Abstract

This paper examines how floodplain buyouts funded through FEMA’s Hazard Mitigation Grant Program (HMGP) have altered the racial and ethnic composition in Harris County, Texas, from 1990 to 2015. A quasi-experimental research design permits the attribution of observed changes to the buyout program, and interviews with households provide context to our findings. We find that buyouts have triggered white flight, shifting neighborhoods from predominantly white to Hispanic, while little changes in the black population. The impact was more pronounced in wealthier neighborhoods and those with more buyouts, suggesting a need for buyouts to include provisions to help stabilize remaining neighborhoods.

Introduction

In the face of growing impacts from climate change, particularly in flood-prone areas, buyouts have become critical for mitigating disaster risks. While the environmental and financial benefits of buyouts are well-documented, their broader sociocultural implications—especially their effects on the racial and ethnic composition of communities—have received less attention. Understanding the influence of floodplain buyouts on these demographic shifts is important not only for comprehending urban dynamics but also for crafting equitable planning policies.

This study examines long-term racial and ethnic shifts following floodplain buyouts over twenty-five years in Houston, Texas, USA. Using smaller neighborhood units in analysis and a mixed-method approach, the study enables a nuanced understanding of the interplay between buyout policies and racial dynamics, filling a significant gap both in urban planning literature and practice. By uncovering the patterns and consequences of racial turnover following floodplain buyouts, this research provides planners and policymakers with insights necessary for developing strategies that mitigate environmental risks while enhancing the social fabric of urban communities.

Literature Review

Buyouts as a Double-Edged Sword

Residential buyouts for homes in the floodplain are often promoted as one of the most effective and enduring hazard mitigation strategies in the United States, particularly from the perspective of reducing damages to physical property and limiting future recovery costs (De Vries and Fraser 2012). Economically, they can help alleviate potential recovery costs for households and the National Flood Insurance Program (NFIP) by limiting future losses (De Vries and Fraser 2012). Yet, the notion of “effectiveness” remains contested: while buyouts may successfully eliminate structures from high-risk areas, they are less effective—and sometimes detrimental—when evaluated in terms of the social, economic, and cultural well-being of the households and communities involved (Jerolleman et al. 2024; Perry and Lindell 1997). Buyout programs, typically implemented by local or county governments with federal, state, or local funding, can vary in design and compensation structures—for example, FEMA’s Hazard Mitigation Grant Program (HMGP) purchases homes at pre-disaster fair market value, while HUD’s Community Development Block Grant–Disaster Recovery (CDBG-DR) may use post-disaster or adjusted values depending on policy and funding availability. These differences influence participation and outcomes, shaping who benefits and who is disadvantaged. Thus, even as buyouts are lauded as a non-structural, cost-effective strategy to reduce flood exposure (Kinder Institute 2018; Salvesen et al. 2018), emerging research underscores that they also function as a double-edged sword, capable of reducing risk in some dimensions while exacerbating inequities and displacing vulnerable populations.

Equity concerns in buyout programs operate along two distinct but interrelated dimensions. First, equity issues emerge for households and neighborhoods that remain adjacent to buyout sites, where vacant lots, declining property values, and fragmented social networks can generate new forms of vulnerability (Binder et al. 2020; Brandon 2019; Hashida and Dundas 2023). Second, equity concerns also arise for households that participate in buyouts, particularly those from marginalized communities, who may face inadequate compensation, wealth loss, or displacement into less desirable neighborhoods (De Vries and Fraser 2012; Jowers, Ma and Timmins 2023). These dual dimensions highlight that buyouts are not only hazard mitigation tools but also mechanisms that can inadvertently reproduce socio-spatial inequalities.

There are a few drawbacks to buyout programs: local buyout projects can scatter communities and displace residents (Phillips, Stukes, and Jenkins 2012), often disrupting social networks and leading to dissatisfaction or isolation in new neighborhoods (Perry and Lindell 1997). Additionally, households remaining in buyout neighborhoods can suffer from neglect by implementing agencies (Binder et al. 2020), exposure to future disasters (Brandon 2019), and community disruption due to delays, mismanagement, and derelict land patterns, all of which can lower housing values and erode community cohesion (Siders, Hino, and Mach 2019). Recent empirical work also shows that voluntary buyouts and acquisitions can significantly depress nearby property values in the short term, with effects varying by program type and spatial proximity (Hashida and Dundas 2023). Such findings highlight that buyouts may transmit signals of decline or vulnerability to the surrounding housing market, reinforcing concerns about long-term disinvestment and socio-spatial inequality.

At the same time, equity issues are experienced by participating households. Even when participation is framed as voluntary, evidence suggests that many residents can feel constrained or pressured to accept buyouts due to limited alternatives and policy structures (De Vries and Fraser 2012). Building on these critiques, a growing body of recent scholarship has drawn attention to the equity dimensions of buyouts, including how program design, implementation, and post-buyout outcomes disproportionately affect marginalized communities (Greer, Brokopp Binder, and Zavar 2022; Kraan et al. 2021; Manda, Jerolleman, and Marino 2023; Zavar et al. 2023). These studies underscore how buyouts, while framed as voluntary and cost-effective, can inadvertently reproduce structural inequities and environmental injustice through the displacement of vulnerable populations and uneven access to retreat opportunities. De Vries and Fraser (2017) highlight how local discretion and weak oversight can result in post-buyout land use decisions—such as relocating flood-damaged homes into marginalized neighborhoods—that perpetuate environmental and racial injustice. Thus, a deeper examination of buyout impacts is warranted, particularly as emerging research highlights their potential to produce long-term, uneven, and often invisible consequences for already vulnerable communities.

These equity concerns are further complicated by inconsistent findings across the literature regarding where buyouts are implemented and who benefits. At the national level, some studies suggest that buyouts disproportionately favor wealthier, whiter areas—possibly due to greater political influence or institutional capacity (Elliott, Brown, and Loughran 2020). Conversely, other research argues that low-income neighborhoods are more likely to be targeted due to the cost-effectiveness of acquiring low-value properties, aligning with cost-benefit analysis logic (Mach et al. 2019; Zavar and Fischer 2021). While economically rational, this strategy often results in the displacement of already vulnerable populations and reinforces long-standing racial and socioeconomic inequities. Moreover, recent work finds that even when buyouts occur in historically marginalized communities, compensation gaps persist, and homeowners of color tend to receive lower payouts relative to property value, often exacerbating wealth disparities (Jowers, Ma, and Timmins 2023). Scholars have also pointed out that cost-benefit analysis tools themselves may embed structural biases by undervaluing social cohesion and prioritizing efficiency over equity (Greer, Brokopp Binder, and Zavar 2022). These apparent contradictions in the literature reflect variation in scale of analysis (national vs. neighborhood), metrics (targeting vs. acceptance vs. compensation), and equity interpretations. A more holistic understanding of buyouts requires attention to both racialized patterns of implementation and the economic rationales guiding program design, as well as their differentiated impacts on both those who leave and those who stay.

Racial and Ethnic Turnover during and after Floodplain Buyouts

Recent buyout research has increasingly focused on understanding the long-term effects of buyouts on racial/ethnic dynamics within communities (Loughran, Elliott, and Kennedy 2019; Martin 2019; Siders 2019). Loughran et al. (2019), using urban ecology as a theoretical lens, demonstrated that floodplain buyouts are more than mere relocations; they reshape the racial fabric, with a notable shift in predominantly white neighborhoods toward increasing Hispanic populations while keeping black residents, implying a shift toward a middle-income group. However, the implications of their study are somewhat constrained by an analysis that did not compare trends in buyout areas with changes in non-buyout neighborhoods.

Siders (2019) presents a theoretical anticipation of outcomes based on an analysis of eight major buyout programs, suggesting that buyouts, often guided by a cost-benefit rationale, tend to favor the wealthier, white-dominant neighborhoods. Similarly, Martin (2019) identifies a pattern of what is commonly referred to as “white flight” in buyout areas—drawing from theories of neighborhood succession, where the arrival or proximity of non-white buyout recipients can sometimes trigger the out-migration of white households. In this study, we define white flight as a significant, sustained decline in the non-Hispanic white population within a neighborhood (i.e., Census block group) over multi-year periods, particularly in response to racial compositional changes or perceived shifts in neighborhood identity or risk.

Meanwhile, Krysan and Bader (2009) show, through survey data, that African Americans often express a strong preference for living in racially similar communities and are often influenced by both cultural cohesion and experiences of discrimination in majority-white areas. These findings align with Crowder and South (2008), who argue that black residents exhibit lower residential mobility compared to whites, due in part to structural constraints but also to a preference for neighborhood continuity. Such findings from broader urban studies point to the relative racial stability of predominantly African-American urban neighborhoods; this refers to a stability shaped not only by structural constraints (Sharkey 2013) but also by strong social networks, place attachment, and a collective preference for remaining in culturally cohesive spaces. This perspective complicates assumptions of uniform neighborhood turnover and highlights the importance of contextualizing racial dynamics within localized historical and social processes.

In brief, these empirical and theoretical explorations offer critical insights into racial dynamics. Yet, there remains a scarcity of studies fully examining the complex interactions among different racial and ethnic groups during and after buyouts. More specifically, these limited explorations of racial and ethnic shifts induced by buyouts suggest they feed into broader patterns of social vulnerability and disadvantage. In other words, both the out-migration of some groups and the concentration of others reveal how buyouts intersect with the two equity dimensions highlighted earlier: the destabilization of neighborhoods for those who remain, and the disproportionate burdens borne by those who relocate. This dynamic informs what we term the hypersocial vulnerability or disadvantage hypothesis, namely that buyouts are enhancing concentrations of socioeconomically vulnerable minority populations in neighborhoods with higher flood hazard exposure, thereby undermining the resilience of these households and communities in the face of ongoing and future socio-environmental challenges.

