Abstract

Based on Arrighi, we empirically investigate whether financialization and militarization are mutually reinforcing phenomena in the United States. Military spending during the 1950–1960s in the United States counteracted the stagnation of the monopolistic stage of capitalism. Monopoly capital was transformed into finance monopoly capital as the intensity of financial capital increased during the late 1970s in response to stagnation. Considering alternative financialization variables and the profit rate in the financial sector, and using several parametric and nonparametric methods, we found a significant relationship between financialization and militarization in the United States for 1949–2019. The results suggest that the rise in financialization is parallel to the decline in the profit rates, leading to larger military expenditure in total, but with relatively smaller share in GDP.

1. Introduction

We empirically examine the argument, based on Arrighi (1994), that financialization and militarization are mutually reinforcing phenomena during the post-World War II period for the United States finance capital, as Hilferding labeled it, or monopoly-finance capital, as Sweezy (1994) preferred, as it began to dominate the dynamics of the accumulation of capital, particularly during the 1980s. According to Keynes, financialization represented the end of capitalist rationality, and he referred to it as “a bubble on a whirlpool of speculation” (Sweezy 1994; Foster 2005). In Monopoly Capital, Baran and Sweezy (1966) argued that stagnation is the normal state of monopoly capitalism. That is, to absorb surplus, the government uses continuous and excessive military spending. Also, sales effort, the financial sector (i.e., finance, insurance, and real estate—FIRE), and capitalists’ consumption and investment help absorbing. This makes the system irrational because it can only protect itself through wasteful sales effort and military spending instead of productive civilian investment and welfare spending. That is, financial capitalism is the system’s response to the decline in profitability.

Military spending during the 1950s and 1960s in the United States, along with other external stimuli, such as a rising sales effort and financial expansion, counteracted the stagnation of the monopolistic stage of capitalism (Baran and Sweezy 1966). Nevertheless, the long-term problem of underconsumption requires further measures. Monopoly capital was transformed into finance monopoly capital as the volume and intensity of financial capital increased during the late 1970s (Magdoff and Sweezy 1987; Foster and McChesney 2012). While the role of military spending as an external stimulus continued, it may be argued that these two stimuli are not independent; rather, they mutually generated and reinforced each other to sustain the financial capitalism centered in the United States. The dominance of the dollar secured the US global economic hegemony, thereby enabling its excessive military budget. This in turn maintained the US political power, thereby securing the dollar’s hegemony. Employing detailed statistical analysis and nonparametric estimation methods, this study contributes to the literature by providing the first empirical evidence on the proposition that financialization and militarization reinforce each other for the United States for 1949–2019.

The next section outlines the literature on the relationship between financialization and militarization. The third section presents the data, statistical analysis, and the method. The fourth section presents the empirical evidence. The conclusion highlights the study’s main inferences and contribution to the literature.

2. Literature on the Relationship between Financialization and Militarization

Financialization is a crucial concept in the periodization of the development of capitalism. Definition of financialization emphasize different aspects of the process. 1 For example, Krippner defines it as “a pattern of accumulation in which profits accrue primarily through financial channels rather than through trade and commodity production” (Krippner 2005: 174; see also Krippner 2011) whereas, for Epstein, it is “[the] increasing role of financial motives, financial markets, financial actors and financial institutions in the operation of the domestic and international economies” (Epstein 2005: 3). For Fine, financialization is the intensive and extensive accumulation of fictitious capital (or interest-bearing capital) in the accumulation of capital (Fine 2009, 2010).

There are different understandings of financialization as the stage of the rapid deregulation and globalization of finance capital during the 1990s. Overall, for post-Keynesians, financialization caused stagnation as wage stagnation and income inequality led to insufficient aggregate demand. Accordingly, “increased financial investment and increased financial profit opportunities crowd out real investment by changing the incentives of the firm managers and directing funds away from real investment” (Orhangazi 2008: 864). From a general Marxist perspective, however, productive sector capitalists shifted their activity to fictitious capital operations to address the problem of lower profitability due to underconsumption/overaccumulation. Yet, Orhangazi notes the downsides of such simplifications to emphasize the contradictory role of financialization in the economy in that while it facilitates capital accumulation, it also hinders it by causing financial crises (Orhangazi 2011, 2016). He argues that explaining the rise of finance “as some external force impinging on the economy” or “as a response to accumulation problems in the non-financial parts of the economy” fails to present the complex and contradictory role of the financial sector (Orhangazi 2016: 249). Among Marxist thought, while Ben Fine (2009, 2010, 2021) and the Monthly Review school used the term along with neoliberalism and globalization within the Marxist analytical framework, Lapavitsas and Bryan referred to financialization as a new stage of capitalism by moving toward a post-Keynesian framework (e.g., Bryan, Martin, and Rafferty 2009; Lapavitsas 2009, cited in Mavroudeas and Papadatos 2018: 457).

The common insight of post-Keynesian financialization hypotheses is to consider finance as “the new and dominant exploiter, not capital as such,” thereby seeing finance capital as the real cause of crises, not underconsumption theory or the tendency for the profit rate to fall, as in Marxist thought (Roberts 2018). In other words, the financialization hypotheses of the post-Keynesian tradition, as well as some Marxist perspectives, such as that of Lapavitsas, argue that financialization has created profit by extracting money from workers and firms operating in the productive sector in the form of financial commissions, fees, and interest charges. That is, it is a “secondary exploitation” that does not come from the exploitation of labor 2 (Roberts 2018). In other words, according to the financialization hypothesis, finance capital has an autonomous structure, independent from productive capital (Mavroudeas and Papadatos 2018). However, in the Marxist framework, surplus value is created through production in the productive sector before being allocated between productive capital, money capital, and commercial capital in terms of profit, interest, and commercial profit, respectively. That is, profit in financial sector is simply a transfer of some part of total profit created in the productive sector; therefore, although money capital appears to dominate productive capital, its existence ultimately depends on productive capital (Hilferding 1910; Sweezy 1942; Mavroudeas and Papadatos 2018).

2.1 Financialization and militarization as a response to economic downturns

Baran and Sweezy in Monopoly Capital analyzed a chronic lack of aggregate demand in a capitalist economy to argue that capitalist development concentrates capital in fewer giant corporations, limiting production, investment, and workers’ buying power in order to reap higher profits. They concluded that “the normal state of the monopoly capitalist economy is stagnation” (Baran and Sweezy 1966: 108). This is not, however, because the economy is not productive enough; rather, it is too productive to absorb the created surplus. Therefore, the surplus is absorbed by the capitalists’ consumption and investment, sales efforts, finance, insurance, real estate, civilian government expenditure, and military spending. 3

A capitalist economy must grow continuously, which requires new markets, new products, and new technologies. The problem with the need for constant growth, however, is that to prevent profit rates from further decreasing in the long term, the nature of capitalist production requires these expenditures to be unproductive spending, such as sales efforts and military spending, rather than productive spending, such as capitalist investment and civilian government spending, which increase wages or capital. However, such surges in unproductive spending along with the dramatic increase of labor exploitation were not enough to prevent stagnation, the decline in the profitability. Global economic transformation was an additional development that impaired this trend for the United States. Despite access to raw materials across the globe, the profitability of the US manufacturing sector fell by around 40 percent between 1965 and 1973 (Brenner 2006: 99; Meyerson and Roberto 2008: 165). Moreover, the economies of Japan and Europe, particularly Germany, substantially increased their share in manufacturing exports to become two major rivals to the United States.

To address the fall in profitability in the real economy, capital shifted to unproductive investment in the financial sector seeking a higher profit rate. Hence, the tendency of the decline in profitability led to a growing investment in the financial sector as opposed to the productive sectors. This led to the deepening in financialization and speculative bubbles in the United States and other major Western economies. 4 However, as noted above, financialization can play a contradictory role in the economy, helping capital accumulation while also undermining it by causing periodic financial crises (Orhangazi 2011, 2016). Demir (2009b) is the only study that tests this hypothesis, examining the effect of financial investments and rate of return on fixed investment and capital accumulation in Mexico and Turkey. According to Fine, the relationship between financialization and neoliberalism has been direct and integral, where the former becomes the short definition of the latter (Fine 2009, 2010). In this setting, monopoly-finance capital has responded to the fall in profitability by expanding its coverage toward new areas, such as insurance and pension systems, by means of the predator state, 5 both in the United States and across the world (Galbraith 2008; Foster and McChesney 2012). In other words, finance capital has expanded both at the national and international levels to redesign the global economic order with the state’s political and military help (Lapavitsas 2013).

One argument that we based our empirical model on is the general Marxist perspective suggesting that financialization is a response to economic sluggishness. Therefore, the US economy particularly started to rely on the financial sector along with persistent military spending as two main stimuli to deal with sluggish economic growth and declining profitability in the productive sector. In other words, based on Arrighi (1994), these two stimuli in the United States are not independent tools but mutually reinforcing. Therefore, we focus on the dialectic relationship between financialization and militarization.

2.2 The dialectical relationship between financialization and militarization

There is a dialectical relationship between financialization and militarization. Financialization is a response to the stagnation due to underconsumption while militarization is needed to impose financialization, thereby reinforcing each other in the United States. Below, we discuss why militarization is a key aspect of financialization in the United States. Arrighi (1994) and others have pointed out the mutually reinforcing nexus of financialization and militarization as a contribution to an anthropology of political economy (Hart and Ortiz 2008, cited in Røyrvik 2010).

Following Braudel (1981), Giovanni Arrighi (1994) argued that, throughout the history of capitalism, the decline of hegemons is associated with financial expansion. 6 As Hobson’s analysis suggests, in hegemons, capital shifts from the real economy to fictitious capital operations and to war-making activities, both as a consequence of and to slow the decline of political and economic power (Arrighi 1994; Arrighi and Silver 1999). Meanwhile, emerging economies use their competitive advantage to increase their share in the world economy. However, as global trade and development hit their limits, big capitalists turn to speculative financial markets, investing in unproductive sectors in response to the decline in profitability. Capitalists in dominant economic centers can exploit their power in the global economy as a taxing mechanism. That is, they can use financial flows to extract wealth from weaker players (Beck and Knafo 2020).

The key point in Arrighi’s analysis is that financialization is a product of power and can only be sustained so long as there are significant economic imbalances between major countries and peripheral countries. These originated in the establishment of three institutions of the Bretton Woods established after the World War II: namely, the General Agreement on Tariffs and Trade, the International Monetary Fund, and the World Bank. As the leading power, the United States designed the structure of capitalist global economy while these institutions in return reinforced the US economic hegemony by making it the enforcer of the rules of the game. Meanwhile, developing countries became caught in a debt trap (Magdoff 1969: 50), creating a permanent economic imbalance that favored the United States. In other words, the steady financial expansion in the US economy was due to the role of the dollar in the global economy that was significantly advantageous to the United States.

The unique role of dollar is also closely linked to the US military power. As Andre Gunder Frank has succinctly argued, “Uncle Sam’s power rests on two pillars only, the paper dollar and Pentagon” (Frank 2005), although he also noted that “[e]ach supports the other, but the vulnerability of each is also an Achilles’ heel that threatens the viability of the other” (Frank 2005 cited in Meyerson and Roberto 2008: 174–75). Similarly, Magdoff argues that “[t]he positioning of US military bases should therefore be judged not as a purely military phenomenon, but as a mapping out of the US dominated imperial sphere and of its spearheads within the periphery” (Magdoff 1969: 50).

Foster (2006: 17) notes that “[if] neoliberalism had arisen in response to economic stagnation, transferring the costs of economic crisis to the world’s poor, the problem of declining US economic hegemony scented to require an altogether different response—the reassertion of US power as military colossus of the world system.” In this sense, David Harvey contends that the goal of the United States in Iraq invasion was “a full-fledged neoliberal state apparatus whose fundamental mission is to facilitate conditions for profitable capital accumulation” (Harvey 2005: 8). In fact, it is no secret that the United States has “a strategy of retaining its economic and political hegemony through military means,” as reported in the National Security Strategy of the United States in 2002 (Foster 2005: 1). Thus, the goal in Iraq went beyond simply controlling oil reserves to protect the dollar’s dominant role, as made clear by a member of Defense Secretary Donald Rumsfeld’s Office of Special Plans, “who noted that the invasion was undertaken in part to secure the dollar as Saddam Hussein and others were in the process of switching from the dollar to the Euro to price their oil” (Clark 2005, cited in Meyerson and Roberto 2008: 174).

The dollar’s hegemony as the global economy’s dominant currency (i.e., the world’s reserve currency) has been allowing the United States to serve as the world’s leading creditor. Since the United States can supply dollars if needed simply by printing them, it need not worry about trade deficits or facing a currency collapse. Since the dollar is the reserve currency and has military “protection” from the United States, other nations use it to trade with each other as they need to obtain dollars to purchase oil. Finally, some of those dollars circulate back to the US economy as other nations invest in the US stocks or treasury bonds. While in the short term, this financial system substantially benefited US businesses “because large dollar holdings in foreign hands helped to facilitate the sale of US exports” in the long run, the decline in profitability and the rise of Japan and West Germany led to “the end of the US role as a leading global exporter of industrial goods” (Brenner 2006: 125, cited in Meyerson and Roberto 2008: 166).

The hardship for the US economy in terms of the imbalance in the positions of the dollar (i.e., a drain in gold reserves) intensified with the US defeat in Vietnam as the flow of dollars abroad created a huge euro-dollar market (Clark 2005; Wallerstein 2003: 18, 49; Foster 2005; Meyerson and Roberto 2008). This led to the end of the dollar-gold regime when Nixon delinked the dollar from gold in 1971 de facto and in 1973 officially (D’Arista 2009). This is considered as the beginning of the decline of US economic hegemony (Foster 2006), which was supposed to be cured by financialization. The oil shock in 1973 led to a vast flow of petrodollars into the oil-producing states, which in turn flowed back to the United States, mostly via American banks. This was a new phase of US economic hegemony. As Clark (2005: 28) puts it, “The process of petrodollar recycling underpins the US’s economic domination that funds its military supremacy. Dollar/petrodollar supremacy allowed the US a unique ability to sustain yearly current account deficits, pass huge tax cuts, build a massive military empire of bases, and still have others accept its currency as medium of exchange for their imported goods and services” (Clark 2005: 28, quoted in Meyerson and Roberto 2008: 167). For the first time in history, a hegemon, the United States, had the ability to be a global debtor to provide a default-risk-free asset to facilitate global capital accumulation (Fields 2015: 146). In other words, the United States as the hegemon, has served as the source of global stability, a lender of last resort, and equally important the source of global demand (Fields and Vernengo 2012).

