Abstract

There is a significant capacity for management research to contribute to addressing the multifaceted challenge of climate change. This includes identifying and then addressing climate change–related risks and opportunities which are already on the horizon and likely to be of critical importance in the future, but which are not yet the focus of our attention. To do this effectively, and ensure the resulting research is impactful, will involve adopting an abductive research approach; one where industry practitioners collaborate with academic colleagues to develop the kinds of research questions they would seek to have them research. This article demonstrates the value of such an approach. Academics and practitioners are brought together into a co-authoring team that engages in the problematisation of climate risk and opportunity. Four issues emerge as common and significant themes: uncertainty, information, motivation, and investment. These are used to construct an industry-informed, future-focused research agenda.

1. Introduction

David Grant and Ben R. Newell

The Australian Government Intergenerational Report 2023 observes that over the coming decades, a number of ‘powerful forces. . . will influence the future path and structure of our economy and change how Australians live, work, and engage with the world’ (Commonwealth of Australia, 2023: vii). One of these forces will be climate change.

Climate change represents the single biggest grand challenge of our time. The consequences of failing to transition the global economy to net-zero carbon emissions by 2050, if not before, present a significant long-term threat to human civilisation (André, 2020; Nyberg et al., 2022; Sevil et al., 2022). In the meantime, the risks attached to climate change are becoming increasingly apparent. More frequent and more intense weather events are heavily impacting socioeconomic activity around the world. Australia is not immune to this.

For industry, the challenges presented by climate change manifest as both physical risks (e.g. impact on operations and supply chains from climate events or adverse influences on workforce health and well-being) and transitional risks, resulting from actions taken – or not taken – to move energy supplies to low-carbon energy sources (Financial Stability Board (FSB), 2017). Allied with transitional risks are governance risks related to not meeting climate change reporting requirements and reputational risks arising from failure to address consumer, employee, and stakeholder expectations.

As is noted in the Commonwealth Intergenerational Report, some of the risks associated with climate change will also generate opportunities. For example, it is anticipated that the move towards renewables and net zero will, in turn, create growth opportunities in some occupations and for existing and new industries (Commonwealth of Australia, 2023: viii).

Many of the risks and opportunities associated with climate change have generated important research questions which have been explored by management scholars both in Australia and overseas. In some cases, this research has been primarily theoretical in orientation (see e.g. Bowden et al., 2021; Daddi et al., 2018; Winn et al., 2011) while in others, theory has been applied to some practical end, often with researcher expertise and knowledge being used to identify, and to help design and implement, industry responses needed to address the risk or opportunity under examination (see e.g. Arteaga et al., 2023; Gualandris et al., 2024; Jarzabkowski et al., 2023).

We make two high-level, overarching observations about these various theoretical and applied contributions. It is these observations that have led us to compile this Engaged Problematisation article for AJM. Our first observation is that taken as a whole, these studies demonstrate the significant capacity for management research to contribute in meaningful and impactful ways to industry’s need to address the multifaceted challenge of climate change. Multiple examples of what this contribution can look like are documented by the UN Global Compact in combination with the Principles for Responsible Management Education in their report, ‘Partner with Business Schools to Advance Sustainability: Ideas to Inspire Action’ (UN Global Compact and PRME, 2015). The examples provided show how management researchers can deploy their expertise in ways that can significantly influence and impact the planning, governance and implementation of climate action initiatives by government and business across a range of economic sectors. Increasingly, these types of contributions are occurring through university climate change institutes and research centres that draw on multidisciplinary, including management, expertise. For example, in Australia, management researchers attached to the Griffith University Climate Action Beacon are involved in a range of research projects with government, business and the wider community that seek to ensure an effective and just transition to net zero. Similarly, at UNSW Sydney, management scholars at the Institute for Climate Risk and Response are engaged in a range of projects with industry that focus on building capability in the identification and measurement of risks and advising on the responses to manage these.

In sum, the mobilisation of management research expertise in this way is encouraging and is to be welcomed. It demonstrates a rich potential to make a difference in respect of addressing the risk and opportunities associated with climate change. However, the challenges associated with climate change are significant and there is much more work to be done. As has been observed elsewhere (André et al., 2025), we should surely look to leverage this capacity even further.

Our second observation about these studies follows on from the work of Saravanan (2021) who, in analysing climate change, draws on what is known as the ‘Rumsfeld Matrix’ (Krogerus et al., 2012: 86–87). We note that, to date, the studies have tended to address the ‘known, knowns’ of climate risk and response – that is the risks and opportunities attached to climate change that are already clear to us and of which we are already aware. They do not address the ‘known, unknowns’; those risks and opportunities associated with climate change that we know we do not yet know, but which are likely to be of critical importance in the future (Saravanan, 2021: 195). 1 The sooner we identify these risks and opportunities and the research questions they engender, the sooner we can take action.

We believe that, for management scholars, addressing the issues raised by these two observations will involve the adoption of an approach that emphasises the kind of abductive research discussed by Collins in her AJM call for ‘Engaged Problematisation’ papers. She describes this as an approach that ‘combines industry and academic perspectives in research. . .’ and one which ‘. . .focuses on important industry questions that are anomalies or surprises; [where] relevant theory and literature are then drawn in to unpack the problem in focus’. (Collins, 2025).

It seems to us that taking such an approach will further leverage the capacity of management scholarship to help address the climate challenges faced by industry. Working in combination with practitioners is an important way of identifying the risks and opportunities that are of concern to them in respect of climate change and to be confident of constructing and addressing research questions that make significant contributions to both theoretical and applied knowledge. It is also an approach that lends itself to identifying and addressing not only the ‘known knowns’ but also the ‘known unknowns’. In other words, engaging with practitioners offers the opportunity to learn about not only those immediate and obvious risks and opportunities they are grappling with but also the longer term, less developed, ones that they believe will manifest in respect of their industry, profession or occupation. If through a process of abductive research, we can act early in respect of these emergent and long-term risks and opportunities, the benefits to industry and society more broadly ought to be considerable.

