Abstract

Export taxation holds a particular place within trade policy, especially so during the mercantilist era. While governments tried to ensure consistent export surpluses, they would at the same time put tariffs on those goods, possibly impeding export growth. This article quantifies export duties in Denmark and Sweden during close to a century, to analyze which intensity they had over time and which role they played within trade policy. The article finds that these taxes were at times rather high, particularly on raw materials partly reserved for domestic use or refinement. The fiscal dimension of export taxation clearly played an important role as well, as revenue needs often delayed the removal of tariffs. One conclusion is that the regulation of exports presents an interesting case of political conflict, between promoting growth and filling state coffers.

Introduction

Mercantilism held a tight grip on trade policy in Europe during the early modern period and, for some countries, even during a substantial part of the nineteenth century. It was a broad set of ideas on how the economy should be governed and regulated, where views on trade formed an integral subset. 1 While there were national differences in scope, scale and content, mercantilist policies with regard to trade typically included broad regulations such as tariffs, prohibitions, monopolies on long-distance trade (such as the East India companies) and restrictions on foreign shipping. Since the general idea was that export surpluses were beneficial for economic development, most political attention was directed at limiting the overall level of imports. Therefore, the most restrictive regulations concerned imports, either through high tariffs or numerous prohibitions. Mercantilists were, on the other hand, generally critical of policies and regulations that restricted domestic exports and merchants’ export business. 2 Despite this, several countries taxed their export commodities, and prohibited certain exports outright, as part of their trade policies. Export tariffs were a mainstay of mercantilism during the eighteenth century and the first decades of the nineteenth century, particularly in European countries such as Great Britain, the Netherlands, 3 Spain, Denmark and Sweden. In several countries, they would remain in place even as these countries liberalized their trade policies during the second half of the nineteenth century. However, the role and intensity (level) of these trade taxes has been underexplored in much of the research on the eighteenth and nineteenth centuries. The main focus in the literature has been on the impact of tariff policy on the import side of the trade ledger.

This article adds to the debates on the role of tariffs in trade policy by looking at how exports were taxed in Scandinavia from the late eighteenth century to the second half of the nineteenth century. It does so by quantifying the tariffs on a large number of export commodities over close to a century, from 1780 to the 1860s, when the last of these taxes were dismantled. This brings to the forefront new tariff data that allows for an analysis of changes over time, and comparisons between Denmark and Sweden, as well as the differences between different types of commodities. It is found that export duties were generally higher in Sweden, where they were also fiscally more important. The fiscal dimension was clearly important, as perceived revenue needs prevented the complete removal of these tariffs in both countries. The article highlights a potential political conflict in trade taxation – between promoting export growth by lowering or completely removing tariffs, and hence reducing costs for export business, and ensuring fiscal capacity. Both countries struggled with this trade-off, although revenue needs would be increasingly switched to imports over time.

The article is organized as follows. First, the ‘Trade policy, mercantilism, export and tariffs’ section extends the discussion on mercantilism and the role of tariffs in trade policy. ‘Trade policy in Scandinavia before 1870’ provides the background on trade policy in Denmark and Sweden before 1870. ‘Data, sources and methodology’ outlines the sources, data and methodology used to calculate the tariffs on exports in both countries. ‘Export tariffs in Denmark and Sweden, 1780–1870’ presents the results, comparing the intensity of export tariffs in Denmark and Sweden on an aggregate level, as well as on the commodity level. Conclusions are offered at the end of the article.

Trade policy, mercantilism, export and tariffs

Export tariffs were used in England from at least the end of the thirteenth century and were generally a cornerstone of European mercantilist trade policies. As we shall see, the existence of export duties has not been exclusive to eras when mercantilism dominated trade policy, but mercantilism serves as a good starting point because of its prevalence in the Scandinavian countries during part of this period, and because of its concern with export-dominated trade. During the eighteenth century and first half of the nineteenth century, several European countries chose to tax their own exports. Around 1820, these taxes were in place in Austria-Hungary, Denmark, France (however, rarely used), Great Britain, the Netherlands, Portugal, Russia, Spain, Sweden and Switzerland. 4 In Britain, export duties had been placed on about 200 articles during the previous century, starting at the rate of five per cent ad valorem. The Dutch Republic typically set all its export tariffs at a uniform and stable one per cent ad valorem during the eighteenth century. By the late 1830s and early 1840s, tariffs were still placed on most exports in the Netherlands, in the order of 0.5–1% ad valorem when it was specified. 5 Export taxes were gradually removed in most of Europe from the 1840s to the 1860s. England did away with its taxes in the tariff law of 1842. In France, they made their last appearance in 1857 and, in the Zollverein, in 1865, while in Norway, for instance, they remained in use until the 1890s. Contrary to many European states, the United States had prohibited the use of taxes on exports in its constitution. During the late nineteenth century, export taxes were used in a few Latin American states, such as in Chile with nitrates. 6 They were also employed in some British colonies and protectorates, such as in the Federated Malay States with tin ore, in Nigeria and the Gold Coast (Ghana) with palm kernels, and in India with hides and skins – in effect, in order to discriminate exports to destinations outside the British Empire. 7 Since the Second World War, export taxes have mostly been used by developing countries to tax the exportation of natural resources, although there have been exceptions in the twenty-first century in the form of Norway and Canada, which have at times taxed the export of one or several commodities.

Taxes on exports have a rather peculiar place in trade policy, but perhaps mostly in more mercantilist-minded policies. If a positive trade balance is good for growing the riches of the nation, and a central goal is to make foreigners pay for your goods, then why make the export trade more costly for producers and domestic merchants? 8 It is generally acknowledged that the existence of export taxes will bring about a downturn in export volumes for the home country. 9 Raising the level of existing export tariffs will lower prices, production and trade; conversely, a decrease in or the complete removal of export tariffs will increase prices, home production and trade growth. 10 One possible answer may lie in the fact that mercantilists were generally more in favour of promoting the export of finished goods, manufactures and semi-refined goods, while prohibiting or limiting the export of ‘precious minerals and raw materials’. 11 Placing a high or even prohibitive tariff on such commodities could be a way of making sure that a sufficient quantity was kept for the domestic economy, and this was integral for domestic manufacturers and proto-industries. Other mercantilist thinkers were in favour of the export of natural resources in cases where they were ‘superfluous’. 12

While this article is mainly concerned with the role of export tariffs in trade policy, it is worth noting that previous research has viewed some of the Scandinavian export tariffs as being so high as to impede higher levels of exports. 13 Whenever Scandinavian eighteenth- and nineteenth-century trade policy has been studied, export taxes have typically only been mentioned in passing, and the main focus has always been on the import side, with taxes and regulations, since it is here that we can analyse protectionism and the fiscal importance of tariffs. 14 With a few exceptions, the same goes for the international literature. 15 For the pre-twentieth-century period, there are two examples that stand out, both concerning the workings and effects of cotton export tariffs in the Americas during the 1800s. 16 From the research we do have, it is possible to determine two main reasons why countries have chosen to willingly tax their own exports: (1) because of revenue need, which typically, but not always, applied to raw materials that carried low-level tariffs, and (2) to maintain a sufficient level of the product for domestic refinement or consumption. The first is found in a variety of cases, from seventeenth-century England to late nineteenth- and early twentieth-century Chile, British colonies during the early twentieth century, and several developing economies after the Second World War. 17 An example of an exception to the rule of taxing raw-material exports low for fiscal reasons can be found in nineteenth-century Brazil, where cotton export tariffs could be relatively high (sufficiently high to be distortionary to some degree) but were put in place to sustain a cash-strapped newly independent nation that largely lacked other forms of taxation than trade taxes. 18 Examples of the second reason can be found in Scandinavia during the pre-industrial era, but have also been a feature of modern developing economies that are rich in natural resources. 19 Countries with a large share of the world production of a specific commodity may also use their market power to set export taxes, which effectively raises the world price of the commodity. 20 Hence, while there are other more specific reasons for imposing and maintaining taxes on exports, such as the British colonial and imperial preferential system mentioned earlier, revenue importance and domestic need will be the two main guiding factors when analysing how Denmark and Sweden set and used these taxes. While there is no clear-cut definition in the literature of what constitutes ‘distortionary’ (that is, impeding trade to some extent) tariff levels, ad valorem duties at around five per cent have been mentioned as ‘non-distortionary’. 21 Denmark typically put ‘prohibitive’ tariffs at 24 per cent ad valorem, while Sweden would put them at 40 or 50 per cent. Hence, duties at around five per cent would distort trade flows to a low degree, while levels of at least above 20 per cent could be considered a noticeable or even large policy intervention. This leaves room for interpretation, as we will find quite a large number of commodities carrying duties of between 5 and 20 per cent.

Trade policy in Scandinavia before 1870

The Danish and Swedish trade policies during the first half of the eighteenth century were quite similar, with a generally restrictive import policy consisting of numerous prohibitions and high tariffs. Several sectors received protection from foreign competition with the mercantilist aim of developing domestic manufactures. One difference between the countries was that Denmark taxed some luxuries lower, such as fine foreign clothing – commodities that at the same time were banned from import into Sweden. 22 Denmark also taxed its exports slightly lower overall, but, during the eighteenth century, several important raw materials were banned from export, such as timber, copper and wool. 23 Both countries’ trade policies remained stable over time overall, but started to diverge as the century drew to a close.

