Abstract

Digitalization is reshaping global competition, yet cross-country differences in informational globalization create challenges for multinational enterprises (MNEs), especially in information technology (IT)-intensive sectors. This study analyzes the impact of information distance, which reflects disparities in national informational environments, on the digital transformation of MNEs’ subsidiaries. By applying a real options perspective, we highlight intra-firm factors (i.e. financial liquidity and operational flexibility) that play critical roles in mitigating pressures arising from information distance. Using a sample of 136 subsidiaries of MNEs in IT-intensive sectors and employing computer-aided text analysis techniques, this study finds that information distance between home and host countries hinders MNE subsidiaries’ digital transformation and negatively affects their financial performance. However, these adverse effects are mitigated by the subsidiary’s financial liquidity and operational flexibility. This research contributes to the cross-country distance literature and offers new insights into digitalization in international business.

Keywords

1. Introduction

The past decade has witnessed numerous new phenomena affecting global business practices, among which digital globalization is rapidly changing and reshaping multinational enterprises (MNEs) (Luo, 2021; Verbeke and Hutzschenreuter, 2021). The emergence of digital platforms, new developments in information and communications technologies, and the rapid evolution of technological infrastructure have shown that the world has entered a digital age (Felin and Holweg, 2024; Ren et al., 2023). Concurrently, increasing global disruptions and new uncertainties have also accelerated the pace of technological development among countries, especially their digitalization (Choudhury et al., 2019; Luo, 2021). Many countries have started to build their technological infrastructure, encouraging their firms to engage in digital transformation and leverage machine learning to compete in global markets. Driven by the shift in global competition, management and international business researchers have devoted considerable effort to investigating governments’ regulations on new technologies (Meyer et al., 2023), risks underlying MNEs’ digitalization (Ren et al., 2023), and how to link digitalization with sustainable social and economic development (George and Schillebeeckx, 2022; Yi et al., 2023).

However, it remains unclear whether and how MNEs and their subsidiaries can effectively navigate the cross-country differences in informational globalization (Gygli et al., 2019) to advance their digital transformation and improve performance. Researchers often use the term “distance” to describe cross-national differences that could affect MNEs’ strategies and performance in the host country (Li et al., 2020; Messner, 2023). The cultural, institutional, geographical, and psychic distances have been widely discussed. However, changes in these traditional types of distance are often negligible or slow over time (Tung and Verbeke, 2010). Geographical distance is constant, and cultural or institutional changes are slow and incremental (Jackson and Deeg, 2008; Tung and Verbeke, 2010), indicating that MNEs are likely to prepare in advance, learn from or cooperate with local market firms, or work out efficient strategies to fit the local environment.

Unlike these distances, where changes vary less, information distance can create dynamic challenges for MNEs as markets evolve over time and available information changes (Lindner and Puck, 2024). Information distance refers to differences in informational efficiency across countries (Lindner and Puck, 2024) and, in the context of international business, captures the gaps in informational globalization between home and host countries (Gygli et al., 2019; Potrafke, 2015). It reflects information asymmetries between countries, which can translate into risks for MNEs and lead to different firm behaviors (Lindner and Puck, 2024). Given the fast-changing technological frontier and countries’ varying national goals, information distance may impact firms more than other types of distance, highlighting a need for further critical discussion and empirical testing of this concept (Lindner and Puck, 2024).

However, not all MNEs’ global value chain activities will be affected by information distance. The heterogeneity of firms results in different exposures to digital risk (Luo, 2022), which subsequently affects their susceptibility to information distance between countries. Forbes (2017) lists 13 main challenges for the digital transformation of firms, of which “getting it right” is highlighted as the top challenge, as not all firms have the expertise to assemble digital technologies effectively. Nguyen (2022) suggests that firms in the banking industry have been slow to adopt cloud computing due to a lack of equipment and high transformation costs. These insights show that firms with higher information and knowledge intensity will engage more in digitalization (Luo, 2022; Monaghan et al., 2020; Nambisan and Luo, 2022), and therefore, these firms are susceptible to the impact of information distance. The existing literature lacks discussion on the role of information distance in MNEs’ digital transformation and performance (Santos and Williamson, 2024). It is critical to address this research gap and explore the diverse intra-firm features that may affect the ability of MNEs and their subsidiaries to deal with information distance. Consequently, this study raises the following research question:

RQ1. How does cross-country information distance affect MNE subsidiaries’ digital transformation and financial performance?

Building on real options theory (Adner and Levinthal, 2004; McGrath, 1999), this study argues that in the presence of information distance (and related uncertainty), MNEs will face different options for making decisions for their digitalization and internationalization. This study focuses on a sample of MNEs from information technology (IT)-intensive sectors (i.e. industries that heavily rely on information technology for operations and value creation) and collects news reports from Dow Jones News Service, using computer-aided text analysis (CATA) techniques to capture firms’ digital transformation at the subsidiary level. The contributions of this study are twofold. First, unlike prior studies that often include all types of MNEs to examine the impact of distance, this study focuses on MNEs from IT-intensive sectors, as they are more involved in the quest for digitalization and susceptible to digital risks in internationalization (de la Boutetière et al., 2018; Luo, 2022; Monaghan et al., 2020). By analyzing the impact of information distance between countries on MNEs and their subsidiaries, this study advances our understanding of firm digitalization in an international business context. It offers new insights into the research of cross-country differences and MNE subsidiaries’ digital transformation.

Second, incorporating insights from real options theory, this study theorizes important intra-firm features (i.e. liquidity and flexibility) that can affect the value of investment options for MNEs and their subsidiaries facing information distance. By examining the dynamics of firms’ involvement in the face of a new form of global uncertainty, this study enriches the real options literature in an international business context (Trigeorgis and Miller, 2025). Our findings also contribute to the digitalization research in management and international business. Important practical and policy implications are discussed.

2. Literature review and hypothesis development

2.1. Real options theory and MNEs’ decision-making

Real options theory has gained growing attention in management and international business research and is often described as an important lens to study firm decisions under conditions of uncertainty (McGrath, 1999; Trigeorgis and Miller, 2025; Verdu et al., 2012). The core concept of a real option is to invest in flexibility to make future business decisions, considering the potential variability in expected losses and returns under conditions of uncertainty (Trigeorgis and Reuer, 2017). In an international context, firms’ internationalization decisions are a complex process largely impacted by foreign market uncertainties regarding the different institutional, social, and monetary systems (Chi et al., 2019; Sahaym et al., 2012). Building on this, researchers increasingly emphasize the value of real options for studying MNEs’ decision-making across diverse environments, as it accounts for uncertainties arising from changing market conditions and cross-country effects (Chi et al., 2019). A recent study by Trigeorgis and Miller (2025) further emphasizes that the real options perspective “can complement other MNE theories” (p. 4), offering a suitable framework for understanding the portfolio of international decisions and performance of MNEs.

In fast-changing environments, MNEs will face more pressure to modify their business models and create new products or processes (Verdu et al., 2012), as changes are necessary when operating in high levels of uncertainty. When facing cross-country differences, MNEs can gather new information and have more options to make investments based on assessments of the demand trend in a foreign market (Chi et al., 2019). Multinationality is a key consideration in the exploration or acquisition of the real option life-cycle stage (Trigeorgis and Reuer, 2017), when firms acquire or create options through actions such as foreign direct investment (FDI) in subsidiaries abroad. In the following stages of development and exploitation of real options, organizational realities such as information structures and strategies, for example, market entry (Belderbos et al., 2020) or switching, play key roles in managing and exercising real options toward strategic change (e.g. digital transformation in subsidiaries), continuation/extension, or discontinuation (Trigeorgis and Reuer, 2017). Real options awareness and exercising of real options toward their exploitation can also lead to better value and performance (Ioulianou et al., 2021).

2.2. Information distance across countries and digitalization of MNEs

Despite widespread research on the types of cross-country distance and the related challenges and opportunities for MNEs (Berry et al., 2010; Li et al., 2020; Messner, 2023; Wu & Fan, 2023), less is known about whether uncertainties created by countries’ different paces in informational globalization (i.e. information distance) affect MNEs’ performance, especially those in industries that rely heavily on digital infrastructures for operating overseas. In an international business context, information distance comprises the distance across two dimensions of informational globalization, according to Gygli et al. (2019). First, de facto informational globalization captures the actual cross-border flows of ideas, knowledge, and technology, including indicators such as foreign patent applications and high-technology exports (Gygli et al., 2019; Haelg, 2022). Second, de jure informational globalization reflects a country’s capacity to share information internationally, assessed through Internet access, television availability, and press freedom, indicating the structural conditions that enable information exchange (Gygli et al., 2019). Our conceptualization of information distance is distinct from a related conceptualization by Lindner and Puck (2024), who stress the role of institutional conditions and socio-political risks, operationalizing their construct using permutation entropy of financial returns in lead indices.

In IT-intensive sectors, it is important to consider informational globalization along with digitalization, which, as a symbol of the fourth industrial revolution, is increasingly changing how firms are organized and how they operate internationally (Luo and Zahra, 2023; Meyer et al., 2023; Teece, 2025). Digitalization involves utilizing information including big data and new information-processing techniques and algorithms to increase production efficiency and economic welfare (Autio et al., 2021; Bhandari et al., 2023). Research indicates that country-level informational globalization is becoming increasingly relevant and influential in today’s interconnected digital economy (Ramzan et al., 2023). Due to the frequent changes in digital technologies, research has also started to examine global digital interconnectivity and interdependence risk due to the linkages between suppliers, distributors, customers, MNEs, and their many stakeholders in different countries (Luo, 2022).

The pace of change in informational globalization across countries can impact the digital transformation in MNEs and their subsidiaries (Autio et al., 2021; Grimpe et al., 2023; Lee et al., 2023). Considering the disparities in digital literacy, technological development, and other aspects of informational globalization between countries (Ciulli and Kolk, 2023; Han and Lee, 2022; Lee and Lee, 2021), new challenges and opportunities may arise due to the home–host country information distance. Significantly, the international activities of MNEs from IT-intensive sectors, which span the areas of data processing and cybersecurity, are more sensitive to information distance compared with traditional MNEs (Meyer et al., 2023).

