Abstract

The increasing penetration of online shopping will have major effects on physical stores. And the question is: In which areas will consumers replace most physical shopping with online shopping? Two apparently competing hypotheses were tested: the diffusion of innovation hypothesis, suggesting openness to new technologies; and the efficiency hypothesis, suggesting accessibility gains. Whether the innovation hypothesis has lost its importance in favor of the efficiency hypothesis was also questioned. The study area was a polycentric urban area in the Netherlands. We distinguished between books, clothes, and groceries. It was assumed that shoppers’ decisions to buy a particular good online or not, and the share of online shopping relative to in-store shopping for this good, were basically driven either by shoppers’ willingness to adopt the new technology of e-shopping or by shoppers’ accessibility to shops. Support was found for both hypotheses, although the impact of shopping seemed limited and varied between different types of goods. In the end, e-shopping behavior remains primarily shaped by households who are open to new technologies, and to a limited extent by efficiency considerations.

Online shopping has grown dramatically in the past decade for almost all types of goods, varying from books to clothes and groceries. As of 2017, the share of the population buying online is 83% in China, about 80% for countries in Western Europe, and 77% for the United States ( 1 , 2 ).

Without doubt, the increasing penetration of e-retail will have major effects on physical stores ( 3 ). Shopping is one of the most important non-work activities in any affluent society, in relation to money and time. With the rising level of e-shopping, the level of store shopping activities will decline, and consequently the amount of shopping floor space. It is unclear however, what the consequences will be for the spatial distribution of retail services.

Although the distribution of physical shopping areas varies between countries, the emergence of e-shopping may well reduce these differences. U.S. shopping areas are generally concentrated in malls at the fringes of the urban areas, highly, and often exclusively, accessible by car. Nevertheless, there is also some opposition from the Smart Growth movement, which aims for mixed-use development. On the contrary, in Europe, it is mainly the city centers that offer a wide variety of consumer goods. Although they also provide daily goods, the majority of supermarkets, bakers, groceries, and drug stores are found in neighborhood shopping centers. However, partly driven by the scale-up of the retail sector, many European cities are showing a tendency toward the spatial model that is common in the United States, and consequently a decline in shopping facilities in city centers, residential neighborhoods, and villages ( 4 – 6 ). Early examples are the French hypermarchés. In the Netherlands, the concentration of shopping facilities in urban areas has always been preserved, forced by policies restricting non-urban shopping areas, to limit travel distances and enable households to use alternatives to the car ( 7 ). Since the early 2000s, however, policies have been relaxed, which has now also led to a trend toward shopping facilities being located in the city fringes. Moreover, in recent years, many countries have experienced a drop in support for traditional village shops, often resulting in widespread closures.

If, as a result of increasing e-shopping, the loss of physical stores occurs mainly in urban centers then that will erode the amenities function that they currently perform. The disappearance of shops from the suburbs and rural villages has been particularly unfavorable because of a loss in variety of shops, accessibility of the shopping facilities, and their social function.

The question is: In which areas will consumers replace most physical shopping with online shopping? As early as 2003, Anderson et al. formulated two apparently competing hypotheses ( 8 ); Cao et al. adopted these and referred to them as the diffusion of innovation hypothesis and the efficiency hypothesis ( 9 ). The first hypothesis argues that urban areas facilitate innovation and creativity. People here are more open to early adoption of new technologies such as e-shopping, partly because they are often better educated and more affluent. The second hypothesis claims that one of the advantages of e-shopping is that it reduces the spatial constraint of low retail accessibility. People on the periphery therefore benefit most from the online accessibility of goods and will therefore adopt e-shopping. An intriguing prediction that Anderson et al. make is that the innovation hypothesis will mainly take place in the short run ( 8 ). In the longer run, when technology has been diffused, accessibility will become the main driver.

Apart from these drivers for online shopping, the decision to buy a particular good online or not will also depend on the type of good. We distinguished between search goods and experience goods ( 8 , 10 , 11 ). In the first category, required information can be offered more efficiently on the Internet, such as material on books and music. This is also the category that has been offered online for a long time. The second category, on the other hand, consists of goods that buyers want to see and try, and which are therefore more difficult to sell online, such as clothing and groceries.

As Cao et al. have already noted, little research has been done into the spatial distribution of e-shopping and the two hypotheses have hardly been tested empirically, which calls for more research to test generalizability ( 9 ). In this paper we also question whether, now that e-shopping seems to have made a breakthrough, the innovation hypothesis has lost its importance in favor of the efficiency hypothesis. The study area is a polycentric urban area in the Netherlands. We distinguish between books, clothes, and groceries. It is assumed that shoppers’ decisions (i) whether to buy online or not for a particular good, and (ii) in relation to the share of online shopping relative to in-store shopping for this good, are basically driven by two processes. Therefore, we estimate a so-called zero-inflated model. In the next sections, we first describe the literature in this field, then we describe the data and the methods, followed by the model results, and end with conclusions.