The processes of trade policy liberalization started quite early in Denmark compared to the rest of Europe. In 1788, the country's grain trade was freed from prohibitions but put under a tariff. The year 1797 marked the introduction of the tariff law, which has become almost synonymous with Danish trade policy and laid the foundations of it for years to come. It notably cut many import tariff rates and removed several import prohibitions. Danish duties were then increased in three steps during the Napoleonic Wars in order to adjust for inflation and raise revenue for the war effort. In the first post-war tariff law of 1816, Denmark initiated an era of agricultural protection when high import tariffs were put on cheese, butter, grains, pork and beef. Most of these tariffs were lowered over time and were eventually removed with the tariff law of 1863. The one exception was the import tariff on cheese, which remained at a protectionist level throughout the 1870s. 24 The 1840s generally saw a wave of liberalization once again, where tariffs on the import of machines and porcelain were cut in 1844 and the import ban on refined sugar was removed, and the import duty on coal was reduced by half in 1847. 25 Furthermore, the import of unprocessed grains was made completely duty-free in 1846. Eventually, the last import prohibitions in Denmark disappeared in 1847. 26

In Sweden, there were numerous trade bans and tariffs were high by the beginning of the 1780s. Some tariffs were lowered slightly during the comparatively more liberal times of the Napoleonic Wars, but the protectionist base of the trade policy was not removed. 27 In 1816, tariffs were increased to make up for the fact that the rates had effectively dropped with the previous war inflation. Import tariffs remained relatively high and stable during the 1820s, and iron, forestry and agriculture were protected. The protection of textiles was somewhat alleviated and tariffs on forestry imports decreased in 1826. The most notable change of the 1830s was that the number of goods that were banned from import decreased from 119 to 40 in 1835. This number then gradually decreased until 1854, when only four import prohibitions remained. Among these liberalized goods were many that did not make a big difference to the overall import structure, such as iron goods, which would only be imported in small quantities anyway, but many fine textiles, cloth and articles of clothing saw an increase in imports in Sweden in the 1830s and 1840s due to the lifted bans. 28 Import tariffs remained quite stable overall until 1854, when the Swedish trade policy was truly made more liberal. Tariffs were cut almost across the board, mainly on agriculture, textiles, forestry and metals, which effectively removed any of the protectionism that remained in these sectors. Several items, such as grains, dairy, flax, hemp and wool, were made completely duty-free, which was a radical political move from a Swedish historical perspective. The average import tariff fell from around 30 per cent ad valorem in 1853 to just over 10 per cent between 1857 and 1860.

Data, sources and methodology

The tariffs have been calculated as ad valorem equivalents following the example in Henriksen, Lampe and Sharp’s 2012 study, ‘The Strange Birth of Liberal Denmark’, meaning that the nominal duties are divided by the price of each commodity. All of the major tariff revisions have been included, which were usually undertaken more often in Sweden than in Denmark. Danish tariff revisions, including export duties, were made in 1768, 1797, 1803, 1806, 1809, 1816, 1823, 1838, 1844 and 1850 (and 1863). Swedish revisions of export tariffs were undertaken in 1782, 1799, 1816, 1818, 1822, 1824, 1826, 1830, 1835, 1841, 1845, 1848, 1851, 1854, 1857, and 1860. 29 Tariffs were usually denoted as specific rates in both countries – that is, per weight, volume or number of units. Where a tariff is noted as ad valorem directly (quite uncommon with exports), that figure has been used without any alteration. Where the aggregate tariffs are presented, the unweighted mean has been used. The duties denoted here strictly concern maritime trade as exports by land rarely occurred in the Swedish case; they only really involved a small number of commodities traded with Norway, which were generally duty-free anyway. In the Danish case, there were slightly larger trade flows to the south, to the duchies of Schleswig and Holstein (considered domestic or intra-realm trade until the Second Schleswig War in 1864) and the Germanic states, but this trade carried other, generally lower duties and was non-existent for many exports. Because of the division of political and economic power within the Scandinavian kingdoms, the tariffs studied here apply to Denmark and Norway before 1813 and to Sweden and Finland before 1809. After these years, the trade policy regulations affected only Denmark and Sweden. 30

Few commodities which were prohibited for export were produced in any higher volumes, other than pig iron and iron ore (see number of commodities prohibited for export in Table 1). 31 Here, it mainly concerns the Swedish export of pig iron, which was officially banned until 1857 (although it was exported from 1817 to Finland exclusively). Since banned goods were placed under a tariff, to be paid in the event that the King granted a license to trade in those goods, that tariff level has been used during the years when the export of pig iron was officially prohibited. Based on the official trade statistics, it seems as though exceptions to export prohibitions were rarely, if ever, granted. The export of pig iron to Finland was one such exception but it was bound by preferential trade agreements and did not carry a high tariff.

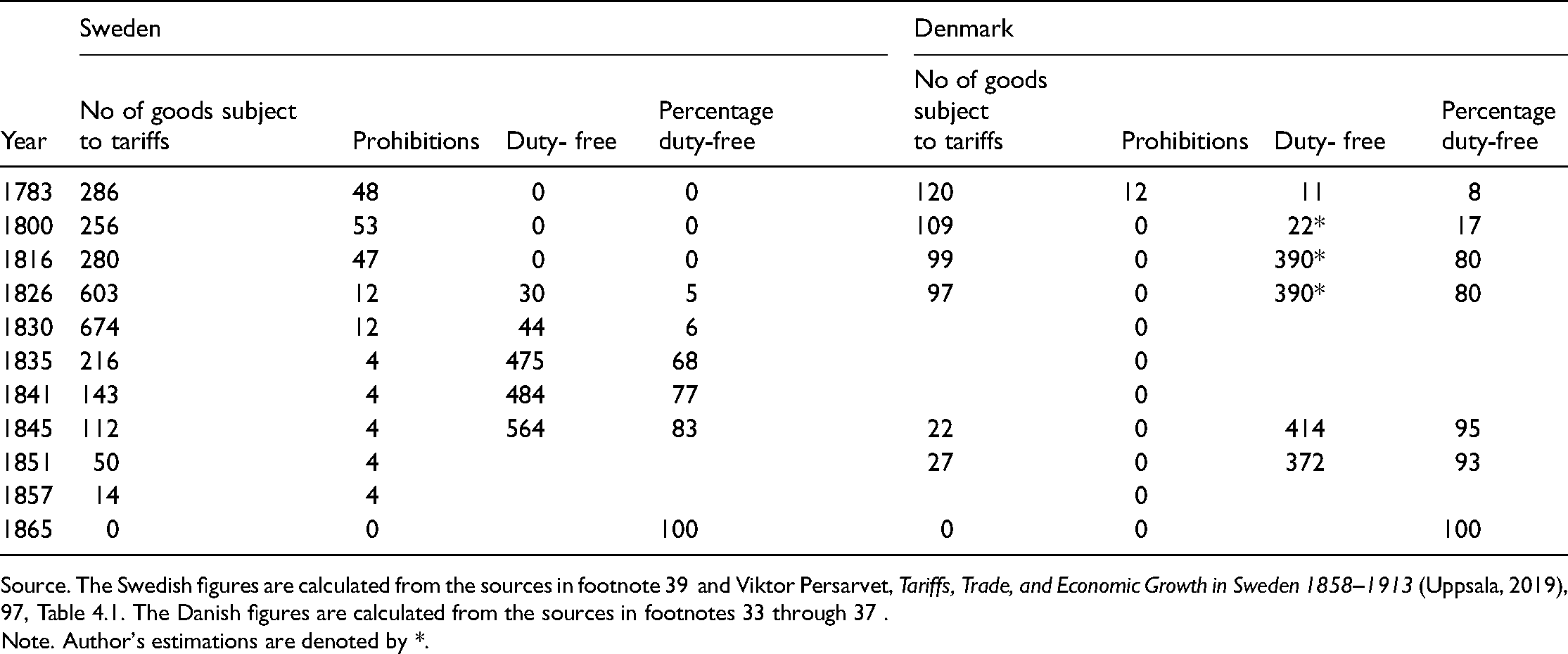

An overview of Swedish and Danish tariff legislation pertaining to export commodities, 1783–1865.

Source. The Swedish figures are calculated from the sources in footnote 39 and Viktor Persarvet, Tariffs, Trade, and Economic Growth in Sweden 1858–1913 (Uppsala, 2019), 97, Table 4.1. The Danish figures are calculated from the sources in footnotes 33 through 37 .

Note. Author's estimations are denoted by *.

