Abstract

This article explores the suppositions that financial education programs in Chile have on the financial behavior of low-income women. For this purpose, through a documentary analysis of the National Strategy for Financial Education (ENEF) and a series of interviews with different actors involved in the financial education program, we seek to explain how the intervention considers the role of women in the financial space, exploring the assumptions that guide the methodologies deployed in the intervention. Our results are divided in two: first, we explore the assumptions of the ENEF and the reasons that make women its priority audience; emphasizing the diagnosis, the assigned roles and the expected behavioral changes. Second, we explore the intervention methodology to account for how, through the teaching of savings and planning skills, women are expected to improve their financial skills and those of their household. We discuss how gender roles persist in these intervention spaces and the importance of incorporating feminist perspectives to think about emancipatory interventions.

This article examines the place of women in the National Financial Education Strategy (hereinafter ENEF) developed in Chile, exploring the assumptions and methodologies that this strategy deploys in specific interventions aimed at poor women.

From international institutions, financial education is understood as a tool that seeks to develop skills so that individuals can recognize the opportunities and risks of the financial system (OECD, 2013). This can be understood as something positive, insofar as it serves as a useful tool to reduce potential financial problems, indicating rational action guidelines to act in the market. It is expected that Financial Education programs not only bring individual benefits, but will also contribute to improve overall social welfare by improving the financial skills of the population favors poverty reduction (Beck et al., 2007). This is explained by an assumed positive relationship between the effective use of financial resources and the rise of welfare indicators (Cull et al., 2014). Accordingly, by developing savings, income generation, investment and budget planning skills, the economic autonomy of households would increase, allowing them to opt for a better quality of life (Solo, 2008).

Although research connecting financial education with social work intervention is underdeveloped (Callegari et al., 2019; Despard, et al., 2016; Krumer-Nevo et al., 2017), the evidence collected on financial education processes in Northern countries recognizes some shortcomings in the models of evaluation and intervention with the population's financial problems (Zhan et al., 2006). Several researchers agree that the financial education models that are developed privilege a micro approach, focused on individuals, which emphasize control and behavioral change of individuals privileging, a moralistic perspective in the intervention (Despard, et al., 2016; Krumer-Nevo et al., 2017). For Despard (2016), these intervention models tend to focus on encouraging beneficiaries to develop “good money management” focusing on strategies associated with the reduction of expenses and debts to the detriment of promoting actions that favor the development of new financial assets, while ignoring that the existing money management carried out by service users may be better than the one recognized by the interveners. In the author's opinion, Social Work requires a more comprehensive approach to evaluate and intervene in the financial problems of the population.

However, incorporating broader understandings of financial processes also requires moving towards the development of a gender perspective. Callegari et al. (2019) explore how the relationship between gender and debt has been addressed. Their work provides an account of how the forms and levels of indebtedness, the uses of credit and debt management responsibilities are all conditions permeated by gender-specific patterns. Taken together, gender is addressed as both a relational and structural matter that directly influences household debt. Callegari and co-authors propose that, in order to advance in “gender-conscious” financial education processes, social work interventions for the indebted, social policy and social work practice “need to acknowledge and challenge how individuals ‘do’ gender, and how gender is ‘done’ to them” (Callegari, et al., 2019, p. 10) For this purpose, debates on women's participation in the labor market and access to money, economic decision-making processes and the division of financial tasks in households should be included in social work interventions.

While the field of social work in Latin America has not undertaken to create a research agenda that takes a feminist perspective to assess intervention processes in the financial arena, what is taking place is the beginning of a critique using the feminist register of the financial inclusion projects that are being developed in the region that label women as priority subjects. Pérez-Roa and Troncoso (2019) critique the financial education programs for their promotion of developing standard financial skills that are built atop restrictive notions of economic life that obscure the structural aspects that reproduce gender inequality. Along these same lines, Cavallero et al. (2021) assess the financial inclusion measures that have been under development in Argentina, locating them within a global programmatic push that aims to promote the inclusion of the unbanked sectors into financial markets primarily in countries in the global south. These are mainly targeted toward working-class women. According to the authors, such policies not only fail to recognize the precarious status of these households, they also characterize impoverished groups as if they were “financially illiterate” in a way that ignores the economic knowhow that has provided an economic underpinning to these households for decades. The authors suggest a financial feminist pedagogy that incorporates the knowledge that arises through feminist debates and encourage reflection about how we get into debt, the kinds of financial instruments we use, and how these contribute to social reproduction in impoverished situations.

Furthering this line of analysis, the objective of this article is to examine how ENEF, through the social programs that stem from it, “make” gender in social intervention. That is, to explore the ways in which the financial education approach develops interventions aimed at low-income women in the financial sphere. In this sense, we seek to explore the expectations that programs and interveners have about the role of women and their financial behavior by identifying how the role of women in the financial space is conceived of in the intervention, and how these assumptions guide the methodologies and techniques deployed. To this end, the results are presented on two analytical levels: first, the assumptions of the ENEF that make women its priority audience are explored, emphasizing the diagnosis, the roles assigned and the expected behavioral changes. Second, we will analyze the intervention methodology to account for how, through the teaching of savings and planning skills, women are expected to improve their financial skills and those of their household.

