Abstract

International customers are increasingly exposed to dynamic currency conversion, that is, the option during checkout to proceed with a transaction in the home currency instead of a foreign currency. As conversion markups can be sizable, it is relevant to gain insight into how distinct groups of customers react at point-of-sale terminals to different markups and different ways of presenting information. The authors build on research on effort–accuracy trade-offs to theorize how international customers with different levels of financial literacy react to conversion markups, different degrees of information transparency, and default settings. The authors find that financial literacy moderates the effect of markups, information, and defaults, and they design an intervention that eradicates the effect of financial literacy on dynamic currency conversion usage. The results contribute to our understanding of how customers with different levels of financial literacy respond to conversion markups, to public policies that are intended to protect customer interests, and to evil defaults used by commercial parties that seek to steer customers to noneconomical options. The authors discuss the implications of these findings for public policy making and research.

Many customers conduct payments in foreign currencies, for example, when using debit or credit cards while traveling or when conducting purchases in international online stores. This phenomenon is not trivial: U.S. tourists spent USD 57 billion abroad in 2021 (Statista 2022), and European Union (EU) customers made 20% of their online purchases outside the EU (Eurostat 2022). Traditionally, customers proceed with these transactions in foreign currency. In this case, the card issuer (for example, the customer's home bank) transfers foreign currency to the acquirer (the retailer's bank), converts the amount into the customer's home currency, and charges the customer accordingly. Nowadays, retailers and ATMs can additionally display the transaction price in the customer's home currency. Paying in home currency is generally known as dynamic currency conversion (DCC, also known as currency choice). In this case, a customer authorizes a DCC service provider (e.g., Adyen, Fexco) to execute the currency conversion. This DCC service provider lets the retailer or ATM owner share in currency conversion revenues (Bouyon and Krause 2018; Paysquare n.d.). According to Worldnet (2017), the extra revenues for retailers typically equal 1% of the value of the transaction. Figure 1 shows two stylized real-world examples of how DCC is presented to customers at different locations. Panel A shows a point-of-sale terminal in Switzerland, and Panel B shows an ATM in Hungary. In both cases, the terminal provides the option to pay in foreign or in home currency. When offered this choice in physical stores, online, or at ATMs, approximately 50% to 60% of international customers opt for DCC (De Groen, Kilhoffer, and Musmeci 2018; Paysquare n.d.). The benefits of DCC for customers include certainty about the applied exchange rate and instant clarity regarding the price in the home currency. However, these benefits come at a cost. For example, the two DCC examples in Figure 1 comprise offered exchange rates that include conversion markups of, respectively, 5% and 8%. Such markups are no exception. Forbrukerrådet (2017) reports a maximum DCC markup, on top of the official Visa rates, of 12.4% and an average markup of 7.6% (also see Allix and Aliyev 2017) and concludes that customers were worse off in 99.7% of the cases.

Examples of DCC for a Eurozone Traveler.

Why do half of international customers opt for DCC even though conversion via their home bank is cheaper in almost all cases? When one option is clearly more economical (i.e., conversion via the home bank generally comes with substantially lower costs), making the right decision should be easy (Tversky and Shafir 1992). In fact, that the most economical option should be selected under such conditions is a widely accepted principle of rational decision making (Payne, Bettman, and Johnson 1992). However, this principle can be violated if the dominance of the most economical option is masked by the way the information is presented (Tversky and Kahneman 1986). If we examine the information presentation during checkouts (see Figure 1), we see that the checkout process is nontransparent. For example, information about the markup applied to the DCC exchange rate is not provided, and the exchange rate at which the home bank conducts the transaction is missing. Selecting the most economical option thus requires that customers recall (or look up) the market exchange rate and home bank conversion fees and calculate the difference between the two offers.

Because of nontransparent information provision, DCC service providers are “able to extract substantial rents from cross-currency consumers” (Ewerhart and Li 2020, p. 27), leading to consumer welfare losses. Given these welfare implications, DCC-specific regulations that protect international customers and stimulate cross-border activities may be appropriate. The European Commission has been at the forefront of developing such regulations. Initial regulations (EU Directive No. 2015/2366) dictated that providers of DCC display the exchange rate applied for conversion during checkout. Yet, in 2017 the European Commission noted that it is still “very difficult for consumers to know which currency conversion offer is the most advantageous” (European Commission 2017, p. 6). Currently, a new regulation (EU Regulation No. 2021/1230) forces providers of DCC to display the markup applied for conversion. The EU continues to evaluate the effectiveness of DCC regulations and seeks to implement additional measures if necessary, but acknowledges that sufficient evidence to assess the current regulation is currently lacking. In addition, no controlled empirical research shows under which conditions international customers systematically select the noneconomical DCC option. 1 The aim of our research is to resolve this gap and to provide a checkout design that protects customers against costly currency conversions.

To explain under which conditions international customers are likely to accept a DCC offer, we build on research on effort–accuracy trade-offs (see, e.g., Bettman, Johnson, and Payne 1990; Johnson and Payne 1985; Payne, Bettman, and Johnson 1992). We report the results of two between-subjects experiments conducted on Amazon Mechanical Turk (MTurk). The experimental setup is based on a checkout process at an international airport. We use financial literacy, defined as the stock of financial knowledge related to personal finance and financial products acquired through education and experience and the ability to apply this knowledge (see Hastings, Madrian, and Skimmyhorn 2013; Huston 2010), to capture differences between individuals in terms of processing financial information and making financial calculations (Bettman, Johnson, and Payne 1990). In the first experiment, we mimic established industry practices. We first use a “standard” DCC transaction screen (i.e., as encountered in most countries) and manipulate the DCC markup to gauge how markups affect DCC usage. Thereafter, we make DCC the default option (see Dynamiccurrencyconversion.info 2018) to test whether such a default setting has the potential to decrease customer welfare (default settings that increase firm profits while decreasing customer welfare are also known as “evil defaults”; see Hansen and Jespersen 2013; Thaler 2018). Finally, we build on existing EU regulations (Regulation No. 2021/1230) to test whether and how transparency regarding conversion fees affects DCC usage. In the second experiment, we move beyond the current regulation and create three experimental conditions in which we provide (close to) optimal information. To understand the effectiveness of optimal information provision in practice, we test these conditions with and without evil defaults. By differentiating in all experiments between different levels of financial literacy, we gain insight into the type of customer that is affected by higher markups, evil defaults, and higher levels of information transparency.

The results of Experiment 1 show that customers display heterogeneous responses to DCC markups, evil defaults, and information transparency based on their level of financial literacy. Customers with lower levels of financial literacy are consistently less likely to select the more economical payment option when markups increase and when evil defaults are implemented. In addition, they benefit less from information transparency. In our optimal information treatments (Experiment 2), DCC usage decreases equally for all financial literacy categories, and evil defaults are no longer effective. Together, these results suggest that the high DCC usage rates that we observe in practice (see Allix and Aliyev 2017; Forbrukerrådet 2017; Paysquare n.d.) mainly result from a customer's inability or unwillingness to accurately calculate and compare the costs of both conversion offers. This consumer welfare problem can be resolved by reducing the amount of information that is provided on the transaction screen and by removing the need to make calculations. More specifically, our findings imply that displaying conversion markups as a percentage over the exchange rate (instead of displaying the exchange rate itself) decreases DCC usage among participants. To further prevent the use of noneconomical checkout options, the transaction prices of both checkout options must be presented in the same currency. These insights are important for policy makers given the increasing number of places where international customers are exposed to DCC (e.g., Visa globally allows DCC transactions on ATMs since 2019) and the ongoing evaluation of the current EU regulations. Our results also provide several insights that are relevant for research. For example, we show that information transparency affects how customers assess offers that are denominated in multiple currencies. This finding can be used as a starting point for researchers studying virtual currencies in customer loyalty programs (e.g., Drѐze and Nunes 2004; Wei and Xiao 2015; Wertenbroch, Soman, and Chattopadhyay 2007) to study how different ways of displaying information can be used to promote certain products and services. Our finding that financial literacy mitigates the effect of evil defaults on DCC usage indicates that, depending on the domain-relevant knowledge base, defaults heterogeneously affect decision-making processes. This finding urges scholars to further explore the interplay between knowledge and the modes of decision making that are activated by (evil) defaults (Brignull 2013; Maier and Harr 2020; Miesler et al. 2017).

