Abstract

The English conquest and colonisation of Ireland, which began in the years around 1170 was accompanied by the introduction of an administrative system based on English models. From the point of view of the crown, perhaps the most important of the new offices of government that it established was the exchequer, which coordinated the financial exploitation of its Irish lordship. The exchequer generated a vast quantity of written documents recording its operations. This paper subjects one such document, detailing the sums received at the exchequer for the year 1301–2, to data science techniques in order to gain added insight into the routine functioning of the financial arm of English government in its oldest colony. It thereby also reveals previously unrecognised patterns in the nature of English power in Ireland. The purpose of the paper is not to assess the state of Irish finances in the early fourteenth century, but rather to argue that a deep reading of a single document produced by an elaborate bureaucratic system, combined with data science visualizations, can help to generate new research questions in relation to a substantial body of financial records which are soon to become more widely available to both scholars and the general public.

Keywords

Introduction 1

Students of Irish history for the period after the English conquest of the late twelfth century have long appreciated the value of the records produced by the exchequer – the institution responsible for the financial affairs of the lordship. Historians have drawn on these records to identify general patterns of revenue collection and disbursement on the island and to understand the place of the exchequer in the broader administrative structure that supported English rule in Ireland. 2 To date, the information they contain has not been interrogated to reveal what might be called the rhythms of the Irish financial year – the patterns of the exchequer's operations in terms of its busy and slack times, the various tasks in which it engaged, and the types of people with whom it dealt. Awareness of such issues breaks down the barriers between administrative history and wider approaches to the past and adds to understanding of the relationship between bureaucracy and the nature of power in a colonial setting. 3

To demonstrate the potential of exchequer material to open up new avenues of research in medieval Irish history, analysis was undertaken of one record produced by the institution, the receipt roll for 1301–2. 4 To make a point at the outset that will bear repeating later: this roll is one of many that survive from the period roughly between 1280 and 1360. We present it as a ‘trial piece’ and deliberately eschew extrapolating from it arguments about longer-term trends that might well be overturned when a wider pool of records is subjected to the same type of analysis. Before discussing the nature of the receipt roll and the reasons for selecting it for examination, it is important to recognise that recent developments in the funding of historical research in Ireland make this an opportune moment to embark upon this type of investigation. 5 The government of Ireland-funded ‘Beyond 2022’ project, phase II of which commenced in 2019, aims to reconstruct digitally the historical archive lost at the outset of the Irish Civil War in 1922. In June 2022, to mark the centenary of the destruction of the Public Record Office in Dublin, an open access ‘Virtual Record Treasury’ containing this digitized material was launched. 6 This includes the surviving medieval Irish exchequer records preserved at The National Archives (TNA) in Kew, as well as later copies of records that have subsequently been lost. Furthermore, the Beyond 2022 project has identified this exchequer material as one of its ‘Gold Seams’. This initiative involves detailed analysis of series of records which on account of their quantity and state of preservation both merit and can sustain intense investigation. The ‘Records of the Medieval Irish Exchequer’ Gold Seam initiative will have as its source base about one million individual data entities, of which half are derived from original TNA manuscripts. 7

The examination of the receipt roll of 1301–2 was undertaken with reference to this developing research environment and its strong digital humanities component. The aim was to employ a set of tools and techniques used by data scientists to extract numerical (financial) and other data and to explore that data in a series of plots and visualisations. 8 The authors secured funding from the Jean Golding Institute (JGI) at the University of Bristol to undertake work on a project entitled ‘Digital Humanities meets Medieval Financial Records: The Receipt Rolls of the Irish Exchequer’. 9 With a view to identifying ways in which the data science methodologies used in the project could be incorporated into the ‘Records of the Medieval Irish Exchequer’ Gold Seam initiative, the Programme Director of Beyond 2022, and medieval specialist, Dr Peter Crooks, was consulted as the project progressed. Mike Jones continues to work as a consultant on the Gold Seam initiative while Brendan Smith is a member of the International Cultural and Scientific Advisory Panel of Beyond 2022. 10

The Irish Exchequer and its Records

It is necessary at the outset to offer a brief account of the history of the Irish exchequer and how it conducted its operations, before discussing in more detail the receipt roll of 1301–2. Some organised way of collecting and recording revenues extracted from Ireland must have been in place from very soon after King Henry II visited his new conquest in 1171–2, and by 1200 an exchequer, based on the English model, was operational. 11 The exchequer year began on 30 September and ended on the following 29 September. It contained four terms: Michaelmas (commencing 30 September), Hilary (commencing 14 January), Easter (commencing eight days after Easter Sunday) and Trinity (commencing the day after the feast of the Holy Trinity, the date of which varied in relation to the date of Easter.) Documents produced by the exchequer were dated with reference to the regnal year of the reigning monarch. Edward I's reign began on 20 November 1272, and the receipt roll of 1301–2 was therefore identified as the roll for 29 & 30 Edward I. 12

As was the case in England, the Irish exchequer consisted of two departments, each of which produced, in Latin, written records of its business. The lower exchequer, or exchequer of receipt, was where money was taken in and given out. The sums disbursed or ‘issued’, were recorded on issue rolls. 13 The format of the issue rolls changed over time, but by the end of the thirteenth century they were produced annually and recorded payments out of royal revenue on a term-by-term basis. Payments were grouped under different categories, such as fees paid to senior government officials and the keepers of royal castles, alms distributed to religious orders, and the smaller sums expended to remunerate exchequer clerks and to supply the office with the equipment it needed to fulfil its functions. Under the latter heading for 1301–2, for instance, the issue roll records the purchase of knives to make tallies, counters to represent monetary sums as accounts were drawn up, dishes and canvas bags in which money could be held and transported, locks for the doors of the exchequer, rushes and mats for the rooms in which it conducted its business, as well as rolls of parchment on which details of exchequer business were entered, ink, and the special green wax used to seal exchequer correspondence. 14

Money due to the crown from its officers and from private individuals and communities was handed into the lower exchequer in return for a receipt in the form of a wooden tally stick on which details of the payment were recorded by notches carved in the wood. This stick was carefully split in two, with half being given to the accountant and half retained in the exchequer, enabling the account of the former to be audited later. A written record of these tallies was entered each day on receipt rolls. A typical receipt roll entry identified the place or activity which generated the money (usually a county, liberty, or town, or a form of occasional taxation), the name and office of the person making the payment, the reason why the payment was being made, and the amount concerned. Totals of sums received were given by the day, week and term and a roll produced for each exchequer year. 15 The receipt roll of 1301–2 records sums being submitted at the exchequer from all eleven of the counties then in existence on the island - Connacht, Cork, Dublin, Kerry, Kildare, Limerick, Meath, Roscommon, Tipperary, Uriel/Louth, and Waterford – four of its five liberties – Carlow, Kilkenny, Trim, and Wexford – and the towns of Drogheda in Meath, Drogheda in Uriel, Dublin, Ross, and Waterford. The escheator, collectors of customs duties, and the merchants of Lucca, who controlled the commerce in wool, also handed in sums at the exchequer. 16

Source of payments per term.

The upper exchequer was where accounts were audited and where legal matters arising from this auditing process were heard. Respectively, these aspects of its work were recorded on the pipe rolls and the memoranda rolls. The pipe roll held the highest position in the hierarchy of exchequer records. Unlike the issue and receipt rolls, its entries were not arranged chronologically but geographically and then thematically, thereby affording the opportunity to cross-check financial information contained in other records. In Ireland as in England, the crown sought to detect and deter corruption in the exchequer. In 1232 a clerk of the Irish chancery was instructed to produce a copy of the pipe roll and this practice was later adopted in the exchequer of receipt, resulting in three copies of each receipt roll and issue roll being compiled simultaneously for different exchequer officers to enable cross-checking. From 1234 the Irish treasurer's account was audited in Dublin and an indenture sent to the king informing him what revenues were at his disposal in Ireland. 17

The limitations of this system of monitoring became apparent in the 1280s, as Irish revenues failed to keep up with the demands generated by Edward I's expansive brand of kingship. The treasurerships of Stephen Fulbourne (1274–85), bishop of Waterford from 1274 to 1286 and archbishop of Tuam from 1286 to his death in 1288, and his successor at the exchequer, Nicholas Clere (1285–91) were characterised by such obvious corruption that the crown was moved to act. 18 The accounts of these treasurers were sent to the English exchequer at Westminster for audit, and Clere's venality was found to be so extreme that he was dismissed and imprisoned. In 1290 the Irish chief governor, John Sandford (1288–94), who was archbishop of Dublin from 1285 until his death in 1294, presented petitions from Ireland to the English parliament demanding reform of the system, with the result that in 1292 and 1293 parliamentary ordinances were passed that instituted new arrangements for the Irish exchequer. 19 From that time the accounts of the Irish treasurer were to be audited at the English exchequer either annually or, more commonly, at the end of the treasurer's term of office. The Irish treasurer was henceforth required to bring with him to Westminster his rolls of receipts and payments and supporting documentation, while one of the duplicate sets of these rolls - that produced by the chamberlains of the exchequer - was also presented at the audit for purposes of verification. With some interruptions, this system of audit operated until the middle of the fifteenth century. 20

Crucially, the Irish treasurer's rolls and supporting documentation remained in the English exchequer after his audited account had been entered on the English records and he had returned to Ireland. The archive of the Irish government in Dublin suffered significant losses from the thirteenth century onwards; by the early nineteenth century almost the entire corpus of medieval chancery material had disappeared, leaving only a handful of rolls to face immolation in the Four Courts fire of June 1922. A greater body of exchequer records had survived down the centuries, allowing calendars to be published of Irish pipe rolls in the decades around 1900, but the records of the lower exchequer had not been tackled by the time they were consumed in the 1922 fire. 21 Were it not for the system of audit at Westminster engendered by the heroic scale of corruption that prevailed at the Dublin exchequer in the late thirteenth century, the great mass of Ireland's medieval financial records now conserved at The National Archives (hereafter TNA) at Kew would no longer exist. With the advent of Beyond 2022, access to this material will be transformed. 22

It was, as we have seen, the records of the lower exchequer – the receipt rolls and issue rolls and associated documents – that the Irish treasurers, accompanied by one of the exchequer chamberlains, brought with them to London., and hundreds of these documents still survive. Thanks to the efforts of the late Philomena Connolly, archivist at the National Archives of Ireland, Dublin, until her early death in June 2002, we possess published translations of all the medieval Irish issue rolls preserved at TNA.

23

No attempt has been made to produce an equivalent publication of the receipt rolls, though for the period up to 1307 calendars of translated receipt rolls can be found in the volumes of Sweetman's Calendar of Documents Relating to Ireland.

24

It was known that Sweetman's calendars of the rolls were incomplete and in 2005 Paul Dryburgh and Brendan Smith published a full translation of the receipt roll for 1301–2. This roll was selected because of its excellent state of preservation and because its size - it comprises eighteen membranes - was representative of receipt rolls from this period. It was found that Sweetman's calendar of the document had omitted about twenty per cent of its contents. It was on this published translation that Mike Jones conducted his data analysis and visualization work.

25

Technical Approaches and Patterns of Business at the Exchequer

The first technical task of the project involved the development of a data processing pipeline that could convert the transcript of the receipt roll produced by Dryburgh and Smith into a format that was easily read and handled by statistical software. The project used the Python programming language to develop a series of scripts to create this data processing pipeline. 26 The pipeline had two stages. The initial stage extracted information into comma-separated values (CSV) files, which is analogous to a spreadsheet with headings and rows of data delimited by a comma. The structure of the entries in the receipt roll, and thus in the transcript, were for the most part regular and it was possible to write a Python script that used regular expressions – a process of finding defined patterns in the text – to extract the information of interest.