To meet this objective, this paper is structured in five sections: first, we briefly present of the Chilean political and economic context and the Financial Education strategy, its objectives and the way in which the strategy is implemented in the financial education project executed by FOSIS (Solidarity and Social Investment Fund); second, we present the theoretical framework that guides our work; then, we present the methodology and the analysis strategy; subsequently, we report the results, and conclude with discussion of how our findings can be used to advance a feminist analysis of financial intervention programs in Chile.

The “Democratization of Consumption": Extension of the Credit Market in Contemporary Chile.

The principal reforms implemented in Chile by the military dictatorship transformed the economic model and the regulatory ground rules of labor relations. Producers of goods and services, including social welfare services, were privatized, enabling access to their financial yields in the marketplace. A large portion of economic activities were deregulated and liberalized, simultaneously increasing access to the credit market. In terms of productive labor, a new plan was implemented that made the job market more flexible and set up a labor relations framework based on individualization, commodification and de-collectivization (Stecher & Sisto, 2020). This set of transformations has centered consumer interaction at the heart of the social relations structure (Moulian, 1997), in turn directly impacting the economic life of Chilean households by encouraging the notion that upward social mobility can be gained through the act of consumption.

Such a change was made possible by extending the credit market to reach a broad segment of the population that had been historically excluded from this process. This operation to “democratize consumption” was positioned in Chile during two stages (Marambio-Tapia, 2017, p. 1)

Thus, the expansion of consumption and the correlated increase in the debt levels of the Chilean population share a common backdrop in the State, within a socioeconomic model that provides neither social stability nor income that ensures a minimum level of economic well-being (Marambio-Tapia, 2021). In Chile, many families use credit as a wage extension mechanism to access the basic goods and services that are key to ensuring their well-being (Pérez-Roa, 2020).

The Financial Inclusion of Women and the Financial Education Strategy (ENEF)

Chilean women's financial behavior has been closely monitored by the Commission for the Financial Market (CMF), which has been producing a report on gender in the financial system for over a decade. This report aims to collect financial information in order to design public policies around gender, discussing the differences between men and women regarding access to credit and savings products. The results from the last report show that, in Chile, a reduction in the gender gap with respect to accessing and using financial services has been achieved. In terms of financial behavior, the report points out that women systematically display better conduct than do men 1 .

Despite a 22.4% increase in women's access to credit, this access is mostly due to acquiring non-bank or store credit cards called retail cards. Women make up 64% of the total debtors with this kind of financial product. These financial products are characterized by having worse repayment conditions. A recent study describes the unequal conditions that this type of debt creates for the poorest Chilean households whose access to credit is more expensive. They principally use credit to acquire the basic goods of social reproduction (food, health, clothing,) and earmark a greater percentage of income to pay such financial commitments (see: Gómez and Pérez-Roa, 2020).

However, despite accessing credit with worse repayment conditions, women have stood out for their responsible financial conduct. Women for the most part pay off the entirety or more of their invoiced credit card debt in comparison with men (45% and 41% respectively). Women also have lower unpaid credit card debt rates compared to men (31% and 38% respectively). The figures seem to confirm the popular notion that women are “good payers”. Despite their “good” behavior, the market continues entrusting higher sums and granting better credit conditions to men (Comisión para el Mercado financier, 2020).

Income differences and the challenge of getting paid work are key elements that explain the gender gap in the financial system. In point of fact, the 2018 Supplemental Income Survey estimates that women receive 27.2% less income (CLP 117,486 per month) than men. The fact that women manage smaller amounts of money than men means that they would have a “low support rate”, and as a result, more limited access to financial products, worse credit conditions, and a greater likelihood of being in debt (CMF, 2019).

Although salary differences are objective conditions that hinder women's access to financial systems, international evidence has stressed the importance of considering gender biases in financial socialization processes to better understand such access gaps (Agnew et al., 2018; Fonseca et al., 2012). Such biases often begin at an early age (Rudeloff et al., 2019) and tend to link women to the practice of savings while excluding them from economic discussions (Yu et al., 2015). This is in contrast to the way in which men are taught from a young age to trust in their economic abilities and are actively included in financial discussions (Al-Bahrani et al., 2020; Bannier & Schwarz, 2018; Cueva et al., 2019; Lind et al., 2020). There is substantial evidence in this regard that shows how the processes of financial literacy are differentiated by gender (Fonseca et al., 2012; Lulup Tripalupi et al., 2020).

The National Strategy for Financial Education (ENEF) set up in Chile acknowledges these economic disadvantages of women, having defined them as a priority target group. This decision is based on the fact that “Women have to deal with less financial inclusion than men due to limited access to employment, entrepreneurship, and formal financial markets, as well as differences in social norms, and their legal and cultural treatment compared to men,” (ENEF, 2017, p.10). The objective is to improve women's financial skills insofar as they are responsible for the economic well-being of their families. The goal is to instill 23 skills in women through an educational strategy that addresses topics of consumption, savings, budgeting, investment, debt and economic citizenship. The strategy is directed toward women beneficiaries of social and productive development programs.

