Abstract

This article employs a panel data econometric approach in order to empirically ascertain the role of the phenomenon of financialization in the deceleration of labor productivity in the European Union countries from 1980 to 2019. During that time, the European Union countries suffered a huge structural transformation based on Reaganomics and Thatcherism and their financial systems have experienced strong liberalization and deregulation, which have contributed to poor evolution of labor productivity and have revived fears around a new “secular stagnation” in the era of financialization. Grounded in post-Keynesian literature, the slowdown of labor productivity in the majority of developed economies in the last decades cannot be separated from the phenomenon of financialization, which has occurred through four different channels, namely, weak economic performance, the decline in the labor income share, the increase in personal income inequality, and the strengthening of the degree of financialization and its corresponding harmful effects on innovation, research and development, technological progress, and productive investments performed by nonfinancial corporations. Our findings confirm that lagged labor productivity, economic performance, and labor income share have a positive impact on labor productivity in the European Union countries, while personal income inequality and the degree of financialization impact it negatively. Our findings also reveal that labor productivity in the European Union countries in the last decades would have grown more if there had been a stronger economic performance, a smaller decline (or even a rise) of the labor income share, a smaller increase (or even a decrease) of personal income inequality, and a weakening of the degree of financialization.

Keywords

1. Introduction

Since the mid-1970s and 1980s, the majority of developed economies have engaged in Reaganomics and Thatcherism and their financial systems have experienced huge liberalization and deregulation, and these factors have contributed to a poor evolution of labor productivity and have revived the fears around a new “secular stagnation” in the era of financialization (Kus 2012; Verceli 2013; Barradas 2016; Tridico and Pariboni 2018; Pariboni, Paternesi Meloni, and Tridico 2020).

Effectively, the post-Keynesian literature tends to emphasize that the slowdown of labor productivity in the majority of developed economies in the last decades cannot be divorced from the phenomenon of financialization, which has impaired it through four different channels, namely weak economic performance, the decline in the labor income share, the increase in personal income inequality, and the strengthening of the degree of financialization and its corresponding harmful effects on innovation, research and development, technological progress, and productive investments performed by nonfinancial corporations (Tridico and Pariboni 2018; Correia and Barradas 2021).

Some of these four channels have already been tested in several econometric works (Sylos Labini 1983; Vergeer and Kleinknecht 2014; Guarini 2016; Micallef 2016; Tridico and Pariboni 2018; Carnevali et al. 2020; Yousef 2020; and Correia and Barradas 2021), although these works do not directly assess all the aforementioned four channels through which the phenomenon of financialization has undermined labor productivity. Tridico and Priboni (2018) and Correia and Barradas (2021) are the only exceptions. The former work focuses on the Organisation for Economic Cooperation and Development (OECD) countries but uses only one proxy to capture the degree of financialization (stock market capitalization) and does not consider in its estimates the potential indirect effects between the degree of financialization (the fourth channel) and economic performance (the first channel), the labor income share (the second channel), and personal income inequality (the third channel). The latter work uses five different proxies to measure the degree of financialization (credit, money supply, financial value added, stock market capitalization, and shareholder orientation) and takes into account in its estimates the potential indirect effects between the degree of financialization (the fourth channel) and economic performance (the first channel), labor income share (the second channel), and personal income inequality (the third channel) through the use of interaction terms, but it is only focused on Portugal.

This article employs a panel data econometric approach in order to empirically ascertain the role of these four channels in the deceleration of labor productivity in the EU countries from 1980 to 2019. This article offers at least five different novelties to the existing literature. First, this article assesses the role of the phenomenon of financialization in explaining the poor evolution of labor productivity in the EU countries, for which the empirical evidence is relatively scarce. The EU countries represent a very interesting case study because the majority of them have indeed experienced a slowdown of labor productivity (figure A1 in the Appendix), which has occurred simultaneously with a weak economic performance (figure A2 in the Appendix), a decline in the labor income share (figure A3 in the Appendix), an increase in personal income inequality (figure A4 in the Appendix), and a strengthening of the degree of financialization (figures A5–A8 in the Appendix). This seems to suggest that the phenomenon of financialization has played a central role in the poor evolution of labor productivity in the EU countries. Second, this article employs a panel data econometric approach, which tends to be more beneficial than cross-sectional econometric approaches and/or time series econometric approaches as it allows for the collection of more observations and larger samples with higher heterogeneity, which improves the consistency and efficiency of the produced estimates (Baltagi 2005). Vergeer and Kleinknecht (2014), Guarini (2016), Tridico and Pariboni (2018), and Carnevali et al. (2020) are examples of panel data econometric works on the determinants of labor productivity, although they do not focus directly on the EU countries and/or the majority of them do not assess all the aforementioned four channels through which the phenomenon of financialization has impaired labor productivity. Third, this article uses four different proxies to measure the degree of financialization (credit, liquid liabilities, stock market capitalization, and stock market value traded), which allows us to take into account different scopes (e.g., size, depth, and efficiency) related to the role played by the financial system (Beck, Degryse, and Kneer 2014; Breitenlechner, Gächter, and Sindermann 2015) and different scopes related to the role played by banks and financial (stock) markets to sustain the phenomenon of financialization (Barradas 2020). A similar strategy was also followed by Correia and Barradas (2021), although their econometric work is also centered on Portuguese labor productivity. Fourthly and similarly to the econometric work performed by Correia and Barradas (2021), this article also estimates a model with interaction terms in order to properly evaluate the potential indirect effects between the degree of financialization (the fourth channel) and economic performance (the first channel), the labor income share (the second channel), and personal income inequality (the third channel). Fifthly and contrary to the majority of econometric works on this matter, this article presents not only the determinants of labor productivity in the EU countries but also the respective drivers, which allows us to better identify the influence of each channel linked to the phenomenon of financialization on the poor evolution of labor productivity in the EU countries.

We estimate an aggregate equation according to which labor productivity depends on lagged labor productivity, economic performance, labor income share, personal income inequality, and degree of financialization. We employed the least-squares dummy variable bias-corrected (LSDVBC) estimator created by Nickell (1981), Bun and Kiviet (2003), Bun and Carree (2005), and Bruno (2005a, 2005b) because of the existence of an unbalanced panel, a dynamic model, and a macro panel and the need to overcome the potential endogeneity due to the omission of relevant variables and/or simultaneity among the different variables (channels).

The remainder of the article is organized as follows. Section 2 provides the theoretical and empirical literature on the relationship between the phenomenon of financialization and the slowdown of labor productivity. In section 3, we present the models to estimate labor productivity and the corresponding hypotheses. Data, stylized facts on labor productivity, and the econometric methodology are described in sections 4 and 5, respectively. In section 6, the findings are described and discussed. Finally, section 7 concludes, presents the main policy implications, and adds some suggestions for further research.

2. Labor Productivity in the Era of Financialization

The majority of the developed economies have faced a radical transformation since the mid-1970s and 1980s, particularly after the collapse of the Bretton Woods system and mainly with the administrations of Richard Nixon and Ronald Reagan in the United States and Margaret Thatcher in the United Kingdom, because of the adoption of a set of reforms and structural adjustments based on supply-side economics, liberal orientations, a laissez-faire paradigm, the abandonment of Keynesian policies and full employment goals, liberalization of trade and capital mobility, labor flexibility and weaker labor market institutions, tax competition for corporations and capital, privatizations, and retrenchments of welfare states (Kus 2012; Verceli 2013; Tridico and Pariboni 2018; Pariboni, Paternesi Meloni, and Tridico 2020). This new paradigm also implied a strong liberalization and deregulation of the financial system, apparently as a motto to promote a higher financial development and stimulate economic growth (Barradas 2016).

Against this backdrop, the financial system has gained great prominence and assumed growing dominance over the real economy and the everyday life of citizens in the most developed economies since that time, leading to a substantial transformation from a “manufacturing-driven” economy to a “finance-orientated” economy (Tomaskovic-Devey, Lin, and Meyers 2015). This has cast doubts on the sustainable nature of this new strong liberalizing and deregulatory environment, which has been fed by the higher recurrence of financial crises, a surge of financial corporate scandals and frauds, greater fragility of banking systems, lower stability of aggregate demand, and the growth of financial instability due to the corresponding rise of financial bubbles and bursts in the last decades (Rousseau and Wachtel 2011; Barajas, Chami, and Yousefi 2013; Dabla-Norris and Srivisal 2013; Tridico and Pariboni 2018). This excessive financial deepening and its negative repercussions in the economic and social spheres are commonly referred to as the phenomenon of financialization (Barradas 2016; Barradas et al. 2018).

Additionally, an important feature linked to the phenomenon of financialization has been the deceleration of labor productivity and the slowdown of economic performance in the majority of the developed economies in the last decades, which has revived fears of a new “secular stagnation” in the era of financialization (Tridico and Pariboni 2018; Pariboni, Paternesi Meloni, and Tridico 2020). This also seems to indicate that the sustained downward trend in both labor productivity and economic performance cannot be divorced from the phenomenon of financialization by refuting the conventional claims on the finance-productivity nexus and on the finance-growth nexus due to the potential positive effects of the financial system on the allocation of savings to investment and to research and development, innovation, and technological progress (Levine 1997; Dua and Garg 2019).

Effectively, the post-Keynesian literature tends to emphasize that the phenomenon of financialization has impaired labor productivity because of four different channels, namely, the weak economic performance, the decline in the labor income share, the increase in personal income inequality, and the strengthening of the degree of financialization and its corresponding harmful effects on innovation, research and development, technological progress, and productive investments performed by nonfinancial corporations (Tridico and Pariboni 2018; Correia and Barradas 2021). The first three channels are indirect channels through which the phenomenon of financialization has undermined labor productivity, and the fourth channel is a direct channel through which the phenomenon of financialization has weakened labor productivity. All of them are described thoroughly in what follows.

