Abstract

Background:

There is an active debate over the potential for market-based strategies to address micronutrient deficiencies in low- and middle-income countries. However, there are questions over the viability of market-based strategies, reflecting limited evidence on the value that low-income households attach to the nutritional attributes of processed foods.

Objective:

The objective of this article is to investigate the willingness to pay of primary food purchasers in low-income households in rural Bangladesh for Shokti+, a nutritionally fortified yogurt produced and distributed by Grameen Danone Foods Limited.

Methods:

A real choice experiment with economic incentives was conducted with 1000 rural food purchasers sampled from the distribution area of Shokti+ in rural Bangladesh. The choices of respondents revealed attribute nonattendance, favoring the fortification attribute over price.

Results:

Results from a random parameter logit model found that respondents were willing to pay an average of 18 BDT (US$0.22) for fortification and 6 BDT (US$0.073) for brand name. The market price for Shokti+ at the time of the study was 10 BDT (US$0.12). The results from a random effects model suggest the magnitude of willingness to pay for fortification was primarily driven by the nutritional awareness of respondents but offset by household food insecurity.

Conclusions:

The article concludes that, while there is a viable market for fortified yogurt in rural Bangladesh, efforts to promote this product as a strategy to address micronutrient deficiency are best targeted at low-income households with some capacity to pay for low priced commercially produced foods.

Keywords

Introduction

Globally, it is estimated that 2 billion people have micronutrient deficiencies at levels that have severe health implications. 1,2 In the past several decades, numerous approaches have been applied to address this problem but with varying success. Since poor dietary quality is one of the leading causes of micronutrient deficiencies, food-based approaches have been directed at increasing the quantity and quality of nutrients consumed through the diet, especially in low- and middle-income countries (LMICs). 3 While there is evidence that food-based approaches are a cost-effective strategy to reduce micronutrient deficiencies, publicly funded interventions have struggled to achieve the scale and/or long-term viability, especially in low-income populations. 3,4 Accordingly, there is increasing interest in how food markets, and the businesses that operate within them, can be leveraged to promote increased consumption of nutrient-dense foods by low-income households to complement public interventions. 5

Ways in which food markets have been leveraged to increase the availability of nutrient-rich foods to low-income households include biofortification of staple crops (eg, orange-fleshed sweet potato [OFSP]) and the fortification of foods during processing (eg, fortified wheat flour). Arguably, these approaches have the potential to achieve substantial scale because they are based on culturally acceptable foods and do not require major changes in household diets. 6 However, the impact of biofortified and fortified foods on micronutrient deficiencies requires that these foods are consumed in sufficient quantities and on a sustained basis. In turn, consumers must be able and willing to pay for these foods, including any premium that is associated with additional costs of production and distribution. 7 Accordingly, numerous studies have investigated willingness to pay by poor consumers for biofortified staple foods (such as OFSP) and fortified infant foods. In general, these studies show that, if provided with information on the nutritional benefits of these foods, even low-income consumers are willing to pay a premium over traditional nonfortified substitutes.

While historically diets of low-income households have been centered on nutrient-deficient staples and other unprocessed foods, in many LMICs there is an increasingly rapid process of nutrition transition, reflecting urbanization of the population and the increasing influence of “Western” eating patterns. 8 Accordingly, consumption of processed foods is increasing, even within low-income households. Within the marketplace for processed foods, businesses are beginning to produce and market products that are nutritionally enhanced, especially through fortification. There is growing evidence that some of these products have nutritional impact when consumed in sufficient quantities. 9 The commercial viability of these ventures, however, remains the subject of question given that the willingness to pay of low-income consumers for the nutritional attributes of processed food products has not been extensively investigated.

The challenges that food businesses are likely to face in producing and distributing processed nutrient-rich foods to the poor can be gleaned from the broader discourse on challenges faced by businesses operating at the so-called bottom of the pyramid. 10,11 These challenges include thin profit margins, high costs (especially in distribution and marketing), and the development of value propositions that are relevant to low-income consumers. There are additional challenges specific to markets for nutrient-dense food, such as the credence nature of nutritional attributes, 12 capturing the degree to which consumers recognize and value nutritional attributes, and the desirability of foods that are more nutritious. 13 In order for viable business opportunities based on the marketing of processed nutritionally enhanced foods to be identified and successfully employed as a nutritional strategy, 4 critical questions need to be addressed: (1) Are low-income consumers willing to pay for the nutritional attributes of processed nutritionally enhanced foods?; (2) Does the price they are able and willing to pay sufficiently remunerate businesses, given the production and distribution costs they face?; (3) What factors affect the price that low-income consumers are willing to pay?; and (4) What is the scope for business models that are commercially viable to achieve substantive nutritional impact on the poor?

To begin addressing these questions, this study examines the case of Grameen Danone Foods Limited (GDFL), a social enterprise selling Shokti+, a fortified yogurt product, in rural Bangladesh. A real choice experiment with economic incentives was used to estimate willingness to pay for the nutritional fortification attribute of the yogurt to determine whether the price that GDFL is able to charge, given the costs it incurs in producing and distributing the product, is viable. A random effects model was then used to investigate the influence of the socioeconomic characteristics, attitudes, and nutritional knowledge of respondents on the willingness to pay for fortification. The article concludes with a discussion of the results for the commercial viability of Shokti+ as well as the external validity of results in terms of the potential role of market-based strategies to address micronutrient deficiencies.

Beyond the specific case of Shokti+, this study aims to contribute to the relatively sparse literature on the willingness to pay of low-income households for commercially produced nutritious foods. The results from the study, thus, present a picture of the propensity of low-income households to “trade up” to foods that are nutritionally enhanced. The findings have important implications both for businesses that are attempting to increase scale operations and new entrants that are interested in contributing to the array of nutritionally enhanced foods that are offered in the market.

Background

Low-Income Consumers’ Willingness to Pay for Nutritionally Enhanced Foods

To date, the majority of willingness-to-pay studies in LMICs have focused on biofortified foods. 14 -16 These studies have consistently demonstrated that low-income consumers are willing to pay a premium for staples that have enhanced nutrient density. For example, Chowdhury et al 14 found that poor Ugandan consumers are willing to pay a 25% premium for OFSP with a content of pro-vitamin A carotenoids that is greater than traditional white varieties. Similarly, there is evidence that Chinese consumers are willing to pay at least a 33% premium for rice that has been biofortified to have a higher folate content. 16 In Kenya, DeGroote et al 15 found that low-income consumers are willing to pay a 24% premium for fortified maize meal. However, the respondents associated a 12% discount with the yellow color of fortified maize meal, compared to the white color of the nonfortified alternative.

A further group of studies has explored the willingness to pay of low-income consumers for fortified complementary foods for infants. 17 -19 The results of these studies are varied. Segre et al 19 found that 25% or more of sampled Ethiopian households were willing to pay at least the unsubsidized price for a week’s supply of a fortified peanut-based nutritional supplement for infants. Conversely, Adams et al 20 found that pregnant or breast-feeding women only had a small positive willingness to pay for a similar lipid-based supplement that generally did not exceed the additional cost of production. While the studies of Pelto and Armar-Klemesu 21 and Pelto 22 indicated that women in low-income households positively value fortified infant complementary foods on the basis of their nutritional value, they are often unable to afford to purchase the complimentary foods that they value most highly. The results of these studies underscore the importance of investigating both the ability and the willingness of poor consumers to pay the additional cost of nutritionally enhanced foods in specific contexts.

The factors that influence the magnitude of low-income consumers’ willingness to pay for fortified foods are more often related to the level of nutritional awareness than socioeconomic characteristics. For example, prior exposure to and/or consumption of nutritionally enhanced foods, and information on their nutritional benefits, is found to have a significant effect on the magnitude of willingness-to-pay estimates in numerous studies. 15,16,23 -25 The acceptability of nutritionally enhanced foods has also been identified as a key factor affecting willingness to pay. For example, Chowdhury et al 14 found that having consumed and liked the taste of OFSP had a significant influence on the willingness to pay of poor consumers in Uganda. Likewise, taste was found to significantly influence willingness to pay for biofortified maize in Mozambique. 26 Contrastingly, the effect of socioeconomic or demographic variables (ie, income, assets, age, geographic location, and level of education) on willingness to pay varied across the results of the aforementioned studies.

