Abstract

The present study is focused on the development of industrial working-class households’ economic life cycle, including income, capital savings, and credits in the nineteenth century. The annual household income was low up to the age of 35 of the head of the household. It then rose and culminated when the head of the household was 55–60 years old. The earnings of other members of the family, foremost the adult sons, being entered on the accounts of their fathers, made the annual income increase higher than the daily wages imply. Credits and savings were used to balance long-term consumption.

Research Problem

The present study is focused on the development of working-class income, capital savings and credits in the nineteenth century, a period for which our knowledge regarding savings patterns is relatively limited. The study is concentrated to a rural area situated in central Sweden. However, sources for studying both capital savings and savings in durable consumer goods are difficult to penetrate. It is often therefore necessary to use a combination of sources to establish a proper view of the general development of savings and debts.

The aim of this paper is to map and analyze, the development of household income, capital savings and credits in a period that is characterized by the transition from a noninstitutionalized to an institutionalized financial market. Such an analysis can only be based on sources including the individuals and households in question. This has set certain quantitative limits to the study. The present study will therefore concentrate on the level and structure of individual household savings connected to Bredsjö ironworks, which is situated in the central iron production region of Bergslagen in Sweden. The village of Bredsjö was thus accordingly dominated by the production of wrought and pig iron, while its surroundings were dominated by small-scale farming and activities which were related to the iron industry, primarily charcoal production, and iron-ore mining. 1

The chosen period of study, 1830–1899, is primarily motivated by the desire to penetrate savings and credits in households from a life cycle perspective. To attain an acceptable quantity of individual life-cycle patterns, a long study period has been necessary.

To map total savings, probate inventories have in previous analysis been used as a crucial source. Probate inventories give access to the value of an individual's savings at a given moment, after the person's death. These sources are particularly useful in mapping the savings of the great number on independent peasants in Sweden, since peasants had assets that motivated the setting up of a probate inventory. The probate inventory was not compulsory in the nineteenth century Sweden and there were few probate inventories set up after the death of individuals who did not own land or other forms of capital investments. Among others Håkan Lindgren, Kristina Lilja and Dan Bäcklund have in several articles demonstrated the use of probate inventories to evaluate the development of savings and the business of private lenders. 2

Saving manners among different age-groups, occupational groups and gender in Sweden has been analyzed during the last decades in a handful of research projects. In a study of Falun's savings bank Lilja showed that women not only were more frequent savings banks customers but also had a more long-term saving strategy (over 25 years) than men. It was also common that parents opened saving banks accounts for their children. 3 Lilja's analysis is developed in an article—founded on probate inventories—which indicate the establishment of life cycle structures in individual savings during the nineteenth century. 4

The source material of savings banks and commercial banks have been used to map the savings of different groups of people in different regions. Pilot studies of Swedish savings banks demonstrate that long-term savings in banks was not unusual in urban areas. This material could be used to analyze behavioral patterns in relation to saving, according to gender and age as well as according to social groups. In several publications it has been shown that savers in Swedish savings banks often came from less wealthy people, while this group of people seldom were among the borrowers in the savings banks. 5 The lack of bank credits for these groups were probably a consequence of the high risks connected with this lending and the lack of sufficient collaterals. 6

The importance of children in families’ economic life cycle is treated in a comparative analysis of middle-sized Swedish towns in the 1820s and early twentieth century. The result indicates that children were especially important for the lower social groups, since they could contribute to the family's maintenance as their parents grew older. On the other hand, persons or families without children could exhibit larger assets when they passed away. This indicates the existence of economic life cycle structures also in preindustrial and early industrial societies. 7

The presence of economic life cycles among American industrial workers 1889–1890 has been studied by Rotella and Alter. They especially point at the work of children to strengthen the family income. During the establishment of new families, the debts increased, while the repayment of these debts could be carried through when the children became of age to perform paid work and before they left the parents’ home. This contributed to a long-term stability of the family's consumption. Loans through trade-credits, pawn shops or from family contacts could also be important to stabilize the family's economy. This does not seem to have created any larger economic stress, since it was a well-established system which was commonly used. This research is based on officially collected sources from two impact years and is not built on individual family life cycles but on a large number of families from different age groups. 8 Nevertheless, it is an interesting result for the comparison with the result of the analysis of Bredsjö ironworks, especially since the American workers in the iron industry is an important research-group.

An important contribution to research about the Swedish noninstitutionalized financial market is Håkan Lindgren's analysis of the credit market in the town of Kalmar. With the use of probate inventories, private debts for different occupational groups and for people of different ages are reconstructed. The result indicates that the noninstitutional credits as late as in the 1870s held 75 percent of the local credit market and that this share was reduced to approximately 40 percent around 1900. Thus, the noninstitutional credit market had a strong position through the nineteenth century in Kalmar and probably was even more important in rural areas where banks were not established. In a later article Lindgren develops this research to other geographical areas in south and central Sweden, concentrating on the indebtedness of households. Among other conclusions Lindgren points at the adjustment of consumption over the life cycle, and that savings and borrowing were closely connected to the life cycle. 9

The interest for the noninstitutionalized financial market have also been visible in international research in for example both the U.K. and the USA. Among others Johnson discuss the problems with small or nonexistent savings during the late nineteenth century among the British working class. This can be explained by low wages and uncertain working conditions, but despite this, small amount of capital could be put aside to handle the loss of incomes connected to sickness or unemployment. 10

The driving forces behind savings and life cycle strategies among the working class has also been discussed for Philadelphia (USA) in the nineteenth century. As in the U.K. “savings for a rainy day” was an important driving force, but also saving for old age, for a specific target or for inheritance to the next generation were important grounds for saving. However, the savings were seldom large enough for an ordinary worker to retire totally. 11 These two international examples suggest that the driving forces behind saving was directly linked to the standard of living. With a low income, savings could not be based on any long-term strategy instead savings was connected to immediate problems that could occur, such as sickness or unemployment.

Life cycle strategies in savings has also been analyzed by Bodenhorn for Cornwall Savings Bank (New York). In this study of individual savings banks accounts, Bodenhorn identifies an increase in the family's wealth connected to the first child, while an increase in the number of children had the opposite effect. This also effected the savings patterns. The ability to work and save, deteriorated from around 55 years of age, but there was no explicit retirement age, instead income gradually fell as did the amounts on the savings account. 12

As in Sweden, the analysis of personal savings, and debts in international research have often been based on the bookkeeping in savings banks and other credit institutes and more unusually on probate inventories. However, the possibilities to follow income, savings, and debts on the individual level for a longer period have been quite limited—above all due to the lack of relevant information. Thus, the research in this paper open for a new way of analyzing long-term economic life cycles for individual households.

Neither probate inventories nor savings banks material present a complete picture of the structure of savings and credits and of course not on the personal income situation, for the nineteenth century Sweden. The banks were by then not yet fully established, and traditional forms of savings were still widespread. A common form of savings for workers in rural areas was to deposit a share of the wages in the company where they were employed. Since this capital could be interest-bearing, as in Bredsjö ironworks, this was an alternative to bank savings. An important advantage compared to banking savings was that the saverś capital was readily available, while deposits and withdrawals from a bank only could be done a couple of hours per week and in a bank situated several kilometres from Bredsjö.

Both probate inventories and banks accounts involve some problems with the representativity compared to the population as a whole, which must be delt with through statistical methods to avoid bias in the analysis. If the aim is to reconstruct individual economic life cycles with savings as well as debts and the role this had in the family's long-term development, it would be preferable to proceed from individual/family accounts. Such accounts can be compiled in the bookkeeping of several Swedish iron and steel companies during the 18th and nineteenth century.

In this micro analysis the company's bookkeeping will be tested for the reconstruction of householdś economic life cycles. Thus, this paper aim both at analyzing family's economic life cycles, as well as testing a new research methodology.

The basic sources in the company's bookkeeping are gathered in the avräkningsböcker (settlement books) which include the employees’ personal accounts as well as financial summaries with customers and suppliers. The personal accounts include works and payments on one side of the account and cash withdrawal, purchases from the company store and other expenditures on the other side. With this information it is possible to reconstruct daily wages as well as annual income, savings in and debts to the company—all necessary for the reconstruction of an economic life cycle.

Consumption Theories and the Life Cycle Structure

Already in 1936, J M Keynes formulated a theory on the connection between consumption and savings in The General Theory of Employment, Interest and Money. Keynes argued amongst other things that the starting point for consumption analysis should be the disposable income of the household, not the individual income. He also noted that short-term income increases seldom led to a higher consumption (higher marginal propensity to consume—MPC) whereas a long-term income raises tended to do so more often. Keynes also noted that the tendency to save capital increased with the size of the income. 13 These relatively general discoveries were fitted into a wider theoretical frame that became the foundation of the consumption theories that developed after World War II.

The Life Cycle Theory

The Life cycle theory has been the most influential of the consumption theories suitable for empirical testing. The theory rests on the hypothesis that individuals plan consumption and savings over a longer period, in order to distribute their consumption over time in the preferred manner. The motive for this behavior is that the individual/household wishes to be insured against a lowered income, so that an even level of consumption can be maintained. 14

The first and foremost advocate of this view was Franco Modigliani, who, together with Richard Brumberg has developed the life cycle theory further. One of their claims is that individuals are expected to set aside means especially for old age, as the incomes then cannot be expected to remain at the previous level. 15

The theory of Modigliani and Brumberg is built on several assumptions, which in practice are difficult to confirm.

One of the conditions is that the individual not only can predict the pension age but also his/her time of death. This knowledge is necessary for the individual to be able to set aside the correct sum of money during the period of activity in working life. The difficulty of correctly predicting these things makes it impossible to calculate a total life income, against which the consumption has to be balanced.

16

Total life consumption is financed by life income plus inherited means, i.e., inheritance is declared to be part of the income base.

17

This assumption is another dubious one. It cannot be held to be sure that inherited means are consumed. On the contrary, there tends to exist a saving which is aimed at coming generations, i.e., children and grandchildren. The existence of national social insurance is another problem for the life cycle theory. When the responsibility of insurance has been transferred from the individual to Society, the basic motivation of savings has, according to the life cycle theory, been reduced. This statement is problematic when applied to developed economies in modern society. However, when applying the theory on historical material, it can be assumed to be valid.

Depreciation of money is another problem, which the theory fails to discuss, but which is important for the analysis of individual savings. The twentieth century has supplied us with several examples of a lowered tendency to save in periods of heavy inflation. The best example is the German hyperinflation of the interwar period. The yield of traditional saving did not keep up with the inflation, and capital saving was thus considered unwise.

