Abstract

This study examines the role of the urban built environment in mitigating or exacerbating flooding. By analyzing census tract-level insurance claims in Miami, we model such relationships during moderate and extreme flood events. Our findings indicate that lower population density, higher urban compactness, and proximity to coastal and riparian zones are linked to elevated flood insurance claims. The study also highlights the potential of nature-based solutions in alleviating flood impacts during extreme events. These insights provide crucial empirical evidence for urban planners and policymakers to adopt a systemic approach considering density, location, and nature-based solutions to foster climate-resilient cities.

Introduction

Flooding is the most common and widespread weather-related natural hazard in the United States (Pralle 2019). It is also among the most frequent and costliest disasters in the nation (FEMA 2017). As flooding is a natural event, it only becomes a disaster when its ramifications interact with human societies, particularly in urban areas where people and valuable assets are densely concentrated. In effect, according to the SHELDUS (Spatial Hazard Events and Losses Database for the United States), direct property damages from flooding (excluding coastal) in urban areas accounted for 73 percent of national total economic losses from 1960 to 2016 (National Academies of Sciences Engineering Medicine [NASEM] 2019). Urban areas emerge as epicenters of severe losses during catastrophic events. For instance, Hurricane Katrina incurred an estimated cost of $170 billion, Sandy $74 billion, Harvey $131 billion, and Irma $52 billion (GAO 2020). In addition to the economic losses, urban flooding can also cause significant social disruption and may even deepen social inequality (Linscott et al. 2022; Moulds et al. 2021).

Across the world, flood-related disasters are becoming more frequent and severe (Wahl et al. 2015). Besides climate change, a key reason is the existing and continuing urban development in flood-prone areas, along with the aging infrastructure in many parts of communities (Fu and Li 2022; Rainey et al. 2021). Urban areas often have a high proportion of impervious surfaces, such as pavement and buildings, which lead to increasing overland flow and discharges during flooding events. Hence, improper design and planning of land use and the urban built environment can make urban areas more susceptible to flooding.

Specifically, different types and spatial configurations of the built environment can explain a community’s varying flood risk as much as its baseline environmental conditions (Brody et al. 2011). While there is a growing body of research examining the relationship between land use and flood damage at the regional level, few empirical studies focus on the actual urban form at a granular spatial scale to investigate the impacts of the built environment on resulting flood damages and losses. In addition, there remains a lack of consensus on how varying built environments can alleviate or exacerbate flood damages in urban areas, thereby calling for more detailed empirical studies to reach an agreement and better support resilient land use or urban design decisions in practice.

Our study aims to contribute to this research gap by empirically investigating the effects of built environment factors on flood losses in urban Miami, Florida. We chose Miami due to its expansive urban footprint, varied urban forms, susceptibility to different types of flooding, and extreme high-risk profile. This study stands out for its: (1) use of more granular spatial units of study at the census tract level; (2) focus on various built environment elements including density/compactness, nature-based measures, and location/proximity, while controlling for geophysical and socioeconomic variations; and (3) differentiation between extreme and moderate flood events. In the following sections, we first examine the literature on urban built environment factors contributing to flood damage. We then describe our research methodology, including the study area, model conceptualization, and analysis. Next, we present modeling results and discuss findings. Finally, we conclude the paper with future research directions.

Urban Built Environment and Flood Damage

Previous studies have indicated that flood damage can be attributed to a combination of drivers (Berndtsson et al. 2019; Winsemius et al. 2016), among which the built environment factors have received relatively less attention. Despite this, in recent years, a growing body of literature underscores the essential role of urban built environment in mitigating flood damage. For example, Löwe et al. (2017) found that shaping urban built environment with flood-resilient plans could be more cost-effective than enhancing the drainage system. Among existing studies, macro-scale land use and land cover (LULC) have been prevalent in explaining flood damage. It is well recognized that impervious surfaces modify the functionality of hydrological systems and raise the frequency and intensity of floods in the watershed (Anderson 1970; Brezonik and Stadelmann 2002; Paul and Meyer 2001). Conversely, wetlands and vegetation cover naturally absorb and store excess water, making them critical components of flood-resilient urban development (Acreman and Bullock 2003; Fletcher et al. 2015; Gill et al. 2007; Yin et al. 2021). Further studies extended the existing evidence on LULC factors that contribute to flooding damage by focusing on urban development patterns and indicated that the compact development is related to fewer reported instances property damage (Brody et al. 2011; Brody, Highfield and Blessing 2015; Brody, Kim and Gunn 2013).