Literature

In the past two decades, a large number of studies have been carried out in which online and physical shopping were related to the location. Weltevreden and Rietbergen show that city centers are more likely to face a reduction in shopping visits and purchases due to online shopping than rural shopping centers ( 12 ). The higher vulnerability of city centers is to some extent surprising in view of their larger number and variety of shops, and also their more appealing atmosphere/environment and therefore ability to attract (recreational) shoppers. On the other hand, the limited effect on rural shopping centers could be explained by their more important function for daily goods purchases (e.g., groceries) that are less sensitive to online shopping.

Urban consumers have been found to shop online more than suburban and rural residents ( 13 – 16 ). Farag et al. found that 61% of online shoppers in the Netherlands in 2001 lived in very strongly urbanized areas, whereas 39% resided in less urbanized and non-urbanized areas (32% and 7%, respectively) ( 14 ).

These findings seem contrary to expectations regarding the influence of store accessibility on online shopping. Since convenience, saving time, and saving money are the most frequently cited reasons for online shopping these motivational factors are likely to be less strong for urban residents that have relatively better access to shops compared with their rural counterparts. When these rural residents visit shops they need to travel over longer distances, particularly when they need a variety of products (chaining of shopping trips) causing more travel time and higher travel costs. Furthermore, due to the larger distances to the shops, these rural residents may be dependent on other transport modes, for example the car, than their urban counterparts. And car use to access shops may bring additional inconveniences, such as finding a parking place, and costs, for example, parking fees. It is, however, interesting to note that, although Farag et al. ( 14 ) discerned a positive relation between store accessibility and online buying they also found that better access to shops also leads to more shopping trips made (probably to explore a product in-store, since a negative relation was found between store accessibility and online search frequency). Thus, Farag et al. postulate that persons who like to shop in-store probably also like to shop online. All in all, the studies’ conclusions regarding the role of accessibility are rather uncertain.

Other studies that tried to identify a relationship between store accessibility and online shopping behavior had mixed findings. Consistent with Farag et al., Cao et al. found store accessibility was positively associated with online shopping in urban areas ( 9 , 14 ). However, for suburban areas no effect of store accessibility was found, whereas the impact in the exurban areas was negative, i.e., lower store accessibility induces more online shopping ( 9 , 14 ). Ren and Kwan similarly found a negative effect on online shopping from store accessibility, but the measure effect was small ( 15 ). On the other hand, Weltevreden and Rietbergen came to other conclusions regarding the relevance of store accessibility in city centers ( 13 ). They examined the role of perceived city center attractiveness by distinguishing three factors: shopping attractiveness, leisure attractiveness, and accessibility attractiveness, which was measured by the total number of shops a person can reach by car, bicycle, or on foot from his/her place of residence in a certain time distance, and taking into account the available parking for cars/bicycles/mopeds and parking fees for cars. The authors found evidence that the higher the perceived city-center attractiveness the lower the probability that consumers make fewer purchases at city-center stores due to online shopping. However, the importance of accessibility attractiveness differed among transport users. With regard to car users, the perceived car accessibility of the city center influenced the extent to which they shopped online, and the extent to which they purchased less in city centers owing to e-shopping. For users of other transportation modes, perceived shopping attractiveness was more important.

Studies in which only the nearest distance to shops is used to measure store accessibility showed different findings. Sinai and Waldvogel found that the further people live from the nearest book or clothing store, the more books or clothing they relatively buy online ( 17 ). In contrast, Lee et al. reported that online shopping is not affected by distance to the nearest shopping center ( 18 ).

Studies on the impact of spatial and accessibility aspects have always controlled for personal, attitudinal, and household aspects. Without exception, these studies show that such factors have a larger impact than accessibility. Although we assume the role of such factors is diminishing, it is still necessary to control for them. As research on online shopping has been dominated by marketing research, shopping attitudes have been extensively investigated. Research has generally focused on people’s motives for shopping (e.g., acquire goods, socialize, entertain) and the relevance of the particularities of in-store shopping versus online shopping (shopping mode characteristics). Motivational factors of individuals (e.g., functional or recreational shopping) play a key role in the decision whether to buy online or in-store ( 14 , 19 ). Recreational shoppers are more inclined to like seeing and handling products before buying and hence will make fewer online purchases, whereas functional shoppers like to save time spent on shopping and hence buy online more frequently ( 19 – 21 ). In relation to time saving the flexibility of opening hours is often quoted as a condition that encourages online shopping ( 22 ). On the other hand, studies have addressed some disadvantages of the online shopping mode, that is, the inconvenience of returning products and uncertainty about the security of transactions ( 23 ). However, since electronic payments have boomed it is unlikely that today the latter is still a concern and mitigating factor for online shopping. Nowadays privacy concerns seem to be a more serious issue ( 24 , 25 ). Other behavioral studies have pointed to the relevance of a positive attitude toward online shopping, such as the perceived quality of vendors on the Internet, on the intention to buy online ( 27 ).

