Abstract

End-of-life (EOL) solar photovoltaic (PV) module waste is a pressing issue, given the expansion of solar PV adoption and the burgeoning number of modules that will enter EOL in the next decade. The drive towards reuse is that it could offer a means to retain the value in PV modules, reduce pollution, bring renewable energy (RE) closer to the average household and offset the costs of recycling. Primary research was undertaken on the perceptions of actors along the South African PV value chain. Interviews were held with key informants in energy and e-waste, and a questionnaire was administered to the solar sector. The findings were interpreted in terms of drivers, barriers and enablers of a PV module circular economy with a specific focus on reuse. The study found that the key enablers were enforcing existing environmental legislation, which includes a mandatory Extended Producer Responsibility (EPR) system, employing EPR fees towards waste system interventions and establishing quality assurance of second-hand products through testing and standards. Barriers to reuse were identified as being complex trade-offs between reuse, recycling and design, as well as the need for international standards and ensuring the market demand and viability of second-life modules. Research on higher-order circular economy activities, such as reuse and repair, has been limited in developing countries, including South Africa. The study adds to the body of knowledge in providing a potential framework for the development of a circular economy for PV modules in South Africa and offers broad policy recommendations for reuse.

Introduction

E-waste is the world’s fastest-growing waste stream (United Nations Environment Programme, 2007), and the waste from solar photovoltaic (PV) energy systems coming to their end-of-life (EOL) is expected to make up a significant proportion of this waste stream (International Renewable Energy Agency (IRENA) and International Energy Agency: Photovoltaic Power Systems Programme (IEA-PVPS), 2016). Unstable electricity supply, above-inflation rise in the cost of electricity, tax incentives and the declining costs of PV modules (GreenCape, 2024a) have incentivised businesses and households across South Africa to adopt solar energy. Expectations for the growth of solar PV in South Africa by 2030 suggest new additions of privately and publicly procured generation capacity of 6 gigawatt (GW) and 2.6 GW, respectively (GreenCape, 2024b). The potential market for rooftop solar, including business, industrial and residential, is estimated at 10 GW by 2030 (GreenCape, 2024c). However, as solar energy adoption grows, so does the need to manage the resulting waste.

Global PV module waste is estimated at a cumulative 60 million tonnes by 2050 on a regular-loss scenario and a higher 78 million tonnes on an early-loss scenario (IRENA and IEA-PVPS, 2016). Total e-waste generated from PV panels is estimated at 0.6 million tonnes in 2022 (Baldé et al., 2024). Based on the average mass of a module being 60 kg kW, for every megawatt (MW) of installed capacity, the resulting EOL waste is estimated to be 60 tonnes (Mukwevho et al., 2025). Production waste is excluded from EOL PV waste models, as it is believed to be well-contained and easier to manage than waste at any other point in a module’s life span (IRENA and IEA-PVPS, 2016).

When electrical and electronic equipment (EEE) is discarded with no intent to reuse, it is referred to as e-waste. PV modules are classified as large equipment within e-waste (Forti et al., 2018) and have a typical life span of 25–30 years (GreenCape, 2024c), with a reduction in solar power output over time. The manufacturer predicted degradation rate of a crystalline silicon PV module’s power output averages 0.5% per annum (p. a.), after an initial 1.5% decrease in the first year (National Renewable Energy Laboratory (NREL), 2018). This rate can vary depending on the module technology. It is expected that a 20-year-old module would still be producing approximately 90% of the energy it produced in year 1 of operation (NREL, 2018).

Waste PV modules are generated during one of four typical life stages: (1) module production, (2) module transportation, (3) module installation and use and (4) EOL disposal (IRENA and IEA-PVPS, 2016). Early-loss scenarios include loss due to defects, damages, faults and wear-and-tear, whereas regular-loss scenarios only account for degradation over a PV module’s life span, eventually falling below its manufacturing specification or warranty performance. A decommissioned PV module may still be functional but is now less efficient than a new model. In a commercial or utility scale operation, having fallen below the warranty performance, there is a strong financial motivation to replace the module, but for residential or small business usage, this may be within acceptable efficiency requirements.

PV plants will at some point in their life span consider revamping or repowering to improve efficiencies, increase return on investments (Zoco, 2018), reduce maintenance costs, extend the life of the installation (Villena-Ruiz et al., 2024) or adapt to changes in the regulatory environment (IEA-PVPS, 2022). Revamping is the replacement of components of a PV solar system to continue its operation over time but without changing the nominal power output of a plant (IEA-PVPS, 2022; Zoco, 2018). Repowering is the upgrading of a PV plant with more efficient components (Villena-Ruiz et al., 2024), which has a major improvement on the power rating of a plant, thus increasing nominal power output (IEA-PVPS, 2022; Zoco, 2018). At EOL, whether due to an early or regular loss scenario, the PV module would be regarded as waste and needs to be managed effectively in line with circular economy principles.

A circular economy is defined within ISO 59004:2024 as an ‘economic system that uses a systemic approach to maintain a circular flow of resources, by recovering, retaining or adding to their value, while contributing to sustainable development’ (International Organisation for Standardisation (ISO), 2024: 1). Options around repair, reuse, remanufacturing, refurbishment, design for disassembly at EOL and recycling would be considered as part of a circular economy.

Recycling is a lower-order activity and has been defined as to ‘transform a product or component into its basic materials or substances and reprocess them into new materials’ (Ellen MacArthur Foundation, 2021: 3). The PV module recycling is considered to be the transformation, whether by ‘. . . physical, thermal, or chemical processes – into secondary raw materials such as glass, metal, and polymers’ (IEA-PVPS, 2021: 11). Reuse of a PV module occurs when, after the first owner has used it, it is passed on to a second owner who uses it with the same functionality and purpose, whereas repurposing occurs when the second owner uses the module with a different purpose or function to that of the first owner (Heath et al., 2022). Examples of repurposing include PV modules used as building material or a tabletop. Refurbishment is considered to occur when improvements are made to the condition and operating efficiency of the module to bring it in line with its original efficiency or upgrade its functionality.

Drivers, barriers and enablers for a circular economy for PV modules have been considered by authors such as Ariolli (2021), Nyffenegger et al. (2024), Salim et al. (2019) and Tsanakas et al. (2020). Hansen et al. (2022) identified a robust regulatory framework as the most effective tool for promoting circularity in the e-waste supply chain. However, in developing countries, the adoption of solar energy has generally not been accompanied by legislation concerning its management at EOL (Badza et al., 2024). Another key challenge is the quality of imported solar products. Groenewoudt et al. (2020) and Hansen et al. (2022) found that the import of poor-quality off-grid solar systems sped up the timeframe for products to enter the waste stream.

Recycling of PV modules has been an area of existing research (Chen et al., 2023; Deng et al., 2019; Gera et al., 2024; Kolte et al., 2024; Mukwevho et al., 2025; Sharma et al., 2019; Tao and Yu, 2015; Tao et al., 2020; Yu et al., 2022). Research has looked at specific constraints to PV recycling, such as economic feasibility (D’Adamo et al., 2023) and technology appropriateness (Chen et al., 2023; Heath et al., 2020; Mukwevho et al., 2025). However, there is a gap in research on the reuse and repair of PV modules (Munro et al., 2022), especially in developing countries (Badza et al., 2024).

Research on higher-order circular economy activities for solar PV has considered the PV module value chain and the inclusion of EOL activities (Franco and Groesser, 2021; Heath et al., 2022; Simiyu et al., 2023); decision-making between reuse and recycling (Tsanakas et al., 2020); digital product passports and platforms (Boukhatmi et al., 2023); testing of safety and quality for reuse (Marinna et al., 2025) and the need for preparation for reuse (Van der Heide et al., 2023). However, there is limited research on a circular economy for PV modules in South Africa, with the exception of Crozier et al. (2024a, 2024b); GreenCape (2024b); Pandarum et al. (2023); Rhode and Wassdahl (2024); Rivett-Carnac (2022) and Simiyu et al. (2023).

This study aimed to develop a conceptual framework on the drivers, barriers and constraints to a circular economy for solar PV modules in South Africa. Achieving a circular supply chain for solar PV has important implications for meeting international sustainability commitments. The circular economy, which is the focus of Goal 12: Sustainable Consumption and Production of the United Nations Sustainable Development Goals (SDGs), is connected to Goal 7: Clean Energy (United Nations, 2025a, 2025b).

The South African solar PV energy context

South Africa needs to move away from carbon-intensive energy while reducing the negative impact of a transition on job losses and still growing the economy to reduce unemployment. South Africa’s energy is highly resource- and carbon-intensive (CSIR, 2022), with coal contributing 80% to electricity generation and renewables contributing only 14% (CSIR, 2022). The energy sector contributes 46% of South Africa’s greenhouse gas emissions (GreenCape, 2023). Furthermore, with an official unemployment rate of 32.1% in the fourth quarter of 2024 (Statistics South Africa, 2024), South Africa has massive socio-economic challenges. The aim of the just energy transition is to decarbonise the economy to within the target range of 350–420 Mt CO2 by 2030 by focusing on priority sectors such as electricity generation, and it includes social measures such as protecting vulnerable workers and communities and expanding energy access (The Presidency Republic of South Africa, 2023).