It is worth noting that the role of population density in influencing flood damage has yielded contradictory findings. Most research has shown that population density is related to impervious surface expansion and higher flood exposure (Jongman, Ward, and Aerts 2012; Rahman et al. 2021). For example, Sarkar and Mondal (2020) noted that the risk of flood damage tends to increase in areas with higher population density. However, Löwe et al. (2017) found that addressing population growth by emphasizing multistory apartment buildings over detached single-unit houses can lead to decreased flood risk, aligning higher population density with lower exposure.

Urban built environment factors related to physical compactness also have enriched the existing body of knowledge concerning the intricate relationship between the urban built environment and flood damage. Among these factors, building density has drawn substantial attention (e.g., Bruwier et al. 2020; Mustafa et al. 2020; Soares-Frazão and Zech 2008; Testa et al. 2007; Tomiczek et al. 2016), as it both constitutes impervious surface and increases urban assets’ exposure to flood risk. Furthermore, characterizing building configuration factors, Lin et al. (2021) indicated that the building number ratio and building coverage ratio significantly affect the occurrence of pluvial flooding. Street density, however, presents a more nuanced picture, with mixed effects on flood damage. Several studies asserted a positive association between street density and flooding (Kalantari et al. 2014; Rahman et al. 2021), due to its impedance of water infiltration and propensity to generate runoff surpassing pipe capacities (Mark et al. 2004). In contrast, other research argued that streets can act as artificial barriers against flooding, suggesting that higher street density might even diminish the likelihood of flooding damage (Sarkar and Mondal 2020). In general, these studies utilizing simulations or experiments provided solid evidence that urban built environment factors affect flood damage, but there is still a lack of empirical studies in this field. It is important to consider both population density and physical compactness as they exert distinct mechanisms in influencing the extent of flood damage.

Besides density-related factors, nature-based measures and location/proximity characteristics also play a vital role in explaining differences in flood losses (Berndtsson et al. 2019; Winsemius et al. 2016). Prior studies have clearly documented the important role of urban green spaces and vegetation in providing buffers against negative flood impacts (Brody et al. 2014). Similarly, empirical studies consistently affirm that naturally occurring wetlands have the potential to mitigate the impacts of floods triggered by precipitation and storm surge events (Brody et al. 2011; Costanza et al. 2008). Notably, coastal and waterfront areas suffer from more frequent and intense floods due to rising sea levels (Nicholls and Cazenave 2010). Research has also elucidated that proximity to floodplains, water bodies, and other geographical features could enhance the understanding of the linkage between residential location and flood risks (Brody et al. 2014). In addition, socioeconomic characteristics, such as income, race, education, and housing quality, are deemed essential factors due to their unequal exposure to flood risk (Cutter, Boruff, and Shirley 2003; Fekete 2009; Neumann et al. 2015).

Notwithstanding the existing body of research, several limitations still persist. First, most empirical studies investigating flood losses have been conducted at the watershed and county levels (e.g., Brody et al. 2014; Brody, Highfield, and Blessing 2015), with limited attention given to the micro spatial scale where flood impacts occur. Second, while the importance of urban design-related built environment factors remains pivotal to flood risk management, empirical scrutiny in this realm remains insufficient (Fletcher et al. 2015; Li et al. 2021; White 2008). The effects of certain urban built environment elements, such as population density and physical compactness, remain ambiguous due to contradictory findings. In addition, with the escalating severity of floods attributed to climate change, the impact of the urban built environment on flood damage may vary across disaster scenarios (moderate vs. extreme disasters), an aspect that has been understudied. Therefore, the present study aims to enhance empirical understanding of how the urban built environment at the census tract level influences flood losses during moderate and extreme flood events.