During the last decades empirical evidence has been used to complement and augment the life-cycle theory. It has been demonstrated that the motive for saving is no longer a need to secure retirement, but rather the wish to leave an inheritance. The increased tendency for the older generation to save can thus be explained. Another motive for the older generations’ savings is the fear of sickness at old age. 18 However, in a simple form the Modigliani/Brumberg's life cycle theory has been used in the analysis of customers in small town savings banks and gives some confirmation for the theory. 19

The Permanent Income Hypothesis

The permanent income hypothesis was developed by Milton Friedman in the late 1950s. Although this theory has often been viewed as a competitor to the life cycle theory, there are great similarities between the two theories. Both assume the individual strives to distribute consumption evenly over time, based on the expected life income. The permanent income hypothesis, however, assumes that the consumption level is dependent on long-term—permanent—income, and not on the present income level. 20

What separates this theory from the life cycle theory is thus that the individual is not expected to consume inherited property but keep it intact. On the other hand, income from interest is included in permanent income. When the income fluctuates, the individual must consider whether this is a permanent change. Nonpermanent income increases are expected to affect consumption only marginally. During periods of stable inflation, increases in salary will be viewed as a normal characteristic of the economic system. The estimation of the permanent income in such circumstances will be based on last year's salary, together with the increase of the present year, and also with some consideration of future expectations. 21

A temporary income change, according to the permanent income hypothesis, will in the short run lead to an increase in saving. The object of maintaining a stable consumption level will, when temporary improvement of the income occurs, tend to adjust the consumption to the permanent income and not to the present condition. The permanent income hypothesis, in line with the life cycle theory, thus attributes an ability to stabilize the business cycle to saving, as the increase in salaries is normally more accentuated in a boom period. 22

The most important difference between the life cycle theory and the permanent income hypothesis lies in the role of property. The former assumes that this capital is part of the life income, while the latter assumes that it does not have to be used for consumption. The life cycle theory moreover devotes more attention to the motives behind saving than does the permanent income hypothesis. Another major difference lies in the view of temporary income fluctuations. According to the permanent hypothesis such fluctuations only affect saving, while the life cycle theory claims an increase in both saving and consumption to be likely.

Analytical and Methodical Foundations

The basis of all consumption analysis is the definition of saving. Consumption theories separate capital savings

Studies of present conditions in Sweden give a relatively homogenous picture of the development of household savings over a lifetime. In the youngest household cohort, saving could even be negative, as the result of low salaries and a high share of school children in this group. Savings, expressed as a share of the income, increase gradually, up to the age of 50–60 years of the head of the family. After that age, savings again begin to decrease. The capital savings of families with children are not remarkably low, while on the other hand the savings in durable consumer goods are lower than for other cohorts. 24 This very general conclusion will of course in reality be affected by several factors, one of which is the business cycle, and another factor is rate of inflation/deflation. These factors lead to accentuated consumption changes.

In the present study the focus lies on the economic life cycle in a rural area in the nineteenth century. It is a pilot micro study, which in the future can be used as point of departure for a more comprehensive research project on households’ life cycles in the period of transition from a rural to an industrialized economy and from a noninstitutionalized to an institutionalized financial economy dominated by savings banks.

The study is based on material from 13 households, in which the heads of the families were workers or skilled workers in the ironworks of Bredsjö. They were all employed in the production of pig-iron, but since this production only was realized during a part of the year, the head of the household—as other household members—also were employed as day shifts workers. The incomes of the individual household members were, during the nineteenth century, entered in the company's books under the name of the head of the household. This meant that children and foremost adult sons who worked for the company and lived with their parents lacked an account of their own in the company books. 25

For a person/household to be included in this life cycle analysis a long-term employment in the company is needed. The lower limit has been sat at 25 years, something which has limited the number of households in the study.

The economic environment of the Swedish ironworks in the late nineteenth century corresponds relatively well to the theoretical assumptions of major consumption theories:

The economic system of Bredsjö and other nineteenth century ironworks was a closed-circuit system. Wages were normally not paid in cash, but in kind, evaluated in Swedish currency in the company's bookkeeping. These currencies have been recalculated to Swedish crowns (SEK), which became the currency in 1873. The employees took their everyday commodities from the shop of the ironworks, and the cost of these items was then subtracted from the wages. At the end of the year the balance was transferred to next years’ books. Cash was rarely in circulation, except for withdrawals from the personal account for specific reasons, such as “cash for medicine.” Transactions were instead balanced on the account with a positive or negative result for the employee at the end of the year. This system was totally dominant for persons with a stable long-term employment but was from the 1880s gradually transformed to a more money/cash related economy. In this article the individual/household accounts are the basis for the analysis. With this material it is possible to reconstruct annual income as well as savings in and debts to the company. It is obvious that the company upheld the position as a bank for the employees, giving them 5 percent interest rate for capital on their accounts, while their debts were not charged with any interest rate. This reduced the incentive for the employees to deposit their capital in a bank. Thus, the employee's economy was based on an open account which made it possible to both save and borrow capital and thereby ward off periods of low incomes. The personal accounts also make it possible to reconstruct family income over longer periods, which is of great importance for the construction of a life cycle pattern. The closed-circuit structure of the iron industry also made it probable that cash seldom was transferred to institutions outside the ironworks.

26

The existence of inherited capital is very difficult to prove. It is however clear that an employee, when he took over his father's rented cottage, also took over his balance in the company books, whether it was positive or negative. The capital involved was however seldom substantial. Inheritance beside this type of transference has not been either proven or refuted. Analyzing the incentives for savings that are so important above all in the life cycle theory, implies that historical material should be especially interesting. The social insurance of the period was not so extensive, and this must have been an incentive not only to save, but also to set aside capital for retirement. Although there was no specific retirement age, the employees could not be expected to continue with the heavier working tasks as they grew older. It is also reasonable to assume that the number of working days carried out by the head of the family decreased as he became older.

Employees, Households, and Income in Bredsjö Ironworks

The Employees

The Bredsjö ironworks was already from the establishment in seventeenth century concentrated on the production of pig- and bar-iron. This production was based on the use of charcoal, which during the nineteenth century was nearly totally obtained from the company's own production. Apart from the specialized employees in the iron production, the company was also dependent on a group of day laborers which could be engaged in different areas of the company's activities, iron production and charcoal production, farming as well as mining or building activities. The day laborers can be divided in two different groups, those—often wandering workers from other geographical regions—which were employed for shorter periods and specific projects, and those with a permanent position as day-laborer at the company.

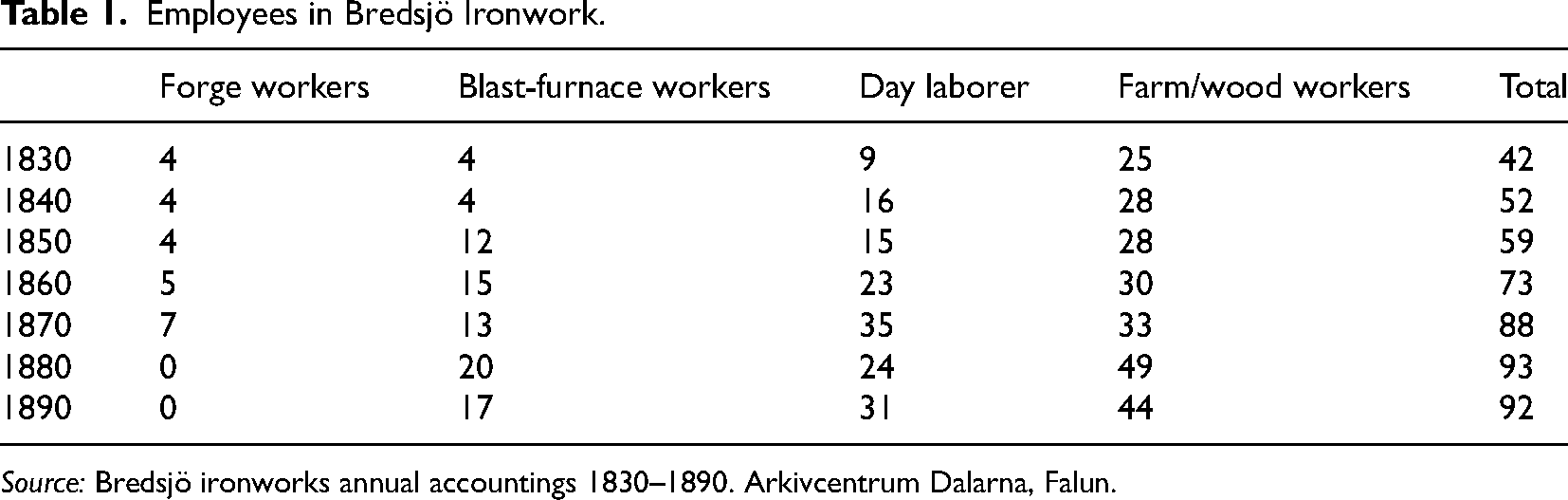

Most of the ironworks employees were categorized in the company's bookkeeping with distinct descriptions of the work tasks. In some cases, the bookkeeping lacks the company's categorization, and I have then categorized the employees according to their work description. The company's employees can be classified in four groups according to their basic assignment; forge workers, blast-furnace workers, day laborer, and farm- and woodsman (see Table 1). Employees at the forge were regarded as the most qualified, even though qualifications depended on their specific work-tasks. Blast-furnace employees also had a comparatively qualified work, while day laborers and farm- and wood workers had more unqualified work-tasks. The requirements of workers qualification were also reflected in the size of wage payments. However, since all employees had a mixture of work-tasks dependent on the time of the year and the weather, wage payments could fluctuate for both employees at the forge as well as day laborers. Especially the day laborers demonstrated a large variation of both work-tasks and wage payments forms. In this article I will focus on the long-term development of the blast-furnace workers’ (also working as day laborers) income, indebtedness, and savings. 27

Employees in Bredsjö Ironwork.

Source: Bredsjö ironworks annual accountings 1830–1890. Arkivcentrum Dalarna, Falun.

Most employees at the Bredsjö ironwork performed comparatively unqualified work-tasks. Farm and wood workers were above all responsible for the production of agricultural commodities, the production of charcoal and chopping wood on the company's own forests and deliver it to the ironwork. With the shutdown of the forge (bar-iron manufacturing) from the 1870s and concentration to the production on pig-iron, the demand for charcoal increased, as did the number of wood workers. The number of day laborers and employees at the blast-furnace also increased as the production for pig-iron was doubled.

To gather a large enough number of households for this analysis the chosen period, as I have already mentioned, is rather long. The workers that have been chosen started their employment in the company between 1830 and 1868, and by 1899, which is the last year of the study period; three of the workers were still employed by Bredsjö ironworks. Since the analyzed households were active during different parts of the nineteenth century, it is impossible to avoid certain changes in the level of wages, due to inflation and general wage increases. As the increases were not substantial, the analysis is however deemed to be of some value. Had it been possible, it would have been preferable to choose individuals who were born in the same year and who had started and terminated their employment in the company approximately at the same time. It would then have been easier to uncover the structural changes that affected the actions of the individuals/households in question. 28 However, the number of employees is too low to perform such analysis.