Despite the fact that processed foods are constituting an increasingly important component of the diets of low-income households in LMICs, 27 there is a paucity of studies on the willingness to pay for nutritionally enhanced processed foods. As a result, there are limited insights available to businesses seeking to target nutritionally enhanced processed foods at the poor, especially where these products are novel. For example, little is known about the prices that low-income consumers are able and willing to pay, the nature and level of demand for such products, 25 and how the nutritional attributes of products are traded-off against other product characteristics (ie, quality, taste, and color). 5 Given the considerable costs associated with catering to bottom of the pyramid markets, especially related to marketing and distribution, 28,29 the resulting risks associated with these endeavors can be prohibitive, especially for micro-, small-, and medium-sized enterprises. Advancing this area of research will support efforts to increase the array of nutritionally enhanced foods offered to low-income households in LMICs and increase the potential for positive nutritional impact through the market.

The Case of Shokti+

The case of GDFL was selected for this study in order to examine the potential of a novel commercially produced processed food to achieve market viability and thus contribute to sustained nutritional improvements in a low-income population. The GDFL is a food business that produces and markets fortified yogurt to households with incomes at or below the poverty line in rural and urban areas in Bangladesh. Established as a joint venture between Groupe Danone and the Grameen Foundation, GDFL is a social enterprise with the dual objectives of improving the health of the poorest children in Bangladesh and reducing poverty by creating employment at various stages of the value chain. 30 In establishing GDFL, the aim was to leverage the expertise of Groupe Danone as a major multinational dairy business and the established linkages and social networks of Grameen Group in rural Bangladesh. The business has attracted significant interest in its scope to bring improved nutrition and livelihoods at scale in Bangladesh. 31 -37

The primary product manufactured and distributed by GDFL is Shokti+, a fresh probiotic yogurt that is fortified with approximately 30% of the recommended daily allowance of vitamin A, iodine, iron, and zinc. At the time of the survey, this was the only product of its kind on the market in Bangladesh. The yogurt is targeted at children aged 3 to 12 years, among which the prevalence of deficiency in these nutrients is high. For example, approximately 74% of children aged 6 to 14 years are deficient in vitamin A, while 40% are deficient in iodine. 38 Among children aged 6 to 11 years, 19% are anemic and 4% are iron deficient. 38 The nutritional efficacy of the product has been demonstrated in a randomized control trial. 9 The GDFL recommends that the product is consumed at least 3 times per week per child. To signal the function of the yogurt in a population that has low awareness of the meaning of fortification, the name Shokti means strength or energy in Bengali.

Shokti+ is distributed in 60-gram plastic pots to rural communities surrounding GDFL’s manufacturing facility in Bogra. A network of local women called the Shokti Ladies has been established by the GDFL. These women purchase the product using microcredit and sell it door to door in their communities. They receive a small margin on the sale of each pot of yogurt and are given a small incentive payment per pot sold by GDFL. The women are trained to communicate the benefits of Shokti+ and market the product in the target regions. Shokti+ is also distributed through small shops in 3 districts in rural Bangladesh, including Bogra, where the retailers purchase the product and resell it to consumers at a price specified by GDFL. The yogurt is also sold in the urban cities of Dhaka and Chittagong, but these markets are beyond the scope of the current research.

Methods

Study Design

Survey data were collected by experienced local enumerators through face-to-face interviews in the rural districts of Bogra, Sirajganj, and Naogaon in Bangladesh. Households were selected for participation in the study using multilevel proportionally stratified sampling. The first level of sampling ensured proportional representation from each of the 3 districts. The second level ensured sufficient representation of unions in which Shokti+ is not currently distributed so as to capture individuals who had not been previously exposed to the product. A total of 98 unions were selected. One village per union was then chosen at random in each union using a random number table. Village leaders were provided with study information and gave signed consent for the study to be conducted in their village. In each of the selected villages, 9 to 11 households were selected by approaching every third household. Selected households had to have at least 1 child aged between 3 and 12 years. If the household did not have a child in that age category, the enumerators moved on to the next third house. A total of 1000 households were surveyed. Participants provided verbal consent (due to issues of literacy) and were provided with the phone number of the organization engaged to undertake the surveys if they had any questions. The research study complied with all requirements of the Research Ethics Board of the University of Guelph (Approval Number 14SE010).

All interviews were completed in Bengali with the primary household food purchaser. Respondents were asked first to participate in a real choice experiment that involved economic incentives. The enumerators explained the experiment and then told respondents that they would be asked to complete a 35-minute questionnaire immediately following the experiment. The questionnaire collected sociodemographic information, prior awareness and/or consumption of Shokti+, awareness and knowledge of nutrition and links to diet, perceptions of Shokti+ and its attributes, and the nature of the children’s’ diets. The survey data were transcribed using a double-entry and reconciliation method. Qualitative data were translated into English by the enumerators and checked by the director of the research team.

Experiment Design

A stated preference method was used to illicit willingness to pay for the attributes of Shokti+. Two alternative nonhypothetical stated preference methods were considered for the study, namely, experimental auctions and real choice experiments. While experimental auctions are known to be effective in revealing the true value placed on products by consumers, given that they use real money and real products, they can be difficult for respondents to understand. 39 Contrastingly, real choice experiments better simulate real life purchasing decisions by presenting respondents with 2 or more products and asking them to select the one they prefer based on varying levels of the product attributes of interest. 39,40 Therefore, real choice experiment was employed, broadly following the method of Lusk and Schroeder, 41 to derive the value that respondents attributed to the attributes of Shokti+. The external validity was enhanced by using a real economic incentive mechanism. 41 Alphonce and Alfnes 42 and Lusk and Schroeder 41 found that, when respondents are required to follow through with their choices by making actual purchases with real money, the reliability of willingness-to-pay estimates increases. This method has been successfully used previously in a developing country context and with low-income consumers. 14

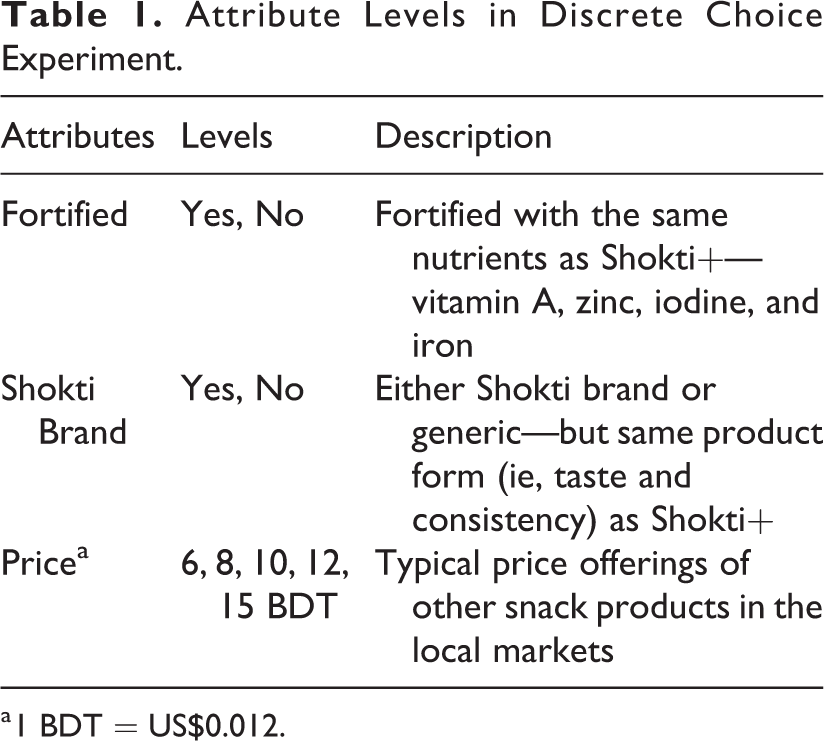

The overall goal of the experiment was to determine whether, and how much, low-income consumers are willing to pay for the attributes of a commercially produced fortified yogurt. The attributes and their respective levels were determined based on interviews with GDFL personnel, in-depth interviews with low-income consumers, and a pilot experiment. The final product alternatives were characterized by 3 attributes: (1) fortification; (2) brand; and (3) price in Taka (BDT). The levels of the 3 attributes are reported in Table 1. Shokti+ was represented in the choice scenarios as the product alternative having both a brand name and fortification. This was explained to respondents.

Attribute Levels in Discrete Choice Experiment.

a 1 BDT = US$0.012.

A full factorial design incorporating the product alternatives described in Table 1 would have resulted in 20 choice sets. Since this number was judged to impose an inordinate burden on respondents, the most efficient design incorporating 10 choice sets was derived using SAS version 9.3. Each choice set consisted of 2 product alternatives and 1 opt-out option. The relative deficiency in the experimental design was 70.43; here, efficiency measures the degree to which each level of an attribute appears equally often and the degree to which each pair of levels occurs equally across pairs of attributes. 43 The 10 choice sets were further randomized into 4 ordered scenarios.

