Abstract

Consumer inclusion efforts are expanding as firms audit data for bias, platforms revise fairness metrics, and policymakers strengthen protections for vulnerable populations. Across these efforts, an assumption guides vulnerability identification: Risk accumulates by adding demographic traits. Race, gender, age, disability, education, and income are treated as separable categories whose effects stack. This logic is intuitive but inadequate.

Consumer vulnerability does not arise in neat layers. It emerges when people collide with how systems classify, surveil, or gatekeep—harms that escape detection because they do not align with single demographic markers. They appear in gaps between categories, where risk is patterned yet statistically overlooked. This gap between how vulnerability is modeled and how it is lived has consequences for inclusion efforts. For example, fairness audits may certify an overall system as unbiased even as certain consumers continue to systematically face higher exposure to discrimination and denial or delay. Vulnerability becomes reorganized, not reduced.

Intersectionality offers language for naming this problem, yet it is sometimes applied through flawed logic that obscures patterned harm. In this commentary, we argue that consumer vulnerability is nonadditive—it is not the cumulative sum of identity-based risks, but an emergent condition produced at the intersection of identity, power, and market design.

Vulnerability

Research on consumer vulnerability began alongside early interest in consumer behavior and public policy and marketing (Andreasen 1975). Many subpopulations were considered “vulnerable” because of marketplace restriction or discrimination due to race, gender, or social class (e.g., Bone, Christensen, and Williams 2014). Other literature took for granted that certain consumers were vulnerable (e.g., children, older individuals). However, recently the idea of experienced or eventual harm entered the scholarly vernacular (Hill and Sharma 2020). This perspective defies marketing's assumption that people enter exchanges for mutual benefit, instead allowing for negative repercussions and harm mitigation strategies. For example, a consumer living in a food desert must buy food from among available unhealthy offerings, negotiating the least objectionable alternative.

To orient the field's understanding of vulnerability, consumption adequacy was developed (Martin and Hill 2012). It suggests that consumers find it impossible to survive or thrive in their material environments without access to essential goods and services: healthful food and drink, protective and culturally appropriate clothing, safe and sufficient housing, preventative and remedial health care, and opportunities for growth. Establishing these requirements revealed that psychological mechanisms supporting consumer well-being (e.g., agency, self-regulation) operate differently under vulnerability. This finding led to two concerns: (1) How do consumers manage multiple consumption inadequacies across different domains? and (2) How is vulnerability different when multiple vulnerability characteristics occur simultaneously? Intersectionality offers a paradigm to address these concerns.

Intersectionality in Marketing

Intersectionality in marketing rests on three commitments: (1) social categories are overlapping rather than independent; (2) lived experiences at these intersections are qualitatively distinct, not merely intensified; and (3) systems of power structure how these identities become consequential (Gopaldas 2013; Uduehi, Saint Clair, and Crabbe 2025). These components must be understood together. For instance, a higher-income consumer can pay to escape vulnerabilities caused by disasters such as climate or conflict. Not all refugees are poor. Yet the new status as a refugee woman may become the dominant vulnerability marker in labor, health, or digital markets regardless of class.

Intersectionality is not simply about having more identities; it is about how power organizes risk, visibility, and access differently at different intersections. These intersectional power dynamics are the perpetual backdrop for marketplace interactions. Yet marketing typically operationalizes intersectionality through additive proxies, coding categories, interacting variables, or tallying disadvantages. Additive identity logic thereby displaces traditional single-identity inclusion. But when intersectionality is reduced to a counting exercise, vulnerability is transformed from an emergent structural condition into a cumulative sum of traits. The result is not just theoretical imprecision; it is systematic misdiagnosis.

