Abstract

Using survey data of owners of micro, small and medium enterprises (MSMEs), we investigate the nexus between financial literacy (FL) and financial inclusion (FI). Furthermore, we examine whether the FL_FI nexus is different by gender. Our results show that FL has statistically significant positive effects on all three dimensions of FI (access, usage and quality). Our findings highlight policy implications for countries desiring to enhance FI by improving the financial literacy and education levels of MSME owners. Furthermore, our findings suggest that targeted financial education programmes result in better outcomes.

1. Introduction

Financial literacy (FL) plays an important and fundamental role in financial decision-making. According to Kozup and Hogarth (2008), FL is a collection of thinking skills that allow an individual to critically assess the benefits and drawbacks of a financial decision relative to their own criteria of needs, values and goals. As such, FL also plays a key role in national economic growth and has attracted the attention of organisations such as major banks, government agencies, grassroot consumers and community interest groups, among others. Concerns from groups, including policymakers, are that FL deficiencies can lead to poor financial decision-making such as overspending, taking on high-interest debt, the inability to save for home deposits, seeking higher education or financing retirement, among others. Poor money management behaviour can lead individuals to be vulnerable during financial crises. FL skills are more important post-COVID-19 as many people have lost jobs and face inflationary pressures caused by supply chain issues due to global instability. Consequently, eroding savings, reducing households’ ability to service mortgages and being faced with an increase in natural disasters (cyclones, flooding and bushfires), mean that people need their funds to travel further and/or have access to finance.

Prior studies have documented that FL is an important factor in improving individuals’ and households’ financial well-being. From a broader perspective, empowering individuals with FL allows them to navigate the complexities of their finances more effectively, thus leading to a more robust, competitive and efficient market. Financially literate consumers can make informed decisions about their finances and demand products and services that meet their needs. This contributes positively to the overall efficiency and dynamism of the market.

Since the focus of prior studies has been on the FL of individuals and households, studies relating to the FL of micro, small and medium enterprise (MSME) owners are scant. An increase in the rate of business failures in many countries raises the question of whether MSME owners’ FL is also required to be considered for the survival of their businesses. Since MSMEs operate in a dynamic economic environment where financial markets are competitive and financial products are complex, the MSME owners’ FL skills play an important role in ensuring that these enterprises are operated successfully and have access to relevant financial services to innovate and exploit growth opportunities. MSME owners’ level of FL will help to reduce credit risk to lenders relating to complexities in financial markets and their access to financial services.

Studies undertaken internationally have reported that the SME sector faces several problems such as a lack of access to adequate and timely financing, and capital and knowledge needed to invest in new technology to improve their production capacity. These constraints make it difficult for SME owners to compete in the market, among other things. According to the Meeting of the OECD Council at Ministerial Level (2017), SMEs worldwide indicate that the greatest obstacle to their growth is access to finance (Ayadi and Gadi, 2013). The number of women who are engaging in entrepreneurial activities rose from 7.3 females per 100 working-age females in 2019 to 8.7 females per 100 working-age females in 2020 (Global Entrepreneurship Monitor [GEM], 2021). However, the literature reports that female entrepreneurs are more prone to financial constraints (Cavalluzzo et al., 2002; Chaudhuri et al., 2020).

In this regard, international organisations (such as the World Bank and the G20) and national governments have focused on improving the access and utilisation of financial services by MSMEs to improve their financial inclusion (FI) 1 and financial well-being (Brüggen et al., 2017). Consequently, the focus in many jurisdictions has shifted to improving the level of FL of both individuals and business owners. A survey of bank regulators in 143 jurisdictions by Demirguc-Kunt et al. (2015) shows that 67% of these regulators have the mandate to promote FI.

Given the importance of MSMEs to a country’s employment and GDP, the investigation into the interaction of FI and FL in general and for women relative to men is important. The increase in knowledge of this subject facilitates a discussion on the importance of FL and FI in countries similar to New Zealand but is also important in countries that do not yet have the support mechanisms for higher FL or for women’s FL. This study makes the following five contributions to the FL literature. First, to the best of our knowledge, this is the first study that investigates the relationship between FL and FI of MSME owners. Prior studies relating to the FL-FI nexus have focused on different age groups, genders and ethnicities (Agnew and Harrison, 2015; Lusardi and Mitchell, 2014; van Rooij et al., 2011). This study focuses on MSME owners as they are a special subgroup of entrepreneurs and risk-takers in comparison to households (van Praag and Cramer, 2001; Xiao et al., 2001). Second, this study focuses on the demand-side barriers to FI faced by MSME owners rather than the supply-side barriers regarding the usage of financial products. While supply-side barriers such as the availability and affordability of financial services have been extensively studied in the literature, demand-side barriers have received comparatively less attention. Although demand-side barriers may be less cited in the literature compared to supply-side barriers, they play a crucial role in shaping MSMEs’ financial behaviours and decisions. Therefore, it is essential to recognise, understand and address these barriers to promote broader financial inclusion and empower MSMEs to improve their financial well-being. Third, FI is a multidimensional construct, which includes access, availability, usage and quality of financial services (Sarma and Pais, 2011). 2 However, prior researchers have focused on only access and usage dimensions of the FL (Grohmann et al., 2018). We extend prior research by considering three dimensions of FI, that is, access, usage and quality of financial services. Fourth, Preston and Wright (2019) show that the male-female FL gap is moderated by several factors including labour market variables (e.g. an individual’s occupation and industry) but did not address the impact of FI. Since the importance of improving FI for women has received an increasing level of attention in recent decades, the findings of this study will help policymakers design better FL programmes for female-owned MSMEs. Fifth, we extend the number of the FL measurement proxies used in prior studies (Lusardi and Mitchell, 2007; Nunoo and Andoh, 2012) to six questions to measure FL compared to the narrow definition of FL used in prior studies.

We report a statistically significant positive relationship between the FL of MSME owners and FI in the three measured dimensions, namely, access, usage and quality. Furthermore, our results indicate that FL may have a greater impact on female MSME owners than on male MSME owners. As such, improving FL skills and knowledge will allow MSME owners to make prudent financial decisions.

The remainder of this article is structured as follows. Section 2 provides a literature review of the current study. Data and methodology are presented in Section 3, while Section 4 provides discussions based on the empirical results. We conclude the article in Section 5.

2. Literature review and hypothesis development

The theory of information asymmetry and transaction costs has often been used to explain the financial constraints that small firms and poor borrowers encounter (Binks and Ennew, 1996; Stiglitz and Weiss, 1981). Information asymmetry between lenders and borrowers leads to sub-optimal allocation and utilisation of financial resources. The information imbalance between borrowers and lenders leads to borrowers experiencing higher funding costs. This is because of the borrower’s lack of knowledge of the availability of other sources of finance, requirements and opportunities as well as insufficient information about the advantages and disadvantages of the funding sources.

The existence of the information gap between borrowers and lenders is exacerbated by borrowers not disclosing all relevant information about their investment projects to the lender, such as its riskiness (Hannig and Jansen, 2010; Sharpe, 1990). As a consequence, banks may either refuse to give loans due to incomplete information about the inherent risk or grant credit without the knowledge of the risk being undertaken. This puts both parties at risk and raises the issue of moral hazard which may require lenders to undertake additional costs of monitoring and auditing and/or legal charges in the case of the borrower defaulting. As such, higher degrees of FL improve the ability to access information and increase awareness about available financial options and products and services which influences access to finance. FL may reduce the impact of a lack of financial knowledge which may reduce lenders’ credit risk, and, in turn, reduce borrowers’ transaction costs.