To fully explore the nuances of this hypothesis, this study examines the longitudinal impact of floodplain buyouts on neighborhood racial and ethnic composition compared to the overall trends in racial composition across the past two and a half decades in Harris County, Texas. Specifically, this hypothesis is explored by examining the consequences of the incidence of buyouts, neighborhood income, and the scale of buyouts. Our general expectations are that buyouts will lead to white flight, particularly from higher income areas, with greater concentrations of Hispanic and relative stability among non-Hispanic black populations. In addition to a unique quantitative assessment, qualitative insights gained from a small sample of interviews with households involved in the buyout process are offered.

Methodology

Study Area, Data Sources, and Turnover Trends

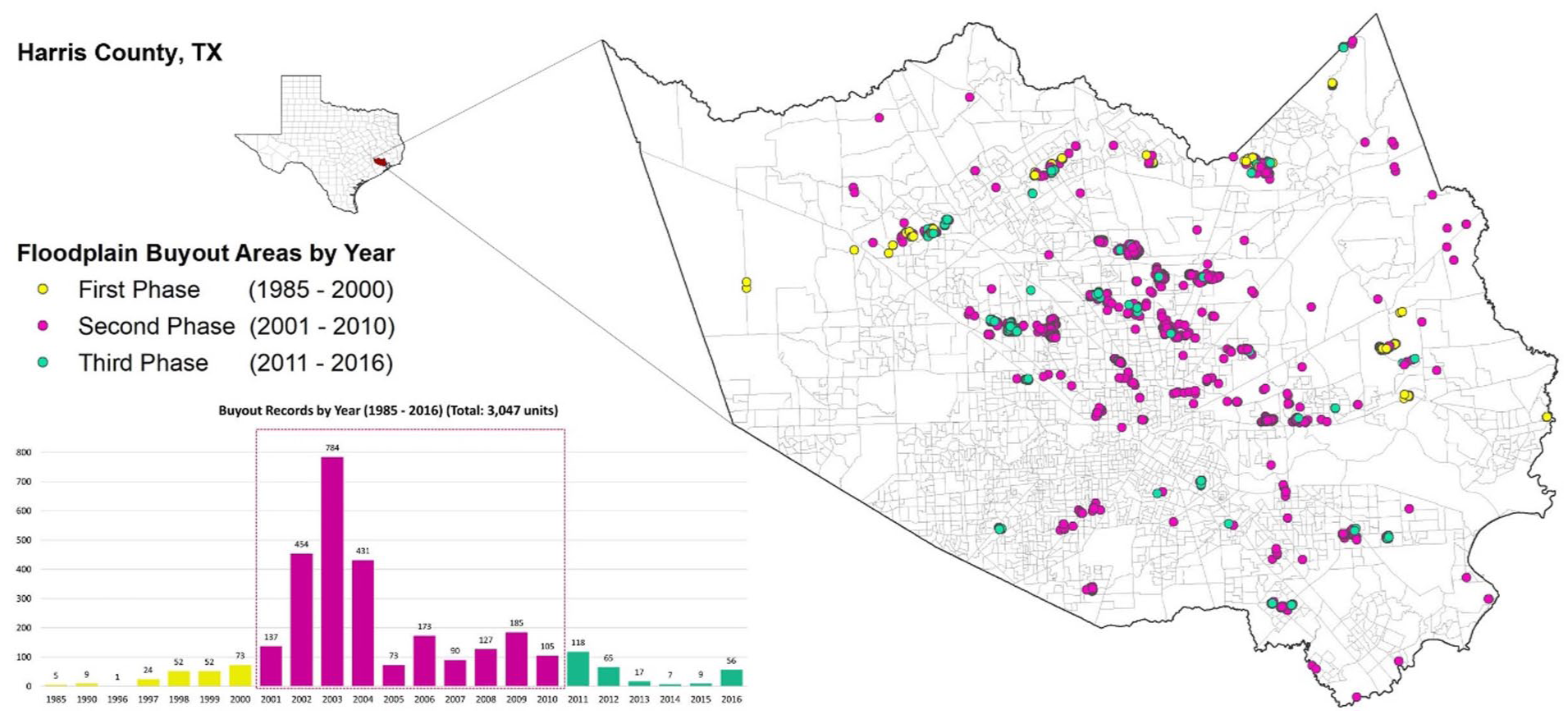

Harris County, hosting the U.S.’s largest buyout program with 3,100 buyout cases since 1985 (Figure 1), accounts for about 14 percent of FEMA’s Hazard Mitigation Grant Program (HMGP) funds. Buyout activity in the county accelerated following Tropical Storm Allison in 2001 and continued to expand after Hurricane Ike in 2008 as well as the 2015 Memorial Day floods. Marked by both its demographic diversity and vulnerability to natural disasters, Harris County’s primary racial and ethnic groups—Hispanic (43.7%), non-Hispanic white (28.7%), and non-Hispanic black (20.0%)—constitute over 92 percent of the population.

Locations of buyout cases in Harris County (1985–2016), Texas, and the frequency of buyout cases by year.

Among the diverse types of buyout programs implemented across the United States, this study specifically focuses on those funded by HMGP, administered by FEMA in Harris County, where approximately 98 percent of buyout implementation in this area has occurred under this program. Our focus is intentionally narrowed to HMGP-funded buyouts to assess the specific policy’s impact on the longitudinal and dynamic shifts in neighborhood-level demographic change among non-Hispanic white, Hispanic, and non-Hispanic black populations.

This study uses a blend of data from the Harris County Flood Control District’s buyout records, the normalized Decennial Census data from 1990, 2000, and 2010, provided by Geolytics, and the 2011–2015 American Community Survey (ACS) from the Census Bureau. 1 Complementary GIS datasets on local highways, central business districts (CBD), water bodies, and parks, and data from the Home Mortgage Disclosure Act (HMDA), provided by the Consumer Financial Protection Bureau (CFPB), were integrated to account for political-economic influences on neighborhood shifts. To account for neighborhood flood risk, we used a time-invariant variable (P_Floodplain) measuring the share of each block group within FEMA-designated Special Flood Hazard Areas (SFHAs). This variable was derived from the Harris County Flood Control District’s Flood Education Mapping Tool, based on the 2007 countywide FEMA Flood Insurance Rate Map (FIRM) and subsequent Letters of Map Revision. The 2007 FIRM, the first comprehensive update using modern hydrologic, hydraulic, and topographic data, provides a consistent baseline for our 1990–2015 study period. While this approach does not capture interim changes in SFHA boundaries, it ensures spatial comparability and long-term consistency for evaluating buyout effects.

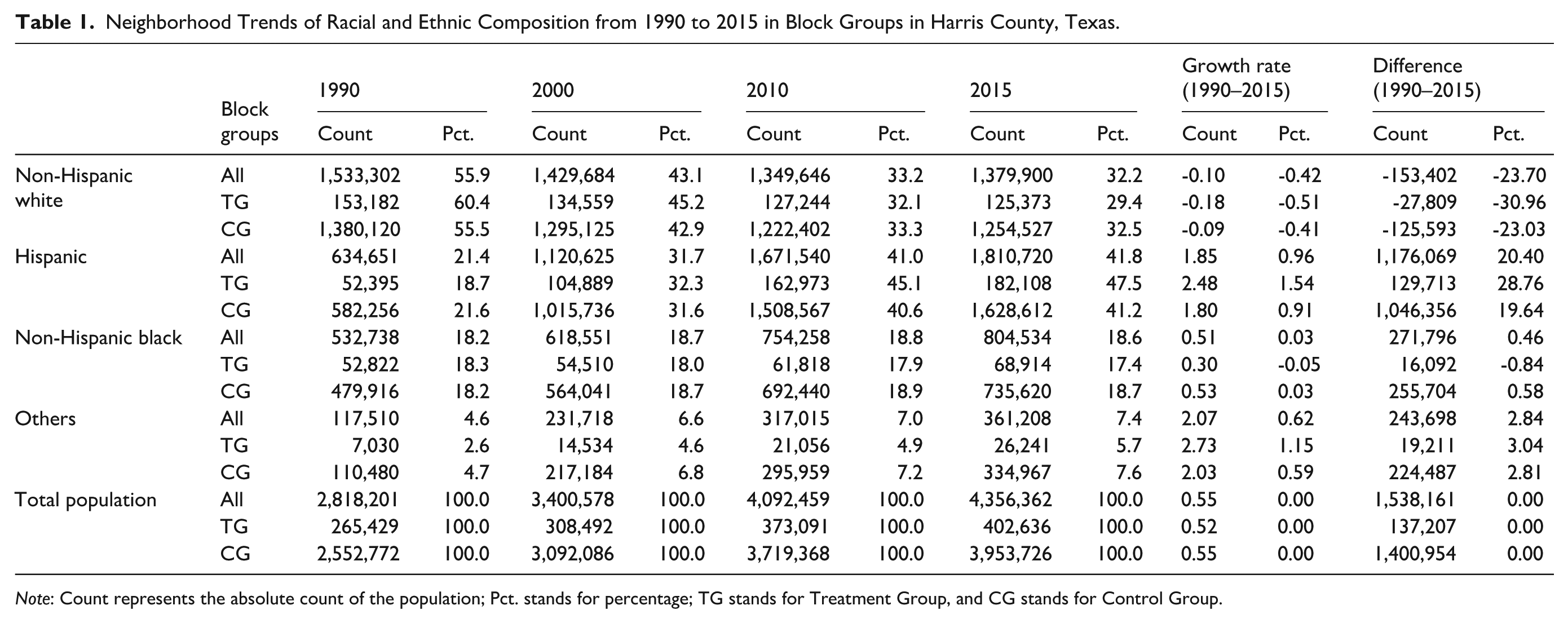

For the data analysis, STATA 16.1, ArcGIS, and Atlas.ti software were used. To provide an overall picture of neighborhood trends with respect to racial/ethnic composition and in relation to buyouts, Table 1 presents the average population sizes and racial/ethnic compositions for Harris County block groups overall and for block groups that have or have not experienced at least one buyout across the time periods under consideration.

Neighborhood Trends of Racial and Ethnic Composition from 1990 to 2015 in Block Groups in Harris County, Texas.