Changes in Annual Income

Wage payments were based on three different types of frameworks; 1) Wages based on piecework—for example workers at the forge and from the 1850s also employees at the pig-iron production were remunerated in proportion to quantities produced. 2) Time-related wages—primarily day-work—were used for several groups of employees, primarily day laborer, but more or less all employees during a year had some part of their wages in relation to working time. 3) Some occupations were also valued in fixed payments, often as annual remuneration. This wage system was used especially for those with a stable employment in the company's farm and wood activities, such as farm hand, forester, or miller. Beside these three forms of wage payments special payments—tips—were occasionally paid out to the employees. This was especially frequent for employees within pig- and bar-iron production. This show that the actual income also depended on the employee's qualifications and skill.

On special occasions temporary social remunerations were paid to workers with stable employments—often to tenants in the company's houses. One such occasion emerged in the middle of the 1850s when increased inflation led to subsidies from the company to several employees. Another occasion came in the late 1850s when all employees at Bredsjö ironworks were given notice, just to be employed again shortly thereafter. However, as the employees new accounts were opened, some of their debts were reduced. These special social remunerations have not been included in the calculation of the employee's income.

The changes in annual incomes depended on the development of wages and the number of working days. The variation in daily wages can be attributed both to changes in the business cycle as well as in productivity. When the work was performed at piece rates it has, with the help of previous research and past time instructions, been recalculated to daily wages. Other factors that affected the wages were general revaluations of the work tasks, personal qualifications and above all the workers change of assignment.

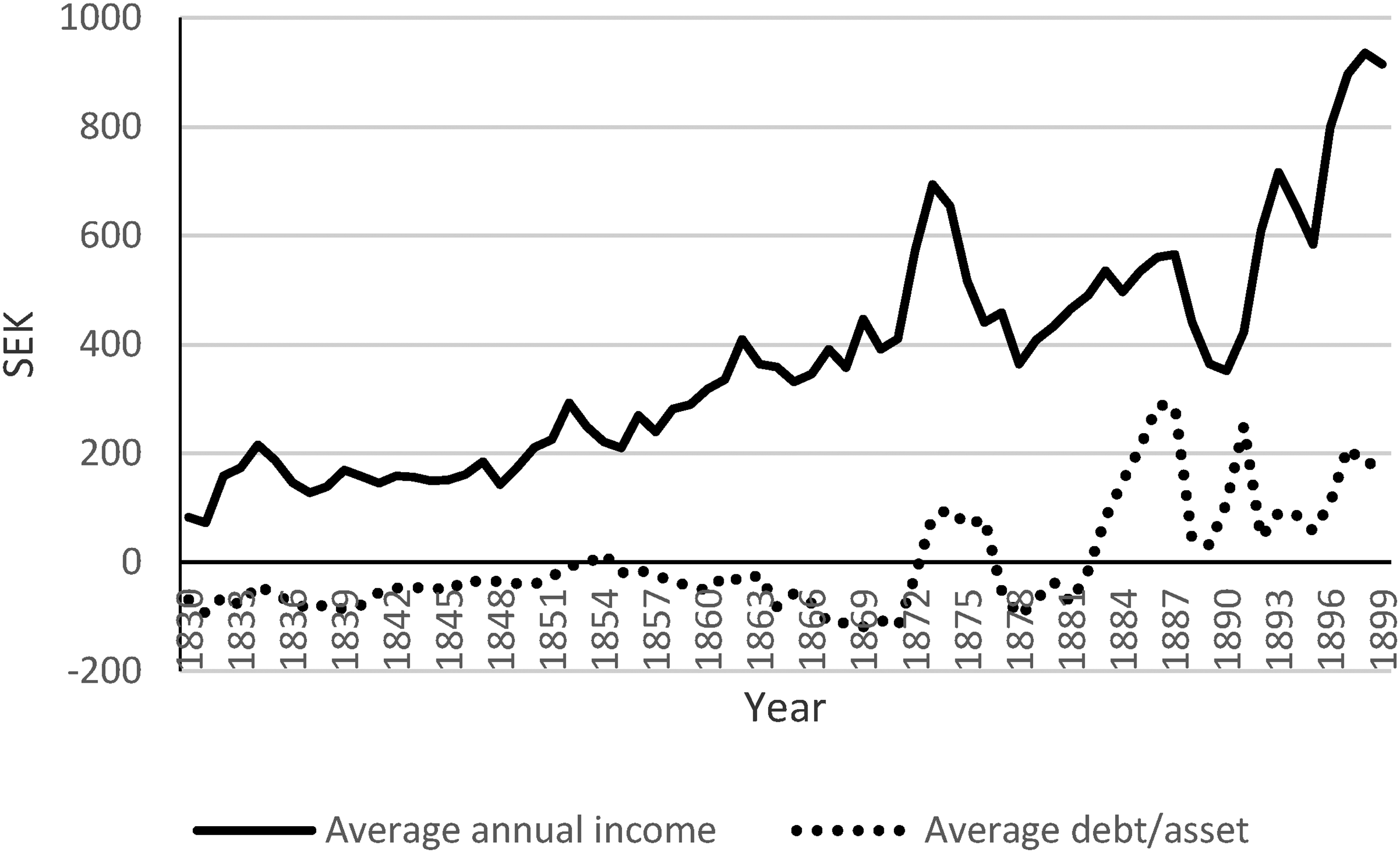

The average annual income for the analyzed households indicates an increase between the 1830s and 1890s (see Figure 1). Fluctuation in the annual income was to some extent directly connected to changes in the business cycle. The Crimean war (1853–1856) and the French–Prussian war (1870–1871) resulted in increases in income, while the economic downturn periods in the late 1870s and late 1880s led to a drop in annual income (see Figure 1). The fluctuations in economy and income also resulted in a better solidity for the employees/households. Up until the early 1870s the average employee showed a debt to the company, but with the boom in the 1870s and the successive inflation the balance went in favor of the employees, just to drop again towards the end of the century. But after this downturn the average employee exhibited a positive balance on the account.

Average annual income and debt/asset in SEK for 13 households.

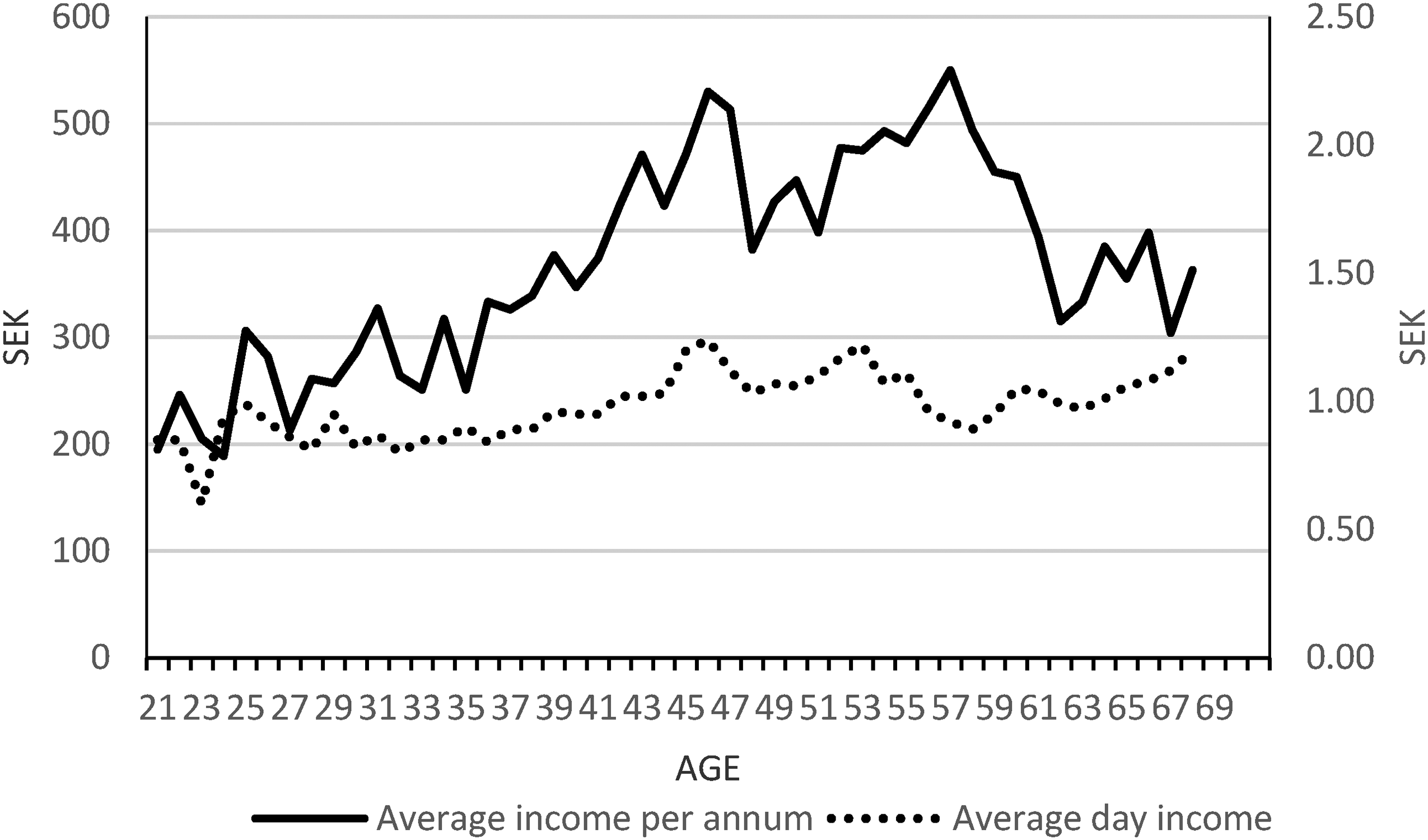

Obviously, the business cycle played a decisive role for the development of the employee's income. But of the greatest importance for a household's annual income was also how many household members that were engaged as wage workers. A comparison between the average annual income and the average day-wage gives us an overview of this, especially if considered over the lifetime of the employee (head of the household). This demonstrates that the variations in daily wages were relatively small over an entire working life (less than half a SEK per day), compared to the variations in annual income (see Figure 2). It can thus be concluded that changes in daily wages cannot explain the entire variations in annual income.

Average daily income and annual income for 13 households, based on the age of the head of the household.

During the first 15 years of employment the difference between annual average income and average daily income was not that extensive. But from the age of around 35 the annual income started to increase faster, to culminate in the age of 45–58 years for the head of the family. The average daily income also increased during this period but at a much slower rate (see Figure 2). Thereafter, the annual income fell sharply from 550 SEK per annum to stabilize around 350 SEK (see Figure 2). This is hardly surprising. From the age around 60+ the work capacity of the head of the family most likely fell. A bit surprising however, was that the daily income at the same time increased. But this could be explained by the work of other persons in the household.

