Abstract

This is a visual representation of the abstract.

Introduction

Resident physicians throughout Canada face the burden of financing their costly education, often using loans to afford the medical school they attend. The Association of Faculties of Medicine of Canada has determined that the median debt of a medical school graduate directly related to their studies is $90 000. 1 This burden of debt has been shown to impact the lives of medical trainees, with the majority of residents indicating that their personal finances are a contributor to their overall well-being and rates of burnout. 2 In addition, high levels of debt may have other effects such as influencing decisions on future practice within the resident’s specialty.3-5 These implications render financial literacy an important consideration for medical trainees.

Previous Canadian surveys have indicated that residents and practicing physicians each only score slightly better than 50% on a financial literacy quiz. 6 Multiple studies have demonstrated that residents from various specialties do not feel well prepared to manage their finances, especially given their high debt loads.7-10 As well, from an educator’s perspective, Lusco et al demonstrated that 92% of surgery program directors believed that residents were inadequately prepared to handle practice management and personal finances. 11 One study by Teichman et al, demonstrated that residents spend more than age- and income-matched members of the general public, raising more concern regarding their understanding of financial literacy. 12 The combination of lacking financial literacy and spending more, renders medical trainees in a worrisome position with regards to finances.

Despite the high financial burden of medical training, financial literacy is variably addressed in residency education.13-15 In a study by McKillip et al, 16 a significant portion of current medical residents had reported that they had not received any financial education throughout their medical education, which is of particular concern. Another systematic review by Gianakos et al 17 demonstrated that incorporation of formal financial education in residency programs in USA ranged from 0% to 36.7%. The study also demonstrated that most residents obtain financial education through their own research, a family member or attending outside financial seminars. It does not help that the “taboo” nature of discussing finances is promoted by the overall culture of medical education. 18 There is perhaps a conflict between the concept of personal gain through financial literacy with the altruistic aspect of becoming a physician. 14 This lack of financial knowledge renders medical trainees often stressed when it comes to financial decisions. 6

From previous studies, there is an indication that both residents and practicing physicians desire more financial education either in residency or in medical school.16,19,20 There have been several studies that examined various financial literacy curricula, particularly in the last 5 years.17,21 However, in the systematic review by Wesslund et al, 21 only 4 out of 13 included studies specifically examined trainee needs with respect to financial topics prior to curriculum development. Ultimately, in order to meet the financial literacy gaps in the current curriculum, it is paramount to perform a targeted needs assessment prior to curriculum development not only to identify the learning gap, but also guides the best way to address it.22-24 In the case of financial literacy, assessing the current financial knowledge of Canadian residents is crucial to identifying gaps in their understanding of specific financial services or concepts. This will help to serve a knowledge baseline and curate an appropriate level of complexity. In addition, identifying their current financial status such as their debt level would allow for assessing the need for teaching concepts such as debt management. This foundational understanding is particularly important when it comes to the Canadian financial landscape, as the majority of studies in this field have been done in the United States.17,21

The primary objective of this observational study was to conduct a nationwide needs assessment of Canadian radiology residents with regards to their finances. The study incorporated 2 components: an in-depth national survey assessing demographics and current financial status, as well as a financial literacy quiz. Ultimately, the financial learning gap found in this study would provide information that can be used by education stakeholders to design and implement financial literacy interventions that can address areas of need.

Methods

Local research ethics board approval was obtained for this study (REB Project Number 13541).

Population

Participation was entirely voluntary, and all responses were recorded anonymously. The survey was disseminated via an email with a link to the online survey sent to all Canadian radiology residents by program administrators and program directors of each radiology residency program across Canada. Approval was obtained from each residency program to distribute the survey to all residents. Responses were collected from December 17, 2022 to March 24, 2023.

Survey Structure

The survey (Supplemental Material 1) consisted of 41 questions, divided in 4 general sections: (1) Demographics/background, (2) Current financial status/financial inclination, (3) Quiz (Financial knowledge assessment), and (4) Moving forward. After obtaining demographics data, the second part of the survey focused on assessing the current participants’ personal financial status, including current debt levels, satisfaction with their financial condition, as well as current and future financial management and planning. The financial quiz portion was an itemized assessment on personal finance derived from Statistics Canada. 25 The “moving forward” component of the survey assessed what financial educational activities are currently being implemented at the participants’ universities, if any, and what changes they would like to see in the future. Questions that required grading, such as interest in dedicated/formal financial literacy training during residency, used a 4-point Likert scale [1 = lowest, 2 = mildly low, 3 = mildly high, 4 = highest]. All survey questions were reviewed for accuracy and clarity by a physician financial expert (AA), as well as a research and education expert (SM) before distribution. The survey was conducted through the Google Forms platform. 26

Study Design

The survey was initially piloted with a group of resident physicians at a Canadian university (not exclusive to radiology or training level) to seek feedback on the survey design and wording. A cognitive analysis was completed with a junior trainee to ensure the survey is interpreted as intended. Three follow-up reminders were sent, and the completion of the survey was incentivized with a chance to win 1 of 6 gift cards.

