Abstract

This study addresses a critical gap by providing an in-depth examination of how cryptocurrency markets respond to U.S. monetary policy shocks at various price levels. This study contributes significantly to our understanding of the nuanced dynamics governing cryptocurrency markets under diverse monetary policy conditions, thereby enhancing our knowledge of the broader financial ecosystem. Through rigorous quantitative analysis, we utilize monthly time series data spanning from January 2015 to December 2023 and employ models such as Markov-switching dynamic regression, Autoregressive Conditional Heteroskedasticity, and Generalized Autoregressive Conditional Heteroskedasticity. This study reveals that monetary policy shocks result in a decrease in cryptocurrency prices and volatility. Moreover, monetary policy tightening stabilizes the market at low cryptocurrency prices. In higher price states, interest rate increases are associated with reduced cryptocurrency prices and volatility. The findings suggest that changes in interest rates influence the opportunity cost of holding cryptocurrencies, impacting their appeal compared with traditional interest-bearing assets.

Keywords

Introduction

The intersection of cryptocurrency markets and U.S. monetary policy remains a complex and underexplored domain. In the face of evolving economic landscapes and policy decisions, there exists a notable gap in our understanding of how cryptocurrencies respond to U.S. monetary policy shocks, particularly at different price levels. The existing literature lacks a comprehensive investigation of the nuanced impact of monetary policy on cryptocurrency prices and volatility, especially when examining both high and low levels of cryptocurrency valuation. Many studies have modeled cryptocurrency using Bitcoin returns and volatility (Bouri et al. (2018); Vidal-Tomás and Ibañez (2018); Corbet et al. (2020); Shaikh (2020). On the other hand, Alam et al. (2024) suggest that Bitcoin can serve as a diversification tool for portfolios during volatile times. Bouri et al. (2018) highlight the impact of exchange rate fluctuations, currency crises, and spillover effects on European banks, which influence investment decisions in cryptocurrencies. It is noted that current research has largely focused on the general reactions of financial markets to monetary policy shocks, often neglecting the unique characteristics of the cryptocurrency market’s different regimes. In contrast, the positive and adverse effects of monetary policy on cryptocurrencies have been explored. Noteworthy studies by Nguyen et al. (2019), Shaikh (2020), and Ma et al. (2022) indicate that an increase in interest rates or monetary tightening results in a fall in Bitcoin or cryptocurrency prices. In contrast, research conducted by Corbet et al. (2020), Elsayed and Sousa (2022), Choi and Shin (2022), and Karau (2023) reveal that monetary policy tightening leads to an increase in cryptocurrency prices.

The existing gap is evident in the absence of a detailed exploration of how cryptocurrency prices and volatility patterns respond specifically to U.S. monetary policy shocks and how these responses vary across different price levels. Understanding the dynamics at both high and low valuation points is crucial for developing a nuanced understanding of the relationship between U.S. monetary policy and cryptocurrency markets. This study bridges this gap by conducting a data-driven exploration of price and volatility patterns in cryptocurrency markets in response to U.S. monetary policy shocks. By analyzing both high and low-price levels, this study seeks to provide a comprehensive understanding of how varying levels of cryptocurrency valuations interact with and respond to changes in monetary policy. This study contributes to the body of knowledge by offering insights into the specific dynamics governing cryptocurrency markets under different monetary policy conditions, thereby enriching our understanding of the broader financial ecosystem. Central banks often use interest rates to influence their economic activities. When interest rates are low, the opportunity cost of holding non-interest-bearing assets such as Bitcoin decreases. Investors may allocate more funds to Bitcoin, seeking higher potential returns than traditional assets. Cryptocurrencies, such as Bitcoin, are non-interest-bearing assets. Changes in interest rates can affect the opportunity cost of holding cryptocurrencies compared with traditional interest-bearing assets. For instance, if central banks lower interest rates, the appeal of holding cryptocurrencies may increase, as the opportunity cost of not earning interest in traditional assets decreases.

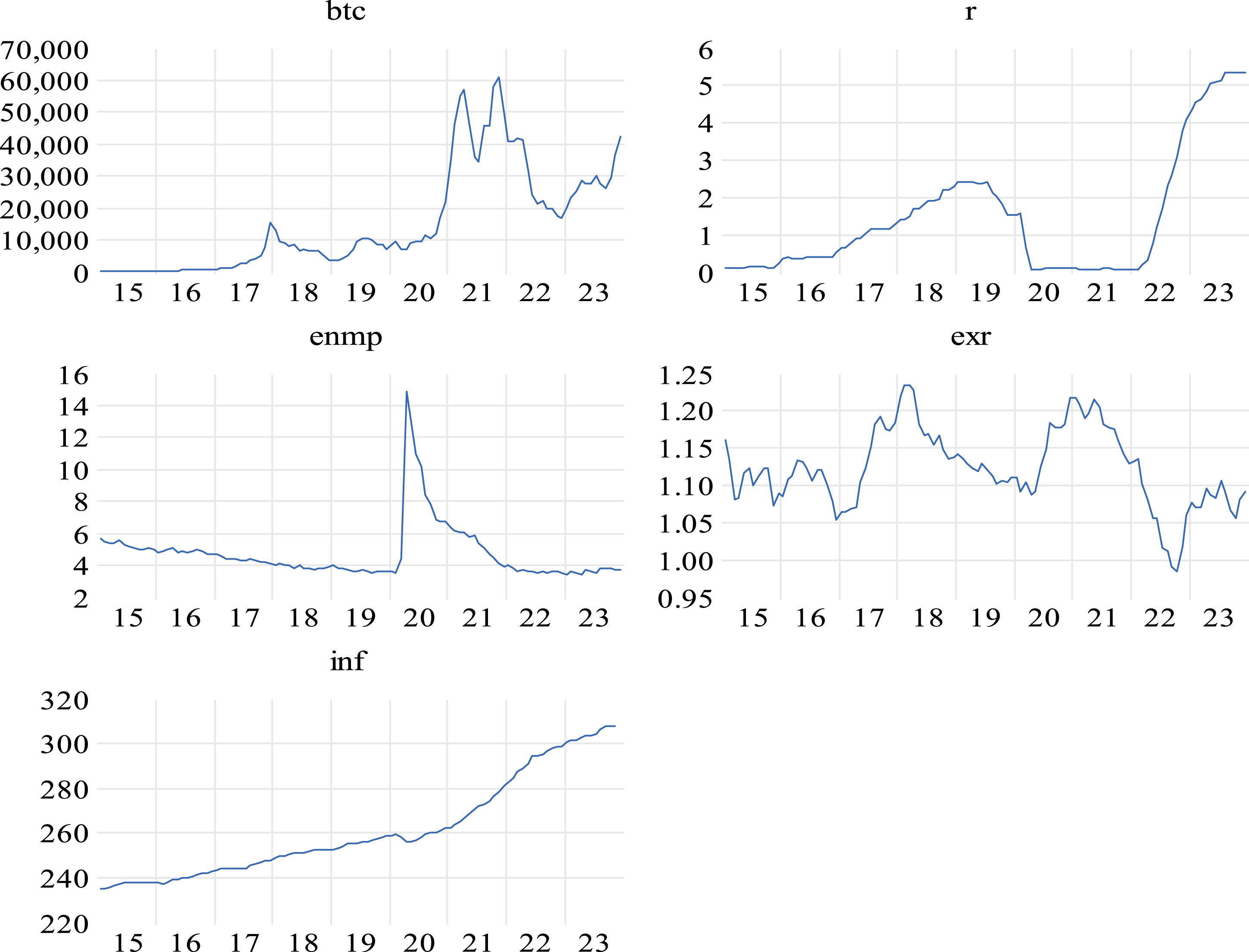

Figure 1 shows the economic variables. The price dynamics of Economic variables.

Considering the background, problem statement, and gap outline above, the key economic question of the study is how do cryptocurrency prices and volatility patterns respond to U.S. monetary policy shocks specifically at different price levels? Given the questions of this paper, the hypotheses are as follows:

Hypothesis 1

Null: Monetary policy (interest rate) has no significant effect on cryptocurrency price. Alt: Monetary policy (interest rate) has significant effect on cryptocurrency price.

Hypothesis 2

Null: Monetary policy (interest rate) has no significant effect on cryptocurrency price volatility. Alt: Monetary policy (interest rate) has significant effect on cryptocurrency price volatility.

This study investigates the impact of U.S. monetary policy shocks on cryptocurrency markets, focusing on both high and low valuation levels. Utilizing Markov-switching dynamic regression models, this study explores the responses of Bitcoin prices and volatility to interest rate changes in different market states. The findings reveal that interest rate increases are associated with positive price movements, even in states of lower Bitcoin prices, suggesting a consistent impact on cryptocurrency values. Additionally, monetary tightening is linked to reduced volatility, indicating potential market stabilization. This study further observes distinctive responses at varying valuation levels, emphasizing the need for a comprehensive understanding of cryptocurrency dynamics under diverse monetary conditions. This study contributes to bridging the existing gap in the literature by offering insights into the specific interactions between U.S. monetary policy and cryptocurrency markets, enriching our comprehension of the broader financial system.

The remainder of this paper is organized as follows. The second part provides a literature review. The third part discusses the methodology used in this study. The fourth part discusses the descriptive statistics and empirical results. Finally, the fifth part presents the conclusions of the study.

Literature Review

Theoretical Review

The dynamic price framework has two dominant views which are Rational Expectations Theory (RET) and the Efficient Market Hypothesis (EMH). However, the empirical reality of Behavioral Finance (BF) casts a critical shadow on the seemingly airtight logic of these traditional frameworks. RET advocates that market participants are rational and use all available information efficiently to form expectations of future events. RET implies that prices incorporate all relevant information. It advocates that expectations are unbiased, reflecting the true underlying value of assets (Ellis & Bernard, 1985; Kale, 2020). Behavioral Finance deviates from the assumption of perfect rationality in RET and introduces psychological factors into the analysis of market behavior. BF acknowledges that market participants may exhibit cognitive biases and make decisions based on emotions, heuristics, and social influence. This departure from rationality may result in market anomalies such as overreactions, underreactions, and herding behavior. Understanding these behavioral patterns provides valuable insights into market inefficiencies and the potential for mispricing (Königstorfer & Thalmann, 2020; Takemura, 2021). The EMH states that financial markets are informationally efficient, with asset prices reflecting all available information. The three forms of EMH—weak, semi-strong, and strong—differ in the scope of the information considered in the pricing process. EMH has implications for investment strategies, suggesting that consistently outperforming the market through active trading or information-based strategies is challenging (Borges, 2010, Kelikume, 2020). The economic theory of volatility is the Random Walk Theory, which suggests that asset prices follow a random walk, meaning that future price movements are unpredictable and not influenced by past prices (Hong et al., 2007; LeRoy & Parke, 1992). Autoregressive Conditional Heteroskedasticity (ARCH) suggests that volatility is not constant over time but rather follows a pattern of conditional heteroskedasticity (Engle, 1982). Generalized Autoregressive Conditional Heteroskedasticity (GARCH) is an extension of the ARCH model, the GARCH model incorporates not only past volatility but also past squared returns in the volatility equation. This allows the model to capture both short- and long-term volatility Bollerslev (1986).