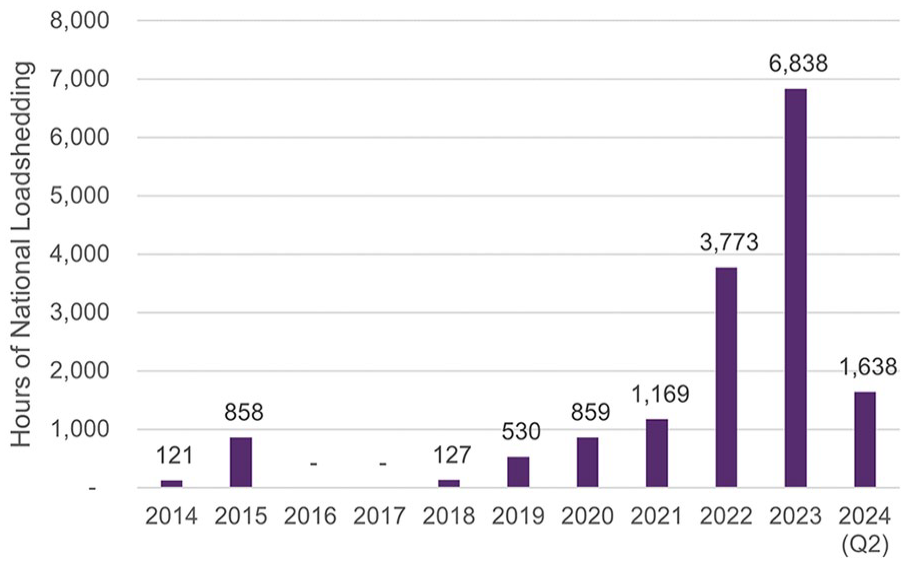

Energy availability is a national crisis in South Africa. Loadshedding occurs when the energy generated by the national energy utility, ESKOM, is rationed through managed rolling power outages to avoid demand exceeding supply and to mitigate the risk of grid collapse. Energy insecurity is socially, economically and politically destabilising for the country (Bhorat and Köhler, 2024; Muller, 2023; Naidoo, 2023). In 2023, loadshedding occurred on 289 days of the year (South African Reserve Bank, 2024), and a total of 6838 (78%) of the hours in the year were lost nationally to loadshedding (Figure 1) (Centre for Renewable Energy Studies (CRSES) Stellenbosch University, 2024). It should be noted that this is the total number of hours in a year that loadshedding occurred anywhere in South Africa and not what a particular household experienced. As loadshedding occurred in managed rolling power outages, areas were cut off from grid electricity in geographical groups at alternating times (typically 4–6 hours per 24-hour period).

Number of hours of national loadshedding per annum, 2014–2024.

Households and businesses have had to absorb the private and social costs of unreliable energy supply (Bhorat and Köhler, 2024) by investing in backup energy sources. This has resulted in the installed capacity of embedded solar PV overtaking utility-scale installed capacity at 5791 MWp (Megawatt peak) compared to 2287 MWp (second quarter 2024) (CRSES, 2024). Other key drivers towards solar energy systems installations have been the above-inflation electricity price increases (GreenCape, 2024a) and declining costs of solar power internationally (IRENA, 2024).

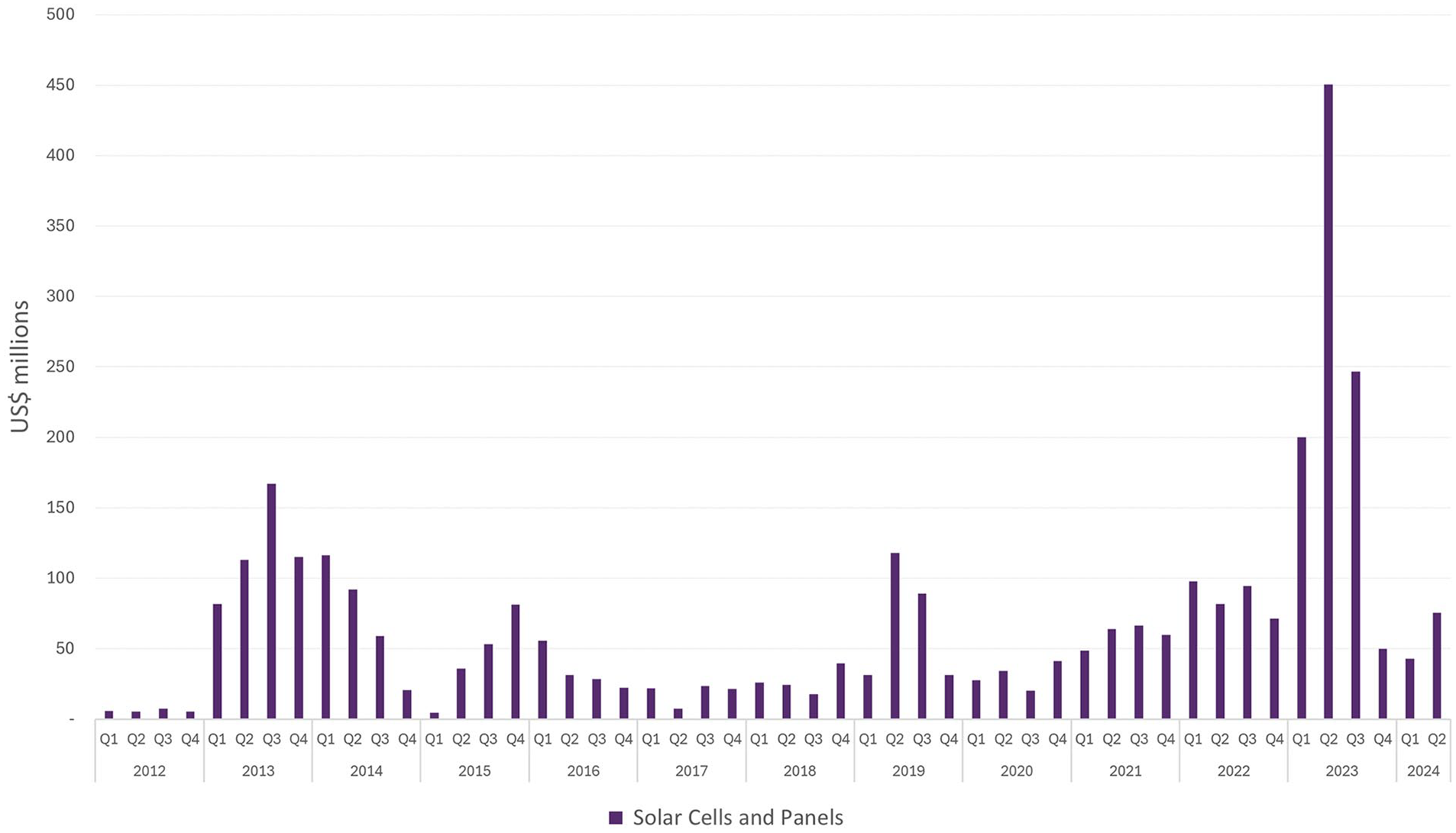

With the increased demand for solar PV systems, the import of solar modules rose exponentially in 2023 and into early 2024. Imports grew to a record US$947 million or R17.5 billion in 2023, a 213% increase on 2022 (Montmasson-Clair, 2024a) (Figure 2). South Africa does not manufacture solar PV modules but it does have a few local assemblers using imported PV module components (GreenCape, 2024c). There are no upstream manufacturers of polysilicon, ingots, wafers or solar cells locally (ECODIT LLC et al., 2022). An import duty, however, was levied in 2024 to help protect local assemblers of PV modules (Jowett, 2024). South Africa imported 90% of its PV modules from China in 2023 by value (Own calculations based on Trade Map, 2023). China produces 80% of PV modules globally across all stages of module manufacturing, that is, ingots, cells and wafers (IEA, 2022).

Imports into South Africa of solar PV cells, panels and modules by value, US$ millions.

IRENA and IEA-PVPS (2016) estimated South Africa’s cumulative PV waste to grow significantly on both regular and early loss scenarios to a cumulative volume of between 8500 and 80,000 tonnes by 2030 and by between 750,000 and 1 million tonnes by 2050. GreenCape (2024c) estimated the number of PV modules coming to EOL annually in South Africa from 2024 to 2060. The forecast, based on dates of installation, estimated limited numbers of waste PV modules from 2024 to 2042, until exponential growth from 2043 onwards, reaching a peak of between 6.3 million and 7.8 million panels p.a. in 2056 (GreenCape, 2024c). Renewable energy (RE) waste has been identified as an emerging waste stream of concern in South Africa (Godfrey, 2021; GreenCape, 2024c; Pandarum et al., 2023; Rhode and Wassdahl, 2024; Rivett-Carnac, 2022).

South Africa is well placed to pursue a circular economy as it has foundational legislation to guide EOL management. Regulations concerning e-waste have been found to be the most important driver of the adoption of a circular economy (Hansen et al., 2022). EEE producers in South Africa are required to contribute towards mandatory EPR programmes through Producer Responsibility Organisation (PRO) membership in terms of the National Environmental Management Act: Waste Act (59 of 2008), which took effect on 5 November 2021. Producers are defined as manufacturers, importers, distributors or refurbishers. Landfilling of e-waste and thus solar PV modules has not been an option in South Africa since 2021 due to the e-waste landfill ban (National Norms & Standards for Disposal of Waste to Landfill of 2013). E-waste is considered hazardous waste and all hazardous waste generators must ensure that their waste is treated within 18 months of generation (RSA, 2013), and they cannot store more than 80 m3 of hazardous waste on-site without undertaking an environmental impact assessment as part of a waste management licence submission (RSA, 2017). Hazardous waste licences are expensive to obtain, and only a few waste management companies in South Africa are accredited to handle waste PV modules due to its hazardous waste categorisation. These regulations offer a strong motivation to develop a circular economy supply chain around regarding PV modules.