Methods

Research Sample

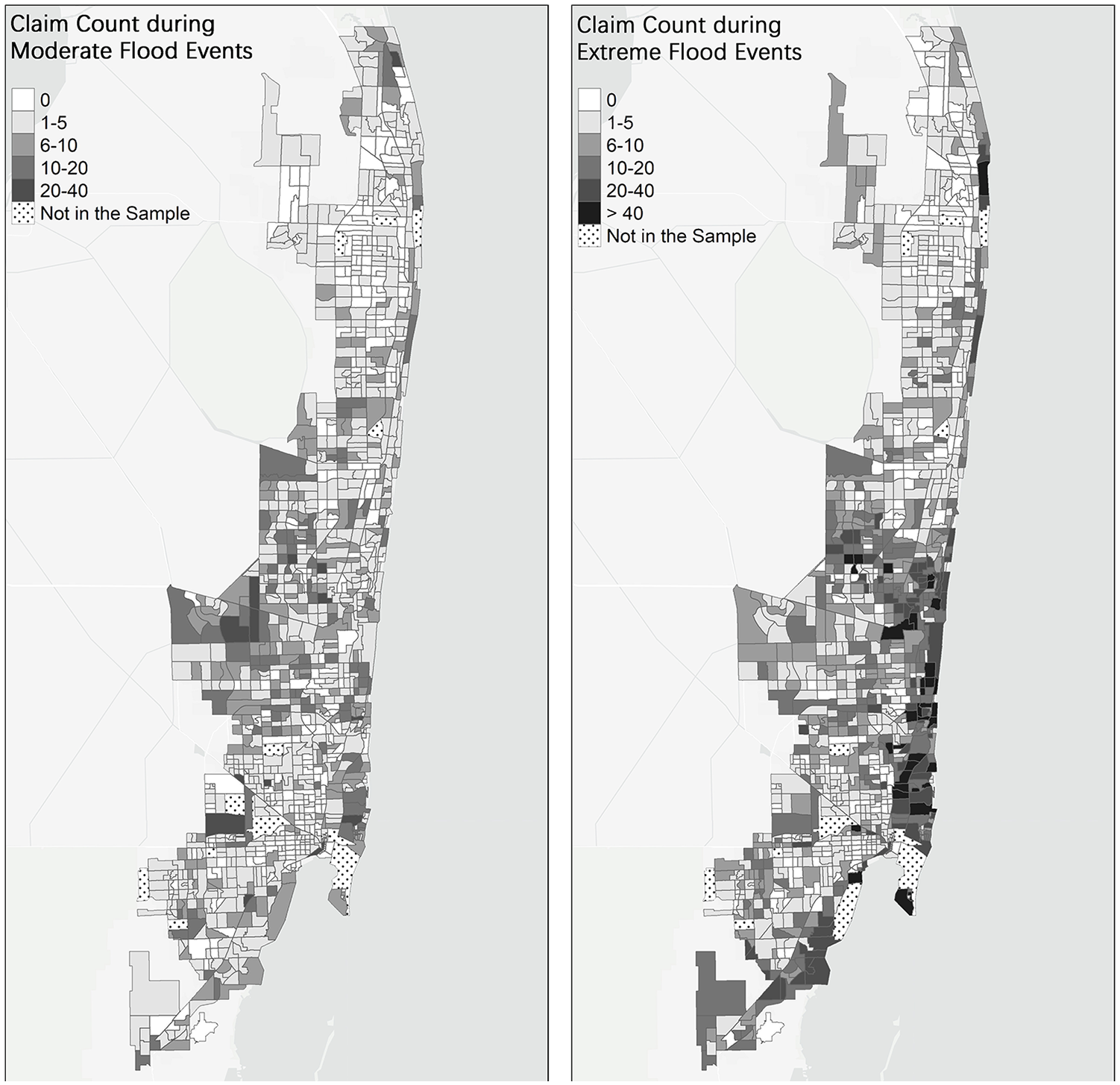

The study area is Miami, Florida, chosen for its extensive urban footprint and vulnerability to hurricanes, thunderstorms, and associated flooding events. We selected 1,143 census tracts within The Miami Urbanized Area boundary as the sample for this study. 1 Notably, with high flooding risk, this area actively participates in FEMA’s Community Rating System program, producing about 2.5 million insurance policies 2 and 12,998 claims from the year 2010 to 2019, which also reflects the variance in flood damage at the census tract level (Figure 1).

Spatial distribution of flood insurance claims during moderate and extreme flood events.