Although wages have been stagnant in the North, particularly in the United States, consumption has been boosted with increased borrowing and using up personal savings. This was “made possible by the infusion of capital from abroad, itself encouraged by the hegemony of the dollar” (Foster and Magdoff 2009: 100). Furthermore, finance capital has imposed the very same addiction to high consumption by means of borrowing and promoted domestic financial markets, and aggressively attacked social welfare institutions (such as the health and education sector) to open up them for local and international private sector by means of the predator state (Galbraith 2008). This is part of what Harvey (2005) has labeled “accumulation by dispossession,” creating profit rather than wealth for the capital groups (in most cases, those that have close organic ties with the government) by exploiting public sources.

With its hegemonic control over technology and communications, and by means of military power, financial capital has been able to sustain such a drain of capital from the South to the North, particularly the United States (Foster and McChesney 2012; Herrera 2013). Militarization of production is indispensable for global finance capital because it is a major source of profit and an extremely useful tool to reproduce itself by protecting and expanding markets. Finance capital increased its power over the military sector by buying stock in giant arms corporations to become a major component of the military industrial complex. Herrera (2013) provides valuable information in this regard: “At the beginning of the 2000s, the proportion controlled by finance capital reached 95.0 percent of the capital of Lockheed Martin, 86.5 percent of that of Engineered Support Systems, 85.9 percent for Stewart & Stevenson Services, 84.7 percent for L-3 Communications, 82.8 percent for Northrop Grumman, 76.0 percent for General Dynamics, 70.0 percent for Raytheon, 66.0 percent for Titan, 65.0 percent for Boeing, etc.” (Herrera 2013: 170). As the neoliberal paradigm reinforces privatization in the “defense sector,” finance capital also increases its share by taking this outsourced defense business (Cicchini and Herrera 2008; Herrera 2013). Gentilucci (2019) provides further evidence on the financialization and concentration in the defense sector.

Finally, Nölke (2020) provides an excellent discussion on the role of financialization in degrading democracy. That is, financialization leads to higher military spending by overcoming objections by weakening democratic structures in the developing countries, thereby helping the interests of the global military financial industrial complex.

2.3 Financial profit rates and militarization

Financialization is a response to the crisis of accumulation due to underconsumption or the tendency of profit rates to decline. This subsection briefly discusses the relationship between militarization and financial profit rate.

The third volume of Das Kapital focused on the financial sphere of a capitalist economy. Marx examined the critical role of credit and financial speculation in capital accumulation, foreseeing the rise of the financial sector, and the centralization and concentration of capital (Roberts 2018). For Marx, financial investment was a counteracting factor to the tendency of the rate of profit to fall. Although credit helps to boost trade, its effect is limited because when the rate of exploitation of labor begins to decline, credits cannot be repaid. Against this background, some have analyzed financialization as a counteracting factor to the tendency of the rate of profit to fall, along with other counteracting factors originally noted by Marx and Engels (Giacché 2011; Guillén 2014; Mavroudeas and Papadatos 2018; Ramirez 2019; Di Bucchianico 2020a).

Financialization keeps aggregate demand high despite stagnant real wages by easing borrowing and creating wealth through increases in prices in the housing market. This in turn prevents the rate of profit from falling while opening up new investment opportunities in the financial sphere. Finally, financialization generates opportunities to earn money by speculating. Investigating the various channels through which financialization impacts the rate of profit, Di Bucchianico (2020b) found effects due to technical innovations in the financial sector, the size of the financial sector in terms of its share in total profits and GDP, and rising household indebtedness. In addition, sociopolitical factors that reduce workers’ bargaining power also had a significant effect on the normal rate of profit. Using semiannual data from 1993 to 2003 for the manufacturing sector in Turkey, Demir (2009c: 607) showed that financialization reduced the negative impact of macroeconomic uncertainty on the profitability by “diversifying firms’ investment portfolios and work as a cushion against unexpected downturns in the market.” However, it is important to distinguish between the normal rate of profit (or nonfinancial profit rate) and the financial profit rate.

Bakir and Campbell (2010: 325) note that, from a Marxist perspective, financial profits are simply a transfer of part of the total profits to the financial sector. That is, profits are created in the real economy (i.e., productive capital), and such a transfer may theoretically have a positive or a negative effect on accumulation. On the one hand, it is a subtraction from the capital accumulation because “net interest payments to the financial sector from the nonfinancial sector are deductions from the produced profit that is available for productive reinvestment and accumulation” (Bakir and Campbell 2010: 326). On the other hand, financial profits may increase the rate of accumulation by improving the conditions for further accumulation (Bakir and Campbell 2010: 325). In other words, Marx argues in the third volume of Das Kapital that credit does not create profits directly but improves the conditions to earn higher profits. The expansion of credit can accelerate the process of capital concentration. In terms of the circuit of capital model, the expansion of credit shortens the “turnover of capital,” thereby reducing finance lag (Foley 1982). Bakir and Campbell (2010) claim that, in financial capitalism, a smaller portion of profits was reinvested in the productive sphere of the economy because corporations were forced to pay significant fees for the money they borrowed from the financial sector, which otherwise would have been redirected to productive investment, causing a decline in the rate of accumulation.

Only a few studies have measured the financial rate of profit (Duménil and Lévy 2004; Bakir and Campbell 2013; Freeman 2012). Freeman shows that when financialization is taken into account, the corrected rate of profit exhibits a consistent long-run fall in the United States and the United Kingdom. Because it would be illogical to assume that monetary assets are capital in the hands of a bank but not in the hands of a company in the nonfinancial sector, one should also consider ownership of financial assets in calculating the profit rate for nonfinancial sector (Freeman 2012). Therefore, Freeman suggests adding medium- and long-run marketable assets to the denominator of the profit rate. Following such an alteration, the profit rate for the United States and the United Kingdom shows a steady decline up to the 1980s instead of a recovery as the traditional method suggests.

As discussed above, military spending has been used as a stimulus to overcome chronic lack of aggregate demand, chronic stagnation problem due to underconsumption, and overaccumulation. Some studies have empirically analyzed the impact of military spending on the rate profit from a Marxist perspective (Elveren and Hsu 2016; Elveren 2019). Elveren (2019), in a comprehensive study, showed that while higher military expenditure is associated with higher profit rates for the whole study period of 1960–2014, this positive relationship between military spending and the rate of profit was not statistically significant when one focused on the neoliberal era. He also noted that the counteracting effect holds for arms-exporting countries but not arms-importing countries. Moreover, using an adapted circuit of capital model, proposed by Foley (1982), he showed that a larger share of military sector is associated with a higher rate of profit as the finance lag is smaller in the military sector. Elveren (2022) provided empirical evidence for this proposition. However, as we discussed, the pattern of the financial rate of profit differs from the normal rate of profit (i.e., the nonfinancial profit rate). To distinguish the difference between the two definitions of profit, financial and nonfinancial, and to reveal their mutual connection with militarization, a comprehensive statistical and empirical analysis follows in the next section.

3. Data and Method

The empirical analysis employs financialization and militarization indicators in the United States based on yearly data from 1949 to 2019, which is the longest possible time series available. 7 The variables for defining financialization and militarization are selected in accordance with the previous literature. In order to measure financialization, interests and dividends as ratios of gross domestic product and various definitions of financial profits are utilized. Davis (2017) presents empirical descriptions of financialization in her comprehensive survey and reveals that these are the most commonly used indicators in the literature. We further consider alternative profit measures commonly referred in the Marxist literature, namely, the two profit rates calculated by Freeman (2012) and the three profit rates defined by Bakir and Campbell (2013).

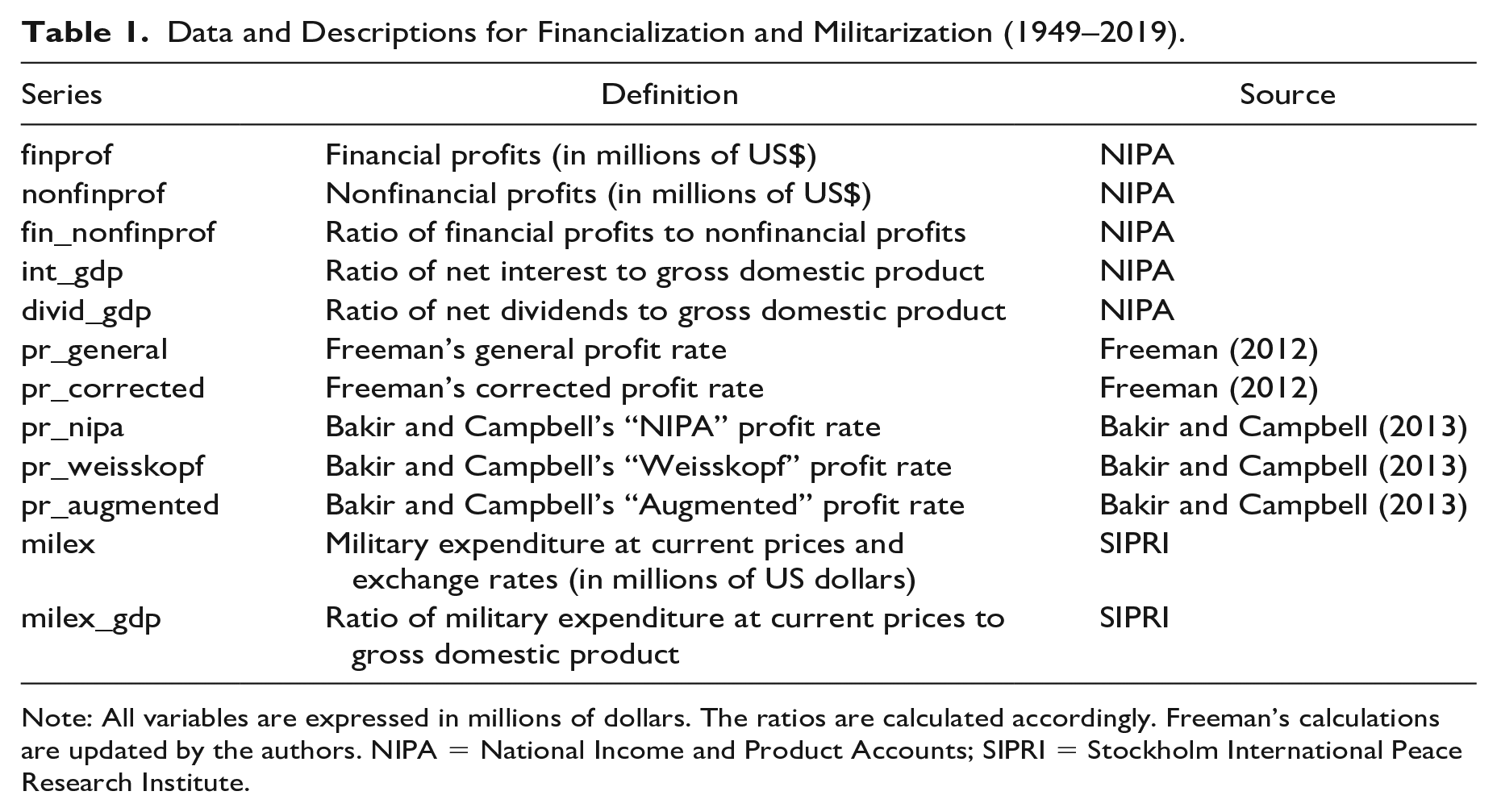

To measure militarization, we use military expenditure and the ratio of military expenditure to gross domestic product. 8 Although militarization and militarism refer to different aspects of the same process, it is not uncommon to use them interchangeably. 9 Militarism is a much broader concept than militarization in that the latter refers to only one aspect of the former, namely, the increase in military spending. However, we acknowledge that it is not easy to operationalize militarism, so it is appropriate for our purposes in this study to limit our focus to militarization measured by military expenditures. The descriptions of the data are presented in table 1 and the summary statistics are available in the appendix.

Data and Descriptions for Financialization and Militarization (1949–2019).

Note: All variables are expressed in millions of dollars. The ratios are calculated accordingly. Freeman’s calculations are updated by the authors. NIPA = National Income and Product Accounts; SIPRI = Stockholm International Peace Research Institute.