Luo (2022) suggests that MNEs and industries with higher data intensity are more affected by digital risk across countries and governments regulating digitalization, with implications for their subsidiaries’ digital transformation and performance. The common features of MNEs from “digitally savvy” IT-intensive sectors include their high degree of information and knowledge intensity, identifiable online presence, and variations in digital transformation (Monaghan et al., 2020; Nambisan and Luo, 2022). According to real options theory, unpredicted uncertainties in the global informational context can affect the potential gains from MNEs’ international activities, reshaping their strategic orientation in digital transformation and leading to greater variance in financial performance. As the evolution of informational environments in different countries is largely virtual (Luo, 2022), it is critical to examine the linkages between country-level information distance and its impact on MNEs’ digitalization and performance.

2.3. The impact of information distance on MNEs’ digital transformation and performance

Greater information distance across countries can hinder MNE subsidiaries’ ability to sustain digital transformation and achieve stronger financial performance. Existing research suggests that high levels of information asymmetry in foreign markets exacerbate MNEs’ risk exposure (Lindner and Puck, 2024), creating a negative sign for MNE transformation due to increased difficulties in understanding the “rule of the game” in the host country. From a real options perspective, a greater information distance also implies increased environmental uncertainty and downside risk (Trigeorgis and Miller, 2025). MNEs are likely to reduce their commitment to the host country and focus on cost-cutting strategies. Also, with a significant gap in the flow of ideas, knowledge, and data between home and host countries, MNE subsidiaries are less likely to implement transformation initiatives effectively and successfully (Murphree et al., 2022).

Differences in key aspects of information sharing, such as digital media access and press freedom, can present formidable barriers to subsidiaries’ initiative and their digital transformation (Figueira et al., 2023; Li et al., 2021). Conversely, a smaller information distance has advantages for the digital transformation of MNE subsidiaries. It reduces uncertainty for both headquarters and subsidiaries and stimulates knowledge sharing so subsidiaries can become vehicles of Industry 4.0 (Jankowska et al., 2021). For example, Ingršt and Zámborský (2021) have shown that knowledge flows between European subsidiaries of Australian and New Zealand multinationals are negatively affected by aspects of cross-border distance linked to the quality of communication channels for organizational information exchange (Gaur et al., 2019), and that this negatively impacts subsidiaries’ innovation performance (e.g. their digital transformation). Taken together, we predict:

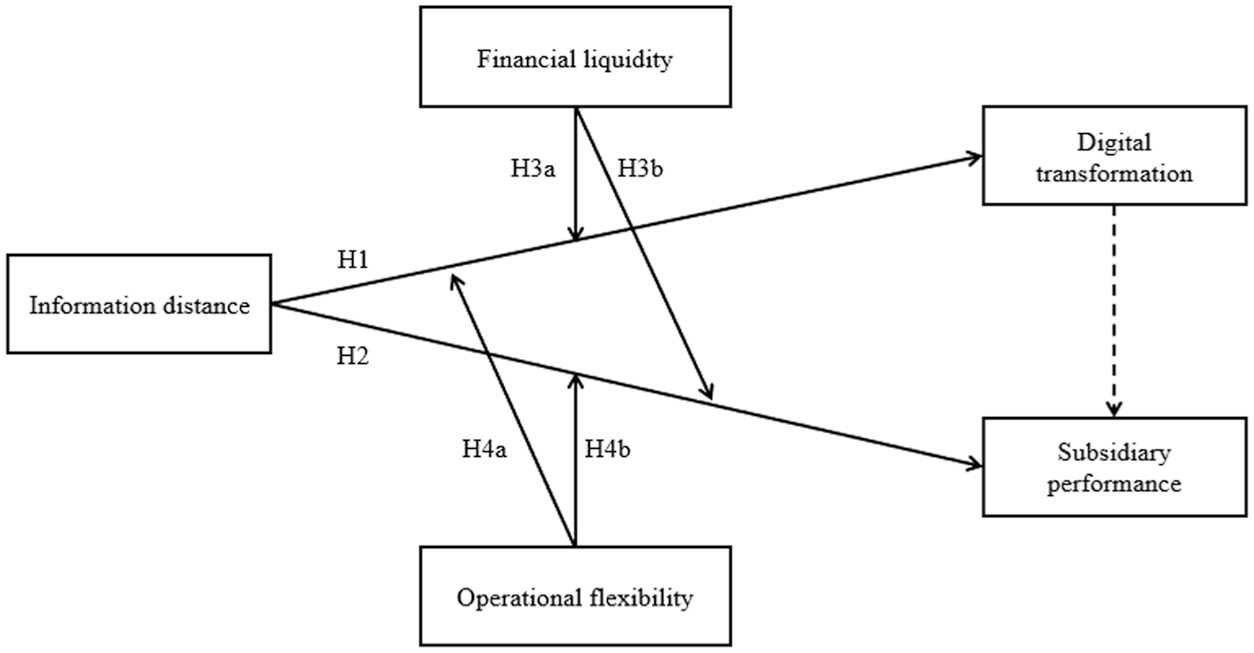

H1. Home–host country information distance negatively affects the digital transformation of MNE subsidiaries.

The growing complexity of internationalization due to entering substantially different informational environments will lead to MNEs facing additional costs to maintain their operation and legitimacy in the host country. If firms choose a proactive adaptation option (Verdu et al., 2012), they need to adapt to multiple technological standards different from the home country’s practices (Kim et al., 2016), thereby directing their attention to modifying their business models to fit the local technological and informational environment. Although real options theory predicts that firms can explore alternative options under uncertainty (Nanda and Rhodes-Kropf, 2017; Wang and Hwang, 2007), there is a trade-off between reducing market adaptation costs and maximizing option values from engaging in innovation activities, especially in digitalization. Fitting the different standards and meeting the local market demand for technological products require MNEs to invest in substantial switching costs (Kim et al., 2016), resulting in these firms’ deteriorating profit margins in the host-country subsidiaries.

The real options view highlights that firms hedge or diversify risks by expanding into other potential business areas or finding alternative markets (Sahaym et al., 2012). In line with this logic, MNEs will either invest in non-digital activities that are less likely to violate changing digital standards or reduce their commitments to the host country and enter other markets with lower information distance. As a result, these firms are prone to slowing down the pace of digitalization and risk performance damage in the host country. Under conditions of unpredictable uncertainty, another option is risk and uncertainty management (Clarke and Liesch, 2017; Zámborský et al., 2022), which requires MNEs to wait for new solutions to emerge for overcoming information distance and digital risk. While the waiting option allows companies to better manage digitization risks in international business (Luo, 2022), it does so in the form of time-consuming and costly modifications (Clarke and Liesch, 2017). However, maintaining the competitive advantage of firms in IT-intensive industries requires technological change or innovation (Sahaym et al., 2012), and such options will be detrimental to MNE subsidiaries’ financial performance. We propose:

H2. Home–host country information distance negatively affects the financial performance of MNE subsidiaries.

2.4. The moderating effects of intra-firm features

To increase strategic options under information distance, real options theory also highlights the importance of increasing strategic and operational flexibility (Verdu et al., 2012). Intra-firm features, especially the firms’ financial liquidity and operational flexibility, affect MNEs and their subsidiaries’ vulnerability to information distance.

2.4.1. Financial liquidity

Financial liquidity is a critical factor affecting the relationship between information distance and firms’ digitalization, as implementing innovation projects (or risk-taking activities) abroad requires firms to have abundant resources and financial slack (Yang et al., 2019). Previous studies show that financing constraints will deter firms’ R&D investments and innovation performance (Howell, 2016; Pellegrino and Savona, 2017), as financial resources are critical to supporting trial and error and assisting firms in modifying business models (including digital transformation) to adapt to information distance. In contrast, greater access to financial liquidity enables firms to ease market adaptation pressures (Howell, 2016), such as paying tax or the high service fees related to their digital transformation efforts or the additional costs for meeting host-country digital standards. With high financial liquidity, MNEs can better cover unexpected expenses or production changes during digital transformation. We propose:

H3a. Financial liquidity positively moderates the relationship between home–host country information distance and MNE subsidiaries’ digital transformation.

However, although financial liquidity is beneficial for firms to digitize under conditions of uncertainty underpinning information distance, it may negatively moderate the relationship between information distance and MNE subsidiary financial performance. There are two key reasons for this. First, research shows that holding more cash may be viewed as poor investor protection (Brockman and Chung, 2003; Yang et al., 2019). Firms with higher financial liquidity will face greater opportunity costs by forgoing some potentially profitable projects. Hence, investors will expect firms to perform poorly in the future, leading to negative market reactions (Yang et al., 2019). With greater information distance, this negative investor reaction will hinder the market adaptation of MNEs, thus negatively affecting their subsidiaries’ performance. Second, financial liquidity may lead to higher agency costs for MNEs under conditions of high information distance, as excess cash reserves enable managers to expand the firm for their own benefit rather than pursue risky or uncertain profitable projects (Yang et al., 2019) related to digital transformation. Hence, we propose:

H3b. Financial liquidity negatively moderates the relationship between home–host country information distance and MNE subsidiaries’ financial performance.

2.4.2. Operational flexibility

Another critical factor is operational flexibility, a firm’s ability to respond profitably to environmental fluctuations by shifting factors of production within a multinational network of subsidiaries (Tang and Tikoo, 1999). It can assist MNEs in coping with information distance to improve digitalization outcomes. Studies find that MNEs maintaining subsidiaries’ flexibility in operating in foreign markets tend to perform better in value creation and innovations (Beugelsdijk and Jindra, 2018; Ingršt and Zámborský, 2021), including those underpinning digital transformation. For instance, MNE subsidiaries with more operational flexibility can better embed in host-country networks (Ambos et al., 2011; Fisch and Zschoche, 2012), helping them learn about digital differences and making their digital transformation more legitimate (Jankowska et al., 2021). Flexibility also enables knowledge transfer across the subunits of firms (Keupp et al., 2011), which allows firms to utilize available resources to cope with country-level information distances that hinder their digitalization. In another aspect, high flexibility allows MNE subsidiaries to pursue strategically valuable real options and act independently instead of following the home country’s technological requirements (Beugelsdijk and Jindra, 2018), particularly under conditions of high information distance. Flexibility also provides switch/growth options for MNEs, which are critical in firms’ digital transformation under information distance. Hence, we propose:

H4a. Operational flexibility positively moderates the relationship between home–host country information distance and MNE subsidiaries’ digital transformation.

