Abstract

In a monetary economy of production, Say’s law is invalid for several reasons. Based on some refutations, it is possible to state that revenues generated by the production process are structurally lower than the supply price of production, which means that firms create insufficient purchasing power to buy what they produce. Herein, we study the dynamics of such an economy and obtain two main results. First, the long-term debt level of that economy must increase during a growth phase to enable demand to grow at the same pace as supply. Second, because of the repayment of this debt, the gap between supply and net revenues generated by the production process widens along a growth phase.

Keywords

1. Introduction

In one of his works, Jean-François Renaud (2000) discusses the possibility of the monetary realization of profits in a post-Keynesian framework and concludes that “in the absence of compensatory factors. . . the rule of a monetary economy of production is the structural inferiority of expenditures in relation to the supply price of total production and the consequent invalidation of Say’s law” (Renaud 2000: 302). According to Renaud, production fails to create a revenue, or a purchasing power, equal to its value, and external compensatory factors such as “government public deficits, trade surpluses and, to a lesser extent, consumer credit” (Renaud 2000: 302) are then required to sell the entire production.

This kind of refutation of Say’s law, based on the discrepancy between revenues and the supply price of production, has rarely been questioned by economists, apart from a few exceptions (Sismondi [1819] 1971; Malthus 1820; Denis 1999). Refutations of Say’s law rely much more frequently on the difference between revenues and demand. If we consider the latter explanation correct, then Say’s law is not valid either because of hoarding or a lack of demand for loanable funds compared to savings. In the first case, however, Say’s law is not valid because firms create insufficient purchasing power to buy what they produce. In other words, economic agents have to spend more than their revenues just to buy what they produce.

Renaud’s article is directly linked to the famous paradox of profits. According to this paradox, which has generated an abundance of literature (Rochon 2005, 2009; Zazzaro 2003; Zezza 2012), it is difficult to explain how firms can make monetary profits based on the expenses they have incurred to initiate their production process. However, other research contributions have been made to explain the existence of a gap between revenues and the supply price of production. According to Cottin-Euziol and Rochon (2013) and Cottin-Euziol and Piluso (2021), the repayment of the principal of past bank credits used to finance investments represents a cost for firms generating no revenues and can explain the existence of a gap between revenues and the supply price of production. Another refutation can be linked to the work of Le Héron and Cottin-Euziol (2021), which examines how firms finance their working capital on their profits rather than by short-term bank credits. In both cases, revenues are insufficient to buy the entire production of an economy.

Herein, we explore this issue along two lines. First, we combine the different explanations above, which has to our knowledge not yet been done. Second, we study the dynamics of an economy in which economic agents have to go into debt just to buy what they produce because the revenues issued by the production process are insufficient. This action should lead to high global debts, both public and private, after a certain period of time and, consequently, increased fragility of the economy. Afterward, we consider whether the results of this study can explain some global patterns regarding the indebtedness of modern economies.

For this purpose, section 2 reconsiders the meaning of Say’s law, and section 3 deals with the notion of a monetary economy of production, which forms the framework of the refutations of Say’s law mentioned above. In section 4, we discuss these different refutations based on the discrepancy between revenues and demand. Section 5 presents a very simple model based on these refutations, which aims to represent the functioning of an economy wherein revenues are lower than the supply price of production. In sections 6 and 7, we study, respectively, the evolution of the long-term debt and the gap between net revenues and supply, according to the model presented in section 5. Finally, we offer conclusions in section 8.

2. Say’s Law

Since its enunciation (Say [1803] 2006), the validity of Say’s law has been the subject of numerous debates (Sowell 1972). It remains the central pillar of the neoclassical theory and is an unrealistic construction according to most heterodox schools of thought. The basic idea behind Say’s law is simple: there is an equivalence between the incomes generated by the production process and the supply price of the goods produced. These revenues are either spent or saved, but savings will be invested and are thus also spent. Therefore, the level of demand cannot be lower than the level of supply in an economy, so aggregate overproduction is impossible, even on a temporary basis. Since overproduction can only be sector-specific, the solution to overproduction is not to increase the level of demand but to increase the level of production. As Say illustrates, “When a nation has too many products of one kind, the means of disposing of them is to create another kind” (Sowell 1972: 20).