Empirical Review

In recent years, the burgeoning popularity of Bitcoin has prompted extensive research aimed at unraveling the intricate connection between this monetary policy and cryptocurrency. Bouri, Das et al. (2018), Vidal-Tomás and Ibañez (2018), Demir et al. (2018), and Nguyen et al. (2019) collectively explore diverse aspects of Bitcoin’s relationship with economic factors and spillovers in market conditions to Bitcoin’s autonomy amidst monetary policy. Bouri et al. (2018) investigated the spillovers between Bitcoin and other assets during bear and bull markets using daily data from July 19, 2010 to October 31, 2017, and the VARGARCH model. The spillovers exhibit some differences in the two market conditions and the direction of the spillovers, with greater evidence that Bitcoin receives more volatility than it transmits. Vidal-Tomás and Ibañez (2018) examined Bitcoin’s semi-strong efficiency regarding monetary policy from September 13, 2011 to December 17, 2017, using a GARCH model. The results indicate Bitcoin’s independence from monetary policy news, emphasizing its autonomy as a financial asset pertinent to investors and policymakers. Demir et al. (2018) empirically explored the predictive relationship between economic policy uncertainty (EPU) and Bitcoin returns from September 16, 2010 to November 15, 2017, utilizing the Global Structural Vector Autoregression (GSVAR) model. This study reveals that EPU significantly predicts Bitcoin returns. Nguyen et al. (2019) examined the asymmetric monetary policy effects on cryptocurrency markets from October 1, 2015 to August 15, 2018, utilizing Fixed Effects and GMM models. They revealed noteworthy responses in four major cryptocurrencies, including Bitcoin, to Chinese monetary tightening policies, whereas U.S. monetary policies exhibited no significant impact on cryptocurrency returns.

Level of volatility spillovers, nonlinear effects of monetary policy, and varied responses to uncertainty in different regions on cryptocurrency have been examined by Corbet et al. (2020), Yang (2020), Lyócsa et al. (2020), and Shaikh (2020). Corbet et al. (2020) used the EGARCH model to analyze cryptocurrency reactions to FOMC announcements. The findings indicate that monetary policy announcements are resilient to volatility spillover. Mineable digital assets are more susceptible to monetary policy volatility spillovers and feedback than non-mineable assets. Yang (2020) investigated the nonlinear relationship between Bitcoin monetary policy using the smooth transition autoregressive model with exogenous variables (STARX) from February 2, 2012 to August 31, 2019. It was found that there is a threshold effect, and the monetary policy threshold has a nonlinear impact on the return on the closing price of Bitcoin. Lyócsa et al. (2020) examined the volatility of BTC from January 2013 to December 2018 using the GARCH model. It was found that responds most significantly to news on Bitcoin regulations and positive investor sentiment. Notably, there is evidence that monetary policy announcements do not influence Bitcoin volatility. Shaikh (2020) investigated policy uncertainty and Bitcoin returns using a Markov regime-switching model with monthly data from January 18, 2010, to September 15, 2018. Bitcoin returns were found to be more responsive to EPU in the US, China, and Japan. In the US and Japan, uncertainty has a negative effect on the Bitcoin market, whereas in China, it has a positive effect.

The diverse methodologies employed by Jiang et al. (2022), Elsayed and Sousa (2022), Marmora (2022), and Ma et al. (2022) shed light on the distinct facets of this relationship, providing a comprehensive view of the impact of factors such as volatility spillovers, international monetary policies, and national monetary policy on the dynamics of Bitcoin markets. Jiang et al. (2022) investigated the volatility spillover mechanism between the financial market and Bitcoin using VMD with the time-varying parameter vector autoregressive (TVP-VAR) model to generate spillover indicators. Bitcoin serves as the volatility communicator. In addition, the role of each major commodity in the volatility spillover system is significantly correlated with its respective financial properties. Elsayed and Sousa (2022) analyzed daily data from August 5, 2013 to September 27, 2019, investigating the dynamic spillovers of international monetary policies on cryptocurrencies. Employing a TVP-VAR model, they find significant cryptocurrency return fluctuations and notable monetary policy spillovers, especially during negative shadow policy rates. The spillovers exhibited minor differences between the Fed’s “unconventional” and “standard” policy eras. Marmora (2022) employed a fixed effects model on 32,147 daily observations across 26 nations spanning from January 1, 2015 to December 31, 2019, to explore the impact of monetary policy on Bitcoin demand. This study discovered that monetary policy influences holders of national currencies to explore decentralized virtual alternatives. Notably, monetary policy announcements correlated with heightened local attention and increased trade volume in Bitcoin. Ma et al. (2022) investigated the influence of US monetary policy shocks on Bitcoin prices using a Vector Autoregression (VAR) model spanning July 19, 2010 to December 31, 2020. The results showed a notable association, resulting in a 0.25% reduction in Bitcoin prices during periods of monetary tightening, a magnitude akin to the observed effect on gold prices.

Bitcoin’s intricate relationship with economic variables, systematic reactions to monetary, parallel currency, and qualitative research have been undertaken by Choi and Shin (2022), Khan and Hakami (2022), Asimakopoulos et al. (2023), and Karau (2023). Choi and Shin (2022) exploration, spanning from July 2010 to June 2019, using a TVP-VAR model, revealed that Bitcoin reacts systematically to monetary and central bank information shocks. Disinflationary shocks from the Federal Reserve increased Bitcoin prices, whereas those from the European Central Bank decreased them, suggesting limited support for Bitcoin as an inflation hedge. Khan and Hakami (2022) examined the nature of cryptocurrency risks and their function as money using an inductive approach to a descriptive analysis of qualitative research. It was found that the cryptocurrency system does not follow a transparent process that can make it parallel to conventional fiat currency. Benigno (2022) examined monetary policy in the cryptocurrency era using a DSGE model and discovered that currency competition influences central banks’ control over interest rates and prices. In a dual currency setting with competing physical or digital cash, the cryptocurrency’s growth rate imposes an upper limit on achievable nominal interest and inflation rates for the government currency to maintain its role as a medium of exchange. Asimakopoulos et al. (2023), a Bayesian DSGE model, revealed that increased cryptocurrency productivity raises the relative price of government currency. Fluctuations in cryptocurrency prices are driven by demand shocks, whereas changes in real balances for government currency result from both government currency and cryptocurrency demand shocks. Karau (2023) examined the relationship between monetary policy and Bitcoin by applying a structural vector autoregression (VAR) model, utilizing monthly data from January 2014 to February 2023. The findings reveal a dynamic evolution in the impact of monetary policy on Bitcoin over a specified period. Notably, the analysis discerned a historical tendency for Bitcoin prices to exhibit an upward trajectory following periods characterized by tight monetary policy measures.

Cheng (2023), Tomić et al. (2020), Palit and Mukherjee (2022), and Alam et al. (2024) contribute to unraveling the complex interplay between monetary policies and cryptocurrency. They explore the dual impact of Federal Reserve rate hikes on Bitcoin prices to assess the evolving role of cryptocurrencies in monetary policy and their sensitivity to structural breaks, these studies offer diverse perspectives on the intersection of traditional financial frameworks and the digital currency revolution. Case in point Cheng (2023) studied the time-varying impact of a Federal Reserve rate hike on Bitcoin, using data from June 1, 2021 to August 15, 2022, employing VAR and ARMA-GARCH models, and revealed a dual impact on the financial market. Additional cash in global financial markets may indirectly shift towards the U.S. and cryptocurrency markets, boosting demand and prices. Conversely, an immediate increase in the exchange rate may prompt funds to exit other markets, leading to reduced demand and prices. Tomić et al. (2020) investigated the effects of cryptocurrency on monetary policy through qualitative analyses. The findings suggest that there is no significant threat to traditional monetary systems. However, given the cryptocurrency market’s early maturity, future trends may reduce the influence of central banks as private cryptocurrency usage grows. Palit and Mukherjee (2022) investigated the cryptocurrency role of in monetary and fiscal policies. Monetary policy was found to play a crucial role in influencing the regulatory framework and acceptance of cryptocurrencies. The effectiveness of monetary policies directly affects the success and integration of digital currency. Alam et al. (2024) investigated monetary policy and cryptocurrencies using the structural break GARCH model from April 2013 to July 2022. They found that cryptocurrencies exhibit long-term volatility sensitive to structural breaks, and there is a need to consider monetary policy to assess cryptocurrency volatility and diversification.

Literature provides that there is multifaceted relationship between Bitcoin and monetary policy, highlighting significant volatility spillovers, predictive capabilities of economic uncertainties, and varied responses to global monetary actions. Key insights reveal that Bitcoin often receives more volatility than it transmits and largely operates independently of monetary policy news, suggesting its potential as an autonomous financial asset. Additionally, the influence of economic policy uncertainty and regional monetary tightening policies on Bitcoin returns has been noted. Despite the extensive research employing diverse methodologies, gaps remain in understanding the long-term implications of cryptocurrency integration into traditional financial systems and the potential regulatory challenges posed by its growing adoption. Literature emphasizes the necessity for further investigation into the evolving dynamics between digital currencies and conventional economic frameworks. On the other hand, literature review highlights several gaps in our understanding of the relationship between Bitcoin and monetary policy. Among these included present conflicting evidence, with some suggesting Bitcoin’s independence and others finding dependence on monetary policy. The impact of monetary policy on Bitcoin returns seems to differ across regions, requiring further investigation. The studies primarily focus on short-term interactions. Research is needed to explore the long-term consequences of a growing cryptocurrency market on monetary policy. While some studies show Bitcoin’s volatility is impacted by monetary policy, a clearer understanding of the underlying mechanisms is needed. The relationship between Bitcoin and monetary policy is likely to change as the cryptocurrency market matures.

Methodology

Economic Variables Utilized.

The Markov-switching dynamic regression model (MSDRM) was adopted in this study. The MSDRM is used because it provides attractive features of transition over a set of finite regimes (Hansen, 1996). The cryptocurrency market is dynamic and evolving. Traditional models such as VAR and SVAR assume constant parameters over time, which may not capture the evolving relationship between economic variables and cryptocurrency prices. The MSDRM model addresses this limitation by allowing parameters to vary across different regimes, thus providing a more realistic representation of the changing dynamics within the market. Cryptocurrency prices and volatility are influenced by myriad factors, and the relationships between these factors can change over time. Therefore, the flexibility of the MSDRM model in capturing the varying relationships between economic variables and cryptocurrency performance makes it a suitable choice for data-driven exploration of price and volatility patterns.