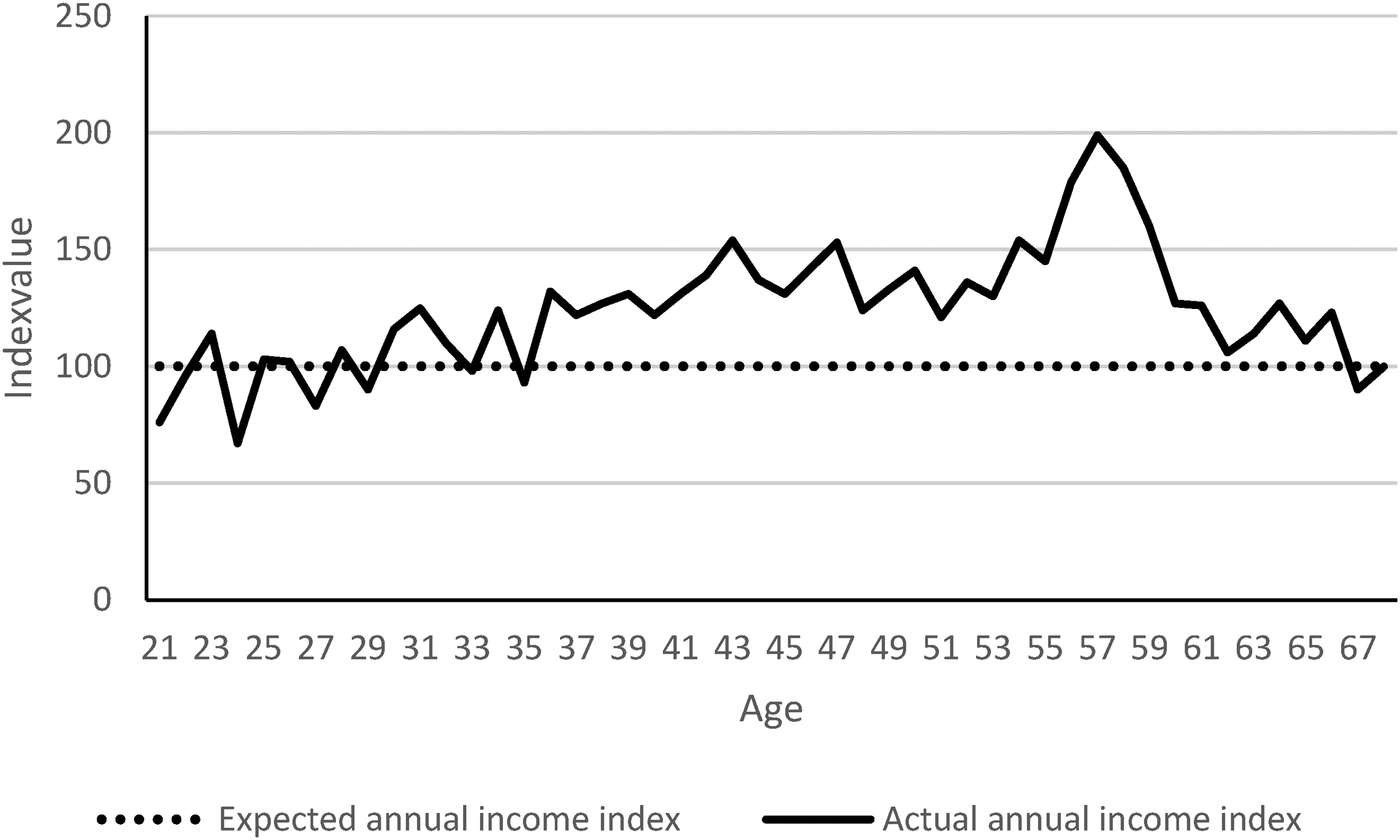

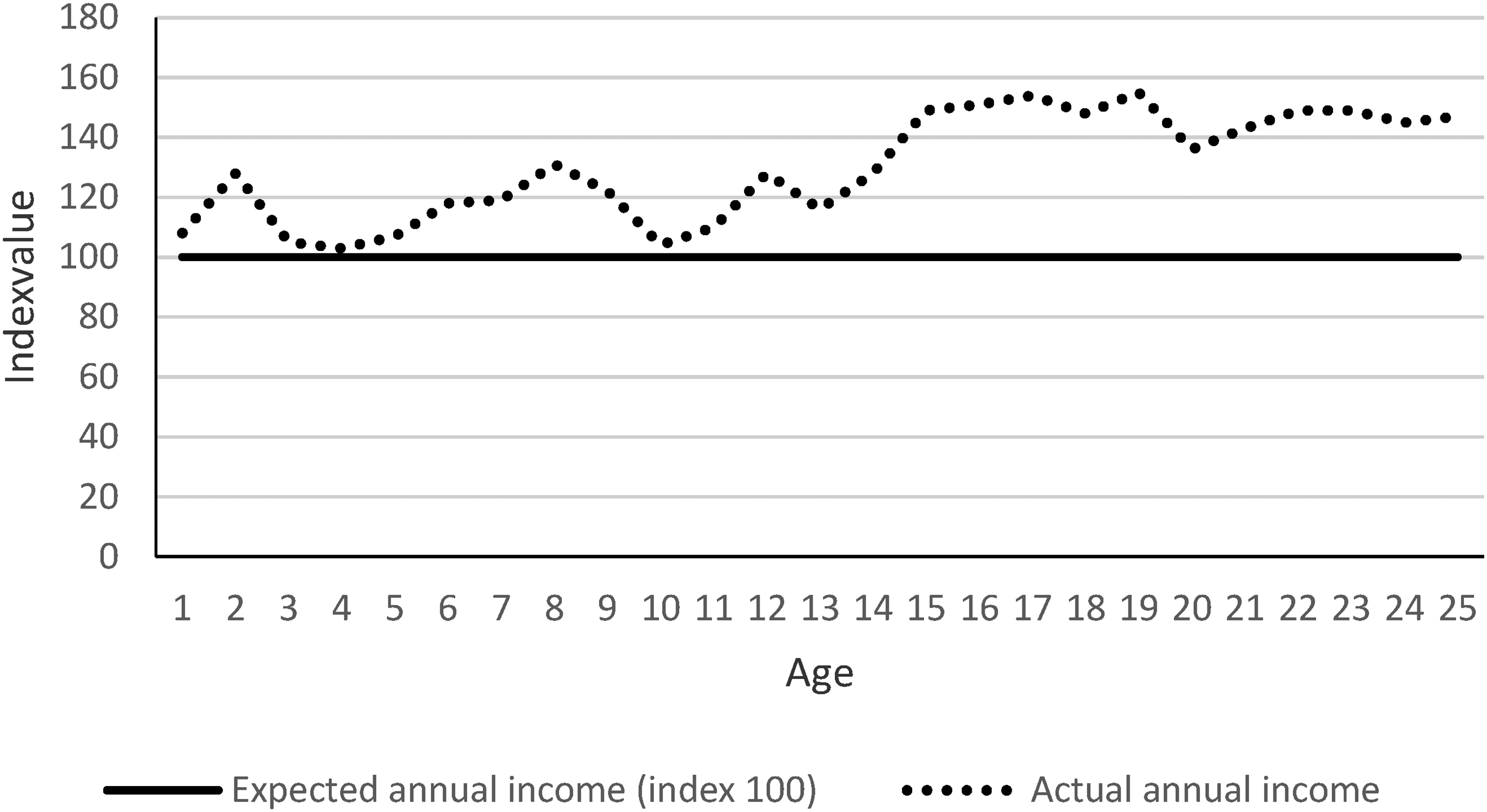

The variations in annual income give rise to the hypothesis that the number of working days put in by each household determined the annual income. This hypothesis is confirmed by a comparison of the actual annual income in relation to the expected annual income, i.e., the daily wages×300 (see Figure 3).

Index-linked expected and actual income for 13 households. Index 100 = Expected annual income (daily wages × 300 days).

During the first 15 year-interval of employment with the company (age 21–35), the average actual annual income was more or less on the same level as the expected income. This point to the conclusion that the households, in the period of establishment, were strongly dependent on the work of the household's head.

At the age of 35, a slow increase of the actual income in relation to the expected income started. This development reached its peak at an age of 55–60, when the actual income was double of the expected income, something that indicates a substantial change in the structure of paid working time within the household. Paid hands—hired by the head of the household—could have worked for the company, but this was quite unusual, and their wages were entered on the account of the household's head. On some occasions women of the households also worked for the company. The most common situation, however, was for the sons of the family to work for the company, their income being entered on the account of the father.

The sons of the families often stayed in their parent's home well into the age of 20–25 years. It was not unusual that one of the sons—often the oldest—succeeded the father as tenant and continued to work for the ironworks. This opened for a stability in the leasing of the company's tenancy and made it possible to keep good workers employed.

The importance of working family members can be studied through the development of household incomes in relation to the age of the oldest son of the family. During the first ten years of the son's life, actual income closely followed expected income. But when the oldest son reached the age of 14, the actual income increased, and by the age of 16, the highest actual income of the household in relation to the expected income was noted (see Figure 4).

Expected and actual income for 13 households related to the age of the oldest son.

The highest income level for the average household was reached as the number of household workers increased, then lasted for a period that foremost depended on the number of employed sons and the time they stayed in the parent's household. The conclusion is that the work of children was fundamental for the annual income of the household. This does not necessarily mean that savings increased. Children caused increases in consumption that were not always covered by the increased income generated by their work.