This law has subsequently occupied a central place in the history of economic thought: The idea that supply creates its own demand—Say’s Law—appears on the surface to be one of the simplest propositions in economics, and one which should be readily proved or disproved. Yet this doctrine has produced two of the most sweeping, bitter, and long-lasting controversies in the history of economics, first in the early nineteenth century and then erupting again a hundred years later in the Keynesian revolution of the 1930s. Each of these outbursts of controversy lasted more than twenty years, involved almost every noted economist of the time, and had repercussions on basic economic theory, methodology, and sociopolitical policy. (Sowell 1972: 3)

Say’s law can be considered as an equality with two core propositions. The first proposition is that production (Y) creates revenues (R) equal to the value of the former. In this case, if all the revenues are spent, the production will be entirely sold. This first equality is generally not questioned by most classical authors. As Renaud (2000: 290) points out, “It is repeated not only by Marx in his demonstration of simple and extended reproduction, but also by Keynes (1936).” However, Sismondi ([1819] 1971) and Malthus (1820) supported the idea that capitalist economies could suffer from a chronic insufficiency of revenues and require supplementary expenditures. The second proposition is that if expenditure (D) is equal to revenues, it will allow the sale of the entire production. Based on this proposition, several criticisms of Say’s law have been formulated. According to these criticisms, revenues are sufficient to buy the entire production, but part of these revenues will be hoarded, preventing the sale of the totality of the production. Overproduction is then not a matter of insufficient revenues in relation to the value of production but of insufficient demand in relation to revenues.

In this article, we focus on refutations of Say’s law based on the discrepancy between revenues and production. To do so, we bring together some recent refutations of this law that have been developed within the framework of a monetary economy of production. Then, we build an economic model in which revenues are structurally lower than the value of production; to our knowledge, such an approach has not yet been adopted.

3. The Main Features of a Monetary Economy of Production

In the 1930s, Keynes called for the development of a monetary theory of production, as opposed to the real exchange economy built by classical economists (Keynes 1930, 1937a, 1937b). Such a framework was for him necessary to understand macroeconomic dynamics and imbalances. Afterward, mainly post-Keynesian economists developed his project (Graziani 2003; Rochon and Seccareccia 2013). Based on their work, we can distinguish three main principles that form the foundation of a monetary theory of production. The first principle is the essentiality of money; the second refers to endogenous money; and the third to debt-money. In this section, we return successively to these three principles.

According to the essentiality of money principle (Parguez 2003), money is not only a medium of exchange but also, and above all else, an essential condition for the realization of production. Taking its roots in Keynes’s A Treatise on Money (Keynes 1930) and in the finance motive (Keynes 1937a, 1937b), this principle explains that firms need an access to money in order to trigger their production process. The focus is thus placed on the desire to spend money rather than to hold it. Money is not only regarded as a stock but also as a flow necessary for the financing of production (Wray 2003). This principle is closely related to the one of real or historical time. Indeed, firms need money to produce because the process of production takes time and precedes the selling of goods (Lavoie 2014; Rochon 1999).

The second principle is the endogenous nature of money. This notion, developed by—among others—Robinson (1956), Kaldor (1970), and Moore (1988), states that the quantity of money is mainly determined by the issue of bank assets for creditworthy agents. Money is then detached from any reference to a standard, and banks can grant credit theoretically without any limitation, obtaining afterward the reserves required by the law. It is assumed here that there is an institutional mechanism in place to allow this endogenous monetization of bank reserves to occur. This feature does not mean that the access to bank credits cannot be constrained, but rather that their scarcity cannot be explained by limits in the emission of money, 1 as was the case, for example, under the gold standard system. According to the above cited authors, interest rates are exogenous and no longer natural.