Data and Variables

Dependent variables

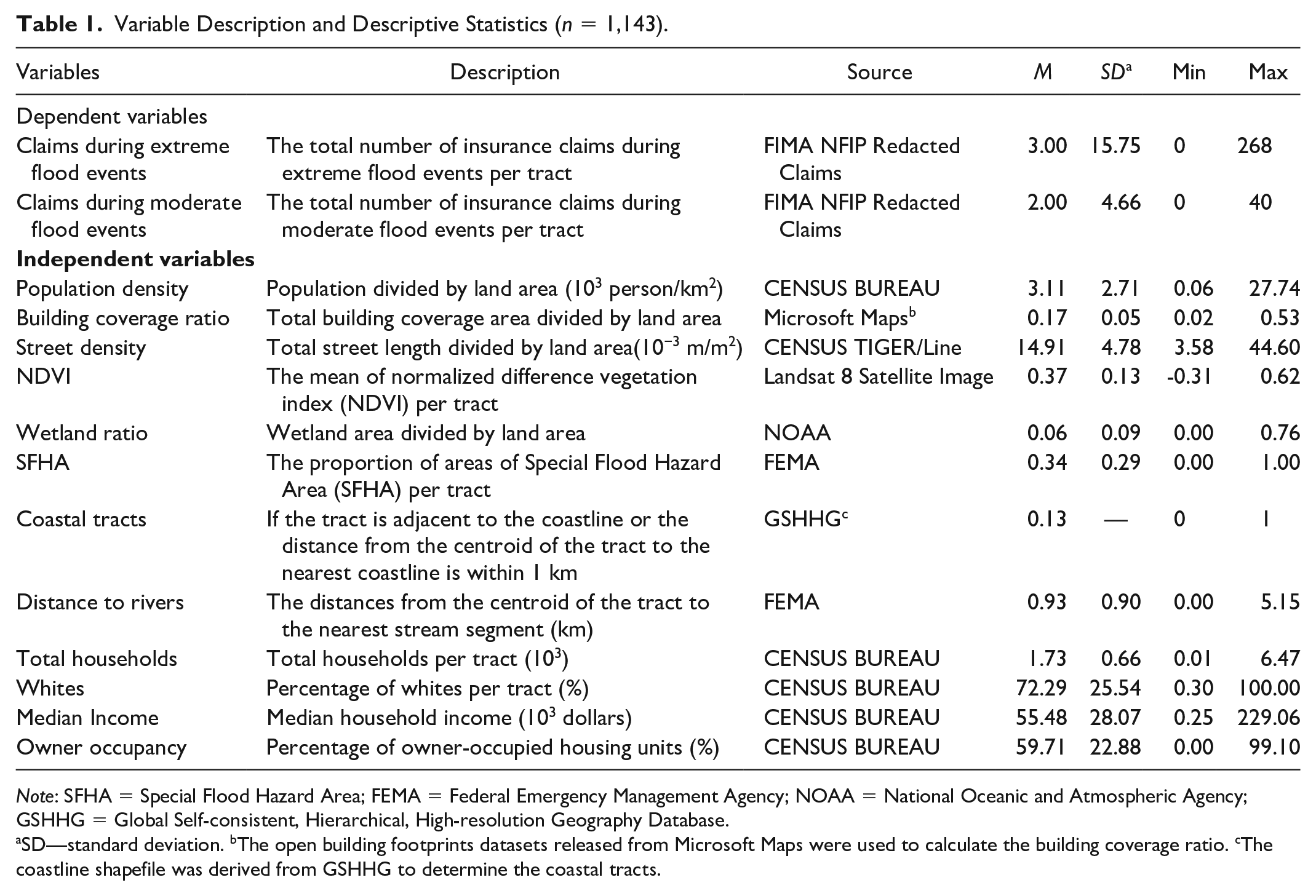

As shown in Table 1, flood damage, the dependent variable of this study, was measured as the number of insured claims per census tract from 2010 to 2019 under the National Flood Insurance Program (NFIP). The data were obtained from the OpenFEMA Dataset, which contains over 2 million claims of insurance coverage for building structures and contents. In this study, we used the number of insured claims to measure flood damage instead of the total dollar loss, to circumvent potential distortion attributed to high-value damaged properties.

Variable Description and Descriptive Statistics (n = 1,143).

Note: SFHA = Special Flood Hazard Area; FEMA = Federal Emergency Management Agency; NOAA = National Oceanic and Atmospheric Agency; GSHHG = Global Self-consistent, Hierarchical, High-resolution Geography Database.

SD—standard deviation. bThe open building footprints datasets released from Microsoft Maps were used to calculate the building coverage ratio. cThe coastline shapefile was derived from GSHHG to determine the coastal tracts.