Prior to the commencement of the choice experiment, respondents received 50 BDT (US$0.64) for their participation. They were informed that they could keep the money or spend it on yogurt at the end of the activity, depending on the choices they had made. Respondents were, furthermore, informed that a binding choice scenario would be randomly selected at the end of the questionnaire and that they would be required to purchase the product selected in the respective choice set for the specified price. If they had selected the “opt-out” choice in that set, they would keep the full 50 BDT (US$0.7). Since no generic yogurt was produced or sold at the time of the study, if the participant had selected any other option other than Shokti+ in the binding scenario, the participant was informed that the option was no longer available and that they were able to keep all 50 BDT (US$0.7). Given this was undertaken at the end of the study, there was no impact on the choices of respondents while avoiding the need to deceive respondents as to the nature of the yogurt they were being required to purchase.

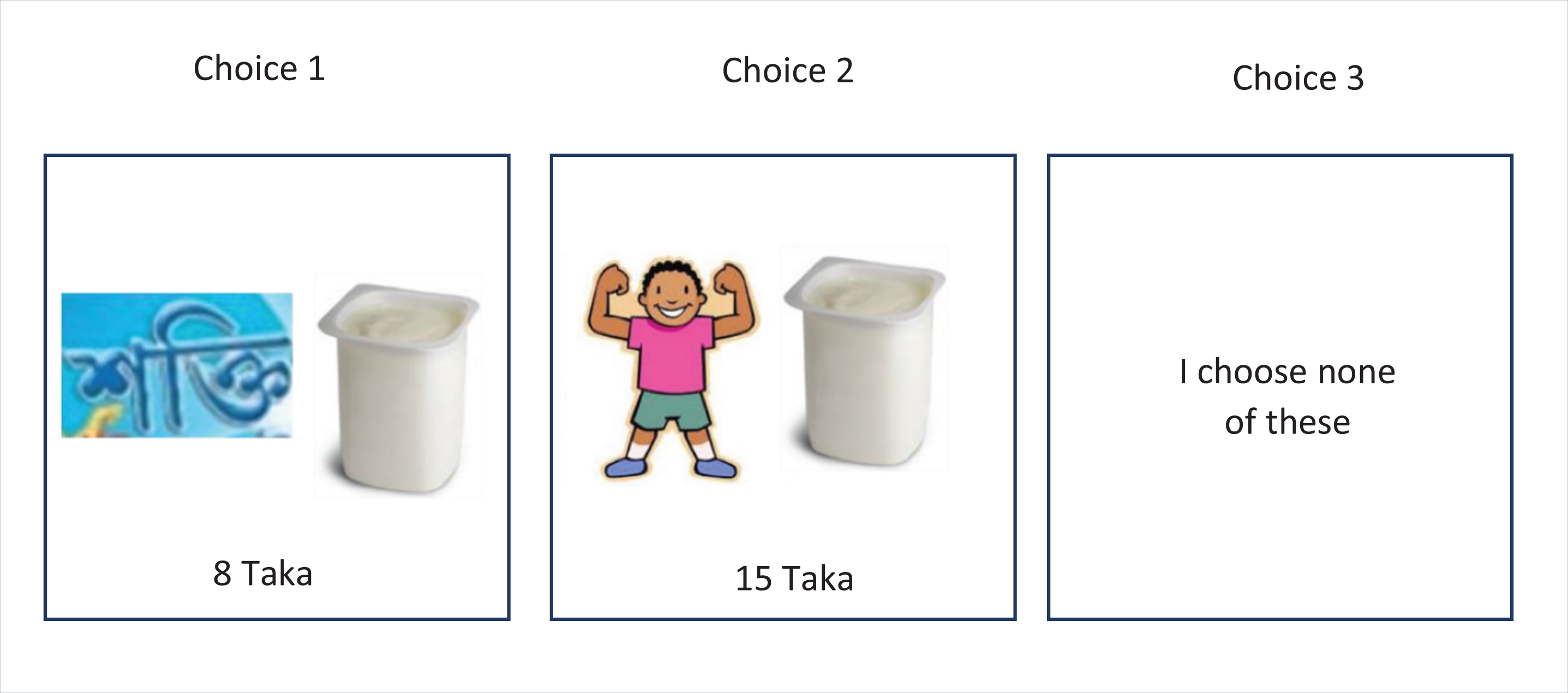

Figure 1 provides an example of the choice sets presented to the respondents. The blue Shokti label, pictured in choice 1, indicated that the product had the Shokti+ brand name. This was blank if the choice had no brand, as in Choice 2. The illustration of a child, pictured in Choice 2, indicated that the product had added nutrients, and was blank otherwise. This image was recommended by GDFL and the team of enumerators to symbolize fortification, since nutrition is associated with strength and energy in other nutritional messaging in Bangladesh. A picture of a cup of yogurt was included in both product alternatives (see choices 1 and 2) to differentiate from the opt-out alternative and to remind the respondent of the product being considered. For each choice set, the enumerator described each of the alternatives (defining the pictures in the choice set) and the prices to the respondents. The cards were translated into Bengali by the research team.

Example of a choice set card presented to respondents during experiment.

Random Parameters Logit Model

The random parameter logit (RPL) model is now common practice for estimating willingness to pay for attributes of products or services. 44 This approach has significant advantages over previously used methods, such as the multinomial logit model, including the relaxation of rigid assumptions regarding the independence of irrelevant alternatives, and accounting for random taste variation within the sampled population.

The RPL model estimates a utility function of the form:

where

Based on the abovementioned utility function, the RPL model estimates the unconditional choice probability that a decision maker will choose alternative k out of j alternatives over choice situations t. The distribution of the parameters is specified a priori, and the parameters are then estimated. The parameter estimation procedure allows for individual taste heterogeneity. 45 -47 Following Campbell, 45 500 shuffled Halton draws were used to estimate the individual-specific parameters.

The willingness to pay for the product attributes was estimated as follows:

where

Two iterations of the RPL model were undertaken to test for the presence of attribute nonattendance (ANA). Attribute nonattendance can occur due to choice complexity, 49 lack of knowledge of product attributes, 50 geographical proximity to the attribute of interest, 51 or the information provided in the choice experiment. 52 This article posits that ANA may also occur if an alternative contains a highly valued attribute to the extent that it leads to nonattendance of other attributes. A number of studies have shown that failure to account for ANA can result in biased parameter and subsequent willingness-to-pay estimates. 46,49,53 In fact, almost all studies that have accounted for ANA have improved the model fit as a result. 54

Random Effects Model

While observable respondent characteristics are typically included in standard logit models in order to estimate the effect on willingness to pay, this approach estimates the impact of these variables on the utility of an alternative rather than on the magnitude of willingness to pay directly. Furthermore, when evaluating consumer choices, there are inevitably unobserved and time-constant variables, known as unobserved effects. These might include the beliefs, attitudes, and/or values of the consumer that are inherently unobservable, cultural factors, and so on. Accordingly, Campbell 45 proposes the use of a random effects model to account for unobservable effects and to allow for systematic group effects by pooling willingness-to-pay estimates for all product attributes and allowing the regression to shift based on variation within the group.

