Abstract

Despite the increasing attention to transparency among academics and practitioners, researchers face a significant challenge in gaining access to foundation information, which limits their ability to study foundation transparency. This research aims to advance our understanding of foundation transparency by exploring various dimensions of transparency, including public visibility, information disclosure, external relational activities, reporting quality, and the timeliness of information. The study uses IRS Form 990-PF e-file datasets from 2011 to 2016, as well as information collected from foundation websites. Foundations with websites were coded using content analysis, and a transparency index was constructed through principal factor analysis. The findings indicate that only around one percent of foundations maintain a website, and publicly available information is skewed towards administrative information with a lack of financial information and information on external relations-building activities. Additionally, the average time taken to file after the tax deadline was approximately four months, and tax filings were found to have reporting quality issues.

Keywords

In the world of foundations, actions taken to increase transparency are a hedge against accusations of unaccountability (Frumkin, 2006a). While not a cure-all, transparency is viewed by practitioners and scholars as a tool that enhances accountability by encouraging foundations to be honest, accessible, and timely about how they do their work (GrantCraft, 2014).

To discuss foundation accountability and transparency, it is important to distinguish the different types of foundations, as different types of foundations require different accountability systems. Foundations are broadly categorized as either private foundations or community foundations based on differences in the origin of their financial support. Community foundations, designated as “public charities” under United States law, receive funding from the public and are thus structured for accountability to the public (Boris, 2001; Hall, 2016). In contrast, a private foundation is regulated by the “private foundation” rules of the U.S. tax code (Boris, 2001) because it receives funding from an individual or group of individuals, a family, or a corporation whom wield exclusive control over grantmaking decisions (Boris, 2001; Cordes & Sansing, 2007). The centralized nature of private foundations lends itself to less transparency and less public accountability, hence this study’s particular interest in them.

The lack of transparency and accountability among foundations manifests in several ways. First, researchers have faced difficulties in gaining access to information on foundations (Diaz, 1999; Lagemann, 1999). Second, in theory foundation boards and trustees should represent the public, but in practice they are known to be self-perpetuating and to be unaccountable to any external constituency (Fleishman, 2007). Public charities are accountable to users and donors and so embrace transparency to better solicit materials and write grants (Rhode & Packel, 2009; Sandy, 2007). However, private foundations were purposely designed to have less structured accountability systems “to create insulation, flexibility, and bold deployment of tax-sheltered resources to advance the public good” (Sandy, 2007, p. 1504).

In recent times, foundations have faced external pressure to be more transparent, as embodied by the public demands made in the Tax Reform Act of 1969 (Frumkin, 2006b). Transparency serves as a tool to prevent the loss of public confidence in charitable nonprofits from mismanagement, corruption, or scandal (Behn et al., 2010; Rhode & Packel, 2009; Sandy, 2007). The transparency movement thus pushes foundations to set up web pages, publish annual reports, and publicize grantmaking guidelines, including their preferred methods to solve problems (Frumkin, 2006b). However, despite such movement, foundation transparency is mostly voluntary in the United States, except for the requirement to file a return with the Internal Revenue Service (IRS).

This research advances understanding of transparency and accountability in public administration on numerous fronts. For one, this study develops several variables measuring different dimensions of foundation transparency, observing downward accountability from funders to grantees, clients, or the public, which has been understudied compared to upward accountability (Ebrahim, 2016). Transparency has been seen as the core of accountability relationships (Ahmad, 2008; Koppell, 2010), notably increases public trust in foundations (Fleishman, 2007) and enhances relationships with grantees (Bolduc et al., 2007). However, foundation transparency remains mostly voluntary, and strict limitations on access to their information has been a hurdle for transparency research. Thus, there has been growing interest in transparency among academics and practitioners in response to increasing demands for accountability. To date, researchers have focused on public charities rather than foundations. By addressing the lack of attention paid to private foundations, this study offers empirical research about what information is available about foundations’ work incorporating multiple dimensions of transparency. As such, this research explores the following question: to what extent are grantmaking foundations transparent? After a brief review of the literature on the importance of foundation transparency and on transparency in the public and private sectors, this study then describes its research design. This study then concludes with a discussion of the implications of its findings.

Why Foundation Transparency Matters

Some argue that the provision of resources by foundations plays an essential role in a pluralistic, civil society (Sievers, 2010b), while others consider whether foundations might harm the civil society because they influence policymaking and hold agenda setting powers while being undemocratic and elitist (Anheier, 2014; Anheier & Leat, 2013; Rogers, 2011; Sievers, 2010a; Zunz, 2012) Due to their wealth, foundations become oversized players in the social policy arena, influencing the provision of public goods and the direction of public policy. While nonprofit organizations and foundations are technically private organizations, they are enabled, supported, and incentivized by public policy. As such, they are embedded in a democratic process.

Understanding the concept of transparency is useful to comprehending the role of foundations in a democratic society, as it has long been a goal of governments in such societies to be responsive and democratically accountable to their publics (Adams, 1856; Lathrop & Ruma, 2010; Radin, 2006; Weiss, 2002). The definition of foundation transparency proposed by GrantCraft (2014, p. 3) is that transparency “shares what it does, how it does, and the difference that it makes in a frank, easily accessible, and timely way” as a means to “greater accountability, and to building relationships between a foundation and other key groups such as grantees, applicants, partners, and other funders.” Transparency matters for foundations for the following reasons.