A Python script was written which generated two CSV files. In the first file, each row represented a proffer to the exchequer and tracked:

membrane number on which the proffer was written financial term, e.g. ‘Hilary’ date of a proffer, in the format ‘YYYY-MM-DD’ week of the financial term, e.g. ‘3’ order of the entry within a day's business within the exchequer place or entity associated with the payment, e.g. ‘Dublin’ details of the proffer from the transcript, e.g. ‘John fitz Adam, ½ mark to have a writ’ value submitted in pounds, shillings, pence or marks value submitted in pennies as a decimal number, e.g. £1 6s. 4¾d. was converted to 316.75, making these sums easier to compute, graph and plot. (This also had the practical advantage of serving as a reminder that the only coin in circulation was the silver penny – the ‘denarius’.)

The second CSV file created a record of the daily totals of the receipts as recorded by the clerk of the exchequer. This second file had a vital function – it enabled a comparison between the daily totals calculated by the clerk and daily totals computed by a Python script from the data in the first CSV file. Developing the regular expressions for content extraction was an iterative process, and widely varying differences in daily totals pointed to issues with the processing. Small variations in the totals suggested issues with the transcript and, indeed, a handful of errors were discovered. Finally, slight variations might denote errors by the medieval scribe or clerk. In this regard, we can demonstrate that the clerk made a single error in the whole financial year, missing a penny on 24 May 1302. 27

The next stage of the pipeline was to process the CSV file and add three additional columns:

people mentioned in the proffers places mentioned keywords

To extract entities (people and places) and keywords, we used the Natural Language Toolkit (NLTK).

28

By using NLTK's default part-of-speech (POS) tagger, it was possible to break down a sentence into tokens, with each token assigned a tag indicating if the token was a proper noun, noun, pronoun, verb, preposition, conjunction etc. The default tokenization was then adjusted to ensure that the use of certain Anglo-Norman French words, namely ‘fitz,’ ‘le’, ‘del’ and ‘de’ – were consistently tagged as foreign words. Also, the tokenization of pound, shilling and pence values caused a lot of ‘noise’ that made the processing of the tagged tokens cumbersome, so a placeholder substituted these values. So, with the entry ‘Walter de Boneville, 3s. 4d. for unjust detention’ the following tokenization is created: [(‘Walter’, ‘NNP’), (‘de’, ‘FW’), (‘Boneville’, ‘NNP’), (‘,’, ‘,’), (‘OVP’, ‘OVP’), (‘for’, ‘IN’), (‘unjust’, ‘JJ’), (‘detention’, ‘NN’)]

In this example, we can see that ‘Walter’ and ‘Boneville’ are tagged as proper nouns, while ‘unjust’ and ‘detention’ are classified as an adjective and noun respectively. By having the details of the proffer tokenized, it was possible to create some pattern matching to provide simple entity extraction. For example, the grouping of the following tags – ‘’ – might indicate a person's name like ‘Walter de Boneville’. Development of this phase of the data processing was, again, an iterative process and more complex patterns were created to capture people (with their occupations if specified) and places. By using entity extraction, it was possible to identify origins and occupations, such as ‘Adam le Fleming’, ‘Richard de Exeter’, ‘Ralph the baker’, ‘Nicholas the clerk’ and ‘William le Archer’. This was a simple approach, adopted due to the resource constraints of the project, and had its shortcomings. For example, using this model, the place ‘Ashby de la Zouch’ would be incorrectly identified as a person. At present, the pipeline is particularly poor at identifying women, since they are often unnamed and described as an adjunct to man, such as someone's ‘wife’, ‘daughter’ or ‘ward’. Finally, each row in the CSV file is processed in isolation, and this results in the meaning of ‘the same’ – when the scribe refers to person, place or reason for a payment in the proceeding entry – being lost.

By converting the transcript to a CSV file, we were able to explore and interrogate the data with the pandas data analysis tool and create plots and graphs with the Matplotlib and Seaborn visualization libraries. 29 As a result, it was possible to extract summary data for the financial year. Before offering contextualization of these data, it is useful to set out some of the general patterns they reveal. For example, 873 transactions were recorded, giving a total value of receipts of £6159 18s. 5d. (As noted earlier, this was one penny more than the total recorded by the Exchequer clerk.) The two smallest payments were eightpence each, namely towards the rent owed on New Grange, Dublin, by William de Meones; and the rent on the lands of the deceased felon, William le Fleming. 30 The largest single payment, £310, was made by Thorosanus Donati, the attorney of the Florentine merchant society of Frescobaldi, for ‘the arrears on his account of the Dublin exchanges’. 31 This large variation between the minimum and maximum results in the mean and medium values of £7 1s. 1d. and £1 10s. 2d. respectively. The most common payment was 6s. 8d. or half a mark. This value of payment occurred 101 times and accounted for just under twelve per cent of the business that year, but in total only provided the crown with £33. 13s. 4d. and thus only accounted for less than half a percent of the yearly total. A half mark was a common fine for obtaining a writ, trespass, or non-appearance when summoned. 32

