Abstract

As one of society’s grand challenges, climate change increasingly presents unprecedented consequences for businesses. Despite assumptions on the effects of climate change, the relationship between carbon emissions and the strength of a firm’s performance is unclear, subject to enduring debate, with mixed outcomes. This article provides a critical view of this relationship, focusing directly on firm growth, market value, and climate change effects. It considers the performance paradox—a contradiction between a course of action and an inability or unwillingness to manage, alter, or problem solve this awareness—derived from increased carbon emissions, and incorporates the effects of industry clockspeed and open innovation. Observing a sample of 640 high-tech manufacturing firms over a 7-year period, producing 4480 firm-year observations, and applying two-stage least squares (2SLS) panel regression modeling, we find that better firm growth generates more carbon emissions that impact negatively on market value of the firm. The study indicates that the positive relationship between prior growth and carbon emissions is more pronounced in high clockspeed industries, while firms that actively collaborate with partners to innovate weaken the negative relationship between carbon emissions and market performance. These findings help explain why despite increased attention on climate change strategies, firms do not (or cannot) actively reduce their carbon emissions while they are profitable. Implications of findings provide a pragmatic avenue to avoid this performance paradox.

Keywords

1. Introduction

Businesses and their leadership today face an intriguing dilemma. Anthropogenic climate change—the effects of human-induced activities leading to increases in global warming—is a broad problem for collective industries and for individual firms. As the UN Intergovernmental Panel on Climate Change (IPCC, 2021) notes, the scale of recent changes across the climate system suggests that global warming will continue to increase dramatically under all emissions scenarios, leading to a bleak future impacting society and raising unavoidable hazards and risks (see also Wright and Nyberg, 2017). This prediction recognizes that as a grand societal challenge, climate change is a long-term problem needing ongoing attention and business-level resolution (George et al., 2016). Yet, despite acknowledging the scale of the problem to address climate change (Hoffman, 2007) businesses and their executives continue to accommodate climate change around traditional, pragmatic approaches to strategy, seeing themselves as central actors in addressing the issue. Typically, they focus on immediate or short-term performance problems—on the next quarterly revenue goal and the measurable bottom-line (Bansal and DesJardine, 2014)—and on how or when it pays to be green (Misani and Pogutz, 2015) because of market demands.

Increasingly though, there is a realization (Gümüsay et al., 2020) that beyond this performance imperative, far from an existential business threat, climate change promotes new insights and opportunities, while raising philosophical dilemmas for organizational researchers (Harley and Fleming, 2021). Solving climate change and the institutional problems it raises is a shared mission because it is a moral response as well as an economic responsibility (Brownstein et al., 2021). In understanding the implications of climate change for business, however, a conventional narrative has typically focused attention on the intersection between business, politics, and climate change practice. The logical assumption taken is that firms will benefit from and grow in the long-run by reducing their carbon emissions (Henderson, 2021). With its direct link to human behavior, and recognizing the extent of climate change as a problem, the firm is viewed as achieving growth outcomes by adopting a logical reduction in and management of their carbon footprint; that reduced carbon emissions eventually results in better firm outcomes. In this article, however, and setting aside the politics shaping corporate responses to climate change (Wright and Nyberg, 2024), we highlight the paradox that this perspective raises. We illustrate that this performance assumption is not as simple as is typically portrayed, and that the pursuit of firm growth can generate carbon emissions that hurt its subsequent market value, opening the possibility of an alternative narrative on dealing with climate change and institutions.

There is already an elaborate set of discussions on the grand challenge of climate change, its impact on institutions, theoretical approaches, and the uncertainty that businesses face from it (see Ferraro et al., 2015; Henderson et al., 2020). With more attention paid to the impact of anthropogenic climate change, there is increased pressure on organizations to reduce their carbon footprint. Yet there also remains a degree of naivete on what business can and should do about the pressing issue of climate change and its myriad effects—a naivete that motivates this article. For ease of access in this article, taking the IPCC’s (2020) stance, we acknowledge carbon emissions as representative of climate change, recognizing that emissions epitomize the most measurable form of this threat.

Addressing climate change is increasingly among the most significant challenges that businesses and society face today (Dahlmann et al., 2019), especially given the role of business in generating greenhouse gas (GHG) emissions, in the form of carbon emissions, that have historically accounted for climate degradation (Damert et al., 2017). Despite the move toward incorporating sustainability into business models (Matos and Silvestre, 2013; Nyberg and Wright, 2022), the debate on climate change effects for business remains confusing, stereotypically revolving around whether measurable and reportable financial performance impacts broad environmental performance and vice versa (Busch and Hoffmann, 2011; Endrikat et al., 2014). It is this confusion that we focus on in exploring carbon emissions and firm performance. The common assumption motivating firm strategy on this challenge typically focuses on observing the serious impacts brought by climate change, and the phenomenon that if firms are destined to pursue growth according to the prevailing business logic, expanding business activities, such as production that simultaneously leads firms to emit more carbon emissions, becomes inevitable. Recognizing that the conflict between the pursuit of firm growth and the escalation of carbon emissions exists means that finding solutions to this conflict is a fundamental challenge for modern businesses. With this motivation, embedded in debate on the grand challenge of climate change as context, this article addresses one of these confusions in an emerging economy context, exploring the contradicting parts (i.e. the paradox) of the relationship between carbon emissions and firm growth; the performance paradox of when firms act in opposition to or ignore performance data (Cohen, 1998), an established theme raised variously in strategy (Back et al., 2020), supply chain (Schmidt et al., 2017), human resources (Ho and Kuvaas, 2020), and social capital (Raffiee and Byun, 2020) research.

Given their impact on climate change, research attention has often focused on big polluter industries, such as petroleum firms (Boon, 2019; Heede, 2014) or on large multinationals (Baird et al., 2012; Damert et al., 2017; Delmas et al., 2015; Doda et al., 2016). Yet recognizing the integrated challenge of global warming and public consciousness of environment, business leaders have increasingly focused on carbon reduction initiatives (Klein, 2015) and their organizational resilience requirements (Howard-Grenville et al., 2014). This approach is logical given both that it is a measurable outcome, and that is a widely regarded and emergent strategic initiative that appeals to investors (e.g. Van der Byl and Slawinski, 2015). Though this is encouraging, in recent years, as developed economy emissions flatten, as Ritchie et al. (2023a) show, the rise in global carbon emissions have come mainly from transitional and emerging economy countries. These markets generally serve the role of manufacturing bases in global supply chains (Engelen, 2019), where manufacturing activities usually consume more energy than other value-added activities, such as marketing or services (Reuters, 2020). For instance, US-based Apple manufactures its iPhone in China through a Taiwanese-based multinational (Foxconn), while its core processor is made by a Taiwanese entity (TSMC). In effect, this geographic spread means that 74% of Apple’s carbon emissions footprint comes from its suppliers based in emerging and transitional markets (Leswing, 2019). Notwithstanding this background, and recognizing that emerging economies are increasingly large carbon emitters (Fekete et al., 2013), Busch and Lewandowski (2018) meta-analysis shows that studies on transitional and emerging economies are limited. In this article, therefore, as part of its add-on contribution to understanding climate change impact, we focus on firm performance in one of the leading emerging market’s focusing on Taiwan’s high-tech industry, to complement earlier findings on carbon emissions in developed economies.

As its primary contribution, this article argues that although previous research shows the performance and societal implications of corporate environmental efforts (e.g. toxic release inventory, water pollution, and spills; Guenther et al., 2012), comparatively few studies have focused exclusively on the specific link between carbon emissions and financial outcomes (Busch and Hoffmann, 2011; Busch and Lewandowski, 2018; Delmas et al., 2015), especially for emerging economies. As we note above, those that do have either considered an amalgam of different effects alongside performance (e.g. views on resources, investor responses, market position, and strategy) or have concluded that a reduction in emissions positively affects corporate financial performance (Albertini, 2013). This latter view is logical given the uncertainty and risks associated with the business effects of anthropogenic climate change. Despite supporting evidence and calls for carbon reduction, however, on average global carbon emissions are still increasing (Ritchie et al., 2023b) raising allied uncertainty about long-term firm performance in this deteriorating environment; of reconciling the rationale that firm behaviors are driven by the pursuit of profitability, growth, and scale (Chandler, 1990; Penrose, 1959) which impacts environmental sustainability (Henderson, 2021). Rationally, performance matches firm adaptation and shapes to climate change. Core to the contribution of this study, and with this understanding, we propose and validate a cyclical approach testing the relationships between firm growth, carbon emissions, and market value.