Various studies have found a positive relationship between Internet usage and online shopping, whereas other studies have not ( 26 , 28 ). Although more recent studies also found the Internet experience to have a positive influence on online shopping, it may well be that the effects of the Internet experience are diminishing because of the increasing penetration of Internet in our daily life ( 24 , 29 ). As regards the influence of mobile technology (smart phones and tablets) on online shopping (M-shopping) there is very little known yet. M-shopping is in fact still in its infancy, but is expected to gain popularity due to the increased use of smartphones. Most studies undertaken so far have addressed issues regarding its adoption by consumers. Among the few studies that focused on the impact of M-shopping on purchases, Wang et al. found an increase in purchases ( 30 ). However, using mobile devices can be supportive for in-store shopping, for instance in finding directions, store locations, and opening hours.

Product characteristics also affect online shopping. Search goods, such as books and CDs, are more suited to purchasing via the Internet than experience goods such as fresh vegetables ( 14 , 22 , 29 , 31 ). Moreover, people tend to buy more expensive products online because of possible larger savings compared with prices in physical shops ( 30 ).

Socioeconomic and demographic characteristics are among the most frequently studied factors in online shopping research ( 14 , 23 , 29 , 31 – 35 ). In the early stages of online shopping, male shoppers made more online purchases and spent more money online than females, but women have caught up. More recent studies have found that gender has little to no effect on online shopping activity ( 18 , 36 , 37 ). However, men and women are rather different in their preference for products online, with women more often purchasing clothing and men more likely to shop for electronics ( 38 ).

The online-shopper profile is dominated by young people, as they are typically more likely to adopt new technologies, live in households with Internet access, and have higher levels of Internet use. However, a significant increase in older (retired) online shoppers can be expected due to an aging society and the increasing engagement of this age group in information and communications technology applications such as online shopping, virtual communities, and online learning ( 37 ). Ultimately, online shopping might be a welcome solution for less-mobile older shoppers.

Online shoppers tend to be in the higher income groups than traditional in-store shoppers, most likely because demand increases as income increases. This could point to online shopping as a complimentary activity.

According to several studies, online shoppers are more educated (e.g., 18 , 19 , 26 , 34 ), but there are also studies that found no effect of education on online shopping (e.g., 35 ). The latter possibly supports the notion that online shopping is actually a relatively easy task that does not require higher education. Households with children tend to engage more often in shopping than households without children, but there is little evidence for any impact of this difference in household type on online shopping. As households with children are expected to be more time-pressured, it is likely that such households are more inclined to shop online. Some support for this was found by Hiselius et al. who observed a higher share of online shoppers among families with children under 10 years of age ( 40 ). Farag et al. discerned that singles shop less often online than other household types ( 20 ). However, it is very doubtful that their explanation that singles often do not have a fast Internet connection is still valid today.

As far as other socioeconomic aspects are concerned, car ownership or access to a car and having a driver’s license tend to be negatively related to online shopping ( 28 ). A possible explanation for this is that the possibility to take goods from the store back home by car makes in-store shopping less inconvenient for people than those who do not have access to a car ( 41 ).