The MSMEs’ high degree of information opacity about their business requires lenders to incur costs to find additional information needed for decision-making. Consequently, this increases the transaction costs of servicing the MSME segment. Servicing this risky segment of the market requires a high premium. The inability to obtain high premiums due to additional costs results in lenders becoming reluctant to service them. Having higher levels of FL may allow borrowers to disclose relevant information to lenders, thus enabling them to make informed decisions without incurring additional costs of information retrieval, while also reducing monitoring costs.

Prior literature that has investigated the impact of FL on financial decision-making has primarily focused on individuals/households (Drexler et al., 2014; Lusardi and Mitchell, 2011; van Rooij et al., 2011). Regarding the measurement of FL, van Rooij et al. (2011) documented that FL proxies need to be relevant for the study group, while Carpena et al. (2011) highlighted the need for FL questions to be appropriate for different economic settings. Furthermore, Lissington and Matthews (2012) pointed out that FL is shaped by the culture, beliefs, skills and habits of participants and, as such, the measurement of FL needs to change according to the economic environment, participant subgroup and the country’s institutional environment. Yang et al. (2023), for instance, showed that higher levels of FL increase the use of digital finance products within a Chinese setting. Since there has been limited investigation of the FL of owners of MSMEs, we have relied on the preceding literature to inform us of the FL measures to apply to MSME owners.

A financially literate MSME owner can maintain accurate financial records and understand their financial statements. In addition, MSME owners can better manage their finances, including cash flows and budgeting, and can better understand the cost of capital. They will be able to articulate their financial needs more effectively and understand the terms of the loans. MSMEs owners become better equipped to assess risks and take appropriate measures to mitigate them. As such, FI makes owners better financial managers, which reduces credit risk for lenders.

Access to credit is the most crucial aspect of FI. A clear and defining outcome of the Investment Climate Survey is that a lack of access to financial services significantly restricts firms’ growth, which, in turn, reduces employment opportunities and economic growth (World Bank, 2008). Furthermore, the lack of access to financial services limits developing countries in their ability to reduce poverty. Prior studies find that the formal methods for sourcing finance and services do not facilitate access to finance for MSMEs. MSMEs have restricted funding opportunities due to the existence of information asymmetry which affects their FI. In addition, Mazanai and Fatoki (2012) highlight four reasons for financiers’ reluctance to extend credit to small enterprises, namely, significant administrative costs of small-scale lending, asymmetric information, the perception of high risk and SMSEs’ lack of collateral. As a result, MSMEs rely heavily on debt financing and may struggle with undercapitalisation. This significantly impacts MSME businesses, as they already lack the resources they need to invest in growth, develop new products or services, or weather unexpected financial challenges (Meeting of the OECD Council at Ministerial Level, 2017). Due to their lack of financial acumen, they neglect to explore other possibilities of finance. The literature on the usage of financial products by MSMEs has focused on supply-side barriers to FI rather than demand-side barriers. While there may be sufficient credit available for MSMEs, the terms and conditions under which it is offered may not be appropriate for the sector it is intended to serve. For example, funds needed for the product design or services offered may not match what MSMEs need. Since the MSMEs sector is considered risky for lenders, a lack of collateral requirements and heavy restrictions are imparted aimed at discouraging MSMEs from applying for credit or financial services.

Prior studies show that FL has an impact on economic decisions (Bernheim, 1995, 1998). Bernheim (1995) reported that an individual’s lack of fundamental financial knowledge impacts their saving behaviour. In addition, poor FL impacts individuals in many ways. For example, individuals with poor FL tend not to plan for retirement (Lusardi and Mitchell, 2007) and/or seek credit from lenders that charge higher interest rates (Lusardi and Mitchell, 2011). Hilgert et al. (2003), reporting on several consumer surveys, identified that individuals with poor FL are more likely to rely on expensive credit cards and predatory lenders. Furthermore, Carpena et al. (2011) reported that FL programmes influence financial behaviour. Specifically, they identified that FL is important for individuals’ awareness of financial products and financial planning tools. In addition, van Rooij et al. (2011) reported a positive relationship between an individual’s level of FL and stock market investment. Finally, Behrman et al. (2012) reported that individual wealth is positively related to FL and school attainment.

Studies identify that access to finance is a challenge (Kou et al., 2021); thereby, FL is one of the detrimental FI components of individuals and firms. However, numerous studies focus on an individual’s comprehension of borrowing and saving matters, representative of their financial knowledge (see, e.g., Agnew and Harrison, 2015; Klapper et al., 2013), while only a few studies have investigated financial concepts, FL, and the implications of FL from the perspective of MSMEs. Given the prior literature on personal FL and the expected benefits to MSMEs, the need for MSME owners to understand financial concepts such as compounding interest rates, the risk and return relationship, and diversification to make informed decisions that have financial ramifications or consequences for their businesses is important and has not been explored. Brown et al. (2006) stated that FL for small business owners must incorporate the ability to read and understand fundamental financial statements, as well as their ability to understand numbers and make effective financial decisions and judgements. Furthermore, Gilliland et al. (2011) reported no significant difference between household and SME owners’ financial management skills.

Using a resource-based view, Eniola and Entebang (2016) argued that FL is likely to enhance SME owners’/managers’ financial knowledge, change attitudes towards risk and enhance awareness of the market. Hasan et al. (2021) showed that business owners with higher levels of financial education (as a proxy for FL) are more likely to engage in financial services. Finally, Nunoo and Andoh (2012) reported that the level of FL of SME owners is modest, and financially literate SME owners are more likely to utilise financial services. Based on the above, our first hypothesis is as follows:

H1: There is a positive relationship between the level of FL and FI of MSME owners.

H1a: There is a positive relationship between the level of FL and financial services accessible by MSME owners (Access dimension of FI).

H1b: There is a positive relationship between the level of FL and usage of financial services by MSME owners (Usage dimension of FI).

H1c: There is a positive relationship between the level of FL and the quality of financial services used by MSME owners (Quality dimension of FI).

Biological and social differences have contributed to gender differences in different societies. These gender differences may lead to social role distinctions in terms of male and female and, depending on their role, individuals may encounter different experiences when dealing with financial institutions such as banks, insurance and credit unions (Croson and Gneezy, 2009). Higher levels of exposure to financial activities tend to promote better FL, which is reflected in social behavioural norms. Lusardi and Mitchell (2011) investigated the level of FL in men and women and concluded that gender is a contributing factor when it comes to FL. In addition, Almenberg and Säve-Söderbergh (2011) and van Rooij et al. (2011) suggested that levels of FL differ by gender, with women generally found to be less financially literate than men. Zissimopoulos et al. (2008) reported that more than 80% of college-educated, middle-aged women are unable to answer basic compounding interest questions compared to approximately 65% of college-educated, middle-aged men. The gender FL difference is evident in later studies, as Klapper and Lusardi (2020) found. Specifically, women, along with other demographics, suffer from financial literacy gaps regardless of income level or the financial market development of the country they reside in. Lower levels of FL among women potentially reduce their active participation in the economy and exacerbate existing social disparities.

Moving to the link between FL and FI of women, it is important to highlight that women-owned MSMEs are relatively more underserved (Moritán, 2020). Females with limited exposure to financial services have low FL (Lusardi and Mitchell, 2011). Therefore, we argue that the FL-FI nexus is moderated by gender. Based on the above, our second hypothesis is as follows:

H2: Female MSME owners weaken the relationship between FL and FI.