The ENEF policy originated in 2018 as a result of the coordinated efforts of public, private and third-party institutions that all shared the same concern; i.e. an increase in debt problems and the difficulties inherent to using credit products. The strategy acknowledges that despite high indices of banking 2 , the population does not have the skills or awareness needed to make effective use of financial instruments (FOSIS 2017; MINEDUC, 2018). It suggests the idea that the country needs to make progress on financial inclusion through a two-pronged approach. The first one is to ensure that individuals can access financial services (Banco Central, 2014). The second is to ensure that people make “good use” of credit (Banco Central, 2014).

The ENEF is made material through a series of public and private programs. One example of the public programs is the Financial Education Program of FOSIS (Solidarity and Social Investment Fund). The focus here is on incorporating financial literacy content into educational plans. The program is intended to educate participants and families with respect to using money and encourages savings and investment to prevent over-indebtedness. It is geared toward people ages 18 or over who are part of the 60% most vulnerable population segment according to the Social Household Registry 3 (RSH in Spanish). Some of the methodologies and activities used by the implementers include workshops and guidance for families and entrepreneurs that take both a theoretical and applied approach to the program content. Despite the program being aimed at both men and women, the latter are the main users, comprising 92% of participants (Fuentes, 2016). This percentage may be due to the fact that the FOSIS happens to be primarily focused on women, not that the women are in fact more interested in the programs.

Beyond “Market Imperfections": Toward a Critical Feminist Reading of Financial Education Programs

The feminist critique in the financial realm is articulated by repudiating the androcentric bias that attributes characteristics to homo economicus that are viewed as universally applicable to human beings, although they pertain to a more specific version, which is “male, white, adult, heterosexual, healthy and of average income” (Rodriguez Enriquez, 2015). This analysis aims to critically describe the political-cultural assumptions that organize economic activity and have relegated women to a subordinate position (Orozco, 2004). The feminist critique specifically questions the role assigned to women in the domestic sphere. Said role is focused on the economic activities of family care and well-being, stresses their reproductive capacities, and sees them as dependents of the men in the family.

After the global financial crisis of 2008, the feminist critique began to turn its interest toward finance and the analysis of narratives that were built to help explain that global crisis. Hozic and True (2016) in their book Scandalous Economics: Gender and the Politics of Financial Crises present a collection of works that analyze the crisis from its gender dimensions and addresses the structural roots of inequality, exclusion and oppression in financial structures. Hozic and True critique the features of the economy that affect well-being, but tend to get ignored by macro-economic analyses. They also question the individualizing, punitive narrative that promotes the idea that the crisis was the result of a series of contagious occurrences exogenous to the capitalist system and that must be addressed via the punitive containment of the perpetrators (homeowners who fail to repay mortgages, greedy public employees accustomed to undue benefits, corrupt traders, and banks that unduly increased their credit capacity) (see: Brassett & Rethel, 2015; Cameron et al., 2011; and Hozic & True, 2016).

Policy analyst Adrianne Roberts (2015, 2016) identifies three narratives told by international institutions (such as the IMF, World Bank, United Nations, OECD, and others) that encourage interventions in financial markets to favor women. The first narrative refers to the concept of “woman as savior”, claiming that increased integration of women into financial markets will help to alleviate poverty and stimulate national economies, especially those in the Global South. The second tale considers “technocratic equality” that purports that new financial technologies have helped eliminate gender-based discrimination by standardizing risk assessment models. The third one is that of “womeconomics” pushing the advantages or “dividends of gender” that can be obtained by promoting women to fill more senior positions in financial Institutions. In Roberts’ opinion, these three narratives create a “commercial argument” in favor of gender that wishes to increase women's participation in the financial markets and improve their capacity to consume goods and services. Such narratives understand gender inequality as a market imperfection and not as a structure shaped by relationships of power and production or the social reproduction of financial markets (Cavallero & Gago, 2019; Fraser, 2016; Roberts, 2016).

In this sense, our work is in line with exploring the links between social reproduction and finance. Understanding the concept of social reproduction refers to the processes involved in maintaining and reproducing people, specifically the laboring population, and their labor power on a daily and generational basis (Bezanson & Luxton, 2006; Laslett & Brenner, 1989) we consider that this process is now structurally linked to the monetary economy, not only through the payment of wages, but also through credit, debt and financial assets (Roberts & Zulfiqar, 2019). In this line of analysis, the work of Melanie Long (2018) on the growth of household debt in the period of the subprime crisis shows how in households headed by female heads of household, mortgage, consumer, and educational debt grew without being accompanied by a sustained growth in income. In a Latin American context, recent works by Cavallero et al. (2021) show how the Covid-19 pandemic that began in 2020 has provoked in popular households an “indebted immobility”, that is, a domestic production where debt becomes an instrument to manage short-term precariousness tying them to payment conditions that end up exploiting women's bodies even more. In this sense, Predmore (2020) warns of the exploitative effects of the financialization of the spaces of social reproduction on women's bodies.