Theoretical Framework

This study uses the EMH as the theoretical framework, which asserts that asset prices fully reflect all available information. The framework is shown in equation (1)

Model Specification

Volatility Specification Using ARCH and GARCH

The ARCH

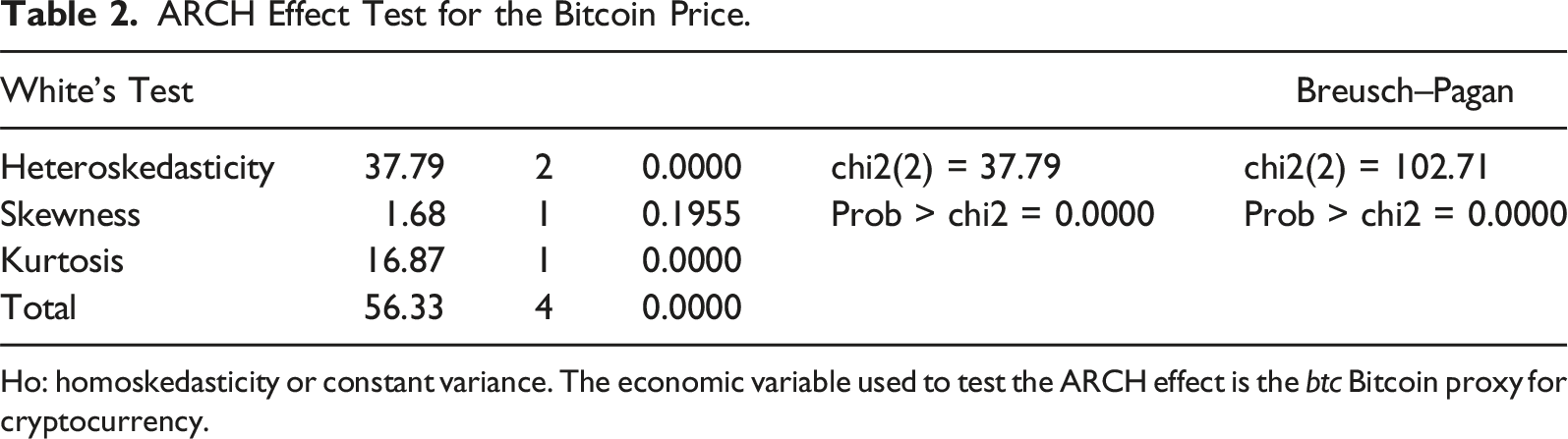

ARCH Effect Test for the Bitcoin Price.

Ho: homoskedasticity or constant variance. The economic variable used to test the ARCH effect is the

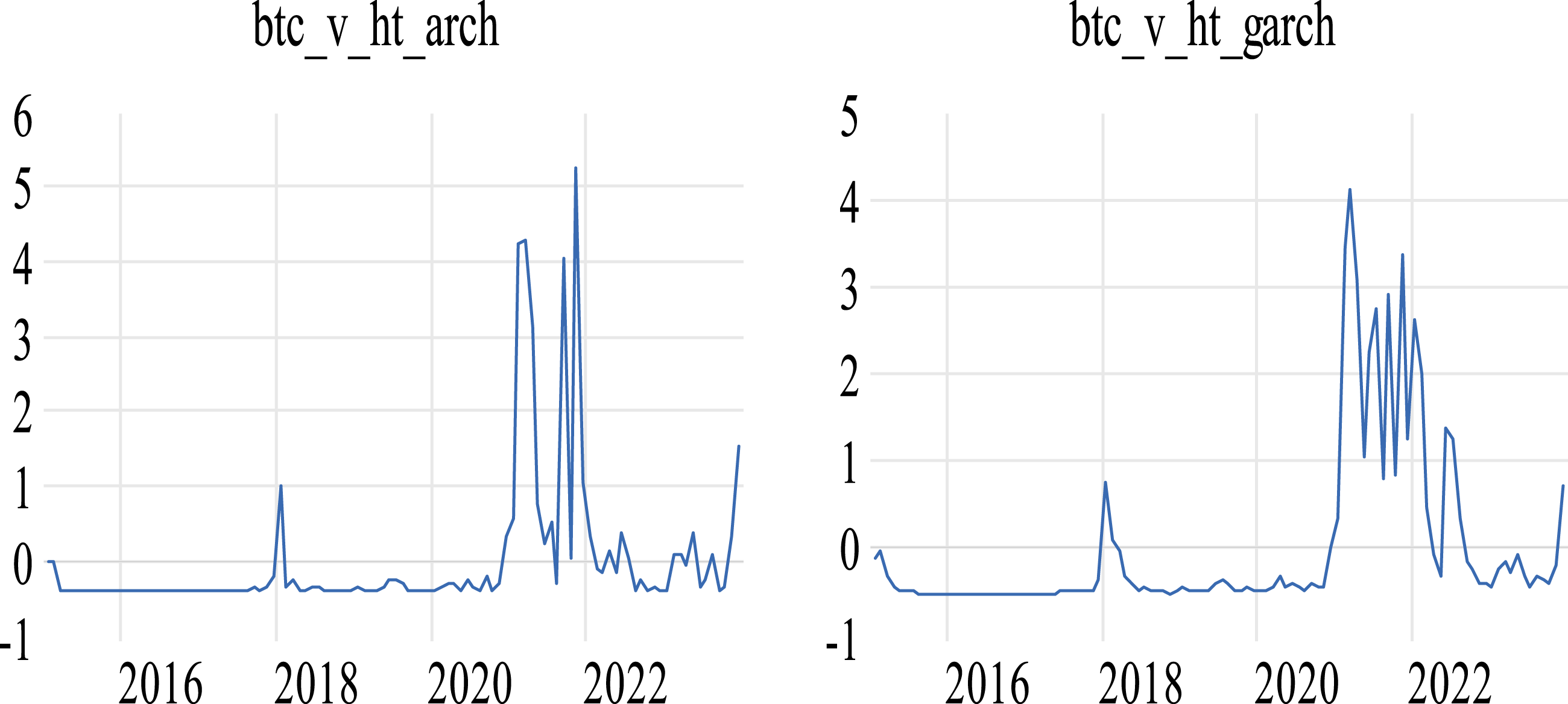

Figure 2 shows the estimated data of the economic variables of volatility used to estimate the effect of monetary policy shocks on cryptocurrency. This result is Economic variables of volatility.

Markov-Switching Dynamic Regression

Markov-switching dynamic regression is used for series that are believed to transition over a finite set of unobserved regimes, allowing the process to evolve differently for each regime. The transitions occur according to a Markov process from one regime to another, and the duration between changes in the regime is random (Hansen, 1996, 2000). If given economic data series denoted by

Because of the dynamics of the explanatory variables, the former has constant transition probabilities, and the latter has time-varying transition probabilities, making them susceptible to changes in the shape of the transition probabilities from one regime to another. Equation (10)

The subscript

The transition probabilities

Results

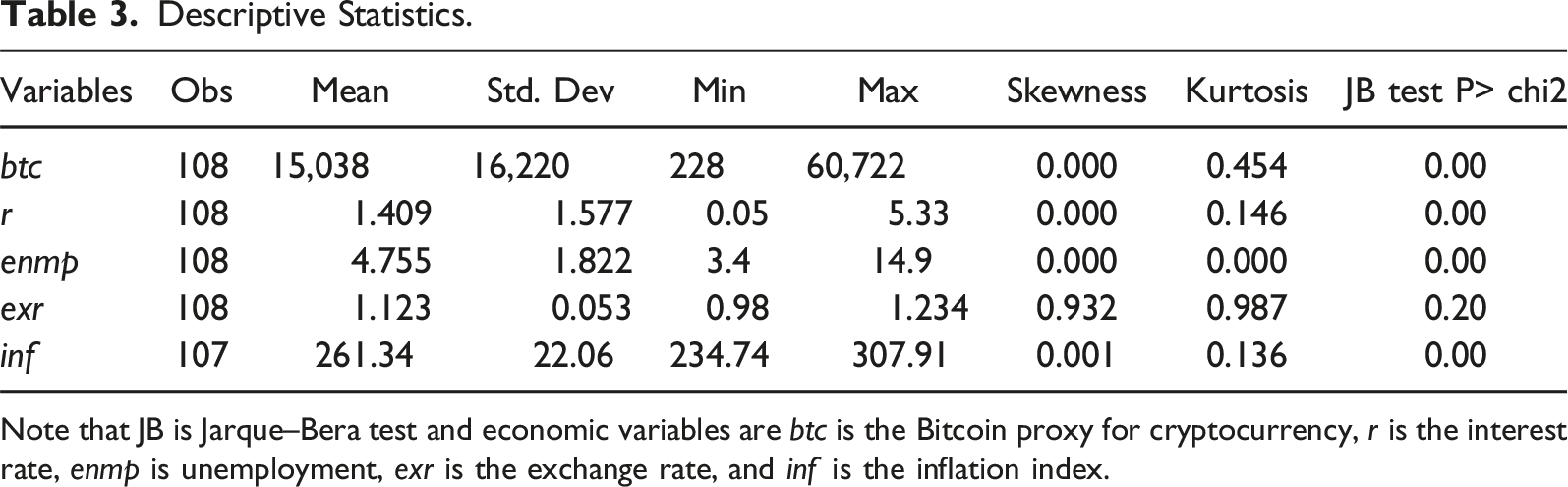

Descriptive Statistics.

Note that JB is Jarque–Bera test and economic variables are

In parallel, an average interest rate of 1.409 reflects a moderate level, mirroring a stable economic environment. Similarly, the unemployment rate at 4.755, with skewness and kurtosis values of 0.000, indicates a symmetric distribution around the mean, reinforcing the notion of stability. Within this stable economic backdrop, characterized by steady interest rates, moderate unemployment, and inflation, the environment appears conducive to both traditional and digital assets. A mean exchange rate of 1.123 indicates stability in the currency, while a mean inflation index of 261.341 suggests a moderate inflationary environment. However, the positive skewness in the exchange rate introduces a nuance, implying the potential risk of currency appreciation.

Table 3 suggests that according to the normality tests proposed by (Jarque & Bera, 1980), the null hypothesis of normality can be rejected 1 for a significant portion of the series at the conventional 5% significance level. This indicates that the variables included in the model exhibit characteristics that deviate from the assumptions of a normal distribution. These deviations, often manifested as non-normal skewness, imply the potential presence of nonlinearities within the data. The detection of non-normal skewness through the Jarque–Bera tests prompts consideration of alternative modeling approaches that can accommodate such complexities. Nonlinear models and dynamic regression analyses incorporating Markov-switching mechanisms offer robust frameworks for capturing the effects of regime changes and non-normalities in the data. By allowing for flexible specifications that adapt to changing patterns over time, these models can enhance the robustness of estimation procedures and improve the accuracy of inference, even in the presence of non-normal skewness.