First, philanthropic giving for the public benefit has an unavoidable effect on people, communities, and neighborhoods (Fernandez & Hager, 2014; Frumkin, 2006a). These effects can be direct or indirect. For example, research on policy feedback indicates that human services supported by not only government, but foundations and public charities carry direct effects for policy beneficiaries and may have indirect effects on citizen advocacy behavior or political activity (Mettler, 2002). For example, Bushouse (2009) found foundation funders played an important role in determining whether some state governments created publicly funded universal preschool programs. Philanthropic funding increased the capacity of advocates to maintain pressure for passing or funding universal preschool legislation by supporting issue campaigns, holding meetings or conferences, developing e-advocacy tools, and creating preschool investment materials or reports. As such, when foundations shape policy, foundations have responsibility for their influence on policies and for incorporating stakeholders, grantees, and other public stakeholders who are directly influenced by the policy changes into their decision making (Kraeger & Robichau, 2017).

Second, giving to foundations and foundation’s investment income are accompanied by tax breaks (Frumkin, 2006a; Sansing & Yetman, 2006). An individual’s giving to a foundation is tax deductible on personal income taxes, and a bequest to a foundation lowers estate taxes if the gift is made upon death. Foundations themselves receive tax exemptions on their investment income. Fleishman (2007) estimated in 2005 about $10 billion would be the U.S. treasury tax revenue without these income and estate tax exemptions, which has grown since then. Mcllnay (1998, p. 101) states “the privacy of foundations is a privilege awarded to them because of their contributions to society, not an excuse to ignore the responsibilities of citizenship in a democracy.” This public subsidization of foundations should involve some responsibility related to their giving decisions (Anheier & Leat, 2013).

Third, the size and impact of the foundation sector has grown enormously, and the aforementioned foundation responsibilities become crucial. In 2010, foundation giving to charitable organizations was $41 billion (Giving USA, 2011). In 2018, that number increased to $66.9 billion (Giving USA, 2018). Along with increased giving, the role of foundation grants in the nonprofit sector has increased. After adjusting for inflation, between 2005 and 2015, foundation giving increased 42.1% (McKeever, 2018). The contribution of $66.90 billion in 2017 makes up 16% of total charitable giving by individuals, foundations, bequest, and corporations ($410.02 billion). Foundations also receive contributions. Gifts to foundations account for 11% of total charitable contributions, the fourth largest recipient in 2017, followed by organizations of the religion, education, and human services (McKeever, 2018). This increasing impact of foundations is also aligned with the growing number of foundations from 71,097 in 2005 to 86,203 in 2015, an increase of 21% (Foundation Center, 2014).

Furthermore, the absence of transparency is a critical societal problem as it can lead to negative consequences such as abuse, scandals, and loss of public confidence (Behn et al., 2010; Rhode & Packel, 2009; Sandy, 2007). Such issues can have a significant impact on the effectiveness and sustainability of foundations. Transparency has been considered to be society’s effective way to prevent unethical behavior (Jennings et al., 2015; Morrison & Mujtaba, 2010; Rhode & Packel, 2009). As a recent example of foundation scandal, Trump Foundation was dissolved in 2016 partially because of “self-dealing,” namely spending money for Trump’s personal benefit as opposed to disbursing for charitable purposes (Jacobs, 2016). As this example illustrates, foundations are required to pay particular attention to transparency and research on this topic is vital.

Dimensions of Foundation Transparency

Considering that private foundations have been characterized as both private and public (Hager & Boris, 2012), it is important to examine multiple dimensions of transparency by reviewing studies of transparency in both the public and private sectors. While there is legal support at the federal level for actions to increase the transparency of government (e.g., Administrative Procedures Act (APA) of 1946), and corporations (e.g., Sarbanes-Oxley Act (SOX) of 2002), there are no such federal laws that apply to the nonprofit sector (Guy & Ely, 2018). Although the influence of the SOX on nonprofit management has resulted in nonprofits adhering to the SOX’s provisions voluntarily, or in certain states by law (Heckler, 2019), this is not legally required at the federal level.

In the nonprofit sector, inculcating transparency by engendering a “Watchful Eye,” that is, creating public access to information or decision making, (Light, 2011, p. 55) is supported by formal and informal actors. The oversight of these actors provides data (e.g., GuideStar and the National Center for Charitable Statistics), monitoring (state attorneys general and the Internal Revenue Service (IRS)), or the evaluation of performance (charity watchdogs; Guy & Ely, 2018).

Suggested nonprofit transparency practices parallel forms of government and corporate transparency. One of the most common transparency practices in the public, private, and nonprofit sectors is administrative transparency (Bushman et al., 2004, Guidestar, 2008; Porumbescu & Grimmelikhuijsen, 2017). In the nonprofit sector, this refers to transparency regarding information about an institution’s board, staff, programs, evaluations, and IRS letter of determination. Another frequently studied dimension is budget transparency, which takes the form of audited financial statements (Bushman et al., 2004, Guidestar, 2008; Porumbescu & Grimmelikhuijsen, 2017). Activities provided in such audits include financial statements pertaining to revenue sources and expenditures, programs and operations, missions, and goals (Guidestar, 2008). While there is empirically little known about the administrative and financial transparency of foundations, Frumkin (2006b) describes foundations releasing information regarding grantmaking guidelines, funding priorities, and assumptions and approaches to particular issues that possibly include relevant administrative and budgetary information.

In addition to administrative and budget transparency, other dimensions that often appear are timeliness and quality. In the public sector, research has examined the timeliness and quality of government data (Caudle, 2010; Islam, 2006). In the private sector, studies examine the quality of audit information (Bushman & Smith, 2003) and timelines of financial reporting (Bushman & Smith, 2003; Kelton & Yang, 2008). In the charitable sector, the timely availability of organizational information regarding operations and financial situations is of interest (Behn et al., 2007; Guy & Ely, 2018; Light, 2011).