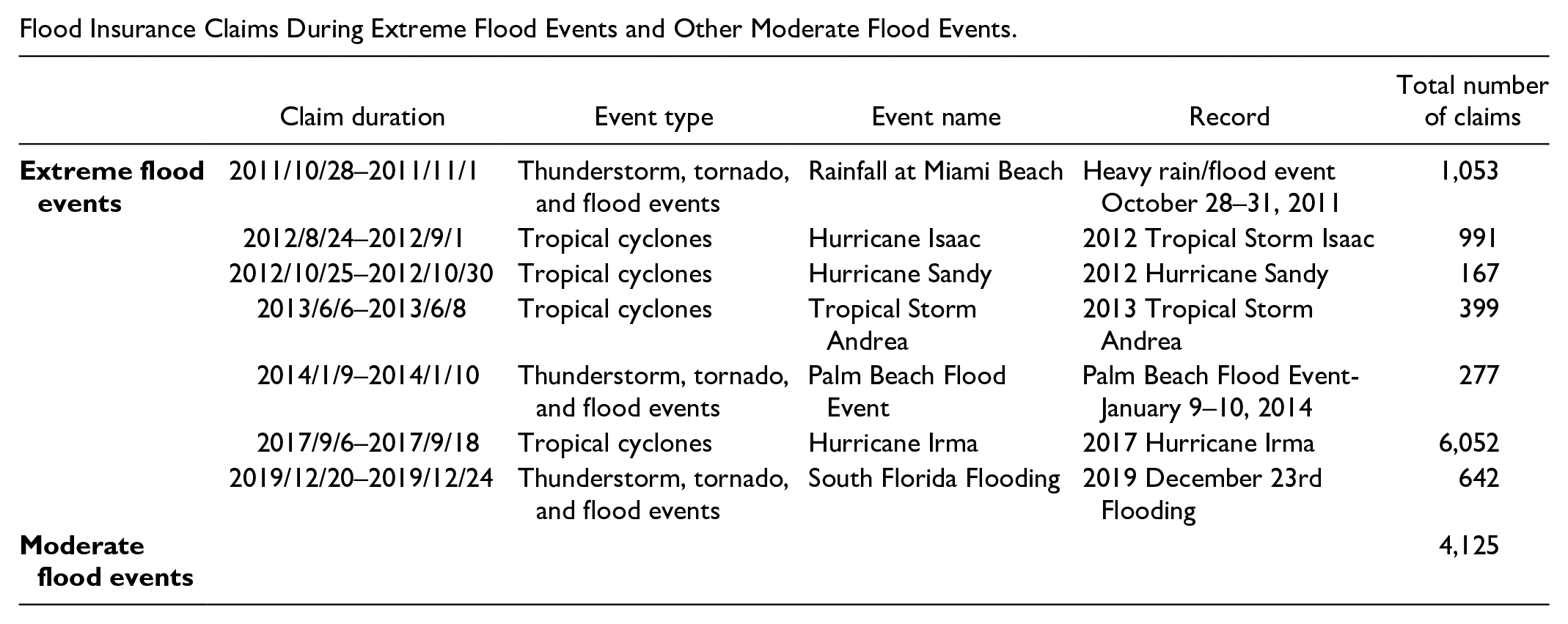

To better depict the heterogeneous effects of the urban built environment on flood damage for different flooding magnitudes, we further differentiated insured claims during extreme flood events and moderate flood events. 3 We identified seven extreme weather events from 2010 to 2019 across Miami-South Florida using the historical information from the National Weather Service (see Appendix 1). We then divided the 12,998 claims into 9,004 claims during extreme flood events and 3,994 claims during moderate flood periods. Finally, we aggregated the number of insured claims at the tract level (Figure 1). Across the 1,143 census tracts, the insured claims ranged from 0 to 40 during moderate flood events. There were generally more claims during the extreme flood events, ranging from 0 to 268.

Urban built environment measures

We considered both population density and physical compactness as important urban built environment indicators that could potentially influence flood damage. Population density was treated as a built environment factor since it often results from corresponding development patterns, reflecting population concentration within a defined geographic area. Unlike population density, street density and building coverage ratio both describe the physical compactness of urban built environments. In this study, building coverage ratio, representing the proportion of land coverage by buildings, was calculated as the total area of building footprint divided by the land area. In addition, we calculated street density as the length of streets from TIGER Streets divided by the total area of the census tract.

We also included nature-based built environment features, as they play a vital role in flood mitigation by absorbing and retaining flood runoff. Specifically, we calculated the normalized difference vegetation index (NDVI) based on the 2016 Landsat 8 images at 30 m × 30 m resolution using Google Earth Engine, which is widely used to measure vegetation intensity in urban environments. We also measured the wetland land ratio within the census tract using the 2016 NOAA C-CAP Land Cover data at 30 m × 30 m resolution.

In addition, we included several location-related measures as urban built environment factors that influence flood damage. The 100-year floodplain, representing areas with a 1 percent annual chance or high risk of flooding, is used to designate Special Flood Hazard Areas (SFHAs) where the mandatory purchase of flood insurance applies. Based on the most current FEMA Flood Maps, we calculated the proportion of 100-year floodplain area per tract. We designated coastal tracts as those adjacent to the coastline or with centroids within 1 km of the nearest coastline, and assigned the value of 1 to costal tracts, while all other tracts were assigned 0, as coastal areas are more susceptible to flooding due to storm surges and sea-level rise. As proximity to inland water bodies increases the risk of riverine flooding, we measured the distance to rivers as the length from tract centroids to the nearest points on the waterline using the most current FEMA Flood Maps and GIS. In addition to urban built environment variables, we also included socioeconomic and demographic features at the census tract level from the U.S. Census, including total households, median income, percentage of whites, and percentage of owner occupancy as control variables.