Re-exports have been completely excluded from the analysis. One reason for this is that they very rarely had a tariff and therefore worked under different regulations and rules than domestic exports. Re-exports were, however, occasionally of great significance for the two Scandinavian countries during the period. Swedish re-exports boomed during both the Napoleonic Wars and the Crimean War (but more so during the former than the latter). The only two Swedish re-exports that had a tariff were sugar and tobacco, which was set at a fixed rate of 0.25% ad valorem for both (between 1782 and 1826, being duty-free thereafter). Denmark re-exported sugar and rum from its Caribbean colonies and sometimes in large quantities, such as during the height of the Napoleonic Wars in 1805–1814. 32

The Danish and Swedish duties on exports (and imports, although not presented here) have been collected from different sources. The first Danish tariff revisions (of 1762, 1768 and 1797) have been taken from Aage Rasch's work on Danish trade policy. 33 They have been complemented by examining the original tariff lists from 1762 and 1797. 34 The duties then increased in three steps during the Napoleonic Wars, across the board – by 12.5% in 1803, 12.5% again in 1806, and then 50 per cent in 1809. 35 The two consecutive tariff laws (of 1816 and 1823) have been taken from primary sources. 36 For the years 1838 and 1844, the duties have been calculated from the export quantities and customs revenue in the official Danish trade statistics. 37 The last two revisions have been taken from secondary, but contemporary, cross-country investigations of tariff rates. 38 The Swedish sources are, in a way, more straightforward, where all of the tariffs concerning foreign trade were noted in the collection of laws and regulations by the King, and later the government. All of the duties have therefore been collected directly from these sources. 39

As far as possible, I have tried to calculate ad valorem equivalents using national market scale prices or approximations thereof. Price notations in Stockholm on iron and steel, other than bar iron and alum, have been used to approximate the Swedish national prices. The goal has been to use Danish prices for Danish exports and Swedish prices for Swedish exports. 40 Due to data limitations, this has not always been possible, and they are therefore complemented by international price data. 41

Export tariffs in Denmark and Sweden, 1780–1870

Denmark and Sweden were similar in the sense that export tariffs remained in use until the 1860s, but, as can be seen in Table 1, Sweden placed prohibitions on a large number of export goods at the beginning of the period. Most of these were of minor importance in terms of domestic production, but some were commodities with sizeable production volumes and would remain prohibited until the late 1850s – most notably, iron ore and pig iron. 42 More than half of the rest of the individual export prohibitions before 1826 were minor forestry goods. Denmark would generally put tariffs on a smaller number of exports, which indicates that more goods were exported completely duty-free. 43 The number of prohibitions is listed as zero after 1797 in the Danish case, but a caveat is that grains were banned from export in certain months of the year at the end of the 1790s and in the early 1800s because of poor harvests and harsh winters. 44 However, the number of goods that were taxed does not reveal a lot about the overall level of taxation. The number of commodities in the tariff rolls also depended on the degree of aggregation – for instance, whether different types of fabric and clothing were listed as one item or were separated by size, colour or quality. It is this type of change that largely explains the increasing number of export items from 1816 to 1826 in Sweden.

We can observe some changes from Table 1, with one of the most notable being the growth in duty-free Swedish exports during the late 1820s and 1830s. The 1826 revision removed a large number of prohibitions on forestry exports, and also introduced a smaller number of duty-free exports for the first time. This can be seen as a continuation of a conscious export-promoting policy, which began in 1816 after interests in the forestry sector lobbied the government for an alleviation of their tariff burden (see the ‘Export tariffs by commodity in Sweden’ section below). The tariff law of 1835 would then increase the number of duty-free goods more than tenfold. The Danish tariff law was generally stipulating a larger number of exports with zero tariffs at the end of the Napoleonic Wars, therefore being two decades earlier than Sweden in this regard. The taxation structure in the two countries then looked more similar during the 1840s and 1850s, before the last of the export duties were finally removed in 1863 in Denmark and 1860 in Sweden.

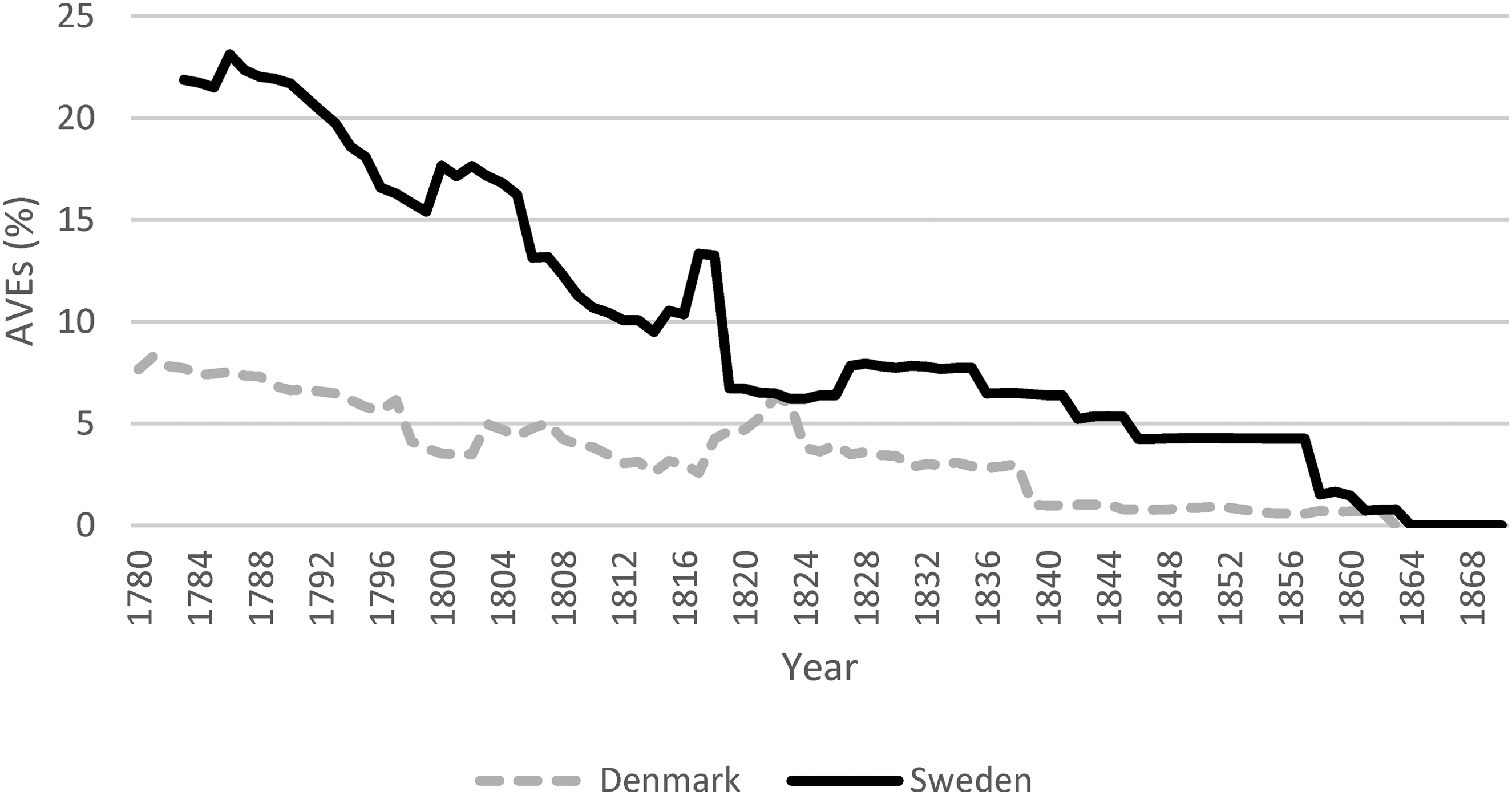

The remainder of this section will deal with the Danish and Swedish export duties themselves, providing a sample of each country's export basket from 1780 to 1870. 45 Measured as ad valorem equivalents, the average Danish export tariffs were not at a high level during this period, never exceeding eight per cent. Export duties had been cut somewhat in the tariff law of 1797 but this did not denote a radical downward push overall. This revision set the rather mercantilist standard of putting lower tariffs on products with a higher degree of refining, some of which were even exported completely duty-free. Meanwhile, raw materials, like timber, unfinished metals and food, carried higher duties. Certain raw materials destined for industrial use, such as wool and flax, were given lower tariffs. 46 According to Rasch, the 1797 revision put more focus on fiscal concerns than previous iterations, also pertaining to exports. 47 Levels decreased between 1810 and 1814 due to war-induced inflation, which was higher than the increase in nominal tariff rates. Specific tariffs were immediately increased once peace was restored, meaning a peak was reached in 1822–1823. Export duties were then significantly lowered in two steps with the tariff laws of 1823 and 1838 – especially with the latter. From 1839 to 1860, export tariffs circled at around one per cent ad valorem, but most commodities were exported completely duty-free. From 1839, tariffs were only levied on livestock, hides, wool, timber (until 1844) and gar copper (from 1845). 48 Because of their low ‘non-distortionary’ levels, these remaining tariffs can be interpreted as being in place almost exclusively due to fiscal concerns. 49 The last of the export duties were removed with the new tariff law in 1863.