Note: Count represents the absolute count of the population; Pct. stands for percentage; TG stands for Treatment Group, and CG stands for Control Group.

Non-Hispanic white percentages fell overall from 55.9 percent in 1990 to 32.2 percent in 2015, a difference of -23.7 points. Importantly, the percentage point losses are higher for those block groups that had at least one buyout (−31.0 pts) versus those without buyouts (−23.0 pts). These trends contrast with Hispanics, who saw an overall increase from 1990 (21.4%) to 2015 (41.8%) of 20.4 percentage points. Again, consistent with our hypothesis, the percentage point gains were much higher (28.8 pts) in buyout than in (19.6 pts) non-buyout block groups. The percentages of non-Hispanic blacks were remarkably stable across the period, whether considering percentages across all blocks or between the two groups. These trends are consistent with expectations, suggesting higher levels of white flight and either increasing concentrations of socially vulnerable Hispanic populations or at least stable, relatively high concentrations of non-Hispanic blacks in block groups with buyouts. Additionally, it should be noted that while populations are increasing in absolute numbers in buyout block groups, this is suggestive that we are seeing turnover and growth, not simply changes due to population loss with minorities being left behind. The question remains as to whether these patterns hold after controls and other factors are introduced and whether income has particularly significant consequences.

Methods

This study employs mixed methods for a complementary integration of quantitative and qualitative analytic approaches. Mixed methods allow researchers to collect and analyze both quantitative and open-ended qualitative data to compare and contrast findings, offering methodological flexibility (Wisdom and Creswell 2013) for a more comprehensive assessment of our research hypothesis. Specifically, this study follows an explanatory sequential design, in which qualitative data were collected after the quantitative phase to help interpret and extend the statistical findings (Creswell and Creswell 2017; Creswell and Plano Clark 2017). The in-depth interviews were intended to provide contextual understanding—particularly around observed demographic shifts, social dynamics, and community responses to buyouts. This design enhances the interpretive power of the quantitative models and offers a more nuanced understanding of the lived experiences behind the data.

Piecewise Discontinuity Multilevel Longitudinal Analysis

For the quantitative analyses, this study uses a piecewise discontinuity multilevel longitudinal analysis to compare changes between the pre- and the post-trajectory of the buyouts, using the year 2000 as a pivot. This year marks a natural breakpoint just prior to the spike in buyouts following Hurricane Allison in 2001, and it aligns with the Decennial Census data, allowing for a clear before-and-after comparison. Block groups with buyouts initiated prior to 2000, including those with continuing acquisitions afterward, were excluded from the analysis to ensure treatment status aligns strictly with the post-2000 breakpoint, thereby avoiding bias from earlier buyout activity.

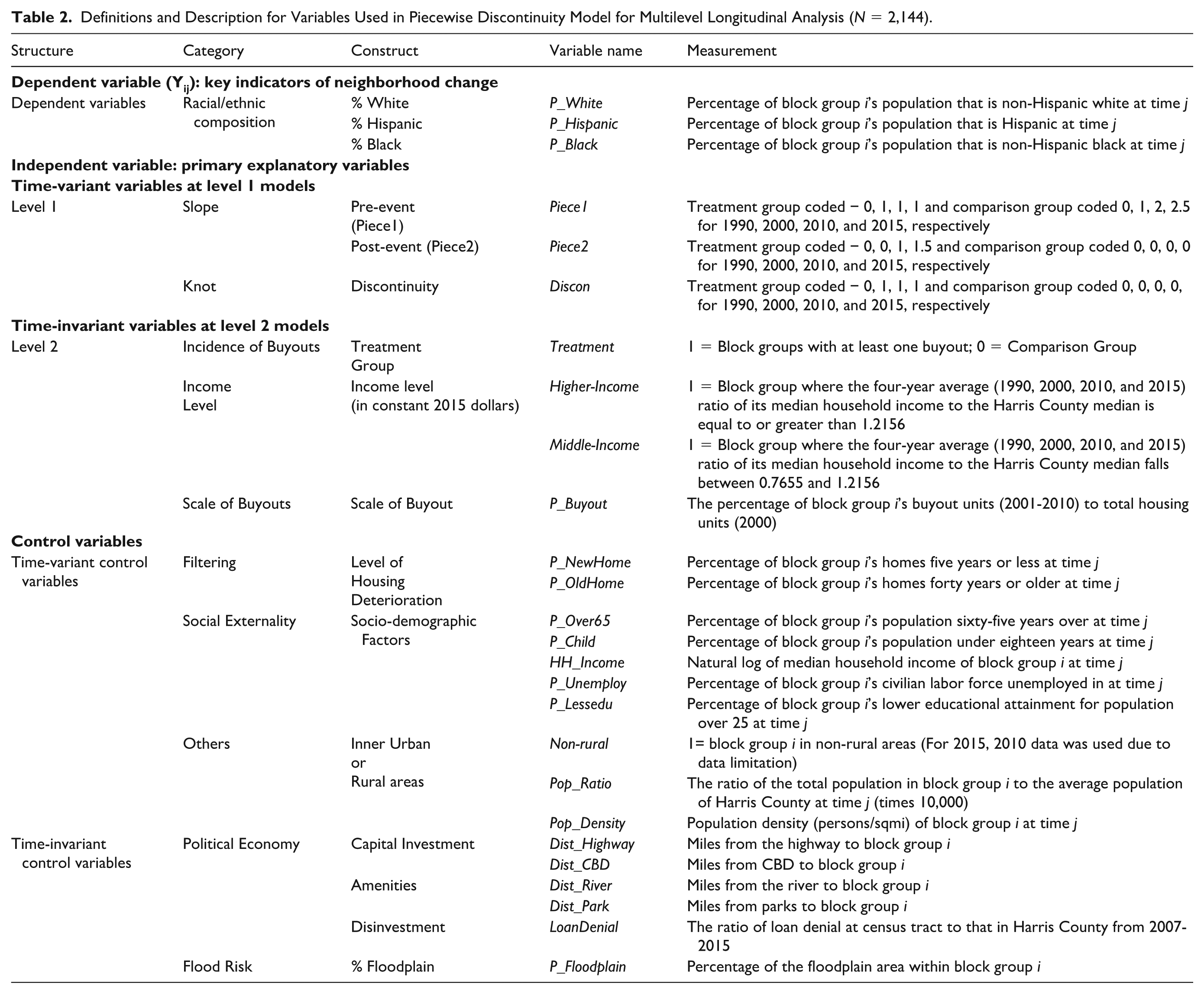

Because our dataset includes repeated measures of neighborhood-level characteristics across four time points (1990, 2000, 2010, and 2015), we use a two-level multilevel model where time (level 1) is nested within block groups (level 2). This structure accounts for the non-independence of observations within the same block group over time and enables us to estimate both within- and between-group variation in demographic change. Given that Harris County is rapidly growing and annexing new territory with block group (our neighborhood areas) changes over time, we used the normalized decennial census that provides adjusted weighted census data that accounts for geographic changes over time (Geolytics 2019). To test the hypersocial vulnerability/disadvantage hypotheses, a series of piecewise discontinuity models, including time-variant and time-invariant control variables generally associated with underlying factors shaping neighborhood change based on the literature review and a set of strategically coded independent variables to capture variables of the impacts of buyouts, trends before and after 2000, and discontinuity in these trends are employed. Primary among the latter is a dummy or indicator coded “1” for block groups that experienced at least one buyout forming a quasi-experimental treatment group, while block groups without buyouts (coded “0”) form the control or comparison group. Additionally, a discontinuity (capturing the break year of 2000) and two trend measures (termed pieces) provide the basic building blocks to capture hypothesized differential in intercepts after 2000 as well as decennial slope trends across the entire period (1990–2015) between treatment and comparison neighborhood groups in racial/ethnic composition due to buyouts. Table 2 provides descriptions for the variables used in the piecewise discontinuity multilevel longitudinal model analysis, and Supplemental Appendices 1 and 2 show the descriptive statistics for time-variant and time-invariant variables, respectively.

Definitions and Description for Variables Used in Piecewise Discontinuity Model for Multilevel Longitudinal Analysis (N = 2,144).

