Abstract

This scoping review examines the job demands and resources impacting financial advisers through the lens of the Job Demands-Resources (JD-R) model. Given the significant challenges facing financial advisers, this review identifies key factors contributing to job stress, satisfaction and turnover in the profession. A comprehensive desktop review and thematic analysis of 53 peer-reviewed articles revealed core job demands such as compliance, emotional strain, and work overload, alongside critical job resources like professional development, support and technology. In addition, personal resources, including self-efficacy and optimism, are explored as potential moderators. The findings offer insights into the complex dynamics within the financial advisory industry, providing a foundation for future studies that may look to enhance job satisfaction and retention.

Keywords

1. Introduction

The provision of professional financial advice is critical in enhancing not only retirement planning and savings but also broader financial well-being (Bowerman, 2021). Financial advisers play a pivotal role globally, equipping individuals with strategies to build substantial savings, secure financial independence, and reduce reliance on public systems, thus bolstering macroeconomic stability (Behrman et al., 2012).

Informed planning enabled by financial advisers not only addresses industry challenges but also promotes psychological well-being by mitigating the stress of fiscal unpredictability (Behrman et al., 2012).

By helping individuals make better financial decisions, advisers contribute to a more stable and resilient economy. They play a critical role in educating clients about financial literacy, encouraging responsible financial behaviour and fostering a culture of saving and investing. The benefits of professional financial guidance extend beyond individuals to the wider socio-economic fabric. Financial advisers help ensure that households are better prepared for economic uncertainties, leading to more stable consumer spending and less strain on public welfare systems. This, in turn, supports economic growth and stability. Studies have accentuated the synergy between financial literacy and professional advice, suggesting a collective enhancement of financial decision-making and preparation for economic uncertainties (Collins, 2012; Robb et al., 2012).

In Australia, financial advisers are instrumental in navigating the complexities of the superannuation system and providing guidance on investments, tax planning and debt management. Similarly, in the United Kingdom, financial advisers help clients manage a range of financial products, including pensions, investments, mortgages and insurance, offering tailored advice to optimise financial outcomes. In the United States, advisers assist with diverse investment portfolios, retirement accounts like 401(k) plans and Individual Retirement Arrangements (IRAs), tax planning, estate planning and managing student loans. While the regulatory frameworks differ across these countries, the core objective remains the same: to help clients achieve comprehensive financial security.

Australia’s financial advisory industry has recently experienced a stark decline in practitioner numbers, from 29,000 in 2019 to 16,000 in 2023 (Rainmaker Information, 2024).

Accompanying this downward trend is a 41% increase in the median cost of financial advice since 2018, raising concerns about the accessibility and affordability of financial planning for the average Australian (Adviser Ratings, 2022).

In Asia, financial adviser markets exhibit unique dynamics. China has seen a remarkable growth in financial planning certifications, with the Financial Planning Standards Board (2024) noting a 15% increase in Certified Financial Planners (CFPs) to nearly 35,000 by the end of 2023, making it second only to the United States. China has been pivotal in reshaping global financial services through the rapid digitisation of its economy. According to the People’s Bank of China, over 85% of retail payments in 2023 were conducted via mobile payment platforms such as Alipay and WeChat Pay (FIS Global, 2023; Pak, 2024). Thailand also experienced a significant 27.8% increase in its CFP population, although it remains smaller in scale with just 593 professionals. While the United States still dominates the global CFP industry with around 99,000 CFPs, Asia has emerged as the fastest-growing region for new certifications. This expansion aligns with projections from an August 2023 Boston Consulting Group study, which anticipates personal financial assets in the Asia-Pacific market to rise by an average of 7.8% annually over the next 5 years, outpacing the global average of 5.3%. In contrast, Japan’s financial advisory market is relatively mature, with around 27,000 registered financial planners, and faces the challenge of catering to a rapidly ageing population, resulting in a focus on retirement planning and wealth preservation strategies (Financial Planning Standards Board, 2024).

In the United Kingdom, recent data from the Financial Conduct Authority revealed a notable decline in the number of financial advice firms, falling by 7% from 6240 in August 2022 to 5805 in February 2024 (Austin, 2024). This reduction, attributed to consolidation and the lingering effects of the COVID-19 pandemic, has raised concerns about the impact on the industry.

Despite this, the number of financial advisers has remained relatively stable, suggesting that advisers are increasingly operating under larger networks or firms to benefit from scale, support, and compliance efficiencies.

In the United States, the financial advisor industry faces its own challenges. According to Cerulli (2023), the number of advisers grew by just 2706 in 2022, barely offsetting trainee failures and retirements. Over the next decade, 109,093 advisers are expected to retire, comprising 37.5% of the industry headcount and 41.5% of total assets (Cerulli, 2023). The attrition rate among new entrants’ hovers around 72%, emphasising the critical need for the industry to attract and retain talent. Professional networking and referrals play a crucial role, with nearly one-third of new advisers being referred by a personal contact (Mseka, 2024).

Compounding these challenges are the evolving demands of financial advisers (Dubofsky and Sussman, 2009; Fox and Bartholomae, 2020). Advisers often help clients with issues such as death, family dysfunctions, divorce, illness and depression (Dubofsky and Sussman, 2009).

Despite aiding up to 40% of clients presenting with these issues, financial advisers report having no training or professional development in these areas (e.g. Dubofsky and Sussman, 2009). It remains unclear how these (and other) shifting demands contribute to job satisfaction and retention and conversely, burnout and turnover in this profession. The Job Demands-Resources (JD-R) Model is one framework through which to explore these dynamics further.

1.1. The JD-R model

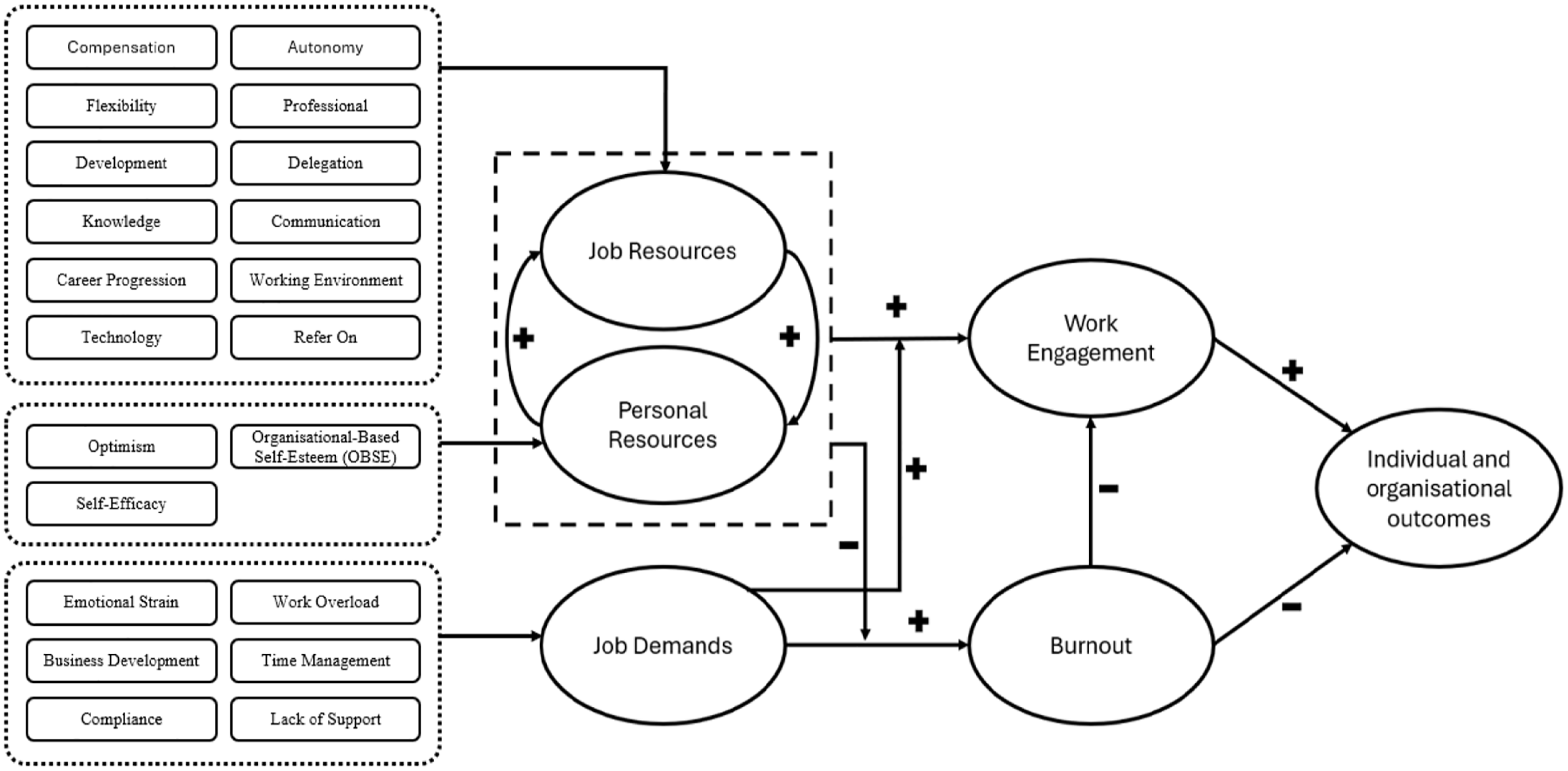

The JD-R model (Demerouti et al., 2014) is influential within organisational psychology and business management as it attempts to stipulate how job characteristics influence employee well-being and organisational outcomes (Demerouti et al., 2001). The model posits that every occupation has specific risk factors associated with job stress and motivation, which can be categorised broadly into two groups: job demands and job resources (Bakker and Demerouti, 2007; Van Den Tooren and De Jonge, 2008).