To illustrate the value of this abductive approach to addressing our two observations we use the remainder of this article to bring together academics and practitioners into a co-authoring team that engages in the problematisation of climate risk and opportunity. To compose the article, we adopted a multiple stakeholder perspective, one where we invited practitioners from four Australian industry sectors – emergency management, insurance, energy, and finance – to each provide a short essay in which they reflected on how the challenge of climate change is understood within their industry and what their priorities are in response to it. More specifically, we provided each of them with the following question in which we asked them to think about and identify the key risks and opportunities associated with climate change that they believed would impact their sector operations over the next decade:

“The 2023 Intergenerational Report projects the outlook of the economy and the Australian Government’s budget to 2062-63. The report considers major forces affecting economic growth in the coming decades, one of which is climate change, and the risks and opportunities associated with it. Looking forward over the next decade, what do you see as the single most significant risk and single most significant opportunity associated with climate change for your industry, and how will these be addressed?”

In this way, we are able to see whether and how the risks and opportunities predicted to occur in the coming decades by the Australian Government’s Intergenerational Report align with the experiences and perspectives of our practitioner contributors. In doing so, we are also able to draw on their essays to propose a research agenda and highlight the kinds of research questions that management scholars will need to consider and address if they are to contribute to the effective planning for and implementation of responses to the climate risks and opportunities identified.

We are not seeking to suggest that our practitioners and the four sectors that they work in should be taken as a representative and exhaustive sample of Australian industry. There are plenty of other sectors we could have included but space does not permit this. Limiting the essay coverage to four sectors does not, however, impact on our goal of demonstrating the potential for an abductive approach to be used to initiate timely and impactful management research on the grand challenge of climate change.

Our four practitioner essays provide a set of fascinating observations regarding the key risks and opportunities arising from climate change in Australia that they perceive emerging over the next decade and how these might play out. In the first essay, Mullins observes that our emergency services are reaching the limits of their capacity to adapt to the escalating impacts of extreme weather events. Faced with this challenge, he reflects on what we will need to do differently in future to keep communities safe. This he believes will entail a significant rethinking of our approach to disaster management; one that includes placing greater emphasis on building community resilience and on the cost-effectiveness of early intervention programmes that mitigate risks associated with extreme weather events.

In the second essay, Mortlock and Cheeseman observe that as climate change causes an escalation in the frequency and intensity of extreme weather events, the insurance industry, using current mechanisms and approaches, is finding it increasingly challenging to provide the coverage needed and to do so at an affordable price. For Mortlock and Cheesman, there is an important opportunity to maintain a healthy insurance industry and thus economic resilience; one that involves it devising and using innovative products and services. They provide several examples of what these might look like. They include greater emphasis on insurance that underwrites assets driving the transition to renewables or that encourages strengthened building codes and planning measures where it is targeted at providing affordable and accessible cover for climate resilient buildings and other infrastructure.

A successful and timely transition to net zero by Australia and the risk of not achieving this, is very much contingent on the mitigative and adaptive efforts of the energy sector. The third essay by Joseph, Papas and Moffitt focuses on a critical element of the sector – network distributors. Here, the challenge is to help ensure that the transition to the supply of renewable power is affordable and fair for consumers and that it occurs as soon as possible while ensuring that services can withstand the impacts of climate change. While Joseph and her colleagues note barriers to achieving this, they also provide an overview of the sorts of opportunities available to overcome them. These pertain to measures enabling wider access across the community to affordable solar and battery power, improved Electric Vehicle (EV) charging infrastructure and a range of innovations designed to build the resilience of the distribution network to extreme weather events and assist consumers in withstanding the impact of climate-induced power outages.

The final practitioner essay, by Bovingdon and Michael, looks at how risks and opportunities associated with climate change impacts the finance sector, specifically the funds management industry. For these practitioners, the most pressing risk facing the sector is a failure to mobilise enough capital to fund the kinds of projects – some of which are highlighted by the preceding essays – that will enable Australia to achieve a transition to net zero as quickly as it needs to. At the same time, they note the opportunity for Australia to become a major global player in sustainable finance thereby enabling it to mitigate this risk. This will involve Australia increasing its presence in global funding markets, such as Green Bonds, and better leveraging its capital market expertise and infrastructure so as to channel local and foreign investment into funding technologies, services and products that will be necessary to support and accelerate the transition.

Following these four essays, we provide a discussion and some concluding remarks in which we consider four issues that emerge from them as common and significant themes: uncertainty, information, motivation, and investment. We argue that these themes and the kinds of research questions that they generate can be used to construct an industry-informed, future-focused research agenda that, if pursued, will enhance the contribution of management scholarship to addressing key risks and opportunities in Australia associated with climate change.

2. Climate-driven disasters: let us get ahead of the game

Greg Mullins

The unseasonal winter firestorms that ravaged Los Angeles in January 2025 are an urgent wake-up call to the world that the worsening impacts of climate change present a clear and present danger which we ignore at our collective peril. That one of the best-resourced fire jurisdictions in the world could suffer such horrendous losses at a time of the year when major fires have never been experienced before begs the question: are we reaching the limits of human capacity to respond to extreme weather disasters driven by climate change? The recovery after this disaster will last for many years and be even more expensive than the massive response effort.

In Australia, we are no strangers to worsening extreme weather. For example, the climate change driven Black Summer bushfires of 2019–2020 (Abram et al., 2021) capped off two decades of worsening fires, including those in Canberra in 2003 that saw the world’s first recorded large-scale fire tornado (McLeod, 2003), while the 2009 Black Saturday fires in Victoria took 173 lives and destroyed around 2000 homes (Teague et al., 2010). These events resulted in the biggest reset to firefighting doctrine since the 1939 Victorian fires, including the introduction of emergency warning apps, introduction of the new fire danger rating Catastrophic, and reversal of decades of fire service advice that well prepared properties can usually be defended.