Following real options theory, flexibility provides switch or abandon options for firms (McGrath, 1999), enabling them to be more flexible in cutting profit-losing projects when operating in the host country with a large information distance. First, local responsiveness enables MNEs to adapt to local informational conditions, thereby achieving better subsidiary financial performance. When firms can remain responsive to the changing needs of host countries, their resource integration configurations are likely to become more efficient (Geleilate et al., 2020; Keupp et al., 2011). Second, research shows that flexibility is needed when MNEs operate in an environment with a greater level of uncertainty and a variety of challenges and opportunities (Beugelsdijk and Jindra, 2018). Operational flexibility implies internal economies of scale (Beugelsdijk and Jindra, 2018), which can help MNEs and their subsidiaries cope with market pressures and uncertainty under the conditions of information distance. As a result, the negative impact of information distance on subsidiary performance can be reduced. Hence, we predict:

H4b. Operational flexibility positively moderates the relationship between home–host country information distance and MNE subsidiaries’ financial performance.

The research framework of this study is depicted in Figure 1.

Research framework.

3. Data and method

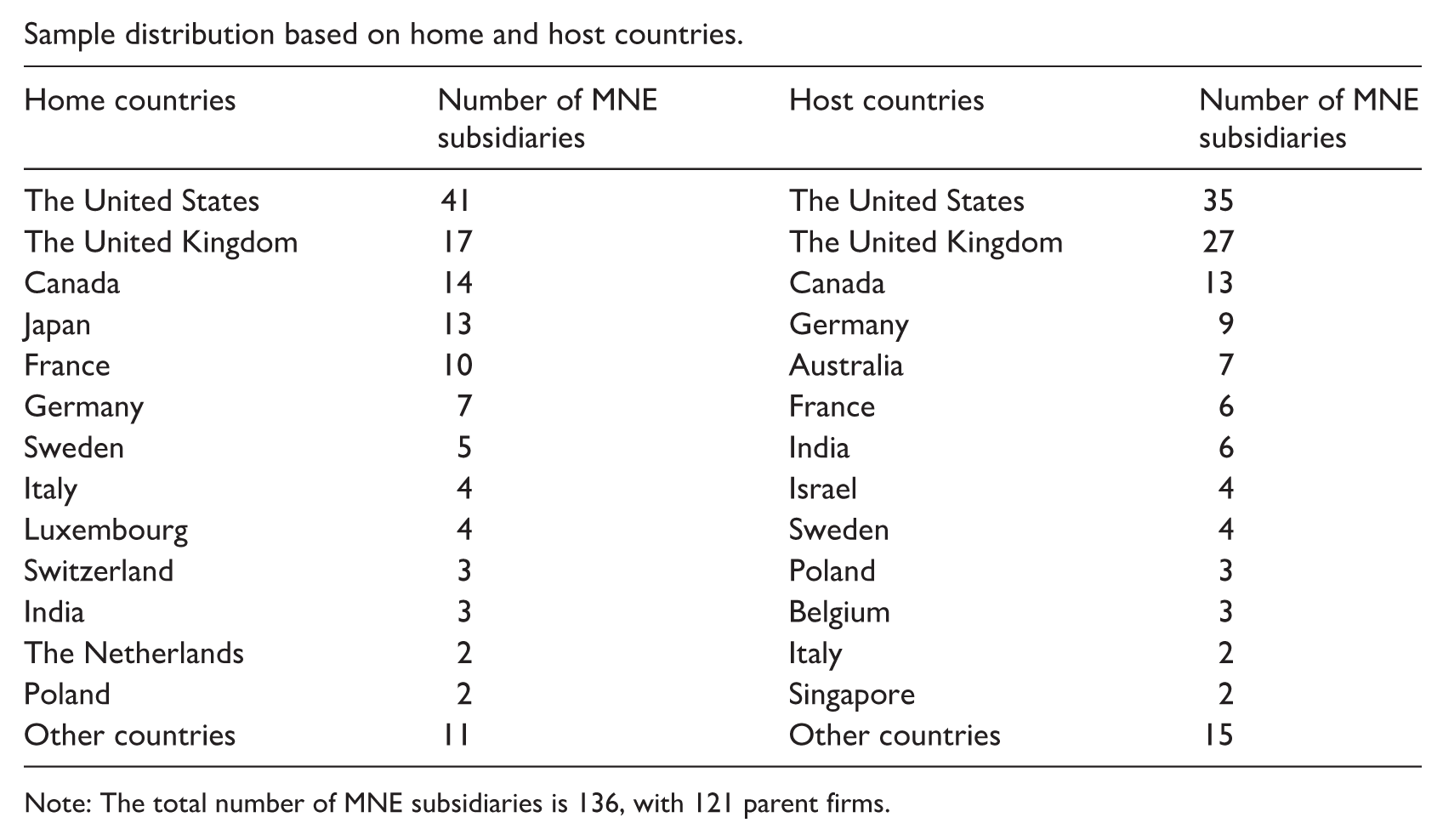

To examine the influence of information distance on subsidiaries of MNEs, this study relies on the North American Industry Classification System (NAICS) industry classifications rather than SIC codes, as the NAICS system can better reflect industry structure, especially the IT-intensive sectors that heavily rely on using information as their inputs (Arora and Forman, 2007; Beverungen et al., 2021; Delgado and Mills, 2020). Following existing studies, we selected firms in IT-intensive sectors, including those in software publishing, computer programming, data processing, and cybersecurity areas (Arora and Forman, 2007; Nagle, 2019). The selected NAICS 2017 codes are 511210, 518210, 541511, 541512, and 541519. We focus on subsidiaries of MNEs—entities based in host countries that differ from the MNEs’ home countries, where their headquarters are located. Considering state-owned enterprises (SOEs) are subject to policy controls that can significantly influence their innovation development and international activities (Genin et al., 2021; Zhou et al., 2017), this study only considers MNEs whose parent firms are not SOEs. After excluding observations with missing data on the main variables, our final sample consists of 136 subsidiaries of MNEs originating from 24 countries and operating in 26 countries (see Appendix 1). Of these, 38 subsidiaries were formed after 2000, while 98 were established before 2000. A small proportion (12 out of 136) of the parent companies of these firms are family-owned.

The firm-level data were collected from the Osiris database offered by Bureau van Dijk, which covers detailed information on firms globally. The research time frame spans from 2003 to 2019, selected primarily based on data availability. The 2019 cutoff year ensured that the analysis remained unaffected by the disruptions caused by the global health crisis in 2020, thus providing a clearer view of firm performance and international activities prior to the pandemic. Country-level data and other explanatory variables were collected for the year preceding the outcome variables (2002–2018). This approach helped address concerns of reverse causality, ensuring that the explanatory factors reflect the conditions that could influence firm digitalization and performance outcomes.

Research shows that using news data enables extensive analysis of firm-level outcomes based on all relevant and large-quantity information (Bajgrowicz et al., 2016; Bernile et al., 2016). This study further used the Factiva database to retrieve corporate news stories. Factiva, owned by Dow Jones, is a news database that provides both licensed and free sources, which enables quantification of aggregated contents to further analyze a specific business topic (Bajgrowicz et al., 2016). For this study, we collected news articles from the Dow Jones News Service in Factiva for each subsidiary, based on their name and for each year in the sample period. A total of 20,573 news articles, comprising over 9 million words, were gathered for text analysis. In addition to the subsidiary- and firm-level data, this study also collected country-level data from the KOF Swiss Economic Institute, the World Bank, the Heritage Research database, the CEPII database, and Hofstede’s cultural data. The next section presents the detailed operations of each variable and the empirical approach used.

3.1. Methods

This study uses the GLS (generalized least squares) regression approach, as it is often used for examining time series panel data. Based on the results of the Hausman test, the random-effects GLS model is more efficient than the fixed-effects models (Jiang et al., 2010; Madsen and Rodgers, 2015). In testing the proposed hypotheses, the following equations are employed:

When moderators are included, the following equations are employed:

Equations (1) and (3) focus on testing the impact of explanatory variables on digital transformation, while equations (2) and (4) examine that impact on the subsidiaries’ financial performance.

3.2. Dependent variables

The two dependent variables (DVs) in this study include the extent of digital transformation of MNE subsidiaries and the financial performance of subsidiaries, which are measured using data collected from Dow Jones Newswires and Osiris. Digital transformation is captured through a CATA method that relies on the news reports collected from Dow Jones Newswires (N = 20,573) and uses the Linguistic Inquiry and Word Count (LIWC) software. The CATA method enables firm activities to be measured in a standardized manner (Haselhuhn et al., 2022; McKenny et al., 2018). It offers greater generalizability and can capture firms’ digitalization efforts, which are often not fully released in archival data. Researchers have developed novel dictionaries that can help better analyze the texts collected and construct variables related to firm digitalization. This study used the Digital Orientation Dimensions Dictionary offered by Kindermann et al. (2021), which enables the firm’s digital technology scope to be analyzed using keywords such as Internet-of-Things, blockchain, and cloud-based. Unlike traditional measurements such as using R&D expenditures or patent counts to capture firms’ technological activities, the text analysis approach allows for the capture of various dimensions of firms’ digital activities using qualitative evidence (Escoz Barragan and Becker, 2025).

This approach has gained increasing popularity as a measure of firm digital transformation (e.g. Escoz Barragan and Becker, 2025; Zhu and Dong, 2025) owing to its ability to assess how MNEs align their structures, processes, and strategies with the integration and utilization of digital technologies, offering a more holistic view of transformation that goes beyond just the technological perspective. In this study, the score of the scope of digital technologies generated by CATA reflects the extent to which firms can create or incorporate new digital tools into their operations (Kindermann et al., 2021), which is used to proxy the firms’ digital transformation.

Subsidiary performance is measured using the gross profit divided by operating revenue (i.e. gross profit margin), which reflects the subsidiary’s earnings or ability to generate profits and its bargaining power in the host country (Moatti et al., 2015; Tang and Tikoo, 1999). The DVs are captured in year t, and all other explanatory and control variables are measured in year t − 1 to establish causal relationships.