Job demands are those physical, psychological, social or organisational aspects of a job that require sustained effort and are therefore associated with certain physiological and psychological costs (Bakker et al., 2003; Hu et al., 2011). Conversely, job resources refer to those physical, psychological, social or organisational aspects of a job that help achieve work goals, reduce job demands, and stimulate personal growth, learning and development (Bakker et al., 2003).

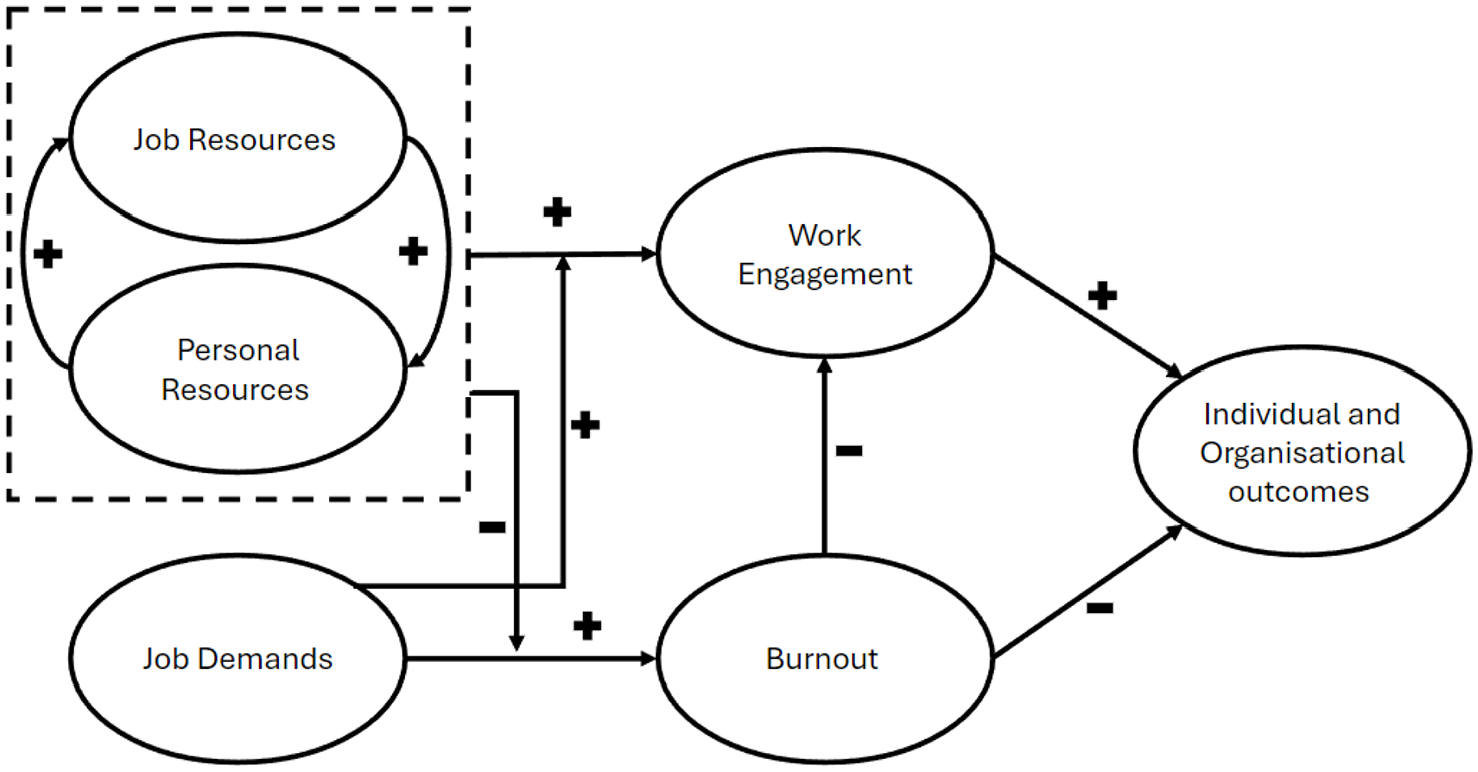

Personal resources are described as aspects of the self, linked to resiliency, reflecting an individual’s sense of control and ability to impact their environment successfully (Hobfoll et al., 2003). The JD-R model (Bakker and Demerouti, 2007) includes three key personal resources: self-efficacy, which refers to individuals’ perceptions of their ability to meet demands across various contexts (Chen et al., 2001); organisational-based self-esteem (OBSE), defined as the degree to which organisational members believe that they can satisfy their needs through their roles within the organisation (Pierce et al., 1989); and optimism, the tendency to expect positive outcomes in life, which enhances the propensity to take action and deal with threats (Aspinwall and Taylor, 1997; Scheier and Carver, 1985). Taken together, these personal resources are viewed as key psychological characteristics that help individuals manage job demands and utilise job resources effectively; they play a moderating role in the relationship between job demands, job resources and various work outcomes (see Figure 1).

Job Demands-Resources (JD-R) model (Bakker and Demerouti, 2007).

The JD-R model is appropriate for examining the reasons behind the current global industry decline in advisers because it specifically recognises the potential interactions between demands and resources (Currie and Hill, 2012; Duvall and Andrews, 2010). The mediating factors of strain and motivation within the model are particularly pertinent (e.g. Broetje et al., 2020). Heightened job demands without commensurate job resources lead to strain – a state of exhaustion that can culminate in burnout and job exit (Bakker et al., 2003). Meanwhile, motivation as a moderator operates through the available job resources, which in the case of financial advisers, may have been eroded by the factors mentioned (Bakker et al., 2003).

The JD-R model posits that organisational commitment and job performance are key outcomes influenced by both job demands and job resources. As demands on advisers increase, there is a risk that these heightened demands could lead to burnout, reduced commitment, and lower job performance. However, by leveraging appropriate job resources – such as support, development opportunities, and recognition – it is possible to enhance organisational commitment and job performance even under increased demands. This approach does not imply that outcomes remain unchanged; rather, it suggests that the negative impact of increased demands can be offset through targeted strategies. By focusing on improving these outcomes, the JD-R model provides a pathway to stabilising the workforce, despite the challenges faced by advisers (Broetje et al., 2020).

The JD-R model has been researched in other industries with similar turnover rates to financial advisers (16%; Adviser Ratings, 2022), such as nursing (15.1%; Hayes et al., 2012). Literature citing the JD-R model in this context highlights work overload, lack of formal rewards, and work–life interference as the main demands for nurses. Such demands have been associated with negative health outcomes (Thapa et al., 2022), emotional exhaustion, and burnout (Burke and Hung, 2015; Lee et al., 2015). Resources for nurses include autonomy, interpersonal relationships, authentic management, transformational leadership, job-crafting and professional resources (Broetje et al., 2020; Castner, 2019). Like nursing, financial advisers face high job demands, such as increased regulatory scrutiny, work overload, and the emotional toll of managing clients’ financial well-being. These demands, coupled with insufficient resources such as limited professional development opportunities and lack of adequate formal rewards, may contribute to emotional exhaustion, burnout and, ultimately, turnover. Understanding the interplay of these demands and resources through the JD-R model can provide valuable insights into addressing the ongoing adviser shortage in Australia.

1.2. Objectives of the current study

To the authors’ knowledge, no existing review examines the job demands and resources impacting financial advisers. The current review aims to address this gap in the literature by systematically examining peer-reviewed articles on the job demands and resources impacting financial advisers, with the aim of identifying key factors contributing to job stress and satisfaction in the profession. Utilising and extending the JD-R model, this study offers greater granularity and nuance in understanding the drivers of job satisfaction and turnover, contributing to the broader theoretical and evidence base of the JD-R model. Through this analysis, the authors seek to elucidate the complex dynamics within the financial advisory industry and provide insights that inform strategies to mitigate challenges faced by financial advisers. In addition, while the primary focus is on job demands and resources, personal resources will be considered as a secondary factor for their potential to moderate the relationships between resources and demands. This work provides a template for applying the JD-R model to other industries and contexts.