Theoretical Background

Retailers traditionally advertise and sell products and services in their native currency. Likewise, ATMs traditionally display only the native currency payment option. For international customers, dealing with foreign currencies can pose several challenges. Customers should, for example, know the exchange rate and be able to convert the foreign currency into their home currency (Juric, Lawson, and McLean 2002). To overcome these challenges, retailers and ATM owners have gradually introduced DCC. If we take Macy's in the United States as an example, DCC allows Macy's to offer non-U.S. customers the option to proceed in their home currency at the point-of-sale terminal during checkout. International regulations dictate that Macy's displays the offered exchange rate of the DCC option and that customers can also proceed with the transaction in Macy's native currency (i.e., U.S. dollars). In case the customer opts to proceed in the home currency, the conversion is conducted by the DCC service provider for Macy's (e.g., First Data, Paysquare) for the exchange rate on display. Like physical stores, online stores can add DCC functionality to their checkout process. In addition to being more convenient, DCC reduces the risks for customers (i.e., fluctuations in the exchange rate between the transaction and the handling of that transaction by the customer's home bank) because the exchange rate is guaranteed by the DCC service provider. Therefore, it is preferable for customers to use DCC as long as the DCC markup applied by the provider of DCC does not exceed the conversion fees applied by the home bank.

Although DCC minimizes the difficulties that customers experience in calculating a transaction price in home currency (Juric, Lawson, and McLean 2002), it introduces a new problem by obfuscating DCC conversion fees (Tversky and Kahneman 1986). Because the costs of proceeding with a transaction in home currency are embedded in the offered exchange rate and are not directly visible (see Figure 1), customers need to make an effort (e.g., reading information, recalling or looking up exchange rates, making calculations) to notice any difference in costs between the two payment options (Bettman, Luce, and Payne 1998; Johnson and Payne 1985; Payne, Bettman, and Johnson 1992). Research on currency calculations (e.g., Juric, Lawson, and McLean 2002; Pettigrew et al. 2010; Raghubir, Morwitz, and Santana 2012; Raghubir and Srivastava 2002) has shown that international customers use different currency conversion strategies (exact calculation, simplification, and avoidance) and that these strategies differ in terms of accuracy and effort. Exact calculation is a demanding but accurate approach in which international customers obtain all relevant information and make a precise conversion (mentally or by using a calculator). Simplification strategies include the use of rules of thumb (e.g., first divide by i and then multiply by j) or rounding (e.g., dividing by a whole number that is close to the exchange rate) to calculate offers denoted in different currencies. Simplification strategies are generally less precise, and customers that use these strategies accept a trade-off between accuracy and effort (Juric, Lawson, and McLean 2002; Raghubir, Morwitz, and Santana 2012). Finally, international customers can decide to avoid making currency conversions altogether, for example, because they do not want to bother with cognitively demanding tasks. Avoidance can lead to decision delegation (Pettigrew et al. 2010), randomly selecting a payment option, or selecting an option because of certain preferences.

The type of conversion strategy that is most likely to be applied by the international customer depends on the ability of the customer (Bettman, Johnson, and Payne 1990; Shanteau 1992). Previous research on financial decision making has typically conceptualized this ability as the level of financial literacy (see Huston 2010). Financial literacy captures the stock of financial knowledge related to personal finance and financial products acquired through education and experience, together with an individual's ability to apply this knowledge (Hastings, Madrian, and Skimmyhorn 2013; Huston 2010). In general, knowledge and experience with financial products allow customers to process financial information more quickly and to make financial calculations with relative ease (García 2013), enabling them to apply exact calculation or simplification strategies with less effort than their less financially literate counterparts (Bettman, Luce, and Payne 1998; Payne, Bettman, and Johnson 1992).

Hypotheses

We start by discussing how markups, evil defaults, and current regulations can affect DCC usage and describe how a customer's level of financial literacy affects the hypothesized relationships. Then, we describe optimal DCC information provision from the customer's perspective and how international customers, regardless of their level of financial literacy, can be protected against excessive DCC markups.

If high markups are applied, the benefits of DCC in terms of instant clarity and reducing risks remain the same, but the transaction price increases. One would thus expect that DCC usage decreases when markups increase (Marshall 1920). However, markup levels do not have an impact on how a customer reaches a decision, since customers infer that markups are applied to the conversion rate only after processing information provided by the DCC provider and making the necessary calculations. Therefore, except for customers that make exact calculations, customers are unlikely to notice that minor markups are applied to the conversion rate because simplification strategies (e.g., rules of thumb, rounding) are expected to result in (minor) errors (Pettigrew et al. 2010). Yet, when markups increase substantially, simplification strategies may already be sufficient to detect markups (Pettigrew et al. 2010). These strategies are more likely to be applied by more financially literate customers than by less financially literate customers, as they can more easily process financial information and can make currency calculations with less effort (Bettman, Johnson, and Payne 1990; Shanteau 1992). This leads to our first hypothesis:

A nudge commonly used by DCC service providers is to present DCC as the default payment option by preselecting it (also see Dynamiccurrencyconversion.info 2018; Forbrukerrådet 2017). Default options provide implicit endorsements. This means that a customer may infer that the default option represents an optimal choice (McKenzie, Liersch, and Finkelstein 2006) or that other customers select it most often (Aldrovandi, Brown, and Wood 2015). In addition, default options address an individual's preference to exert less effort when making (routine) decisions (Dinner et al. 2011; Johnson et al. 2012). Although the overall effectiveness of default settings in guiding the behavior of individuals is well established (Blumenstock, Callen, and Chani 2018), we expect that customers with higher levels of financial literacy are less affected by DCC, as they are more likely to (accurately) calculate which conversion offer is advantageous and, therefore, to bypass the default. This leads to our second hypothesis:

EU regulations (Regulation No. 2021/1230) seek to increase information transparency by specifying that DCC providers must disclose their total charges as a percentage markup over the latest available European Central Bank exchange rate. Other information, such as exchange rates, can still be presented on-screen as long as it is disclosed in a clear and accessible manner (EU Regulation No. 2021/1230). Which type of customer benefits the most from this type of information transparency? Traditionally, policies that improve information transparency are assumed to mainly protect nonexpert customers (in our case, customers with lower levels of financial literacy) (Hertwig and Grüne-Yanoff 2017). However, we propose that higher levels of financial literacy may still be needed to quickly and easily process all financial information (exchange rates, conversion fees, and transaction costs denominated in two different currencies) provided at international point-of-sale terminals. We base this proposition on the work of Bettman, Johnson, and Payne (1990) and Payne, Bettman, and Johnson (1992), who find that the mere presence of additional information or the necessity to make simple calculations is already sufficient to increase the likelihood that certain customers avoid active decision making. This leads to our third hypothesis:

If transparent information provision can increase the likelihood that customers avoid active decision making, what is then an optimal solution from a customer's point of view? By removing information that is not essential to reaching a decision (e.g., information related to exchange rates when markups are on display), information processing can be reduced (Bettman, Johnson, and Payne 1990; Payne, Bettman, and Johnson 1992). In addition, home bank conversion fees can be added to reduce information search such as looking up or remembering the home bank conversion fees. Finally, given the problems that customers experience when offers are denoted in different currencies (Juric, Lawson, and McLean 2002; Raghubir, Morwitz, and Santana 2012), an optimal solution may require that the total transaction amount for both payment options be displayed in the customer's home currency. When such a solution is implemented, we expect that almost all customers choose the most economical payment option regardless of their level of financial literacy and that evil defaults are no longer effective. This leads to our final two hypotheses:

Experimental Design

The data for our study were collected in two waves. The first wave of data collection provides input for Experiment 1, and the second wave provides input for Experiment 2. Although the experiments were conducted at different times, the baseline setup of Experiments 1 and 2 is identical. We subsequently discuss the experimental design and treatments in more detail.