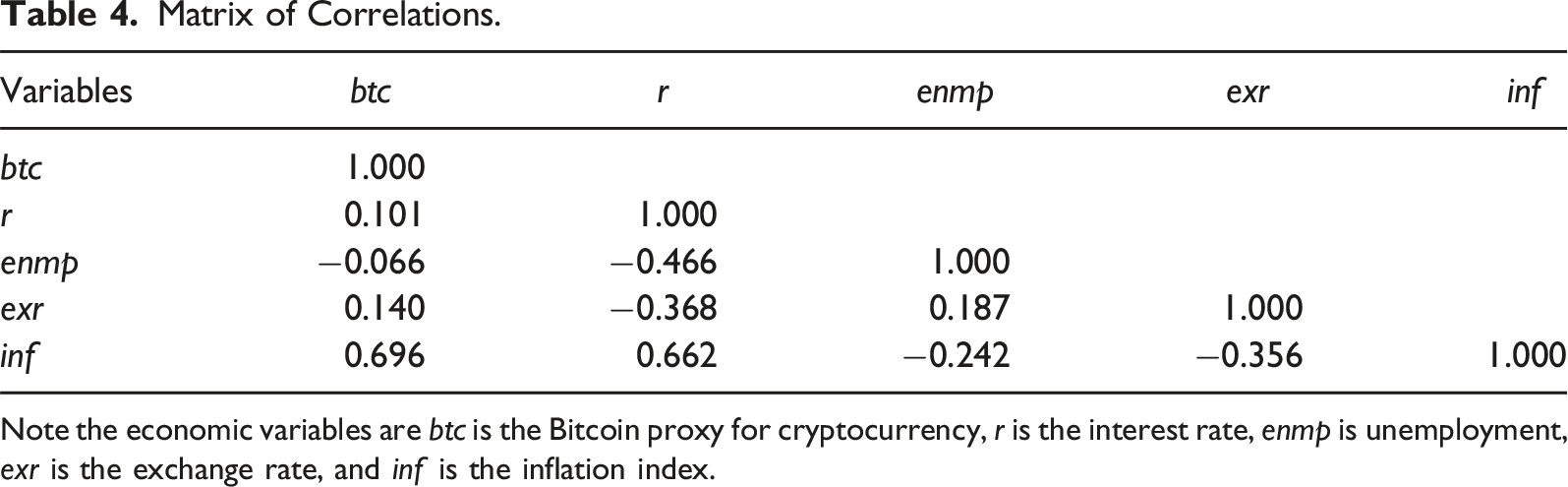

Matrix of Correlations.

Note the economic variables are

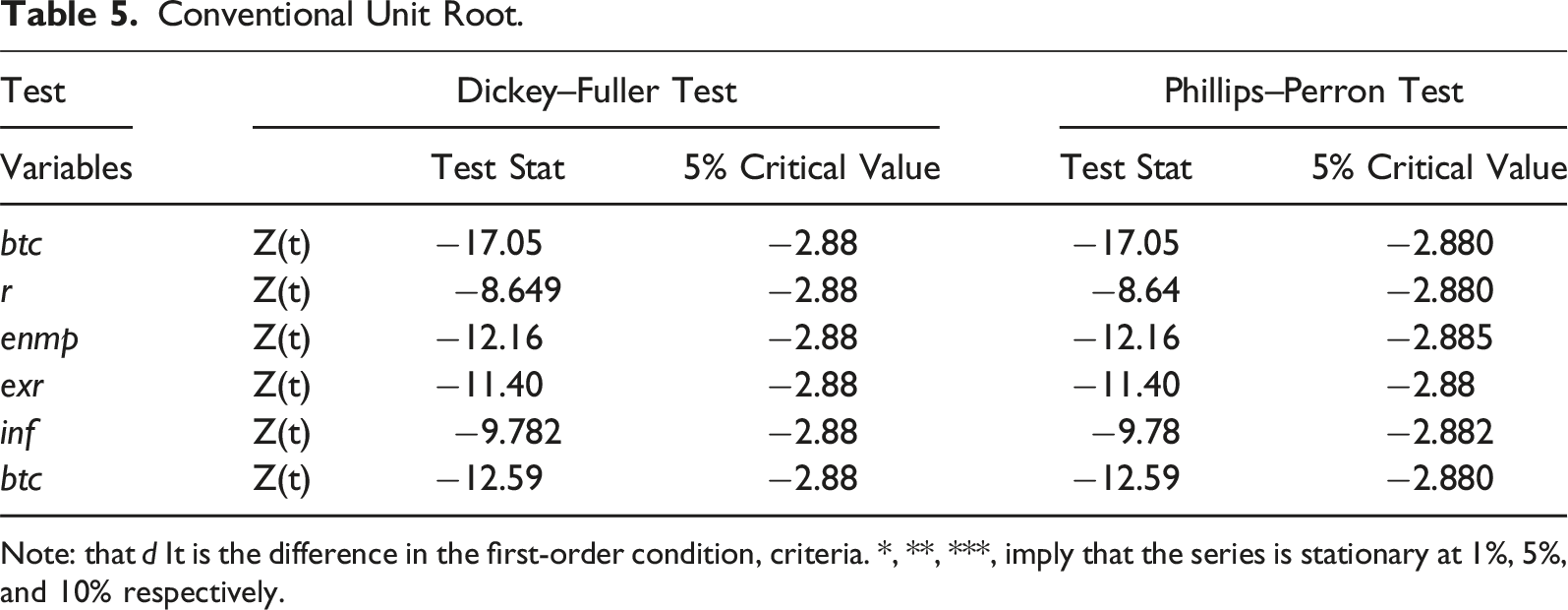

Conventional Unit Root.

Note: that

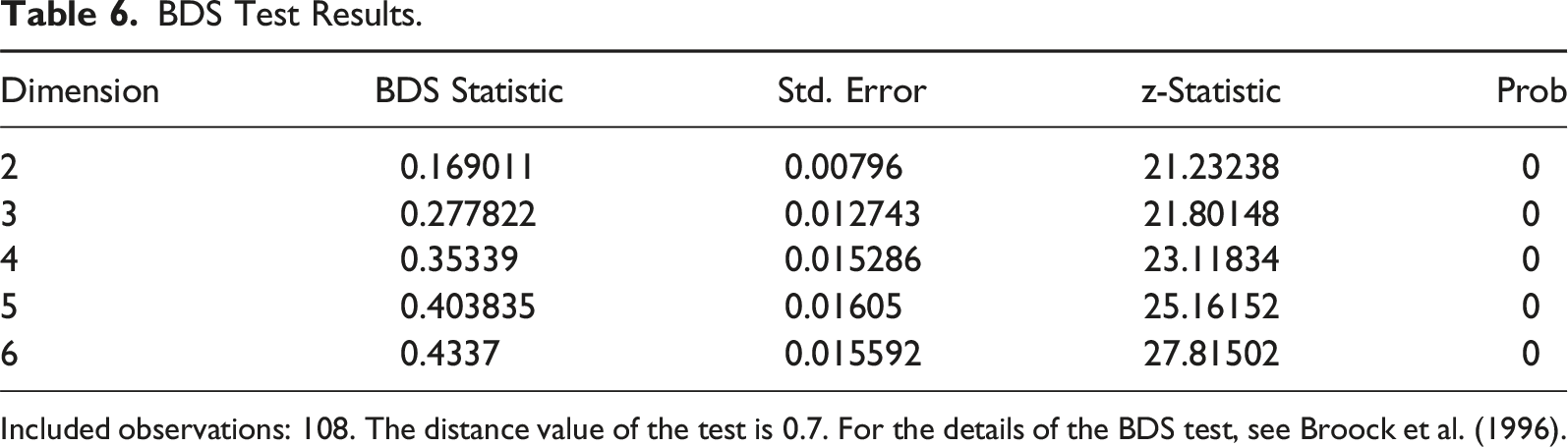

BDS Test Results.

Included observations: 108. The distance value of the test is 0.7. For the details of the BDS test, see Broock et al. (1996).

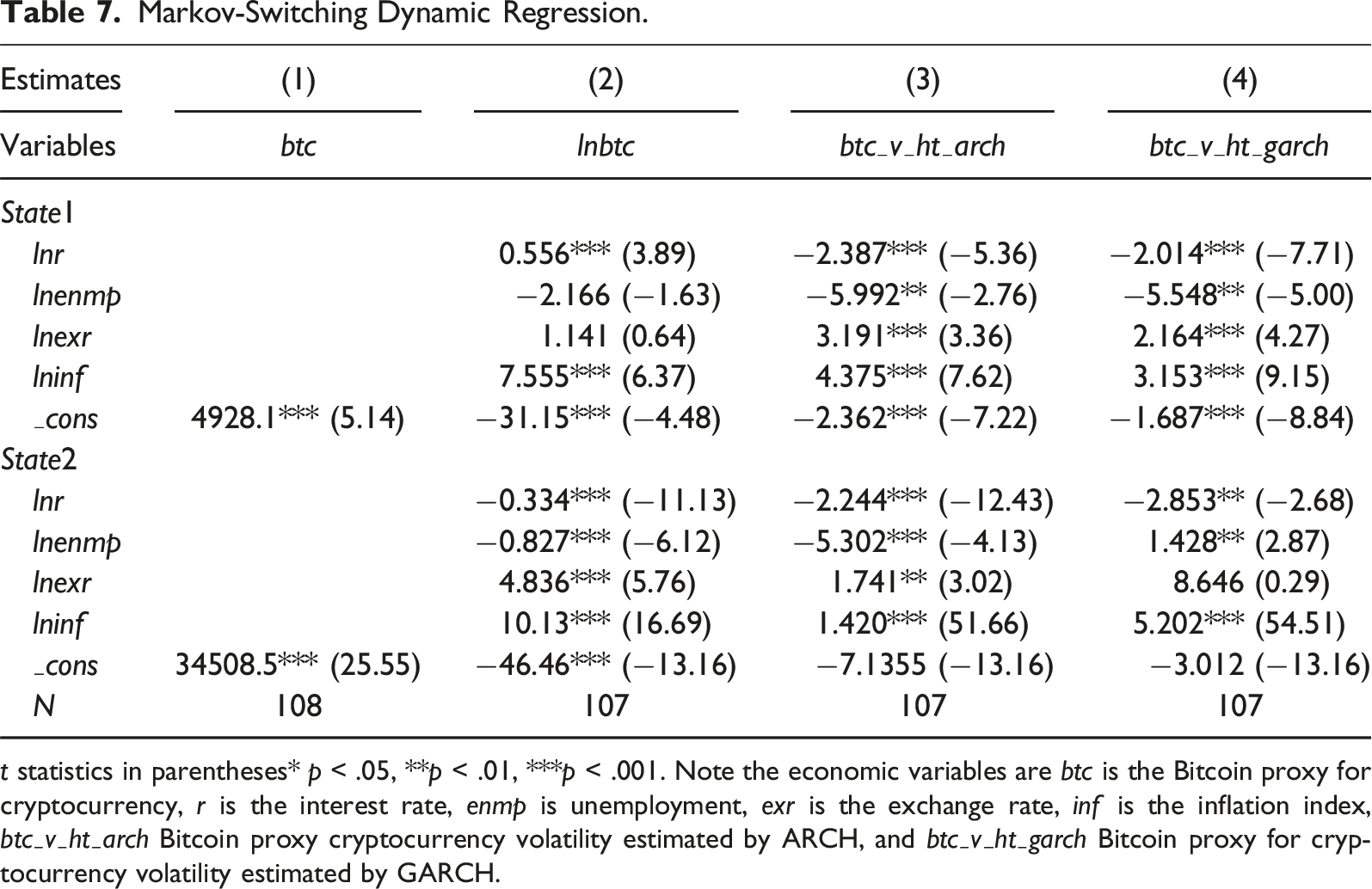

Markov-Switching Dynamic Regression.