The authors will use a structured ‘top-down’ framework for analysis by investigating a predetermined set of job resources and demands specific to financial advisers based on a desktop review. A desktop review is a research method that involves gathering and analysing existing information from various secondary sources such as academic literature, industry reports, organisational documents, and online databases (Shanthasiri Thero, 2023).

In this study, the authors conducted a comprehensive desktop review to identify the key job demands and resources relevant to financial advisers. By reviewing a wide range of sources, including academic articles on occupational stress, industry reports on financial advisory practices, and O*NET online (an online database that outlines job roles and responsibilities), the authors compiled a comprehensive list of job demands and resources. The identified job demands include compliance, emotional strain, lack of support, work overload, business development, and time management challenges. On the contrary, the job resources highlighted are flexibility, delegation, professional development opportunities, knowledge, career progression, effective communication, a supportive working environment, the ability to refer clients when necessary, compensation and technology. In addition, the personal resources crucial for financial advisers were identified, such as self-efficacy, OBSE, and optimism. A list of definitions for each demand and resource is included in the Supplementary Materials, Appendix A.

2. Methods

This study followed the Preferred Reporting Items for Scoping Reviews (Moher et al., 2015) guidelines to categorise job demands and resources experienced by financial advisers. Given the diverse and scattered nature of the existing research on this subject, a scoping review was deemed suitable. A scoping review allows for a structured synthesis of the literature, ensuring a comprehensive understanding of the topic by evaluating the quality and relevance of the available studies. This approach, which can range from broad to detailed (Munn et al., 2018), is particularly beneficial for scrutinising nascent evidence when further specific research questions are undefined. The review aimed to identify and map available evidence, elucidate key concepts and categorise the current job demands and resources. The scope of the review is not restricted by the year of publication and comprises peer-reviewed articles addressing financial advisers’ job demands and resources.

2.1. Protocol

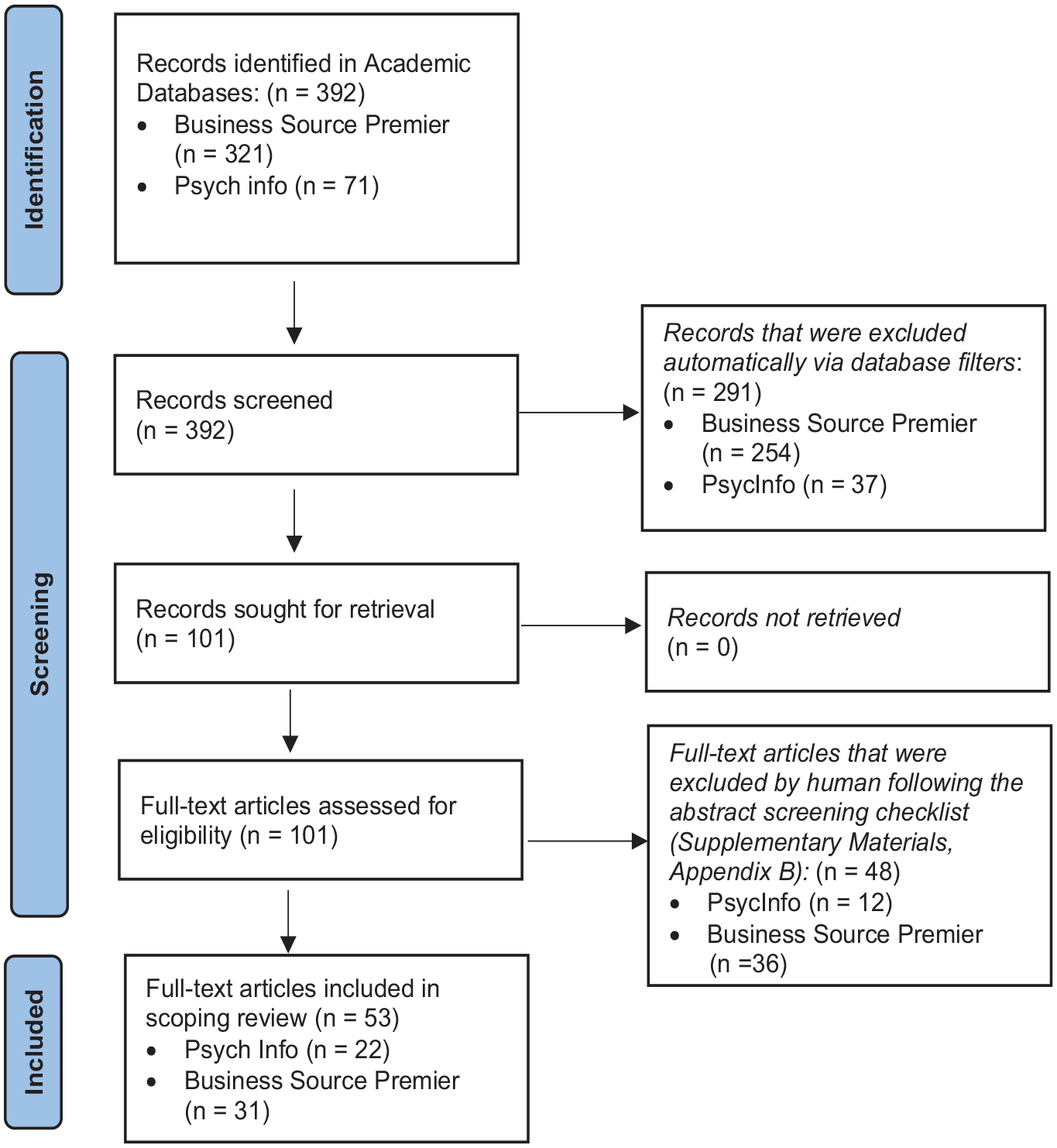

The PRISMA protocol, checklist and statement were used (Moher et al., 2015) (refer to Figure 2). The search was conducted in September to October 2022. This search was replicated in March 2023. Scoping reviews enable the synthesis of a line of research and development by accessing a breadth of data sources and eliminating non-relevant material using post hoc criteria. The application of that process within the current review is described below.

PRISMA flowchart for study selection.

2.2. Eligibility criteria

The following eligibility criteria for this scoping review were designed to provide clear guidance for the selection of relevant articles:

Use of Search Terms. A comprehensive search strategy was implemented, encompassing terms related to ‘financial adviser*’. Terms such as ‘demand’ or ‘job demand’ were not used due to their tendency to refer to the demand for talent or service provision, rather than the demands placed on financial professionals.

Exclusion of Client Satisfaction. Articles primarily focused on client satisfaction were deliberately excluded from the search (N = 6). The primary objective of this review was to explore job satisfaction and stress among financial advisers.

Date Restrictions. No limitations pertaining to the publication date were imposed during the search process. This approach aimed to ensure inclusivity, considering the limited availability of peer-reviewed literature on the subject matter, which was uncovered during the desktop review.

Geographic Inclusivity. The search was conducted without any geographical restrictions. This decision aligned with similar reviews (Tummers and Bakker, 2021) using the JD-R model, which has validity across geographical boundaries (Tummers and Bakker, 2021). Only peer-reviewed papers in English were included.

To ensure a comprehensive analysis, articles discussing the ‘financial services’ industry were included if they broadly addressed the role of financial advisers, advisers or planners, particularly after the initial abstract screening. It is important to clarify that the inclusion criteria were specifically focused on those providing financial advice, targeting articles that explored the experiences, practices and challenges faced by financial planners as a professional group. This approach allowed for a more precise understanding of the population of financial planners within the broader financial services context.

2.3. Information sources

The use of two or more databases decreased the risk of missing relevant studies (Ewald et al., 2022). The search for this scoping review was conducted using two high-quality databases: Business Source Premier (BSP) and PsycInfo. The selection aimed to balance efficiency with comprehensiveness. BSP was chosen for its extensive coverage of peer-reviewed articles in business and management, while PsycInfo was selected for its comprehensive indexing of psychology literature. Together, these databases provide a robust foundation for capturing relevant interdisciplinary research.