Analytical Model

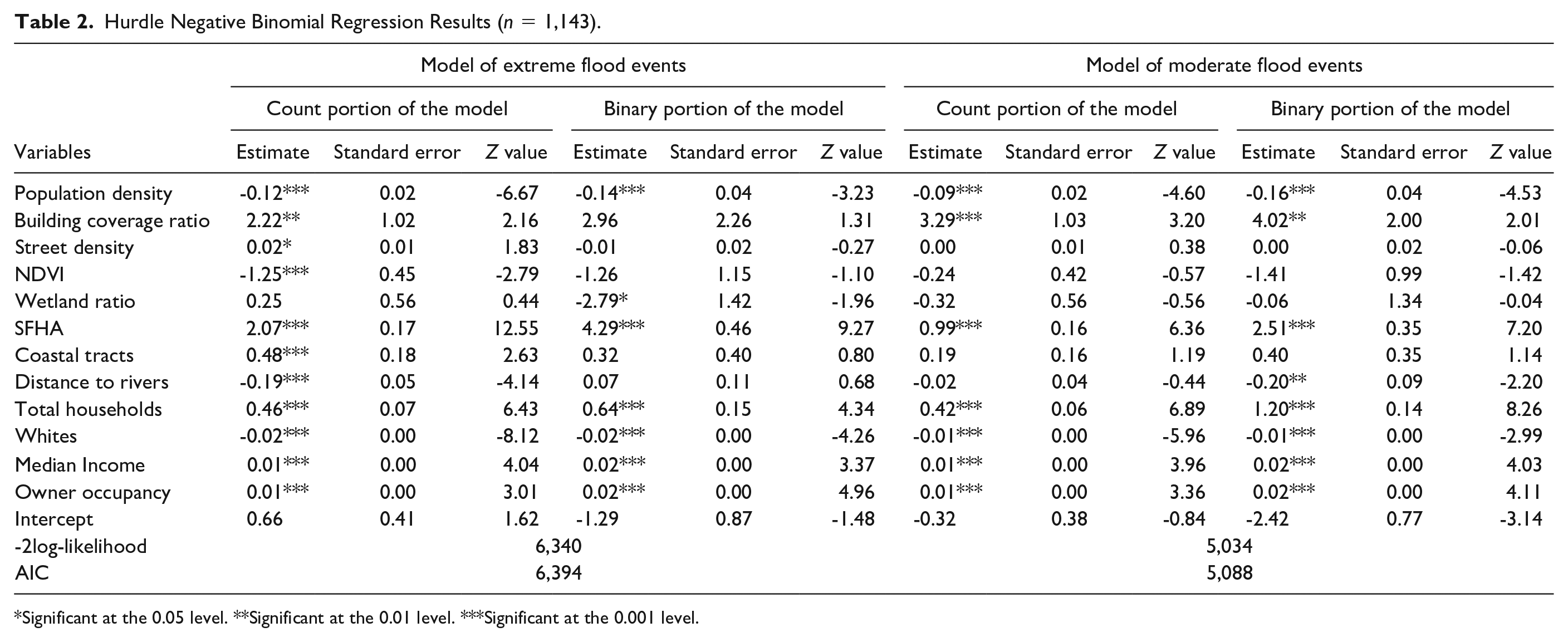

Because our dependent variables were the total numbers of claims per census tract (including excessive zero-value observations) and non-negative counts with over-dispersion, we decided to use the hurdle negative binomial regression model. The hurdle model, with its two-part structure, is employed to differentiate between zero and positive count values in the first part; once the positive count is established, the model proceeds to the second part, which is applied with a truncated count distribution. It is proved to outperform the conventional count models in addressing the issue of excessive zero counts in hazard and traffic accident studies (Son, Kweon, and Park 2011; Tan-Soo et al. 2016; Yu et al. 2019), where all observations are subject to the associated risk of having the outcome. Furthermore, we constructed two separate hurdle negative binomial regression models to further differentiate the heterogeneous effects of urban built environments on flood damage under moderate and extreme flooding events, respectively. The models were estimated using the pscl package in R.

Results and Discussion

Overall, the regression model results suggest that built environment characteristics are significantly associated with flood damage in urban Miami, but these associations may vary during moderate and extreme flooding events (Table 2). Specifically, we found that population density is not only negatively associated with the likelihood of property damage claims at the census tract level (p < .001) but also negatively associated with the extent of damage as measured by the number of claims (p < .001). This association between population density and property damage holds true for both moderate and extreme flood events, consistent with relevant previous studies (Brody et al. 2011; Brody, Kim, and Gunn 2013). This can be explained by several factors, such as better and more robust infrastructure designed to mitigate the impact of flooding, increased resources for timely responses, and higher standards of construction and stricter land-use/building codes in high-density areas. In contrast, low-density developments often lack substantial stormwater drainage systems, and many established or new developments are situated in flood-prone areas deemed relatively safe due to their location outside the 100-year floodplain and/or protection by levees, typically designed to withstand a 100-year flood (Brody, Kim, and Gunn 2013). However, it is increasingly clear that the traditional approach of relying on higher levees or expanding drainage system capacity is inadequate for managing the growing residual risk posed by climate change and ongoing development (Fu et al. 2023). This false sense of security provided by protective structures has been highlighted in recent studies (Bubeck et al. 2017; Serra-Llobet et al. 2022).