Recycling of PV modules currently occurs in South Africa, whereby broken or decommissioned PV modules are transported by accredited waste handlers who separate and aggregate components for different recycling solutions (GreenCape, 2024a) and export materials to processors overseas. One e-waste recycler is undertaking repurposing of the residual waste from recycling PV modules as infill in cement pavers (V&A Waterfront, 2024).

The South African e-waste value chain is categorised by collection through a combination of informal and formal collectors (Lydall et al. 2017). The EPR Waste Association of South Africa (EWASA) estimated that the informal sector accounts for 25% of e-waste recycling in South Africa (EWASA, 2013). Informal collectors called waste pickers collect and sort recyclables, including e-waste from curb-side refuse and landfills to sell to recyclers (Lydall et al., 2017). Earlier, Godfrey and Oelofse (2017) estimated that there could be as many 215,000 waste pickers working in South Africa. However, informal recycling of e-waste is often characterised by limited application of environmental, health and safety controls (Badza et al., 2024; Baldé et al., 2024; Yu et al., 2010). This reduces the quantity and type of materials recovered from e-waste due to cherry-picking (Lydall et al., 2017) is associated with crude and unsafe extraction techniques (Sadan, 2019; Yu et al., 2010).

A circular solar energy supply chain: A conceptual framework

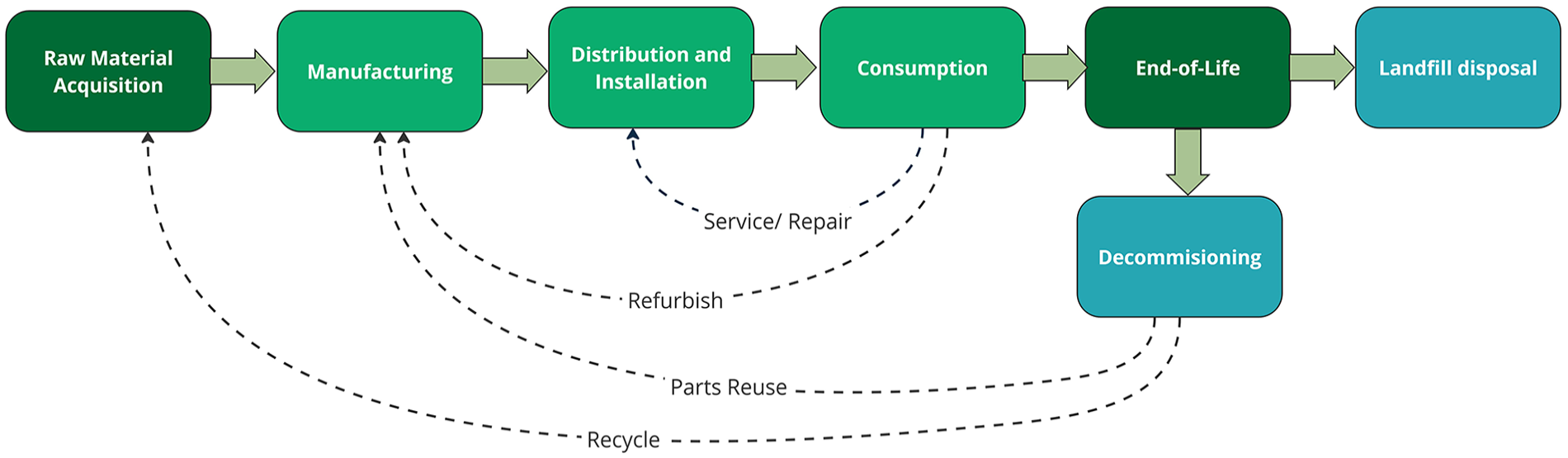

Traditional supply chains are based on a linear flow of materials from extraction to manufacturing, consumption and then EOL, which is usually landfilling. A circular supply chain, which adopts a circular economy perspective, ‘consists of a distributed and interconnected network of partners; relies on multidirectional flows of information, goods and money; delivers and captures value using circular inputs and processes’ (Ellen MacArthur Foundation, 2023: 12). A circular solar energy supply chain might look like Figure 3, where modules are kept in use at the consumption phase through repair and servicing. Alternatively, modules are sent back to the producer for refurbishment. At the decommissioning phase, working components could be reused by manufacturers or consumers. The last alternative is recycling, when broken or defective modules that cannot find an application in higher-order circular economy activities are broken into their material components and re-enter the supply chain. Recycling of PV modules involves thermal, chemical or mechanical processes (Chen et al., 2023). Van der Heide et al. (2023) noted that following the principles of circularity, only unsafe or non-functional decommissioned components should be sent for recycling. Adopting reuse into the supply chain would mean including new steps around the preparation for reuse; such as confirming eligibility, testing, transportation, collection and quality assurance (Van der Heide et al., 2023).

Circular supply chain for solar PV systems.