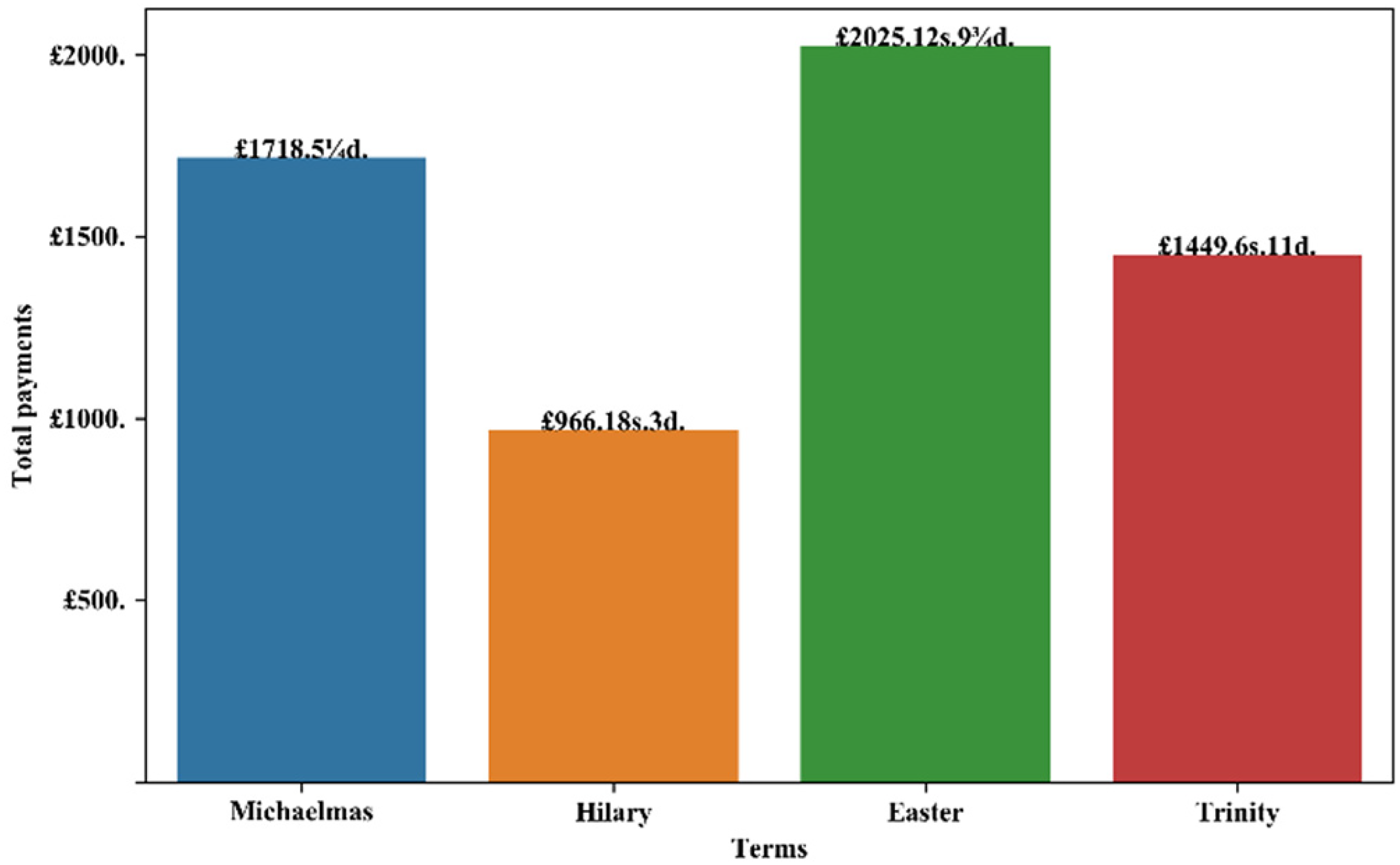

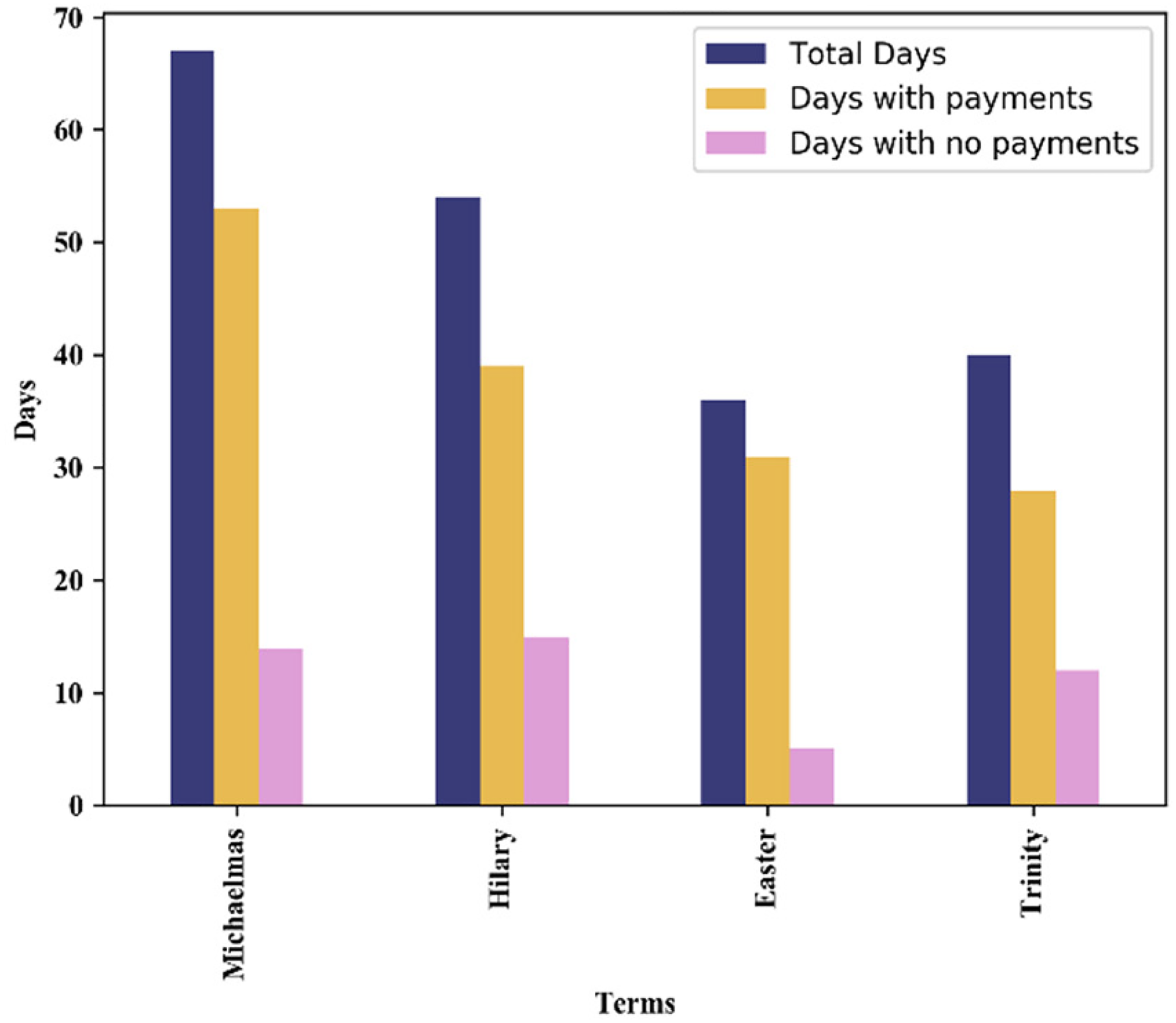

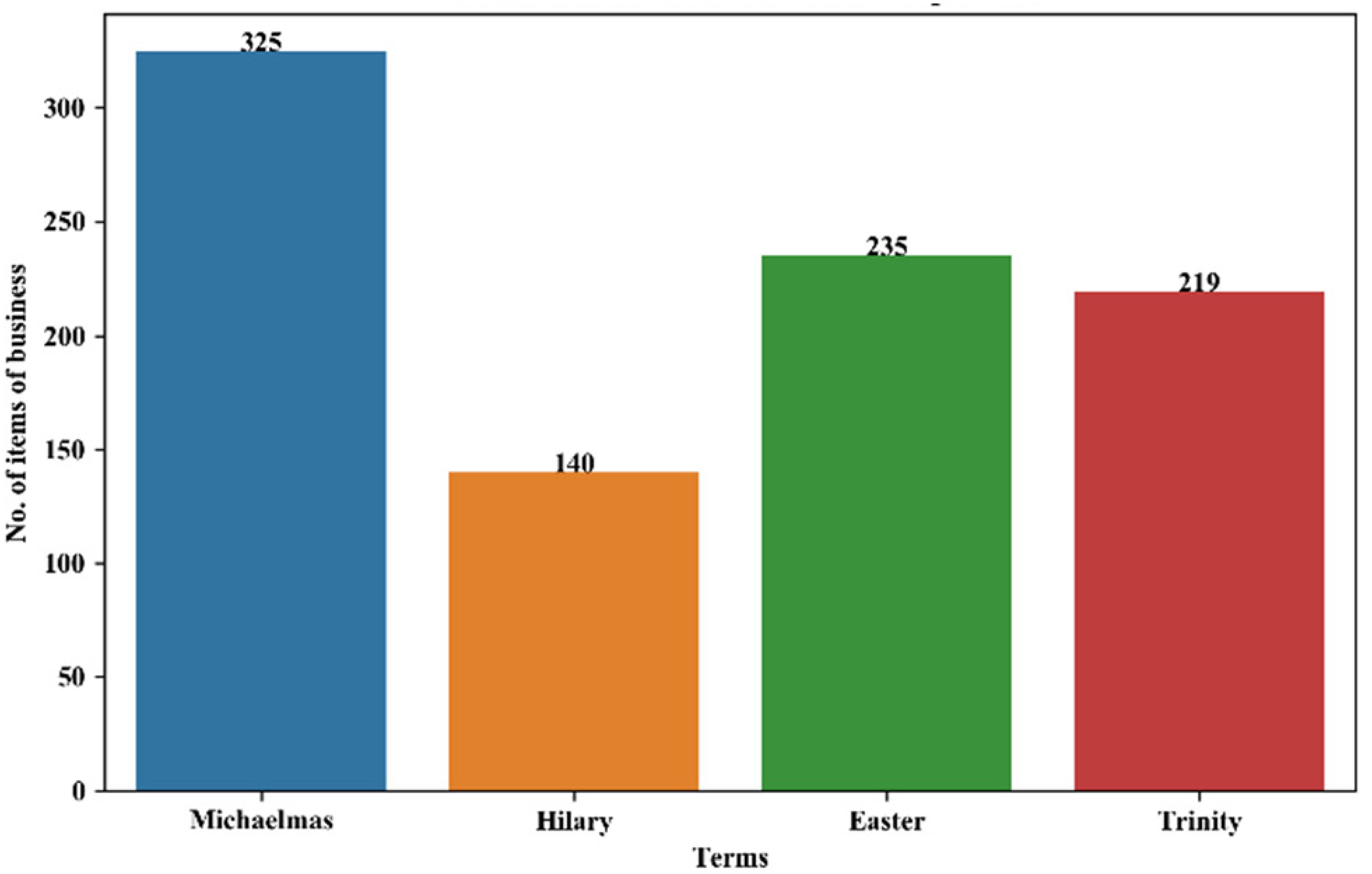

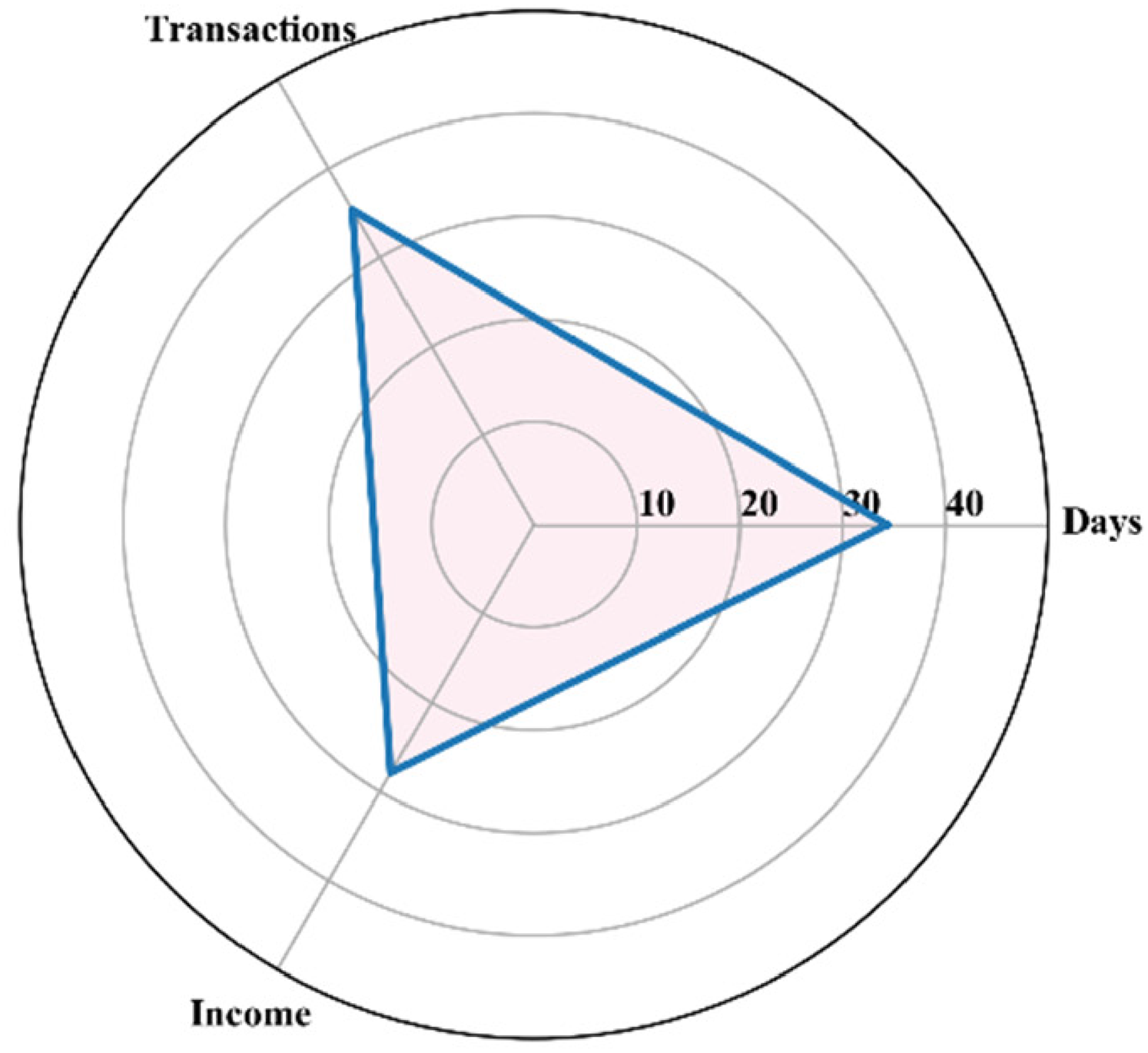

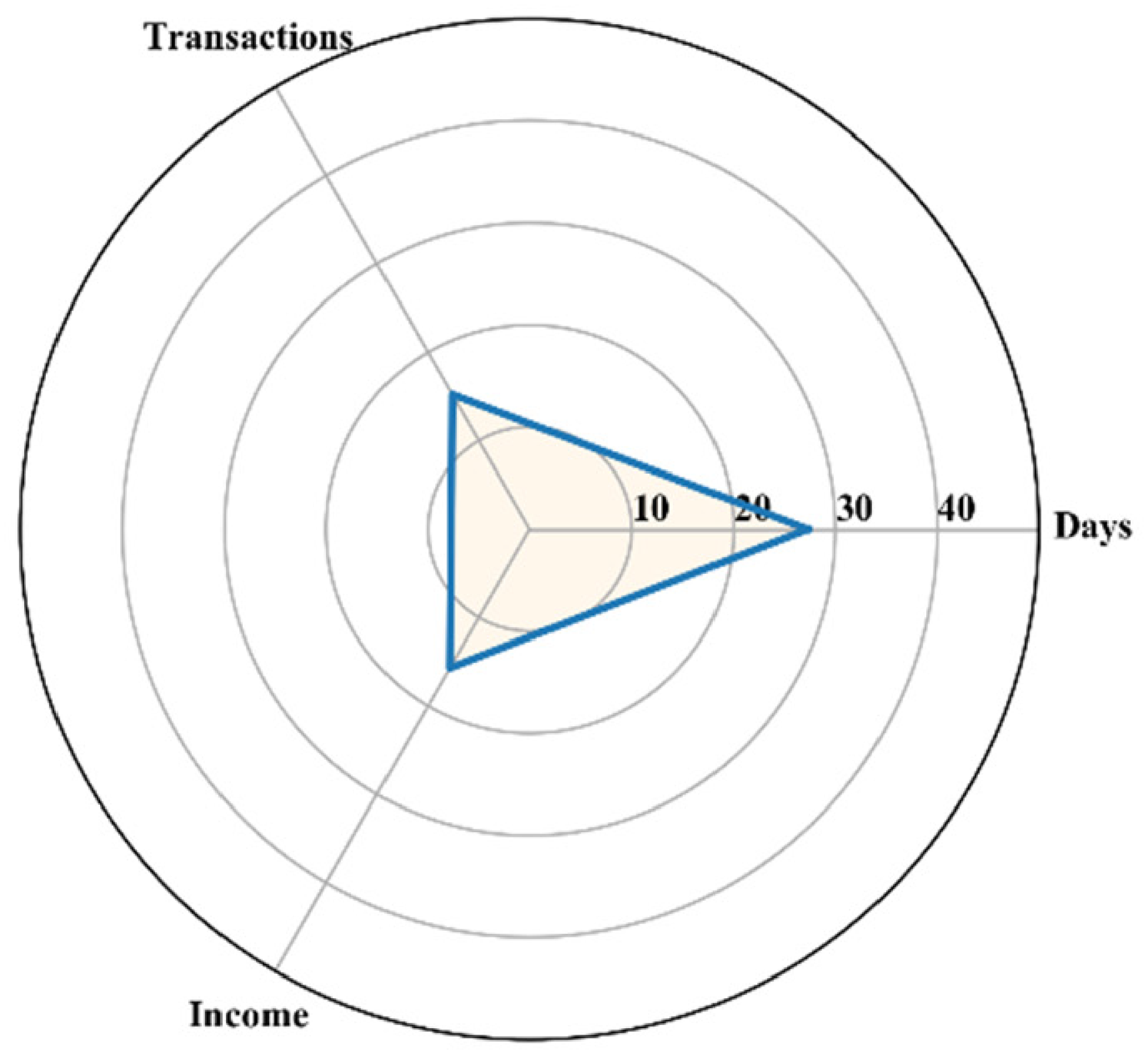

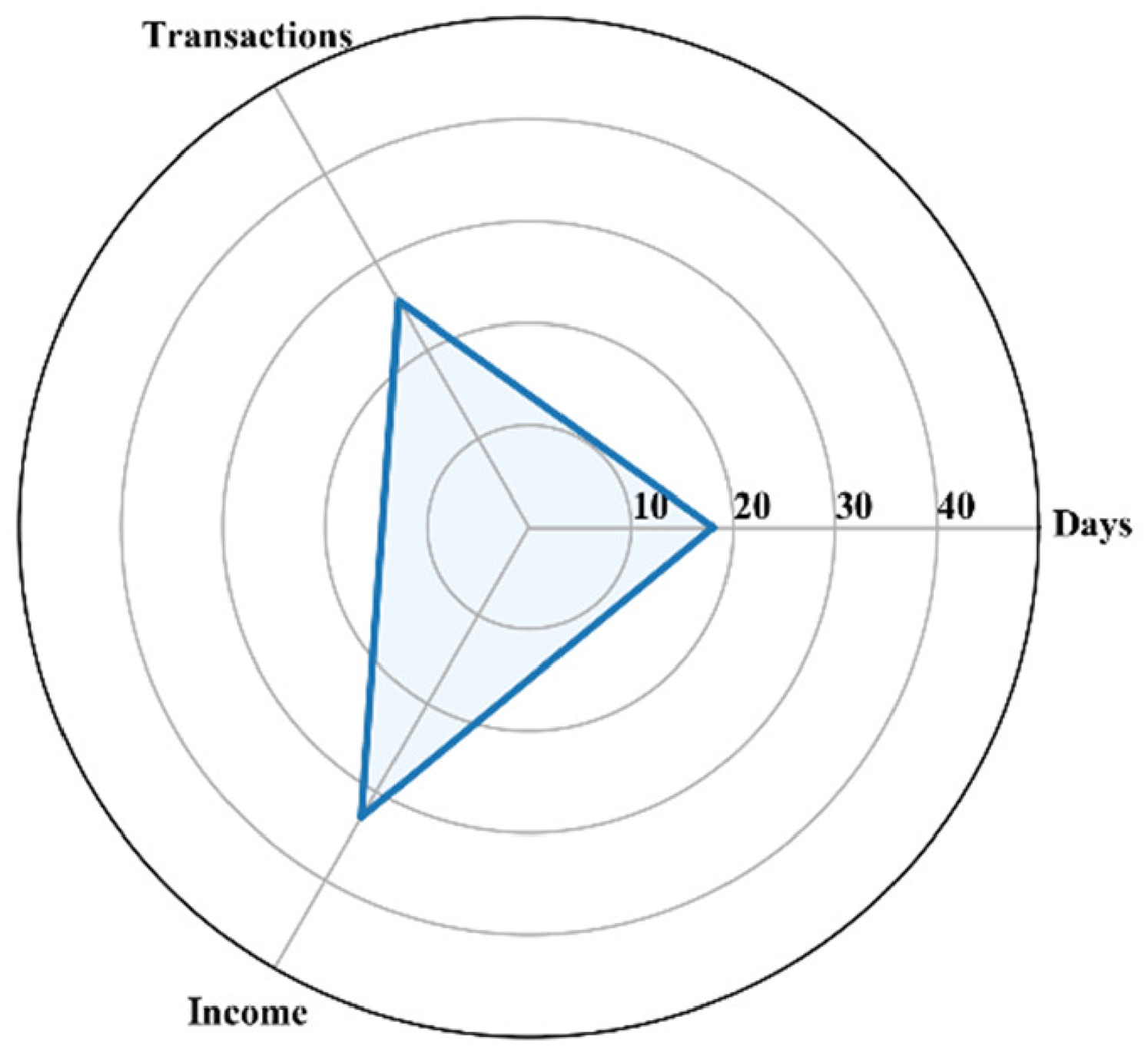

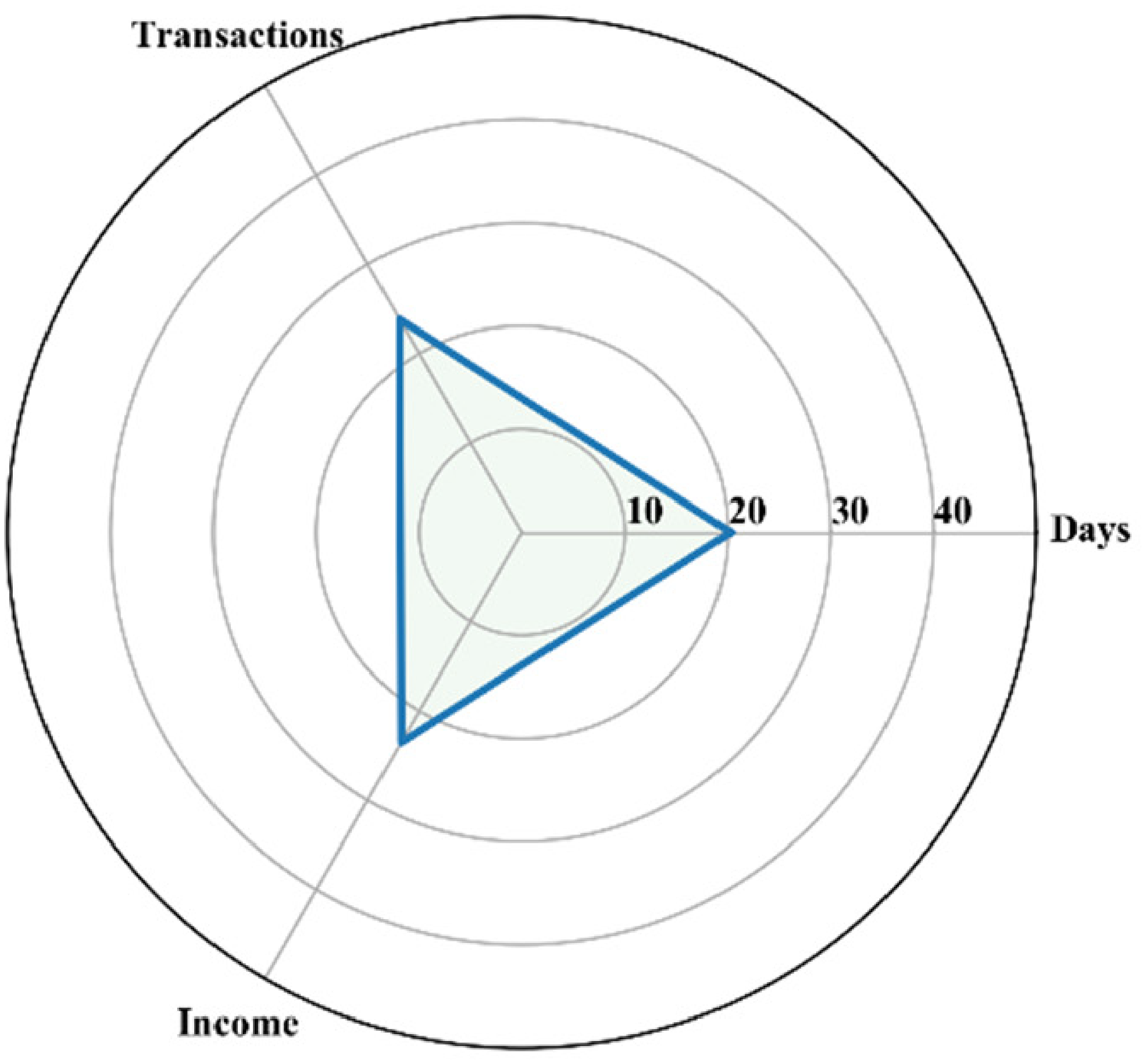

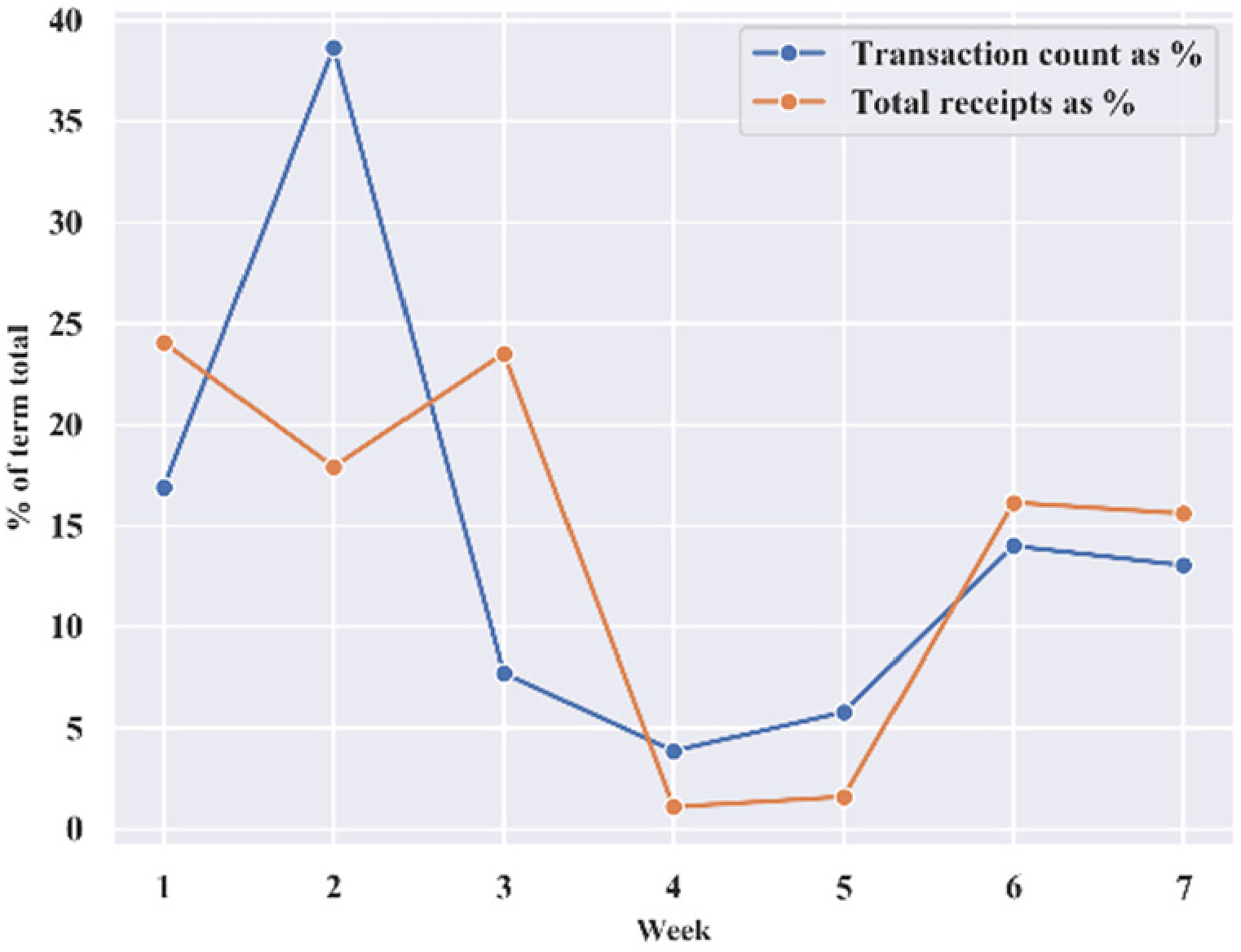

The payments were unevenly distributed across the four financial terms, with Easter bringing in the largest value in receipts (Figure 1). 33 However, the terms themselves were of unequal length, and the number of days during each term on which the exchequer did not sit on account of the observation of Christian feast days, or on which no payments were received, also varied (Figure 2). Also subject to variation was the amount of business conducted across the year, as signified by the number of proffers received. Michaelmas term was the longest and busiest term (Figure 3). A set of radar plots can better illustrate the relationship between the amount of money received, the number of transactions (proffers) recorded, and the length of each financial term (Figures 4–7). In the plots, each variable is given as a percentage of the whole year. Michaelmas was the longest and busiest term and accounted for around 35 per cent of the proffers made to the exchequer, whereas Easter (Figure 6) was the shortest term, accounting for less than 20 per cent of the time the exchequer was in session. On the other hand, as noted above, Easter was the most financially rewarding for the crown, accounting for over 30 per cent of the revenue for the financial year 1301–2.