On the heels of our worst-ever fires, from 2020, Australians endured a rare triple La Nina event, with record rainfall and flooding. In 2022, Lismore in New South Wales exceeded the previous flood record by an astounding 2 m (Poncet, 2024).

We are now seeing emergency services being periodically overwhelmed by the size, geographic spread and intensity of floods, storms and fires, with cascading disasters that sometimes hamper recovery efforts. I see this as the paramount issue facing the emergency management sector in Australia today – if emergency response and recovery capacity are increasingly being overwhelmed by worsening climate change impacts, what can we do differently to keep communities safe?

It is heartening to see a new focus on research efforts to develop new response ideas, and some may ultimately have practical applications. However, thus far, there do not appear to be any emerging ‘silver bullets’ capable of quickly solving the climate-driven disaster crisis, with rapid sustained action to reduce climate pollution, the only assured way of eventually stabilising temperatures that drive wilder weather.

So where best to focus new research efforts? There is significant evidence that investment in the prevention, mitigation and resilience spaces can reduce the impact of disasters, with the Australian National Emergency Management Agency (NEMA) finding that every dollar invested in disaster risk reduction can generate savings of A$9.60 (Chow et al., 2023). We also need to be cognisant that those most affected by natural disasters are often the least able to afford increasing insurance premiums (Cassidy, 2023; Insurance Council of Australia (ICA), 2024), with insurance a key component of resilience, or the ability to ‘bounce back’ after a disaster.

There has been much discussion about disaster risk reduction and resilience, and some notable examples of progress due to changes implemented in the last 4 years. The current Australian Government has vastly increased investment in disaster preparation and prevention, matched by co-investment from states and territories (NEMA, 2025). There have been several recent reviews of disaster risk reduction, including Australia’s progress on the Sendai Disaster Risk Reduction Strategy 2015–2030 (NEMA, 2022), and the more recent Independent Review of Commonwealth Disaster Funding (Colvin, 2024) of disaster arrangements and governance. Such reviews are valuable as they help quantify the benefits of greater investment before a disaster, and how it can reduce expenditure after an event.

In healthcare, the cost-effectiveness of early intervention programmes has long been known and accepted – for example, reducing obesity through better diets and exercise programmes can reduce healthcare costs associated with diabetes and coronary disease. This knowledge and experience illustrates a critical opportunity for research effort in the emergency management sector: how to increase the focus on disaster risk reduction and resilience so that communities are better prepared, and response and recovery costs can be reduced.

By necessity there must be a continuous improvement in response and recovery because the increasing frequency and impact of disasters requires a rapid, comprehensive response to save as many lives and properties as possible, and after an event, comprehensive recovery efforts are necessary to rehouse those directly affected and get communities back to normal functioning as soon as possible. However, this should not come at the expense of proactive measures to better prepare communities and critical infrastructure before a disaster.

Much has been researched and written about disaster risk reduction, community resilience and the cost-effectiveness of early intervention programmes. Yet in Australia, we see practical implementation of strategies such as the buyback of flood-prone properties sometimes floundering due to a range of factors, including cost (McLeod and Ittimani, 2024). This underlines a need for more research into how such programmes can be better designed and implemented to improve their speed, efficiency and effectiveness.

In some communities devastated by disasters, there have been spontaneous responses to develop local capacity to improve disaster resilience, sometimes driven by dissatisfaction with a perceived one-size-fits-all response by governments. In the hard-hit Northern Rivers region of NSW, community-driven organisations have grown spontaneously in response to fires and floods. Resilient Uki (2024) and Plan C (Plan, 2024) are two examples of grass roots efforts to design multifaceted community resilience programmes targeted at identified local needs. These two programmes have achieved significant local buy-in and support, with participants far more aware of the risks they face and what they can do to reduce their vulnerability.

With this experience in mind, further research into how centralised government approaches can be more flexible and accommodate unique and differing community needs would be beneficial, and research into how best to build social connection and collaboration between spontaneous community responses, non-government organisations, and government agencies including the emergency services.

In summary, evidence of the escalating impacts of climate change now surrounds us. This should serve as an urgent call to action, both in mitigation of climate pollution as quickly as possible, and also in adapting to worsening impacts. Disaster risks will continue to increase until mid-century due to greenhouse gases already in the atmosphere, no matter how quickly we reduce pollution (Commonwealth of Australia, 2020). This means that emergency response and recovery agencies globally will become busier and increasingly face out-of-scale disasters that threaten to overwhelm them. Australia will not be immune to this challenge which in turn underlines the urgent need to broaden thinking and place greater emphasis on community resilience, preparation and disaster risk reduction.

3. Breaking the Catch 22: an affordable and profitable insurance industry

Thomas Mortlock and Peter Cheesman

The insurance industry in Australia and overseas is at the forefront of building economic resilience to climate change, most notably in the form of transferring risk associated with extreme weather events. By providing insurance cover for natural catastrophe events, individuals, businesses, and governments can transfer a portion of this risk to national and global (re) insurance markets. Through this process, catastrophic weather-related risk is transferred and diluted across global markets. As long as the fine balance of premiums being higher than claims costs, yet still affordable – is maintained in the long term – the system works well, and ‘oils the cogs’ of economic growth. In fact, this mechanism has allowed economies to grow over the past several hundred years despite the physical damage caused to assets and infrastructure from extreme weather events.

In many parts of the world, climate change is modifying the frequency and magnitude of insured weather events, such as cyclones, floods, wildfires, and convective storms. This – along with several other factors – is shifting the delicate balance between (re)insurer losses, the cost and availability of insurance, and the ability of insurers to purchase adequate cover. When this happens, the result is either a widening of the insurance protection gap (the difference between the value of all assets in an economy and the value of insured assets), or pervasive under-insurance. The second outcome is often a precursor to the first, whereby in response to unaffordable premiums, insurers reduce their coverage by either making policy exclusions or reducing their sums insured.