t statistics in parentheses* p < .05, **p < .01, ***p < .001. Note the economic variables are

Estimation 3 reflects the lower state of Bitcoin prices. It was found that a one-unit increase in the interest rate is associated with a 2.387 unit decrease in the Bitcoin volatility price estimated by ARCH in State 1 and is statistically significant at the 1% level. Estimation 4 reflects the lower state of Bitcoin prices. We find that a one-unit increase in the interest rate is associated with a 2.014 unit decrease in the Bitcoin volatility price estimated by GARCH in State 1, which is statistically significant at the 1% level. This finding suggests that monetary policy measures, particularly interest rate adjustments, may be effective in stabilizing the cryptocurrency market, especially during periods of lower Bitcoin prices. These findings suggest that interest rate hikes can stabilize the cryptocurrency market during low-price states. Ma et al. (2022) noted Bitcoin price reductions following U.S. monetary tightening, while Choi and Shin (2022) observed Bitcoin’s reactions to central bank shocks. These studies show that traditional monetary policies influence digital assets like Bitcoin. This insight is crucial for policymakers aiming to reduce market instability and for investors managing cryptocurrency volatility amid changing interest rates. Estimation 2 reflects the higher state of Bitcoin prices, and it is found that a one-unit increase in the interest rate is associated with a 0.334 unit decrease in the natural logarithm of Bitcoin prices in State 2 and is highly statistically significant at the 1% level. This result is not in line with that of Corbet et al. (2020), Elsayed and Sousa (2022), and Karau (2023) among others, who reveal that monetary policy tightening leads to an increase in cryptocurrency prices. This relationship is economically meaningful and robust; investors may consider diversifying portfolios or hedging against potential Bitcoin price declines during periods of rising interest rates. In Estimation 3, reflecting the higher state of Bitcoin prices, it is found that a one-unit increase in the interest rate is associated with a 2.244 unit decrease in Bitcoin volatility price estimated by ARCH in State 2, which is statistically significant at the 1% level. Estimation 4, a one-unit increase in the interest rate, is associated with a 2.853 unit decrease in the Bitcoin volatility price estimated by GARCH in State 2, which is statistically significant at the 5% level. Investors may perceive lower volatility positively, as it implies a more stable and predictable market environment.