3. Data and method

3.1. Sampling design

We used a cluster sampling design technique to analyse New Zealand MSME data. The total population is separated into several geographical clusters, with the surveys sent to a random sample of MSMEs in each cluster. Our sample is selected from four regions in New Zealand – Auckland, Canterbury, Waikato and Wellington. These regions were chosen because they contain the highest number of small businesses (Stats NZ, 2020).

The questionnaires are subsequently sent to the owners of 1500 MSMEs operating in the geographic clusters using an Internet-based survey system operated by the Qualtrics Online Survey Platform. The survey is structured such that the main owner completes the majority of the survey; however, a section of the survey is specifically for the business partner to address. We limited responses to a single completed survey per MSME to avoid multiple submissions from the same MSME. The survey was open for seven weeks (from 24 May 2016 to 12 July 2016), and we received 571 completed questionnaires, equivalent to a 38% response rate. Our response rate is similar to others who conducted questionnaire surveys in this sector (see Newby et al., 2003). Of the total returned questionnaires, 291 were from female-owned and managed firms, which leaves the remaining 280 from male-owned and managed firms.

3.2. Variables

The survey questionnaire consists of 37 questions designed to collect data at both the individual (such as the respondents’ demographics, FI and FL) and the firm level (such as firm core activities, firm size and legal status). The questionnaire can be found in Appendix 1.

We employ six FL questions, all of which were pre-tested and validated in prior studies (Klapper et al., 2013; Lusardi and Mitchell, 2011), to assess the financial skill and knowledge of respondents. Following the approach used by Lusardi and Mitchell (2011), with some modifications, we measure respondents’ FL using a series of six quiz-like questions 3 that evaluate the respondents’ knowledge of basic and advanced FL. The questions cover: (1) inflation; (2) simple interest; (3) compound interest; (4) risk and return trade-off; (5) inflation and living cost; and (6) risk diversification. Correct responses are coded one and incorrect responses are coded zero. 4 Finally, we sum the responses, ranging from zero to six, to construct an aggregate FL score for each respondent as an FL total score. 5 Respondents with a higher total FL score indicate higher FL and vice versa.

The dependent variable in this study is FI. We follow the World Bank method for measuring FI. Based on their guidelines, we employ the following three basic dimensions of financial services as alternative proxies for FI: (1) access; (2) usage and (3) quality of financial services. Nevertheless, most recent studies have heavily relied on these three dimensions of FI.

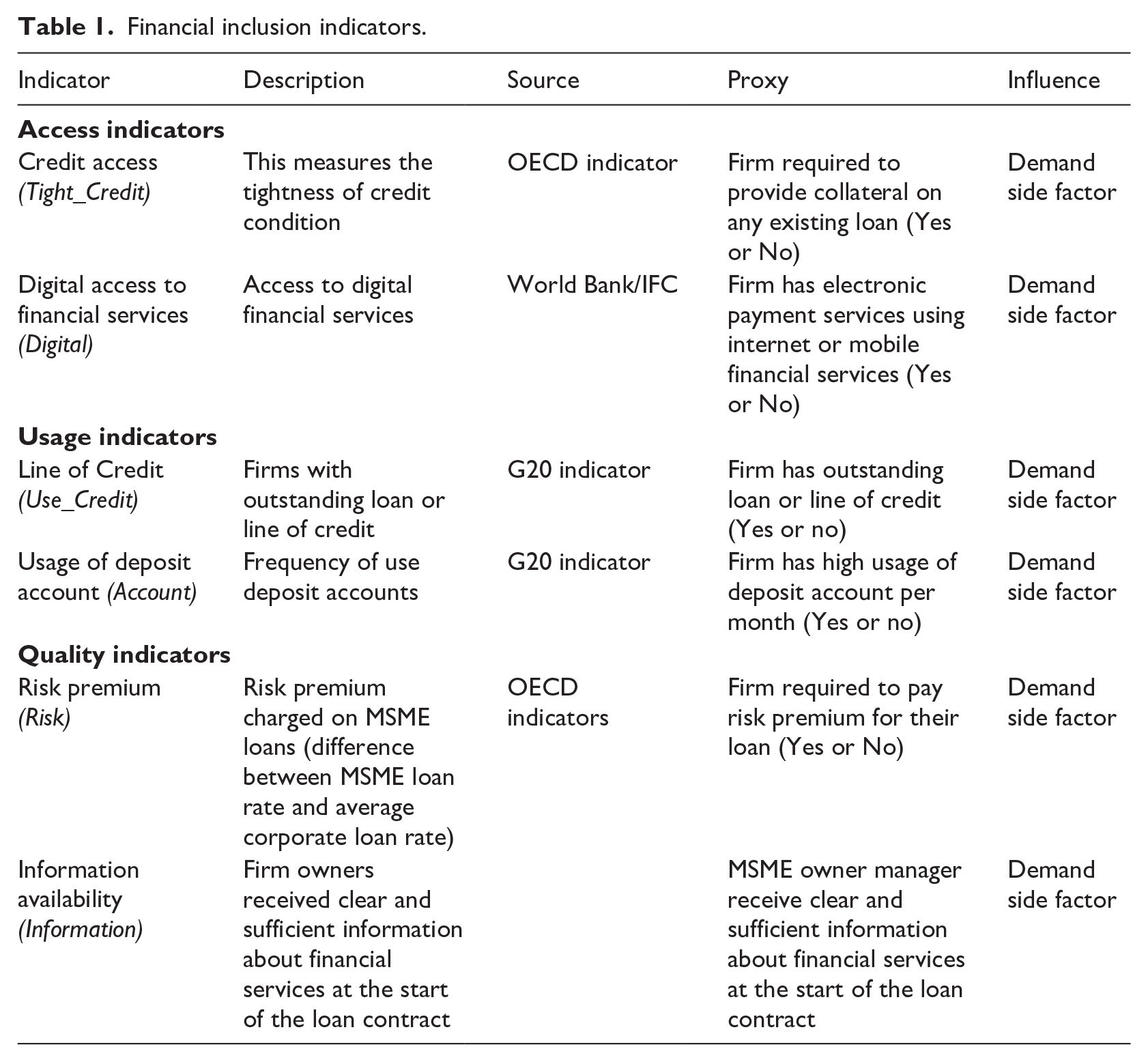

Access indicators measure the depth of outreach of financial services, that is, demand-side barriers that MSMEs face to access financial institutions. Access to formal financial services represents a higher level of FI. This study uses two access indicators: the tightness of credit condition (Tight_Credit) and access to digital financial services (Digital).

Usage indicators measure how MSMEs use financial services. Although firms may have access to financial products, access does not mean that a firm will use a particular financial product. Thus, while all firms have theoretical access to financial services, this does not automatically infer that they are financially included. Following G20 indicators, this study uses a line of credit (Use_Credit) and usage of a deposit account (Use_Account) as usage indicators. For the proxy of a line of credit (Use_Credit), we use a dichotomous variable that takes the value of one if a firm has an outstanding loan or a line of credit, and zero otherwise. For the proxy for the usage of a deposit account (Use_Account), we use a dichotomous variable which takes the value of one if a firm has high usage of a deposit account per month, and zero otherwise. Our usage dimension captures the extent to which MSMEs make use of the services they can access.

Quality indicators measure whether financial products and services match MSMEs’ needs, the range of options available to MSMEs, and MSMEs’ awareness and understanding of financial products. The quality of financial services will determine whether improved FI is useful and sustainable. Based on the OECD indicator, we use the relative cost of credit, that is, we proxy the difference in the risk of SME lending and corporate lending by the Risk variable. For the proxy for risk premium payment (Risk), we use a dichotomous variable that takes a value of one if a firm is required to pay a risk premium for their loan and zero otherwise.