3.3. Independent variable

The independent variable, information distance, is measured using the informational globalization indexes collected from KOF, which is a relatively new and comprehensive dataset that calculates a range of country-level globalization indexes including trade, financial, interpersonal, informational, cultural, and political aspects (1970–2021) (Dreher, 2006; Potrafke, 2015). The informational aspect covers six subindices, including a country’s Internet bandwidth, international patents, and high-technology exports—the de facto measures; and television access, Internet access, and press freedom—the de jure measures (Dreher, 2006). The six subindices allow us to consider a country’s informational environment and capacity for digital globalization. To construct the independent variable, the indices for each country are condensed into one dimension using factor analysis, as the de facto and de jure measures are highly correlated. That is, a comprehensive dimension is created for the home-country list (Cronbach’s alpha = 0.871) and the host-country list (Cronbach’s alpha = 0.894). With the two informational dimensions (one based on home countries and the other based on host countries), information distance is calculated based on the Euclidean distance approach as follows:

3.4. Moderators

Following previous studies, financial liquidity is measured using the current assets stocks divided by current liabilities (Chang and Singh, 1999; DeSarbo et al., 2009). The prominent source of control power by the headquarters of MNEs is reflected by equity ownership (Ambos et al., 2011). When an MNE subsidiary is fully controlled by its headquarters, its operational flexibility in foreign countries may be restricted (Ambos et al., 2011; Geleilate et al., 2020). Hence, this study created a dummy variable to capture a subsidiary’s operational flexibility, which equals 1 if it is not fully controlled by the headquarters (not 100% ownership stake) and 0 otherwise.

3.5. Control variables

We included a set of control variables at the subsidiary, headquarters, and country levels, which may influence the main effects. At the subsidiary level, firm age is controlled, as younger firms may undertake riskier innovation activities (Coad et al., 2016), resulting in them reacting differently to information distance. Firm age is measured by taking the natural logarithm of the total number of years since the firm was established. Firm size, measured by the total assets of firms in each year (natural logarithm-transformed), is also related to scale economy effects and affects firm performance (Randøy and Goel, 2003). Intangible resources are crucial for competitive advantage and innovation (Randøy and Goel, 2003); hence, we controlled for the intangible asset ratio by dividing intangible assets by total assets. The gearing ratio, measured using total debts divided by total assets (Randøy and Goel, 2003), reflects the firm’s financial burden and is included as a control variable.

Given that the strategic orientation of subsidiaries is often shaped by their headquarters (Dahms et al., 2023; Scott-Kennel and Giroud, 2015), we controlled the headquarters’ scope of internationalization and intangibility, as the global presence and strategic focus on technological expertise can influence the subsidiary’s digitalization decisions. We included a dummy variable, scope of internationalization (equals 1 if the firm has multiple target countries, and 0 otherwise), to capture whether the MNEs have multiple foreign locations. We controlled the intangible asset ratio at the headquarters level to account for its impact on subsidiaries’ digitalization. We also controlled for news intensity using total word count.

At the country level, previous studies show that the institutional environment of an MNE’s home country impacts its ability to deal with difficult conditions when operating in a foreign country (Cuervo-Cazurra and Genc, 2008). Voice and accountability and political stability are controlled, as these are important institutional dimensions that can reflect the home governments’ influence. Geographic distance between countries can impact the performance of MNEs; hence, it is controlled using the distance (per 1000 km) between the capital cities of the home and host countries. Considering that using shared language in a foreign country enables firms to better understand the specific challenges, such as information distance, a dummy variable was created that equals 1 if the two countries use a common language.

In addition, the host country’s characteristics, such as macroeconomic uncertainty, IP (intellectual property) protection, and trade openness, are controlled. First, in countries that lack strong protections for IP rights, firms face potential appropriation risk and may lack incentives to engage in innovative activities. Host-country IP protection is controlled using data collected from the Heritage Research database. Second, the standard deviation of inflation rates is controlled, as it reflects macroeconomic uncertainty in the host country (Bennett et al., 2023). Third, trade openness reflects the degree of trade liberalization of a foreign country, which may affect MNEs’ investment (Bertrand, 2011). Host-country trade openness is controlled using the total exports as a percentage of gross domestic product (GDP) (collected from the World Bank database).

4. Results

Table 1 presents the descriptive statistics of all variables and their correlation coefficients. The two DVs show a positive correlation (r = 0.087), and both are negatively correlated with information distance between home and host countries (r = −0.121 for firms’ digital transformation and r = −0.039 for subsidiary performance). To address potential multicollinearity concerns, this study uses variance inflation factors (VIF) to examine the VIF scores of all variables across the models. The results reveal that the average VIF for all variables is below 5 (Hair et al., 1998), indicating that multicollinearity is not an issue, and the regression results are unbiased.

Descriptive statistics and correlations.

Note: SD (standard deviation); correlations greater than |0.07| are significant at 0.05.

4.1. Main findings

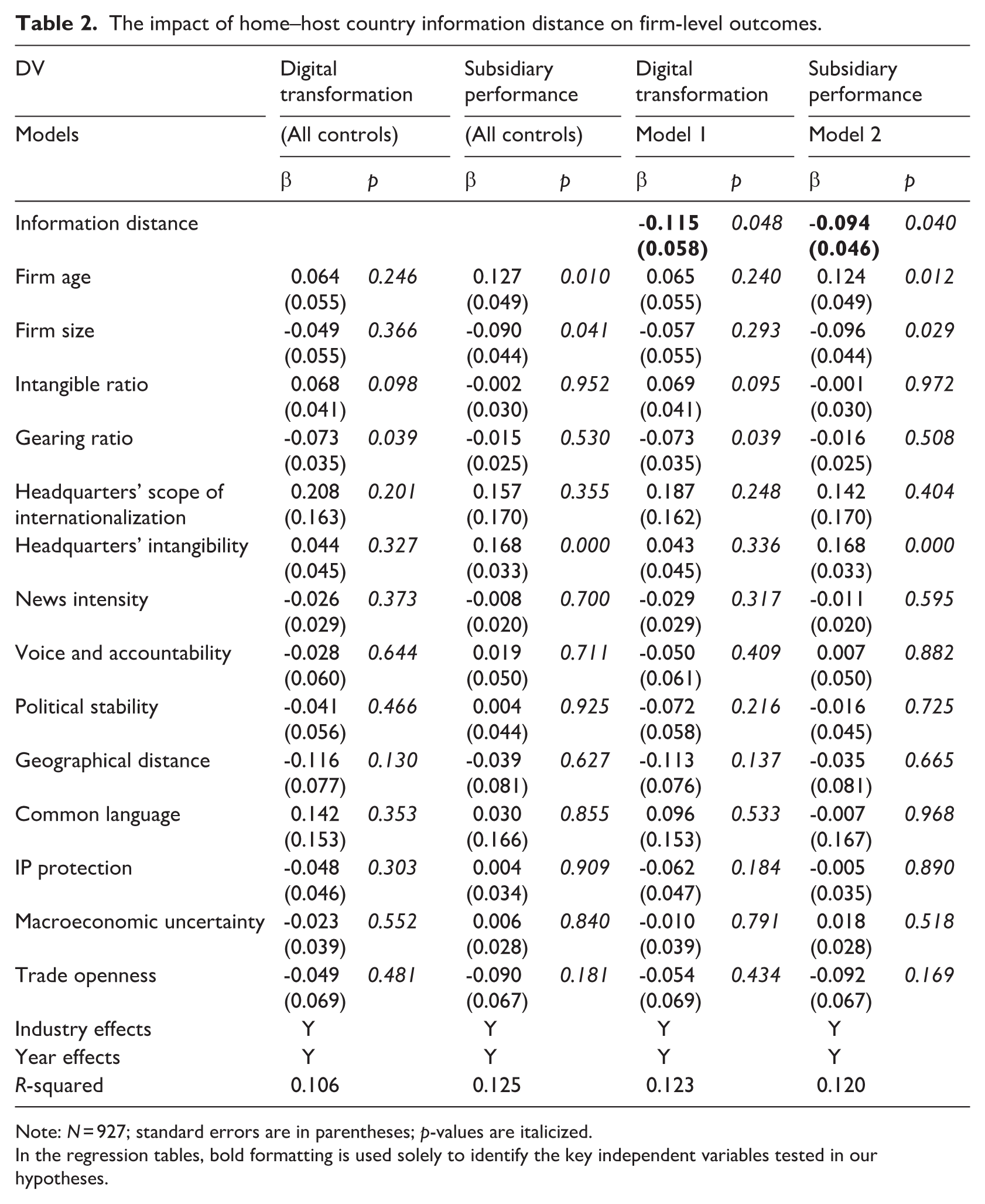

In presenting the regression results, the first two models only included control variables (for the two DVs). In Table 2, Model 1 examines the impact of information distance on firms’ digital transformation, and Model 2 is based on subsidiary performance as the DV. Models 1 and 2 aim to test H1 and H2, respectively. Table 2 shows that the regression coefficient of information distance in Model 1 is negative and significant (β = −0.115, p < 0.050), providing support to H1 that information distance between home and host countries leads to firms facing more difficulties to improve their digitalization. In Model 2, the impact of information distance on firms’ subsidiary performance is also significantly negative (β = −0.094, p < 0.050), confirming our prediction in H2 about the negative influence of country-level information distance.

The impact of home–host country information distance on firm-level outcomes.

Note: N = 927; standard errors are in parentheses; p-values are italicized.

In the regression tables, bold formatting is used solely to identify the key independent variables tested in our hypotheses.