Through a feminist lens, addressing financial education by focusing on the need to improve women's financial skills is problematic because it fails to consider the structural aspects that lead to gender inequality. Accordingly, this could be a way to individualize and depoliticize the social problem of gender inequality that arises when assuming that the issue that needs correcting is a “lack of skills” as well as the ways these women handle their money that is seen as insufficiently effective (Pérez-Roa & Troncoso, 2019). Rather, the problem should be situated within a context of the heterosexist market logics and dynamics that reproduce a traditional and stereotypically gendered order. More specifically, it is a sexist and sex-based division of labor that functions by justifying and reproducing the very gender inequality theoretically being addressed. Such an approach would consider assumptions that represent men as more reliable, rational providers in charge of the productive work while women are held responsible for a lack of financial skills, simultaneously assuming that their labor by definition is linked to reproduction, and their care and devotion to the family.

Methodology

This investigation aimed to explore the place of women in the National Strategy for Financial Education (ENEF). We were specifically interested in exploring the discourse and expectations that justify focusing these activities on women and assuming that, from the intervention perspective, women must take care of household finances. The study was done between March and December of 2020 and conducted under the framework of the Socioeconomic Relations and Social Struggles Center at the Department of Social Work of the Universidad de Chile 4 . The research received funding support from the Fondo de Fomento de la Investigación (FPCRI or Research Promotion Fund 2019) of the Faculty of Social Sciences at the Universidad de Chile.

The research strategy used for this purpose was qualitative and consisted of the analysis of a set of official documents and press releases related to ENEF. In addition, in order to corroborate and stress the preliminary results obtained from this first analysis, a series of 4 qualitative interviews were conducted with experts and implementers involved in the implementation of ENEF, specifically in the Financial Education for Families program, which is run by FOSIS.

We kept our research in line with feminist inquiry for three main reasons: 1) it underscores the relevance of the personal knowledge of those who intervene in the financial education space by recognizing their “expert testimonies” (Cole, 2008) that produce knowledge and situated reflections; 2) it seeks to problematize the hegemonic versions that place women in a subordinate position in relation to men in terms of finance management; 3) it aims to problematize the intervention space in the financial arena in order to transform practices that can increase oppressive situations for women. In keeping with Gringeri et al. (2010), we took a feminist perspective insofar as we aimed to assess how the ENEF constructs gender to gain a better understanding of how oppression and privilege interact in the financial system.

Sample

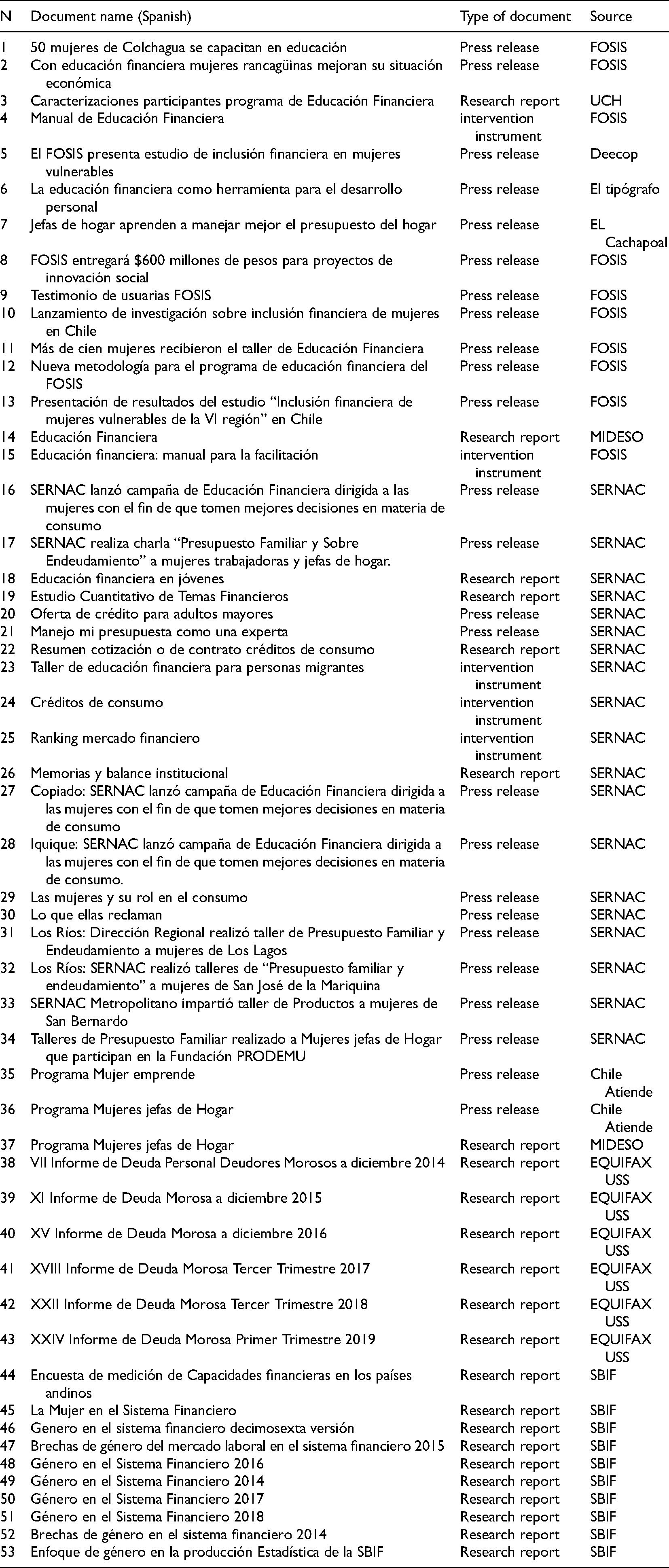

While working with documents is considered to be supplementary to other information gathering techniques (Atkinson & Coffey, 2004), the ease of access to such information means this method can facilitate an understanding of given social phenomena (Valles, 1999). Based on this premise, the documentary review was done using online sources in the early months of 2019. Two criteria were used to select the documents: The presence of assumptions regarding the financial behavior of poor women; and explicit reference to the methodologies that are preferentially applied in interventions aimed at women.