Beyond Arithmetic: Emergent Vulnerabilities

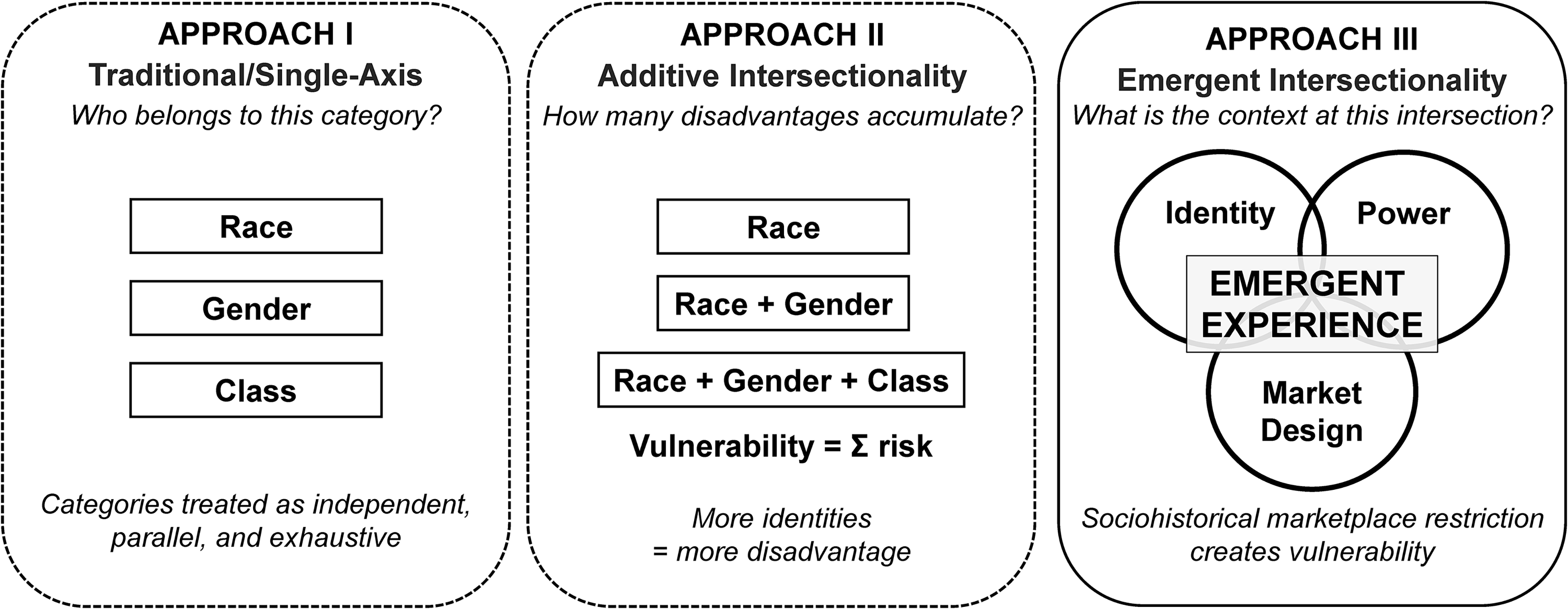

Intersectional scholarship has broadened attention to compounded disadvantage beyond traditional single-identity inclusion efforts and mechanistic studies of power and vulnerability that abstract away from identity and lived experience, but additive logic still dominates. A model of emergent vulnerabilities is therefore critical to advance intersectional inclusion (Figure 1).

Three Approaches to Consumer Vulnerability: From Single-Axis to Emergent Intersectionality.