The third principle is that the main counterpart of money is represented by credits offered by financial institutions to firms, states, and households. As Rochon states (2003: 123), “Capitalist economies are debt economies: production cannot be separated from the discussion over credit, bank and debt.” Economic actors will then have to repay borrowed sums to banks, leading to a destruction of money. The functioning of economies is therefore characterized by the flux and reflux of money, mainly from banks to firms and firms to banks. This principle is at the core of the monetary circuit theory (Graziani 1990, 2003; Piégay and Rochon 2003; Rochon 2009) and stock-flow consistent models (Godley and Lavoie 2007).

Combining these three notions, we construct the description of an economy in which money is necessary for production, is endogenous, and relies on the issue of bank credits. In such an economy, the supply price of production, revenues, and expenditures are not necessarily identical. Indeed, several refutations of Say’s law have been formulated within this framework to explain how revenues can be lower than the supply price of production in an economy. We explore these refutations in the next section using a theory that fits well into this framework: the monetary circuit theory. We use this theory rather than stock-flow consistent models (cited above) because we believe that the more sequential nature of the former makes it easier to set out these refutations of Say’s law.

4. Refutations of Say’s Law in a Monetary Economy of Production: The Case of the Monetary Circuit Theory

In this section, we present different refutations of Say’s law in the context of a monetary economy of production in which overproduction can be explained by a lack of revenues generated by the production process. More precisely, we study these different refutations within the framework of the monetary circuit theory, as explained in the previous section. First, we briefly present the monetary circuit theory, and then discuss different refutations of Say’s law within this framework.

The monetary circuit theory fits well into the framework of a monetary economy of production. Money, or rather bank credit, represents an essential precondition for the production process to take place. As Lavoie posits, “Firms cannot produce without having access to monetary advances from banks” (1987: 68; our translation). Moreover, money is endogenous and relies on credits issued by the banking system. These credits will then be repaid by firms after the sale of their production (for a summary, see Cottin-Euziol and Rochon 2022). This theory highlights the fact that money, production, and debts are intrinsically linked. As Seccareccia (1988: 51) claims, production is a “process of debt formation.”

Monetary circuit models are made up of four phases that correspond to the period between the creation and the destruction of money (figure 1): (1) firms first ask for bank advances to finance their production expenditures and then start production; (2) while producing, firms pay wages, leading to a new monetary flow from firms to households; (3) households then begin spending and consuming goods, so money returns to firms as they sell their products to consumers; and (4) firms repay debt to banks. In doing so, money is destroyed, and this ends a period of the monetary circuit.

The four phases of the monetary circuit.

In this framework, we now wonder whether firms can generate enough revenues to sell their entire production with a given margin.

A first refutation of Say’s law in this framework relates to the noninjection by firms of the sums allowing them to make profits. This refutation relies historically on the work of Sismondi ([1819] 1971) and Malthus (1820) and is directly linked to recent debates among post-Keynesian economists about the monetary origin of profit (Renaud 2000; Rochon 2005, 2009; Zazzaro 2003; Zezza 2012). After trying to answer this question, Renaud (2000) concludes, as quoted in the introduction, that capitalism might suffer a “structural inferiority of expenditures in relation to the supply price of total production” (302). To understand this statement, let us consider figure 2. In this figure, firms ask for a monetary advance (W) from banks to finance their current production expenditures, generating similar revenues for households. Households will then consume on these revenues. The following question then arises: how can firms make profits based on the credits they have taken out to initiate their production process? Even if households consume the totality of their revenues, firms can then just be able to recover their production costs and repay the monetary advances to banks.

The profit puzzle.

Two main types of solutions have been envisaged to resolve this paradox. The first one assumes the existence of numerous phases of flow and reflux within the period (Renaud 2000; Zezza 2012). Firms and banks will immediately spend and inject back into circulation the profits and interests they started to collect. These injections can then enable them to sell their entire production with a given margin. The second solution assumes that credits can be issued over several periods and therefore do not have to be fully repaid within the period considered (Cottin-Euziol and Rochon 2013; Rochon 2009). However, in both cases, according to Renaud (2000: 301), “in the real world, the conditions for this realization [of profits] can only be satisfied accidentally.” Revenues and expenditure are then likely to be lower than the supply price of production.