One of the reasons why tariffs on certain commodities remained for so long was fiscal. By 1857, it was estimated that the complete elimination of export duties would have removed about 340,000 Danish kroner from the treasury, which was little compared to the close to 14 million Danish kroner brought in by taxes on imports, but enough to be a concern for lawmakers. 50 Between 1820 and 1860, the customs revenue from exports fluctuated between 250,000 and 400,000 Danish kroner in nominal terms. 51

Compared to Denmark, Swedish export duties were at a higher level at the beginning of the period, starting off at over 20 per cent ad valorem. Even though rates fell until 1815, mostly due to increasing prices, the overall level was comparatively high. One reason for this is that certain exports carried very high duties – over 10 per cent of the export price on commodities such as bar iron, pitch and tar. 52 With the tariff law of 1818, many rates were cut, meaning the average ad valorem tariff fell from 13 to 7 per cent. With three consecutive tariff laws (1835, 1841 and 1845), export duties were further lowered or removed completely, meaning that from 1846 the average export tariff was only at 0.1% ad valorem. The only significant export tariff that remained until the 1860s was on copper, while the tariff on the consistently biggest export – bar iron – was removed in 1857.

Just as in Denmark, the reason why export tariffs were kept in place for so long in Sweden was largely fiscal. Between 1783 and 1815, exports made up on average 25 per cent of total customs revenue, and from 1816 to 1841, exports stood for about 15 per cent (but it was markedly lower thereafter, at below two per cent). In particular, the potential removal of the bar iron tariff caused some headaches for lawmakers, as it was still seen as fiscally important in the late 1830s (see the ‘Export tariffs by commodity in Sweden’ section below). The last of the Swedish export tariffs were removed with the tariff revision of 1863, which took effect the following year, meaning that tariffs were put at zero mainly on copper, pig iron, iron ore and some forestry goods of minor importance (Figure 1).

Average Danish and Swedish export tariffs, 1780–1870.

Export tariffs by commodity in Denmark

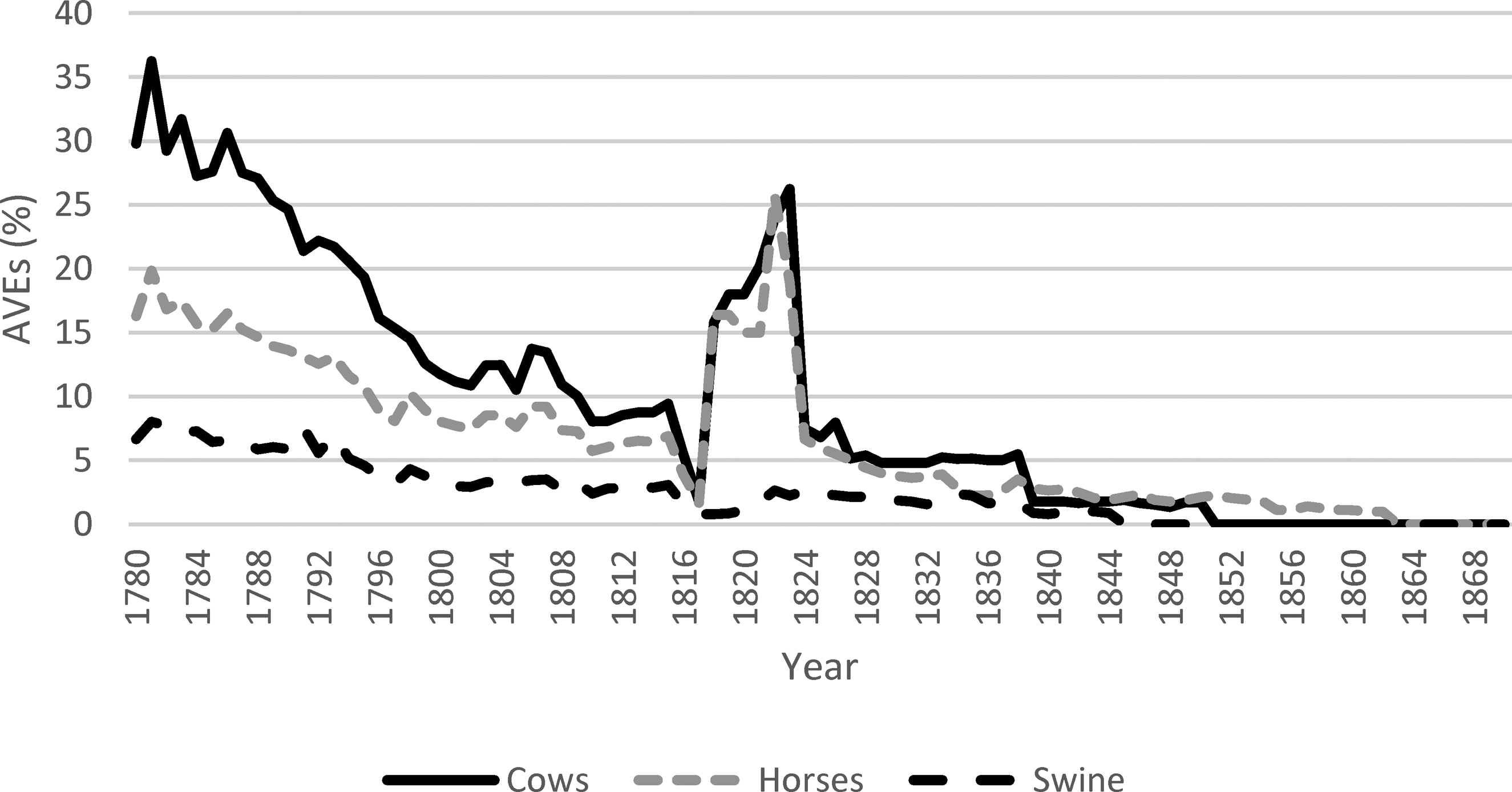

Export duties on, cows (including oxen) and horses were high at the beginning of the period, where the government argued that the high tariffs were a way of limiting exports and maintaining a sufficient level for the domestic market. 53 However, it has also been argued that these tariffs were fiscal in nature, in practice bringing in a large share of the total customs revenue from exports. 54 These commodities would bring in decent amounts of customs revenue after the tariff rates were increased at the end of the Napoleonic Wars. Duties were lowered by a third in 1823, meaning that export revenue dropped. The level of the tariff before 1800 and between 1818 and 1824 could have been high enough to be export-limiting, particularly in relation to the fact that the Danish typically set ‘prohibitive’ export duties at 24 per cent ad valorem before 1797 (Figure 2).