The same conclusion is drawn by Lilja and Bäcklund in a comparative analysis of Swedish towns in the 1820s and 1900. Towards the end of the nineteenth century the cost of having children had increased compared to the 1820s and the economic importance of children decreased. They argue that this could be a reason why the number of children especially among more skilled workers that were well off, declined towards the late nineteenth century. 29

Reconstructing the Life Cycle Economy

Changes in Savings and Debt

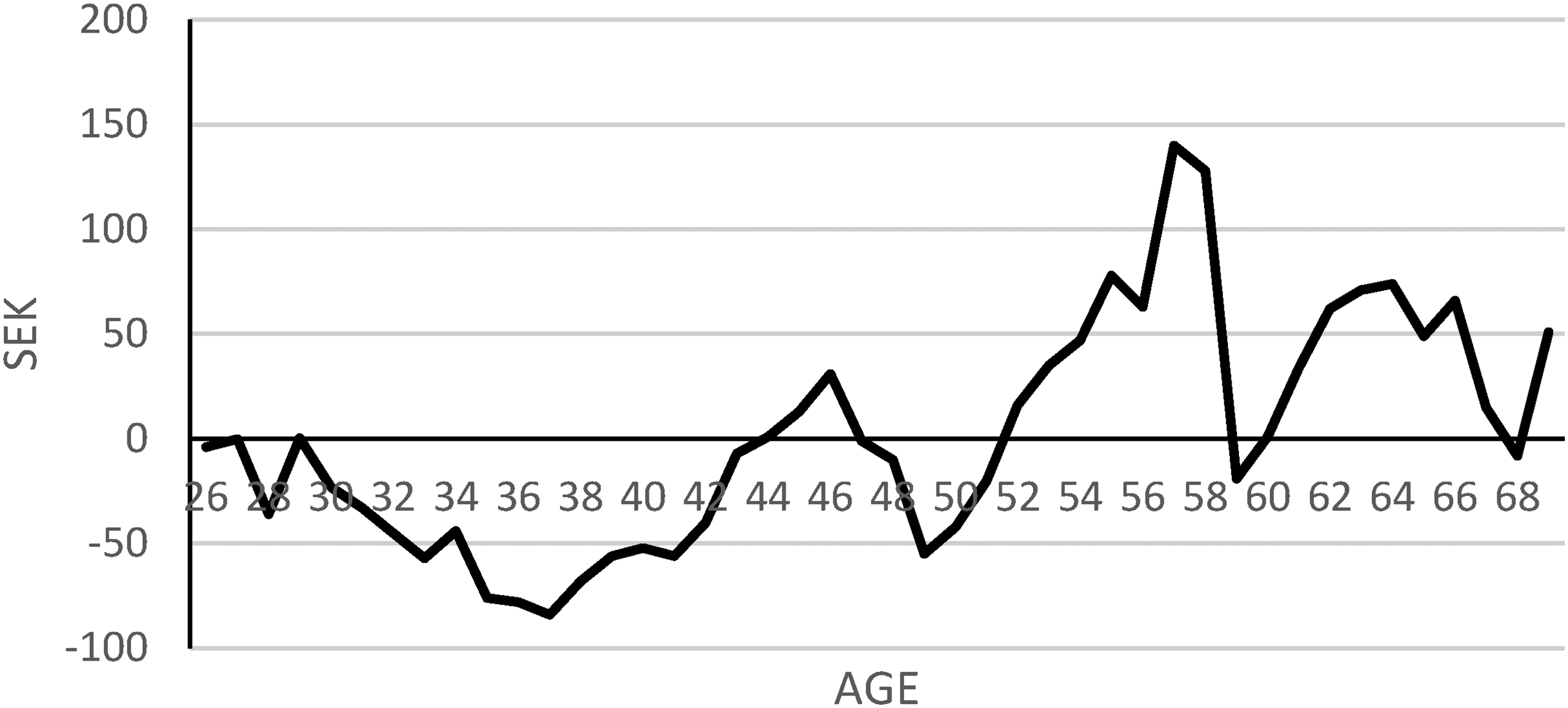

The extensive change in the size of the annual income during the first decade of a person's employment does seem to have affected the development of savings, as it appeared in the assets and credits of workers. At the age of 25–35 years there was no substantial saving, instead for several years the average studied household was indebted to the company (see Figure 5). This was caused by the consumption of goods exceeding the annual income. However, the variations between households were extensive. Since the employee's personal accounts were open—allowing both savings and borrowing—it was easy to compensate loss of income with loans from the company. These credits were repaid as the personal economic situation improved—when the oldest son began working in the fathers account. The employee's open account with the company, probably made it easier to establish a family, compared to most other employments, were the worker had to rely on their income or private loans.

Average credit/asset in SEK for 13 households according to the age of the head of family.

It was not unusual that small loans circulated among the working-class. These were mostly used to overcome short-term income shocks, for example when the household could not provide labor. The loans were often circulated between households, which made social networks an important asset. 30 An open economic account at the company reduced the need for these types of loans.

The average savings increased after the age of 40, and saving was then—with some exceptions stable until the age of 68. The fact that the saved capital did not begin to shrink before, was an effect of workers continuing to work for the company despite their higher age. Workers did not become pensioners in the respect that they lived of capital set off for retirement, in line with the discussed consumption theories. It was not unusual that one or several sons continued to work at the father's account.

It can be claimed that both the life cycle theory and the permanent income hypothesis gain support from the results. A period of limited or nonexistent saving was followed by a period of increasing saving, and although the study doesn’t actually show this, it can be assumed that the saved capital was consumed after retirement. The study also demonstrates that the households, in spite of a low income, had the possibility to save. Considering the changes in the rate of inflation/deflation it is difficult to directly relate the average savings to the annual income. But it is most likely that the increased savings was closely related to the increased work of other household members than the head of the household. The average saving of a household, at the age of 55 of the head of the family approximately equaled 4–6 months of expected income. Thus, a bit more than “saving for a rainy day.” But the variations between the monitored families were extensive. It is obvious that individual extreme values strongly affected especially the average savings. This is also displayed when the median of debt/savings are presented in Figure 6.

Median credit/asset in SEK for households in Bredsjö and Vällnora according to the age of the head of family.

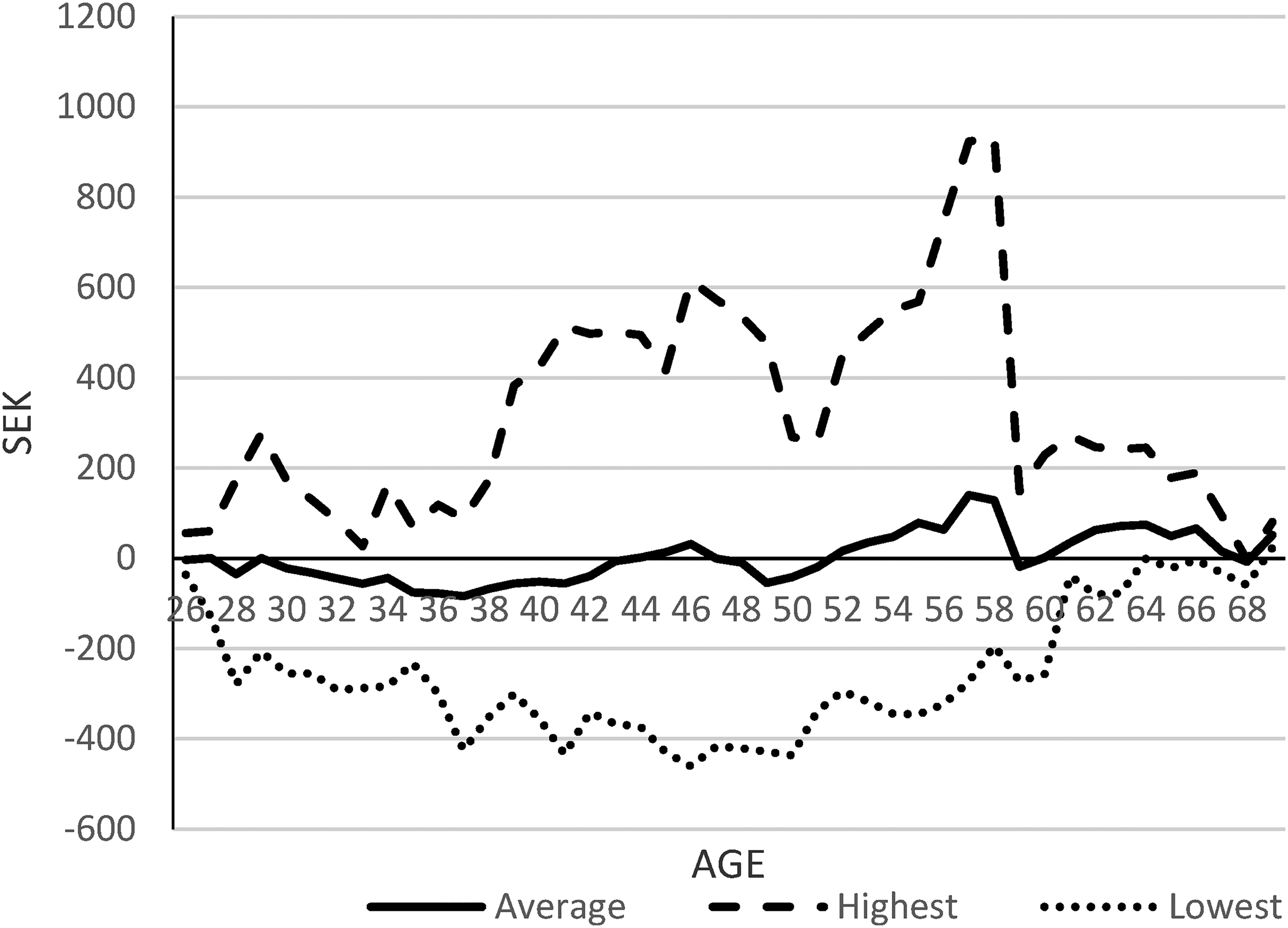

Even though the average values indicate that the workers were in debt until the age of 43, and that there were households indebted for their whole life cycle, there were also households with an extensive asset in deposit at the company. The largest deposits were noticed in the mid 50 years of age, with an asset of over 900 SEK (see Figure 7). This equaled three annual incomes for an ordinary employed, working 300 days per year. This is an impressive sum which could secure a person's survival also after retirement. It is also more than the average one-year income that were saved on personal accounts in American small-town savings banks. 31

Highest asset and lowest debt in SEK for 13 households according to age of the head of family.