To explore this theme, we ask: if firms face a performance/growth paradox, why don’t or can’t they reduce their carbon emissions? To do so we consider the scale, scope and timing of the carbon emissions in Taiwanese high-tech—the heartland of global high-tech manufacturing—by focusing on the nature of a firm’s emissions output and the contingent factors affecting this paradox and the possible solutions to address it. Therefore, we explore whether the external environment and internal factors can affect this relationship. Specifically, we examine how the external environment, represented by the industry clockspeed or rate of industry change (Fine, 1998; Nadkarni and Narayanan, 2007), affects this paradox. Clockspeed assesses the velocity of change in the external business environment as a means of setting the pace of the firm’s internal operations (Mendelson and Pillai, 1999). This measure enables firms to assess their reaction to change, providing benchmarks to compare and classify the organization, its performance, and subsequent carbon emissions. We also look at an internal factor—coupled open innovation or collaborative innovation across organizational boundaries—that may make it possible to sidestep this paradox, because various studies have previously suggested that an open innovation approach can mitigate grand challenges and social issues such as global hunger, health issues, and climate change (e.g. Ahn et al., 2019; Sims et al., 2019). By investigating these two contingent factors through our research question, we are able to better capture and understand this paradoxical relationship. Our study complements previous research on environmental and financial performance by providing add-on evidence regarding which firms do or do not engage in climate action and which can practically mitigate the harm to performance caused by a given level of carbon emissions.

2. Theoretical background on a grand challenge for firms

The scale and challenge of climate change is stark. It is widely agreed that the world is observing unprecedented change across whole climate systems, visible through extreme weather events such as floods, longer droughts, more frequent wildfires, and more intense tropical storms (IPCC, 2014). Unchecked, the consequences of climate change are likely to be severe and prolonged, with widespread and profound effects on governments, labor productivity, human health, investment, and societal systems we have come to rely on (see Fattorini and Regoli, 2020; Henderson, 2021). In this context, we reassert in this article that climate change is an intractable grand challenge that demands broad attention. Yet despite this foundation, firms face a complex set of tasks to reduce carbon emissions while at the same time remaining competitive globally and socially engaged. This aspect is confusing for industry—assuming that firms need to grow while minimizing negative global emissions outcomes.

The basis of the link between climate change and firm growth is long-debated, albeit with confusing outcomes (Busch and Hoffmann, 2011). Clearly, climate change challenges impact all facets of organizing, such as value chains and industry, organizational resilience, governance systems, work practices, and social choices (Howard-Grenville et al., 2014). Yet despite decades of research on trying to link environment and firm performance, the notion remains a contested debate. As Albertini’s (2013) meta-analysis on environmental and financial performance shows, notwithstanding assumptions of the causal relationship between environment and performance, there is limited understanding of the complexities between firm growth and internal environmental responses outside of this narrative. Moreover, within this realm, there is a strong tendency to present the impact of environment on firm performance in a linear way—that positive returns are linked to strong environmental management (and vice versa, Klassen and McLaughlin, 1996).

This focus recognizes the historical tendency to ignore the endogeneity between performance and growth, both of which enhance each other. Profitable firms pursuing growth (especially those in emerging economies; Peng et al., 2018), however, are likely to emit more carbon due to expansion in business scale or scope driven by corporate capitalism (Nyberg and Wright, 2022), which, in turn, harms their subsequent market value. With this framing, such research only captures unidirectional causality (i.e. emissions affecting performance), ignoring alternative causality (i.e. performance affecting emissions). Recognizing that this endogeneity may be related to the divergence between the empirical evidence supporting carbon reduction and the tendency toward increased carbon emissions in industries, in this article we consider whether firms are trapped in an endogenous performance paradox. That is, a paradox in which prior performance triggers expansions and, thus, a rise in carbon emissions that subsequently harm performance.

2.1. Carbon emissions and performance paradox

Central to our study is recognition that there exists a performance paradox related to global carbon emissions. As Cohen (1998) defined it, a performance paradox denotes a contradiction between a course of action and an inability or unwillingness to manage, alter, or problem solve this awareness (e.g. Abilene paradox, Harvey, 1974). That is, organizational members clearly know what to do to improve performance, but rationalize their response, and despite their instinct or data available (see Argyris, 2004). Key to this phenomenon in the context of climate change, as meta-analyses by Albertini (2013) and Endrikat et al. (2014) highlight, is recognition that after three decades of research the link between firm financial benefit and its carbon emissions or environmental policy remains the standard outlook; based on an expectation that there is a positive relationship between environmental performance and financial performance. This assertion focuses on an assumption that good environmental policy logically aligns with positive firm performance; that carbon emissions need to be part of a firm’s strategy, leading to tangible performance outcomes. With its basis in environmental research (e.g. Czerny and Letmathe, 2024), we question this reasoning by recognizing an underlying performance paradox between individual firm growth and carbon emissions.

Common questions asked of businesses typically revolve around existential themes of reacting to and dealing with evolving environment. The assumption is that organizations need to adapt and change while still operating within a competitive, performance-based model. Muddying the waters, however, is the perspective that value creation and growth is a widely accepted objective for the firm (Varaiya et al., 1987) and that is not always compatible with carbon emission adjustments. While empirical evidence generally suggests that reducing carbon emissions brings about positive performance outcomes (Busch and Hoffmann, 2011; Delmas et al., 2015), firms’ carbon emissions are still increasing (Jones et al., 2023). Accordingly, although many firms increasingly acknowledge the responsibility of needing to react to and limit carbon emissions, the potential tradeoff between emissions reduction and sustained financial performance restricts action. For instance, Delmas et al. (2015) and then Busch et al. (2022) note that carbon emission reduction has a negative effect on short-term performance but a positive effect on long-term performance, guiding the tenor of managerial decision-making.

The problem with such a focus on aspects of performance that is measured, however, is that it can be used to manipulate and constrain decision-making on climate into the future (Kor et al., 2016; Van Thiel and Leeuw, 2002). This notion corroborates a long-standing assumption that organizations focus primarily on short-term growth and thus, that they tend to continue investing in production to achieve cost advantages of scale and scope. The assertion is that firms are motivated to grow, and adopt strategy and business choices to facilitate this growth (Peng and Heath, 1996). This aspect reflects the gap we noted earlier which calls for firms to pursue growth and profitability as a matter of course. With this basis, profits are viewed as a necessary condition for growth and one that drives firms and their strategy (Penrose, 1959).

This logic, however, is challenged in the context of carbon emissions. To keep growing, a firm often follows an existing trajectory and tends to invest in what is best for its financial performance goals, which may then paradoxically lead to increases in the byproduct of carbon emissions. Rooted in Kerr’s (1975) recognition that firms may often signal one strategy but its executives adopt a different approach, this relationship challenges historically-based assumption on firm productivity that increased resources will always increase performance positively, regardless of emissions output. Yet carbon emissions reduction is an evolving challenge for firms. Despite its prominence as a material concern, few firms have extensive prior experience needed to tackle this problem directly. This effect is two-fold – (1) that firms rely on habit and previous strategy, leading to a focus on performance over emissions, and (2) that capital market pressure characterizes emissions negatively.

To reduce carbon emissions, firms need to adapt not only their operational routines, including energy consumption, manufacturing process, and technological procedures, but also their mind-set or the dominant logic they use. One way for firms to acquire these adaptation abilities is from their lived experience (Levitt and March, 1988). Organizations with past success in coping with challenges tend to adopt this retrospection because they usually interpret their history as a rationale for existing practices and logic (Askvik and Espedal, 2002). Consequently, this reaction makes firms less open to learning from new experiences and knowledge, and less ready to engage in the adaptation required by their business environment (Eisenhardt and Martin, 2000; Helfat and Martin, 2015). With the resultant habit, a success trap (Levinthal and March, 1993) forms. By continuing to exploit opportunities in the same activity domain, firms also tend to avoid the opportunity cost of exploration. As Cohen (1998) underscores, with this experience, firms risk maintaining the status quo when it comes to performance measures, continuing to engage in habit and the same activities to avoid uncertainty or high risk, regardless of outcome.

This reaction explains how, despite emissions data and ongoing climate-based challenges, the paradox is one of how firms can continue to increase their carbon emissions following prior positive performance that is explicitly linked to emissions management. At the same time, as firms increase their carbon emissions, the response of the market may not reflect positively (especially with growing government policy focusing on correcting climate futures). After all, investors and funding sources increasingly specify in their investment policies the aim to invest in firms that can help mitigate the threat of global warming. In addition, previous studies also provide evidence that firms’ increase in carbon emissions is negatively associated with market value (Al-Tuwaijri et al., 2004; Chang, 2016; Konar and Cohen, 2001). This outlook presents firms with intense capital market pressure to adjust their emissions while still emphasizing corporate performance. Thus, we propose the following:

Hypothesis 1 (H1). An increase in carbon emissions presents a performance paradox for firms.

Hypothesis 1a (H1a). Firm growth induces an increase in carbon emissions.

Hypothesis 1b (H1b). An increase in carbon emissions decreases a firm’s subsequent market value.

2.2. Translating speed: the role of industry clockspeed in impacting performance

As the IPCC (2021) notes, time, and relatedly, the speed, frequency, and intensity of climate change matters increasingly to anthropogenic carbon emissions. Accordingly, and given its use as a measure of performance effects—we focus on the timing orientation and speed of industry and industry segment change—clockspeed—as intrinsic to understanding firm performance in this evolving business environment.