Statistical Analysis

Descriptive analysis was conducted for all survey responses and participant demographics. Pearson’s correlation coefficient was calculated for continuous variables for total knowledge scores versus postgraduate year of training, debt level, and previous financial knowledge. Data analysis was conducted using Microsoft Excel Version 16.70 (Microsoft Corporation, King County WA).

Results

Participants

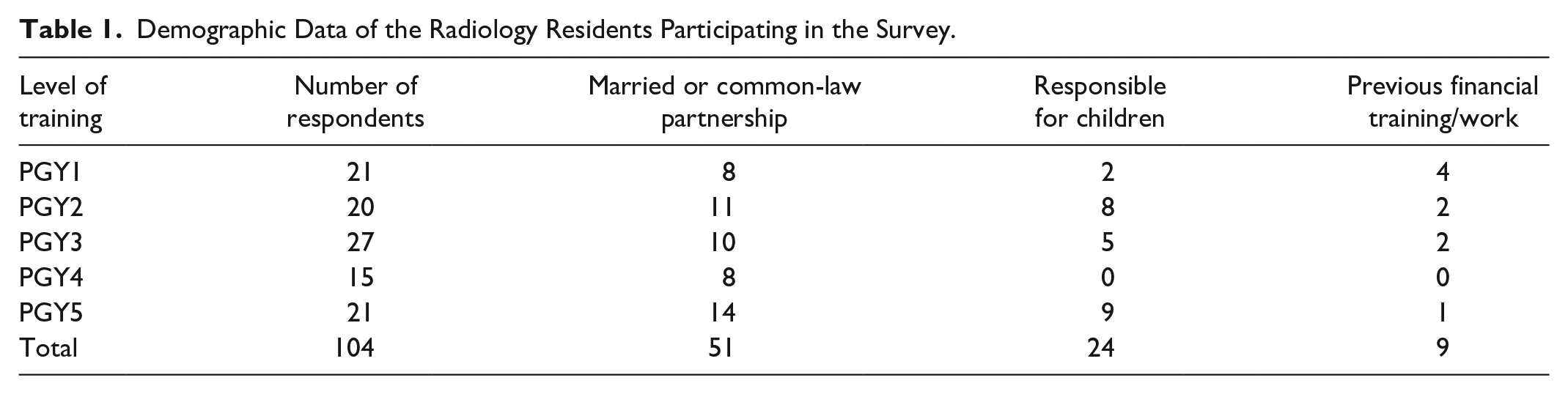

A total of 104 radiology residents, across 16 Canadian post-graduate institutions, completed the survey. Common demographic characteristics are summarized in Table 1.

Demographic Data of the Radiology Residents Participating in the Survey.