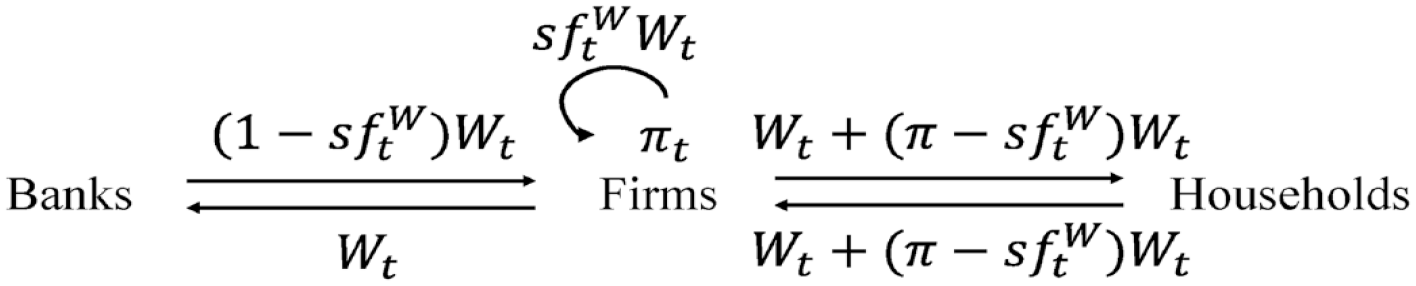

Another possible answer is provided by considering that firms generally start a period with the profits made during the previous period, as shown in figure 3. Subsequently, spending on these profits will enable firms to make new profits. To simplify, we assume that banks do not receive interest on the credits granted, profits are entirely distributed to households, and households consume the totality of their revenues. As a result, firms will then make profits that are equal to the difference between their receipts and the production costs:

The profits puzzle with the spending of past profits.

Thus, the profits of firms within a given period will be equal to their profits from the previous period. Firms can both repay the monetary advances to banks and make profits. However, the limits of such an approach are immediately evident. It would mean that, in a growing economy, the amount of profit would stay unmodified. Thus, this explanation cannot account for the existence of increasing profits. Mathematically, for a given growth rate of the economy (g) and assuming that production is sold by firms with a constant margin (m) across periods, the revenues generated by firms within a period (

On the other side, the supply price of production during this period is assumed to be:

Revenues are thus lower than the supply price of production:

In this case, even if all the revenues injected within the monetary circuit are spent, the resulting demand is lower than the supply price of production. Denis (1997, 1999) has proposed a refutation of Say’s law based on this argument. Revenues are therefore insufficient to buy the whole production, even in the absence of savings.

Next, we consider other cases for which the revenues generated by the production process can be lower than the supply price of production. To understand this aspect, we need to go back to the previous figure, and we now assume that firms can sell their production with a given margin in each period based on the monetary advances financing their current production expenditures as well as the spending of their profits. However, even in this case, the revenues generated by the production process can be lower than the supply price of production.

This result can be the case if firms decide to use their profits to self-finance a part of their current production expenditures. The idea is that, at the beginning of each period, firms will not simply borrow the sums necessary to finance their production expenditures. This action can make them too dependent on banks. If a bank, for example, refuses to grant the corresponding monetary advances, the company will lack the liquidity to continue its activity and will find itself in default of payment. It is therefore in a company’s interest to finance its current production expenses with its own funds.

Firms will therefore devote part of their profits to finance current production expenses, which means that, instead of financing the totality of their production expenditures by monetary advances from banks, firms will gradually finance these expenses out of their own profits. Let us assume that firms devote a part (

Say’s law and self-financing of firms’ production expenditures.

On the other hand, the supply price of production during this period is supposed to remain the same as in equation (3). Thus, in this case, revenues are once again lower than the supply price of production:

This refutation can be linked to the work of Le Héron and Cottin-Euziol (2021), who studied different ways of financing current production expenditures in a stock-flow consistent model. If firms use their profits partly to finance their current production expenditures, then the level of global demand and firms’ profits will decrease because in financing part of their production expenses on profits, firms substitute short-term bank credits by spending on their profits. The sums used to self-finance production expenses will then reduce the other expenses on profits. This method of financing current production expenses is completely rational from a microeconomic point of view but can lead to a decrease of global revenues on a macroeconomic scale.