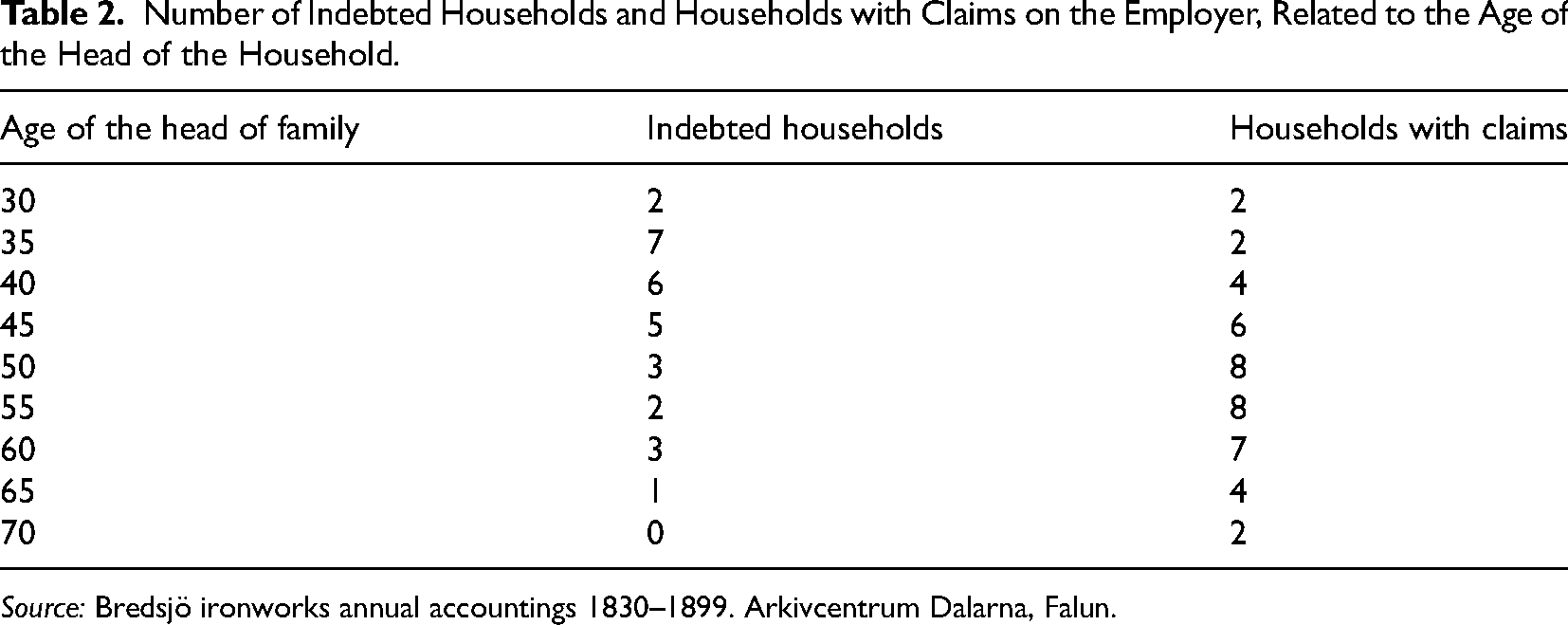

However, additional information regarding the number of indebted households and the number of households who had claims on the company supports the idea of a life cycle structure (see Table 2). The indebted households were most common in the age 35–45 of the head of the household. When the head had reached the age of 50 the debt of the household had been replaced by a claim, a situation relevant until retirement.

Number of Indebted Households and Households with Claims on the Employer, Related to the Age of the Head of the Household.

Source: Bredsjö ironworks annual accountings 1830–1899. Arkivcentrum Dalarna, Falun.

Analyzing the total balance certainly gives a picture of the situation at the end of every year, but in order to study the development over time it is preferable to analyze the annual changes. Net savings are not necessarily reflected in the increase of a claim but can also be reflected in the decrease of a debt. The development of the annual net savings does not demonstrate the obvious relation to the life cycle that is encountered in the annual total balance. The period before 43 years of age was, as has been stated before, dominated by a negative saving, but the following period was not characterized by an overall positive saving. It seems as though the households have generally saved money for 10–15 years, having later, through extensive cash withdrawals, reduced their claims on the company.

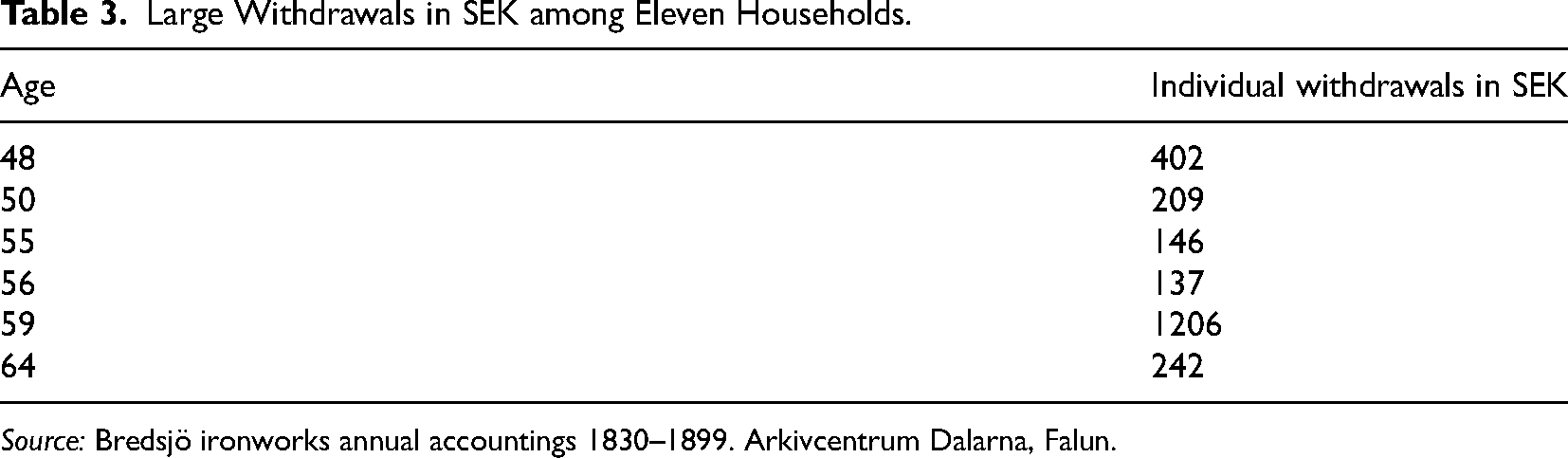

Analyzing the structure of these withdrawals show that savings was diminished as the result of substantial cash withdrawals by one or two individuals. The size of these withdrawal causes considerable changes in average net savings, for the analyzed households. This points to the hypothesis that they were not meant for immediate consumption. It is possible that the money was instead used to repay private credits or help the children who left home. It has however not been possible to support this hypothesis through a study of national registration. Another likely explanation to these cash withdrawals is that saving was more targeted than has been assumed. It is possible that the cash withdrawals were meant for investments in cattle or land. It is also possible that the money was transferred to a bank account, though this seems unlikely.

Should the cash withdrawals over 135 SEK be regarded as investments in durable consumer goods, silver

Large Withdrawals in SEK among Eleven Households.

Source: Bredsjö ironworks annual accountings 1830–1899. Arkivcentrum Dalarna, Falun.

A major difference between the life cycle theory and the permanent income hypothesis lies in the view of temporary income fluctuations. According to the permanent income hypothesis such fluctuations only affect savings, while the life cycle theory claims an increase in both saving and consumption to be likely. The studied households permit this issue to be analyzed.

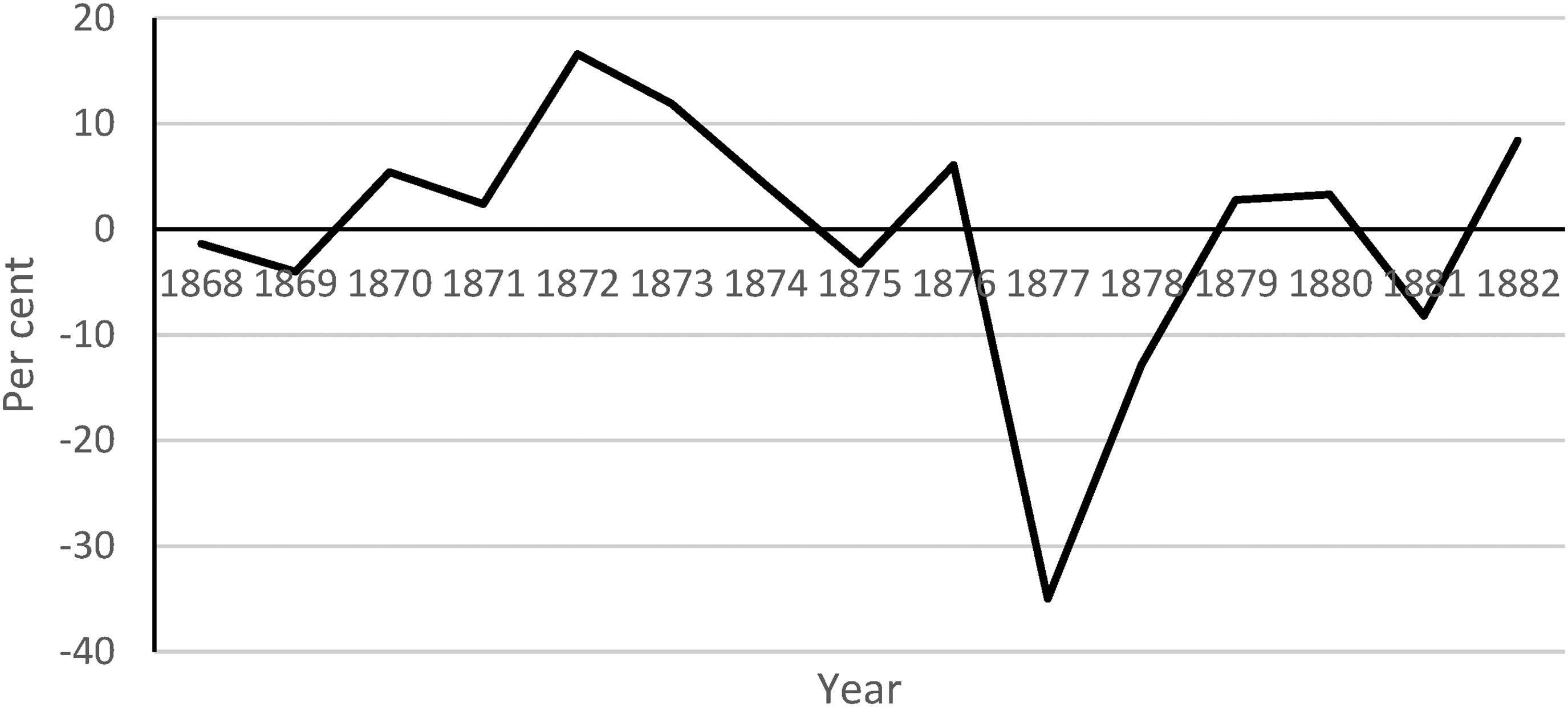

The trade boom in the beginning of the 1870s resulted in heavy inflation and increased wage levels. At the same time the demand for labor increased at Bredsjö ironworks. This meant that additional members of the studied households were employed for a period. Several factors thus coincided to create a sharp rise in the annual income of the households. But in the middle of the 1870s the business cycle turned down, and both demand for labor and wages fell. It has been possible to follow seven of the households during this period to see how these temporary wage fluctuations affected the households, and whether the higher income led to increased consumption or saving (see Figure 8).

Annual net savings/annual income in percent for seven households 1868–1882.

The result show that the tendency to save grew stronger in the period of 1872–1874, compared to the preceding years. The highest relative savings was 17 percent of the income in 1872 and 12 percent in 1873, while on the other hand the inflation and falling income of 1874 is likely to have diminished the possibility to save. 32 The share of saving then fell, and for the period of 1877–1878 there is even a negative saving. This is not surprising. The annual income for the selected households dropped 48 percent between the top year 1873 and 1878, while consumption prices fell with between 10 and 15 percent. 33 Capital saved during early 1870s was probable a welcome backup to maintain the consumption level in 1877 and 1878.