The above outcomes may occur in an environment where insurers are free to price according to the underlying risk. In such a market, if, for example, a property next to a river gets flooded more frequently now than it did 20 years ago, the insurer is free to price for this increased risk. As a result, the premium may become unaffordable for the homeowner, but it also becomes a problem for the bank lending on the property, and government levying taxes on insurance. In Australia, insurers have been undertaking ‘risk-based pricing’ for over 10 years (since the Brisbane 2011 floods).

Before this, ‘community-based pricing’ was more common, where pricing was undertaken at suburb levels where risk was more evenly shared. Now, only those having climate risk at their property location pay, with no contributions beyond those directly at risk. There are arguments both for and against risk-based pricing, as while it acts as a clear risk signal to deter development in high hazard areas, it also contributes to the insurance affordability issues experienced by those already living in these areas.

Due to this risk-based pricing environment, Australia’s variable and extreme weather setting, and several pressures currently impacting discretionary income – in addition to climate change driving up the hazard – insurance affordability has emerged as an acute, and growing, issue for many Australian homeowners.

In other jurisdictions, such as California, for example, the rising risk profile cannot be adequately priced for by insurers because of a State-imposed premium cap designed to protect against unaffordable premiums. However, this ends up resulting in an insurance availability, rather than affordability, issue, as it becomes no longer profitable for insurers to underwrite business in areas where they can no longer properly price for the underlying risk.

To maintain the balance between profit and loss in the face of climate change, insurers are behind efforts to improve the resilience of the built environment to acute climate risks. Risk transfer is no good if everywhere is getting riskier. Risk is the confluence of hazard, exposure, and vulnerability. While the hazard component can only be reduced through global carbon mitigation efforts, a more tangible and short-term route to addressing the underlying risk is to reduce exposure and vulnerability. Exposure refers to ‘stuff in the way’ – that is where we choose to live. In both Australia and overseas, we see that exposure growth explains most of the upwards trend in insurance losses over the past several decades. In other words, as urban centres grow, the bullseye for extreme weather events is getting bigger. To a certain extent, this can be constrained by developmental controls that better consider the natural hazard environment, particularly in floodplains and in the coastal zone.

Unfortunately, tighter developmental controls squeeze housing supply, which is a problem for another intergenerational trend – housing affordability. Insurance affordability and housing affordability, therefore, have a common thread that is working in opposite directions. How to solve for this problem will require careful consultation and collaboration between government, insurers, and financial institutions, to make sure that market and legislative forces are all working in the same direction on this issue. In Australia, we will need to ensure that the increase in housing supply required to match population growth in the coming decades is not to the detriment of affordable and available insurance needed to protect homeowners and businesses against growing climate risks.

In addition to controlling exposure, Australian insurers can also influence the vulnerability of the built environment to climate risks through advocating for better building codes and standards and encouraging more climate-resilient design. While future exposure growth is important, we are still living with a legacy of existing development that lies in (increasingly) hazardous areas. Some insurers are now offering discounted premiums for homes that are retrofitted with more resilient building materials. Likewise, some banks are beginning to offer ‘resilience loans’ to finance these retrofits. Ever-more-granular analytics on property characteristics can also help insurers understand the in situ risk better, and price for it. High premiums may reflect uncertainty (and therefore conservative pricing) on the risk at a property, rather than the true risk that exists there. Insurers also have a vested interest in ensuring that Government hazard mitigation schemes, such as flood levees, maximise risk reduction. Likewise, government should have a vested interest in ensuring these schemes deliver maximum insurance benefit to communities.

Indeed, the parliamentary inquiry into insurers’ responses to the 2022 floods (Parliament of Australia, 2024a) recommended that no new developments occur in high-risk areas, and that there is ongoing commitment to household and community hazard mitigation. The inquiry also recommended that building codes and planning rules be strengthened and future-proofed to improve resilience in accordance with projected increase in risks based on climate modelling.

Finally, insurers also have a role to play in the energy transition. First, insurance attracts and scales investment in green technologies that underpin the transition away from a fossil fuel-based economy. These may include renewables, such as wind or solar farms, or carbon extraction technologies, such as carbon capture and storage. Without insurance to de-risk investments, there would be no capital flowing to these new technologies. Second, is the move towards ‘net zero underwriting’. Over the past half decade, there has been a significant shift in appetite away from underwriting assets linked to coal. Over the coming half decade, insurers (along with other companies) in Australia will be required to disclose the emissions associated with their underwriting activities (which makes up the bulk of their scope 3 emissions). While this shift in appetite away from underwriting coal occurs, it could be argued that there still needs to be sufficient market capacity to continue to underwrite some hard-to-abate sector companies – that have a credible, certified transition plan in place – as they look to complete their own transition pathway.

Even if we zeroed global carbon emissions tomorrow, physical climate risks are baked in for decades to come. An affordable and competitive insurance marketplace is a first-order economic defence against physical climate impacts – and it is in everyone’s best interest to maintain. The single most significant risk to the insurance industry from climate change in Australia and overseas, is to remain affordable, yet profitable. Climate change both increases the need for, and cost of, insurance, and it should be a focus for the insurance industry to find ways of breaking this catch 22. There is a significant opportunity for the industry to capitalise on this renewed relevance. By creating innovate risk-transfer products to serve new markets and applications, working more closely with governments and financial institutions, and trending towards an ethos of net zero underwriting, the insurance industry can continue to close the protection gap while incentivising the transition away from fossil fuels.

4. Making the energy transition accessible to all

Penny Joseph, Marissa Papas and Shannon Moffitt

In Australia, the energy transition narrative has concentrated at the two ends of the energy supply chain; on one end, it has focused on large-scale generation and at the other on consumer energy resources. Network distributors, who manage the ‘poles and wires’ in the middle of this supply chain, have largely been hidden from view but are vitally important to a cheaper, faster and fairer transition. Adjusting policy and regulatory settings to enable network distributors to play a greater role is a significant opportunity. At the same time, the changing climate is a significant risk to the physical resilience of distribution networks.