Both experiments are between-subjects experiments. The experiments were conducted on the MTurk platform, and we simulated a purchase-and-checkout process at a foreign airport. We focused on airports because they are a location where individuals regularly encounter DCC. To ensure that participants carefully executed the experimental task, we informed them, “Your reward for this task will depend on the choices that you make” (see Figure A2 in Web Appendix A). To ensure that participants paid attention throughout the experiment, we did not explicitly state that the payment decision during checkout was the determinant of their reward level. In addition, and similar to a real-life situation, this avoids a situation in which participants were immediately aware of price differences during checkout. Each experiment (plus survey) took around 15 minutes to complete. The baseline reward was set at USD 2.25. This reward increased by USD 1 if a participant opted for the most economical checkout option. 2 Participants were randomly assigned to one of the different control or treatment conditions. We continued sampling until we reached at least 50 unique participants per treatment, equally divided into EU participants and U.S. participants, with all EU participants being from countries that adopted the euro as currency. Our participants were on average 34 years of age; 34.99% identified as female, 64.80% as male, and .21% as other.

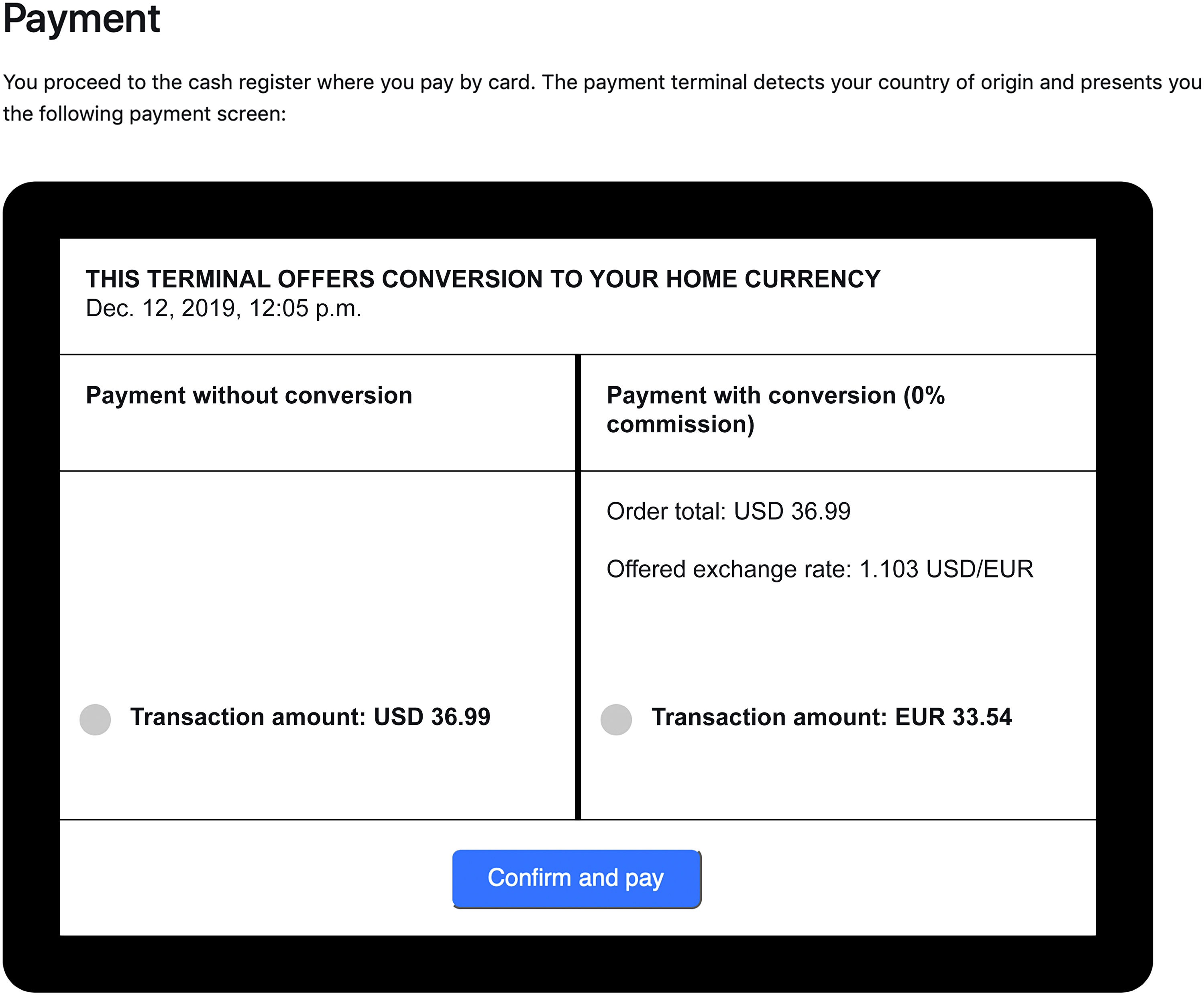

Both experiments started with an introductory screen in which EU participants were told that they would go on a fictional holiday and that they would get a budget of EUR 50 (or USD 50 for U.S. participants) for one or more fictional purchases. We asked participants to make purchases as if they were shopping with their payment card during holidays. To start the simulation, EU participants could choose Miami, New York, or Boston as their preferred destination (see Web Appendix A); U.S. participants could fly to Amsterdam, Paris, or Madrid. On the next screen, participants were informed that they had arrived at the airport of their preferred destination. We then asked participants to purchase one of the following three items: a book, a T-shirt, or a three-course meal. All items were priced at USD 36.99 for EU participants and EUR 30.49 for U.S. participants, so conversion markups had sizable effects on the price without compromising the credibility of the transaction. The last step was the checkout, where participants indicated whether they wanted to purchase the item in foreign or home currency. The exchange rate—and thus the price of the product in home currency, including the markup—received real-time updates and fluctuated from 1.07 to 1.12 USD in exchange for 1 EUR during our study. We used the chosen payment option as the dependent variable (named DCC) throughout our analyses. This is a binary variable coded as 1 if a participant opted for payment in home currency (i.e., DCC) and 0 otherwise.