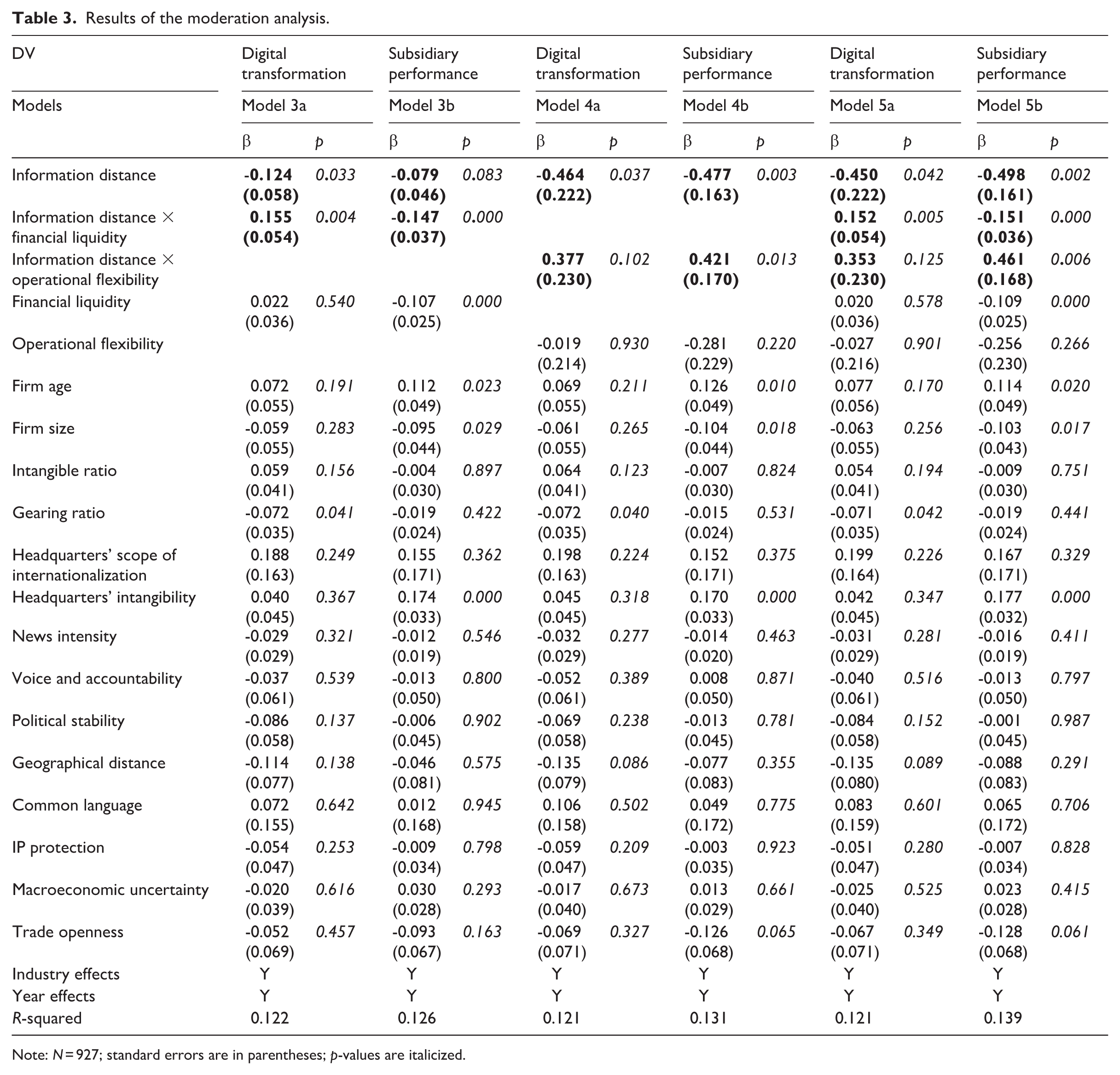

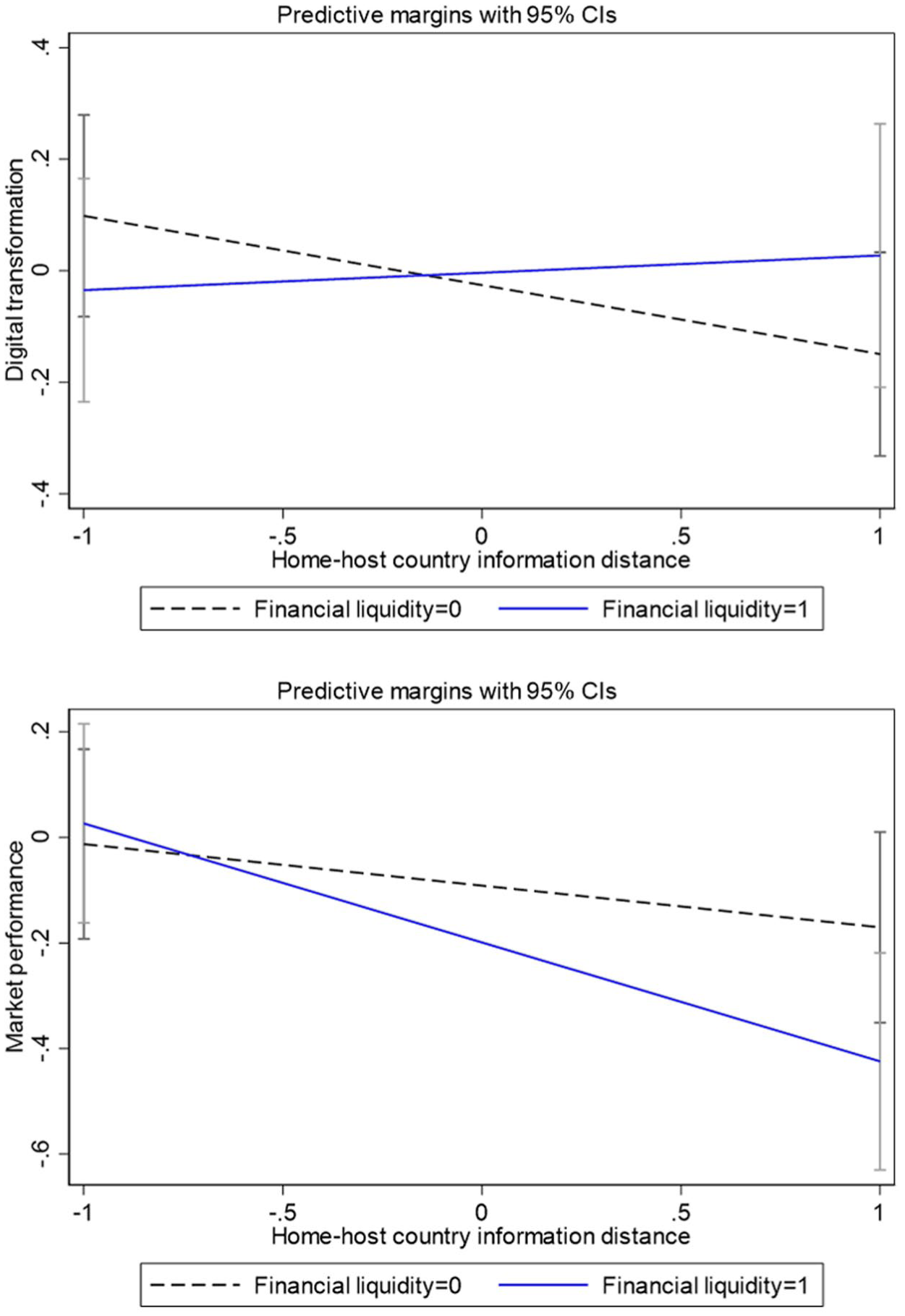

In Table 3, Models 3a and 3b examine the moderating effect of financial liquidity on the relationship between information distance and digitalization and the relationship between information distance and subsidiary performance, respectively. The results show that financial liquidity can reduce the negative impact of information distance on firms’ digitalization but not on subsidiary performance. The coefficient of the interaction term “information distance × financial liquidity” is significantly positive in Model 3a (β = 0.155, p < 0.010) and significantly negative in Model 3b (β = −0.147, p < 0.001). Such a moderating effect is illustrated in Figure 2.

Results of the moderation analysis.

Note: N = 927; standard errors are in parentheses; p-values are italicized.

The moderating effect of financial liquidity.

The different moderating effects show that financial slack is important for MNEs’ prompt digitalization when facing large information distance between home and host countries, as they can better cover unexpected expenditure or production changes in digitalization (e.g. Lang et al., 2012; Ren et al., 2023). However, maintaining slack resources cannot help these firms enhance their subsidiary performance due to the lower rate of expected return (e.g. Amihud and Mendelson, 2008; Brockman and Chung, 2003). Hence, H3a and 3b can be accepted.