Defined as the rate of industry change (Fine, 1998), clockspeed assesses the velocity of change in the external business environment as a means of setting the pace of the firms’ internal operations (Mendelson and Pillai, 1999). This measure enables firms to assess their reaction to change, providing benchmarks to compare and classify the organization and its performance. With speed as its basis, clockspeed is categorized as either fast or slow. These categories differ in various aspects, such as their rate of new product introduction and sustainable competitive advantage (Carrillo, 2005; Nadkarni and Narayanan, 2007). To succeed in fast-paced industries (e.g. semi-conductor), firms need to be flexible and execute change quickly or risk misfit with environment and competition. Firms in slower-paced industries (e.g. manufacturing) can be more measured, and achieve sustainable competitive advantage by changing more gradually. It is measurably clear that global warming’s broad impact is taking place far quicker than expected (Henderson et al., 2020), highlighting the value in understanding the role of speed and time to firm performance in tackling climate issues. Thus, with this cyclical temporal framing, we assume that the velocity and tempo of industry change moderates firm growth and carbon emissions.

The placement and fit of speed in organizational operations and its performance is previously well-established, based on evidence that firms attempt to match corporate practice to their environmental practices (e.g. Eisenhardt and Schoonhoven, 1990). Rooted in Lawrence and Lorsch’s (1967) evaluation of the moderating role of the rate of industry change, the speed of technological, scientific, and market changes can affect the relationship between organizational behavior and firm performance (Mudambi et al., 2012). In this context, clockspeed captures the rate of industry change driven by endogenous technological and competitive factors (Nadkarni and Narayanan, 2007). It denotes that industries are characterized by an internal measurement reflecting the speed of the cycle in terms of observed change, such as industry prices, new product development, production and inventory costs, and competitive factors that variously requires different processes, decision-making strategy, resource deployment, competitive actions and focus (Carrillo, 2005; Dedehayir and Mäkinen, 2011; Mendelson and Pillai, 1999; Mudambi et al., 2012). Technically, clockspeed focuses on the rate (i.e. frequency and span of changes) of industry change rather than its variations or scope because it focuses on changes that are endogenous (inside) to the industry and which affect the firm. This focus links neatly to a measure of firm responses to carbon emission change.

While clockspeed can capture a variety of different aspects on competitiveness such as strategic flexibility and actions, resources, or decision-making (Nadkarni and Narayanan, 2007), our focus in this article is at its simplest level, on the speed of change itself and the examination of the effect on the relationship between firm growth and their carbon emissions. To survive in fast-clockspeed industries, firms must introduce new product and process technology more quickly (Cottrell and Nault, 2004; Nerkar and Roberts, 2004) and carry out frequent strategic and organizational changes (Eisenhardt and Martin, 2000; Fine, 1998) to maintain strategic advantages. By contrast, slow-clockspeed industries are relatively stable, and do not require the same ongoing vigilance and response (Keck, 1997: 152).

The connection between industry clockspeed and the nature of a firm’s carbon emissions output is linked in two ways, relative to firm performance and environmental responsibility. First, a fast-clockspeed industry requires firms to constantly monitor and match its competitor’s actions (Nadkarni and Narayanan, 2007), which potentially leads to poorer environmental decisions and outcomes, related to increased carbon emissions. Previously, Klassen and McLaughlin (2001) establish this bond in showing how environmental performance and its management is clearly linked to firm performance and market value, In this fast-paced industry context, firms are driven to pursue profit-oriented actions due to competitive industry pressure. The belief in the need for growth is strengthened because firms often strategically match corporate practices to their business environment, believing that this approach leads to better performance outcomes (Chandler, 1962; Eisenhardt and Schoonhoven, 1990; Keck, 1997).

Second, firms need to continually evaluate and differentiate their positioning in the broader market, which impacts on the embrace or dilution of an environmental strategy (e.g. Wright and Nyberg, 2017). In this setting, as Hull and Rothenberg (2008) note, corporate social responsibility (CSR) plays a central role in enabling a firm to differentiate itself from its competitors, but is often done to conform to short-term market opportunities, which may explain why innovation diminishes the effect of CSR on financial performance over time (McWilliams and Siegel, 2000, 2001). The intangible nature of CSR is pertinent to understanding clockspeed given that while environmentally responsible practices reflect strategy other than profit, clockspeed influence focuses attention on competitive advantage and thus profit through speed to market. Despite the adoption of CSR-led “green management practices” (Babiak and Trendafilova, 2011) that are viewed in terms of reputation or societal benefit (e.g. decision-making for socially responsible organizations; moral and strategic imperatives for environment), these initiatives are marginalized by clockspeed conditions.

At the base of this dual view on clockspeed is that organizations often seek to manage an environmentally responsible posture guided partially by the need for regulatory compliance and partially by societal responsibility (Shrivastava, 1995) but framed heavily by the market, which then impacts on firm strategy and its performance. Firms competing in a fast-clockspeed industry need to innovate and allocate resources quickly to retain competitive advantages (Nadkarni and Narayanan, 2007), which minimizes or relegates long-term goal options, such as climate-related carbon emissions reduction. By contrast, in slow-clockspeed industries firms can use environmental and social responsibility to differentiate themselves from competitors (Klein and Dawar, 2004). Without the pressure for speed, such an engagement strategy can provide these firms with a competitive edge or reputational repositioning (Hull and Rothenberg, 2008). Asserting that fast industry clockspeed will bring about greater discrepancy between climate change and firm growth, we propose the following:

Hypothesis 2 (H2). A positive relationship between firm growth and carbon emissions is more pronounced in fast-clockspeed industries than it is in the slow-clockspeed industries.

2.3. Greening innovation: open innovation and the impact on performance

Firms have continuously viewed the need to innovate as a means to competitive advantage, and thus to increase growth and performance possibilities (Crossan and Apaydin, 2010; Lengnick-Hall, 1992). With this basis, as a measure of innovation performance, and in an environment of striving for improved efficiencies and competitive competencies (Chesbrough, 2003), open innovation has helped shape strategies for industries. Open innovation describes how firms innovate by interacting with other firms—that is, innovation derived from external sources of collaboration, rather than internal processes such as R&D (i.e. closed innovation) (Greco et al., 2016). Open innovation recognizes that the more firms interact with other organizations, the more access they have to resources and assets. This assumption is based on the expectation that firms need to be open to collaboration and to interaction to source knowledge, competencies, and relationships in a competitive way; that useful, shared knowledge creates value to the firm. Its strategies include coupled open innovation, which refers to active collaborations with partners to innovate (see Sims et al., 2019).

With mixed results relative to open innovation and performance (Greco et al., 2016), the pressure for firms to succeed and perform (Hung and Chou, 2013), especially in emerging economies (e.g. Kafouros and Forsans, 2012), feeds into existent tensions with climate change and business pressures. Whereas the focus of much discussion on innovation and climate change focuses on policy development, or the role of markets and policy in delivering on climate change mitigation (Lee and Min, 2015; Newell, 2010), the question remains: To what extent can firms openly share innovation knowledge when carbon emissions make the firm vulnerable to the market? Given its focus on value creation, open innovation presents an integrated way forward for dealing with this competing demand between firm interests and environmental challenges, and the performance paradox this holds.

This link is relevant to understanding the problem that carbon emissions presents for firms, given how open innovation helps identify opportunities that are beyond their current knowledge boundaries. As Dittrich and Duysters (2007) highlight, the breadth of innovation is measured by the extent to which it is anchored to the firm’s knowledge base—the difference between local versus distant search (i.e. between capabilities close or distant to the firm’s current capabilities). Dealing effectively with carbon emissions in a performance paradox presents firms with a novel problem, despite its extensive global spread, so searching for new opportunities outside existent (local) boundaries enables more diverse outcomes, resulting in better solutions and performance (Mazzola et al., 2012). This activity requires constant dialogue among different external players, which also makes open innovation an attractive choice for firms dealing with climate change challenges given its variability.

Coupled open innovation is a type of co-innovation with complementary partners through structured cooperation, which often involves a set of inter-firm relationships and recombination of external knowledge with existing knowledge (Mazzola et al., 2012; Schumpeter, 1934). It refers to the exchange of knowledge and collaboration across and between different firms to innovate. Several representations of coupled open innovation have been identified, including establishing a platform between firms, co-patents, and R&D alliances. It is widely regarded as a viable method to solve complicated problems due to its nature of constant exploration with different partners (Enkel et al., 2009; West and Bogers, 2014). When collaborating with different partners, a common language is needed and increased interactions are required. By focusing on complex social problems, such as the grand challenge of carbon emissions, firms show their capacity and determination to maximize the probability of discovering a high-value solution, which requires a mechanism that can efficiently govern the search process (Nickerson and Zenger, 2004). Whereas market forces suggest reacting to climate change as a strategy solution, coupled open innovation and its collaborative knowledge sharing facilitates an alternative pathway to market performance.

With the expectation that firms devoted to innovation create growth (Kor et al., 2016), firms trying to solve a complex problem by using the coupled open innovation method also send a clear signal to stakeholders that they intend to truly face the problem, with attendant performance outcomes. Firms usually announce their collaboration with other technology partners publicly with this outcome in mind. Recognizing that increased carbon emissions make a firm vulnerable to negative market valuation (Matsumura et al., 2014), and thus partnerships, the adoption of coupled open innovation provides potential solutions to manage emissions but also as a signal to the market that the firm is attempting to solve its contribution to global warming. For example, in the mature product market of personal computers, in 2015 Acer highlighted their efforts to address emissions in the production of their Chromebook C740 by publicly linking their processes to Taiwanese government standards, having “set out a plan to broaden the carbon footprint inventory across indicator products, completing a carbon footprint report for the Chromebook C740” (Acer, 2015). Since most stakeholders understand there is no simple solution to carbon emissions management (e.g. carbon capture and storage is still in its nascent stage; Klein, 2015), this attempt by the firm was aimed at helping allay investor’s concerns about its emissions output.