We use information availability (Information) as a quality indicator as well. For the proxy of information availability (Information), we use a dichotomous variable which takes a value of one if an MSME owner-manager receives clear and sufficient information about financial services at the start of the loan contract, and zero otherwise.

Certain firm-level characteristics and location-specific factors limit full access to financial services and these factors may limit firm-level FI. Therefore, we include the town size in which the firm operates (A village, hamlet or rural area (fewer than 3000 people), a small town (3000 to about 15,000 people), a town (15,000 to about 100,000 people), a city (100,000 to about 1,000,000 people), a large city (with over 1,000,000 people)), firm size (self-employed, >= 5 employees, >= 20 employees and >= 100 employees), firm core activities (property, investment, primary, goods and services), owner’s risk attitude (high risk-taker or not), firm’s legal status (shareholding company or not) and firm age (firm_age) as firm-level control variables of this study.

Furthermore, in explaining FI, individual characteristics have been found to be strong determinants. Hence, we include the owner’s gender (male), the owner’s age group (less than 35, 35–45, 45–60 and above 60 years), the owner’s ethnicity (European, Maori & Pacific, Asian and others) and the owner’s risk-taking ability (high risk) as dichotomous variables. In addition, the owner’s highest education level is captured as follows: primary school, secondary school, polytechnic and university degree or above.

Table 1 provides a detailed description of the FI indicators used and their source. Following Klapper et al. (2013) and Lusardi and Mitchell (2011), we control for firm-level characteristics and owners’ demographics that may have potential effects on the utilisation of financial services.

Financial inclusion indicators.

3.3. Model specification and estimation approaches

The empirical model for this study is formalised as follows:

where Y is the dependent binary variable (FI, yes/no); α is the constant term; β is a k × 1 vector; X’ is MSME owner’s finance literacy score; Z is an n × k matrix of covariates and u is the error term.

4. Empirical results and discussion

4.1. Descriptive statistics

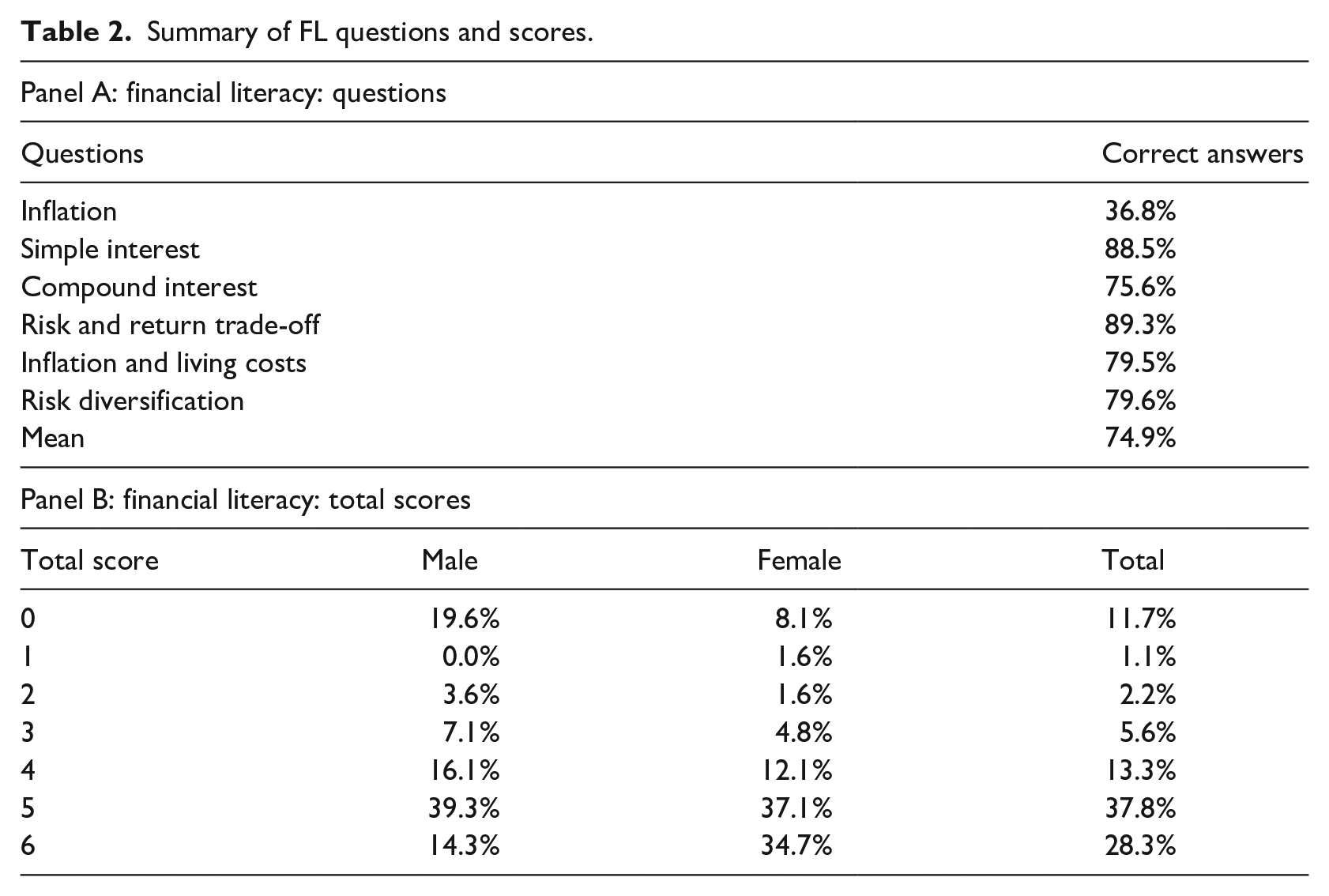

Table 2 summarises the FL questions (Panel A) and FL total scores (Panel B). Following the literature, we ask the respondents six quiz-like questions to evaluate their knowledge of basic and advanced FL in six categories. The respondents (MSME owners) in our sample, on average, answered approximately 75% of the FL questions correctly. Notably, only 37% of respondents correctly answered the first question regarding basic financial knowledge (inflation). This finding is corroborated by Lusardi and Mitchell (2011), who observed that ‘people are more knowledgeable about inflation if their country has experienced it recently’. 6 On the other hand, very few respondents answered the questions on simple interest and risk-return trade-offs incorrectly (approximately 12% and 11%, respectively).

Summary of FL questions and scores.

According to the questions presented in Panel A of Table 2, we have calculated FL total scores that range between one and six. As seen in Panel B of Table 2, while approximately 28% of our respondents answered all six questions correctly, nearly 38% of sampled MSME owners answered five questions correctly. Panel B provides an overview of FL scores by gender. It is evident, from Panel B, that the proportion of male and female owners who have FL scores of five or six is different (approximately 53.6% for male owners and 71.7% for female owners). Our finding of overall high FL, for both genders, is unsurprising in that our respondents are based in New Zealand where MSME owners have a high degree of exposure to financial services.

Prior research has reported women have lower financial literacy compared to men. For example, Lusardi and Mitchell (2011) and Xue et al. (2019) reported that females with limited exposure to financial services have low FL. However, this is not always the case. Wagland and Taylor (2009), for instance, reported that women have a slightly higher financial literacy compared to males in their Australian-based sample. In our sample, we find that approximately 72% of female MSME owners show a high level of financial literacy. This is aligned with recent Australian findings which report that 60% of female small business owners in Australia feel very confident in their financial literacy. Furthermore, the study reports that 72% of female small business owners feel confident they can make the right decisions for their small businesses in Australia (QuickBooks Australia, 2023).