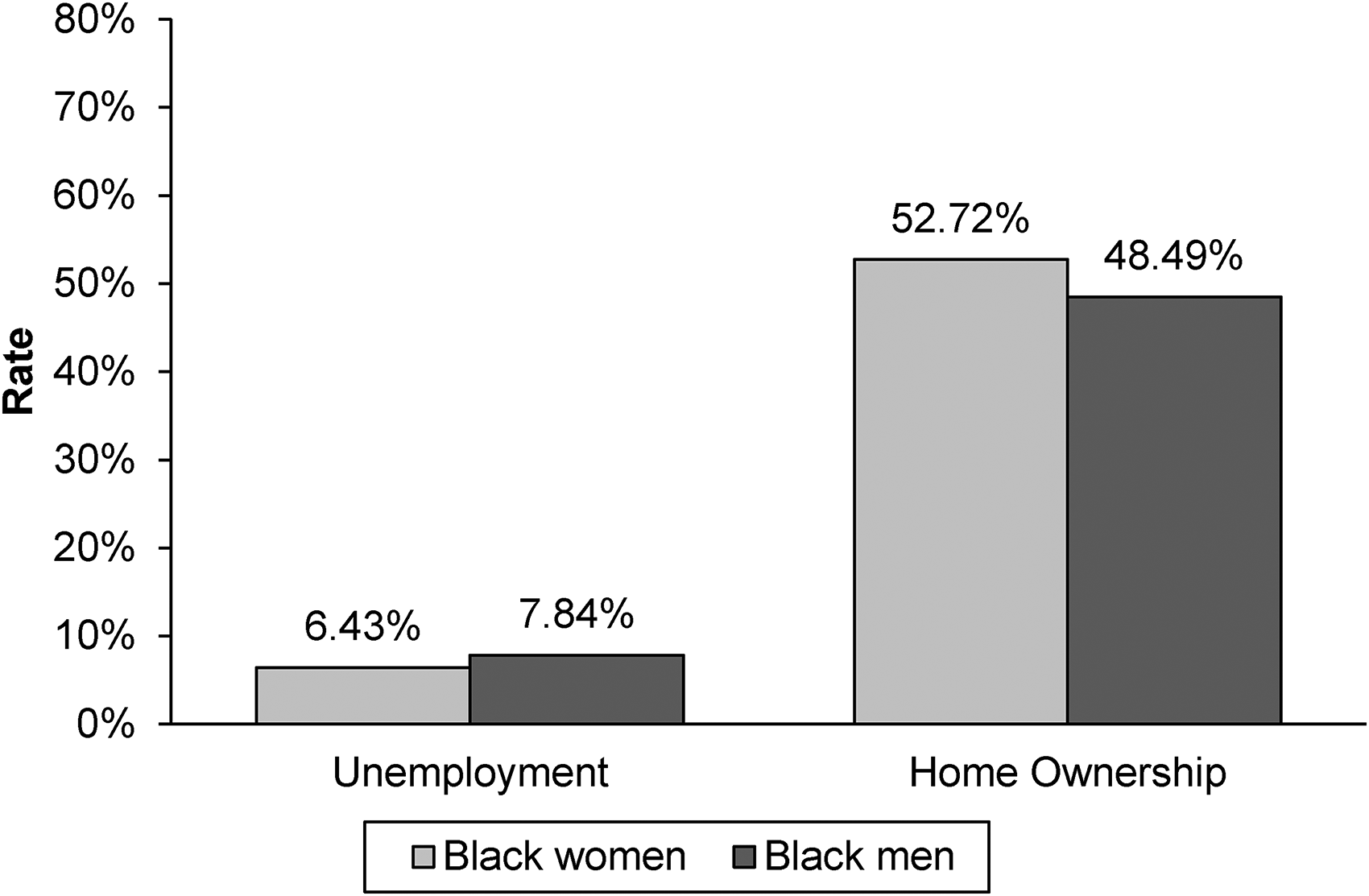

Consider that women and Black people historically face barriers in the United States’ employment and housing markets (Pager and Shepherd 2008), yet 2023 census data shows that Black men have higher rates of unemployment (7.84%) and lower homeownership (48.49%) than Black women (6.43% and 52.72%). This defies an intuitive additive race + gender model and requires holistic theory situated in sociohistorical context (e.g., Uduehi, Saint Clair, and Crabbe 2025).