Given its basis for providing competitive surety through open innovation (Chesbrough, 2003), with its structured cooperation in mind, and given the existence of a performance paradox, the adoption of coupled open innovation can thus be a way to minimize the carbon emissions–performance paradox. With this basis, we explore the following:

Hypothesis 3 (H3). Firms’ engagement in coupled open innovation weakens the negative relationship between carbon emissions and subsequent market value.

3. Methodology

3.1. Sample and data

To test our hypotheses, this study focused on Taiwanese electronics firms. Taiwan is considered a rapid growth economy using economic liberalization as its primary engine of growth (Hoskisson et al., 2000: 249), and has been the manufacturing base for global high-tech products since 1980 (Engelen, 2019). Focusing on Taiwan enables testing firm growth and carbon emissions in a broad, generalizable, and relevant market context. While the fossil fuel industry is the major producer of global greenhouse gas emissions (CDP, 2018), the electronics and high-tech industry accounts for 12% of global power consumption (and growing, Greenpeace, 2019). In this sector, 80% of power consumption is related to manufacturing activities along the supply chain (Greenpeace, 2019). Given their low involvement in manufacturing activities, we excluded information service, distributors, network and communication service sectors from the sample. Consequently, the final sample contained 640 listed high-tech firms in four industries—namely, semiconductor, optoelectronics, computer & peripheral (PC), and others.

For the empirical analyses of this study, we combined data from two sources—an economic database and annual reports. The study archived the data regarding firm characteristics and financial figures from the database maintained by the Taiwan Economic Journal (TEJ), which provides the most comprehensive information on listed firms in Taiwan and has been widely adopted in academic research when it comes to Taiwan and related emerging economies (e.g. Chen and Jaw, 2014; Chiu and Wang, 2015; Weng and Cheng, 2019; Yang and Schwarz, 2016).

The data for carbon emissions were collected from the CSR module of the TEJ database, which has recorded firms’ self-reported emissions figures since 2012. These data were validated by the firms’ electricity usage in the same period. The data concerning firms’ engagement in coupled open innovation were identified, documented and counted separately from the annual reports of the sample firms. The observation timeframe was set between 2012 and 2018 due to data availability on carbon emissions.

3.2. Measures

3.2.1. Dependent variable

Tobin’s Q is considered an adequate indicator when analyzing corporate environmental performance, as it reflects reputational effects, investor trust and investor risk (Guenster et al., 2011), and has been previously used by Misani and Pogutz (2015) to measure carbon impact on performance. Tobin’s Q is defined as the ratio of the market value of a company to its book value (i.e. the replacement costs of all assets) in TEJ. In parallel to the measure of the independent variable (carbon emissions), which was measured in terms of change rate, the study measured Tobin’s Q in terms of its change rate between two consecutive years (i.e. (Tobin’s Qt + 1-Tobin’s Q t )/Tobin’s Q t ).

3.2.2. Instrumental variables

This study employed two-stage least squares (2SLS) panel regression models to account for potential endogeneity bias (Antonakis et al., 2014) between growth and carbon emissions. Following relevance and exclusion restriction criteria (Imbens, 2014; Roberts and Whited, 2013), we selected an instrumental variable to eliminate possible endogeneity in the study, namely the scale of production as measured in terms of the number of plants of a firm.

3.2.3. Independent variables

Given the logic of the theory of firm growth, growing and profitable firms are likely to emit more carbon due to expansion in business scale or scope driven by corporate capitalism (Nyberg and Wright, 2022). Firm growth was calculated as the percentage change in total sales between two consecutive years.

The second independent variable measuring the relationship between firm growth and firm performance is carbon emissions. A meta-analysis on the relationship between corporate carbon emissions and performance summarized the two most commonly used measures of carbon emissions: annual carbon emissions and carbon reduction (Busch and Lewandowski, 2018). To mitigate the concern of endogeneity, this study adopted the perspective of reduction (Gallego-Álvarez et al., 2015) and measured Carbon emissions by calculating the change rates of carbon emissions disclosed by the firms between two consecutive years. The calculation can be formulated as follows

where i represents a certain individual firm, t represents the time of year t and the amount of carbon emissions included Scopes 1, 2, and 3 (in tons). A positive value of the variable indicates an increase in carbon emissions, whereas a negative value signifies a decrease in carbon emissions, as compared with the previous year.

3.2.4. Moderating variables

Having previously defined industry clockspeed as the rate of industry change (Fine, 1998; Nadkarni and Narayanan, 2007), fast-clockspeed industries experience frequent changes, and thus firms “require flexibility to cope with the flow of opportunities that are typically faster, more complex, more ambiguous and less predictable” (Davis et al., 2009: 414). By contrast, firms in slow-clockspeed environments emphasize stability over flexibility (Mudambi et al., 2012). The definition of industry clockspeed in the literature suggests that the distinction between low- and high-clockspeed industries can be based on the R&D activities at the industry level (Berger and Gattorna, 2001), because firms in high-clockspeed industries must continuously reengage in scanning and searching activities and move from one innovation to another by committing to intensive R&D investment in order to maintain superior performance (Mudambi et al., 2012). In addition, the deployment of R&D activities of firms in high-clockspeed industries must also be flexible enough to adapt to rapidly changing environments. Thus, it is expected that both the intensities and volatilities of R&D at the industry level should be higher in high-clockspeed industries than in low-clockspeed industries.

As our sample data constitute four major sectors in the Taiwanese high-tech industry, the R&D patterns of the four sectors may differ. This study conducted a priori test (ANOVA) to examine the differences in R&D patterns among the four sectors. The results confirmed that the average R&D intensity of the semiconductor sector (RDI = 12.24%) was significantly higher than that of any of the other three sectors (mean RDI = 3.83%, p < .01 for all post hoc tests). Meanwhile, its R&D volatility, as measured by the standard deviation of the R&D intensities, was also significantly higher (p < .01) than that of the rest three sectors as a pool. These statistics show that the innovation activities in the semiconductor industry were intense and that the adjustment of R&D activities was flexible. Thus, the study considered clockspeed in the semiconductor sector to be the fastest of the four sectors. We used a dummy variable to represent the semiconductor industry (D = 1) and otherwise (D = 0), where the semiconductor industry represents the high-clockspeed group and other industries represent the low-clockspeed group. This measurement is consistent with studies by Fine (1998) and Nadkarni and Narayanan (2007). The dichotomous measure of industry clockspeed is similar to that used in Mudambi and Swift’s (2011) study.

Coupled open innovation measures the extent to which firms engaged in bi-lateral innovation activities with complementary partners across organizational boundary (Mazzola et al., 2012). This study selected nine types of two-way activities from the open innovation activities discussed in the literature (Chesbrough and Crowther, 2006; Gassmann and Enkel, 2004; Mazzola et al., 2012; Moschieri and Mair, 2011); these included cross patenting, cross licensing of technology, R&D collaboration, co-construction of platforms, strategic alliance, and others. We then counted the number of types of activities that firms engaged in each year as disclosed in their annual reports. This number was then used as the measure of coupled open innovation that a firm engaged in. In parallel with the measure of industrial clockspeed, the study classified those whose scores were above the average as “high” coupled open innovation and otherwise “low.”

3.2.5. Control variables

This study includes a wide range of control variables at three different levels. At the time level, this study conducted a longitudinal observation on the sample firms; thus, the analytical regression models employed in this study require the time effect to be controlled. Therefore, six year-dummy variables were included in all models to control for the time effect on the relationships being examined.

At the firm level, large firms consume more energy and emit more carbon than small firms (Prado-Lorenzo et al., 2009). Therefore, we included firm size in the models to account for its correlation with carbon emissions. Firm size was measured by the logarithmic numbers of employees. Firm age signifies firms’ innovation trajectories and can influence financial performance (Mazzola et al., 2012). Accordingly, we computed firm age by subtracting the inception year of each firm from the observation year and included firm age in the models to control for its effect. Profitability is a driving force of a firm’s future growth and a key indicator for a firm’s market value (Kiani et al., 2011). This study measures profitability of firms by returns on equity (ROE). Financial structure has a direct effect on financial performance (Waddock and Graves, 1997). The study controlled the influence of financial structure in terms of debt level (i.e. the ratio of total debt to total assets) in the models. Organization slack resources have an impact on resource allocation and firm performance; we measured organization slack by the current ratio (Greenley and Oktemgil, 1998) and included it as a control variable in the models.

