Abstract

This study examines the determinants of payment times to small suppliers. It draws on panel data submitted by Australian firms at six different time points between 2021 and 2023 as part of their obligations under the Payment Times Reporting Scheme (PTRS). The theoretical framework for examining the determinants comes from Christine Oliver’s work into the conditions under which firms respond to institutional pressures; paying small suppliers promptly is one such institutional pressure impacting Australian firms. The results show that dependence on small suppliers, existing commitment to responsible payment, industry type and firm size are linked to better payment terms and/or faster payment for small suppliers. These correspond to constituent, content, context and cause factors in Oliver’s predictive framework, respectively. Overall, the study helps to explain why some firms are more likely than others to pay small suppliers promptly. Implications for scholarship and practice are contained within.

1. Introduction

Getting paid on time is a perennial challenge for suppliers. The latest payment data from Australia, for example, shows that 52% of the total value of business-to-business (B2B) invoices were overdue in the first quarter of 2025 and up to 11% was classed as bad debt (Atradius, 2025a). Governments and industry stakeholders have tried various ways to solve it, albeit with questionable success (Cowton and San-Jose, 2017). Early research on this subject examined payment delays from the perspective of small firms (Howorth and Reber, 2003; Paul and Boden, 2011; Peel et al., 2000) while recent studies have investigated the payment practices of large corporations towards suppliers of all sizes and types (Chuk et al., 2025; Flynn and Li, 2023; Grewal et al., 2024, 2020). A specific focus on the payment terms that large firms offer small suppliers and the actual time it takes them to settle invoices is missing from the literature, however, even though small suppliers are most vulnerable to corporate customers exploiting their trade credit (Hajikazemi et al., 2020; Paul and Boden, 2011; Walker and Hyndman, 2025).

Payment delays have serious consequences for small suppliers, defined in this study as any firm with under AUS $10M in revenue [see Note 1]. In the first instance, it can cause cash flow crunches that make it harder for them to pay their own bills, invest in projects, hire staff or onboard new customers (Atradius, 2025a, 2025b; Barclays, 2022; Barrot and Nanda, 2020; Intrum, 2023). There are also the resources involved in chasing up overdue payments; resources that could be used for value-adding activities like customer relationship management (Intrum, 2023; Paul and Boden, 2011). Payment delays are not without consequences for buyers either. Suppliers can retaliate by raising prices (Walker and Hyndman, 2025) or, in more extreme cases, terminating the relationship (Kovach et al., 2023). The direct effects of poor payment practice on suppliers, and its ripple effects throughout the supply chain, eventually show up in macroeconomic data as depressed commercial investment, tax revenue forgone, reduced job creation and lower enterprise survival rates (Australian Small Business & Family Enterprise Ombudsman, 2019; Federation of Small Business, 2017).

Given what is at stake for suppliers and the wider economy, it is not surprising that practitioners are interested in promoting a culture of responsible payment practice. We see this, for instance, in the annual Payment Practices Barometer country reports published by Atradius Group (Atradius, 2025a, 2025b). Academics are also interested in this subject, although perhaps not to the extent that its importance would suggest. Quantitative studies have tested how firm characteristics, financial status and procurement policies influence payment punctuality (De Carvalho, 2015; Flynn and Li, 2023; Lorentz et al., 2016) and qualitative studies have explored the underlying dynamics of payment delays, including power imbalances between buyers and suppliers and weak credit management practices (Chen, 2012; Cowton and San-Jose, 2017; Hajikazemi et al., 2020). On the plus side, this body of scholarship explains in part why some firms pay suppliers promptly while others are slow to pay or never pay. Yet, it is predominantly a-theoretical, tends not to distinguish between supplier sizes, and typically relies on cross-sectional data.

This study is undertaken to address the aforementioned theoretical and research design limitations, thereby contributing to a better understanding of supplier payment times. It uses Oliver’s (1991) operationalisation of institutional theory (DiMaggio and Powell, 1983; Meyer and Rowan, 1977) to hypothesise a series of conditions under which large firms are likely to offer small suppliers favourable payment terms and settle invoices with them promptly. Institutional expectations over prompt payment to small suppliers are embedded in government regulations and policies, industry payment codes and civic society campaigns and advocacy work. However, it cannot be assumed that firms will comply with institutional expectations. As Oliver (1991: 174) states, corporate responses to institutional expectations are ‘behaviours to be predicted rather than theoretically predefined outcomes of institutional processes’. Whether firms comply will depend on why the institutional pressure is being exerted, how it is being exerted, who has a stake in it, what it means for organisational objectives, and the context in which it plays out (Oliver, 1991).

To test our hypotheses, we use panel data from Australia’s Payment Times Reporting Scheme (PTRS). Since 2021 large firms in Australia are required to provide information about their payment terms and payment times (Australian Government, 2022). ‘Payment terms’ is the number of days within which a firm says it will pay its small suppliers whereas ‘payment times’ is the number of days it takes a firm to pay its small suppliers. The analysis involves over 400 firms and covers the years 2021–2023 inclusive. The 3-year timespan is crucial as it allows us to control for disruptions to business and society across Australian states and territories during and after the Covid-19 pandemic (Edwards et al., 2022). Previous research by Lorentz et al. (2016) and Caniato et al. (2020) suggests that the type of economic contraction witnessed during the pandemic, and the subsequent spike in inflation and interest rates that followed it [see Note 2], can cause firms to lengthen their payment terms and delay payment to suppliers. We supplement the PTRS data with data from secondary sources like Dun & Bradstreet, Business Council of Australia and Aus Tender to build a profile of the sample.

In terms of contributions, the study’s application of Oliver’s (1991) predictive framework provides theoretical ballast to the subject and explains the conditions under which firms are likely to treat small suppliers fairly over payment. Relatedly, it considers institutional factors like involvement in government contracting and adherence to payment codes as determinants of supplier payment times. By contrast, foregoing research mainly considers organisational characteristics and financial indicators (De Carvalho, 2015; Grewal et al., 2020; Howorth and Reber, 2003; Lorentz et al., 2016). Our study’s exclusive focus on small suppliers is novel, as it recognises that prompt payment is most salient for them because of their limited cash reserves and difficulties in accessing external finance. Indeed, the salience of prompt payment for small suppliers is reflected in corporate procurement policies. BHP, for instance, has 7 day payment terms for small, local and Indigenous-owned suppliers (BHP, 2021). In a methodological sense, the panel data set we use yields a more robust set of empirical results than cross-sectional studies on this subject.

The study has particular resonance for debates about responsible business practices in Australia. It is carried out against a backdrop of Australian Government intervention in this space. Here, we are talking not only about the PTRS but other legislative requirements for public sector organisations and government contractors to pay suppliers within 20 days (Australian and Government, 2023a, (Australian Government, 2023a, 2023b). The insights the study generates should also be viewed in relation to responsibility and resilience in the post-Covid era where Australian firms are confronted with heightened economic, regulatory and geo-political risks. Notably, themes of risk and resilience were recently explored in an Australian Journal of Management Special Issue dedicated to Sustainable Supply Chains in a Turbulent World (Feng et al., 2023). Finally, this study makes the case for recognising supplier payment times as a strand of sustainable procurement and complements research by Grob and Benn (2014), Young et al. (2015) and Lau et al. (2023) on this subject in an Australian corporate context.

2. Theoretical framework

Across most countries, institutional stakeholders have applied various forms of regulative, normative and cultural-cognitive pressure on firms to pay suppliers, especially small supplies, promptly. Examples include setting maximum payment times for public and private sector organisations, instituting voluntary payment codes, and accrediting firms with Fast Payer Awards (Australian Government, 2023a; Cowton and San-Jose, 2017; Good Business Pays, n.d.). Latterly, legislation has been enacted in Australia and the UKingdom that obliges large firms to publicly disclose payment time data, as part of pressuring them to behave ethically towards suppliers (Australian Government, 2022; UK Government, 2019). Applying these institutional pressures on firms is motivated by a concern over the ramifications that payment delays have for suppliers, supply chains and the health of the economy, as described in the Introduction (Australian Small Business & Family Enterprise Ombudsman, 2019; Barrot and Nanda, 2020; Intrum, 2023; Kovach et al., 2023).

To understand how firms might respond to institutional pressures over supplier payments, we turn to institutional theory. Institutional theory explains organisational behaviour in terms of institutional forces (Meyer and Rowan, 1977). It asserts that firms adjust their practices to reflect rules and norms set by institutional stakeholders like legislators, regulators, professional bodies, industry associations and corporate networks. As part of this adjustment, firms come to exhibit similar characteristics in a process known as isomorphism (DiMaggio and Powell, 1983). According to institutional theorists, much of organisational behaviour is institutionally determined and cannot be explained by market forces. The impetus for firms to align with institutional norms is social legitimacy (Dowling and Pfeffer, 1975). To quote the same authors, ‘organizations seek to establish congruence between the social values associated with or implied by their activities and the norms of acceptable behaviour in the larger social system’ (Dowling and Pfeffer, 1975: 122). To be out of step with prevailing social values can damage a firm’s reputation and make it difficult to secure investment, retain customers or form new business relationships.

Applied to our subject, institutional theory implies that firms will pay small suppliers on time to satisfy institutional stakeholders and maintain their social legitimacy. As indicated above, institutional momentum is building on the issue of supplier payment times and there is an elevated reputational risk for firms who appear to be defying institutional expectations. Illustrative of this risk, a survey of the British public found that over half of respondents would be willing to boycott a firm if it was revealed to be a persistent late payer (Barclays, 2022). Institutional theorists acknowledge, however, that institutional pressures are not deterministic of organisational behaviour in every instance. Sometimes firms deal with institutional pressures by paying lip service to them and not making any substantive changes to their operations. Meyer and Rowan (1977) labelled this scenario institutional conformity of a ‘ceremonial kind’. In our context, ceremonial conformity could mean that firms adopt supplier-friendly payment policies but fail to implement them.