2.4. Search terms

Boolean phrases/terms were used, and the syntax was as follows: (‘financ* planner*’ OR ‘financ* advis*’) AND (Employ* OR job* OR occupation* OR workplace*) AND (stress* OR satisf* OR burnout OR ‘burn out’ OR turnover OR ‘turn over’). To ensure the validity and reliability of the search terms, the search process was independently replicated by an Organisational Psychologist at Macquarie University, a librarian at Macquarie University, and an industry expert, the Group Risk Manager at an ASX-listed company. There were no differences in the search results on each separate occasion. While terms such as exhaustion, mental health and well-being are indeed relevant, they were not included in our initial search strategy to maintain a focused scope. Our goal was to target studies that specifically address job-related outcomes and their impact on financial planners and advisers. Including broader terms like mental health and well-being could have yielded a wider range of results that may not be directly relevant to our specific research questions. A total of 392 articles were identified from BSP (N = 321) and PsycInfo (N = 71) in the search results (see Figure 2).

2.5. Screening

The databases automatically excluded 291 articles based on duplicate results (N = 36), non-English language articles (N = 4), and articles that were not classified as peer review (N = 251) based on the addition of filters in the search parameters. This resulted in a data set of 101 studies that were subject to human abstract screening. The decision to include only peer-reviewed articles in this review was made to ensure the highest possible standard of academic rigour and credibility in the evidence base.

To enhance the reliability and validity of the abstract screening process, an abstract selection checklist (found in Supplementary Materials, Appendix B) was developed and employed to assess the articles for inclusion in the review. This checklist aided in systematically identifying and selecting abstracts that met the specific criteria for the scoping review’s research objectives.

The checklist was used to determine relevance across several key criteria, including whether the abstract mentions financial-related terms, job resources, or job demands, and if it is relevant to the financial industry. Articles were excluded from the review if they covered a different industry (e.g. retail or customer service), did not refer to potential demands or resources, or focused on client outcomes rather than financial advisers. Furthermore, two additional assessors independently replicated the screening process, ensuring thorough and consistent evaluation. A further 48 articles were excluded by abstract screening. In assessing the inter-rater reliability (IRR) of the abstract screening stage, the percentage agreement between the raters was calculated, yielding a high level of agreement (94%). Articles that were not agreed upon were discussed by the reviewers and either excluded or included from the review. A total of 53 articles were selected for review (see Figure 2).

2.6. Data extraction

The 53 articles were extracted from the databases into PDF format for review. Relevant metadata (e.g. title, authors, year of publication, country of publication) were downloaded into an Excel spreadsheet. The articles were then coded into thematic variables (Bates et al., 2007; Grant and Booth, 2009).

2.7. Synthesis of results

Once the data were extracted, the authors followed the procedure for the synthesis and analysis section of this article (outlined below), which was based on Grant and Booth (2009) Search, Appraisal, Synthesis and Analysis (SALSA) framework. The authors coded the articles into thematic variables relating to job demands and job resources using the below procedure:

Each full-text article was reviewed in detail by the researcher to identify relevant job resources and job demands.

Relevant quotes were extracted and transferred into an Excel spreadsheet.

Similar concepts or activities were grouped into subcategories that align with each of the existing broad JD-R categories. For example, feedback, mentoring and training were all related to the ‘Professional Development’ resource category. Isolation and poor support were concepts that related to the demand category ‘Lack of Support’.

Articles were mapped across each category, and then the original list of concepts or activities was cross-checked for that article to ensure none were missed. The broad categories were adequate to describe the demands and resources for each article.

Three observers independently verified the categorisation process, addressing any subjectivity through thorough questioning. These independent observers collaborated to clarify the coding, ultimately reaching a unanimous agreement on the ratings, collectively deciding to either include or exclude articles.

The analysis sought to explore variability across studies by refining definitions in light of newly acquired insights. The review process involved a secondary assessor who independently cross-verified the coding using the checklist and instructions (see Appendix B), to ensure rigour and accuracy. Subsequently, comparisons were drawn among the studies to further elucidate and contextualise the relationships between the variables under investigation.

A table was created to highlight the authors, country, number of participants, occupation, type of study, main outcomes and categorise into ‘job resources’, ‘job demands’ and ‘personal resources’ (see Appendix C).

2.8. Risk of bias and applicability

To mitigate the potential impact of confirmation bias due to the use of pre-defined variables and the ‘top-down’ approach used, the researchers employed the method of ’bracketing’. This method is commonly used in qualitative research to address the potential influence of the researchers’ own beliefs, biases and values on the research process (Tufford and Newman, 2012). Bracketing involves reflecting on and acknowledging one’s own subjective experiences, assumptions and preconceptions regarding the research topic and deliberately setting them aside while conducting the study. The aim of this process is to minimise researcher interference and increase objectivity in the data collection and analysis process, thereby maintaining the credibility and rigour of the qualitative research. The researchers followed the conceptual framework for bracketing outlined by Tufford and Newman (2012) and used a reflexive journal to document their reflections on the research topic. This method is believed to raise the researchers’ awareness of the topic in their daily lives (Ahern, 1999).

The coding of the thematic variables was confirmed through a multi-stage validation process. First, two academics with relevant subject-matter expertise reviewed and evaluated the thematic coding independently. Their academic backgrounds ensured the rigour and theoretical alignment of the identified themes. Simultaneously, an industry expert with practical experience in the field provided an applied perspective, verifying that the themes were relevant and reflective of current industry trends and practices. After this, a thorough discussion was held to compare the insights of these three reviewers, resolving any discrepancies and reaching a consensus on the final coding structure. This collaborative effort ensured that the themes were both theoretically sound and practically relevant. Finally, to ensure the search process was robust and could be replicated, a librarian ran the search terms independently. The librarian’s review focused on evaluating the accuracy, relevance, and replicability of the search strategy, ensuring that the process could be repeated with the same results across different contexts. This combined approach enhanced the reliability of both the coding and the search methodology.

3. Results

This results section summarises the primary outcomes and key themes identified across the included studies. Supplementary Materials, Appendix C contains comprehensive details of each study, including author, year, country, occupation, type, main outcomes, and mapping to each JD-R category.

The core themes were selected from the outset using a top-down approach. An a priori definition for each thematic variable (as outlined in Supplementary Materials, Appendix B) was formulated by the authors based on existing research in the field. The authors then searched for and counted those thematic variables in each article. Job Resources

3.1. Job Resources

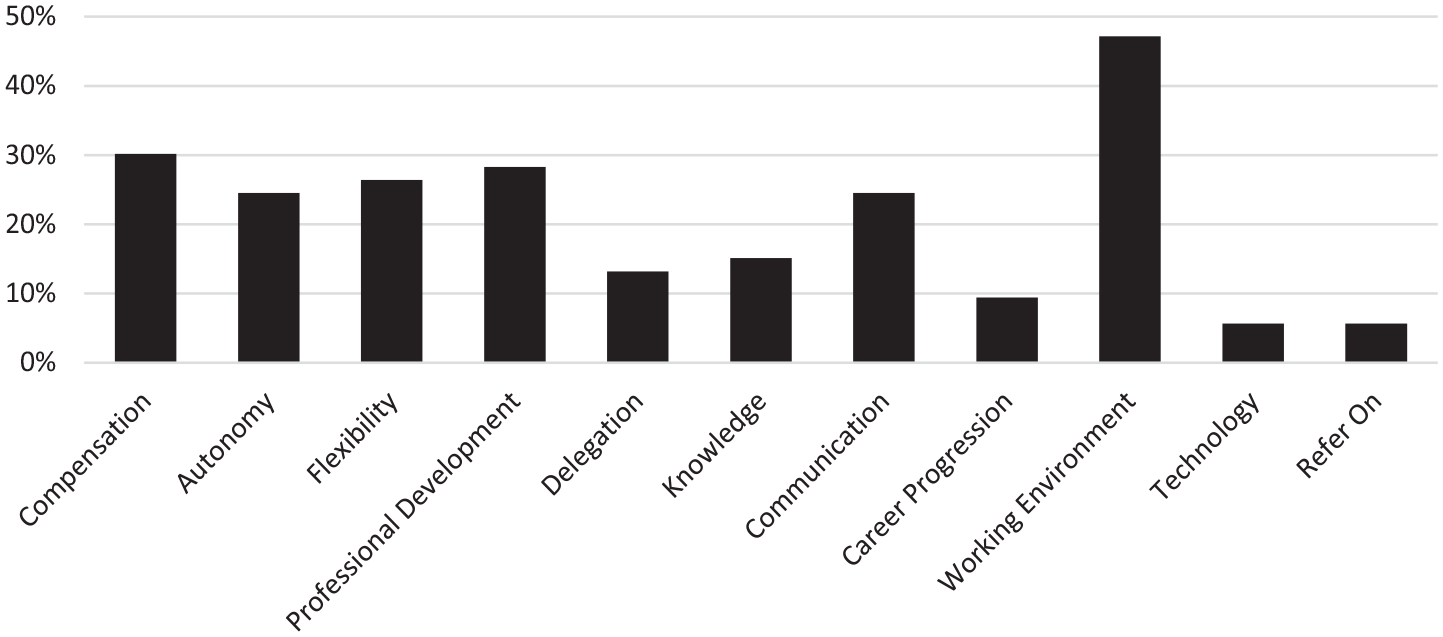

From the 53 articles reviewed, the top three resources mentioned were working environment (40%; 21 articles), followed by compensation (30%; 16 articles) and professional development (28%; 15 articles). Figure 3 shows a full breakdown of resources.