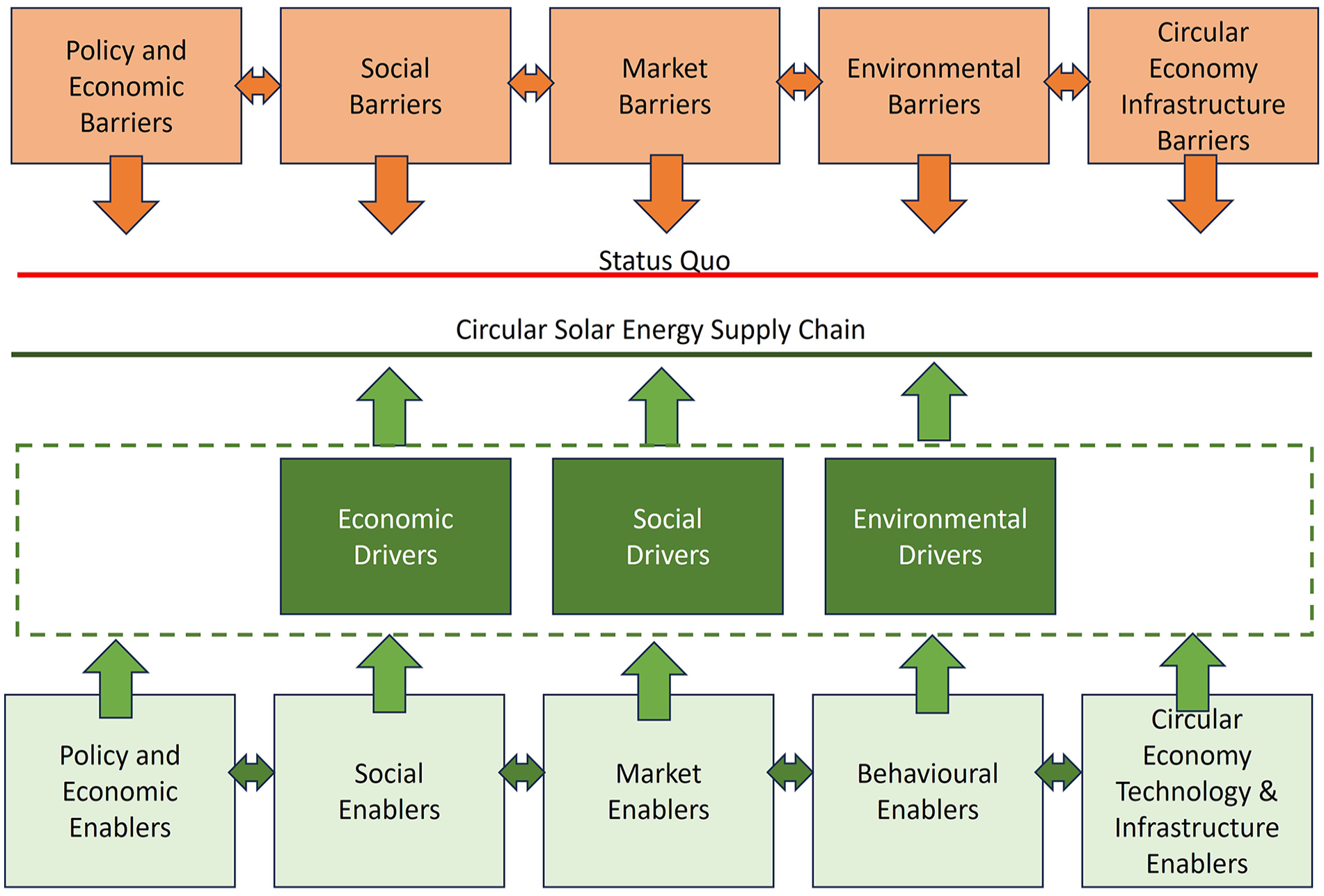

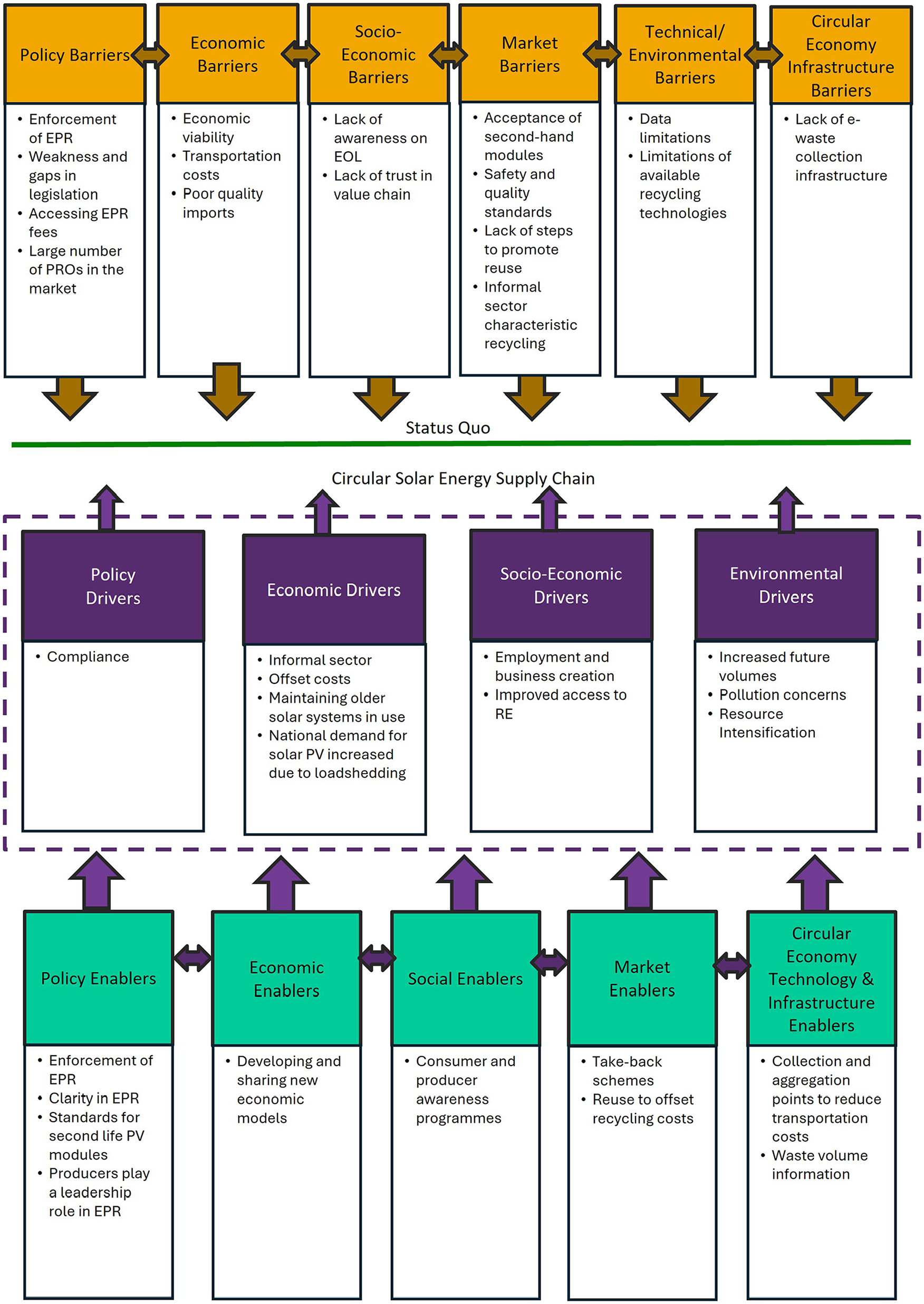

A framework applied by Salim et al. (2019) was used to illustrate the move from a linear to a circular economy for solar PV energy. The framework uses the terms drivers, barriers and enablers. Drivers motivate stakeholders to undertake EOL initiatives; these are the benefits or issues that drive or incentivise change (Salim et al., 2019). Barriers are the challenges and obstacles in transitioning from a linear to a circular economy. Barriers need to be acknowledged so that they can be addressed and mitigated for by policymakers (Salim et al., 2019). Enablers are the implementation tools to overcome challenges and operationalise a circular economy supply chain.

Figure 4 illustrates the circular solar PV energy supply chain proposed by Salim et al. (2019). The diagram shows barriers, enablers and drivers, and how barriers ensure that the economy remains within the status quo unless enablers and drivers are combined. The current study explored the views of stakeholders in the South African PV module value chain on drivers, barriers and enablers to develop a conceptual framework for a circular economy solar supply chain.

Conceptual framework for a circular solar energy supply chain.

Methods

A mixed methods approach was employed, and two data collection instruments were used: (1) a semi-structured interview guide and (2) a survey questionnaire. Data collection was undertaken between November 2023 and March 2024.

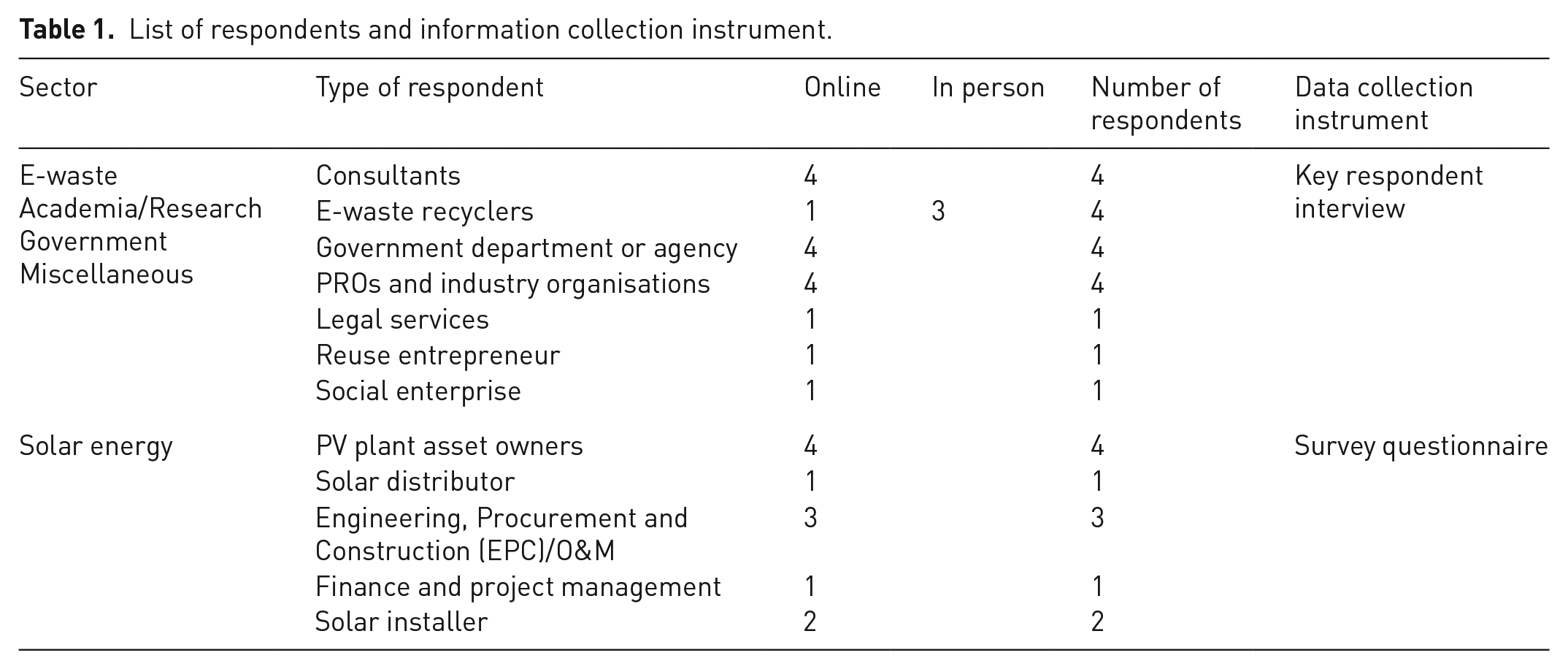

The semi-structured interview guide was employed for key informants and representatives of the e-waste sector using snowball sampling. This was aimed at assessing the general context of the EOL of PV modules in South Africa and constraints and opportunities. Key informants were identified in the government e-waste directorate, industry associations dealing with solar energy, e-waste PROs and e-waste recyclers. The make-up of respondents was as follows: seven respondents were at the executive level; three were consultants in e-waste, circular economy or environmental impact assessments; three were research officers; two were government officials specialising in e-waste and standards, respectively; one was a business owner; one was a RE specialist and one a scientist in waste management. The interview considered aspects of challenges and opportunities to inform the adoption of a circular economy for PV modules, especially regarding reuse. Eighteen interviews were conducted in total.

A survey questionnaire was employed for energy sector representatives to access more specific data on the energy sector’s current approach to roles, responsibilities, budgets and volumes. The sample was drawn from publicly available databases of the South African Photovoltaic Industry Association members. The sample drew on all major independent power producers (IPPs) in South Africa and then used snowball sampling to expand the sample further. A combination of structured and snowball sampling was undertaken. The survey was administered to asset owners, distributors, O&Ms firms and solar installers. Six respondents were at the executive level, four were managers, one was an environmental officer, one was an engineer and one was a business owner. The managers represented technical, plant and supply chain management. A cross-section of the solar industry was surveyed, from utility and large-scale commercial to rooftop residential applications. Twelve survey questionnaires were undertaken in total.

A database of e-waste and solar energy stakeholders was developed. The database contained 109 organisations and 161 persons but was not an exhaustive database of all energy and e-waste operators in South Africa. In total, 30 interviews and/or surveys were conducted out of the 67 organisations approached. Of the sampled persons who were approached but did not take part, eighteen did not respond to email communication and follow-ups, nine indicated some interest but could not be committed to an interview, four indicated they were unable to respond on the topic, three declined and three referred the researchers to another contact.

Table 1 provides the profile of respondents and the type of data collection instrument used.

List of respondents and information collection instrument.

Research ethics (HS23/8/2) was approved by the University of the Western Cape, and all participants were provided an informed consent form and an information sheet prior to undertaking the research.

Three of the 30 interviews were undertaken in person; the remainder were conducted online using the online meeting platform Zoom. All interviews were recorded and later transcribed using AI and then manually checked and proofread against the recording. The final transcripts were uploaded and analysed for themes in Atlas.ti. All survey questionnaires were completed using the online platform QuestionPro.