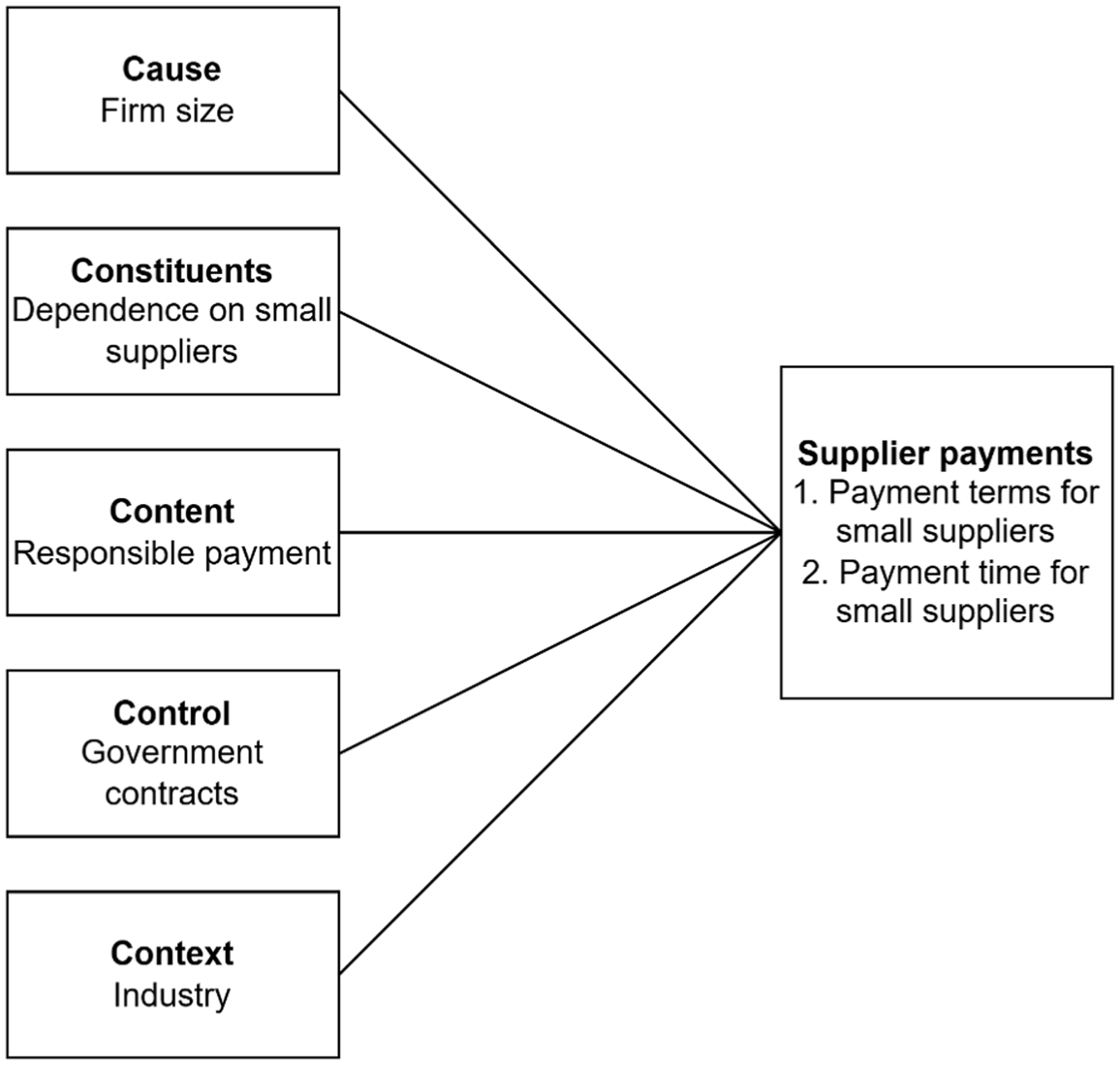

Building on the work of earlier theorists, Oliver (1991) proposed a contingent view of how institutional pressures influence organisational behaviour. By integrating institutional and strategic choice theories, Oliver (1991) developed a framework for predicting corporate responses to institutional pressures. As well as acquiescence, Oliver (1991) sees firms as being able to compromise on, avoid, defy and manipulate institutional expectations. There is a range of responses, in other words, and institutional pressures are not deterministic in all cases. For Oliver (1991), how a firm responds to institutional pressures depends on the following five factors (1) cause or rationale for the institutional pressure (2) internal or external constituents associated with the institutional pressure (3) content of the institutional pressure (4) control mechanisms through which the institutional pressure is exerted and (5) context in which the institutional pressure plays out. The same institutional pressure may be deterministic of some firms’ behaviour but not others.

In this study we use Oliver’s (1991) framework as the theoretical basis for predicting how firms respond to institutional pressures to pay small suppliers promptly (see Figure 1). To operationalise the framework, we draw on quantitative and qualitative research into supplier payment times as well as insights from the supply chain management (SCM) and corporate social responsibility (CSR) literatures. This includes investigations into how organisational practices and industry characteristics affect the likelihood of timely and compliant payment (Caniato et al., 2020; Flynn and Li, 2023; Grewal et al., 2020; Lorentz et al., 2016; Paul and Boden, 2011). It also includes studies that have modelled or tested institutional determinants of sustainable procurement practices and CSR (Campbell, 2007; Ferri et al., 2016; Grob and Benn, 2014; Hoejmose et al., 2014b, 2014a; Kauppi and Hannibal, 2017). The next section presents five hypothesised relationships between institutional pressures and payment times to small suppliers.

Institutional determinants of supplier payment times.

3. Hypotheses

3.1. Cause

There is a rationale behind every institutional pressure, which Oliver (1991) sees as either to do with social fitness or economic efficiency. The rationale for institutional pressure over prompt payment to small suppliers is primarily about social fitness in that it is viewed as ethical business conduct. How firms respond to this, or any type of institutional pressure will depend on their assessment of its intent. A positive assessment makes conformance likely while doubts over it can lead to resistance. Most firms outwardly profess support for institutional efforts to ensure small suppliers are paid on time, especially given its connotations of fairness, ethics and trustworthiness (Cowton and San-Jose, 2017). Moreover, it exemplifies socially responsible purchasing and SCM, which most firms claim to be committed to practising (Ferri et al., 2016; Hoejmose et al., 2014a; Kauppi and Hannibal, 2017). Arguably, larger firms will be more inclined to respond positively because they have a public reputation to defend with regulators, investors and customers (Grewal et al., 2024). The social fitness implications of paying small suppliers on time are greater for them. Grewal et al. (2020) lend credence to this view by finding a positive relationship between a firm’s media presence and payment punctuality. As such, we hypothesise the following:

H1a: Larger firms have better payment terms for small suppliers.

H1b: Larger firms pay small suppliers faster.

3.2. Constituents

The degree of dependency on pressuring constituents, whether internal or external, is a critical factor in predicting corporate responses to institutional expectations (Campbell, 2007; DiMaggio and Powell, 1983; Oliver, 1991). High dependency on pressuring constituents increases the likelihood of institutional compliance, according to the same authors, while low dependency creates space for non-compliance. One pressuring constituent group central to payment times are small suppliers. As they are most impacted by payment delays, they and their representative bodies have a vested interest in pushing corporate customers to pay promptly (Walker and Hyndman, 2025). This can be witnessed in campaigning by industry representative associations like the Federation of Small Business (2017) over prompt payment for small firms. On this basis, we expect that buying firms with a high dependence on small suppliers will experience greater pressure over prompt payment, particularly as disclosure legislation and industry codes are explicitly aimed at empowering small suppliers in Australia and elsewhere (Grewal et al., 2024). The net effect should be a more responsive stance towards small suppliers. Firms that are unresponsive to such pressure could find small suppliers reducing service levels, raising prices or even severing relationships, with all the implications this has for their competitiveness (Kovach et al., 2023; Walker and Hyndman, 2025). As such, we hypothesise:

H2a: Firms with a high dependence on small suppliers have better payment terms for small suppliers.

H2b: Firms with a high dependence on small suppliers pay small suppliers faster.

3.3. Content

According to Oliver (1991), the content of institutional pressures also determines corporate responses. Institutional pressures that are consistent with a firm’s goals are more likely to be complied with whereas inconsistency raises the prospect of rejection. This same principle applies to institutional pressure over prompt payment, and there is already evidence to corroborate it. Flynn and Li (2023) and Chuk et al. (2025) found that firms with an existing commitment to responsible payment, indicated by their membership of a voluntary payment code, had a better record of sticking to payment terms and settling invoices quickly with suppliers of all sizes, especially during the Covid-19 pandemic. Similar findings were returned by Ferri et al. (2016) where firms already committed to CSR showed a greater inclination to implement socially responsible procurement. For firms without such commitments, institutional expectations over shortening payment times are more likely to be interpreted as inconsistent with organisational goals and requiring changes to procurement operations and financial strategy that they would prefer not to make. The probability of non-compliance increases as a result. As such, we hypothesise:

H3a: Firms with an existing commitment to responsible payment have better payment terms for small suppliers.

H3b: Firms with an existing commitment to responsible payment pay small suppliers faster.