The first channel corresponds to an indirect effect between the phenomenon of financialization, economic performance, and labor productivity. By relying on the post-Keynesian literature, this channel states that the phenomenon of financialization has contributed to a weak economic performance, 1 which impairs labor productivity due to the so-called Smith effect (Smith 1776) or the Classical Kaldorian-Verdoorn effect (Verdoorn 1949; Kaldor 1961). These two effects consider the existence of a positive relationship between economic performance and labor productivity due to the rising returns to scale (Kaldor 1957). Sylos Labini (1983) adds that this positive relationship between economic performance and labor productivity occurs in both the short term and the long term. With regard to the short term, the author claims that a better economic performance tends to promote a more efficient use of labor, often by exploiting earlier innovations, which contributes to the growth of labor productivity. Regarding the long term, the author highlights that a better economic performance will promote the introduction of new and more efficient plants and machines to replace the existing ones, which also fosters the growth of labor productivity. Moreover, a better economic performance suggests an extension of the domestic market, which will induce a greater division of labor with workers focusing on and specializing in specific tasks, which determines the growth of labor productivity (Sylos Labini 1999; Carnevali et al. 2020).

The second channel occurs through an indirect effect between the phenomenon of financialization, labor income share, and labor productivity. Drawing on the post-Keynesian literature, this channel considers that the phenomenon of financialization has damaged the labor income share, 2 which undermines labor productivity because of the so-called Webb-Sylos Labini effect (Sylos Labini 1983, 1984, 1999) or the Marx and Hicks effect (Hein and Tarassow 2010). These effects support the existence of a positive relationship between labor income share and labor productivity because of at least six different motives. First, the positive relationship between the labor income share and labor productivity is linked with the so-called organization effect (Carnevali et al. 2020), according to which the rise of labor income share stimulates the adoption of new technologies and the reorganization of the production process in order to limit production costs by supporting the rise of production even without an increase in the number of workers and the growth of labor productivity (Webb 1912; Sylos Labini 1983, 1984, 1999; Altman 1998). Second, the positive relationship between the labor income share and labor productivity is related to the so-called wage-efficiency effect (Tridico and Pariboni 2018), according to which the rise of labor income share induces a decline of the “x-inefficiencies,” which causes an improvement in working conditions, the reinforcement of more cooperative labor relations, improved motivation, decreased levels of turnover, increased discipline and effort among workers, and a corresponding growth of labor productivity (Altman 1998). Third, the positive relationship between the labor income share and labor productivity is connected to the so-called savings effect (Altman 1998), according to which the rise of the labor income share increases the pressure to adopt new technologies and reorganize the production process, which forces high-wage corporations to increase their propensity to save in order to sustain the rise of investment, which will cause the growth of labor productivity. 3 Fourth, the positive relationship between the labor income share and labor productivity is associated with the so-called Marshall effect (Marshall 1890), according to which a rise in the labor income share attracts highly productive workers and motivates them to be more efficient by determining the growth of labor productivity (Carnevali et al. 2020). Fifth, the positive relationship between the labor income share and labor productivity is linked with the rise of market share of the most innovative corporations and the corresponding growth of labor productivity of the whole economy when there is a rise of the labor income share because routine corporations and/or laggards are thrown out of the market in a process of “natural selection” or “creative destruction” (Carnevali et al. 2020). Sixth, the positive relationship between the labor income share and labor productivity is related to countries that are characterized by “wage-led growth models” (Onaran and Obst 2016), according to which the rise of labor income share is beneficial to the economic performance by supporting the growth of labor productivity in these countries through the aforementioned Smith effect (Smith 1776) or Classical Kaldorian-Verdoorn effect (Verdoorn 1949; Kaldor 1961).

The third channel relates to an indirect effect between the phenomenon of financialization, personal income inequality, and labor productivity. Based on the post-Keynesian literature, this channel states that the phenomenon of financialization has caused an increase in personal income inequality, 4 which weakens labor productivity because workers put less effort into their jobs (Tridico and Pariboni 2018) because of their increased vulnerability and reduced confidence in job stability in the labor market (Vergeer and Kleinknecht 2014) in the face of more unstable and precarious jobs, higher flexibility, scarcer incentives, and lower-paid jobs (Pariboni and Tridico 2020). Against this backdrop, the majority of workers, but particularly unskilled or low-skilled ones, feel less encouraged to invest in training and education in order to upgrade their skills, which also impairs labor productivity (Pariboni and Tridico 2020). Note that the increase in personal income inequality, the decline of the labor income share, the weak economic performance, and the slowdown of labor productivity have been stylized facts in the era of financialization, particularly because of the abandonment of Keynesian policies and full employment goals, the emergence of a paradigm based on “shareholder value orientation,” an excessive focus on short-term profits, the proliferation of multinational corporations that reallocate their production to low-wage countries, the deregulation and flexibilization of labor markets (at the level of unemployment benefits, employment protection, employment rights, and minimum wage), the propagation of practices such as outsourcing, the increase of precarious labor conditions, and the deterioration of workers’ bargaining power (Tridico and Pariboni 2018).

The fourth channel is associated with a direct effect between the phenomenon of financialization and labor productivity. Grounded in the post-Keynesian literature, this channel considers that the phenomenon of financialization has been harmful to innovation, research and development, technological progress, and productive investments performed by nonfinancial corporations, 5 which directly reduces labor productivity (Hein 2010). This negative relationship between the phenomenon of financialization and innovation, research and development, technological progress, and productive investments realized by nonfinancial corporations could be explained by two different motives. First, the phenomenon of financialization has instigated a rise of financial investments made by nonfinancial corporations, which diverts funds from innovation, research and development, technological progress, and productive investments and compromises the growth of labor productivity. This “crowding-out effect” or “management preference channel” (Hein 2012) has been exacerbated by the existence of shorter planning horizons and the corresponding “managerial myopia” (Crotty 2005; Samuel 2000); an excessive focus on short-term profits (so-called rent-seeking behavior) instead of long-term expansion (Orhangazi 2008); the decreasing trend of profits in productive activities and the increasing trend of external funding costs since the mid-1980s (Crotty 2005; Orhangazi 2008; Baud and Durand 2012); the rise of macroeconomic uncertainty and heightened risks (Akkemik and Özen 2014); the learning process with other nonfinancial corporations (so-called mimetic behavior); and the strong influence of some agents (e.g., financial executives or independent consultants) concerning the advantages of higher engagement in financial activities (Soener 2015). Second, the phenomenon of financialization has instigated lower retention ratios because of the strong pressures exerted by shareholders over nonfinancial corporations to increase their financial payments (e.g., interest, dividends, stock buybacks), which decreases the funds available for innovation, research and development, technological progress, and productive investments and compromises the growth of labor productivity. This “profit without investment” hypothesis or “internal means of finance channel” (Stockhammer 2006; Hein 2012; Cordonnier and Van de Velde 2015) has been exacerbated by the “principle of increasing risk” and the corresponding difficulty of accessing external funding in the presence of imperfect capital markets (Kalecki 1937; Hein 2010); the higher levels of indebtedness exhibited by nonfinancial corporations (Orhangazi 2008); the proliferation of remuneration schemes based on profits (Orhangazi 2008); the increasing significance of institutional investors (Orhangazi, 2008); and the excessive focus on the primacy of shareholder value (so-called shareholder value orientation) by underestimating other corporations’ stakeholders (Lazonick and O’Sullivan, 2000).

From an empirical point of view, we identify in the existing literature several econometric works that address the determinants of labor productivity, namely, Sylos Labini (1983), Fortune (1987), Vergeer and Kleinknecht (2014), Guarini (2016), Micallef (2016), Tridico and Pariboni (2018), Dua and Garg (2019), Pariboni and Tridico (2020), Carnevali et al. (2020), Yousef (2020), and Correia and Barradas (2021). Nevertheless, the majority of these econometric works face at least one important flaw because they do not consider the aforementioned four channels through which the phenomenon of financialization has slowed down labor productivity in the majority of the developed countries. This increases the risk that their results could be biased and inconsistent because several relevant variables are clearly omitted (Baltagi, 2005). The econometric works performed by Tridico and Pariboni (2018) and Correia and Barradas (2021) are the only two exceptions. The former conducts a panel data econometric analysis for 26 countries of the OECD (Australia, Austria, Belgium, Canada, Chile, Denmark, Finland, France, Germany, Greece, Iceland, Israel, Italy, Japan, Luxembourg, Mexico, New Zealand, Norway, Portugal, Republic of Korea, Spain, Sweden, Switzerland, the Netherlands, the United Kingdom, and the United States) from 1990 to 2013, and the latter performs a time series econometric analysis for Portugal from 1980 to 2017. Nonetheless, the former applies only one proxy to capture the degree of financialization (stock market capitalization) and does not consider in its estimates the potential indirect effects between the degree of financialization (the fourth channel) and economic performance (the first channel), the labor income share (the second channel), and personal income inequality (the third channel). The latter uses five different proxies to measure the degree of financialization (credit, money supply, financial value added, stock market capitalization, and shareholder orientation) and employs interaction terms in its estimates in order to take into consideration the potential indirect effects between the degree of financialization (the fourth channel) and economic performance (the first channel), the labor income share (the second channel), and personal income inequality (the third channel). Both of these econometric works find that economic performance and labor income share exert a positive impact on labor productivity, while personal income inequality and the degree of financialization exert a negative impact on labor productivity. Sylos Labini (1983) for the United States and Italy, Guarini (2016) for thirty European countries (Austria, Belgium, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Lithuania, Luxemburg, Macedonia, Malta, Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, Switzerland, and the United Kingdom), and Carnevali et al. (2020) for eight euro-area countries (Austria, France, Greece, Germany, Italy, the Netherlands, Portugal, and Spain) also conclude that economic performance impacts labor productivity positively. Vergeer and Kleinknecht (2014) for twenty OECD countries (Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Spain, Sweden, Switzerland, the United Kingdom, and the United States) and Carnevali et al. (2020) and Yousef (2020) for Jordan also find that labor income share exerts a positive effect on labor productivity.

Similarly to the econometric works carried out by Tridico and Pariboni (2018) and Correia and Barradas (2021), this article aims to assess the role of the phenomenon of financialization in labor productivity by performing a panel data econometric work for all the EU countries from 1980 to 2019.