Hurdle Negative Binomial Regression Results (n = 1,143).

Significant at the 0.05 level. **Significant at the 0.01 level. ***Significant at the 0.001 level.

While we found fewer claims in areas with higher population density, our results also suggest that more physically compact areas are associated with a higher number of insurance claims for property damages due to flooding. Specifically, building coverage ratio is positively correlated with property damages, both during extreme (p < .001) and moderate flood events (p < .001). In simple terms, more physically compact areas, which have more insured properties and impervious surfaces, experience more property damage due to worse flooding impacts (Du et al. 2015). These results are also consistent with recent simulation studies (Bruwier et al. 2020). Similarly, street density is associated with significantly exacerbated property damage in extreme flood events (p < .01), whereas the association is not significant in moderate flood events. This finding aligns with the literature, which indicates that water in the urban drainage system returns to the streets when the capacity of the pipe system is exceeded during extreme rainfall events (Mark et al. 2004).

From a nature-based solution standpoint, our model results suggest that greater vegetation intensity, as measured by NDVI, is associated with fewer insurance claims, but only during extreme flood events. Having more green spaces and pervious surfaces may not be effective during moderate events, as indicated by our model results. In addition, vegetation intensity cannot prevent property damage during extreme flooding events. However, at the macro-scale, vegetation intensity is negatively associated with property damage during extreme flood events. This may be due to the ability of vegetation to diminish storm surges (Sheng et al. 2012) and absorb rainfall, thereby mitigating property damage. We also found that the presence of wetlands, while not significantly associated with property damages like vegetation intensity, is negatively associated with the likelihood of property damage during extreme events. This suggests that wetlands can prevent extreme flooding (Neri-Flores et al. 2019; Wamsley et al. 2010) from causing property damage, but once the flooding exceeds the wetlands’ capacity, they are no longer effective in reducing damages.

The rest of the explanatory variables in our model also align with our expectations. Specifically, location-based factors are generally associated with potential property damage from flood events. This is evident even without the models, as illustrated in Figure 1, where greater claim counts cluster near the coastline and riparian areas. As expected, the proportion of SFHA within a census tract has significant associations with both the likelihood and the severity of insured property damage, consistent both in moderate and extreme flood events (p < .001). All other variables being equal, coastal census tracts experience more property damage claims from extreme flood events, while census tracts farther from the rivers suffer less flooding damage during extreme flood events. Interestingly, these location factors (i.e., coastal tract, distance to rivers) do not have significant associations with the severity of property damage during moderate flood events, although distance to rivers is associated with a lower likelihood of property damage during moderate flood events. In summary, apart from the form of the urban built environment, location is also key to actual exposure to flooding, reinforcing the importance of spatial planning for reducing flood exposure and risk.

Finally, socioeconomic control variables are also significant predictors of flooding damage in both moderate and extreme flood events. Median household income and homeownership ratio significantly increase insured property damage at the census tract level (p < .001). Although existing literature highlights that people with lower income are more likely to be exposed to higher flood risks (e.g., Rentschler, Salhab, and Jafino 2022), the findings of this study make sense in this context. Higher income and homeownership rate are often associated with greater capacity and desire to purchase flood insurance (Brody et al. 2011; Fu and Nijman 2021), thus leading to more claims. Ironically, census tracts with a higher white population ratio generally have fewer claims in moderate and extreme flood events, indicating a clear racial disparity in terms of flooding damage. This is consistent with prior research on social disparity of flood risk exposure in Miami (Chakraborty et al. 2014).

Conclusion and Future Research

Our study is among the limited body of empirical research that evaluates the influence of urban built environment characteristics on flood-related damage at a granular spatial scale. Specifically, we have investigated the influence of diverse urban built environment attributes on insured property damage arising from both extreme and moderate flood events at the census tract level in Miami, Florida. Our study not only corroborates existing literature on how different urban environments can either exacerbate or mitigate flood damage but also introduces new insights into the potential applications of nature-based solutions for enhancing urban resilience to flooding. Our findings provide essential evidence for urban planners and policymakers to adopt a systemic approach that accounts for density, geographical location, and nature-based solutions in making informed decisions about resilient urban forms and land-use planning.