3.4. Control

Regulations, professional standards and cultural conditioning are among the ways institutional pressure is applied to firms (Campbell, 2007; DiMaggio and Powell, 1983; Oliver, 1991). These same mechanisms are used to challenge the culture of late payment and help small suppliers by, for example, affording them a legal right to claim interest on late payment in jurisdictions like Australia and the European Union (Australian Government, 2023a; European Commission, 2014) or publishing corporate league tables of payment performance in the United Kingdom (Good Business Pays, n.d.). An example of regulatory coercion is linking the award of government contracts to timely payment. Firms awarded high value contracts with the Australian Government are contractually bound to pay sub-contractors within 20 days (Australian Government, 2023b) while bidders for high value contracts with the UK Government must declare that their supplier payment record meets minimum standards (UK Cabinet Office, 2023). Even lower value government contracts assume that the awardee will discharge their financial obligations to sub-contractors fairly. Leveraging government contracting in this way is no different from corporations pressuring suppliers to adopt environmentally friendly SCM practices (Hoejmose et al., 2014b; Kauppi and Hannibal, 2017). As such, we hypothesise:

H4a: Firms with government contracts have better payment terms for small suppliers.

H4b: Firms with government contracts pay small suppliers faster.

3.5. Context

Environmental context also influences how firms respond to institutional pressures. As Oliver (1991) states, environments vary on dimensions like uncertainty and inter-dependence, and this feeds through to the probability of institutional compliance. We know that environmental context matters for supplier payment times, as some industries offer better terms and are faster to pay than others (Australian Small Business & Family Enterprise Ombudsman, 2019; Federation of Small Business, 2017; Intrum, 2023). One explanation for inter-industry differences is Days Sales Outstanding (DSO). Consumer-facing industries have zero DSO as payment is collected at the point of sale, which means firms are in a position to settle invoices quickly. By contrast, business-to-business industries like manufacturing have lengthy DSO, which limits how quickly they can settle invoices (Grewal et al., 2020; Lorentz et al., 2016). Another explanation is that revenue generation in industries like finance and administrative services does not depend on the re-sale of supplier inputs, but it does in industries like processing and production where firms must convert raw materials or works-in-progress into saleable products (Chuk et al., 2025).

The configuration of supply chains is a further aspect of environmental context that affects supplier payments. Industries like professional services tend to have flat, geographically bounded supply chains, which makes supplier payments relatively straightforward. Electronics or automotive manufacturing have complex, multi-tier, international supply chains, which invariably leads to lengthier payment times. The construction industry has a unique triadic supply chain configuration, consisting of project owners, main contractors and sub-contractors (Chen, 2012). Funds flow from the project owner to the contractor and then to the sub-contractor, which is associated with an increased risk of payment delay. Proof of this, Bolton et al. (2022) found that 46% of the 355 payments across the 30 construction projects they examined were late. Finally, environmental context can be shaped by industry-specific regulations governing payment times. The EU’s Unfair Trading Practices (UTP) Directive requires firms purchasing perishable food products to settle invoices within 30 days while some jurisdictions direct their public sector organisations to pay suppliers within defined time periods (Australian Government, 2023a; European Commission, 2014). As such, we hypothesise:

H5a: Firms in industries like retail, finance and services have better payment terms for small suppliers compared to industries like mining, manufacturing and construction.

H5b: Firms in industries like retail, finance and services pay small suppliers faster compared to industries like mining, manufacturing and construction.

4. Method

4.1. Research setting

The Australian government introduced the PTRS as part of a 2020 Act under the same name (Australian Government, 2022). PTRS legally requires large firms operating in Australia to make twice-yearly disclosures on their payment terms and payment times to small suppliers (see Note 3). Like the UK’s Duty to Report on Payment Practices and Performance (UK Government, 2019), the logic behind PTRS is to increase transparency around supplier payment times and, by extension, encourage firms to settle invoices quickly. One of the benefits of the PTRS is that it provides suppliers with information about the payment performance of current or prospective customers; information that can be used in negotiations or when deciding to extend trade credit. Firms covered by PTRS submit data through a dedicated government portal, which is refreshed monthly and released into the public domain. The Treasury Department of the Australian Government administers the Act, monitors compliance and has the power to impose civil penalties on firms who fail to submit data or submit erroneous data.

PTRS is one of several Australian Government-led initiatives aimed at fostering a responsible payment culture. Another is the Pay-on-Time or Pay-Interest Policy, which instructs Australian Government Agencies to settle invoices within 20 calendar days, or 5 days if the Agency and the supplier have Pan-European Public Procurement On-Line (PEPPOL) compliant e-Invoicing capability. This policy appears to be effective, as over 90% of invoices by number and value were paid within 20 days in 2022 (Australian Government, 2023a). The Payment Times Procurement Connected Policy, which was mentioned in section 3.4, stipulates that major government contractors must agree to pay sub-contractors within 20 days for work valued at up to AUS $1M (Australian Government, 2023b). Mirroring international trends, the Australian Government is using both direct and indirect interventions to speed up payments to suppliers, especially small suppliers. Such interventions attest to the importance of supplier payments as a policy issue in Australia.

4.2. Data collection

The data collection process for this study consisted of two stages. The first involved collecting data on supplier payment times. To do this, we downloaded an .xls file from the PTRS website and used systematic random sampling to identify 750 firms from approximately 11,000 listed entries. The sample reduced to 728 firms after the deletion of 22 duplicates. We then checked to ensure that firms had payment data available for 2021, 2022 and 2023. This was necessary because we wanted to observe supplier payments during and after the Covid-19 pandemic. A significant number of firms (301) did not meet this criterion, either because they did not submit data in one or more of the 3 years or made no payments to small suppliers. Their deletion left a final usable sample of 427 firms (see Table 1). The second stage of the process involved gathering data on the independent and control variables, which we describe in section 4.4.

Data collection and screening process.

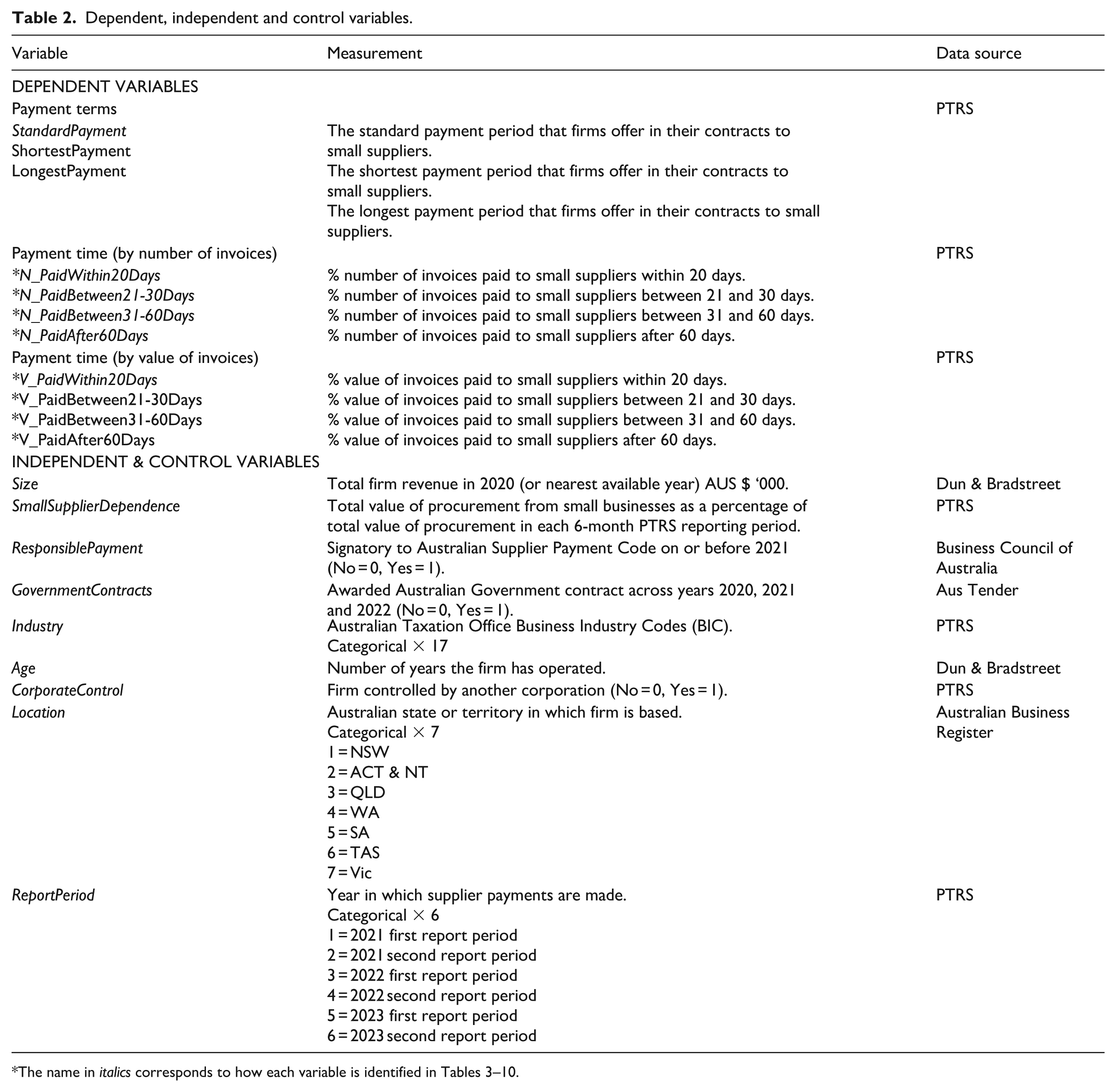

4.3. Dependent variables

There are two dependent variables in this study: payment terms and payment times. Payment terms is the number of days within which a firm says it will pay its small suppliers, for example, 30 days. Under the PTRS, firms must provide information on their standard, shortest and longest payment terms. This reflects the fact that firms often vary their payment terms by supplier type or procurement category. We use these three discrete measures of payment terms in the analysis. Payment times is the time it takes a firm to pay its small suppliers. If payment terms represent intentions, payment times represent action. The PTRS requires firms to submit data on the percentage of invoices paid by number and by value within 20 days, 21–30 days, 31–60 days and after 60 days. To illustrate, a firm might pay 15% of invoices within 20 days, 50% between 21 and 30 days, 25% between 31 and 60 days and 10% after 60 days. This percentage data provides the basis for our analysis of payment times. Our panel data set comprises twice-yearly observations on payment terms and payment times for each firm between 2021 and 2023 inclusive.