Current Financial Status/Financial Inclination

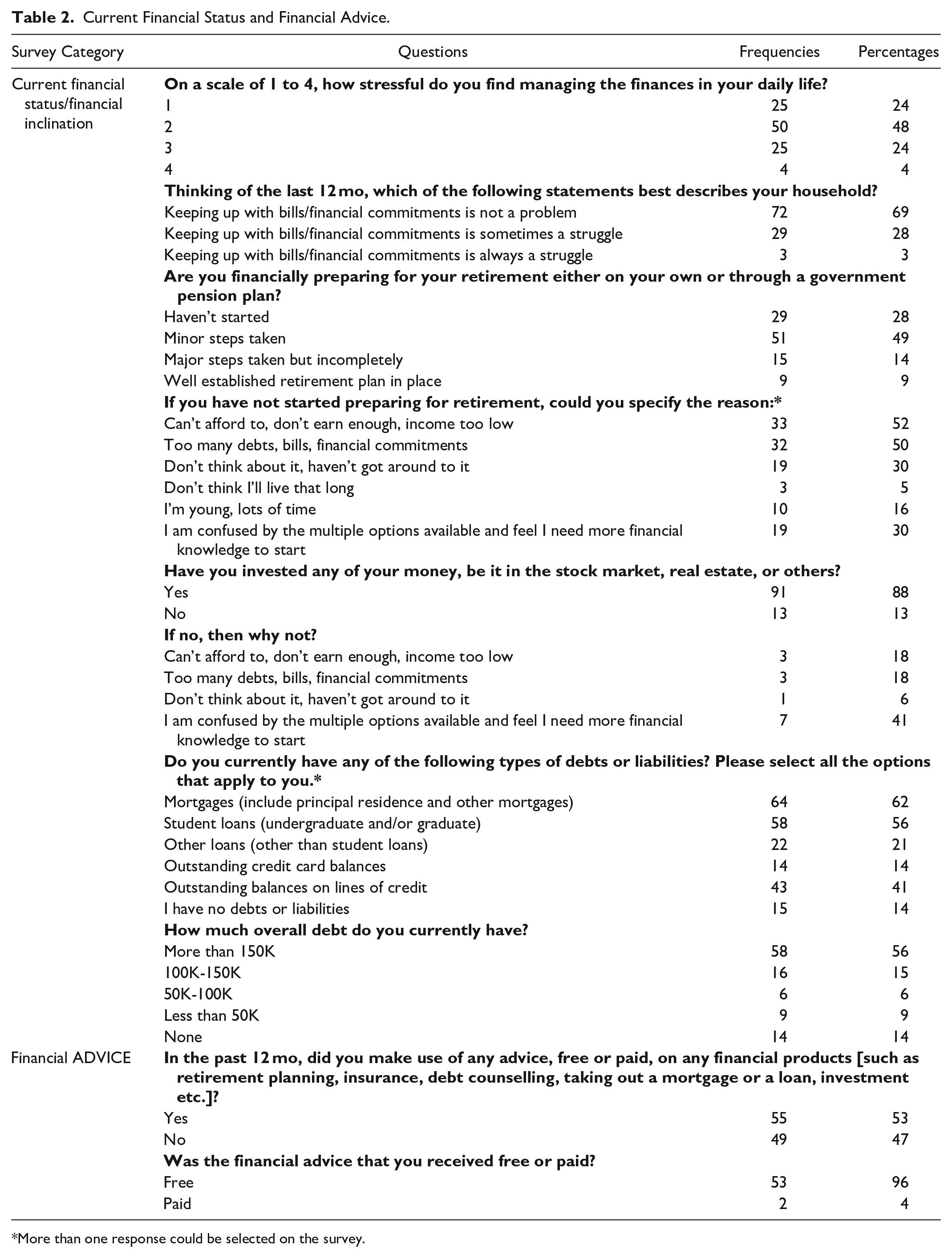

Responses for this section are provided in Table 2. Overall, 56% (n = 58) of respondents stated having debt in excess of $150 000. Only 9% (n = 9) of respondents had received any form of financial training or have had previous experience in the financial workplace. Regarding retirement planning, only 23% (n = 24) of respondents reported having taken major steps in their retirement planning or had a plan in place, with the majority of residents having not started planning or having only taken minor steps. Approximately 52% (n = 33) of those that have not started retirement planning stated they are not able to currently afford this or do not have enough money to plan for this, and 50% (n = 32) stated they have a high debt burden, significant bills, and/or other financial commitments to start retirement planning. Regarding investments, 88% (n = 91) of residents have invested some of their savings in the stock market, real estate, or other forms of investment. Of the residents who did not invest, approximately 37% (n = 7) stated being confused by the innumerable investment options, with the next most common reason being high debt burden, significant bills, and/or other financial commitments.

Current Financial Status and Financial Advice.

More than one response could be selected on the survey.