The random effects model is estimated as follows:

where

Results

Respondent Characteristics

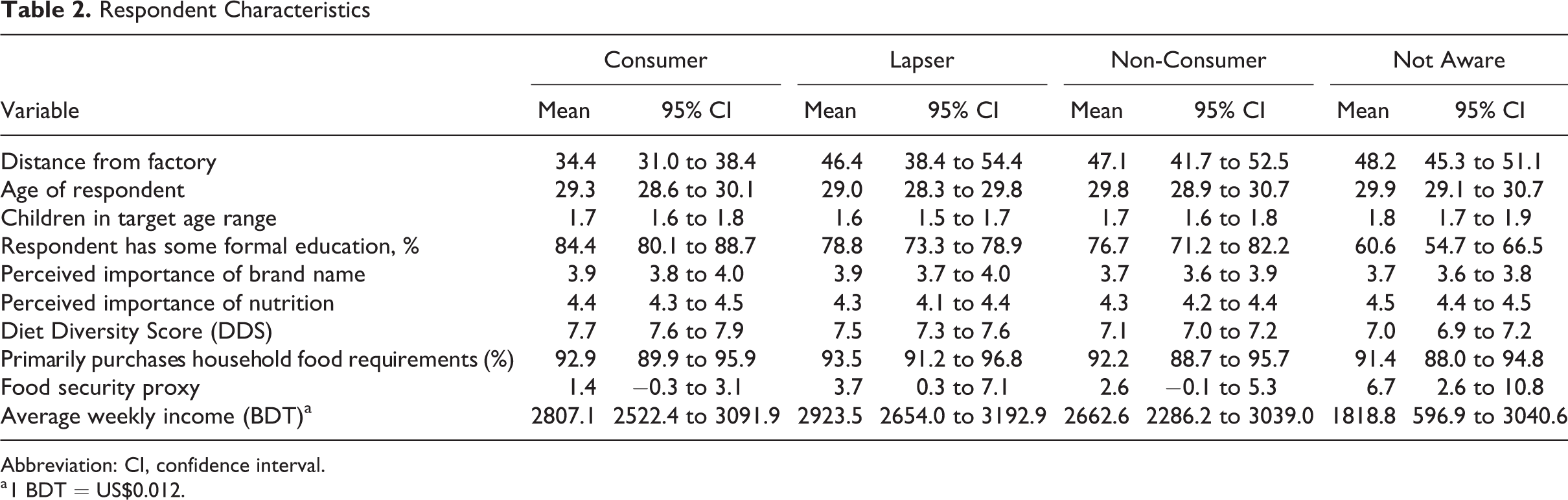

Following consultation with GDFL regarding the profile of consumers of Shokti+ in the context of the broader population in the study region, the sample was subdivided into 4 segments as follows: (1) “Consumers,” defined as households having purchased Shokti+ for at least one of their children within the last 14 days; (2) “Lapsers,” defined as households having consumed Shokti+ in the last 3 months but not within the last 14 days; (3) “Non-Consumers,” defined as households that were aware of Shokti+ but had not purchased it in the last 3 months or had never purchased it; and (4) “Not Aware,” defined as households that had not seen or heard about Shokti+ previously. Each segment accounted for approximately 25% of the total sample. Distinguishing between these segments helped to better understand the profile of current, past, and potential consumers and increase the reliability of the willingness-to-pay estimates. 37

Table 2 reports the characteristics of respondents in each of the 4 segments. Using a Tukey multiple means comparison, no significant differences were detected across demographic variables. The typical respondent was a woman around 30 years of age with 2 children aged between 3 and 12 years. This corresponds the a priori assumption that women are primarily responsible for food purchasing in this region of Bangladesh.

Respondent Characteristics

Abbreviation: CI, confidence interval.

a 1 BDT = US$0.012.

Looking across the 4 segments, there were significant differences with respect to income and level of education. While the average income of respondents in all 4 segments exceeded the national poverty line in Bangladesh of 1487 BDT per week (US$17.87), 56 households in the Not Aware segment had an average income between 844 BDT (US$10.14) and 1105 BDT (US$13.28) less than the other segments analysis of variance (AOV < 0.0001). The proportion of respondents in the Consumer, Lapser, and Non-Consumer segments that had completed at least some formal education was more than 15% higher than the Not Aware segment (AOV < 0.0001).

There were also differences across the consumer segments in terms of the nutritional quality of the diet of children and the level of food security. A 9-point Diet Diversity Score (DDS) was constructed for each household based on foods consumed by the respondent or children in the previous 7-day period. 57 Diet diversity was lowest in the Not Aware segment. The average DDS for the Not Aware segment was 7.0, while the Consumer segment had an average score of 7.7 (AOV < 0.0001). The Not Aware segment also exhibited greater food insecurity, with an average of 5 additional days per month where they had gone without food for a whole day due to lack of income compared to the Consumer segment (AOV = 0.06).

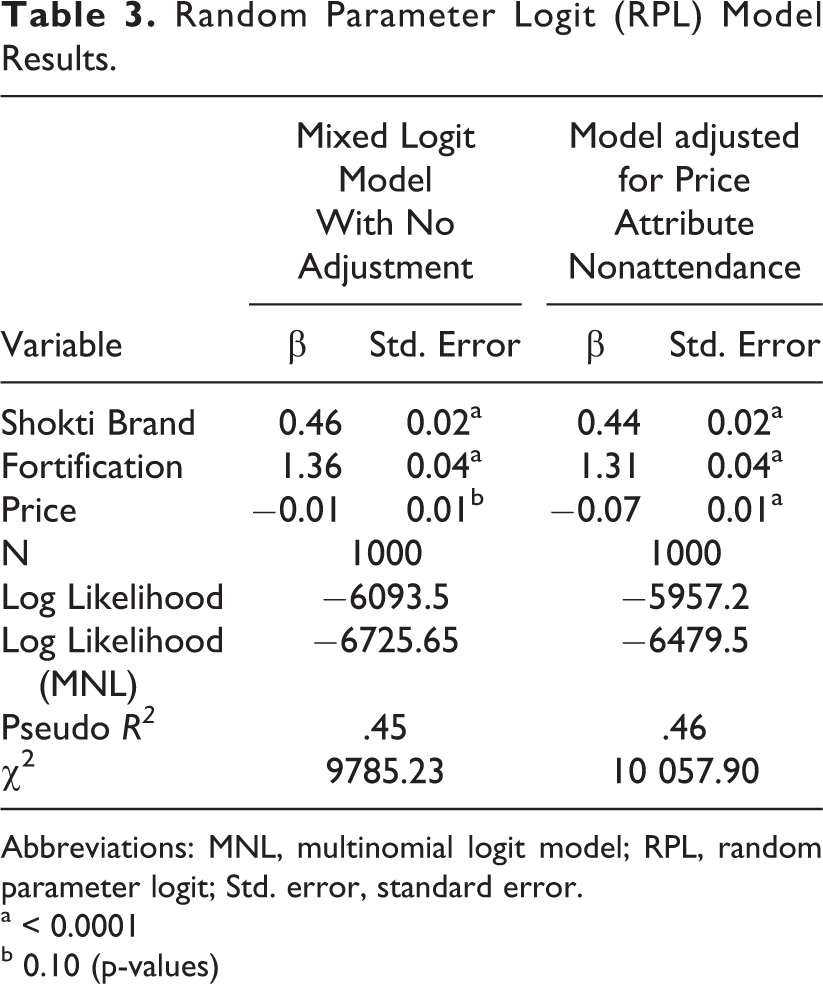

Random Parameter Logit Model Results

The RPL estimation was conducted using NLOGIT. The resulting parameter estimates are reported in Table 3. The model was statistically significant, with a χ2 statistic beyond the critical value of 16.27

Random Parameter Logit (RPL) Model Results.

Abbreviations: MNL, multinomial logit model; RPL, random parameter logit; Std. error, standard error.

a < 0.0001

b 0.10 (p-values)

Since the median willingness-to-pay estimate exceeds the 2014 market price of Shokti+ (10 BDT, US$0.12) by more than 120 BDT, the data were investigated for the presence of ANA. This revealed that a nontrivial proportion of respondents had put greater weight on the fortification attribute than either brand or price. Approximately 40% of respondents had chosen the fortified alternative in all 10 choice sets. Contrastingly, only 2% had selected the Shokti brand alternative in each choice set. This suggests that respondents largely ignored price in favor of the fortification attribute and, to a lesser extent, brand. Therefore, an ANA-adjusted model was estimated to allow for the specification of nonattendance attributes using NLOGIT. 58 The adjusted results are reported in the second column of Table 3. Comparing the log likelihoods of the 2 models confirms the presence of ANA; according to the findings of Welker et al, 54 model fit is improved if ANA is present and accounted for.

The magnitude of the price parameter in the ANA-adjusted model is greater than that of the nonadjusted model, has the a priori expected negative sign, and is significant at the 99% significance level. The magnitude of the parameter estimates for brand name and fortification are almost unchanged. According to the ANA-adjusted RPL estimates, the median willingness to pay for fortification was 18.1 BDT (US$0.22). This estimate is far more plausible than that provided by the standard RPL model without ANA adjustment.