A total of 53 documents were reviewed to conduct the analysis. Of these 53, 37 were public reports available on the web pages of the Ministries connected to the ENEF implementation (FOSIS, Mujer Emprende or Women Entrepreneurs and SERNAC). Six were national debt reports and 10 were gender reports on the financial system. Texts were selected for two reasons: 1) they make direct reference to any of the financial education programs that will be included in the ENEF; 2) the texts provide data on the financial inclusion of women.

(Table 1)

Document Review.

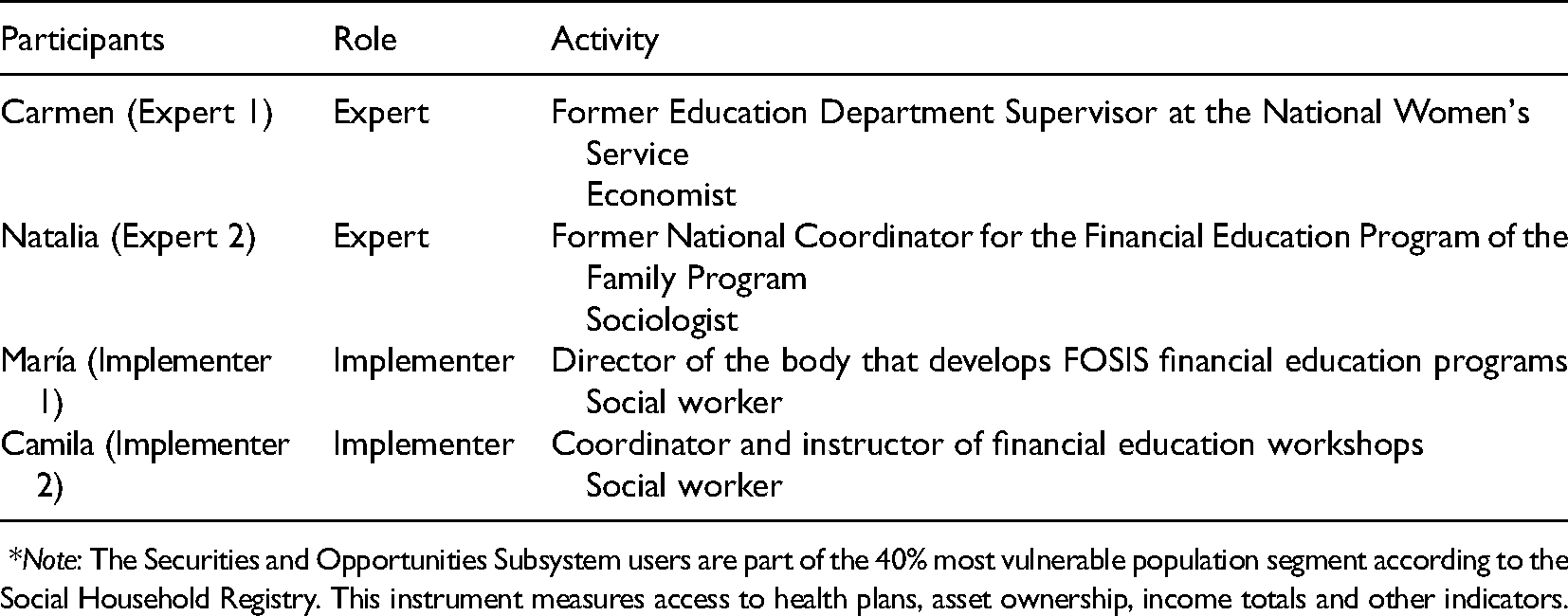

Four interviews with people linked to the implementation of the ENEF were held to discuss assumptions about the relationship between women and finances revealed during document analysis. The participants were chosen using an intentional or purposeful sample (Otzen & Manterola, 2017), prioritizing the cases that could give more detailed and deep information about the research topic (Martínez-Salgado, 2012). The first female interviewees were selected through their previous contact with the lead researcher who had worked with some of them before. Next the “snowball” method was used (Martínez-Salgado, 2012) to contact the other interviewees. Bear in mind that while the research originally planned to interview program users, technological limitations imposed by the covid-19 pandemic and the socio-health concerns affecting users caused us to dispense with that plan (Table 2).

Characterization of the Interviewees.

*Note: The Securities and Opportunities Subsystem users are part of the 40% most vulnerable population segment according to the Social Household Registry. This instrument measures access to health plans, asset ownership, income totals and other indicators.