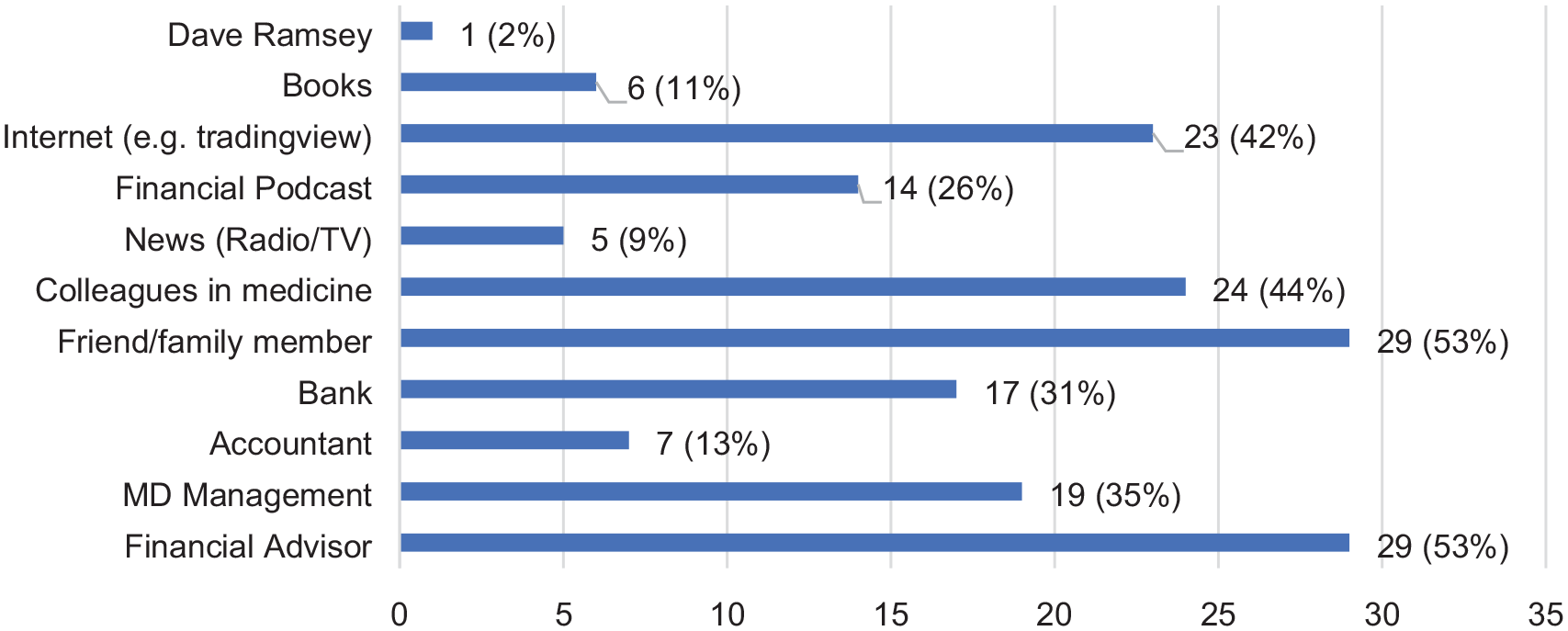

With regards to financial advice, 96% (n = 53) of respondents that had received financial advice, stated that this was free. The sources of financial advice are shown in Figure 1. When asked about which books, podcasts, or social media resources the respondents utilized, the majority (23%, n = 12) stated using the Facebook group dedicated to physician finances. Other resources that were frequently cited were: books (eg, Millionaire Teacher and Wealthy Barber), websites (eg, Canadian Couch Potato blog), as well as podcasts (eg, Canadian Investor and Rational Reminder).

Sources of financial advice provided to residents.*

Financial Quiz

As part of the financial literacy survey, respondents underwent a 15-question financial knowledge quiz. The full results of the quiz are provided in Supplemental Material 2. The average score for the respondents was 71.2% ± 17.4%. The 2 questions with the lowest percentage of correct answers included a question about whether an incorporated radiologist can contribute from their corporation to their Tax Free Savings Account (TFSA) (40.4% selecting False, which is the correct answer), and a question about the various options for withdrawing non-taxable income from a Registered Retirement Savings Plan (RRSP) (only 34.6% of respondents selected the correct combination of options). There were no statistically significant differences in the correlation between financial literacy quiz scores with level of training (P = .71) and previous financial knowledge (P = .15) and levels of debt (P = .68).