4.4. Independent and control variables

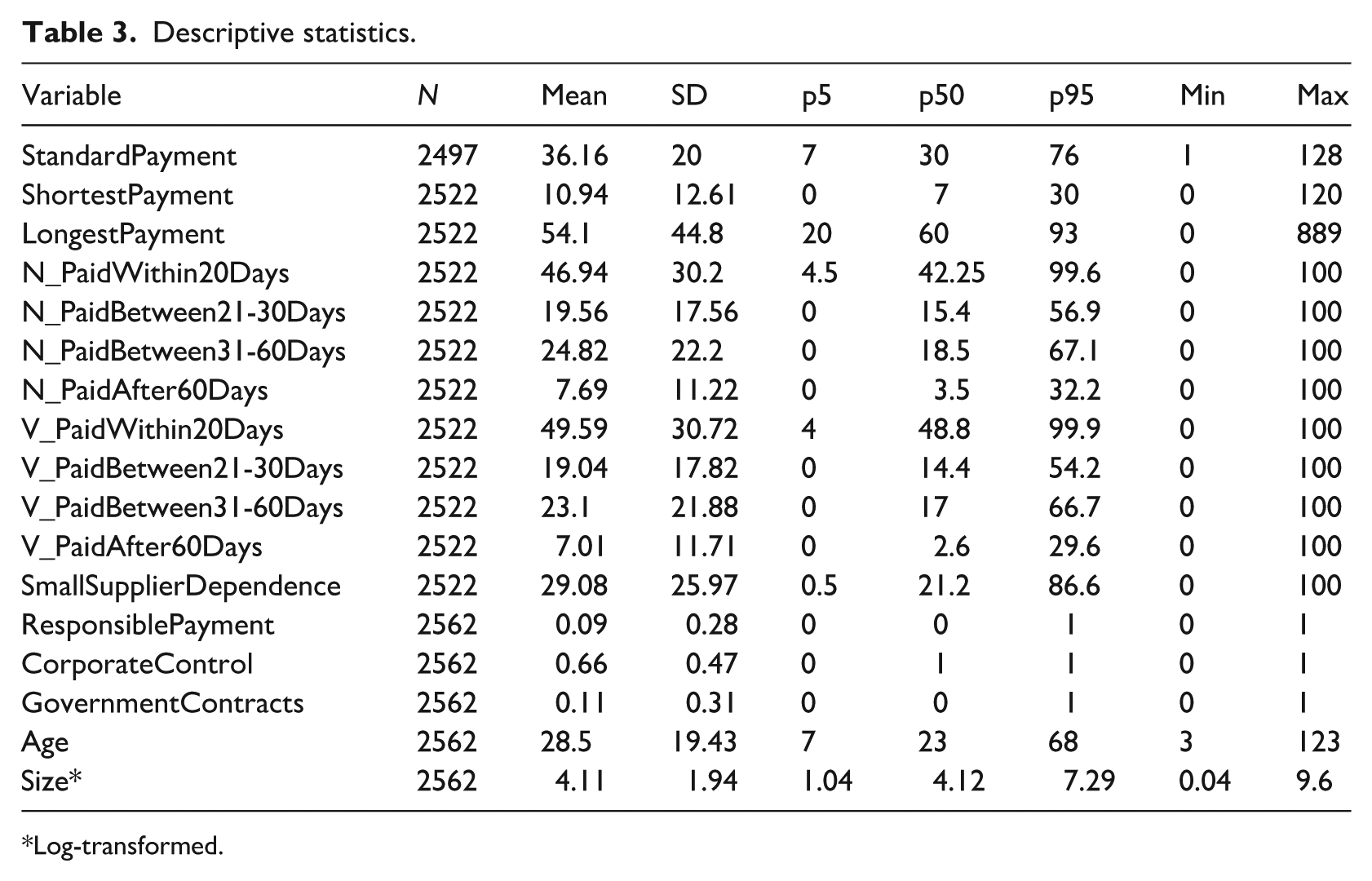

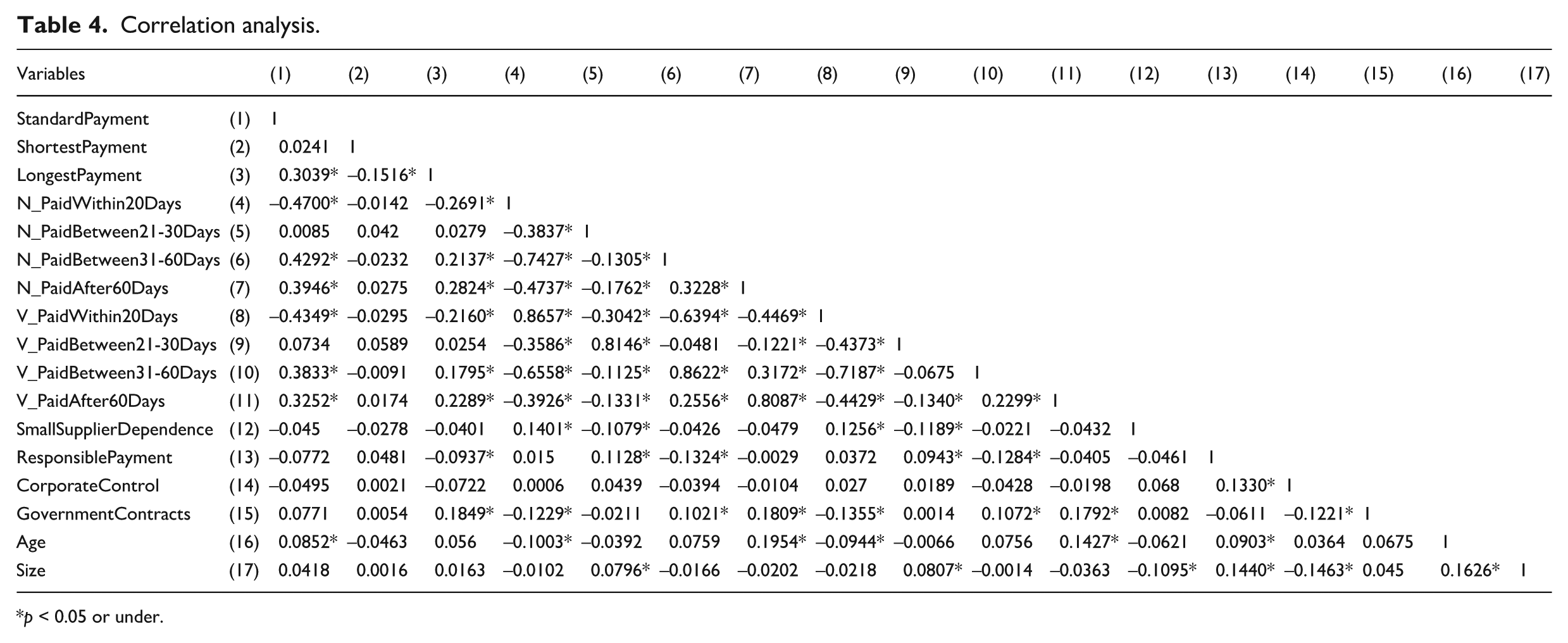

The five independent variables used in this study are firm size, dependence on small suppliers, responsible payment, government contracts and industry. Firm size is measured as total revenue, dependence on small suppliers is measured as the proportion of a firm’s total procurement spend with small suppliers, responsible payment is measured as signatory to the Australian Supplier Payment Code, government contracts is measured as winning an Australian Government contract, and industry is classified according to the Business Industry Codes (BIC) system. Firm size, responsible payment and industry are measured at fixed points in time while dependence on small suppliers and government contracts are measured year-by-year. In addition to the five independent variables, four control variables form part of the analysis. These are firm age, corporate control, location in Australia, and the year in which supplier payments are made. Further information on all variables, including their sources, is contained in Table 2. Descriptive statistics are contained in Table 3 and correlations in Table 4.

Dependent, independent and control variables.

Descriptive statistics.

Log-transformed.

Correlation analysis.

p < 0.05 or under.

4.5. Model specification

To test the determinants of our two dependent variables, we estimate panel data regression models using firm-level data from the PTRS. Our empirical approach is designed to capture both cross-sectional and temporal variations while controlling for unobservable heterogeneity across firms and time. We specify two core equations: one to model payment terms (Equation 1) and another to model payment times (Equation 2). Both models are estimated using multivariate regressions with firm-level panel data, incorporating year fixed effects to control for macroeconomic shocks and policy changes, and industry fixed effects to account for sector-specific payment norms and practices.

The econometric equations are specified below:

where i indexes the sample of firms, t indexes years, and the outcome variable PaymentTerms in Eq. (1) represents three continuous outcome variables (1) standard payment terms (2) shortest payment terms and (3) longest payment terms. The outcome variable PaymentTime in Eq. (2) represents the four dependent variables related to payment times by number or value, as discussed in section 4.3 and listed in Table 2. The independent variables and control variables used in Eq. (1) and Eq. (2) are the same.

Th independent variables of Size, SmallSupplierDependence, ResponsiblePayment and GovernmentContracts are measured by the firm’s revenue, dependence on small suppliers, signatory status with the Australian Supplier Payment Code, and involvement in Australian Government contracts, respectively. CONTROL includes firm age, corporate control, location in Australia, and the year in which supplier payments are made. µt represents year fixed effects, and µi represents industry fixed effects. Year fixed effects account for temporal shocks like the Covid-19 pandemic or macroeconomic changes. Industry fixed effects are used to absorb persistent unobserved differences across sectors. This panel fixed-effects structure helps to mitigate omitted variable bias by controlling for unobservable time-invariant characteristics at industry level and common shocks over time. ɛ represents the error term, with robust standard errors clustered at firm level.