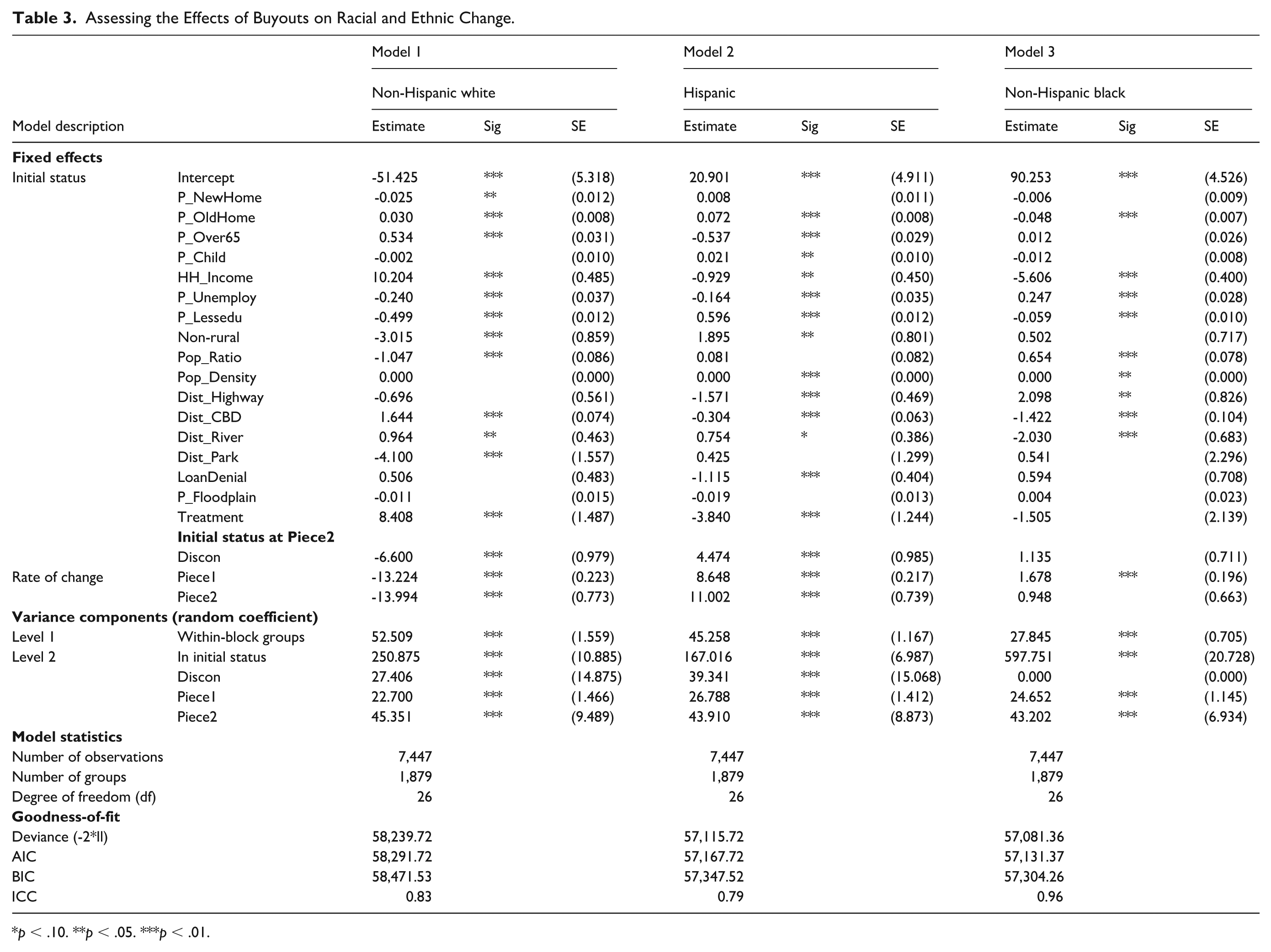

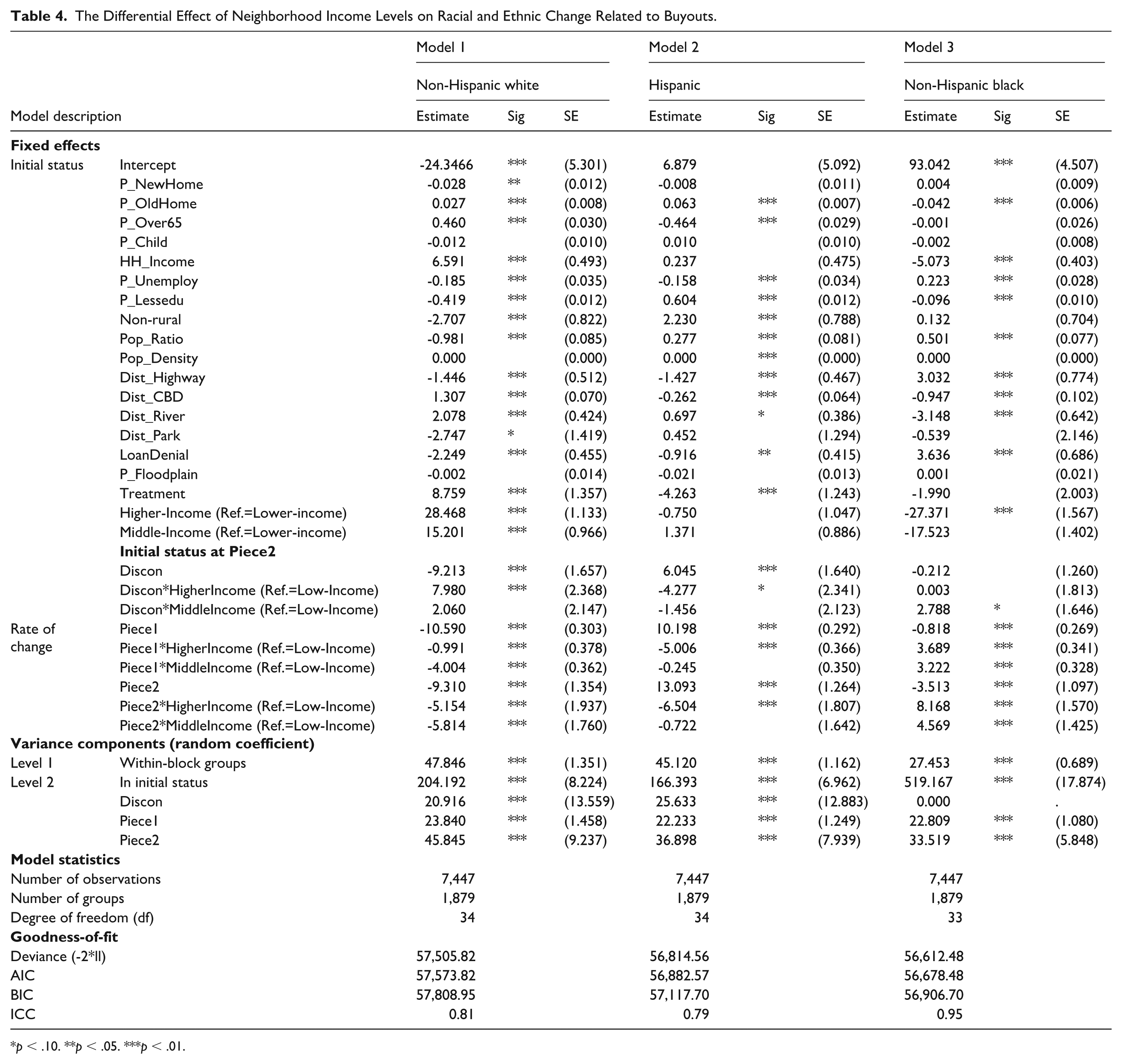

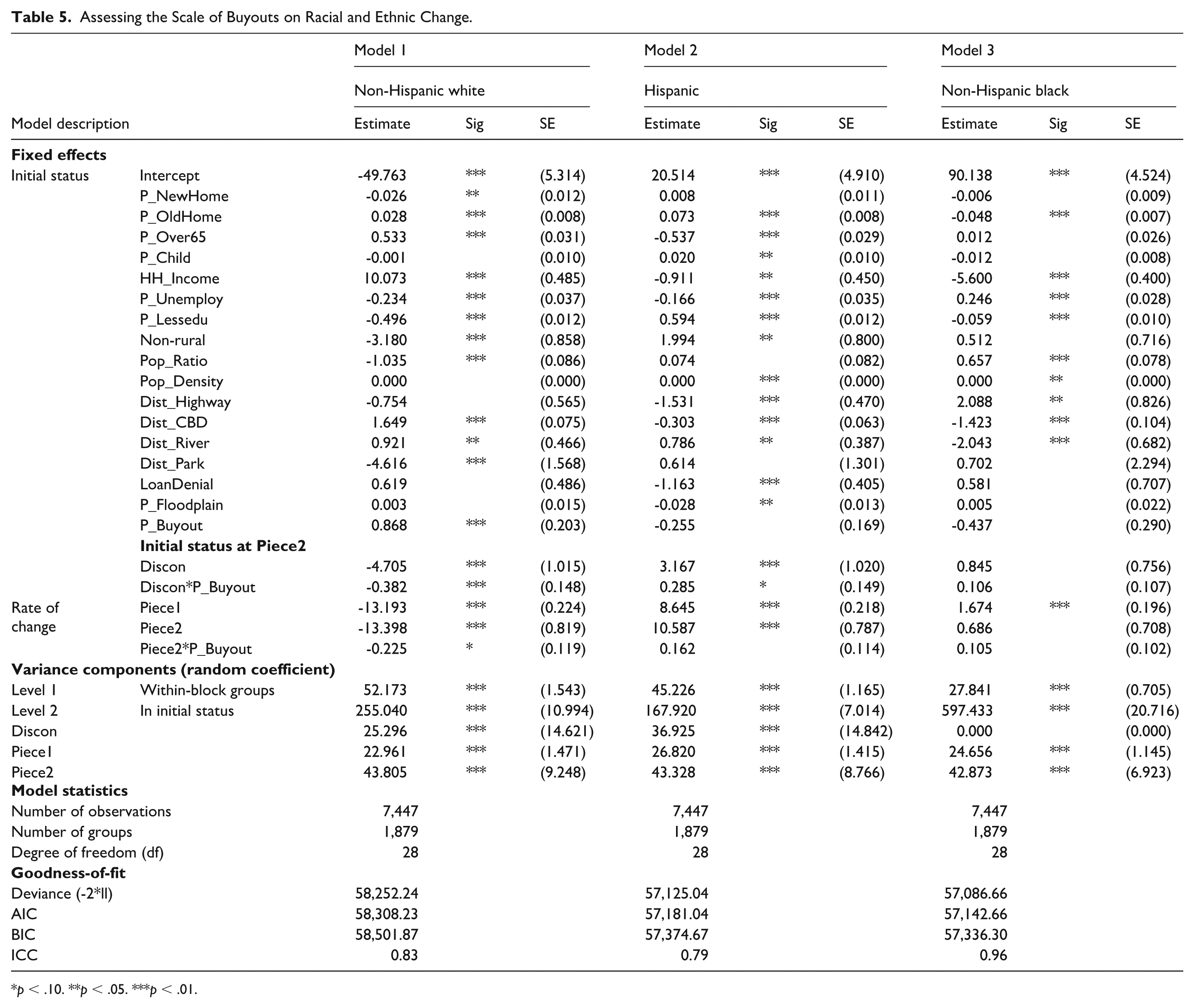

Three sets of models are offered to test the consequences of buyouts more fully and better assess the nature of the factors shaping racial/ethnic compositional change across the period. To account for potential correlation within groups and non-constant error variance, we employed Restricted Maximum Likelihood (REML) estimation within a multilevel modeling framework, which directly models correlated errors through random effects rather than relying on post-estimation corrections like robust standard errors. Table 3 offers results for the basic set of models that estimate the consequences of buyouts for racial/ethnic composition for non-Hispanic white (model 1), Hispanic (model 2), and non-Hispanic black (model 3) populations in neighborhoods by introducing three time-predictors into the level 1 sub-model and the treatment group dummy (Treatment), indicating at least one buyout implementation into the level 2 sub-model. It is hypothesized that treatment effects will be positive in the white model, but negative in the Hispanic and non-Hispanic black models, yet discontinuity and slopes will be negative in the former and positive in the latter. In combination, these findings indicated that buyouts are happening more in non-Hispanic white neighborhoods but resulting in higher concentrations of minority populations and with greater or hyper effects in buyout neighborhoods. The specific equation for the conditional piecewise discontinuity model with the buyout effect is provided in Supplemental Appendix 3. Table 4 presents a second set of Models that assesses the nonlinear effects in high-, medium-, and low-income neighborhoods for racial/ethnic change, both in terms of intercepts and slopes. Specifically, block groups are categorized into three income levels based on their median incomes across the period of interest, as specified in Table 2. These models include dummy coded variables for block groups with high-income and middle-incomes, with low-income block-groups serving as the reference category. Supplemental Appendix 4 presents the equation used for the conditional piecewise discontinuity model with the income level effects. Table 5 presents a final set of models evaluating the effects of the scale of buyouts (P_Buyout) among block groups with different levels of buyouts. Since the scale of buyouts can only impact racial/ethnic composition after the transition year, and during the second “piece” or phase, P_Buyout was included in the intercept, piece2, and discontinuity equation at level 2. The equation detailing how buyout scale effects are modeled within the conditional piecewise discontinuity framework can be found in Supplemental Appendix 5.

Assessing the Effects of Buyouts on Racial and Ethnic Change.

p < .10. **p < .05. ***p < .01.

The Differential Effect of Neighborhood Income Levels on Racial and Ethnic Change Related to Buyouts.

p < .10. **p < .05. ***p < .01.

Assessing the Scale of Buyouts on Racial and Ethnic Change.

p < .10. **p < .05. ***p < .01.

Semi-Structured Interviews