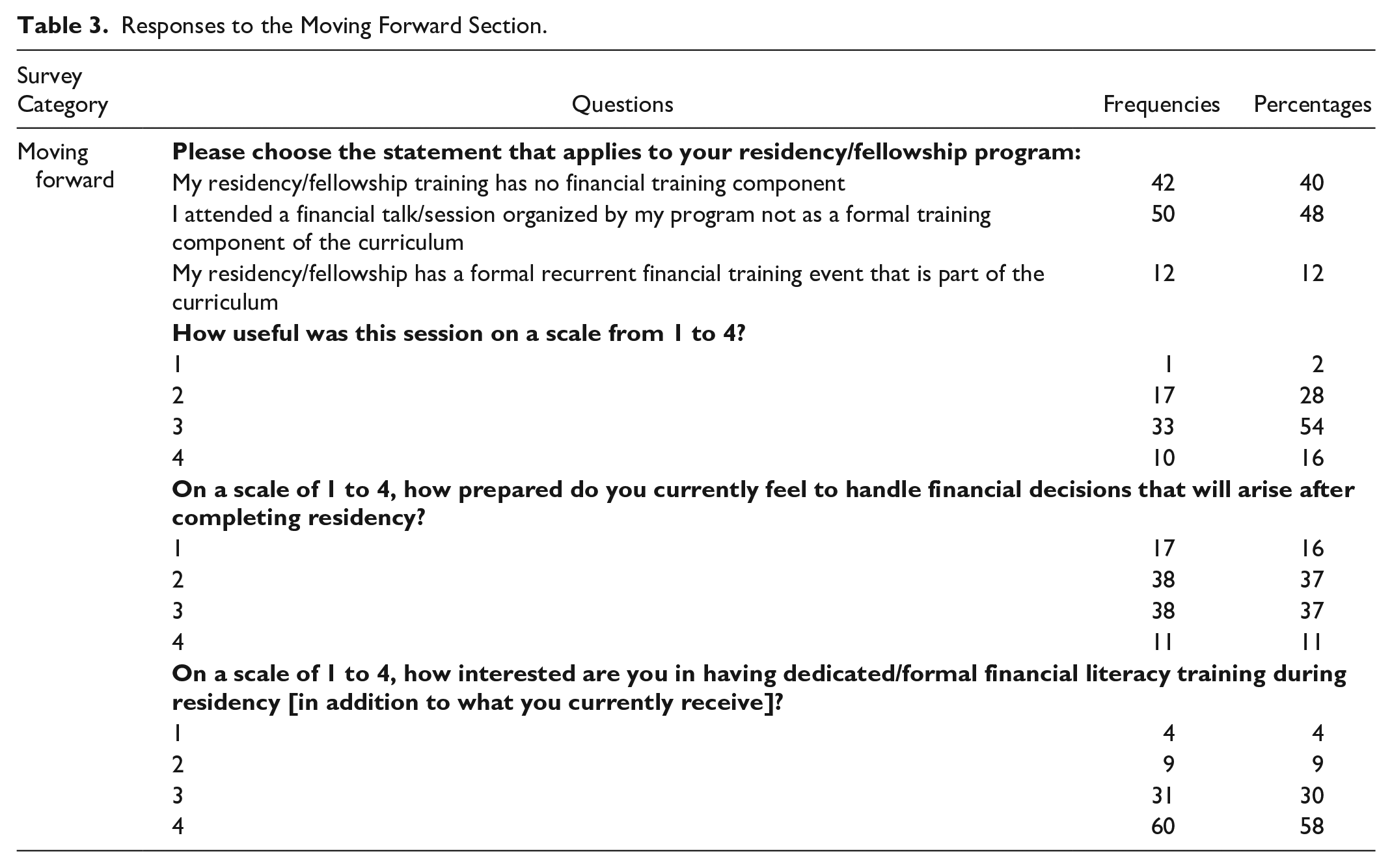

Moving Forward

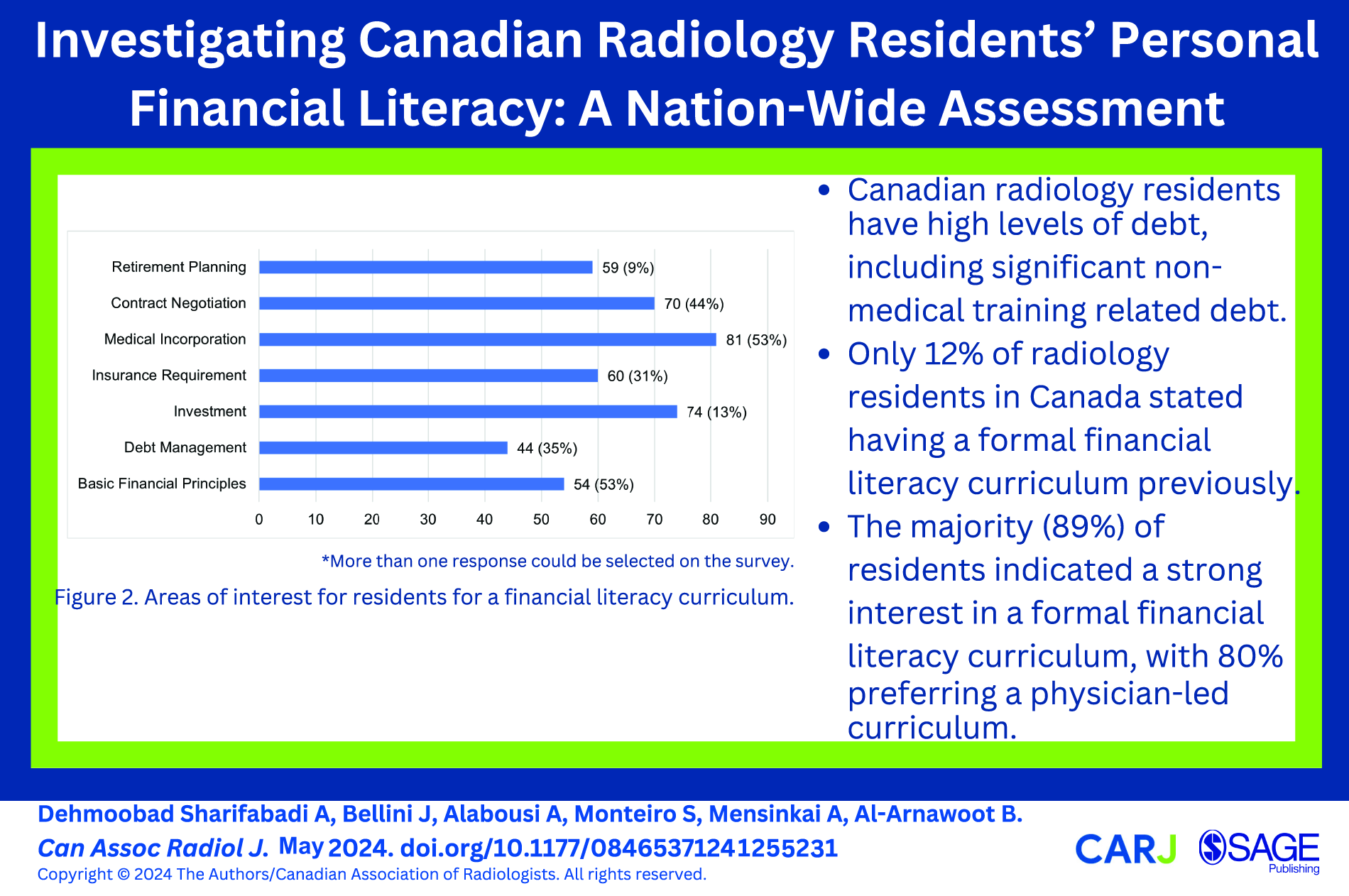

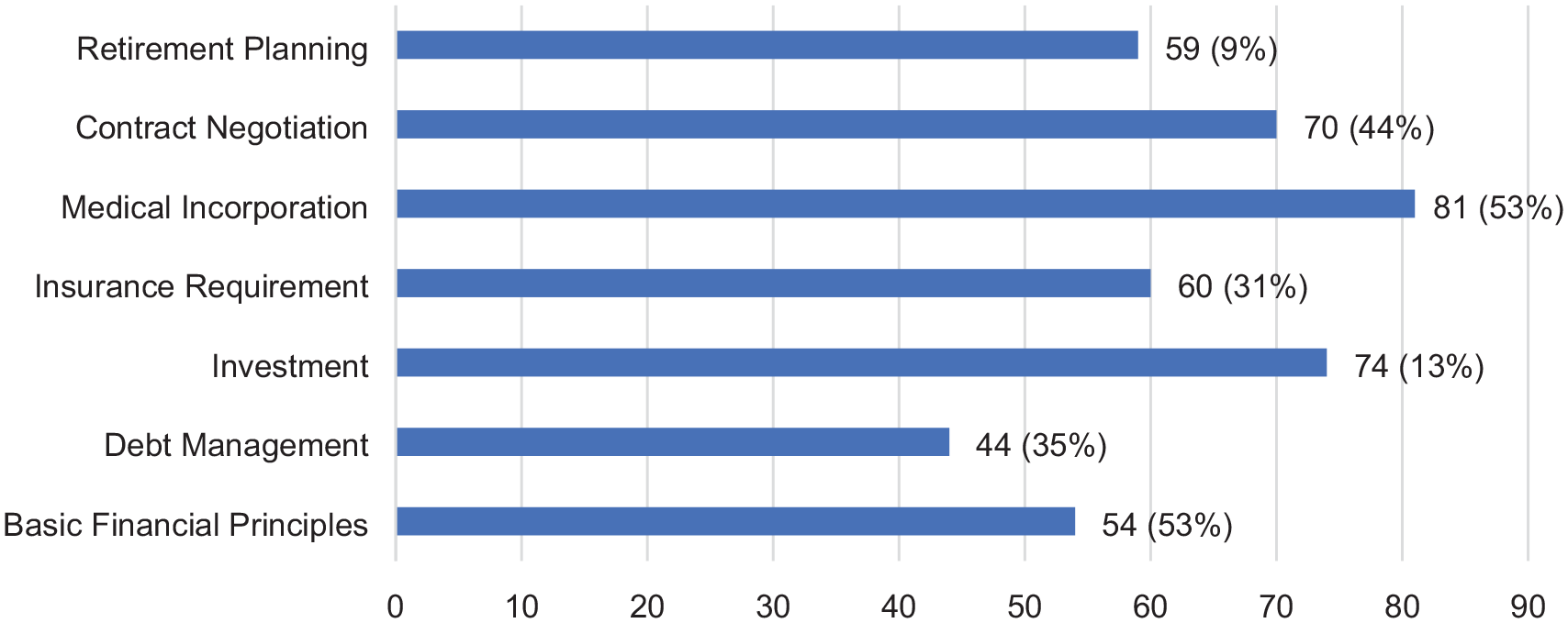

Responses to this section can be found in Table 3. The majority of respondents (88%, n = 91) indicated high interest in a formal financial literacy curriculum as part of their radiology residency training. Specific topics of interest to residents are described in Figure 2. The top 3 topics of interest, in descending order, are: incorporation, investing, and contract negotiation. Two of the residents stated that common topics such as basic financial knowledge and retirement planning are generally self-learned; however, they would be more interested in radiology specific topics such as finances pertaining to an academic versus community radiology career, partnership track jobs, as well as information on buy-ins to radiology practices. One learner also stated that they would not want another “mandatory” aspect of the curriculum, but rather a tailored curriculum with more latitude to one’s needs.

Responses to the Moving Forward Section.

Areas of interest for residents for a financial literacy curriculum.*

Importantly, the majority of residents (92%, n = 94) stated that they are interested in receiving this curriculum from other physicians (radiologists or otherwise). Additionally, 73% (n = 74) of residents stated wanting to receive components of this curriculum from financial advisors/experts. Four residents answered this question in free text, stating that they would want “non-bank affiliated financial advisors,” “experienced tax accountants and tax lawyers who are experienced in handling radiologists’ finances,” “financial advisors but only if they are not promoting their services,” and “financial advisors who are well-versed with medical training.”

Discussion