The New Zealand MSME landscape is different compared to other countries. In New Zealand, women make up one in three business owners, the fourth highest rate in the world and the highest among developed countries (Baker, 2018). According to the Mastercard Index of Women Entrepreneurs (2022), New Zealand’s world-leading entrepreneurial support framework for women is driven by (1) high opportunities for education (female tertiary education enrolment rate 97.8%, world rank 6); (2) little marginalisation as financial customers (‘Women Financial Inclusion’, rank 1); (3) strong entrepreneurial optimism (‘perceived opportunities’ and ‘perceived capabilities’ in business, both rank 2) and (4) very high ‘quality of governance’”, rank 1.

We identify two possible pathways for the higher propensity of FL among female MSME owners than male counterparts in our sample. First, it could be that women who enter the MSME sector in New Zealand have a high level of FL. On the one hand, due to the high level of opportunity-driven entrepreneurship, we can assume that female MSME owners in New Zealand may have high FL. On the other hand, it might require a higher FL for a woman to become an entrepreneur compared to a man. Women who become small business owners also face more background risk and barriers than male owners, suggesting that these women would need to have high FL to choose entrepreneurship. Second, women who enter the MSME sector may be less FL than men. However, over time they learn to be more FL to survive and thrive in business. Due to the high support for female entrepreneurs in New Zealand, over time female FL may become higher than male MSME owners. However, it is interesting to investigate whether these two groups’ FL levels impact FI differently.

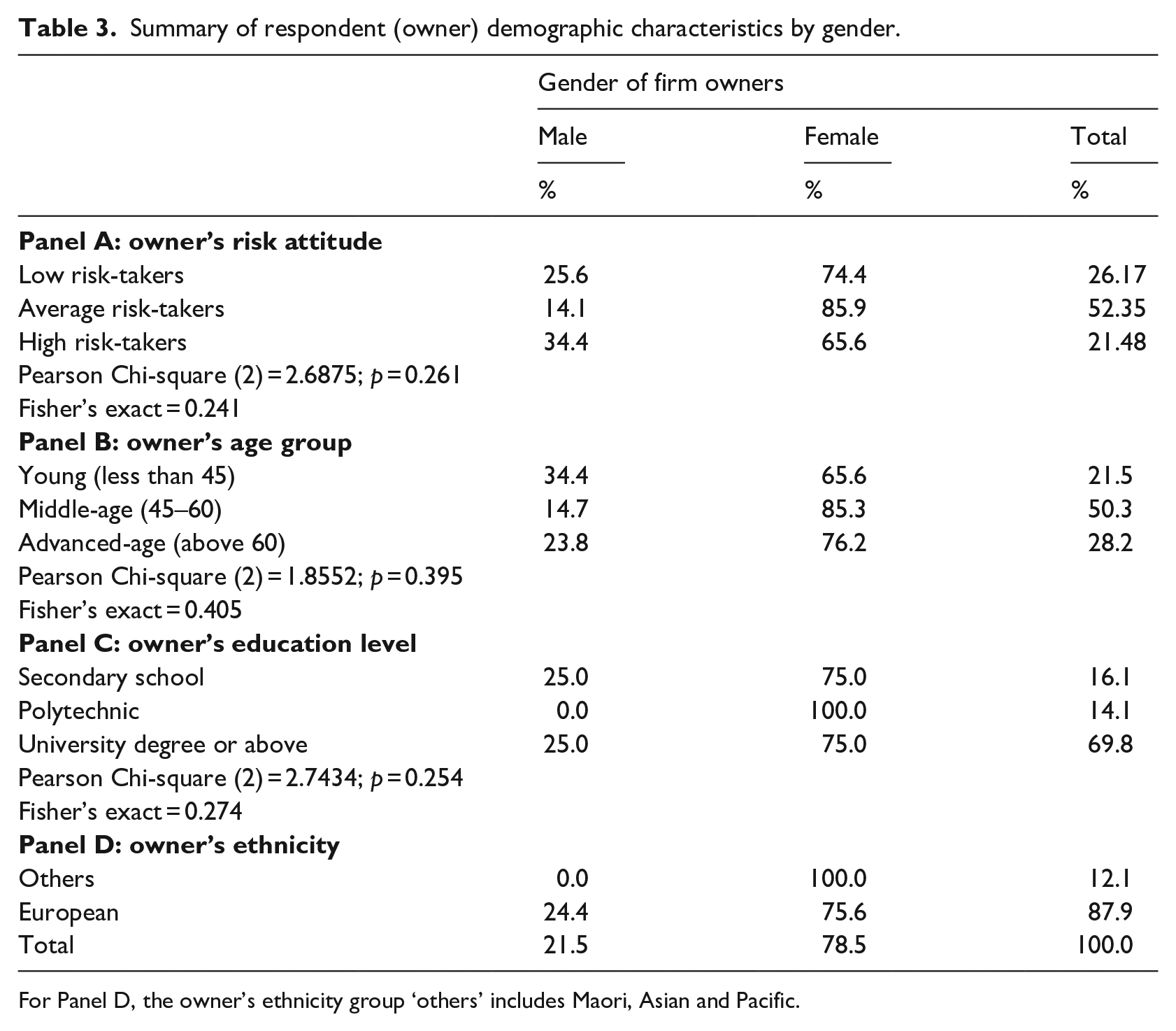

Table 3 presents a contingency table of MSME owners’ demographic information and owners’ gender. Panel A of Table 3 shows that while the majority of respondents are average risk takers (approximately 52.4%), risk-averse entrepreneurs account for approximately 26.1% of the sample. As reported in Panels B and D of Table 3, our sample is predominantly made up of Caucasian respondents (87.9%), with half of the respondents being middle-aged (50.3%). Panel C of Table 3 shows that the respondents who have tertiary education qualifications make up 69.8% of our sample.

Summary of respondent (owner) demographic characteristics by gender.

For Panel D, the owner’s ethnicity group ‘others’ includes Maori, Asian and Pacific.