5. Results

5.1. Descriptives

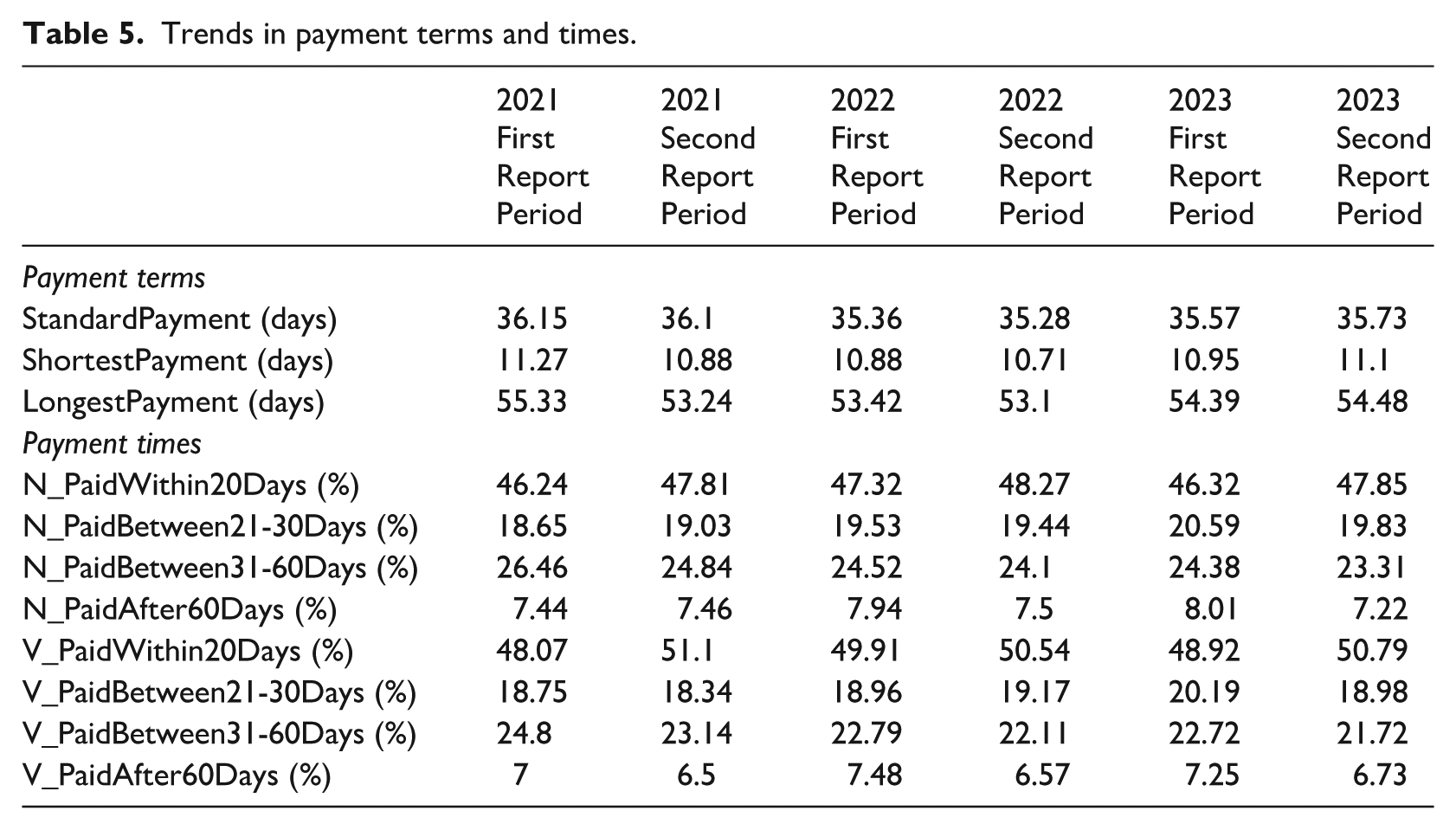

We begin the presentation of results with a description of payment trends (see Table 5). Payment terms for small suppliers improved marginally between 2021 and 2023. Standard terms reduced from 36 days in 2021 to 35 days in 2022 and 2023 while longest terms reduced from 55 days in the first half of 2021 to 53 days in 2022 before climbing to 54 days in 2023. Payment times also showed improvement (see Table 5). Whether measured by number or value, the percentage of invoices paid to small suppliers within 20 days and between 21 and 30 days increased from 2021 onwards. Over 48% of invoices by value were paid within 20 days in the first half of 2021, but this figure had risen to over 50% by the second half of 2023. There was a corresponding decrease in invoices paid between 31 and 60 days while the proportion paid after 60 days remained constant. Notably, the pattern of improvement in payment times is similar irrespective of whether we use number or value of invoices settled.

Trends in payment terms and times.