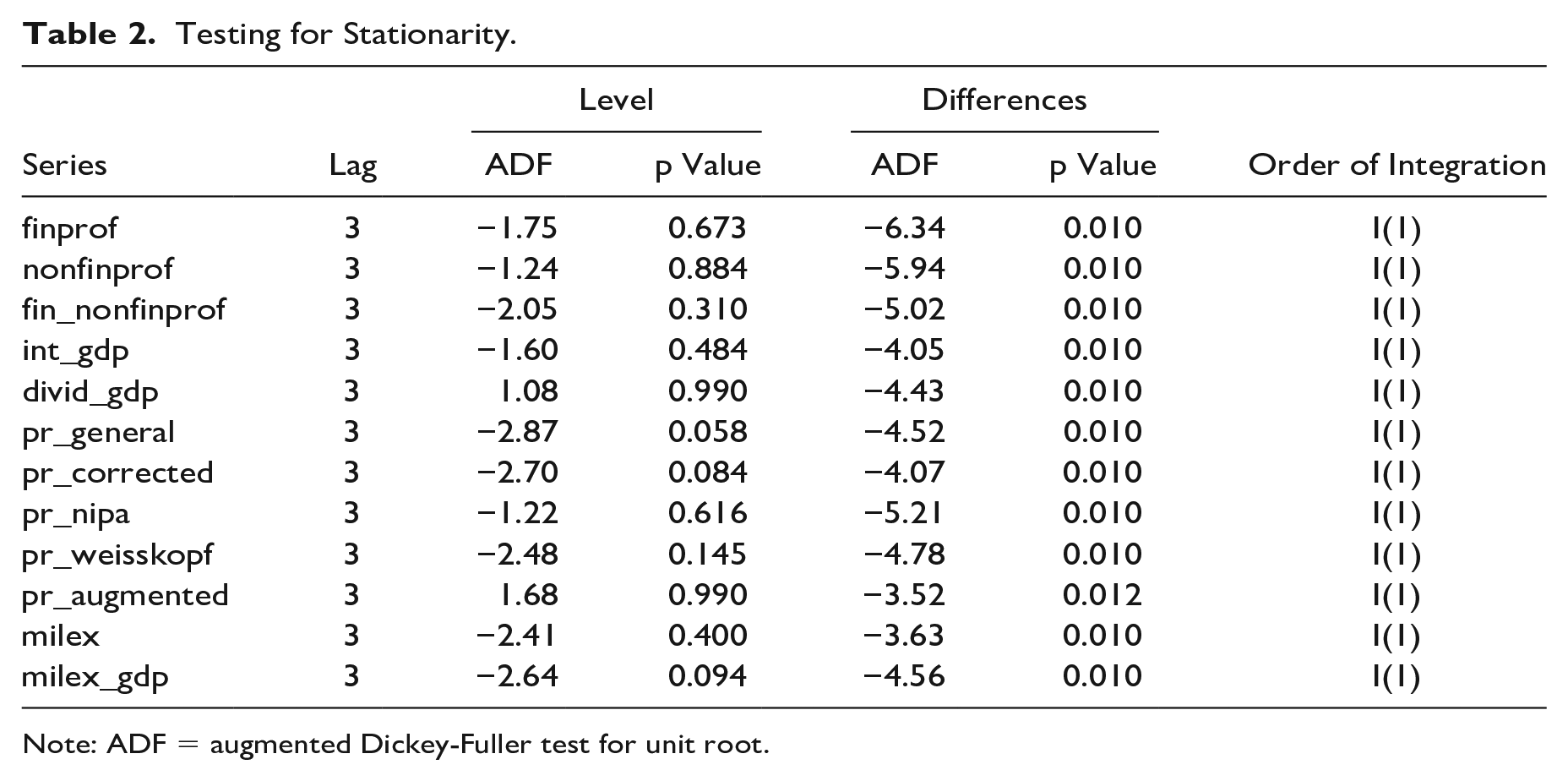

Prior to an elaborate discussion on the empirical model, the characteristics of the data need to be determined using appropriate statistical tests. As the data set is a rather long time series, we first tested for nonstationarity. The outcomes in table 2 reveal that all variables are integrated at order one.

Testing for Stationarity.

Note: ADF = augmented Dickey-Fuller test for unit root.

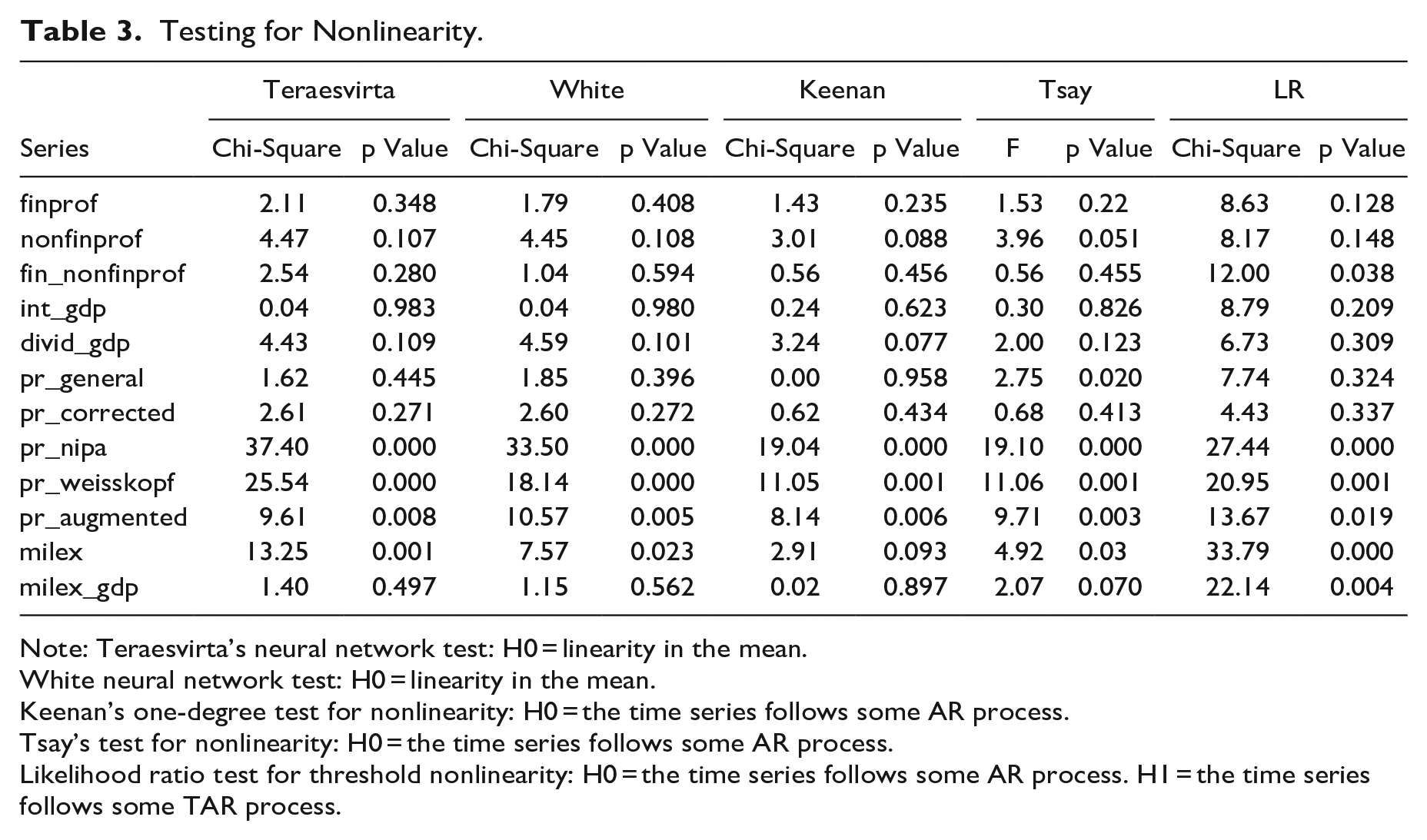

After conducting the unit root analysis, the empirical time series literature mostly uses cointegration methods to find the parameters explaining the overall structure. While such parametric models are quite common, they rely on several critical underlying assumptions, with linearity being the most important and restrictive. If the true data-generating process does not satisfy these assumptions, the results are misleading since the estimated coefficients become biased and inconsistent. Thus, unless it can be shown that a linear functional form between the dependent variable and the covariates holds globally, parametric models are not the best choice.

We therefore conduct statistical tests for possible nonlinearity in the model. There are numerous test statistics used in the literature based on distinct nonlinearity structures expressed by different null and alternative hypothesis. The neural network tests of Teraesvirta, Lin, and Granger (1993) and Lee, White, and Granger (1993) both test for the nonlinearity in the mean. This type of nonlinearity is profound such that its presence would affect the overall modeling structure. Table 3 presents the results along with the alternative test statistics for further reference.

Testing for Nonlinearity.

Note: Teraesvirta’s neural network test: H0 = linearity in the mean.

White neural network test: H0 = linearity in the mean.

Keenan’s one-degree test for nonlinearity: H0 = the time series follows some AR process.

Tsay’s test for nonlinearity: H0 = the time series follows some AR process.

Likelihood ratio test for threshold nonlinearity: H0 = the time series follows some AR process. H1 = the time series follows some TAR process.

The nonlinearity test results show that profit rates defined by Bakir and Campbell and the military expenditure data exhibit nonlinearity in the mean. For financial profits and nonfinancial profits, the test results do not reject the null hypotheses of autoregressive (AR) process while the unit root tests already showed that financial profits and nonfinancial profits are nonstationary. As for the ratio of financial to nonfinancial profits and military expenditure to GDP, the neural network tests show linearity in the mean, but the LR statistic suggests evidence of a threshold autoregressive process. Finally, net interests and dividends as a ratio of GDP and the Freeman profit rates show linearity in the mean. In sum, the nonstationarity and nonlinearity test results for our financialization and militarization indicators necessitate an empirical model that is flexible enough to handle nonlinear mean relationships.

We use nonparametric methods for dealing with these complexities in the empirical model, which provide flexible tools by avoiding assumptions on the functional form of the regression equation including linearity. Specifically, we employ generalized additive models (GAMs), which can be specified as follows (Wood 2017: 249):

where

4. Empirical Results and Discussion

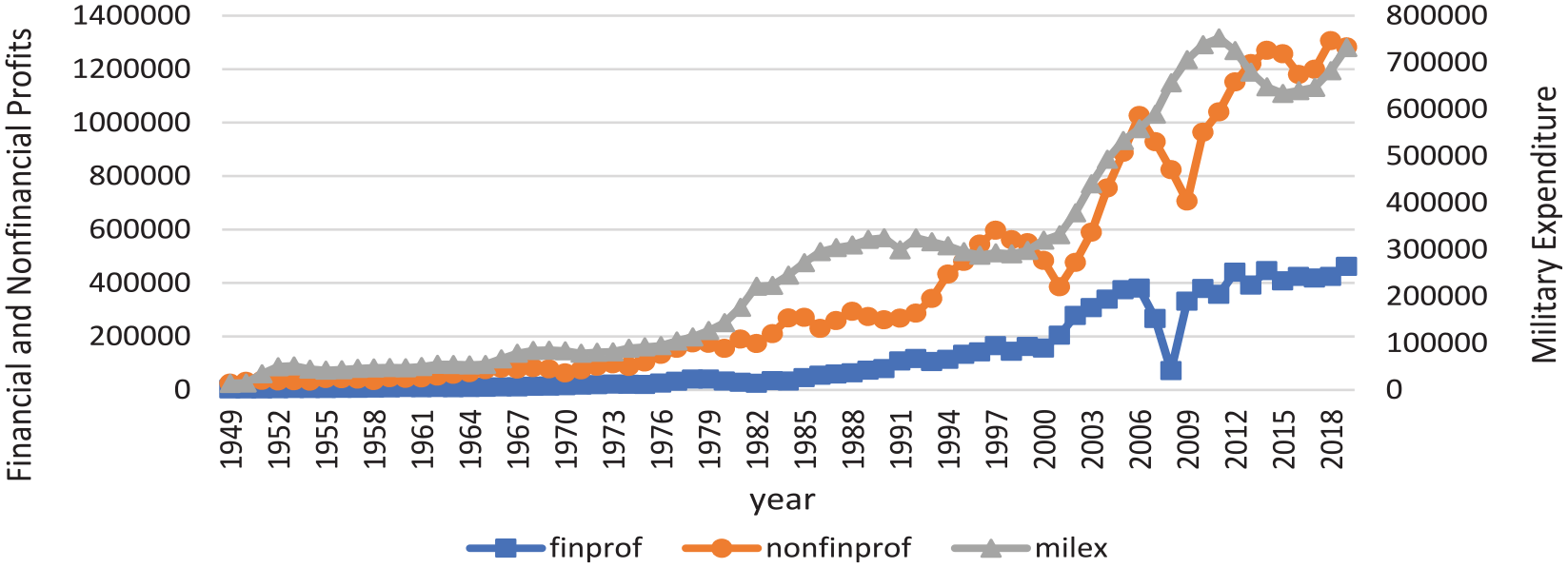

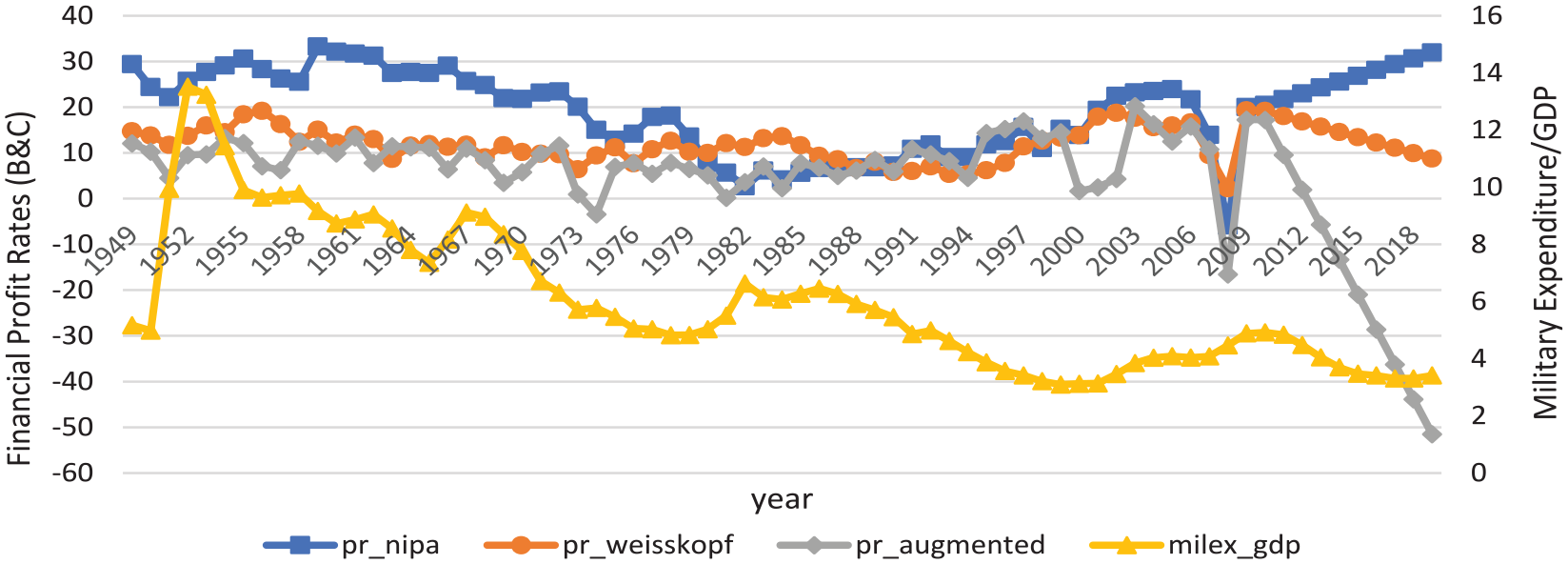

Figure 1 shows that financial and nonfinancial profits increased after the neoliberal transformation. Nonfinancial profits, which still represent the larger portion of total corporate profits, experienced more volatility after 1980 whereas financial profits increased more slowly and steadily, except for the financial collapse during the mortgage crisis in 2008–2009. Even in 2001, when nonfinancial profits declined, financial profits were relatively stable. Moreover, this rise in financial profits paralleled the upsurge in the military expenditure with even more accelerated amounts. However, one should control for the effect of GDP as an underlying factor before obtaining an empirical model as the co-movement in the two indicators may potentially be reflecting a response to the overall economic conjuncture.