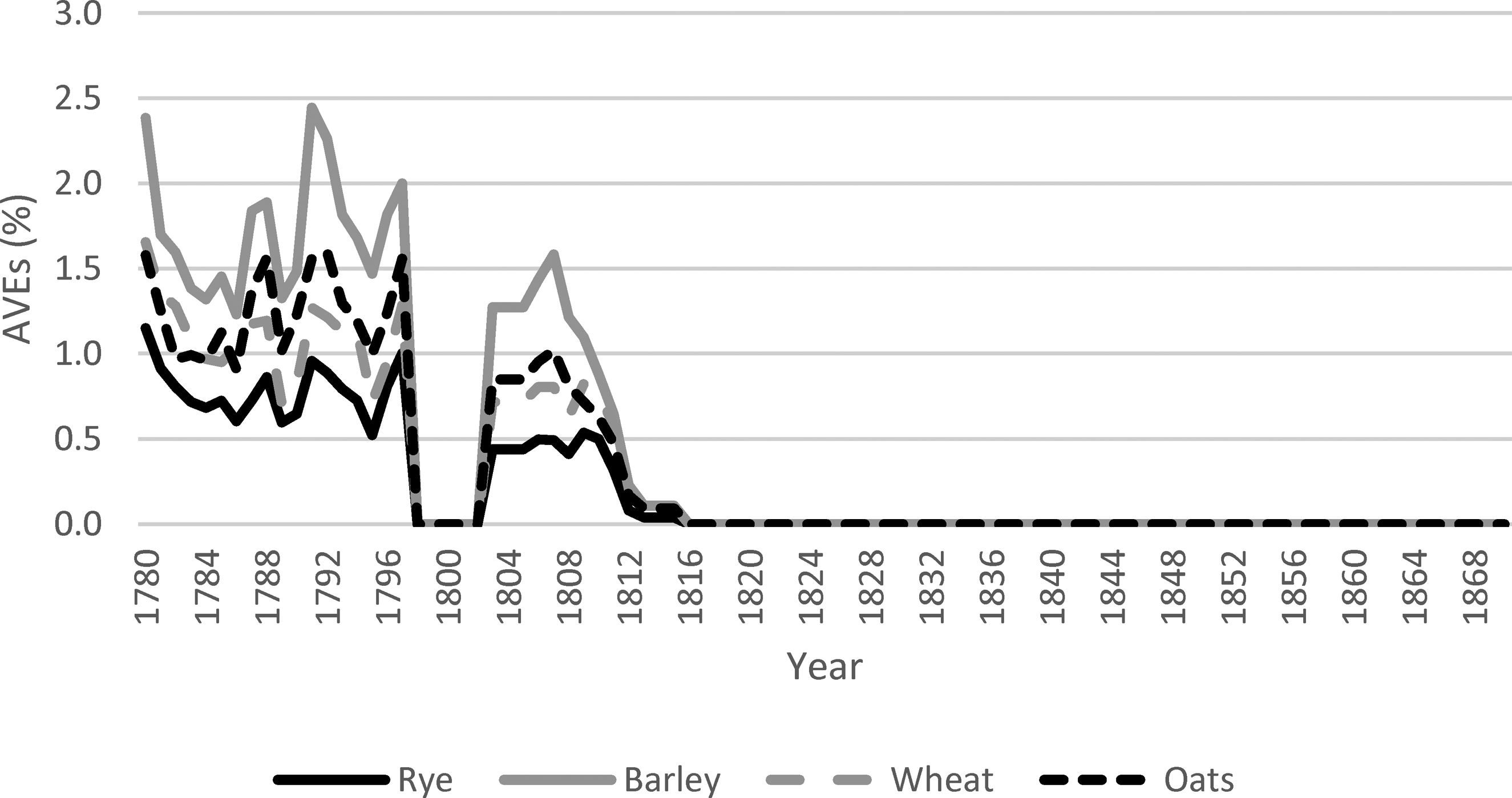

Grain export tariffs were strictly fiscal throughout the period, at no more than 2.5% ad valorem at any time. They were set at zero in 1797, but were reinstated with the onset of the Napoleonic Wars, although they quickly lost their meaning due to rampant inflation with quickly increasing grain prices. 55 After the Wars, they were completely removed once again, partly as a government package to alleviate agricultural recession; they were not reintroduced during the period of this study (Figure 3). 56

Danish export tariffs on live animals, 1780–1870.

Danish export tariffs on grains, 1780–1870.

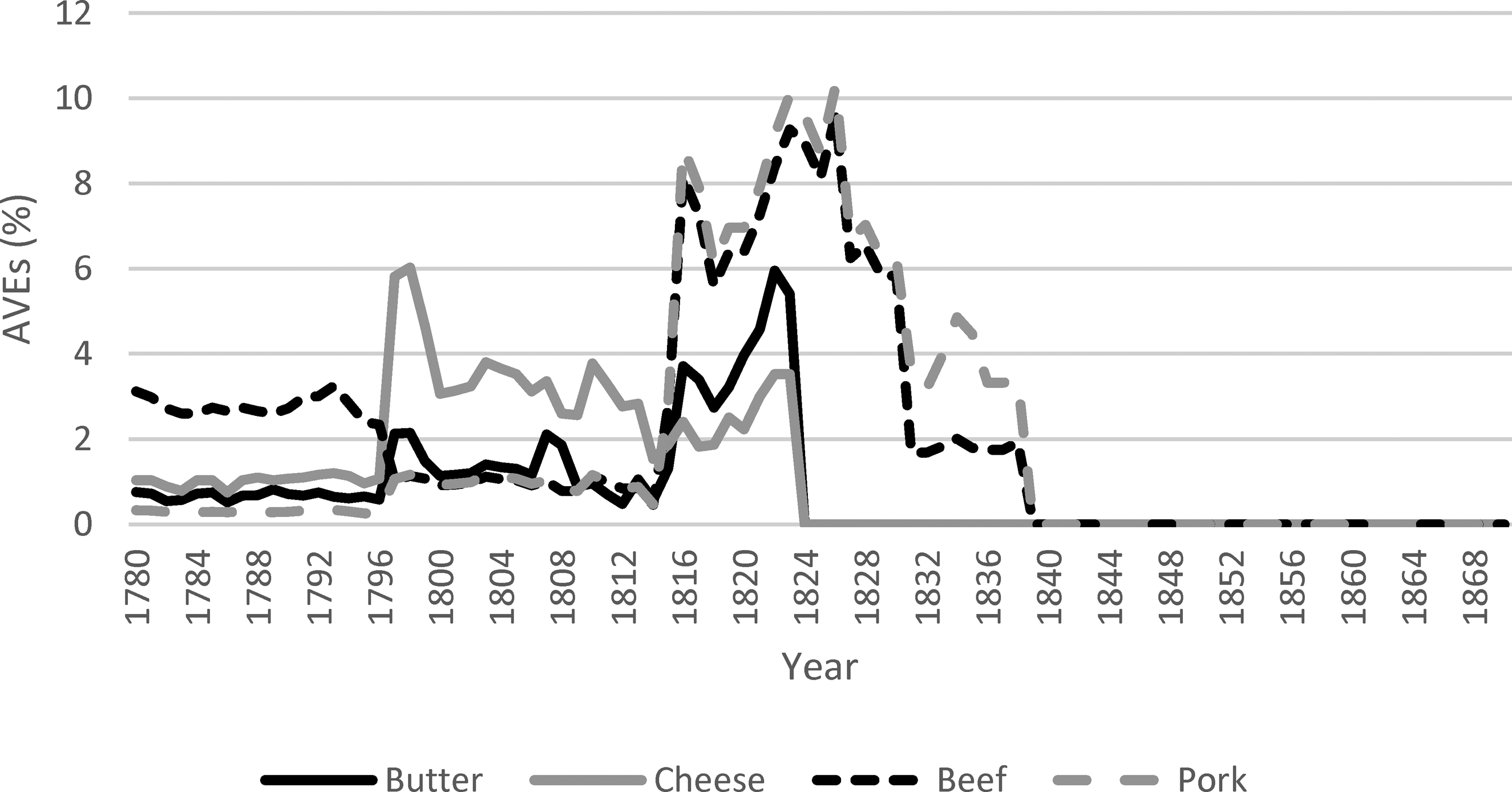

For the other agricultural goods – dairy and meat – the overall picture varies between the individual goods over time. The cheese tariff was increased in 1797 but still kept at a moderate level. The duties on beef and pork, and butter to some extent, were raised quite markedly in 1816 and remained at close to 10 per cent for the next decade. Dairy tariffs were then removed in 1824, while the meat tariffs were kept at low levels until the tariff revision of 1838 (Figure 4).

Danish export tariffs on dairy and meat, 1780–1870.

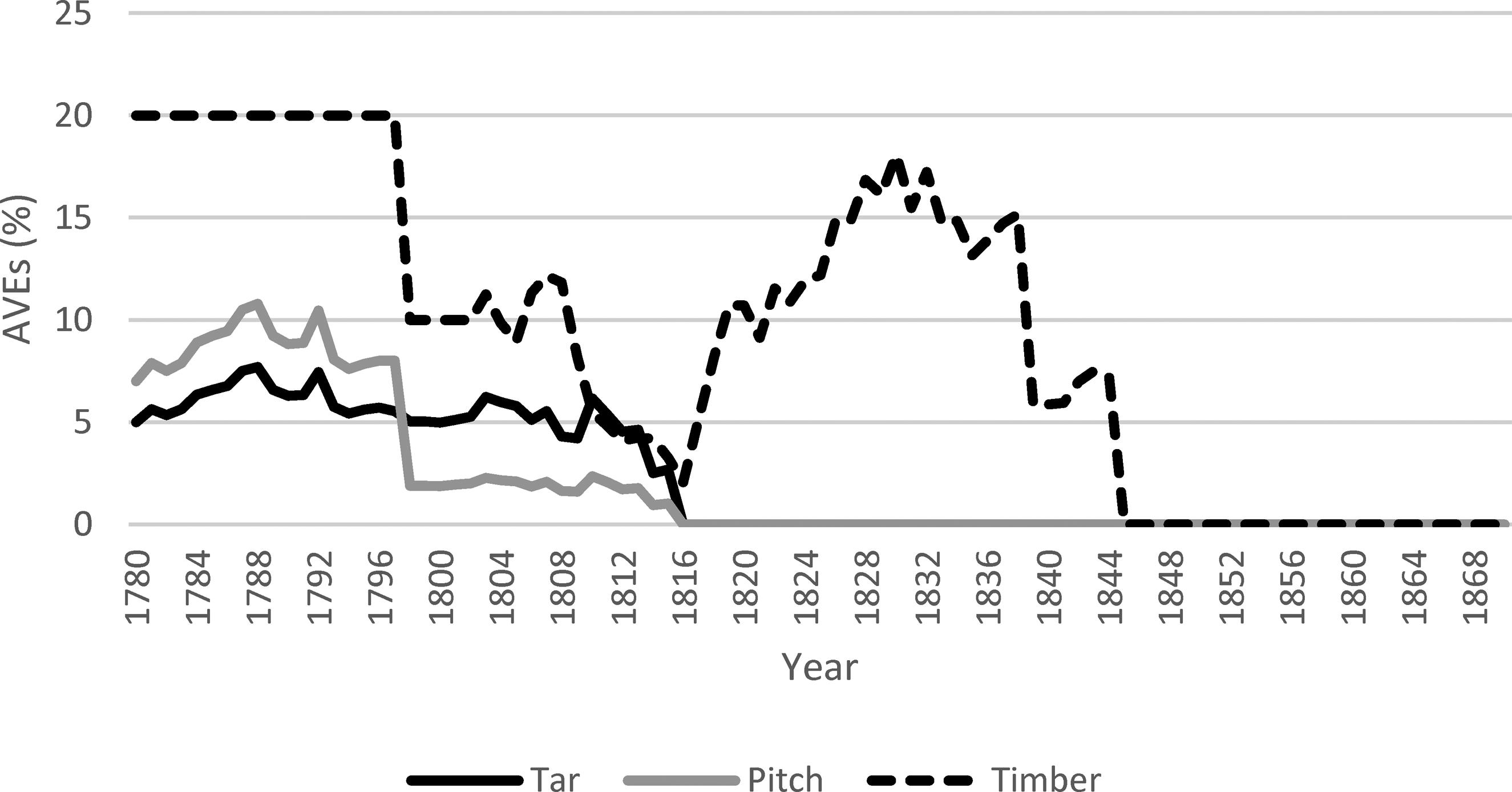

Forestry commodities (especially timber) were mostly exported from Norway before 1814. 57 This tariff was rather high before the revision of 1797, which cut it in half. The duty remained in place up until the tariff law of 1844, and was at a moderately high level before the revision of 1838. Tar and pitch were minor export commodities, where the pitch tariff was similarly cut in half in 1797. Both duties were then removed in 1816 (Figure 5).