Total payments per term.

Number of days per term.

Total number of items of business per term.

Michaelmas.

Hilary.

Easter.

Trinity.

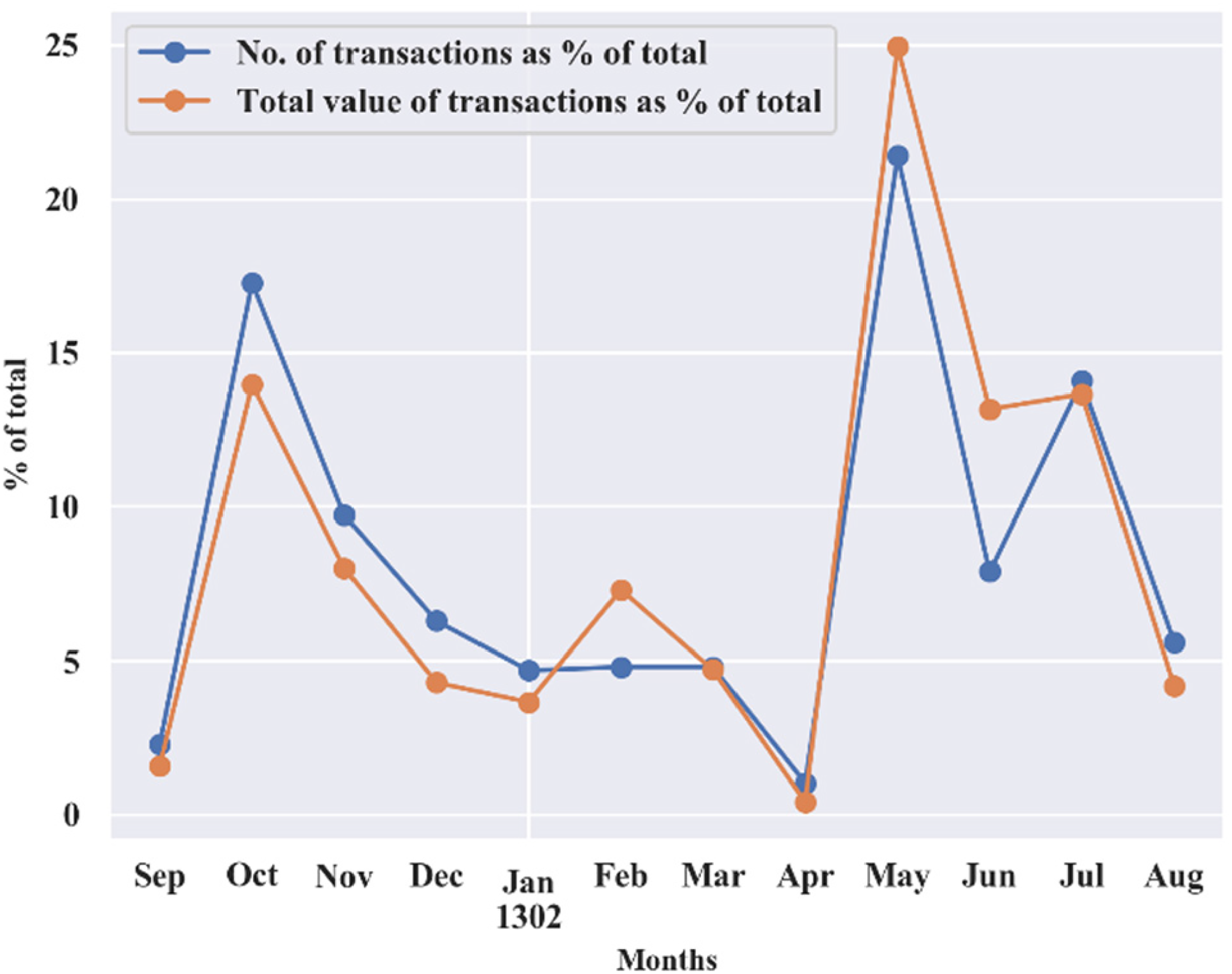

These general features of exchequer activity will come as no surprise to students of medieval English finance and government. 34 In both England and Ireland sheriffs were required to appear in person at the exchequer in both the Michaelmas and Easter terms, a procedure known as the adventus. It was to be expected that they would bring with them substantial portions of the sums they were mandated to collect. It should be remembered that the only coin in circulation was the penny, meaning that delivering significant sums into the exchequer required the transportation of large quantities of coin. In the English exchequer in the thirteenth century, the adventus led to receipt of income being concentrated in the first two weeks of those two terms. The data for the Irish exchequer for 1301–2 displays both similarities and differences to this pattern. Figure 8 plots the monthly payments received by the exchequer in terms of their value and business, that is, the number of transactions (proffers) received. The values are normalized, so they are represented as a percentage of the whole year. The peaks and troughs of the transactions and the income from those transactions broadly follow each other, which indicates that a small number of proffers of high value do not dominate the receipts. Two prominent peaks are evident for October and May, the start of the Michaelmas and Easter terms, with smaller peaks in February (Hilary) and July (Trinity). This is in line with patterns observable at the English exchequer. 35

No. of transactions and their total value, per month, as a per cent of the total for the year.