Indicators of profits and military expenditure.

Taking this into account, the empirical investigation includes three nonparametric GAM estimations each referring to different approaches. First, we investigate the dialectical link between financialization and militarization by employing the commonly used indicators in the literature. Then, we discuss the Marxist analysis of declining profit rates in relation to military expenditure. For this purpose, the profit rate definitions of Freeman (2012) and their potential link with militarization are discussed. Finally, the alternative profit rate descriptions of Bakir and Campbell (2013) are evaluated.

4.1. The dialectics of financialization and militarization

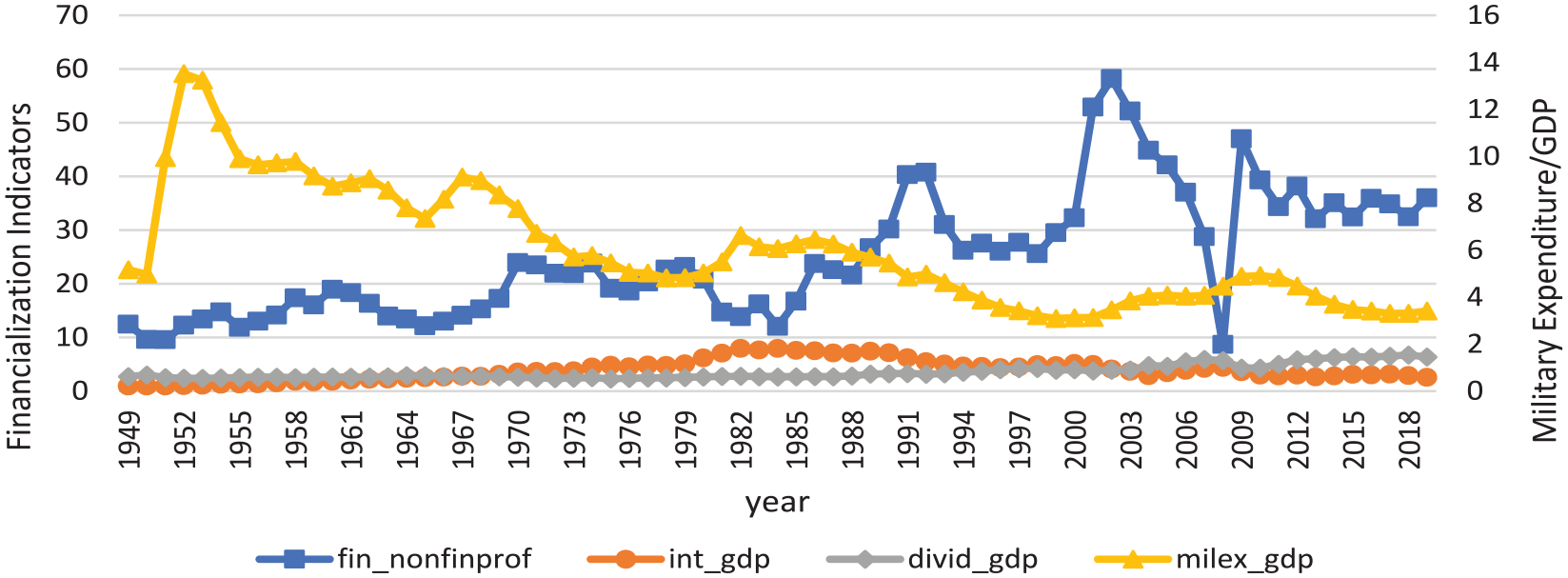

Figure 2 displays the most frequently used measures for financialization and militarization. It appears that the rate of financial profits to nonfinancial profits generally increased despite local deviations. Military expenditure as a share of GDP declined slightly before 1980 but remained relatively stable thereafter. Net interest and dividends as a ratio of GDP did not change much, which may not alter the overall pattern between the financialization and militarization.

Selected indicators for financialization and militarization.

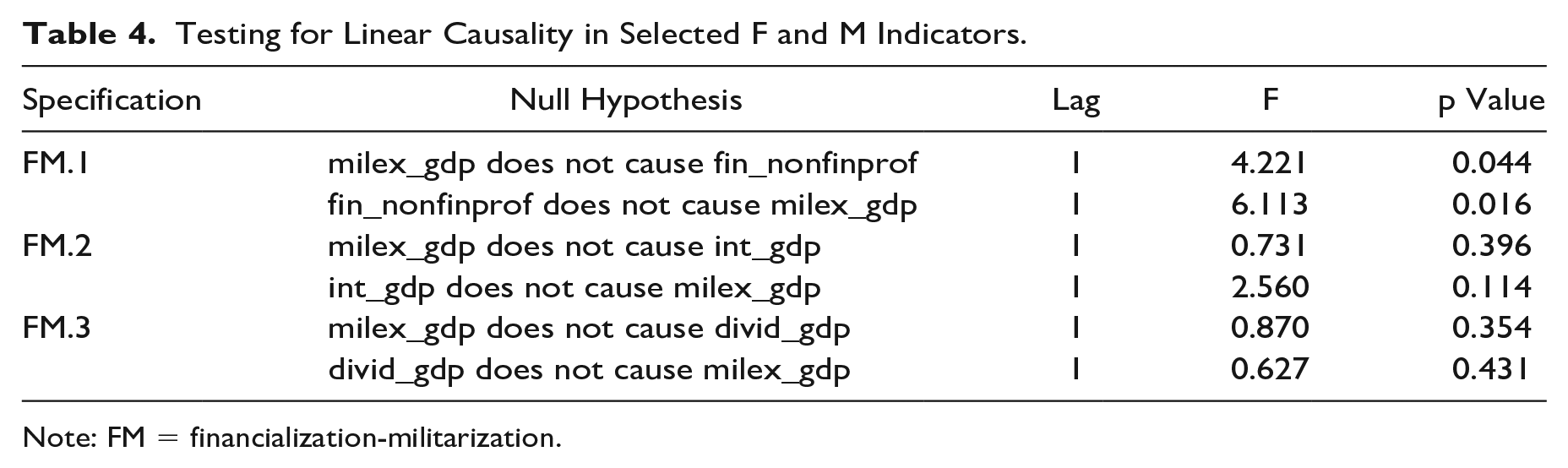

Before constructing the formal model, we should identify the response variable and consider possible endogeneity in the model. The nonlinearity test results have revealed before that all four variables are linear in mean, which allows testing for usual Granger causality. We found bivariate causality between military expenditure as a ratio of GDP and financial profits as a ratio of nonfinancial profits (table 4).

Testing for Linear Causality in Selected F and M Indicators.

Note: FM = financialization-militarization.

On the other hand, there is no causality between military expenditures/GDP and net interests/GDP or net dividends/GDP. Also, the ratios of net interest rates and dividends displayed strong concurvity 10 with the ratio of financial profits. As these outcomes may affect the precision of the estimates, we used univariate rather than multivariate GAM models. 11 Based on the bivariate causality found in table 4, we estimate the following financialization-militarization (FM) models:

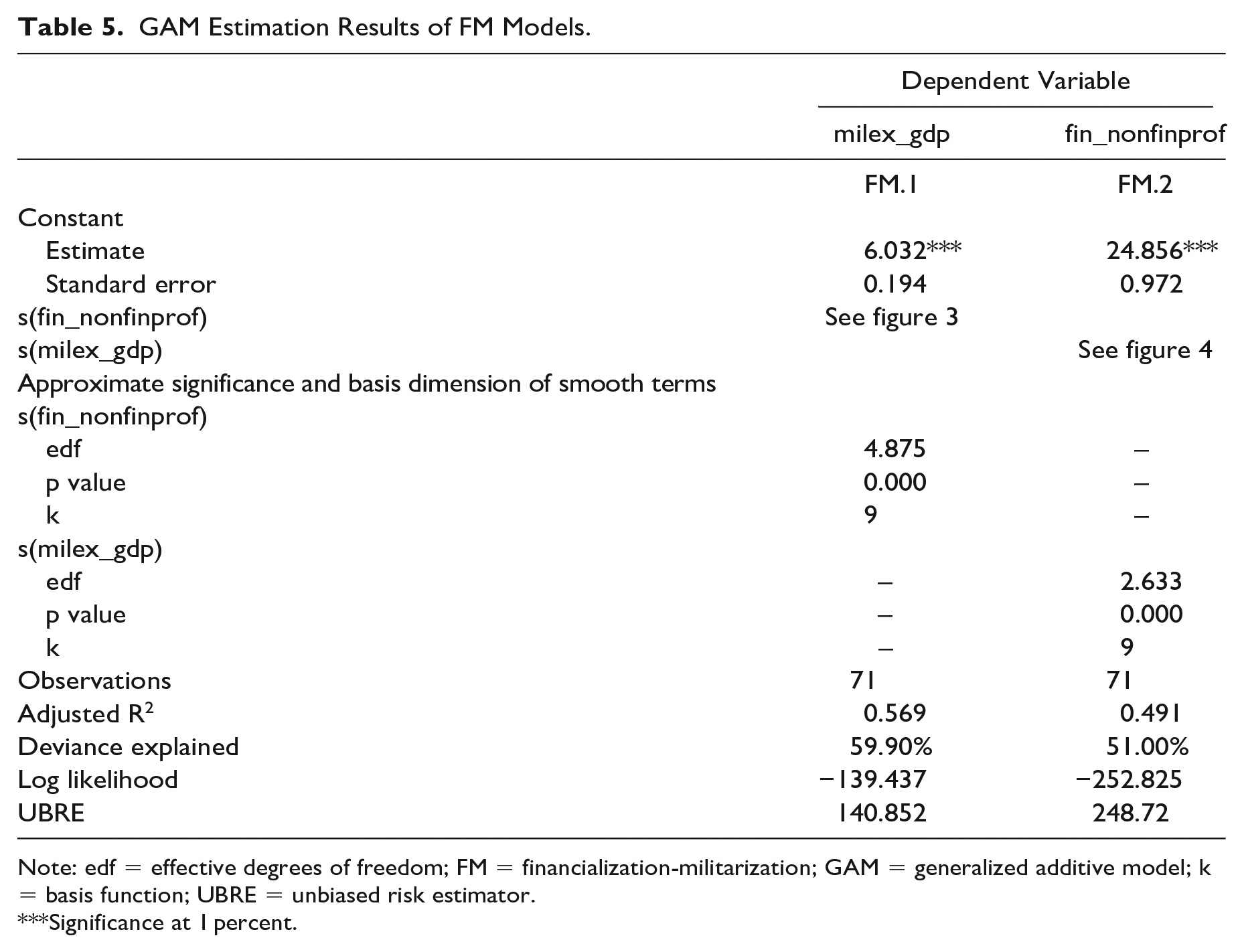

Table 5 presents the estimation results for the FM.1 and FM.2 models. In both of our estimated models, there are nine basis functions, and the effective degrees of freedom (edf) are significant and greater than one. The value of edf measures the complexity of the smoothness or wiggliness in the estimation. If it is close to one, the estimated model is closer to a straight line whereas higher edf values describe more wiggly curves.

GAM Estimation Results of FM Models.

Note: edf = effective degrees of freedom; FM = financialization-militarization; GAM = generalized additive model; k = basis function; UBRE = unbiased risk estimator.

Significance at 1 percent.

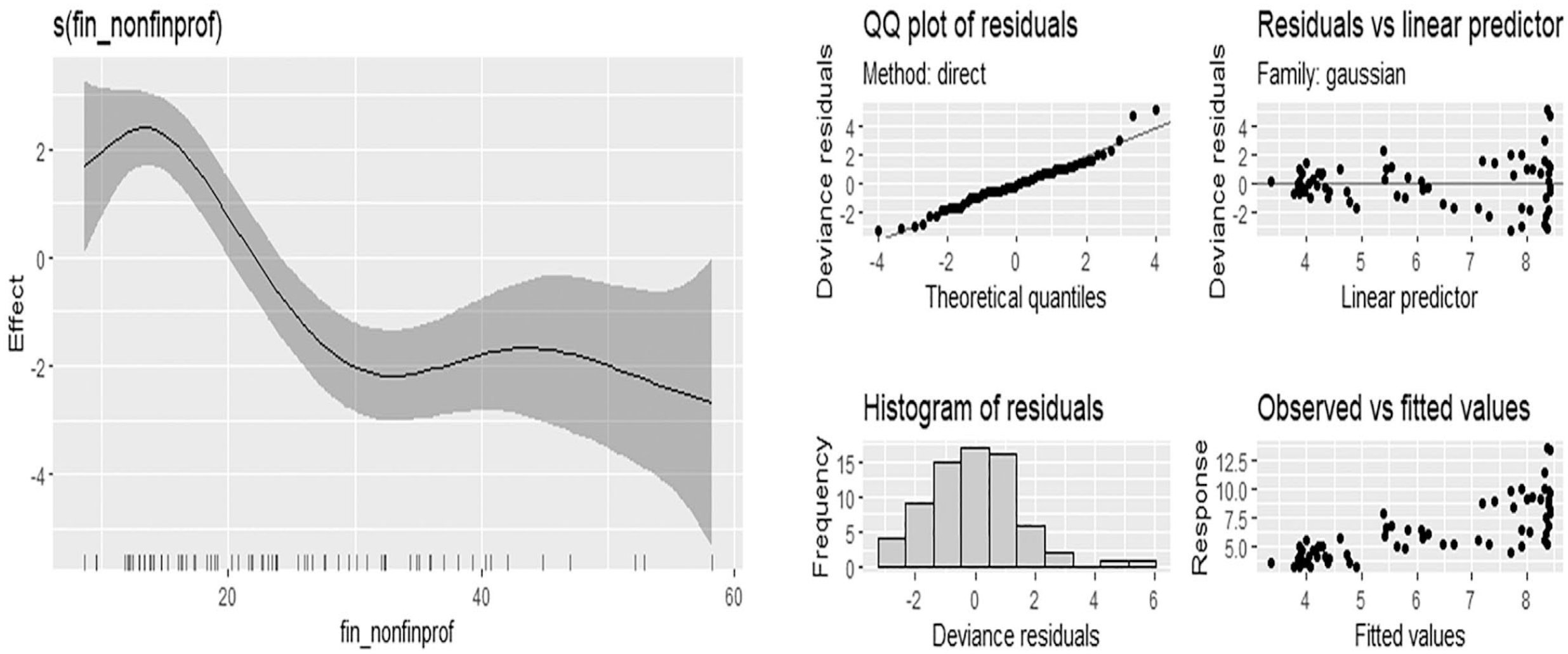

The resultant smooths are presented using plots rather than printing the coefficients since each smooth has several coefficients, in fact as many as the basis functions. The estimated smooth curve of the FM.1 model in the left panel of figure 3 demonstrates that, at the overall level,

GAM estimations for FM.1 model. (FM = financialization-militarization; GAM = generalized additive model).