Furthermore, studies also examine relational dimension of transparency. The relational dimension illustrates the flow of information that is regarded as an important dimension of transparency in government (Porumbescu & Grimmelikhuijsen, 2017) and nonprofits (Gray et al., 2006). The relationship dimension suggests outward transparency that an organization views or receives information from external stakeholders, which has been neglected compared to inward transparency (Porumbescu & Grimmelikhuijsen, 2017).

However, while transparency as enhancing a relationship with grantees and other stakeholders is imperative for improving giving effectiveness, and thus accountability (Bolduc et al., 2004), inward and outward transparency in foundations seems to be not fully achieved. According to a survey of foundation evaluation practices by Buteau et al. (2016), performance information flows outward at a low rate. Among the foundations that create evaluation findings, 28% report sharing information with grantees, 17% with other foundations, and only 14% with the general public. Foundations mostly share their performance information with insiders, but the rate differs depending on the information recipients. About 77% of evaluation or program staff report that performance information is shared with the foundation’s CEO, but the information sharing percent decreases to 66% with foundation staff and 47% with the foundation’s board. While inward and outward transparency is less common among foundations, it is still important to consider relational dimensions of transparency like these to comprehensively understand foundation transparency.

Why Online Transparency

Information disclosure by foundations is the most commonly implemented transparency practice. Examples include information disclosed via web pages, annual reports (Frumkin, 2006b) and, more recently, social media (Maxwell & Carboni, 2016; Wu, 2022). Thus, this research considers online transparency to be a primary form of transparency in addition to the mandated disclosure of tax filings. With the development of Internet-based technologies, citizens have gained unprecedented access to the information they need. In turn, foundations began to use internet-based technologies to disclose financial and operational information (Saxton & Guo, 2011). A number of studies examine how the web practices in the public and private sectors facilitate increased transparency (Campbell & Lambright, 2019; Lowatcharin & Menifield, 2015; Saxton & Guo, 2011; Waters, 2007). A few studies investigate the use of social media by foundations (Maxwell & Carboni, 2016; Wu, 2023). However, there is still little known about how foundations use the web to practice transparency. Foundation Directory Online, on its own webpage, says that only 10% of U.S. foundations have websites. While this statistic is not empirically tested, the low online visibility of foundations implies the challenge of studying how the web is used to facilitate foundation transparency. Despite the lack of online presence, it is vital to explore and understand what information is available online about foundations and their grantmaking, given foundations are, at best, only publicly visible through their websites and regulatory filings to the Internal Revenue Service via Form 990-PF.

Research Design

Given the lack of empirical studies on private foundation transparency, this research uses foundation websites and compulsory tax filings, two key settings, to investigate the multiple dimensions of foundation transparency.

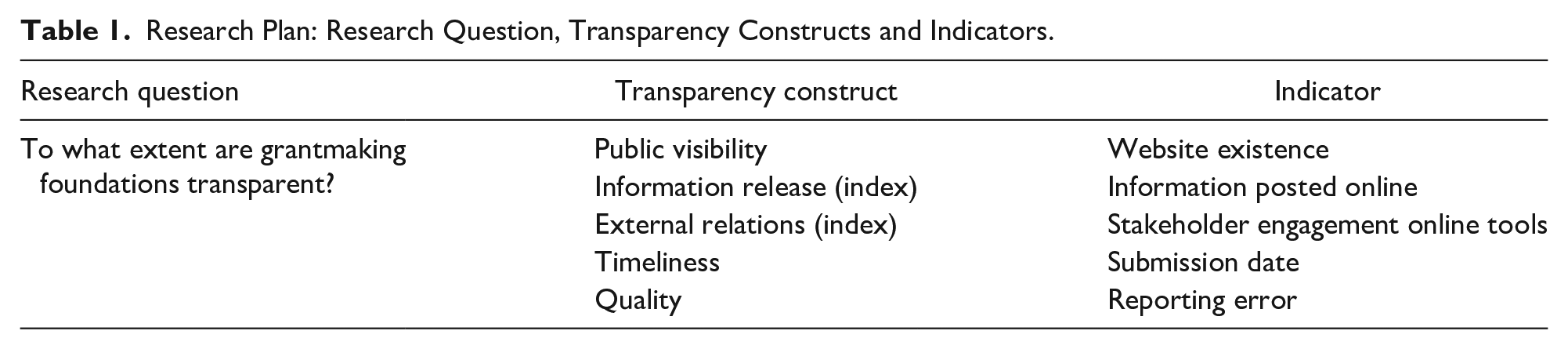

This investigation has three main goals. The first goal is to understand efforts by foundations to be transparent. The second goal is to develop a transparency index to measure information release and external relations-building activities using data on administrative transparency, financial transparency, and external relations-building activities. The third goal is to better understand the transparency of foundation tax filings by examining the quality of reporting and the timeliness of information release. Table 1 summarizes the research design, including a research question, constructs, and indicators.

Research Plan: Research Question, Transparency Constructs and Indicators.