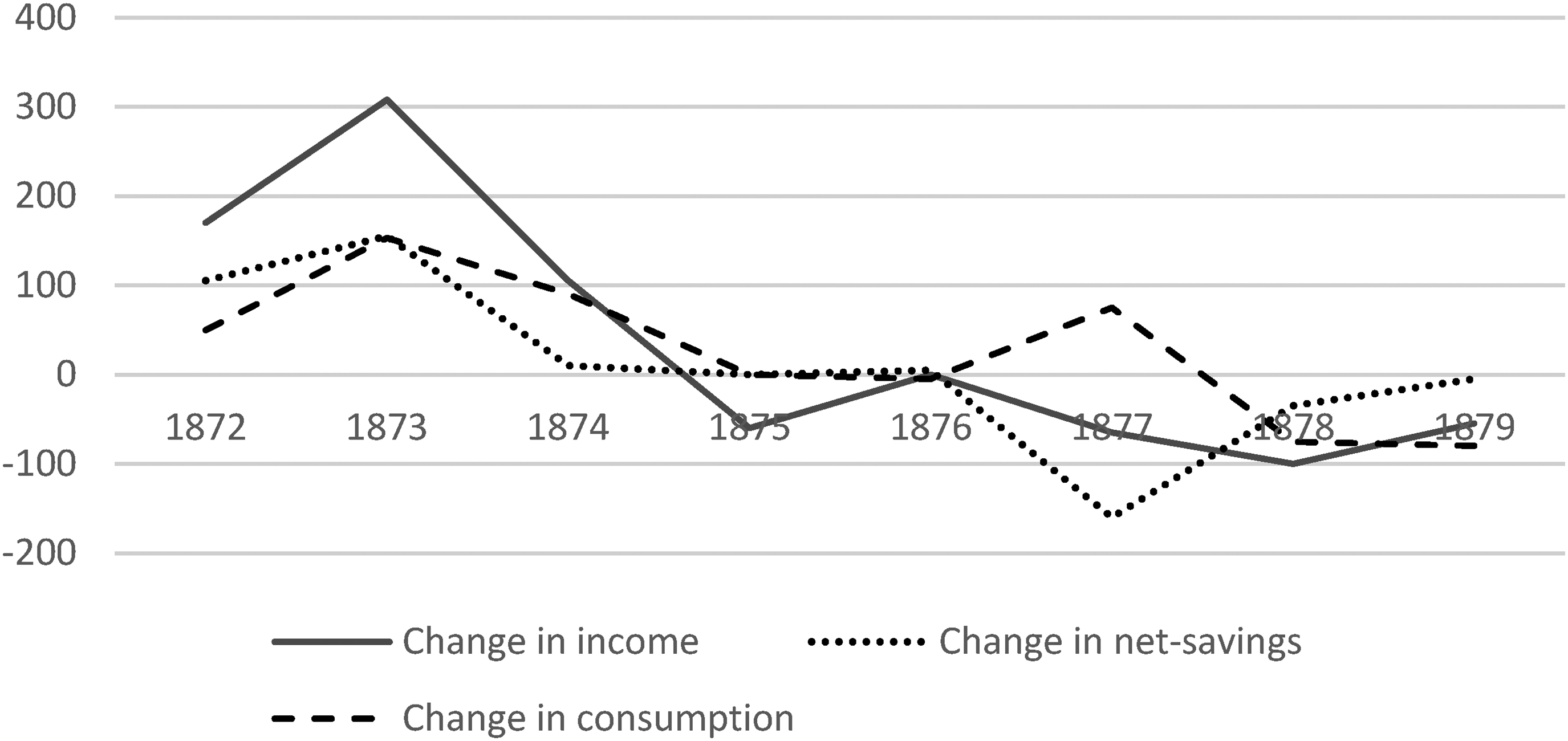

The savings increased with the temporary raise in income, but so did consumption mostly as an effect of inflation. During the sharp increase in income in the beginning of the 1870s the temporary raise was split in two equal halves, one for consumption and one for savings (see Figure 9). When wages fell in 1874–1875 consumption followed, as did net-savings while still kept positive. The capital accumulated in the beginning of the decade was largely spent in 1877, as the share of consumption then rose. This picture may however be wrong, as the spending consisted of cash withdrawals which may have been transferred to a saving in durable consumer goods. 34 Anyhow, it was more economic to use this capital in 1877 than it would have been in 1874, since deflation had increased the value of money in the meantime.

Average annual changes in income, savings and consumtion in SEK for seven households 1872–1879.

This result give proof for the life cycle theory, which presume that temporary incomes will be used for both savings and consumption—not only savings. In a somewhat longer perspective, the handling of the temporary income increase in the 1870s was aiming at a stable consumption level. Thus, a large part—most of the capital saved in 1870–1874 was used for consumption in 1877–1878.

Bredsjö Ironwork in Comparison

During the last three decades of the nineteenth century Bredsjö ironwork invested in the development of pig-iron production both from a qualitative and quantitative aspect, which paved the way for a more effective production and improved living condition for the employees. This development can be compared with the Vällnora ironworks, situated in the east of the large iron producing region of Sweden. Both these ironworks were of the same size during first half of the nineteenth century. But, while Bredsjö developed the capacity, Vällnora remained a smaller blast furnace, producing for a local forge.

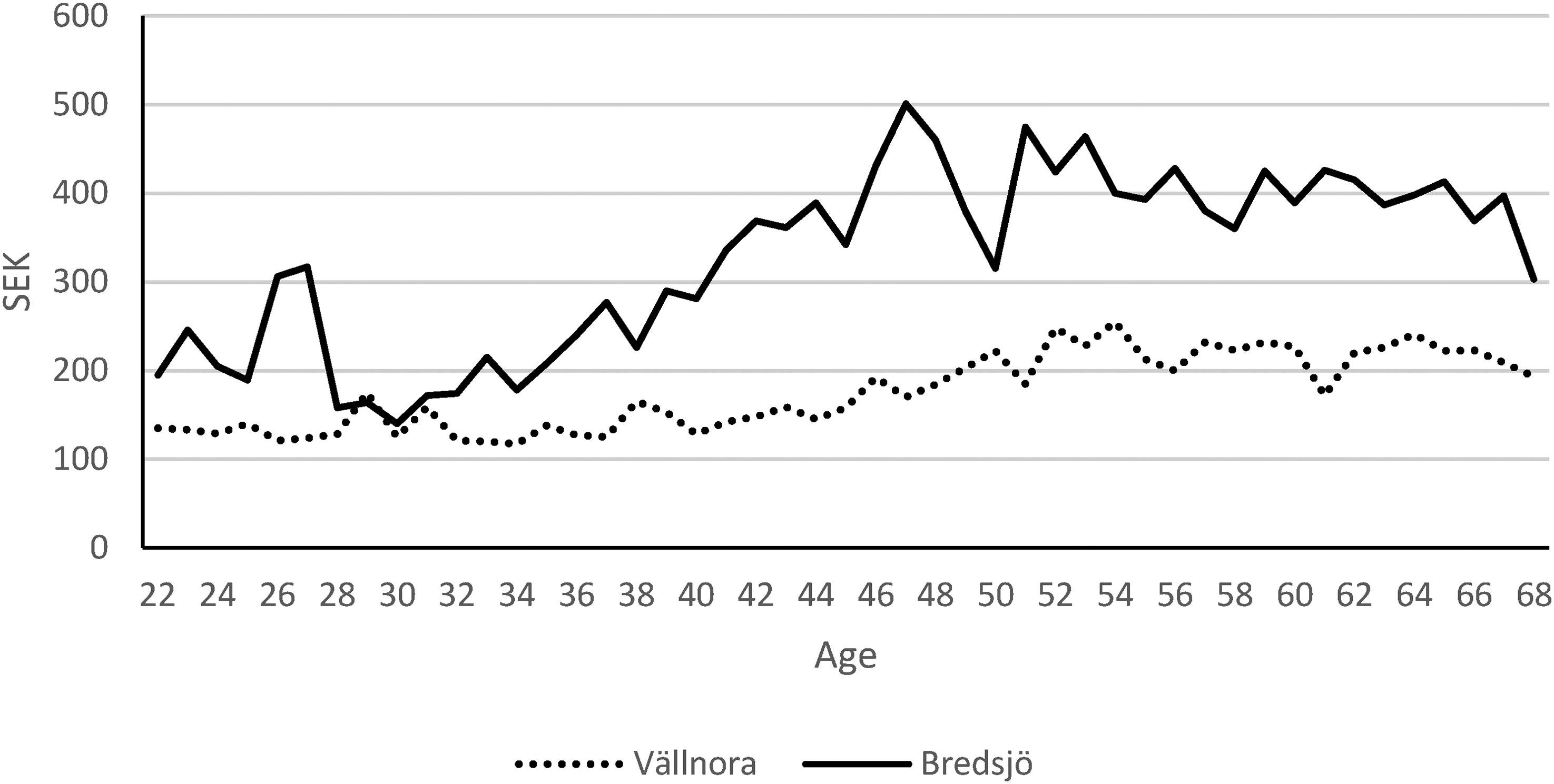

The most important aspect of this comparison is to determine if the use of the companies bookkeeping can help us understand the development of employee's economic life cycles in different ironworks. Even though the economic situation was different between these two ironworks, the development for the employees was similar. In both cases the selection of employees/households consisted of blast furnace workers combining this employment with day shift job. And in both cases the work effort of family members was of greatest importance as the head of the family reached about 35–40 years of age and further (see Figure 10).

Median annual income for 13 households at Bredsjö ironworks and 15 households at Vällnora ironworks, based on the age of the head of the family.

However, there were important differences between the two ironworks, in the comparison of the annual income. The obvious difference is that the size of the annual income, was much higher in Bredsjö than in Vällnora—sometimes more than twice that high—and that the difference increased especially from the age of 40, to decrease after the age of 60 years. But despite this, employees at both ironworks exhibited an income life cycle that culminated around 55–58 years of age for the head of the family.

The fluctuation in annual income at the Swedish ironworks can be explained by both the number of family members engaged in the families’ work effort, but also in the size of daily wages. A comparison between the remuneration for a man's day job during the summer between the two ironworks confirms this. In 1860 a day's work was paid with 0.40–0.45 SEK in Vällnora while it was 0.92–1.25 SEK in Bredsjö. This difference had increased to 0.55–0.70 SEK in Vällnora 1890 and to 1.10–1.35 SEK in Bredsjö the same year. However, even with this difference in mind it appears that the family sons still living at the parent's home were of greater economic importance for the families in Bredsjö compared with Vällnora.