The results of the FM.2 model, to the contrary, show that

GAM estimations for FM.2 model. (FM = financialization-militarization; GAM = generalized additive model).

These results imply that militarization is negatively associated with the degree of financialization, when commonly used measures in the literature are employed. However, the interpretation of these two models should be regarded with caution. Although financial profits increasing more quickly than nonfinancial profits indicates a degree of financialization, it is an ambitious measure to assess the overall financialization. When financial profits and nonfinancial profits increase simultaneously, the ratio between them may still be falling. In other words, we are observing the acceleration rather than the increase in the financial tools. 12 Different definitions of financial deepening may also be taken into consideration, and Marxist literature provides a rich discussion on that. Bearing this in mind, we now consider alternative measures for financial profits and their relation to militarization.

4.2. Financial profit rates in relation to militarization: Freeman definitions

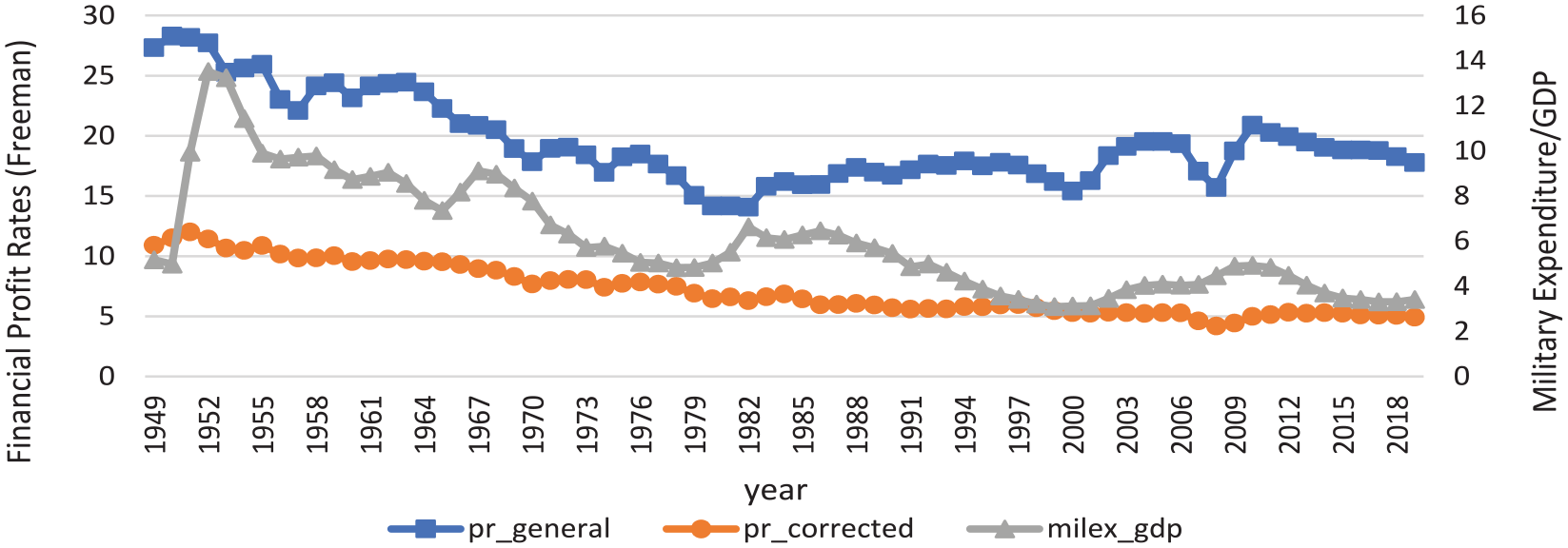

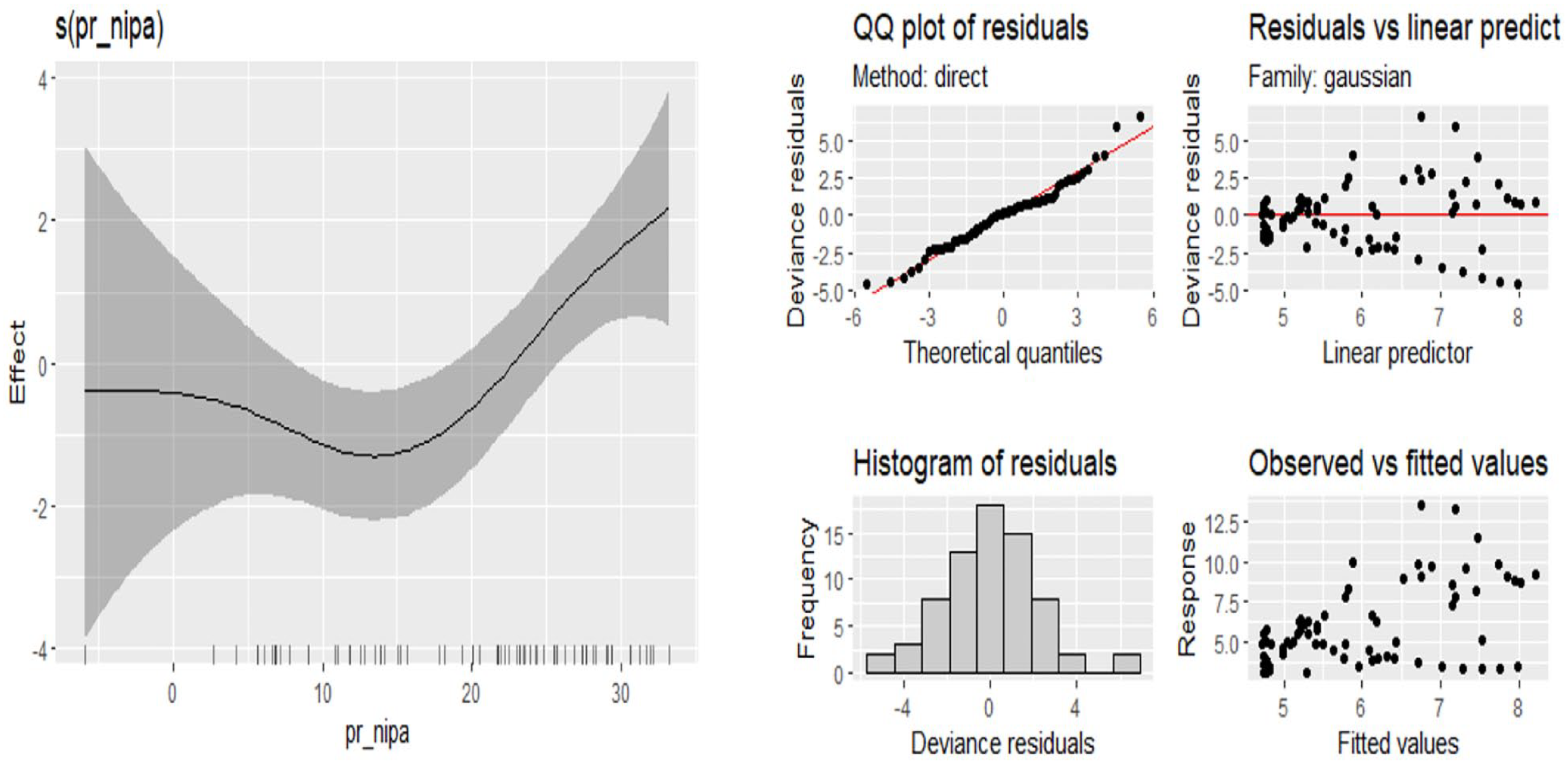

Freeman (2012) discusses two different definitions for profit rates tied up with financialization. First, he discusses the general profit rate traditionally measured by most Marxist scholars. This definition is calculated as a ratio of corporate value added with respect to corporate capital stock. This has tended to rise since the 1970s. Freeman then presents a corrected measure of the profit rates that includes financial securities in the denominator. After this adjustment, he claims, the tendency of the rate of profit to fall becomes apparent both in the UK and the US economies, even after the 1980s. Our research question follows from this: Are these general or uncorrected profit rates in the US economy also related to militarization of the country? Our initial observations based on the graphical analysis of figure 5 suggest that there may be such a correlation.

Financial profit rates (Freeman definition) and militarization.

Military expenditures as a ratio of GDP and the two profit rate definitions of Freeman seem to have a similar long-run pattern

13

(figure 5). We believe Bayesian inferences may more reliably detect the underlying relationship, since the likelihood ratio test suggested the possibility of threshold nonlinearity in the

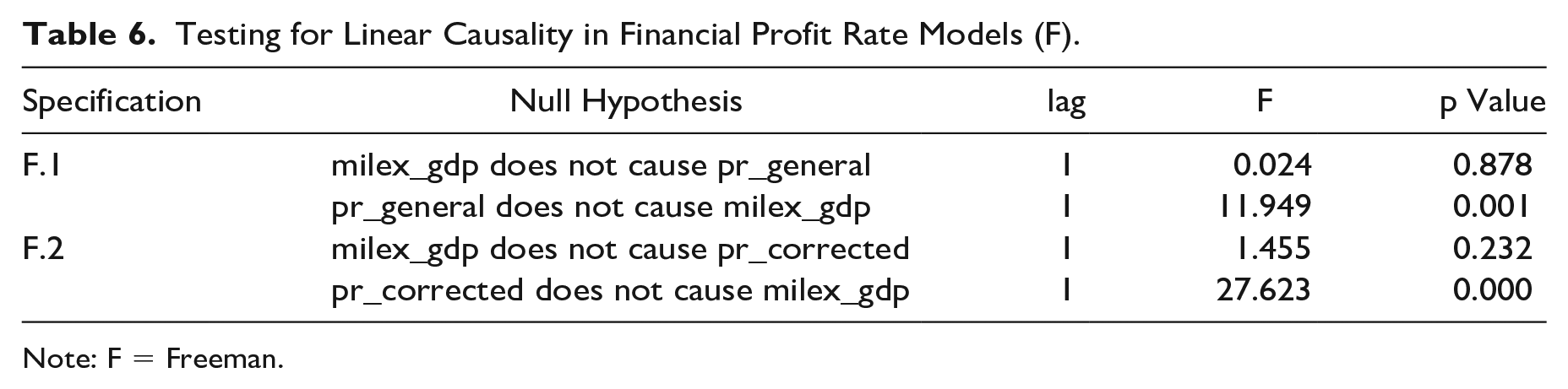

Table 6 presents the causality test results for the profit rates

Testing for Linear Causality in Financial Profit Rate Models (F).

Note: F = Freeman.

Thus, we specify the following two univariate models to determine the effect of financial profit rates on militarization:

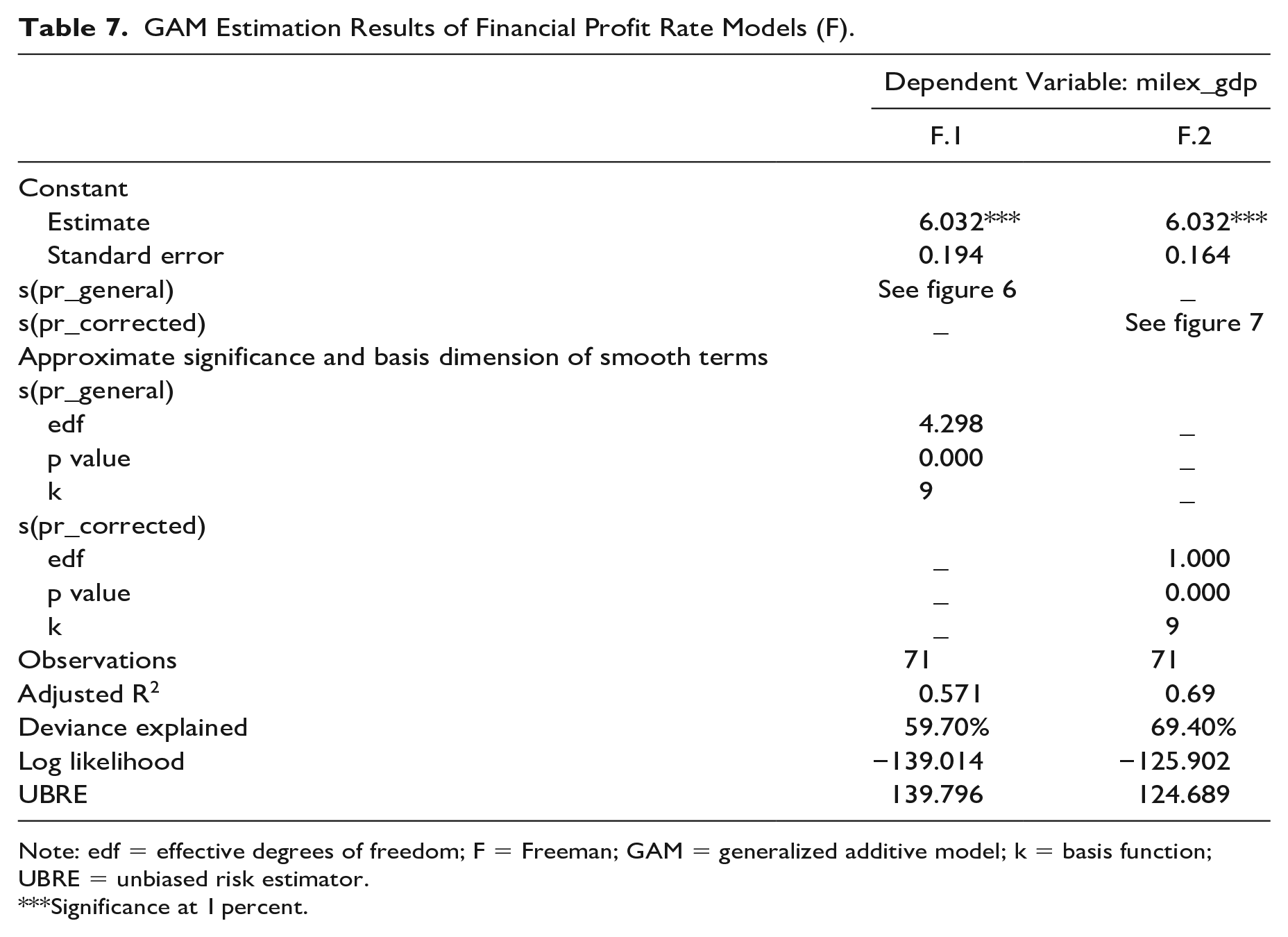

Table 7 presents the estimation results for the F.1 and F.2 models. Both smoothing splines are significant with nine basis functions. The effective degrees of freedom indicate that the general profit rates result in a wigglier curve, whereas the Freeman-corrected profit rates appear to be smooth.