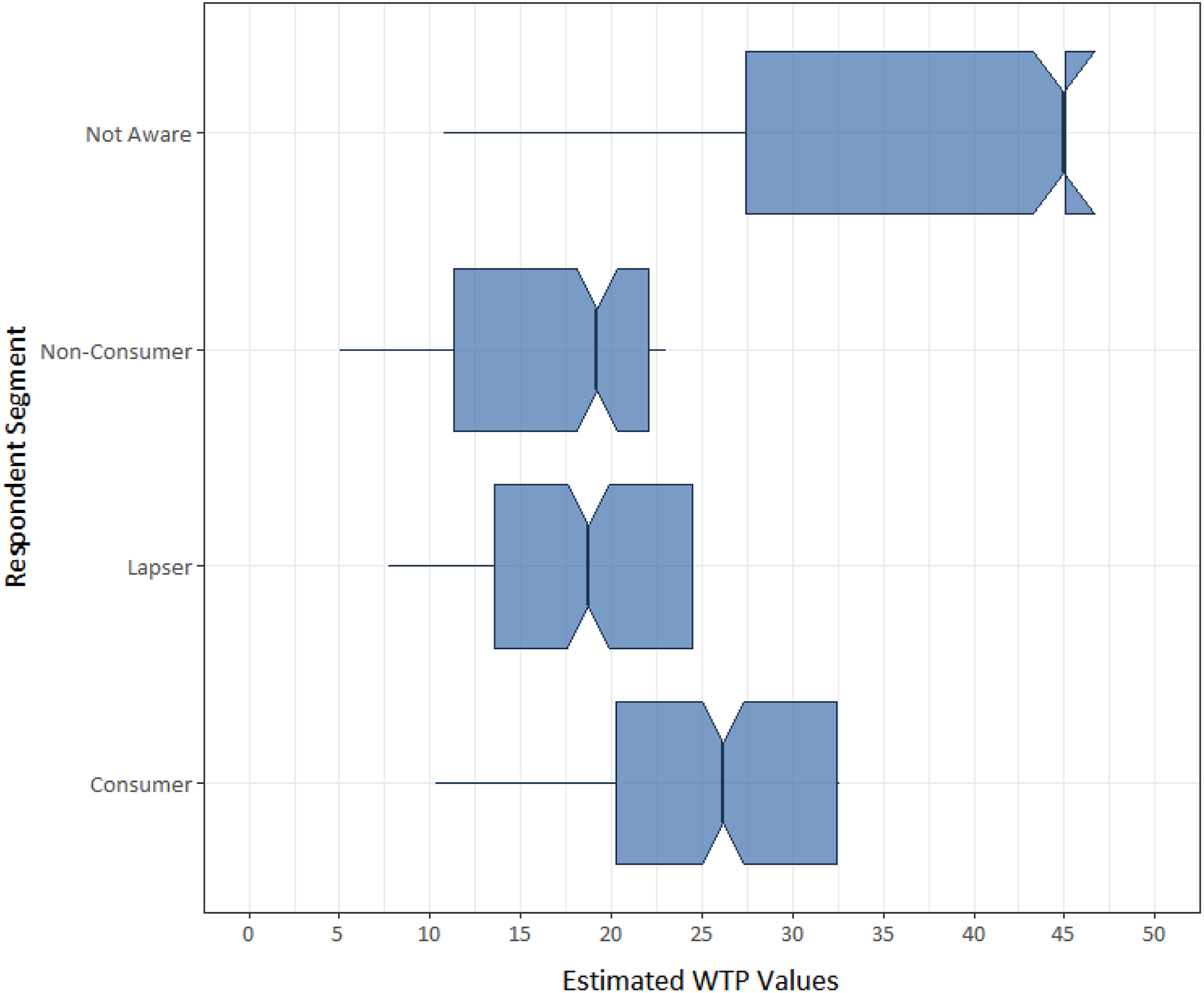

According to Azucena Gracia and Nayga Jr, 39 the external validity of willingness-to-pay estimates from a real choice experiment are improved by breaking out estimates by consumer segment. Table 4 reports the ANA-adjusted mixed logit model for each of the 4 segments. In all segments, the price coefficient is negative and significant but smaller in magnitude than for the fortification and brand attributes. Both the fortification and the brand coefficients are significant and positive in all segments. While the fortification attribute consistently has the largest coefficient, its influence on utility varies by segment. Fortification had the largest on utility in the Non-Consumer segment, followed by the Not Aware segment. Fortification has the smallest impact in the Consumer segment. The relatively greater influence of brand in the Consumer and Lapser segments presumably reflects the fact that these consumers had some previous engagement with Shokti+.

Random Parameter Logit (RPL) Results by Segment (Adjusted Model).

Abbreviations: RPL, random parameter logit; Std. error, standard error.

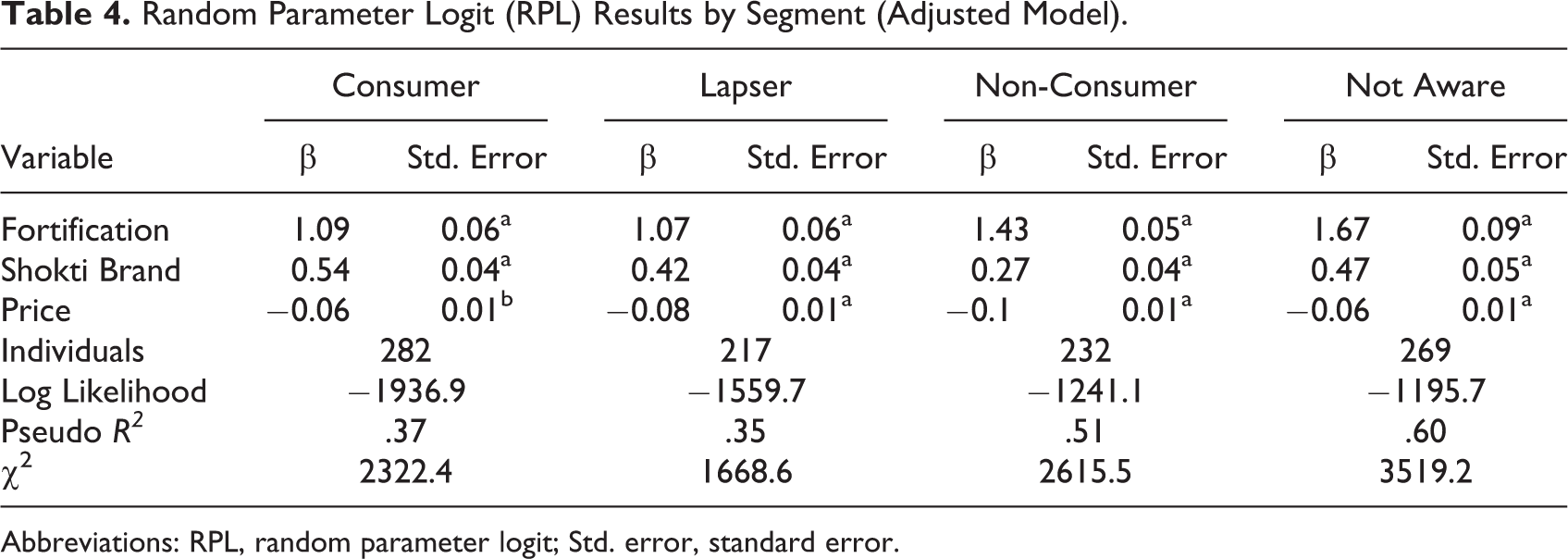

Figure 2 reports the location and distribution of the willingness-to-pay estimates for the fortification attribute of individual respondents. Since the notches of the segments do not overlap, there is strong evidence that the median willingness to pay for each of the segments are statistically different. This is confirmed by the Mood Median test (χ2 = 97.31 > CV0.01,3 = 11.34). The Not Aware segment has the highest average willingness to pay for fortification (37.1 BDT; US$0.45), exceeding the median of all other segments by at least 20 BDT. The median willingness to pay for the Consumer segment is lower (17.3 BDT; US$0.21) than that of the Not Aware segment but greater than that of both the Lapser (12.1 BDT; US$0.15) and Non-Consumer (16 BDT; US$0.19) segments.

Willingness-to-pay values for fortification by segment.