Danish export tariffs on forestry goods, 1780–1870.

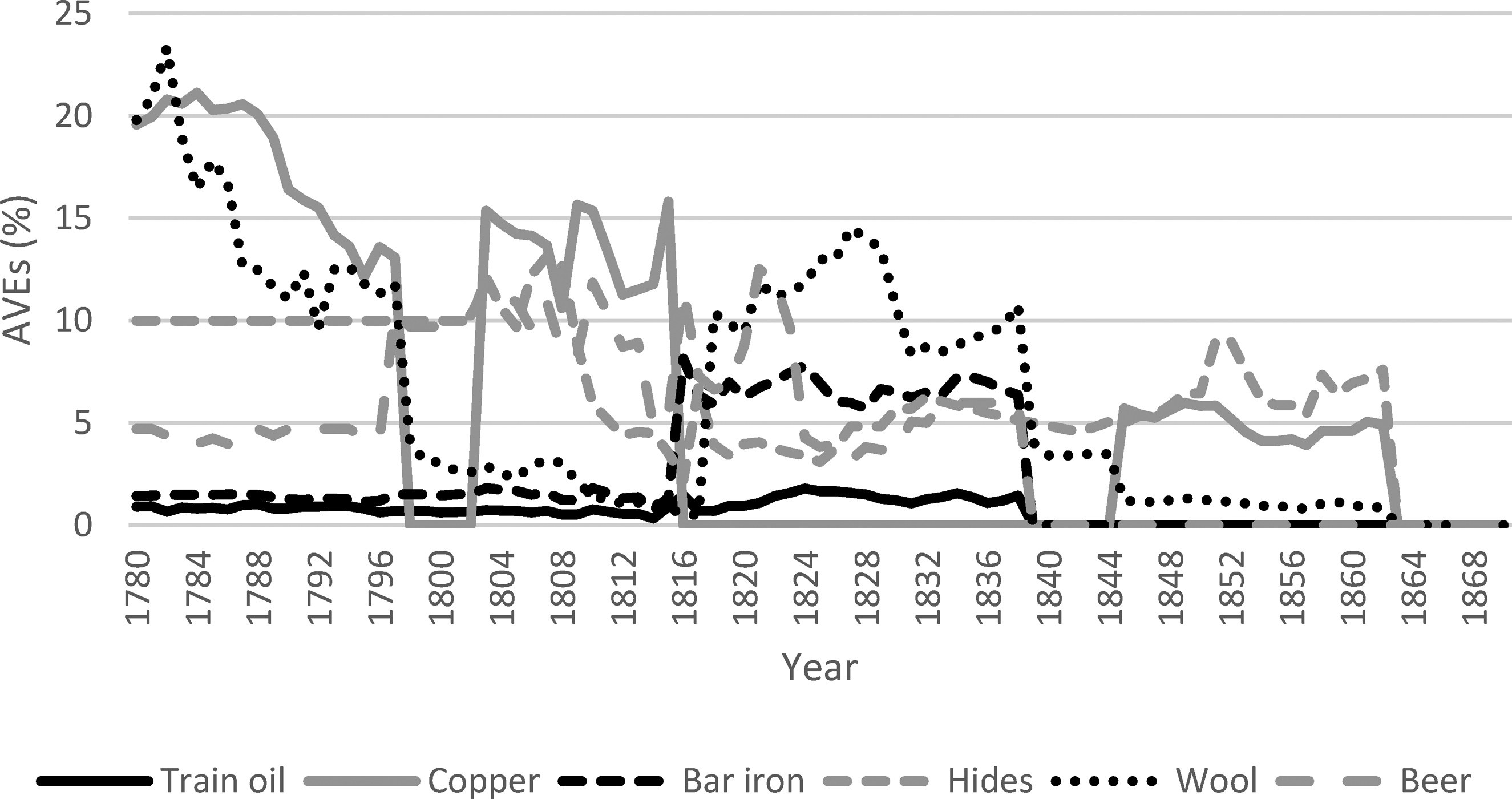

Export duties on relatively large export commodities such as hides and wool were kept up until 1863, although at moderately low rates before they were removed, particularly for the latter. Having high export volumes, these two commodities also brought in a fair amount of customs revenue. Together with livestock, they were the two most fiscally important exports during the first half of the nineteenth century. A perceived revenue need has been deemed as a motive for these duties being only completely removed relatively late in the period. 58 Bar iron was an important export only during the Denmark-Norway era before 1814 before 1814, which makes the increase in the tariff in 1816 somewhat confusing. Some amounts of train oil were also exported from Iceland and Greenland (Figure 6).

Danish export tariffs on miscellaneous goods, 1780–1870.