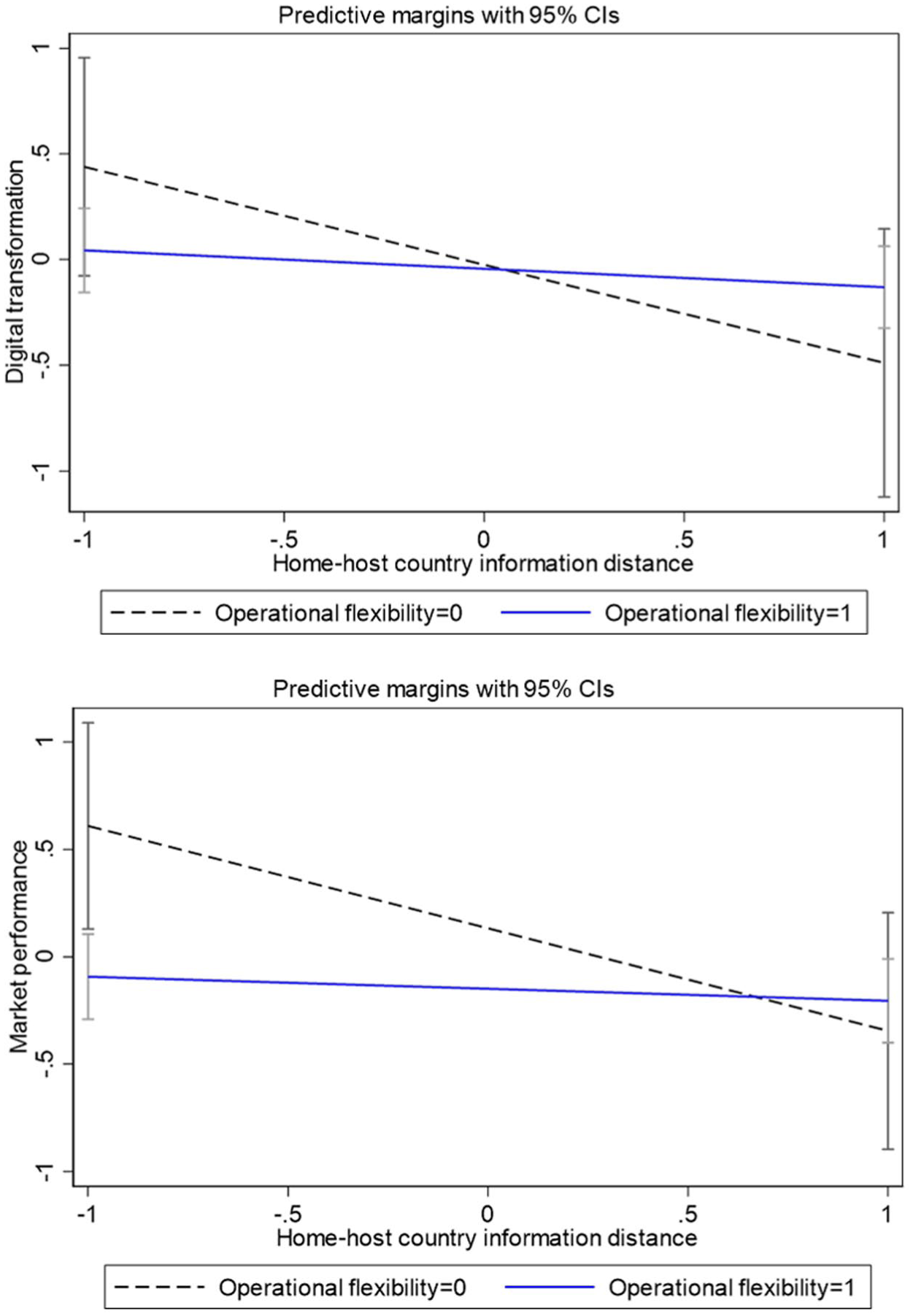

Model 4a of Table 3 shows that the moderating effect of operational flexibility on the relationship between information distance and firms’ digitalization is positive but insignificant (β = 0.377, p > 0.100). Yet, in Model 4b, the coefficient of the interaction term is positive and significant (β = 0.421, p < 0.050). This shows that maintaining operational flexibility is critical for MNE subsidiaries to gain more profits from information distance, as they can be more embedded in the host country to better understand the different digital trends and deploy resource configurations (Geleilate et al., 2020). However, a higher degree of subsidiaries’ operational flexibility cannot help firms leverage the different digital trends in countries to develop broader sets of digital technologies, which implies greater complexity of the digital transformation of firms (e.g. Kronblad, 2020). Therefore, H4b is accepted, while H4a is not. The moderating effect of subsidiaries’ operational flexibility is illustrated in Figure 3.

The moderating effect of operational flexibility.

4.2. Endogeneity concerns and robustness checks

4.2.1. Endogeneity

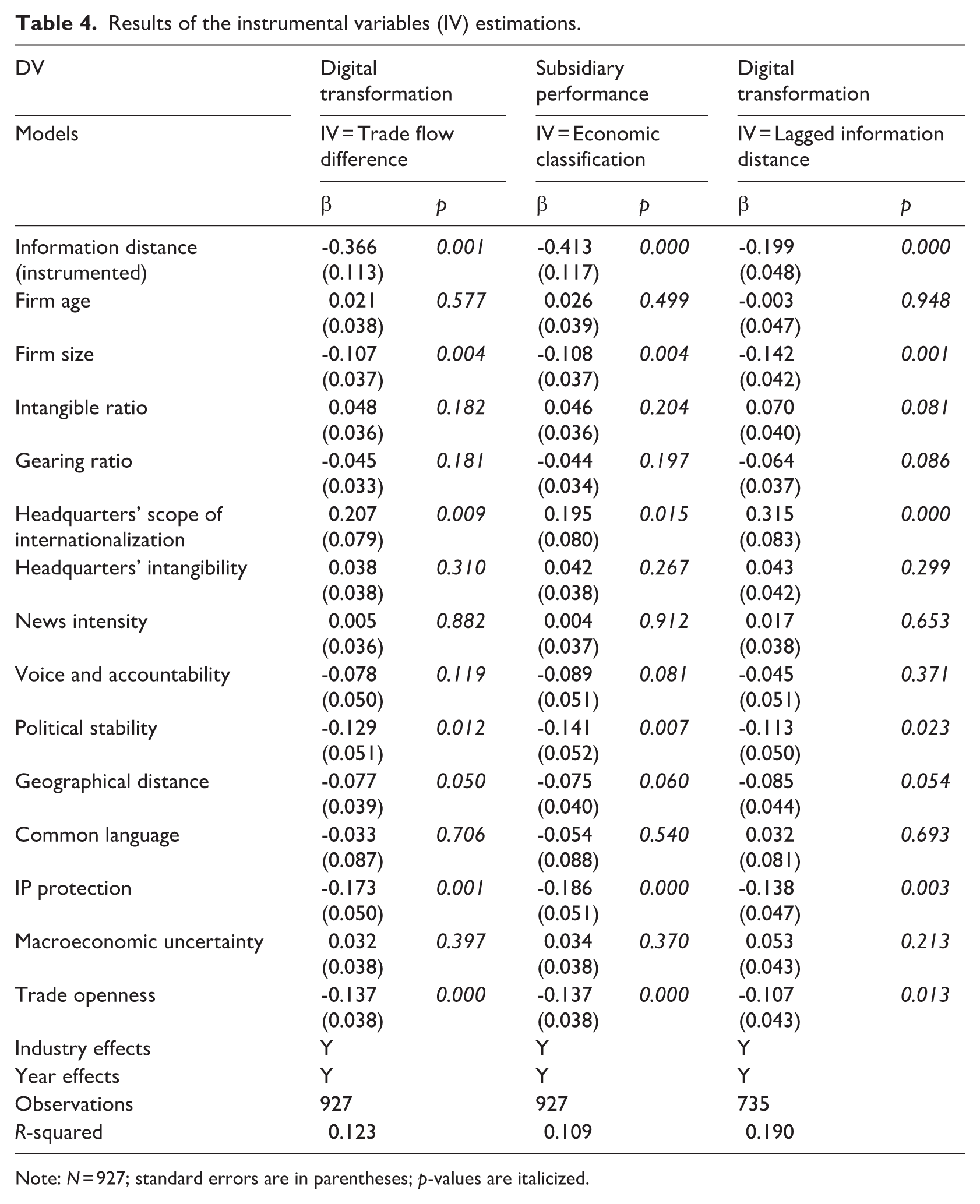

Although our results show low partial correlations between the main variables, and we controlled multiple variables at different levels to account for potential factors influencing the main relationships, the risk of omitted variable bias remains (Lindner et al., 2020), which could undermine the validity of our findings. To address concerns of endogeneity, we employed an instrumental variable (IV) approach and used two-stage least squares regression (2SLS) (Bascle, 2008). In selecting appropriate IVs, we focused on variables that affect the information distance between countries (the endogenous explanatory variable) but do not directly impact the DVs.

First, we used the trade flow difference, measured by the Euclidean distance approach, between home and host countries. Trade flow differences can impact country relationships and information transmission (Mansfield and Pevehouse, 2000; Wu et al., 2012), but they do not directly affect firms’ digitalization or performance, making them a suitable instrument for analysis. Second, we considered the economic classification of home and host countries (i.e. whether both are developed or developing), which affects information distance through market sophistication and information exchange. However, it does not directly affect MNE subsidiaries’ digitalization and strategic decisions. Third, we included a 2-year lagged explanatory variable, following previous practices (Cui et al., 2018; Nguyen et al., 2019), to capture historical differences in information exchange between countries that could influence current cross-country information flows but are unlikely to be directly correlated with future firm decisions or performance.

We tested the strength and validity of the IVs by conducting the first-stage regression and overidentification tests. The results showed that the F-statistic for all three IVs was greater than 10 in the first-stage regression, and the Sargan test supported the validity of the instruments (Nguyen et al., 2019). The IV estimation results, presented in Table 4, indicate that the regression coefficient for information distance remained significantly negative across different IVs. The Hausman test of endogeneity showed no significant evidence of endogeneity, further addressing the potential concerns.

Results of the instrumental variables (IV) estimations.

Note: N = 927; standard errors are in parentheses; p-values are italicized.

4.2.2. Potential mediating relationships between variables

The positive correlation between the two DVs (Table 1) suggests potential links between digital transformation and performance (Fawad Sharif et al., 2024; Merín-Rodrigáñez et al., 2024). For example, Fawad Sharif et al. (2024) argue that digital transformation helps firms navigate market uncertainty, improve knowledge management, and boost performance. Merín-Rodrigáñez et al. (2024) show that digitalization investment helps small- and medium-sized enterprises (SMEs) improve performance and innovate their business models. While we explored the moderating effects of liquidity and ownership, their mediating role in the relationship needs further exploration.

We conducted a post hoc analysis and found that digital transformation does not significantly mediates the relationship between information distance and subsidiary performance (p > 0.100). This may be due to the deep integration of digital transformation in IT-intensive firms, where it does not significantly affect performance. In addition, we found that information distance between countries does not have a direct effect on financial liquidity (p > 0.100) but positively affects operational flexibility (p < 0.010). The Sobel mediation tests showed that neither financial liquidity nor operational flexibility significantly mediate the relationship between information distance and digital transformation. Detailed results are available upon request.