3. Models and Hypotheses

Our model to estimate labor productivity is an extension of the model presented by Sylos Labini (1983, 1984, 1999) and by Tridico and Pariboni (2018), according to which labor productivity depends on the aforementioned four channels through which the phenomenon of financialization has impaired the evolution of labor productivity in the majority of the developed economies in the last decades.

Against this backdrop, our model to estimate labor productivity includes five independent variables, namely, lagged labor productivity, economic performance, labor income share, personal income inequality, and degree of financialization. 6 The inclusion of lagged labor productivity among the independent variables aims to control for state dependency and to assess the degree of persistence and inertia shown by labor productivity (Vergeer and Kleinknecht 2014).

Our model to estimate labor productivity assumes the following configuration:

where i is the country, t is the time period (year), LP is labor productivity, EP is economic performance, LIS is the labor income share, PII is personal income inequality, DF is the degree of financialization, and α is the two-way error term component to account for unobservable country-specific effects and time-specific effects.

Our hypotheses assume that lagged labor productivity, economic performance, and labor income share should positively impact labor productivity, whereas personal income inequality and degree of financialization should negatively impact labor productivity. Our estimated coefficients should exhibit the following signs:

We also present a second model to estimate labor productivity by including three interaction terms between the degree of financialization and economic performance, the degree of financialization and labor income share, and the degree of financialization and personal income inequality. This model, similar to the one proposed by Correia and Barradas (2021), aims to better assess the aforementioned three indirect effects through which the phenomenon of financialization has undermined the evolution of labor productivity.

Our second model to estimate labor productivity assumes the following configuration:

According to our second model to estimate labor productivity, the impact of economic performance, labor income share, and personal income inequality on labor productivity depends linearly on the degree of financialization, that is:

Here, β2, β4, and β6 measure the impact of economic performance, labor income share, and personal income inequality on labor productivity if the degree of financialization is zero. In that situation, economic performance and labor income share should positively impact labor productivity, whereas personal income inequality should negatively impact labor productivity. At different (positive and higher) values of the degree of financialization, the impact of economic performance, labor income share, and personal income inequality on labor productivity tends to be lower because of the arguments described previously according to which the phenomenon of financialization has favored a weak economic performance, a decline in the labor income share, and an increase in personal income inequality by impairing labor productivity. Our estimated coefficients should exhibit the following signs:

Our two models to estimate labor productivity represent an aggregate equation to assess the extent to which the phenomenon of financialization has contributed to the decline of labor productivity in the EU countries in the last few decades. Our macroeconomic approach introduces at least two important flaws in our analysis. On the one hand, we cannot assess the role of the phenomenon of financialization in the slowdown of labor productivity in different corporations, sectors, industries, and/or regions. On the other hand, we cannot assess the role of the phenomenon of financialization in the slowdown of labor productivity in the different countries, namely, because we are dealing with a panel data econometric work that produces estimates that represent an average effect of the phenomenon of financialization on labor productivity for all the EU countries as a whole. Nonetheless, our macroeconomic approach allows us to assess the general macroeconomic effect of the phenomenon of financialization on the decline of labor productivity in the EU countries. Against this backdrop, if the aforementioned four channels linked to the phenomenon of financialization are proved to impact labor productivity in the EU countries, we cannot assess whether their impact affects only some corporations, sectors, industries, regions, and/or countries or affects all corporations, sectors, industries, regions, and/or countries indifferently. If the aforementioned four channels related to the phenomenon of financialization are proved to not impact labor productivity in the EU countries, we cannot assess whether their impact affects some corporations, sectors, industries, and/or countries but not enough to generate a global impact in all corporations, sectors, industries, regions, and/or countries.

4. Data Set and Stylized Facts on Labor Productivity

We collected annual data from 1980 to 2019 for all the EU countries, constituting a panel dataset composed of a total of twenty-eight cross-sectional units (N = 28) observed over time (T = 40). 7 This represents the span and the frequency for which all data are available. Note that the proxy for personal income inequality is only available on a yearly basis from 1980 to 2019.

Because of the natural complexity related to the phenomenon of financialization, we used four different variables to measure the degree of financialization, namely credit, liquid liabilities, stock market capitalization, and stock market value traded. On the one hand, these four variables reflect different scopes related to the role played by the financial system, namely, its size, depth, and efficiency (Beck, Degryse, and Kneer 2014; Breitenlechner, Gächter, and Sindermann 2015). On the other hand, these four variables reflect different scopes related to the role played by banks and by financial (stock) markets to sustain the phenomenon of financialization (Barradas, 2020). Credit and liquid liabilities are more connected to the role played by the banking system, while the stock market capitalization and the stock market value traded are more linked to financial (stock) markets. These four proxies are used separately from each other in order to avoid multicollinearity problems and to confirm the robustness of our results to the proxy chosen.

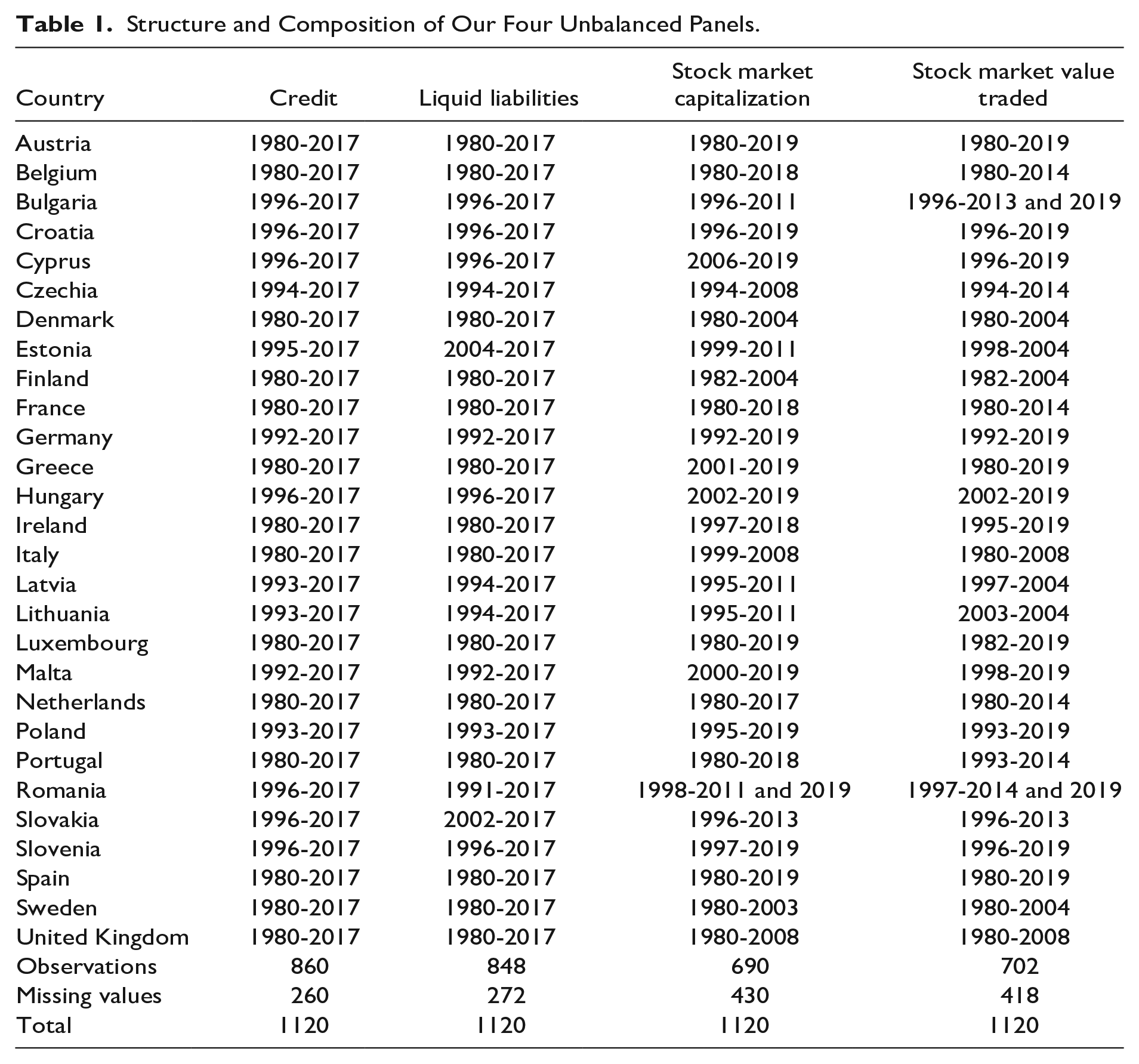

Nonetheless, the available data differ slightly according to each proxy for the degree of financialization, although for each of them there is not data available for all the years for each country. Thus, and in order to maximize the number of observations and to minimize the number of missing values, four unbalanced panels were created. Table 1 describes the structure and composition of our four unbalanced panels.

Structure and Composition of Our Four Unbalanced Panels.