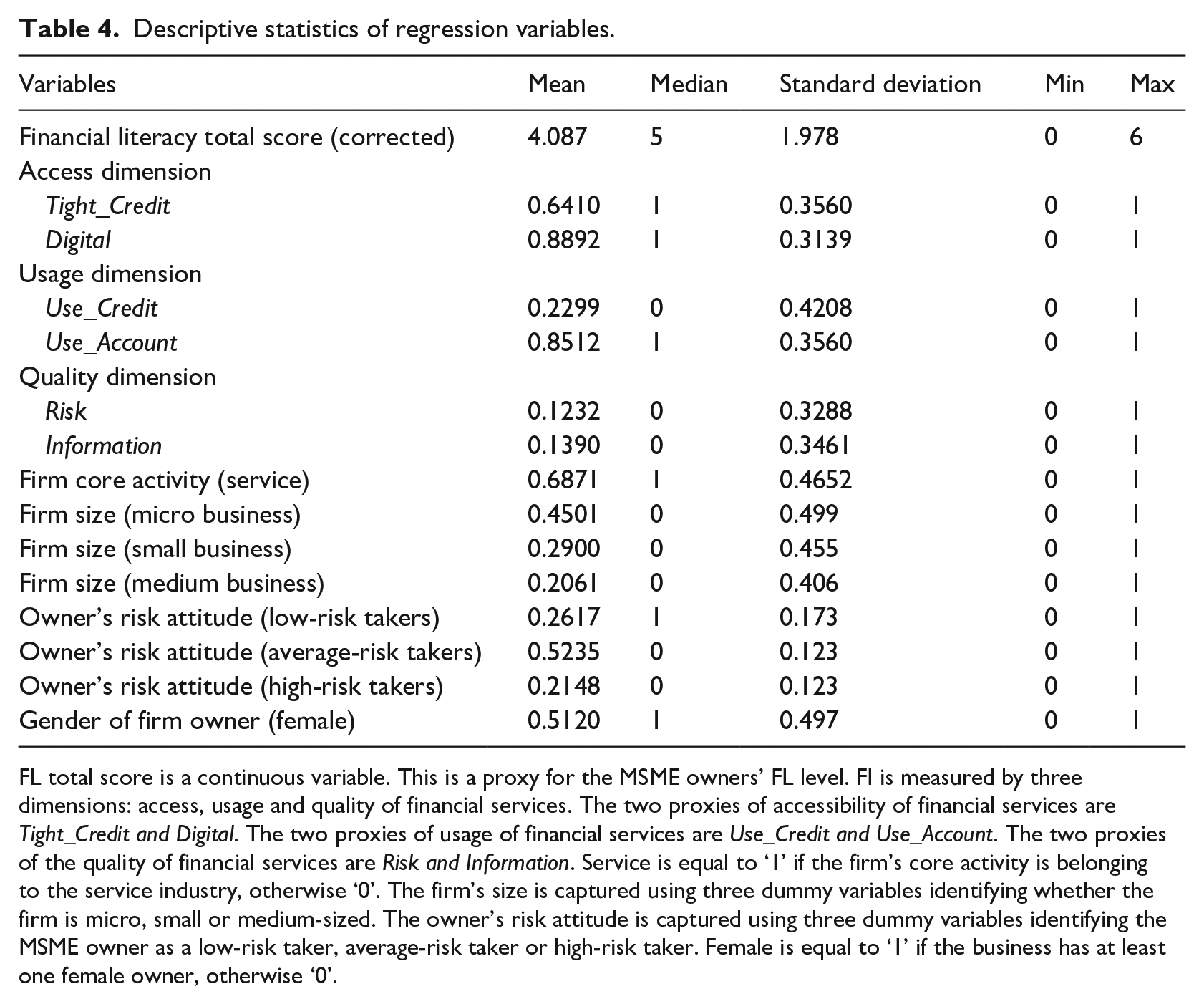

Table 4 provides descriptive statistics of variables used in the regression analysis. The mean FL total score is 4.087, indicating that the majority of MSME owners in New Zealand have a considerable level of financial knowledge. The Tight_Credit variable indicates that approximately 64% of the sample MSMEs need to provide collateral for their existing loan.

Descriptive statistics of regression variables.

FL total score is a continuous variable. This is a proxy for the MSME owners’ FL level. FI is measured by three dimensions: access, usage and quality of financial services. The two proxies of accessibility of financial services are Tight_Credit and Digital. The two proxies of usage of financial services are Use_Credit and Use_Account. The two proxies of the quality of financial services are Risk and Information. Service is equal to ‘1’ if the firm’s core activity is belonging to the service industry, otherwise ‘0’. The firm’s size is captured using three dummy variables identifying whether the firm is micro, small or medium-sized. The owner’s risk attitude is captured using three dummy variables identifying the MSME owner as a low-risk taker, average-risk taker or high-risk taker. Female is equal to ‘1’ if the business has at least one female owner, otherwise ‘0’.

The Digital variable indicates that approximately 89% of MSMEs in New Zealand have reasonable and secure access to electronic payment services using the Internet or mobile financial services. Based on the descriptive statistics, only 23% of sample firms have an outstanding loan or external credit line. Similar findings are also reported in prior MSME studies (Hewa Wellalage and Reddy, 2020; Wellalage and Locke, 2016). According to Table 4, above 85% of the sample MSMEs have a high usage of deposit accounts per month. Only 12% of MSMEs indicate that they pay a risk premium for their loan. The mean value of the information availability (Information) variable indicates that only 14% of MSME owner-managers receive clear and sufficient information about financial services at the start of the loan contract.

Services account for about 69% of sample firms. This is in alignment with the current facts in New Zealand, where the services sector contributes the highest to the gross domestic product (The Small Business Sector Report and Factsheet, 2017). About 45% of the sample represents micro-firms. This gives a true reflection of the MSME sector in New Zealand. The descriptive statistics reported in Table 4 indicate that 78.5% of MSME owners belong to the low and average risk category. The descriptive statistics also reveal that about 51% of the sample MSMEs are owned by women.

4.2. Multiple variable regression analysis

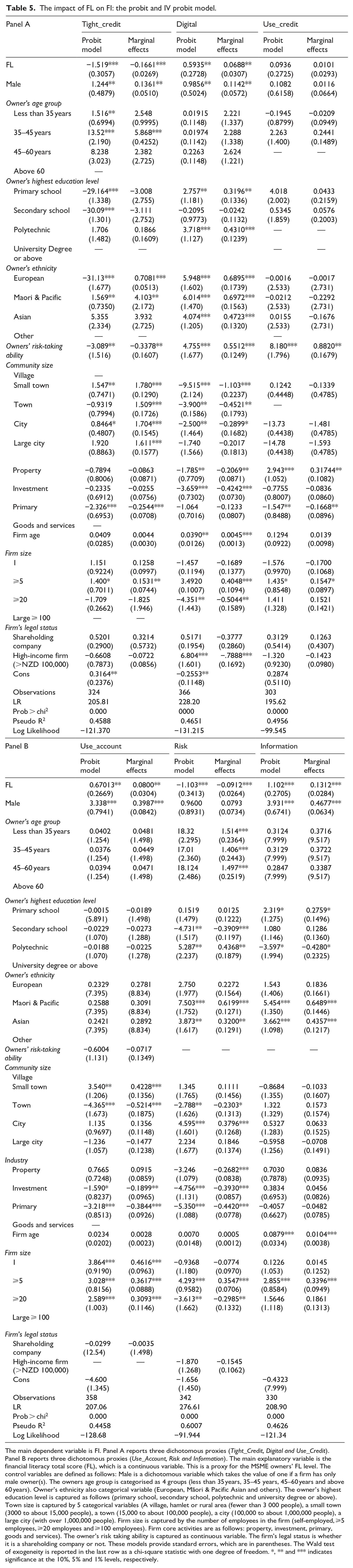

Table 5 reports probit results for the FL on FI relationship for MSMEs. 7 Panel A reports the dimensions of FI, Tight_Credit, Digital and Use_Credit, while Panel B reports the dimensions of FI, Use_Account, Risk and Information. Using Tight_Credit 8 as the FI proxy (Table 5, Panel A, Column 2), the marginal effect reports that increases in the FL level of MSME owners lead to a decrease in the tightness of the credit condition of MSMEs. Specifically, the magnitude of the effect of FL on FI for MSME owners is −0.1661. This indicates that all else being equal, one standard deviation increase in FL is associated with a 16 percentage point lower probability of an MSME experiencing tightness of credit. The second proxy of the financial access dimension, the Digital variable (Panel A, Column 4) indicates that all else being equal, a one standard deviation increase in FL is associated with approximately 7 percentage points higher probability of MSMEs gaining access to digital financial services. Both FI proxies for the financial access dimension (Tight_Credit and Digital) show that FL has a significant positive impact on MSME owners’ FI. This finding is in line with Servon and Kaestner (2008), who find that financially literate consumers have more access to financial services. Overall, this finding leads to acceptance of H1a: Considering causality, there is a positive relationship between the level of FL and financial services accessibility by MSME owners (Access dimension of FI).

The impact of FL on FI: the probit and IV probit model.