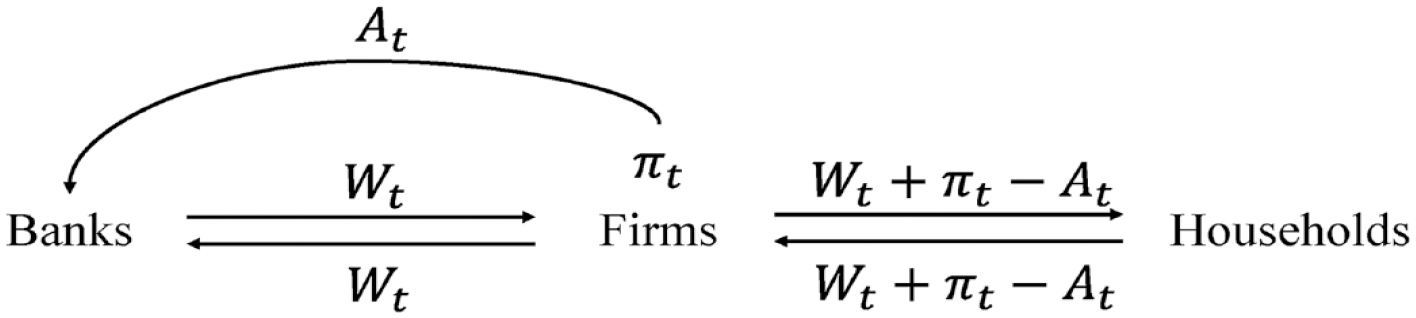

Finally, a third refutation of Say’s law is based on the repayment of long-term bank credits. Bank credits issued during a given period have to be repaid during the following periods, which means that firms have to devote part of their revenues to make these repayments. Repayments thus reduce profits as well as the level of revenues and demand in the economy. Indeed, repayments represent an expense, but the repayment of the bank loan principal does not generate any income since it leads to the disappearance of the corresponding credit line. The repayment of bank loan principal can then be seen as a non-revenue-generating cost (Barrère 1990). Loan repayments can therefore create a mismatch between the value at which firms wish to sell their production and the level of revenues. Although long-term bank credits have increased demand in the past, they will decrease it in the future when these loans have to be repaid. The repayment of past bank credits will then modify the dynamics of the economy, as has been highlighted in some recent studies (Cottin-Euziol 2015; Cottin-Euziol and Piluso 2021; Cottin-Euziol and Rochon 2013). If the amount of repayment is denoted as A, and assuming that firms make these repayments on their profits, we obtain the situation shown in figure 5. In this case, revenues generated by firms during the production process can be expressed as follows:

Say’s law and the repayment of past bank credits.

However, the supply price of production is still the same (equation 3). Revenues generated by the production process will then also be lower than the supply price of production:

These different refutations can explain why revenues can be structurally lower than the supply price of production in a monetary economy of production. We note that these refutations are valid because we are considering a monetary economy. Indeed, in a nonmonetary economy in which production costs are paid in kind and profits are made in kind, none of these refutations are valid. In the next section, we present a simple model that takes these refutations into account.

5. A Simple Representation of a Monetary Economy of Production

In the previous section, we provided some reasons why revenues can be lower than the supply price of production in a monetary economy of production. If these explanations are correct, then economies should suffer chronic overproduction and firms will accumulate more unsold goods or underused capital regardless of their decisions on production. However, economies do not behave that way. This phenomenon can only be explained in a closed economy if expenditures exceed revenues as a result of the issue of medium- or long-term bank credits. For example, governments can implement a budget deficit, which will increase global demand and profits (Kalecki 1943). Firms and households also have access to bank credits to increase their spending over their income. These different elements will contribute to increasing the level of demand in the economy. Money created by bank credit plays a crucial role here because it is the only way in a closed economy to add purchasing power to that created by firms while producing.