Export tariffs by commodity in Sweden

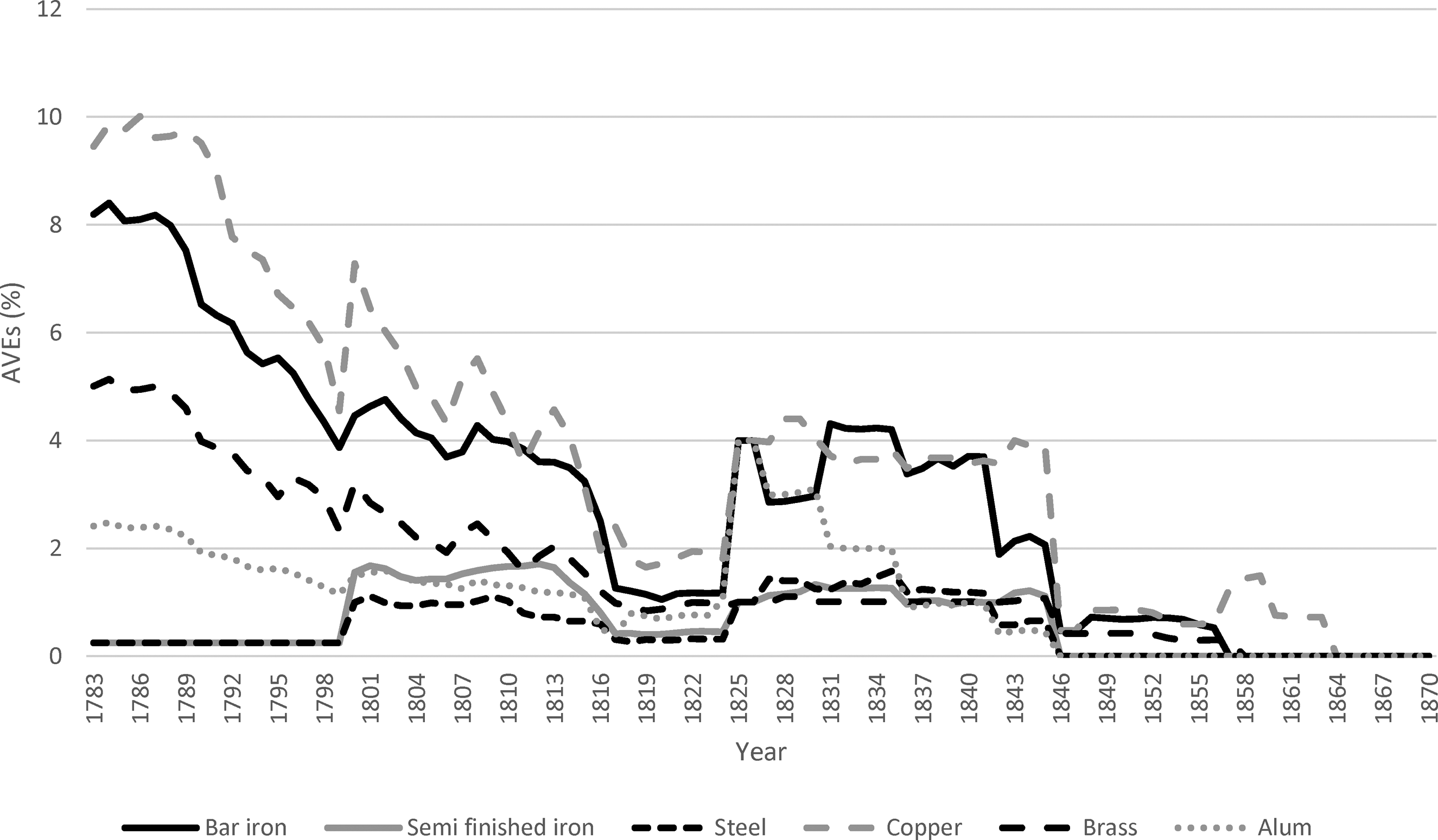

Because of a higher degree of export concentration and a more simplified general export structure, Swedish export duties can more easily be divided into three main categories: iron and other metals, grains and forestry. First, bar iron was a large enough export commodity to make up a relatively large share of the total customs revenue by itself. This figure was close to 20 per cent before 1800, but even when the duty was cut in 1816, it made up close to ten per cent. Even as late as the 1830s, bar iron brought in about half a million Swedish krona in revenue – close to 10 per cent of the total customs revenue. There were several debates in parliament and the government throughout the period on how to deal with the conflict between fiscal concerns and export promotion – mostly concerning bar iron as the single largest export item. This was the case in 1782, when the tariff commission preparing the new duties voiced the possibility of lowering the bar iron export tax in order to be able to better compete with the cheaper Russian bar iron in the British market, but it quickly came to the conclusion that the subsequent loss of state income that this would entail would not be acceptable. 59 When the tariff was lowered in 1816, the loss of revenue had to be compensated for by the increased taxation of ‘luxury’ imports (such as sugar, coffee and wine). Even as late as 1839, when there were renewed debates on the removal of the bar iron export duty, fiscal concerns were raised as a reason to keep the tariff at least at a low revenue-creating level. 60 The copper export tax was relatively high before 1800, but was never singled out by lawmakers as particularly important. For the rest of the period, metal tariffs were kept at low non-distortionary levels, at below four per cent ad valorem (Figure 7).

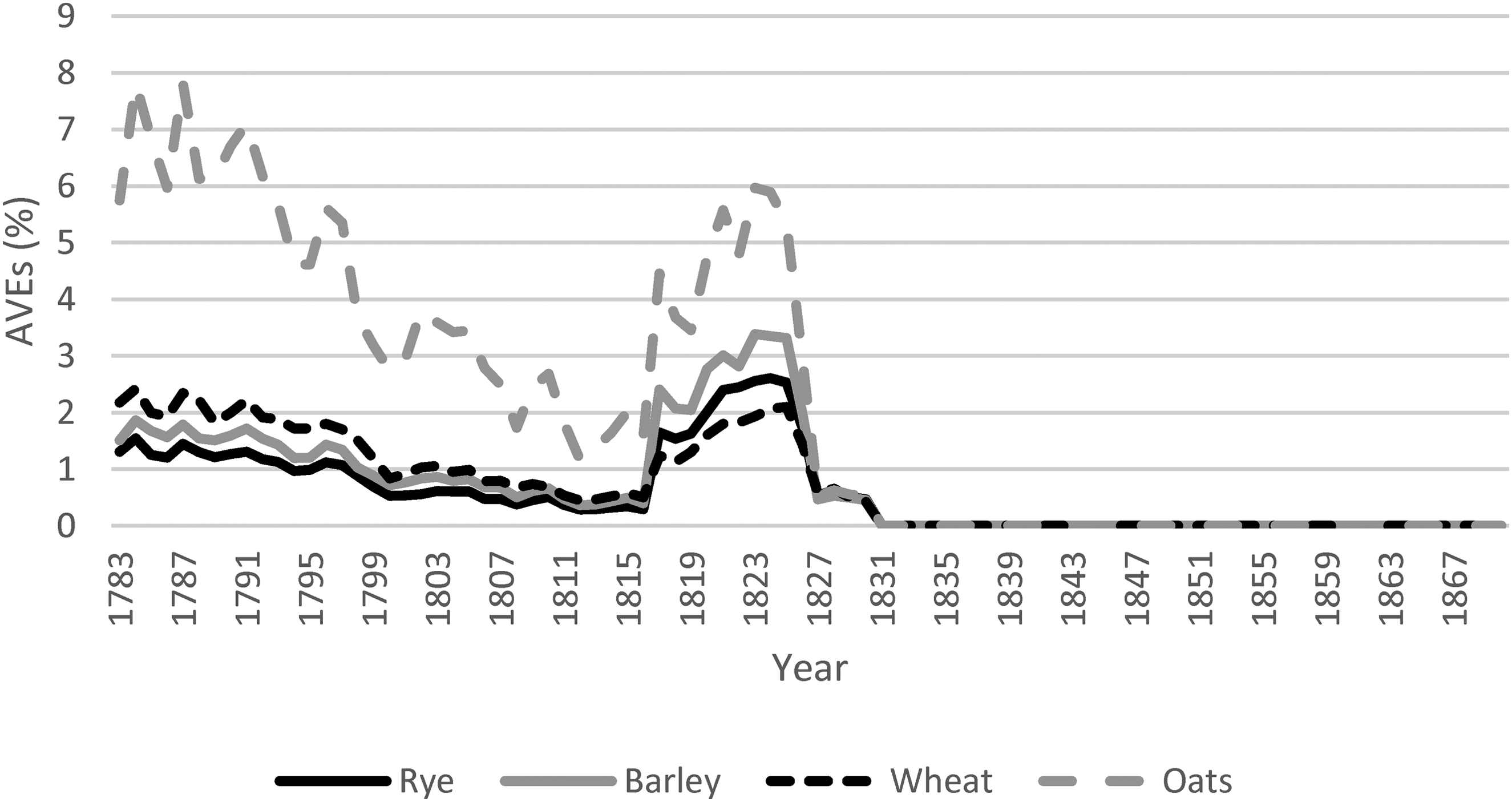

Similarly to the Danish situation, Sweden taxed its grain exports at low rates during most of the period. Oats carried a higher tariff in practice because lawmakers did not adjust the nominal rate to account for a lower commodity price compared to other grains. Increasing prices lowered the rates before 1815, while they were raised in the first post-war revision of 1816. Swedish grain exports experienced a modest increase towards the end of the 1820s, after which the duties were first cut in 1826 and then completely removed in the 1830 revision (Figure 8).

Swedish export tariffs on metals, 1783–1870.

Swedish export tariffs on grains, 1783–1870.