Data and Sample

There are two sets of data used in this study. The first dataset comes from a random sample of foundations drawn from a list of all private non-operating grantmaking foundations that submitted a Form 990-PF electronically in 2015 (N = 41,203) and the second data set comes from a list of all private grantmaking foundations that electronically submitted an IRS Form 990-PF from 2011 to 2016 (N = 208,081). These datasets are available via Amazon Simple Storage Service (Amazon S3) in an XML file. Submissions from the year 2015 for the first data set are used because the corresponding data for them are complete and the most recent population data available from Candid on private foundations are from 2015. The population of foundations in 2015 was 81,957 grantmaking-non-operating foundations. The sampling frame is the list of electronically submitted 990-PF files submitted by foundations in 2015, from which the sample of 1,099 foundations is randomly drawn. The sample size is 1,099, determined by using the sample size table provided by Israel (1992). The sample size is at the 95% confidence level with a 3% margin of error.

Using this sample, transparency data on public visibility, information release and external relations are collected from a foundation’s website. This research first gathered a website link from GuideStar, and then performed further search via google if the link did not work. This sampling frame encompasses the entire population of e-filing foundations in 2015.To check the robustness of using links provided by GuideStar, I randomly sampled 50% (550 foundations) of the sample of 1,099 to compare the web presence found in GuideStar to the counterpart via Google search. Only 3.8%, or 21 foundations, out of 550 had a website although their website was not provided by GuideStar.

Transparency Measures

Based on transparency studies in the public, private, and charitable sectors, five dimensions of transparency are chosen for study in this research: (1) public visibility, (2) information release, (3) external relations, (4) reporting quality, and (5) timeliness. Based on these dimensions, I construct three transparency dependent variables: (1) public visibility, (2) online transparency index (information release and external relations), and (3) tax filings transparency (reporting quality and timeliness).

Public Visibility

Public visibility is used as a proxy of online transparency to understand voluntary efforts by foundations to be transparent. It is operationalized as whether a foundation has a website. Foundations in the sample were coded as 1 if they had a website using GuideStar information and Google search between October 2019 and November 2019 and 0 if they did not.

Online Transparency Index

I developed a private grantmaking foundation online transparency index by combining existing academic research with work by practitioners. I selected GlassPockets, an example of work by practitioners, because of its high relevance to this study’s research, as the goal of GlassPockets is to support foundation transparency in an online world. Saxton and Guo (2011) developed comprehensive foundation transparency indicators that incorporated dimensions discussed in the literature section (administrative, budgetary, and relational transparency). Their indicators were tailored to community foundations, but their work is also applicable to private foundations given their similar organizational purpose. Also, comparing this study’s results to transparency data for community foundations serves to highlight the differences between community foundations and private foundations, which enriches the understanding of nonprofit transparency.

In this index development, two different dimensions of transparency are used: information release and external relations. The process utilized is described below. First, I identified all the dimensions and indicators of private foundation transparency established in GlassPockets (2019) and Saxton and Guo (2011) as well as one additional item, goal, or strategy because it is a commonly used transparency indicator in both the nonprofit and government sectors (Dumont, 2013). 1