Qualitative data from the interviews and questionnaires was then analysed and coded into themes around the circular economy of solar energy framework by Salim et al. (2019) using the software program Atlas.ti. Themes were classified into drivers, barriers and enablers. The codes cited by respondents were further grouped and consolidated or differentiated as the analysis continued. The codes were summed up to identify the most popular themes for drivers, barriers and enablers. A framework was developed from previous literature to contrast and compare the South African situation with a conceptual framework and international literature. Stakeholders from the database were invited to attend an online workshop to report back on the findings and gain comments. Thus, the workshop included both respondents and other stakeholders. The final conceptual framework is presented in the ‘Results’ section.

The advantage of this methodology is that it offers a means to access primary data on drivers, barriers and enablers from a variety of stakeholders in the value chain by asking respondents to air their perceptions. The limitation of the study is that it asked respondents to participate, and thus, companies and respondents with a level of interest in the topic of waste and circular economy were more likely than others to respond. It was also identified that there is a high degree of competition between actors in the value chain and thus, accessing certain groups or more sensitive information was difficult.

Results

Drivers

Key drivers identified by respondents towards circular economy adoption were new business and employment opportunities, improved solar energy access, compliance with the legal framework and increased future waste volumes. These were followed by the need to make better use of resources and thus reduce pollution, the informal sector’s uptake of circular economy activities, offsetting costs and growth in solar PV due to energy insecurity in South Africa.

Employment and business creation (eight respondents)

Eight out of 30 respondents indicated job and business opportunities around reuse and recycling were a potential opportunity and driver towards a circular economy. However, they thought the employment impact would be small.

Greater access to RE (eight respondents)

Reused solar modules can be sold at a fraction of the price of new PV modules and could therefore lower the costs of investing in solar energy, thus expanding RE access:

I think the market is clearly there, [there] is good demand for reused PV modules [. . .] especially, [. . .] the bottom end, there would be good demand for low-cost modules (Respondent 30, Solar Industry).

O&M firms are already receiving requests from local communities and charitable organisations for their decommissioned solar modules. Four respondents identified increased requests or needs from the community sector for donations of solar modules as a driver. However, asset owners and O&Ms indicated they were unsure of how the transfer of responsibility would work when donating PV modules at the end of their commercial life and were concerned about potential risks.

Compliance (seven respondents)

South Africa’s legislative framework has created an environment in which formal companies need to take circular actions in order to be legally compliant. Respondents identified compliance as one of the most important drivers of EOL actions (7 out of 30 respondents). It was also ranked high in the survey of energy sector respondents as a crucial determinant in the EOL strategy, with the majority (82%) ranking it as highly important at a 5 out of 5.

Increased waste volumes (six respondents)

As more South Africans adopt solar PV energy, the number of PV modules imported and in circulation increases. These modules will eventually need to be treated at EOL, whether they perform for their entire expected life span or experience an early failure. Furthermore, four respondents mentioned the increased volumes of PV modules in circulation in South Africa to be driven by the energy insecurity caused by loadshedding. This has increased the demand for both small-scale embedded generation (SSEG) and commercial and industrial applications:

Some of those products are really, really good products, and will have a 10, 15-year, 20-year life span. Some have got a few months life span, but the bottom line is the volumes of product that become end-of-life or potentially end-of-life is increasing and will continue to increase on a monthly basis (Respondent 7, PRO and Industry Association).

Pollution concerns (three respondents) and intensity resource usuage (five respondents)

Increased volumes of waste solar PV modules also result in pollution concerns around the hazardous content of PV modules and the need to use resources more intensively. Respondents identified concerns about managing hazardous waste and preventing the dumping of e-waste.

Informal sector in e-waste (five respondents)

The informal e-waste sector is another driver towards a circular supply chain. South Africa has a vibrant informal e-waste recycling and refurbishment sector. If there is any monetary value to be generated in recycling, repairing or reusing PV modules, then the informal sector will likely take advantage of this. Necessity and survivalist activities of the informal sector may mean that circular economy activities are undertaken but not in the most efficient or safe manner. Five of the 30 respondents identified the informal sector as a driver.

. . . the ingenuity that comes from the need in informal markets [. . .] is light years ahead of the formal market (Respondent 18, PRO and Industry Association).

Offset costs of recycling (four respondents)

Four respondents recognised themes of offsetting costs. The reuse of modules offers the opportunity to offset costs associated with decommissioning, repowering or revamping solar plants for asset owners and O&M service providers. For recyclers, reuse is of interest as it could offset the cost of recycling by providing an additional income stream. E-waste refurbishment by recyclers is a practice that is well-established in the information and communication technologies recycling sector. Respondent 1, an e-waste recycler, noted that refurbishing laptops offered better returns than recycling them. The respondent indicated that they could sell a refurbished laptop for R2000 compared to earning R50 to recycle it. Another respondent used the analogy of the refurbished cell phone market:

. . . if you look at it in terms of the second-hand cell phone market, [. . .] 20 years ago, nobody anticipated a second-hand smartphone market to be the size that it is, [. . .].So that’s going to be exactly the same with solar panels . . . (Respondent 13, Consultant).

Another means to save money is for an end-user to maintain older solar systems for longer by replacing failed system components with like-components from reused modules. This could offer cost savings since the entire string of PV modules does not need to be replaced. The difference between end-of-commercial-life and EOL was also identified as offering this gap for the replacement of household systems with reused modules:

It’s still a lot of useful power generation potential in that [decommissioned] panel. The analogy is that if your car is operating at 80% of its power, do you scrap it, or do you sell it? . . . So that’s the thinking we are trying to cultivate. Instead of modules being a waste stream, after the end of commercial life. There is this secondary market (Respondent 10, PRO and Industry Association).

Barriers

Barriers identified by respondents included the lack of enforcement of EPR legislation, weaknesses and gaps in said legislation, the economic viability of reuse, the dearth of awareness on EOL and the limits of available recycling technology. Furthermore, there was a need for quality assurance to ensure safety and peace of mind for consumers, the waste stream was not visible yet, there was an absence of cooperation along the value chain and a lack of information on EOL.

Enforcement of EPR (twelve respondents)

The lack of implementation and enforcement of the EPR legislation was seen as a major barrier. Respondents indicated that there was confusion about the application of policies, that is, who along the value chain must comply with EPR and if EPR was applicable to PV modules. This resulted in ‘free-riding’ when individuals or organisations benefit from a public good but do not contribute towards the provision of that good (Cambridge Dictionary, 2024). When producers do not contribute towards EPR schemes, their competitors shoulder additional costs that they themselves do not, and there are fewer funds available to treat products at EOL. Non-compliant producers were either unaware that they needed to join a PRO or were knowingly non-compliant, as enforcement was limited. There was also a lack of industry support towards the EPR system. Industry role-players felt that it was not a priority for the solar sector at the moment. There was confusion as to whether solar PV modules fell under EEE or rather construction materials due to their very long life spans. Some respondents queried how funds would be safeguarded for use in future years. Of the energy sector representatives interviewed, only two indicated they belonged to a PRO, of which only one correctly named a PRO, and the other provided the name of an organisation which is not a PRO. Thus, there is confusion as to which organisations are PROs versus industry associations and who in the value chain should join a PRO:

There is, unfortunately; I don’t know if there is wilful or just ignorance, but there is very low compliance rate (Respondent 10, PRO and Industry Association). What are the guarantees and the certainties? Will the PROs be around in 20 years? Or 25 years or 30 or 40 years when modules actually reach the waste stream? (Respondent 10, PRO and Industry Association).

Gaps in EPR legislation (eight respondents)

Further to this, respondents identified weaknesses and gaps in EPR legislation (eight respondents). EPR legislation lacks specifics on the types of e-waste to be collected and thus does not specify target volumes of PV modules, and it lacks targets for reuse for any type of e-waste. Recyclers indicated that they have trouble accessing EPR fees from the PROs, and there are difficulties in tracing products back to a particular importer or producer. This is because the system works backwards and tries to associate the waste with the producer or importer, and then recyclers claim fees from the PRO to which that producer belongs. A respondent indicated that improved traceability was needed from the point of entry in the country up until EOL.

EPR legislation has also encouraged a plethora of PROs to register, and there is intense competition between PROs to sign up paying members from the same pool of producers. There were eight PROs registered for e-waste in South Africa as of 1 September 2024 (Department of Forestry, Fisheries and Environment (DFFE), 2024). Respondent 25 was concerned that the competition would lead to reduced outcomes:

I mean, I think what’s going to happen is you’re going to see producers flocking to the ones with the lowest EPR fees. They’re not necessarily going to be the best ones (Respondent 25, Government Department or Agency).

Economic viability (nine respondents)

The profitability of reused PV modules is questionable due to the ever-declining cost of new PV modules and because the capital investment in PV modules makes up a small percentage of the total installation costs. Full recycling of the module is also expensive, and there are limited valuable materials that can be extracted from a PV module:

. . . that’s the problem with solar panels; there’s nothing of value in there. Like a laptop has a PC board, which has quite a lot of value (Respondent 3, Waste Sector).

Transportation costs (six respondents)

The cost of transport is a major economic barrier for recyclers and the potential reuse market. Most PV utility-scale plants are located in remote regions of the country and are a considerable distance from recyclers located in Johannesburg, Durban and Cape Town. PV modules are stockpiled until threshold volumes or length of time in storage is triggered, and they must be processed. Then, recyclers will be contacted for transportation and disposal. Respondents indicated that they thought IPPs had not budgeted for EOL activities. There was limited ability to negotiate the cost of recycling as transportation was the main component, and there were limited accredited service providers:

It’s funny because, unfortunately, no one really budgeted for the end-of-life management on the panels. So, it’s just all the IPPs popped up and they thought all the investment was at the beginning . . . they don’t have to worry about it after that (Respondent 3, Waste Sector).