This study included two control variables with respect to corporate governance to control for its effect. Asian enterprises have been characterized by the governance forms of family business and group affiliation, which have significant performance implications (Yang and Schwarz, 2016). The study used two dummy variables to record the governance forms of the sample firms, with the value of one representing family or group governance and zero otherwise. Finally, while corporate governance, CSR engagement, and firm values are interrelated (Harjoto and Jo, 2011), CSR reports have become the major source for disclosing firms’ records of carbon emissions. Those firms that publish CSR reports may intend to show their satisfactory levels of carbon emissions that meet the social anticipation of their stakeholders. Thus, the study observed and coded whether a firm published its CSR report in a certain year using a dummy variable (CSR disclosure as 1 and otherwise 0), and included it as a control variable.

At the industry level, the electronics firms in Taiwan can be categorized into four major subsectors—semiconductors, optoelectronics, computer & peripheral (PC), and miscellaneous others. Thus, we controlled the effect of sectoral differences on the relationships being examined with three dummy variables to separately represent the sectors of PC, optoelectronics, and miscellaneous others, while leaving the semiconductor industry as the contrast group.

3.3. Analysis

This study observed 640 firms over 7 years (2012–2018), with the sample data forming a panel structure that contains 4480 firm-year observations in total. Because it frames carbon emissions both as a consequence of firm growth and as an antecedent of market value of the firms, endogeneity arises from this framework and should be accounted for. As noted previously, we adopted two-stage least squares (2SLS) panel regression models (Antonakis et al., 2014) to separate the effect of prior performance on carbon emissions and the effect of carbon emissions on subsequent market value of firms. The Hausman test was utilized to ensure model fitness when specifying the model selection between random-effects model and fixed-effects model.

4. Results

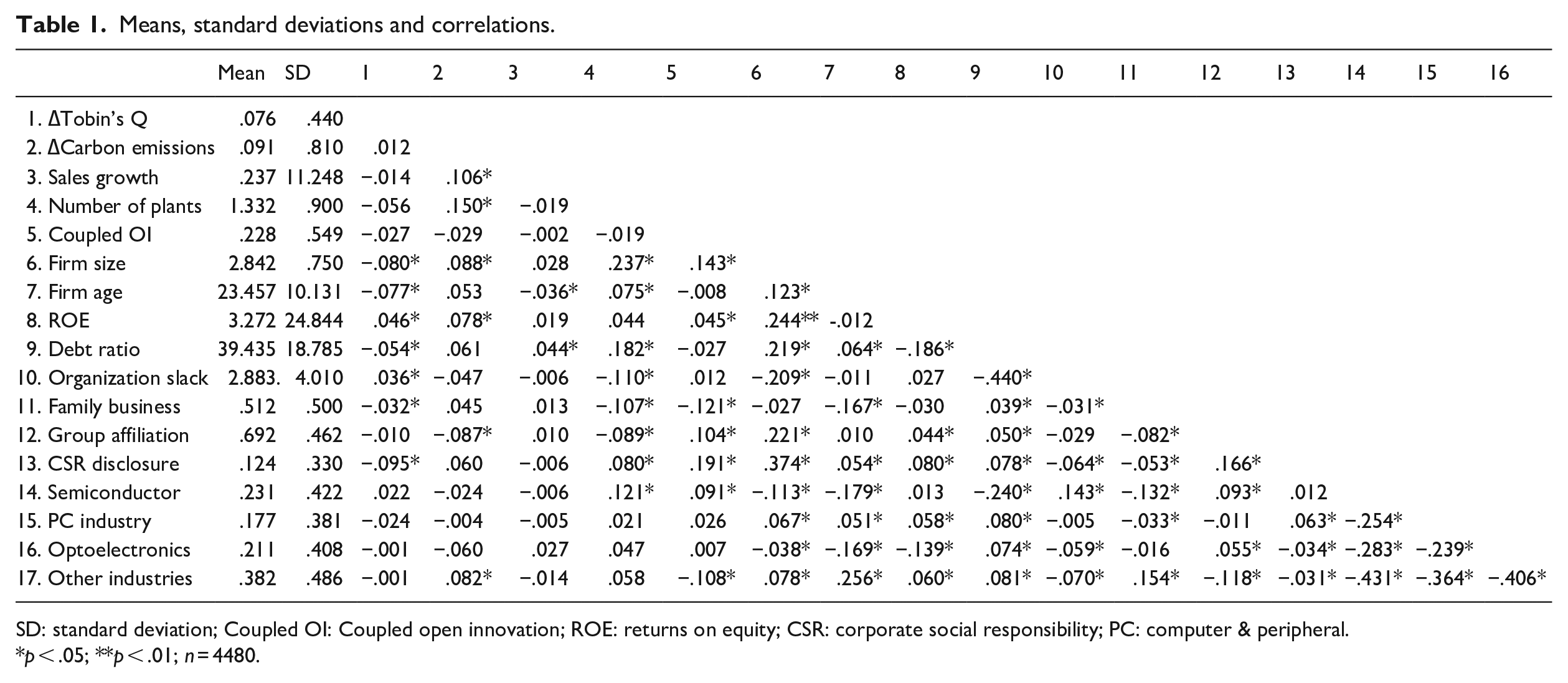

Table 1 shows the means, standard deviations, and correlation coefficients of all studied variables. On average, the sample firms exhibited an increasing tendency in sales growth (23.7%) during the observation years. Meanwhile, the sample firms increased their carbon emissions at the rate of 9.1% per year. These figures provide initial support for H1, which states that growing firms tend to emit more carbon due to expansion in scale.

Means, standard deviations and correlations.

SD: standard deviation; Coupled OI: Coupled open innovation; ROE: returns on equity; CSR: corporate social responsibility; PC: computer & peripheral.

p < .05; **p < .01; n = 4480.

The semiconductor sector accounted for 23.1% of all sample firms, and the rest of the sectors are optoelectronics (21.1%), computer and peripheral (17.7%), and others (38.1%). A further comparison between the semiconductor industry and the other three industries shows that the semiconductor sector had the highest intensities with respect to R&D investment (p < .01) and coupled open innovation (p < .01) among the four sectors, suggesting a significantly high rate of clockspeed for the sector. Table 1 also demonstrates the correlation matrix among the variables, where only one coefficient, except for the correlation coefficients among industrial dummies, was greater than 0.4 which was found between two control variables (the debt level and current ratio, r = −.44). The healthy correlation structure minimizes the concern of the multicollinearity problem in regression analyses.