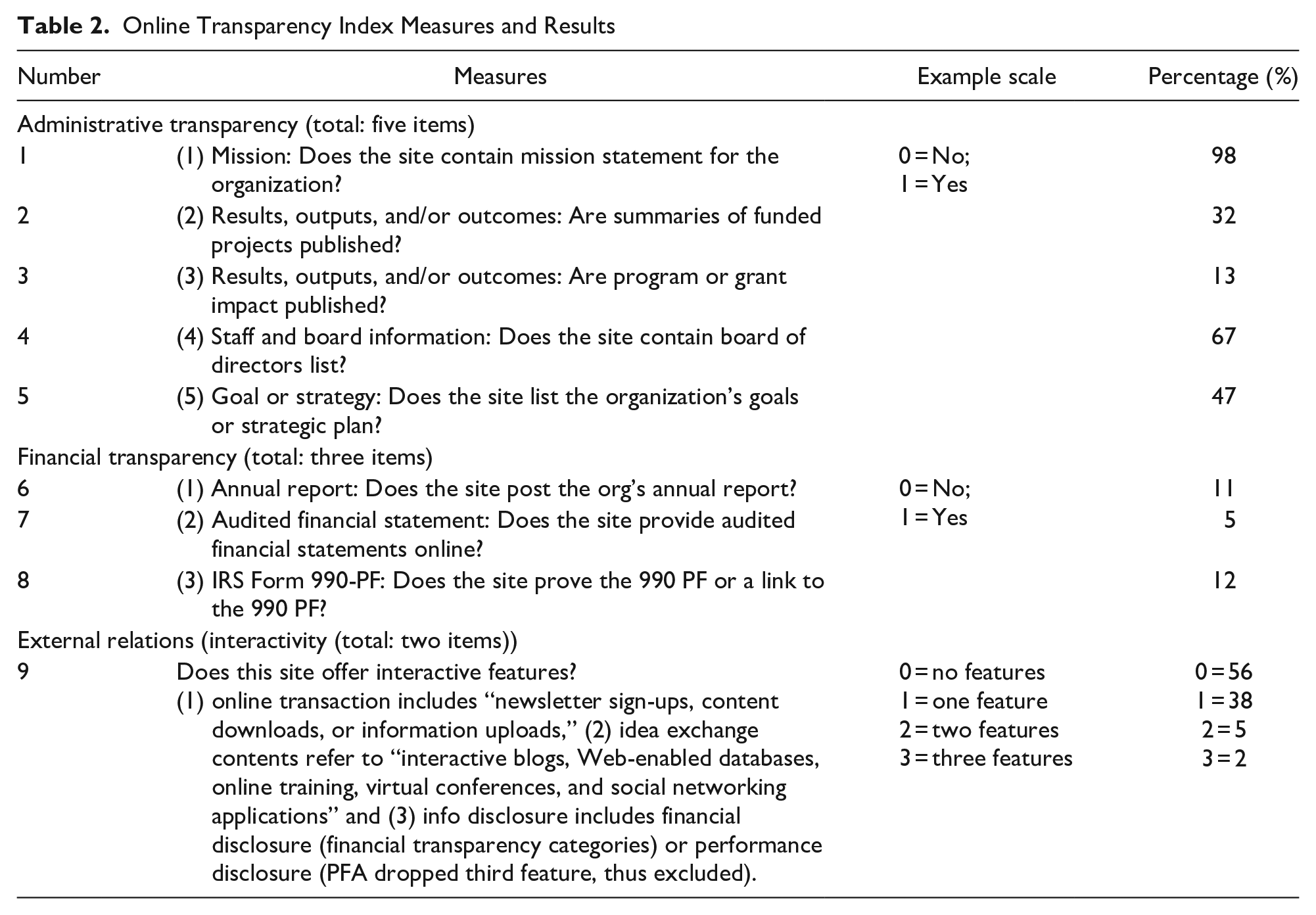

Second, I selected a sample of foundations that have websites. Third, I coded the websites of the sampled foundations based on the found items. I excluded three staff-related questions (staff list and biography and whistleblower policy) in the index after reviewing foundations’ spending on salaries and wages for employees. This revealed that most of foundations do not need such information as they do not have staff. Also, I excluded seven items including information on sustainable development goals, committee charters, open licensing policies, transparency values or policies, executive compensation process, diversity data, and online stakeholder survey because none of the coded websites had these features, resulting in a lack of variation in the corresponding data. I included the remaining 14 items in the PFA test. Fourth, I constructed the index using an internal consistency test (Cronbach’s alpha) and principal factor analyses (PFA) to ensure that its component measures are grouped coherently under the outlined theoretical concepts. Last, I finalized the indicators to be included in the online transparency index in Table 2.

Online Transparency Index Measures and Results

Administrative Transparency Index (ATI)

Information release, as a dimension of transparency, involves examining whether foundations make certain content available on their website that can be categorized as a form of either administrative or financial transparency.

To develop the administrative transparency index (ATI), I tested the internal consistency of all measures of administrative transparency described as third process in the above coding process. Principal factor analysis (PFA) implied the existence of three factors: one with an eigenvalue of 2.10 on which 5 out of 14 items loaded at 1.0 or greater, another with an eigenvalue of 1.92 on which 3 out of the 14 items loaded at 0.62 or greater, and the other with an eigenvalue of 1.80 on which 2 out of the 14 items loaded at 0.43 or greater. I retained the strongest factor out of these three factors, thereby excluding the nine poorly loading measures. The measures included appear in Table 2. A Cronbach’s alpha coefficient of .70 indicates a high level of internal consistency.

ATI for a given foundation is the sum total value of the dummy variables corresponding to the five measures that were included. If a feature exists on a foundation’s web site, it is coded as 1 and 0 otherwise.

Financial Transparency Index (FTI)

Financial transparency is operationalized as the availability of a foundation’s financial information, including (1) annual reports, (2) audited financial statements, and (3) IRS Form 990-PF’s. While Saxton and Guo (2011) used other measures such as privacy policy, investment pool performance, investment policy and/or strategy, and the cost of administrating funds, these are not used in this study because they are less relevant to private foundations from a public accountability standpoint. Such investment-related measures are more important aspects of transparency for community foundations because their spending is funded by contributions received from the public. In contrast, spending by private foundations is funded from their privately-held endowments, making financial information release to donors relatively less important.

After I coded the websites, I tested the internal consistency of these measures. A PFA suggested a single factor exists with an eigen value of 1.0 on which three items loaded at 0.45 or greater. Despite a low coefficient of Cronbach’s alpha (.53), I decided on theoretical grounds to include the index in the analysis. Thus, I define the financial transparency index (FTI) for a given private foundation as the sum total of the dummy variables testing for these three features in Table 2. If a foundation’s web site has a given feature then the corresponding dummy variable is coded as 1 and 0 otherwise.

External Relations

As per Saxton and Guo (2011), external relations have two dimensions: stakeholder input solicitation and interactivity with stakeholders. Stakeholder input solicitation captures how private foundations use Web-based tools to solicit feedback from their stakeholders, engage them in communications, or assess their needs. Solicitation is operationalized as whether the following contents can be found on a given foundation’s website: (1) “contact us,” “feedback,” or “ask a question” features, (2) grant recipient evaluation forms, (3) a guestbook, (4) an online stakeholder survey, (5) a message forum, (6) online needs assessment, and (7) links to external sites. Online stakeholder survey (4) was dropped due to a lack of variation (0%).

As with administrative and financial transparency, I tested the internal consistency of my external relations measures after I coded the sampled websites. The stakeholder solicitation index returned an unacceptable Cronbach’s alpha of .04. The confirmatory factor analysis (CFA) also showed a single factor with a low eigenvalue (.66). This result is similar to what Saxton and Guo (2011) found in in their work. They assumed that this might be caused by the skewed distribution of the data. While most foundation websites contain a contact-us link (92%) and external links (53%), the number of foundations that have only one of the other four features is extremely small. As a result, there is insufficient variability for multivariate analysis of this variable.