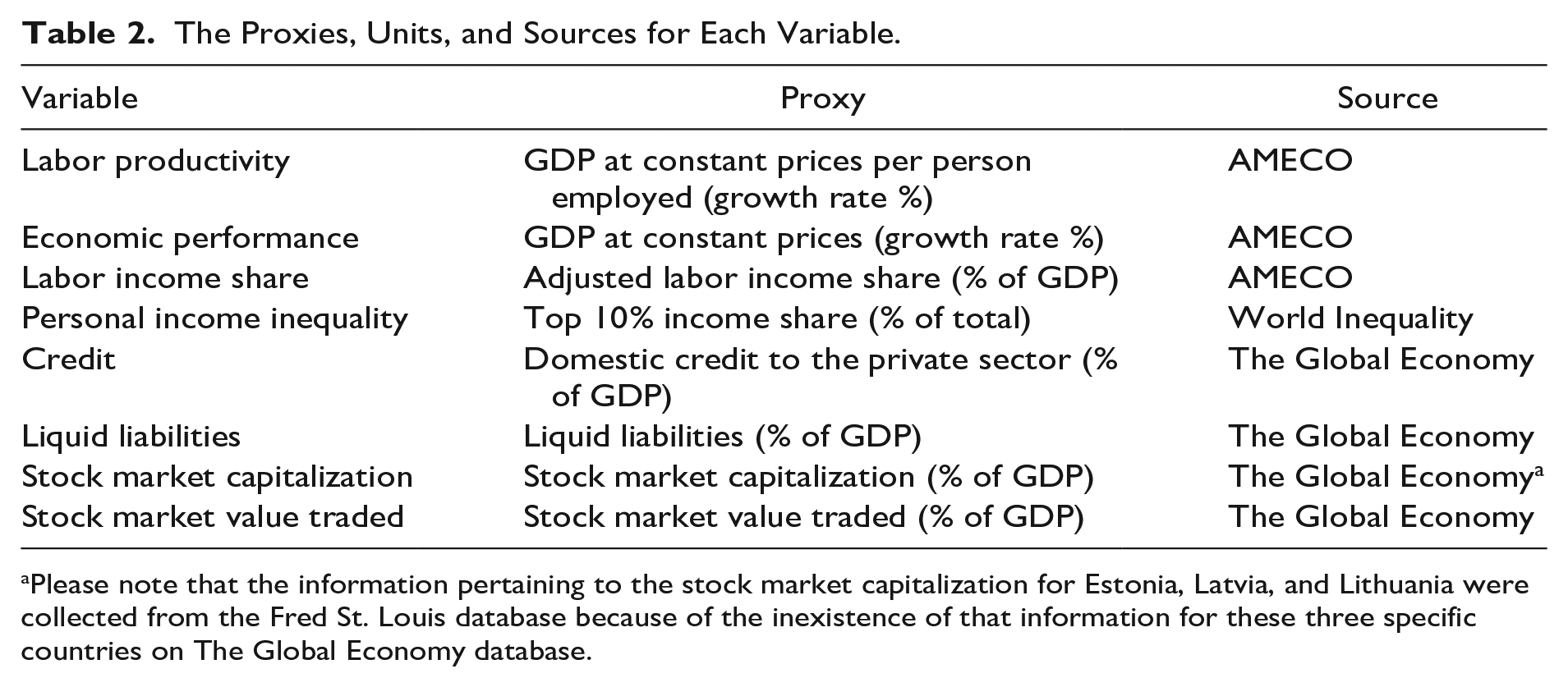

In what follows, we describe definitions, units, and sources for each variable. Labor productivity corresponds to the growth rate of the GDP at constant prices per person employed, available in the Eurostat database. Economic performance is quantified through the growth rate of the GDP at constant prices, from the Eurostat database. The labor income share corresponds to the adjusted labor share, that is, the ratio of the compensation of employees per employee to the GDP at current market prices per employee, available in the AMECO database. 8 The personal income inequality is proxied through the top 10 percent income share, available in the World Inequality database. Credit is assessed by the domestic credit to the private sector in percentage of the GDP at current prices, which was collected from the Global Economy database. Liquid liabilities correspond to the broad money in percentage of the GDP at current prices, extracted directly from the Global Economy database. 9 The stock market capitalization is assessed through the total value of all listed shares in the Portuguese stock market in percentage of the GDP at current prices, available in the Global Economy database. The stock market value traded is measured through the total value of all traded shares in the Portuguese stock market in percentage of the GDP at current prices, from the Global Economy database. Table 2 exhibits proxies, units, and sources for each variable.

The Proxies, Units, and Sources for Each Variable.

Please note that the information pertaining to the stock market capitalization for Estonia, Latvia, and Lithuania were collected from the Fred St. Louis database because of the inexistence of that information for these three specific countries on The Global Economy database.