Information Production Techniques

After contacting the professionals, the interviews were conducted using a semi-structured interview style. This means information is exchanged between the researcher and respondents using a question guide that can be adapted by adding new questions as a function of the reflexive paths taken by the subjects in their responses (Díaz-Bravo et al., 2013). The general topic guideline included characterizing the women program users, representations of their financial behavior; the intervention's objectives, methodologies used, and observed results. In our work we see the interview process as a collective learning space that lets participants problematize the intervention (Monetta, 2016). We sought to include a space for reflection within the process that would allow the interviewees to deconstruct the roles assigned to low-income women in such intervention arenas. All of the interviews were done online using the videoconference application Zoom with a standard duration of one to one and a half hours. Each of these conversations was audio recorded and stored on the research team's computers. Interview transcription was delegated to one of the members of the Center where the research was done.

Prior the interviews, study objectives were explained to each respondent and their consent was recorded, having been obtained using ethical safeguards that included asking for consent and maintaining confidentiality. Participants’ real names were changed during interview transcription in keeping with the ethics committee standards of the Faculty of Social Sciences at the Universidad de Chile.

Analysis

The thematic analysis technique (Paillé & Mucchielli, 2008) was employed for analyzing the resulting information. The first step was identifying and classifying the elements that came up in the data (Guest et al., 2011). This stage was directed by two researchers on the team who built an analysis matrix using the Microsoft Excel program. Next the first matrix of codes was collectively reviewed in light of the theoretical positioning that gave rise to this research (Gingeri et al., 2010). Analysis sessions were conducted every two weeks for six months for this purpose. Once the first matrix of thematic codes had been discussed, we proceeded to create matrices of thematic families (savings, beneficiaries, financial education, use of income, money management, generational differences and intervention methodologies) in which these constructed codes were grouped in accordance with their similarities and differences (Ryan & Bernard, 2003). This process was done collaboratively, just like the earlier ones.

The results of this analytical process were organized in light of the objectives of this research and the theoretical framework that guides it, which draws on the feminist critique of finance - coming mainly from political economics - and the Latin American feminist economy. The results of this strategy are organized around two central axes: 1) assumptions about the relationship between women and finance uncovered in the financial education strategy; and 2) the methodologies used during the intervention. These results account for the documentary analysis that was done and the way in which the interviewees reference the financial education program.

Findings

The Place of Women in the Financial Education Strategy

In the analysis of secondary documents, women are defined as one of ENEF's target audiences. Women are considered to be a financially vulnerable group since their access to employment, entrepreneurship and formal financial markets is limited (OECD, 2013). It is also suspected that banks treat women differently due to cultural biases (MINEDUC, 2018). Including women financially is understood as a strategy to improve economic opportunities, autonomy and well-being (Hendriks, 2019).

Although the FOSIS financial education program does not state that women are its target population, recent studies have shown that those who make the most use of this program are mostly women. In 2016, 92% of program participants were women with an average age of 40 who were not contributors to the pension system (Fuentes, 2016). Reviewed institutional documents (FOSIS, 2017) show that the program explicitly favors women's participation and views them as key actors when it comes to domestic finances. The program assumes that economic decisions made by women have an impact on the everyday financial status of households, especially concerning the economic education of their children (FOSIS, 2013).

Our interviews confirm this notion across the board: educating women on their finances is a way to indirectly educate their entire households. Expert 1 understands this idea as follows: “A mother that is well-educated financially has a greater likelihood of passing those behavioral patterns or healthier financial decision-making on to her children (…) Women transmit certain values and knowledge to their kids”.

Beyond the strategic relevance, the interviewees believe that high female participation in these programs can be explained by the fact that women tend to have more available time. Women may have more free time to participate in these programs because they do not perform salaried work, thus they do not spend any part of their time traveling between the home and workplace. Despite the fact that the interviewees recognized that women are mainly responsible for everyday household tasks that take up a lot of time, they assume that because they are “at home” they have more time available than men do to participate in such initiatives. 5

The low participation of the women beneficiaries in the formal job market would also explain the low level of financial awareness that the women program users have. The men are “a lot more organized with their bills. It's not very common for them to have a lot of debt,” said implementer 2 in her interview. The cultural attribute assigned to men of worker-provider associates them with virtues linked to financial planning and organization, whereas the women are in charge of domestic finances who, as expert 2 said, “need to be taught how to save, plan and better manage their expenses” since they “par excellence” are in charge of managing the household.

Meanwhile, the credit market has accepted this role of good household money administrator as it has systematically increased its offer aimed at low-income women. At least that is how implementer 1 perceives it,

Despite the fact that they were not the ones working or earning a salary, they were inundated with credit cards (…) all of the small department stores and local businesses overwhelm homemakers with these cards. This happens as they begin to realize that women manage the household money, meaning they know where and how it gets spent. Also, they are really good at paying back debt, so it’s a sweet deal for the department stores.

Essentially, according to statements made by implementer 1, interveners recognize the financial education program beneficiaries as “female home-makers who are vulnerable and over-indebted in very complex financial situations.” They believe easy access to retail cards and a lack of financial education are the primary reasons that can explain why the majority of the beneficiaries are dealing with complicated financial situations. Implementer 1 interprets it like this: “These women are very vulnerable and one step away from facing financial prosecution… These issues come for us up repeatedly. They have to permanently change their phone numbers and when we ask them why, they say it’s the only way to avoid store collections departments.”