Methodology

Study Area

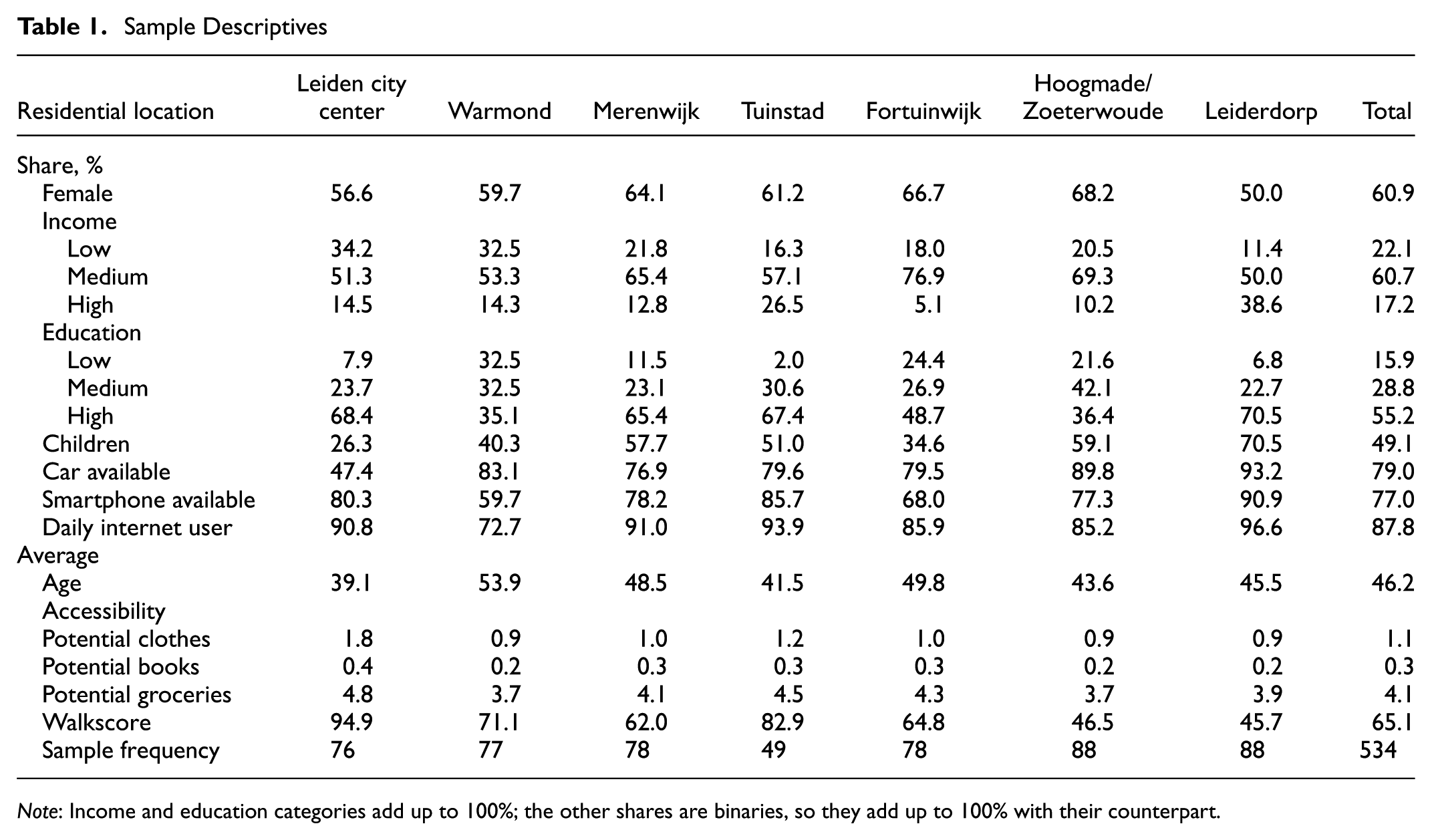

Data was collected in the Leiden urban region in the Randstad area in the Netherlands. The Randstad is the economic and population core of the Netherlands. As our research question is spatially oriented, and therefore we selected a medium-sized polycentric urban region with a core city, suburbs and exurban villages. The city of Leiden is such a medium-sized polycentric urban region, with a historical city center, surrounded by city neighborhoods, suburbs and rural villages. Leiden’s city center is the main shopping area for nondaily goods, with an emphasis on clothes. Leiderdorp is a suburb, adjacent to Leiden, with a highly educated population and high income groups. Merenwijk is a medium-income neighborhood from the 1970s with mainly single family homes. Tuinstad is a neighborhood that was created between the 1930s and 1950s, close to the city center. Fortuinwijk is a 1960s neighborhood with mainly cheap apartment flats. Warmond is a larger village, Hoogmade and Zoeterwoude are smaller and relatively remote villages. Some neighborhoods have their own shopping center with the focus on daily goods (such as food and personal care); the villages have only a limited number of shops.

Data

A personal survey was conducted in 2014, in the first week of December. In each of the residential areas, respondents were selected and asked to complete a short questionnaire at their home. They were randomly selected on a map to ensure a good spatial distribution across the neighborhoods. If nobody was at home, the surveyors went to the neighbors. The questionnaire took them at most 10 min. The address has been added by the surveyors. The total sample of (almost) complete questionnaires consisted of 534 respondents. For households that were at home, the response rate was about 20%; not at home was not recorded. Thanks to this face-to-face method, a reliable representation over the selected neighborhoods was ensured.

The sample reflects the profile of the Leiden urban area. Females are slightly over-represented, although this varies over the neighborhoods. In general the respondents are well-paid workers, predominantly belonging to medium-income classes. The educational level is over-represented compared to Dutch averages, which makes sense as Leiden is a university town with science-related business clusters, and also because higher educated people are usually more willing to participate in surveys.

In addition to gender, income and education the following demographic and socioeconomic characteristics that may influence respondents’ e-shopping behavior have been included in the survey: age, employment status, household composition (limited to children or not) and car availability. To discover the possible impact of the affinity with Internet use on e-shopping the survey included a question on time that is spent on Internet use and use of smartphone.

The three product categories focused on in the current research were books, a so-called search good, and one of the first shopping goods to appear online; clothes is the fastest growing category, an experience good, which people want to see and try on; and groceries, also a “see and feel” category, referred to as daily shopping. For each of these product groups, respondents were asked how often they purchased these products in-store and online. Responses were collated on a ratio scale, that is, the number of purchases per month or year. A seven-point Likert scale was used to measure participant responses to gain insight into attitudes toward shopping for these three product groups and toward online shopping in general. The possible answers ranged from “very unpleasant” to “very pleasant.”

Furthermore, to investigate the impact of general attitudes to e-shopping behavior the respondents were asked to provide some general opinions. The questions included attitudes toward family, technology, environment, culture, sports, and employment. Respondents could answer each question on a seven-point Likert scale, ranging from “very unimportant” to “very important.”