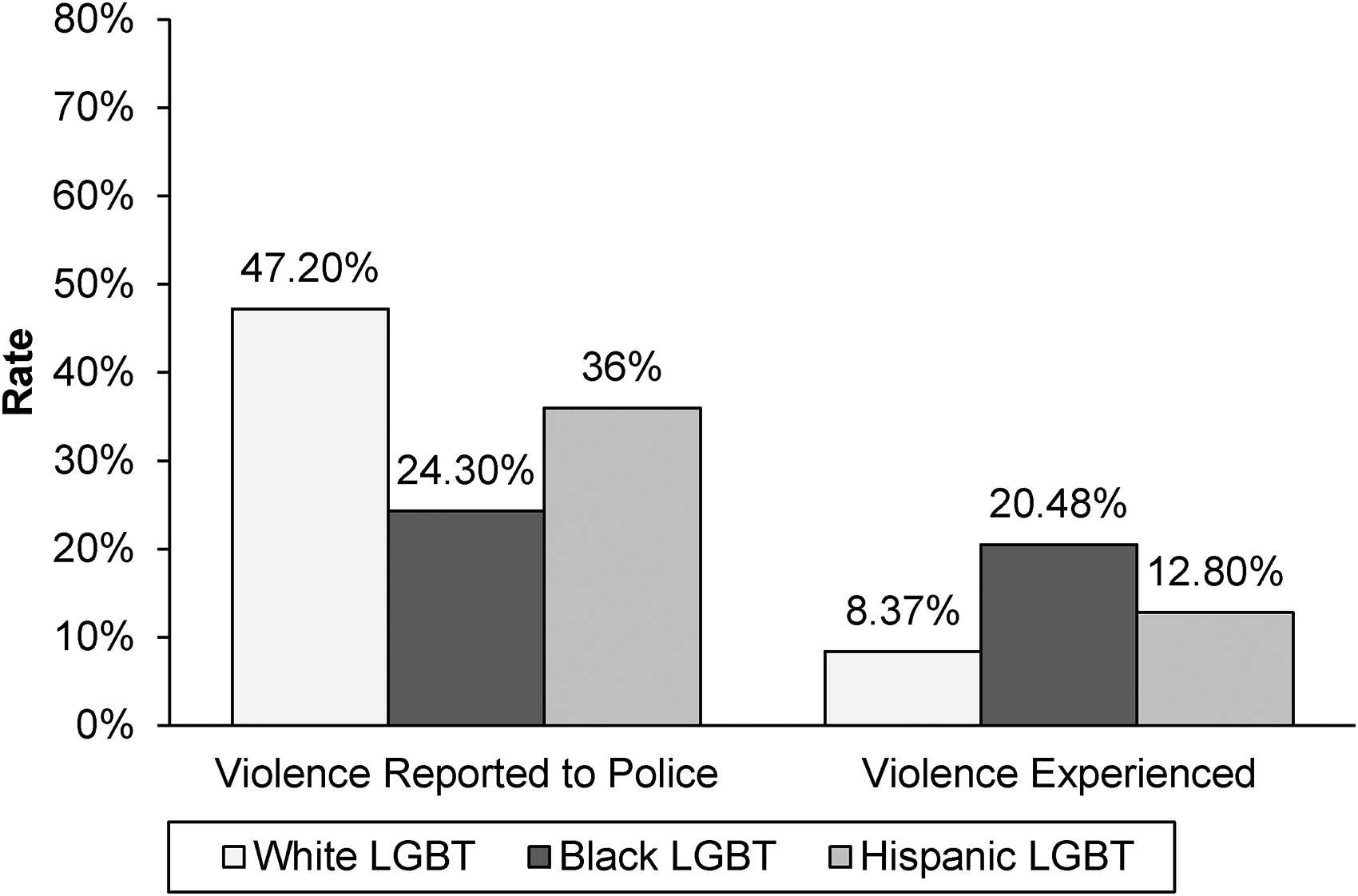

A second example concerns sexual minority victimization by race. Surveys show that White LGBT respondents are 94% more likely to report incidents of violent victimization to police than Black LGBT respondents, and they more readily identify incidents as hate crimes (Flores et al. 2023). Thus, policy interventions that reduce reports by White LGBT people to rates similar to other groups might be considered successful. However, Black LGBT people actually experience the highest rates of violent victimization (20.48%), followed by Hispanic (12.8%) and White (8.37%) LGBT people (Meyer and Flores 2025). These divergent patterns reflect how visibility regimes, historical relationships with law enforcement (Ritchie 2017), and institutional trust shape both exposure to violence and engagement with formal reporting systems—dynamics of lived experience that cannot be understood through simple addition of identity categories.

Together, these cases (Figures 2 and 3) show that intersectional vulnerability is emergent, produced through interactions between identity and historically embedded systems of power that must be interrogated to transform theory and practice. Treating intersectionality as arithmetic recasts structural inequality as individual difference, reproducing the exclusions that inclusion efforts seek to undo.

Additive Inadequacy: Black Men's and Black Women's Unemployment and Homeownership Rates Defy an Additive Model.

Systemic Mismeasurement: Black LGBT People Have Lowest Rate of Violence Reported but Highest Rate of Violence Experienced.

Implications of Emergent Intersectional Vulnerability

For research, emergent intersectional vulnerability implies relying more on qualitative exploration of lived experience to build theory, which in turn can inform testable hypotheses and interventions for intersectional inclusion. This contrasts with extant approaches that might predict interactions between identity categories (e.g., race and sexuality) based on observed patterns of additive categorical differences (e.g., White LGBT vs. Black LGBT police reporting). Moving from interaction-first to centering lived experience is critical.

For policy and practice, it is important to recognize that inclusion metrics may appear to improve for some categories even as other intersectional disparities persist. For instance, a firm may advance gender diversity while reproducing racial exclusion. A platform may expand access for low-income users while intensifying surveillance practices that burden racially minoritized groups. From an additive perspective, these appear as trade-offs; from an intersectional view, they are regimes of protection and exposure. The data must indeed often be subsegmented and persistent gaps must be highlighted and qualitatively explored.

Finally, we highlight the necessity of “seat at the table” approaches to intersectional inclusion. Researchers, policymakers, managers, and consumers must collaborate authentically and humbly with a diverse array of consumers in the target (intersectional) populations they serve, from conception to execution. Race, gender, and class are a good starting point (Gopaldas 2013), and frameworks like GEARS or ADDRESSING help identify other identities as the context demands (Uduehi, Saint Clair, and Crabbe 2025). This will ensure lived experience is honored. The saying popularized in the disability movement captures the sentiment: “Nothing about us without us.”

Conclusion

Consumer vulnerability is not the property of individuals, nor is it a sum of isolated disadvantages. It is produced where identity and power meet market design. When vulnerability is treated as cumulative, inclusion becomes partial by design. Systems optimized to detect single-axis disparities may appear fair while reorganizing harm into less visible forms. An intersectional approach does not require abandoning demographics. It requires recognizing what those categories cannot reveal. It urges all to examine not only who is represented but also how exposure and protection are distributed across markets and time. If vulnerability is intersectional, then inclusion cannot be additive. It must be structural.

Footnotes

Joint Editors in Chief

Jeremy Kees and Beth Vallen

Special Issue Editors

Samantha N.N. Cross, Rebeca Perren, Eileen Fischer, and Anders Gustafsson

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Data Availability

The data referenced in this article are from publicly available sources (U.S. Census Bureau, research articles).