Figure 2 shows the checkout screen for EU participants. We use an exchange rate of 1.12 USD to 1 EUR throughout the explanation of our experimental design. The left-hand side of the screen provided the option to conduct the transaction in USD 36.99 without conversion. The option on the right-hand side offered conversion via DCC. Similar to real-life encounters (see, e.g., Dynamiccurrencyconversion.info 2018), we mentioned that there was no commission charged on the transaction. In most countries, DCC providers must disclose the offered exchange rate by law. Figure 2 shows our low markup scenario, in which the two payment options are economically similar. In line with currency conversion costs that typically range from .5% to 2% if a European home bank conducts the conversion, we applied a 1.5% markup to the DCC exchange rate. This resulted in an offered exchange rate of 1.103 USD to 1 EUR (i.e., 1.12

Checkout Screen for an EU Participant in Our Experiment.

The data collection was conducted in two waves. The first wave (used for Experiment 1) consists of three parts (Part A, Part B, and Part C). All participants were randomly allocated to a treatment condition of Part A, B, or C. In each part, we altered the standard checkout process. In Part A, we manipulated the applied DCC markup. Part B introduces a default on the DCC payment option (i.e., an evil default), and we compare the propensity of DCC usage to that of Part A, where no default is implemented. In Part C, we build on EU regulations by providing more markup-related information to participants. Again, we compare the propensity of DCC usage with that of Part A, where no additional information is provided. We use the insights that we obtained in Experiment 1 to design a checkout situation that will optimally protect against excessive DCC markups in Experiment 2. Participants were recruited in a second wave and were again randomly allocated to a treatment condition. Those that participated in the first wave could not participate in the second wave. Both experiments were programmed in oTree (Chen, Schonger, and Wickens 2016). We filed our experimental design with the ethics commission of Utrecht University and gained Institutional Review Board approval.

Across all experiments, we included five standard financial literacy questions (Van Rooij, Lusardi, and Alessie 2012). Each question follows a multiple-choice format with four options, of which one is the correct option. We divided our participants into three distinct financial literacy categories, each of equal size. As there were relatively few participants who answered either zero, one, two, or three questions correctly, we bundled these participants into one group (“less financially literate”). Participants who correctly answered four questions were termed “moderately financially literate,” and participants answering all questions correctly were labeled “more financially literate.”

In all estimations, we include four variables to statistically control for individual differences between participants. First, we control for risk aversion. The DCC payment option provides the customer with a guaranteed exchange rate. When a customer chooses to proceed in foreign currency, the costs in home currency are typically calculated later (i.e., at the end of the day or sometimes one or two days later), exposing the customer to exchange rate fluctuations between the time of transaction and the handling of that transaction by the home bank. Therefore, risk-averse customers may prefer DCC. We measure risk aversion with Holt and Laury's (2002) multiple price list where switching consistency was forced (see Holzmeister 2017). A score of 1 stands for the least risk-averse, and a score of 11 represents the most risk-averse. Second, we asked participants whether they had experienced DCC before (coded as 1 if yes, 0 if no) since previous costly experiences may drive concurrent choices. Third, if customers travel to other currency zones or conduct online payments in different currencies, they experience fewer difficulties in handling offers in different currencies (Raghubir and Srivastava 2002). We asked participants to describe the number of times they traveled outside of their currency area and how often they bought outside their currency area. If they indicated “never” on both questions, we treated them as inexperienced with foreign currencies and coded the variable “FX experience” as 0. Otherwise, we treated them as experienced (coded as 1). Fourth, we include a variable “Origin,” which captures the location of the participant (1 = United States, 0 = EU). Research (see, e.g., Wertenbroch, Soman, and Chattopadhyay 2007) has shown that, when confronted with two offers, customers generally choose the offer expressed in the smallest number (also known as the numerosity effect). Therefore, U.S. participants could be less likely to opt for DCC, since the transaction amount expressed in USD is higher than the amount expressed in EUR in almost all of our experimental treatments. Hence, the numerosity effect would predict that U.S. participants in our experiment are less likely to opt for DCC than EU participants. Alternatively, U.S. participants might be more prone than EU participants to using DCC since it is a reasonable assumption that U.S. participants have had less exposure in general to foreign currencies than EU participants. 3

Table 1 depicts the summary statistics for all variables across both experiments. In Part A of Experiment 1, an average of 54% of the participants opted for DCC over the different markup conditions, and this percentage is in line with anecdotal evidence (Paysquare n.d.). For Parts B and C, we present the means for the treatments only, since we use certain groups from Part A as control in Parts B and C. The percentage of DCC users in Part B, Part C, and Experiment 2 was between 28% and 66%, with deviations caused by specific treatment manipulations. Our participants answered on average four questions on financial literacy correctly, leading to a mean value for financial literacy of around 2 across both experiments. The mean risk aversion varies from 5.3 to 5.7 in the two experiments. A little over half of the participants (i.e., 53%–59%) reported experience with DCC. Between 88% and 93% of our sample had foreign currency experience. Finally, roughly half of all participants originated from the United States, and the other half were from the EU.

Summary Statistics: Means.

In the next section, we discuss the results of our experiments. For each part of Experiment 1 and for Experiment 2, we start by discussing the specific experimental design. This is followed by a brief discussion of the usage of DCC per treatment, after which we present the results of our regression equations. All regression models are specified as follows. First, we use a probit model to regress DCC on only our treatment variables. Second, we estimate our full model, in which we include financial literacy and control variables. We refer to the different probit coefficients as β. To ease the interpretation, we also provide marginal effects for the full model, which we refer to as dydx. For our statistical analyses, we use probability threshold values of p < .1, p < .05, and p < .01. The threshold of p < .1 is included due to the small sample size, which is common for experimental research (Gerber and Green 2012).

Experiment 1

In Experiment 1, we mimic established industry practices to better understand how markups (Part A), default settings implemented by DCC providers (Part B), and existing EU regulations (Part C) affect DCC usage.

Part A: Markups and DCC Usage

Background and experimental design

In Part A of Experiment 1, we test participants’ sensitivity to different DCC markups (negative and positive). Our control group is the “negative markup” treatment and involves a −7.5% markup. This control group includes 58 participants. The “low markup” treatment (n = 52) involves a 1.5% markup and creates a situation in which both payment options are approximately economically equivalent. For the “moderate markup” treatment (n = 54), the markup increases by 4.5 percentage points to 6%. This percentage is close to the average markup, as reported by the European consumer organization BEUC in Allix and Aliyev (2017). In the “high markup” treatment (n = 54), the markup increases by another 4.5 percentage points to 10.5%. This increase brings the markup up to some of the higher markups observed in practice (see Allix and Aliyev 2017). Finally, we add an “extreme markup” (19.5%) treatment (n = 52). Hence, Part A involves 270 participants and a between-subjects design with five markup conditions. Figure 3 shows the checkout screens for the different markups applied to an exchange rate of 1.12 USD to 1 EUR.

Treatments in Experiment 1 Part A.

Sample and results

Table 2 depicts the percentage of participants per treatment that opted for DCC and shows that around 63% opted for it in the negative, low, and moderate markup scenarios. Only in the high and extreme markup treatments does DCC usage decline. In Experiment 1 Part A only, we asked our participants to state the motivation of their choice to pay in either USD or EUR during the transaction. Web Appendix B provides the motivations. In short, participants use DCC because of convenience and certainty, whereas non-DCC users are more aware of cost differences.

Summary Statistics: DCC Usage per Condition for All Experiments.

Notes: For Experiment 1 Part B and Part C, we report the DCC usage in percentage for treatments only.