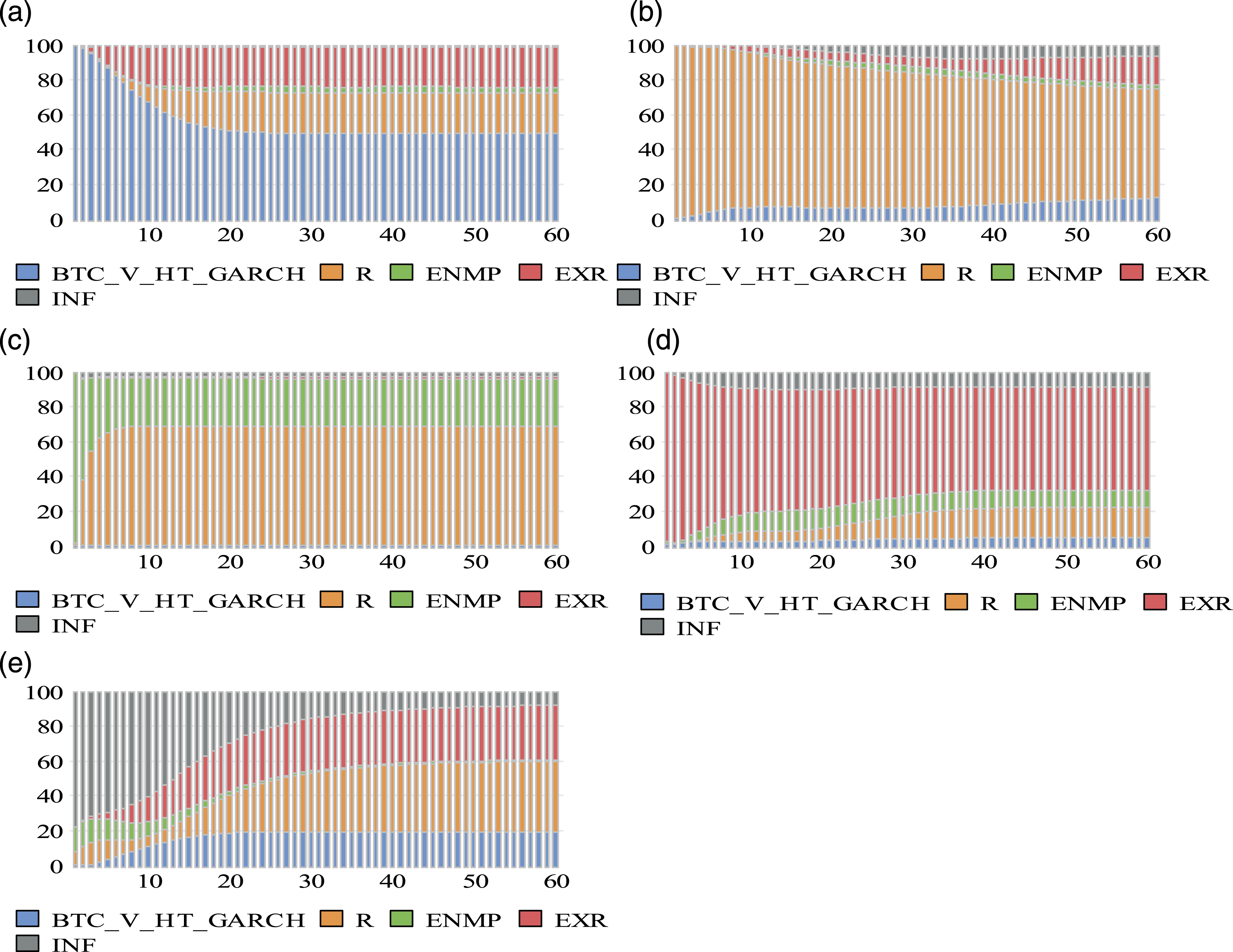

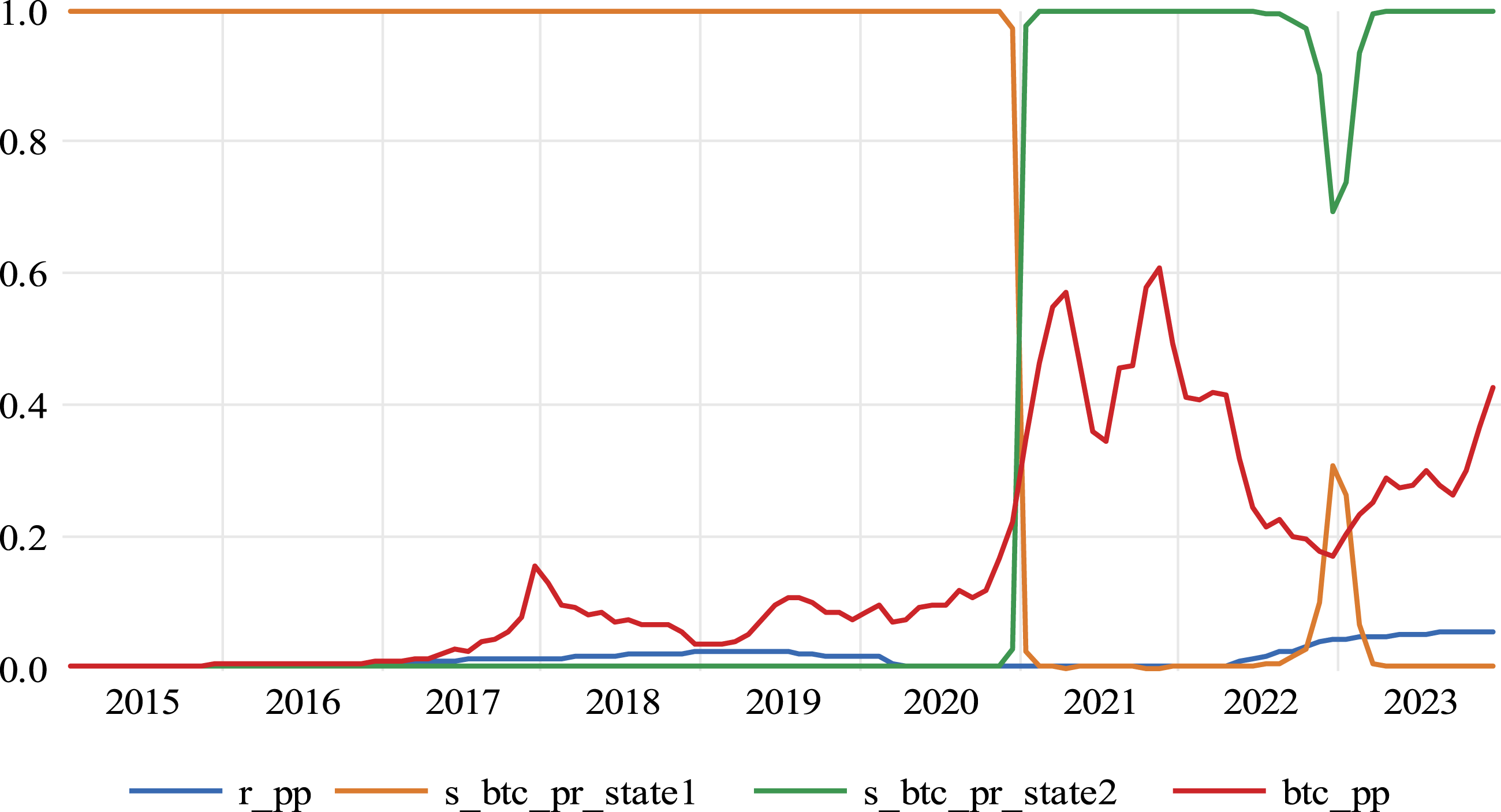

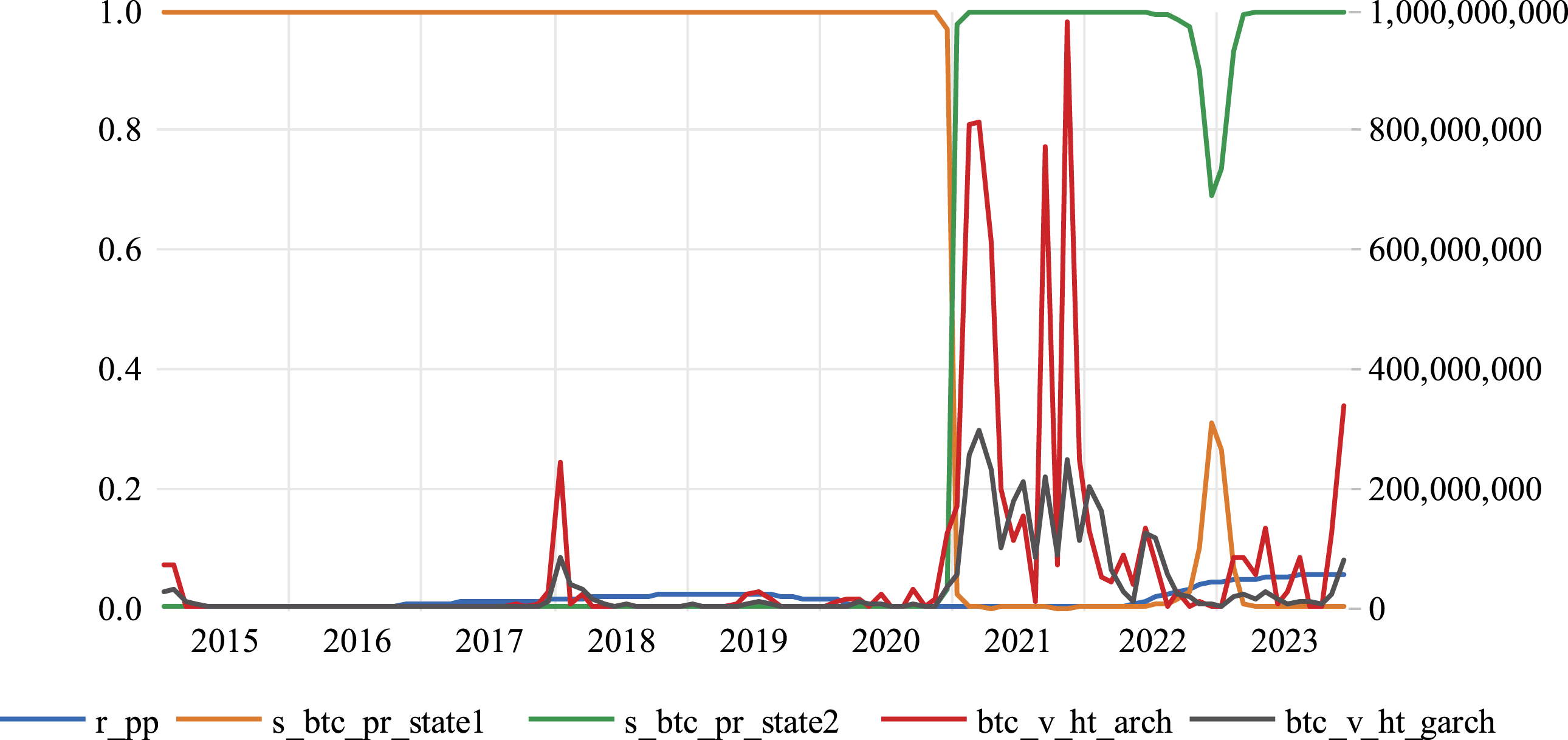

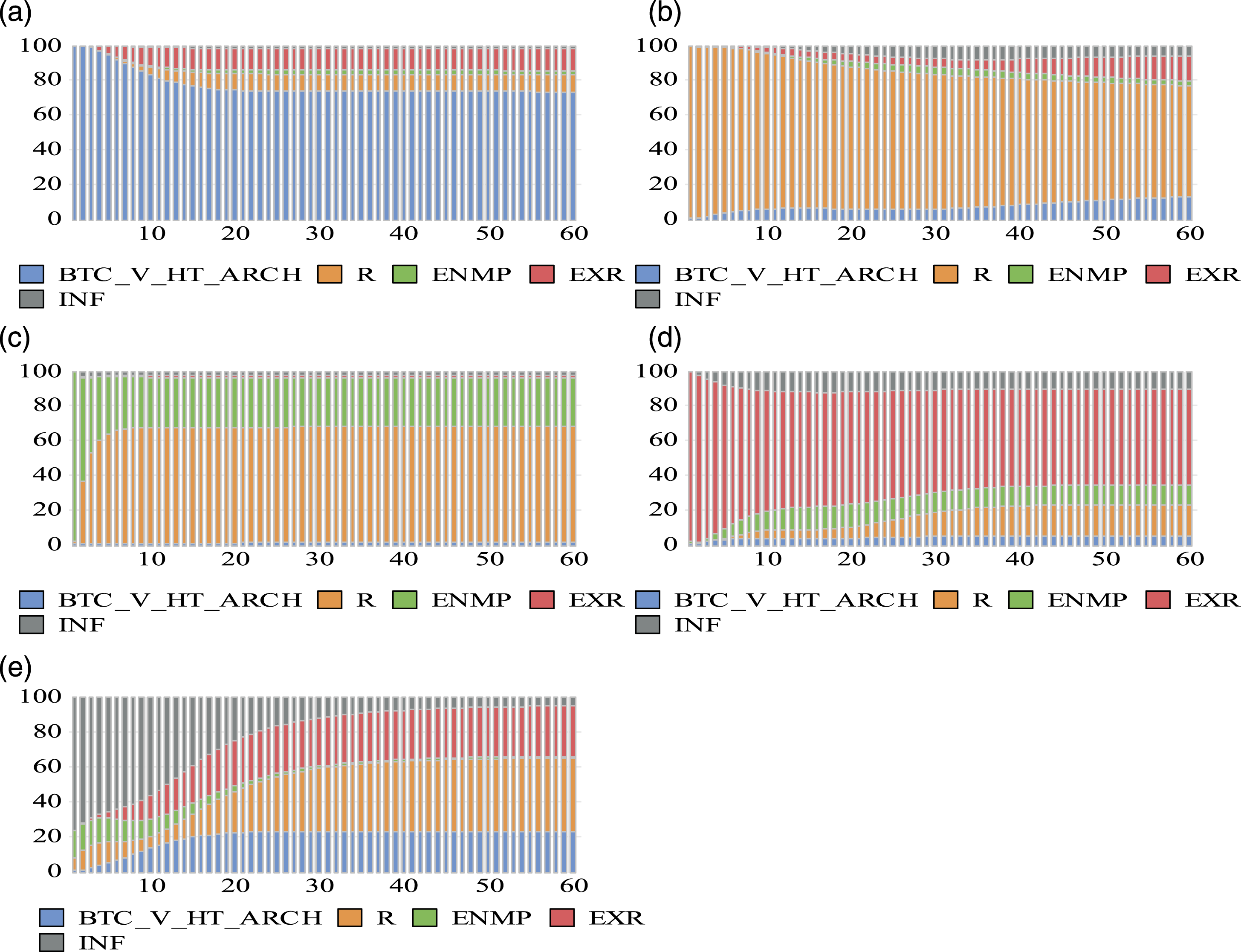

Figure 3 displays the transition probability by integrating Bitcoin prices. From 2017 to 2019, the lower Bitcoin price is correlated with an interest rate ratio that avoids the zero lower bound. This might indicate reduced confidence or heightened risk aversion, with investors perceiving Bitcoin as riskier, influencing overall market sentiment. This association implies an effective monetary policy for shaping economic conditions. By contrast, from 2021 to 2023, elevated Bitcoin prices coincide with an interest rate at the zero lower bound between late 2020 and 2021. However, Bitcoin prices and interest rates will rise in 2022. The transitional period from 2022 to 2023 exhibits weak transition probability, indicating uncertainty or indistinct market trends. The observed relationships between Bitcoin prices and interest rates can be understood through Behavioral finance which examines how psychological factors and investor sentiment influence financial markets. The correlation between lower Bitcoin prices and interest rates avoiding the zero lower bound from 2017 to 2019 suggests heightened risk aversion among investors. During this period, investors may have perceived Bitcoin as riskier, opting for safer assets amid economic uncertainties (Hirshleifer, 2015). The transition probability of including Bitcoin price.

Figure 4 provides a visual representation of the transition probabilities derived from incorporating Bitcoin volatility into the analysis. In State 1, which is typified by lower Bitcoin price levels, four distinct episodes of price deviation were identified. These episodes occurred at various points in time: one instance was observed at the conclusion of 2014, marked by lower volatility, while another occurred in 2017 amidst higher volatility. Subsequent instances took place in 2018, 2019, and 2020, all characterized by lower volatility. This variability in price behavior suggests a dynamic and fluctuating market environment within State 1. In contrast, State 2 represents periods of higher Bitcoin price levels spanning from 2021 to 2023. During this period, a notable increase in Bitcoin price volatility is evident. Specifically, heightened volatility episodes are observed in 2021, at the outset of 2022, and persisting from 2022 to 2023, albeit with moderately high volatility levels. Notably, this heightened volatility is observed despite interest rates operating at or near zero levels during this time frame. The persistence of elevated volatility levels in State 2, even in the presence of low or zero interest rates, underscores the intricate dynamics at play within the cryptocurrency market. These findings suggest that factors beyond monetary policy, such as market sentiment, technological advancements, regulatory developments, and macroeconomic conditions, significantly influence Bitcoin price volatility. The transition probability of including Bitcoin volatility.