The purpose behind the interactivity measure is to help comprehend how private foundations employ website tools to be more responsive to the needs and demands of stakeholders by focusing on three dimensions of information, transaction, and interaction. As such, the interactivity measure contains the following three components: (1) information disclosure (either financial disclosure, e.g., financial transparency categories, or performance disclosure), (2) online transactions (“newsletter sign-ups, content downloads, or information uploads”), and (3) idea exchange content as interaction (“interactive blogs, Web-enabled databases, online training, virtual conferences, and social networking applications”; Saxton & Guo, p. 282).

I tested the internal consistency of the three measures of interactivity. A PFA suggested two factors exist. The first factor exists among online transactions and idea exchange content components with an eigen value of 0.23 on which two times loaded at 0.34, while the second factor exists in the information disclosure component with an eigen value of 0.04 on which one item loaded at 0.2. This result leads to the decision of including only two components loaded at the first factor in the interactivity index: (1) online transactions and (2) idea exchange content. These two components have a low coefficient of Cronbach’s alpha (.31), but I decided on theoretical grounds to include the index in the analysis.

Composite Online Transparency Index

This index is the summation of a given foundation’s ATI, BTI, and Interactivity measure values. The highest possible value is 10. A Cronbach’s alpha of .73 indicates a high level of internal consistency. A PFA returned a single factor (eigenvalue = 2.30) on which all items load at 0.3 or better.

Tax Filings Transparency

This variable operationalizes transparency in terms of reporting quality and the timeliness of information release by examining Form 990-PF filings. Data are gathered by observing all grantmaking foundations from 2011 to 2016 that electronically submitted an IRS Form 990-PF (N = 208,081). For the reporting quality variable, an inductive approach is used with the panel data to identify measures of reporting quality such as the amount of missing data or the number of “none” entries reported as a grant recipient’s name, address, type of organization, or purpose of grant. For timeliness of information release, I use the IRS’s due date rule that Form 990-PF is due by the 15th day of the fifth month after the end of the tax deadline. While this due date rule is not mandatory (e.g., foundations can request a 6-month extension using Form 8868), from a transparency perspective it is critical to understand how long it takes for public reporting to be made publicly available.

Data Analysis

This study explores diverse aspects of transparency to answer the research question, "To what extent are grantmaking foundations transparent?" In this analysis, descriptive statistics are used to show the extent of transparency by illustrating different dimensions of public visibility, specifically information release, external relations, timeliness, and reporting quality.

How Transparent?

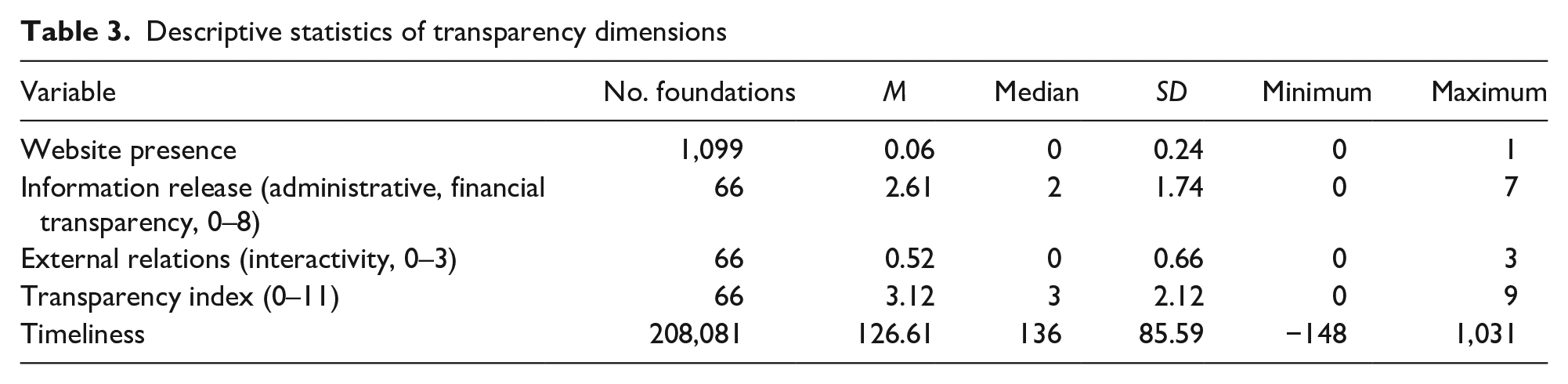

This section examines website presence, information release, external relations, timeliness, and reporting quality. As shown in the descriptive statistics in Table 3, only a small portion of foundations have a website. Out of the 1,099 randomly-sampled foundations, only 86 have a website link as of Fall 2019. Of those, only 66 are operational as of February and March 2020. These 66 foundations comprise about 1% of the sample.

Descriptive statistics of transparency dimensions

The 66 foundations with websites have information release values ranging from 0 to 7 out of a possible maximum of 8, with an average value of 3. The information release index has eight measures capturing different dimensions of administrative and financial transparency. Out of the eight items mission appears most frequently (34%), followed by list of board members (23%), goals or strategy (16%), summaries of grant project (11%), grant impacts (5%), Form 990-PF (5%), annual report (4%), and audited financial statement (2%). The information release components are mostly derived from administrative information (90%) rather than budgetary (10%). The transparency index has an average and median value of 3, meaning foundations on average and at the median have 3 of the index features out of 10 appearing on their website.

According to comparable findings from Saxton and Guo (2011), specifically those on annual reports and audited financial statements for private foundations (11% and 5%, respectively) is lower than for community foundations (62% and 44%, respectively). Among administrative measures there is relatively more information available on mission for private foundations (89%) than for community foundations (80%), while there is relatively less information available on grant project summaries for private foundations (29%) than for community foundations (35%).