Job resources by percentage.

3.1.1. Working environment

The work environment comprises all elements that can affect day-to-day productivity, including when, where, and how one works. These articles included social features (Koesten, 2005), physical conditions and collaboration (Lipson, 2014). These articles included references to co-workers, effective management, Human Resources (HR), colleague support, teamwork, a conducive work environment, positive work–life interactions, and work–life enrichment (King, 2010; Kirchenbauer, 2018; Van De Voorde, et al., 2014). It remains unclear how this would affect sole traders in the industry, who may not have colleagues or HR support.

3.1.2. Professional development

Professional development was defined as the education, observation, and mentoring that can help enhance employees’ workplace experience and job prospects. In the articles identified, professional development was expanded to include networking (Lipson, 2014), feedback (Youngwirth, 2010), peer relationships (Finley, 2011), teamwork collaboration (Journal of Financial Planning, 2011; Opiela, 2000), training (Longfellow, 1995; Sirianni and Frey, 2001), observation and shadowing (Opiela, 2000), educational opportunities (Opiela, 2000) and ongoing mentoring between senior and junior personnel (Lipson, 2014). For example, during the profession’s early years, the need for feedback and mentoring was crucial for financial advisers’ success (Lipson, 2014).

3.1.3. Compensation

Compensation of employees was referenced as pay rises, general happiness with remuneration/salary (Cohan, 2003; King, 2010), incentives (Opiela, 1997), commissions and fee for service (Journal of Financial Planning, 2009, 2011, 2013).

Appropriate compensation levels in the literature were linked to job satisfaction and organisational commitment. The literature does not establish a monetary compensation range for financial advisers conducive to satisfaction.

3.1.4. Flexibility

In the articles identified, flexibility included elements such as freedom (Journal of Financial Planning, 2000), work–life balance (Finley, 2011; Gordon et al., 2007), the option to work part-time (Figueroa et al., 2009; Griffiths et al., 2011), the ability to take time off for a sabbatical without repercussions (Kirchenbauer, 2018), and recovery time away from work (Vessenes, 2008). Indeed, when financial advisers who were mothers were given more flexibility in working part-time, their general levels of job satisfaction increased (Figueroa et al., 2009). There was limited literature explaining flexible working conditions for financial advisers who are sole traders. It is hypothesised that sole traders work flexibly by the nature of job design.

However, there may be a greater need for time spent on business development, which offsets this flexibility, or they may be dependent on their clients’ schedules.

3.1.5. Autonomy

Autonomy in the articles included autonomy for self and team (Finley, 2011), working from home arrangements (Griffiths et al., 2011), choosing when and where to do tasks (Journal of Financial Planning, 2000), how to outsource their work (Opiela, 1997), and the use of technology and systems (Vessenes, 2008). When those in the industry were given higher levels of autonomy, their perception of the workplace was more positive, and these employees had higher levels of job satisfaction (Opiela, 1997). While existing research has established a link between autonomy and job satisfaction, there are several areas that remain underexplored. For instance, the long-term impact of autonomy on employee mental health and well-being warrants further investigation.

3.1.6. Communication

Internal communication with senior managers was the most common resource referenced (Journal of Financial Planning, 2011; Koesten, 2005; Martin and Bennett, 1996; Peck, 2005). In addition, a form of communication deemed valuable within the financial advisory profession is ‘emotional communication’ (Dubofsky and Sussman, 2009). This concept encompasses the knowledge and interpersonal skills necessary for effective interaction with clients and service providers while mitigating the adverse consequences of emotional contagion. Overall, effective communication is associated with reduced levels of burnout and stress for financial advisers (Miller and Koesten, 2008; Peck, 2005). While emotional communication is a personal attribute that would be favourable for the clients, it is unknown whether this may negatively impact professionals.

3.1.7. Knowledge

Knowledge in this study was categorised as both general knowledge required of practitioners in the profession and knowledge of oneself (including personality traits and shortcomings). High levels of education were associated with higher job satisfaction for full-time working mothers (Figueroa et al., 2009). The ability to be more mindful increased satisfaction and decreased fatigue, anxiety, and stress based on a brief mindfulness-based intervention (Gregoire and Lachance, 2015). Stress management was found to increase job satisfaction and organisational commitment (Koesten, 2005). Financial planners who possessed the knowledge of distinguishing luck from skill were found to be less stressed (Connelly, 1998). While existing literature covers the impact of mindfulness, stress management, and education on job satisfaction, there is limited research on how self-knowledge, specifically understanding one’s personality traits and limitations, influences job satisfaction and professional well-being.

3.1.8. Delegation

Delegation is the process of effectively reassigning tasks from oneself to other individuals or systems. The articles reviewed emphasised the significance of delegating responsibilities to less experienced employees, such as assistants, para-planners, and junior advisers (Kurtz, 2011). These tasks ranged from scheduling appointments and greeting clients to preparing for reviews and executing trades. Business owners were also encouraged to delegate managerial responsibilities, such as purchasing new technology and securing office space, to office managers or vice presidents of operations. The literature consistently underscored the importance of adhering to the fundamental principles of delegation, including selecting the appropriate individuals for the job (Finley, 2011), providing adequate training for new hires (Youngwirth, 2010), setting clear expectations (Opiela, 1997), and relinquishing control (Vessenes, 2008; Youngwirth, 2010).

When executed effectively, delegation can alleviate some of the typical demands of the role, such as managing compliance and high workloads (Opiela, 2000; Vessenes, 2008). Moreover, studies have shown that effective delegation can increase productivity and client and employee satisfaction and generate positive organisational outcomes (Opiela, 2000; Vessenes, 2008). The structure of different practices varies, and what is yet to be determined is the extent to which para-planners or administrative staff are accessed to relieve the administrative burden.

3.1.9. Referring on

The logical continuation to delegation was the ability to refer on when needed. The expanded skill set required to deal with personal issues points to emotional contagion becoming more prevalent in the profession (Walker, 2011). Many advisers spend time with clients who have recently lost loved ones and are going through periods of upheaval and change (e.g. grieving partners, workplace redundancies), which can lead to increased levels of stress (Walker, 2011). Financial advisers are spending more time (estimated 25%) on non-financial-related issues (Dubofsky and Sussman, 2009). While financial advisers are spending more time moving from focusing on money and logic to focusing on creativity and life planning, their professional development in the latter may be virtually non-existent. Part of the solution may be the adoption of a multidisciplinary approach leveraging qualified psychologists or medical experts. This requires further investigation to determine the extent of use and resulting satisfaction.

3.1.10. Technology

Technology and tools were noted to be a resource among financial advisers. E-working significantly positively affects the flow of work and productivity (Sarappo, 2007). Since the COVID-19 pandemic, technology has been found to increase employee flow of work. However, technostress and loneliness were found to moderate the positive impacts on flow (Taser et al., 2022). More research is needed to consider some practical implications of e-working post-pandemic for financial advisers.

3.1.11. Career Progression

Career progression was found to be a significant driver of employee satisfaction (Malik et al., 2010). To stay motivated to continue to stay in the same role, financial advisers needed to know that there was an opportunity to progress in their roles (Cheng and Chang, 2016; Lipson, 2014; Malik et al., 2010). However, external factors such as the organisation’s size may impact the possibilities for progression. For example, those who independently own a business will not have the scope to promote themselves. Larger organisations will have more opportunities for career progression and potentially in related fields but different jobs, for example, chief financial officers. Further investigation may help understand the differences between sole traders and small- and medium-sized businesses.