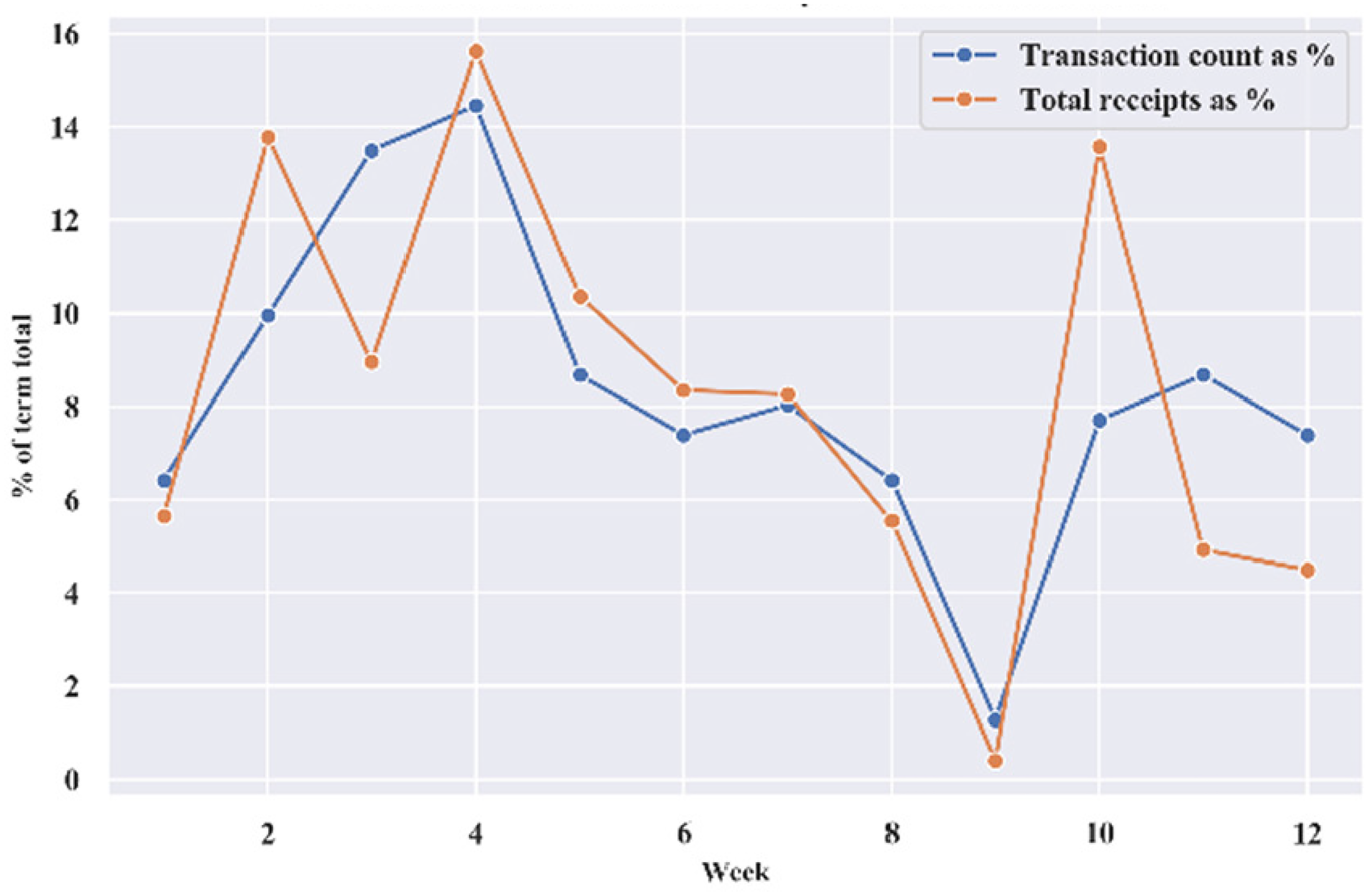

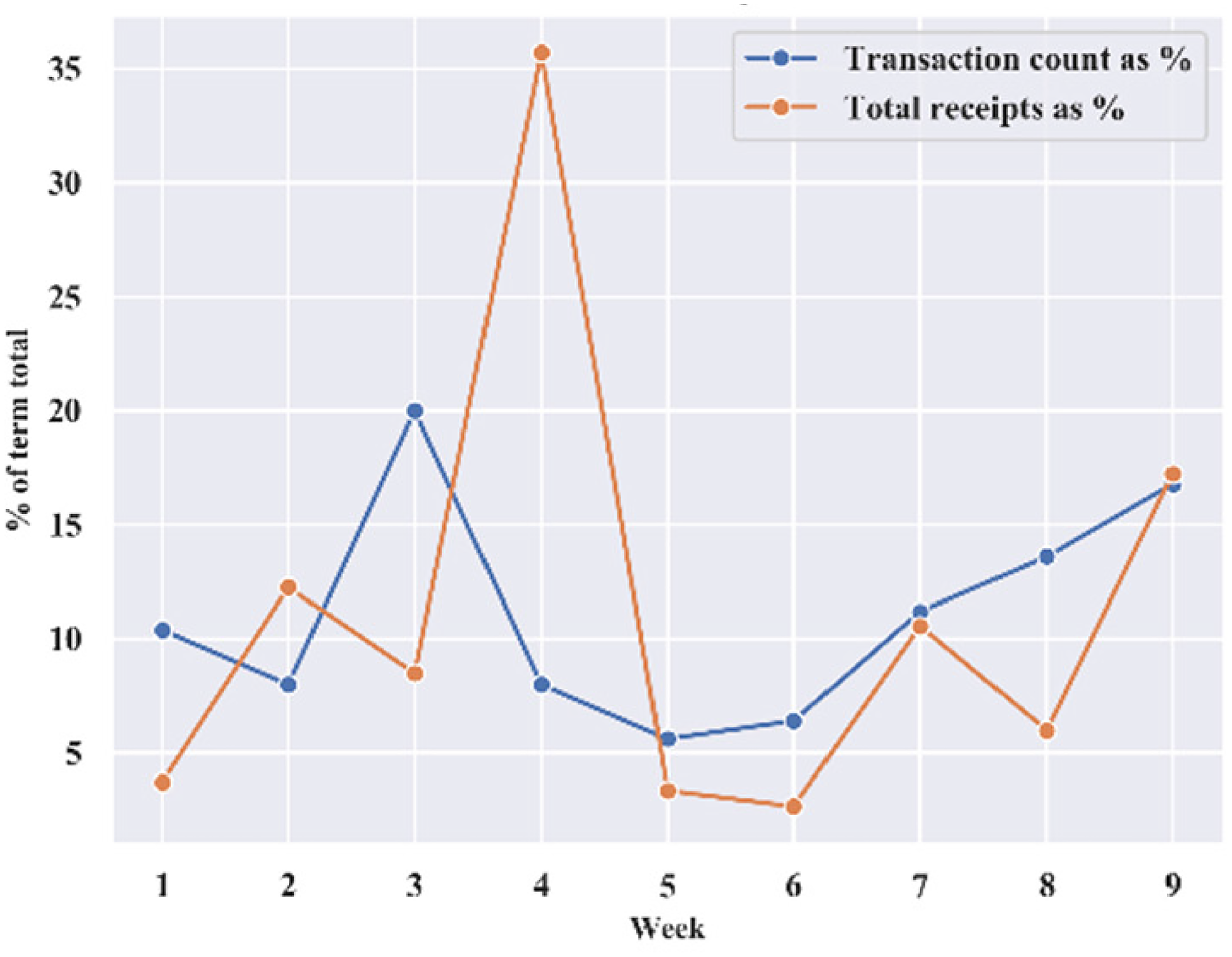

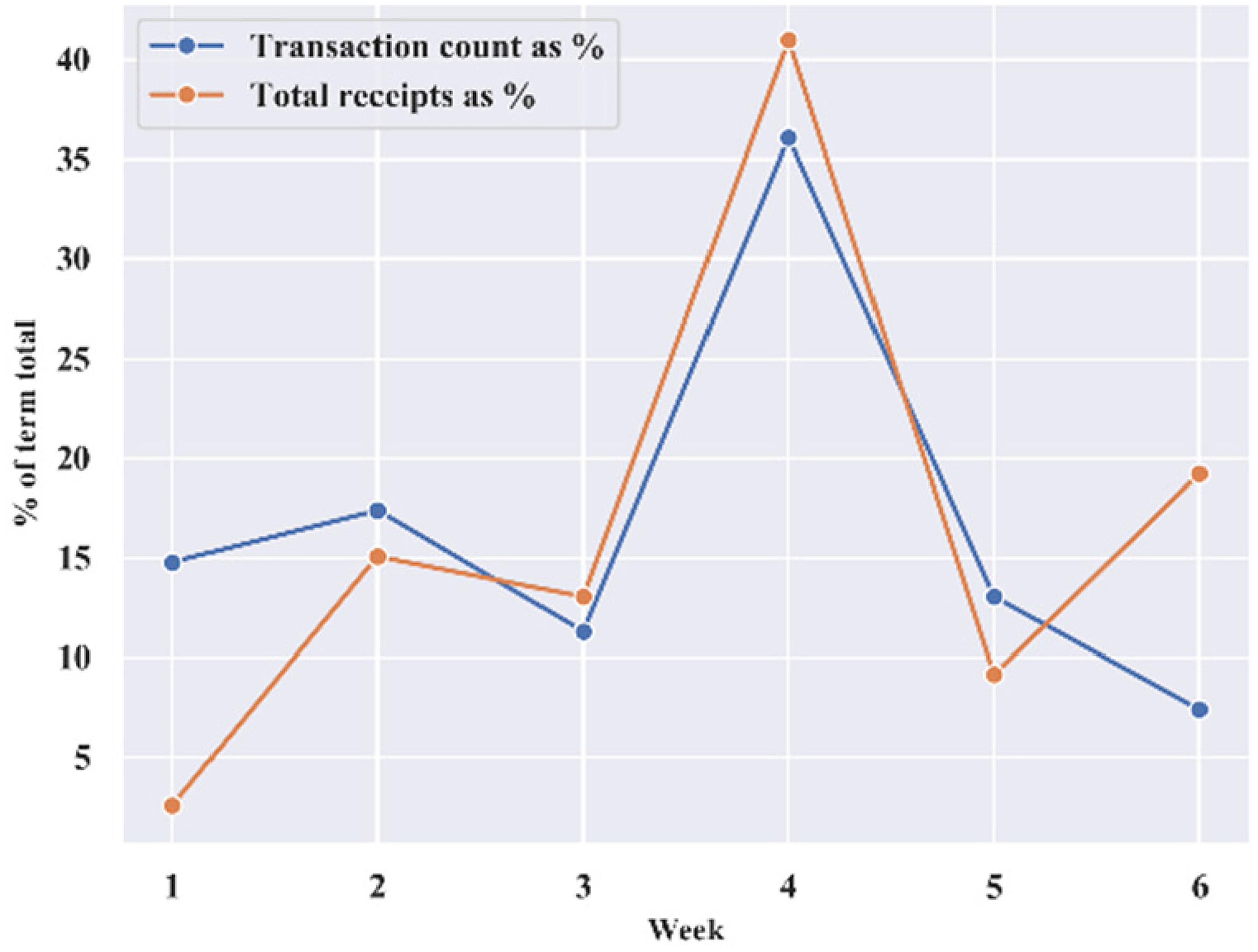

A more complicated picture emerges, however, when plots are generated that focus on weekly, rather than monthly, payments. The patterns of the peaks and troughs of transactions against total income received again broadly match each other, with some glaring exceptions since, at this level, individual receipts of high value can dominate. In Michaelmas term (Figure 9), the peaks of income are in the second, fourth and tenth weeks, while the largest number of transactions occur in the fourth week. An individual payment of £154 3s. 7d. from the merchants of the society of Riccardi of Lucca accounts for the disparity in the second week. 36 In the tenth week, a small number of proffers of large amounts made by two sheriffs explains the high value of income compared to the lower level of transactions. Roger Bagot, sheriff of Limerick, returned £76. 6s. 8d. for the ‘debts of divers persons’, while William de Cauntone, sheriff of Cork, proffered £100 in forfeited property of felons and fugitives. 37 The lack of payments in the ninth week was caused by exchequer not sitting for the feasts of St Edmund (20 November), St. Clement (23 November) and St Catherine (25 November) with only a small number of proffers received from Dublin on the few days it was sitting. 38 In Hilary term (Figure 10), the peak of transactions appears in the third week while a larger amount of income comes in the following week. The latter is mainly accounted for by two payments – £173 6s. 8d. and £99 13s. 7d. – from the city of Cork for aid promised to the king. 39 Easter term (Figure 11) is more straightforward, with the bulk of transactions and income received in the fourth week. In Trinity (Figure 12), the basic pattern is similar to that of Hilary term. The second week sees the largest number of receipts received, whilst the bulk of income appears in the first and third weeks. The first week saw another payment from the merchants of the society of Riccardi of Lucca, this time amounting to £197 6s. 8d., while the third week saw the Frescobaldi pay £310. 40

Michaelmas. No. of transactions and total receipts as per cent of the term total.

Hilary. No. of transactions and total receipts as per cent of the term total.

Easter. No. of transactions and total receipts as per cent of the term total.

Trinity. No. of transactions and total receipts as per cent of the term total.