On the journey of becoming a physician, finances play a large and often stressful role. 15 However, despite the highly onerous academic and clinical training, financial literacy is often lacking or limited during training. Our study illustrated that while residents score relatively high on the financial literacy questionnaire, there is still high demand for further financial literacy curriculum to be integrated into Canadian radiology residency training.

Our study found that more than half of respondents have debt in excess of 150 000 (56%, n = 58). This is in keeping with reported debts of Canadian medical graduates averaging $84 172 for medical school expenses and $80 516 of non-education related debt. 6 Interestingly however, 62% of residents (n = 64) stated mortgage to be a part of their debt. This is important as allocation of income to managing multifactorial debt is more complicated. Previous studies also show that non-medical debt including credit cards can be significant 27 ; for example, Ahmad et al 15 showed 32% of residents in their study were expecting to carry over more $10 000 of credit card debt to the next month. Interestingly, in our study, 81 (53%) residents selected medical incorporation as a topic of interest for a financial curriculum while 44 (35%) selected debt management. A systematic review of previous financial literacy curricula demonstrated that almost all programs included a component of loan repayment/debt management education. 21 There appears to be discordance between the residents’ desired topics of interest versus what is deemed necessary by educators. Perhaps this could be due to the fact that in general, medical incorporation and specifics of radiology practices are more challenging and unfamiliar concepts compared to managing credit card or mortgage debt. However, as illustrated in our study, there is a clear need for basic financial principles including managing multifactorial debt.