Semi-structured, in-depth interviews were conducted with residents to provide additional insights into the quantitative findings. 2 A modified version of Dillman’s (1978) recruitment approach using direct mailers was sent to 120 relocated buyout participants and 153 remaining homeowners from buyout neighborhoods in November 2020. The home addresses of buyout participants were located using the online address lookup service FastPeopleSearch.com. Despite two mailouts and offers to conduct interviews via phone or Zoom, only ten homeowners (five each from the buyout and non-buyout groups), representing a response rate of 3.7 percent, agreed to be interviewed, which lasted between forty and sixty minutes. The COVID-19 pandemic drastically impacted recruitment and participation in the survey. The interviews were transcribed and coded using Atlas.ti, employing a standard iterative open, inductive coding approach initially (Miles, Huberman, and Saldaña 2018), followed by a hierarchical coding frame based on repetitive concepts and phrases. While the number of interviews is small, the resulting findings provide additional insights that should not be ignored and, hence, will be discussed below.

Findings

Results of Longitudinal Analysis

Incidence of buyout models

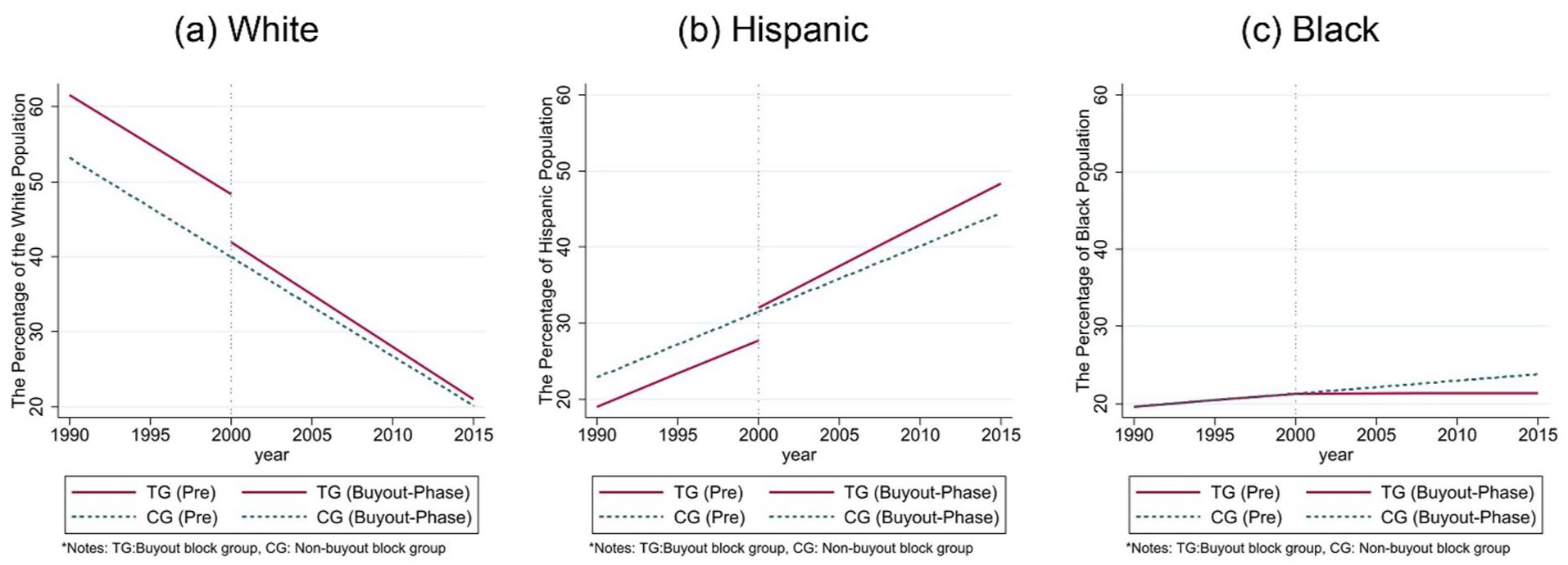

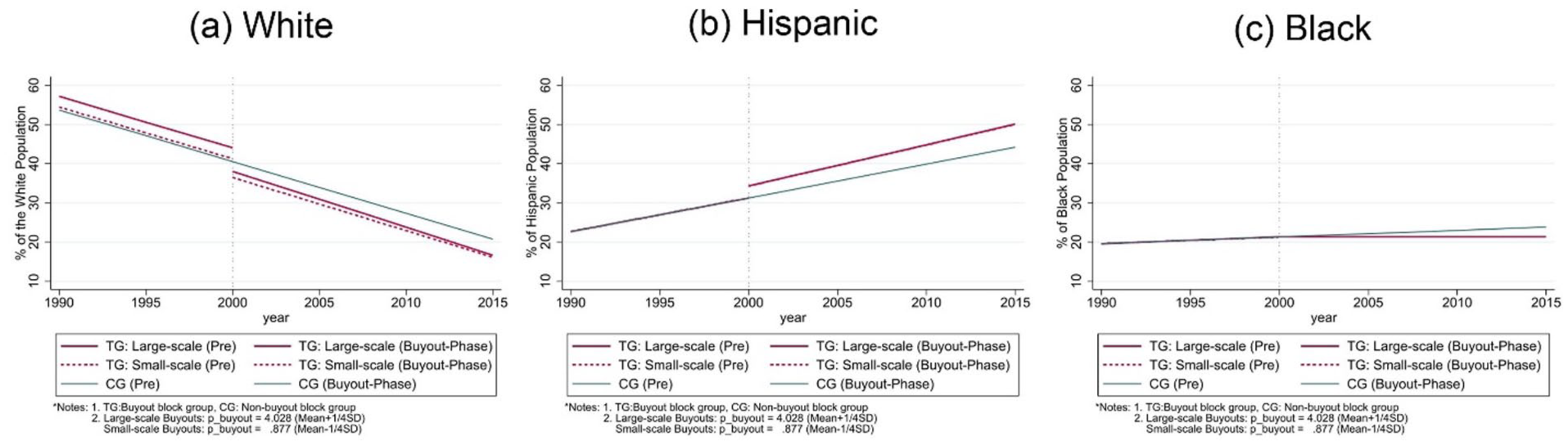

Table 3 presents the three controlled piecewise discontinuity models assessing the effects of the incidence of buyouts for each race/ethnic composition, respectively. The findings for the non-Hispanic white and Hispanic models are consistent with the hypothesized expectations. First, the treatment coefficients in models 1 and 2, respectively, suggest that buyout block groups have, after controlling for other factors, a significantly higher percentage (8.1 pts) of whites and a significantly lower percentage (−4.4 pts) Hispanics than in respective comparison block groups. Furthermore, the discontinuity coefficients in each model suggest that following 2000, treatment block groups were significantly less white, by 6.6 points, and more Hispanic, by 4.5 points. Finally, the rates of change overall were toward reduced white percentages in model 1 and increased Hispanic percentages in model 2 (see piece1 and piece2 coefficients); the trends were doubled across the decades in treatment neighborhoods. These variations are illustrated graphically in the first two panels of Figure 2.

The buyout effect on the percentage of (A) white, (B) Hispanic, and (C) black populations.

The findings for non-Hispanic black percentages (model 3) are quite distinct in that they suggest relative stability. The nonsignificant treatment variable suggests no differences in non-Hispanic black percentages between buyout and non-buyout neighborhoods, nor is there evidence of discontinuities post-2000 for treatment neighborhoods. The findings for piece1 suggest a significant increase in black percentages of 1.7 percentage points over the decades, but there are no detectable slope variations for treatment neighborhoods. Thus, the results support our hypothesis that the incidence of buyouts is more likely in areas with higher concentrations of non-Hispanic whites and less likely in areas with higher concentrations of Hispanics. Additionally, the decadal trends also suggest higher percentage point losses of non-Hispanic whites and gains in the Hispanic population in buyout neighborhoods. However, the findings with respect to non-Hispanic black concentrations do not suggest buyouts are occurring in areas with lower black concentrations, nor is there evidence of increasing concentrations or tends in that direction post-2000 in buyout neighborhoods.