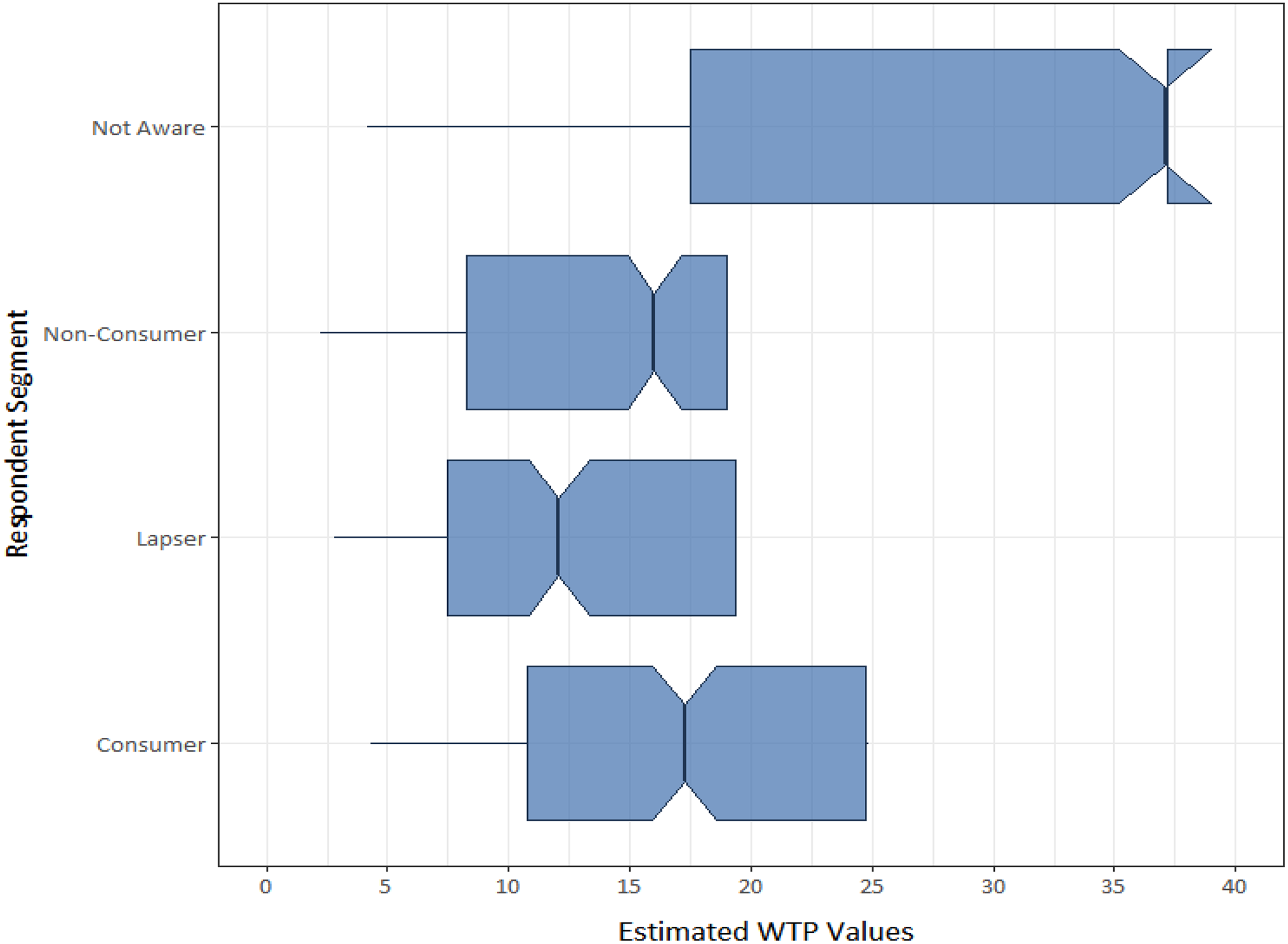

The segment with the lowest willingness to pay for the Shokti brand is Non-Consumers (2.8 BDT; US$0.04; Figure 3). Consumers have the highest median willingness to pay (8.2 BDT; US$0.11), although this is only slightly greater than the Not Aware segment (7.9 BDT; US$0.10). It is both surprising and insightful that respondents who had not previously heard of Shokti+ valued the brand almost as much as those that currently consumed the product. Less surprising, perhaps, is the fact that the willingness to pay of Lapsers (5.2 BDT; US$0.063) and Non-Consumers was significantly lower than that of Consumers. All estimates of median willingness to pay are statistically different (χ2 = 705.39 > CV0.01,3 = 11.34) across the segments.

Willingness-to-pay values (BDT) for brand by segment.

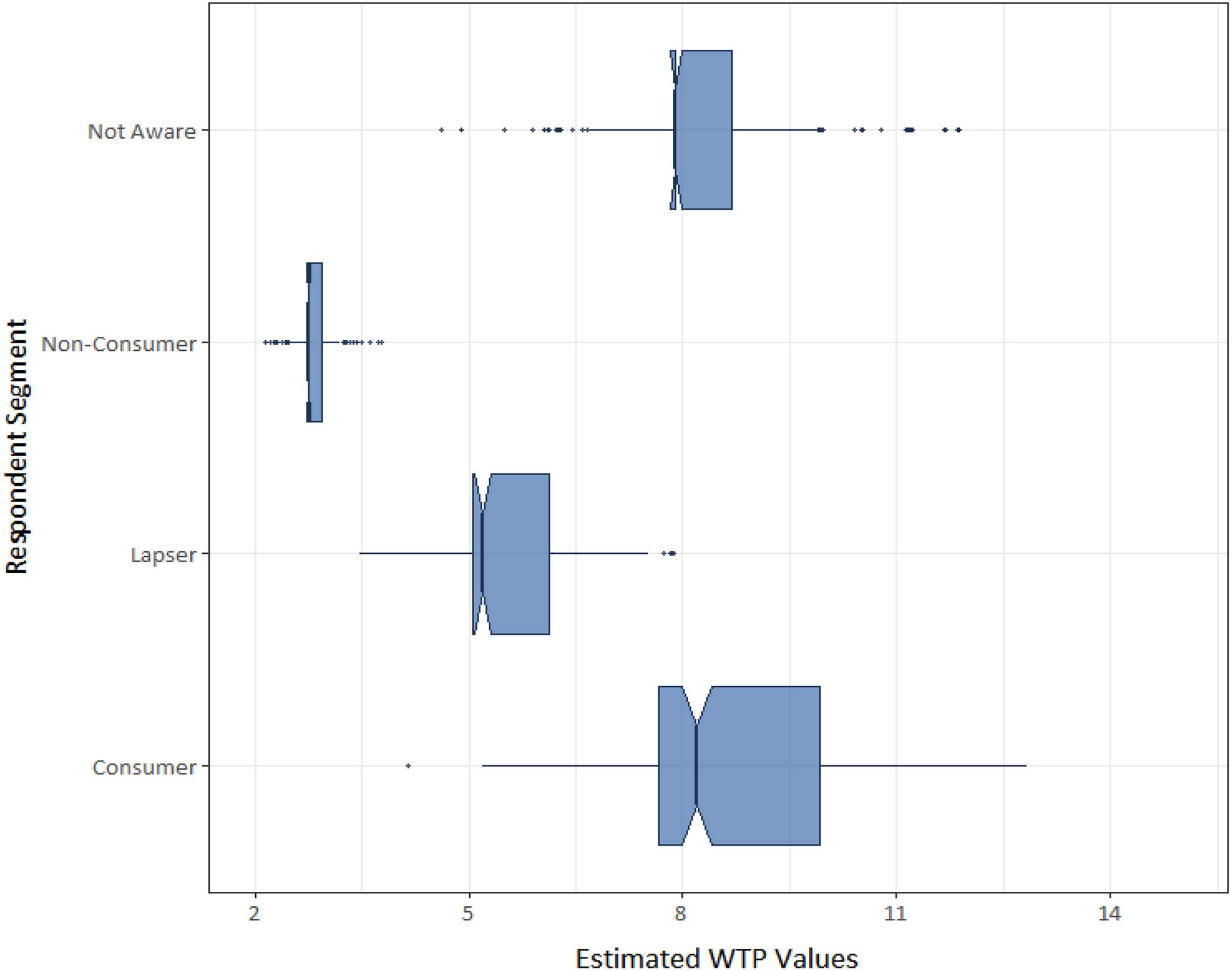

The overall willingness to pay of respondents for Shokti+ can be approximated by aggregating the estimates of willingness to pay for the fortification and brand attributes (Figure 4). The Not Aware segment has the highest median willingness to pay for both attributes (45 BDT; US$0.54). The Consumer segment has the second highest willingness to pay (26.2 BDT; US$0.31), although this is 42% lower than the Not Aware segment. The willingness-to-pay distributions of the Not Aware and Consumer segments indicate that 100% of respondents are willing to pay at least the current market price for Shokti+. Unsurprisingly, the Lapser segment has the lowest willingness to pay for both attributes (18.7 BDT; US$0.22), although this is just marginally lower than the Non-Consumer segment (19.2 BDT; US$0.23). The willingness-to-pay distributions of the Non-Consumer and Lapser segments indicate that only 19% and 5% of respondents, respectively, are not willing to pay at least the market price of Shokti+. All median willingness-to-pay estimates are statistically different (χ2 = 379.93 > CV0.01,3 = 11.34) across the segments.