The average score of the Canadian radiology residents on the financial survey was approximately 71%. Prior studies of financial literacy quizzes among residents predominantly in the United States demonstrated scores between 51% and 61%.9,15 There is large heterogeneity between the various financial literacy quizzes used in these studies and our study, therefore a direct comparison to these studies is challenging. Our survey was derived from a Statistics Canada financial literacy survey, on which the general Canadian population scored 61%, 28 which may suggest that perhaps radiology residents in Canada score slightly higher than the general population. A similar finding was also demonstrated by Nowotny for American medical residents where financial literacy in a group of residents and medical students was higher than the general population. 29 This is an interesting and unexpected finding and could be related to the high levels of stress associated with debt levels, which may prompt trainees to seek out knowledge on their own time. 30 Given the lack of significant correlation found in our study between training level and financial literacy, the time at which this knowledge is acquired may be variable.

In our sample of respondents, only 12% had a formal financial literacy curriculum as a mandatory component of their residency program. This is in agreement with multiple studies demonstrating an established residency curriculum deficit in financial literacy, recognized by educational experts. 17 The Royal College of Physicians and Surgeons of Canada does not include resident financial education as a standard for accreditation of residency programs and the Accreditation Council for Graduate Medical education only includes finance-related topics pertaining to patient health decisions as a standard rather than pertaining to resident career development.31,32 An important step toward implementation of a financial literacy curriculum may be recognition by educational stakeholders regarding the importance of this topic toward accreditation of a program.