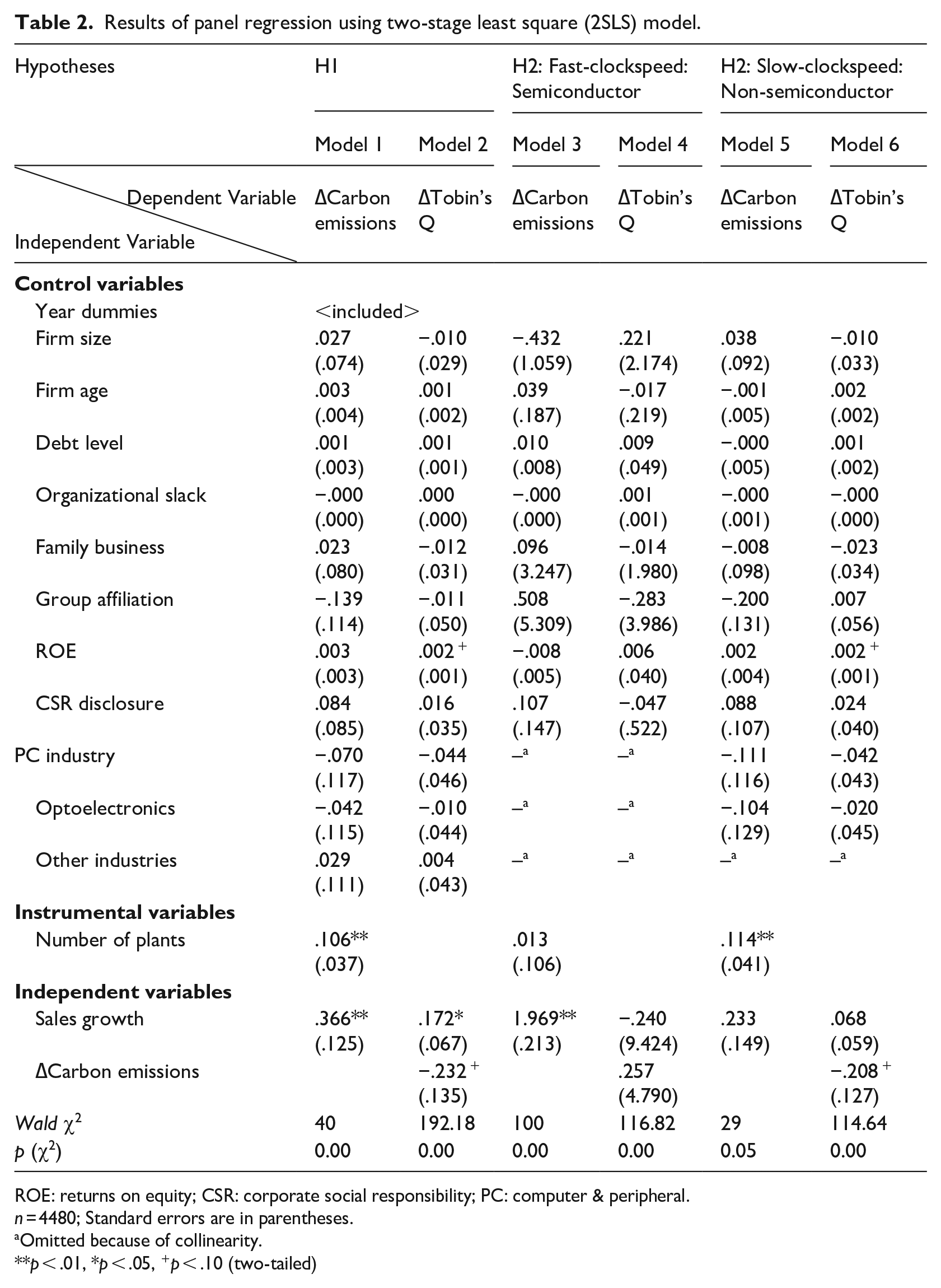

The study employed the impact threshold of a confounding variable (ITCV) to test the omitted variable bias (Busenbark et al., 2022; Xu et al., 2019). Results suggest a potential bias of omitted variables in the relationship between firm growth and carbon emissions. When the relationship is instrumented by the instrumental variable (i.e. number of plants), however, all the impact values are below the threshold value, indicating that the causal inference of the instrumented model is validated and relatively robust. We also conducted the Hausman test to compare the model fitness between the random-effects model and the fixed-effects model that were specified when employing panel regression models. The p-value of the testing statistic (χ2 = 3.18, p > .10), suggests that random-effects model is better fitted than the fixed-effects model. We report the results of the random-effects model via Tables 2 and 3.

Results of panel regression using two-stage least square (2SLS) model.

ROE: returns on equity; CSR: corporate social responsibility; PC: computer & peripheral.

n = 4480; Standard errors are in parentheses.

Omitted because of collinearity.

p < .01, *p < .05, +p < .10 (two-tailed)

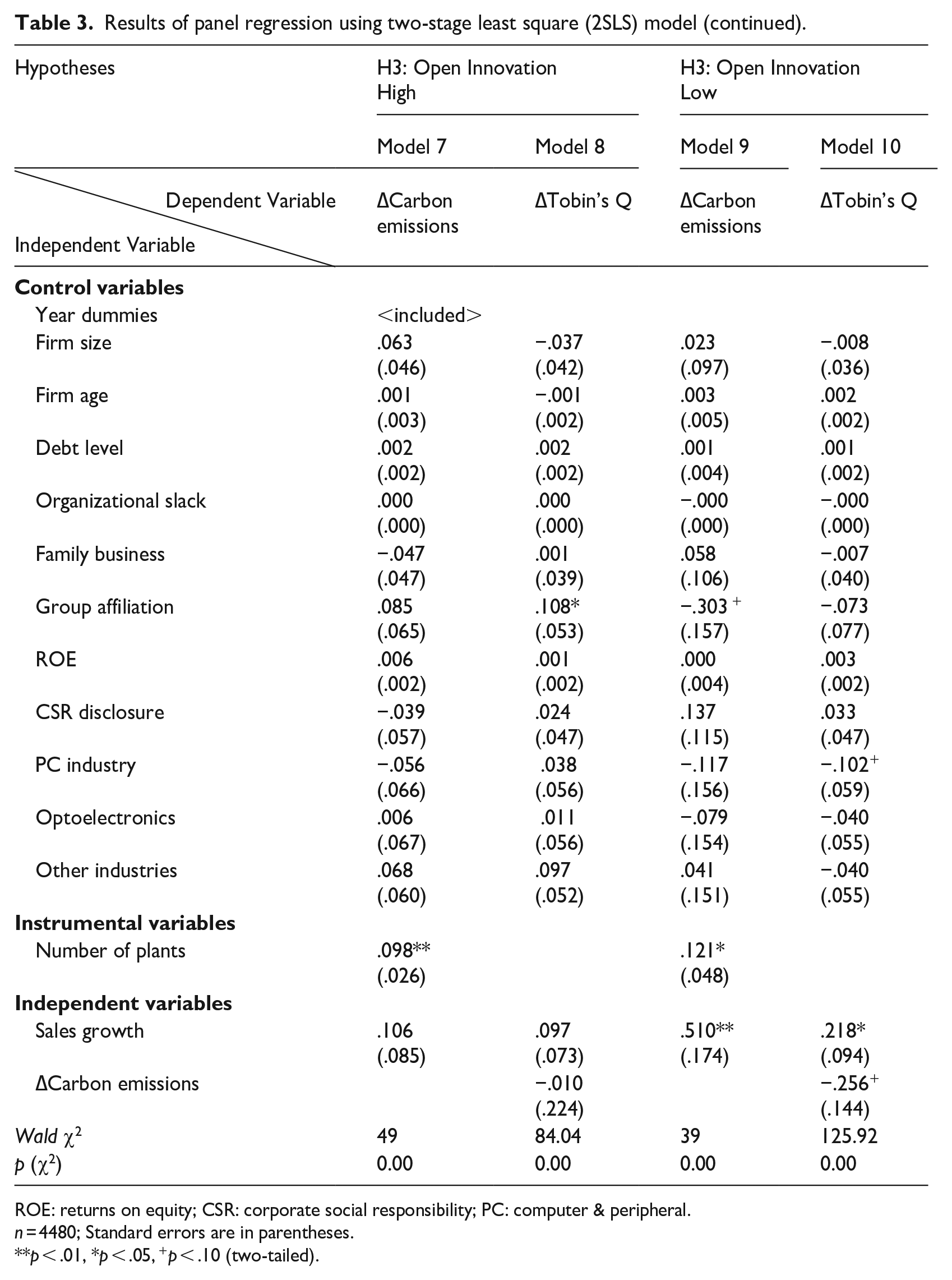

Results of panel regression using two-stage least square (2SLS) model (continued).

ROE: returns on equity; CSR: corporate social responsibility; PC: computer & peripheral.

n = 4480; Standard errors are in parentheses.

p < .01, *p < .05, +p < .10 (two-tailed).

Tables 2 and 3 demonstrate the results of the 2SLS panel regression models for the hypotheses. The carbon emissions were explained by an instrumental variable in addition to the control variables in the first-stage regression. The results of Model 1 in Table 2 show that sales growth is positively correlated with carbon emissions (β = .366, p < .01), suggesting that sales growth boosts carbon emissions. Thus, the result supports Hypothesis 1a. In addition, the number of plants also displays a positive association with carbon emissions (β = .106, p < .01). The predicted values of carbon emissions were introduced as the independent variable of the second-stage regression model in Model 2. The results of Model 2 show that the carbon emissions were negatively correlated with the change rates of Tobin’s Q (β = −.232, p < .10), suggesting that higher carbon emissions led to lower firms’ market value. Thus, the result supports Hypothesis 1b. The combination of the two-stage regression results suggests that firm growth boosts a high level of carbon emissions, which, subsequently, leads to lower market value. Therefore, Hypothesis 1 is supported.