Willingness-to-pay values (BDT) for Shokti+ attributes (fortification + brand).

Random Effects Model Results

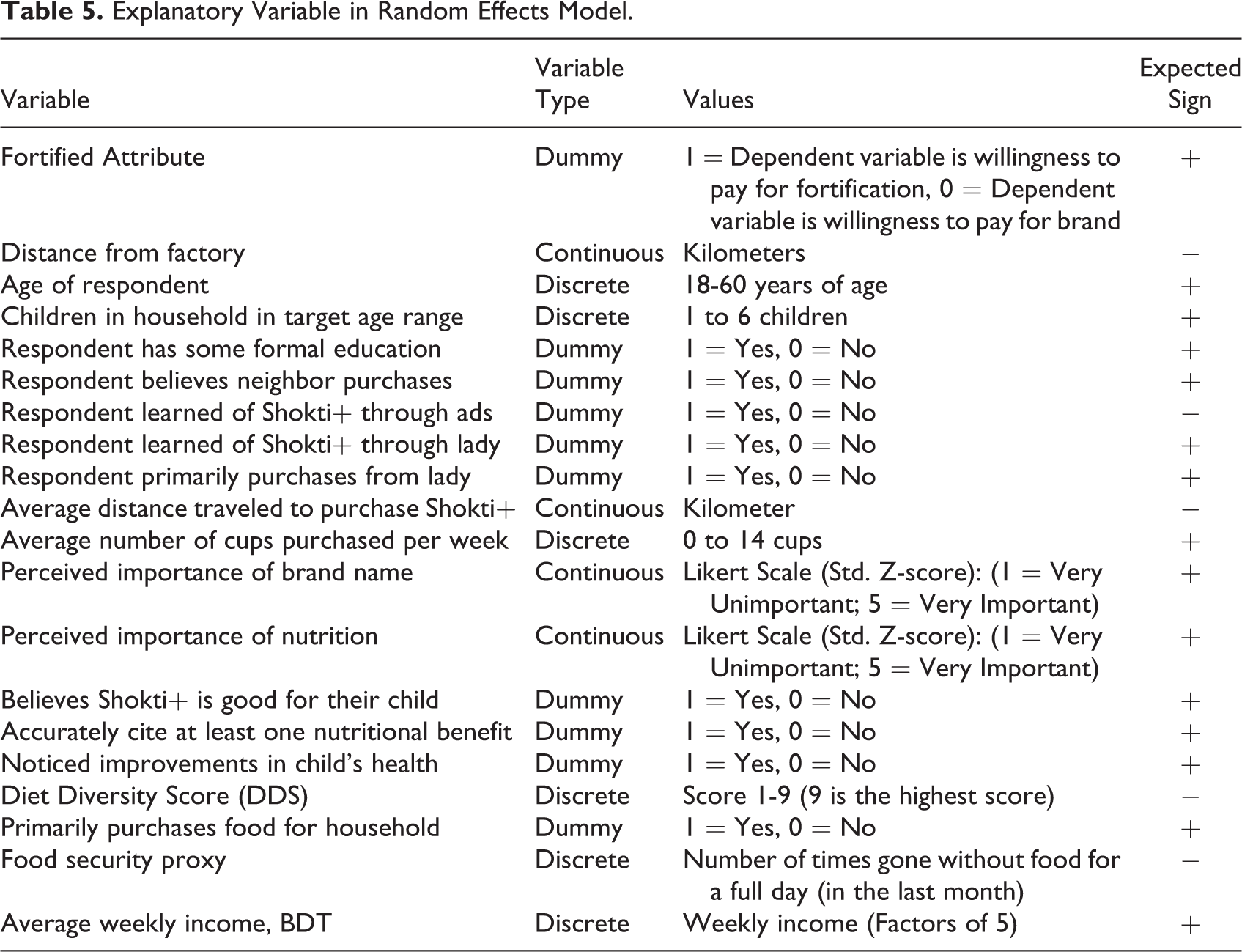

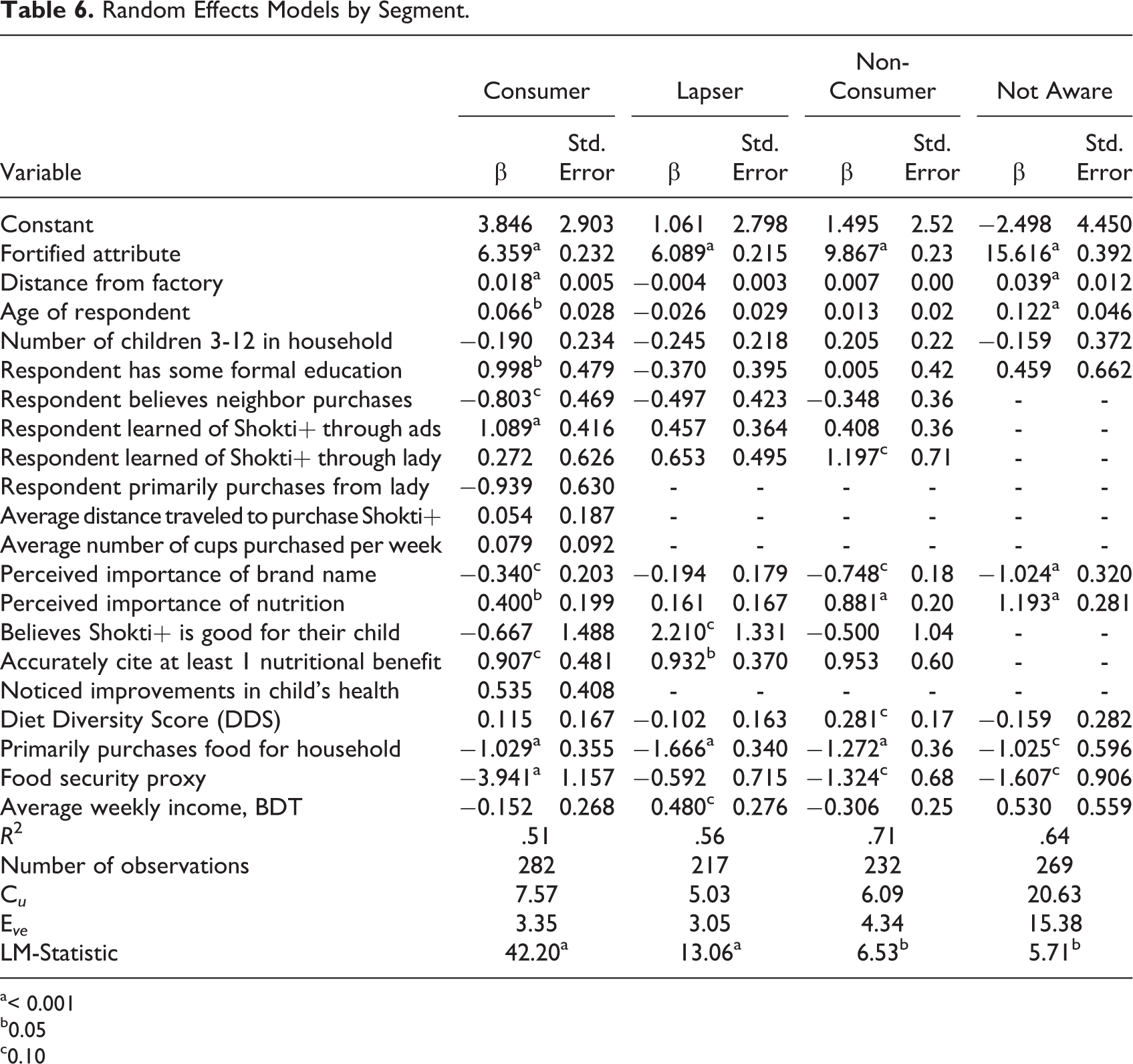

The explanatory variables included in the random effects model with the a priori expected sign for each are detailed in Table 5. The results or the 4 segments are presented in Table 6. The LM-statistics confirm that the random effects model is preferred over a traditional ordinary least squares model for all segments

Explanatory Variable in Random Effects Model.