The main dependent variable is FI. Panel A reports three dichotomous proxies (Tight_Credit, Digital and Use_Credit). Panel B reports three dichotomous proxies (Use_Account, Risk and Information). The main explanatory variable is the financial literacy total score (FL), which is a continuous variable. This is a proxy for the MSME owners’ FL level. The control variables are defined as follows: Male is a dichotomous variable which takes the value of one if a firm has only male owner(s). The owners age group is categorised as 4 groups (less than 35 years, 35–45 years, 45–60 years and above 60 years). Owner’s ethnicity also categorical variable (European, Māori & Pacific Asian and others). The owner’s highest education level is captured as follows (primary school, secondary school, polytechnic and university degree or above). Town size is captured by 5 categorical variables (A village, hamlet or rural area (fewer than 3 000 people), a small town (3000 to about 15,000 people), a town (15,000 to about 100,000 people), a city (100,000 to about 1,000,000 people), a large city (with over 1,000,000 people). Firm size is captured by the number of employees in the firm (self-employed, ⩾5 employees, ⩾20 employees and ⩾100 employees). Firm core activities are as follows: property, investment, primary, goods and services). The owner’s risk taking ability is captured as continuous variable. The firm’s legal status is whether it is a shareholding company or not. These models provide standard errors, which are in parentheses. The Wald test of exogeneity is reported in the last row as a chi-square statistic with one degree of freedom. *, ** and *** indicates significance at the 10%, 5% and 1% levels, respectively.

We note that the Use_Credit proxy for the financial usage dimension is not statistically significant (Table 5, Panel A, Column 6). This result indicates that Fl has no impact on whether an MSME uses a line of credit. The proxy for financial usage, namely, Use_Account (Table 5, Panel B, Column 2), shows that FL increases MSME owners’ frequency of use of deposit accounts. In particular, all else being equal, a one standard deviation increase in FL is associated with an eight-percentage point higher probability of an MSME frequency of use deposit accounts. Overall, this finding leads to acceptance of H1b: Considering causality, there is a positive relationship between the level of FL and financial services usage by MSME owners (Usage dimension of FI).

Looking at the Risk marginal effect (Table 5, Panel B, Column 4), the risk premium charged on MSME loans, we find that all else being equal, a one standard deviation increase in FL is associated with 9 percentage points lower probability of paying a risk premium on their loans. Information (Firm owners received clear and sufficient information about financial services at the start of the loan contract) is the second proxy for financial services quality. The marginal effect Information (Table 5, Panel B, Column 6) shows that all else being equal, a one standard deviation increase in FL is associated with a 13 percentage point higher probability of having received clear and sufficient information about financial services. Overall, this finding leads to acceptance of H1c: Considering causality, there is a positive relationship between the level of FL and the quality of financial services used and access by MSME owners (Quality dimension of FI). Overall, the results shown in Table 5, indicates that FL has a significant positive impact on FI. Consistent with Carpena et al. (2011), this study provides evidence that FL positively influences FI. Hence, we accept the first hypothesis that indicates a positive relationship between the level of FL and FI by MSME owners.

However, a sceptical reader may note that FL has an endogenous effect on the FI proxies. It may be possible that reverse causality exists between FL and FI. In addition, the cross-sectional data can be subject to unobservable heterogeneity. When unobserved factors are correlated with the exogenous variables, estimated coefficients can be biased. However, finding a noncontroversial strong instrument that is determined outside the firm is nearly impossible for our small cross-sectional sample. In future studies using larger panel datasets will find suitable instrumental variables to control possible endogeneity biases. Consequently, we state this as the limitation in the conclusion section of this study.