GAM Estimation Results of Financial Profit Rate Models (F).

Note: edf = effective degrees of freedom; F = Freeman; GAM = generalized additive model; k = basis function; UBRE = unbiased risk estimator.

Significance at 1 percent.

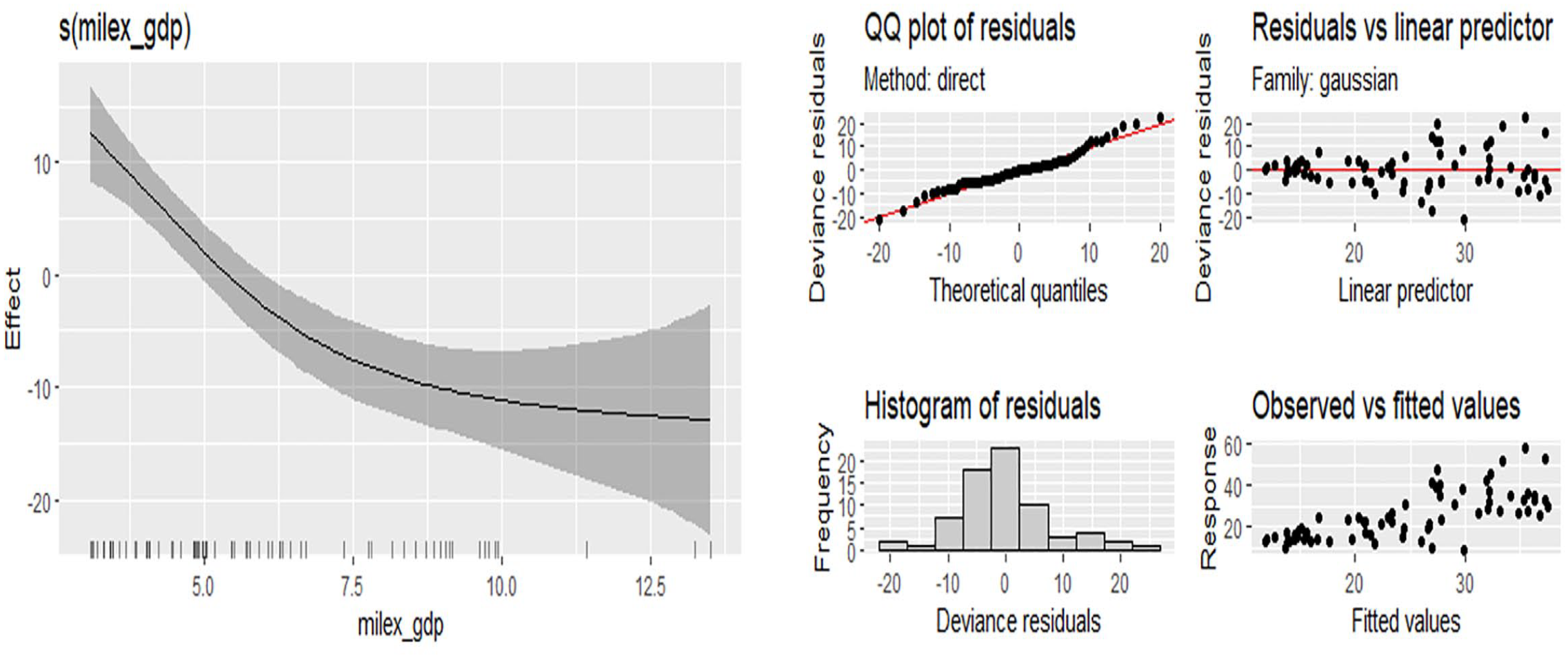

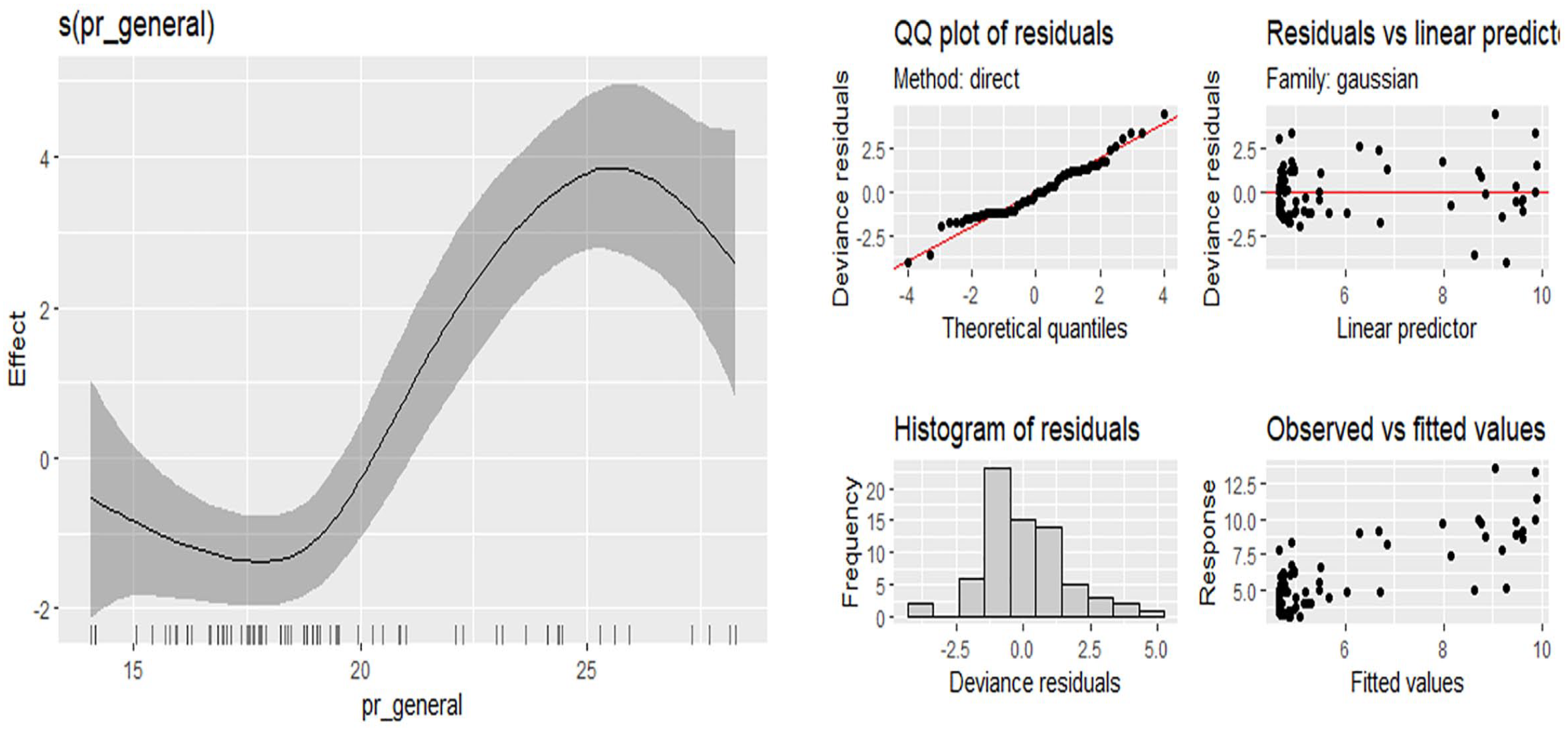

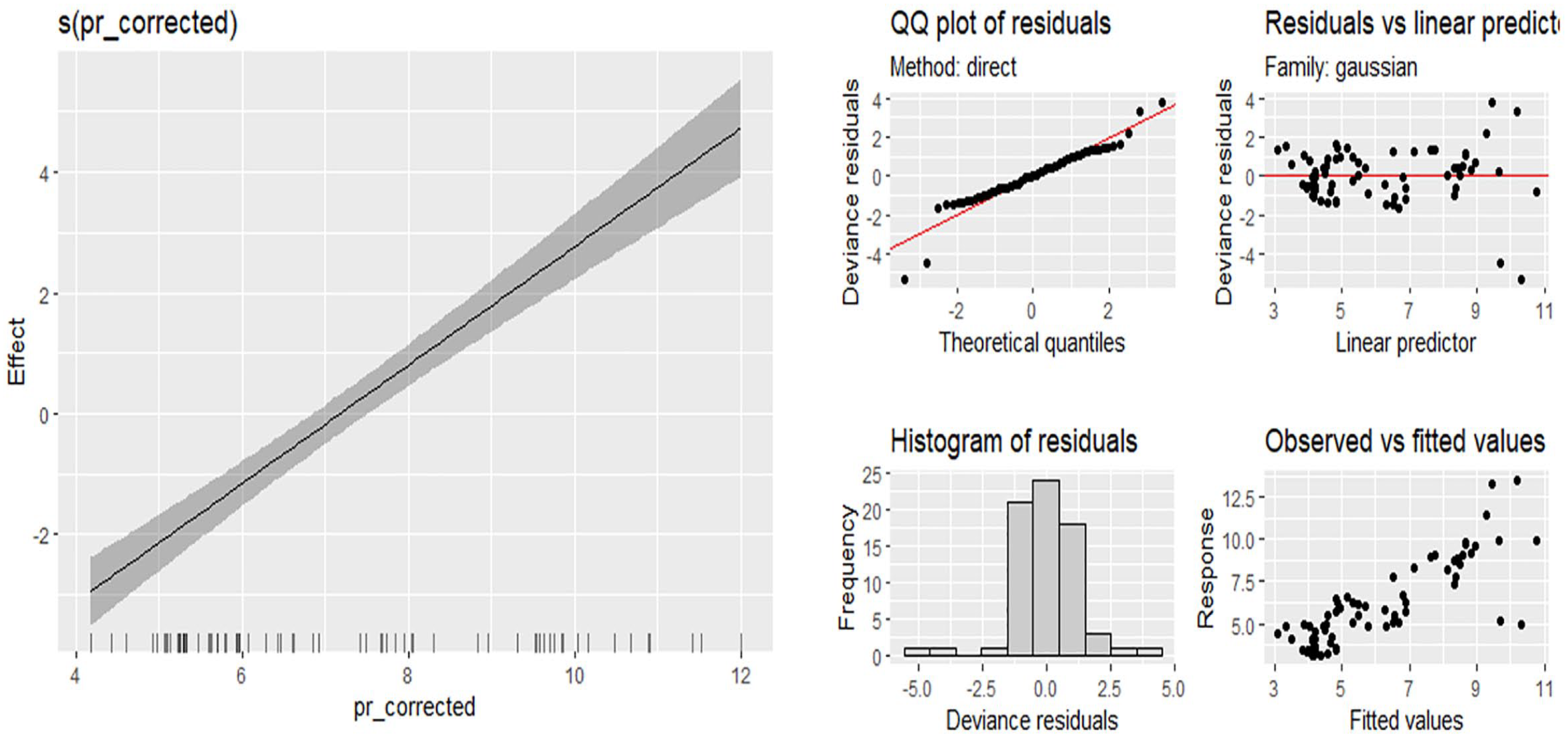

Figures 6 and 7 show the resultant smooths for the estimated F.1 and F.2 models. At the overall level,

GAM estimations for the F.1 model. (F = Freeman; GAM = generalized additive model).

GAM estimations for the F.2 model. (F = Freeman; GAM = generalized additive model).

Estimating financial profit rates using Freeman definition provides interesting results. Freeman (2012) argues that fictitious capital is also a form of capital that must be accounted for when calculating the profit rate. Our analysis is in line with his results in that the corrected profit rate calculation suggests a more coherent measure representing how the profit rates are changing with financialization. His basic hypothesis is that, after including this financial component, profit rates continued to decline after the 1980s, unlike the general profit rates used in the previous literature. He observes that “it smooths out some of the volatility in the uncorrected rate before 1982” (Freeman 2012: 178). This smoother effect is observed also in our analysis when the corrected and general profit rates are compared.

For both definitions of profit rates, the estimation results reveal a positive relationship with military expenditure as a ratio of GDP. The causal relationship is now univariate and runs from the profit rates to militarization. A couple of observations follow in conjunction with the previous financialization-militarization model. First, the graphical analysis in figure 5 shows that the military expenditure/GDP ratio tends to decline and declines more quickly than the Freeman-corrected profit rates, which include financialization. In fact, Freeman notes that the “US economy has, for the past 30–40 years, performed worse than at any time since the 1930s” (Freeman 2012: 168). The surplus shared by capitalists has been shrinking, which leads to a decline in all expense items, including military expenditure. Under these conditions, the decline in the profit rates is inevitable and may lead also to a decline in military expenditure as a ratio of GDP. Thus, the causality running from the contracted profit rates to the military expenditure as a rate of GDP can be expected.