Foundation transparency in terms of external relations has an average value of around 0.5, with the highest value in the descriptive statistics being 3. This number indicates that among the three types of interactivity, more than half of foundations have less than one. Among foundations that have at least one of the three types of interactivity, idea exchange is the most common (25%), followed by budgetary and performance information (11%) and online transaction (11%). Among the examples of the idea exchange type of interactivity that appear on foundation websites, social networking applications or social media buttons on a website appear the most often, with one foundation having a virtual conference.

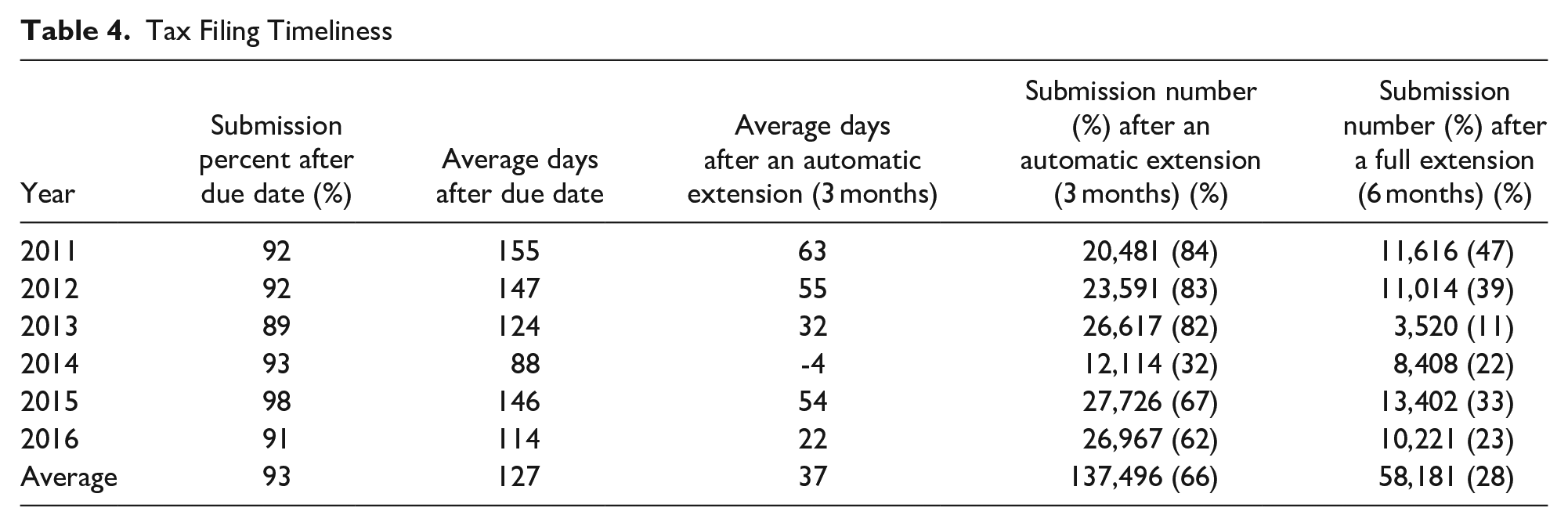

The timeliness dimension of transparency shows that the average number of days taken to file after the tax deadline during the period from 2011 to 2016 was 127 days with a median value of 136 days (Table 4). On average, from 2011 to 2016, 93% of foundations submitted their Form 990-PF after the tax filing due date. The highest portion of foundations that submitted their Form 990-PF after the IRS due date was in 2015, while the lowest portion of foundations that submitted their Form 990-PF after the IRS due date was in 2013.

Tax Filing Timeliness

Considering foundations receive an automatic extension for 3 months or approximately 92 days, the average days that foundations take to submit Form 990-PF after the automatic extension are about 37 days. About 66% of foundations submit Form 990-PF after an automatic extension on average. Foundations can further request the additional 3 months after the automatic extension. Taking the full extension of 6 months into account for the timeliness measure, on average 28% of foundations submit Form 990-PF after the full extension of 6 months.

As for reporting quality, the following data errors were found among the 2011 to 2016 Form 990-PF filing data. The first and largest issue regards contact information. A total of 12,900 foundations (about 1%) out of 208,081 do not provide their phone numbers. The second type of error regards submissions. A total of 615 foundations reported that their grant activity was greater than zero but did not provide supplementary information, such as a list of grant awardees, award amounts, or grant purpose. The third issue regards the quality of grantee information. A total of 565 foundations did not provide grantee names.

Limitations

The sample size for the index development is limited by using website links provided by GuideStar, as Google search found 3.8% of the foundation sample of 1,099 do not have website listed with GuideStar. This portion is quite small, but the index findings already suffer from limited generalizability to the foundation sector since they only represent foundations with websites listed on GuideStar. Thus, future studies can increase generalizability by using a broader range of search engines to collect foundation websites. Also, the consideration of foundation size in sampling is critical, as this study finds that it is even more unlikely for small foundations to maintain a website than foundations in the Foundation Directory Online database, of which only 10% had websites. Thus, a stratified sampling technique would provide more context about a more diverse range of foundations. However, the benefit of this study’s approach is that its sample is more representative of the entire foundation sector, encompassing the sector’s large number of small foundations rather than just of a selected portion of the sector limited to its larger foundations.

Additionally, while this study considers web pages to constitute online visibility, there are other ways for foundations to increase their online presence such as via social media (Campbell & Lambright, 2019; Maxwell & Carboni, 2016). While this study attempts to captures foundation social media presence by counting links on foundation websites to their corresponding social media accounts, a more in-depth analysis of foundation social media would enhance the understanding of foundation transparency practices.