Even though the most important issue here is to see whether the companies bookkeeping can help us understand workers’ economic life cycles, it is also important to reflect over the big differences in annual income between the two ironwork's employees. Both companies were engaged in pig-iron production, but under different traditions. Bredsjö had adjusted to the open market, selling their pig iron to the highest bidder, while Vällnora sold their production to the forge in Rånäs which was a company in the same business group. Consequently, Bredsjö also had adapted their employment conditions to the market, which resulted in increased wages, lease payment for the employees’ cottage and market prices in the company store. Vällnora on the other hand, was a representative of an old-fashioned corporate culture where wages were partly paid in kind—without being valued in currency—such as free housing and subsidized products in the company store. This can to some extent explain the lower incomes in Vällnora.

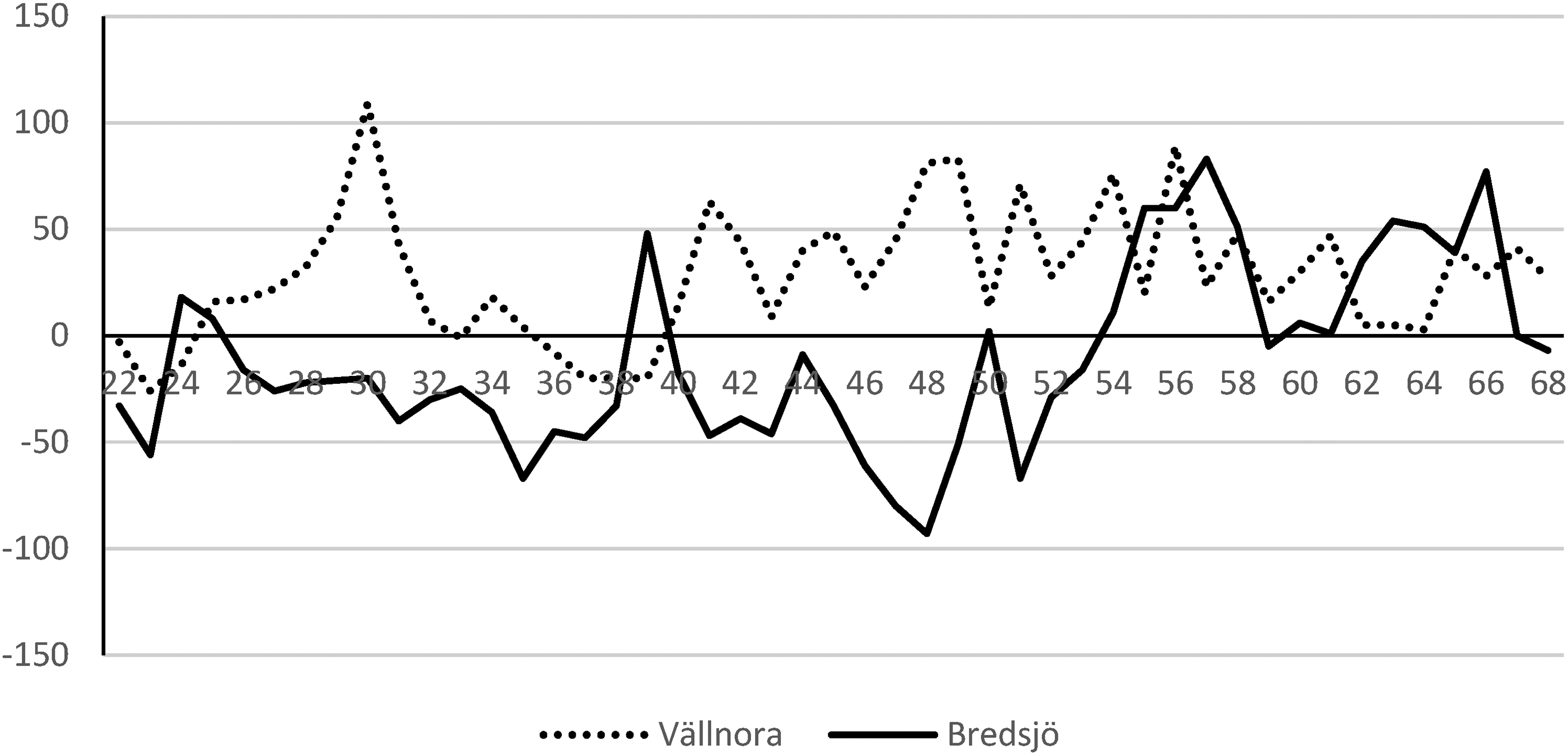

Earlier in the paper it was stated that not only average day wages and annual incomes in Bredsjö exhibited a life cycle structure, but also that debts and savings had the same cyclical structure. It was also noted that this to some extent was an effect of some employees/households—especially with high savings—affected the savings average. This is confirmed if we compare the median—instead of average—for savings and debts in Bredsjö with Vällnora ironworks (see Figure 6). For Vällnora there was no obvious life cycle structure, while Bredsjö still displayed some changes that could be related to the age of the head of the household—especially increased savings around 50–60 years of age. The high savings in the late 60 years of age is not that easy to explain. According to consumption theories savings were supposed to fall as a person became older, as in the case of Vällnora, but this was not the case in Bredsjö. This could perhaps be explained by the few employees (2–3) still active in the labor force.

A strong tradition in Sweden's iron industry was the patriarchal care for the employees—especially for blacksmiths and other employees at the forge. But also, other employees could benefit from different economic support. In both Bredsjö and Vällnora workers from the pig-iron production enjoyed a small retirement pension and could also be given reimbursements for accidents at work and long sickness. These benefits could also include widows and younger children in case of death of the head of the family.

During the establishment of families, a child benefit in grain was given until the children were 12 years old. The system was kept in Vällnora until the 1890s but was from the 1860s gradually disassembled in Bredsjö. This could have affected the employees’ savings behavior, but on the other hand, size of pensions and other benefits was not enough to secure a long-term survival.

Conclusions

This pilot study is a longitudinal analysis of individual economic life cycles in the Swedish iron industry during the nineteenth century. It is also a test of the use of business accounting for the reconstruction of workers economy. The sources of the Bredsjö ironworks gives us a unique opportunity—as also some other Swedish iron producing companies—to closely follow the development of the employee's/household's economy and consumption.

The focus in this article is on the relationship between income, savings, and debts for employees at the blast furnace. These workers where not especially well paid, compared to for example miners or blacksmiths. 35 During working periods at the furnace, the salary was somewhat higher than for the unskilled workers. But since these workers—and their sons working on fathers account—also were employed as day shift workers during the rest of the year, the average day wages were not much more than that for the unskilled worker. However, as shown in the comparison between Bredsjö and Vällnora ironworks, the difference in wages between companies could be quite extensive as an effect of the use of wages in kind.

The result of this research points to the existence of an income development cycle for the analyzed households. The annual income was low up to the age of 35 of the workers. It then rose and culminated when the head of the household was 55–60 years old. The earnings of other members of the family, above all the young adult sons, being entered on the accounts of their fathers, made the annual income increase higher than the daily wages would lead us to expect. The average annual income for the analyzed households was for some years close to double what could be expected based on the daily income.

The extensive changes in the annual income were also reflected in the development of saving. When the head of the household was younger than 35 years of age the saving was negative. As the annual income rose the claim on the company also rose, and it culminated at the age of around 60. As the number of working days fell the annual income also fell as did savings. Using the individual household as basis of the analysis, this investigation supports the general theses of consumption theories.

The importance of Childrens’ work for the support of the family was noted by Bodenhorn for savers in the Cornwall savings bank in New York. 36 This result is also directly related to research made by Rotella and Alter in their analysis of income, debt, and savings in the American working class in 1889/1890. Not only did family's annual income fluctuate as an effect of the husbands age, but it was also directly correlated to the work of children on the father's account. When the head of the family was in the age between 40 and 49 years the children contributed with nearly 25 percent of the family income. This increased as the father grew older and in the age of 60+ years the children contributed with 36.5 percent of the family income. This can be compared to the children's estimated income contribution in Bredsjö, which was 38 percent when the head of the family was between 40 and 49 years of age, 57 percent in the age interval 50–59 years of age, but only 17 percent when the head of the family was 60+ years of age. This not only indicates that children's income was more important in the Bredsjö family's economic situation than in the American working class. It also suggests that children left their parent home earlier in Bredsjö since their income contribution dropped considerably when the head of the family reached 60+ years. 37 However, differences in methodology and the low number of selected families in the Swedish example makes the result a bit uncertain. An analysis including several different Swedish companies would make the result more reliable.

Among the long-term savers in savings banks there were also a large number of children that became customers through their parents, who opened accounts in their name, making regular deposits on these accounts. Among the reliable savers in the savings bank there was also a substantial share of older women from well-to-do families. Such customers often saved large sums of money, sometimes equaling several years’ income for a worker. 38 This can be compared to the average savings in the Bredsjö investigation, which equaled 4–6 months’ pay for the workers. However, the difference between an ordinary saver and those with highest saving on their working account was considerable. The largest assets on a personal account could amount to three annual incomes, which gave an income of interest to around 45–50 SEK per annum (5 percent), or equal to 1, 5–2 month's income for a day-laborer.

The long-term capital savings in Falu savings bank—as in other savings banks—was accumulated above all through regular deposits. Withdrawals from these savings accounts were unusual and occurred only after several years’ saving. 39 This pattern of behavior is similar to that of the Bredsjö households. Once or twice during their lifetime savers withdrew substantial sums of money from their accounts at the ironworks, perhaps to invest in durable consumer goods or as an inheritance to children. It is thus not unlikely that there was a share of targeted saving even among the lower classes, and that their saving did not only aim to secure their retirement. However, the number of persons who managed to build their assets to a level that made it possible to do larger withdrawals from their accounts, were very limited, and it only occurred after the age of 50 for the head of the family.

Economic fluctuations also affected the employee's savings at Bredsjö ironworks. This was especially evident during the economic boom and the subsequent down-turn of the 1870s. The number of working days as well as annual income increased substantially—considerably more than inflation—during the period 1870–1873. This resulted in both an increased consumption and larger savings—which might come as a surprise considering the inflation. Most of the accumulated capital remaining on the accounts were used during the latter half of the 1870s when the number of working days as well as daily and annual incomes were reduced considerable. This made it possible for the households to maintain their standard of living. We can thus conclude that this example from Bredsjö ironworks give support for the life cycle theory,

Consumption theories have to some extent been proven to be applicable on both the material emanating from savings banks and companies’ bookkeeping. But to draw more general conclusions the demographic and social situation should be more thoroughly analyzed. The lack of a national social security was probably an important incentive to save. At the same time there was a motive for parents to leave some inheritance to the next generation. This has for example been shown for saving societies in Philadelphia (US) and for Swedish savings banks.40 However, to understand and evaluate if consumption theories are applicable on the 19 century ironworkers’ situation the analysis must be extended to other companies and with an increased number of occupational groups. The result of this pilot study indicates that further research is needed. Since bookkeeping from Swedish ironworks are available well into the eighteenth century, it would be possible to extend this research also in time.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

This work was supported by Jan Wallander & Tom Hedelius Stiftelse (Foundation) under grant P21-0070.