4.1. Electricity network distributors have an opportunity to deliver a cheaper, faster and fairer transition

Electrifying households, industry and the broader economy is critical in mitigating the worst impacts of climate change. It also unlocks an opportunity to enable a cheaper and fairer energy system. Households that invest in efficient, all-electric homes can make significant savings compared with households that do not. Energy Consumers Australia (2023) estimates that the savings from installing a solar-battery system could be as high as $1250 p.a., while the Institute for Energy Economics and Financial Analysis (IEEFA, 2023) calculates that an average household could save a similar amount each year just by replacing gas appliances with efficient electric alternatives.

Despite the financial benefits, there are barriers that prevent many Australian consumers from electrifying. Initial capital is needed to electrify a home or business, locking some customers out of accessing longer term bill relief. Others may be locked out of the benefits of electrification simply because they live in an apartment or rent.

Distributors, as regulated utilities are well positioned to help enable solar and battery installations for households at the lowest possible cost. Ausgrid, the largest distributor of electricity on Australia’s east coast, is in the early stages of developing a pilot to test this initiative within a boundary of our network called a ‘Distribution Energy Zone’ (DEZ). We envisage customers could sign up to the DEZ via a subscription model or other payment structures that promote a cheaper, fairer energy transition.

If battery storage capacity envisaged to go into Australian homes over the next 25 years at the consumers’ expense were instead to be provided by community batteries, this would save billions of dollars. Batteries can be installed on land close to substations, keeping them out of sight and bringing connection costs down. Community batteries also share the benefits of solar with those renting, or who live in apartments or who cannot afford personal batteries. Allowing network distributors to connect community batteries into the grid at scale with the appropriate level of community consultation, would not only facilitate the journey to net zero but it would also create a more stable network and offer cost-of-living benefits.

Another example of the role distributors can play is the availability of EV charging, which is often pointed to as a barrier to EV adoption. Australia has a ratio of 68 cars per public charger whereas The Netherlands has 5. The problem is further exacerbated by around 30% of Sydney residents not having access to a garage or driveway. This presents an opportunity to use poles and wires differently. Regulated network distributors can install chargers at scale, ahead of the demand curve, and ensure they are maintained, much like streetlights.

These examples demonstrate that distributors can ensure greater access for more people to take advantage of the benefits of the energy transition and enjoy a faster deployment of renewables with a less detrimental impact on communities than current pathways. To help achieve this, the regulatory system could be developed to facilitate these solutions alongside governmental support to drive the scale required to bring down costs and speed up delivery. Long-term policy stability to provide businesses and consumers confidence to invest, and the coordination necessary to ensure that the efforts of diverse entities are complementary.

4.2. Network distributors must be resilient to the impacts of climate change

As electrification takes place, collective dependence on electricity supply will grow, and the electricity sector must carefully consider how it will respond to the new interdependencies that this will create. The progressive electrification of sectors such as transport, manufacturing and heating in commercial buildings will intensify the already highly interconnected and mutually interdependent nature of our infrastructure systems. For example, during the 2020 bushfires, across NSW 818 telecommunication facilities were affected, with 514 being impacted for 4 hours or more, causing additional distress, anxiety and risks for affected communities.

Australian network distributors will face more frequent and intense weather events. Climate-related events already have caused two-thirds of outages on Ausgrid’s electricity over the past 15 years, and without intervention are expected to grow by 1% per year due to climate change. Significantly, the impact of climate events is not experienced evenly, with some of the most socioeconomically disadvantaged cohorts experiencing 10 times the length of outages than the average customer.

The Australian Energy Regulator has released a guidance note on how distributors should consider the impacts of climate change. While this enables some investment, the guidance is still in a formative stage; for example, it does not say what climate scenarios to analyse or how analysis should be done. Ausgrid was among the first distributors to apply the regulatory note for its FY25–29 regulatory submissions and will invest in wind resilience (replacement of bare conductor with covered conductor to reduce vegetation-related faults), bushfire resilience (by wrapping poles with resistant materials), improving response effectiveness (by installing fault indicators to assist with effective crew deployment) and building community resilience (helping vulnerable customers be able to withstand electricity outages).

Like the energy transition, the regulatory environments must adapt to enable investment in resilience. For example, currently Australian networks are regulated to ‘maintain’ service outcomes. Regulatory change is required for them to be able to ‘improve’ outcomes for customers.

4.3. Network distributors are committed to their changing role

Australian distributors have already demonstrated their commitment to help customers navigate the energy transition and to establish access for all customers to participate. For example, Ausgrid is streamlining connection processes, providing automated approval for EV charging infrastructure, sharing data on network capacity with partners and providing guidance to customers thinking of changing over appliances or buying an EV. Unlocking further opportunities for distributors to contribute is key to the transition and reinforces the need for policymakers to consider the missing middle; the network distributors who operate the poles and wires, and the opportunities they can unlock.

5. Funding the future: sustainable finance and the decarbonisation of Australia

Bill Bovingdon and Anthony Michael

Drawing on the Australian Government 2023 Intergenerational Report, over the next decade, the single most significant risk associated with climate change for the funds management industry in Australia is a failure to mobilise sufficient capital, in sufficient time, to enable decarbonisation, which is the prime investment imperative of our generation. Success, on the other hand, will not only enable action on climate and the creation of new era industries but will also provide an opportunity for Australia to grow as a regional financial centre, bringing with it economic, social and political benefits.

Much must happen this decade to meet the decarbonisation targets agreed under the Paris Agreement and thereby significantly reducing the risks and impacts of climate change. It is estimated that by 2030, the investment required globally for climate action that aligns with achieving the targets will amount to around $6.3–$6.7 trillion per year (Bhattacharya et al., 2024: 11). This has given rise to a ‘green industry race’ between the United States (notwithstanding some inevitable rollback from the current US administration and the unpredictable impacts of their still evolving tariff regime) and the European Union who, in a bid to catch the market leader, China, have been providing generous green subsidy programmes to incentivise investment and innovation in renewable technologies.