5.2. Hypotheses testing

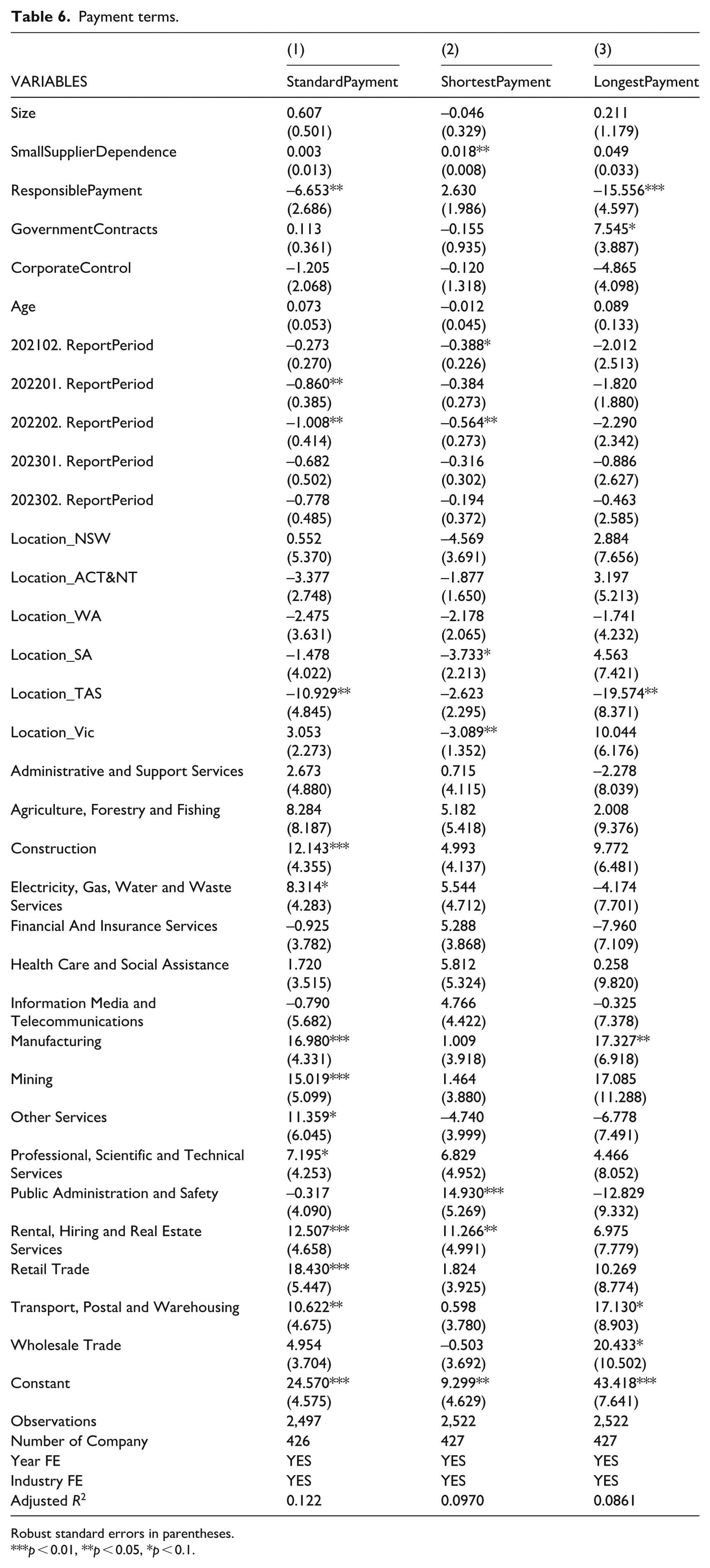

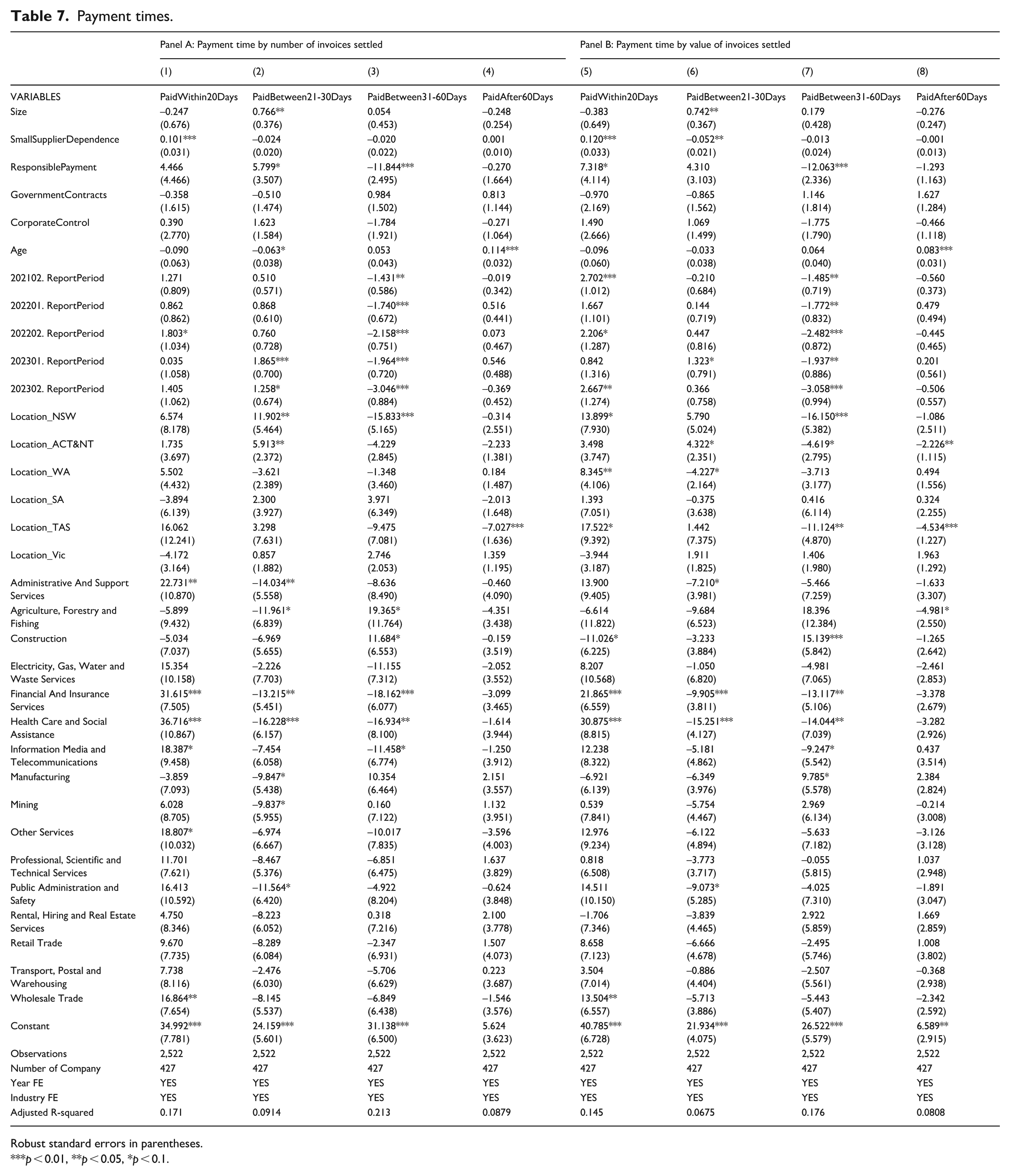

We now turn our attention to the hypotheses. Table 6 contains the results for payment terms and Table 7 contains the results for payment times. The first hypothesis (H1) concerns the relationship between firm size and payments to small suppliers. Larger firms are not found to offer better payment terms, which means H1a is rejected. Larger firms are statistically more likely to pay small suppliers within 21–30 days, measured by number and value of invoices settled (p < .05), which supports H1b. The second hypothesis (H2) is that dependence on small suppliers is associated with better payment terms and times for small suppliers. Firms with high dependence on small suppliers are not statistically more likely to offer better payment terms, which leads to rejection of H2a. In fact, firms with a high dependence on small suppliers have less attractive shortest payment terms (p < .05). A positive significant result in Table 6 means extra calendar days in the payment terms offered to small suppliers, whether they are standard, shortest or longest payment terms. In line with expectations, dependence on small suppliers does increase the probability that firms pay within 20 days (p < .01), measured by both number and value of invoices settled. H2b is therefore accepted.

Payment terms.

Robust standard errors in parentheses.

p < 0.01, **p < 0.05, *p < 0.1.

Payment times.

Robust standard errors in parentheses.

p < 0.01, **p < 0.05, *p < 0.1.

The third hypothesis (H3) is that firms with a commitment to responsible payment have better payment terms and times. Support is returned for this hypothesis. These firms have quicker standard payment terms (p < .05), and their longest payment terms are less than other firms (p < .01). H3a is accepted on this basis. When it comes to payment times, this group is statistically less likely to pay small suppliers after 30 days (p < .01), although the evidence for them paying suppliers within 20 days or between 21 and 30 days is weaker (p < .10). As such, H3b is only partially accepted. The fourth hypothesis (H4) is that firms awarded government contracts have better payment terms and times for small suppliers. Neither contention is statistically supported, leading to rejection of H4a and H4b. If anything, government contracting is associated, albeit weakly, with longer payment terms (p < .10).

The fifth hypothesis (H5) concerns the relationship between industry and supplier payments. A priori, consumer-facing and service industries are predicted to have better payment terms and times compared to manufacturing, construction and primary extractive industries. This proves to be correct. Manufacturing, construction and mining firms have lengthier standard payment terms (p < .01), although surprisingly so do retail and real estate firms (p < .01). In respect of payment times, firms in finance, healthcare and wholesale trade are statistically more likely to pay small suppliers within 20 days (p < .01), measured by number and value of invoices settled, as are firms in administration (p < .05). The opposite holds for construction firms, which are more likely to pay small suppliers after 30 days (p < .01). Manufacturing firms also more likely to pay small suppliers after 30 days, although the statistical effect is weak (p < .10). As the results align with overall predictions, H5a and H5b are accepted.

Finally, it is worth commenting on the control variables. In terms of age, older firms are more likely to pay small suppliers after 60 days (p < .01). This differs from De Carvalho (2015) who found that older firms paid faster, although their study did not distinguish between small and large suppliers. Time period shows a clear pattern of effect. Since the second half of 2021 when pandemic restrictions were relaxed, firms have been less likely to pay small suppliers after 30 days (p < .01), with the effect strengthening year-on-year. The effect of geographic location is mixed. Firms in states like Tasmania and Victoria offer more attractive payment terms while firms in states like New South Wales (NSW) are associated with faster payment times. Even though firms in NSW and Victoria were hardest hit by pandemic restrictions, for example, extended workplace shutdowns and stay-at-home orders (Edwards et al., 2022), this did not adversely affect their payment performance relative to firms in other Australian states and territories.

5.3. Additional analysis

As an additional step in the analysis, we interacted the independent variables with year on the assumption that PTRS should become more impactful over time as suppliers start to use the data disclosures and firms experience greater pressure to demonstrate institutional compliance. The interaction results lend very little support to this assumption (see Tables 8–10, Appendix 1). Only firms with a commitment to responsible payment had reduced their longest payment terms by 2023 (p < .05). Likewise, the effect of the independent variables on payment time did not increase over the three years. The only significant effect was for firm size. Larger firms were more likely to pay small suppliers between 21 and 30 days by 2022, although the effect had reversed by 2023 (p < .05). Thus, the main effects that we find with the independent variables in section 5.2 are not replicated by the interactive effects between these same variables and the year in which supplier payments were made.