4.2.3. Robustness checks

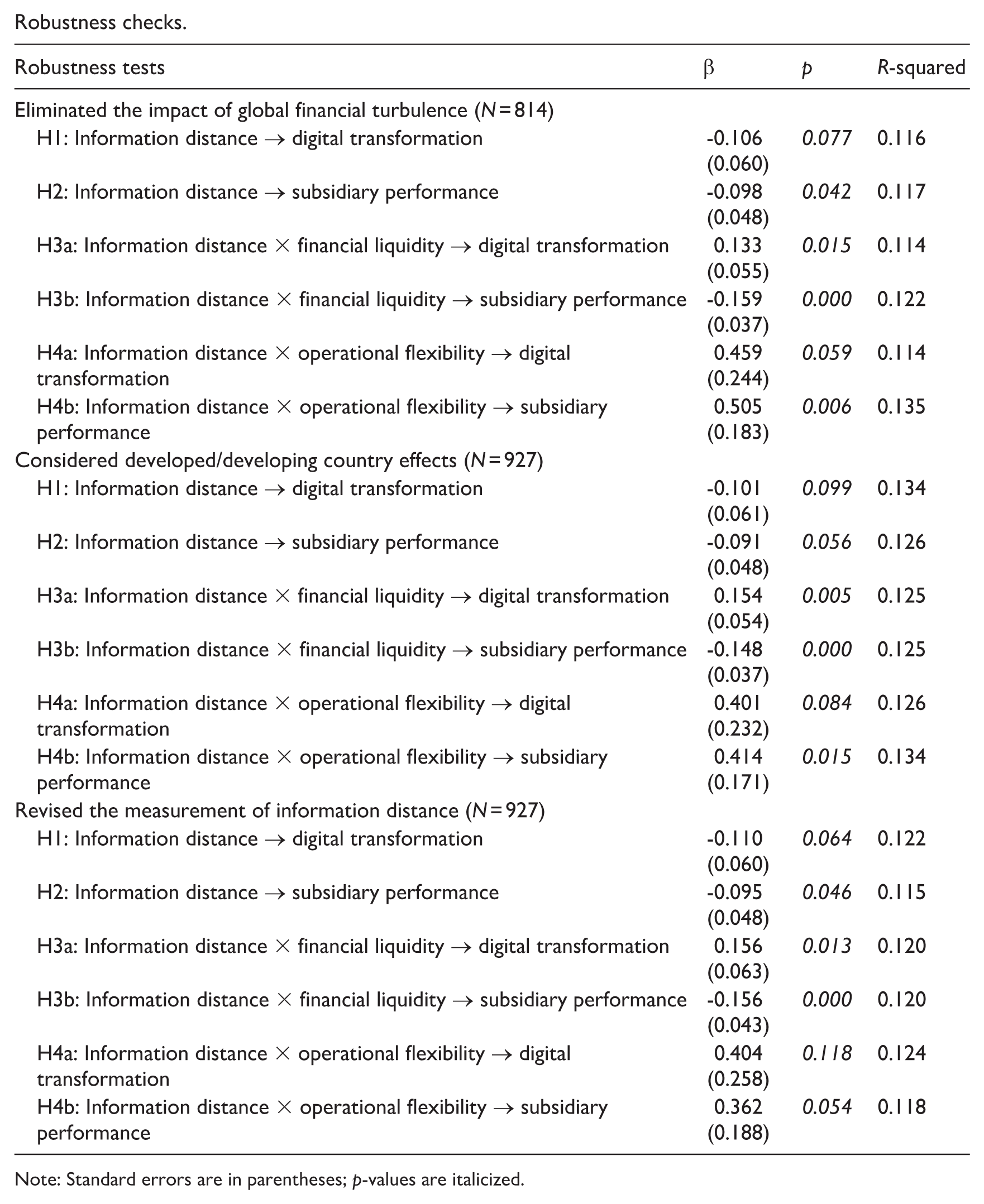

To ensure the robustness of the main findings, we conducted additional tests to re-examine all hypotheses. First, given that financial crises could exert a considerable impact on firm profitability and market confidence (DesJardine et al., 2019; Murinde et al., 2022), we excluded the years 2008 and 2009 from the dataset and reran all the analyses. The results (see Appendix 2) show that information distance negatively affects both firms’ digital transformation (β = −0.106, p < 0.100) and subsidiary performance (β = −0.098, p < 0.050). Financial liquidity positively moderates the relationship between information distance and digitalization (β = 0.133, p < 0.050) but negatively moderates the relationship with subsidiary performance (β = −0.159, p < 0.001). In addition, operational flexibility exerts a positive moderating effect on both relationships.

Second, to examine how information distance affects firm digital transformation across country contexts, we used seemingly unrelated estimation (suest) tests to compare subgroups. Two dummy variables indicate whether the home and host countries are developed (1) or developing (0). The sample was divided into two groups based on the home country (subsample 1 = firms from developed countries; subsample 2 = firms from developing countries). Similarly, two groups were created based on the host country (subsample 3 = firms in developed host countries; subsample 4 = firms in developing host countries). The suest test results reveal significant differences between the home-country group (chi-square = 136.93, p < 0.001) and the host-country group (chi-square = 158.96, p < 0.001). The inclusion of the two dummy variables in our model does not alter the main findings 1 , as shown in Appendix 2, and further supports the robustness of our results.

Third, this study revises the measurement of independent variables by using the overall informational globalization index instead of calculating information distance. The findings for this set of tests, in Appendix 2, are consistent with the main analyses, showing that except for H4a, all hypotheses are supported. The additional tests confirm that the main findings of this study are robust.

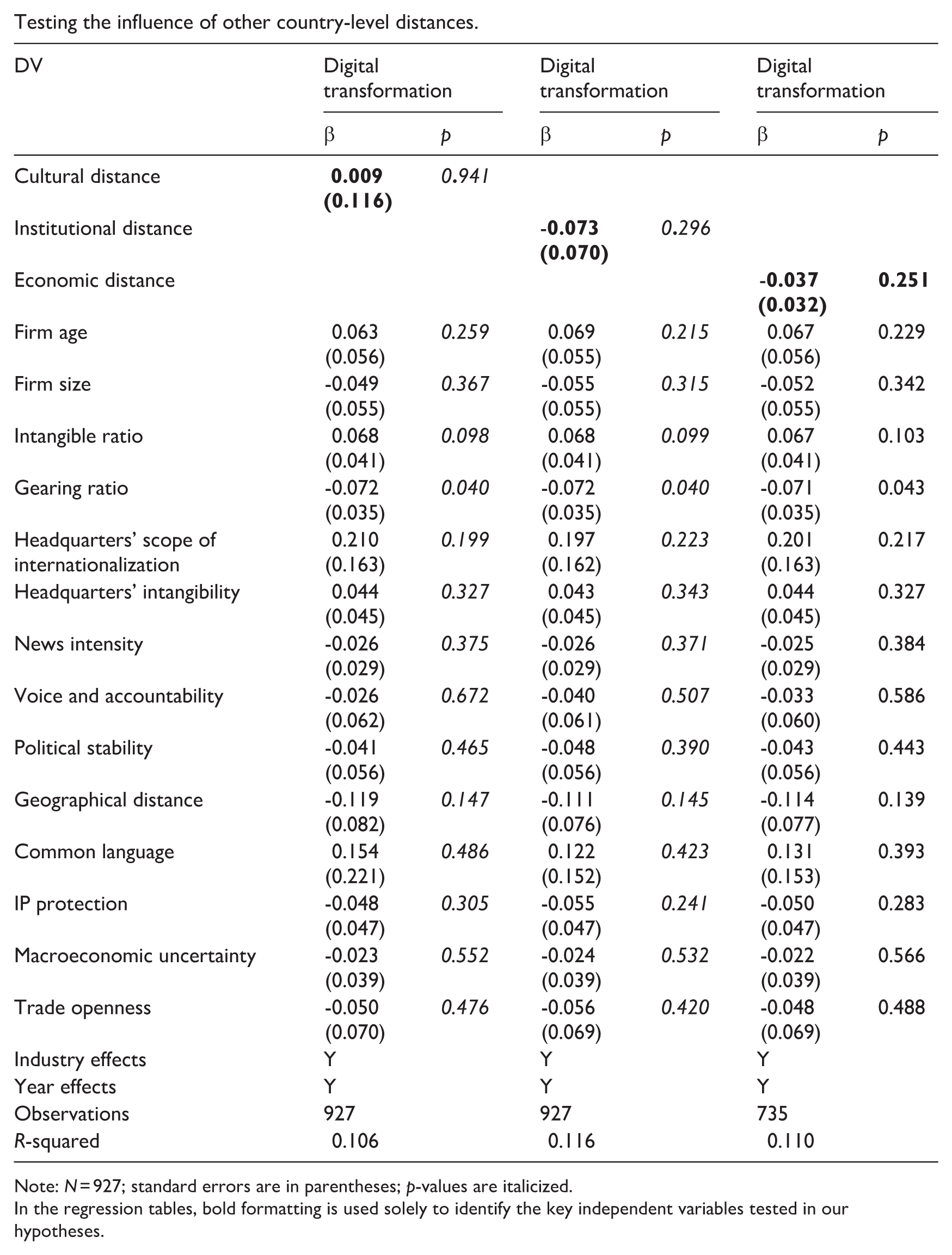

While we highlight the unique impact of information distance, other types of distance also require further exploration. To test if our hypotheses hold for other types of distance, we conducted additional analyses. Cultural distance was measured using Hofstede’s six cultural dimensions 2 (Kogut and Singh, 1988). Institutional distance was assessed based on the six institutional indicators 3 from the World Governance Indicators Project, while economic distance was measured by the difference in GDP per capita between home and host countries. The results show that the impact of these other types of distance on digital transformation is insignificant (see Appendix 3). Geographical distance, which was controlled for in all models, does not significantly affect firm digital transformation. These findings reinforce the importance of information distance for MNEs in IT-intensive sectors.

5. Discussion

The disparities in informational globalization between countries have resulted in MNEs, especially those that rely heavily on information and knowledge (i.e. those in digital technology-intensive industries), facing new challenges and opportunities (Ciulli and Kolk, 2023; Luo, 2022). This study attempts to explore the influence of cross-country information distance in the digital era. Building on real options theory (Adner and Levinthal, 2004; McGrath, 1999), we find that information distance hurts the digital transformation and performance of MNE subsidiaries. However, the relationships are contingent upon the firms’ liquidity and flexibility, which alter options availability under market uncertainty in different ways. On one hand, financial liquidity eliminates the negative impact of information distance on MNE subsidiaries’ digital transformation, but maintaining liquidity does not help improve their subsidiaries’ financial performance. On the other hand, subsidiaries’ operational flexibility is crucial to cope with information distance, helping firms to embed themselves in local knowledge networks and adapt to differing local standards. Our study provides important insights into management and international business literature on cross-country distance and digitalization.

5.1. Contribution to research

The contribution of this study is reflected in several ways. First, this study enriches the growing stream of literature on digitalization by connecting it to the concept of information distance. While studies in the international business field often discuss how cross-country distance impacts MNEs’ activities and performance (Li et al., 2020; Messner, 2023; Zámborský and Yan, 2022), the discussions focus mainly on the geographical, cultural, and institutional aspects of distance that are less likely to change or may change slowly over time. The impact of information distance, which emphasizes informational efficiency between countries (Lindner and Puck, 2024), on MNEs remains largely underexplored.

This study fills the research gap by conceptualizing and testing the role of a new type of distance that is becoming increasingly important in the literature on international business in the digital age (Lindner and Puck, 2024; Meyer et al., 2023). Our construct of information distance is valuable as it goes beyond the existing conceptualizations that assume that financial markets are sufficiently efficient interpreters of information stemming from the underlying national context (Lindner and Puck, 2024). We contribute to the literature by stressing a broader conceptualization of information distance based on informational globalization (Gygli et al., 2019), which acknowledges the actual flows of ideas, knowledge, and images, and the ability to share information across countries. By doing so, our study enriches research on cross-country distance and MNE digital transformation.