Many major economies are intent on securing positions in the nascent supply chains that will dominate these new industries, for both economic and national security reasons. As a result, global energy investment is ‘set to exceed USD 3 trillion for the first time in 2024, with USD 2 trillion going to clean energy’ (International Energy Agency (IEA), 2024: 8).

The global green industry race means fierce competition for resources, technology and skills. In Australia, the energy transition will require investment at least comparable to the $200b invested in mining over the last decade. Given Australia benefits from preferred partner status under the US Inflation Reduction Act 2022 (IRA), that activity will be more widespread and integrated than was the case during the mining boom.

Against this backdrop, the key opportunity for Australia’s funds management industry is to develop a ‘turbo-charged’ Sustainable Finance Market, with an increased share of systemically important global funding markets, such as Green Bonds. Australia’s capital market expertise and well-established capital market infrastructure means it is well placed to become a linchpin for channelling local and foreign investment into regional projects, creating profitable investments with environmental and social impact.

5.1. Creating a sustainable finance market

The development of a deep and trusted sustainable finance market in Australia is essential for meeting the challenge of financing decarbonisation. Capital with a preference for sustainable development is ready and waiting. For example, in the year ended 2023, Australia’s total managed funds reached A$3.9 trillion, with Responsible Investment (RI) assets under management (AUM) growing to A$1.6 trillion – a 24% annual increase. Climate change remains the top priority among these investors (Dandarvanchig et al., 2024: 8–9).

The Responsible Investment Association Australasia (RIAA) also notes that long-term performance in products that it certifies have ‘generally demonstrated strong performance, particularly over the medium to long term (five, and ten years)’ but also observes that ‘greenwashing’ concerns have escalated to become the top barrier to growth in the market, with more than half of respondents citing it as a major deterrent (Dandarvanchig et al., 2024: 23). Greenwashing (in this case, misrepresentation of the sustainable credentials of investment products) undermines confidence in market integrity and is a key contributor to the risk of failure to marshal sufficient capital. In response, Australian regulators such as Australian Securities and Investments Commission (ASIC, 2025) have recently held several funds to account for overreach in sustainability claims, a long-term positive, but a short-term hit to confidence. Better sustainability reporting and clear taxonomy guidance will be key to expanding investor demand.

In addition, Australia has been plagued with unnecessary investment uncertainty for decades due to a lack of political bipartisanship on climate and energy policies, while the significant rate of technological change makes early-stage investments particularly challenging for private capital. This lack of consistently supportive government policy and regulation has stymied the development of sustainable investment as a central part of Australia’s most significant pool of savings, the A$3.9 trillion Superannuation industry. Here, RI or Sustainable Investment options are rarely offered as a default option. Moreover, there is a lack of ambition in the sustainable choices that are provided. For example, it is not uncommon to offer investment options where only 10% of the portfolio is invested in climate solutions or is constructed from passive index strategies that are not fit for purpose.

The lack of consistent policy direction in Australia has also arguably fed into suboptimal regulation – the ‘Your Future, Your Super’ performance test is seen by many as having too short an investment horizon for assessment, and lacking representative benchmarks for sustainable investment (which by its nature constrains exposure to many sectors contained in traditional benchmarks).

The opportunity exists for Australia to piggyback on 10 years of global development of best practice and fast-track our way to a larger and more diversified sustainable finance market. Europe has been the forerunner with policies and regulation supportive of all forms of sustainable investment, including debt, equity and asset-backed securities. European policymakers and the finance industry have collaborated to create a clear regulatory framework (or ‘taxonomy’), which provides credibility and transparency. A large and growing investor base has been supported by ongoing investor education and the encouragement of clearly defined Sustainable investment options.

From the first Green Bond issued back in 2007 by the European Investment Bank, there has been steady progress with involvement of other quasi-sovereign and Sovereign Benchmark Issuers from across the region, together with, financial and non-financial issuers from key industries. Proceeds from green bonds have allowed the energy sector to begin a move away from fossil fuels and to finance grid connection for renewables. Property companies and Trusts have also issued green bonds. These have been used to finance water and waste efficiency measures and to reduce the carbon footprint of their buildings.

The establishment of the ‘European Green Bond Standard’ has further boosted the market, and today, green bonds outstanding exceed US$3.2tn (Climate Bonds Initiative, 2024). This provides a clear pathway that Australia can follow, at pace.

5.2. Australia’s progress

Following a lost decade, significant progress has been made since the Australian Government announced a coordinated and ambitious sustainable finance agenda in late 2022. The Government’s Sustainable Finance Roadmap (The Australian Government the Treasury, 2024) outlines a plan to develop and reform financial markets to support the mobilisation of private capital needed to finance the transition to a net-zero economy, including providing a key pillar: its own green bonds. An inaugural issue of A$7 billion bonds took place in June 2024.

Following public consultation, an Australian taxonomy designed to create transparency and consistency and build confidence among investors is due for release in 2025. It will be a key foundation for Australia’s sustainable finance landscape and support international alignment and interoperability. Adequate disclosure is also key with the introduction of legislation requiring large businesses and asset managers to report on climate risks and transition plans commencing January 2025 (Parliament of Australia, 2024c). The legislation is largely aligned with international reporting frameworks, with entities required to report on their climate risk management and transition planning under higher and lower warming scenarios.

More broadly, the Federal Government has also committed further funding to the Australian Renewable Energy Agency (ARENA) and the Clean Energy Finance Corporation (CEFC) financing programmes (Department of Climate Change, Energy, the Environment and Water (DCCEEW, 2022). Other initiatives such as its ‘Powering Australia Plan’ (DCCEEW, 2024), the National Reconstruction Fund (Roe, 2024) and the ‘Future Made in Australia Act’ (Parliament of Australia, 2024b) are designed to respond to the ‘global green industry race’.