5.4. Robustness test

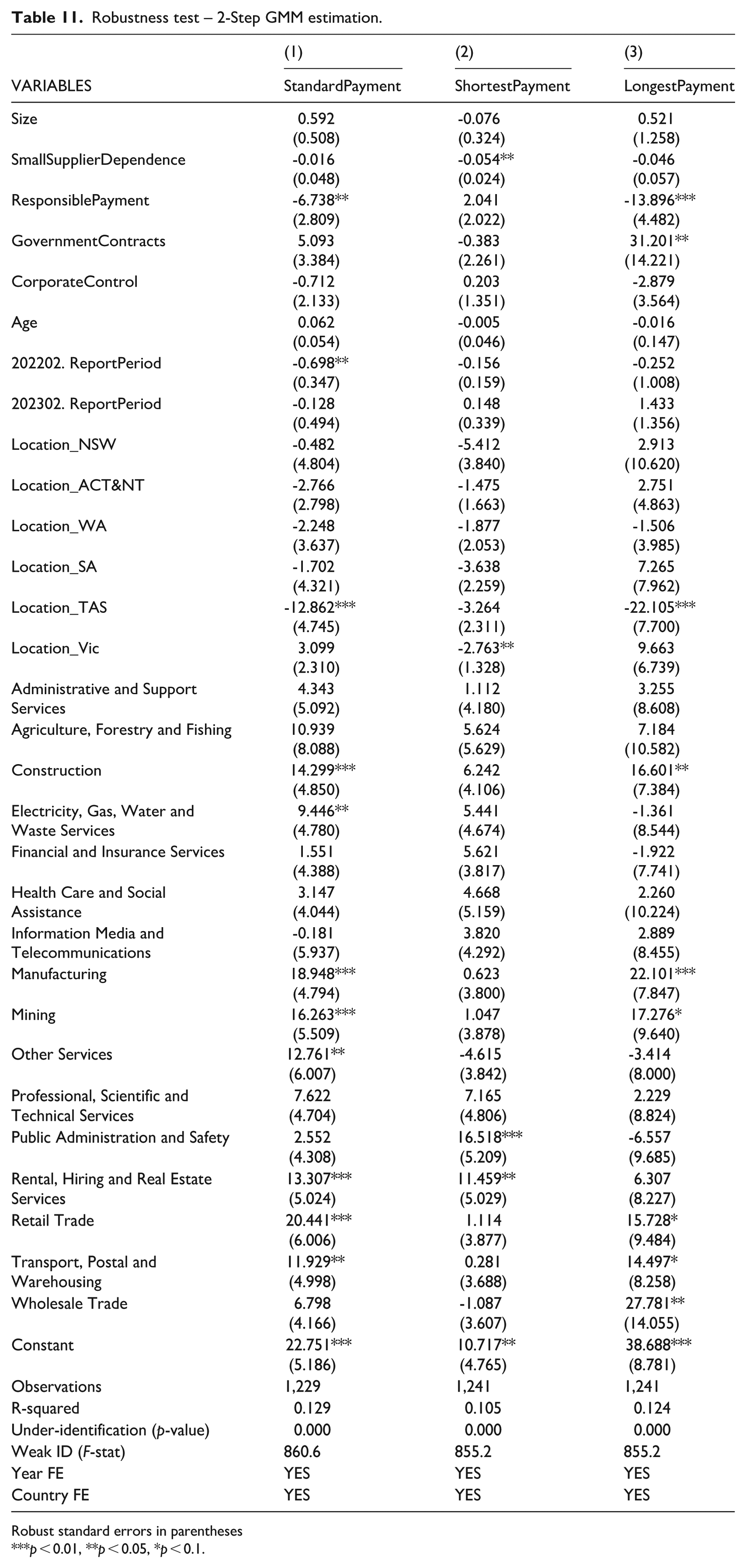

To address potential endogeneity, particularly from reverse causality or omitted variable bias, we implemented robustness tests using the Generalised Method of Moments (GMM) with instrumental variables. GMM estimation, which corrects for heteroskedasticity and allows for efficient use of instrumental variables, is suitable for this context. Specifically, we treat SmallSupplierDependence as potentially endogenous and use its lagged value (L_SmallSupplier) as an instrument. The results are reported in Table 11 in the Appendix 1. The GMM models passed key instrument diagnostic tests. The Kleibergen-Paap LM statistic confirms the model is identified (Chi-square p-value < 0.001). The Cragg-Donald and Kleibergen-Paap F statistics far exceed the Stock–Yogo thresholds, indicating that our instruments are not weak.

The results largely confirm the robustness of our main findings. For example, in the GMM model where StandardPayment is the outcome, the coefficient on SmallSupplierDependence was statistically insignificant (p = 0.745), suggesting no strong causal effect. In the LongestPayment model, the effect of SmallSupplierDependence was also negative but not statistically significant. In addition, the impact of ResponsiblePayment and GovernmentContracts on the dependent variables are similar to the results in Table 6. The only opposing result is for ShortestPayment where the coefficient on SmallSupplierDependence is negative and statistically significant (coef = −0.054, p = 0.023), suggesting that higher dependence on small suppliers is associated with attractive shortest payment terms. While this is consistent with hypothesised predictions, it differs from the result reported in Table 6 where the coefficient was positive and statistically significant.

Taken together, the GMM results support the robustness of our conclusions and strengthen the claim that our variables are not spuriously correlated with payment behaviour due to endogeneity. In further unreported results, we considered treating Size and ResponsiblePayment as endogenous. However, Stat models automatically reclassified Size and ResponsiblePayment as exogenous because their instruments (L_Size, L_RespPay) are co-linear with endogenous variables – meaning they add no new information. This is likely due to insufficient variation or perfect prediction in our sample. We also tested external instruments such as Gross State Product (GSP) and state-level unemployment rates. These economic conditions can influence payment behaviours indirectly by affecting business operations and financial health. Unfortunately, the Kleibergen-Paap F statistics suggest that these external instruments are relatively weak, so they may not be suitable to address endogeneity effectively.

6. Discussion

Supplier payment times has been a long-standing topic of debate, drawing in practitioners (Atradius, 2025a, 2025b) and academics (Barrot and Nanda, 2020; Caniato et al., 2020; Cowton and San-Jose, 2017; Kovach et al., 2023). There has been renewed focus on it of late, driven by payment time disclosure schemes in the United Kingdom and Australia (Australian Government, 2022; UK Government, 2019) and changing attitudes towards responsible procurement and sustainable SCM, especially in the aftermath of the Covid-19 pandemic (Feng et al., 2023; Hu et al., 2023). Against this backdrop, we set out to examine the determinants of payment times to small suppliers in Australia using Oliver’s (1991) predictive framework on institutional compliance. Our study represents one of the first academic attempts to mine PTRS data and sits alongside similar investigations that have been undertaken using UK data (Chuk et al., 2025; Flynn and Li, 2023; Grewal et al., 2024). The results, which are discussed next, help to explain why some firms pay small suppliers faster than others.

6.1. Theoretical confirmation

Several of Oliver’s (1991) predictions about the conditions under which firms satisfy institutional expectations are confirmed in this study. External constituents whom the firm depends on appear to be able to nudge them towards compliance, which is consistent with the arguments of institutional theorists (Campbell, 2007; DiMaggio and Powell, 1983; Oliver, 1991). The results show that firms with a high dependence on small suppliers are more likely to settle invoices within 20 days. We surmise that representations made by small suppliers and their supporters like industry associations cause firms to accept their need for prompt payment. Put slightly differently, the firm is asked to be responsive to the constrained financial circumstances of its average supplier. The advent of disclosure legislation designed to empower small suppliers has made responsiveness more salient. Grewal et al. (2024), for example, found that small suppliers in the United Kingdom are using data disclosures to negotiate better payment terms with existing customers and identify new customers. It stands to reason that firms dependent on small suppliers are more impacted by these developments and will adjust their payment practices accordingly.

The study also finds that firms are more likely to meet institutional expectations when they are consistent with organisational goals and do not constrain operational decision-making, as theorised by Meyer and Rowan (1977) and Oliver (1991). Specifically, it finds that firms with a commitment to responsible payment, proxied through membership of the Australian Supplier Payment Code, offer better terms to small suppliers and pay them faster. This is because institutional expectations over timely payment complement rather than contradict their organisational goals and working capital strategies. The economic cost of institutional compliance for this category of firms is negligible. Similar results to ours have been returned by Flynn and Li (2023) and Chuk et al. (2025) on how complementarity between institutional expectations and commitments to responsible payment leads to faster invoice settlement. Firms without a commitment to responsible payment have reason to view institutional expectations over timely payment with scepticism. For them, compliance means bringing supplier payments forward, with implications for their cash flow position. This can cause misgivings over the appropriateness of institutional expectations and an increased likelihood of resistance (Meyer and Rowan, 1977; Oliver, 1991), as our findings indicate.

The environmental context in which institutional pressures play out also matters for compliance. As Oliver (1991) observed, the characteristics of the environment, including its level of uncertainty and interconnectedness, have a bearing on firms’ ability to conform to institutional norms. This observation is borne out in our study by how firms in different industries manage supplier payments. Industries like manufacturing and construction that are characterised by lengthy DSO, complex supply chain configurations and a reliance on the re-sale of supplier inputs have less attractive payment terms and take longer to settle invoices. Environmental context constrains their ability to satisfy institutional expectations over prompt payment to small suppliers. Other industries like finance, services and wholesale trade do not experience the same constraints, and this is reflected in better payment terms and earlier payments. Our results about industry effects on supplier payment times are supported by previous academic and practitioner research (Australian Small Business & Family Enterprise Ombudsman, 2019; Bolton et al., 2022; Lorentz et al., 2016).

Institutional exposure is also related to compliance. All firms are exposed to institutional pressures over timely payments, but larger firms with an established market presence and public profile have greater exposure (Grewal et al., 2020). Greater exposure, in turn, raises the social legitimacy stakes, thereby inducing corporate compliance (Oliver, 1991). This is what our study finds, with larger firms statistically more likely to pay between 21 and 30 days. Institutional control, however, is not found to have any effect on payment terms or times. Based on what is known about corporate customers pressuring firms to embrace sustainable procurement practices (Hoejmose et al., 2014b; Kauppi and Hannibal, 2017), we predicted that firms involved in public contracting would experience coercive control from the government – sometimes contractually enforced – to practise responsible payment. The lack of an observed effect could be because government contracts do not constitute a big enough share of revenue among the firms in our sample to alter average payment times. Alternatively, the problem may be methodological in that our measure of government contracts is too blunt to detect any effect.

6.2. Scholarly contributions

By testing variables like dependence on small suppliers and involvement in government contracting, this article extends earlier research into the determinants of payment times that has its antecedents in the finance and accounting literature (De Carvalho, 2015; Howorth and Reber, 2003; Lorentz et al., 2016; Paul and Boden, 2011; Peel et al., 2000). It is also notable for tracking payment terms and times over 3 consecutive years, thus strengthening the robustness of the findings and controlling for economic volatility during and after the Covid-19 pandemic. Interestingly, the interaction tests show that the influence of the independent variables on payment performance did not increase as the PTRS bedded down between 2021 and 2023. The study’s use of data from Australian firms is novel and expands the range of institutional contexts in which supplier payment times is examined. So is its exclusive focus on small suppliers – the enterprise cohort most impacted by payment delays. Comparable studies by Grewal et al. (2020), Flynn and Li (2023) and Chuk et al. (2025) do not distinguish between different sized suppliers in their analyses of payment times.

The study also brings much needed theoretical grounding to research on supplier payment times through its deployment of institutional theory generally (DiMaggio and Powell, 1983; Dowling and Pfeffer, 1975; Meyer and Rowan, 1977) and Oliver’s (1991) framework for predicting institutional compliance specifically. This is significant in two respects. First, it provides a coherent explanation for why firms are more likely to offer small suppliers favourable payment terms and settle invoices promptly. Foregoing studies on this subject lacked unifying theoretical frameworks (e.g. Howorth and Reber, 2003; Paul and Boden, 2011; Peel et al., 2000). Second, it connects supplier payments to other facets of sustainable SCM that are known to be institutionally determined. Of particular relevance here are several Australian studies that have examined the emergence of socially responsible procurement through the lens of regulative, normative and mimetic institutional pressures (Grob and Benn, 2014; Young et al., 2015; Lau et al., 2023). By recognising commonalities between the institutional drivers of supplier payment times and responsible procurement practices we can begin to situate the former in its wider research and practitioner context.