Differential effects across neighborhood income levels

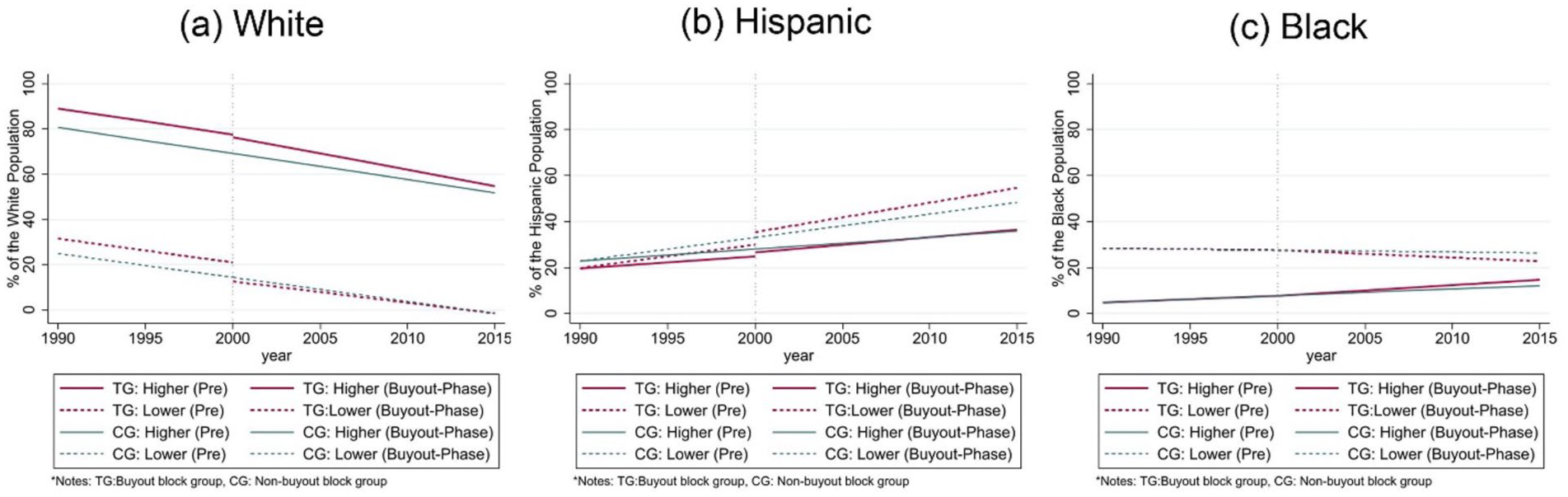

Table 4 displays models assessing the additional consequences of neighborhood income levels. First, it should be noted that the treatment effects display the same cross-model patterns and magnitudes as seen in Table 3; however, the discontinuities following 2000 display substantially different patterns. Focusing on the discontinuity variable and associated neighborhood income interactions that capture shifts in treatment block groups, model 1 suggests a 9.2 percentage point loss of whites in low and middle-income neighborhoods post-2000, while the decrease is only about 1.2 percentage points in high-income neighborhoods. Conversely, model 2 indicates that the Hispanic population increases by about 6.0 percentage points in low-income and middle-income neighborhoods while increasing by about only 1.8 percentage points in high-income buyout neighborhoods. Thus, the racial/ethnic shifts from non-Hispanic white to the Hispanic population largely occurred in poorer and middle-income neighborhoods when considering the post-2000 buyout period as a whole.

The slope effects (piece1 and piece2), as well as associated neighborhood interactions, in model 1, indicate decadal losses in white percentages. However, when considering the added rates of change over the decades for treatment neighborhoods (piece 2), the results of model 1 suggest that rates are more pronounced and negative in middle- and upper income neighborhoods. After 2000, low-income treatment neighborhoods lost 9.3 percentage points in the white population per decade, but the combined decreases were −14.5 and −15.1 points per decade, respectively, in high and middle-income neighborhoods. Although the decreases in the white population in high and middle-income neighborhoods are not statistically different from each other, both decreases are greater than in low-income neighborhoods after 2000 (p < .01, respectively). The stark discontinuity post-2000 for low-income treatment neighborhoods and significant slope variations for all treatment neighborhoods are readily apparent in Figure 3, panel A. Conversely, model 2’s results for piece1, piece2, and associated interactions indicate that Hispanic populations grew, particularly in low- and middle-income neighborhoods, relative to high-income neighborhoods. However, the results were even more pronounced in buyout areas where, on average, low-income block groups experienced an additional 13.1-point gains in Hispanics, with essentially the same holding for middle-income buyout neighborhoods, but gains were only 6.6 percentage points per decade in affluent neighborhoods. Again, in Figure 3, panel B displays the 2000 breaks and steeper slopes, particularly in low-income treatment neighborhoods, reflecting growth in Hispanic percentages that can clearly be visualized.

The added impact of income level on the percentage of the (A) white, (B) Hispanic, and (C) black population.

The results for model 3 related to non-Hispanic black percentages are again quite different, particularly with respect to the Hispanic model. The treatment variable is not statistically significant, suggesting no variations in buyout versus non-buyout areas, and there is no discontinuity effect, although there is a marginally significant discontinuity middle-income effect, suggesting a potential increase in black populations in middle-income buyout neighborhoods. The results with respect to post-2000 trends overall (piece 1) and with respect to buyout areas are particularly interesting. The overall trends indicated a significant percentage point (0.8 point) reduction in the black population each decade in low-income neighborhoods but significant increases of 2.9 and 2.4 percentage points in high- and middle-income neighborhoods, respectively. This pattern is even more pronounced for buyout neighborhoods where low-income areas saw dramatic percentage point losses of 3.5, but high- and middle-income areas saw added gains of 4.7 and 1.1 points per decade, respectively.

The patterns for non-Hispanic white and Hispanic composition are generally consistent with expectations, while the findings for non-Hispanic black composition are distinct and more nuanced. Buyouts are happening in areas with relatively high white concentrations, and there is rather a rapid decline in white concentrations, suggestive of significant white flight post-2000 in low- and middle-income buyout neighborhoods. The trends in white flight from all neighborhoods are evident throughout the post-2000 period but are clearly higher in buyout neighborhoods, particularly in both high- and middle-income neighborhoods. On the other hand, buyouts are more likely to be associated with neighborhoods with lower concentrations of Hispanics, and yet post-2000, buyout areas, particularly in low- and middle-income neighborhoods, experienced significantly higher increases in the percentage of Hispanics. Increases in Hispanic percentages did occur in high-income neighborhoods. However, the levels were approximately half those experienced by low- and middle-income neighborhoods. Overall, these findings are quite consistent with the hypersocial vulnerability/disadvantage hypothesis. When considering non-Hispanic black populations, we again find no treatment effect, nor is there a significant relatively sudden growth in black concentrations following 2000. There is a general increase in black concentrations overall, but when considering buyout neighborhoods, there is actually a decline in the percentage of blacks in low-income buyout neighborhoods but significant increases in the percentage of blacks in high-income neighborhoods. Thus, there is an increase in concentration, but it is more indicative of high-income neighborhoods.

The scale of buyouts

Table 5 presents models assessing the scale of buyouts, measured as the percent of total block-group housing units bought out, on the change in non-Hispanic white, Hispanic, and non-Hispanic black composition. These models do not explicitly include the “treatment” variable since, by definition, non-buyout block groups are those in which the scale is equal to zero. At the initial status in model 1, a 1 percent increase in buyouts results in a 0.88 percentage point increase in whites, clearly indicating that buyouts were occurring in neighborhoods that had a greater white concentration. While the effect is marginally significant in model 2, buyouts declined with a higher percentage of Hispanics. In model 1, the discontinuity measure suggests that the whole neighborhoods with any buyouts experienced a 4.7 percentage point loss in the white population post-2000, and the interaction indicates that for every percentage point increase in housing units bought out, there was an additional 0.38 percentage point loss in whites. In model 2, the discontinuity effect indicates that in buyout neighborhoods, there was a significant increase of 3 percentage points in Hispanics post-2000, and for every percentage point increase in housing units bought out, the Hispanic percentage increased by 0.29 points. The results for models 1 and 2 also suggest that overall, there were declines in the white population and increases in the Hispanic population across all neighborhoods (see piece 1 in both models). However, both the white losses and Hispanic gains were substantially enhanced in buyout neighborhoods (see piece 2 in both models). Furthermore, for every additional percentage point increase in housing units bought out, white percentage points fell by 0.38 points, as shown in Figure 4. Finally, the results for model 3 suggest that the scale of buyouts did not have a significant added effect on the black population concentrations, both immediately and throughout the buyout phase. In sum, the results show that buyouts accelerate the normal trend of a decrease in the white population and an increase in the Hispanic population in buyout neighborhoods but yielded no impacts on non-Hispanic black neighborhood concentrations.

The impact of the buyout scale on the percentage of the (A) white, (B) Hispanic, and (C) black population.

Results of Semi-Structured Interviews

Based on the results from the longitudinal quantitative analysis—showing that neighborhoods undergoing floodplain buyouts experience significant demographic shifts from predominantly white populations toward greater Hispanic representation, particularly in high-income areas—we developed subsidiary research questions for the in-depth qualitative interviews to deepen and contextualize these findings. Specifically, the qualitative interviews explored the following questions: Why and how do wealthier white households move out of buyout neighborhoods? What makes people decide to either participate in the buyout program or stay in a flood-prone neighborhood? And do the buyouts intensify neighborhood inequality?