According to the above considerations, a monetary economy of production can be described as a system in which the revenues generated by production, and thus the demand resulting from these revenues, are structurally lower than the supply price of production. Nevertheless, such an economy does not face chronic overproduction because medium- and long-term bank credits issued in response to financing the investments of firms—or the requirements of households and states—can also increase the level of demand. If these credits are sufficient, the whole production can be sold, and all the factors of production can be used.

We illustrate this simple representation of a monetary economy of production in equations (9) and (10) below. Because of the refutations of Say’s law mentioned above, we consider a structural gap (x) between revenues (R) and the supply price of production (Y). Revenues generated by production are therefore structurally lower than the supply price of production. However, the level of demand (D) can reach the supply price of production if enough medium- and long-term bank credits (BC) are issued to finance the investments of firms or the requirements of households and states:

As long as these bank credits are sufficient to enable the demand to grow at the same pace as global supply, firms will not have unsold goods. Production and investment decisions are then likely to maintain at a high level. Conversely, if these bank credits are not sufficient, firms will be left with unsold goods, which will affect their future decisions of production and investment.

To complete this representation, we need to consider the repayments of these long-term bank credits. Indeed, bank credits issued during a period to fill the gap between demand and supply will have to be repaid during subsequent periods. These repayments may therefore increase this gap in the future by decreasing revenues and the level of demand, as explained in the previous section. More bank credits will then have to be issued in the future to counterbalance these repayments, thereby leading to more repayments, which will modify the dynamics of the economy.

More precisely, the repayment of a bank credit comprises two parts: the interest, which forms the bank’s revenues, and the principal, which eliminates the corresponding credit line. The interest paid represents the bank’s earnings, so it cannot be regarded here as an outflow. On the contrary, the principal repayment of past bank credits reduces the money stock and constitutes an outflow outside the economic circuit. Such repayments will therefore decrease the level of demand and increase the gap between demand and supply. By considering capital repayments (A), we obtain two new equations, (11) and (12). In equation (11), net revenues

In equation (12), net demand (

The volume of repayments within a period depends on the volume of bank credits issued during the previous periods:

Equation (12) can then be rewritten as follows:

This equation provides a simple representation of the dynamics of a monetary economy of production. Long-term bank debts are necessary to enable the selling of the entire production. However, debt repayments tend to increase the gap between global demand and the supply price of production in the future. Using this equation, we focus in the next section on the required level of long-term bank debt in such an economy. In section 7, we discuss the evolution of the structural gap between revenues and supply throughout a growth phase, as it applies to considering the repayment of past bank credits.

6. The Required Level of Long-term Debt in a Monetary Economy of Production

In the previous section, we considered a monetary economy of production in which revenues are insufficient to enable the selling of the entire production. Nevertheless, long-term bank credits issued in response to the financing requirement of firms, households, and states can increase the level of demand arising from these revenues and enable it to reach the value of production. In this section, we explore how these financing requirements—and hence the level of long-term debt in a monetary economy of production—can evolve during a growth phase.

To determine this level of long-term debt, we need to calculate the volume of money that has to be injected throughout the periods to fill the structural gap between revenues and the supply price of production. To simplify the analysis, by assuming a constant gap between the two, we can rewrite equation (9) as follows:

The amount of long-term bank credits that has to be issued within each period to fill this gap then becomes the following:

Starting from an initial period 0, we can determine the required amount of long-term bank debt (B) in this economy for a given period. This debt corresponds to the sum of all the injections of long-term bank credits required to fill the structural gap between revenues and supply from period 0 to the current period, as presented in equation (17):

Assuming a constant growth rate (g) of supply, we obtain the following geometric series:

Using the formula of the sums of terms of a geometric series, we can compute the value of such a series:

For a long enough period of time, we can determine the ratio of long-term bank debt to supply required to balance revenues and the supply price of production. This ratio gives us the level of indebtedness of the economy:

According to this equation, the amount of long-term debt in such a monetary economy of production will depend mostly on the structural gap between revenues and supply, as well as on the growth rate of the economy. It can reach high values, showing that a monetary economy of production can be highly leveraged. For example, if the structural gap between revenues and supply is identical to the growth rate of the economy, the quantity of long-term debt would have to reach more than 100 percent of the value of production to enable revenues to grow at the same pace as supply. To give a numerical example, if the nominal growth rate of the economy is about 3 percent and revenues within each period represent 97 percent of the supply price of production, then it would be necessary to have a long-term debt representing about 100 percent of the supply price of production. With a lower growth rate or a larger structural gap between revenues and the supply value of production, this long-term debt could reach much higher values. This result can help us understand why economies today rely on such high debt to GDP ratios.