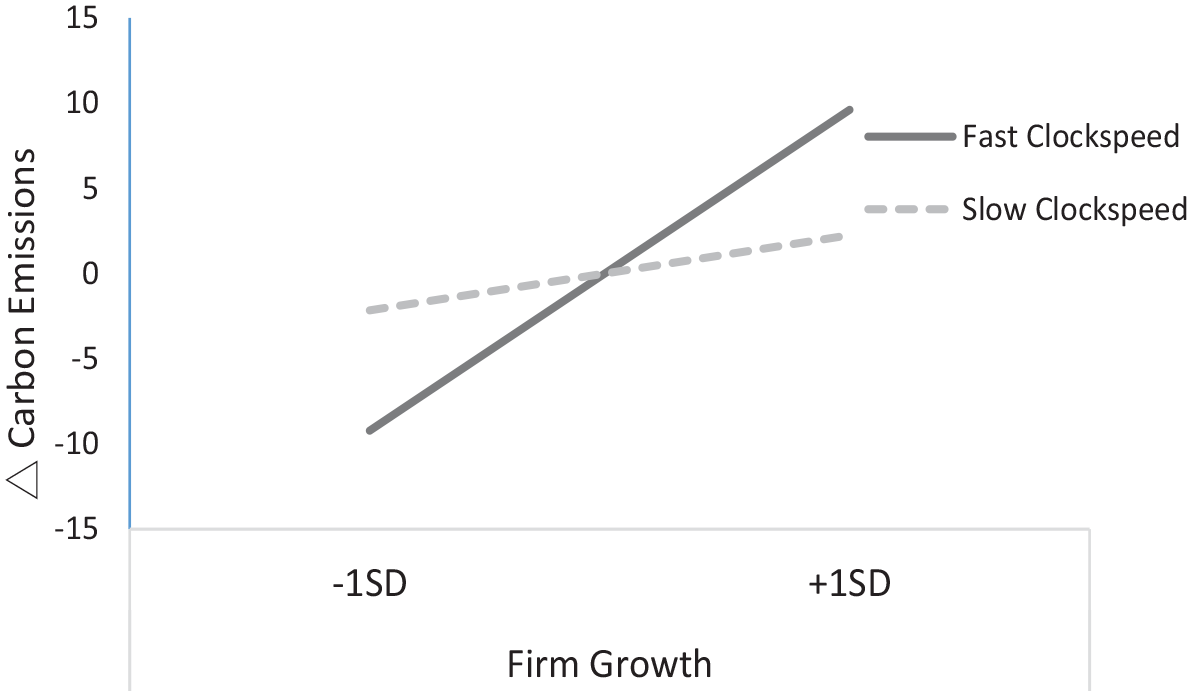

The study adopted a two-group design to test the moderating effect of industrial clockspeed on the growth–carbon emissions relationship as depicted in Hypothesis 2. Model 3 and Model 4 of Table 2 tested the two-stage regression models for the subsample of semiconductor industry, which represents the high-clockspeed group. For contrasting purposes, Model 5 and Model 6 tested the same models for the non-semiconductor industries, which represent the low-clockspeed group. As reported in Model 3, the first-stage regression results show that the positive relationship between sales growth and carbon emissions remain significant (β = 1.969, p < .01) in the semiconductor industry. The effect of sales growth on carbon emissions remains positive and significant, which coincides with H1a. Conversely, this relationship in the group of non-semiconductor industries become weaker and insignificant (β = .233, p > .10) in Model 5. By contrasting the results between Models 3 and 5, the moderating effect of industrial clockspeed is salient in that the proposed causality in H1a is more pronounced in the group of high clockspeed industry (i.e. semiconductor) than in the group of low clockspeed industry (i.e. non-semiconductor industries). Thus, Hypothesis 2 is supported. Using the regression coefficients of Model 3 and Model 5, Figure 1 graphically displays the moderating effect of industrial clockspeed on the relationship between firm growth and carbon emissions, where the line with a steeper positive slope represents the high-clockspeed group and the line with a mild positive slope represents the low clockspeed group.

The interaction effect between firm growth and industry clockspeed on carbon emissions.

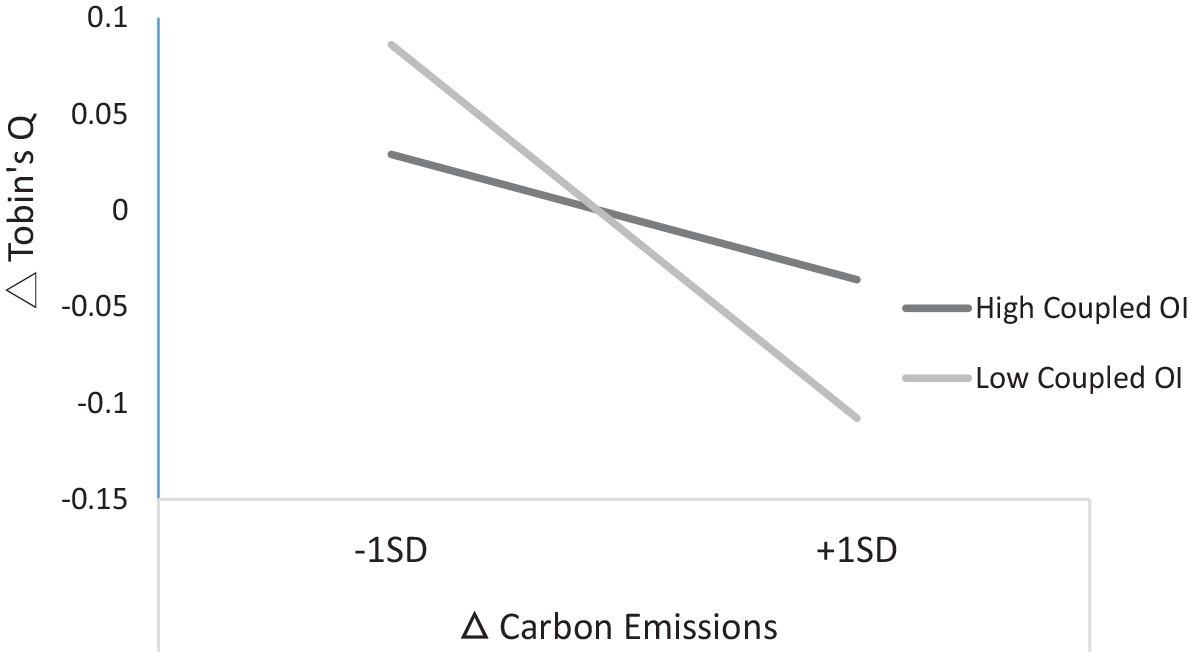

Hypothesis 3 proposes that firms’ engagement in coupled open innovation weakens the negative relationship between carbon emissions and subsequent market value. The results of Model 8 in Table 3 show that the negative association between carbon emissions and subsequent market performance turns insignificant in the group of high open innovation (β = −.010, p > .10). The result suggests that engagement in open innovation activities can weaken the negative effect of carbon emissions on market values of firms. Nevertheless, the negative effect of carbon emissions on market values of firms remains negative and significant (β = −.256, p < .10) in the group of low open innovation as shown in Model 10. The results of Model 8 and 10 together provide evidence for the moderating effect of the engagement in coupled open innovation that weakens the negative effect of carbon emissions on performance. Thus, Hypothesis 3 is supported. Using the regression coefficients of Model 8 and Model 10, Figure 2 graphically displays the moderating effect of coupled open innovation on the relationship between carbon emissions and Tobin’s Q. When the engagement of coupled innovation is low, carbon emissions diminishes firms’ market value. Conversely, the detrimental effect of carbon emissions on Tobin’s Q is lessened when firms’ engagement of coupled innovation is high.

The interaction effect between firm growth and industry clockspeed on carbon emissions.

5. Discussion

Climate change is a global problem that needs addressing (George et al., 2016) but which organizational research still struggles to articulate solutions. Testing the paradox of increased carbon emissions and firm performance, this study’s findings illustrate an alternative narrative on firms adjusting to climate change. The relationship between carbon emissions and firm performance feeds into the breadth and depth of the grand challenge that climate change presents for organizations, communities, and society. Coloring this concern is the assumption that firms operating in market-based economies strive to grow and adopt a series of strategy and innovation choices to do so. Despite continued growth in carbon emissions (IEA, 2021), there is pressure on organizations to reduce their carbon footprint and remain competitive.

Answering the question of why firms do not or cannot reduce their carbon emissions, this article investigates whether firms are trapped in an endogenous paradox in which prior performance triggers expansions in scale and scope and, thus, greater carbon emissions, which subsequently cause the firm to suffer from lower market valuation. Our data show that despite assumptions of the value of climate change policy for business (Henderson, 2021), and recognizing ongoing confusion about climate change and performance (Busch and Hoffmann, 2011), paradoxically, the pursuit of performance growth generates more carbon emissions that contribute to climate change but which impact negatively on subsequent market value of the firm.

At its core, and the theme that motivated this study was that although the bifurcation narrative we present is philosophically established it remains largely unresolved in the context of framing the challenge climate change presents (see Ferraro et al., 2015). Logically, executives would not pursue something that impacts performance negatively. But as we establish earlier, and recognizing the centrality of climate change to current debate and worldview, although carbon emissions have subsumed attention globally, the paradox we test still exists—that firms may signal one thing on climate but do another, via performance and executive behavior. This outlook is previously acknowledged by Kerr (1975) and then specifically for climate by Slawinski et al. (2024) confirming the paradox we explore. As our study shows, attempts to deal with climate change promotes performance deterioration, despite expectations of both the need to care about climate change, and to develop strategies for its ongoing impacts.

With this finding, and unlike previous studies focused on dimensions of environment management and firm performance (Endrikat et al., 2014; Misani and Pogutz, 2015), this article adds an alternative stance on explaining this persistent paradox. Despite assumptions about the incentives and constraints on the growth of the firm built around profitability (i.e. value), and the push to finding a link between environment and performance, we show that firms do not or cannot reduce carbon emissions while they are profitable (or strive to be so). Notwithstanding assumptions of corrective actions on managing emissions, climate change represents a broad risk to businesses, rather than an absolute market opportunity. This assertion challenges the inference that firm growth in profit and carbon emissions present a clearly delineated pathway (for the firm and for climate policy for firms). By coupling performance measures, represented by different industry clockspeed, with forms of open innovation, the study presents a practice orientation for how firms can mitigate increased emissions in managing the relationship between carbon emissions and market performance. Thus, the analysis of firm growth is more precise than that of firm growth strategies. Given that our data show the results of firm growth strategies without knowing what specific strategies managers chose, more research is needed to highlight how different successful or failed results may derive from specific strategy adopted.

In this way, and as a primary contribution, we propose and validate a cyclical approach concerning the relationships between growth, carbon emissions, and market value: that the logic of firm growth can offset a firm’s motivation to reduce carbon emissions. Building on Howard-Grenville et al.’s (2014) call to arms to extend modeling on climate change and business, the study thus raises a clear societal challenge around climate change and business norms—about what it is firms are doing given the grand challenge raised by carbon emission growth. Our study is particularly meaningful given its focus on an emerging economy, given that grouping’s growth, and adoption of market-based policies (Hoskisson et al., 2000). Most emerging economy firms are deeply embedded in global supply chains and undertake the role of production that consumes the largest portions of energy adding to carbon footprints. Understanding the impact of carbon emissions is increasingly relevant to businesses, and therefore, investigating its effects and relationships makes sense. Still, corporate efforts tend to focus on responding to climate change as a means of legitimacy, because it is of concern to external stakeholders of firms, such as governments, customers, financial markets, and given public debate on measures needed to counter climate deterioration (Henderson et al., 2020). Historically missing in this debate is deconstructing the performance itself.