Wealthier homeowners have options for residential mobility decisions

Floodplain buyouts are a favored solution for residents frequently impacted by floods, allowing them an escape from disaster traps. As was found in the quantitative analysis, particularly in Table 4, buyouts appear more likely in non-Hispanic white and high-income areas. This trend may be partially attributed to homeowners in these areas receiving, from their perspective, more favorable or “fairer” offers. Such a pattern is consistent with other literature findings, which suggest that benefit-cost analysis in buyout programs often results in higher offers for properties in upper income or high-property-value areas. Our qualitative interviews provide evidence that supports for this observation. A couple of homeowners from upper income areas reported receiving offers they perceived as favorable, enabling them to relocate to homes outside the 100-year floodplains and in newer neighborhoods: (Through the buyout) I was able to buy a house that doesn’t flood. I was able to buy a larger, newer house and a house in a little bit nicer neighborhood. (High-income white Homeowner A) They told me that, once you did the buyout, you have to find a new home that was not located in a floodplain, which was fine. It made sense to me that they also paid the moving costs. . . . I felt that I got fair market value. . . . So, for me, it was a win-win situation. I moved away from an area that had flooded, where homes were already demolished, and the values were declining. And I was able to move to a new area that was not in a floodplain. And I got great value for the home. (High-income white Homeowner B)

In contrast, low-income homeowners faced markedly different challenges. Their experiences often involved receiving offers that were perceived as inadequate, failing to provide them with similar opportunities for relocation: My house was worth double what they were offering. And it was not enough money to move to a place where I’m comfortable living. It was not even equal, and they wouldn’t even negotiate on it. (Low-income black Homeowner E)

Concerns regarding potential declines in property values due to the neighborhood buyout program are widespread among homeowners, transcending socioeconomic boundaries. While homeowners with high-valued properties, including those viewing their homes as real estate investments, have expressed concerns about the potential impact on the local housing market, it is crucial to recognize that this anxiety is not confined to wealthier homeowners alone. Historical context, as mentioned by Wilson in the 1980s, shows how fluctuating property values critically impact middle- and low-income minority households, leading to reduced wealth accumulation, limited mobility, and increased vulnerability to gentrification (Wilson 2012). These groups often face disproportionate value losses and bear a heavier burden due to their relatively lower levels of wealth and income. The impact of any loss in property value can be more consequential for them, underscoring the need for a more inclusive understanding of these concerns.

A number of high-income homeowners, particularly those with sufficient financial resources, opted to participate in the buyout program early on. Their decision was influenced by the opportunity to receive compensation based on the pre-disaster fair market value of their homes, aiming to avoid potential depreciation in property values: I believed if I stayed, the value of my home would diminish. I would not get fair market value because if I was even ever able to sell it, I didn’t know if people would buy it there. No one knows it’s flooded, but buyers are able to see all of the homes being taken out around it. (High-income white Homeowner A)

While shared across various income levels, this issue manifests differently based on homeowners’ financial capabilities. In our study, a low-income white homeowner (Homeowner F) expressed their concerns, which mirror the understanding about property value decline: Becoming a parking lot and nobody living there caused the (home) price to go down. . . . Everybody left. So, there was no property value left. That is why we could not sell the house. (Low-income white Homeowner F)

It not only highlights the universal concern over property values but also sheds light on a critical issue: the lack of options for low-income homeowners. They face the same fears of declining property values, but with limited financial resources, their ability to relocate is constrained. Finding affordable housing outside their current neighborhoods can be a significant challenge, leaving them with fewer choices in the wake of neighborhood transformations.

Some chose to stay in the flood-risk areas because they prefer living in a less populated residential environment. They felt the living environment became even better after the buyout as it provided them a quieter place to live within the Houston area, which is relevantly closer to the downtown area, with a reasonable home value. As wealthier residents are likely to have the option to choose whether or not they relocate, the reason to remain in the flood-prone area was one of their voluntary decisions based on their geographic preference: Having fewer people in the neighborhood, more empty plots, more trees or plants, makes it perhaps a more pleasant place to live. It’s less populated, which is sort of rare to find in Houston. . . . This was even within the Houston city limits, but it seems almost rural. (High-income white Homeowner C)

Financial and informational obstacles for poorer homeowners for relocation

Low-income minority homeowners expressed frustration about finding affordable housing to which to relocate through the buyout program. They felt the buyout compensation was not enough to find a home of equivalent quality, a better location, or a safer area, restricting their choices to substandard homes and neighborhoods with conditions no better than those they left. Thus, in many cases, they chose to remain in flood-prone areas due to complex social and financial reasons. A statement reinforcing this claim from a respondent is: I can’t afford that. I found several houses that I would move to. And neither one of them is in Harris County. That would mean I would have to move out of the County. (Low-income Hispanic Homeowner D)

Low-income homeowners faced significant challenges during the buyout process, particularly regarding the impacts on their lives. The homeowners observed the consequences of the buyout program on the neighborhood setting and also indicated that emotional, psychological, and logistical challenges were significant factors in their decision-making process: I think if my parents felt it wasn’t enough to justify the emotional, psychological, and logistical challenges associated with moving, then I sort of trust their judgment on that. . . . I get the sense that it wasn’t nearly enough to move to somewhere kind of similar. (Low-income Hispanic Homeowner G

3

)

Not having flood insurance was another significant barrier to buyout participation for low-income residents. Since the program is only eligible for residents with flood insurance who have reported flood damages over time, wealthier residents are more often eligible for the buyout applications while relatively excluding many low-income minority homeowners as they are less likely to have flood insurance: Many of them (neighbors) did not get offered the buyout because they did not have flood insurance. . . . Several of the people were confused about that. They didn’t realize that they would not be bought out if they didn’t have flood insurance. (Low-income Hispanic Homeowner H)

Shift in racial composition from white to Hispanic

Our findings indicate a trend among some financially able residents to swiftly accept buyout offers they deemed fair. Notably, this was observed more among our white interviewees, who moved out early in the program, often receiving reasonable relocation packages. In contrast, those who entered the program later faced reduced property value offers. During this process, the richer white population with financial resources who wanted to relocate swiftly took the buyout offer and moved out of the flooded districts, while minority groups filtered in: The demographics have shifted primarily from Caucasian to Hispanic. I think that’s sort of the biggest change there, . . ., families of color have moved in while Caucasian families and maybe single people have moved out. (Low-income Hispanic Homeowner G) . . . More Hispanic families remained. (Now) I’m the only White person down here. . . . Everybody that was White has moved out, you know, hundreds of them. And now there are just young Hispanics that live there. (Low-income white Homeowner F)

In neighborhoods where homeowners remained because they did not take or were not offered buyouts, real estate prices fell, and there was a significant migration of minorities—mainly Hispanics—into the neighborhoods, accompanying white flight. Non-white families began to move in, primarily in areas where buyouts were executed, and this tendency progressively spread to properties near buyout properties as housing prices decreased.

However, given our sample’s limited diversity, particularly the lack of middle and upper income people of color, the authors note that these observations cannot be generalized across all demographics, highlighting certain tendencies rather than providing a comprehensive overview of all homeowners’ experiences in the buyout program.

Discussion

Both quantitative and qualitative studies indicate a racial shift in neighborhoods immediately upon buyout implementation, with a notable decrease in the white population. Quantitative data highlights intensified racial changes in affluent, predominantly white neighborhoods undergoing large-scale buyouts. Our qualitative study found that wealthier white homeowners often have more relocation options due to higher insurance payouts, allowing them to quickly escape from hazardous areas.

Qualitative interviews provided deeper insights into these statistical patterns, clarifying the mechanisms underlying neighborhood change. Resident narratives revealed that wealthier white homeowners typically had greater flexibility and financial resources (often due to higher insurance payouts and better access to relocation assistance), which enabled them to rapidly move away from flood-prone areas. This qualitative finding vividly illustrates why demographic transitions appeared swift and pronounced in the quantitative analysis for high-income neighborhoods. Conversely, interviews also highlighted how low-income minority homeowners, constrained by financial limitations and fewer affordable housing alternatives, frequently faced significant barriers to relocation, thereby remaining in hazardous areas longer. These qualitative perspectives illuminate why low-income neighborhoods experienced less immediate demographic turnover, reinforcing and contextualizing quantitative observations of slower demographic shifts in low-income areas. Overall, the findings reinforce the statistical findings of neighborhood racial/ethnic composition changes, where all buyout areas experienced a decline in the white population and an increase in the Hispanic community, while little changes are observed in the black population.

Given that racial composition is defined by the total of out-migration and in-migration among various racial groupings, the transition from white to Hispanic and the persistence of black populations might be explained through three key factors. First, it might indicate that the white population is fleeing the buyout communities that minority groups leave behind. This shows that the white population will be more inclined than other racial groups to escape a flood-prone location via the buyout program or the housing market. Recent studies on post-disaster buyouts and relocation have revealed that floodplain buyouts and hazard protections disproportionately benefit richer, non-minority neighborhoods (Hersher and Benincasa 2019; Mach et al. 2019; Seong 2021; Seong, Losey, and Zandt 2021; Siders 2019). As a result, floodplain buyouts may result in racial inequity because the program inequitably benefits white communities while leaving others in hazardous areas.

Second, the racial transition from whites to Hispanics may be accounted for by Hispanic in-migration into the buyout communities. From the interviews, we observed a significant increase in rental units and remodeled flooded homes during the buyout process (Hunn and Dempsey 2018), which may attract Hispanics. The literature on neighborhood change and white flight explains that when the threshold for people of color (non-white) hits a “tipping point,” many whites leave the community. In white-dominant buyout communities, a rise in the Hispanic population—induced by an increase in rented or remodeled units and higher housing turnover—might induce transition, causing the white population to leave. Our results support the hypothesis that white flight happens in affluent white-dominant buyout communities, altering the racial composition of the neighborhoods from white to minority groups. These findings prompt thought-provoking inquiries regarding where the departing white residents are relocating and whether their movements may be fueling gentrification in other regions. This aspect may need additional attention in future research.