The opportunities for Australia are many, including the chance to become a full, card-carrying member of the global financial market, building on its globally significant savings market, mature sophisticated capital market infrastructure and experienced, well-qualified workforce to become a dominant regional financial centre. This would drive greater depth and diversity in the scope and character of its financial market. For cash and fixed income market investors, a fully-fledged corporate bond market with a significant representation of green bonds, would be an obvious ambition.

5.3. ‘Failure is not an option’

Fully grasping the opportunities from building a robust sustainable finance market would be aided and accelerated by further research into some of the major impediments to sustainable investment demand. This research would focus on questions such as: what information do investors need so as to be confident they can avoid greenwash? What would investors want to see alongside financial data when it comes to assessing the impact of their investments? Would more independent studies refuting the widely held notion that sustainable investment comes at a cost in terms of performance move the dial? And how do we ‘nudge’ Australian superannuation members so that they demand that their funds provide sustainable investment options as the default, rather than the exception?

The world’s major central banks and financial regulators, including Australia (Debelle, 2021: 3), have repeatedly warned that a ‘late and disorderly’ transition to a low-carbon society could be destabilising and disruptive, potentially causing ‘abrupt increases in risk premia across a wide range of assets’ (FSB, 2020: 1). This underlines the risk of not mobilising sufficient, timely capital for the transition to a low-carbon future. At the same time, it points to a significant opportunity for Australia; one where it embraces a leadership role that is focused on mitigating this risk by building on recent positive policy initiatives and becoming a major hub for sustainable finance in our region.

6. Discussion and conclusions: navigating the known unknowns

Ben R. Newell and David Grant

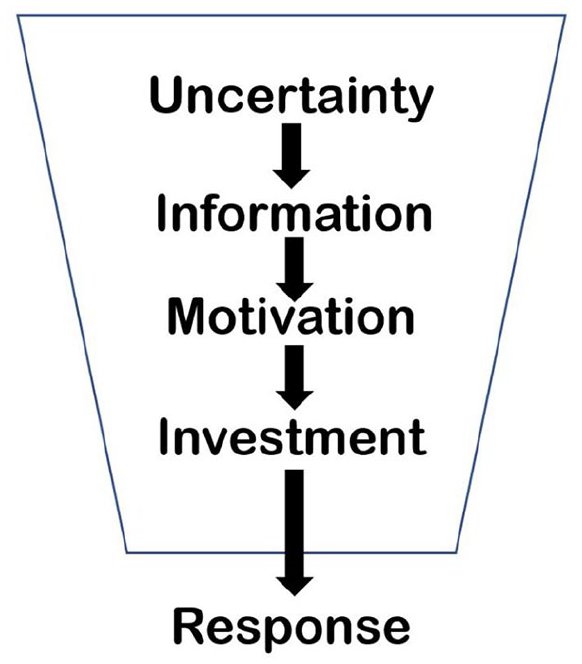

In this concluding section, we offer some insights aimed at achieving the key goal of this article: to propose research questions that management scholars will need to address if they are to contribute to the effective planning for and implementation of responses in Australia to the risks and opportunities of climate change. In doing so, we draw on four issues that surface as common and significant themes across the four essays: uncertainty, information, motivation, and investment. Figure 1 provides a schematic illustration of how we might envisage these themes interrelating in the pursuit of effective responses to climate change. Put simply, uncertainty needs to be reduced by the provision of information which will only be acted on if there is sufficient motivation which in turn will drive investment.

Responding to the risks and opportunities of climate change: Four themes.

6.1. Uncertainty

As we noted in the introduction, the concept of ‘known unknowns’ provides a useful framing for thinking about research needs that are on the horizon but not yet clearly formulated. Thus, characterising the nature of the uncertainties we face is a natural first step in generating research questions. In their respective essays, Mullins, and Mortlock and Cheesman both emphasise that physical climate risks and the disasters that they will cause are ‘baked in’ for decades to come, regardless of our current levels of (in)action, because of the effect of historical emissions on the climate. Such a conclusion is surely sobering but should also be enabling. Our overwhelming tendency to be ‘ambiguity averse’ (Ellsberg, 1961) and look for other options in the face of uncertainty should now be overcome by our repeated experience with the impacts of climate change and the certainty we now have about future impacts and the need for response (cf., Güney and Newell, 2015). However, many uncertainties remain.

Perhaps most evident in the essays is the need for policy certainty. The need for policy certainty and the risks associated with its absence – especially the economic risks, is well documented (see e.g. Al-Thaqeb and Algharabali, 2019). Joseph et al. argue that in Australia, long-term policy stability is necessary for driving an effective energy transition (a view echoed by Mortlock and Cheesman), and more specific guidance (certainty) from regulators on the kinds of climate scenarios distributors should be planning for and modelling. Similarly, Bovingdon and Michael point to the lack of government policy-certainty and consistency as a key impediment to sustainable investment not only in terms of large-scale energy developments but also the decisions individuals can make about their superannuation. Mullins calls for the development of more effective policy for buy-back schemes in climate risk-prone areas; an outcome which would reduce affected communities’ uncertainty about what to do in the face of disasters (e.g. leave or rebuild).

These variants of uncertainty about policy direction and effectiveness point to several fruitful avenues for research. These include understanding the kinds of climate policies the Australian electorate will support – and thus that governments are more likely to propose and stick to (Leviston et al., 2024); further work on the impact of plausible future climate scenarios for effective business planning and policy development (Fiedler et al., 2024); and the types of policy responses and market-based instruments that can drive effective climate adaptation (Filatova, 2014; Sanchez et al., 2024).