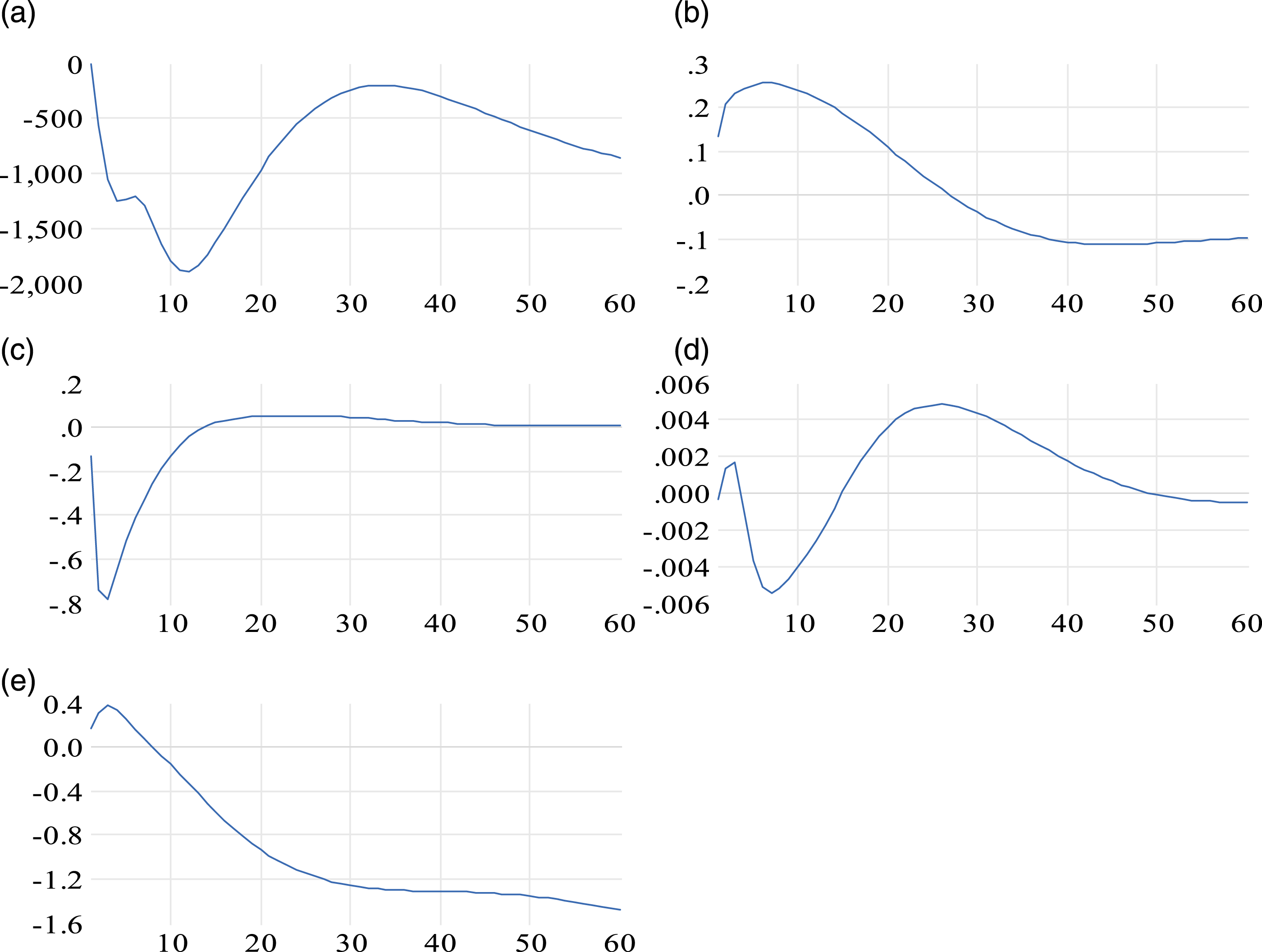

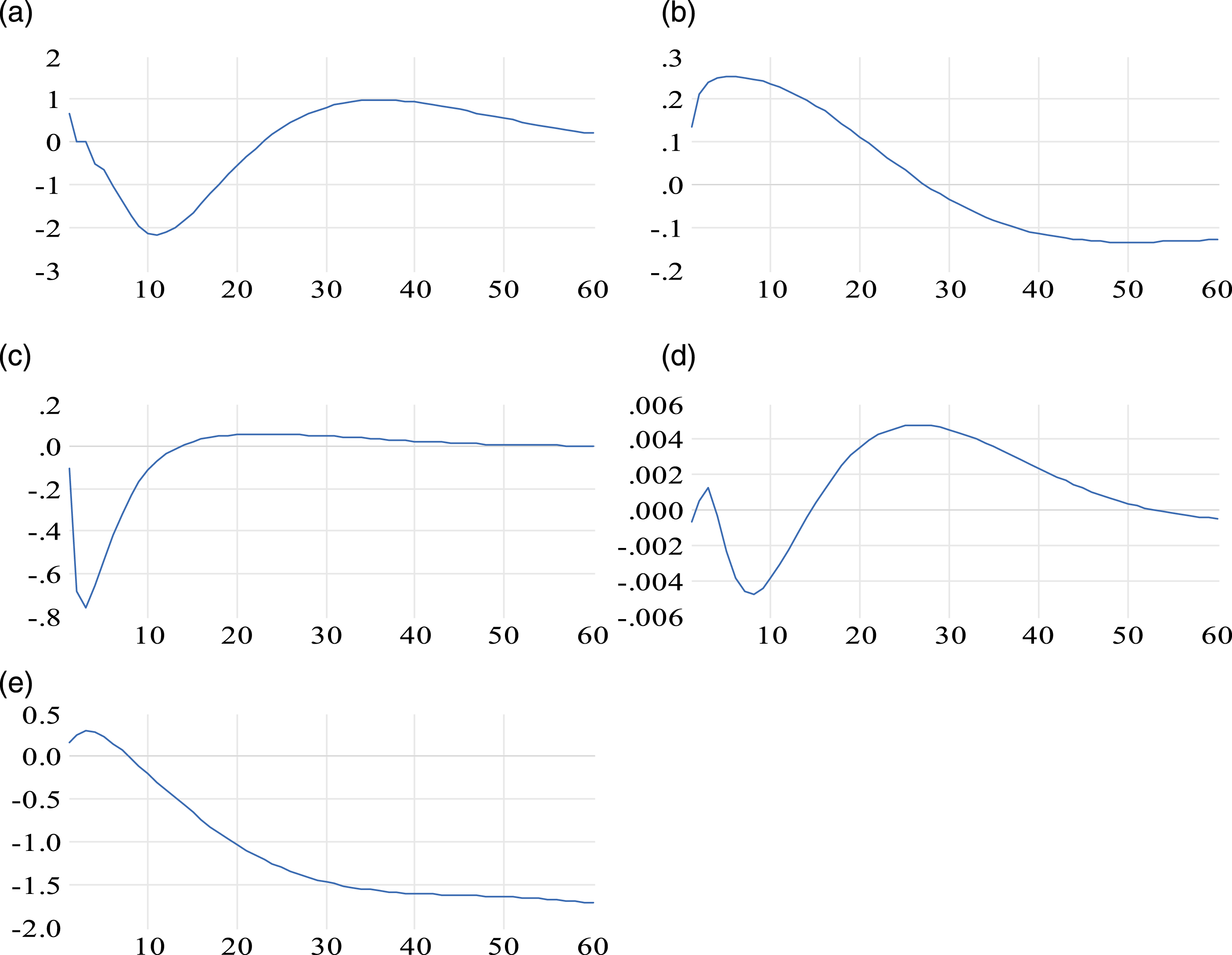

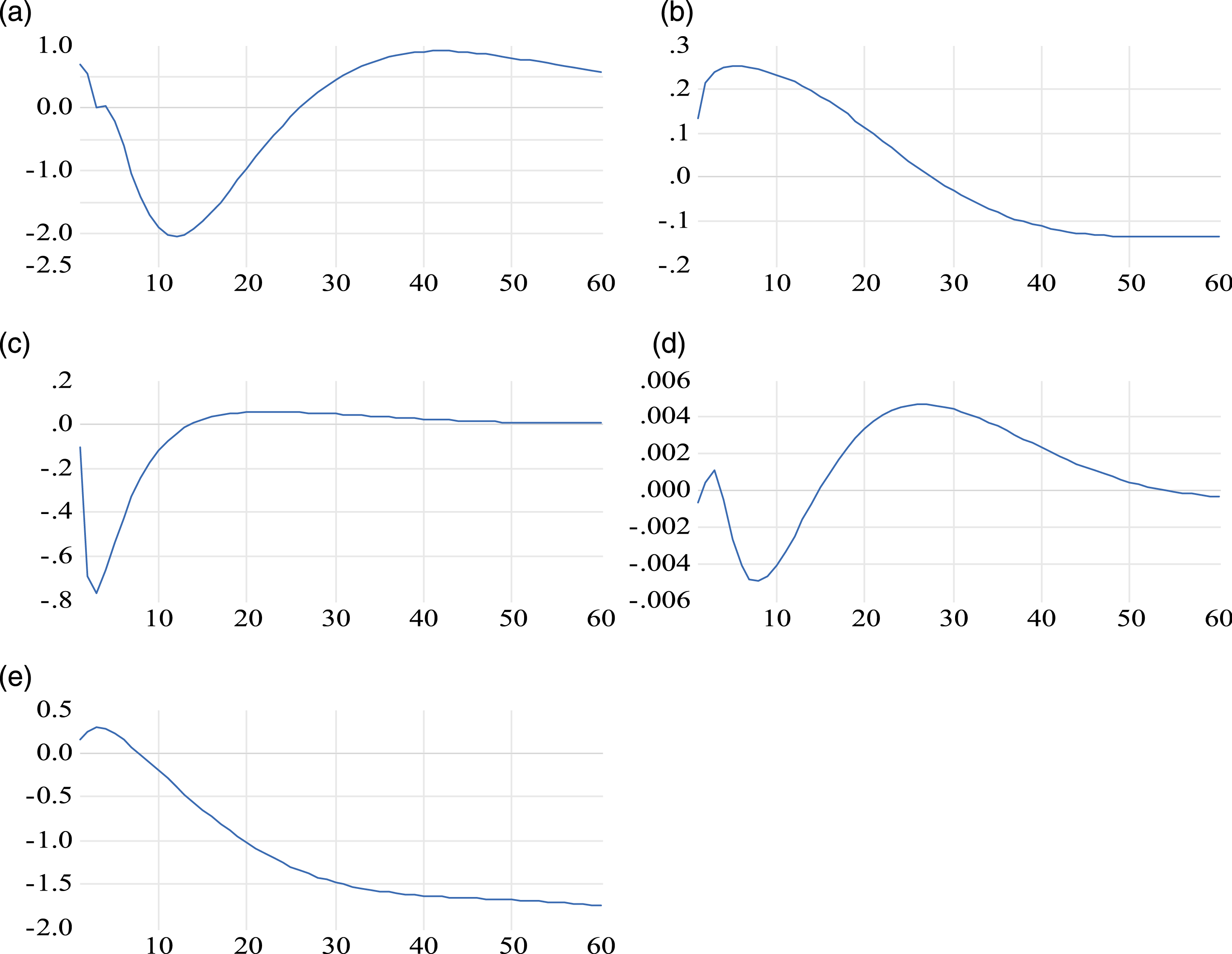

Figure 5 shows the impact of a monetary shock on the Bitcoin proxy for cryptocurrency. It was found that the impact of a monetary tightening shock, characterized by an increase in interest rates, resulted in a decline in the Bitcoin proxy for cryptocurrency during the first 10 months. Subsequently, there was a gradual recovery with a diminishing rate of increase, persisting below equilibrium until month 33. Beyond this point, the Bitcoin proxy experiences a subsequent fall. The negative response of the Bitcoin proxy to monetary tightening aligns with the notion that higher interest rates may prompt investors to shift towards traditional assets, leading to a temporary decrease in the demand for cryptocurrencies. The gradual recovery and decreasing rate of increase in the Bitcoin proxy could be indicative of a lagged response or adaptation of market participants to the changed monetary conditions. Investors can gradually reintegrate cryptocurrencies into their portfolios. The subsequent decline after month 33 may suggest that the prolonged impact of monetary tightening may eventually outweigh the initial recovery, potentially influenced by other economic factors or changes in market sentiment. Impact of monetary shock on Bitcoin proxy for cryptocurrency.