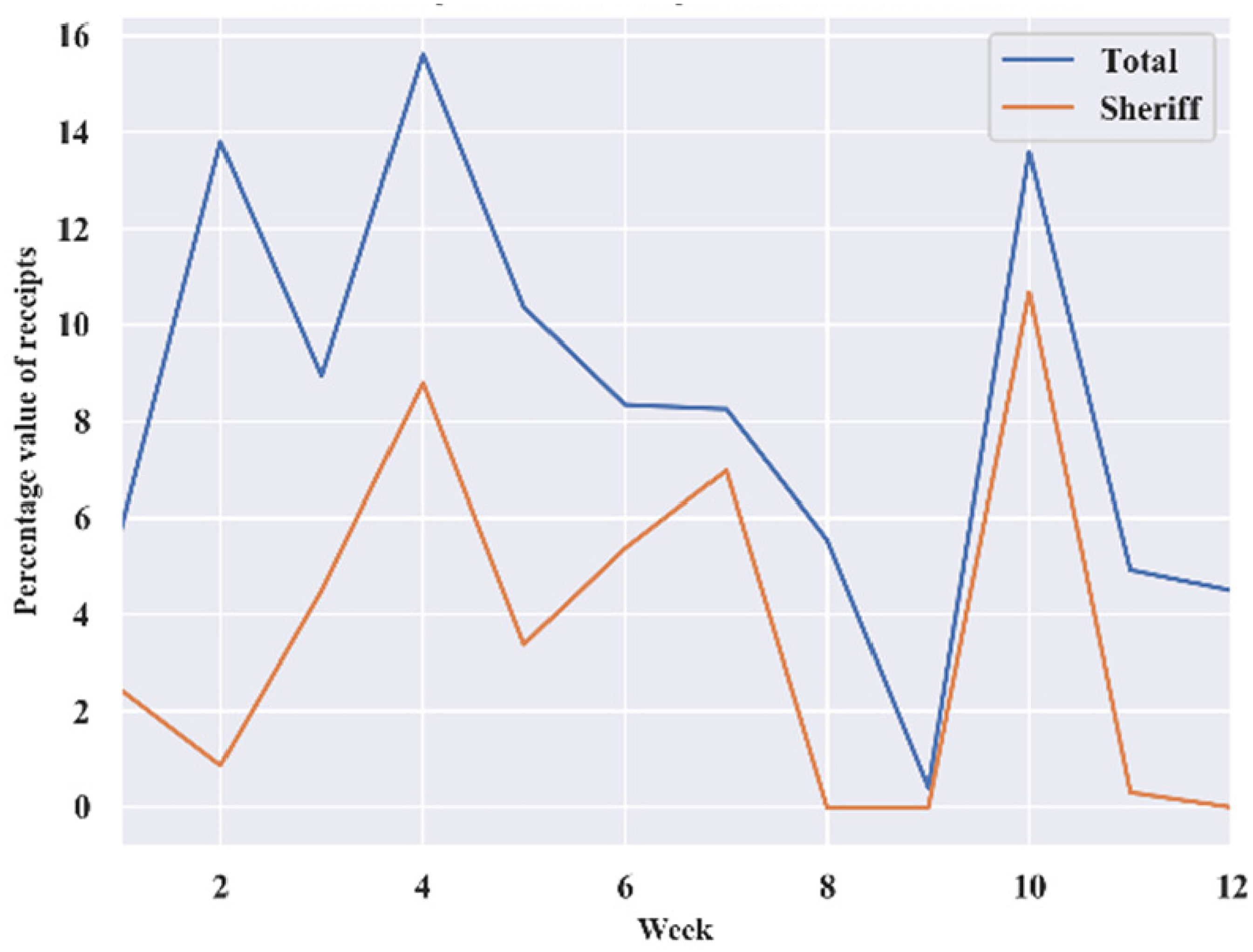

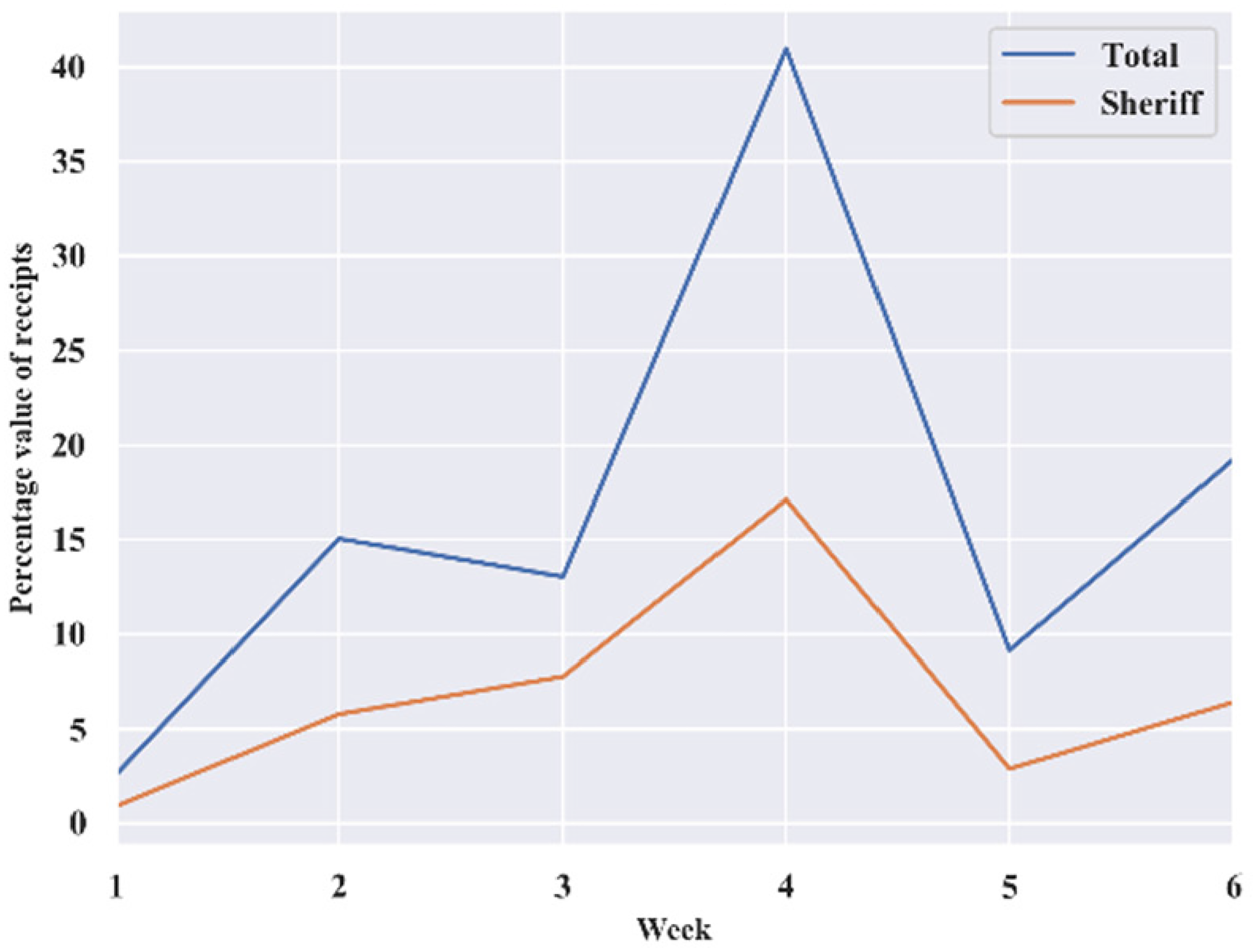

In short, in a pattern close to that which pertained at the English exchequer, most of the income that reached its Irish equivalent was received in October (Michaelmas) and May (Easter). A variation from the English model is observable, however, in that it was during the fourth week rather than the second that these sums arrived at the Irish exchequer. By extracting payments that refer to sheriffs in Michaelmas and Easter and plotting them against the income received in those terms, we can see that in Michaelmas (Figure 13) the sheriff accounted for half of the revenue in the fourth week and most of the receipts of the tenth week. In contrast, during Easter (Figure 14), the sheriff brought in less than half of the income of the tenth week. The peaks that appear in the plots (most clearly demonstrated in Figure 8) suggest that the crown expected proffers to the Irish Exchequer in Michaelmas and Easter, in accordance with practice in England. This snapshot indicates that the weeks in which the payments occurred differed from England. 41 More than one year of exchequer receipts would need to be analysed in order to determine whether this was a regular occurrence and it must be stressed again that what we offer here is a trial piece with no claims to ‘typicality’. The point is that this unexpected feature of Irish exchequer procedure becomes apparent only when close attention of the kind described here is paid to the information contained in the receipt roll. The potential of this approach to yield further insights and generate new research questions is obvious.

Weekly value of receipts returned Michaelmas.

Weekly value of receipts returned Easter.

Contextualization: Ireland in 1301–2

To capitalize on the capacity of data science to render accessible the hidden riches of the receipt rolls, it is necessary to understand the context is which these records were produced. With specific reference to the roll of 1301–2, it can be observed that not until the seventeenth century would English rule in Ireland again be as secure as it was in the early 1300s.

42

In general, throughout the thirteenth century the Irish lordship had posed few political problems for the English crown – no English king had felt the need to visit the lordship since 1210 – and had contributed useful sums to royal coffers.

43

At the turn of the fourteenth century most Gaelic lords who retained their lands were clients of settler magnates, while recently established colonial settlements in Derry and Clare seemed set to prosper and to extend English power still further.

44

The reach of the colonial government is suggested by the itinerary of the chief governor, John Sandford, archbishop of Dublin, in the summer of 1290. In the space of three months, he conducted judicial and other government business in twenty-six locations, ranging from Drogheda on the Irish Sea to Athenry in Galway, and Cork and Youghal on the south coast.

45

As Edward I, following his conquest of Wales between 1278 and 1282, entered into further conflict in Flanders and Scotland, Ireland provided significant levels of manpower, supplies and money to support his war efforts.

46

If the strength of English power in Ireland at the beginning of the fourteenth century should not be underestimated, neither should the challenges it faced. A case can be made that whereas the capacity of the crown to extract resources from its Irish lordship peaked in the decade either side of 1300, the high-point of English power in the island had been reached in the 1270s. As has been discussed above, financial corruption among officers of the crown was perceived to be a serious and growing problem, while faction among the settler nobility was entrenched and had led to extensive violence as recently as 1294. 47 Attacks on colonial settlements in different parts of the island by Gaelic lords, some of whom had added to their military capabilities by importing from western Scotland and settling on their lands the heavily armed fighting men known as galloglasses, became more common. 48 The issue roll for 1301–2, for instance, reveals that large sums needed to be spent ‘to suppress the rebellion’ of the Mac Murroughs and O’Byrnes, in the parts of Leinster south of Dublin. 49 Finally, while Edward I's wars provided important opportunities for settler lords to serve with the king and thus reinforce the strength of the links between the English kingdom and the Irish lordship, they also placed increasing strain on Irish revenues. 50 In 1297 royal demands for money for its military campaigns had come close to sparking rebellion in England, and in Ireland also concerns grew as resources needed to defend settlements from Irish attacks were diverted to Scotland. 51

The receipt roll of 1301–2, and other exchequer records for that year, therefore, provide insights into the workings of the institution responsible for Irish finances at a moment when English power in Ireland was at its height and when the machinery of government was working at full throttle to meet the needs of the crown. The issue roll for the same year reflects the degree to which the war effort was affecting Irish finances. In Michaelmas term total payments from the exchequer came to just under £769, of which over £300 were made to the masters and sailors of fourteen ships from the Cinque Ports and south-west England who had assembled their vessels in Dublin before proceeding to support the war in Scotland. 52 In Easter term money was paid to the bishop of Ossory for corn purchased from him ‘for the sustenance of the king's army’ in Gascony, while the sending of victuals to Scotland continued apace. 53 Finally, in Trinity term payments to those who had led armies from Ireland to Scotland in previous years, and payments to purchase corn and wine for the Scottish war, consumed over £3,000 of the c.£4,000 disbursed. 54 In total, of the roughly £7,100 paid out by the Irish exchequer in 1301–2, over half went to support the king's wars. 55 In early 1302 Edward I took the highly unusual step of instructing the chief governor, John Wogan, to supervise an inspection of exchequer records and provide an estimate of how much money would be available by March 1303 to support yet another Scottish expedition: there would be no quick end to the pressure on Irish finances. 56

Over £7,120 was paid out by the Irish exchequer in 1301–2, whereas only £6,160 was received. Before drawing conclusions from these figures about the more general state of Irish finances, it is important to bear in mind that the issue and receipt rolls do not provide a full picture of revenues for 1301–2 or any other exchequer year. Crucially, not all money due to, or spent by, the crown passed through the exchequer. Those sums that were, with royal permission, spent locally, were recorded not on the receipt or issue rolls but on the pipe rolls, which contained the audited accounts of crown officials and included the ‘allowances’ made to them for money they spent in this manner. 57 The Irish treasurer was not required to bring the pipe rolls to London for audit, and those that survived until 1921 were destroyed in the Four Courts blaze of that year. Short, calendared versions of the pipe rolls for the period 1229–1384 had been published before the originals were destroyed, and those for the exchequer year 1301–2, imperfect as they are, indicate that just as the crown spent more than the sum of £7,124 0s. 4½d. recorded on the issue roll, it also raised more than the £6,159 18s. 4d. itemised in the receipt roll. 58