Our regression results are presented in Table 3, where the negative markup treatment serves as our reference category. Column 1 shows the result for our main variables of interest only. While the coefficients for low markup and moderate markup are close to zero, those for high and extreme markup are larger and negative (βHigh markup = −.354; βExtreme markup = −.756). Only extreme markup is statistically significant in this estimation (p < .01). Column 2 presents our full model. In this model, also, high markup is statistically significant (βHigh markup = −.410; p < .1). Comparing coefficients, we find that a high markup has a statistically significantly larger effect than a moderate markup (p < .1), whereas there is no significant difference in effect size between a high and extreme markup (p > .1). The coefficient of financial literacy is insignificant. To ease interpretation, we add the marginal effects of the full model in Column 3. This column shows that participants confronted with a high markup opt 15.8% less often for DCC (p < .1). The size of the effect of the extreme markup is approximately twice as large (dydxExtreme markup = −.297; p < .01).

Experiment 1 Part A: Probit Estimations Excluding Interaction Effects.

*p < .1. **p < .05. ***p < .01.

Notes: Negative markup used as benchmark treatment; robust standard errors are in parentheses.

Regarding our control variables, U.S. participants opted 15.9% more often for DCC than EU participants (p < .05). This finding goes against the numerosity effect as an alternative explanation for choosing DCC. Instead, the finding suggests that more frequent exposure to foreign currencies decreases the propensity to use DCC. This is suggestive evidence at best, since we do not find statistically significant effects for either the DCC experience or the foreign currency experience. 4 The coefficients of other control variables are not statistically significant.

Table 4 shows the interaction effects between our markup treatments and the level of financial literacy for our full model. Marginal effects are measured separately for less, moderately, and more financially literate participants. Within each group, the marginal effects capture the propensity to use DCC relative to the negative markup condition. Less financially literate participants do not use DCC less when markups become higher. Moderately financially literate participants opt for DCC less when confronted with an extreme markup (dydx = −.323; p < .01). More financially literate participants opt less for DCC if markups are high (dydx = −.345; p < .01) or extreme (dydx = −.403; p < .01). 5

Experiment 1 Part A: Interaction Effects.

*p < .1. **p < .05. ***p < .01.

Notes: Within all categories of financial literacy, negative markup is used as the benchmark treatment; robust standard errors are in parentheses.

Conclusions

In line with anecdotal evidence from the field (e.g., Allix and Aliyev 2017; European Commission 2018; Forbrukerrådet 2017), our results show that many customers do not opt for the economically optimal option. With markups of 10.5% and higher, DCC usage decreases significantly. Participants who scored higher on the financial literacy scale are the main drivers of the change in the use of DCC as they opt less for DCC when faced with high and extreme markups. Moderately financially literate participants opt less for DCC with extreme markups only, whereas less financially literate participants seem not to respond to markup levels. Therefore, we find support for our conceptual reasoning that when markups increase, DCC usage decreases (H1a), and this effect is stronger for customers with higher levels of financial literacy (H1b). Combined, these findings thus suggest that moderately and more financially literate participants use decision-making strategies that are better able to detect additional DCC markups in the high and extreme markup conditions.

Part B: Evil Defaults and DCC Usage

Background and experimental design

Part B mimics another industry practice, namely the provision of DCC as the default option. For example, for customers with a home currency different from U.S. dollars, Amazon applies the Amazon Currency Converter, whereby during checkout the option in home currency is prechecked. To gauge the effectiveness of this approach, we manipulate the standard checkout screen from Part A by prechecking the DCC payment option (see Figure 4). We label this treatment “evil default.” As incentives for DCC providers to implement evil defaults increase with higher markups, we test the effect at low, moderate, high, and extreme markups. Thus, Part B is a 2 × 4 between-subjects design with the default either absent or present and four different markups.

Treatment in Experiment 1 Part B for Low Markup.

Sample and results

We recruited 211 participants for our positive markup categories, and we compared their DCC usage with that of participants who did not have a DCC default (i.e., 212 participants in Part A). Therefore, the analysis comprises 413 participants. In Table 2, we show the percentage of participants who opted for DCC when the default is present (i.e., for participants in the treatments of Part B). With a low markup (n = 56), 79% opted for DCC. This percentage remains high for a moderate markup (70%; n = 50) and decreases to 62% for participants exposed to a high markup (n = 52) and to 53% for participants exposed to an extreme markup (n = 53).

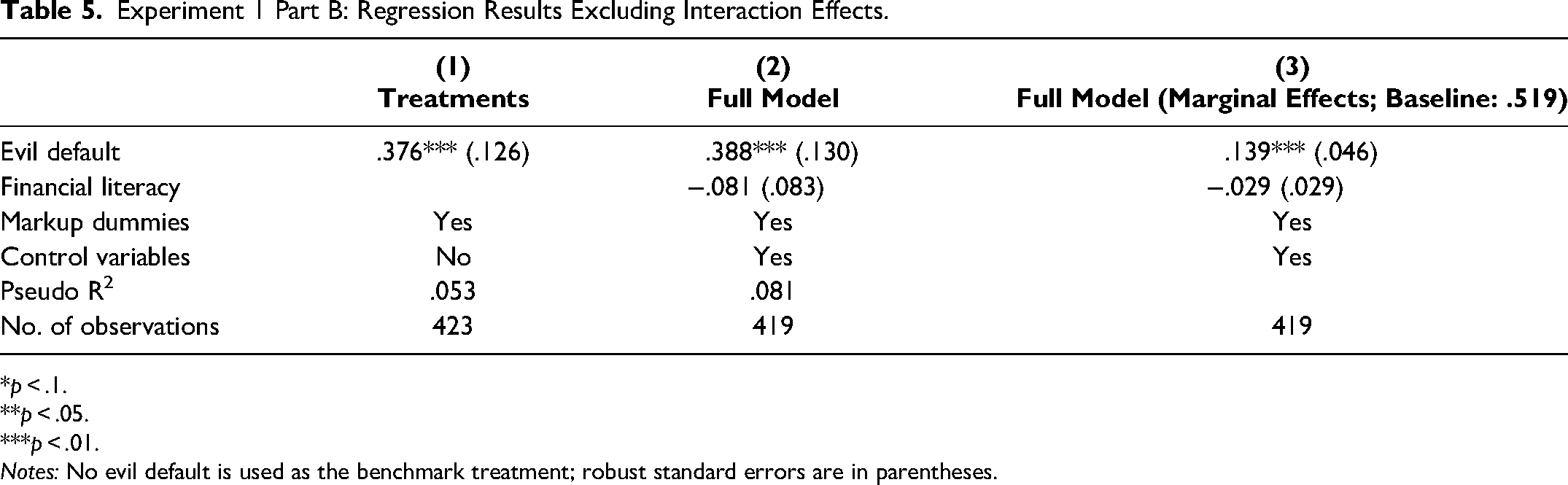

Table 5 presents our regression results, in which we compare the effect of a default on DCC usage. 6 Column 1 contains our model excluding control variables. We see that the “evil default” treatment is highly significant (βEvil default = .376; p < .01). Columns 2 and 3 show the result of our full model. As the marginal effects are more interpretable, we focus here on Column 3. The presence of an evil default increases DCC usage by 13.9% (p < .01). For the sake of brevity, we do not report the individual coefficients of our controls.

Experiment 1 Part B: Regression Results Excluding Interaction Effects.

*p < .1. **p < .05. ***p < .01.

Notes: No evil default is used as the benchmark treatment; robust standard errors are in parentheses.

Table 6 presents the marginal effects of interacting financial literacy with the evil default. We find that only individuals with a lower and moderate financial literacy significantly responded to the default. Less financially literate participants opted for DCC 17.4% (p < .05) more often when DCC was presented as a default, compared with a “no default” representation. For moderately financially literate individuals, this percentage was 14.2% (p < .01). For more financially literate individuals, we do not observe significant effects from the presence of a default option. 7

Experiment 1 Part B: Interaction Effects.