Thus, the interveners recognize a “financial illiteracy” that prevents the women participants from differentiating between “bad debt” and “responsible debt”. This is why the program aims to educate women to understand the difference between wants and needs. They try to teach the women to put a halt to their spending impulses inspired by consumer desires.

Learning Finance from and for the Home: Recording, Planning and Saving

Educating on finance meant dual tasks for the interveners. First, they had to understand finances themselves so they could then teach others about the subject. This process required them to “untangle the cryptic language of finance” and understand that, despite what they used to think, finances are in fact a part of everyday life. As expert 1 says, “We make financial decisions every day.”

This led the interveners to realize that the first step was to understand that finance is a topic that not only pertains to economists, but can also be taught by social workers. In our interviews the professionals point out that broadening their concept of financial practices and understanding them as part of daily life was key to creating methodologies that would be “more attractive and relatable to people”.

In order to do this, the program has developed a work methodology based on a table game called “You Decide”. The game puts the users in an array of everyday scenarios and asks them to reflect on the economic choices they would make and the resources they would use to carry them out. This enables the users to apply their financial knowledge by identifying with the situations proposed by the game board. In the estimation of the implementers, this game has two strong points. First, it connects the women to financial topics and eliminates the idea that finances “are matters for experts”. Second, it opens up a conversation among the users so they can share their financial experiences. 6

The implementers believe that one of the biggest financial problems affecting users is the difficulty they have in recognizing their expenses. Implementer 1 describes it this way: “They claim to be organized with their money, but don't acknowledge the importance of the money they spend when they go to the store and buy sweets for their children, for example.” Such “small expenses” are what they address through the intervention, teaching the women to record, plan and save.

They do this by teaching the women to record their household income and expenses in a notebook specially designed for this purpose. They hope the program users will be able to “understand where their money evaporates.” This exercise encourages the users to be aware of their consumption patterns and think about “superfluous” spending motivated by wants rather than needs. The record is thought of as a family activity with the goal of raising awareness, especially that of children, about problems with “expenditure control”.

The record book tool helps the users work with the notion of savings and expense planning. Learning how to save is one of the fundamental aims of the intervention. Savings is understood as a practice that helps establish “family financial goals” and contemplate “making changes to the family's economic functioning”. As implementer 1 states, savings motivates families to change certain consumption habits: “For example, we tell the users to ‘go one month without buying soft drinks’ and save that money. They then start realizing how much they can save by making small behavioral changes.” Rather than focusing on the money saved, the intervention tries to help users and their families adopt an economic behavioral style that regulates expenses and is oriented toward saving.

These savings strategies not only consider reserving funds, but they are also understood as adjusting economic practices in order to reduce everyday consumption costs. As interpreted by the implementer 2: “Savings is not only storing up money, but it also includes things like when boiling water, storing it in a thermos to keep it hot so you don't have to boil it again.” By decreasing the use of domestic resources, families can start saving and simultaneously lightening the pressure on the family budget.

Discussion and Implications

This study aimed to explore the assumptions made in financial education programs about the role of women and their financial behavior. For this purpose, we conducted a document analysis of the ENEF and held a series of interviews with various actors of the direct intervention of FOSIS financial education programs. We looked at how the intervention views the role of poor women in the financial arena, exploring the way in which these assumptions orient the methodologies and techniques employed in the intervention.

As concerns the assumptions made about women's roles in the domestic economy, the results suggest they continue to reproduce the same gender biases both in terms of the role assigned to women as well as the economic behaviors that women are expected to adopt. While the ENEF acknowledges that women have worse financial inclusion conditions than men, the interventions continue reproducing the very same gender biases that, paradoxically, would explain such divisions and then continue to support a sexual division of labor.

In our analysis we uncovered three gender biases that are manifest in the specific intervention methodologies: 1) the relationship between women and finance is limited to only household administration and the economic education of their children; 2) a lack of awareness about the financial skills that women develop in the course of reproductive work; 3) moralizing about financial behaviors.

Regarding point number one, both the ENEF and the interviewees assume that the financial behavior of the women is directly connected to household administration tasks in two ways. One assumption is that the majority of women's activities of consumption, savings and planning are aimed at household management. The other is that a woman's financial education influences the economic behavior of her children. While the evidence concerning women's financial practices agrees that they earmark a large percentage of their income to family subsistence (Guérin, 2008; Han, 2012; Villarreal, 2009) this role is subject to structural conditions that are not necessarily related to individual responsibility. This means that the program's emphasis on spending reduction and savings behaviors tends to overlook the budgetary limitations of low-income women. In concordance with some of the work from economic social studies (Zelizer, 2011) and studies on couples’ money management (Belleau, 2017; Pérez-Roa & Troncoso, 2019), we sustain that savings is essentially a recurrent practice of women in light of the historic challenges that they have faced trying to access money. Some of the other factors that help explain women's savings patterns include the fact that women obtain money from other people (Belleau, 2017), frequently work in the informal market (Villarreal, 2009), transfer economic resources throughout support networks (Pérez-Roa, 2018), and are affected by wage gaps that persist in the salaried labor market.