6.3. Managerial and policy implications

This study contains several implications for practice. First, firms should monitor their payment performance against peers and take corrective action as necessary. Given that payment data is now in the public domain, the risks of not being competitive include loss of preferred customer status with small suppliers and reputational damage with regulators, investors and customers. There are signs that firms are taking heed by, for instance, greater investment in e-invoicing technologies to expedite payment and regular communication with suppliers (Grewal et al., 2024). Second, firms should be aware that supplier selection decisions increasingly have implications for payment practices. Payment legislation like Australia’s PTRS (Australian Government, 2022) and multi-stakeholder initiatives like the Fair Payment Code (Small Business Commissioner, n.d.) prioritise small firms, thus placing firms who work with them under added obligation to settle invoices quickly. While the commercial and CSR rationales for partnering with small suppliers are strong (Federation of Small Business, 2017; Kovach et al., 2023), firms should be mindful of institutional expectations to pay them faster than medium or large suppliers.

A third implication concerns external payment codes. Signatories to Australia’s Supplier Payment Code in this study offered better terms to small suppliers and paid them faster. This suggests a way forward for managers who want to improve their payment performance but are unsure where to begin. The advantage of external codes is that they signpost firms towards best practice and establish performance targets to be achieved, which is what some firms need to motivate a change in behaviour (Perez-Batres et al., 2012). Committing to payment codes is not cost free, admittedly, as firms lose some discretion over when they pay suppliers, especially small suppliers (Flynn and Li, 2023). This has consequences for working capital management, which is why the benefits and drawbacks of payment codes need to be carefully evaluated.

Australian policymakers are advised to further explore how government procurement can be used as a lever to bring about improvements in the payment times of major contractors. While our study could find no evidence that firms with Australian government contracts had better payment performance, public procurement undoubtedly has a role to play. In practical terms, public buyers could be instructed to use a firm’s record on supplier payment times as part of the qualification process for higher value contracts, as happens in the (UK Cabinet Office, 2023). Finally, there is scope for policymakers or civic society organisations to increase firms’ exposure on payment times by publishing league tables based on their performance. Good Business Pays produces an annual list of the fastest and slowest paying companies sector-by-sector in the United Kingdom (Good Business Pays, n.d.), which could serve as a template for Australia.

6.4. Research limitations and future research directions

This article has limitations, which we acknowledge. Our operationalisation of Oliver’s (1991) predictive framework on institutional compliance is not exhaustive, mainly due to difficulties in obtaining valid measures of variables for the sample of firms. Ideally, we would like to have measured internal as well as external pressuring constituents, for example, board of directors, and cultural-cognitive as well as coercive control mechanisms, for example, firms’ embeddedness in professional networks. These are model specification considerations for future research. We were also unable to assign firms to one of the five strategic response categories that Oliver (1991) identifies – acquiescence, compromise, avoidance, defiance and manipulation – because the payment data did not lend itself to objective categorisation. Since 2024 the PTRS requires firms to submit new data indicators on payment times, which may allow the type of categorisation that Oliver (1991) envisaged. We encourage researchers to explore possibilities in this regard.

Another limitation is that our analysis of payment practices starts in 2021, which was during the Covid-19 pandemic. PTRS data for Australian firms pre-Covid is not available, which makes comparison between the two time periods impossible. By contrast, research into the predictors of supplier payment times in the United Kingdom has compared pre- and post-pandemic time periods, with interesting results furnished by Flynn and Li (2023). Finally, the study did not collect qualitative data to supplement its panel data set, which deprives it of a certain depth and richness. Interviewing senior management across procurement and finance departments to explore the ‘how’ and ‘why’ of their responses to institutional pressures for prompt payment to small suppliers therefore presents itself as a future research opportunity.

6.5 Research summation

Not receiving payment on time is a recurring problem for small suppliers, who often struggle to enforce trade credit terms with corporate customers (Cowton and San-Jose, 2017). Institutional stakeholders have redoubled their efforts of late to hold large firms to account and challenge a culture of late payment; efforts that have become more important in the current period of relatively high inflation, interest rates and trade barriers (Atradius, 2025a, 2025b). This study provides theoretically grounded insights into why firms are responding to institutional pressures over prompt payment to small suppliers. The starting assumption was that organisational responses in this situation are behaviours to be predicted, not pre-determined outcomes of institutional processes (Oliver, 1991). The results support this assumption. Dependency on small suppliers, consistency of institutional expectations with existing commitments on responsible payment, institutional exposure and industrial context are among the factors that explain why some firms offer better payment terms and pay small suppliers faster than others. Overall, our study adds to the growing body of contemporary scholarship on this subject (Barrot and Nanda, 2020; Grewal et al., 2024; Walker and Hyndman, 2025) and provides the basis for further research on a critical aspect of business operations.

Footnotes

Appendix 1

Robustness test – 2-Step GMM estimation.

| VARIABLES | (1) | (2) | (3) |

|---|---|---|---|

| StandardPayment | ShortestPayment | LongestPayment | |

| Size | 0.592 (0.508) |

-0.076 (0.324) |

0.521 (1.258) |

| SmallSupplierDependence | -0.016 (0.048) |

-0.054**

(0.024) |

-0.046 (0.057) |

| ResponsiblePayment | -6.738**

(2.809) |

2.041 (2.022) |

-13.896***

(4.482) |

| GovernmentContracts | 5.093 (3.384) |

-0.383 (2.261) |

31.201**

(14.221) |

| CorporateControl | -0.712 (2.133) |

0.203 (1.351) |

-2.879 (3.564) |

| Age | 0.062 (0.054) |

-0.005 (0.046) |

-0.016 (0.147) |

| 202202. ReportPeriod | -0.698**

(0.347) |

-0.156 (0.159) |

-0.252 (1.008) |

| 202302. ReportPeriod | -0.128 (0.494) |

0.148 (0.339) |

1.433 (1.356) |

| Location_NSW | -0.482 (4.804) |

-5.412 (3.840) |

2.913 (10.620) |

| Location_ACT&NT | -2.766 (2.798) |

-1.475 (1.663) |

2.751 (4.863) |

| Location_WA | -2.248 (3.637) |

-1.877 (2.053) |

-1.506 (3.985) |

| Location_SA | -1.702 (4.321) |

-3.638 (2.259) |

7.265 (7.962) |

| Location_TAS | -12.862***

(4.745) |

-3.264 (2.311) |

-22.105***

(7.700) |

| Location_Vic | 3.099 (2.310) |

-2.763**

(1.328) |

9.663 (6.739) |

| Administrative and Support Services | 4.343 (5.092) |

1.112 (4.180) |

3.255 (8.608) |

| Agriculture, Forestry and Fishing | 10.939 (8.088) |

5.624 (5.629) |

7.184 (10.582) |

| Construction | 14.299***

(4.850) |

6.242 (4.106) |

16.601**

(7.384) |

| Electricity, Gas, Water and Waste Services | 9.446**

(4.780) |

5.441 (4.674) |

-1.361 (8.544) |

| Financial and Insurance Services | 1.551 (4.388) |

5.621 (3.817) |

-1.922 (7.741) |

| Health Care and Social Assistance | 3.147 (4.044) |

4.668 (5.159) |

2.260 (10.224) |

| Information Media and Telecommunications | -0.181 (5.937) |

3.820 (4.292) |

2.889 (8.455) |

| Manufacturing | 18.948***

(4.794) |

0.623 (3.800) |

22.101***

(7.847) |

| Mining | 16.263***

(5.509) |

1.047 (3.878) |

17.276*

(9.640) |

| Other Services | 12.761**

(6.007) |

-4.615 (3.842) |

-3.414 (8.000) |

| Professional, Scientific and Technical Services | 7.622 (4.704) |

7.165 (4.806) |

2.229 (8.824) |

| Public Administration and Safety | 2.552 (4.308) |

16.518***

(5.209) |

-6.557 (9.685) |

| Rental, Hiring and Real Estate Services | 13.307***

(5.024) |

11.459**

(5.029) |

6.307 (8.227) |

| Retail Trade | 20.441***

(6.006) |

1.114 (3.877) |

15.728*

(9.484) |

| Transport, Postal and Warehousing | 11.929**

(4.998) |

0.281 (3.688) |

14.497*

(8.258) |

| Wholesale Trade | 6.798 (4.166) |

-1.087 (3.607) |

27.781**

(14.055) |

| Constant | 22.751***

(5.186) |

10.717**

(4.765) |

38.688***

(8.781) |

| Observations | 1,229 | 1,241 | 1,241 |

| R-squared | 0.129 | 0.105 | 0.124 |

| Under-identification (p-value) | 0.000 | 0.000 | 0.000 |

| Weak ID (F-stat) | 860.6 | 855.2 | 855.2 |

| Year FE | YES | YES | YES |

| Country FE | YES | YES | YES |

Robust standard errors in parentheses

p < 0.01, **p < 0.05, *p < 0.1.

Acknowledgements

We, the authors, would like to extend our thanks to the two anonymous reviewers who provided constructive feedback on the original submission and highlighted areas for improvement. We would also like to thank the Associate Editor, Yaowen Shan, for handling our paper.

Final transcript accepted on 19 August 2025 by Yaowen Shan (AE Accounting).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

1.

The PTRS defines small firms as generating less than AUS $10M in annual revenue.

2.

Consumer price inflation (CPI) in Australia went from approximately 1% in January 2021 to 8.5% in December 2022, before falling back to 3.5% by the end of 2023. To control inflation, the Reserve Bank of Australia increased interest rates from 0.10% in December 2021 to 3.1% by the end of 2022 and 4.35% by the end of 2023.

3.

Firms are able to check if suppliers are ‘small’ by using the Small Business Identification (SBI) Tool, which is available through the Payment Times Reporting Portal.