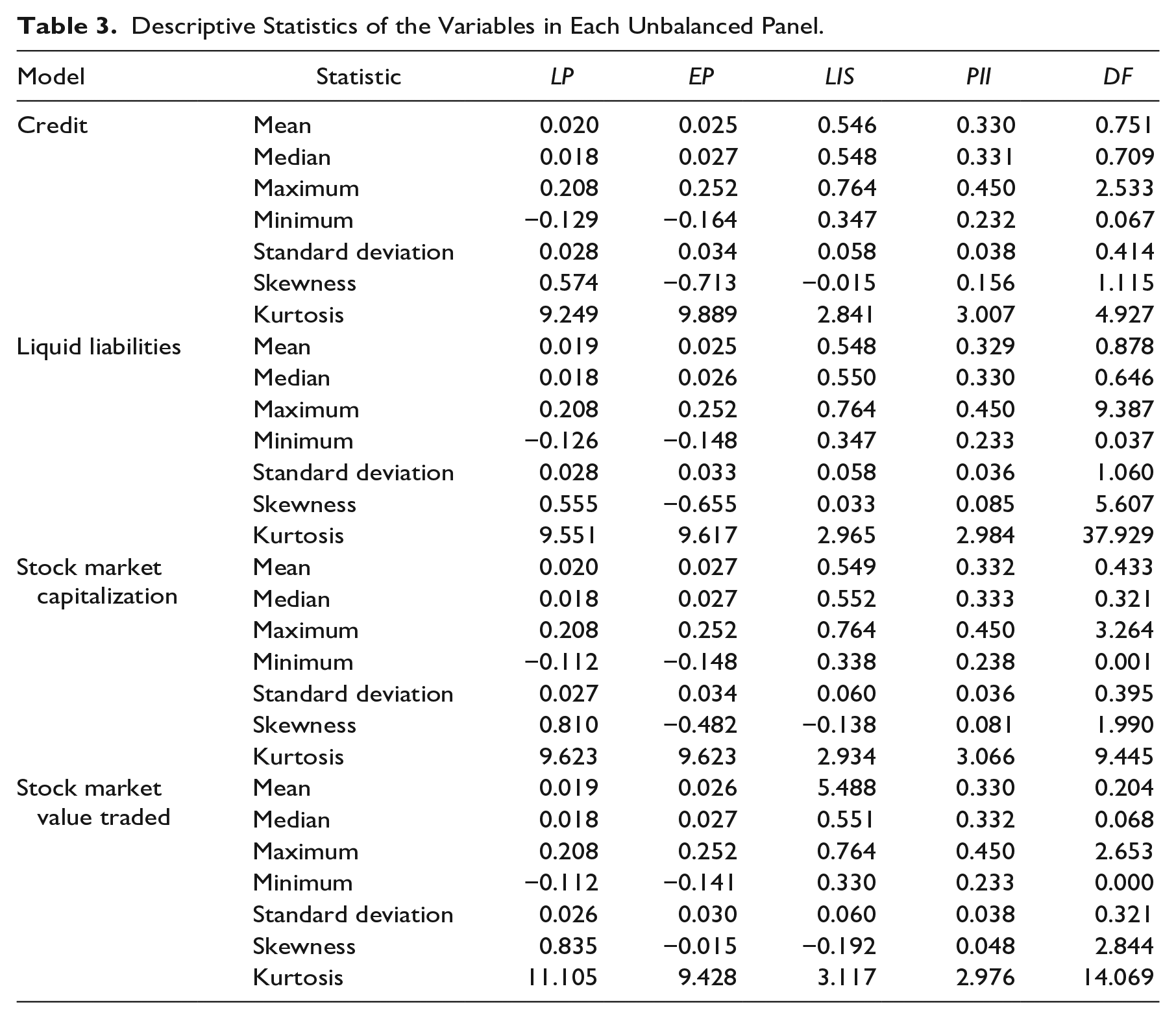

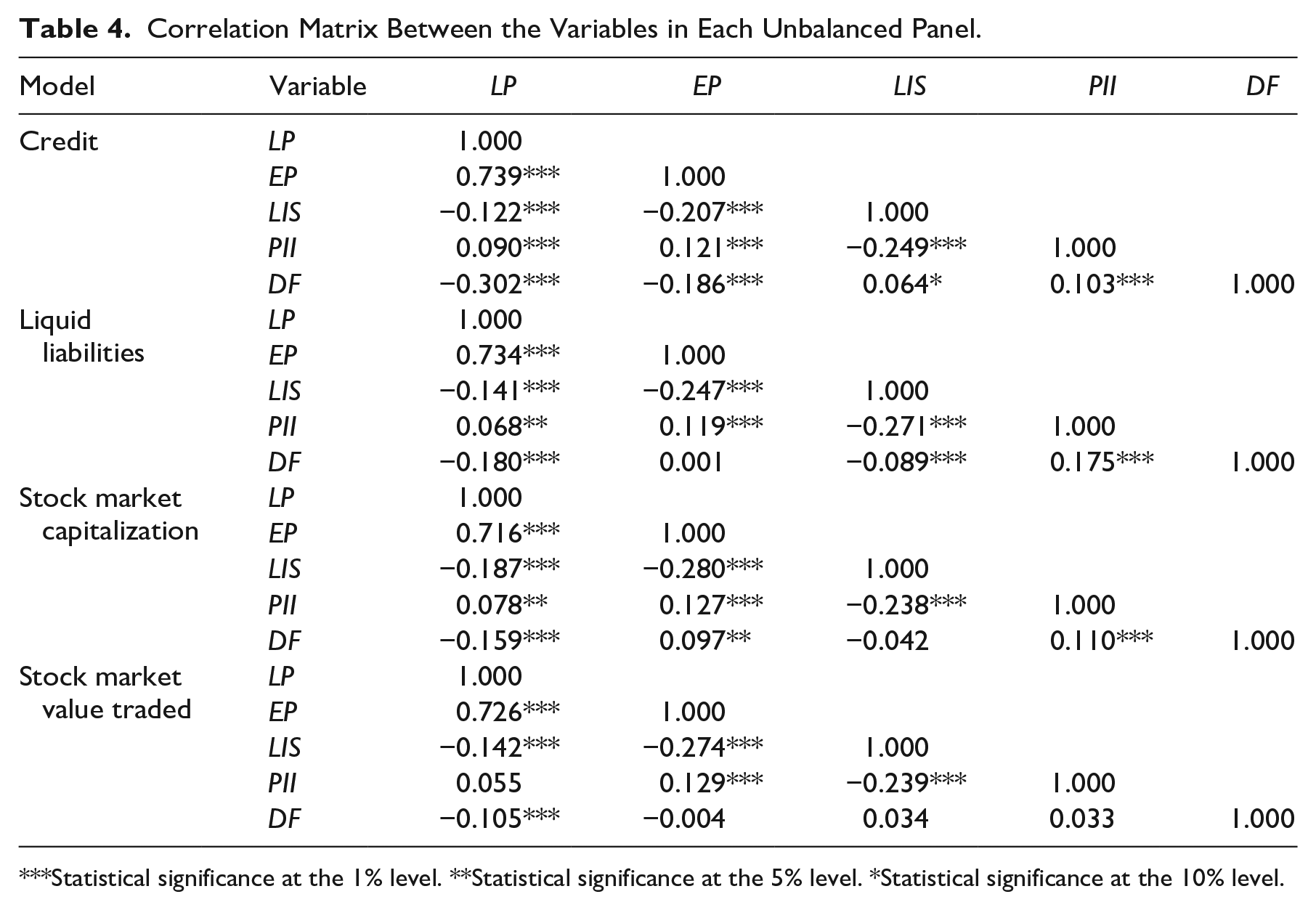

Table 3 includes the descriptive statistics of each variable in each unbalanced panel, table 4 contains the correlation matrix between all the variables in each unbalanced panel, and figures A1 to A8 in the Appendix show the plots of each variable.

Descriptive Statistics of the Variables in Each Unbalanced Panel.

Correlation Matrix Between the Variables in Each Unbalanced Panel.

Statistical significance at the 1% level. **Statistical significance at the 5% level. *Statistical significance at the 10% level.

All correlations between the variables in each unbalanced panel are less than 0.8 in absolute terms, which disproves the hypothesis on the existence of multicollinearity among them (Studenmund 2005). We also confirm that labor productivity has exhibited a timid growth of around 2 percent on average in the EU countries from 1980 and 2019 (table 2), in a context where its slowing down has been a stylized fact in the majority of EU countries (figure A1 in the Appendix). Similarly, the weak economic performance, the decline in the labor income share, the increase in personal income inequality, and the strengthening of the degree of financialization have also been stylized facts in the majority of EU countries in the last decades (figures A2–A8 in the Appendix), which suggests that the aforementioned four channels through which the phenomenon of financialization has made labor productivity sluggish has also occurred in the case of the EU countries.

It also important to note that the slowdown of labor productivity is a general phenomenon occurring across the majority of the EU countries, independently of their types of financial systems. 10 Effectively, the sustained downward trend in labor productivity has been especially more evident in Austria, Portugal, and Spain (“bank-based” countries); in Belgium, France, and the United Kingdom (“market-based” countries); in Croatia, Estonia, Poland, Slovakia, and Slovenia (Eastern European countries); and in Cyprus and Luxembourg (the outlier countries). In the remaining countries, labor productivity has maintained a steadier growth from 1980 to 2019, although it is also quite anemic. During that time, countries where the labor productivity exhibited lower growth rates included Cyprus (outlier country), Germany (“bank-based” country), Greece (“bank-based” country), Italy (“bank-based” country), Luxembourg (outlier country), and the Netherlands (“market-based” country), with growth rates of approximately 1.1 percent, 0.9 percent, 0.2 percent, 0.9 percent, 1.2 percent, and 1.2 percent on average, respectively. This seems to confirm that the disruptive relationship between the phenomenon of financialization and the deceleration of labor productivity has been common to all the EU countries, independently of their institutional specificities in terms of the different types of financial systems. This is not overly surprising due to the general recognition that all these types of financial systems have been ineffective at promoting productive investments, economic growth, and, consequently, labor productivity in the era of financialization (Levine 2002; Sawyer 2015; Barradas 2017).

5. Econometric Methodology

Our econometric methodology involves the implementation of the LSDVBC estimator proposed by Nickell (1981), Bun and Kiviet (2003), and Bun and Carree (2005) and extended by Bruno (2005a, 2005b) for the specific case of unbalanced panels. Stata software is used to produce our estimates by employing the “xtlsdvc” routine.

This particular estimator was chosen for four different reasons, which are directly related to the characteristics of our four panels (unbalanced, dynamic, and macro panels) and the need to deal with the potential problem of endogeneity. On the one hand, our four panels described previously are indeed unbalanced because of the existence of some missing values because it was not possible to collect data for all the variables for all the years for each country, are also dynamic because of the inclusion of lagged labor productivity among the independent variables, and are also macro because of the relatively small number of cross-sectional units (countries). On the other hand, we need to take into account the hypothetical existence of endogeneity for two different reasons, namely, the omission of the aforementioned “Ricardo effect” (Ricardo 1821) and/or other relevant variables not directly or indirectly linked to the phenomenon of financialization but that are typically used in some econometric works on this subject (Fortune 1987; Vergeer and Kleinknecht 2014; Guarini 2016; Micallef 2016; Dua and Garg 2019; Carnevali et al. 2020; Pariboni and Tridico 2020; Yousef 2020) and the possibility of simultaneity among our variables (Vergeer and Kleinknecht 2014; Carnevali et al. 2020).

In what follows, we describe the four reasons that explain our choice to implement the LSDVBC estimator. First, the conventional panel data estimators (e.g., pooled ordinary least squares, least-squares dummy variables, fixed effects, and random effects) do not produce unbiased and consistent estimates in the case of dynamic panel data models, particularly because the lagged dependent variable is correlated with fixed effects in the error term component (Nickell 1981; Baltagi 2005). Second, the conventional panel data estimators for dynamic panel data models (e.g., Anderson and Hsiao 1982; Arrellano and Bond 1991; Arrellano and Bover 1995; Blundell and Bond 1998) also do not produce unbiased and consistent estimates in the case of macro panels with a relatively small number of cross-sectional units (Bruno 2005a, 2005b). Anderson and Hsiao (1982) follow an instrumental variable approach by transforming the model in first differences to remove the constant term and the individual effects in order to obtain consistent estimates, but their estimates are not necessarily efficient because this methodology does not use all the available moment conditions (Holtz-Eakin, Newey, and Rosen 1988; Ahn and Schmidt 1995; Batalgi 2005). Arrellano and Bond (1991) use the generalized method of moments (GMM) estimator proposed by Hansen (1982), based on the first differences of the respective model (so-called difference GMM), which implies the use of more instruments that tend to contribute to increasing its efficiency in comparison to Anderson and Hsiao (1982). Nevertheless, this estimator magnifies gaps in the case of unbalanced panels (Roodman 2009). Arrellano and Bover (1995) and Blundell and Bond (1998) still allow the incorporation of more instruments (the lagged levels and the lagged differences) (so-called system GMM), but they also minimize the sample size in the case of unbalanced panels (Roodman 2009). Third, the Monte Carlo simulations show that the LSDVBC estimator outperforms the aforementioned estimators in terms of efficiency and consistency in the case of macro panels (Kiviet 1995; Judson and Owen 1999; Bruno 2005a, 2005b). Fourth, the Monte Carlo simulations also show that the LSDVBC estimator performs reasonably well in terms of efficiency and consistency even in the presence of endogeneity (Behr 2003).

The LSDVBC works in two different steps in order to produce the corresponding estimates (Bruno 2005a, 2005b). In the first one, the LSDVBC estimator produces consistent estimates by requiring an initial matrix of starting values to be defined through the implementation of one of three consistent estimators, namely, Anderson and Hsiao (1982), Arrellano and Bond (1991), and Blundell and Bond (1998). In the second one, the LSDVBC estimator corrects the bias by performing several multiple replications to bootstrap the standard errors. Nevertheless, the choices in the aforementioned two steps related to the consistent estimator and the number of replications do not affect the estimates produced by the LSDVBC estimators in terms of statistical significance and/or signs (Bun and Kiviet 2003; Bruno 2005a, 2005b). In order to produce our estimates for labor productivity in the EU countries, Arrellano and Bond’s (1991) estimator was employed in the first stage and a number of replications equal to 250 was used in the second stage.