Second, existing studies often discuss digitalization at the firm level (Ciulli and Kolk, 2023; Kindermann et al., 2021; Kronblad, 2020; Yi et al., 2023), yet less is known about the linkages between country-level information distance and subsidiary-level digital transformation. This study enriches the literature on MNE subsidiaries and digitalization (e.g. Grimpe et al., 2023; Lee et al., 2023; Murphree et al., 2022) by recognizing both country-level information distance and subsidiary-level digital transformation while exploring the boundary conditions that impact the country–firm (subsidiary) linkages. By applying the real options perspective to examine the role of intra-firm features, our study contributes to the literature on MNE strategic changes, particularly digital transformation, in an era of increasing global uncertainty (Trigeorgis and Miller, 2025).

Our study has important implications for research on international business in the digital age (Meyer et al., 2023). Research on digital firms and their various types such as born-digital firms (e.g. Stallkamp et al., 2023) and digital platform firms (e.g. Stallkamp and Schotter, 2021) emphasizes the need for FDI—for example, MNE subsidiaries—and analyzes the roles of cultural and geographic distance, business models, and industry differences. Our study implies that the relationship between national contextual factors (information distance) and digital transformation and performance of subsidiaries can be explained by incorporating a real options perspective, as financial liquidity and operational flexibility alter options availability under market and digital uncertainty.

5.2. Contribution to practice

This study offers important practical implications for government officials and managers of MNEs. The impact of information distance on MNEs shows that government officials should support MNEs’ digital transformation by providing clear technological standards and assisting firms in learning about taxation, digital regulations, and potential risks when entering different countries. Countries lagging behind their technological competition could see their firms facing additional pressures in internationalization due to information distance. Hence, governments need to understand the importance of digital infrastructure development and formulate solid policies to encourage informational globalization.

Managers of MNEs, especially those in information-intensive sectors, need to pay more attention not only to adapting to geographical, cultural, and institutional distance between home and host countries but also to learning about information distance. By utilizing firm-specific capabilities and proactively embedding them into the host-country knowledge networks, MNEs can convert challenges of information distance into new opportunities and investment options. Managers need to enhance the internal governance of firms by keeping sufficient liquidity to cope with unexpected digital disruptions. More importantly, maintaining operational flexibility can help firms better leverage informational and technological gaps between countries and promote digitalization.

5.3. Limitations and future research directions

The limitations of this study leave room for future improvement. One concern is our reliance on content extracted from news reports to capture firm-level digital transformation. While this approach enables large-scale analysis, it may not fully reflect firms’ actual investments or the true intensity and scope of their digital initiatives. We therefore encourage future research to incorporate more direct measures to enhance construct validity. Also, our study chose MNEs from IT-intensive sectors as the research subject, as these firms are seeking digitalization and are more affected by the changing informational environment. However, other types of firms may also embrace the potential for digitalization, such as those in transportation, construction, or energy industries. Future research could explore the impact of information distance on both digital and non-digital firms to broaden the study’s scope and applicability. While this study examined multiple aspects of a country’s informational globalization, other areas, such as blockchain usage and artificial intelligence (AI) applications, could also be explored (Ciulli and Kolk, 2023). Future studies could also explore the different dimensions of digitalization and improve the measurement of information distance in this study. The digitalization process of MNE subsidiaries is also likely influenced by their parent companies, not solely by information distance (Murphree et al., 2022). Due to data limitations, the role of MNE parent companies was not emphasized in our study, presenting opportunities for further research.

Key practical and research implications

Explores the complexities of cross-border operations by examining how information distance between home and host countries shapes the digital transformation and performance outcomes of MNE subsidiaries.

Brings theoretical contributions to the International Business literature by applying the real options perspective to analyze how MNE subsidiaries mitigate risks associated with information distance through leveraging financial liquidity and operational flexibility.

Deepens our understanding of cross-country distance and contributes to the literature on MNE digital transformation, especially in the context of growing global uncertainty.

Managers of MNEs in IT-intensive sectors should navigate both traditional cross-country distances and information distance by leveraging firm-specific capabilities and strengthening internal governance to better manage digital disruptions. Maintaining liquidity and operational flexibility is essential for overcoming information barriers and capitalizing on new opportunities in global markets.

Governments should facilitate MNEs’ digital transformation by establishing clear technological standards, enhancing digital infrastructure, and addressing the challenges of information asymmetry, particularly for firms facing competitive disadvantages in global markets.

Footnotes

Appendix 1

Sample distribution based on home and host countries.

| Home countries | Number of MNE subsidiaries | Host countries | Number of MNE subsidiaries |

|---|---|---|---|

| The United States | 41 | The United States | 35 |

| The United Kingdom | 17 | The United Kingdom | 27 |

| Canada | 14 | Canada | 13 |

| Japan | 13 | Germany | 9 |

| France | 10 | Australia | 7 |

| Germany | 7 | France | 6 |

| Sweden | 5 | India | 6 |

| Italy | 4 | Israel | 4 |

| Luxembourg | 4 | Sweden | 4 |

| Switzerland | 3 | Poland | 3 |

| India | 3 | Belgium | 3 |

| The Netherlands | 2 | Italy | 2 |

| Poland | 2 | Singapore | 2 |

| Other countries | 11 | Other countries | 15 |

Note: The total number of MNE subsidiaries is 136, with 121 parent firms.

Appendix 2

Robustness checks.

| Robustness tests | β | p | R-squared |

|---|---|---|---|

| Eliminated the impact of global financial turbulence (N = 814) | |||

| H1: Information distance → digital transformation | -0.106 (0.060) |

0.077 | 0.116 |

| H2: Information distance → subsidiary performance | -0.098 (0.048) |

0.042 | 0.117 |

| H3a: Information distance × financial liquidity → digital transformation | 0.133 (0.055) |

0.015 | 0.114 |

| H3b: Information distance × financial liquidity → subsidiary performance | -0.159 (0.037) |

0.000 | 0.122 |

| H4a: Information distance × operational flexibility → digital transformation | 0.459 (0.244) |

0.059 | 0.114 |

| H4b: Information distance × operational flexibility → subsidiary performance | 0.505 (0.183) |

0.006 | 0.135 |

| Considered developed/developing country effects (N = 927) | |||

| H1: Information distance → digital transformation | -0.101 (0.061) |

0.099 | 0.134 |

| H2: Information distance → subsidiary performance | -0.091 (0.048) |

0.056 | 0.126 |

| H3a: Information distance × financial liquidity → digital transformation | 0.154 (0.054) |

0.005 | 0.125 |

| H3b: Information distance × financial liquidity → subsidiary performance | -0.148 (0.037) |

0.000 | 0.125 |

| H4a: Information distance × operational flexibility → digital transformation | 0.401 (0.232) |

0.084 | 0.126 |

| H4b: Information distance × operational flexibility → subsidiary performance | 0.414 (0.171) |

0.015 | 0.134 |

| Revised the measurement of information distance (N = 927) | |||

| H1: Information distance → digital transformation | -0.110 (0.060) |

0.064 | 0.122 |

| H2: Information distance → subsidiary performance | -0.095 (0.048) |

0.046 | 0.115 |

| H3a: Information distance × financial liquidity → digital transformation | 0.156 (0.063) |

0.013 | 0.120 |

| H3b: Information distance × financial liquidity → subsidiary performance | -0.156 (0.043) |

0.000 | 0.120 |

| H4a: Information distance × operational flexibility → digital transformation | 0.404 (0.258) |

0.118 | 0.124 |

| H4b: Information distance × operational flexibility → subsidiary performance | 0.362 (0.188) |

0.054 | 0.118 |

Note: Standard errors are in parentheses; p-values are italicized.

Appendix 3

Testing the influence of other country-level distances.

| DV | Digital transformation | Digital transformation | Digital transformation | |||

|---|---|---|---|---|---|---|

| β | p | β | p | β | p | |

| Cultural distance |

|

0.941 | ||||

| Institutional distance | - |

0.296 | ||||

| Economic distance | - |

|

||||

| Firm age | 0.063 |

0.259 | 0.069 |

0.215 | 0.067 |

0.229 |

| Firm size | -0.049 |

0.367 | -0.055 |

0.315 | -0.052 |

0.342 |

| Intangible ratio | 0.068 |

0.098 | 0.068 |

0.099 | 0.067 |

0.103 |

| Gearing ratio | -0.072 |

0.040 | -0.072 |

0.040 | -0.071 |

0.043 |

| Headquarters’ scope of internationalization | 0.210 |

0.199 | 0.197 |

0.223 | 0.201 |

0.217 |

| Headquarters’ intangibility | 0.044 |

0.327 | 0.043 |

0.343 | 0.044 |

0.327 |

| News intensity | -0.026 |

0.375 | -0.026 |

0.371 | -0.025 |

0.384 |

| Voice and accountability | -0.026 |

0.672 | -0.040 |

0.507 | -0.033 |

0.586 |

| Political stability | -0.041 |

0.465 | -0.048 |

0.390 | -0.043 |

0.443 |

| Geographical distance | -0.119 |

0.147 | -0.111 |

0.145 | -0.114 |

0.139 |

| Common language | 0.154 |

0.486 | 0.122 |

0.423 | 0.131 |

0.393 |

| IP protection | -0.048 |

0.305 | -0.055 |

0.241 | -0.050 |

0.283 |

| Macroeconomic uncertainty | -0.023 |

0.552 | -0.024 |

0.532 | -0.022 |

0.566 |

| Trade openness | -0.050 |

0.476 | -0.056 |

0.420 | -0.048 |

0.488 |

| Industry effects | Y | Y | Y | |||

| Year effects | Y | Y | Y | |||

| Observations | 927 | 927 | 735 | |||

| R-squared | 0.106 | 0.116 | 0.110 | |||

Note: N = 927; standard errors are in parentheses; p-values are italicized.

In the regression tables, bold formatting is used solely to identify the key independent variables tested in our hypotheses.

Acknowledgements

We sincerely thank the Editors and the anonymous reviewers for their insightful feedback and constructive suggestions on earlier versions of this manuscript.

Final transcript accepted 1 November 2025 by Lingli Luo (Associate Editor—Strategy)

Authors’ Note

This manuscript has not been published previously and is not under consideration for publication elsewhere.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We acknowledge the support we received from the University of Auckland Business School’s MIB Department Collaborative Research Fund. The first author is grateful for the financial support from the National Natural Science Foundation of China (NSFC) (72372119).