Figure 6 depicts the impact of a monetary shock on a Bitcoin proxy representing cryptocurrency volatility estimated using ARCH. The analysis highlights that a monetary tightening shock realized through an increase in the interest rate initiates a decline in the Bitcoin proxy for cryptocurrency volatility within the first 10 months. This decline implies that alterations in interest rates may influence the perceived risk or uncertainty in the cryptocurrency market. Investors interpreting a monetary tightening policy as a signal of economic stability may experience a temporary reduction in cryptocurrency volatility. Following this, the price undergoes a diminishing rate of increase until equilibrium is reached in Month 23. The observed equilibrium at this point suggests potential stabilization in the cryptocurrency market following the initial shock. The subsequent ascent, albeit at a reduced pace, continued until it reached its peak in month 35. The gradual price decrease, persistently operating above the equilibrium after the peak, implies a lingering impact on market dynamics, potentially influenced by factors beyond the initial shock. In Figure A.1, where the influence of a monetary shock on the Bitcoin proxy for cryptocurrency volatility is estimated using GARCH, a comparable pattern emerges; however, the magnitude is notably elevated. Impact of monetary shock on Bitcoin proxy for cryptocurrency volatility estimated by ARCH. Note the economic variables are

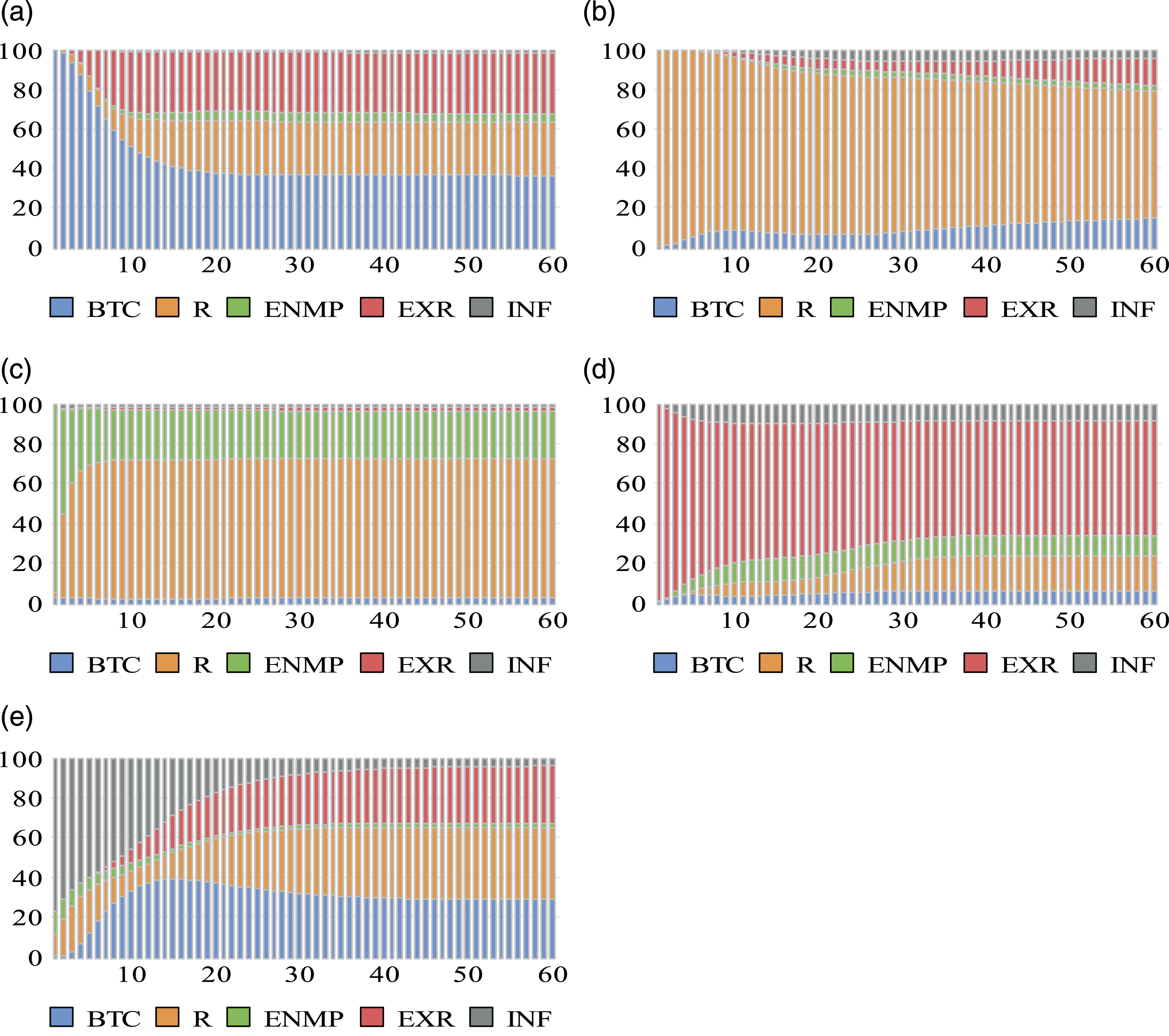

In Figure 7, the variance decomposition, utilizing Cholesky (d.f. adjusted) factors and focusing on Bitcoin prices, reveals distinct patterns. Initially, in the first month, there is a 1% variance decomposition of the interest rate’s impact on Bitcoin prices, suggesting a limited immediate effect of interest rate shocks on the cryptocurrency market. However, by the tenth month, this decomposition increased to 15%, indicating a growing influence over the medium term. Notably, from months 23 to 60, a relatively consistent 23% variance decomposition was observed, suggesting a sustained and significant influence of monetary policy decisions on shaping the dynamics of the cryptocurrency market throughout this extended period. Variance decomposition using Cholesky (d.f. adjusted) factors with a focus on Bitcoin price.

Figure 8 displays the variance decomposition employing Cholesky (d.f. adjusted) factors, with a focus on the Bitcoin proxy for cryptocurrency volatility estimated using ARCH. The analysis indicates that the variance decomposition of the interest rate effects on the Bitcoin proxy for cryptocurrency volatility estimated by ARCH is 5% in the tenth month. The initial 5% variance decomposition in the tenth month indicates a moderate immediate impact of monetary policy on cryptocurrency volatility. Monetary policy actions may have a discernible, yet not overwhelmingly significant, effect on shaping short-term volatility. Subsequently, from months 15 to 60, there is a relatively consistent 15% variance decomposition of the interest rate’s impact on the Bitcoin proxy for cryptocurrency volatility. This result are contra to that of Corbet et al. (2020) and Yang (2020) among others they don’t explicitly focused on variance decomposition, likely provide valuable insights into the relationship between monetary policy and cryptocurrency volatility. Variance decomposition using Cholesky (d.f. adjusted) factors with a focus on Bitcoin proxy cryptocurrency volatility estimated by ARCH.

This finding suggests that monetary policy, as reflected in interest rate changes, has a sustained and effective transmission mechanism in the cryptocurrency market. The enduring impact of cryptocurrency volatility reflects the importance of considering the potential spillover effects of monetary policy decisions, beyond traditional financial markets. Conversely, Figure A.2 depicts the variance decomposition employing Cholesky (d.f. adjusted) factors, centering on the Bitcoin proxy for cryptocurrency volatility estimated by GARCH. The variance decomposition in Figure A.2 is consistently 8% higher at all points than that observed in Figure A.1.

Conclusion

In conclusion, this study delves into the intricate dynamics of cryptocurrency responses to U.S. monetary policy shocks by employing sophisticated models and extensive data from 2015 to 2023. The findings reveal nuanced relationships between interest rate changes, Bitcoin prices, and volatility across different valuation states. In states with lower Bitcoin prices, a positive association between interest rates and prices is identified, suggesting a consistent impact, irrespective of the prevailing conditions. Notably, interest rate adjustments exhibit efficacy in stabilizing the cryptocurrency market during periods of low prices. Conversely, in higher price states, interest rate increases correlate with decreased Bitcoin prices and volatility, signaling potential investor strategies and market stability considerations. The impact of interest rate changes on Bitcoin prices and volatility is state-dependent. During periods of lower Bitcoin prices, increasing interest rates can stabilize the market by reducing volatility. Policymakers should consider adjusting interest rates more dynamically, considering the current state of the cryptocurrency market to optimize economic stability.

Given the influence of traditional monetary policies on digital assets like Bitcoin, there is a need for comprehensive regulatory frameworks that encompass both traditional financial instruments and cryptocurrencies. This will help manage potential spillover effects and enhance market stability. Continuous monitoring of market conditions, including Bitcoin price states, is crucial. Policymakers should use advanced analytical tools to assess market sentiment and economic indicators, enabling more informed decisions regarding interest rate adjustments. On the other hand, investors should account for the state-dependent effects of interest rate changes when making investment decisions involving Bitcoin. During periods of lower Bitcoin prices, interest rate hikes might present opportunities due to their stabilizing effects, while during higher price periods, they may need to hedge against potential price declines.

The findings underscore the need for policymakers to consider the state-dependent effects of interest rate changes on cryptocurrency markets. Understanding these dynamics can aid in crafting monetary policies that effectively mitigate market instability and protect investors, particularly during periods of significant economic uncertainty. This study confirms previous findings by Ma et al. (2022) and Choi and Shin (2022) that traditional monetary policies significantly influence Bitcoin prices and volatility. However, it complements these studies by showing that interest rate hikes can stabilize the market during low-price states, a finding not previously highlighted. The divergence from studies such as Corbet et al. (2020) and Elsayed and Sousa (2022), which found that monetary tightening could increase cryptocurrency prices, suggests that market context and investor behavior play crucial roles in determining the impact of interest rate changes. This discrepancy may be due to different market conditions or investor perceptions during the study periods.

Transition probabilities and variance decompositions illustrate the evolving nature of the relationship between interest rates and cryptocurrency dynamics. The varying impacts on Bitcoin prices and volatility over time highlight the need for a dynamic understanding of these markets. Our findings hold significant practical implications for various stakeholders, including policymakers, investors, and regulatory frameworks. Firstly, policymakers must recognize the persistent impact of interest rate changes on cryptocurrency markets when formulating monetary policy decisions. Our analysis underscores the need for a nuanced approach to monetary policy considering the increasing integration of digital assets into the global financial system. For investors, our study highlights the importance of considering cryptocurrency assets as part of diversified portfolios, particularly in response to interest rate changes and market volatility. Effective risk management strategies and a thorough understanding of the dynamics between monetary policy and cryptocurrency markets are essential for navigating this evolving landscape.

Future research in this area could explore additional factors influencing cryptocurrency market dynamics, such as regulatory developments, technological innovations, and macroeconomic indicators. Moreover, longitudinal studies tracking the evolution of cryptocurrency markets over extended periods could provide further insights into the long-term implications of monetary policy shocks on digital asset valuations. The study provides a nuanced understanding of the intricate interplay between U.S. monetary policy and cryptocurrency markets. As digital assets continue to gain prominence, it is imperative for stakeholders to consider the implications of monetary policy decisions on cryptocurrency market dynamics for informed decision-making and risk management strategies.

Footnotes

Author Contributions

I am a single author who conceived, designed, analyzed, and interpreted the data. I drafted the paper and revised it critically for intellectual content.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data used in the paper can be provided upon request.

Notes

Appendix

Impact of monetary shock on Bitcoin proxy for cryptocurrency volatility estimated by GARCH. Note the economic variables are

Variance decomposition using Cholesky (d.f. adjusted) factors with a focus on Bitcoin proxy cryptocurrency volatility estimated by GARCH. Note the economic variables are