6. Results and Discussion

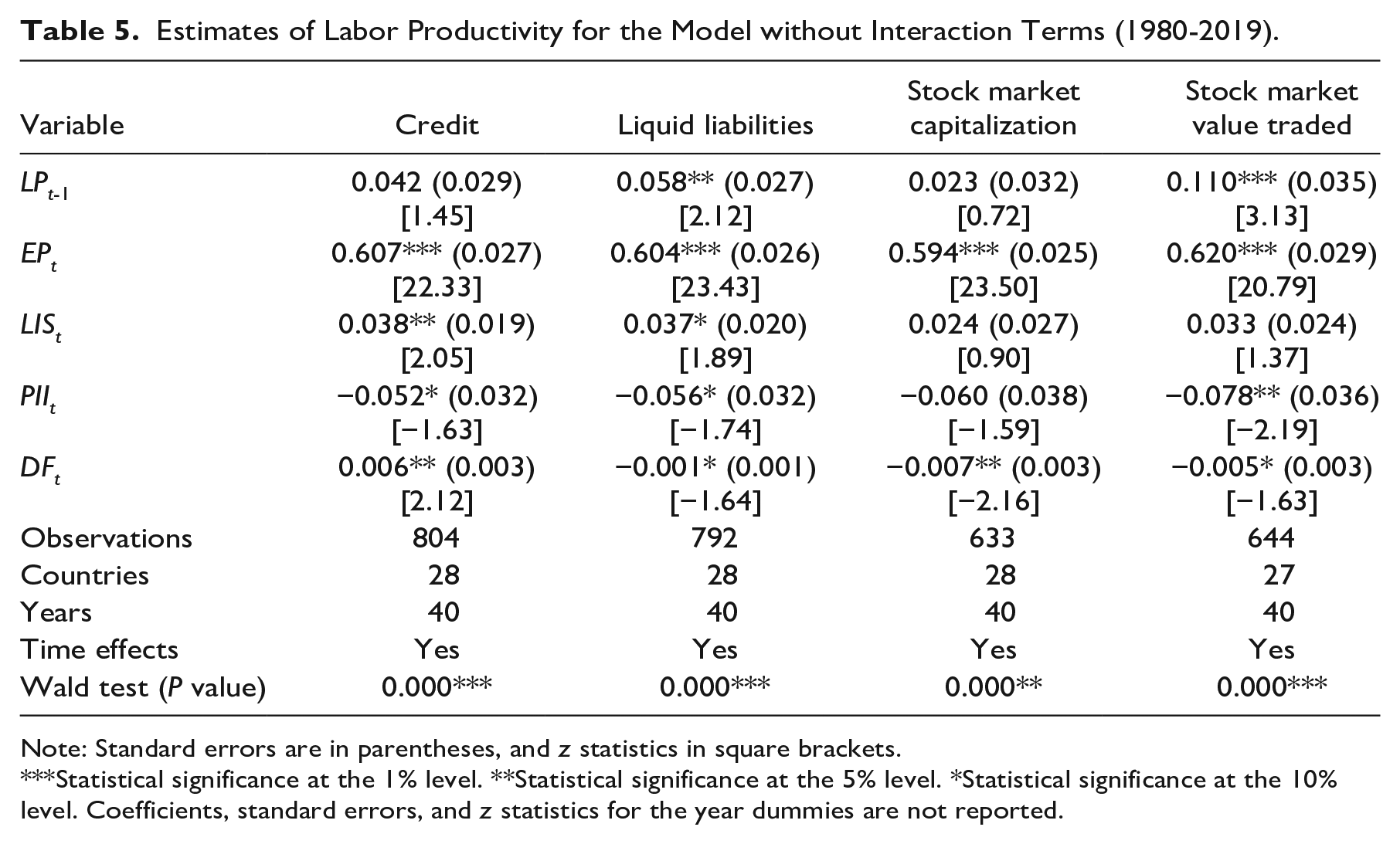

In this section, we present our estimates for labor productivity in the EU countries for the model without interaction terms (table 5) and for the model with interaction terms (table 6). For the two models, we included time dummies in order to take into account the specific features of each year in the evolution of labor productivity in the EU countries. Wald tests were also performed in order to assess the statistical significance of the time dummies.

Estimates of Labor Productivity for the Model without Interaction Terms (1980-2019).

Note: Standard errors are in parentheses, and z statistics in square brackets.

Statistical significance at the 1% level. **Statistical significance at the 5% level. *Statistical significance at the 10% level. Coefficients, standard errors, and z statistics for the year dummies are not reported.

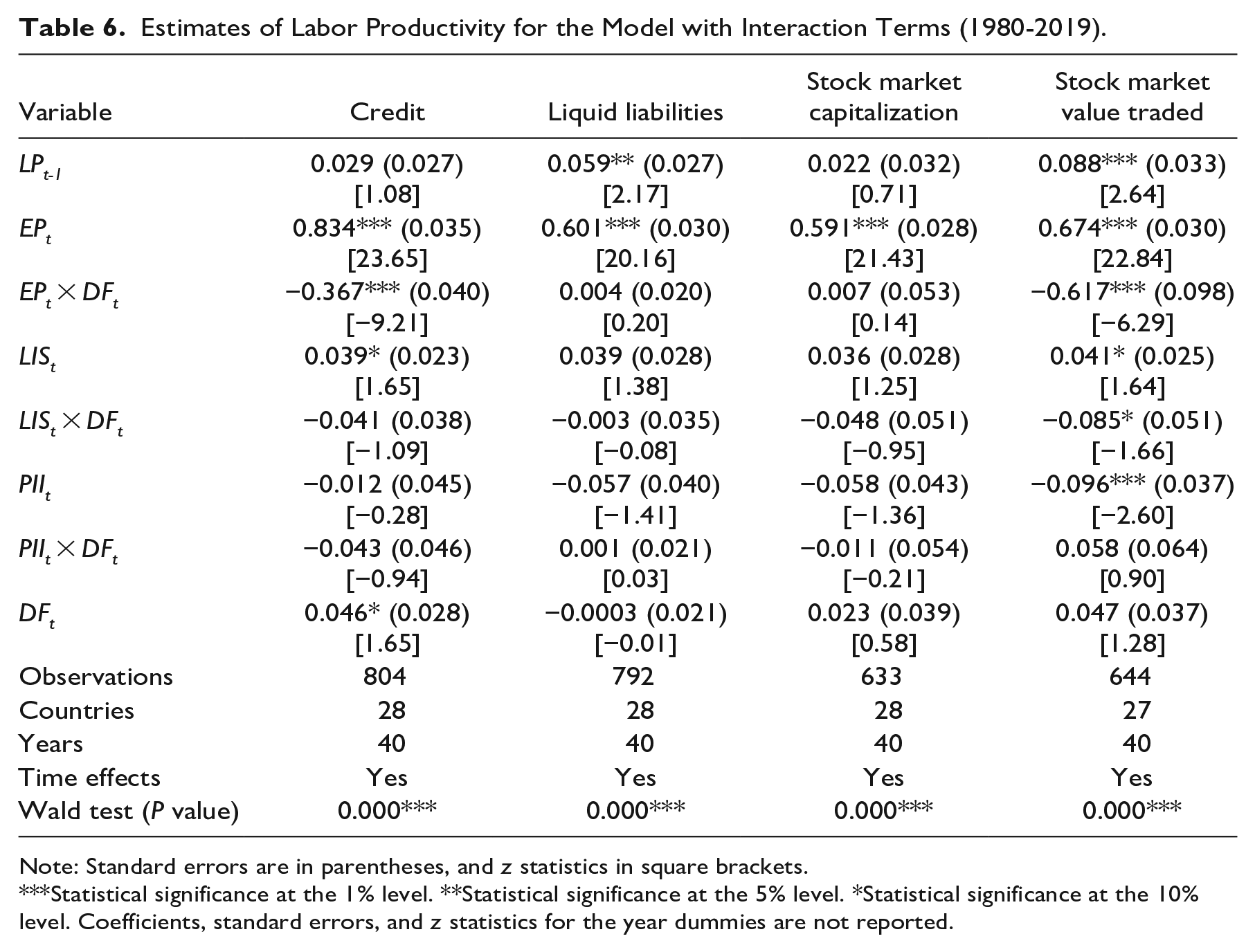

Estimates of Labor Productivity for the Model with Interaction Terms (1980-2019).

Note: Standard errors are in parentheses, and z statistics in square brackets.

Statistical significance at the 1% level. **Statistical significance at the 5% level. *Statistical significance at the 10% level. Coefficients, standard errors, and z statistics for the year dummies are not reported.

In relation to the estimates for labor productivity in the EU countries for the model without interaction terms (table 5), our findings confirm that all variables are statistically significant at the traditional significance levels and have the expected signs. This confirms the robustness of our estimates, namely, because our results do not change considerably when using the different proxies for the degree of financialization. We find that the lagged labor productivity positively impacts the actual labor productivity in the EU countries by confirming that this variable evolves with a strong inertia, which is in line with the results found by Vergeer and Kleinknecht (2014) and Correia and Barradas (2021). This reinforces the urgent need for the adoption of several policies to reverse this downward on the evolution of labor productivity in the EU countries; otherwise, the current slowdown will persist in the coming years. We also find that economic performance is a positive determinant of labor productivity in the EU countries, which is in line with the Smith effect (Smith 1776) or the Classical Kaldorian-Verdoorn effect (Verdoorn 1949; Kaldor 1961). Sylos Labini (1983), Guarini (2016), Tridico and Pariboni (2018), Carnevali et al. (2020), and Correia and Barradas (2021) also report a positive effect of economic performance on labor productivity. Our findings also confirm that the labor income share also determines labor productivity in the EU countries by exerting a positive effect. This result supports the Webb-Sylos Labini effect (Sylos Labini 1983, 1984, 1999) or the Marx and Hicks effect (Hein and Tarassow 2010). Vergeer and Kleinknecht (2014), Tridico and Pariboni (2018), Carnevali et al. (2020), Yousef (2020), and Correia and Barradas (2021) also found that labor income share exerts a positive impact on labor productivity. As also expected, personal income inequality exerts a negative effect on labor productivity in the EU countries. 11 A similar result was reported by Tridico and Pariboni (2018) and Correia and Barradas (2021). As also found by Tridico and Pariboni (2018) and Correia and Barradas (2021), our results confirm that the degree of financialization negatively impacts the labor productivity in the EU countries. The only exception pertains to the case with the proxy of credit, according to which labor productivity depends positively on credit. This counterintuitive result could be explained by two different reasons. On the one hand, this is related to the structure of the productive system in the EU countries, where the majority of corporations (approximately 99 percent) are small and medium-sized. These corporations face higher funding constraints in comparison to larger ones, and they are more dependent on credit to improve labor productivity through new investments in human capital and/or on physical capital. On the other hand, this is related to the relatively small importance of credit in the EU countries by around 75.1 percent on average (table 3), which is below the traditional threshold by approximately 90 percent through which a further growth of credit impairs labor productivity (Cecchetti and Kharroubi 2012). This seems to suggest that credit in the EU countries is still producing beneficial effects regarding labor productivity because, on average, it continues to be below that threshold in the majority of the EU countries (figure A5 in the Appendix).