Third, although we observe a dynamic contrast in the demographics of white and non-white populations in wealthier neighborhoods, there are more muted shifts in black communities in low-income neighborhoods. This disparity, viewed through the lens of hypersegregation (Massey and Denton 1989), is rooted in the historical confinement of black-dominant communities to flood-prone areas due to persistent discriminatory practices. Although buyouts aim to help homeowners relocate from high-risk zones, socioeconomic barriers, and strong community ties may restrict black residents’ participation in buyouts and their residential mobility. Moreover, the simultaneous emergence of a growing Hispanic population alongside a persistent black community in flood-prone areas might inadvertently generate “places of the truly disadvantaged (Wilson 2012)”—zones marked by a concentration of highly vulnerable populations coupled with heightened environmental risk. This evolving landscape calls for actions for those neglected areas and demands further empirical examination to understand the full implications of such policies on urban racial dynamics and their intersection with disaster risk management.

Drawing from both quantitative trends and qualitative narratives, we recommend three key strategies to reduce unintended consequences and enhance the effectiveness of future buyout programs: (1) ensuring equitable retreat policies that consider the differing socioeconomic capacities of households, as highlighted by qualitative insights on relocation constraints faced by low-income and minority residents; (2) strategically integrating buyout initiatives with comprehensive land-use planning policies, informed by many quantitative findings, demographic shifts, and qualitative narratives that illustrate community disruption and concerns; and (3) providing targeted and context-sensitive mitigation infrastructure investment in neighborhoods where buyouts remain incomplete or in progress, which will address qualitative concerns about community resilience, safety, and equity for residents who remain in partially bought-out communities.

Equitable Retreat

To better support low-income minority residents in relocation efforts, governments must ensure that HMGP buyouts incorporate equity-oriented mechanisms already available within the program, especially since financial challenges are one of the primary barriers to relocation (Muñoz and Tate 2016; Shi et al. 2022). For example, FEMA allows supplementary payments when the buyout offer falls short of enabling the purchase of a comparable property outside the floodplain (FEMA 2023). Local administrators should actively apply this option to strengthen participation among low-income households. Additionally, the remaining communities are likely to have a higher concentration of renters living in a variety of different types of housing in low-lying locations (i.e., single-family detached units, duplexes, triplexes, fourplexes, and apartments). Hence, the HMGP program should include such residents by strategically diversifying the purchase alternatives for various types of dwelling units. For renters, who are not direct recipients of HMGP funds, complementary housing supports such as the US Department of Housing and Urban Development’s (HUD) Housing Choice Voucher mobility counseling can be paired with buyout activity to facilitate relocation to safer, opportunity-rich neighborhoods. Together, these programmatic adjustments would help reduce inequities without relying solely on external funding streams.

Integration with Land Use Policy and Community Engagement

To address the concerns about community cohesion following buyouts, it would be beneficial to incorporate policies that transform acquired lots into assets that serve the public good for communities left behind after buyouts. For instance, policies could be developed to repurpose these vacant lots into amenities, such as parks or community spaces, created through active engagement with the local population (Center for Community Progress 2023). This approach goes beyond merely having vacant lots and ensures that these spaces become valuable assets. Inspired by successful strategies in shrinking cities, where vacant areas are often repurposed into recreational zones and community facilities (HUDUser 2014), we can apply similar principles to buyout neighborhoods. Additionally, there is an opportunity to revitalize brownfields or previously contaminated sites within these areas, unlocking their potential while ensuring environmental safety. Given their central location and infrastructure connectivity, these areas offer “location efficiency.” Buyout neighborhoods also present similar advantages. Therefore, agencies executing buyouts can collaborate with government entities to repurpose these spaces, ensuring the optimal use of acquired properties for the benefit of the remaining communities while also speeding up property acquisitions in target areas.

Mitigation Infrastructure Investment for the Remaining Communities

While buyout programs are often viewed as a cost-effective alternative to major structural infrastructure projects—by permanently removing properties from high-risk flood zones—it is important to recognize that buyouts are rarely implemented all at once or across entire neighborhoods simultaneously. In communities where buyouts are ongoing or only partially executed, a gap in protection may remain for households that have not relocated. In these transitional contexts, linking buyout programs to other hazard mitigation strategies can provide critical support for remaining residents during the interim period.

Rather than implementing large-scale structural investments in areas targeted for retreat, this approach emphasizes context-sensitive and complementary solutions that can reduce residual risk while reinforcing long-term resilience goals. For instance, green infrastructure such as subsurface infiltration trenches, stormwater ponds, or underground storage systems may be suitable in neighborhoods vulnerable to localized flooding, especially where full retreat is not feasible. Geographic-information-based strategies—including the preservation of open space along watersheds, the use of permeable soils in urban areas, and ecologically informed buyout targeting—can be integrated into buyout planning to enhance broader community resilience and ecological benefit (Atoba et al. 2021). Thus, targeted, interim, and nature-based investments in areas of partial retreat can support those who remain while advancing equitable and cost-effective flood risk management.

While this study focuses specifically on Harris County, it is important to contextualize its findings within the broader landscape of floodplain buyouts in the United States. Harris County is one of the most active jurisdictions for federally funded buyouts, with a long history of large-scale implementation following repeated flood events. Compared to other regions, Harris County’s demographic diversity, urban scale, and institutional capacity may shape buyout outcomes differently. As such, while the patterns observed here may inform broader discussions about racial and socioeconomic impacts of buyouts, caution should be taken when generalizing to rural areas, regions with different housing markets, or places with less administrative experience in managing buyout programs.

Conclusion

Floodplain buyouts are a useful tool for hazard mitigation for communities and climate change adaptation for households living in impacted areas. Due to the long-term nature of buyout programs, neighborhood change within and surrounding communities is inevitable, and planners should be aware of the environmental, economic, and social consequences caused by buyout implementation. In this study, we highlight that white flight occurred in many buyout neighborhoods in Harris County, TX, shifting the white population to the Hispanic and black families in the buyout-implemented neighborhoods, showing greater impacts on all income level and the large-scale buyout neighborhoods.

Our study has a few limitations that should be noted. First, due to limited data availability, the longitudinal dataset was not identical at four time points. The authors combined the 2011-2015 five-year ACS data instead of using the 2020 Decennial Census, which resulted in the five-year term estimation. Despite the compatibility and reliability assessment of using the Decennial Census and the ACS data, conducting the same analysis with the identical dataset of the 2020 Decennial Census is highly recommended for future research. Second, while P_Floodplain controls for neighborhood-level flood risk, it does not fully capture the differential impacts of actual flooding events or temporal variation in exposure. Therefore, although we can account for general flood-proneness, we cannot perfectly match non-buyout block groups that experienced similar flood impacts to those that received buyouts. Future research could enhance this analysis by incorporating parcel-level flood claims data or detailed flood event histories to more precisely assess the demographic effects of flooding without buyout programs. Third, while the longitudinal piecewise design helps control for neighborhood-specific unobserved characteristics, we recognize that treated and untreated neighborhoods differ on key pre-treatment characteristics, such as flood risk and socioeconomic status. Although we adjust for flood exposure and model within-neighborhood change, we acknowledge that the control neighborhoods do not represent perfect counterfactuals. This limitation should be considered when interpreting causal claims. Future studies could explore alternative matching or weighting strategies to further strengthen the comparison. Fourth, our smaller samples for interviews due to COVID-19 may cause sampling bias as they are unintentionally concentrated in the northern area of Harris County, and most buyout participation occurred between 2008 and 2009. Qualitative studies with larger, balanced samples should be conducted further to verify the results. In addition, future research could benefit from applying more flexible modeling approaches, including machine learning and AI-based techniques such as random forests, gradient boosting, or neural networks. These methods are well-suited to capturing complex, nonlinear relationships and may uncover patterns that traditional models cannot—for example, AI could help identify tipping points in racial or ethnic turnover following large-scale buyouts, or detect nonlinear interactions between income level, flood risk, and demographic shifts over time. Incorporating these tools could enhance our understanding of how environmental interventions reshape neighborhood composition in diverse urban contexts.

Since our study used publicly available data, including the Decennial Census, American Community Survey, and open data from the City of Houston, the approach can be reproducible and generalizable. In addition, methodologically, our longitudinal multilevel analysis can be expanded to test the impacts of other disaster policies (i.e., FEMA’s Hazard Mitigation Grant Program [HMGP], HUD’s Community Development Block Grant Disaster Recovery [CDBG-DR] program, the National Flood Insurance Program [NFIP] or recently introduced Community Disaster Resilience Zones [CDRZ]) or socioeconomic impacts of different types of natural hazards (i.e., urban and coastal flooding, sea-level rise, hurricanes, earthquake). Such methodological applications will assist in a better understanding of pre-and post- changes for climate adaptation. Additionally, we encourage buyout policymakers and practitioners to consider how to best balance efficiency with equity for remaining communities, considering buyouts’ long-term impacts on neighborhoods. Our suggestions inform researchers and practitioners to respond to future needs of understanding and better designing floodplain buyout programs and promoting equitable community resilience.

Supplemental Material

sj-docx-1-jpe-10.1177_0739456X251397310 – Supplemental material for Racial and Ethnic Change in Floodplain Buyout Neighborhoods: Twenty-Five Years of Evidence from Houston

Supplemental material, sj-docx-1-jpe-10.1177_0739456X251397310 for Racial and Ethnic Change in Floodplain Buyout Neighborhoods: Twenty-Five Years of Evidence from Houston by Kijin Seong, Shannon Van Zandt, Walter Gillis Peacock and Galen Newman in Journal of Planning Education and Research

Footnotes

Acknowledgements

The authors would like to thank all the interview participants for their contribution, which has substantially enhanced this research by sharing their personal experiences with floods, property buyouts, and neighborhood change. In addition, special thanks to Mr. James Wade, a Property Acquisition Department Manager at the Harris County Flood Control District, for providing his invaluable insights into property acquisition services.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research was supported through a 2020–2021 Dissertation Fellowship Program at Texas A&M University, the Texas Sea Grant Grants-in-Aid of Graduate Research Program 2019–2021 (NA18OAR4170088) funded by the National Oceanic and Atmospheric Administration (NOAA), and the Center for Risk-Based Community Resilience Planning at Colorado State University through a cooperative agreement with the U.S. National Institute of Standards and Technology (70NANB15H044).

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.