In fact, this is consistent with our earlier observations on the acceleration of financialization. We found before that the ratio of financial profits to nonfinancial profits is negatively associated with the ratio of military expenditure to GDP while the causality was bivariate. Under the economic crisis conditions as outlined by Freeman, it is always easier to shift to unproductive sectors represented by financial instruments. Thus, when all expenditures are shrinking—including military expenditure—we may observe an escape to unproductive capital. This leads to an overall rise in the degree of financialization, measured by the ratio of financial profits to nonfinancial profits. In other words, the acceleration in financialization may be accompanied by a fall in the Freeman-corrected profit rates. The uncorrected profit rates, on the other hand, may have an erratic pattern, as shown by the nonlinear pattern observed in our model (figure 6).

This explains why Dunne, Pieroni, and D’Agostino (2013) and Elveren (2019) found that military spending has a less significant impact on the general rate of profit rate. For instance, using four different general rates of profit covering different time periods, Elveren (2019) found that only one of the rates had a significant relationship (but only at the 10 percent level) with militarization in the United States. Once again, an increase in military spending is associated with an increase in financial profits more clearly than an increase in the general rate of profit.

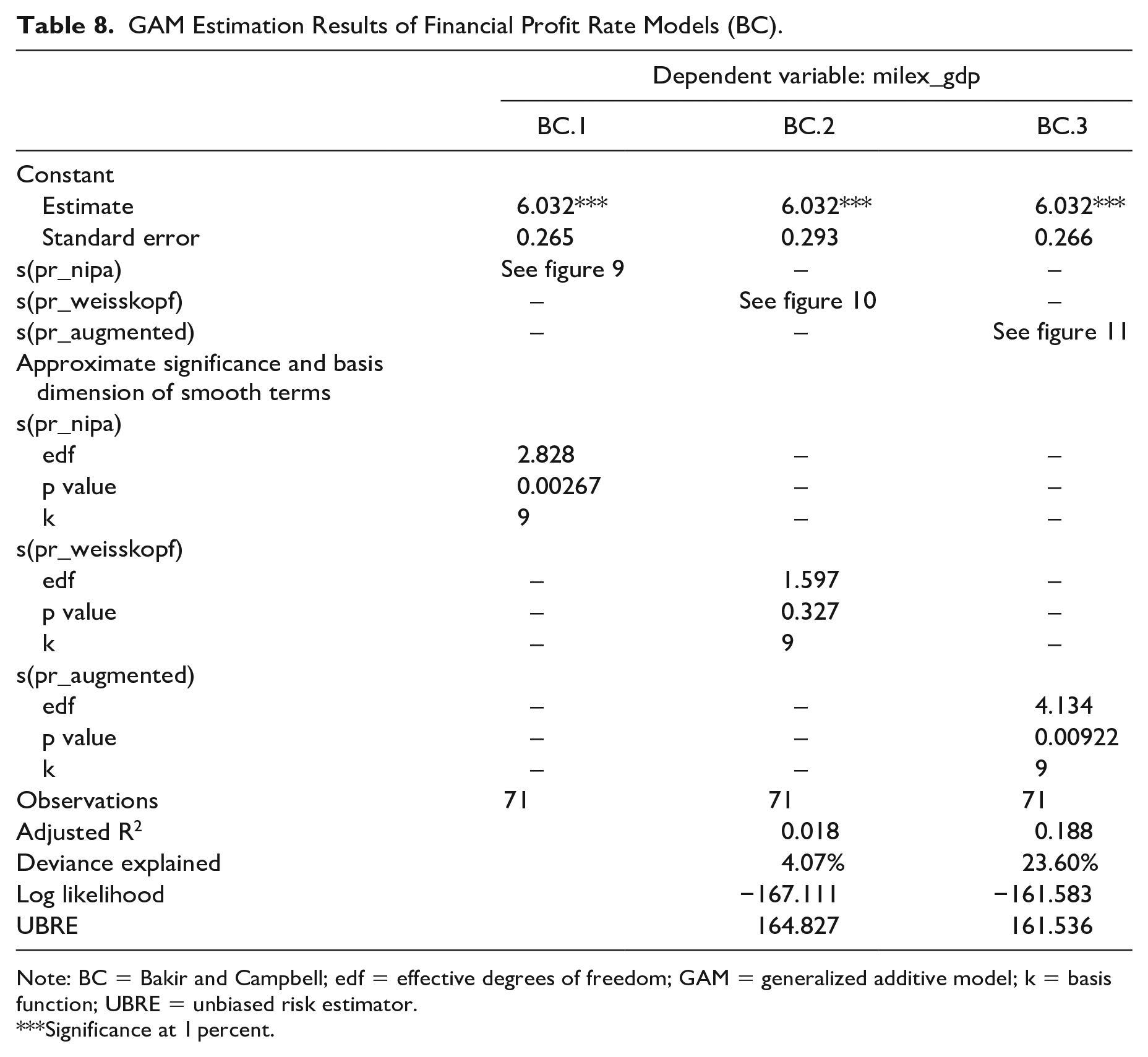

4.3. Financial profit rates in relation to militarization: Bakir and Campbell definitions

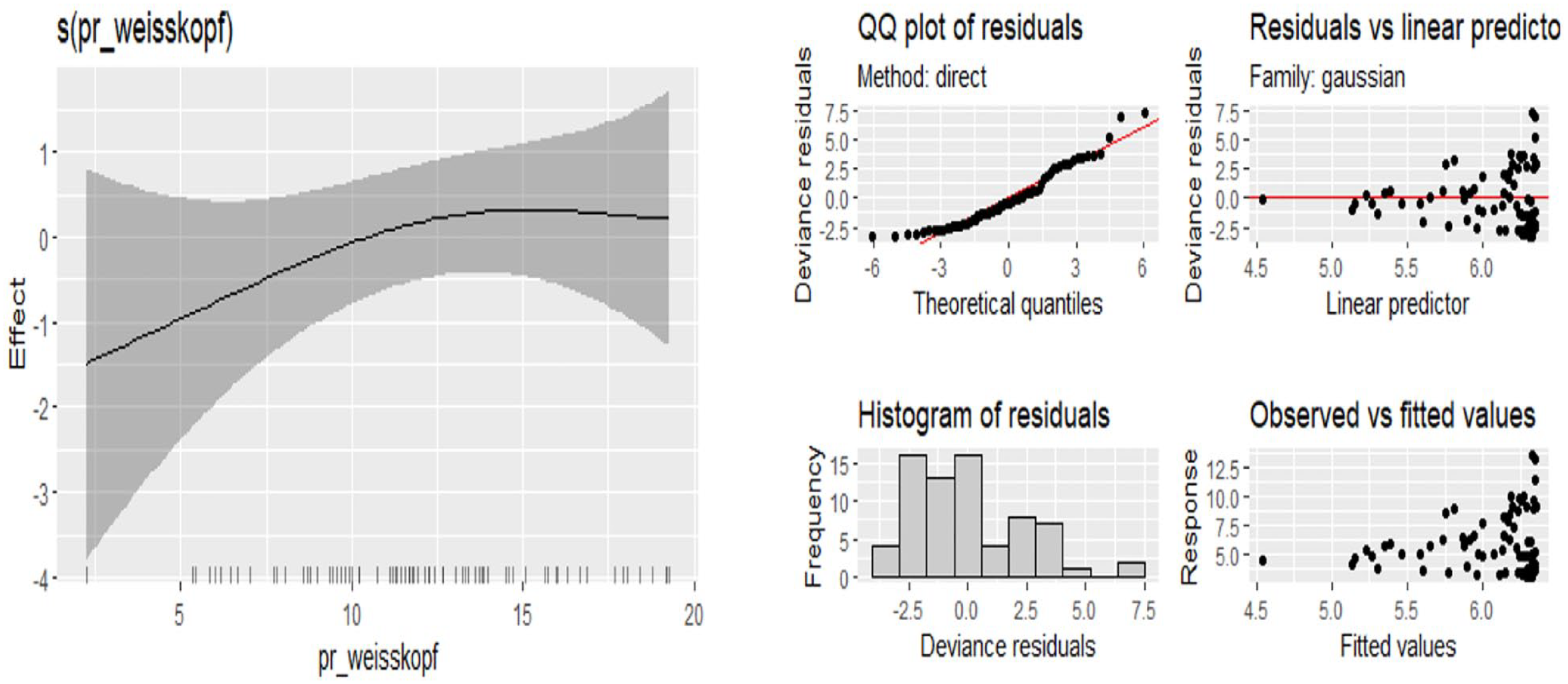

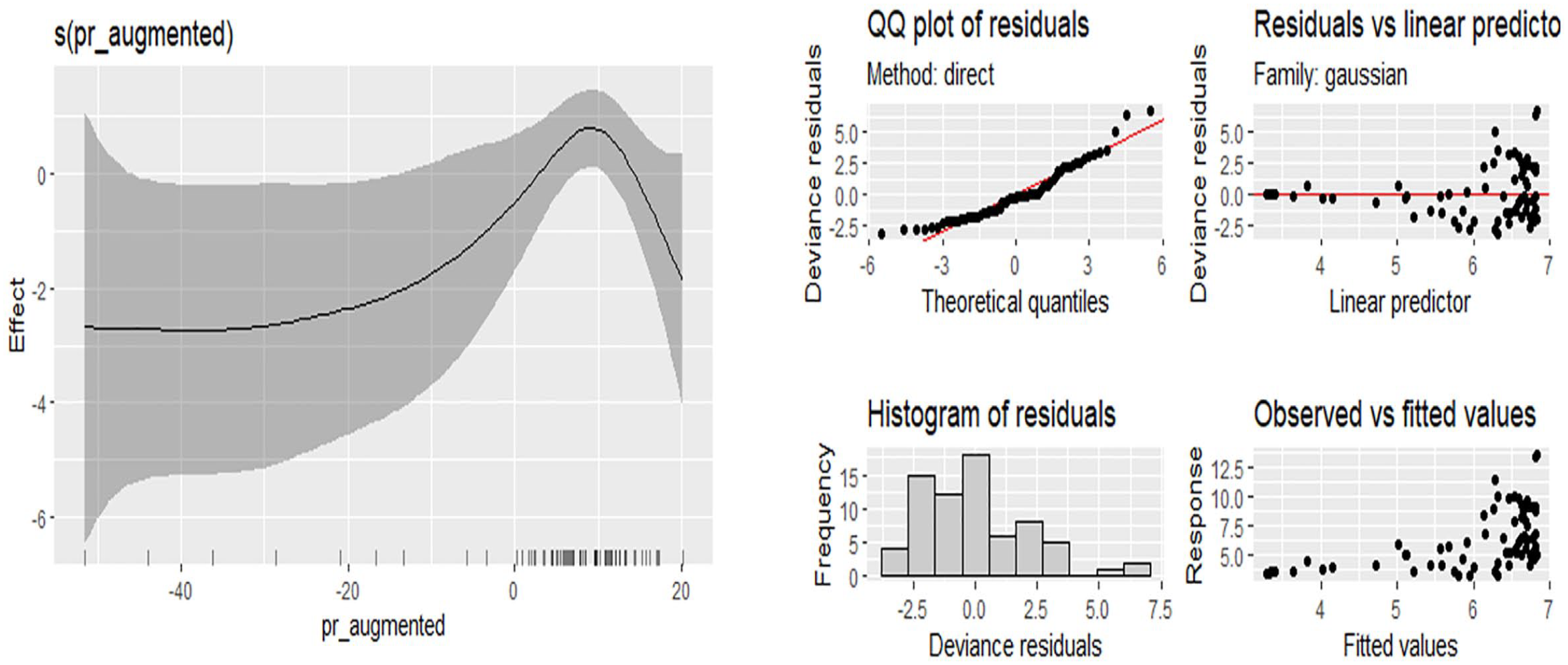

Bakir and Campbell (2013) differentiate between three types of financial profit rates: Weisskopf, NIPA, and augmented. The augmented profit rates exhibit greater volatility as they include financial earnings and capital. Figure 8 presents Bakir and Campbell (BC) financial profit rates in relation to the ratio of military expenditure to GDP. The Weisskopf rate is slightly better at tracking the augmented financial profit rates, whereas the NIPA rate is a much poorer proxy. Similar to Freeman’s discussion before, these profit rates cannot capture the declining trend when they fail to properly describe the financial components.

Financial profit rates (BC [Bakir and Campbell] definition) and militarization.

Since all three financial profit rates are nonlinear in mean (table 3), empirical Bayesian estimation method is utilized as before. We form the specifications in an analogous way to Freeman-type profit rates, not only for the sake of obtaining comparable results but also because both discuss the same underlying pattern between financial profits and militarization:

The estimation results presented in table 8 imply that the augmented profit rate model exhibits the highest wiggliness. This is because it reflects the complexity of financial components and hence has much greater volatility, as Bakir and Campbell (2013: 299) also suggest.

GAM Estimation Results of Financial Profit Rate Models (BC).

Note: BC = Bakir and Campbell; edf = effective degrees of freedom; GAM = generalized additive model; k = basis function; UBRE = unbiased risk estimator.

Significance at 1 percent.

Figures 9 to 11 present the estimated effects of financial profit rates on the military expenditure/GDP ratio. The outcomes are parallel to what we found before for the Freeman-type profit rates. At the overall level, the three BC financial profit rates are positively associated with the military expenditure/GDP ratio. However, one interesting observation follows for the augmented profit rate models. For very large values of the financial profit rates, the relationship is reversed. This actually corresponds to higher stages of financialization where an escape toward unproductive financial capital is accompanying the decline in military expenditure as a ratio of GDP. Since the NIPA and Weisskopf profit rates are poor proxies that represent the financial variables only partially, this reversal does not emerge in the BC.1 and BC.2 models.

GAM estimations for BC.1 model. (BC = Bakir and Campbell; GAM = generalized additive model).

GAM estimations for BC.2 model. (BC = Bakir and Campbell; GAM = generalized additive model).

GAM estimations for BC.3 model. (BC = Bakir and Campbell; GAM = generalized additive model).