With regard to the estimates for labor productivity in the EU countries for the model with interaction terms (table 6), our findings do not change considerably in comparison with the results for the model without interaction terms. Effectively, we continue to find evidence that labor productivity is strongly persistent, positively affected by economic performance and labor income share, and negatively affected by personal income inequality. The main change occurs with the degree of financialization, which loses its statistical significance in the majority of cases, with the exception of the case where credit is used as a proxy, which continues to exhibit a positive effect on labor productivity. Our findings confirm that the interaction term between economic performance and the degree of financialization is statistically significant at the traditional significance levels and exhibits a negative sign, which confirms that the impact of economic performance on labor productivity in the EU countries depends linearly and negatively on the degree of financialization. We also find that the interaction term between labor income share and the degree of financialization is also statistically significant at the traditional significance levels and exhibits a negative coefficient, which corroborates that the impact of labor income share on labor productivity in the EU countries also depends linearly and negatively on the degree of financialization. These results are in line with the post-Keynesian predictions on the existence of the aforementioned indirect channels between the strengthening of the degree of financialization, the weak economic performance (and the decline of the labor income share), and the corresponding slowdown of labor productivity in the EU countries (Tridico and Pariboni 2018; Correia and Barradas 2021). The statistical insignificance of the interaction term between personal income inequality and labor productivity does not confirm the indirect channel between the strengthening of the degree of financialization, the increase of personal income inequality, and the deceleration of labor productivity in the EU countries (Tridico and Pariboni 2018; Correia and Barradas 2021), probably because the increase of personal income inequality in the EU countries is explained not only by the phenomenon of financialization but also by a host of different factors.

In order to confirm the robustness of our estimates to resampling, we also employ a jackknife analysis (Quenouille 1949, 1956; Tukey 1958) through the reestimation of our results for the model without interaction terms and for the model with interaction terms by excluding one country at a time and one year at a time. 12 For both models, the results of the jackknife analysis show that the majority of our variables maintain their statistical significance and the same impacts on labor productivity vis-á-vis the results for all the EU countries for all the years that are shown in tables 5 and 6.

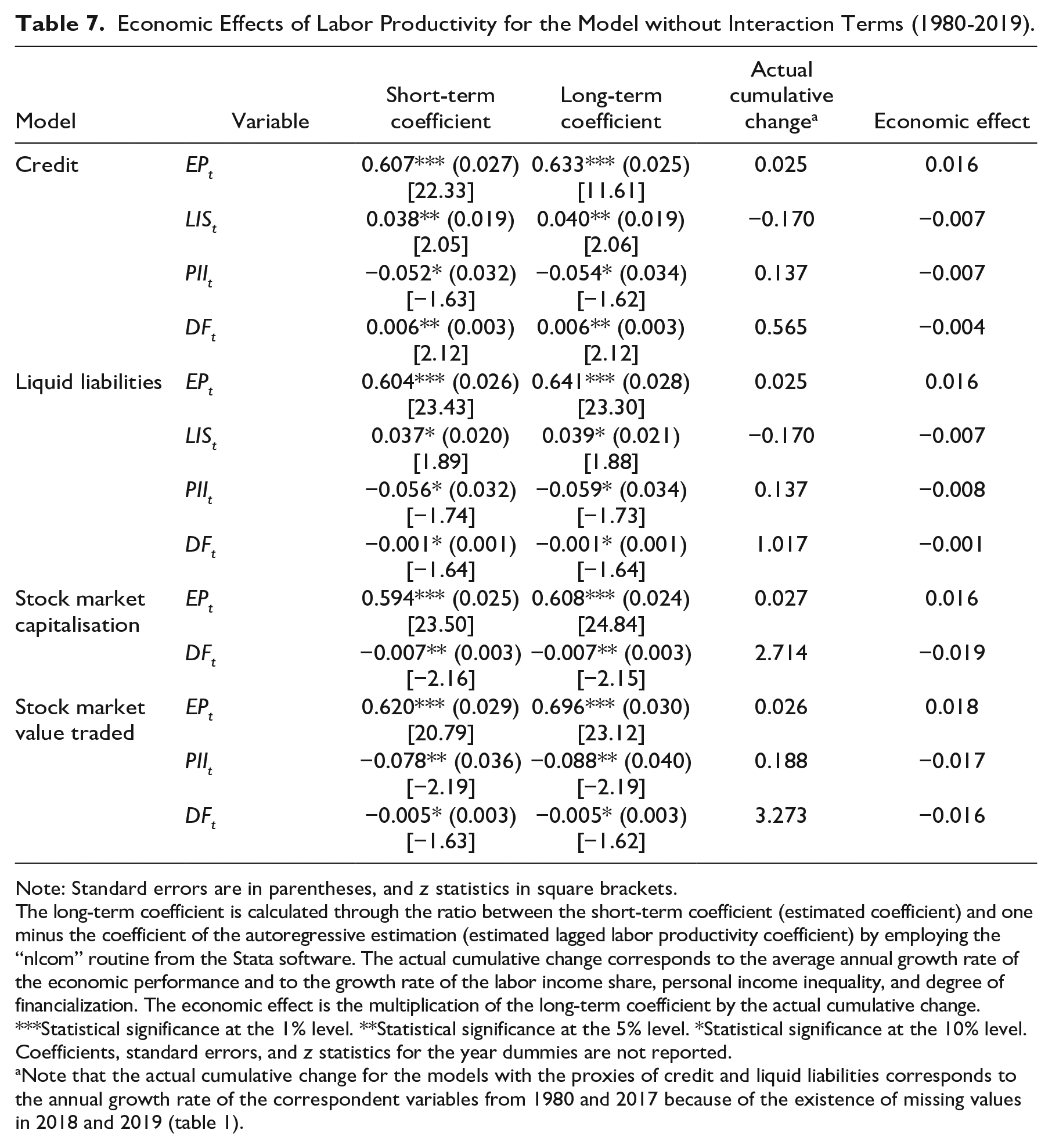

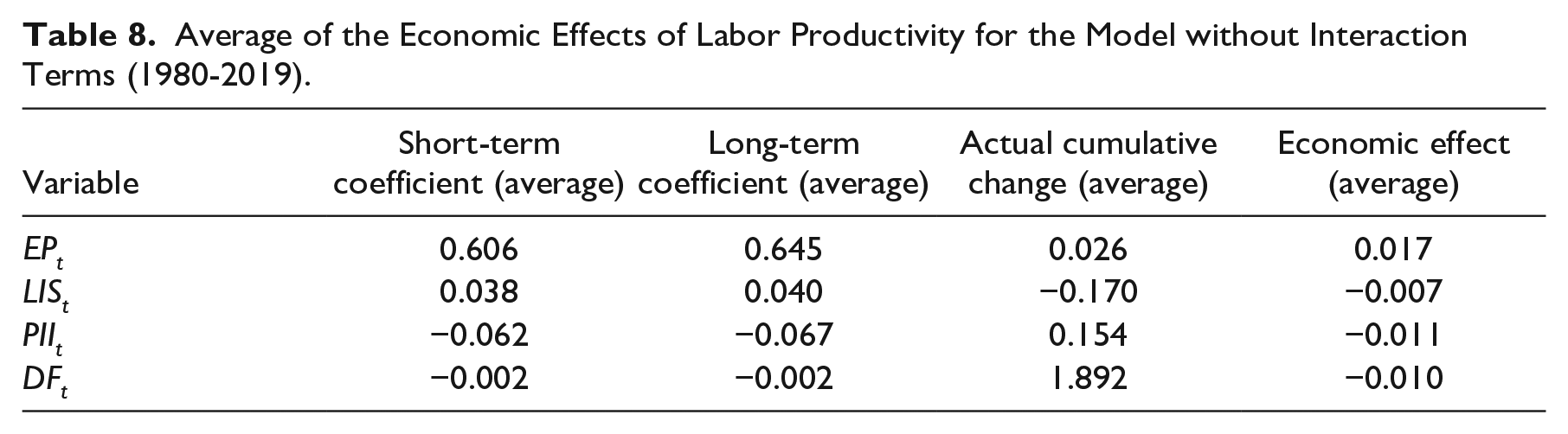

Our results confirm that the poor evolution of labor productivity in the EU countries cannot be divorced from the phenomenon of financialization and its corresponding four channels. Tables 7 and 8 describe the economic effects of our estimates (McCloskey and Ziliak 1996; Ziliak and McCloskey 2004) in order to assess the role of each channel in the evolution of labor productivity in the EU countries. Just for simplicity, we present the economic effects only for the model without interaction terms.

Economic Effects of Labor Productivity for the Model without Interaction Terms (1980-2019).

Note: Standard errors are in parentheses, and z statistics in square brackets.

The long-term coefficient is calculated through the ratio between the short-term coefficient (estimated coefficient) and one minus the coefficient of the autoregressive estimation (estimated lagged labor productivity coefficient) by employing the “nlcom” routine from the Stata software. The actual cumulative change corresponds to the average annual growth rate of the economic performance and to the growth rate of the labor income share, personal income inequality, and degree of financialization. The economic effect is the multiplication of the long-term coefficient by the actual cumulative change.

Statistical significance at the 1% level. **Statistical significance at the 5% level. *Statistical significance at the 10% level. Coefficients, standard errors, and z statistics for the year dummies are not reported.

Note that the actual cumulative change for the models with the proxies of credit and liquid liabilities corresponds to the annual growth rate of the correspondent variables from 1980 and 2017 because of the existence of missing values in 2018 and 2019 (table 1).

Average of the Economic Effects of Labor Productivity for the Model without Interaction Terms (1980-2019).

We conclude that all four channels associated with the phenomenon of financialization explain the evolution of labor productivity in the EU countries. The increase of personal income inequality, the strengthening of the degree of financialization, and the decline of the labor income share have contributed to the sluggish labor productivity in the EU countries from 1980 to 2019 by around 1.1 percent, 1 percent, and 0.7 percent on average, respectively. Economic performance has been the main driver of labor productivity in the EU countries by favoring a growth of about 1.7 percent on average, which has not been enough to compensate for the detrimental economic effects of the increase in personal income inequality, the strengthening of the degree of financialization, and the decline of the labor income share. During that time, labor productivity in the EU countries would have grown more if there had been a stronger economic performance, a smaller decline (or even a rise) of the labor income share, a smaller increase (or even a decrease) of personal income inequality, and a weakening of the degree of financialization.