There is a lack of e-waste collection and sorting infrastructure for solar modules. The potential for utility-scale plants to cooperate, which could assist in reducing transportation costs, has not been considered.

Negative consumer perceptions (six respondents)

Respondents also associated economic viability with negative consumer perceptions on second-hand products (six respondents). They stated that second-hand products are traditionally seen as having poorer quality or safety. Respondents were concerned that South African consumers were unfamiliar with solar modules and would struggle to determine differences in performance between new and second-hand modules, thus being unable to judge value for money. Consumers would also need to be trained on maintaining their reused solar modules. Solar installers and those working in the SSEG sector were the least positive about reusing solar modules. They were concerned about costly and time-consuming callbacks from customers. The most positive respondents were those in the large-scale commercial and industrial (C&I) and utility-scale sectors. They saw opportunities for reuse to reduce the costs of revamping or decommissioning solar systems.

Quality concerns (four respondents)

Poor quality imports will also have an impact on the economic viability of reuse. Respondents indicated they were concerned about the quality of recent PV module imports. The quality in the utility and large C&I markets is generally better as they have procurement contracts that specify the equipment quality and procure from top-tier manufacturers. Poor quality imports mean PV modules are likely to enter the waste stream faster, and they may also have latent defects that make them unlikely candidates for reuse:

It also speaks to the life cycle of those solar panels. The expected life cycle may be 20 years, but if it is a cheap or bad import, then the life cycle definitely would not be 20 years (Respondent 18, PRO and Industry Association).

Invisible waste stream as yet (seven respondents)

The waste stream is not visible yet, and there are low numbers of modules that can actually be reused so as to allow a reuse offering to be viable. Thus, steps need to be introduced into the value chain to promote reuse. There are currently low volumes of waste PV modules that can be repaired and given another life. Being an as yet invisible, this waste stream also has implications for PV module EOL activities to access financial incentives and government assistance.

Lack of leadership from producers and absence of awareness on EOL (nine respondents)

Producers need to be made aware of and educated on their role and importance in the EPR system. End-users can also be made aware of their role in promoting circularity through proper care, knowing that solar modules have an EOL and that there are recycling providers within South Africa:

I think there’s very little awareness around the fact that it [the PV module] does actually fall under the EPR regulations. And there’s very little awareness that there actually are recyclers in South Africa who are prepared to take them and recycle them (Respondent 25, Government Department).

Recycling technology (nine respondents)

Another area of concern is the lack of a recycling technology in South Africa. There are positive and negative aspects associated with the different recycling technologies – the negatives may include the emission of toxic substances as by-products or being highly energy-intensive. Investing in these technologies costs recyclers money, and they have no access to financial incentives to support the investment. The type of technology selected is also based on which waste fractions are commercially viable to recover or whether legislation will enforce the recovery of certain materials. Informal sector recycling may lead to only the easy-to-access waste fractions being recovered, while the residuals are dumped or burnt. Thus, interventions are needed to support the informal and formal sectors through innovation, research and development into the best technologies for the South African market.

Recycling is influenced by the market demand for materials, and the bulk of PV module composition is made of glass. The easiest material to recover from a PV module is the aluminium frame. One respondent indicated that their previous market for recovered glass recyclate had ceased after the glass processor client had closed. Others referred to the issue of glass being contaminated with additives:

There’s glass from e-waste. No one will even touch it with a barge pole (Respondent 3, Waste Sector).

Quality assurance is needed through standards (seven respondents)

A major barrier to reuse, cited by respondents and in the international literature (Ariolli, 2021; Tsanakas et al., 2020), is the lack of a standard for a second-life PV module. Without developing standards, quality, value for money and safety will be impossible to ensure. Seven respondents in the study cited concerns about fire risks, reputational damage and customers not receiving value for money if no standards were in place:

You don’t want a case of someone buys a second-hand panel from you, and six months later it stops working because it’s going to damage your brand . . . (Respondent 3, Waste Sector).

Lack of coordination and cooperation in value chain (six respondents)

There is a lack of trust and cooperation in the value chain. The poor enforcement of waste legislation and the draconian penalties for non-compliance have added to conflict among stakeholders:

We’ve got very, very punitive measures in place for non-compliance, which is not normally the case if you look at many of the EU EPR schemes (Respondent 25, Government Department or Agency). We don’t want to fight with them [producers], but at the same time, we’re trying to educate them. Uh, and it’s a big frustration [. .] because DFFE should be the ones who are doing the fighting (Respondent 3, Waste Sector).

Data limitations (five respondents)

There is a lack of data on the extent of the waste PV modules in South Africa, which makes it impossible to adequately understand the extent of the problem:

Once we have a better understanding of those amounts being pulled off and the amount going to the secondary market, going to recycling, I think then we could start having those conversations (Respondent 10, PRO and Industry Association).

Enablers

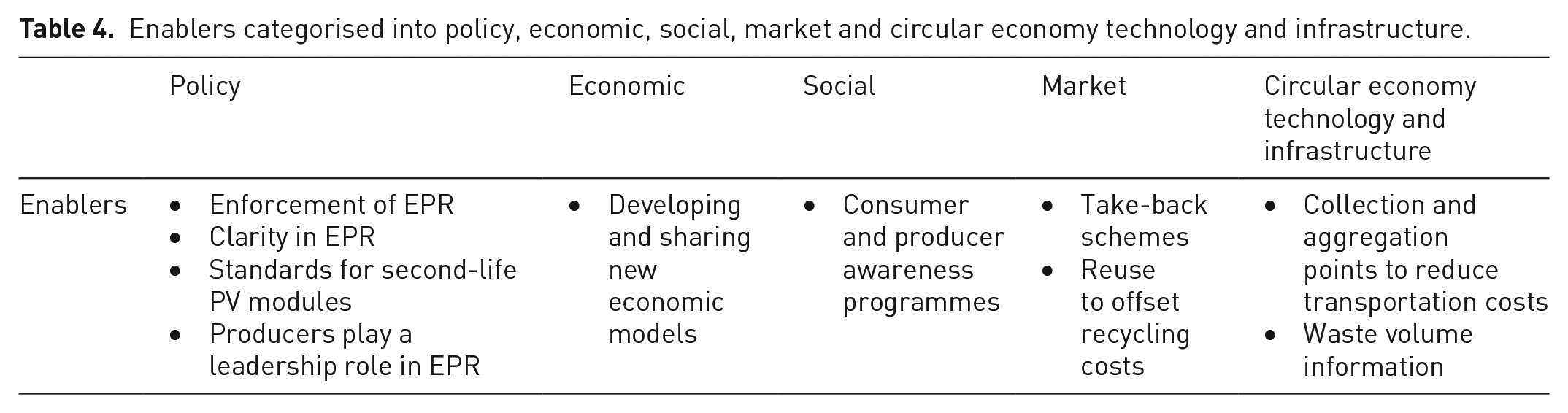

The main enablers identified by respondents were testing and standardisation for module recertification, instituting take-back schemes, collecting and aggregating points and producers leading the cooperation regarding EPR. These were followed by improved enforcement of EPR, instituting awareness programmes and cooperation along the value chain, developing and sharing circular economy models and case studies and reuse to offset costs.

Testing and standardisation for module recertification (nine respondents)

Respondents identified the need for standards for quality and safety to be adopted in South Africa; this includes testing protocols and standards for second-life solar PV modules. These standards are needed to recertify PV modules so that they can be legally and safely resold in formal markets.

Development of take-back systems, collection and sorting infrastructure (eight respondents)

Aggregation points in remote provinces and recycling schemes could be developed through EPR fees and the support of producers. This could assist in reducing transportation costs, especially if the modules’ hazardous waste components are removed prior to transportation. EPR fees could also be accessed to develop repair and refurbishment centres and training programmes for technicians. Through these repair centres, the informal sector could be supported.

Producers should play a leadership role in EPR (seven respondents). Producers can play their part in EPR through payment of PRO membership fees and directly contributing towards the development of targets and strategies. Producers are vital stakeholders and must take up a leadership position in policy, enforcement and planning:

The producers just need to step up now and take responsibility for their products at end-of-life (Respondent 25, Government Department or Agency).

Enforcement of EPR (four respondents)

This entails better enforcement of policy and would include targets to increase participation in EPR schemes and the involvement of the South African Revenue Service and Customs Authority at ports of entry. These interventions would aim to reduce free-riding and promote wider PRO membership:

But working together with customs has significantly reduced the number of free-riders. You can easily catch them at the ports of entry when they bring in the product (Respondent 20, Government Department or Agency).

EPR policy clarity (five respondents) and Norms and Standards (four respondents)

The afore mentioned enabler also links to the need for greater clarity on EPR, to clearly define and articulate PV modules within e-waste and their targets and to the drafting of National Norms and Standards (four respondents). National Norms and Standards have been drafted for e-waste generally, but the solar industry can assist in developing technical guidelines for managing waste PV modules specifically:

It [Norms and Standards] might be able to remove that bottleneck that we currently have with the waste management licence and also to provide opportunities for informal sector integration (Respondent 23, Consultant).

Consumer and producer awareness programmes (six respondents)

Consumer awareness programmes would focus on maintenance, installation and EOL management. This would assist in extending the life span of products and ensuring that decommissioned PV modules are of good quality and more likely to find a second life. Awareness campaigns with producers could also assist in improving relations within the value chain by making producers aware of their responsibilities. There is a need to improve trust in the value chain through better information sharing, facilitating cooperation and enforcing legislation to prevent free-riding.