We observe that census tracts characterized by lower population density, a higher proportion of impervious surfaces, and increased street density are correlated with elevated instances of insurance claims and property damage. To mitigate flood risk from an urban form perspective, urban planners should aim to promote higher population density and reduce urban footprints. This aligns with the existing urban sustainable development agenda, which advocates for compact, transit-oriented development to prevent urban sprawl and mitigate climate change. Flood-risk reduction is another co-benefit planners can now add to the sustainability agenda to make a stronger case. However, increasing density is not necessarily beneficial in all places. In other words, the decision of where to intensify development has critical implications and tremendous opportunity costs due to the expected lifespan of developments and the existing supporting infrastructure. According to our analysis, the geographical proximity of developments to coastal and riparian zones is a key factor that can significantly heighten the exposure to flood risks, leading to an increase in property damage. Urban planners and policymakers should, therefore, aim to promote greater density only in areas where flood risk (and other hazards) is low, with a long-term vision considering climate change. This also aligns with the urgent need for an adaptive flood risk management approach that shifts away from the conventional methods, such as building higher levees and increasing drainage capacity, toward preventing developments in flood-prone areas and creating more room for water.

Furthermore, we find that nature-based interventions, such as the incorporation of pervious surfaces or green spaces, can significantly reduce the extent of flood damage during extreme weather events. Wetlands also demonstrate a capacity to mitigate the impact of such events up to their functional thresholds. Our findings empirically validate the effectiveness of nature-based solutions in mitigating the impacts of flooding, but there is a caveat. Pervious surfaces cannot prevent extreme events from occurring or handle excessive amounts of water in a short period during extreme events. Similarly, wetlands can potentially reduce the likelihood of extreme flooding events, but they become ineffective once their functional capacity is reached. Hence, although effective, nature-based solutions may have their limitations. Internationally, attention is shifting toward building “sponger” cities with more pervious surfaces and creating more room for water by preserving or creating wetlands to better manage the rising risk of flooding. However, we need to be cautious because nature-based solutions are not a panacea, and they are most effective when used in combination with other flood mitigation measures. In conclusion, the reality of increasing flooding frequency and intensity demands a multifaceted response to make cities more resilient. This includes promoting urban density in safe areas, mitigating physical compactness, adopting nature-based solutions, and discouraging or even preventing developments in flood-prone areas, including those considered to be relatively safe behind levees.

This study is subject to several limitations. First, due to data constraints, we use a cross-sectional research design, which does not account for potential changes in the built environment during the study period. Future research could adopt longitudinal approaches, such as panel models, to better capture temporal changes in the built environment. Second, the insurance claim data in this study is susceptible to potential biases, as insurance coverage may only apply to a subset of the total population within the census tract. Thus, the insurance claims might not fully depict the total damage within the referenced census tract. Third, we focus on examining the role of built environment features at the census tract level on flood damage. Future studies could include additional control variables, such as drainage system characteristics and flood risk mitigation measures at the census tract level, if available, to further isolate the effects of the built environment. Fourth, we only focus on one coastal city in the United States for analysis. Future studies could conduct comparative assessments of different cities, offering insights into the relative effectiveness of urban built environment measures in mitigating flood damage across various locations. Finally, this study only differentiates between moderate and extreme flood events. Future study could explore the heterogeneous effects of built environment on different types of flood events (e.g., coastal storms, king tides, and pluvial stormwater flood events) to better reveal the mechanisms through which the built environment influences flooding damage.

Footnotes

Appendix

Flood Insurance Claims During Extreme Flood Events and Other Moderate Flood Events.

| Claim duration | Event type | Event name | Record | Total number of claims | |

|---|---|---|---|---|---|

|

|

2011/10/28–2011/11/1 | Thunderstorm, tornado, and flood events | Rainfall at Miami Beach | Heavy rain/flood event October 28–31, 2011 | 1,053 |

| 2012/8/24–2012/9/1 | Tropical cyclones | Hurricane Isaac | 2012 Tropical Storm Isaac | 991 | |

| 2012/10/25–2012/10/30 | Tropical cyclones | Hurricane Sandy | 2012 Hurricane Sandy | 167 | |

| 2013/6/6–2013/6/8 | Tropical cyclones | Tropical Storm Andrea | 2013 Tropical Storm Andrea | 399 | |

| 2014/1/9–2014/1/10 | Thunderstorm, tornado, and flood events | Palm Beach Flood Event | Palm Beach Flood Event-January 9–10, 2014 | 277 | |

| 2017/9/6–2017/9/18 | Tropical cyclones | Hurricane Irma | 2017 Hurricane Irma | 6,052 | |

| 2019/12/20–2019/12/24 | Thunderstorm, tornado, and flood events | South Florida Flooding | 2019 December 23rd Flooding | 642 | |

|

|

4,125 |

Acknowledgements

We would like to thank the editor and the two anonymous reviewers for their insightful comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the National Natural Science Foundation of China (Grant No. 52378079), the Guangdong Basic and Applied Basic Research Foundation (Grant No. 2024A1515011609), and the Ministry of Business, Innovation, and Employment (MBIE) Endeavour Fund (Grant No. C01X2014). Any errors are solely the responsibility of the authors.