Shopping accessibility measures were developed by relating the zip code of the respondents to data about the location of shops and their number of retail jobs in the Leiden region. Three different shopping accessibility indicators were created. A potential accessibility indicator (or gravity-based indicator) was calculated on the basis of the number of shops, weighted by home-shop distances and a distance decay (i.e., shops at further distance get a lower weight in the calculation). A second accessibility indicator was calculated by summing the number of shops within 5-km buffers. The third indicator, Walkscore (www.walkscore.com), was based on shopping in the direct neighborhood, using Google Maps data, with a distance decay also applied. Walkscore is the most local indicator of all and has a restricted upper distance value. It has the largest potential distance range (basically to infinity, although strongly limited by the distance decay). All three indicators were specified and applied in our model estimations, but only the potential accessibility indicator led to significant estimates. Therefore the results concern only the models in which the potential accessibility indicator was used. The values of the potential accessibility indicator as well as other important descriptive statistics of the sample are presented in Table 1.

Sample Descriptives

Note: Income and education categories add up to 100%; the other shares are binaries, so they add up to 100% with their counterpart.

Modeling Approach

We estimated models for each of the three categories of goods. For each category, we asked about both the number of in-store and online purchases per month or per year and recalculated this to the number of purchases per month. Then we calculated for each goods category the share of online purchases in the total number of purchases. An appropriate model for shares is a fractional regression model, which exists both in a logit and a probit version ( 42 ). Fractional responses concern outcomes between zero and one, for example the average of dichotomous variables such as participation rates, or variables that are naturally on a zero to one scale, such as pollution levels. Or, as in the present study, the number of online shopping purchases as a share of the total purchases (for a particular good). If we assume that almost all people shop both online and in-store, and only some of them just do online or in-store shopping, we could simply calculate shares, which would vary from zero to one: zero for those who just shop in-store and a one for those who just shop online, and all others in between. In that case, we would simply assume that such shares represent the same decision-making process, and would be influenced in the same way by a certain set of predictors. In such cases, a fractional logit model is the most appropriate model. However, if we observed that a large share of the respondents just bought in-store, that would mean the data was zero-inflated. Therefore, we assumed that shoppers’ decisions whether to buy online or not for a particular good, and the share of online purchases, are two distinct processes. Hence, we developed two model types. For the decision to be involved in online shopping for a particular good, we developed a binary logit model, whereas we estimated a fractional logit model for the fraction above zero. Basically, it would make sense to not only estimate models taking into account zero-inflation, but also one-inflation, assuming that a person only buys online. However, as this is (still) rather rare, we did not estimate this. An alternative model for the fractional logit model is the beta regression model, but this model type cannot deal with zeros and ones at all. Model fit is approached by pseudo R-squares (rho); in binary logit it is assumed that Cragg and Uhler better approaches the proportion of explained variance.