Researching and promoting new circular business models in select sectors (five respondents)

Researching the opportunities and constraints of sector-specific reuse applications could assist in understanding future applications and identifying suitable sectors with lower barriers to entry. This would allow for information sharing on potential applications of reuse and recycling. Certain sectors may be better positioned to trial new circular economy models concerning PV modules than others.

Information on the extent of volumes of EOL PV modules (five respondents)

Data on the numbers of EOL PV modules would assist role-players in planning and investment decisions.

Reuse to offset cost (five respondents)

Recyclers may wish to offer reuse as a means to offset the high costs of recycling for clients. Reverse logistics and reuse could make recycling more affordable. Careful decommissioning, packaging and transportation would assist in maintaining the quality of PV modules destined for reuse. Reuse would need to be supported by testing services of PV modules and the support of the insurance sector for extended warranties.

Discussion

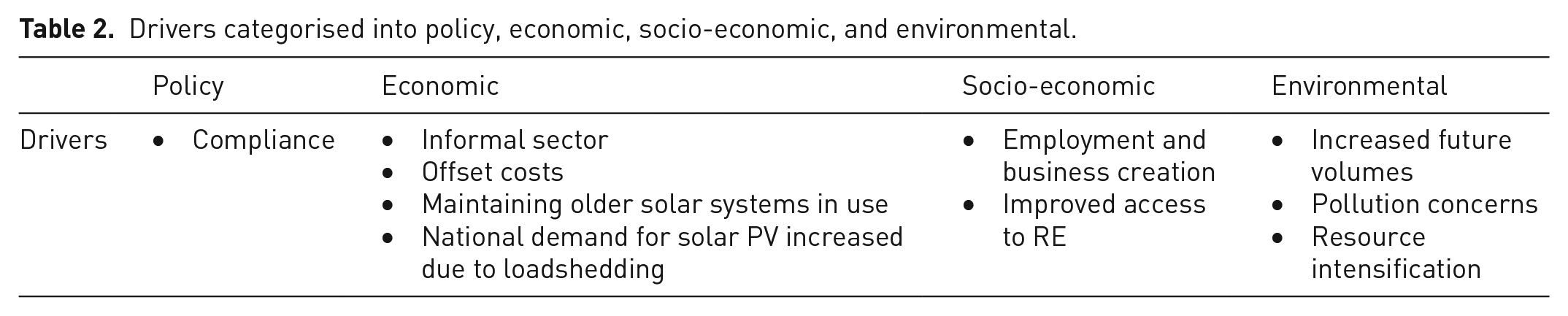

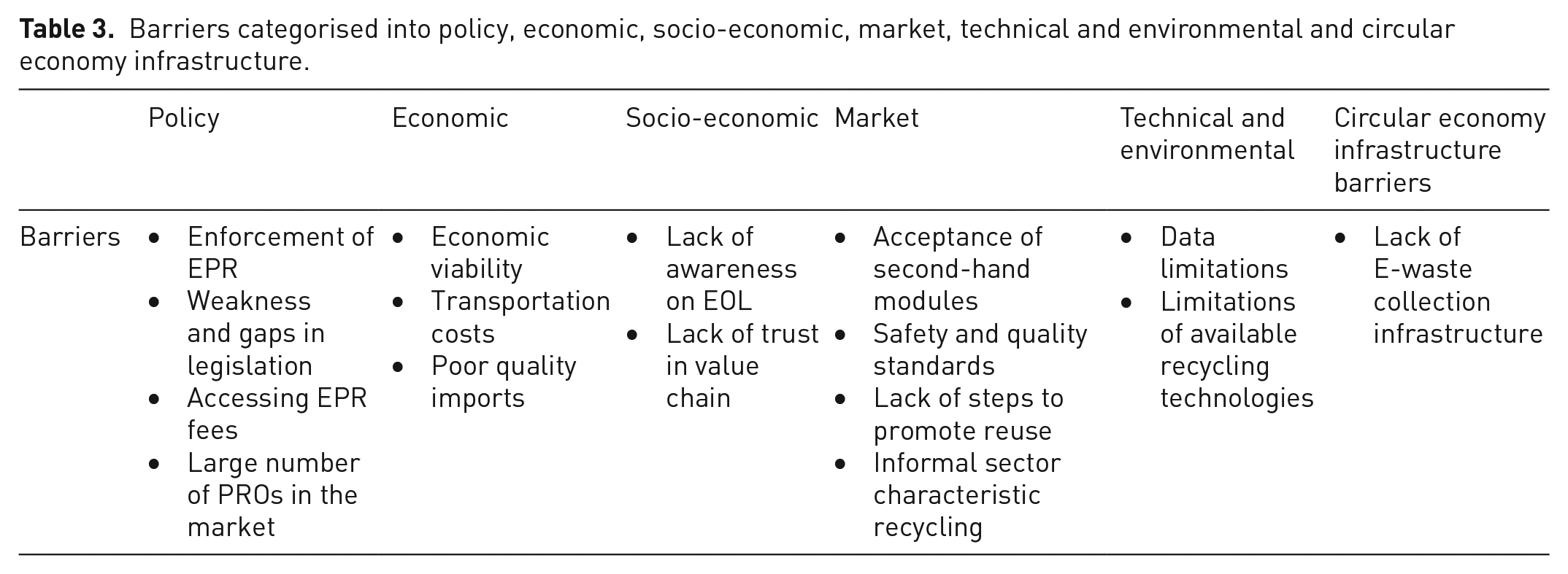

Figure 5 provides a graphical summary of the findings on the drivers, barriers and enablers for a circular South African solar PV module supply chain. Tables 2–4 list the results under each sub-category.

Drivers, barriers and enablers for a circular South African solar PV module supply chain.

Drivers categorised into policy, economic, socio-economic, and environmental.

Barriers categorised into policy, economic, socio-economic, market, technical and environmental and circular economy infrastructure.

Enablers categorised into policy, economic, social, market and circular economy technology and infrastructure.

The findings of this study are illustrated in an expanded version of Salim et al. (2019) original framework.

Drivers identified in the study are categorised in Table 2. A policy driver is the presence of a robust regulatory framework in South Africa. Economic drivers identified were the growth in demand for solar PV energy due to energy insecurity and the interest from actors in the value chain to bring down the cost of recycling or extend the life of their solar systems through reuse interventions, as well as the presence of an active informal sector that would take up opportunities in the supply chain. Socio-economic drivers include the possibility of job creation, new business development and greater access to RE. This aligns with the just energy transition and a just circular economy transition. Environmental drivers are the increased volumes of EOL modules, the dangers of pollution and the need for resource intensification.

A robust regulatory framework was identified by Hansen et al. (2022) as the most effective tool for promoting circularity in the e-waste supply chain. South Africa’s legal framework concerning e-waste and EPR creates an excellent foundation for a circular supply chain to be developed, although compliance is centred on formal businesses. Kinally et al. (2022) linked the lack of a legislative framework for PV waste management to dangerous recycling practices and the informalisation of the recycling sector in Africa. In developed economies, pressures from external stakeholders have compelled governments to develop e-waste policies and make investors comply due to a fear of reputational damage (Ariolli, 2021; Hansen et al., 2022; Salim et al., 2019). Ariolli (2021) noted that as a driver the opportunity for solar systems could be kept in use for longer by using reuse modules to replace or repair older installed systems.

In this study’s findings, socio-economic and economic drivers were the most prominently mentioned drivers towards a circular economy model for solar PV systems. This aligns with South Africa’s developing country context, where aspects of social and economic improvement and development are of immediate concern. Encouraging employment and business development in South Africa are of critical importance. The RE transition has been identified as a route to generating new industries and job opportunities. Job opportunities of the circular economy for PV systems was recognised in Salim et al. (2019). The labour-intensive nature of reuse means it offers greater job creation potential than recycling (RREUSE, 2021). Reuse was estimated to create between 60 and 140 jobs per 1000 tonnes of collected waste electrical and electronic equipment in a developed country context (RREUSE, 2021).

Making RE more accessible would align with national aims concerning the just energy transition (The Presidency Republic of South Africa, 2023) and achieving the SDGs. To achieve SDG target 7.2 that by 2030, there is a substantial increase in the share of RE in the global energy mix (United Nations Department of Economic and Social Affairs, 2024) will require not only new PV module applications but also a vibrant second-hand market for modules.

Neglecting PV waste modules could impact ecosystems through pollution, and drive more demand for virgin material extraction, thus causing biodiversity loss and reducing the positive environmental impact of solar energy (Tan et al., 2022). The focus of innovation in PV modules has been on improvements in efficiencies with little to no focus on designing for circularity (Chen et al., 2023). Now researchers, recyclers and policymakers need to fill the research gap and recommend the best methods to recycle this waste stream. However, PV modules are highly complex products to recycle because they are a combination of a number of materials and most challenging of all is to remove the encapsulant layer of ethylene-vinyl acetate (EVA) to access the materials within the silicon cells. Although the module contains valuable materials, they are in small amounts compared to glass, which constitutes the bulk of the module. Glass made up 68–72% of crystalline silicon modules but only 10–11% of their value in 2021 market prices (IEA, 2022). There needs to be an emphasis on not only developing environmentally sound recycling practices that can access materials at a preferred recovery rate and purity level, but they must also be cost-effective (Franco and Groesser, 2021). This implies not only technology developments but also processes and systems to reduce recycling costs.