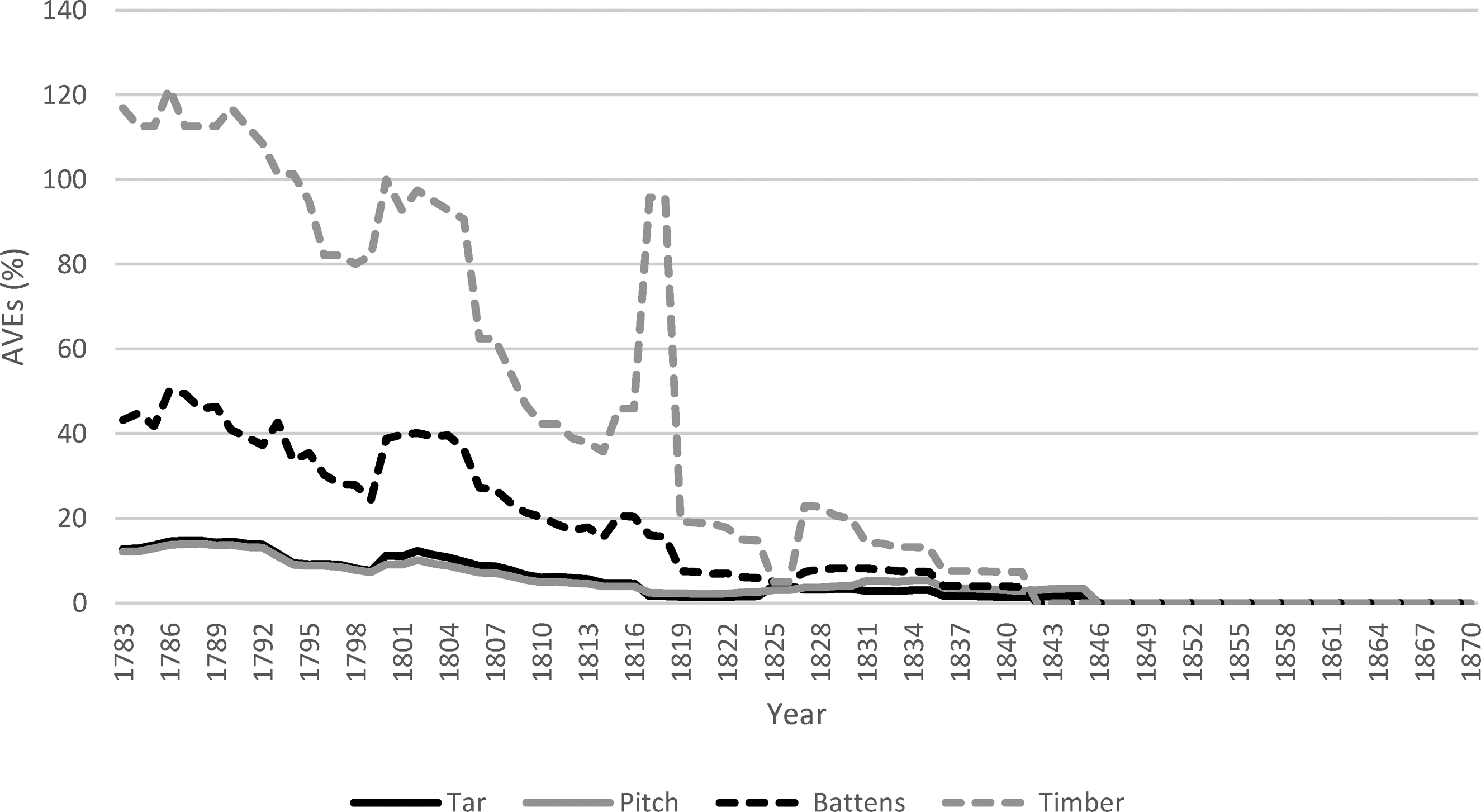

Swedish export duties on forestry goods were very high before the Napoleonic Wars, particularly on timber, at around 100 per cent ad valorem, but also on battens, at between 30 and 40 per cent ad valorem. The duties on tar and pitch were lower but still relatively high compared to some other goods, at between 10 and 15 per cent ad valorem. According to Högberg, forestry export taxes were high enough to have had a detrimental effect on export volumes. 61 Reductions were especially made to the rates on battens and timber in 1816, when the government argued that the change would yield an increase in exports ‘without depleting the forests’. 62 The duties put in place for forestry commodities were a type of quantitative restriction in order to keep domestic supplies steady. 63 These arguments were hence similar to those made in Denmark regarding the export of livestock. The change in 1816 came about after export interests, mainly from the forestry and metallurgy sectors, had lobbied the government for a cut in tariffs, arguing that they had suffered from the drop in exports during the Napoleonic Wars and that their tariff burden was too high. Duties on timber were still at close to 20 per cent by 1830, and so were cut further in three steps in 1830, 1835 and 1841. Some revenue was created by forestry exports, but it was still moderate compared to that from bar iron. Tar and pitch decreased in importance as exports with the resumption of peace after the Napoleonic Wars and as a result of the loss of Finland, which had made up a significant share of this export market, and so the government tried to promote exports with lower duties in 1816 (Figure 9).

Swedish export tariffs on forestry goods, 1783–1870.

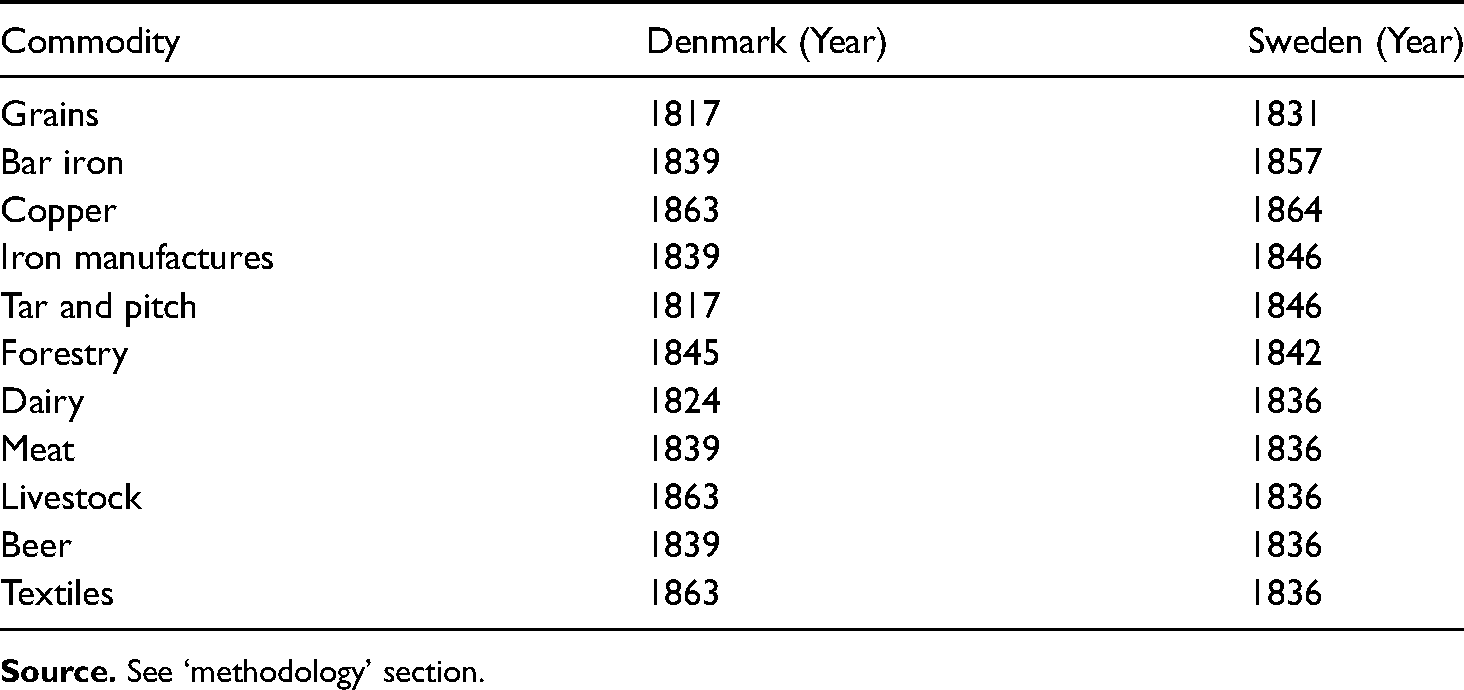

This section ends with a comparison of when export taxes were removed in the two countries. In general, Denmark was earlier in removing duties, which was partly a result of the revision of 1797, which has been deemed radical relative to the Swedish trade policy of the time. 64 The share of duty-free exports was also higher in Denmark at an earlier stage than in Sweden (see also Table 1). Then, after about 1836, the countries look more similar, with gradual removals across the ensuing tariff laws. In both countries, large exports that were considered fiscally important remained taxed for the longest – livestock, hides and wool in Denmark, and bar iron in Sweden (Table 2).

Year of removal of export tariffs.

Conclusions

Denmark and Sweden chose to tax their own exports, to varying degree and with varying intensity, all the way up until the 1860s. In both countries, these duties were removed in several steps from 1817 to 1863. In general, Sweden was later in making exports completely duty-free; before 1826, all exports were taxed at some level. Duty-free exports made up the majority of goods only from 1836. Most commodities were taxed at low, ‘non-distortionary’ levels at around five per cent ad valorem, but some tariffs were set higher, either for the explicit reason of keeping export volumes down and maintaining a sufficient supply for domestic consumption or refining. Other goods were taxed mainly for fiscal reasons, and these were also some of the goods that would remain under a tariff for the longest time, such as with bar iron in Sweden and hides and wool in Denmark. While exports were fiscally more important in Sweden, it was also argued in Denmark that removing export duties would create revenue difficulties.

It is more difficult to see any major distinction between raw materials and goods of higher refinement, since the export baskets of both countries were still dominated by raw materials during this period. 65 In Sweden, iron manufactures (and semi-finished iron) and more finished textiles were taxed at low rates before they were made duty-free, but so were certain raw materials, such as brass and grains. Hence, we cannot see a consistent mercantilist policy of wanting to keep raw materials in the home country while promoting more industrial exports.

While this article has not been primarily concerned with the connection between tariffs and export growth, we can note that the removal of duties on what would later become some of the largest exports occurred fairly early – such as with grains in 1797 and dairy in 1823 in Denmark, and grains in 1830 and forestry in 1841 in Sweden – hence preceding export growth in both countries. 66 The question is, of course, whether exports grew once the tariffs were reduced or when they were removed completely.

Taxes on exports occupy an interesting place in trade policy, particularly in a mercantilist setting where export surpluses were always desirable. In an environment and at a time where states often found themselves cash-strapped and means of taxation were generally lacking, fiscal concerns would often prevail when it came to regulating trade – even exports. Even when Denmark moved to a more free-trade-oriented regime after 1797, revenue needs concerning export commodities still existed, although to a lesser degree. Fiscal motives would, in effect, delay export liberalization in both Denmark and Sweden, although with different timings. This highlights an interesting potential political conflict in trade taxation between filling the state coffers and wanting to promote export development. Governments would often choose the former, but whether export taxes actually hindered export growth is a question for further research.

Footnotes

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The article was written with the financial support of the Jan Wallander and Tom Hedelius foundation, project number P2016:0135.

Notes

Author biography

Henric Häggqvist graduated from Uppsala university in 2008 with a master's degree in social science, with political science as major. Started the PhD program in economic history in September 2011 after an opportunity to participate in a research project revolving around economic integration in times of war and de-globalization, particularly during the French Revolutionary War and the Napoleonic Wars. In December 2015, he defended his dissertation which treated the issue of Swedish trade policy, and the structure of tariffs and foreign trade between 1780 and 1830. Since 2016, he is working as post-doc researcher at the department of Economic History at Uppsala University.