3.2. Job demands

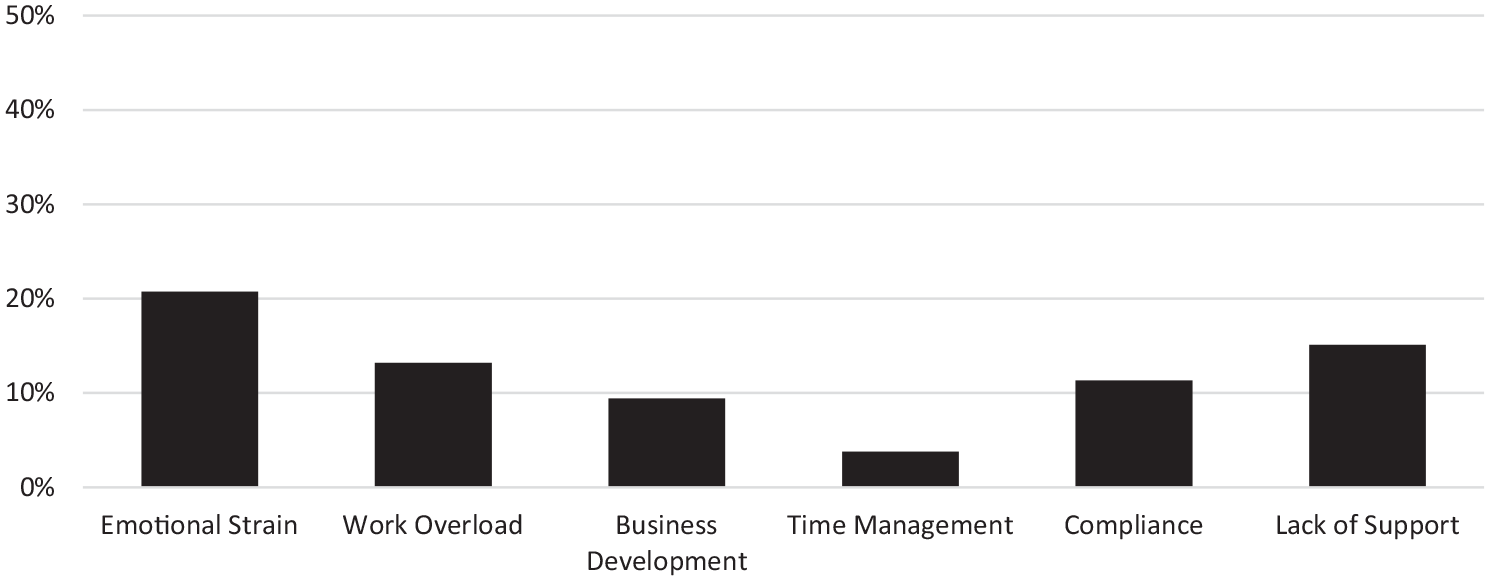

The top three most frequent demands were emotional strain (17%; 9 articles), lack of support (15%; 8 articles) and work overload (13%; 7 articles) (see Figure 4).

Job Demands by percentage.

3.2.1. Emotional strain

Emotional strain emerged as a recurring demand for financial advisers (Allison, 2011; Dubofsky, 2010; Elefant, 1989; Proudfoot et al., 2001; Walker, 2011) and is associated with a leading cause of job stress for the profession (Connelly, 1998; Dubofsky, 2010; Wu, 2017).

Emotional strain includes dealing with complex and emotional issues (Jeung et al., 2018). Emotional contagion forms part of emotional strain. That is the tendency to ‘feel’ with your client to the extent that the client’s grief or pain is experienced according to one’s own emotional response (Herrando and Constantinides, 2021). As financial advisers engage in emotional communication, they are likely to experience the negative impacts of stress and burnout that are correlated with emotional contagion, which is already well-documented in other professions, such as nursing (Hayes et al., 2012).

Emotional exhaustion and emotional strain are interconnected concepts within psychological and occupational health. Emotional strain refers to the psychological tension from ongoing challenges that exceed an individual’s coping capacity, manifesting as anxiety, irritability and difficulty concentrating. If persistent, this strain can deplete emotional resources, leading to emotional exhaustion, characterised by a chronic state of physical and emotional depletion that results from excessive job and/or personal demands and continuous stress (Jin et al., 2020). Emotional exhaustion was included on the list of demands, and this occurs when day-to-day contact with clients results in a general loss of energy and fatigue without any relief (Koesten, 2005). The natural response to this feeling is to distance oneself from work, which can lead to negative outcomes for the organisation, such as burnout and turnover. Financial advisers might not be adequately trained to handle their clients’ stress and anxiety without it affecting them. In addition, they may struggle to differentiate between issues that they can manage and those that require the expertise of specially trained professionals. The increase in emotional strain on employees may be contributing to burnout, as witnessed in other professions already trained to deal with interpersonal issues, such as nursing and psychology (e.g. Petitta et al., 2017). Whether financial advisers are suffering from vicarious trauma, like these professions, is yet to be determined.

3.2.2. Lack of support

There is reportedly a general lack of perceived support in the profession. The reviewed articles indicated that there were inexperienced managers (Orpen, 1994a), role ambiguity (Von Emster and Harrison, 1998), autocratic decision-making (Orpen, 1994a, 1994b), and isolating working conditions and working silos (Kurtz, 2011; Taser et al., 2022). Lack of support also encompassed a general lack of direction from management and opportunities for career progression (Vessenes, 2008). One article specifically mentioned a lack of support for rural financial advisers working in isolated conditions (Griffiths et al., 2011). A general lack of support is known to lower engagement and is subsequently linked to negative organisational outcomes such as stress, burnout and turnover (Bakker and Demerouti, 2007). It is anticipated that sole traders may feel even less support than those in larger organisations.

3.2.3. Compliance issues

The compliance burden in the industry is well documented (Goss, 1989; Griffiths et al., 2011; King, 2010; Roman and Munuera, 2005; Vessenes, 2008; Wagner, 2010). Results have shown that 73% of advisers reported they were ‘dealing with too much paperwork’, and 60% of respondents thought that reducing compliance was a top priority, rating it as either ‘extremely important’ or ‘important’ (Vessenes, 2008). Financial advisers are spending considerable time on these issues, which may be reducing their job satisfaction and organisational outcomes. Given that the current landscape for financial advisers in Australia appears to have been heavily influenced by regulatory burden, a cross-cultural analysis comparing compliance and turnover intentions may be helpful.

3.2.4. Work overload

Most financial advisers are working more hours than the ordinary working week (Griffiths et al., 2011; King, 2010; Von Emster and Harrison, 1998; Wefald et al., 2012; Youngwirth, 2010). One study found that 81% of advisers reported working more than 40 hours per week, 53% reported working more than 51 hours a week, and 15% reported working more than 60 hours per week (Vessenes, 2008). High levels of workload and overload have also been reported to directly and negatively impact work–life balance, work enrichment and satisfaction (Koesten, 2005; Vessenes, 2008). Indeed, there is evidence that high workloads can lead to fatigue, burnout and high levels of job stress in the financial industry (Khan et al., 2011). Whether this trend is increasing or decreasing since the COVID-19 pandemic has yet to be determined.

3.2.5. Business development (increasing revenue/business)

The key focus for many advisers is increasing revenue and profitability (Griffiths et al., 2011; Vessenes, 2008); 91% of respondents placed a high priority on growing business (Vessenes, 2008). A recurring theme throughout the literature was that a top priority for advisers was to bring in more clients and make money (Vessenes, 2008). Increasing revenue and business has been classified as a demand, as the need to continually find business can be uncertain with the changes in market and economic conditions (e.g. COVID-19 and the Global Financial Crisis), growing pains as the business expands (e.g. inadequate resources to cope with increased business), the emergence of new products (e.g. artificial intelligence and robo-advisers), and competition. It is unclear whether increasing business is more stressful for small/medium businesses or large organisations.

3.2.6. Time management

The ability to manage time effectively was another leading demand of financial advisers (Dubofsky, 2010; Fox and Bartholomae, 2020; Vessenes, 2008). The advisers’ time appears to be spent on compliance and paperwork, and 25% of the time is spent on non-financial-related issues (Dubofsky, 2010). Post COVID-19 pandemic, a key finding is that financial planners have faced increased time management challenges, including the rapid transition to virtual meetings, increased client communications, and the need for administrative adjustments to digital processes (Fox and Bartholomae, 2020). These challenges were exacerbated by high client demand due to financial instability and the learning curve associated with new technologies. As a result, poor time management led to increased stress for planners, missed financial opportunities and reduced efficiency (Fox and Bartholomae, 2020). There are no clear guidelines on how to manage time efficiently in this context. However, some advisers may experience consequences if they do not correctly allocate resources (Vessenes, 2008). Ineffective time management is thought to increase strain and burnout in the profession. The time spent on non-financial issues is expected to increase (post-pandemic and inflation). Yet, financial advisers are primarily trained on how to help an individual achieve financial success. Whether the profession is upskilling its employees on soft skills needed to respond to the changing demand is yet to be determined.