Barriers drawn from the results are classified in Table 3. Policy barriers were identified around implementing and enforcing the laws fairly and effectively to prevent free-riding and to provide greater clarity. There were also inherent weaknesses within the legislation that resulted in confusion and ineffectiveness, such as how fees were charged and accessed, how products were traced through their life spans and the number of PROs collecting EPR fees. The economic viability of reuse still needs to be proved, especially with low international prices of new modules and an oversupply of modules in the market. There are also high transportation costs due to the distance from recyclers and the hazardous nature of the product being transported. Poor quality imports make reuse unlikely and may also contain little critical raw materials for recyclers. Socio-economic barriers include the lack of cooperation between stakeholders in the supply chain and the need for consumer confidence in second-hand products. The lack of standards for reused modules and testing is a market barrier to consumer safety, peace of mind and formalisation of the market. Modules at EOL will need to be prepared for reuse, and this will require a change in the treatment of EOL PV modules and new steps in the value chain. Technical and environmental barriers are that recycling currently focuses on low-value materials and sends the remainder to be crushed and disposed of. There is no ideal recycling innovation that is nationally or internationally accepted, and it is not economical to recover all the materials within a PV module in South Africa. Circular economy infrastructure barriers include the lack of collection and aggregation points.

Recycling of PV modules can either be considered as bulk, semi-high value or high-value recycling (Chen et al., 2023). Bulk recycling of crystalline silicon modules involves recovery of the basic materials, that is, metal and glass. There is no recovery from the semi-conductor and cells. This means a greater volume of the module is recycled, but the recovered materials are of a lower quality. Semi-high value recycling is a selective recovery approach that prioritises certain valuable metals from the module. High-value recycling is the most comprehensive approach, since both basic materials and materials from the semi-conductor are recovered. The aim is to maximise the amount and variety of materials extracted. A major barrier to recycling is that there is no internationally agreed-upon best practice technology. There are many concerns that need to be balanced in selecting a technology. The three main technologies are mechanical, thermal and chemical (Chen et al., 2023). Mechanical techniques are labour-intensive and thus have low investment requirements but mechanical crushing causes noise (Chowdhury et al., 2020) and dust pollution that contains lead or silicon and the materials recovered have low purity and thus low utilisation rates (Chen et al., 2023). Thermal techniques, especially pyrolysis, are the best for removing the EVA layer to access valuable materials in the cells. Unlike chemical methods, pyrolysis does not produce harmful by-products such as dioxins and polychlorinated biphenyls (PCBs) (Zhang et al., 2016). However, it can emit hazardous elements such as lead and cadmium (Preet and Smith, 2024). It is also very energy-intensive and thus expensive to undertake (Chen et al., 2023). Chemical processes are also effective in removing the EVA layer to extract high-purity silver and silicon. The purity of the silicon is high enough to potentially allow for closed-loop recycling (Dias et al., 2016). The disadvantages are that the recycling process includes the handling of toxic chemicals, which in the case of organic solvents can create harmful by-products (Preet and Smith, 2024). It is also time-consuming and requires specialised chemicals and knowledge to undertake (Gera et al., 2024), thus making it an expensive method. Although research has found recycling to be more beneficial to the environment than the extraction of new raw materials, especially around carbon emissions, recycling does have negative effects (Maani et al., 2020). Thus, recycling is not the silver bullet of EOL waste management strategies for PV modules, certainly not until research and innovation catch up.

Other challenges identified in literature regarding circular economy for solar modules are illegal flows of waste to developing countries (D’Adamo et al., 2023). Sometimes under the guise of reusable PV modules but of very poor quality, they instantly become waste. Global production of PV modules is concentrated in China, which makes localising value chains to recover materials and form closed-loop recycling a challenge. Increased geopolitical tensions (D’Adamo et al., 2023) and the need to reduce supply chain vulnerability (Ariolli, 2021) are also concerns.

The economic viability of recycling is a key barrier. Research by D’Adamo et al. (2023) found that PV module recycling plants were only profitable, even under favourable market conditions, when a landfill disposal cost was applied. Costs that make recycling expensive include high transportation costs as the modules are often transported from remote areas to processors and the waste categorisation as hazardous (Xu et al., 2018). Furthermore, a great deal of manual labour is needed in decommissioning, dismantling and recovery of materials (Franco and Groesser, 2021), and there is a risk of cross-contamination between materials (Besiou and van Wassenhove, 2016). Chen et al.(2023) noted that the high costs could lead to improper recycling practices; thus, cost-saving processes should be prioritised.

The challenges of reuse also lie with the economic viability of recycled materials. Tsanakas et al. (2020a) point out that these include low accessible volumes and concerns over the efficiency and reliability of the second-life products.

Enablers identified in the results can be classified as per Table 4. Policy enablers involved stronger enforcement of legislation, greater clarity on EPR and the need for standards for recertification. Norms and standards for PV module e-waste could be developed nationally to provide guidance on the handling of modules. This could also help bridge the gap until an international testing and performance standard is developed. Another policy enabler would be greater compliance and leadership from producers to implement and plan for EPR. Economic enablers include the development of new markets and business models that should be further researched and promoted, as well as how they could be adopted by different role-players in the supply chain. Social enablers include consumer and producer awareness programmes. Market enablers include take-back schemes and reuse being used to offset recycling and decommissioning costs. Research on volumes and potential sectors where reuse would be most appropriate, and circular economy technology and infrastructure enablers identified were using EPR to support PV module collection, sorting and aggregation systems, and repair and refurbishment. Training could tap into EPR funds to cover proper installation, module maintenance over lifetimes and basic repair skills for common module repairs. Information was needed on waste volumes and here, facilitation by government or industry third parties could assist in the collection of data on EOL PV modules to forecast future volumes.

Efforts by the International Electrotechnical Commission and research programmes such as CIRCUSOL and the Photovoltaics Quality Assurance Task Force (PVQAT) Task 15 (Van der Heide et al., 2021) are currently underway to develop a reuse standard for PV modules. Standards play an important role in value chains, especially for new technologies, as they promote adoption and acceptance.

New business models for reuse are being explored internationally. For the utility and large C&I plants, it could involve selling decommissioned modules, direct trading, turnkey solutions, or donations (Trust-PV, 2023). Circular business models concerning the finance of PV systems, such as leasing (Leaseurope, 2024) and product service systems (Van Opstal and Smeets, 2023) may also make circularity a greater possibility.

Recommendations for a circular economy for PV modules have included defined regulations and legislation, awareness campaigns, national and regional collection systems, incentives for recycling and reuse, facilitating better access to new technologies for recycling and better health and safety and environmental controls during recycling (Badza et al., 2024). Chen et al. (2023) identified the need to establish pre-treatment sites near PV plants to reduce the volume of solar panels transported and to remove hazardous components. This could prioritise local usage of components and materials and is critical to improve the economic viability of both recycling and reuse.

From analysis of the findings, the following broad recommendations for initiatives to support reuse activities for PV modules can be made:

Adopt international testing and quality standards for recertification of second-life PV modules.

Expand PV module testing services and make testing more accessible.

Provide incentives and financial support for recycling and reuse initiatives, through EPR or other funding instruments.

Use EPR funds to support collection, sorting and aggregation points; repair centres and offer training on repair.

Develop Norms and Standards for PV module handling.

Research sector-specific applications for reuse, for example, in agriculture.

Enhance the traceability of products through their life span.

Include steps for reuse preparation in the value chain.

Ensure enforcement of EPR with producers and at ports of entry with the customs authority.

EPR fees must be related to quality to promote better quality imports.

Conclusion

Globally, countries have committed to achieving the United Nations SDGs, which requires concerted action on pollution, climate change, inequality and peace. The most relevant SDGs to PV module EOL are SDG Goal 7 on Clean Energy and SDG Goal 12 on Sustainable Consumption and Production (United Nations, 2025a, 2025b). A circular economy can help achieve Goal 7 by increasing access to RE through second-life PV modules and ensuring that critical raw materials for clean energy production are conserved and do not enter our environment as pollution. In turn, as solar PV producers are made aware and public pressure builds, they will increasingly design for circularity, and there will be better adoption of EPR, thus aligning with SDG 12.

There is a compelling case for reuse, but until there is an agreed performance and quality standard, the trade in second-life modules will be a marginal economic activity. The practical application of a circular economy to PV modules in South Africa is a balancing act between a complex set of considerations and trade-offs. It requires consideration of challenges of technology availability, standards, economic feasibility and environmental impacts. This study considered the perceptions of role players in the value chain, but there is a need for modelling of the extent of the PV waste problem and empirical studies of the application of reuse. Further research should be undertaken on the market viability, consumer acceptance of second-life PV systems and the role of the informal economy in the South African PV EOL value chain.

Footnotes

Acknowledgements

The authors would like to thank the Technology Innovation Agency of South Africa (TIA) and the National Research Foundation (NRF) funded Community of Practice: Waste to Value (UID 128149) for their financial support towards this study. The NRF accepts no liability for the views expressed by the authors of this paper.

Author contributions

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Technology Innovation Agency of South Africa (TIA) and The National Research Foundation (NRF) funded Community of Practice: Waste to Value (UID 128149).

Ethical considerations

Research ethics was granted under HSSREC Reference Number: HS23/8/2 by the University of the Western Cape, Humanities and Social Sciences Research Ethics Committee.

Consent to participate

The University of the Western Cape, Humanities and Social Sciences Research Ethics Committee approved interviews and surveys (HS23/8/2) on 16 October 2023 for the period 27 September 2023 to 26 September 2024. Respondents gave written consent for review and signature before starting interviews or surveys.