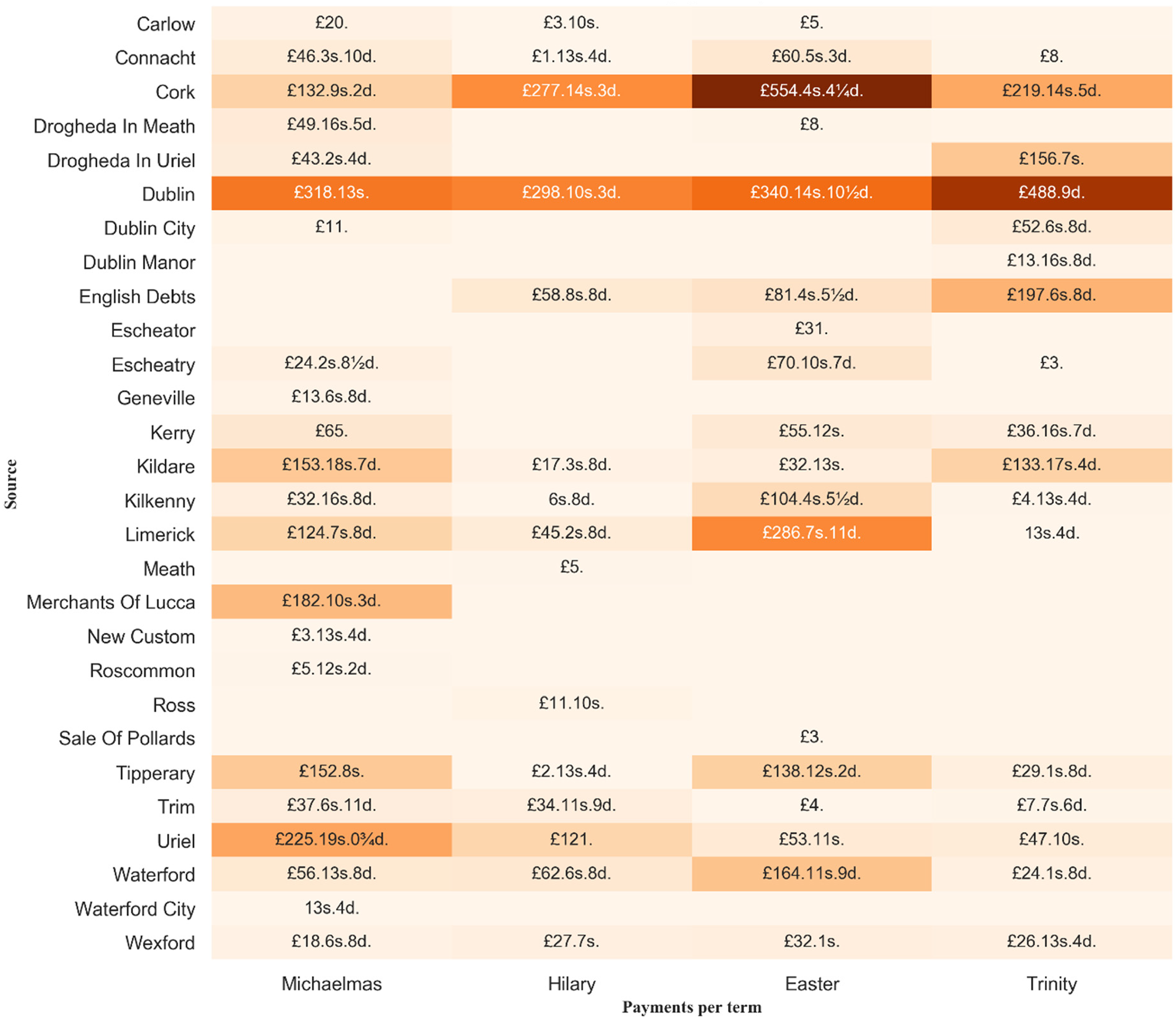

Only when the prevailing financial system is understood, and when the political realities operating at the particular moment it was produced are recognised, can the potential of applying data science techniques to the receipt roll for 1301–2, or any similar document, be fully exploited. If the roll does not offer us a comprehensive picture of Irish revenues for the year it covers, the data it contains can nevertheless be presented in ways that reveal much about the extent and intensity of English power in Ireland at the turn of the fourteenth century. Figure 15 lists in alphabetical order the marginal headings entered on the roll by the exchequer clerks to indicate the sources of the sums of money they recorded. For each source the sums are given for each of the four exchequer terms. Arranging the data contained in the receipt roll in this manner allows for identification and analysis of numerous patterns in Irish financial affairs in 1301–2. For example, it can be seen that all eleven Irish counties sent money to the exchequer in the course of the year, with eight doing so in each of the four exchequer terms. Kerry did not account in Hilary term, while Roscommon accounted only in Michaelmas term and Meath only in Hilary term. Turning from frequency of appearance at the exchequer to the amounts lodged there, the table reveals that Dublin and Cork provided the greatest sums throughout the year, while Roscommon's contribution was tiny. To extend an analysis such as this over the full set of surviving receipt rolls from the 1280s to the 1360s would add significantly to our understanding of the extent of English government in medieval Ireland.

Beyond Finance: The Receipt Roll as a Source for Irish History

Funding constraints did not allow for sustained application of data science to the type of information presented in Figure 15, but careful reading of the entries in the receipt roll prompted by this overview suggests the riches that such an approach is likely to reveal. 59 It is no surprise that sheriffs and other officers from places closest to Dublin, such as Trim, Kildare and Louth appeared most often at the exchequer throughout the year. More arresting is the fact that the sheriffs of Connacht, Henry Bermingham and John le Poer, accounted there on eight separate occasions in the same period, involving visits to Dublin in October, March, May and August. In total these men proffered over £115 - a small sum in the context of overall receipts of over £6,100, but not inconsequential, coming as it did to more than the combined amounts proffered by the city of Dublin and the king's manors in county Dublin. Kerry, which was even further from Dublin than the nearer parts of Connacht, was represented at the exchequer by its sheriff, Richard de Cantilupe, in October, June and August. Again, the sums proffered over the course of the year, amounting to close to £160, were modest but not insignificant, almost matching the combined total yielded by Carlow and Kilkenny. At the start of the fourteenth century, such information indicates, contact between distant regions and central government in Dublin was being maintained and revenue-raising mechanisms were operating effectively. When he accounted on these three occasions, over several days in each case, Cantilupe would have met his fellow-sheriffs, Hugh Purcel of Tipperary, Roger Roth of Uriel, Maurice Russell of Waterford and Albert de Kenlee of Kildare. The opportunity for networking and the sharing of information among the crown's representatives in the shires that accounting at the Dublin exchequer provided was important. It surely made the long journeys to the city bearing small sums of money worthwhile for those concerned and should be considered alongside the convening of parliament as a crucial mechanism by which the English identity of those colonists who represented the interests of the crown at local level was routinely reinforced. 60

The receipt roll was produced as part of an accounting regime, and the focus of the data investigation conducted on it here was on revenue totals and exchequer practice. But each receipt roll – and the same is true for each issue, pipe, and memoranda roll – contains disparate information that can be subjected to data analysis of the type outlined in this paper. Various aspects of the operation of the legal system, which provided substantial sums to the exchequer, are recorded on the receipt roll for 1301. 61 We read of courts meeting regularly on the royal manors around Dublin, namely Newcastle, Saggart and Crumlin. Four felons and three fugitives are identified by name and there are several more references to unnamed felons and fugitives. Outlawry is mentioned only once, with Philip le Bret of Cork paying 100s. to be freed from this sentence. 62 John Archer of Meath appears to have narrowly avoided outlaw status: having forfeited his possessions by fleeing from justice – his crime is not recorded – he later paid for their restoration. 63 There are also many instances of individuals paying to have possession of the forfeited chattels of those who had been deprived of them. Whether they hoped to benefit from the misfortune of their neighbours, or instead chose to act as temporary custodians of property they expected to see returned to their owners, is unclear. Escapes from incarceration are mentioned frequently, with five instances recorded in the account of the sheriff of Cork in July 1302. Two individuals from Cork also paid for release from prison and ransom in the same return. 64

The receipt roll contains the names of several hundred individuals. Women appear by name on thirty-two occasions on the roll, with seventeen different individuals being identified. Colonial women appear almost exclusively in relation to their marital status; either as wives, widows, or brides-to-be. In the former capacity they sometimes account jointly with their husbands, or sometimes account on behalf of their spouses. They also appear alongside their husbands in paying fines for trespasses or purchasing writs. In Dublin, Leticia, widow of Hugh Tyrel, paid £4 to have licence to marry. In Kilkenny and Kildare Nicholas de Avenil and John Wogan paid the large sums of 56 marks and £60 respectively for the marriages of Juliana de Clare and Margaret Staunton.

65

The topic of female Christian-name choice in medieval Ireland is under-researched, but this tiny sample suggests that a wider pool of names was in use. The most common female Christian name was Margaret, which was borne by three individuals, followed by Cristiana or Cristine which was borne by two. The other names listed were Agatha, Anastacia, Cecelia, Cristok, Denise, Eve, Gonorra, Isabella, Joan, Juliana, Juvana, Leticia, Matilda and Regenilda.

66

The reference to Roger of Newcastle (de Novo Castro) from Swords in Dublin, who is described as an Irishman, highlights the need for care in using Christian names and surnames as indicators of ethnic identity in Ireland by the fourteenth century.

67

More generally, the quite frequent references to Irish men and women deserve scrutiny. Often, they are mentioned in the context of being pledged by colonists, though at least as many instances of such pledging do not concern Irishmen. The only mention of betaghs – Irish agricultural labourers of unfree status – comes in relation to two individuals who bear the word as a surname.

68

Looking Ahead

The receipt rolls, and other exchequer documents, abound in evidence for various aspects of late medieval Irish life. The Beyond 2022 project offers the prospect of applying the digital humanities methodologies employed with reference to the receipt roll of 1301–2 to the wider corpus of this documentation. Many of these Latin documents, including the full range of receipt rolls, will be translated into English as the project advances and will be encoded into TEI/XML, giving them both structure and making them machine-readable. The Text Encoding Initiative (TEI) defines a schema for marking up a text document with the Extensible Markup Language (XML). 69 Elements or tags can encompass paragraphs, sentences or words to add structure and meaning, with additional attributes added to the elements to convey additional information. By encoding a text in an XML format, several related technologies can be deployed to support searching and transformation into other digital formats. It will be possible to update the data processing pipeline so that it can be employed in the Beyond 2022 project to use the TEI/XML as a canonical source from which to extract data into a CSV file. We can then undertake ‘distance reading’ with exploration and visualisation of a much larger range of years but coupled with the ability to focus in on ‘close reading’ by examining the details of individual proffers. At the same time, the availability on the Beyond 2022 website of digitized images of the original documents will allow for their close scrutiny and the possible identification of significant developments in exchequer practice.

The full potential of this approach to increase our understanding of Ireland's medieval past, and identify new topics of research will become apparent when the people and places named in the TEI/XML are linked to the Beyond 2022 knowledge graph, which represents thousands of historical entities using Semantic Web or Linked Data technologies. 70 Using a rich ontology, the knowledge graph models the various aspects of religious and secular institutions in medieval Ireland and England, in addition to various geographical entities, such as towns, lordships and shires. Underpinned by the Resource Description Framework (RDF), the knowledge graph models entities, and their interconnectedness, through a subject – predicate – object relationship. 71 For example, ‘Hugh Purcel’ (subject) – ‘is sheriff of’ (predicate) – ‘Tipperary’ (object). It is therefore possible not only to query the knowledge graph for a list of other offices that Hugh Purcel might have held, but also a list of other individuals who held the Tipperary shrievalty. Each subject, predicate and object in the knowledge graph is assigned a unique Uniform Resource Identifier (URI). For example, <https://kb.beyond2022.ie/person/hugh_purcel > might be used to identify Hugh Purcel. In turn, a TEI/XML element might use the URI in a ‘ref’ attribute to indicate that this entity is represented in the knowledge graph. Ultimately, this will improve knowledge discovery and retrieval, allowing the receipt roll, or a fragment of XML, to be retrieved if a researcher searches, for example, Purcel or sheriffs or sheriffs of Tipperary. In turn, entities in the knowledge graph can be linked to other linked data datasets. For example, Tipperary is identified by https://www.wikidata.org/wiki/Q680220 in Wikidata, the large knowledge graph used by Wikipedia. The identification and linking of entities within the receipt rolls creates a vast network of interconnected nodes which can be queried by network analysis tools and algorithms.

Network analysis allows us to examine the network in terms of nodes (entities) and edges (relationship between the nodes), looking for patterns in these relationships. As Ahnert et al. note:

The use of computational network analysis can lead to the creation of new knowledge, and to the corroboration of theories. It makes it possible, with relative ease and speed, to measure the relationships between many entities in multiple ways, allowing a rich, multidimensional reading of complex systems never possible before.

72

This means in the context of the receipt rolls that we can go beyond quantitative analysis based around counting sums received during various financial terms, to see what other information the rolls can tell us about not only the machinery of government that created it, but the society and economy itemized within its membranes. Since network analysis can often break through hierarchical power structures, can such a study break through hierarchies inherent in the system that produced the rolls? 73 Can patterns be uncovered that show relationships between the individuals and communities mentioned in the rolls, rather than simply seeing relationships in terms of periphery and centre? If the knowledge graph were extended to cover, for example, aspects of trade or law, could this be directed towards the identification of patterns in mercantile activity or the use of writs? The application of data science to a single exchequer document, the receipt roll of 1301–2, combined with appropriate historical contextualization of the source, illustrates what can be achieved.

Brendan Smith

Mike Jones

University of Bristol

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.