*p < .1. **p < .05. ***p < .01.

Notes: Within all categories of financial literacy, no evil default is used as the benchmark treatment; robust standard errors are in parentheses.

Conclusions

Part B of Experiment 1 provides support for both H2a and H2b. When an evil default is implemented, participants are more likely to select DCC. Interacting financial literacy with the default option shows that this effect is mainly driven by less and moderately financially literate participants, while more financially literate participants seem to remain unaffected by the default option. This is most likely due to the tendency of more financially literate participants to calculate (using exact calculation or simplification strategies) which conversion offer is advantageous despite the implicit recommendation to opt for a payment in home currency.

Part C: Information Provision and DCC Usage

Background and experimental design

Currently, EU regulations (Regulation No. 2021/1230) stipulate that parties offering DCC must disclose their total charges as a percentage markup over the latest available European Central Bank reference exchange rate and that this information must be disclosed in a clear and accessible manner. As the focus of Part C is on the effect of information transparency (and not on markups), we test the impact of information transparency using only a moderate markup of 6%. 8 We consider the effects of increasing information transparency by revealing markup-related information and compare participants’ DCC usage with that of participants assigned to the moderate markup in Part A (n = 54), in which no specific information was provided. Figure 5 illustrates the different treatments. Participants in our control condition were exposed to the standard checkout screen. In Treatment 1 (n = 51), we informed participants that the applied conversion fee was 6% and provided information on the current exchange rate, in addition to the rate that the DCC provider offered. We label Treatment 1 “Information: DCC.” In this treatment, the information is more transparent, as participants can obtain the costs of the conversion (i.e., fees) via DCC without having to make any currency conversion calculations. In addition, because we provide participants with the actual exchange rate, they do not have to know it or look it up.

Treatments in Experiment 1 Part C.

EU Regulation No. 2021/1230 further stipulates comparability between the markup applied by the provider of DCC and the markup applied by the home bank. The home bank must communicate the charges in terms and conditions and has to periodically make that information known via websites and/or mobile banking applications. In Treatment 2 (n = 52), we take the transparency of information one step further by providing relevant information (i.e., the conversion fee and the exchange rate) about the conversion process of the home bank on the left-hand side of the checkout screen (see Figure 5).

Since we provide information on-screen instead of via a different channel as is done in practice, it should be easy to compare the two payment offers, and hence the treatment represents the upper bound of a potential information transparency effect. We label this treatment “Information: DCC and home bank.” Part C involves a total of 157 participants and a between-subjects design with three conditions of information provision.

Sample and results

Table 2 depicts the percentage of participants per treatment who opted for DCC. This percentage was equal to 33% in the DCC information treatment and equal to 23% once we exposed the participants to the applied exchange rates for both options (i.e., DCC and home bank information). The results of the probit estimations are provided in Table 7. Column 1 shows the relation between the DCC choice and the information treatments. The information on DCC has a negative effect on the propensity to choose DCC (βInformation: DCC = −.762; p < .01). The additional provision of home bank information has an even larger negative effect (βInformation: DCC and home bank = −1.067; p < .01). However, the difference in effect size is insignificant (p > .1). Column 2 contains financial literacy and control variables. Column 3 presents the marginal effects. The provision of DCC information decreases DCC usage by 28.1% (p < .01). The additional provision of home bank information has an even greater effect (dydx = .380; p < .01).

Experiment 1 Part C: Regression Results Excluding Interaction Effects.

*p < .1. **p < .05. ***p < .01.

Notes: No provided information is used as the benchmark treatment; robust standard errors are in parentheses.

Table 8 provides the marginal effects of the interaction of financial literacy with the two information transparency treatments. All marginal effects can be interpreted relative to the control condition of no information within the relevant financial literacy category. None of the treatments has a significant effect on less financially literate participants. For moderately financially literate participants, the DCC information has a marginal effect of −28.7% (p < .01), and the DCC and home bank information has a marginal effect of −36.4% (p < .01). The coefficients for more financially literate participants are larger; DCC information decreases DCC usage by 32.3% (p < .05), and DCC and home bank information decreases DCC usage by 57.8% (p < .01). 9

Experiment 1 Part C: Interaction Effects.

*p < .1. **p < .05. ***p < .01.

Notes: Within all categories of financial literacy, no provided information is used as the benchmark treatment; robust standard errors are in parentheses.

Conclusions

Part C provides support for H3 as information transparency decreases DCC usage (H3a), but this provision of DCC information decreases DCC usage for moderately and more financially literate participants only (H3b). Less financially literate participants do not opt less for DCC when information transparency increases. This empirical finding stands in sharp contrast to previous research (e.g., Hertwig and Grüne-Yanoff 2017) that shows that information transparency mainly protects nonexpert customers. However, unlike the case in many other settings, DCC information transparency, as advocated in EU regulations (Regulation No. 2021/1230), does not necessarily make information easier to process. In fact, leaving the option open to provide various forms of financial information (e.g., exchange rates) that are supposed to make the process more transparent can be confusing for less financially literate customers (see Hastings, Madrian, and Skimmyhorn 2013; Huston 2010). As a result, this information does not support their decision-making process and can even cause them to neglect relevant information that would otherwise have been incorporated into this process (Bettman, Johnson, and Payne 1990).

Experiment 2: Optimal Information and DCC Usage

Our goal in Experiment 2 is to assess which type of information provision during checkout is optimal for less financially literate customers, in particular. In making information more accessible to all customers and testing to what extent an evil default still has an effect, we build on the insights we obtained from Experiment 1 and recruit new participants.

Experimental Design

The control condition in this experiment (n = 52) entails a standard checkout screen with a moderate markup applied (see Figure 6). Our main goal for the treatments is to minimize information processing and to make currency calculations obsolete (Bettman, Johnson, and Payne 1990). Treatment 1 (n = 51) is based on the “Information: DCC” treatment of Experiment 1 Part C, as this treatment significantly reduced DCC usage among moderately and more financially literate individuals. However, to address the difficulties that participants with lower levels of financial literacy may have with exchange rates, in Treatment 1 we show conversion fees only (see Figure 6). Participants may not know the home bank conversion fees and thus lack a benchmark for these fees. Therefore, we add home bank conversion fees in Treatment 2 (n = 51) and additionally inform the participants about the party that handles the conversion. This treatment can thus be seen as a more simplified version of the “Information: DCC and home bank” treatment of Experiment 1 Part C, which, again, was successful in reducing DCC usage among moderately and more financially literate individuals. In addition to the potential abundance of financial information in both treatments of Experiment 1 Part C, a transaction amount denominated in two different currencies can create difficulties for customers (Juric, Lawson, and McLean 2002). In Treatment 3 (n = 56), we therefore additionally provide the transaction price for both payment options in the home currency. We study interaction effects between treatments and the level of financial literacy to assess the extent to which our designs help less financially literate customers. The analysis involves 210 participants and a between-subjects design with four different information conditions.

Treatments in Experiment 2.

From a regulatory perspective, an optimal design of the checkout process should also protect international customers from evil defaults. Therefore, we extend Treatments 1, 2, and 3 by setting the DCC option as default. The implementation of the DCC default is identical to Experiment 1 Part B (see Figure 6). This creates Treatments 4 (n = 50), 5 (n = 52), and 6 (n = 50). This additional analysis involves 310 participants and represents a 2 × 3 between-subjects design as the default (absent or present) is applied to three optimal information conditions.