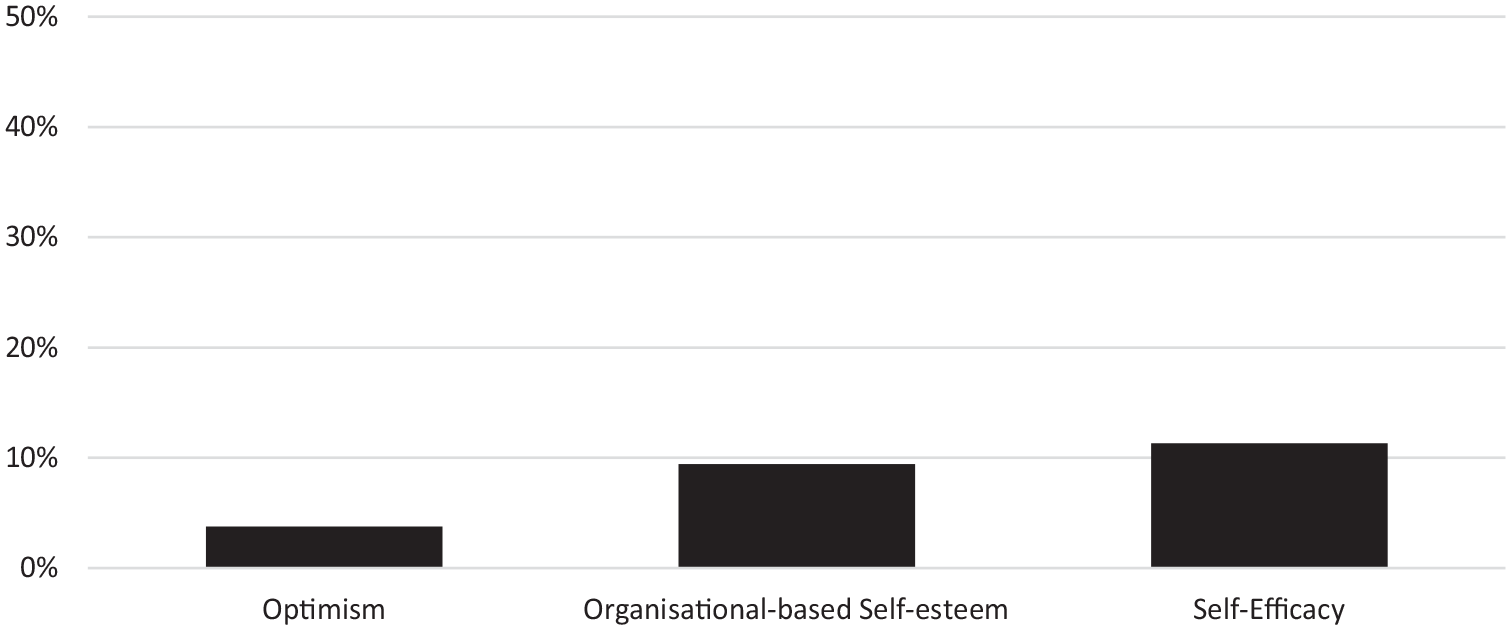

3.3. Personal resources

Self-efficacy was the leading personal resource mentioned 11% of the time, OBSE was mentioned 9% of the time and optimism was mentioned 4% of the time (see Figure 5).

Personal Resources by percentage.

3.3.1. Optimism

Advisers who exhibit higher levels of happiness, often a manifestation of optimism, tend to foster stronger client relationships, communicate more effectively, and achieve better professional outcomes (Walker, 2011). The prevalence of stress and burnout in the profession is significantly shaped by a combination of personality traits, known as Knowledge, Skills, and Abilities and Other characteristics (KSAOs), as well as the working environment and communication dynamics. Effective stress management and remaining more optimistic not only enhance job satisfaction but also strengthen occupational commitment, leading to more sustained and positive career outcomes (Koesten, 2005). It is hypothesised that higher levels of optimism may lead to the individual perceiving demands as more challenges than hindrances and taking advantage of more resources.

3.3.2. OBSE

OBSE refers to an employee’s perception of their value and competence within their organisation. King (2010) shows ownership options and involvement in core services as key drivers of employee satisfaction, expanding ownership options is correlated with increased levels of OBSE (Pan et al., 2014). Arokiasamy et al. (2010) highlight that perceived organisational support (POS) significantly influences job satisfaction, affective commitment and turnover intentions, reinforcing OBSE. Cheng and Chang (2016) discuss job embeddedness (JE) as a stress-reducing mechanism, which supports OBSE by fostering a sense of connection and promoting professional development and career progression. It is hypothesised that higher levels of OBSE may lead to the individual perceiving demands as more challenges than hindrances and taking advantage of more resources. It is also associated with much lower levels of turnover (Oguegbe and Edosomwan, 2021).

3.3.3. Self-efficacy

Self-efficacy, the belief in one’s ability to achieve goals and manage tasks, was the leading personal resource. Finley (2011) emphasises understanding strengths and weaknesses, setting goals, and exercising autonomy, all of which build self-efficacy. High job satisfaction often stems from advisers’ ability to help clients achieve goals, reflecting their self-efficacy. Koesten (2005) links personality traits (Knowledge, Skills, and Abilities (KSAs)) to stress management, highlighting self-efficacy’s role in coping with emotional strain. Connelly (1998) underscores the importance of distinguishing skill from luck, requiring high self-efficacy in managing client assets. Orpen (1994a) shows that personal control enhances job satisfaction and performance, moderated by self-efficacy. It was found that high role ambiguity and low perceived control correlate with burnout, which can be mitigated by strong self-efficacy.

Collectively, these articles demonstrate that high role ambiguity and low perceived control correlate with burnout, which can be mitigated by strong self-efficacy. Collectively, these articles demonstrate that self-efficacy may help with managing challenges, improving job satisfaction and achieving success in financial advising.

3.4. JD-R model extension

The scoping review of job demands and job and personal resources for financial advisers has led to an extension of the JD-R Model, as illustrated in Figure 6. This extension uniquely identifies and integrates job demands and resources specific to the financial advisory profession. The job demands include compliance, emotional strain, lack of support, work overload, business development, and time management. By contrast, the job resources identified encompass flexibility, delegation, professional development, knowledge, career progression, communication, working environment, referring on, compensation, and technology. In addition, the personal resources highlighted are optimism, self-efficacy and OBSE. By categorising these profession-specific factors, the extended JD-R model enhances its applicability to financial advisers, providing greater detail and specificity to this profession. This extension demonstrates how the JD-R model can be adapted to address the distinct challenges and resources in the financial advisory industry.

JD-R model extended for financial advisers.

The extended JD-R model not only provides a detailed understanding of the job demands and resources specific to financial advisers but also reveals several opportunities for workplace change, intervention initiatives and strategic selection practices. These opportunities are crucial for enhancing the well-being and performance of financial advisers, addressing the unique challenges they face:

Workplace Change: To address the identified job demands, financial advisory firms may implement key changes. For instance, improving support systems by introducing mentoring programmes, peer networks and support groups may reduce emotional strain and prevent burnout among advisers.

Intervention Initiatives: The extension of the JD-R model also highlights potential targeted intervention initiatives. Given the high levels of emotional strain and compliance pressures in the financial advisory profession, implementing stress management programmes can be highly beneficial. Mindfulness training, counselling services and resilience workshops may equip advisers with the tools to manage stress effectively.

Selection and Recruitment: The recruitment process presents another area where the extended JD-R model may inform practice. Firms could focus on selecting candidates who exhibit strong personal resources, such as optimism, self-efficacy and OBSE. These traits may assist with coping with the profession’s demands and can lead to better long-term performance.

4. Discussion

The aim of the article was to extend and leverage the JD-R model to better understand the experiences of financial advisers. This application to the specific contextual variables associated with the profession provides greater granularity and nuance, which is crucial in revealing the drivers of job satisfaction and turnover and informing the design of interventions to assist workers. The work contributes to the general theory and evidence base relating to the application of the model more broadly while providing a specific lens for workers in this industry. Furthermore, the work offers a template for how others may extend the model into other industries and areas of work.

A key theoretical contribution of this study lies in illustrating the capacity of the JD-R model to identify and prioritise demands and resources across different professions. This comparison highlights both shared and unique elements within specific work environments, helping practitioners and organisations tailor support strategies accordingly. To underscore this point, an illustrative comparison between financial advisers and another industry, such as healthcare professionals (e.g. nurses), can be drawn. Nurses, like financial advisers, face high job demands, including emotional labour, workload, and compliance requirements (Bakker and Demerouti, 2007). However, the nature of these demands differs significantly.

For example, while nurses’ demands often relate to patient care and life-or-death decision-making, financial advisers experience demands in areas such as compliance burdens, emotional strain from client interactions, and the need to work outside their immediate expertise. The resources available to mitigate these demands also differ – nurses may rely on teamwork and institutional support, whereas financial advisers often benefit from professional autonomy and targeted skill development (e.g. micro-counselling or para-planner support).

This comparison underscores the unique contextual demands and resources that shape the experience of financial advisers, distinguishing them from other professions and emphasising the need for tailored interventions. For instance, professional training tailored to managing client emotional responses, coupled with alliances with specialists from disciplines like grief counselling, can enhance advisers’ capacity to meet complex client needs.

