that pose fewer concerns for common method biases.

Third, we relied on self-reports in measuring task performance. It is hypothetically possible for self-rated performance to be biased and show differences when compared with other performance measures; a good way to address this issue is to utilize multiple sources in collecting data for task performance (Demerouti et al., 2005). However, we were unable to obtain information regarding employees’ task performance from additional sources, such as via supervisors and company records. Alas, we at least cautiously point out that there is meta-analytic evidence indicating that, when compared with other performance measures, there generally is no upward bias in self-report measures of performance (see Churchill et al., 1985).

Fourth, although we controlled for various factors that may affect the associations across our studied variables, other factors that we could not account for may also influence the relationships. For instance, it may be possible that executive managers’ HR philosophies confound the relationship between procedural pay transparency and employee outcomes. Thus, we encourage future research to try replicating procedural pay transparency’s relationships with motivational climates and employee outcomes while additionally controlling for other important factors.

While our methodology should be critically reviewed in light of these limitations, it also has noticeable strength. Specifically, our sample had an extraordinarily large number of observations collected from numerous work units across a multitude of public and private organizations. In this regard, our research offers findings that are somewhat robust in terms of generalizability.

We hope that our study will spur further research on the impact of pay transparency on work climates, such as the mastery and performance climate studied here. Among other things, future research could study the impact of different degrees of procedural and distributive pay transparency across organizations with different organizational strategic aims, designs, and compensation models. Also, future research could more carefully examine how transition to more procedural and/or distributive pay transparency molds organizational climates and cultures over time, relating to sorting and motivational effects through the recruitment and retention of different kinds of personnel.

Footnotes

Acknowledgements

The authors wish to thank the organizations and individuals who supported the research project, employees who participated in the research, and researchers Elina Moisio, Anu Hakonen, Roosa Kohvakka, Johanna Maaniemi, Hertta Niemi, Jari Alahuhta, Tuomas Liiri, and Matti Vartiainen, who worked on the data collection and participated in the results dissemination to the institutions and companies involved.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the State Research Agency (AEI) - 10.13039/501100011033 (PID2019-108043GA-I00).