It is important to note that by no means does this quantity of debt mean that people in this economy live beyond their means. Indeed, just considering a closed economy, society cannot as a whole consume more than it has produced. The debt simply reflects the fact that monetary injections are necessary—beyond the short-term injections made by firms to finance their production costs—in order to fill the gap between revenues and supply.

7. The Evolution of the Structural Gap between Revenues and Supply throughout a Growth Phase

We consider here the consequences of the repayments of long-term debt on the gap between net revenues and supply. As explained in the previous section, debt repayments will reduce revenues in the economy, and hence the level of demand. More long-term bank credits will then have to be issued within a given period to offset the repayment of long-term bank credits issued in the past. In our study, net revenues refer to the level of revenues generated by the production process minus the volume of repayments. We investigate here how these repayments might modify revenues and the gap between net revenues and global supply throughout a growth phase.

For this purpose, we first incorporate equation (13) into equation (11), while assuming, as in the previous section, a constant structural gap between revenues and supply. We thus obtain the following equation:

As previously stated, we assume a constant growth rate of supply. By considering the results obtained in the last section, equation (21) can be used to express the volume of long-term bank credits as a function of the value of global supply:

As proposed by Rochon (2009) in the framework of a single period model, let us assume that a part

We can then determine the value of the ratio of net revenues to global supply:

This ratio gives us the gap between the level of net revenues and supply within a period t. Therefore, it reflects the amount of long-term bank credits that needs to be granted within a period t to enable global demand to reach the supply price of production. This gap between net revenues and supply will increase for higher values of the structural gap (x) and repayment rate

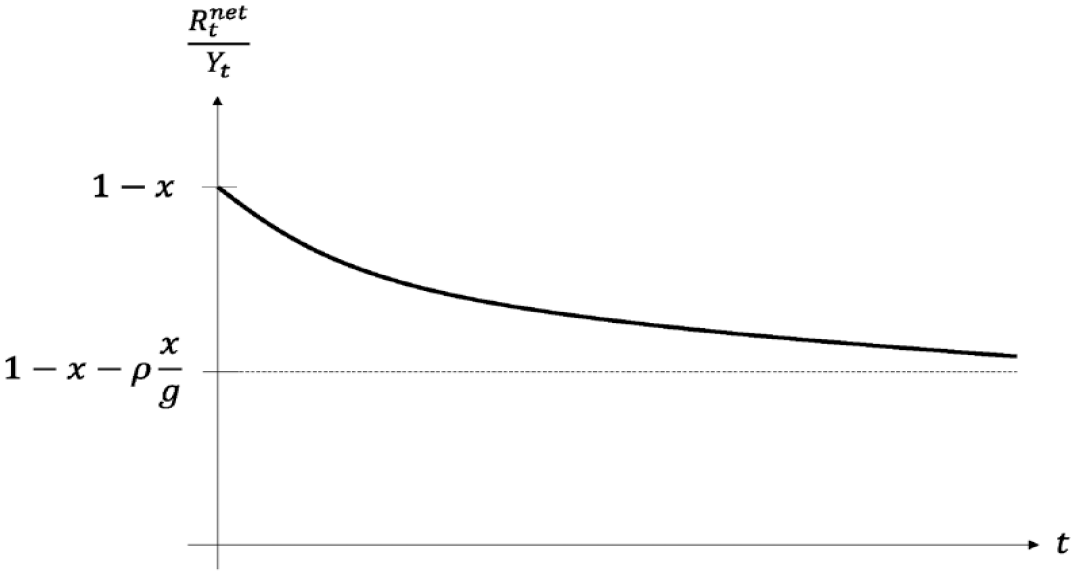

We can now draw a curve (figure 6) showing the evolution of the ratio of net revenues to global supply throughout a growth phase. For the hypothetical period 0, it will depend on the structural gap between supply and demand. It will then decrease due to the repayment of past bank credits until it reaches the threshold value of

Evolution of the ratio of net revenues to global supply throughout a growth phase.