The comprehensive review of the extant literature has allowed for a successful categorisation of job demands and job resources specific to financial advisers, thereby facilitating a greater understanding of the complex nature of the profession from a global context. There was a predominant emphasis on the United States (N = 38), and to a lesser extent, the United Kingdom (N = 3) and Australia (N = 2). This distribution underscores the need to understand the differences in findings across these countries, providing valuable insights into the global financial advisory profession. Moreover, the research methodologies range from empirical studies to scholarly articles, reflecting a mix of qualitative and quantitative approaches that enrich the overall understanding of the field. This categorisation marks an important first step towards enhancing knowledge and awareness of the financial adviser role and the determinants of optimal performance and wellbeing in the field.

While the study identified similar job demands and resources reflected in the original JD-R model, such as workload and autonomy (Bakker and Demerouti, 2007), it also revealed several additional job demands and resources that are applicable to financial advisers. These include demands related to compliance, emotional strain, delegation, career progression, and technology. The review’s findings effectively extend the JD-R model, emphasising the unique demands and resources essential for financial advisers to achieve enhanced job performance and satisfaction. However, it is important to note that job satisfaction and turnover were not necessarily examined in every study reviewed. Therefore, the unique factors identified may only partially explain the current outlook for financial advisers and their intentions to leave the profession.

The findings highlighted that the most frequently reported demands facing financial advisers are emotional strain, lack of support, high workload and compliance burden. Furthermore, the review has revealed that financial advisers are likely working in areas outside of their expertise. This highlights a need for sufficient training to respond to these issues, whether that be increasing micro-counselling skills of professionals, using para-planners, or creating a multidisciplinary approach to financial planning.

The JD-R model posits that enhancing job resources can offset the adverse effects of increased job demands, potentially leading to more favourable organisational outcomes such as improved retention and productivity (Bakker and Demerouti, 2007). If financial advisers are provided with the right support, this could potentially reduce the imbalance between demands and resources and associated negative consequences. For example, professional training tailored to the evolving needs of advisers, including areas like managing emotional reactions to grief, might be one way to increase resources to meet demands. Alternatively, adopting a comprehensive strategy that incorporates expertise from various fields outside the industry, such as grief counselling, relationship counselling, and psychology, could offer greater benefits in a multidisciplinary, holistic approach (Mooney et al., 2023). This objective might be realised through the establishment of cooperative alliances with subject-matter experts across the aforementioned disciplines, thereby cultivating a comprehensive support network. Clients would thus be able to be directed towards these specialists when their requirements transcend the purview of financial advice.

This research is both pertinent and opportune, considering the evolving dynamics within the Australian financial advising sector. Moreover, the demographic shift towards an ageing population, coupled with challenges in retirement planning, potentially imposes a significant fiscal burden on the government via increased dependency on the old-age pension system (Alavi et al., 2023). Financial advisers play a crucial role in mitigating this economic strain by facilitating effective retirement preparedness among Australians (Bowerman, 2021). Peer-reviewed literature consistently highlights compliance burdens and work overload as critical challenges confronting financial advisers internationally (Goss, 1989; Griffiths et al., 2011; King, 2010; Roman and Munuera, 2005; Vessenes, 2008; Wagner, 2010).

If the industry can successfully improve the outcomes for financial advisers through increasing resources or reducing demands, such a situation is likely to benefit both organisations and consumers. It is documented that when financial advisers are satisfied with their job, the clients are more likely to be satisfied with the service provided (Irving et al., 2011). Thus, ensuring the job demands and resources are sufficient is crucial to both the adviser and the consumer.

4.1. Limitations

This study represents a first effort to examine the job demands and job resources specific to the financial advisory profession, marking an important step towards a deeper, empirical understanding of this evolving and shrinking field. However, the study is not without its limitations. One limitation is the use of a top-down approach, which inherently carries the risk of confirmation bias. The initial hypotheses were developed based on predetermined principles, deductions from prior studies, and a desktop review. While the authors implemented bracketing strategies to mitigate the influence of confirmation bias, the top-down nature of the selection method still poses a potential risk. This approach could inadvertently shape the research direction according to existing beliefs or theories, potentially limiting the scope of findings.

To address this limitation in future research, it would be advantageous to incorporate a more diversified selection method that combines both top-down and bottom-up approaches. By integrating these approaches, future studies could achieve greater objectivity, ensuring a broader range of data is considered. This would reduce the likelihood of overlooking contradictory evidence and provide a more comprehensive understanding of the financial advisory profession.

Another limitation of this article was the literature review indicated that personal resources such as self-efficacy, OBSE and optimism have a significant impact on job satisfaction and stress management; their role as moderators within the JD-R framework may require further empirical validation. Existing studies suggest their potential to influence the relationship between job demands and outcomes; however, the specificity of this moderating role should be approached with caution unless robust supporting evidence is available. Thus, these insights, while aligned conceptually with the JD-R Model, may serve more as a basis for future hypotheses rather than definitive conclusions.

Another limitation of this study is the limited availability of literature outside of the United States, particularly in regions such as Australia and the United Kingdom. The scarcity of research in these areas poses a challenge in developing a comprehensive understanding of the job demands and resources specific to financial advisers in different cultural and regulatory contexts. Given the current state of affairs globally, and especially in Australia, future studies could benefit from focusing on the Australian context. Such research would not only address this gap but also provide insights that are more relevant and applicable to the unique challenges faced by financial advisers in Australia. By concentrating on the Australian market, future studies could contribute valuable knowledge to the global understanding of the financial advisory profession while also informing policy and practice in a region that is currently under-represented in the literature.

4.2. Future research

There were several notable gaps in the literature relating to the job demands and resources experienced by financial advisers. Three prominent features appeared to be recurring: (1) the need to understand the differences between sole traders, small-medium businesses, and large organisations in relation to the impact each resource or demand has based on the specific scale; (2) the increase of emotional strain on the profession and the need to understand this in greater detail and explore whether vicarious trauma may be present and (3) the need for contemporary, empirical research to account for changes to the profession.

Furthermore, the contrast between China’s focus on digital financial inclusion and Japan’s emphasis on senior wealth management illustrates the need for financial advisory adaptability across Asia. Exploring these regional trends in more depth could provide valuable insights for Australasian financial practitioners aiming to stay ahead of shifting market dynamics.

5. Conclusion

This study sheds light on the intricate issues facing financial advisers, contributing valuable insights towards developing effective strategies to overcome these challenges. The findings are crucial for the continued efforts to tackle the obstacles financial advisers face. Moreover, based on the findings and the extended JD-R Model, it would be reasonable to expect that by successfully deploying targeted interventions that balance job demands and resources in the financial advising sector, this may lead to improved job performance, increased career satisfaction, and possibly better client services and results. These results highlight the importance of sustained collaboration and research to equip financial advisers with the necessary resources and support for their success now and in the future.

Key Practical and Research Implications

This study extends the JD-R model to the financial advisory profession, revealing unique job demands and resources that influence job satisfaction, turnover, and well-being. This adaptation provides a framework for understanding industry-specific dynamics and guiding tailored interventions.

Significant demands for financial advisers include emotional strain, compliance burden, high workload, lack of support, and pressures related to business development. Practical strategies should focus on reducing these burdens through support systems, efficient compliance processes and better workload management.

Effective resources include a positive working environment, professional development opportunities, autonomy, flexibility and supportive compensation structures. Organisations should prioritise these elements to improve job satisfaction and reduce turnover.

Recommendations include enhancing support systems through mentoring, providing targeted professional training (e.g. managing client emotional responses), and adopting multidisciplinary approaches with allied professionals (e.g. grief counsellors) to better serve client needs.

The findings underline regional differences in job demands and resources. Context-specific strategies for Australia and other regions are essential to improve outcomes for financial advisers and their clients globally.

Supplemental Material

sj-pdf-1-aum-10.1177_03128962251350337 – Supplemental material for The Job Demand-Resources (JD-R) model through the eyes of financial advisers: A scoping review

Supplemental material, sj-pdf-1-aum-10.1177_03128962251350337 for The Job Demand-Resources (JD-R) model through the eyes of financial advisers: A scoping review by Phoebe Arthur, Ben Morrison and Joanne K Earl in Australian Journal of Management

Footnotes

Acknowledgements

We would like to express our sincere gratitude to all those who contributed to the completion of this paper. We are especially thankful to the reviewers at AJM for their insightful feedback and constructive suggestions that enhanced this article. Furthermore, we acknowledge the dedication and resilience of professionals in the financial advisory field, whose experiences and challenges inspired this research.

Final transcript accepted 15 May 2025 by Catherine Collins (Deputy Editor).

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This review was funded by Macquarie University as part of an Australian Research Council (ARC) linkage programme LP190100574.

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.