6.2. Information

A simple (perhaps simplistic) way to think about reducing uncertainty is by replacing it with information. Information takes us from the known unknowns to the known knowns of the Rumsfeld matrix. Mortlock and Cheesman provide a clear example, noting that more granular information on Australian property characteristics (e.g. the kind of floor covering in a house) could reduce the uncertainty in premium pricing to better reflect the actual, rather than estimated in situ risk – thereby potentially making insurance more affordable. How best to obtain this information, as well how to communicate climate risks to individuals and businesses before building or buying new properties are urgent topics for research, with some work in the United States already showing the potential impact on behaviour and markets of providing ‘climate risk scores’ for properties (Fairweather et al., 2024; Hino and Burke, 2021).

6.3. Motivation

Provision of information alone is, however, rarely sufficient. To overcome the ‘frictions’ to the kinds of desirable behaviour change identified by Joseph et al. (e.g. uptake of batteries and EVs) and Bovingdon and Michael (e.g. default sustainable investment options, sensitivity to greenwashing), motivation to change is also crucial. Research focussing on how to achieve this ‘cognitive’ and ‘motivational’ alignment between individuals and those who wish to drive behaviour change, be that business, government or a combination of the two, is becoming increasingly important and relevant (Krijnen et al., 2017; Szollosi et al., 2025). Such approaches acknowledge that it is not only individual-level behaviour that needs to be targeted but also the systems and communities within which we operate (Chater and Loewenstein, 2023). As Mullins notes in his essay, research identifying the drivers of social cohesion and connectedness that can provide resilience and motivation to act is fundamentally important; a fruitful place to look is the painful – but also uplifting – lessons learned from the COVID-19 pandemic (Jetten et al., 2020).

6.4. Investment

Ultimately, for Australia to avoid the worst risks of climate change and to maximise the opportunities we must invest in our collective future. This message comes across very strongly in all of our practitioners’ essays. It is a message that is easy to write (or say) but incredibly complex to enact. Investment is required at many levels and via several channels. Mullins repeats the compelling argument from NEMA that a $1 invested in disaster reduction now, saves almost $10 of anticipated clean-up costs in the future. Joseph et al. cite the potential savings to individuals of upfront investment in electrifying one’s home. Overcoming this inertia to invest exemplifies our much-lambasted tendency to be ‘present-biased’ and to excessively discount the future (Duckworth et al., 2018).

At times, such criticism is unwarranted – not investing in solar panels and batteries may have nothing to do with being biased to the present but merely reflect an unaffordable goal (as Joseph et al. note). Not insuring one’s house might similarly be driven by lack of resources rather than absence of foresight. Nevertheless, research focussing on how in Australia we frame different climate futures (Constantino and Weber, 2021), how we decide on the right ‘discount-rate’ for climate change (Newell and Pizer, 2004) and, as Mortlock and Cheesman urge, discussions on innovative models for insurance, (Moss and Burkett, 2021) are all good candidates for precipitating investment against coming climate risks.

As Bovingdon and Michael argue forcefully, none of this kind of preparation will happen unless the required capital is mobilised in a timely and systematic fashion. Scholarly approaches that highlight the lessons learned from massive investments in jobs and infrastructure like that which occurred under The New Deal or Marshall Plan in the past (Kennedy, 2009; Reymen, 2004), and which evaluate new and innovative ways (e.g. the Green New Deal, hybrid Public–Private Partnerships, Green Bonds;) by which such levels of investment might be achieved and effectively deployed in the present (Bhutta et al., 2022; Boyle et al., 2021; Pinilla-De La Cruz et al., 2022) may be useful in helping to bring about this step change in how business and industry address climate risk. So too might approaches that promote the changes needed to create the kinds of agile, adaptable, ambidextrous organisations able to effectively leverage these new forms of investment (Bushe, 2021; Hugos, 2009; O’Reilly and Tushman, 2013; Sarta et al., 2021; The World Bank, 2024). These systemic changes together with changes in consumer attitudes, fuelled by concerted efforts to address greenwashing, and policy settings that make choosing sustainable investment options less effortful (Schubert, 2017), have the potential to help maximise the opportunities that climate change affords while minimising the risks it portends.

As we observed in our introduction, management scholars have the expertise and knowledge necessary to identify and help implement the responses needed to address the newly emerging risks and opportunities posed by climate change. Leveraging this capacity offers the discipline an important opportunity to meet the challenge set by those such as Hoffman (2021) of increasing the impact and relevance of its research while simultaneously contributing to climate action.

Gioia (2024: 93) observes meaningful attempts to address the climate crisis will likely emerge from and be led by industry. Indeed, there is plenty of evidence that this is starting to happen (Black et al., 2021). Thus, if we are going to seize the opportunity to help shape and bring about this transformation in Australia, we need to engage with industry practitioners so as to construct research agendas that prosecute the kinds of research questions that they need us to address. In this Engaged Problematisation article, we have demonstrated that one way of achieving this is to adopt an abductive research approach. It has allowed the formulation of an agenda and research questions focused on the four themes of uncertainty, information, motivation and investment. We do not suggest that this agenda is generalisable in that it should be applied to all Australian industry sectors. It is, after all, based on the experiences and expertise of those representing the four sectors of emergency management, insurance, energy transmission and finance. Rather, we believe that generalisability lies where the potential value of the abductive research approach we have adopted can be used to generate climate change–related research agendas across a range of industries.

In conclusion, the involvement of both practitioners and academics in putting together an agenda such as that outlined in this article allows, in our view, for research to occur where we can be confident of three things. These are (1) the veracity of the climate-related risks and opportunities the research focuses on; (2) that the right kinds of research questions are being asked and; (3) that the research outcomes generate theoretically informed, methodologically rigorous knowledge that will be of value to both the academy and industry. Given the imperative of addressing climate change, its effects on management and organisation, and the need to identify and put in place responses that effectively manage the risks and opportunities associated with it, these are vitally important attributes.

Footnotes

Acknowledgements

The authors would like to express their gratitude to AJM Deputy Editor, Catherine Collins as well an anonymous reviewer for their constructive feedback and guidance throughout the review process.

Final transcript accepted on 20 February 2025 by Catherine Collins (Deputy Editor).

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.