5.1. The grandest of challenges: theoretical implications

Our research contributes to discussion on grand environmental challenges and organizations in three ways. First, we present a cyclical intersection of the relationships between growth, carbon emissions, and market value. Following Busch and Lewandowski (2018), most research in this area has suggested that carbon reduction contributes to financial performance; however, these may have failed to establish that the fundamental logic of firm growth can essentially offset firms’ motivation to reduce carbon emissions. In the present study, we demonstrate the conflicting nature of carbon emissions and firm performance. More importantly, findings help explain the existence of the gap between the assertion of the need for carbon reduction and the reality that industries continue to increase carbon emissions (Matos and Silvestre, 2013). Understanding the paradoxical performance implications of carbon emissions is critical to both practice and policy. This add-on revisits and develops Wright and Nyberg’s (2017) findings that businesses often regress when it comes to innovations and actions to deal with climate change. Thus, we highlight an alternative and counterintuitive restriction based on performance.

In this way, we leverage Howard-Grenville’s (2021) narrative that grand challenges like climate change and organizational performance are inherently complex, and without easy solution, inducing a need for a different kind of researcher attention. Research has tended to examine the subsequent performance outcome of carbon emissions to address why firms cannot reduce their carbon emissions given a preoccupation with short-term rather than long-term performance (Delmas et al., 2015). Nonetheless, firms do not willingly adopt a performance paradox. Rather, they are limited by their learning capabilities and prior performance, which delineates their strategic constraints. As Van Thiel and Leeuw (2002) note broadly, performance indicators risk losing their value as a measure of actual performance due to an inability to detect poor performance in this context. As we present it, this endogenous limitation is a real obstacle for firms to pursue low-carbon practice. Without including an understanding of this paradox, any explanation of why firms do not mitigate the harm they cause to the environment is incomplete. In other words, overemphasizing profitability from carbon emissions does not provide a persuasive reason for firms to pursue a strategy of emission reduction.

Despite its logic, and building on the basis of our primary contribution, continuing to directly link performance to climate change may be a naïve measure for firms to adopt in the first place. When firms follow a growth path to increase their scope and scale, alongside increases in carbon emissions, they initially profit from this decision; however, the market will ultimately punish the firm by lowering their stock price or capital investment. Conversely, as we show, planning early on to mitigate carbon emissions and deviate from a growth path may seem challenging, but in the long-term, the market will compensate firms for making this choice. This assertion is especially relevant given the growing demand from institutional investors for government action to regulate organizations with regard to climate change (Jessop and Chestney, 2019). In this context, it may be worthwhile for further future research to explore pressure from investors as an effective way to motivate firms to reduce carbon emissions.

As a second contribution, addressing climate and firm performance enables a more nuanced account of decision-making and risk-taking in firms facing climate change challenges, given perceptions of threat that some executives see to their firm viability (Henderson, 2021). While the relationship between corporate carbon emissions and financial performance attracts attention (Busch and Lewandowski, 2018), the inclusion of performance measurement moderating effects from industry clockspeed and open innovation enriches our understanding of this complex process. Complementing previous research, our study provides evidence of how firms do or do not engage in climate action and how open innovation can enable firms to practically mitigate the harm to performance caused by a given level of carbon emissions. Using clockspeed and open innovation enables us to add to previous discussion on markets and environmental practice, and how firm strategies and practices on environment are influenced by regulation or on market forces (e.g. Bansal and Hoffman, 2012). Together, clockspeed and open innovation explain the performance paradox, providing add-on evidence regarding which firms do or do not engage in climate action and which can practically mitigate the harm to performance caused by a given level of carbon emissions.

This integration provides a way forward to address this grand challenge. As the substitution effect between carbon emissions and innovation in our findings shows, firms in an environment where the fast rate of change determines immediate winners and losers tends to allocate their resources to technological advancement or innovation-centered activities. This reality makes carbon emissions reduction a less attractive choice and subsequently results in poor capital market evaluations. This result may explain why even successful firms cannot necessarily reduce their carbon emissions in a market-based system (Nyberg and Wright, 2022). The effect of variability in the speed of industry and industry segment change should not be underestimated, however, given that firms in slow-clockspeed industry can allocate their resources to mitigate their carbon emissions, representing a new positioning for these companies. As we show, costs associated with carbon reduction can be compensated by the firm’s market performance later, and thus the performance paradox can be avoided. This finding provides a way forward to manage market-environment tensions, pointing to the folly of viewing environmental policy and response primarily through an economic or an organizing lens, because firm performance is not as connected as businesses may believe. In this way, coupled open innovation not only brings alternative potential solutions to resolve climate-related issues but also serves as a signal to the market that the focal firm is attempting to devote its efforts to these issues.

As a third, allied contribution, with its focus on Taiwan’s high-tech manufacturing firms, the findings of this study have important implications regarding climate change for emerging economies. These markets are important contexts to understand climate change and its consequences, given their market share growth potential and trajectory. As we note earlier, with a heavy reliance on manufacturing, emerging countries are increasingly significant contributors to carbon emissions growth (Fekete et al., 2013). Given their high emissions output, the World Economic Forum stress the importance for manufacturing industries to create a low-carbon future (Tricoire, 2019). Yet despite their prevalence, studies on emerging economies are still limited with a focus on US and Western samples (Grewatsch and Kleindienst, 2017). Rededicating this focus is relevant given that emerging or growing economies’ carbon emissions are increasing progressively, whereas those of developed economies show a flat growth path (Ritchie et al., 2023a). With this gap, and given its placement as the manufacturing heartland of global high-tech products, our emphasis on Taiwan as an exemplar provides further insight into climate change implications from emerging markets, complementing earlier findings (e.g. Pankratz et al., 2023) on climate change and performance in developed economies.

5.2. Climate . . . changes: implication for practice

With its performance paradox findings, this study also highlights clear consequences and lessons for practitioners and executive decision makers. With the growing importance of climate change to businesses, many firms facing its associated challenges are distracted by similar sets of items—on environmental management and its regulation, ecological footprint, carbon disclosure, market impact and risks, and sustainability in order to maintain legitimacy (e.g. Albertini, 2013; Babiak and Trendafilova, 2011; Endrikat et al., 2014)—providing a link between environment and financial performance. As our findings show, however, despite this commonality, sustaining this link might not be as straightforward as is routinely presented. While carbon emission reduction might seem a logical approach for firms given prior business growth and success from such strategy, our study illustrates that this growth and profitability priority may impact negatively on the firm’s market performance when carbon emissions continue to increase as expected. Executives thereby should pay closer attention to and better match clockspeed characteristics in how they engage in emissions management. Those in slow-paced markets are better able to target direct carbon emissions reduction as an alternative positioning in the market, while those in high clockspeed industries are better matched to growth with less direct attention on impacts of emissions increases on market placement.

By highlighting the performance paradox alongside climate change, practitioners need to consider both its occurrence (existence) and to develop their toolkit for detecting and preventing what it represents. As a grand societal challenge, understanding climate change impact on business should be at the forefront of all business policy and strategy. Yet this focus is often influenced by the debate itself (for/against, policy etc.). With our findings, we highlight an alternative pragmatic approach—of strategizing for the existence of weaker performance. This response could entail revisiting performance indicators and measures from the existing metrics, reconsidering performance assessment systems, and better linking financial and emissions performance differently. Following Meyer and Gupta (1994) and Van Thiel and Leeuw (2002), it could also mean constructing or adopting multiple, uncorrelated, and varying performance indicators specific to climate change, beyond current convention.

5.3. Conclusion

This article illustrates why firms do not or cannot reduce their carbon emissions while they are profitable, as well as an avenue for them to mitigate this performance paradox. It highlights that even though climate change represents one of society’s grand challenges, “many organizations and their management teams really do know what to do to improve performance” (Cohen, 1998: 38) in this context. By examining the performance paradox derived from increased carbon emissions, we show this outcome as one reason why this perpetual focus on firm performance may be misleading for contemporary carbon emissions management. Central to this messaging—and what our findings concretize—is that it challenges exactly what constitutes firm performance (growth) during climate change; where results of performance paradox are inaccurate assessments of evaluating or sanctioning an organization based on what we perceive to be measurable, good performance. With this theme, this article highlights future research avenues to consider more nuanced measures of climate change and its effect on firm growth, and the mutual relationship between firm growth and carbon emissions, rather than simply its impact on the bottom line or the business value of “going green.”

Key practical and research implications

Footnotes

Final transcript accepted 17 December 2024 by Rui Xue (AE Strategy).

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author(s) received funding from National Science and Technology Council, Taiwan, NSTC 110-2410-H-259 -016 -MY2 and NSTC 112-2410-H-259-005.