Results

Clothes

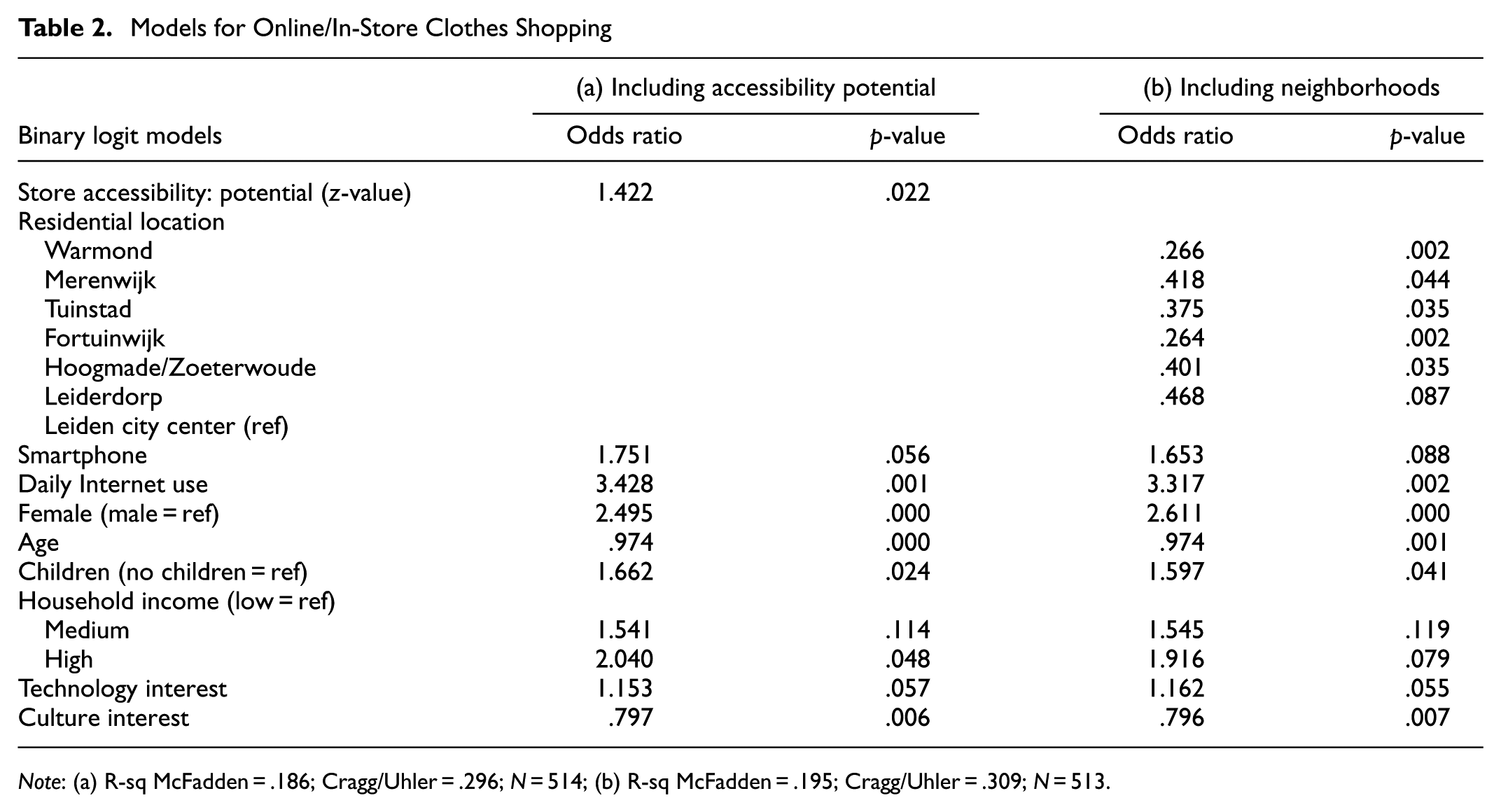

Table 2 shows two models estimating the likelihood that someone shops for clothes online. The left model (a) estimates the likelihood that someone shops online with the potential an indicator for accessibility. Model (b) is comparable with model (a) but uses the residential location with Leiden city center as the reference category. The two models are more or less comparable, although the pseudo R-squares suggest that the residential location model performs slightly better.

Models for Online/In-Store Clothes Shopping

Note: (a) R-sq McFadden = .186; Cragg/Uhler = .296; N = 514; (b) R-sq McFadden = .195; Cragg/Uhler = .309; N = 513.

Model (a) suggests that the more accessible the clothing shops (i.e., an increasing potential value), the greater the share of people shopping online. At first sight, this sounds counterintuitive, as people with a high accessibility have more in-store shops at their disposal and have, consequently, less need to shop online. To get a better insight, we inspected the model in which potential was replaced with residential location. We then found that respondents in the city center were most likely to shop online, and the inhabitants of the less affluent neighborhood of Fortuinwijk and the village of Warmond were least likely. This suggests that there are other mechanisms at play, and confirms the innovation hypothesis. For completeness, we also tested simple buffers and Walkscore, however, they were not significant.

The impact of the other variables was as expected: those who use the Internet on a daily basis and also those who have a smartphone (rather than a simple phone or no mobile phone at all), significantly shop more online. Previous literature found that more men shop online, however this seems an effect of the early days, as now women shop online much more often, especially for clothes. We found households with children had a greater likelihood of shopping online. Age was negatively correlated with online shopping. Educational level and household income were almost comparable, but income was included as it explains the likelihood of shopping online slightly better. We also tested the effects of being a student or having a job, but these were not significant.