Importantly, our study demonstrates that residents are strongly interested in the implementation of a formal curriculum and that residents wish to have a physician perspective, radiologist or not. Two systematic reviews on current personal finance training programs for medical trainees demonstrated that the majority of the primary studies rely on physician instructors.22,33 It is probable that residents wish to be taught by physicians who have an implicit understanding of their training journey through medical training and can offer guidance as they start their career. However, physicians may not be able to have the time and resources to dedicate to financial literacy curricula. Instead, financial advisors may be a more accessible and cost-effective resource, however trainees may be opposed to the inherent conflict of interest and the possibility of receiving commission from selling their financial products.16,34-36 The preference of physicians as instructors also explains our findings that residents identified physician led financial blogs and Facebook groups as a major source of financial advice. Moving forward, this is a consideration when selecting instructors for financial literacy curricula; there is ongoing evidence that trainees wish to be taught by those who understand medical training, physician payment models and are unbiased.

The mode of curriculum delivery, whether self-directed versus didactic, is an important consideration. One resident stated that another “mandatory curriculum” to replace already strained training time would be problematic. There have been multiple studies assessing financial literacy interventions in residency training.13,15,36 For example, Ahmad et al 15 had suggested focusing on teaching multiple topics through a mini-MBA 6-week curriculum with demonstrated differences in financial knowledge scores. Other strategies included Bar-Or et al 36 who implemented 4, 2-hour sessions over the span of 4 weeks, and Mizell et al 13 who implemented an 18-hour curriculum during protected teaching time at grand rounds. Implementation of both curricula was met with increased financial knowledge and increased resident satisfaction. Gianakos et al 17 suggest a 5-year curriculum throughout residency with progressive and more specific financial knowledge. Future research is warranted to assess a curriculum that assesses residents’ baseline knowledge and provides for a tailored program in addition to specialty-specific practice knowledge.

In addition to a structured curriculum, one of the respondents discussed the possibility of a tailored financial literacy curriculum for each learner. This is an interesting finding as our study demonstrates that prior general financial knowledge in the form of prior university/college education or work in the financial industry was not associated with better financial literacy scores. While this may be due to knowledge lost through the years of medical school training, it may also represent the importance of tailored education based on trainees’ current understanding of fundamental financial concepts. This is particularly relevant in a competency-based design environment. A targeted resource, such as a physician financial coach (similar to an academic advisor) can serve to provide additional support for residents besides a standardized blanket curriculum. The feasibility and resource burden of this type of program may be an area for future research.

There are several limitations to this study. This study only included participants from radiology and as such may not be generalizable to other residency programs or specialties. This was identified as a future research focus to provide more generalizable data across a wider range of programs. In addition, there also may be an element of sampling bias in participation, with residents who are not comfortable with their finances being possibly less likely to complete the survey. Finally, the questions were derived from a literature review and from Statistics Canada and therefore scores may not be generalizable to other trainee resident populations in other countries. The survey was also conducted on an online platform in an uncontrolled test environment rendering the possibility that a participant searched for the answers before responding to a question.

Conclusion

Overall, Canadian radiology residents face a high debt burden and the majority do not have an adequate financial literacy curriculum in their residency programs. Nearly all residents were interested in a formal financial literacy curriculum to further help them with their finances. Considering the implications of financial well-being on residents’ overall well-being, our survey analysis provides further data on a need for a physician-led financial literacy curriculum, which is tailored to the residents’ current understanding of finances. The high existing financial knowledge of residents should serve as a baseline for dedicated physician financial literacy curriculum. Furthermore, a dedicated curriculum allows trainees to feel empowered to tackle financial challenges rather than further propagate the taboo culture surrounding financial discussions in medicine.

Supplemental Material

sj-docx-1-caj-10.1177_08465371241255231 – Supplemental material for Investigating Canadian Radiology Residents’ Personal Financial Literacy: A Nation-Wide Assessment

Supplemental material, sj-docx-1-caj-10.1177_08465371241255231 for Investigating Canadian Radiology Residents’ Personal Financial Literacy: A Nation-Wide Assessment by Anahita Dehmoobad Sharifabadi, Jonathan Bellini, Abdullah Alabousi, Sandra Monteiro, Arun Mensinkai and Basma Al-Arnawoot in Canadian Association of Radiologists Journal

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The gift cards provided for participants in this study were funded by the Department of Radiology at McMaster University.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.