The results of the overall empirical analysis of the financialization-militarization models explain different pieces of the theory of fictitious capital and their determination with respect to militarization. The main results can be summarized by several crucial observations. First, the graphical analyses reveal that both financial and nonfinancial profits generally rose after the neoliberal transformation. Even when nonfinancial profits declined, financial profits remained relatively stable and this rise in financial profits went hand in hand with an upsurge in military expenditure. Moreover, the degree of financialization, measured by the ratio of financial profits to nonfinancial profits, generally increased despite local deviations. Military expenditure as a share of GDP, on the other hand, declined slightly.

However, the deepening in the financial system has not always accompanied higher profitability. As the profit rate calculations of Freeman (2012) and Bakir and Campbell (2013) show, profits rates tend to decline steadily especially after accounting for financial instruments. The decline in the profit rates may have also led to a decline in all expense items, including military expenditure as a ratio of GDP. This is reflected by the negative effect of financial profit rates on the military expenditure/GDP ratio. Whenever financial profits rose during crises, military expenditure as a ratio of GDP contracted slightly as a compulsory measure. Following Arrighi (1994), we can argue that financialization and militarization are mutually affecting each other, and this relationship gets more intricate as the degree of financialization accelerates.

5. Conclusion

This study aimed to provide the first comprehensive empirical evidence on the nexus of financialization and militarization. We focused on the United States as the key country because of its hegemonic role in the world economy and politics, analyzing this relationship for 1949–2019 with respect to the argument of Arrighi (1994) that financialization and militarization are mutually reinforcing phenomena in the United States.

One key contradiction of a capitalist economy is that it must grow continuously. However, constant growth is restricted by the availability of new markets, new products, and new technologies. This inevitably leads to a decline in profitability. To prevent profit rates from further decreasing in the long term, there must be spending in the unproductive sphere of the economy. The system responded with two counteracting stimuli: the increasing volume of financialization and the growing role of the financial sector in the economy, and militarization in terms of consistently excessive military spending. However, we stressed that they may be mutually interacting rather than independent factors. The dominance of the dollar secured the US global economic hegemony as the center of global financialization. This economic power allowed it to have an excessive military budget and hundreds of military bases across the world. This, in turn, maintained the US political power, thereby securing the dollar’s hegemony.

To investigate this argument empirically, we used data on military spending and its share in GDP together with various financialization indicators including interests, dividends, and alternative definitions of financial profits. Employing nonparametric models, we provided suggestive evidence on the relationship between financialization and militarization in the United States.

First, we found significant and complex relationships between different measures of financialization and militarization. Whereas increased financialization coexists with increased military expenditure at the overall level, a more careful analysis is required for describing the acceleration of financial variables. While there were no causal relationships between military expenditure/GDP and the net interests/GDP or net dividends/GDP ratios, there was bivariate causality between the ratio of military expenditure to GDP and the ratio of financial profits to nonfinancial profits. The model estimations suggest a dialectical relation in which the rise in the degree of financialization is intertwined with a relative decline of military expenditure as a ratio of GDP.

Second, based on different financial profit variables, our results suggest that the definitions of the profit rate and whether they reflect the financial components are crucial. For instance, for very large values of augmented financial profit rates calculated by Bakir and Campbell, there exists a negative relationship with military spending. This corresponds to higher stages of financialization, where an escape toward the unproductive financial capital goes hand in hand with a decline in the military expenditure as a ratio of GDP. However, this effect cannot be captured by Weisskopf or NIPA definitions. This result also holds true for Freeman’s corrected profit rates. Here, the link with militarization is more apparent when financial instruments are included in calculating the profit rates.

Third, the results complement the findings of Dunne, Pieroni, and D’Agostino (2013), Ansari (2018), and Elveren (2019), who found that military spending increased the general rate of profit in the United States for 1949–2010, 1973–2015, and 1951–2016, respectively. The findings in this study show that military expenditure is positively associated with both the general profit rate and financial profit rate. As in the case of the profit rates of Freeman, both the general and corrected rates of profits have a causal effect on military expenditure.

Finally, our findings suggest that military expenditure is more significantly correlated with financial profit than the general (i.e., uncorrected) rate of profit as in the case of Freeman’s corrected profit rate and Bakir and Campbell’s alternative financial profit rate definitions. While corrected profit rates (i.e., financial profit) have a linear positive impact on military spending, the uncorrected profit rates show an erratic pattern. This is an important result, particularly when considered in relation to the finding that the financial profits/nonfinancial profits ratio is negatively associated with the military expenditure/GDP ratio, and the causality is bivariate. These two findings together explain why previous studies reported a less significant effect of military spending on the (general) profit rate.

We acknowledge that there are several ways to further investigate this important relationship. While the implications of our analysis are informative for the United States, it should be stressed that the techniques employed in this study can be readily extended to other major countries in the global financial system. In a similar vein, using alternative statistical methods would also provide further insights.

Footnotes

Appendix

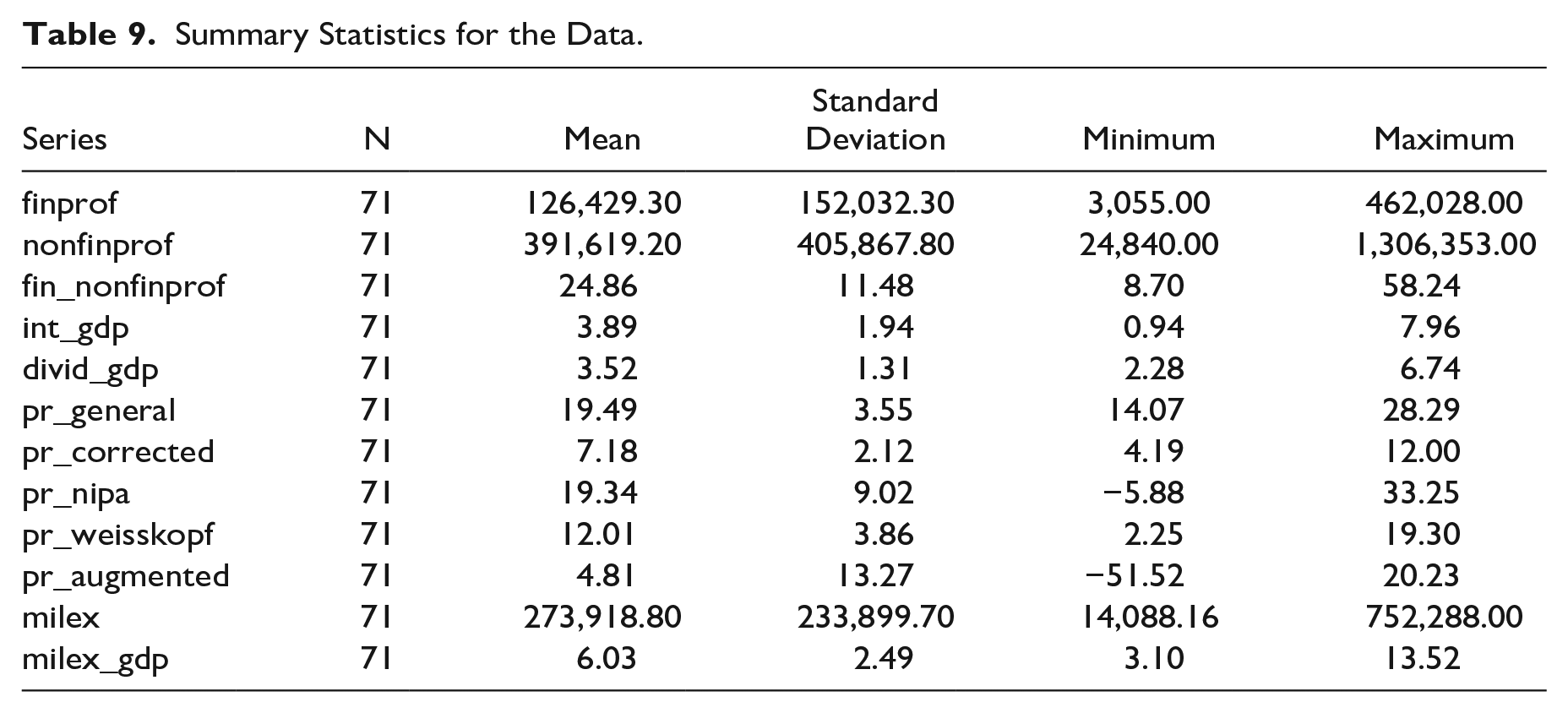

Summary Statistics for the Data.

| Series | N | Mean | Standard Deviation | Minimum | Maximum |

|---|---|---|---|---|---|

| finprof | 71 | 126,429.30 | 152,032.30 | 3,055.00 | 462,028.00 |

| nonfinprof | 71 | 391,619.20 | 405,867.80 | 24,840.00 | 1,306,353.00 |

| fin_nonfinprof | 71 | 24.86 | 11.48 | 8.70 | 58.24 |

| int_gdp | 71 | 3.89 | 1.94 | 0.94 | 7.96 |

| divid_gdp | 71 | 3.52 | 1.31 | 2.28 | 6.74 |

| pr_general | 71 | 19.49 | 3.55 | 14.07 | 28.29 |

| pr_corrected | 71 | 7.18 | 2.12 | 4.19 | 12.00 |

| pr_nipa | 71 | 19.34 | 9.02 | −5.88 | 33.25 |

| pr_weisskopf | 71 | 12.01 | 3.86 | 2.25 | 19.30 |

| pr_augmented | 71 | 4.81 | 13.27 | −51.52 | 20.23 |

| milex | 71 | 273,918.80 | 233,899.70 | 14,088.16 | 752,288.00 |

| milex_gdp | 71 | 6.03 | 2.49 | 3.10 | 13.52 |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

1

There are several comprehensive studies on financialization, e.g., Davis (2017) and ![]() .

.

2

On the other hand, Demir (2009a, 2009b, ![]() ) argued that productive sectors can, and indeed do, benefit from financialization by moving away from traditional/real sector activities toward rentier investments.

) argued that productive sectors can, and indeed do, benefit from financialization by moving away from traditional/real sector activities toward rentier investments.

3

Note that Smith (1977) challenged Baran and Sweezy’s underconsumptionist explanation of high military spending in the 1950s and 1960s in the United States. He showed that military expenditure reduces economic growth because it crowds out investment, and therefore productivity. Accordingly, for Smith, high military spending can be best explained by its strategic role in maintaining capitalism rather than its economic effect on growth. In fact, our general hypothesis is in line with Smith’s argument in that higher military spending in the United States is not solely due to its economic purposes in the domestic economy but rather due to strategic reasons to reinforce its economic power by maintaining the international capitalist order. That is, military power of the core nations sustains hegemony over peripheral capitalist countries and regulates the rivalry between core countries as well as protects social order against internal treats (Smith and Smith 1983: 43). We also acknowledge that there are different explanations of how the level of military spending is determined. For instance, similar to underconsumptionist view, for Military Keynesianism military spending is used as a countercyclical economic tool. From a long-term and institutional perspective, the military-industrial complex provides an alternative approach. Based on Veblen’s view and Baran and Sweezy’s monopoly capital, Cypher (1987) argues that military spending is an indispensable tool for the militaristic structure in the United States to divert “energies of the working class into patriotisms” (![]() : 608). Gentilucci (2019) diligently discusses some more heterodox theories to explain the high share of military budget in the United States. Among them, according to the Social Structure of Accumulation (SSA) theory, high military spending was one key element of Keynesian SSA in the post-World War II period (Kotz 1994: 66; Tabb 2010: 145; Gentilucci 2019: 609). Mampaey and Serfati (2004) argue that because of globalization, changing link between civil and military technologies, and expanding and strengthening relationship between political elites and (military) corporations, the military-industrial complex has evolved to the military-industrial system in which the concept of defense has been replaced by a much broader concept of security (Mampaey 2008; Gentilucci 2019: 610).

: 608). Gentilucci (2019) diligently discusses some more heterodox theories to explain the high share of military budget in the United States. Among them, according to the Social Structure of Accumulation (SSA) theory, high military spending was one key element of Keynesian SSA in the post-World War II period (Kotz 1994: 66; Tabb 2010: 145; Gentilucci 2019: 609). Mampaey and Serfati (2004) argue that because of globalization, changing link between civil and military technologies, and expanding and strengthening relationship between political elites and (military) corporations, the military-industrial complex has evolved to the military-industrial system in which the concept of defense has been replaced by a much broader concept of security (Mampaey 2008; Gentilucci 2019: 610).

4

We acknowledge that there are some countries, such as China, where massive financialization goes hand in hand with high rates of productive investment.

5

The predator state can be defined as the state where public institutions undermine their power and authority to serve corporate elites, boosting private profit at the expense of public interest.

6

We acknowledge that the decline of all hegemons cannot be associated with financialization.

7

After the COVID-19 outbreak at the end of 2019, overall indicators of economic performance, particularly the dynamics of financial as well as the military system were affected drastically. Hence, to uncover the true long-term relationship between financialization and militarization and to obtain robust estimates, the outlier period after 2019 is ruled out from the empirical analysis.

8

The estimations are based on military expenditures to GDP ratio rather than the level of military expenditures in constant dollars. This is because, in order to measure militarization, we are interested in the proportion of the economy that is devoted to military industries. Thus, we refrain from any indicator that may potentially contain information also about the size of the economy, and for this, we eliminate not only the inflation but also the growth effects. Since the militarization indicator is evaluated in relation to financialization, it further helps us to eliminate the possibility that the correlation of the two are due to the growth in the economy as an external determinant.

9

E.g., while Peterson and Runyan (1999: 258) define militarization as “processes by which characteristically military practices are extended into the civilian arena,” ![]() : 1) define militarism as “the social and international relations of the preparation for, and conduct of, organized political violence.”

: 1) define militarism as “the social and international relations of the preparation for, and conduct of, organized political violence.”

10

Additional covariates may sometimes have concurvity even if they are not collinear, which implies that they may behave like smooth curves of each other. For these three variables, the concurvity test values were greater than 0.6 for each pair.

11

In fact, the effect of interest rates and dividends are negligible and do not follow a causal pattern and hence their inclusion as additional covariates do not change the overall pattern between the ratio of financial to nonfinancial profits and militarization. Further estimations can be provided for the interested readers.

13

Both the Johansen trace and maximum eigenvalue test statistics show that there is cointegration between the variables

14

The estimation outcomes do not change significantly when the original data for 1949–2011 are used. The results can be provided upon request.