Random Effects Models by Segment.

a< 0.001

b0.05

c0.10

Factors affecting willingness to pay in the Consumer segment

For respondents in the Consumer segment, the most significant influences on willingness to pay for fortification were related to the level of education, awareness and perceived importance of nutrition, and exposure to marketing messages related to Shokti+. Thus, having some level of formal education and/or having learned about Shokti+ through advertising increased willingness to pay by approximately 1 BDT (US$0.01). Accurately being able to cite at least 1 nutritional benefit of Shokti+ likewise increased willingness to pay by almost 1 BDT (US$0.01). Belief in the importance of nutrition to child health had a positive but lesser impact on willingness to pay of 0.4 BDT (US$0.005). Conversely, the perceived importance of the Shokti+ brand reduced willingness to pay by 0.3 BDT ($0.004).

Having experienced food insecurity in the household decreased willingness to pay by almost 4 BDT (US$0.05). This is, perhaps, unsurprising, since Shokti+ is a snack food and therefore could be considered a nonessential product. Further evidence that Shokti+ was considered nonessential comes from the fact that respondents who purchased the majority of their household’s food requirements were willing to pay approximately 1 BDT (US$0.01) less for Shokti+. Somewhat surprising, however, is the finding that willingness to pay is negatively impacted by the belief that a neighbor is purchasing Shokti+; typically, such forms of social demonstration are expected to positively influence the propensity to purchase a good and to be willing to pay more.

Factors affecting willingness to pay in the Lapser segment

Among respondents who had stopped purchasing Shokti+ sometime in the last 2 weeks, the only factor that negatively impacted willingness to pay was being a household that purchased the majority of its food requirements; this factor reduced willingness to pay by 1.5 BDT (US$0.02). Conversely, accurately citing at least 1 nutritional benefit of Shokti+ increased willingness to pay by 0.9 BDT (US$0.01) while believing that Shokti+ was good for the respondent’s child increased willingness to pay by 2.2 BDT (US$0.03). The Lapser segments was the only one in which income had a significant positive effect on willingness to pay.

Factors affecting willingness to pay in the Non-Consumer segment

The variable having the most significant positive effect on willingness to pay in the Non-Consumer segments was having learned about Shokti+ through the Shokti ladies (1.2 BDT, US$0.02). Belief in the importance of nutrition to child health also had a positive influence on willingness to pay, although this was somewhat offset by the perceived value of the Shokti+ brand name, such that the net effect was only 0.13 BDT (US$0.002). The diversity of the diet of children aged 3 to 13 years in the household were more likely to be willing to pay more for Shokti+. Similar to the Consumer segment, occurrence of food insecurity in the household had a negative effect on willingness to pay of more than 1 BDT (US$0.01) for each additional day the household had gone without food in the previous month.

Factors affecting willingness to pay in the not Aware segment

The most significant factor impacting willingness to pay in the Not Aware segment was the strength of belief in the importance of nutrition to child health. However, as in the Consumer and Non-Consumer segments, the influence of this factor was offset by belief in the importance of the Shokti+ brand, giving a net effect of 0.17 BDT (US$0.002). The age of the respondent and the distance of their home from the GDFL factory had positive but small effects on willingness to pay. As in the Consumer segment, the occurrence of food insecurity in the household and the household purchasing the majority of its food requirements reduced willingness to pay by in excess of 1 BDT (US$0.01).

Discussion and Conclusions

Perhaps the most critical question addressed by the current study is whether poor households are able and willing to purchase Shokti+. The nutritional impact of market-based strategies to reduce micronutrient deficiencies are reliant on the fact that target households have the economic means to purchase nutritionally enhanced processed foods on a sustained basis and that they value the nutrient content (alongside the other attributes) of these products. The commercial viability of the businesses offering such products depends on the consumers’ ability to pay a price that sufficient remunerates the costs of production and distribution to bottom of the pyramid markets. The results of the study provide a positive picture in this regard, indicating that the vast majority of consumers across all 4 segments are willing to pay a price that exceeds the current market price (10 BDT [US$0.14]) of Shokti+. Further credence to this conclusion, and which also negates the possibility that the results of the study reflect instead an endowment effect among respondents, is provided by other data from the questionnaire used in the study; when asked whether they could afford to pay the current market price of Shokti+, 96% of respondents indicated the affirmative.

The appropriate pricing of Shokti+ has been an ongoing challenge for GDFL. First, efforts to increase price in response to rising production and distribution costs (note 1) have been met with reductions in sales; this reflects the acute price sensitivity that typifies low-income consumers. In these times, GDFL recognizes that consumers have turned to widely available, cheaper substitutes that are less nutritious, reflecting the relatively high price of Shokti+ and the fact that it is likely seen by consumers as a nonessential snack product. Over time, however, sales have tended to recover such that the long-term trajectory of market demand for Shokti+ has been positive. Second, sales of Shokti+ exhibit significant volitivity and can decline significantly, given declines in income, food insecurity, and so on. Clearly, GDFL needs to continue developing and finessing its business strategy to be sufficiently robust to remain commercially viable during these downturns in market demand.

The fact that the choices of respondents exhibited nonattendance to the price attribute in favor of fortification suggests that consumers are drawn to Shokti+ by the nutritional fortification (note 2). Furthermore, willingness to pay for Shokti+ is more strongly associated with the fact that the product is fortified than its brand name. The estimated willingness to pay for fortification is positively associated with the ability of the respondents to accurately articulate the nutritional benefits of the product and the degree to which they recognize the importance of nutrition to the health of their children. These findings suggest that the key challenge and priority for GDFL is to communicate in an effective manner the nutritional attributes and associated health benefits of Shokti+. This is especially the case with consumers who are unaware of the product or are aware of Shokti+ but have not consumed the product. Given the credence nature of the nutritional attributes of food, this can be challenging in that they cannot be evaluated by consumers prior to purchase or even immediately following consumption. The fact that willingness to pay was driven by distinct factors across the consumer segments, and especially that the influence of nutrition-related knowledge and attitudes varied, suggests that tailored approaches to communicating the benefits of Shokti+ to target consumers are needed.

The socioeconomic characteristics of the sample segments show that GDFL has been successful at reaching households that are in the second poorest income quintile rather than the poorest. Indeed, Agnew and Henson 28 suggest that the marketing strategy of GDFL may have put Shokti+ beyond the reach of the lowest income households. While GDFL has come to recognize that these households may be better served by publicly funded interventions, there is still significant potential for nutritional impact among households with slightly higher incomes. The results of the study present a positive picture with respect to these consumers. The willingness to pay of 100% of respondents in the Not Aware segment, and 81% of respondents in the Non-Consumer segment, exceeded the current market price of the product. This suggests that, at the time of the study, GDFL had not fully captured the market potential of Shokti+, and there is scope for GDFL to expand appreciably the nutritional impacts of its product. While these households are not the “poorest of the poor,” they still exhibit high rates of micronutrient deficiency, especially in children.

The results of this study have important implications for policies and strategies aimed at reducing micronutrient deficiencies, in both Bangladesh and LMICs as a whole. While the specific results of the study are applicable to Shokti+ in particular, they do possess significant external validity. They suggest that there are commercially viable business opportunities in producing and distributing nutritionally enhanced foods for the poor. However, given the high costs of production and distribution that businesses face, and the income constraints and food security challenges faced by the poorest households, market-based strategies must be seen as complementary to, rather than substitutes for, publicly funded interventions. The results also demonstrate how the factors influencing willingness to pay for nutritionally enhanced foods can differ appreciably across consumer segments, requiring that strategies aiming to promote consumption of these products must be tailored to the particular circumstances and characteristics of the target market. Further exploration is still required of how best to engage market-based approaches in addressing nutritional deficiency. This study aims to catalyze further research into the types of business models and products that can increase the availability of nutritionally enhanced foods to low-income consumers in LMICs.

Footnotes

Authors’ Note

The views expressed in this article belong to the authors alone and do not reflect that of any other agency or of GDFL. J.A. was the student investigator on this research study, completed to fulfill the requirements of the Master of Science degree in Food, Agriculture, and Resource Economics at the University of Guelph. J.A. oversaw the data collection, performed the statistical analysis, and was a major contributor in the writing of the manuscript. S.H. was the principal advisor for this research, oversaw the research design, and was a major contributor to the design of the data analysis, interpretation of the results, and writing of the manuscript. Y.C. contributed to the development of the experimental design. The data sets generated and analyzed during the current study are available from the corresponding author upon request.

Acknowledgments

The authors thank Grameen Danone Foods Limited (GDFL) for their participation and help in facilitating this research project, and for facilitating the study of the business model and providing key information necessary for the completion of this work.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research study was funded under the Leveraging Agriculture for Nutrition in South Asia (LANSA) programme (GB-1-202042) supported by UK Department for International Development (DFID).