Additionally, the financial problems of the users are due to the deregulated system that offers high-cost consumer loans to women who have no fixed income (Gago and Cavallero, 2019; Pérez-Roa and Gómez, 2019). This asymmetry in the creditor-debtor relationship is recognized both in the ENEF documents and by the accounts of implementers who explicitly acknowledge the abuses of the credit system and the “financial vulnerability” of users. However, this appraisal does not materialize as concrete intervention activities that bring about any critical action vis-à-vis the credit market. The intervention assumes that the women can understand the financial products if they understand the correct financial information. Such an assumption fails to consider the challenges inherent to digesting complex and deregulated information, which is the case of the retail credit market in Chile. It constructs a business model based on “seeding” new consumers (Ossandón, 2014) and indebting them with small sums without considering their repayment capacities in terms of income (Gago and Roig, 2019).

In this line, we have observed a discrepancy between the ENEF's assumptions and what the implementers have to say regarding the goals that the financial education aims to meet. While the ENEF emphasizes the development of financial skills the women must learn in order to perform well financially, the implementers emphasize the relevance of turning finance into a “conversation”, thus changing it into a collective learning experience and stripping it of its status as a tool. The interveners understand that finances are implicit to multiple aspects of daily life and that the financial practices the women develop are part of a cumulative set of knowledge that should be put at the center of the intervention. The implementers recognize that the users value the opportunity for conversation that arises among peers more than they do learning specific financial techniques. All the interviewees share the opinion that the dynamics generated by the game in which users make financial decisions and discuss them with peers is the best methodology “for turning finances into an everyday thing” and achieving effective learning.

Second, when we refer to the invisibility of the financial skills women develop in the field of reproductive work, we mean that both for the ENEF and the interveners, the official spaces for learning about finances are viewed as limited to the formal productive work arena. Planning, saving and “appropriate” consumer behaviors are those learned by following schedules, receiving a formal salary, and working outside of the domestic sphere. Thus, when our interviewees state that because the users are not engaged in productive work, they have more time to participate in the intervention and less financial understanding than men, they are assuming that finance is fundamentally a space for male expertise. Such a reading assumes an androcentric view of the economy that relegates the role of women to a subordinate level (Federici, 2014; Orozco, 2004; Roberts, 2015).

Viewed from the methodology that the program employs, a tension becomes clear between what the users “should learn” and the learning outcomes the program recognizes as valid. The program assumes that they need to learn about finance, while simultaneously recognizing that financial practices already make up part of the users’ daily lives. The program intends for the users to learn “proper finance” or “healthy finances”, which pertain to the masculine or rational register.

Lastly, as concerns the moralization of women's financial behavior, two points should be highlighted. First, it is important to understand that finances are structurally linked to the methods of social reproduction in lower-income households in Chile. Recent work by Gómez and Pérez-Roa (2020) shows how in the last ten years the household consumer debt of lower-income Chileans has grown, and such debt is primarily used to purchase items of everyday reproduction (food, health, clothing) and not for conspicuous consumption as people often think. Second, the program should work toward recognizing and denouncing the place of women in the financial system. Vulnerable women are viewed as “an untapped resource” (Roberts, 2015) that must use financial resources to offset the immediate costs of social reproduction and commit their future work capacity to ensuring repayment (Federici, 2018). Thus, we are referring to the ways in which the financial system can causes the exploitation of women without formal incomes, yet still prioritizes their access to the system.

When the ENEF and its programs create the objective of educating the users to learn how to distinguish between “wants” and “needs” so as to prevent “bad debts”, they place the responsibility for financial decisions on the women while failing to acknowledge that: 1) vulnerable women do not have access to the best credit options, only the most expensive ones with the highest risk; 2) debts fill a strategic financial security and protection role in households, given the lack of state protections; and 3) women have learned about finance in their everyday living, and these skills are what enable them to support their domestic economies under highly precarious conditions. We believe it is important to think about interventions in such a way as to “take debt out of the closet”, to borrow a phrase from Cavallero and Gago (2019), by seeing that debt makes up part of the financial tools that women have and stop the moralization of their financial behaviors.

Although the ENEF strategy aims to financially include women to improve their economic opportunities, autonomy and well-being, the intervention reinforces some distinctions between the feminine and the masculine in the financial sphere, which hinder a more complex approach to women's economic reality. In this sense, and in line with the work of Callegari et al. (2019) in order to advance in “gender-conscious” financial education processes, debates on women's participation in the labor market and access to money, economic decision-making processes and the division of financial tasks in households should be included. In this sense, more than integrating women into the global financial system, we need processes that favor reflection on how we get into debt, what type of financial instruments we use, and how these contribute to social reproduction in contexts of dispossession (Cavallero et al., 2020).

Footnotes

Acknowledgments

Financial support for this research was provided by the Concurso para el fortlaecimiento de productividad y continuidad en investigación (FPCI) Facultad de Ciencias Sociales, Universidad de Chile. The authors are grateful to Iniciativa Científica Milenio del Ministerio de Economía, Fomento y Turismo de Chile adjudicado al Centro Núcleo Milenio Autoridad y Asimetrías de Poder Code NCS17_ 007.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.