Sample and Results

Table 2 presents the DCC usage for the control condition and all treatments. Relative to our control condition, in which 65% of participants opt for DCC, all treatments are characterized by significantly lower DCC usage rates. The provision of a conversion fee decreases DCC usage to 27%. Providing the home bank conversion fee as well decreases DCC usage to 22%. Last, the additional provision of the transaction amount in home currency decreases DCC usage to 7%. We see that DCC usage increases as a result of the implementation of an evil default. This holds for the provision of the conversion fee (from 27% to 50%) and the additional provision of the home bank conversion fee (from 22% to 38%), but less so for the checkout option with both transaction amounts in home currency (from 7% to 12%).

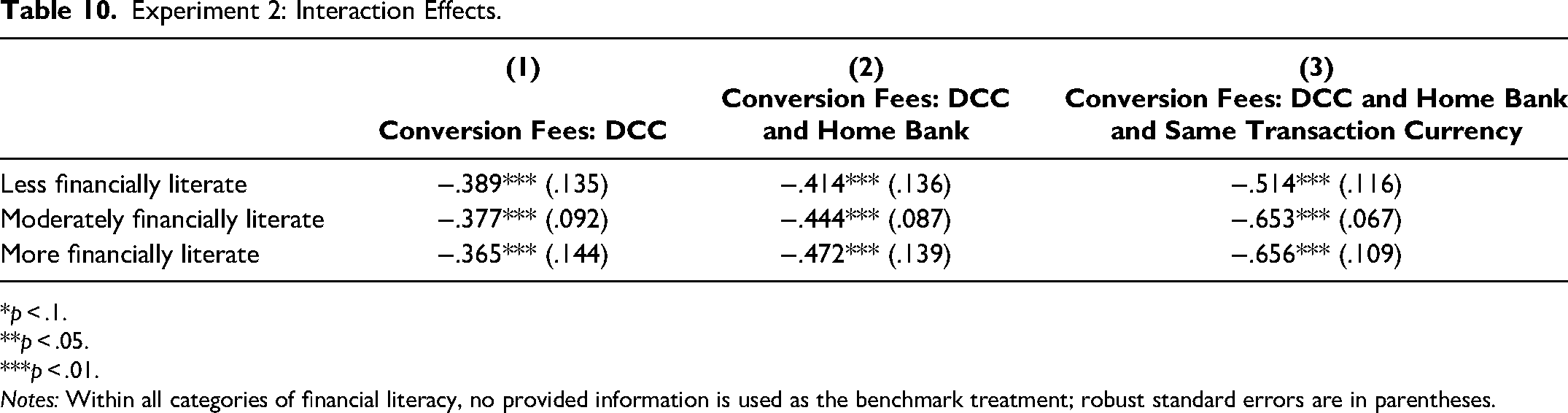

Table 9 contains the results of our regression analysis. In our main analysis, we are interested in the effects of the different optimal information treatments. In Column 1, we regress DCC choice on our three different treatments. All treatments have a negative effect on DCC choice (p < .01). In Column 2, we add financial literacy and control variables. The statistical significance of our treatments remains intact. In Column 3, we show the marginal effects of this estimation. Providing the DCC conversion fee leads to 36.9% less usage of DCC (p < .01). Furthermore, providing home bank conversion fees reduces DCC usage by 44.1% (p < .01). This difference in effect size is not statistically significant (p > .10). If we also provide the transaction amount for both options in the home currency, we see that the use of DCC decreases by 58.4% (p < .01). This decrease is statistically distinct from the first two treatments (p < .05). In Table 10, we present the marginal effects of interactions with financial literacy. All treatments reduce the usage of DCC at all levels of financial literacy. The effect of the provision of the DCC conversion fee is roughly equal among all financial literacy groups, namely a decrease of 36.5% to 38.9% (p < .01). The additional provision of home bank conversion fees further increases the effect size, but less so for less financially literate participants. For these participants, the provision of all markups together with the presentation of both transaction amounts in home currency decreases DCC usage by 51.4% (p < .01). The effect is greater for moderately financially literate participants (dydx = −.653; p < .01) and more financially literate participants (dydx = −.656; p < .01).

Experiment 2: Regression Results Excluding Interaction Effects.

*p < .1. **p < .05. ***p < .01.

Notes: No provided information is used as the benchmark treatment; robust standard errors are in parentheses.

Experiment 2: Interaction Effects.

*p < .1. **p < .05. ***p < .01.

Notes: Within all categories of financial literacy, no provided information is used as the benchmark treatment; robust standard errors are in parentheses.

We now study to what extent evil defaults are still effective in the optimal information treatments. Here, we compare the participants in Treatments 4–6 with evil defaults to those in the corresponding treatments without evil defaults (Treatments 1–3). We regress DCC usage on the three treatments, an evil default dummy, financial literacy, and control variables. In Table 11, we provide the interaction effects between the three information treatments and the evil default. The evil default increases DCC usage by 17.7% (p < .1) when only the conversion fee is presented and by 17.5% (p < .05) when both conversion fees are presented. When for both payment options the transaction amount is presented in home currency, the effect of an evil default disappears. 10

Experiment 2: Evil Default Effects on Treatments.

*p < .1. **p < .05. ***p < .01.

Notes: Within all categories of information, no evil default is used as the benchmark treatment; robust standard errors are in parentheses.

Conclusions

We find support for H4 as we show that our treatments are effective for all types of financially literate participants. We find partial support for H5: the effect of an evil default disappears only when we, in addition to providing the conversion fees, provide the transaction amount for both payment options in the same currency.

Discussion

Potentially, DCC increases the competitiveness of international transactions by creating a choice at point-of-sale terminals, ATMs, and online shops. Competitive pressure can lead to a decrease in markups applied by banks and DCC service providers. In practice, however, there seems to be a lack of effective competition: a large proportion of customers use DCC even though the conversion markups charged by DCC service providers are generally substantially higher than those of the customer's home bank. From a welfare perspective, higher markups lead to consumer welfare losses. The goal of this research is to understand under which conditions international customers select the noneconomical payment option and to provide a checkout design that protects customers against costly currency conversions. The results of two between-subjects experiments show that especially less financially literate customers (1) are less likely to decrease DCC usage when markups increase, (2) are more likely to be affected by evil defaults, and (3) benefit less from information transparency. The provision of conversion fees instead of exchange rate information decreases DCC use among all types of participants. Only when both payment options are displayed in the home currency do almost all customers select the most economical payment option. We discuss the practical and theoretical implications of these findings in the following sections.

Insights for Public Policy Makers

DCC regulation is not high on the agenda of most governments. Regulation usually protects foreign customers at the potential expense of local DCC service providers. Yet, countries that fail to protect international customers against excessive markups may face negative side effects. For example, excessive DCC markups can trigger emotional responses and dissatisfaction among international travelers once they find out that they have paid unnecessary conversion fees (e.g., when checking their bank or credit card statement), thereby decreasing their revisit intention and generating negative word of mouth (Ma, Li, and Shang 2022). Given its nine currency zones, the EU is a special case where customers can conduct transactions outside their currency zone but within the EU. Differently from most jurisdictions, DCC-specific regulations in the EU thus protect local customers as well. 11

Thus far, EU regulations have mainly targeted the information that is on display during checkouts. Our results show that the display of conversion fees (as required by EU Regulation No. 2021/1230), in addition to exchange rate information, decreases DCC usage but that especially less financially literate customers still select the noneconomical payment option. The intervention we identified to be most effective for all types of financially literate customers entails displaying only the conversion fee information and presenting both conversion offers in the home currency (see Figure 6, Panel D, for Treatment 3). Although the display of both options in home currency is part of the optimal solution from a normative perspective, this is difficult to implement in practice because it requires additional communication between a payment terminal and the customer's home bank. A more feasible solution is to replace the DCC exchange rate with the DCC conversion markup as a percentage markup over the latest market exchange rate while leaving the presented transaction amounts in two different currencies (see Figure 6, Panel B, for Treatment 1). 12 We therefore recommend revisiting the current practice that stipulates that the exchange rate must be displayed for DCC payment options as this generally decreases the understanding among less financially literate customers and thereby increases their vulnerability to high DCC markups.