Lastly, the index sample was drawn from 2015 tax fillings, but the website data were collected in 2019 and 2020. Wayback Machine offers archives of past versions of given websites taken from multiple specific points in time. However, as Wayaback Machine shows the captures in points in time, not all information included on the website now was available in its previous iterations. While there is a time gap between the sample and the data collection, it was critical to the development of the index to code all available information on websites. Thus, using websites from 2019 and 2020 was preferred to using those from 2015.

Implications and Conclusions

This research explores the extent to which private grantmaking foundations are transparent by analyzing website presence, an online transparency index, and tax filings. This study produces several meaningful practical and theoretical implications.

First, it contributes to the public accountability literature by exploring diverse dimensions of transparency. This study utilizes existing work that highlights the web-enabled transparency practices of nonprofits (Dumont, 2013; Saxton & Guo, 2011; Tremblay-Boire & Prakash, 2014) and the transparency indicators used by established practitioners such as Candid’s GlassPockets and GuideStar. In addition to this, this study also explores private foundation-oriented transparency by measuring foundation public visibility online, creating a comprehensive transparency index, and demonstrating tax filling timeliness and reporting quality. The online transparency index used in this study captures key dimensions of foundation transparency. Both scholars and practitioners can use these measures in future research. These conceptual groundings offer a better understanding of foundation accountability to external stakeholders, such as grant applicants, grantees, or the public.

Second, this research shows how private foundations can optimize their transparency efforts to build accountability. Findings illustrate the lack of transparency among foundations. The national sample reveals that about 1% of private foundations maintain a website, which is far less than the 67% of public charities with a website (Dumont, 2013). Although they did not empirically establish the percentage of community foundations with a website, every single community foundation in Saxton and Guo’s (2011) sample of 117 community foundations had a website. The lower incidence of websites among private foundations relative to community foundations may be related to lack of administrative capacity. While community foundations had average assets of $87 billion in 2018 (Candid, 2022), the average assets of private grantmaking foundations in 2018 was $13 million (Ely et al., 2021). The dataset in this study shows that foundations with a website tend to be much larger, with a mean of $71 million in assets, compared to foundations without a website that have a mean of $12 million. Foundations with a website have a median of $2 million, compared to those without a website with a median of $800,000. Thus, capacity factors in future transparency studies need attention to offer further insights. The transparency index suggests that publicly available foundation information is disproportionately administrative information, with a relative lack of financial information and external relationship-building activities. The lack of financial transparency among private foundations shows how they differ from community foundations, which promote more financial information on their websites (Saxton & Guo 2011). This might be due to private grantmaking foundations being less incentivized to post financial information because, as opposed to community foundations or public charities as a whole, they do not typically solicit new donors. Saxton and Guo (2011) also find a lack of transparency about external relations-building activities among community foundations.

The frequency of external relations-building activities conducted by private foundations and community foundations appears similar. To summarize online features comparable between private and community foundations, private foundations in this research have a higher proportion of the contact-us feature (92% vs.78%), grant recipient evaluation forms (9% vs. 3%), and needs assessment (2% vs. 1%), while having a smaller proportion of online stakeholder survey (0% vs. 2%). Guest book and message forum features are found among 2% of those private and community foundations with websites. Saxton and Guo’s findings on external relational activities (or stakeholder input solicitation as they call it) are generalizable to private foundations.

About 93% of foundations submit their Form 990-PF after the IRS-regulated due date, which indicates that tax filings are available an average of four months after the due date. Among foundations for which tax filings are available some do not report contact and grantee information, although these are small proportion of the sample (1%).

Third, this research incorporates foundations without websites into empirical work for understanding organizational differences in accountability that is normally reserved for foundations with websites. This attempt is critical to the study of private foundations as they are the much less publicly visible than public charities.

Fourth, while transparency is voluntary for private foundations, transparency studies on public charities suggest that transparency produces positive outcomes including trust of stakeholders, collaboration with stakeholders, innovation (Hale, 2011), donations (Blouin et al., 2018), and accountability (Ebrahim, 2005). For future studies, investigation of outcomes of transparency in the context of private foundations could further the understanding of public accountability.

Additionally, future studies might utilize the dimensions of transparency proposed in this study to explore other types of foundations. For example, operating foundations fund their own programs to achieve mission objectives rather than making grants to other charities. Since their activities are in-house, they might be more incentivized to share what they do and how they do it with their beneficiaries and with the public. Future studies in other types of nonprofits such as community foundations or public charities could offer further insights into nonprofit reporting quality and the timeliness of tax filings in addition to the knowledge developed by existing nonprofit online transparency studies. As such, exploring all these dimensions of transparency can offer a collective understanding of transparency at the sector level and at the organizational level. Those future studies can build on this model by refining the index.

Last, since private foundations are not automatically incentivized to be transparent as they have less societal pressure on transparency, increasing public interests in foundation activities might most efficiently promote transparency. Such action can be taken by formal and informal actors. While those actors already exists, for example, those who provide data (like GuideStar and the National Center for Charitable Statistics), monitor (state attorneys general and the Internal Revenue Service (IRS)), or evaluate their performance (charity watchdogs; Guy & Ely, 2018), most of them focus on public charities. Thus, more actors focusing on private foundations can enhance an understanding of foundation transparency or opacity. Without such efforts, the gap between public expectations and foundation transparency is likely to remain.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.