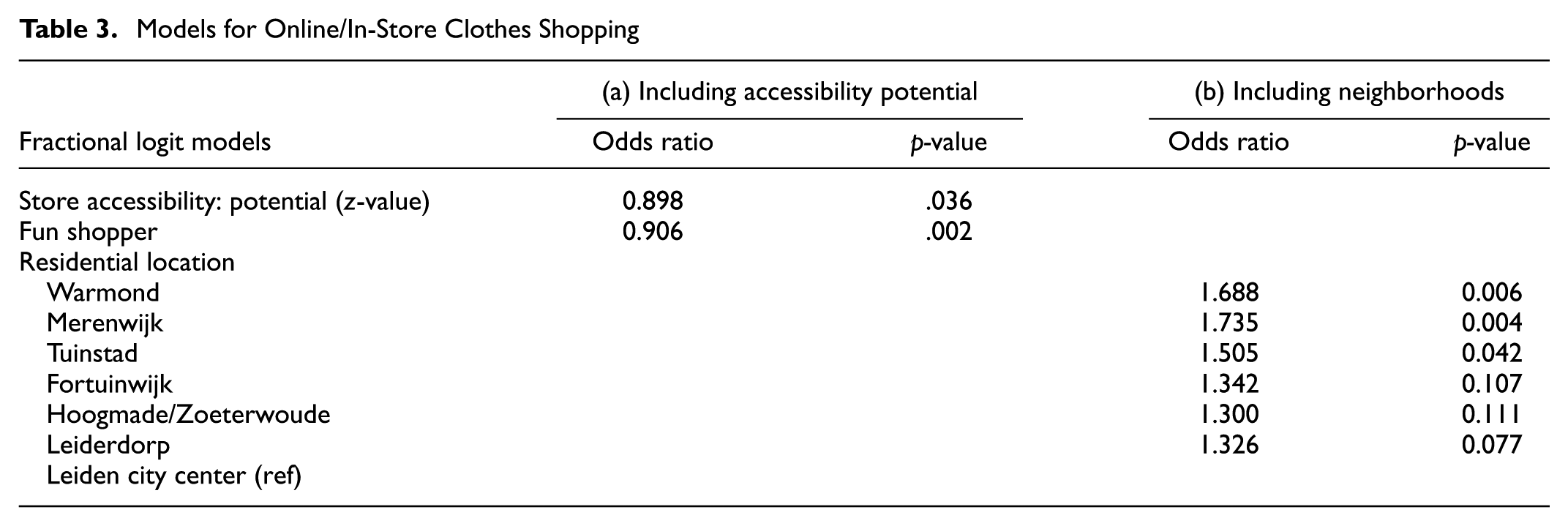

Next we estimated the share of online shopping for those who shop for clothes online (Table 3) using fractional logit. We found a negative relation between shopping accessibility and the proportion of online shopping. In addition, an interesting observation was that the negative effect of the respondents’ attitude toward “fun” shopping suggests that people who enjoy shopping tend to purchase relatively more in-store.

Models for Online/In-Store Clothes Shopping

Groceries

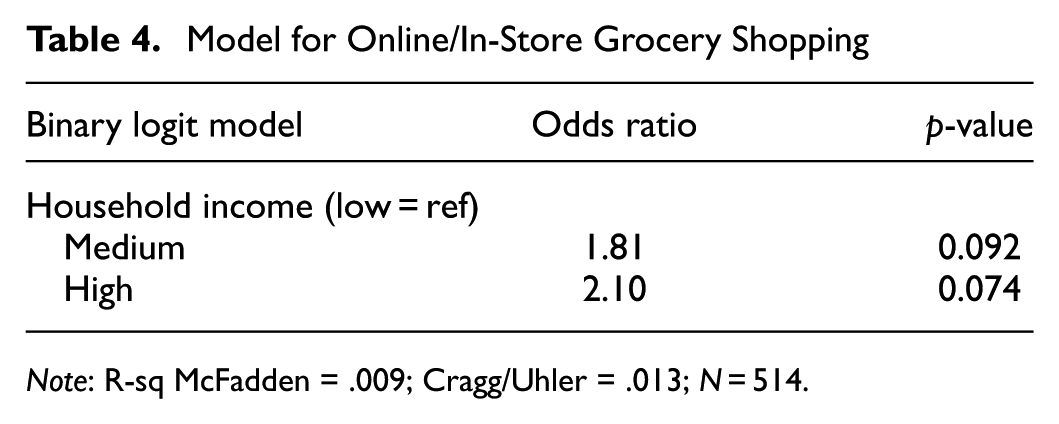

Shopping online for groceries is still in its infancy in the Netherlands. In our sample only 81 respondents (15%) bought groceries online. Groceries are typically experience goods. The role of shopping accessibility may also differ due to the need to purchase groceries frequently. Therefore store accessibility can be assumed to be important and hence, we can hypothesize that lower accessibility will go together with more online shopping.

The results of the binary logit analysis show, however, that shopping accessibility does not affect the likelihood of online grocery shopping. The only significant effect is income (Table 4). Higher income households are more inclined to buy groceries online. This confirms the innovation hypothesis, and is also plausible as home delivery for groceries comes with a delivery fee, to which higher income households are less sensitive. It is not surprising that no significant differences were found for accessibility, as grocery shops in the Netherlands are almost always nearby. The estimates of the fractional model did not lead to any significant effects.

Model for Online/In-Store Grocery Shopping

Note: R-sq McFadden = .009; Cragg/Uhler = .013; N = 514.