When DCC usage rates drop as a result of customers making more economical decisions due to the visibility of the conversion fee, DCC service providers are incentivized to lower their fees in order to retain market share. However, it may take some time for these competitive pressures to lead to significantly lower DCC markups. In the meantime, a substantial percentage of international customers may continue to use DCC. Policy makers may, therefore, want to impose a price cap on the total fees charged by DCC service providers (also see Bouyon and Krause 2018). In addition, we argue that future regulations should require that DCC be presented as a nondiscriminatory option (e.g., not as a default option) to protect less financially literate customers. We argue that completely prohibiting DCC as suggested by, for example, Forbrukerrådet (2017) is not an optimal long-term solution, as a potential side effect could be that home bank conversion markups increase due to the absence of competition.

Finally, the U.S. Consumer Financial Protection Bureau, the Organisation for Economic Co-operation and Development, and the EU are currently implementing various educational programs to spur the level of financial literacy among underserved or economically vulnerable individuals such as consumers, students, and older adults. Previous research has mainly investigated the benefits of financial literacy in relation to products such as retirement plans or mortgages (see Hastings, Madrian, and Skimmyhorn 2013; Huston 2010). Routine financial decisions (such as checkouts at a foreign airport, purchases at online stores located in another currency zone, or cash withdrawals at foreign ATMs) occur more frequently and, although the impact of a single decision is much smaller, also affect an individual's financial position. Thus, our research highlights the relevance of financial literacy for a broader array of financial decisions than previously addressed and reemphasizes the importance of programs that aim to raise the overall level of financial literacy in society.

Insights for Researchers

A subset of the literature on currency calculations focuses on how the denomination of offers in multiple currencies affects purchasing decisions. This phenomenon occurs most frequently in customer loyalty programs (e.g., Starbucks loyalty program, frequent flyer miles, Air Miles) in which points can serve as a virtual currency (see Drѐze and Nunes 2004; Wei and Xiao 2015; Wertenbroch, Soman, and Chattopadhyay 2007). One of the basic ideas in this line of research is that customers anchor on the nominal value (i.e., the actual amount) of a product/service denoted in a virtual currency and adjust for the exchange rate to determine the real value. However, because these adjustments are inaccurate, they can cause a face value effect, that is, “a biased evaluation in favor of the nominal rather than the real value of the price posted in the foreign currency” (Wertenbroch, Soman, and Chattopadhyay 2007, p. 1). Depending on exchange rates, this can lead to over- or underspending (Raghubir, Morwitz, and Santana 2012). Our results show (1) that the degree in which inaccuracies play a role depends on a customer's level of financial literacy and (2) that the accuracy can be improved by providing conversion rate information so that customers do not have to make currency calculations. This is relevant because exchange rates affect the probability that a customer chooses to use loyalty points for one purchase over another (Wei and Xiao 2015). By making exchange rates more transparent, firms can more effectively promote certain products and services. In addition, exploring the different contingencies that may lead to over- or underspending is a promising avenue for future research. In the present study, we focus only on financial literacy, but a variety of knowledge factors and personal characteristics can affect how customers deal with offers denoted in different currencies.

Our second contribution pertains to the literature on evil defaults (Hansen and Jespersen 2013; Thaler 2018). Originally, defaults and other types of nudges have been proposed as a means of improving decision making and improving (social) welfare (De Haan and Linde 2018; Thaler and Sunstein 2021). More recently, researchers have started to explore how governments (Wilkinson 2013), marketers (Dinner et al. 2011), websites, and mobile applications (Maier and Harr 2020) use defaults to profit from an individual's preference for default options or even from mistakes such as accidentally proceeding with a particular option (Brignull 2013; Maier and Harr 2020). DCC creates an interesting setting to study the effect of evil defaults because it involves a situation in which customers have to choose between two similar services that have different costs attached to them. We contribute to this emerging stream of research by showing that, within the context of financial decision making, higher levels of financial literacy mitigate the effect of evil defaults. We attribute this effect to the increased likelihood that more financially literate customers will use some form of calculation to determine which option is advantageous. However, as most conversion strategies result in some level of error, a certain level of uncertainty remains, thereby leaving room for evil default settings to continue to steer the behavior of customers toward noneconomical decisions. Little is known about this interplay between an individual's knowledge base, different modes of decision making (active versus inactive), and uncertainty (see Miesler et al. 2017 and Web Appendix E). We urge scholars to further explore these relationships.

Limitations

First, since actual DCC transaction data are not publicly available, we rely on data obtained via an online experiment. Although we (1) witnessed DCC usage rates that are similar to those reported by consumer organizations (e.g., Allix and Aliyev 2017) and (2) used a bonus structure to ensure that participants were paying attention, the exact size of the effect that is obtained cannot be generalized. Second, we used discrete cutoff points for DCC markups, and thus we cannot identify exactly at which markup the DCC usage drops significantly. Third, we only measured and did not experimentally manipulate a customer's level of financial literacy. Fourth, our bonus payment was communicated to be dependent on the choices that participants made, without specifying that the DCC payment decision determined the bonus. This could confound our results if more financially literate participants were more likely to figure out that they could earn a bonus if they calculated which payment option was more economical.

Conclusion

As international customers are frequently exposed to DCC, it is important to gain insight into their behavioral responses. Our results show that DCC service providers are able to extract substantial rents from all customers, in particular among those with lower levels of financial literacy. Evil default settings are also more effective among customers with lower levels of financial literacy, while increasing information transparency fails to protect this particular customer group. Replacing the exchange rate by the conversion fee as a percentage markup over the exchange rate is an effective way to protect customers against DCC. Moreover, if both payment options are shown in the same currency, almost all customers choose the most economical option. These findings have important implications for researchers that study how information and default settings affect the behavior of heterogeneous customer groups. For policy makers, our findings show that customers with lower levels of financial literacy must be kept in mind when designing effective DCC regulations.

Supplemental Material

sj-pdf-1-ppo-10.1177_07439156231157721 - Supplemental material for Dynamic Currency Conversion Payment Options Specifically Harm Less Financially Literate Customers

Supplemental material, sj-pdf-1-ppo-10.1177_07439156231157721 for Dynamic Currency Conversion Payment Options Specifically Harm Less Financially Literate Customers by Dirk F. Gerritsen, Bora S. Lancee and J.P. Coen Rigtering in Journal of Public Policy & Marketing

Footnotes

Acknowledgments

The authors thank the JPP&M review team for excellent feedback. In addition, they are grateful to Jeroen de Jong, Frank Verbeeten, and Peter O. van der Meer for sharing insights and providing valuable suggestions. Furthermore, the authors thank Carla Janse van Vuuren for her contributions to an earlier stage of our research and Lotte van Leengoed for helping with the artwork.

Editor

Kelly D. Martin

Associate Editor

Klaus Wertenbroch

Author Contributions

All authors contributed equally.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

,_2021.png){kind=link}

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.