The main result of this study is that the ratio of net revenues to global supply decreases throughout a growth phase. For example, if the structural gap between revenues and the supply price of production corresponds to 3 percent, assuming the growth rate of the economy is about 3 percent and that 10 percent of the global debt is repaid every year, then the level of net revenues will decrease progressively until it represents 87 percent of the value of production.

This process can be explained by the depressive effect of the repayment of long-term bank credits on revenues. Although bank credits filled the gap between revenues and supply in the past, they will increase this gap in the future, which means that more and more bank credits—in relation to the level of global supply—will have to be issued during a growth phase to enable the selling of the whole production, thereby leading to more and more repayments. In other words, it becomes more and more difficult to maintain a balanced growth between revenues and the supply price of production throughout a growth phase because of the natural fall in net revenues and increasing indebtedness. Such a result therefore helps us understand why economies often face overproduction crises after several years of growth.

8. Conclusion

In The General Theory of Employment, Interest and Money (hereafter General Theory), Keynes (1936) regarded Say’s law as the classical theory’s axiom of parallels and suggested building a non-Euclidean economic theory instead. The monetary economy of production, in which Say’s law is not validated for the reasons previously discussed, clearly fulfils this prophecy. It is thus possible to build a model in which revenues generated by production appear to be structurally lower than the supply price of production.

A structural gap will then appear between demand and supply that can only be filled if enough credits are issued by banks in response to the requirements of households, firms, and governments. Indeed, bank credits will increase expenditures and demand beyond the net revenues of the economy. The structural gap will depend on the configuration at any given moment of the social and institutional patterns framing the economy. For example, a balance of power less favorable toward labor, as has existed since the middle of the 1970s, should widen the gap. It then becomes necessary for economic players to incur more long-term debts in order to enable global demand to reach global supply. However, the repayment of these long-term bank credits will widen the gap between demand and supply in the future because such expenditure will decrease disposable income, thereby requiring even more bank credits to be issued in the future.

Based on all these considerations, we have built a very straightforward model that yields two main results. The first result is that a monetary economy of production requires an increasing long-term debt throughout a growth phase in order to enable the selling of the production. This long-term debt can reach high amounts in comparison to the value of production, which can help us understand why the level of debt is high in modern economies. The second result is that the gap between the net demand arising from production and the value of global supply widens during a growth phase. In combination with the analysis of the regulation theory (Bénassy, Boyer, and Gelpi 1979) and past explanations of business cycles (Minsky 1986), this result can contribute to understanding why economies often face overproduction crises after several years of growth.

These two results are fundamentally linked to the monetary nature of economies and the banking nature of money. In a nonmonetary economy, wherein profits are made in kind and production costs are paid in kind, none of the features highlighted here will appear, which strengthens the idea that building a proper monetary theory of production is essential to understanding the functions and dynamics of our economies.

This study also raises the question of the relevance of monetary creation mechanisms. Indeed, if there is a structural gap between the revenues generated by the production process and the supply price of production, we can wonder whether it is fair to fill it with bank credits. In such circumstances, society has to get into debt just to buy what it produces, which does not seem reasonable because it can give the impression that society lives beyond its means, when in reality it just consumes what it produces. In addition to the implementation of stimulus policies to fill the gap between revenue and production, we might find a solution to this problem by modifying the mechanisms of monetary creation and destruction. This conclusion coincides with the point of view of Jean de Largentaye, the French translator of General Theory, who writes in his second preface to this book: The key to full employment is not to be found in monetary expansion, or in Revenue Policy, nor in the other expedients deduced from the General Theory. As far as we are concerned, it is to be found in the abandonment of an empirical institution that is unfair and inefficient, namely credit money, and its replacement by rational money adjusted to its economic and social functions. May Keynes’ work help to make this point understood. (De Largentaye 1998: 28 [authors’ translation] quoted in Keynes [1936] 1998)]

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.