Books

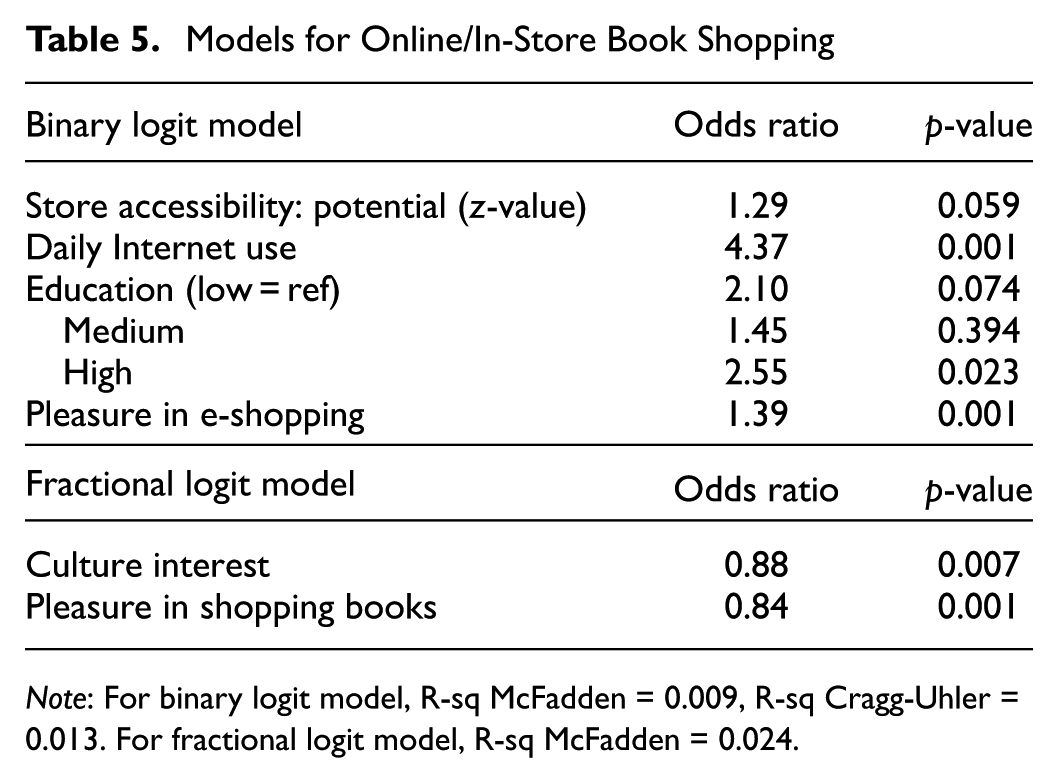

Books are search goods, which makes them very suitable to buy on the Internet. We found that higher shopping accessibility increases the likelihood of online shopping. This finding is contrary to the efficiency hypothesis; possibly the presence of book shops nearby and likely visits to these shops inspire readers to buy books, which they actually do not buy in-store but online. Buyers of books that are higher educated, spend more time on the Internet, and enjoy shopping online in general are also more inclined to buy online (Table 5).

Models for Online/In-Store Book Shopping

Note: For binary logit model, R-sq McFadden = 0.009, R-sq Cragg-Uhler = 0.013. For fractional logit model, R-sq McFadden = 0.024.

The results of the fractional model demonstrate that the proportion of online shopping for books is not related to shopping accessibility. So there is a higher probability that consumers will buy books online when book stores are nearby, but the proximity of these stores will not have an impact on the proportion of books bought online. On the other hand, interest in culture and pleasure in shopping for books do have an impact. It appears that buyers of books that have an interest in culture and take pleasure in buying books purchase less online than their counterparts.

Conclusions

The increasing penetration of e-retail will have major effects on physical stores, and the question is: In which areas will consumers replace most physical shopping with online shopping? Two apparently competing hypotheses were tested: the diffusion of innovation hypothesis and the efficiency hypothesis, formulated by Anderson et al. ( 8 ). In this paper we also tested these hypotheses by analyzing the influence of shopping accessibility on online shopping, controlling for demographic and socioeconomic factors and shopping-related attitudes. For this purpose two models were developed to explicitly consider the shoppers’ decisions regarding (i) whether or not to buy online, and (ii) the share of online shopping relative to in-store shopping. The models were estimated for three categories of goods (clothes, groceries, and books).

We found support for both hypotheses. For clothes shopping the results suggest that people with greater access to shops are more likely to buy on the Internet, which did not confirm the hypothesis of efficiency in relation to accessibility. However, a more likely explanation could be that people with greater shopping accessibility, who live in the city center more often, have a different demographic and socioeconomic profile (younger, higher educated, Internet-oriented) from their counterparts that makes them more inclined to buy online. This therefore confirms the innovation hypothesis. On the other hand, analyzing the proportion of online shopping compared with store shopping revealed that online consumers with lower access to shops purchase more online. This is plausible, considering that these consumers face greater inconvenience (time and cost) when visiting shops and therefore may use online shopping to reduce the number of trips. This supports the efficiency hypothesis.

For grocery shopping our study did not find any direct evidence for the influence of shopping accessibility on shopping online. In general, the inconvenience of visiting stores is low in the Netherlands, because of a high density of grocery shops. Moreover, the number of consumers that buy groceries online is small as it is still a rather new shopping service that is also not yet widely offered. Our findings demonstrate that higher income households are inclined to use online grocery shopping, as they are less sensitive to the additional costs of home delivery, and may be also more open to new technologies, as the innovation hypothesis suggests.

For book shopping we had a somewhat surprising result regarding the impact of accessibility on online shopping. Potential buyers living near bookstores are more likely to buy online than their counterparts. It seems that the presence of bookstores nearby and likely visits to these stores inspire people to buy books that are actually not bought in these in-store shops but online. The motivation for this behavior is, however, unclear. Conversely, we found that taking pleasure in buying books and an interest in culture discourage online shopping and encourage buyers to purchase books in-store.

Overall, we can conclude that shopping accessibility may have an impact on online shopping, but its impact seems limited and varies between different types of goods. In the end, e-shopping behavior remains primarily shaped by households who are open to new technologies, and only to a limited extent by efficiency considerations.

Footnotes

Author Contributions

The authors confirm contribution to the paper as follows: study conception and design, data collection, analysis and interpretation of results, draft manuscript preparation: KM, RK. Both authors reviewed the results and approved the final version of the manuscript.

The Standing Committee on Effects of Information and Communication Technologies (ICT) on Travel Choices (ADB20) peer-reviewed this paper (18-00303).