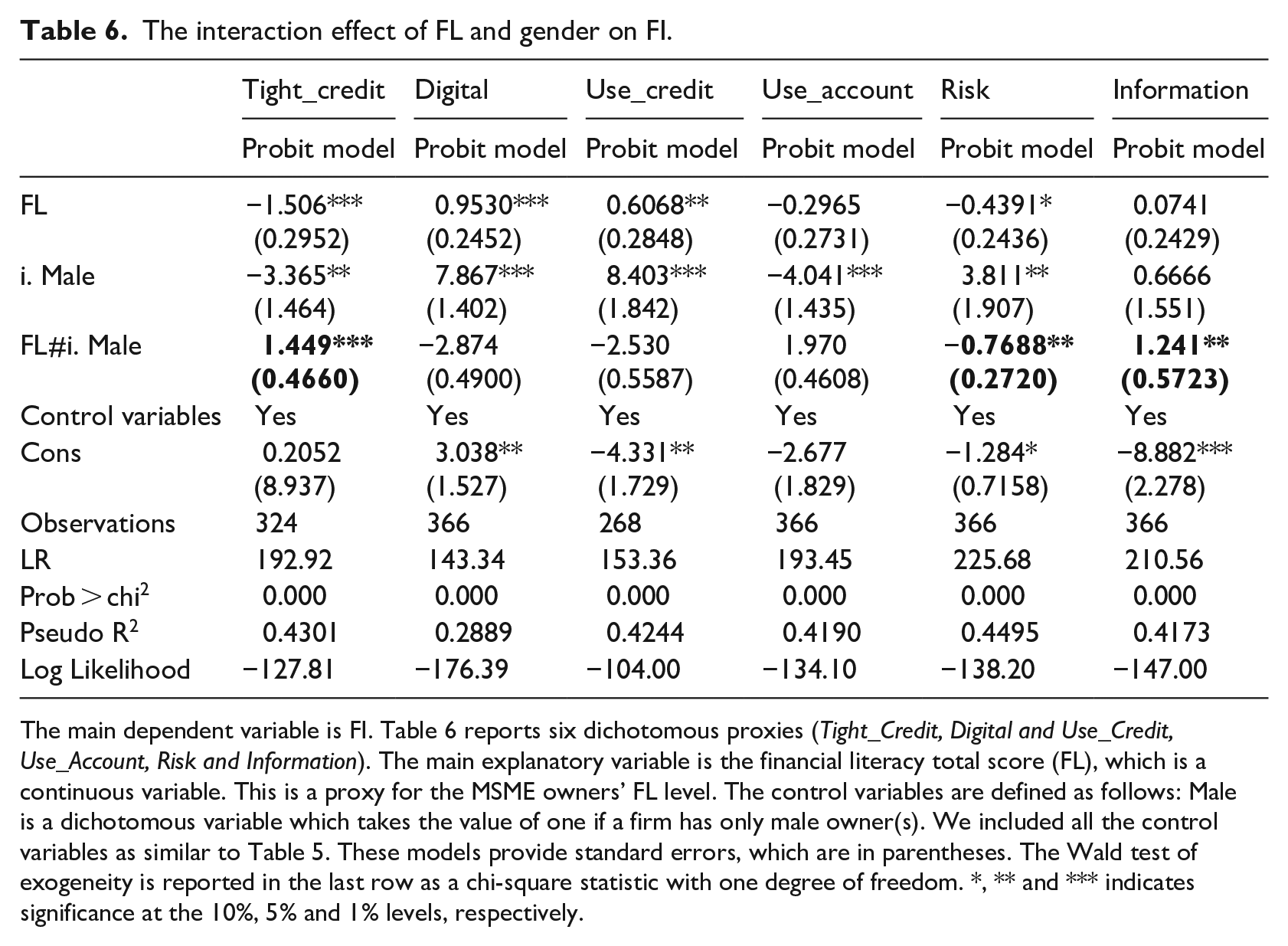

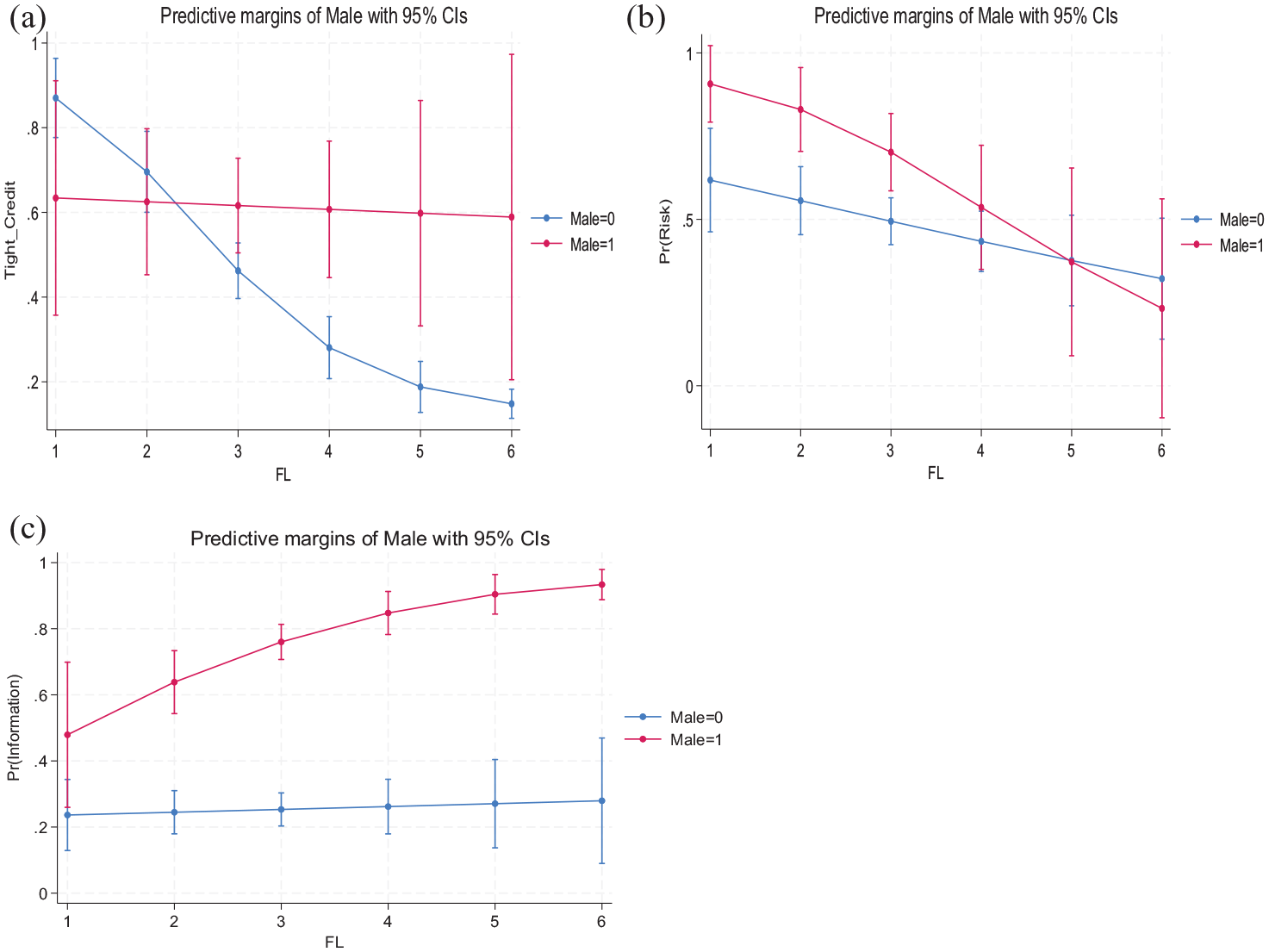

Table 6 and Figure 1 report probit results for the gender impact on the relationship between the level of FL and FI of MSMEs. The coefficients of FL#i.Male indicate that the interaction has a significant impact on the FI proxies. Figure 1(a) shows the probability of tight credit conditions decreases for firms when FL increases, regardless of the owners’ gender. However, the coefficients indicate that the impact of FL on the tight credit condition is significantly higher for the female group compared to their male counterparts. Figure 1(b) shows the probability of risk premium payment decreases for firms when FL increases, regardless of the owners’ gender. The impact of FL on the risk premium payment is higher for the male group compared to the female group. Figure 1(c) shows the probability of information availability increases when the FL level of MSME owners increases. The impact is higher for male MSME owners compared to female MSME owners. Overall, our results indicate that MSME owners’ gender moderates the FL-FI nexus.

The interaction effect of FL and gender on FI.

The main dependent variable is FI. Table 6 reports six dichotomous proxies (Tight_Credit, Digital and Use_Credit, Use_Account, Risk and Information). The main explanatory variable is the financial literacy total score (FL), which is a continuous variable. This is a proxy for the MSME owners’ FL level. The control variables are defined as follows: Male is a dichotomous variable which takes the value of one if a firm has only male owner(s). We included all the control variables as similar to Table 5. These models provide standard errors, which are in parentheses. The Wald test of exogeneity is reported in the last row as a chi-square statistic with one degree of freedom. *, ** and *** indicates significance at the 10%, 5% and 1% levels, respectively.

Marginal graph. Figures a, b and c show the predicted probability and the 95% confidence level around those margins for MSME owners access to credit, risk and infrmation, respectively.

5. Summary and conclusion

This study first seeks to determine whether FL matters regarding MSMEs’ FI. Second, we extend the prior literature by investigating the impact of gender on the FL-FI nexus. Although FL has received an increasing level of attention worldwide, the focus has primarily been on the development of the FL concept as a personal finance tool. This is the first study to investigate the relationship between FL and FI in the context of MSME owners. We extend the literature by examining MSMEs as a subgroup. We report that the FI of MSME owners increases with FL. Furthermore, our results show that the owner’s gender moderates the FI and FL nexus.

Our findings suggest important implications for policy formulation, especially for the MSME sector. First, we suggest to policymakers that increasing MSME owners’ FL level may have a positive effect on owners’ access, use and quality of financial services. This can be implemented through the introduction of financial education training programmes for MSME owners. Financial education programmes are a low-cost intervention with the potential to enhance financial skills and ultimately increase the demand for financial services by MSME owners. More importantly, the owner’s gender has a moderation effect on the FI-FL nexus. Hence, targeting financial education programmes based on gender may result in more effective outcomes. We suggest that policymakers encourage financial service providers to improve their marketing strategies and expand their financial services to ensure FL is not a barrier to the demand for financial services among MSME owners.

We caution readers from generalising the findings of this study as it is based in a developed country, New Zealand, where access to financial services is not a barrier and equality of gender is encouraged. Furthermore, due to a low response rate, our sample size is small, which means that we are not able to undertake some analysis that future research could address. Prior studies suggest that underlying heterogeneous factors, such as the firm owner’s risk-taking ability and attitude, may affect the level of both FL and FI. When unobserved factors are correlated with the exogenous variables, estimated coefficients can be biased, and the estimated relationships may not reflect the true relationships between the variables of interest. In addition, we did receive a number of ‘don’t know’ responses for certain survey questions. Similar to prior studies such as Klapper and Lusardi (2020), it is unclear how these responses may have affected our results. Therefore, we caution readers from generalising the findings. Hence, future studies with larger samples may be able to control for this endogeneity effect.

Our study does highlight some fruitful avenues for future research. The possibility of extending the research to other countries is important for policymaking in countries that are recipients of MSME development funding from funding agencies. As we have only considered a limited number of personal attributes affecting FI, future studies could also include other personal and social factors that may influence FI with the time dimension.