7. Conclusion

This article employed a panel data econometric approach in order to empirically ascertain the role of the phenomenon of financialization in the deceleration of labor productivity in the EU countries from 1980 to 2019.

Theoretically and by relying on the post-Keynesian literature, the phenomenon of financialization cannot be divorced from the deceleration of labor productivity in the majority of the developed economies since the mid-1970s and 1980s, namely, because of four different channels: the weak economic performance, the decline in the labor income share, the increase in personal income inequality, and the strengthening of the degree of financialization and its corresponding harmful effects on innovation, research and development, technological progress, and productive investments performed by nonfinancial corporations (Tridico and Pariboni 2018; Correia and Barradas 2021).

Some of these four channels have already been tested in several econometric works (Sylos Labini 1983; Vergeer and Kleinknecht 2014; Guarini 2016; Micallef 2016; Tridico and Pariboni 2018; Carnevali et al. 2020; Yousef 2020; and Correia and Barradas 2021), although they do not directly assess all the aforementioned four channels through which the phenomenon of financialization has undermined labor productivity. Tridico and Priboni (2018) and Correia and Barradas (2021) are the only two exceptions. The former work focuses on the OECD countries but uses only one proxy to capture the degree of financialization (stock market capitalization) and does not consider in its estimates the potential indirect effects between the degree of financialization (the fourth channel) and economic performance (the first channel), the labor income share (the second channel), and personal income inequality (the third channel). The latter uses five different proxies to measure the degree of financialization (credit, money supply, financial value added, stock market capitalization, and shareholder orientation) and takes into account in its estimates the potential indirect effects between the degree of financialization (the fourth channel) and economic performance (the first channel), the labor income share (the second channel), and personal income inequality (the third channel), through the use of interaction terms, but it only focuses on Portugal.

Hence, we estimated an aggregate equation according to which labor productivity depends on lagged labor productivity, economic performance, labor income share, personal income inequality, and degree of financialization. We used the LSDVBC estimator created by Nickell (1981), Bun and Kiviet (2003), Bun and Carree (2005), and Bruno (2005a, 2005b) because of the existence of an unbalanced panel, a dynamic model, and a macro panel and the need to overcome the potential endogeneity due to the omission of relevant variables and/or simultaneity among the different variables (channels).

Our findings confirm that the weak evolution of labor productivity in the EU countries cannot be dissociated from the phenomenon of financialization and its corresponding four channels. Lagged labor productivity, economic performance, and labor productivity positively impact the labor productivity in the EU countries, while personal income inequality and the degree of financialization impact it negatively. Our findings also reveal that labor productivity in the EU countries in the last decades would have grown more if there had been a stronger economic performance, a smaller decline (or even a rise) of the labor income share, a smaller increase (or even a decrease) of personal income inequality, and a weakening of the degree of financialization.

Our findings suggest that policy makers in the EU countries should engage in policies that could promote a stronger economic performance, a rise of the labor income share, a decrease of personal income inequality, and a weakening of the degree of financialization in order to support higher growth of labor productivity in the coming years and to avoid a new “secular stagnation” in the era of financialization. Following post-Keynesian insights, policy makers should put in place several measures to interrupt the continuously decreasing demand, which should involve international coordination to abandon the paradigm of Reaganomics and Thatcherism and to resume a focus on demand-side economics, full employment goals, welfare state expansion, labor market protection, expansionary budget policies, and redistributive policies (Pariboni, Paternesi Meloni, and Tridico 2020). Re-regulation of the financial system, a process of de-financialization, and a Global Keynesian New Deal could be desirable to achieve all of these goals (Hein 2012).

The use of micro data at corporate level, industry level, sector level, regional level, and/or country level could represent a suggestion for further research on labor productivity in EU countries. This will be crucial to assess whether these four channels linked to the phenomenon of financialization have a detrimental effect on labor productivity in all corporations, sectors, regions, industries, regions, and/or countries or only in some of them. An analysis of the consequences of the slowdown of labor productivity in the EU countries could represent another suggestion for further research on this matter.

Footnotes

Appendix

Acknowledgements

The author thanks the helpful comments and suggestions of Ana Costa, Ana Drago, Annina Kaltenbrunner, Ivan Rubinić, Michael Keaney, the participants in the Dinâmia’CET-Iscte Workshop on Dinâmicas Socioeconómicas e Territoriais Contemporâneas (Iscte–Instituto Universitário de Lisboa, April 2022), and the participants in the 12th Annual Conference in Political Economy (University of Bologna, September 2022). The usual disclaimer applies.

1

Barradas (2020) discusses the extent to which the phenomenon of financialization has contributed to a weak economic performance in the last decades, which has been confirmed by several econometric works (Rioja and Valev 2004a, 2004b; Aghion, Howitt, and Mayer-Foulkes 2005; Kose et al. 2006; Prasad, Rajan, and Subramanian 2007; Rousseau and Wachtel 2011, Cecchetti and Kharroubi 2012; Barajas, Chami, and Yousefi 2013; Dabla-Norris and Srivisal 2013; Beck, Degryse, and Kneer 2014; Breintenlechner, Gächter, and Sindermann 2015; Alexiou, Vogiazas, and Nellis 2018; Ehigiamusoe and Lean 2018; Barradas 2020; Pariboni, Paternesi Meloni, and Tridico 2020).

2

Hein (2012), Barradas and Lagoa (2017a), Barradas (2019), and Kohler, Guschanski, and Stockhammer (2019) clarify the extent to which the phenomenon of financialization has damaged the labor income share in the last decades, which has been confirmed by several econometric works (Kristal 2010; Dünhaupt 2013; Lin and Tomaskovic-Devey 2013; Alvarez 2015; Barradas and Lagoa 2017a; Stockhammer 2017; Barradas 2019; Kohler, Guschanski, and Stockhammer 2019).

3

Please note that we do not discuss this effect further because it relies on the neoclassical (mainstream) loanable funds theory, which is not consistent with the post-Keynesian literature.

4

Lagoa and Barradas (2020) examine the extent to which the phenomenon of financialization has caused an increase in personal income inequality in the last decades, which has been confirmed by several econometric works (Greenwood and Jovanovic 1990; Banerjee and Newman 1993; Galor and Zeira 1993; Baldacci, de Mello, and Inchauste 2002; Roine, Vlachos, and Waldenströrm 2009; Atkinson and Morelli 2011; Gimet and Lagoarde-Segot 2011; Assa 2012; Fournier and Koske 2012; Jauch and Watzka 2012; Jaumotte, Lall, and Papageorgiou 2013; Karanassou and Sala 2013; Denk and Cournède 2015; Furceri and Loungani 2015; Jaumotte and Buitron 2015; de Haan and Sturm 2017; ![]() ).

).

5

This disruptive relationship between the phenomenon of financialization and innovation, research and development, technological progress, and productive investments performed by nonfinancial corporations has been confirmed by several econometric works (Stockhammer 2004; Orhangazi 2008; Van Treeck 2008; Onaran, Stockhammer, and Grafl 2011; Seo, Kim, and Kim 2012; Barradas 2017; Barradas and Lagoa 2017b; Davis 2017; Tori and Onaran 2018, ![]() ).

).

6

Please note that we do not include in our model to estimate labor productivity the cost of labor in relation to the price of investment goods—the so-called Ricardo effect (Ricardo 1821)—because of three different theoretical motives. First, and taking into account a Sraffian point of view, the Ricardo effect changes with the distribution of income by implying that the cost of labor and the price of investment goods are interdependent, which constitutes an objection to including the Ricardo effect among the independent variables of our model to estimate labor productivity (Sylos Labini 1983). Second, the validity of the Ricardo effect is quite limited because it is restricted to an extremely special case by requiring very specific assumptions about the available set of production methods from which producers can choose (Gehrke 2003). Third, the impact on labor productivity of the Ricardo effect is rather analogous to the one exerted by the aforementioned Webb-Sylos-Labini effect or the Marx and Hicks effect, namely, because both of them will induce the adoption of new technologies and the reorganization of the production process in order to limit production costs, which supports the growth of labor productivity (Tridico and Pariboni 2018). A similar empirical strategy was carried out by Tridico and Pariboni (2018) and ![]() .

.

7

The United Kingdom was also included in our sample because our data set encompasses annual data from 1980 to 2019 and Brexit only occurred at the beginning of 2020.

8

As argued by Guerriero (2012), the compensation of employees includes wages, salaries, and other forms of nonwage compensation, which also constitute returns from labor. We use the adjusted labor share to proxy labor share because it includes both dependent and self-employed workers, which allow us to circumvent the bias related with the fact that the earnings of self-employed are treated as labor income in certain cases and as capital income in others (![]() ).

).

9

Liquid liabilities are also known as broad money, or money supply (M3). They correspond to the sum of currency and deposits in the central bank (M0); plus transferable deposits and electronic currency (M1); plus time and savings deposits, foreign currency transferable deposits, certificates of deposit, and securities repurchase agreements (M2); plus travelers checks, foreign currency time deposits, commercial paper, and shares of mutual funds or market funds held by residents.

10

Bijlsman and Zwart (2013) and de Haan, Oosterloo, and Schoenmaker (2015) cluster the EU countries into four different groups, namely, the “bank-based” (Austria, Denmark, Germany, Greece, Italy, Portugal, and Spain), “market-based” (Belgium, Finland, France, the Netherlands, Sweden and the United Kingdom), Eastern European (Bulgaria, Croatia, Czechia, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovakia, and Slovenia), and outlier countries (Cyprus, Ireland, Luxembourg, and Malta). The bank-based countries have financial systems that are quite similar to the Japanese one due to the strong importance of banks. The market-based countries have financial systems that more closely resemble that of the United States. The Eastern European countries possess small financial systems, and some of them have recently decided to apply for entry to the euro area. The outlier countries have banking systems that are both very large and extend a large amount of credit.

11

It is worth noting that the negative effect of personal income inequality on labor productivity in the EU countries would be maintained if we used the top 1 percent income share or the Gini coefficient instead of the top 10 percent income share. Results are available on request.

12

Please note that the results of the jackknife analysis are available on request.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.